Ameren Corporation: America's Midwest Power Play

I. Cold Open & Episode Setup

Picture this paradox: In the heart of America's industrial midwest, where the Mississippi River once powered the nation's westward expansion, sits a 140-year-old utility company betting billions that the future of energy looks nothing like its past. Ameren Corporation manages rusting coal plants scheduled for demolition while simultaneously deploying cutting-edge solar farms and smart grid technology. It's a company that generates reliable dividends from regulated monopolies while racing against time to reinvent the very foundation of its business model.

On New Year's Eve 1997, as the world partied its way toward Y2K fears, two century-old utility companies—Union Electric Company of St. Louis and Central Illinois Public Service Company—quietly merged to form Ameren Corporation. The timing was symbolic: one era ending, another beginning. The newly minted company inherited hydroelectric dams from the 1920s, nuclear plants from the 1980s, and coal facilities that had powered America's industrial revolution. Today, that same company is orchestrating one of the most ambitious clean energy transitions in the utility sector, targeting net-zero carbon emissions by 2045 while investing $26.3 billion over the next five years alone.

The fundamental question isn't whether Ameren can keep the lights on—it's whether a regulated utility, bound by century-old regulatory compacts and serving some of America's most economically challenged regions, can transform itself into a clean energy powerhouse while delivering the steady returns that make utilities the bedrock of conservative portfolios. Can you innovate when your returns are capped by regulators? Can you take risks when reliability is non-negotiable? Can you invest tens of billions in new infrastructure while retiring perfectly functional assets?

What makes Ameren particularly fascinating is its unique position straddling two states with vastly different regulatory philosophies—Missouri's traditional approach versus Illinois's aggressive clean energy mandates. It's like running two different companies under one roof, each with its own rules, politics, and investment opportunities. The company serves 2.4 million electric customers and 900,000 natural gas customers across 64,000 square miles, making it both massive in scale and intimate in its community relationships.

This is a story about transformation at geological speed—rapid for a utility, glacial for Silicon Valley. It's about managing the tension between shareholders demanding growth, regulators controlling prices, environmentalists pushing for change, and customers who just want their bills to stay flat. Most importantly, it's about how a business model everyone calls boring might actually be one of the most interesting investment opportunities of the energy transition. Because when you peel back the layers, utilities aren't just infrastructure companies—they're the ultimate platform business, and electrification is about to make them more essential than ever.

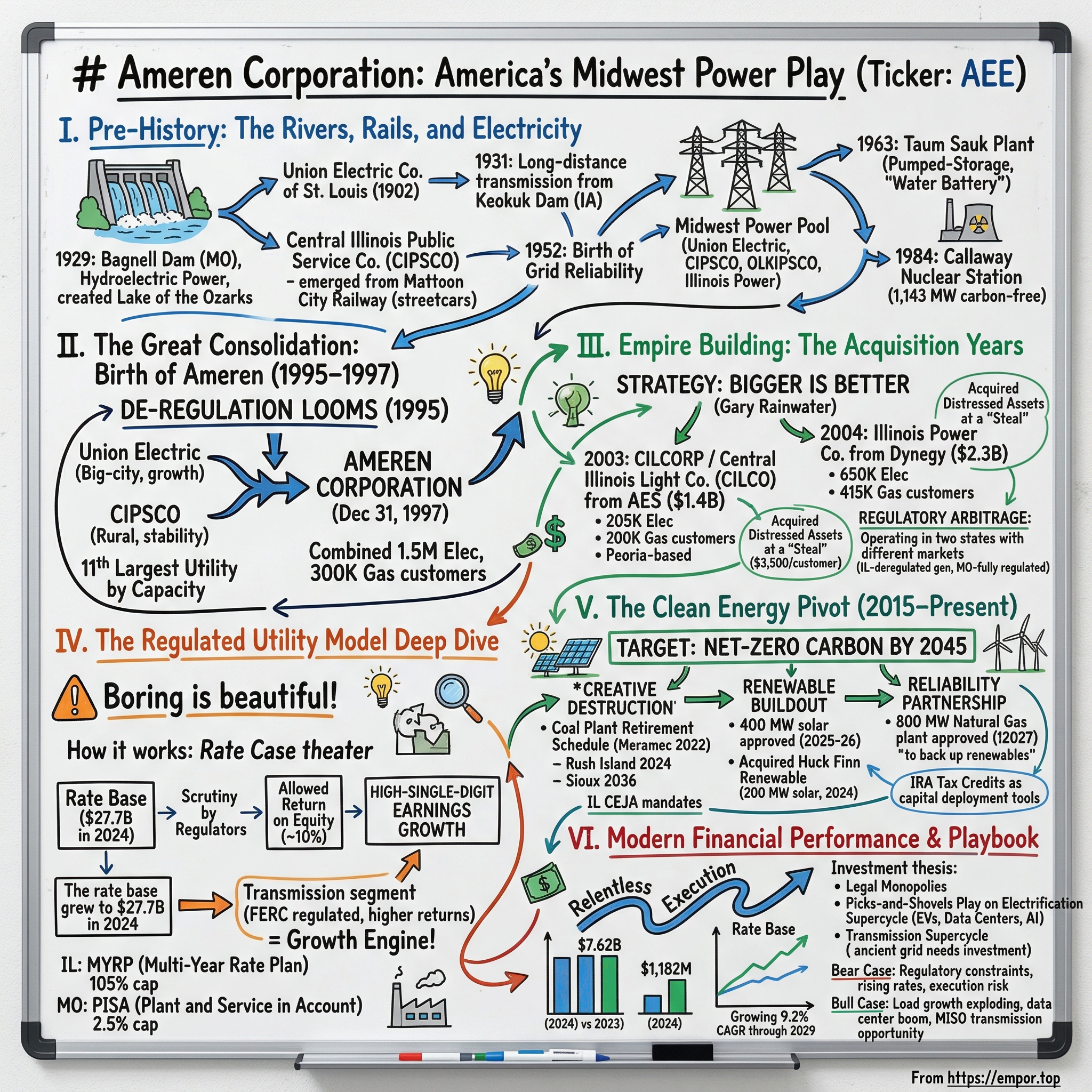

II. Pre-History: The Rivers, Rails, and Electricity

The story of Ameren begins not in boardrooms but on riverbanks. In 1929, as America teetered on the edge of the Great Depression, engineers completed what seemed impossible: the Bagnell Dam on Missouri's Osage River. This wasn't just another infrastructure project—it was an audacious bet on electricity's future. The dam generated 175 megawatts of hydroelectric power for Union Electric Company, but perhaps more remarkably, it created the Lake of the Ozarks with 1,400 miles of shoreline. Think about that engineering marvel: they didn't just build a power plant; they created Missouri's playground, a massive recreational destination that would define the region's identity for generations.

Union Electric itself had emerged from the chaos of St. Louis's early electrical industry in 1902. Picture turn-of-the-century St. Louis: horses still dominated the streets, gas lamps flickered at dusk, and dozens of small power companies fought territorial battles over who would wire which neighborhoods. The company that would become half of Ameren started as Union Company, consolidating these warring factions into something resembling order. Meanwhile, 175 miles northeast in Mattoon, Illinois, the other half of Ameren's DNA was taking shape in an unlikely form: a streetcar company. Central Illinois Public Service Company began life as the Mattoon City Railway, because in those days, whoever ran the trolleys often ended up running the power plants too.

The real breakthrough came in 1931, when Union Electric did something that redefined what utilities could be. They started buying power from the Keokuk Dam in Iowa, 150 miles north of St. Louis. This wasn't just a power purchase—it was a leap of faith in long-distance electricity transmission. The dam provided 134 megawatts carried over a distance that engineers of the day considered borderline impossible. Union Electric didn't just buy the power; they eventually bought the entire dam. It was a move that would establish a pattern: think bigger, reach farther, consolidate relentlessly.

By 1952, the pieces of what would become Ameren were learning to work together in ways that presaged modern grid operations. Central Illinois Public Service Company and Union Electric Company formed the Midwest Power Pool, one of the nation's first power-sharing arrangements. They were joined by what would later become another Ameren subsidiary, Illinois Power Company. This wasn't just bureaucratic reshuffling—it was the birth of grid reliability as we know it today. When one utility's generators failed, another's could instantly fill the gap. It was socialism for electrons, capitalism for companies.

The 1960s brought the golden age of American utility expansion, and Union Electric was determined not to be left behind. In 1963, they completed construction of the Taum Sauk Plant, one of the largest pumped-storage facilities of its era. Here's how audacious this project was: they built a reservoir on top of a mountain, pumped water uphill when electricity was cheap, then released it through turbines when power was expensive. It was a 350-megawatt battery made of water and gravity, decades before anyone talked about energy storage. The plant would later suffer a catastrophic failure in 2005, but in 1963, it represented the cutting edge of grid flexibility.

Then came the nuclear age. In 1984, Union Electric brought online the Callaway Nuclear Generating Station, adding 1,143 megawatts of carbon-free power to its portfolio. The timing was terrible—Three Mile Island had soured public opinion, Chernobyl was just two years away, and natural gas was cheap. But Union Electric pressed forward, spending billions on a bet that nuclear would be the future. They were both right and wrong in ways they couldn't have imagined. The plant would become one of their most valuable assets, but it would also be their last nuclear facility, as the economics and politics of atomic power shifted beneath their feet.

By the mid-1990s, these two utilities—Union Electric and CIPSCO—had spent nearly a century building the backbone of Midwest electricity. They'd mastered every generation technology from hydroelectric to nuclear, created one of the nation's first power pools, and learned to transmit electricity over distances their founders couldn't have imagined. But the world was changing. Deregulation loomed, competition threatened, and scale suddenly mattered more than ever. The stage was set for a merger that would create something entirely new from very old parts.

III. The Great Consolidation: Birth of Ameren (1995–1997)

The boardroom at Union Electric's St. Louis headquarters hummed with tension in early 1995. CEO Charles Mueller stared at spreadsheets showing a stark reality: deregulation was coming whether utilities liked it or not. California was already dismantling its regulated monopolies, and whispers from Washington suggested the Midwest would be next. Mueller's counterpart at CIPSCO, Gordon Voss, faced the same existential question from his Peoria office: How do you compete in a deregulated market when you've never had to compete at all?

The numbers told a compelling story of two companies that needed each other. Union Electric commanded assets of nearly $600 million but carried $1.8 billion in long-term debt—a leverage ratio that made Wall Street nervous. CIPSCO was smaller but proportionally more indebted, with $210 million in assets against nearly $500 million in long-term obligations. Separately, they were regional players vulnerable to whatever deregulation might bring. Together, they could create something with the scale to survive, maybe even thrive.

The merger negotiations revealed fascinating corporate cultures shaped by geography and history. Union Electric executives, schooled in the big-city dynamics of St. Louis, pushed for aggressive expansion and modern management techniques. CIPSCO's leadership, rooted in downstate Illinois's agricultural communities, emphasized customer relationships and conservative operations. The cultural divide was real—urban versus rural, Missouri versus Illinois, growth versus stability. But both sides recognized that their differences might actually be strengths if properly combined. The shareholders voted in 1995, but it would take over two years to close the deal. The $1.3 billion transaction—expected to save the firm approximately $759 million over a ten-year period—was eventually completed in December 1997 after undergoing scrutiny by several regulatory commissions. Six different regulatory bodies had to sign off: the SEC, FERC, the Illinois Commerce Commission, the Missouri Public Service Commission, the Nuclear Regulatory Commission, and antitrust authorities. Each had their own concerns, their own politics, their own conception of what utility consolidation meant for the public interest.

The name itself revealed ambition: Ameren, combining "American" and "Energy." Not St. Louis Electric, not Midwest Power, but American Energy—a name that suggested continental aspirations even as the company remained firmly rooted in two states. It was classic utility hubris, the kind of grandiose thinking that would later drive the company to make even bigger acquisitions.

Pursuant to the merger agreement, each outstanding share of Union Electric common stock was exchanged for one share of Ameren common stock and each outstanding share of CIPSCO common stock was exchanged for 1.03 shares of Ameren common stock. That 3% premium for CIPSCO shareholders was the price of getting the smaller company to the altar. Small in percentage terms, but when multiplied across millions of shares, it represented real money—and a bet that the synergies would more than compensate.

When the merger closed on December 31, 1997, Ameren instantly became the 11th largest utility in America by generating capacity. With assets of approximately $9 billion, Ameren was parent of Union Electric (now known as AmerenUE) and Central Illinois Public Service Company (now known as AmerenCIPS). The combined company served 1.5 million electric customers and 300,000 natural gas customers across a 44,500-square mile footprint.

What's fascinating about this merger is how it presaged every major utility combination that would follow. The playbook was simple but powerful: combine adjacent service territories, eliminate duplicate functions, spread fixed costs over more customers, and use the savings to fund infrastructure investments. It was economies of scale applied to electrons and molecules. But unlike manufacturing or retail, where consolidation often meant plant closures and layoffs, utility mergers were different. You couldn't close a power plant just because you owned two—customers still needed electricity. The efficiencies came from back-office consolidation, joint procurement, and optimized dispatch across a larger fleet.

The timing proved prescient. Deregulation, which seemed inevitable in 1997, largely fizzled in the Midwest after California's disastrous experiment in 2000-2001. Ameren got the benefits of scale without the brutal competition everyone expected. They prepared for a war that never came, and the peacetime dividend was substantial. The merger would provide the financial strength and operational scale needed for the acquisition spree that followed, transforming Ameren from a two-state utility into a regional powerhouse positioned perfectly for the energy transition ahead.

IV. Empire Building: The Acquisition Years (2000–2004)

Gary Rainwater took the helm as CEO in 2003 with a simple philosophy: in the utility business, bigger is almost always better. He'd watched from his COO perch as deregulation swept through California and Texas, creating chaos and opportunity in equal measure. While those experiments largely failed, they taught a crucial lesson—scale would determine survival in whatever market structure emerged. Rainwater didn't wait for regulators to force consolidation; he decided to drive it himself.

The first major move came that same year when Ameren acquired CILCORP Inc. and its crown jewel subsidiary, Central Illinois Light Company (CILCO), from AES Corporation for $1.4 billion. This wasn't just any utility—CILCO had been paying dividends continuously since 1921, through the Depression, World War II, and every economic cycle since. Based in Peoria, CILCO brought 205,000 electric and 200,000 natural gas customers, essentially filling the geographic gap between Ameren's existing Missouri and downstate Illinois territories. AES, desperate for cash after its international adventures went sideways, was a motivated seller. Rainwater got a bargain.

But the real prize came in 2004 with the acquisition of Illinois Power Company from Dynegy Inc. This deal was a masterclass in distressed asset acquisition. Illinois Power had about $360 million in assets but carried long-term debt of over $2 billion. Dynegy, reeling from the Enron scandal's fallout and its own failed trading strategies, needed to dump Illinois Power to survive. Ameren paid just $2.3 billion in cash and assumed debt for a utility serving 650,000 electric and 415,000 natural gas customers. When you did the math, Ameren was paying roughly $3,500 per customer—a steal in an industry where customer acquisition costs typically ran much higher.

The integration of Illinois Power revealed both the promise and peril of utility consolidation. On paper, the synergies were compelling: Illinois Power's service territory literally surrounded Ameren's existing Illinois operations, creating opportunities for operational efficiencies that investment bankers dream about. Combined dispatch, shared transmission infrastructure, consolidated customer service—the savings potential was enormous. But Illinois Power came with baggage. Its coal plants were aging, its distribution infrastructure needed billions in upgrades, and its regulatory relationships were strained after years of Dynegy's financial engineering.

What made these acquisitions brilliant wasn't just the price—it was the regulatory arbitrage Rainwater recognized. Illinois had embraced deregulation for generation while keeping distribution regulated. Missouri remained fully regulated. By owning utilities in both states, Ameren could optimize its generation fleet across different market structures, selling power where prices were highest while maintaining stable regulated returns on distribution assets. It was like playing chess on two boards simultaneously, moving pieces between them as market conditions shifted.

The cultural integration proved surprisingly smooth, perhaps because misery loves company. All three acquired utilities—CILCO, Illinois Power, and the original CIPSCO—had been battered by their previous owners' ambitions. Their employees were grateful for stability, for an owner that understood the utility business wasn't about quarterly earnings surprises but decades-long infrastructure planning. Ameren offered something their previous corporate parents couldn't: patience.

By the end of 2004, Ameren had assembled a utility empire serving 2.4 million electric and 900,000 natural gas customers across 64,000 square miles. The company controlled 14,500 megawatts of generating capacity, making it one of the largest utilities in the Midwest. The acquisition spree had cost nearly $5 billion, funded through a combination of cash, debt, and equity issuances that tested Wall Street's appetite for utility paper. But Rainwater had built what he wanted: a utility with the scale to compete, the diversity to manage risk, and the regulatory relationships to navigate whatever energy policy emerged from Washington and state capitals.

The timing, in retrospect, was perfect. These acquisitions were completed just before the shale gas revolution transformed American energy economics, before renewable mandates reshaped generation planning, and before climate concerns made coal plants stranded assets rather than cash cows. Ameren bought at the end of one era, giving it the resources to invest in the next. The empire Rainwater built would soon face its greatest test: transforming from a coal-dependent utility into a clean energy leader while keeping the lights on and the dividends flowing.

V. The Regulated Utility Model Deep Dive

To understand Ameren's business, you need to grasp a fundamental paradox: this is a company whose prices are set by government bureaucrats, whose returns are capped by mathematical formulas, and whose every major decision requires regulatory approval—yet it consistently generates returns that make growth investors jealous. The secret lies in the regulated utility model itself, a century-old compact between monopolies and the public that turns conventional capitalism on its head.

Here's how it actually works. Ameren operates through four distinct segments, each with its own regulatory framework. Ameren Missouri serves 1.2 million electric and 132,000 natural gas customers under traditional cost-of-service regulation. Ameren Illinois Electric Distribution and Ameren Illinois Natural Gas operate under performance-based formulas. Ameren Transmission plays by federal rules that offer the highest returns. Each segment is essentially a different business with different economics, united only by common ownership and shared infrastructure.

The rate-setting process is theater with predetermined outcomes. Every few years, Ameren files a rate case—thousands of pages documenting every dollar spent, every kilowatt generated, every mile of wire strung. Regulators scrutinize these costs, consumer advocates object, industrial customers lobby, and after months of hearings, a number emerges: the allowed return on equity, typically between 9% and 10%. This becomes Ameren's speed limit—it can't earn much more, but critically, it's virtually guaranteed to earn this much. It's socialism for capitalists, and it works brilliantly.

The magic happens in something called the rate base—the value of assets on which Ameren earns its allowed return. Ameren's rate base grew to $27.7 billion in 2024, up from $25.8 billion in 2023. Every dollar added to rate base generates roughly 10 cents in annual allowed earnings. This creates a powerful incentive: utilities love capital projects. Building a new substation, upgrading transmission lines, installing smart meters—these aren't expenses to minimize but investments to maximize. The more Ameren spends (prudently, as judged by regulators), the more it earns.

This dynamic explains why utilities embrace massive infrastructure projects that would terrify normal companies. Ameren's planned $26.3 billion capital expenditure program through 2029 isn't a drag on earnings—it's the source of earnings growth. The company expects to grow its rate base at a 9.2% compound annual rate through 2029. Simple math: 9.2% rate base growth plus a ~10% allowed return equals high-single-digit earnings growth with minimal risk. It's the closest thing to a perpetual motion machine capitalism has created.

The transmission segment deserves special attention because it's where the regulated model gets turbocharged. Transmission assets are regulated by FERC, not state commissions, and FERC allows returns typically 100-200 basis points higher than state-regulated distribution assets. Better yet, transmission investments often qualify for special incentive rates recognizing their regional benefits. Ameren Transmission has become the company's growth engine, contributing an outsized portion of earnings growth despite being the smallest segment by revenue.

But the model has constraints that frustrate MBA-trained executives. In Illinois, Ameren operates under a Multi-Year Rate Plan (MYRP) with a 105% reconciliation cap—if the company earns more than 105% of its allowed return, it must refund the excess to customers. Missouri's Plant and Service in Account (PISA) mechanism limits annual revenue requirement increases to 2.5%. These caps mean Ameren can't capture the full value of operational improvements or favorable weather. It's like running a race where going too fast disqualifies you.

The regulatory compact also means political risk is existential. A hostile utilities commission can destroy billions in market value with a single adverse decision. This makes regulatory relationships paramount. Ameren executives spend as much time in Jefferson City and Springfield as they do in St. Louis, cultivating relationships, building trust, demonstrating reliability. It's a business where being boring is a virtue, where steady competence beats flashy innovation, where the worst thing you can do is surprise your regulator.

What makes this model brilliant for investors is its predictability in an unpredictable world. Recessions barely dent electricity demand. Inflation gets passed through to customers via fuel adjustment clauses. Competition is illegal—try starting your own utility and see how far you get. Technology disruption happens at geological pace. It's the ultimate defensive business, which is why utilities anchor pension funds and widow-and-orphan portfolios. But as Ameren is discovering, this stable, predictable model is perfectly positioned for the massive capital deployment required for the energy transition. Sometimes boring businesses are exactly where you want to be when the world changes.

VI. The Clean Energy Pivot (2015–Present)

Warner Baxter became CEO in 2014 with a problem that would have seemed absurd to his predecessors: Ameren's coal plants, once the crown jewels of its generation fleet, were becoming liabilities. The math was brutal—natural gas prices had collapsed thanks to fracking, renewable costs were plummeting, and environmental regulations were tightening like a vice. But here's what made Baxter's challenge extraordinary: he had to execute one of the most ambitious clean energy transitions in the utility sector while maintaining reliability for 2.4 million customers and keeping investors happy with steady dividend growth. No pressure.

The transformation began with a target that seemed fantastical when announced: net-zero carbon emissions by 2045. The interim goals were even more aggressive—60% reduction by 2030 and 85% by 2040, all from 2005 levels. For a utility that generated 75% of its electricity from coal just a decade earlier, this was like promising to turn an oil tanker into a sailboat while keeping it moving at full speed. But Baxter understood something his critics missed: the clean energy transition wasn't just an environmental necessity—it was the greatest capital deployment opportunity in Ameren's history.

The coal plant retirement schedule reads like a industrial obituary. Ameren shuttered its Meramec Energy Center in 2022, ending 70 years of coal combustion on the Mississippi River. The Rush Island Energy Center follows in 2024, and the massive Sioux Energy Center will close in 2036. Each closure eliminates millions of tons of annual CO2 emissions but also removes thousands of megawatts of dispatchable generation that has kept the lights on for generations. It's creative destruction on a massive scale. But here's where the strategy gets sophisticated. Ameren received approval to build or acquire approximately 400 megawatts of solar energy, with the first of three solar projects scheduled to go into service in 2025, and two more set to begin serving customers in 2026. The real acceleration came in 2024 when Ameren acquired the Huck Finn Renewable Energy Center, a 200-MW solar facility, the third utility-scale solar facility acquired this year. The three facilities having a combined capacity of 500 MW representing a total acquisition cost of approximately $900 million—that's $1,800 per kilowatt, remarkably cheap for utility-scale solar.

The renewable buildout is impressive, but what makes Ameren's strategy brilliant is recognizing that renewable energy alone can't maintain grid reliability. Solar panels don't generate electricity at night, wind turbines don't spin when the air is still, and batteries aren't yet cheap enough to provide days of backup power. So Ameren received approval to build an 800-megawatt simple-cycle natural gas energy center expected to be ready in 2027, representing an investment of approximately $900 million. This Castle Bluff Energy Center isn't a betrayal of clean energy goals—it's what makes them possible. Castle Bluff is designed to deliver energy on the coldest winter days, the hottest summer afternoons and back up the grid when renewable energy generation is otherwise unavailable.

The integration of renewables with dispatchable gas generation reveals the engineering reality behind the energy transition. When solar generation predictably rises and falls each day, you need fast-ramping gas turbines to fill the gaps. It's a dance between intermittent and dispatchable resources, choreographed by grid operators working with sub-second precision. Ameren's investment in both technologies isn't hedging—it's system design.

Illinois's Climate and Equitable Jobs Act (CEJA) added another layer of complexity, mandating specific renewable procurement targets and equity requirements that go far beyond Missouri's voluntary approach. But rather than resist, Ameren embraced the requirements as an opportunity to accelerate capital deployment. Every mandate becomes a justification for rate base additions, every requirement an earnings opportunity. It's regulatory jujitsu—using the force of environmental regulation to drive shareholder returns.

The financial engineering behind the clean energy transition is equally sophisticated. Renewable projects qualify for federal investment tax credits, production tax credits, and accelerated depreciation that dramatically improve their economics. Ameren can monetize these credits through tax equity partnerships, reducing the net cost of renewable investments while keeping the full rate base value. It's having your cake and eating it too—lower costs for customers, higher rate base for shareholders.

What's remarkable is how Ameren has turned climate risk into competitive advantage. Every coal plant retirement removes stranded asset risk from the balance sheet. Every renewable addition attracts ESG-focused investors. Every grid modernization investment improves reliability while earning regulated returns. The company that seemed most threatened by the energy transition has become one of its biggest beneficiaries. The transformation from coal-dependent laggard to clean energy leader isn't complete—Ameren still generates significant power from fossil fuels—but the trajectory is clear and the economics are compelling.

VII. Modern Financial Performance & Strategy

The numbers tell a story of relentless execution masked by accounting complexity. In 2024 the company made a revenue of $7.62 Billion, an increase over the revenue in 2023 of $7.50 Billion. But revenue in the utility business is almost meaningless—what matters is the relationship between rate base, allowed returns, and actual earnings. Ameren announced 2024 net income attributable to common shareholders of $1,182 million, or $4.42 per diluted share, with adjusted net income of $1,237 million, or $4.63 per diluted share.

The adjusted earnings story reveals the real performance. Strip away the one-time charges—including a $59 million hit related to the Rush Island Energy Center NSR litigation settlement—and you see a utility executing its playbook with machine-like precision. Adjusted earnings results for 2024 were driven by strong operating performance and execution of the company's strategy, with higher earnings primarily the result of increased infrastructure investments and disciplined cost management.

As of July 2024 Ameren has a market cap of $21.17 Billion, placing it squarely in the mid-cap utility universe—big enough to access capital markets efficiently, small enough to deliver meaningful growth. The valuation reflects both the stability of the business model and the growth potential of the capital program. At roughly 18 times forward earnings, Ameren trades at a premium to slow-growth utilities but a discount to renewable pure-plays, exactly where you'd expect for a company transitioning between the two.

The capital allocation strategy is breathtaking in its ambition. Ameren plans capital expenditures of $26.3 billion from 2025 through 2029. To put that in perspective, they're planning to invest more than their entire market cap over the next five years. This isn't reckless spending—every dollar goes into rate base, earning that regulated return. The company expects to grow rate base at a 9.2% compound annual rate through 2029, which should translate directly into earnings growth given stable allowed returns.

But here's where it gets interesting: Ameren needs to fund this massive capital program without destroying its balance sheet. The solution? Plans to issue approximately $600 million of equity annually from 2025 through 2029. That's $3 billion in dilution over five years, yet the company still expects to grow earnings per share at 6-8% annually. The math only works because the rate base growth more than offsets the dilution—a beautiful example of the utility model's capital recycling machine in action.

The 2025 earnings guidance tells the near-term story: $4.85 to $5.05 per share, with a 6% dividend increase resulting in an annualized rate of $2.84 per share. That's a roughly 3% dividend yield with 6% annual growth—the holy grail for income investors. The dividend payout ratio of roughly 60% leaves room for both dividend growth and balance sheet flexibility, crucial given the massive capital program ahead.

The segment performance reveals the growth drivers. Ameren Transmission reported adjusted earnings of $333 million in 2024, with GAAP earnings of $323 million compared with $296 million in the prior-year period, driven by increased earnings from infrastructure investments. Transmission is the rocket fuel—highest returns, fastest growth, federal regulation that's generally more favorable than state oversight.

Meanwhile, Ameren Illinois Electric Distribution faces headwinds. The segment reported earnings of $234 million in 2024 compared with $258 million a year ago, with the decline due to a lower allowed return on equity for 2024 under the new multi-year rate plan. This is the regulatory compact in action—sometimes you win, sometimes you lose, but over time the system delivers predictable returns.

What makes Ameren's financial strategy particularly clever is how they're using the energy transition to accelerate earnings growth while maintaining financial flexibility. Every coal plant retirement frees up capital for renewable investment. Every renewable project qualifies for federal subsidies that improve returns. Every transmission upgrade earns FERC-approved returns that exceed state-allowed levels. It's financial engineering meets energy engineering, and when executed properly, both shareholders and customers win. The company that seemed boring a decade ago has become one of the most dynamic stories in the utility sector, all while maintaining the steady, predictable characteristics that make utilities attractive to conservative investors.

VIII. Playbook: The Utility Investment Thesis

The utility sector represents the ultimate paradox of modern capitalism: companies with monopoly power that can't exploit it, businesses with guaranteed returns that still manage to fail, infrastructure so critical that society can't function without it yet so boring that investors ignore it. Understanding why utilities are the ultimate infrastructure play requires grasping a fundamental truth—they're not really energy companies. They're toll collectors on the electron highway, and traffic is about to explode.

Start with the basics: utilities are the only businesses where being a monopoly is explicitly legal and extensively regulated. You literally cannot compete with Ameren in its service territory—it's against the law. Try running your own power lines to homes in St. Louis and see how far you get. This monopoly status comes with a bargain: in exchange for exclusive franchise rights, utilities accept regulated returns. It's socialism and capitalism having a baby, and that baby prints money with stunning regularity.

The regulated return model is beautifully predictable once you understand the game. Regulators set an allowed return on equity, typically 9-10% for Ameren. The utility then invests capital, adds it to rate base, and earns that return year after year until the asset is fully depreciated. It's like buying a bond that pays 10% forever, except you get to issue the bond to yourself. The more you invest (prudently), the more you earn. This creates a perverse incentive where utilities love capital projects the way social media companies love user engagement—it's the core driver of value creation.

Capital recycling is where the magic happens. Ameren spends $5 billion on infrastructure, adds it to rate base, earns 10% returns ($500 million annually), uses that cash flow to fund more investments, rinse and repeat. It's compound interest for infrastructure, and over decades, the results are staggering. A utility that steadily grows rate base at 7% while earning 10% returns will double earnings every decade without taking any real business risk. It's the most boring path to wealth creation ever invented, which is precisely why it works.

ESG has transformed from compliance burden to business driver. Climate-conscious investors now pour money into utilities leading the energy transition. Ameren's net-zero commitment by 2045 isn't just environmental virtue signaling—it's a massive capital deployment opportunity dressed up as climate action. Every renewable project, every grid modernization initiative, every electric vehicle charging station goes into rate base and earns returns. The energy transition isn't a threat to utilities; it's the greatest growth opportunity in their history.

The transmission supercycle deserves special attention. America's grid is ancient, inadequate, and about to face unprecedented demand from data centers, EVs, and electrification. Transmission investments earn the highest returns (often 11-12%), face the least regulatory pushback (because everyone agrees we need more transmission), and benefit from federal rather than state regulation. Ameren's participation in MISO (Midcontinent Independent System Operator) positions it perfectly to capture this opportunity. Think of transmission as the highway system of the 21st century, except privately owned and gorgeously profitable.

Managing political and regulatory risk across multiple jurisdictions is where utilities earn their returns. Ameren navigates Missouri's conservative politics and Illinois's progressive mandates simultaneously. It's like being married to two people with opposite personalities and keeping both happy. The key is never surprising anyone—utilities that spring unexpected rate increases or massive write-offs quickly find themselves facing hostile regulators. Boring is beautiful in this business.

The load growth story is just beginning. For decades, electricity demand was flat as efficiency improvements offset economic growth. That's over. Data centers alone could double electricity demand in some regions. Electric vehicles will add another layer of growth. Heat pump adoption means even gas customers become electric customers. Industrial reshoring requires massive amounts of power. We're entering an electrification supercycle just as the generation fleet needs wholesale replacement. It's the perfect storm for utility investment.

Here's what most investors miss: utilities are platform businesses. The poles, wires, pipes, and plants are just the physical manifestation of a network that society cannot function without. Every new technology that requires electricity—from AI data centers to Bitcoin mining to hydrogen production—must connect to the utility's platform. The utility doesn't need to understand the technology or take technology risk; it just needs to deliver electrons reliably. It's the ultimate picks-and-shovels play on every technology trend simultaneously.

The regulatory compact means utilities are essentially government-sponsored enterprises with private ownership. They can't go bankrupt (regulators won't allow it), can't earn excessive returns (regulations prevent it), but also can't earn inadequate returns (the regulatory compact requires fair returns). It's the Goldilocks business model—not too hot, not too cold, just right for risk-averse investors who want equity-like returns with bond-like predictability. In a world of zero interest rates, negative-yielding bonds, and cryptocurrency speculation, boring utilities suddenly look like genius investments.

IX. Bear vs. Bull Case

Bear Case: The Constraints Are Real

The bearish case starts with a brutal reality: Ameren operates in a straitjacket of regulatory constraints that would make most CEOs quit in frustration. Illinois's Multi-Year Rate Plan includes a 105% reconciliation cap—if Ameren earns more than 105% of its allowed return, it must refund the excess to customers. Think about that: you literally cannot succeed too much. It's like playing basketball where scoring too many points means you lose. Missouri's PISA mechanism limits annual revenue requirement increases to 2.5%, regardless of inflation, interest rates, or investment needs. These aren't temporary restrictions; they're fundamental features of the business model.

The execution risk on Ameren's $26.3 billion capital plan is staggering. This isn't just writing checks—it's building massive infrastructure projects on time, on budget, while maintaining reliability. One major project failure, one nuclear incident, one transmission line that takes twice as long to build as planned, and the carefully orchestrated financial plan falls apart. The Taum Sauk reservoir collapse in 2005 cost hundreds of millions and took years to resolve. The Rush Island Energy Center NSR litigation just settled for $59 million. These aren't black swan events; they're the regular cost of operating massive industrial infrastructure.

Rising interest rates represent an existential threat that most utility investors underappreciate. Utilities are essentially leveraged bond proxies—they borrow at one rate and earn a regulated return at another rate. When interest rates rise faster than regulatory proceedings can adjust allowed returns, utilities get squeezed. Ameren's long-term debt totaled $17.26 billion as of December 31, 2024, up from $15.12 billion a year earlier. Every 100 basis point increase in interest rates costs roughly $170 million annually. Regulators move at geological speed; bond markets move at light speed. That timing mismatch can destroy earnings.

The distributed generation disruption threat is real and accelerating. Solar panels keep getting cheaper, batteries keep getting better, and every wealthy customer who goes off-grid is one less customer paying for the infrastructure that serves everyone else. It's a utility death spiral: fixed costs spread over fewer customers, raising rates, driving more customers to self-generate, raising rates further. Ameren can't stop customers from installing rooftop solar any more than Blockbuster could stop Netflix. The monopoly only works if customers have no alternative.

The environmental litigation overhangs keep piling up. The $59 million Rush Island settlement is just the latest in a long string of environmental challenges. Every coal plant is a potential Superfund site. Every ash pond is a lawsuit waiting to happen. Every emission is measured, monitored, and potentially litigated. Ameren still operates massive coal plants that won't close for years. In a world where climate litigation is exploding, owning coal plants is like walking through a minefield—you might make it through, but the risk is enormous and growing.

Bull Case: The Tailwinds Are Stronger

But here's why the bulls might be right: Ameren is riding three massive secular trends that dwarf the regulatory constraints. First, weather-normalized retail sales grew approximately 2% at Ameren Missouri, breaking decades of stagnant demand. This isn't a blip—it's the beginning of an electrification supercycle. Every electric vehicle sold, every heat pump installed, every data center built increases electricity demand. We're moving from a world where electricity was one energy source among many to a world where electricity IS energy.

The data center opportunity alone could transform Ameren's growth profile. A single large data center can consume as much electricity as a small city. AI training clusters require staggering amounts of power—we're talking hundreds of megawatts for a single facility. Missouri and Illinois have the land, the transmission infrastructure, and the relatively cool climate that data centers need. Ameren is perfectly positioned to capture this demand, and unlike competitive markets, they don't need to bid for the business—if you build in their territory, you buy from them.

The transmission investment opportunity through MISO is a money machine hiding in plain sight. MISO's long-range transmission planning process has identified tens of billions in needed transmission investments. These projects earn FERC-approved returns typically 150-200 basis points higher than state-regulated distribution assets. Better yet, the costs are spread across the entire MISO footprint, so Ameren's customers only pay a fraction while Ameren earns returns on the full investment. It's like owning toll roads where someone else pays for construction.

Ameren's regulatory relationships are actually strong where it matters. Yes, there are caps and constraints, but Ameren has operated in Missouri and Illinois for over a century. They know every regulator, every intervener, every political player. This isn't adversarial—it's a dance where everyone knows their steps. Missouri just approved an 800-megawatt gas plant and massive solar investments. Illinois's climate laws actually guarantee cost recovery for clean energy investments. The regulatory compact isn't breaking; it's evolving to support exactly the investments Ameren wants to make.

The clean energy transition creates a massive investment opportunity that utilities are uniquely positioned to capture. Ameren isn't competing with NextEra or Brookfield for renewable projects—they're using regulated utility status to earn guaranteed returns on renewable investments. Every coal plant retired creates room for renewable investment. Every renewable project qualifies for federal tax credits that improve returns. Every grid upgrade to accommodate renewables goes into rate base. The energy transition isn't a disruption; it's a rate base growth accelerator.

The balance sheet and financial flexibility remain strong despite the massive capital program. Ameren's regulated utility model means cash flows are predictable, capital markets remain accessible, and the dividend aristocrat status (paid continuously since 1907 if you trace back to predecessor companies) provides credibility with investors. The planned $600 million annual equity issuances are manageable given the earnings growth trajectory. This isn't a leveraged bet on commodity prices; it's a steady infrastructure buildout funded by predictable cash flows.

The ultimate bull case is simple: society cannot function without electricity, demand is growing, the infrastructure needs massive investment, and Ameren has a legal monopoly on providing it. Everything else is just details. The regulatory constraints that bears fear are actually the moat that protects the business model. The execution risks are real but manageable with proper planning. The interest rate sensitivity is offset by regulatory true-ups over time. The distributed generation threat is overblown—industrial customers and reliability needs ensure grid dependence for decades. When you strip away the noise, Ameren is a toll collector on critical infrastructure facing unprecedented demand growth. That's not a bear case; it's an investment dream.

X. Lessons & Reflections

The paradox of innovation in regulated industries reveals a profound truth about business: sometimes the most innovative thing you can do is execute the basics flawlessly for decades. Ameren isn't trying to disrupt anything—it's trying to deliver electrons reliably while earning a fair return. Yet within those constraints, it's orchestrating one of the most complex transformations in industrial history. The company is simultaneously retiring coal plants, building renewable generation, upgrading transmission infrastructure, modernizing the grid, and maintaining reliability for millions of customers. That's not innovation in the Silicon Valley sense, but it's innovation where failure means hospitals lose power and people freeze in winter.

The lesson here is that innovation doesn't always mean disruption. Sometimes it means taking a 140-year-old business model and adapting it to new realities without breaking it. Ameren's innovation is in financial engineering, regulatory strategy, and operational excellence—boring competencies that compound over decades. While tech companies chase moonshots, utilities quietly rebuild the entire energy infrastructure of modern civilization. Both types of innovation matter, but only one keeps the lights on.

Why boring businesses can be great investments is perhaps the most important lesson for fundamental investors. Ameren will never have a viral moment, never ship a breakthrough product, never have a charismatic founder on magazine covers. What it will do is generate predictable cash flows, grow earnings at mid-single digits, pay rising dividends, and compound wealth slowly but surely. In a world obsessed with disruption, there's alpha in stability. The very characteristics that make utilities boring—regulation, capital intensity, slow change—also make them predictable, and predictability is valuable in an uncertain world.

The importance of political capital and regulatory relationships cannot be overstated in this business. Ameren's most valuable asset isn't its power plants or transmission lines—it's the trust built over decades with regulators, politicians, and communities. This political capital is what allows the company to get rate increases approved, build controversial infrastructure, and navigate the energy transition without facing revolt from stakeholders. Tech companies can afford to "move fast and break things." Utilities must move deliberately and break nothing. The relationship capital required for the latter is far harder to build and easier to destroy.

Climate change is both risk and opportunity, and Ameren exemplifies how companies can prosper by embracing rather than resisting this reality. Every climate regulation becomes a justification for infrastructure investment. Every renewable mandate becomes a rate base growth opportunity. Every extreme weather event demonstrates the need for grid hardening. The companies that fought climate science are writing down stranded assets; the companies that embraced the transition are earning regulated returns on massive capital programs. Ameren chose wisely, and its shareholders are benefiting from that choice.

What tech companies can learn from 140-year-old utilities is humility about time horizons and the value of infrastructure. Silicon Valley measures success in quarters; utilities measure it in decades. Tech companies obsess over user engagement; utilities obsess over reliability. Tech platforms can be built in years and disrupted in months; utility infrastructure takes decades to build and centuries to fully depreciate. Both models can create enormous value, but the utility model has proven remarkably resilient across world wars, depressions, technological revolutions, and regulatory upheavals. There's wisdom in that resilience.

The ultimate infrastructure play in an electrifying world is what Ameren represents. We're entering an era where electricity isn't just one form of energy among many—it's becoming THE form of energy that powers everything else. Transportation is electrifying. Heating is electrifying. Industrial processes are electrifying. Even the production of alternative fuels like hydrogen requires massive amounts of electricity. In this world, companies that own the infrastructure to generate, transmit, and distribute electricity aren't just utilities—they're the platforms on which the entire economy runs.

The meta-lesson is about the nature of essential services and the businesses that provide them. Ameren doesn't need to be loved, doesn't need to be exciting, doesn't need to be innovative in any conventional sense. It just needs to be utterly reliable at providing something society cannot function without. That's a powerful position, perhaps the most powerful position in business. While everyone else fights for customer attention and market share, utilities enjoy guaranteed demand and regulated monopolies. It's boring, it's stable, and it's brilliant.

Looking forward, Ameren's story suggests that the most interesting investments might be hiding in the most boring places. The energy transition isn't happening in Silicon Valley boardrooms or Wall Street trading floors—it's happening in regulatory proceedings in Jefferson City and Springfield, in engineering departments designing transmission lines, in construction sites where solar panels replace coal plants. The companies managing this transition might not make headlines, but they're rebuilding the foundation of modern civilization. For long-term investors seeking compound returns rather than lottery tickets, utilities like Ameren offer something increasingly rare: predictability in an unpredictable world, growth in a mature industry, and essential services that society cannot do without. Sometimes the best investment is the one that keeps the lights on—literally.

XI. Recent News

Ameren Corporation announced second quarter 2025 net income attributable to common shareholders of $275 million, or $1.01 per diluted share, compared to second quarter 2024 net income of $258 million, or $0.97 per diluted share. Second quarter 2025 earnings reflected increased infrastructure investments, new Ameren Missouri electric service rates that became effective June 1, 2025, and continued disciplined cost management. The earnings beat expectations, demonstrating the company's consistent ability to execute its infrastructure investment strategy while managing costs effectively. Ameren Missouri announced a significant change to its generation strategy in February 2025, aiming to accelerate generation investments to support robust economic expansion. The revision to Ameren Missouri's Preferred Resource Plan in its Integrated Resource Plan (IRP) is designed to provide for 1.5 gigawatts (GW) of expected new energy demand by 2032, with a balanced mix of generation resources. This represents a major shift in the company's growth expectations, driven by data center demand and industrial expansion in the region.

The renewable energy buildout continues to accelerate. Ameren Missouri received approval to build or acquire approximately 400 megawatts (MW) of solar energy. The first of the three solar projects is scheduled to go into service in 2025, with two more set to begin serving customers in 2026. The updated generation strategy includes building 1,600 megawatts (MW) of natural gas generation resources by 2030, with a total planned addition of 6,100 MW by 2045. Continuing investments in renewable generation resources across the region includes another 2,700 MW of wind and solar energy by 2030, with a total planned addition of 4,200 MW by 2045.

Grid modernization progress has delivered tangible benefits. Smart Energy Plan investments in a stronger grid saved customers 8 million minutes in outages in 2024, demonstrating the value of infrastructure investment in reliability improvements. Smart technology prevented more than 150,000 customer outages during major severe weather outbreaks in 2025, validating the company's grid hardening strategy.

Regulatory developments continue to shape the investment landscape. Beginning in 2025, changes took effect for new interconnections in the Net Metering Program in Illinois, creating new opportunities and challenges for distributed generation integration. Meanwhile, the company's constructive relationships with Missouri regulators enabled approval of both renewable and gas generation projects, maintaining the balanced approach that ensures reliability while advancing clean energy goals.

XII. Links & Resources

Annual Reports and Investor Presentations: - Ameren Investor Relations: AmerenInvestors.com - 2024 Annual Report and 10-K Filing - Quarterly Earnings Presentations - Capital Allocation Framework Updates

Regulatory Filings: - Missouri Public Service Commission Dockets - Illinois Commerce Commission Proceedings - FERC Transmission Rate Cases - Integrated Resource Plans

Industry Research and Analysis: - EEI (Edison Electric Institute) Industry Reports - MISO Transmission Planning Documents - S&P Global Market Intelligence Utility Reports - Moody's and Fitch Credit Ratings Analysis

Historical Documents and Archives: - Union Electric Company Historical Archives - Central Illinois Public Service Company Records - Lake of the Ozarks Dam Construction Documentation - Midwest Power Pool Formation Papers

Clean Energy Transition Resources: - Ameren's Path to Net-Zero Report - Climate and Equitable Jobs Act (CEJA) Implementation - Federal Infrastructure Investment and Jobs Act Opportunities - IRA Tax Credit Guidance for Utilities

The story of Ameren is ultimately the story of American infrastructure—built by previous generations, maintained by the current one, and transformed for the next. It's a company that proves boring can be beautiful, that regulated can mean reliable, and that the transition to clean energy isn't just an environmental imperative but potentially one of the greatest investment opportunities of our time. For those willing to think in decades rather than quarters, utilities like Ameren offer something increasingly rare in modern markets: predictability, sustainability, and the quiet satisfaction of owning the infrastructure that keeps civilization running.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube