Flutter Entertainment: The Story of a Global Betting Empire

I. Introduction & Episode Roadmap

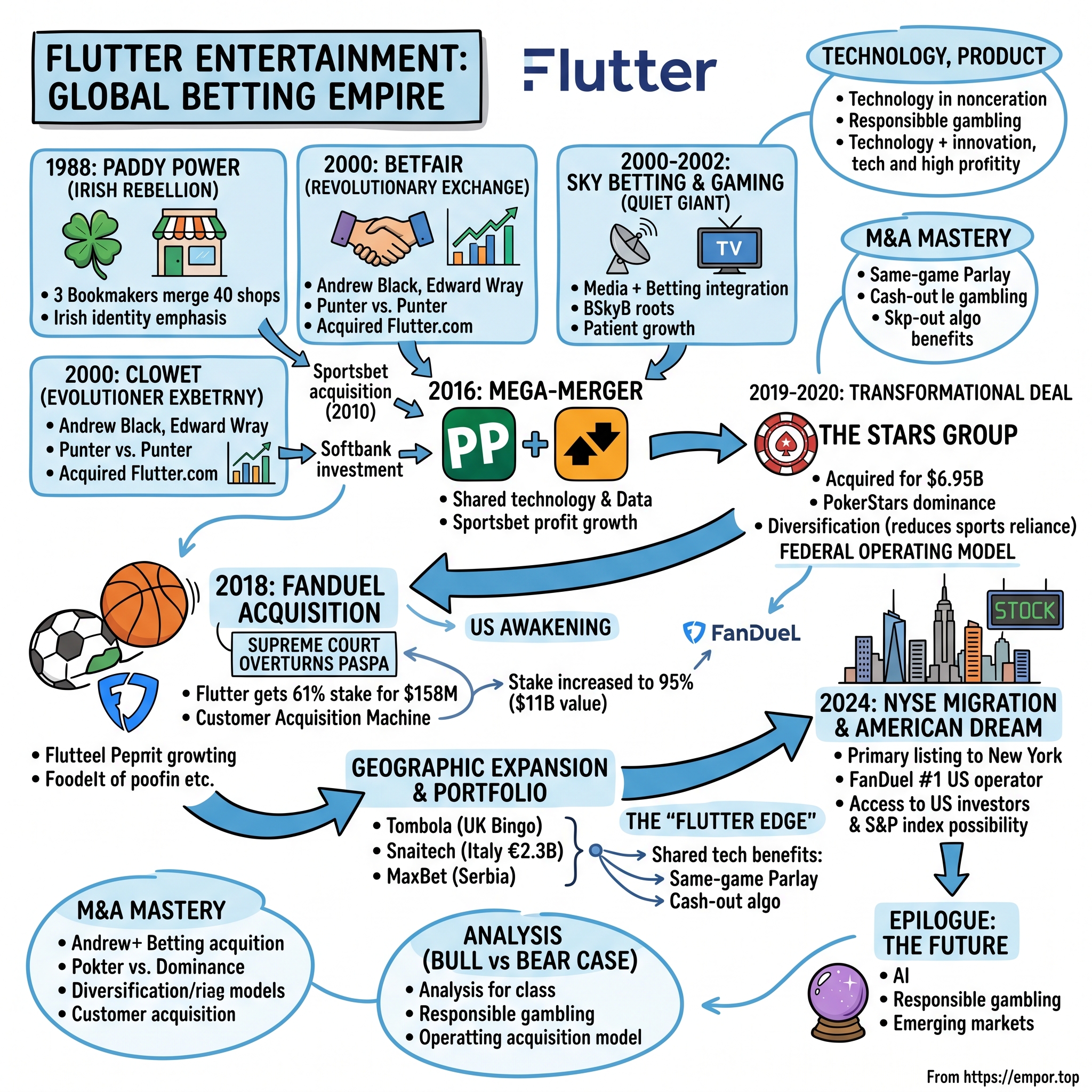

Picture this: It's May 31, 2024, and the opening bell rings at the New York Stock Exchange. But this isn't your typical IPO celebration. Instead, it marks the moment when Flutter Entertainment—a company born from Irish rebellion against British bookmakers—officially moves its primary listing from London to New York, cementing its status as the world's largest online betting company with a market capitalization exceeding $53 billion.

Flutter today commands $53.5 billion in market value with trailing twelve-month revenue of $14.3 billion, owning an empire that spans FanDuel, Betfair, Paddy Power, PokerStars, Sky Betting & Gaming, and Sportsbet. The company operates in over 100 countries with nearly 14 million average monthly users. But how did we get here?

The story of Flutter isn't just about consolidation in the gambling industry. It's about three revolutionary origin stories converging: Irish bookmakers fighting British invasion, a grandson of an anti-gambling MP creating the world's first betting exchange, and a satellite television company quietly building a digital betting powerhouse. Each thread weaves into a narrative about timing, technology, and the transformative power of strategic acquisitions.

The central question driving our exploration: How did two Irish rebels and a betting exchange revolutionary create what would become a $50+ billion gambling empire that now dominates from Dublin to Las Vegas?

II. The Founding DNA: Three Origin Stories Converge

The Irish Rebellion: Paddy Power (1988)

The year was 1988, and British bookmaking giants like Ladbrokes and Coral were crossing the Irish Sea, eager to colonize Ireland's betting market. Three Irish bookmakers—Stewart Kenny, David Power, and John Corcoran—saw the writing on the wall. Separately, they were sitting ducks. Together, they might just survive.

The three men merged their forty shops to form Paddy Power in 1988. Stewart Kenny brought ten shops he'd opened after selling Kenny O'Reilly Bookmakers to Coral in 1986. John Corcoran contributed shops that had traded as Patrick Corcoran. David Power, son of Richard Power and inheritor of the Power betting legacy, brought the strongest brand name to the table.

The Power name was considered the strongest brand among the merged shops, while the "Paddy" name and green colouring emphasised the chain's Irishness at a moment when national identity mattered in the betting shop wars. This wasn't just a business decision—it was a declaration of independence.

The company went public in December 2000 on the London Stock Exchange, using the capital to fund UK expansion. By 2005, they operated 195 outlets across Ireland and the UK. But physical shops were just the beginning. In May 2010, Paddy Power acquired a majority stake in Australian bookmaker Sportsbet.com.au, planting a flag in what would become one of their most profitable territories.

The Revolutionary: Betfair (2000)

Meanwhile, in a London garden party in 1998, two men were having a conversation that would revolutionize gambling. Andrew Black, a software developer and professional gambler, was explaining his idea to Edward Wray, a JP Morgan vice president. Black's vision was radical: What if punters could bet against each other directly, cutting out the bookmaker entirely?

The irony was delicious. Black was the grandson of Sir Cyril Black, a Tory MP for Wimbledon who had campaigned against gambling. Yet here was Andrew, having been kicked out of Exeter University for spending too much time at the bookies, proposing to turn the entire industry upside down.

The company was founded in June 2000, by Andrew Black and Edward Wray. Their launch campaign was pure theater: Black and Wray appeared in gangster clothing, set up fake bookmakers picketing outside the launch party, and held a New Orleans style funeral running a coffin through the city of London with the slogan "Death to the bookmaker."

The concept was brilliant in its simplicity. Betfair operated on a model more similar to a financial exchange, allowing multiple small bets to fill a position offered by a gambler wishing to place a large stake on a wager. Within months, they had a competitor problem to solve. In January 2002, Betfair acquired rival Flutter, securing 90% of the bet exchange market in the UK within a few years of launch.

By 2006, the company's value had exploded. Softbank purchased 23% of Betfair in early April 2006, valuing the company at £1.5 billion. When Betfair went public in October 2010, the company floated on the London Stock Exchange at £13, valuing it at £1.4bn, making Black's 15% stake worth approximately £200 million.

The Quiet Giant: Sky Betting & Gaming (2000-2002)

While Paddy Power fought for Irish independence and Betfair proclaimed the death of bookmakers, a third player was emerging from an unexpected corner: satellite television. BSkyB (now Sky) had acquired Sports Internet Group in 2000, seeing an opportunity to leverage its sports broadcasting dominance into betting. In July 2002, they rebranded the operation as Sky Bet.

What made Sky Bet different wasn't revolutionary technology or provocative marketing—it was integration. Sky controlled the UK's premium sports broadcasts. They knew exactly when viewers were most engaged, which matches drew the biggest audiences, and how to seamlessly blend content with commerce. While others were betting companies trying to create media, Sky was a media company learning to bet.

III. The Early Digital Revolution (2000–2010)

The 2000s were the Wild West of online gambling. Regulatory frameworks were nascent, technology was rapidly evolving, and customer acquisition costs were a fraction of what they'd become. Each of our three protagonists took radically different approaches to this frontier.

Paddy Power embraced controversy as strategy. Their marketing campaigns deliberately pushed boundaries, understanding that regulatory fines were simply a cost of customer acquisition. In November 2008, they offered 16–1 odds that United States President Barack Obama 'would not finish' his first term, and after Stoke City lost their opening game of the 2008–09 season, controversially paid out on bets on them being relegated.

This wasn't recklessness—it was calculated brand building. Every controversial market, every early payout, every cheeky advertisement built Paddy Power's reputation as the "punter's pal," the bookie that was on your side even when they were taking your money.

Betfair, meanwhile, was building a different kind of moat. In their first year, they did a few hundred thousand pounds in commission, the second year six million, and the third year 35 million. The network effects were extraordinary—more liquidity attracted more punters, which attracted more liquidity.

The 2008 financial crisis created unexpected opportunities. Traditional bookmakers, laden with retail property and fixed costs, struggled. But online-first operators with variable cost structures thrived. Paddy Power went shopping, acquiring smaller operators and consolidating the Irish market. Betfair expanded internationally, moving operations to Gibraltar in 2011 to optimize their tax structure.

Sky Bet operated with the patience only a subsidiary can afford. Backed by BSkyB's billions, they didn't need to show immediate profits. Instead, they invested in technology, integration, and slowly building a customer base that trusted the Sky brand. By 2010, they had quietly become one of the UK's largest online bookmakers, though few outside the industry noticed.

IV. The First Mega-Merger: Paddy Power + Betfair (2016)

September 8, 2015: The impossible was announced. Paddy Power and British rival Betfair agreed terms for a merger, structured as an acquisition of Betfair by Paddy Power with the enlarged entity based in Dublin. The cultural clash seemed insurmountable—Paddy Power, the cheeky Irish bookmaker, merging with Betfair, the technology-driven exchange that had proclaimed the death of bookmaking.

The business was owned 52% by the former Paddy Power shareholders and 48% by the former Betfair shareholders. The merger was completed on 2 February 2016. The strategic rationale was compelling: Paddy Power brought brand strength, retail presence, and the crown jewel—Sportsbet in Australia. Betfair brought technology, the exchange model, and credibility with sophisticated punters.

But mergers are where culture eats strategy for breakfast. On 5 April 2016, it was announced that 650 jobs in the United Kingdom and Ireland would be lost at the company. The cuts were brutal but necessary—duplicate functions, overlapping territories, competing technologies all needed rationalizing.

The hidden genius of the deal only became apparent later. Sportsbet, Paddy Power's Australian acquisition from 2010, was growing at extraordinary rates. Australia's gambling culture, high smartphone penetration, and concentrated media market created perfect conditions. By 2018, Sportsbet was generating more profit than the entire UK retail operation.

Betfair's exchange, meanwhile, provided something invaluable: data. Every bet placed, every price movement, every market inefficiency was captured and analyzed. This data would power the risk management and pricing algorithms that would give the combined entity an edge traditional bookmakers couldn't match.

V. The US Awakening: FanDuel Acquisition (2018)

May 14, 2018, 10:00 AM Eastern: The Supreme Court struck down the Professional and Amateur Sports Protection Act (PASPA), ending the federal prohibition on state-authorized sports betting. The decision had been telegraphed for months, but its impact was seismic.

Paddy Power Betfair had been preparing. They'd been watching FanDuel, one of America's two daily fantasy sports giants, struggle to find a path to profitability. Daily fantasy was a brutal business—massive marketing spend, regulatory uncertainty, and a duopoly with DraftKings that resembled trench warfare.

In May 2018, Paddy Power Betfair announced its intent to acquire FanDuel following the overturning of the federal prohibition on sports betting. The company paid $158 million and merged its existing US operations into FanDuel Group, taking a 61% controlling stake with options to increase to 80% after three years and 100% after five.

The price seemed absurdly low for a brand that had raised over $400 million in venture capital. But Flutter (as the company would soon rebrand itself) saw what others missed: FanDuel wasn't buying a daily fantasy company—they were buying a customer acquisition machine with 8 million registered users, brand recognition in every state, and most importantly, regulatory relationships that would take years to replicate.

The integration was masterful. Flutter provided the treasury betting technology, risk management, and deep pockets for bonuses. FanDuel provided the brand, the customer base, and the local knowledge. New Jersey launched retail sports betting just one month after the PASPA ruling, on June 14, 2018, and FanDuel was ready.

In December 2020, Flutter announced it would purchase an additional stake in FanDuel Group from Fastball Holdings for $4.1 billion, increasing its stake to 95%. The same asset they'd bought for $158 million just 30 months earlier was now valued at over $11 billion. It might be the greatest acquisition in gambling history.

VI. The Transformational Deal: Stars Group Acquisition (2019–2020)

October 2, 2019: Flutter announced its largest deal ever. Flutter Entertainment announced its acquisition of Canadian gambling operator The Stars Group for US$6.95 billion, creating the world's largest online gambling company based on revenues.

The Stars Group brought PokerStars, the world's dominant online poker platform, but that wasn't the real prize. In April 2018, Stars Group had acquired UK-focused Sky Betting & Gaming for cash and stock worth $4.7 billion. Flutter was essentially buying back one of the UK's best operators that CVC had acquired from Sky for £600 million in 2014, then flipped to Stars for £3.4 billion in 2018.

The timing was exquisite. The combined companies would have had annual revenues of £3.8 billion in 2018. But more importantly, the deal brought diversification. At the time, Flutter derived 75% of its revenues from sports betting. The acquisition expanded product offerings and significantly reduced reliance on sports-related income, a decision that proved pivotal during the Covid-19 pandemic when there was no sport to bet on.

The mega-merger was completed on May 5, 2020, with Flutter purchasing all shares in TSG. The entire enlarged issued share capital was admitted to the premium listing at 8am BST on May 5.

The integration philosophy was revolutionary for the gambling industry. Rather than forcing everything onto one platform, Flutter maintained a "federal" model. Flutter would employ a federal operating model, where each regional arm has independence rather than having strategy determined by group management, leveraging teams' local knowledge while having access to broader group resources.

VII. Geographic Expansion & Portfolio Building (2020–2024)

With the Stars deal complete and the US market exploding, Flutter could have rested. Instead, they accelerated, pursuing a "local hero" strategy—buying the number one or two player in each market and keeping the local brand.

The shopping spree was relentless. In January 2022, they acquired Tombola, the UK's leading online bingo operator. In September 2024, Flutter announced its acquisition of Snaitech, one of Italy's leading gambling operators, in a €2.3 billion deal. They took a 51% stake in Serbia's MaxBet for €141 million, giving them a foothold in the Balkans.

Each acquisition followed the same playbook: Keep the local brand and management, plug in Flutter's technology platform and risk management, leverage global supplier relationships for better terms, and watch margins expand. The "Flutter Edge"—their shared technology platform—meant each new acquisition immediately benefited from billions in cumulative R&D spend.

The geographic diversification also provided regulatory hedging. When the UK introduced stricter affordability checks, Australian profits compensated. When Australia raised taxes, the US growth accelerated. No single market could tank the entire business.

VIII. The NYSE Migration & American Dream (2024)

The boardroom discussions started in early 2023. Flutter was generating more revenue in the US than the UK. FanDuel had achieved what seemed impossible— US net gaming revenue market share of 53.4%, up from 43.2% in 2022. Yet the company traded at a discount to pure-play US competitors like DraftKings.

On January 29, 2024, Flutter's ordinary shares began trading on the NYSE. On May 1, 2024, shareholders passed the special resolution to transfer Flutter's listing category from a Premium Listing to a Standard Listing on the LSE.

On May 31, 2024, Flutter Entertainment announced that its primary listing was now on the New York Stock Exchange, with the London listing becoming secondary.

The rationale was more than symbolic. If Flutter could get itself added to the S&P index one day, it would be another meaningful bump in the value of its shares, since holdings of that index are mimicked by trillions of dollars' worth of investment funds. US investors understood the US opportunity in ways European investors never could.

Peter Jackson, Flutter's CEO, was blunt about the ambition: "This closely follows the recent move of our operational headquarters to New York, reflecting the increasing importance of the US sports betting and iGaming market to our business. We have a fantastic position in the US, with FanDuel the clear number one operator".

IX. Technology, Product & The Flutter Edge

Inside Flutter's technology centers in Dublin, Leeds, and Porto, 5,000 engineers and data scientists work on what the company calls the "Flutter Edge." This isn't marketing fluff—it's a genuine competitive advantage built over two decades and billions in investment.

Consider the complexity: Every second, Flutter's systems process thousands of bets across hundreds of markets in dozens of currencies while simultaneously calculating real-time odds, managing risk exposure, detecting problem gambling patterns, preventing money laundering, and personalizing content for millions of users.

Sky Bet alone made 30,000 software releases in 2020—that's 82 per day. This isn't moving fast and breaking things; it's moving fast and nothing can break because millions of pounds are at stake every minute.

The data science is staggering. Flutter knows not just what you bet on, but when you bet, how you bet, what makes you bet more, and critically, what makes you stop. They can predict with alarming accuracy which customers will become valuable, which will cause problems, and which will churn.

The shared platform means innovations in one brand immediately benefit all others. When FanDuel develops a same-game parlay product that increases handle by 20%, Sportsbet can launch it in Australia within weeks. When Sky Bet creates a cash-out algorithm that improves margins by 10 basis points, Paddy Power implements it immediately.

X. Playbook: M&A Mastery & Portfolio Management

Flutter's M&A playbook should be taught in business schools. While competitors overpaid for declining assets or forced integration destroyed value, Flutter developed a reproducible formula for creating value through acquisition.

First, they only buy leaders. No turnarounds, no "synergy plays," no number three players they'll somehow make number one. They pay premium prices for premium assets—FanDuel at $158 million seemed expensive until it wasn't, Stars Group at $7 billion seemed crazy until the synergies materialized.

Second, they preserve entrepreneurial culture. The founders and management teams usually stay, brands remain unchanged, and local decision-making is preserved. This isn't kindness—it's economics. The cost of customer acquisition in gambling is so high that destroying brand value through integration is corporate suicide.

Third, they're patient with capital. FanDuel lost money for years while Flutter poured in billions for customer acquisition. But they understood the unit economics—once you acquire a sports bettor, getting them to try casino games is relatively cheap, and casino margins are double sports betting.

The regulatory expertise accumulated across 100+ countries creates a massive moat. When new markets open, Flutter can navigate licensing, comply with regulations, and launch products faster than anyone. They've seen every regulatory framework, faced every challenge, and built relationships with every regulator.

XI. Analysis & Bear vs. Bull Case

The Bull Case

The numbers tell a compelling story. Flutter's stock price sits at $304.02 with a market cap of $53.5B and trailing 12-month revenue of $14.3B. US sports betting is still in its infancy—only 23 states have launched, with California, Texas, and Florida still to come. Each new state is worth hundreds of millions in revenue.

The iGaming opportunity is even larger. Only seven states have legalized online casino, but it generates double the revenue per capita of sports betting at triple the margins. If iGaming follows sports betting's adoption curve, Flutter's US revenue could triple.

FanDuel's dominance appears sustainable. Network effects in betting are real—liquidity attracts bettors, which improves pricing, which attracts more bettors. The brand is becoming synonymous with sports betting in America, like "Kleenex" or "Google."

Internationally, emerging markets offer decades of growth. Brazil is regulating, India is opening up, and Africa is digitizing rapidly. Flutter's playbook—buy the local leader, plug in technology, expand margins—works everywhere.

The Bear Case

Regulation is the existential threat. Problem gambling concerns are rising, affordability checks are spreading from the UK to other markets, and advertising restrictions are tightening. A single scandal—match-fixing, money laundering, underage gambling—could trigger a regulatory backlash.

Competition is intensifying. DraftKings isn't going away, ESPN Bet has Disney's marketing might, and every casino company is pouring billions into digital. Customer acquisition costs in New Jersey now exceed $1,000 per player. At some point, the economics break.

Market saturation is real. UK online gambling revenue has been flat for three years. Australia is implementing severe restrictions. Once markets mature, growth comes only from market share gains or margin expansion, both finite resources.

The valuation assumes perfect execution. At 25x earnings, Flutter is priced for perfection. Any stumble—a failed acquisition, a regulatory surprise, a technology breakdown—could trigger a severe correction.

XII. Epilogue: The Future of Gambling

Standing in Flutter's New York headquarters, looking at screens showing millions of bets flowing through their systems, it's hard to imagine this empire emerged from forty Irish betting shops resisting British invasion. Stewart Kenny, David Power, and John Corcoran probably never imagined their local rebellion would create a global empire.

Andrew Black and Edward Wray's vision of peer-to-peer betting revolutionized the industry, even if the exchange model ultimately became just one product among many. Their "death to the bookmaker" campaign was premature—the bookmaker didn't die, it evolved, absorbed the exchange model, and became stronger.

The future of Flutter—and gambling—will be shaped by artificial intelligence, regulatory evolution, and changing social attitudes. AI will make pricing perfect and personalization precise, but also raise ethical questions about exploiting behavioral patterns. Regulation will become more sophisticated, potentially mandating affordability checks and loss limits that could halve industry revenues.

Yet gambling is as old as humanity itself. The urge to risk something valuable for the chance of gaining something more valuable is fundamental to human nature. Flutter hasn't created this demand—they've simply made it more accessible, more entertaining, and arguably more dangerous.

The next decade will test whether Flutter can maintain growth while promoting responsible gambling, expand globally while respecting local cultures, and innovate technologically while protecting vulnerable customers. The empire is built, but empires require constant vigilance to maintain.

What would the founders think today? Kenny, Power, and Corcoran would marvel at the global reach but might worry about the distance from the punter. Black and Wray would appreciate the technology but perhaps lament that the "betting exchange revolution" became just another feature in a traditional bookmaker's arsenal.

But they'd all recognize the fundamental truth that made them successful: In gambling, as in business, the house always wins. The only question is who owns the house.

The story of Flutter Entertainment teaches us that industry disruption often comes not from destroying incumbents but from combining their strengths. It shows that strategic M&A, executed with discipline and patience, can create extraordinary value. Most importantly, it demonstrates that in winner-take-all markets with network effects, being number one isn't just better than being number two—it's the only position worth having.

For investors, Flutter represents both the best and worst of modern capitalism: a brilliantly executed roll-up strategy creating enormous shareholder value, built on an industry that profits from human weakness. Whether that's a bug or a feature depends entirely on your perspective.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube