Zillow: The Portal That Became a Real Estate Empire

I. Introduction & Episode Roadmap

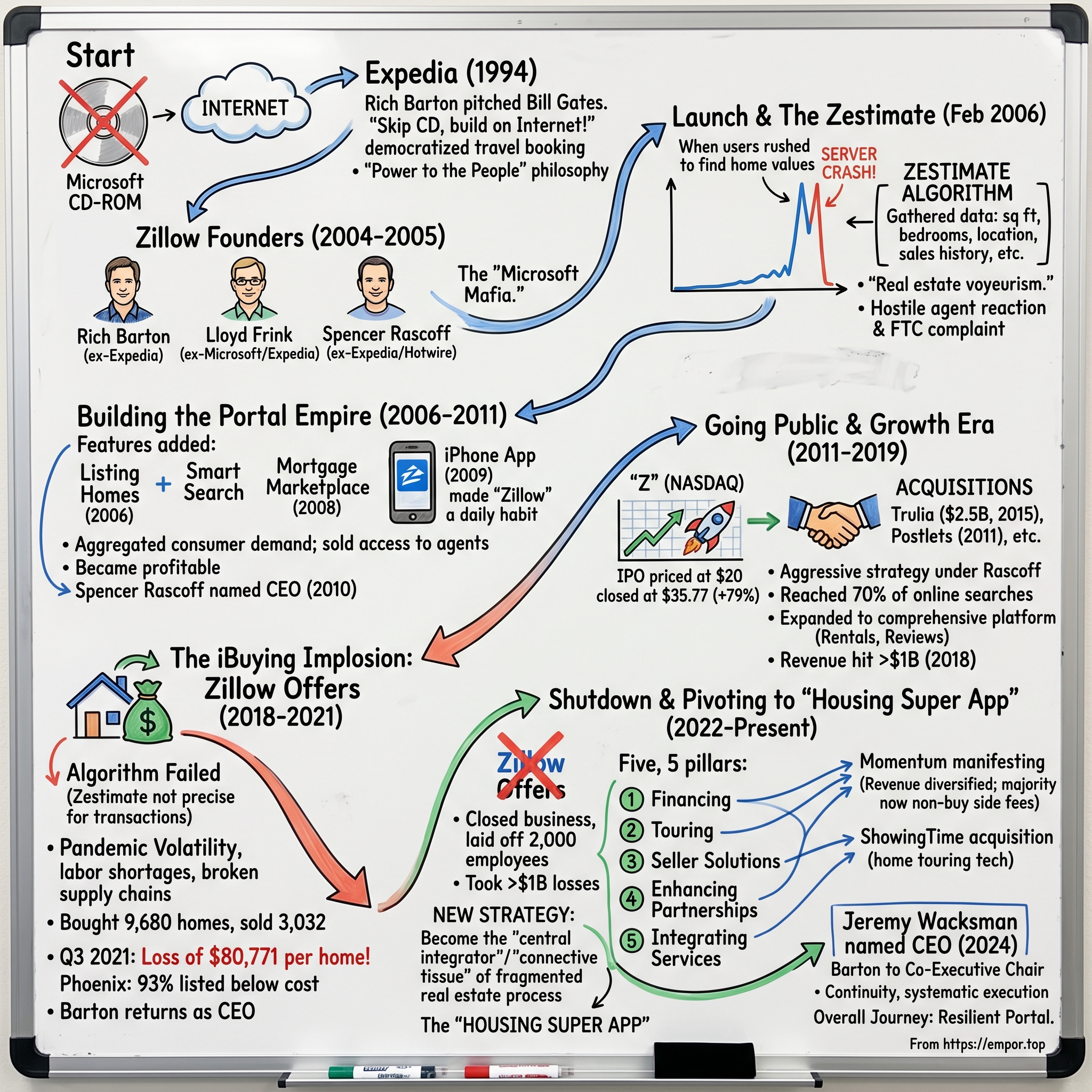

Picture this: It's February 8, 2006, 9 AM Pacific. A small Seattle startup launches a website that promises to tell Americans what their homes are worth—for free. Within minutes, the servers crash. Not from bugs or bad code, but from millions of homeowners frantically typing in their addresses, desperate to know a number that had been hidden from them for decades. That startup was Zillow, and that morning marked the beginning of a revolution in how Americans think about real estate.

Today, Zillow Group commands a market capitalization of $19.58 billion, making it one of the most valuable real estate technology companies in the world. But here's what's fascinating: Zillow doesn't own homes (anymore), doesn't employ agents, and doesn't handle transactions. It's essentially a portal—a digital window into the American housing market. Yet somehow, this "simple" website has become more powerful than century-old brokerages and has fundamentally rewired how 200 million monthly users interact with the largest asset class in America.

The story of Zillow is really three stories woven together. First, it's the tale of Rich Barton, a Microsoft executive who built not one but three category-defining companies—Expedia, Zillow, and Glassdoor—all based on the same radical principle: "Power to the People." Second, it's a case study in marketplace dynamics, showing how a company can thrive by serving two groups who fundamentally distrust each other (agents and consumers). And third, it's a cautionary tale about the limits of technology, culminating in one of the most spectacular business failures of the 2020s: the $2.8 billion iBuying implosion.

What makes Zillow particularly compelling for investors is its resilience. The company has survived the 2008 financial crisis, multiple competitive threats, a CEO transition, a massive strategic pivot, and most recently, the complete shutdown of what was supposed to be its future growth engine. Yet here it stands, stronger than ever, processing over 2 billion searches annually and generating $2.24 billion in revenue.

This is the Acquired-style deep dive into how a Microsoft spin-off team built the most visited real estate site in America, why they nearly destroyed it trying to become something more, and what their journey teaches us about marketplaces, disruption, and the surprising durability of information asymmetry in the internet age.

II. The Microsoft Mafia: Rich Barton's Origin Story

The conference room at Microsoft's Redmond campus in 1994 was typical for the era—beige walls, overhead projector, and a whiteboard covered in flowcharts. Rich Barton, a young product manager with an economics degree from Stanford, was supposed to be presenting plans for a travel guide on CD-ROM. Instead, he pitched something audacious to Bill Gates, Steve Ballmer, and Nathan Myhrvold: "What if we skip the CD entirely and build this on the internet?"

Gates, famous for his ability to see around corners, immediately grasped the implications. This wasn't just about travel—it was about disintermediating an entire industry. Within months, Barton was leading a team to build what would become Expedia, Microsoft's first major consumer internet property. The project was classic Microsoft: well-funded, aggressively executed, and aimed directly at the jugular of established industries. What made Barton different from other Microsoft product managers was his ability to see beyond software features to fundamental market inefficiencies. Barton founded Expedia within Microsoft in 1994. In 1994, Microsoft was planning to build a travel guidebook on a CD-ROM. But he wound up pitching Bill Gates on an idea that was transformative at the time: to let everyday travelers book their own flights and hotels by giving them online access to previously hidden reservation systems.

The key insight was deceptively simple: travel agents were essentially gatekeepers to a computerized system called SABRE that airlines used for reservations. Why not cut out the middleman and give consumers direct access? Barton persuaded Microsoft to invest $100 million in order to make a group of personal computers do what in the past only a mainframe airline-reservation system could do—retrieve flight information and purchase a ticket.

Barton's management philosophy, forged in those Microsoft years, would become the foundation for everything that followed. He called it "Power to the People"—a belief that technology should democratize access to information that institutions hoarded for profit. Barton uses a slogan "power to the people", the staunch philosophy behind his each start-up. It wasn't just corporate speak; it was a deeply held conviction that would drive him to build three separate billion-dollar companies.

Expedia launched from inside Microsoft but was so successful at transforming the travel industry that it was spun out into a public company with Rich as CEO. The 1999 IPO was a watershed moment—In the fourth quarter of 1999 Microsoft spun off Expedia (while still maintaining a controlling interest) with an initial public offering (IPO) of $14 per share. The stock jumped 280 percent on the first day of trading, producing a market cap of $2 billion and making Barton a rich man.

But what happened next was even more interesting. He remained as CEO of Expedia till 2003 after which the company was acquired by IAC Corp. Rather than immediately jumping into another venture, Barton did something unusual for a Silicon Valley entrepreneur: he took a year off. He moved to Italy with his family, disconnected from the tech world, and thought deeply about what came next. When he returned from Italy in 2004, Barton reconnected with Lloyd Frink, his longtime lieutenant from Expedia. Lloyd Frink co-founded Zillow in 2005, but their partnership went much deeper. From 1999 to 2004, Mr. Frink was at Expedia, where he held many leadership positions, including Senior Vice President, Supplier Relations from 2003 to 2004, during which he managed the air, hotel, car, destination services, content, merchandising, and partner marketing groups. What's remarkable is that From 1988 to 1999, Mr. Frink was at Microsoft Corporation, a technology company, where he was part of the founding Expedia team—and even more incredibly, He initially joined Microsoft in 1979 as a summer intern at 14 years old and then joined full-time in 1988.

The third key member of the founding team was Spencer Rascoff, who brought a different perspective. He is the co-founder and former chief executive officer of Zillow Group, as well as one of the co-founders of Hotwire.com. Rascoff then served as vice president of lodging for Expedia before leaving to co-found Zillow. Rascoff served various roles through the years including chief operating officer, chief financial officer, and VP of Marketing until his appointment to CEO in 2010.

This wasn't just a team of ex-colleagues—it was the "Microsoft Mafia" in action. They'd learned from Gates and Ballmer how to think big, move fast, and disrupt entire industries. They'd seen how Expedia transformed travel by exposing hidden information. Now they were ready to apply the same playbook to an even bigger market: American real estate.

The philosophy was consistent across all of Barton's ventures. Barton uses a slogan "power to the people", the staunch philosophy behind his each start-up. Whether it was airline tickets at Expedia, home values at Zillow, or later, company salaries at Glassdoor (which he co-founded in 2007), the pattern was the same: find information that institutions hoarded, liberate it, and build a business around the resulting transparency.

III. Founding & Launch: The Zestimate Gambit (2004–2006)

The eureka moment came during a frustrating personal experience. In 2004, Richard Barton and Lloyd Frink, unsatisfied with their own home-buying experience, decided to make this process more efficient with technology, the same as they did with the travel industry. They realized that homeowners had no easy way to know what their largest asset was worth without calling a real estate agent—who would immediately try to sell them something.

This was the kind of information asymmetry that Barton lived to destroy. In the travel industry, airlines and hotels had controlled pricing information. In real estate, agents and brokers controlled valuation data. The average American homeowner was flying blind, checking their home's value maybe once a decade when they were ready to sell.

The solution they conceived was audacious: an algorithm that could instantly estimate the value of any home in America. They called it the "Zestimate"—a portmanteau that perfectly captured both its function and the company's irreverent spirit. The core feature at launch was the Zestimate algorithm. This automated valuation model was able to accurately estimate the market value of homes clients were interested in and help them understand the potential worth of properties they are interested in or already own. Zestimate gathered and processed data from various sources, including square footage, number of bedrooms, sales history, property location, and market trends.

Building the Zestimate required solving massive technical challenges. They needed to aggregate data from thousands of county assessors, each with different formats and update cycles. They had to normalize millions of property records, build statistical models that could account for local market dynamics, and create an interface simple enough for anyone to use. The team worked in stealth mode for nearly two years, raising initial funding and building out the technology. The launch on February 8, 2006, was both a triumph and a disaster. Zillow launches, attracting more than 1 million visitors within the first three days, ultimately overloading the servers and crashing the website. More specifically, We had over a million people visit the site by the second day and I think by the fifth day we had over two million people and the site crashed. We were down for, gosh, probably about 6 hours or so and we were scrambling to add capacity and to get the site back up.

The crash turned into a marketing coup. It turned out to be a blessing in disguise of course, because going down … "I want to go to that website." No, that was not intentional, that was inadvertent but beneficial. Media coverage exploded. Stories about the startup online real estate service in major U.S. newspapers -- including The Wall Street Journal, The New York Times and Los Angeles Times -- helped swamp Zillow's servers throughout the morning and early afternoon. By 7 a.m. Wednesday, the company had already served up more then 300,000 pages. By 4:30 p.m., the total had surpassed 2 million.

But the real victory wasn't just traffic—it was validation. Americans were desperate for this information. Spencer Rascoff, who would later become CEO, recalled: I knew before we launched that we were going to have a great reaction because I remember when the test site was up, I was Zillowing all of my friends and family, for a couple of weeks, just pulling up any address that I could remember or had some association with or had lived in or had a friend that lived in.

The industry reaction was swift and hostile. Real estate agents saw the Zestimate as an existential threat. In October 2006, the National Community Reinvestment Coalition filed a complaint with the Federal Trade Commission stating that Zillow was "intentionally misleading consumers and real estate professionals to rely upon the accuracy of its valuation services despite the full knowledge of the company officials that their valuation Automated Valuation Model (AVM) mechanism is highly inaccurate and misleading." The FTC eventually declined to investigate, but the battle lines were drawn.

By July 2006, the momentum was undeniable. In July 2006, Zillow announced a $25 million second-round investment. By then the company had grown to 118 employees. The company had struck a nerve, tapping into what Barton called "real estate voyeurism"—the universal human desire to know what things are worth, especially the house next door.

IV. Building the Portal Empire (2006–2011)

The post-launch period required a fundamental strategic decision: Would Zillow be a disruptor trying to eliminate real estate agents, or would it become their digital partner? The answer would define everything that followed.

In December of that year, the Zillow website included features allowing users to put homes for sale online. Zillow launches Smart Search, a dynamic new version of its search system, developed to make it easier for customers to find the homes most relevant to them. Zillow launches Mortgage Marketplace, a free and transparent tool that allows borrowers to request anonymous and hassle-free mortgage loan quotes from lenders directly through Zillow.

The mobile revolution arrived just in time. Zillow launches the Zillow iPhone app with dynamic map technologies, delivering data on 88 million homes directly into users' hands. This wasn't just another app—it transformed real estate browsing into a daily habit. People could now "Zillow" houses while walking their dogs, sitting in traffic, or lying in bed at night.

The business model crystallized around a brilliant insight: Zillow would aggregate consumer demand and sell access to real estate professionals. Agents might hate the Zestimate, but they couldn't ignore millions of motivated home shoppers. The company became a two-sided marketplace where the product (consumer attention) was generated by the very information that agents wished didn't exist.

2010 marked a crucial transition. In 2010, Zillow became profitable for the first time. In September of that same year, Spencer Rascoff was named CEO of the company. Rascoff was formerly Zillow's COO and VP of marketing, and before that had been at Expedia. Rich Barton stayed as executive chairman.

The Spencer Rascoff appointment was significant. At just 35 years old, he represented a new generation of leadership—someone who understood both the startup mentality and the discipline needed to build a public company. His background was perfect: he'd co-founded Hotwire.com, worked at Expedia, and had been with Zillow since the early days. He knew the playbook.

By early 2011, the company was ready for its next act. The metrics were compelling: tens of millions of unique visitors, hundreds of millions in market value implied by private valuations, and most importantly, a business model that was working. Real estate professionals were spending serious money to reach Zillow's audience, validating the portal model that many had doubted could work in real estate.

V. Going Public & The Spencer Rascoff Era (2011–2019)

The morning of July 20, 2011, marked a defining moment. Zillow, Inc. (NASDAQ: Z), which operates real estate site Zillow.com®, Zillow Mortgage Marketplace, and Zillow Mobile, today announced the pricing of the initial public offering of 3,462,000 shares of its Class A common stock at $20.00 per share. Last week, the company upped the pricing of its IPO to $16 to $18 per share, from the initial range of $12 to $14 per share. The consistent price increases reflected surging investor demand.

What happened next was extraordinary. Zillow (Z) priced its IPO late Tuesday at $20 per share. The stock quickly rose to $44 a share Wednesday, where it traded for most of the morning, before drifting as low as $32.50. The stock ended at $35.77, or 79% higher. The market had delivered its verdict: Zillow was the real deal.

But the company wasn't profitable yet. Zillow has not yet turned a profit, just like many other Internet companies to make IPO filings this year, including Pandora (P) and Groupon. Zillow revealed in its S-1 filing to the SEC that losses narrowed to $6.8 million in 2010 from a $12.9 million loss in 2009. In the first quarter of 2011, Zillow lost $865,000.

Spencer Rascoff, now CEO, understood that the path to profitability lay in scale and market dominance. Rascoff has led Zillow Group as CEO from 2010 through its IPO, overseeing 15 acquisitions and growing the company from 200 employees to more than 4,000. Under his leadership, Zillow Group has consistently been recognized as among the best companies to work for, and its annual revenue has grown from $30 million to $1.3 billion.

The acquisition strategy was aggressive and strategic. The company made its first acquisition in 2011 when it purchased Postlets, a digital real estate listing and distribution platform. In 2015, Zillow purchased Trulia, a major competitor, in a $2.5 billion deal. At that time, Zillow and Trulia combined to account for 70 percent of online real estate searches.

The Trulia acquisition was particularly brilliant. Rather than fighting a costly war for market share, Zillow simply bought its biggest competitor, creating an unassailable position in online real estate. The combined entity controlled the vast majority of consumer real estate searches, giving it unprecedented leverage with agents and advertisers.

Since July 20, 2011, Zillow Group's market cap has increased from $902.10M to $19.58B, an increase of 2,070.00%. That is a compound annual growth rate of 24.41%. These returns crushed the broader market and validated the portal model that many had doubted.

Under Rascoff's leadership, Zillow became more than just a valuation website. It evolved into a comprehensive real estate platform, adding mortgage services, rental listings, agent reviews, and mobile apps. The company was building what Rascoff called a "real estate transaction platform"—a one-stop shop for everything related to buying, selling, or renting a home.

By 2018, the company was generating over a billion dollars in annual revenue, primarily from advertising sold to real estate agents. The irony was delicious: the same agents who had once protested the Zestimate were now Zillow's biggest customers, spending thousands of dollars monthly to reach its massive audience.

VI. The iBuying Adventure: Zillow Offers (2018–2021)

The boardroom at Zillow's Seattle headquarters in early 2018 was electric with possibility. Spencer Rascoff, now seven years into his CEO tenure, was pitching the board on the company's most audacious bet yet: becoming not just a marketplace for real estate, but an actual participant—buying and selling homes directly.

The vision was compelling. After finding success with its pilot home-flipping business in Phoenix and Las Vegas, the real estate listing site took the program, known as Zillow Offers, nationwide in 2018. At the time, Zillow CEO Rich Barton told investors that within three to five years the home-flipping business could bring in up to $20 billion in annual revenue for Zillow.

The logic seemed unassailable. Zillow had the best data in the industry, millions of users, and deep pockets from its successful portal business. If anyone could crack the code on "iBuying"—using technology to instantly purchase homes from sellers—it should be Zillow. Competitors like Opendoor and Offerpad were already proving the model could work. Why shouldn't Zillow, with all its advantages, dominate this space too?

Online real estate giant, Zillow, launched a home iBuying program back in 2018. The platform used a sophisticated algorithm to value homes and project future value if minor repairs were performed. Zillow's business model was to use the algorithm to purchase homes directly from sellers, do light renovations, and flip homes for a profit.

The early results were encouraging. The company expanded rapidly, moving into market after market. By 2021, the business was generating billions in revenue. But something was fundamentally wrong beneath the surface. The Zestimate algorithm—brilliant for consumer engagement—wasn't designed for the precision required in actual transactions. Zestimates, Zillow's market valuation tool that drives these buying/forecasting decisions, was designed to attract and engage consumers, not to drive a massive home buying and selling business. Companies built around iBuying designed their pricing algorithms specifically for the purpose of maximizing margins in buying/selling real estate at scale.

Then came the perfect storm of 2021. The pandemic had created unprecedented volatility in housing markets. Supply chains were broken. Labor was scarce. And most critically, Zillow's algorithms couldn't keep up with rapidly changing prices. In Q3 -- the three months that broke the business -- Zillow purchased more houses than in the previous 18 months combined.

The scale of the disaster was breathtaking. During the third quarter, Offers bought 9,680 homes, but only sold 3,032, partially due to its constrained logistical capacity to renovate and resell the properties. The company's statements show the average Offers gross profit per home sold was a loss of USD$80,771, while the average Offers revenue per home was USD$386,722.

By October 2021, the situation was untenable. The company was hemorrhaging money on nearly every transaction. In Phoenix, one of its key markets, the numbers were catastrophic: In the Phoenix market, 93% of Zillow-owned properties are listed for sale for less than what Zillow bought them for.

VII. The Shutdown & Aftermath (2021–2022)

The emergency board meeting on November 2, 2021, would go down as one of the most dramatic moments in Zillow's history. Rich Barton, who had returned as CEO in 2019, delivered the verdict personally. The company would immediately shut down Zillow Offers, lay off 2,000 employees—25% of its workforce—and take massive writedowns on its inventory.

"We just determined that being an iBuyer was too risky, too volatile and ultimately addressed too few customers," Barton said. But his next words revealed the human cost: He added that, in closing the business, "the logic is clear, the emotion is difficult" because of the layoffs.

The financial carnage was staggering. After racking up over $1 billion in losses over 3.5 years, Zillow is closing the business down. The third quarter alone saw the business lost more than $380 million in the third quarter. The company announced quarterly losses of $330 million (vs positive earnings of $40m from Q3 2020).

What made the failure particularly painful was how preventable it seemed in hindsight. "We've determined the unpredictability in forecasting home prices far exceeds what we anticipated and continuing to scale Zillow Offers would result in too much earnings and balance-sheet volatility." This wasn't a technology failure—it was a fundamental misunderstanding of the business they had entered.

The contrast with competitors was stark. While Zillow was imploding, Opendoor and Offerpad continued operating. The difference? This may be because they started from the ground up to be iBuyers (Opendoor, Offerpad). They had built their entire operations around buying and selling homes, while Zillow had tried to bolt this capability onto an existing advertising business.

The market reaction was swift and brutal. Zillow's stock plummeted, wiping out billions in market value. But interestingly, Shares of Opendoor rose 7% in extended trading. The market understood something important: iBuying itself wasn't dead—Zillow just couldn't execute it.

The disposal of inventory became its own saga. We found that Zillow closed 32,292 home sales from January 2019 to March 2022. Zillow sold 5,013 of those homes to institutional homebuyers, with the majority of the sales occurring after Zillow announced it would shutter its iBuying business. The company was essentially conducting a fire sale, often to the very institutional investors it had once hoped to compete against.

For employees, the shutdown was devastating. These weren't just numbers on a spreadsheet—they were people who had believed in the vision of transforming real estate transactions. Many had joined Zillow specifically to work on Offers, seeing it as the future of the company. Now they were being shown the door.

VIII. The Phoenix Rising: Post-iBuying Strategy (2022–Present)

The aftermath of the iBuying disaster could have broken Zillow. Instead, it catalyzed one of the most impressive corporate pivots in recent tech history. In February 2022, just three months after the shutdown announcement, Rich Barton unveiled a new vision that would redirect the company's ambitions while staying true to its core strengths.

"The size of the prize is large when we become the central integrator — connecting pieces of the fragmented process and turning dreamers into transactors within the 'housing super app,'" Barton wrote. The company expects the plan to translate into $5 billion of annual revenue with a 45% margin (calculated by EBITDA) by the end of 2025.

The "housing super app" concept was brilliant in its simplicity. Rather than trying to become a principal in transactions (buying and selling homes), Zillow would become the connective tissue—the platform that links all the disparate parts of a real estate transaction. "Anyone who has been through a move knows how challenging it can be to research, shop, select, finance, appraise, close and have to connect all these separate vendors and spend time taking down information and managing the process yourself," Zillow Group CEO Rich Barton told analysts.

The execution began immediately. Zillow shares its vision for the future of home buying, selling and renting: the "housing super app." ... Zillow Group acquires ShowingTime, the industry leader in home-touring technology. This acquisition, completed in 2021 for a reported $500 million, gave Zillow the infrastructure to coordinate home tours—a critical piece of the transaction puzzle.

The strategy was multi-pronged. Since infamously shuttering its iBuying program in November 2021, Zillow has refocused itself on its "Five Growth Pillars": financing, touring, seller solutions, enhancing partnerships and integrating services. Each pillar represented a different revenue stream and a different way to monetize the massive audience Zillow had built.

By 2024, the transformation was evident. Zillow's latest momentum is a manifestation of its strategy to diversify revenue across the transaction as it transitions from a lead gen platform to a housing "super app." As Zillow scales new revenue streams, including Zillow Home Loans, Rentals, ShowingTime+, and Seller Solutions, it is planting important seeds for its next phase of growth.

The numbers told the story of resilience. Even with flat revenue, Zillow has significantly outperformed the market during this period, with the magnitude dependent on whether you consider Zillow a lead generation platform or a housing "super app." The company had successfully diversified: "Our revenue base has diversified to the point where a majority of our revenue is now derived from sources other than buy side fees. "The most recent chapter in Zillow's story came in August 2024, with another leadership transition that felt more like a graduation than a crisis. Zillow Group named a new CEO, longtime company executive Jeremy Wacksman, announcing that co-founder and two-time CEO Rich Barton will be shifting to the new role of co-executive chair of the real estate media and technology company, joining co-founder Lloyd Frink in the role.

He was CEO of the company from its founding until 2010, returned to the position in 2019, and transitioned to the role of co-executive chairman in August 2024. The timing was telling—unlike his 2019 return during crisis, this transition happened during success. "The strategy is working really well," Barton said. "The business is in great shape. The top line is growing nicely. The profits are growing nicely. The outlook is good."

Wacksman, 47, with a background in both engineering and business, is a veteran of companies including Microsoft and Procter & Gamble who has been at Zillow Group for more than 15 years, serving in roles as chief marketing officer, president of the company's flagship Zillow brand, and since early 2021 as its chief operating officer. His appointment represented continuity rather than disruption—a sign that Zillow had finally found its sustainable path forward.

IX. Playbook: Business & Investing Lessons

The Zillow story offers a masterclass in marketplace dynamics, strategic pivots, and the limits of technology disruption. Each phase of the company's evolution teaches distinct lessons about building and scaling technology businesses in traditional industries.

The Power of Network Effects in Marketplaces

Zillow's core strength has always been its network effects, but they work differently than typical social networks. Every home that gets "Zillowed" creates value for neighbors curious about property values. Every agent who advertises brings listings that attract more consumers. Every consumer who searches provides data that improves the Zestimate. It's a virtuous cycle that becomes nearly impossible to disrupt once it reaches critical mass.

The numbers prove the moat's depth: over 200 million monthly users generating 2 billion searches annually. This isn't just traffic—it's intent. People don't browse Zillow casually; they're planning life's biggest financial decision. That focused attention is worth billions to real estate professionals desperate to reach serious buyers and sellers.

When to Pivot vs. When to Persevere

The iBuying shutdown decision was remarkable for its decisiveness. Many companies would have tried to "fix" the algorithm, raise more capital, or gradually wind down the business. Barton didn't hesitate: complete shutdown, immediate layoffs, full pivot. The lesson? When a strategic bet threatens the core business, cut quickly and completely.

Compare this to Zillow's approach with the Zestimate controversy in 2006. Despite industry backlash and accuracy concerns, they persevered because the Zestimate was fundamental to their consumer value proposition. The difference? The Zestimate enhanced their core business model; iBuying replaced it with something fundamentally different.

The "Power to the People" Disruption Playbook

Barton's pattern across Expedia, Zillow, and Glassdoor reveals a repeatable disruption formula: find industries where institutions hoard valuable information, liberate that information for consumers, then monetize the resulting attention from the very institutions you disrupted. It's judo economics—using an opponent's strength against them.

The genius is that once consumers have access to information, they can't be convinced to give it back. Real estate agents may have hated the Zestimate, but once millions of Americans expected instant home valuations, agents had no choice but to work within Zillow's ecosystem.

Capital Allocation: Build vs. Buy

Zillow's acquisition strategy demonstrates sophisticated capital allocation. The Trulia acquisition for $2.5 billion eliminated their biggest competitor and created an unassailable market position. The ShowingTime acquisition for $500 million gave them critical transaction infrastructure. Each acquisition either eliminated competition or added capabilities that would have taken years to build organically.

But the iBuying experiment shows the flip side: sometimes building internally leads to expensive failures. The company tried to develop a completely new competency—operational excellence in real estate transactions—that was orthogonal to their core skills in software and marketplaces.

Managing a Two-Sided Marketplace with Antagonistic Participants

Perhaps Zillow's greatest achievement is successfully serving both consumers and agents despite their inherently conflicting interests. Consumers want transparency, low commissions, and maximum information. Agents want to control information flow, maintain commissions, and intermediate transactions.

Zillow threads this needle by making agents more efficient rather than obsolete. The company provides tools that help agents identify serious buyers, manage leads, and close deals faster. Agents may not love Zillow, but they need it—and Zillow profits from that dependency.

The Risks of Moving from Asset-Light to Asset-Heavy

The iBuying disaster perfectly illustrates why software companies struggle with physical operations. Zillow went from a business with 80%+ gross margins and minimal capital requirements to one requiring billions in working capital with single-digit margins. They underestimated everything: operational complexity, market risk, capital intensity, and execution difficulty.

The lesson for investors: when asset-light businesses venture into asset-heavy operations, the risk isn't just financial—it's existential. Different business models require different organizational capabilities, and those capabilities can't be acquired overnight.

X. Analysis & Bear vs. Bull Case

In 2024, Zillow Group's revenue was $2.24 billion, an increase of 14.96% compared to the previous year's $1.95 billion. Losses were -$112.00 million, -29.11% less than in 2023. These numbers tell a story of recovery and resilience, but they only scratch the surface of the investment thesis.

Competitive Moats

Zillow's moat has three layers, each reinforcing the others. First is brand recognition—"Zillow" has become a verb like "Google," representing a massive intangible asset. Second is data superiority—decades of user behavior, property information, and transaction data that improves their algorithms and user experience. Third is audience scale—when you have 200 million monthly users, you become the unavoidable partner for anyone wanting to reach home buyers.

The network effects are particularly powerful because they work in multiple directions. More users attract more agents, who bring more listings, which attract more users. More data improves the Zestimate, which drives more traffic, which generates more data. It's a flywheel that accelerates over time.

Major Risks

The bear case centers on three critical vulnerabilities. First, the commission structure disruption following recent NAR settlements could fundamentally alter Zillow's revenue model. If buyer agent commissions decline or disappear, Zillow's core advertising revenue could face severe pressure.

Second, CoStar's aggressive entry with Homes.com represents the first credible, well-funded threat to Zillow's dominance. CoStar has deep pockets, existing real estate industry relationships, and a proven ability to build dominant marketplaces. Their "Your Listing, Your Lead" model directly attacks Zillow's value proposition to agents.

Third, technological disruption remains a constant threat. AI could enable new models we haven't imagined—perhaps direct consumer-to-consumer transactions, or AI agents that negotiate on behalf of buyers and sellers, eliminating human intermediaries entirely.

Growth Opportunities

The bull case rests on Zillow's ability to capture more value from each transaction. Currently, they monetize only a tiny fraction of the $2 trillion in annual U.S. real estate transactions. Every additional service they integrate—mortgages, title insurance, home insurance, moving services—represents billions in potential revenue.

International expansion remains largely untapped. While Zillow has focused exclusively on the U.S. market, the playbook could work in many other countries with similar real estate structures. Markets like Canada, Australia, and the UK present obvious opportunities.

The rental market represents another massive opportunity. As homeownership becomes less attainable for younger generations, Zillow's rental marketplace could become increasingly valuable. The company already has strong traction here, with rental revenue growing consistently even during the housing market downturn.

The Future of Real Estate Transactions

The long-term question isn't whether Zillow will survive—it's whether real estate transactions will remain complex enough to require Zillow's orchestration. If transactions simplify dramatically through regulatory changes or technological innovation, Zillow's role as coordinator becomes less valuable.

But complexity in real estate seems remarkably persistent. Despite decades of technological advancement, buying a home remains byzantine, involving multiple parties, extensive paperwork, and significant emotional and financial stress. As long as that complexity exists, there's value in a platform that makes it manageable.

Zillow's position is similar to other dominant marketplaces that survived predictions of disintermediation. Just as travel agents were supposed to disappear but Expedia thrived, and job boards were supposed to die but Indeed prospered, Zillow has found a way to remain essential even as the industry evolves.

XI. Epilogue & Final Thoughts

Standing back and surveying Zillow's 18-year journey, what emerges is a story of remarkable adaptation. This is a company that has reinvented itself three times: from startup disruptor to public company, from advertising platform to aspiring market maker, and now to something approaching a true real estate operating system.

If we were running Zillow today, the focus would be on three priorities. First, accelerate the integration of services to make the super app vision reality—every friction point removed increases transaction likelihood and revenue per user. Second, expand internationally before competitors establish dominant positions in other English-speaking markets. Third, invest aggressively in AI not for pricing homes, but for personalizing the home search experience and predicting user intent.

The biggest surprise from researching this story is how personal real estate remains despite all attempts at digitization. Zillow succeeded not by eliminating human agents but by making them more effective. The iBuying failure occurred partly because it removed the human element that buyers and sellers value. The lesson: in emotional, high-stakes transactions, technology amplifies human capability rather than replacing it.

For founders, Zillow offers a masterclass in marketplace building. Start with something people desperately want but can't get (information), build habit-forming engagement (the addictive Zestimate), then gradually expand your value proposition. Most importantly, be willing to serve multiple stakeholders with conflicting interests—that complexity creates defensibility.

For investors, the key lesson is about business model fit. Zillow as an advertising and software business works brilliantly—high margins, network effects, minimal capital requirements. Zillow as an asset-heavy real estate operator was a disaster. The best businesses know their core competencies and resist the temptation to venture beyond them, no matter how adjacent the opportunity appears.

The future of real estate technology won't be about eliminating friction entirely—some friction serves a purpose, providing time for consideration and protecting consumers from impulsive decisions. Instead, it will be about intelligent friction: keeping the valuable human elements while automating the mindless paperwork, maintaining emotional support while eliminating information asymmetry.

Zillow's next chapter under Jeremy Wacksman will likely be less dramatic than the Barton era—fewer moonshots, more systematic execution. But that's exactly what the company needs. The foundation is solid, the strategy is clear, and the market opportunity remains enormous. The portal that became a real estate empire isn't done growing; it's just growing more intelligently.

The real estate industry spent years fearing that Zillow would disrupt them out of existence. Instead, Zillow became their largest customer acquisition channel, their technology provider, and increasingly, their operating system. It's a reminder that in complex industries, the most successful disruptions don't destroy the old system—they rewire it, making it work better for everyone involved.

That's the true genius of Rich Barton's "Power to the People" philosophy. By empowering consumers with information, he didn't eliminate the need for professionals—he made those professionals more valuable by forcing them to compete on service rather than information asymmetry. In doing so, he built not just a company, but a new equilibrium in one of America's largest industries.

The portal that started with a simple question—"What's my home worth?"—has become the answer to a much bigger one: "How do we make real estate work better?" Eighteen years in, Zillow is still finding new answers to that question. And with a market cap approaching $20 billion and growing, investors are betting those answers will be worth quite a lot indeed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube