Xcel Energy: From Regional Utility to Clean Energy Pioneer

I. Introduction & Episode Roadmap

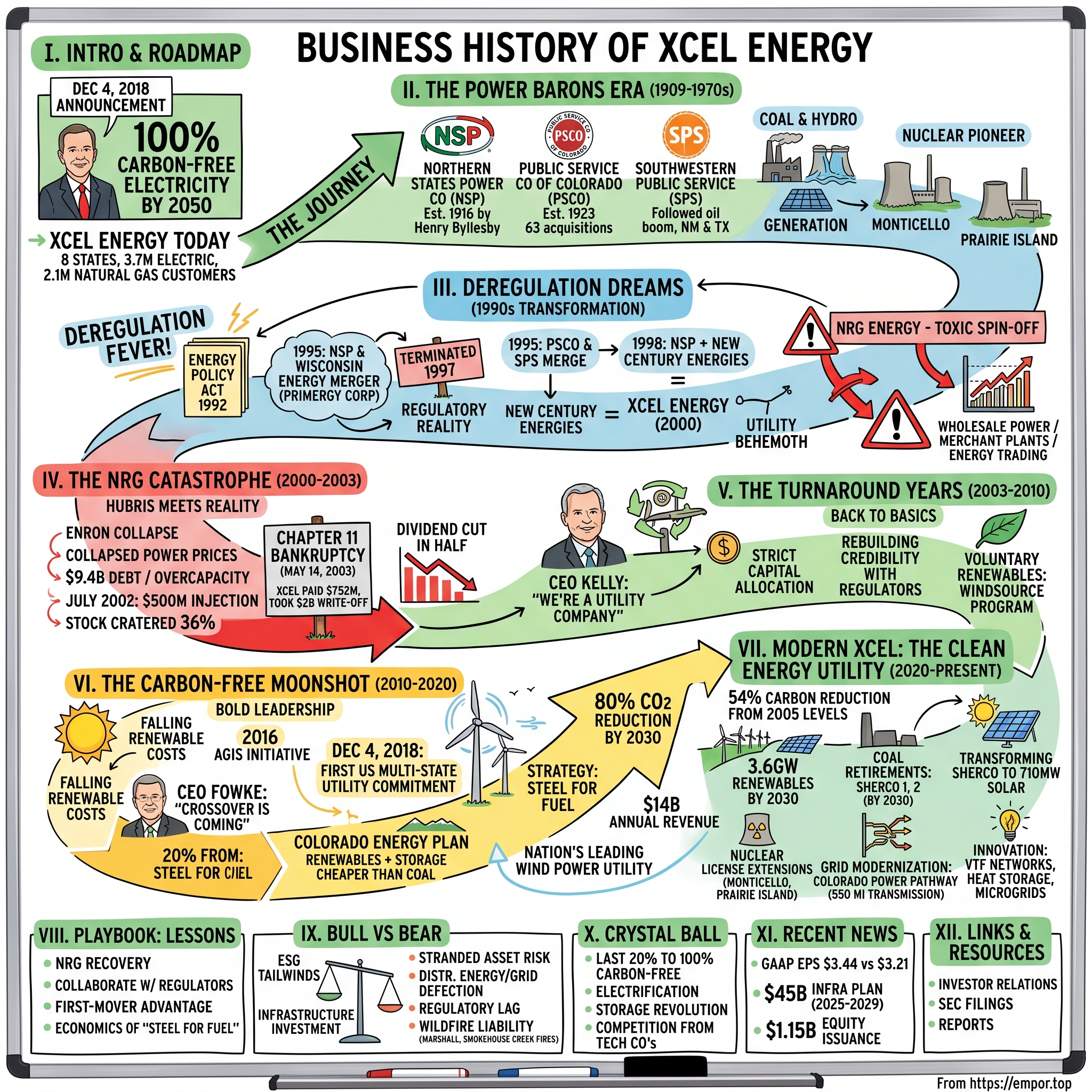

Picture this: It's December 4, 2018, and in a nondescript conference room in Minneapolis, Ben Fowke, CEO of Xcel Energy, is about to make an announcement that will send shockwaves through the utility industry. No major American utility had ever committed to what he was about to promise—100% carbon-free electricity by 2050. The board had signed off, the lawyers had vetted it, but Fowke knew this moment would either position Xcel as the industry's transformation leader or expose them to decades of execution risk.

Today, Xcel Energy stands as a $42.5 billion market cap utility serving 3.7 million electric customers and 2.1 million natural gas customers across eight states—from the frozen plains of Minnesota to the high deserts of New Mexico. But this isn't just another sleepy regulated utility collecting predictable returns. This is the story of how a patchwork of regional power companies, born in the era of Edison and Tesla's current wars, survived near-death from trading desk hubris, and emerged as America's unlikely clean energy pioneer.

The question that drives this entire narrative: How did a collection of century-old regional utilities—companies that once burned coal like it was going out of style—become the first major U.S. utility to commit to complete decarbonization? The answer involves visionary engineers, catastrophic missteps in energy trading, regulatory chess matches, and a bet that getting ahead of the energy transition would create more value than fighting it.

We'll trace this journey from the power baron era of the early 1900s through today's renewable revolution, with particular attention to the NRG disaster that nearly destroyed the company in 2003—a cautionary tale of what happens when utilities try to play investment banker. Along the way, we'll unpack the strategic playbook of regulated utility transformation, examine the economics of the clean energy transition, and assess whether Xcel's first-mover advantage in renewables will translate to superior returns for shareholders.

II. The Power Barons Era: Origins & Early Consolidation (1909-1970s)

The lights first flickered on in 1909 when Washington County Light & Power Company strung its first transmission lines across the rural Minnesota countryside. But the real story begins with Henry Marison Byllesby, an electrical engineer turned empire builder who saw opportunity where others saw only scattered farm towns and fledgling industries. In 1916, Byllesby orchestrated the transformation of that small rural utility into Northern States Power Company—a name that would dominate upper Midwest electricity for the next century.

Byllesby wasn't alone in this consolidation game. Down in Colorado, the Public Service Company of Colorado emerged in 1923 from the merger of several smaller utilities. Within twelve months, PSCo had swallowed 63 electric companies across the state—a feeding frenzy of acquisitions that would make today's private equity firms blush. The playbook was elegantly simple: buy up local utilities, integrate their grids, lobby for exclusive service territories, and enjoy monopoly returns blessed by friendly regulators.

Meanwhile, in the dusty expanses of the Southwest, another piece of the future Xcel puzzle was taking shape. Southwestern Public Service traced its roots back to 1904 in Roswell, New Mexico—yes, that Roswell, though aliens wouldn't become the town's claim to fame for another four decades. SPS grew by following the oil boom across Texas and New Mexico, stringing power lines to pump jacks and refinery towns, building an empire on petroleum's insatiable appetite for electricity. The post-war decades saw NSP transform from a regional utility into a nuclear pioneer. The company wasn't content with coal and hydroelectric—it wanted to harness the atom. NSP began operations at its first nuclear power plant, the Pathfinder Atomic Power Plant in South Dakota in 1966, though this experimental sodium-cooled reactor would prove troublesome and was converted to natural gas after just one year. Undeterred, NSP doubled down on nuclear with Monticello Nuclear Generating Plant, which began operating in 1971 with a single General Electric BWR-3 reactor generating 671 MWe, followed by Prairie Island Nuclear Power Plant in 1973, featuring two Westinghouse pressurized water reactors producing a total 1,076 megawatts.

The consolidation playbook these utilities followed was elegantly ruthless: acquire competitors, secure exclusive service territories through regulatory capture, achieve economies of scale, and enjoy monopoly returns. State utility commissions, ostensibly protecting consumers, often became partners in this arrangement—guaranteeing returns on capital investments while shielding utilities from competition. It was capitalism without the messy competition part, socialism for shareholders wrapped in the flag of public service.

By the 1970s, these three companies—NSP, PSCo, and SPS—had become regional powerhouses, each dominating their respective territories with a mix of coal, nuclear, and hydroelectric generation. They were the epitome of the boring, stable utility: predictable earnings, steady dividends, and about as much excitement as watching paint dry. Little did anyone know that deregulation fever was about to turn these sleepy monopolies into wannabe Wall Street wolves.

III. Deregulation Dreams: The 1990s Transformation

The 1990s arrived with promises of market liberation. Electricity, the thinking went, was just another commodity—why shouldn't it trade like pork bellies or orange juice futures? The Energy Policy Act of 1992 had opened wholesale power markets to competition, and utility executives everywhere were drunk on visions of unregulated profits. No longer would they be shackled to the plodding world of cost-plus regulation. They could be energy traders, merchant power barons, masters of the universe in hard hats.NSP wasn't immune to merger mania. On May 3, 1995, Northern States Power Company and Wisconsin Energy Corporation each filed an SEC Form 8-K to combine in a merger-of-equals transaction to form Primergy Corporation, which would be the tenth largest investor-owned electric and gas utility company in the United States, based on market capitalization at that time of about $6.0 billion, with 1994 combined revenues of $4.2 billion and total assets of more than $10.0 billion. NSP shareholders would receive 1.626 shares of Primergy stock for each NSP share, while WEC shareholders would receive one-for-one shares.

The Primergy merger was supposed to be the deal that proved utilities could consolidate across state lines, creating regional powerhouses that could compete in the coming deregulated marketplace. James J. Howard, NSP's CEO, would become chairman and CEO of the combined company, with Wisconsin Energy's Richard Abdoo as vice chairman, president, and COO, positioned to succeed Howard upon his retirement in 2000. The headquarters of the two utilities would remain distinct and separate in their existing respective state locations—Milwaukee for Wisconsin Energy and Minneapolis for NSP. The merged company would have been headquartered in Minneapolis (with NSP as the nominal survivor), but incorporated in Wisconsin. The Primergy board of directors were to be equally split, composed of six from each company.

But regulatory reality crashed the party. The delay had put the merger five months behind schedule and had reduced earnings for both utilities by a total of $58 million to that point, costs which had not been passed on to consumers. Adding to the discomfort was a growing gap between the performance of the two companies by early 1997. Wisconsin Energy's stock had by then fallen about 13% since early 1995 when the deal had been announced, due to other ongoing problems that had developed within the company, including issues with its Point Beach Nuclear Generating Station in Manitowoc County, Wisconsin. But Northern States Power's stock had risen by 6%.

On May 16, 1997, both CEOs announced that their boards had voted to terminate the merger. Approval had been granted by the state regulatory commissions in Michigan and North Dakota, but not in Minnesota or Wisconsin or by the FERC. Howard said in a press release, "What we encountered were regulatory agencies that were changing their merger policies as they were considering our filing." The case was considered to be a bellwether in the utilities industry, putting an end to the rapid pace of mergers and acquisitions that had been ongoing up to then.

But NSP wasn't done dreaming big. While Wisconsin Energy licked its wounds, NSP found a new dance partner out west. In 1995, Public Service Company of Colorado and Southwestern Public Service had merged to form New Century Energies—a name that screamed dot-com era optimism despite being a utility company. However, in 1998, after the failed Primergy merger, NSP merged with New Century Energies of Denver, owner of Public Service Company of Colorado and Southwestern Public Service, to form Xcel Energy.

The merger, finalized in August 2000, created a utility behemoth serving customers from the Canadian border to the Mexican frontier. But this wasn't just about regulated utility operations. Hidden within the combined company was a ticking time bomb: NRG Energy, NSP's former wholesale power subsidiary that had been spun off as an independent company but remained majority-owned by the newly formed Xcel. NRG represented everything exciting about the deregulated future—merchant power plants, energy trading, global expansion. What could possibly go wrong?

IV. The NRG Catastrophe: Hubris Meets Reality (2000-2003)

The conference room at Xcel Energy's Minneapolis headquarters on July 26, 2002, felt like a funeral parlor. CEO Wayne Brunetti had just announced that the company would need to inject $500 million into its struggling subsidiary NRG Energy—money Xcel didn't have without an emergency stock sale. Within hours, Xcel's stock price would crater 36% in a single trading session, vaporizing billions in market value. The merchant power gold rush that was supposed to transform sleepy utilities into growth machines had become a death spiral.NRG Energy had been formed in 1989 as one of NSP's wholly owned subsidiaries. In 1997, NRG Energy, Inc. had 2,650 MW of generation and operational responsibility for a supplementary 5,374 MW. By 1998, the company began an aggressive acquisition campaign. It bought plants from Niagara Mohawk, San Diego Gas and Electric, Consolidated Edison, Montaup Electric, Rochester Gas and Electric, and Connecticut Light & Power. It continued to grow through acquisitions and in 2000, acquired Cajun Electric Power Cooperative's facilities. The company was supposed to be NSP's vehicle for participating in the deregulated power markets—building merchant plants that would sell electricity on the open market without the burden of regulatory oversight.

In 2001, NRG Energy had a net ownership of 24,357 MW of generation globally, with 19,077 MW in the United States. From 1996 to 2001, the operating revenue increased from $104 million to $3 billion, and the debt increased from $212 million to $8.3 billion. The numbers looked impressive on paper—a 29-fold increase in revenue! But that debt figure should have set off alarm bells. By 2002, the debt had reached $9.4 billion, and NRG Energy sold its power plants in Hungary and the Czech Republic.

The perfect storm that destroyed NRG began with the Enron collapse in late 2001. Suddenly, energy trading wasn't sexy anymore—it was toxic. Banks that had thrown money at merchant power developers now wanted their cash back. Meanwhile, wholesale power prices collapsed as the market realized there was massive overcapacity. NRG found itself with billions in debt for power plants that were worth a fraction of what they'd paid.

The bankruptcy filing had been expected at least since last fall when a credit rating downgrade triggered the need for about $1.3 billion in collateral payments by NRG to its creditors. To avert default by NRG, Xcel sold $500 million in stock in July 2002. The emergency stock sale was a desperate move that crushed Xcel's share price—Xcel shares were at $14.10 on Wednesday up about 20 cents for the day but down from more than $23/share last summer.

The end came swiftly. On May 14, 2003, NRG Energy filed for chapter 11 bankruptcy. The Minneapolis-based merchant power subsidiary of Xcel Energy filed its long anticipated voluntary petition for reorganization in the U.S. Bankruptcy Court for the Southern District of New York. The company has $11.6 billion in debt, but only $10.9 billion in assets. NRG became the first merchant power company to file for Chapter 11 bankruptcy protection since Enron—a dubious distinction that sent shockwaves through the utility industry.

In 2003, Xcel Energy paid NRG Energy $752 million for the benefit of NRG Energy's creditors and took a $2 billion write-off. The settlement was painful but necessary—it limited Xcel's exposure and allowed the company to finally separate from its toxic subsidiary. The voluntary, prepackaged bankruptcy, which is nearly identical to the settlement agreement announced in March, limits Xcel's obligation to NRG creditors to $752 million. When the bankruptcy plan is filed, NRG will become the property of its creditors and will no longer be a subsidiary of Xcel, which also owns six utility subsidiaries that serve electric and natural gas customers in 12 states. As a result, Xcel will be a utility holding company with minimal nonregulated operations.

The financial damage was staggering. It reported a net loss of $5.26/share in 2002 — an NRG net loss of $8.40/share was offset by utility earnings of $1.59/share and a $1.77/share tax benefit related to Xcel's investment in NRG. The company had to cut its dividend in half—from $1.50 per share to 75 cents—a move that devastated income-focused investors who had bought utility stocks for their reliable payouts.

In the company's reorganization, Xcel Energy relinquished its ownership interest, and NRG Energy became an independent, public company after bankruptcy. As of NRG's emergence, Xcel Energy no longer owns any portion of the company. The lesson was brutally clear: utilities should stick to the boring business of keeping the lights on, not playing Wall Street wannabe. The NRG disaster would shape Xcel's conservative approach for the next decade—a painful education in the dangers of unregulated ventures for regulated utilities.

V. The Turnaround Years: Back to Basics (2003-2010)

Richard Kelly stood before a hostile crowd of shareholders at Xcel's 2004 annual meeting in Denver. The stock had lost two-thirds of its value, the dividend had been slashed, and trust had evaporated. "We're going back to what we do best," Kelly declared, his Minnesota accent cutting through the tension. "We're a utility company. We serve customers. We keep the lights on. That's it." The simplicity of the message belied the complexity of the turnaround ahead.

The post-NRG era required nothing less than a complete cultural transformation. Out went the merchant power cowboys and energy trading hotshots. In came engineers, regulatory experts, and operators who understood that in the utility business, boring is beautiful. The company instituted strict capital allocation guidelines: no more unregulated adventures, no more growth for growth's sake. Every dollar would be invested in the regulated utility business where returns were predictable and blessed by regulators.

Rebuilding credibility with regulators became job one. Xcel executives spent countless hours in state utility commission offices across their eight-state territory, essentially apologizing for the NRG debacle and promising a return to utility fundamentals. The message was consistent: we're not those guys anymore. We're focused on reliability, affordability, and serving our communities. Slowly, painfully, trust began to rebuild. Even during the darkest days of the turnaround, seeds of the future were being planted. Since 1998, Xcel Energy's Windsource program has allowed customers to designate that part or all of their electricity comes from a renewable energy source. The program had been launched years before the NRG disaster, allowing customers to voluntarily pay a small premium to support wind energy development. It was a tiny program initially—mostly appealing to environmentally conscious customers in Boulder and Minneapolis—but it proved that renewable energy could work within the regulated utility model.

The financial crisis of 2008-2009 actually helped Xcel in an unexpected way. While other companies were scrambling for liquidity, Xcel's regulated utility model provided stable, predictable cash flows. Regulators, understanding the essential nature of utility services, continued to approve rate increases to cover infrastructure investments. The company that had nearly destroyed itself chasing unregulated growth now looked prescient for returning to its regulated roots.

By 2010, the turnaround was largely complete. The stock had recovered from its NRG-induced lows, the dividend had been partially restored, and the company had regained its investment-grade credit rating. More importantly, a new strategic vision was emerging. Climate change was becoming impossible to ignore, renewable costs were beginning to fall, and forward-thinking utilities were starting to see opportunity where others saw only regulatory burden. The stage was set for Xcel's next transformation—from utility survivor to clean energy leader.

VI. The Carbon-Free Moonshot: Bold Leadership (2010-2020)

Ben Fowke took the CEO reins at Xcel Energy in August 2011 with an engineer's precision and a strategist's vision. Standing in the company's wind operations center in Denver, watching real-time data from turbines scattered across the Great Plains, Fowke saw something his peers didn't: renewable energy wasn't just an environmental nice-to-have—it was becoming an economic imperative. "The crossover is coming," he told his team. "Wind will be cheaper than coal. We need to be ready."

The industry context was shifting dramatically. Natural gas prices had collapsed thanks to the fracking revolution, making coal plants increasingly uneconomic. Meanwhile, wind turbine technology was improving rapidly—bigger blades, taller towers, better capacity factors. Solar costs were plummeting even faster, following a Moore's Law-like trajectory that would soon make it competitive with fossil fuels. Environmental regulations were tightening, with the Obama administration's Clean Power Plan looming. The writing was on the wall: the age of coal was ending. In 2016, Xcel launched its Advanced Grid Intelligence and Security (AGIS) initiative—a $500 million intelligent grid investment that would enable two-way communication between the utility and its customers, integrate distributed energy resources, and optimize grid operations in real-time. This wasn't just about smart meters; it was about fundamentally reimagining the grid as a dynamic, responsive network rather than a one-way power delivery system.

But the truly historic moment came on December 4, 2018. Standing at the Denver Museum of Nature and Science, Ben Fowke made the announcement that would position Xcel as the industry's transformation leader: Xcel Energy, Colorado's largest electric utility, unveiled an ambitious goal Tuesday of reducing its carbon emissions to zero across its eight-state service area by 2050. The Minneapolis-based company that serves eight states has been a leader in the quest to increase the use of renewable energy sources, said Ben Fowke, the utility's chairman, president and CEO. "This isn't new to us. We've been leading the clean-energy transition at Xcel for quite a while now. Investing in renewables has really been part of our DNA for over 20 years now," Fowke said at a news conference for the announcement Tuesday at the Denver Museum of Nature and Science.

Xcel Energy already had a goal of reducing carbon dioxide emissions by nearly 60 percent and increasing its use of renewable energy sources to 55 percent of its mix by 2026 as part of its Colorado Energy Plan, which was approved by state regulators in August. The new plan includes a goal of reducing carbon emissions by 80 percent by 2030 across eight states and getting to zero emissions of the greenhouse gas by 2050. Fowke and Alice Jackson, president of Xcel's Colorado operation, said they don't know of any other utility in the country that has set a goal and timeline for producing no carbon emissions.

The announcement sent shockwaves through the industry. Two years ago, one of the country's largest investor-owned utilities set this wave in motion, and much of the sector's successive action is in part thanks to leadership at that utility, according to observers. Ben Fowke, who has led Xcel Energy as chairman and CEO since 2011, is credited with setting a precedent when in 2018 Xcel became the first multi-state U.S. utility company to commit to phasing out carbon emissions entirely.

Fowke's "steel for fuel" strategy became the company's mantra—"Steel for fuel" refers to Xcel's strategy to swap fossil fuels for fuel-free resources such as wind and solar. Under that strategy, the utility is currently on track to be more than 60% carbon-free by 2027, with 38% of its generation coming from wind and 8% from solar. It will also retire half its coal capacity between 2006 and 2027, retiring "nearly all" its plants in the next devade. The economics were compelling: wind and solar required upfront capital investment (the "steel") but eliminated ongoing fuel costs, creating value for both shareholders and customers.

The Colorado Energy Plan exemplified this approach. Through competitive bidding, Xcel discovered that renewable energy with battery storage was now cheaper than running existing coal plants. The plan called for retiring two units at the Comanche coal plant in Pueblo by 2025, adding 1,100 MW of wind, 700 MW of solar, and 275 MW of battery storage. When Colorado regulators approved the plan in August 2018, it marked a watershed moment—renewables weren't just competing with new fossil plants; they were displacing existing ones.

Since 2005, Xcel Energy has cut carbon emissions 35 percent and expects to surpass 50 percent by 2022, largely through retiring aging coal plants and using more power from renewable sources. Last year, about 40 percent of the electricity Xcel supplied came from carbon-free sources, and half of that amount from wind. The transformation was accelerating, and what had seemed impossible just a decade earlier was becoming inevitable.

By 2020, Xcel had emerged as the nation's leading wind power utility, with renewable energy no longer a regulatory burden but a competitive advantage. The company that had nearly destroyed itself chasing unregulated growth had found a new path to value creation—leading the regulated transition to clean energy.

VII. Modern Xcel: The Clean Energy Utility (2020-Present)

Bob Frenzel took the helm as CEO in August 2021, inheriting a company transformed but facing new challenges. Standing in Xcel's grid operations center during the February 2021 Texas freeze that had crippled the state's power grid, Frenzel watched as his team managed through minus-30-degree temperatures in Minnesota without a single forced outage. "Reliability isn't negotiable," he told his team. "We're not just building a clean grid—we're building a resilient one. "The current portfolio tells a remarkable transformation story. Xcel Energy has reduced carbon emissions 54% from the electricity it provides to customers from 2005 levels, with the company's 2018 goal aims to provide customers with 100% carbon-free electricity by 2050 and reduce carbon emissions from its operations 80% from 2005 levels by 2030. The company now serves 3.8 million electric and 2.2 million gas customers through NSP-Minnesota, NSP-Wisconsin, PSCo, and SPS, generating $14 billion in annual revenue.

The renewable transformation is accelerating at breathtaking speed. The proposal will deploy 3.6GW of renewable energy generation capacity by 2030 (2.3GW of wind and 400MW of solar PV) in addition to 900MW of energy storage output as part of the Upper Midwest Energy Plan agreed in 2024. The renewable mix is projected to jump from 41% to 63% by 2040, with plans to nearly double wind capacity by decade's end.

The coal plant retirement schedule reads like a countdown to the end of an era. The massive Sherco plant—once the pride of Minnesota's coal fleet—is being transformed. The utility specifically highlighted the Sherco plant, a retired coal generation site which Xcel is replacing with a 710MW solar PV site. Allen S. King and the remaining Sherco units will close by 2030, marking the end of coal-fired generation in Xcel's upper Midwest territory.

But the transition isn't without its challenges. Grid modernization requires massive investment—the Colorado Power Pathway alone spans 550 miles of new transmission lines to connect renewable resources in eastern Colorado to load centers. Virtual power plant networks are being developed to aggregate distributed resources like rooftop solar and home batteries. Heat storage batteries are being tested to provide long-duration storage that can shift spring wind energy to summer peak demand.

The nuclear question looms large. Xcel will also extend the use of its two carbon-free nuclear plants at Prairie Island and Monticello through the early 2050s. These plants provide about 30% of Minnesota's electricity and are critical to maintaining reliability as coal retires. Without them, achieving carbon-free electricity becomes exponentially more difficult and expensive.

The gas plant debate exemplifies the transition's complexity. This has been replaced with more concrete plans for a hydrogen-capable natural gas-fired power plant in Lyon County, Minnesota. Critics see new gas as locking in decades of emissions; Xcel sees it as essential backup for renewable intermittency, with the option to convert to hydrogen when that technology matures. It's the classic bridge fuel versus stranded asset debate playing out in real time.

Innovation projects showcase the utility of the future. The company is testing everything from grid-scale batteries to microgrids, from demand response programs to electric vehicle integration. Each technology represents a bet on what the future grid will require—flexibility, resilience, and the ability to orchestrate millions of distributed resources.

The financial performance reflects this transformation's success. The stock has more than doubled since the carbon-free announcement, outperforming utility peers. Regulated returns remain stable while growth capital expenditures drive rate base expansion. ESG investors have poured in, attracted by Xcel's leadership position in the energy transition. The company that nearly died from unregulated adventures has found growth through regulated transformation.

VIII. Playbook: Lessons from Crisis and Transformation

The conference room where Xcel's board meets today features a subtle reminder of corporate mortality—a framed stock certificate from NRG Energy, dated 2003, worthless. It's there by design, a monument to hubris and a warning about the dangers of straying from core competencies. Every strategic decision gets measured against a simple question: "Is this another NRG?"

The NRG bankruptcy recovery playbook has become required reading in utility boardrooms. First, acknowledge reality quickly—denial only deepens the hole. Xcel's management recognized by mid-2002 that NRG was unsalvageable and focused on containment rather than rescue. Second, negotiate from strength while you still have it. The $752 million settlement was painful but manageable; waiting longer could have meant substantive consolidation and potentially Xcel's own bankruptcy. Third, use the crisis to reset expectations. The dividend cut and strategic refocus gave management breathing room to rebuild.

The danger of unregulated ventures for regulated utilities cannot be overstated. Utilities enjoy stable, regulated returns precisely because they accept regulatory oversight and limitations. When they chase unregulated growth, they're competing against players with different risk tolerances, funding costs, and strategic timeframes. It's like a submarine trying to win a car race—wrong vehicle, wrong environment, inevitable disaster.

Working with, not against, regulators represents the fundamental shift in Xcel's strategy. Instead of viewing regulation as a constraint to be minimized, Xcel embraced it as a framework for value creation. When the company wanted to build renewables, it didn't fight for deregulation—it worked with regulators to create mechanisms for cost recovery. This collaborative approach has yielded far better results than the adversarial stance many utilities adopt.

First-mover advantage in regulated markets operates differently than in competitive ones. It's not about capturing market share before competitors arrive—the service territories are fixed. Instead, it's about shaping the regulatory framework, building operational expertise, and positioning for future policy directions. Xcel's early commitment to carbon-free electricity didn't just generate positive headlines; it influenced how regulators think about utility transformation and created a template others must now follow.

The economics of renewable transition in regulated markets flip traditional utility economics on its head. Historically, fuel costs were pass-throughs that didn't generate returns. Capital investments in generation assets earned regulated returns. As renewable costs plummeted, "steel for fuel" became a win-win-win: customers get stable or lower rates (no fuel cost volatility), utilities earn returns on capital investment, and emissions decline. It's a rare alignment of stakeholder interests.

Managing stakeholder expectations requires constant calibration. Investors want growth and returns. Regulators want reliability and reasonable rates. Customers want low bills and increasingly, clean energy. Communities want jobs and tax revenue. Environmental groups want rapid decarbonization. Employees want job security. Threading this needle requires clear communication, realistic timelines, and the ability to find creative compromises that give each group enough of what they need.

Why utilities can lead on climate stems from their unique characteristics. Unlike competitive businesses that might relocate or shut down when facing environmental regulations, utilities are rooted in their service territories. Their long-term planning horizons—decades for major infrastructure—align with climate timescales. Stable cash flows from regulated operations provide the financial foundation for massive capital investments. Perhaps most importantly, they have existing customer relationships and billing systems that can support new energy services.

Capital allocation in a transitioning industry requires a portfolio approach. Some investments are no-regret moves—grid modernization benefits any future scenario. Others are option bets—hydrogen-ready gas turbines that might run on natural gas for years but could convert later. Still others are learning investments—small-scale pilots that build capabilities for uncertain futures. The key is maintaining flexibility while moving decisively where the direction is clear.

The transformation also requires cultural change. Engineers who spent careers optimizing coal plants must now learn wind forecasting and battery management. Regulatory teams accustomed to adversarial rate cases must build collaborative stakeholder processes. Finance teams modeling steady baseload plants must understand intermittent resource economics. It's not just teaching old dogs new tricks—it's teaching them an entirely different game.

IX. Bull vs. Bear: The Investment Case

Walk into any utility investor conference today and Xcel Energy inevitably comes up. The bulls see a transformed utility leading the energy transition. The bears see execution risk and stranded assets. Both have compelling arguments that deserve serious consideration.

The Bull Case:

The regulatory environment has never been more constructive for utilities investing in clean energy. State mandates for renewable energy, federal tax credits, and increasing carbon regulations all push in Xcel's direction. The company isn't fighting these trends—it's surfing them. Xcel Energy has reduced carbon emissions 54% from the electricity it provides to customers from 2005 levels, demonstrating execution capability that regulators trust and reward with approved rate increases.

The infrastructure investment opportunity is staggering. Grid modernization alone could require $100+ billion industry-wide over the next decade. Xcel's regulated utility model means these investments earn guaranteed returns—typically 9-10% on equity—for decades. As one bull puts it: "It's like having a license to print money as long as you're building infrastructure society needs."

ESG tailwinds are transforming utility valuations. Institutional investors managing trillions in assets increasingly screen for climate leadership. Xcel consistently ranks among the top utilities in sustainability indices, attracting premium valuations from ESG-focused funds. This isn't virtue signaling—it's value creation through access to lower-cost capital.

Carbon-free energy accounted for 50% of its total electricity generation in 2023, with wind and nuclear as the largest contributors. This positioning matters as carbon prices—whether explicit through legislation or implicit through regulation—increasingly favor clean generation. Every coal plant competitors still operate becomes a liability; every wind farm Xcel has already built becomes more valuable.

The execution track record post-NRG speaks volumes. Management has consistently met or exceeded guidance for nearly two decades. The Colorado Energy Plan came in under budget. Wind capacity additions have exceeded targets. This isn't a utility promising transformation—it's one delivering it quarter after quarter.

The Bear Case:

Stranded asset risk lurks in every coal and gas plant still operating. Sure, Xcel plans to retire coal by 2030, but what if regulators deny cost recovery for early retirement? What if communities dependent on coal plants successfully delay closures? That new gas plant in Minnesota might be "hydrogen-ready," but if hydrogen doesn't materialize at scale, it's a stranded asset by 2040.

Distributed energy and grid defection threaten the fundamental utility model. As rooftop solar and battery costs fall, customers might increasingly self-generate. Commercial customers are already installing microgrids. If enough customers reduce grid dependence, remaining customers face higher costs, accelerating defection—the utility death spiral. Xcel's response—embracing distributed resources—might just manage the decline rather than prevent it.

Regulatory lag and cost recovery challenges grow with the pace of change. Utilities typically recover costs through rates set in periodic rate cases. But with billions in annual capital expenditure, there's always a lag between spending and recovery. If inflation accelerates or construction costs overrun, shareholders eat the difference until the next rate case—which might be years away. Wildfire liability concerns reached crisis levels with the Marshall Fire and Smokehouse Creek incidents. A 2023 investigation by the Boulder County Sheriff attributed the fire to the merging of two independent ignitions: kindling from an old fire on a property owned by the Twelve Tribes, a religious organization, and sparks from an Xcel Energy power line. Insurance data suggest the fire caused about $2 billion in damages. Meanwhile, CFO Brian Van Abel reported that Xcel Energy has so far committed to $176 million in settlement agreements for claims related to the Smokehouse Creek fire, which he said remains on track to trigger a total of about $290 million in liability. The specter of PG&E's bankruptcy from California wildfire liability haunts every Western utility.

Execution risk on ambitious clean energy targets multiplies with scale. Getting to 80% carbon-free by 2030 requires everything to go right—permitting, construction, transmission upgrades, regulatory approvals. One major project delay or cost overrun could cascade through the entire plan. The last 20% to reach 100% carbon-free requires technologies that don't yet exist at commercial scale. Betting the company on innovation timeline is inherently risky.

Competition from tech companies and new energy models poses existential questions. Amazon is building its own renewable projects. Google is contracting directly with nuclear plants. Tesla's virtual power plant ambitions could disintermediate utilities entirely. The companies that were Xcel's biggest growth customers might become its biggest competitors.

The balanced view acknowledges both perspectives have merit. Xcel has successfully navigated the energy transition better than most peers, but the hardest challenges lie ahead. The company's regulated utility model provides stability but limits upside. Clean energy leadership creates value but also execution risk. The wildfire liability wild card could overwhelm everything else if not contained.

For investors, the decision comes down to time horizon and risk tolerance. Short-term investors might worry about rate case outcomes and wildfire trials. Long-term investors might focus on the infrastructure buildout opportunity and ESG positioning. Risk-averse investors might prefer utilities with less transformation risk. Growth investors might see Xcel as the best way to play the energy transition within the utility sector.

X. Crystal Ball: The Next Decade

Standing in Xcel's advanced grid operations center, watching real-time feeds from thousands of sensors, weather stations, and smart meters, you can glimpse the utility of the future. Artificial intelligence predicts equipment failures before they happen. Machine learning optimizes power flows across a grid increasingly dominated by variable renewable resources. But the hardest questions aren't technical—they're strategic, economic, and ultimately existential for the traditional utility model.

The path to 100% carbon-free electricity resembles a climbing expedition where the last thousand feet are the most treacherous. Getting to 80% by 2030 is largely mapped—retire coal, build wind and solar, extend nuclear licenses, add batteries for daily cycling. But that last 20% requires technologies that either don't exist commercially or remain prohibitively expensive: seasonal storage, advanced nuclear, carbon capture, or green hydrogen at scale.

Nuclear's role becomes pivotal and contentious. Prairie Island and Monticello's licenses extend to the early 2050s, but even that might not be enough. Small modular reactors promise safer, more flexible nuclear, but costs remain uncertain and public acceptance questionable. Without nuclear's baseload contribution, reaching 100% carbon-free might require overbuilding renewables by 2-3x with massive curtailment—economically painful even if technically feasible.

Storage technology needs revolutionary, not evolutionary, improvement. Current lithium-ion batteries work for 4-8 hour storage, managing daily cycles. But storing spring wind energy for summer peaks requires seasonal storage—hundreds of times current capacity. Iron-air batteries, liquid air storage, gravity systems, underground compressed air—all show promise but none have proven at grid scale. The winning technology might not even be invented yet.

Electrification represents both massive opportunity and fundamental challenge. If transportation and heating electrify as projected, electricity demand could double by 2050. That's enormous growth for a utility industry accustomed to flat demand. But it also means building infrastructure twice—once to decarbonize current demand, again to serve new load. The capital requirements are staggering, the execution complexity unprecedented.

Grid resilience in an extreme weather era changes every assumption. The February 2021 Texas freeze, the 2020 California blackouts, Hurricane Ida's devastation—all demonstrate that reliability can no longer assume normal weather. Future grids must withstand 500-year events that now happen every decade. That means redundancy, hardening, and flexibility that traditional planning never contemplated.

Regulatory evolution could accelerate or derail everything. Performance-based rates that reward outcomes over inputs. Federal transmission planning that overrides state boundaries. Carbon pricing that finally makes externalities explicit. Alternatively, political backlash against rising rates, reliability concerns about renewable-heavy grids, or wildfire liability could freeze progress. The regulatory framework of 2035 might be unrecognizable from today's.

Competition from tech companies intensifies yearly. Data centers don't just want clean power—they want dedicated clean power, contracted directly, possibly behind the meter. If your biggest customers bypass the grid, who pays for the infrastructure? The utility death spiral, long threatened, could finally materialize if load defection accelerates.

What success looks like in 2035 depends on perspective. For Xcel, it might mean 90% carbon-free electricity, stable returns on massive infrastructure investment, and maintained reliability despite weather extremes. For customers, success might mean stable rates, reliable service, and choice in energy sources. For society, success means substantial progress on climate goals without sacrificing economic growth or energy equity.

The uncomfortable truth is that nobody knows if the traditional regulated utility model can survive the energy transition intact. Xcel is betting it can not just survive but thrive by leading the transformation. That's either visionary leadership or dangerous overconfidence. The next decade will reveal which.

XI. Recent News**

Latest Quarterly Earnings and Guidance Updates**

Xcel Energy Inc. reported strong 2024 year-end results with 2024 GAAP earnings per share were $3.44 compared with $3.21 per share in 2023. 2024 ongoing earnings per share were $3.50 compared with $3.35 per share in 2023. The company has reaffirmed 2025 EPS guidance of $3.75 to $3.85 per share, demonstrating management confidence in continued growth trajectory.

Second quarter 2025 results showed continued momentum with second quarter GAAP earnings of $444 million, or $0.75 per share, compared with $302 million, or $0.54 per share in the same period in 2024. Second quarter ongoing earnings reflect increased recovery of infrastructure investments, partially offset by higher interest charges, depreciation and O&M expenses.

Regulatory Proceedings and Rate Case Outcomes

NSP-Minnesota filed an electric rate case in Minnesota, seeking a total revenue increase of $491 million (13.2%) over two years, based on an ROE of 10.3%, a 52.5% equity ratio and rate base of $13.2 billion in 2025 and $14 billion in 2026. In December, the state Public Utilities Commission approved a 5.2 percent interim rate increase for Minnesota's largest electric utility. That amounts to an extra $5.39 a month for a typical household.

Major Renewable Project Announcements

The company continues aggressive renewable expansion with its $45 billion infrastructure plan (2025–2029) is a masterstroke of capital discipline and visionary planning. The breakdown—$25 billion for renewable energy, $10 billion for grid modernization, $7 billion for customer electrification, and $3 billion for transitional natural gas—reflects a balanced approach to decarbonization

Grid Modernization Milestones

Xcel Energy issued approximately $1.15 billion of equity through its at-the-market program in the six months ended June 30, 2025. In May 2025, Xcel Energy Inc., NSP-Minnesota, NSP-Wisconsin, PSCo and SPS each entered into an amended five-year credit agreement with a syndicate of banks. The aggregate borrowing limit was increased to $4.75 billion. These financial moves support massive grid investment needs.

Climate and ESG Developments

The company maintains its leadership position in clean energy transition, with customer growth patterns reflecting electrification trends: The company's 2025 earnings report highlights a 2.7% year-to-date increase in electric customer volume, while natural gas demand fell 0.4%. This shift mirrors national trends, as industries and households pivot toward cleaner energy sources.

Strategic Partnerships and Technology Investments

Leadership continues to engage on critical policy issues. "We're in an unprecedented period of electric demand growth and believe that we need a broad scope of energy resources to meet those needs," Frenzel said. Top of mind, Frenzel said, is advocating for the preservation of tech-neutral tax credits for wind, solar, nuclear and energy storage projects.

XII. Links & Resources

Annual Reports and Investor Presentations - Xcel Energy Investor Relations: investors.xcelenergy.com - SEC Filings: sec.gov/edgar (Ticker: XEL) - Quarterly Earnings Reports and Conference Call Transcripts - Annual Sustainability Reports

State Regulatory Filings and Decisions - Minnesota Public Utilities Commission Dockets - Colorado Public Utilities Commission Proceedings - Texas Public Utility Commission Filings - Regional transmission organization reports (MISO, SPP)

Industry Research and Analysis - Edison Electric Institute Reports - S&P Global Market Intelligence Utility Research - Wood Mackenzie Power & Renewables Analysis - BloombergNEF Clean Energy Reports

Books on Utility Transformation - "The Grid: The Fraying Wires Between Americans and Our Energy Future" by Gretchen Bakke - "Electrify: An Optimist's Playbook for Our Clean Energy Future" by Saul Griffith - "The Quest: Energy, Security, and the Remaking of the Modern World" by Daniel Yergin

Clean Energy Transition Resources - National Renewable Energy Laboratory (NREL) Publications - International Energy Agency (IEA) Reports - Rocky Mountain Institute Analysis - Lawrence Berkeley National Laboratory Grid Studies

Historical Utility Industry Materials - "Power Struggle: The Hundred-Year War over Electricity" by Richard Rudolph - Federal Power Commission Historical Archives - Public Utility Holding Company Act History

NRG Bankruptcy Case Studies - U.S. Bankruptcy Court Southern District of New York Case No. 03-13024 - "When Good Companies Go Bad: The NRG Energy Story" - Harvard Business School Case - Securities and Exchange Commission litigation releases

Grid Modernization White Papers - GridWise Alliance Publications - Smart Electric Power Alliance Resources - Department of Energy Grid Modernization Initiative Reports

Renewable Energy Economics Research - Lazard's Levelized Cost of Energy Analysis - International Renewable Energy Agency (IRENA) Cost Studies - Energy Information Administration (EIA) Renewable Statistics

Climate and Energy Policy Resources - Clean Air Task Force Reports - Environmental Defense Fund Utility Analysis - Resources for the Future Climate Economics Papers - Center for Climate and Energy Solutions Policy Briefs

The story of Xcel Energy is far from over. From its origins in the early days of electrification through near-death in the merchant power collapse to its current position as America's clean energy leader, the company exemplifies both the perils and promise of utility transformation. Whether Xcel's carbon-free moonshot succeeds or fails will shape not just one company's future, but the entire utility industry's response to climate change. For investors, policymakers, and citizens alike, Xcel Energy represents a critical test case: Can a century-old utility reinvent itself for the energy transition while maintaining reliability, affordability, and shareholder returns? The next decade will provide the answer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube