DTE Energy: Powering Michigan's Transformation from Industrial Age to Clean Energy Future

I. Introduction & Episode Setup

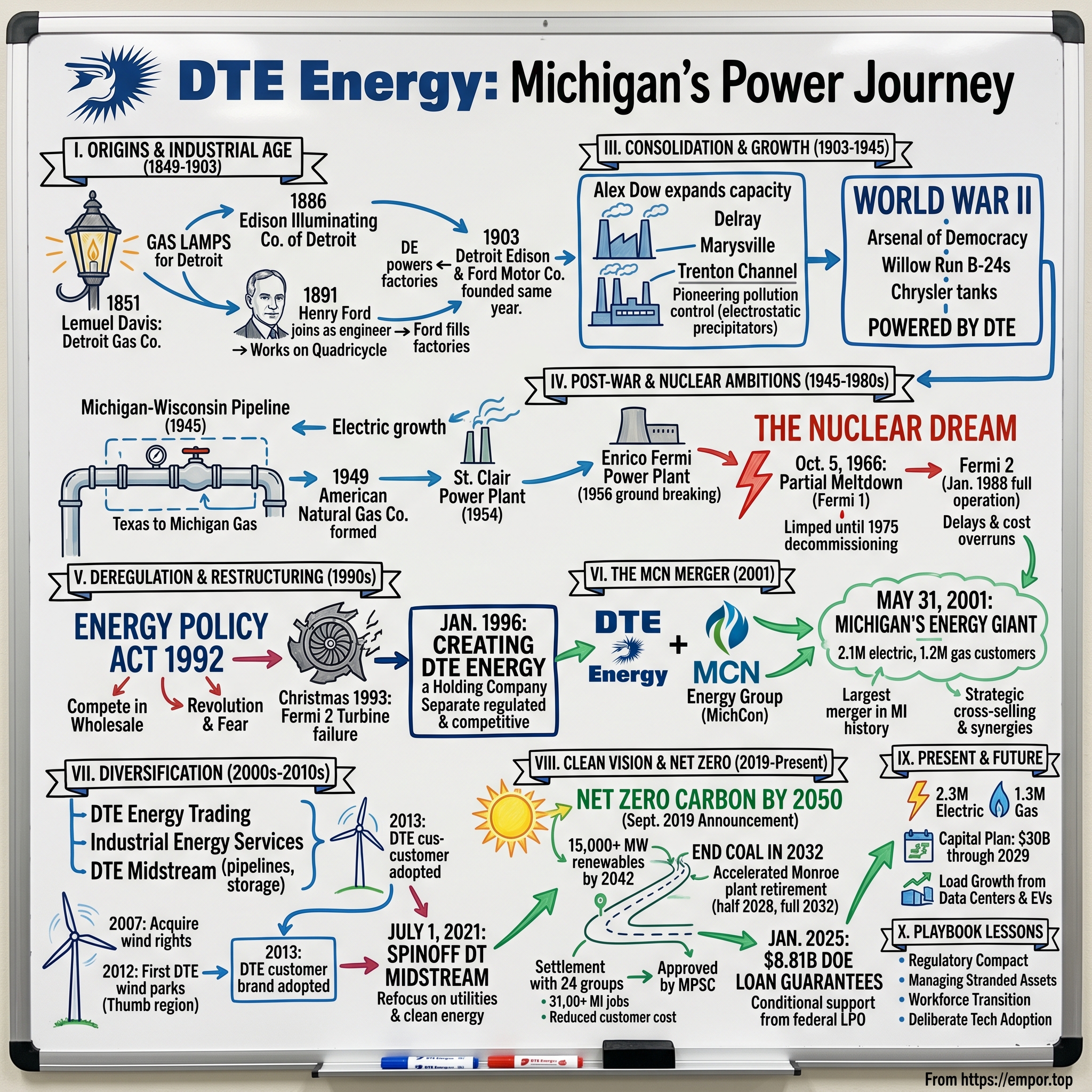

Picture Detroit in 1851: A city of 21,000 souls, muddy streets, and ambitious merchants. On a June evening that year, something magical happened—53 gas street lamps flickered to life for the first time, casting a warm glow across Woodward Avenue. The man behind this transformation was Lemuel Davis, a Philadelphia entrepreneur who saw opportunity where others saw frontier darkness. He couldn't have imagined that his City of Detroit Gas Company would evolve into a $29 billion energy giant powering the entire state of Michigan.

Today, DTE Energy serves 2.2 million electric customers and 1.3 million natural gas customers across Michigan, managing everything from nuclear reactors to wind farms, from century-old gas pipes to cutting-edge battery storage. But here's the fascinating question: How does a company born in the age of whale oil and gas lamps reinvent itself for the era of solar panels and electric vehicles? How does a regulated monopoly—bound by political oversight, public utility commissions, and century-old infrastructure—execute one of the most ambitious clean energy pivots in American corporate history?

The DTE story is really three intertwined narratives. First, it's the archetypal American industrial story—a company that literally powered the rise of Detroit from frontier town to the world's automotive capital. Second, it's a masterclass in navigating regulated markets, where success isn't measured by disrupting competitors but by threading the needle between ratepayers, regulators, politicians, and investors. And third, it's a transformation story happening right now—a 175-year-old utility attempting to completely rewire its business model while keeping the lights on for millions.

What makes DTE particularly compelling is timing. While tech companies grab headlines for their moonshots, utilities like DTE are quietly executing the largest capital redeployment in corporate history. DTE alone plans to invest $30 billion over the next five years—that's more than the market cap of most S&P 500 companies—to shut down coal plants that have run for decades and build renewable infrastructure that will power Michigan for the next century.

This is the regulated utility paradox: boring until it isn't, predictable until it transforms, local until it becomes the linchpin of national energy policy. So let's dig into how a gas lamp company became Michigan's energy backbone—and why its next chapter might be its most audacious yet.

II. Origins: From Gas Lamps to Electric Dreams (1849-1903)

The story begins not in Detroit but in Philadelphia, where Lemuel Davis had built a reputation as a gas works engineer. In 1849, Detroit's city fathers, tired of their city's reputation as a dark and dangerous frontier outpost, invited Davis to solve their illumination problem. Davis saw opportunity—not just to light streets, but to build an empire.

By 1850, Davis had organized the City of Detroit Gas Company, convincing local merchants and industrialists to invest $50,000 (roughly $1.8 million today) in his vision. Construction of the gas works began at the foot of Third Street, where coal could be easily unloaded from ships. The plant used a process that seemed almost alchemical to observers: heating coal in sealed retorts to produce "illuminating gas," which was then purified, stored in massive telescoping holders, and distributed through underground mains. That first successful lighting ceremony on June 21, 1851, represented more than just technological progress—it was Detroit's declaration that it belonged among America's modern cities. The gas lamps transformed Woodward Avenue from a muddy trail where citizens feared to tread after dark into a promenade where merchants stayed open late and families strolled in safety.

But even as gas lighting spread through Detroit's streets, a more revolutionary technology was brewing. In 1879, Thomas Edison's incandescent lamp promised to make gas lighting obsolete. By 1886, a group of Detroit investors saw the writing on the wall and formed the Edison Illuminating Company of Detroit, securing rights to Edison's electrical patents for the city. The plant they built on Washington Boulevard would become the launching pad for one of history's most consequential careers.

In 1891, a young mechanic named Henry Ford left his small lumber business to work as a night engineer at the Edison Illuminating Company of Detroit. By early 1894, he would be promoted to chief engineer. The irony wasn't lost on anyone who knew Ford—here was a farm boy who hated farming, now running the electrical infrastructure for a booming industrial city. While working at the Edison Illuminating Company, Ford was also building his first horseless carriage, the Quadricycle, with the help of some of his coworkers.

The relationship between Ford and Edison illuminates something fundamental about this era. In 1896, Ford attended a meeting of Edison executives, where he was introduced to Thomas Edison. Edison approved of Ford's automobile experimentation. Encouraged by Edison, Ford designed and built a second automobile, completing it in 1898. Edison's endorsement wasn't just personal validation—it was industrial legitimacy from America's greatest inventor.

By 1899, the paths diverged. Ford left Edison after working there for eight years, backed by the capital of Detroit lumber baron William H. Murphy, and founded the Detroit Automobile Company on August 5, 1899. The timing was exquisite: Detroit Edison was about to embark on its greatest expansion, while Ford was about to revolutionize transportation.

In January 1903, two corporate births occurred almost simultaneously. Detroit Edison was officially incorporated, immediately beginning construction on the Delray 1 power plant—a massive facility designed to power Detroit's industrial ambitions. That same year, after two failed automotive ventures, Ford Motor Company was founded in mid-June 1903, rolling out its first car—a Model A—that July.

The symbolism was perfect: Detroit Edison would power the factories, Ford would fill them with purpose. In 1904, Detroit Edison signed its first power contract with Cadillac Motor Car Company. The age of industrial Detroit had begun, with electricity and automobiles advancing in lockstep. Gas lamps still flickered on side streets, but the future belonged to electrons and internal combustion.

III. Building Industrial Detroit: The Consolidation Era (1903-1945)

The 1920s arrived with a roar in Detroit—literally. The city's population had exploded from 285,000 in 1900 to nearly a million by 1920, and every new resident needed power. Alex Dow, who became president of Detroit Edison in 1912, understood that incremental expansion wouldn't suffice. The company needed to think at the scale of Detroit's ambitions.

Between 1924 and 1929, Detroit Edison increased its production capacity by building the Marysville, Trenton Channel and Delray 3 power plants. Each represented a technological leap forward. The Trenton Channel Power Plant began operating in 1924. The plant had six turbine generators with 13 coal-fired boilers. The sixth and last turbine generator arrived by 1929. At that time, Trenton Channel was the largest project Detroit Edison had undertaken, and the first plant to use pulverized coal as fuel rather than the older style stoker-fired beds of coal.

The innovation didn't stop at fuel efficiency. Trenton Channel was the first electric power plant in the world to use electrostatic precipitators to limit ash particulate emissions—a prescient move that positioned Detroit Edison as an early leader in pollution control, decades before environmental regulations would make such technology mandatory.

Meanwhile, on the gas side of the energy equation, consolidation was creating its own industrial giant. In 1903, Detroit Gas Co. was renamed Detroit City Gas Co., securing franchises for Highland Park and Hamtramck and growing to serve over 67,000 customers. By 1905, American Light & Traction Co. had acquired a majority stake, recognizing the strategic value of controlling Detroit's gas infrastructure. The truly transformative moment came in 1937. Detroit City Gas Company merged with Grand Rapids Gas Light Company, Washtenaw Gas Company and Ann Arbor Gas Company to form Michigan Consolidated Gas Company (MichCon). The merger, approved in 1938 by state and federal regulators, created one gas provider for most of the southern half of the Lower Peninsula. This wasn't just corporate consolidation—it was the creation of a utility scaled to match the geographic and economic ambitions of an entire state.

The timing proved fortuitous. As World War II transformed Detroit into the "Arsenal of Democracy," both Detroit Edison and MichCon found themselves at the center of America's industrial mobilization. Every B-24 bomber rolling off the assembly line at Willow Run, every tank produced at the Chrysler Arsenal, every Jeep built for the war effort—all required massive amounts of electricity and gas. The utilities weren't just supporting the war effort; they were essential to it.

Detroit Edison's power plants ran at maximum capacity throughout the war, with workers pulling double shifts to keep the factories humming. The company deferred maintenance, postponed upgrades, and pushed equipment to its limits—all in service of victory. MichCon, meanwhile, struggled to meet surging demand for natural gas, both for industrial processes and for heating the hastily-built housing for the flood of workers arriving from the South.

By 1945, both companies emerged from the war exhausted but triumphant. They had proven that Michigan's energy infrastructure could meet any challenge—but they also knew that the post-war boom would require even greater expansion. The stage was set for the next chapter: the atomic age.

IV. Post-War Expansion & Nuclear Ambitions (1945-1980s)

The end of World War II brought both celebration and anxiety to Michigan's energy companies. Defense contracts were evaporating, but returning veterans were starting families, buying homes, and demanding all the modern conveniences that electricity and gas could provide. The challenge was no longer surge capacity for wartime production but sustained growth for peacetime prosperity.

To meet the increasing demand for natural gas, the Michigan-Wisconsin Pipeline was completed in 1945. This 500-mile pipeline connected Michigan to the vast natural gas fields of Texas and Oklahoma, fundamentally changing the economics of gas distribution. No longer dependent on manufactured gas from coal, MichCon could now deliver cleaner, cheaper natural gas to homes and businesses across the state.

In 1949, Michigan Consolidated Gas, the Milwaukee Gas Co., the Michigan-Wisconsin Gas Co., the Austin Field Pipeline Co. and the Milwaukee Solvay Co. became the American Natural Gas Co. This merger created a vertically integrated gas giant, controlling everything from wellheads to burner tips—a structure that would define the industry for decades.

On the electric side, Detroit Edison was thinking bigger than ever. Detroit Edison added the St. Clair Power Plant in 1954 — one of the largest power plants in the world at the time. The scale was staggering: six units eventually producing over 1,400 megawatts, enough to power a city of a million people. The plant's location on the St. Clair River provided both the massive water flow needed for cooling and easy access to Great Lakes shipping for coal delivery.

But the real ambition lay in the atom. In 1956, Detroit Edison broke ground for the Enrico Fermi Power Plant and also began work on the River Rouge Power Plant. Named after the Nobel Prize-winning physicist who had achieved the first controlled nuclear chain reaction, Fermi represented Detroit Edison's bet on the future of energy. Fermi 1 was supposed to be Detroit Edison's crown jewel—a fast breeder reactor that would produce more fuel than it consumed, the perpetual motion machine of the atomic age. Cisler believed that the breeder cycle would dominate the future commercial market because it would provide an effectively limitless supply of fuel. Construction began in 1956, with operations planned for 1959. But nuclear reality proved messier than nuclear dreams.

Operation had been planned for 1959 or early 1960 but Fermi 1 achieved criticality on August 23, 1963. While slowly increasing its power over the next two years, on October 5, 1966 it suffered a partial meltdown when the flow of sodium was disrupted by blockage of the inlet holes at the bottom of the reactor. The blockage caused an insufficient amount of coolant to enter the fuel assembly; this was not noticed by the operators until the core temperature alarms sounded. Several fuel rod subassemblies reached high temperatures of around 700 °F (370 °C) (with an expected range near 580 °F, 304 °C), causing them to melt.

The incident became infamous through John Fuller's 1975 book "We Almost Lost Detroit," though the actual danger was far less dramatic than the title suggested. According to the Nuclear Regulatory Commission (NRC), there was no abnormal radioactivity released into the environment. Still, the psychological damage was done. Fermi 1 limped along until 1972, never achieving its promised potential, and was officially decommissioned December 31, 1975.

But Detroit Edison wasn't ready to abandon the nuclear dream. Plans to build [Fermi 2] were announced in July 1968. Initial criticality was achieved in July 1985, and full commercial operation commenced on January 23, 1988. The construction of Fermi 2 became an epic saga of delays, cost overruns, and regulatory battles—a microcosm of the American nuclear industry's struggles.

Meanwhile, the start of the Fermi 2 nuclear plant in 1970 and Monroe Power Plant Units 1-4, which came online from 1971-74, marked Detroit Edison's commitment to baseload generation at massive scale. The Monroe Power Plant would eventually become one of the largest coal-fired plants in the United States, a distinction that would later become a liability in the age of climate consciousness.

The 1970s energy crises—first the oil embargo of 1973, then the Iranian Revolution of 1979—transformed how utilities thought about fuel diversity. Natural gas, once considered too valuable to burn for electricity, became increasingly attractive. Coal, despite environmental concerns, offered energy independence. Nuclear promised abundant power but delivered construction nightmares. Detroit Edison, like all utilities, was learning that the future of energy would be about managing trade-offs, not finding perfect solutions.

V. Deregulation & Restructuring: Creating DTE Energy (1990s)

The 1990s opened with the utility industry standing at the edge of a cliff. In 1992, Congress passed the Energy Policy Act, which allowed competition in the utility industry's wholesale sector by mandating existing utilities to transmit electricity generated by other producers through their lines. For companies like Detroit Edison, which had operated as regulated monopolies for nearly a century, this was revolutionary—and terrifying.

Detroit Edison faced immediate operational challenges that underscored the risks of their aging infrastructure. The plant's worst accident came on Christmas Day 1993 when a blade from a 510-ton turbine generator snapped and caused an explosion and fire. It also flooded the plant's basement with 1 million gallons of water and 17,000 gallons of lubricating oil. The accident shut down Fermi 2 for a year while Edison spent $49 million to fix the turbine.

The Christmas Day 1993 turbine failure at Fermi 2 became a watershed moment for Detroit Edison. Here was a company trying to position itself for a competitive future while literally putting out fires from its past investments. The incident—though involving non-nuclear systems—heightened public fears about nuclear safety and added ammunition to critics who questioned whether utilities could safely operate complex facilities while cutting costs to compete.

Against this backdrop of operational challenges and market uncertainty, Detroit Edison made a bold strategic move. In January 1996, Detroit Edison established a holding company — DTE Energy. "DTE" was selected because it was the existing stock symbol for Detroit Edison. "Energy" was chosen to represent the company's vision to provide integrated energy (not just electric) solutions to customers.

The creation of DTE Energy represented more than a corporate reorganization—it was a philosophical shift. The old Detroit Edison was a utility company that happened to have some side businesses. DTE Energy would be an energy company that happened to own utilities. The distinction mattered enormously in the dawning age of deregulation.

The holding company structure allowed DTE to separate its regulated utility operations from competitive ventures. This wasn't just about regulatory compliance; it was about optionality. If full deregulation came to Michigan—as many expected—DTE could spin off or sell its regulated assets while keeping its merchant generation and energy trading businesses. If regulation persisted, the utilities would remain the cash flow engine funding new ventures.

Throughout the late 1990s, DTE navigated Michigan's halting steps toward electricity restructuring. The state legislature passed and then modified restructuring legislation, allowing some customer choice while maintaining most of the regulated framework. It was the worst of both worlds for utilities—enough competition to pressure margins, not enough to allow true market pricing.

But DTE's management saw opportunity where others saw chaos. They recognized that natural gas and electricity were converging—customers wanted integrated energy solutions, not separate bills from separate companies. The stage was set for the transformative deal that would define DTE's next chapter.

VI. The MCN Merger: Creating Michigan's Energy Giant (2001)

The year 2000 opened with utility consolidation fever sweeping the nation. Enron was still flying high, promising to transform energy markets through trading and financial innovation. Against this backdrop, DTE management recognized a fundamental truth: in a consolidating industry, you either eat or get eaten.

DTE Energy Co. announced the purchase of MCN Energy Group in a cash and stock transaction valued at $2.6 billion. Including the assumption of MCN's debt, the value of the transaction is around $4.6 billion. For context, this was the largest utility merger in Michigan history and one of the biggest energy deals nationally that year.

The strategic logic was compelling. Upon completion, the new DTE would have approximately 11,500 employees, serving 2.1 million electric customers and 1.2 million natural gas customers in Michigan. Critically, about 775,000 customers used both services—creating immediate cross-selling opportunities and operational synergies.

Under the terms of the agreement, the holder of each share of common MCN stock can elect to receive either $28.50 in cash/share or 0.775 shares of DTE Energy common stock per share. DTE's offer represents a 60% premium over MCN's Oct. 1 share price. That premium raised eyebrows on Wall Street, but DTE's management argued MCN was undervalued due to recent write-offs and operational issues.

The expected synergies were substantial—$60 million annually from eliminating duplicative functions, shared infrastructure, and integrated customer service. But the real prize was strategic positioning. The combined company will be well positioned to capture the enormous growth opportunities in the attractive Great Lakes-to-Northeast corridor, which currently accounts for about half of the nation's total energy consumption.

Integration, however, proved challenging. DTE expects a staff reduction in the 500-person range because of the transaction. The companies had promised to minimize layoffs through attrition and voluntary retirement, but merging two century-old corporate cultures—Detroit Edison's engineering-focused electric utility mindset with MichCon's customer service-oriented gas distribution culture—created tensions that would persist for years.

Positioning itself to become a major regional energy player, DTE Energy announced the closing of its approximately $3.9 billion merger with MCN Energy Group. The merger was consummated after DTE Energy acquired all outstanding shares of MCN Energy Group for a combination of cash and shares of DTE Energy common stock on May 31, 2001.

The Federal Trade Commission required minor divestitures to address competitive concerns, but these were relatively painless—mostly involving some overlapping service territories where both companies had small operations. The real regulatory battle would come at the state level, where the Michigan Public Service Commission would scrutinize every rate case for evidence that merger savings were being passed to customers rather than shareholders.

What made the MCN merger particularly prescient was timing. Within months of closing, Enron would collapse, taking with it the era's enthusiasm for energy trading and merchant generation. Suddenly, owning regulated utilities with predictable cash flows looked brilliant rather than boring. DTE had doubled down on the regulated utility model just as the market was about to reward it.

VII. Diversification & Non-Utility Growth (2000s-2010s)

The post-merger DTE faced a strategic crossroads. While the MCN integration proceeded, management saw opportunities beyond traditional utility operations. The question wasn't whether to diversify—it was how far to push beyond their regulated comfort zone.

In 2007, DTE Energy began acquiring wind development rights on more than 100,000 acres of land in the Thumb area. The first DTE Energy-owned and constructed wind parks were commissioned (connected to the grid and generating power) in December 2012. Two of these wind parks are located in Huron County and one in Sanilac County.

The wind development marked DTE's first major foray into renewable generation at scale. The Thumb region of Michigan—that distinctive peninsula jutting into Lake Huron—offered consistent winds and sparse population, ideal for wind farms. But the real motivation was portfolio diversification. Natural gas prices had spiked post-Katrina, coal plants faced mounting environmental pressure, and Michigan's renewable portfolio standard, though modest, signaled where policy was heading.

Beyond renewables, DTE built an impressive non-utility portfolio. DTE Energy Trading became a significant player in physical and financial gas and power markets. The company's industrial energy services division developed on-site generation for major manufacturers. DTE Biomass Energy, founded in the late 1980s, expanded from landfill gas collection to biomass power plants and renewable natural gas projects.

The crown jewel of the non-utility strategy was DTE Midstream, which owned and operated natural gas pipelines, storage, and gathering systems. Unlike the regulated utility business with its predictable but capped returns, midstream assets offered market-based pricing and growth potential. By 2020, DTE Midstream had grown to generate nearly $1 billion in annual revenues.

But the non-utility expansion wasn't without controversy. Activist investors questioned why a regulated utility was taking shareholder capital to invest in competitive businesses. Regulators worried that management attention was being diverted from core utility operations. And when severe storms in 2017 left hundreds of thousands without power for days, critics pointed to DTE's non-utility investments as evidence of misplaced priorities.

In 2013, DTE Energy adopted "DTE" as its customer-facing brand. Accordingly, Detroit Edison Company changed its name to DTE Electric Company, while Michigan Consolidated Gas changed its name to DTE Gas. The rebranding represented more than marketing—it was an attempt to present a unified face to customers who increasingly expected integrated energy solutions.

The strategic tension came to a head in 2020. On October 27, 2020, DTE announced its plan to spin off DTE Midstream into an independent, publicly traded business called DT Midstream. On July 1, 2021, DT Midstream successfully spun off. The spinoff valued DT Midstream at approximately $4 billion, returning significant value to DTE shareholders while allowing the parent company to refocus on its regulated utilities and clean energy transition.

The message was clear: DTE's future lay not in financial engineering or merchant energy, but in the fundamental transformation of Michigan's energy infrastructure. The stage was set for the most ambitious strategic pivot in the company's history.

VIII. The Clean Energy Pivot: CleanVision & Net Zero (2019-Present)

In September 2019, Jerry Norcia stood before a packed auditorium at DTE headquarters and made an announcement that would have seemed impossible just a decade earlier: DTE would achieve net zero carbon emissions by 2050. The room—filled with employees who had spent careers operating coal plants—went silent. Then, slowly, applause began to build. The impossible had become inevitable.

The announcement wasn't made in a vacuum. Climate activists had been pressuring Michigan utilities for years. Major customers like Ford and General Motors were demanding renewable energy options. And perhaps most importantly, the economics had shifted. Wind and solar, once expensive novelties, were now competitive with coal on pure cost basis—before even considering carbon regulations or public health benefits.

DTE's 2022 CleanVision Integrated Resource Plan represented the detailed roadmap for this transformation. The plan was breathtaking in scope: Developing more than 15,000 megawatts of Michigan-made renewable energy by 2042. This carbon-free generation is the equivalent to powering approximately 4 million homes. Ending DTE's use of coal in 2032 with a responsible, phased retirement schedule of the Belle River and Monroe coal power plants – dramatically reducing the Company's use of coal from 77% in 2005 to 0% in less than three decades. The Company has further accelerated the retirement of the Monroe Power Plant – with half of the plant retiring in 2028 and full retirement in 2032.

The negotiations around CleanVision revealed the complex stakeholder dynamics of modern utility regulation. Environmental groups pushed for faster coal retirement and more distributed generation. Labor unions worried about job losses at coal plants. Industrial customers feared rate increases. Low-income advocates demanded protection for vulnerable communities.

DTE Energy (NYSE: DTE ) today received approval from the Michigan Public Service Commission (MPSC) on the Company's landmark CleanVision Integrated Resource Plan (IRP). This approval comes just 14 days after a historic settlement agreement was reached between DTE and nearly two dozen organizations on the Company's 20-year plan that dramatically transforms how DTE generates electricity as part of its mission to invest in the future of Michigan.

The settlement that emerged was a masterclass in stakeholder management. Investing over $11 billion into the clean energy transition over the next 10 years, supporting more than 32,000 jobs in Michigan, while reducing the future cost of the plan for the Company's customers by a projected $2.5 billion. Directing an additional $110 million to support income-qualified home energy efficiency programs, customer affordability programs and access to clean energy resources for the Company's most vulnerable customers.

The acceleration of coal retirement schedules was particularly dramatic. Monroe Power Plant—once one of the largest coal plants in America—would close by 2032, three years earlier than initially proposed. Belle River would be converted to natural gas, providing backup power during the transition while avoiding the cost of building entirely new plants.

On the renewable side, DTE committed to adding approximately 3,200 MW of solar, 1,000 MW of wind, and 430 MW of battery storage by 2029. The scale was unprecedented for Michigan—enough to fundamentally reshape the state's generation mix within a decade.

The MIGreenPower program exemplified DTE's approach to customer engagement. Rather than waiting for mandates, the voluntary program allowed customers to pay extra for renewable energy, with nearly 100,000 residential customers enrolled. Major corporations signed up for massive blocks of renewable power, providing DTE with the customer commitment needed to justify large-scale renewable investments.

But challenges remained enormous. Grid reliability during the transition was paramount—Michigan winters don't forgive power outages. The intermittency of renewables required massive investments in battery storage and grid flexibility. And the workforce transition from coal to renewables required retraining thousands of workers.

The financing was equally complex. Coal plants with decades of remaining book value had to be retired early, creating stranded assets. DTE negotiated securitization arrangements to spread these costs over time, while federal tax credits from the Inflation Reduction Act helped offset renewable investment costs.

IX. Modern Operations & Strategic Positioning

Today's DTE Energy operates at a scale that would have been unimaginable to its founders. Market cap as of August 14, 2025 is $29.05B. As of August 2025 DTE Energy's TTM revenue is of $14.20 Billion USD. The company serves approximately 2.3 million residential, commercial, and industrial customers in southeastern Michigan with electricity and approximately 1.3 million residential, commercial, and industrial customers throughout Michigan with natural gas.

The infrastructure footprint is massive. DTE owns and operates 702 distribution substations with a capacity of approximately 37,710,000 kilovolt-amperes (kVA) and approximately 455,300 line transformers with a capacity of approximately 33,570,000 kVA. On the gas side, the segment has approximately 20,500 miles of distribution mains; 1,238,000 service pipelines; and 1,352,000 active meters, as well as owns approximately 2,000 miles of transmission pipelines.

The 2022 generation mix reveals the transformation challenge: As of 2022, 54.16% of DTE's electricity was generated from coal, 18.16% from nuclear, 14.22% from natural gas and 13.11% from renewable energy including wind, solar and hydroelectric. But change is accelerating rapidly.

Capital investment has reached unprecedented levels. DTE Electric invested over $2.5 billion in infrastructure improvements and $1.1 billion in cleaner generation, while DTE Gas invested $740 million to upgrade its natural gas system and expand service to rural communities in 2024 alone. The five-year capital plan calls for $30 billion in investment through 2029—a staggering sum that exceeds the market capitalization of most utilities.

Grid modernization has shown tangible results. Customers experienced a nearly 70% improvement in time spent without power from 2023 to 2024. This dramatic improvement came from targeted investments in infrastructure hardening, tree trimming, and advanced grid technologies—addressing longstanding criticism about DTE's reliability record.

The financial engineering behind the clean energy transition is complex but crucial. In January 2025, The Department of Energy's (DOE) Loan Programs Office (LPO) announced conditional commitments for loan guarantees to two utility subsidiaries of DTE Energy Company – up to $1.64 billion to DTE Gas Company and up to $7.17 billion to DTE Electric Company. LPO's financing comes at a lower interest rate than traditional capital market financing, helping to keep energy affordable for millions of Michiganders.

This federal support is transformative. The $8.81 billion in conditional loan guarantees represents nearly 30% of DTE's market cap—providing low-cost capital to accelerate the clean energy transition while keeping customer rates manageable. The guarantees specifically support renewable energy generation and battery storage, with LPO review[ing] and perform[ing] an eligibility assessment and environmental review on one anchor project for DTE Electric: the Trenton Channel Battery Energy Storage System Project.

The regulatory environment remains supportive but demanding. Michigan's clean energy mandates require increasing renewable portfolio standards, while federal policies through the Inflation Reduction Act provide tax credits that fundamentally alter project economics. DTE must navigate between aggressive environmental goals and reliability requirements, between keeping rates affordable and investing billions in new infrastructure.

Strategic positioning for the data center boom represents a potential game-changer. Michigan's proximity to Great Lakes water for cooling, relatively stable climate, and DTE's growing renewable portfolio make it attractive for hyperscale data centers. Each major data center can add 100-500 MW of load—equivalent to a small city—providing the demand growth that utilities crave in an era of otherwise flat electricity consumption.

But challenges remain formidable. The rapid retirement of dispatchable coal generation creates reliability risks, especially during extreme weather. Battery storage technology, while improving rapidly, remains expensive at the scale needed. And the workforce transition from traditional power plants to renewable energy requires massive retraining efforts.

X. Playbook: Lessons from a Regulated Utility Transformation

DTE's transformation offers a masterclass in managing change within regulatory constraints. Unlike tech companies that can pivot overnight, utilities must orchestrate complex transitions involving billions in stranded assets, thousands of workers, millions of customers, and multiple regulatory bodies—all while keeping the lights on 24/7.

Managing the Regulatory Compact

The fundamental challenge of regulated utilities is that they're private companies operating as public trusts. DTE's approach has been to embrace this duality rather than fight it. The CleanVision settlement with 24 different stakeholder groups exemplifies this strategy—building consensus before regulatory proceedings rather than litigating afterward.

The company has learned to speak multiple languages simultaneously. To investors, it emphasizes predictable earnings growth and dividend stability. To regulators, it focuses on reliability metrics and customer affordability. To environmental groups, it highlights carbon reduction targets. To labor unions, it guarantees retraining and transition support. The art lies in finding genuine alignment rather than making empty promises.

Capital Allocation in a Capital-Intensive Industry

DTE's capital allocation framework has evolved from simple reliability investments to sophisticated portfolio management. The company must balance: immediate reliability needs (tree trimming, pole replacement), long-term infrastructure (transmission lines, substations), generation transformation (renewable development, coal retirement), and emerging technologies (battery storage, grid software).

The DOE loan guarantees represent a new tool in this framework—using federal support to lower the cost of capital for qualifying projects. This isn't just about cheaper financing; it's about making projects economically viable that wouldn't pencil out with traditional utility returns.

The Stranded Asset Challenge

Perhaps no issue better illustrates the complexity of utility transformation than stranded assets. Monroe Power Plant, with hundreds of millions in remaining book value, must close by 2032. The traditional utility response would be to fight for extended life. DTE instead negotiated securitization—spreading costs over time while moving forward with closure.

This approach requires political courage. Closing coal plants means losing jobs in communities that have depended on them for generations. DTE's strategy of converting Belle River to natural gas, while not ideal from a climate perspective, provides transitional employment while avoiding the cost of entirely new construction.

Political Navigation

DTE operates in a purple state where energy policy can shift dramatically with elections. The company's approach has been steadfastly bipartisan—emphasizing jobs and economic development to Republicans, climate action to Democrats, and reliability to everyone.

The MIGreenPower program exemplifies this political dexterity. It's voluntary (appealing to market-oriented conservatives), supports renewable energy (appealing to environmental progressives), and creates Michigan jobs (appealing to labor Democrats and economic development Republicans).

Technology Adoption Strategy

Unlike Silicon Valley's "move fast and break things," utilities must "move deliberately and break nothing." DTE's technology adoption follows a careful sequence: pilot programs to test feasibility, targeted deployments in controlled environments, gradual scaling with continuous monitoring, and only then system-wide implementation.

Battery storage illustrates this approach. Starting with small demonstrations, moving to the 220 MW Trenton Channel facility, then planning for 2,900 MW by 2042—each step building on lessons from the previous.

Customer Program Innovation at Scale

In the 2023-2024 fiscal year, DTE continued its partnership with human service agencies to connect vulnerable customers to nearly $144 million in energy assistance, providing access to more than $660 million in financial aid over the last five years. Worked shoulder to shoulder with community leaders to double the Michigan Energy Assistance Program (MEAP) funding to $100 million in five years and increase the eligibility of MEAP funds to 200% of the Federal Poverty Level. DTE's Energy Efficiency Assistance (EEA) program provided $63 million in critical home upgrades at no cost to income-qualified customers, helping them lower their energy bills while improving their comfort and safety.

These programs aren't charity—they're strategic investments in customer retention and political capital. Every customer who receives assistance becomes an advocate. Every efficiency upgrade reduces system peak demand. Every voluntary renewable subscription demonstrates market demand for clean energy.

Workforce Transition Management

The human dimension of energy transition often gets overlooked in financial analysis. DTE employs thousands of workers at coal plants slated for closure. The company's approach combines retraining programs, early retirement incentives, and strategic redeployment to renewable projects.

Critically, DTE involves unions early in planning processes. Rather than presenting fait accompli decisions, the company works with labor leaders to design transition pathways. This collaborative approach has avoided the labor strife that has plagued other utility transformations.

The Integration Challenge

Perhaps the most underappreciated aspect of DTE's strategy is system integration. It's not enough to build renewables, upgrade the grid, and retire coal plants—all these pieces must work together seamlessly. This requires sophisticated modeling, real-time coordination, and constant adaptation.

The company is essentially rebuilding the plane while flying it. Every coal plant retirement must be preceded by replacement capacity coming online. Every renewable addition requires corresponding grid upgrades. Every customer program must integrate with system operations. The complexity is staggering, and the margin for error is zero.

XI. Analysis: Bull vs. Bear Case

The Bull Case: Riding the Clean Energy Supercycle

The optimistic view sees DTE at the beginning of a multi-decade infrastructure supercycle. Start with the regulatory tailwinds: Michigan's clean energy mandates create guaranteed demand for DTE's renewable investments. The regulatory construct allows the company to earn returns on its $30 billion capital program, providing earnings visibility through 2029 and beyond.

Federal support through the Inflation Reduction Act fundamentally changes project economics. The production tax credits for wind and solar, investment tax credits for storage, and now $8.81 billion in DOE loan guarantees provide a massive subsidy for DTE's transformation. The company is essentially being paid to do what it needs to do anyway.

The load growth story is compelling. After decades of flat demand, the combination of vehicle electrification, building electrification, industrial reshoring, and especially data centers could drive 2-3% annual load growth. Each percentage point of load growth translates directly to revenue growth in a regulated utility model.

DTE's first-mover advantage in Michigan matters. While Consumers Energy also has aggressive clean energy plans, DTE is larger, more diversified, and further along in its transformation. The company's relationships with major industrial customers, established renewable development capabilities, and political influence create meaningful competitive moats.

The financial metrics support multiple expansion. With 5-7% annual earnings growth, a secure dividend yielding ~3%, and improving ESG scores attracting sustainable investment funds, DTE could see its valuation multiples expand from current utility averages toward renewable energy comparables.

Climate resilience adds another dimension. As extreme weather becomes more frequent, the value of reliable energy infrastructure increases. DTE's grid hardening investments, while expensive, create a more valuable and defensible asset base. The company that keeps the lights on during polar vortexes and summer heat waves earns pricing power and political capital.

The Bear Case: Execution Risk Meets Rate Fatigue

The skeptical view sees massive execution risk inadequately compensated by regulated returns. Start with the sheer scale of transformation: DTE must execute $30 billion in capital projects while maintaining grid reliability during the most complex operational transition in its history. The margin for error is zero—one major blackout during the transition could trigger political backlash and regulatory penalties.

Stranded asset risk looms large. Accelerated coal retirements mean writing off billions in undepreciated assets. While securitization helps, it still represents dead weight on customer bills. If natural gas plants also face early retirement due to climate policies, the stranded asset problem multiplies.

Regulatory lag poses persistent challenges. DTE invests capital today but doesn't earn returns until the next rate case—potentially years later. With inflation volatile and interest rates elevated, the company could face systematic under-earning on its massive capital program.

Rate fatigue is reaching critical levels. Michigan already has above-average electricity rates for the Midwest. Adding billions in transformation costs, even with federal support, will pressure affordability. Political backlash could lead to regulatory disallowances, ROE compression, or even municipalization threats.

Competition from distributed generation represents an existential threat. As solar-plus-storage costs decline, large commercial and industrial customers may defect from the grid—or at least dramatically reduce their usage. This "utility death spiral" would leave remaining customers bearing fixed costs across a shrinking base.

Grid reliability during the transition terrifies operators. Replacing dispatchable coal with intermittent renewables requires perfect orchestration of battery storage, demand response, and grid management. One mistimed coal retirement or delayed renewable project could trigger rolling blackouts.

Technology risk compounds operational challenges. DTE is betting billions on battery storage scaling successfully, wind and solar performing as modeled, and grid software managing unprecedented complexity. Technology disappointments could require expensive workarounds or duplicative investments.

High debt levels limit financial flexibility. With debt-to-capital already elevated and billions more borrowing required, DTE faces interest rate sensitivity and potential credit downgrades. Even with DOE loan guarantees, the company's balance sheet will be stretched.

The Verdict: Transformation with Training Wheels

The reality likely lies between these extremes. DTE's transformation is genuinely ambitious and fraught with execution risk. But unlike merchant generators or competitive retailers, the company operates within a regulatory framework that provides both constraints and protection.

The DOE loan guarantees are particularly important—they're essentially training wheels for the energy transition, providing cheap capital and implicit federal backing for DTE's transformation. This support, combined with IRA tax credits and Michigan's supportive regulatory environment, significantly de-risks the clean energy pivot.

The key variables to watch: execution on major projects (especially battery storage and grid modernization), regulatory decisions on cost recovery and ROE, customer rate impacts and political reactions, and competition from distributed resources and alternative energy providers.

For investors, DTE represents a relatively safe way to play the energy transition—not the highest upside, but with regulated utility downside protection. The company will likely muddle through its transformation, neither spectacular success nor dramatic failure, earning regulated returns on an ever-growing asset base while gradually becoming a cleaner, more modern utility.

XII. Epilogue: The Future of Regulated Utilities

Standing at the site of the old Trenton Channel coal plant, where smokestacks once dominated the Detroit River skyline, you can now see construction crews building what will be Michigan's largest battery storage facility. The symbolism is perfect: the infrastructure of the 20th century giving way to the technology of the 21st, on the same ground, serving the same fundamental need—keeping the lights on in Michigan.

DTE's transformation represents more than one company's strategic pivot. It's a template for how century-old utilities can navigate the energy transition while maintaining their social compact. The lesson isn't that every utility should copy DTE's specific moves, but that transformation is possible within regulatory frameworks, with the right stakeholder engagement and political support.

The tension between monopoly utilities and competitive energy markets will only intensify. As technology enables greater customer choice—from rooftop solar to community microgrids to peer-to-peer energy trading—the traditional utility model faces existential questions. DTE's answer has been to embrace the platform role: becoming the essential backbone that enables various energy resources to interconnect reliably.

The climate-reliability-affordability trilemma remains unsolved, but DTE's approach suggests a path forward. By securing federal support, building stakeholder consensus, and maintaining political neutrality, the company has created space to manage these trade-offs. It's not perfect—coal plants are still running, rates are still rising, and reliability challenges persist—but it's progress.

For other utilities watching DTE's transformation, several lessons emerge. First, early action creates options—DTE's head start in renewables positioned it to capture federal support. Second, stakeholder engagement is investment, not overhead—the CleanVision settlement saved years of litigation. Third, workforce transition must be proactive—retraining programs and early retirement packages prevent labor strife. Fourth, regulatory relationships are strategic assets—trust built over decades enables ambitious programs.

The next decade will test whether DTE's transformation succeeds. Can the company retire coal plants on schedule while maintaining reliability? Can battery storage scale to provide grid stability? Can rates remain affordable as billions flow into new infrastructure? Can the utility model itself survive the rise of distributed resources?

What's certain is that the status quo is not an option. Climate change, technology advancement, and customer expectations are forcing utilities to transform. DTE's journey from gas lamps to grid batteries shows that even the most traditional companies can reinvent themselves—slowly, carefully, but fundamentally.

The story that began with Lemuel Davis lighting 53 gas lamps in 1851 continues today with Jerry Norcia planning thousands of megawatts of renewable energy. Both men faced the same challenge: providing reliable, affordable energy to power Michigan's economy. The technology changes, the regulations evolve, the stakeholders multiply—but the mission remains constant.

As we look toward 2050 and DTE's net-zero target, one thing becomes clear: the utility of the future will look nothing like the utility of the past. But if history is any guide, DTE will still be there, adapting to whatever comes next, keeping the lights on in Michigan. The company that powered the rise of the automobile industry will power whatever industry defines Michigan's next century.

The transformation is far from complete, the challenges remain immense, and success is not guaranteed. But for investors, policymakers, and citizens alike, DTE's journey offers both lessons and hope. In an era of climate crisis and technological disruption, even the most entrenched incumbents can change. Sometimes it just takes 175 years of practice.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube