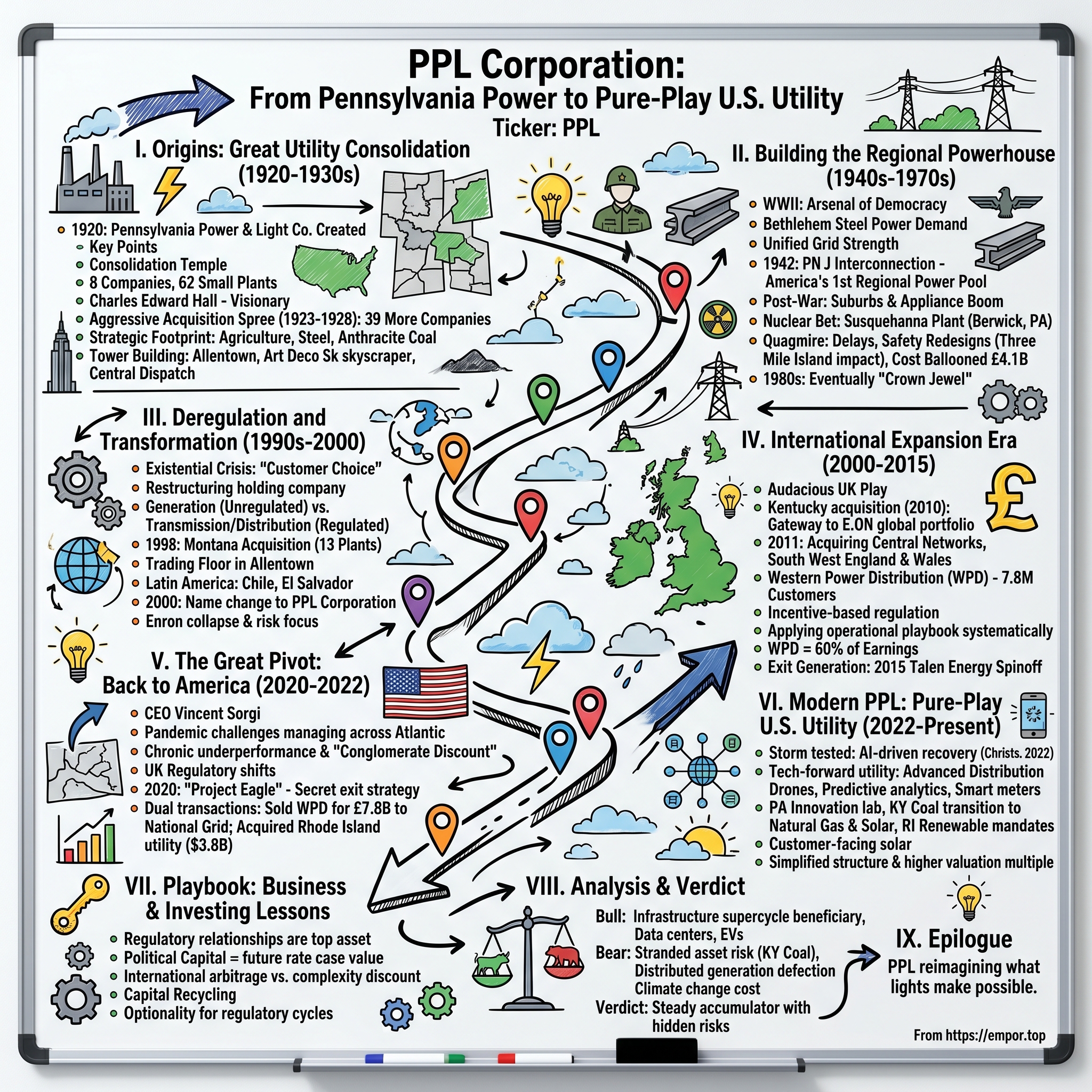

PPL Corporation: From Pennsylvania Power to Pure-Play U.S. Utility

I. Introduction & Episode Roadmap

Picture this: It's June 2021, and Vincent Sorgi, CEO of PPL Corporation, is about to execute one of the largest international utility divestitures in history. With a stroke of a pen, he's selling the company's crown jewel—the UK's largest electricity distribution network—for £7.8 billion to National Grid. In the same breath, he's acquiring Rhode Island's utility operations for $3.8 billion. This wasn't just a transaction; it was a complete strategic reversal of two decades of international expansion. The company that once operated power networks from Wales to Chile was returning home to its Pennsylvania roots. Today, PPL Corporation stands as a streamlined American utility powerhouse: $7.9 billion in revenue, 6,500 employees, over $37 billion in assets, and serves 3.6 million customers. But those numbers tell only part of the story. This is a century-old company that's reinvented itself more times than a Silicon Valley startup—from a Depression-era consolidator to a nuclear power pioneer, from a deregulation warrior to an international conglomerate, and now back to its roots as a pure-play U.S. regulated utility.

The real story here isn't just about poles and wires. It's about how a utility company navigates the fundamental tension between being a regulated monopoly and a growth-oriented public company. How does a business whose core product—electricity—hasn't fundamentally changed in a century create value for shareholders? How does management allocate capital when your returns are literally set by government officials? And perhaps most intriguingly, why would a company spend two decades building an international empire only to dismantle it in a single transaction?

These are the questions that make PPL fascinating. It's a masterclass in regulatory relationships, capital recycling, and strategic pivots. It's also a story about Pennsylvania itself—from the coal mines of Scranton to the steel mills of Bethlehem, from industrial titan to rust belt survivor to the modern energy transition. The company's footprint traces the economic history of the Keystone State like a seismograph.

What we're going to explore today is how PPL became the utility equivalent of a boomerang—traveling far from home only to return stronger. We'll dive into the consolidation playbook that created modern utilities, the nuclear bet that nearly broke the company, the international expansion that made it a global player, and the dramatic reversal that brings us to today. Along the way, we'll extract the lessons that matter for investors: how to evaluate regulated utilities, why geography matters more than you think in this business, and what the energy transition really means for traditional power companies.

II. Origins: The Great Utility Consolidation (1920-1930s)

The lights flickered on in a boardroom in Allentown, Pennsylvania, on June 4, 1920. Eight utility executives sat around a mahogany table, their companies' service territories spread across a map like pieces of a jigsaw puzzle. By the end of that day, they would sign papers creating Pennsylvania Power & Light Company—not the first utility consolidation, but one that would become the template for an entire industry transformation.

The pre-1920 electricity business in Pennsylvania looked nothing like today's grid. Imagine hundreds of tiny fiefdoms, each with its own power plant, its own standards, its own pricing. The Allentown Electric Company served downtown Allentown. The Harwood Electric Company powered a few coal mining towns. The Edison Electric Illuminating Company of Sunbury lit up a single county. These weren't interconnected systems—they were islands of electricity in a sea of darkness. Some ran on direct current, others alternating current. Voltages varied wildly. A factory might need its own generator because the local utility couldn't provide enough power.

Enter the consolidators, and chief among them was Charles Edward Hall. Hall wasn't your typical utility executive—he was a visionary who saw electricity not as a luxury but as a fundamental right. A Penn State engineering graduate, Hall had literally helped invent modern college football in his spare time (he's credited with introducing the forward pass to the game). But his real passion was power—specifically, the idea that economies of scale could make electricity affordable for everyone.

Hall's genius wasn't technological; it was organizational. He recognized that the fragmented utility landscape was economically insane. Each tiny company maintained its own power plant, its own maintenance crews, its own billing department. The redundancy was staggering. Worse, the lack of interconnection meant that when one plant failed, entire towns went dark. There was no way to share load, no backup power, no efficiency of scale.

The initial consolidation that formed PP&L brought together eight companies with a combined 62 power plants. Think about that number—62 plants to serve what today would be considered a modest service territory. Most were tiny coal-fired generators, barely more sophisticated than industrial boilers with turbines attached. The largest produced maybe 5 megawatts; many generated less than one. Together, they served about 370,000 customers across 12,000 square miles of central and eastern Pennsylvania.

But Hall was just getting started. Between 1923 and 1928, PP&L went on an acquisition spree that would make modern private equity firms blush. The company absorbed 39 additional electric companies, methodically filling in the gaps in its service territory. Each acquisition followed the same playbook: identify a struggling local utility, offer a premium to shareholders desperate for liquidity, integrate the operations, standardize the equipment, and connect it to the growing grid.

The financing of these acquisitions was creative for its time. PP&L pioneered the use of preferred stock and mortgage bonds specifically designed for utility consolidation. They would issue securities backed by the combined assets of the merged companies, essentially using the stability of regulated returns to access cheap capital. The financial engineering was sophisticated—different classes of securities for different risk appetites, all structured to maintain control while raising maximum capital.

By 1928, PP&L had assembled something remarkable: a crescent-shaped service territory stretching from Lancaster County in the south, through the Lehigh Valley, up to the anthracite coal regions of Scranton and Wilkes-Barre. This wasn't random geography—it was strategic. The southern portion included rich agricultural areas and growing manufacturing centers. The Lehigh Valley was becoming the center of American steel production. The northern territories sat atop the world's largest deposits of anthracite coal. PP&L had positioned itself at the heart of American industrial might.

The company needed a headquarters that matched its ambitions. In 1928, PP&L began construction of the Tower Building in downtown Allentown—a 23-story Art Deco masterpiece that would become the Lehigh Valley's first skyscraper. The building was more than offices; it was a statement. The lobby featured murals depicting the march of electrical progress. The executive floors had wood paneling from around the world. The building's illumination at night—visible for miles—served as a constant reminder of PP&L's product.

The Tower Building also housed something revolutionary: a central dispatch center where operators could monitor and control the entire PP&L system. Using analog computers (essentially sophisticated electrical circuits), they could route power from any plant to any customer, balance loads across the network, and respond to outages in real-time. This was the birth of the modern electrical grid—not just wires and transformers, but an intelligent network.

Then came October 29, 1929. The stock market crash hit utilities particularly hard because they had borrowed heavily to fund expansion. PP&L stock, which had traded as high as $100 per share in September 1929, fell to $15 by 1932. The company's aggressive acquisition strategy suddenly looked reckless. Customers who had been adding electrical appliances stopped paying bills. Industrial demand collapsed as factories closed.

But PP&L had an advantage that pure financial companies lacked: it provided an essential service. People might stop buying cars or clothes, but they still needed light and power. The company's regulated rate structure provided some protection—though regulators did force rate reductions, they couldn't allow the utility to fail without plunging entire regions into darkness.

Hall and his team made crucial decisions during the Depression that would define PP&L for decades. First, they maintained employment, becoming one of the region's most stable employers when unemployment hit 25%. Second, they continued investing in infrastructure, taking advantage of cheap labor and materials to upgrade transmission lines and build new substations. Third, and most importantly, they pioneered the "grow the load" strategy—actively working to increase electricity consumption by promoting electrical appliances, offering financing for home wiring, and partnering with manufacturers to build factories in PP&L territory.

The company even created "Electric Home" showrooms in major cities where families could see the latest electrical appliances in action. They offered free home economics classes teaching women how to use electric stoves and refrigerators. They worked with farmers to electrify dairy operations and chicken coops. This wasn't charity—it was a long-term growth strategy. Every new appliance, every electrified barn, every neon sign meant more kilowatt-hours sold.

By the late 1930s, PP&L had emerged from the Depression stronger than it entered. The consolidation was complete—the company now operated as a single, integrated utility serving nearly 500,000 customers. The patchwork of incompatible systems had been unified into a robust grid. Most remarkably, electricity rates had fallen by more than 40% since 1920, even as service reliability improved dramatically. The average customer experienced less than two hours of outages per year, down from dozens.

The foundation was set. PP&L had proven that utility consolidation worked—that bigger really was better in the electricity business. The company had survived economic catastrophe, built lasting infrastructure, and created a template that utilities across America would follow. As the 1930s ended and war clouds gathered in Europe, PP&L was perfectly positioned for what would come next: the industrial mobilization that would transform American manufacturing and, with it, the demand for electric power.

III. Building the Regional Powerhouse (1940s-1970s)

The telegram arrived at PP&L headquarters on December 8, 1941, the day after Pearl Harbor: "Essential war production requires immediate expansion of electrical capacity. Report maximum possible output within 30 days." Signed by the War Production Board, it transformed PP&L overnight from a regional utility into a critical component of the Arsenal of Democracy.

The Lehigh Valley in 1941 was about to become the steel capital of America. Bethlehem Steel, located squarely in PP&L territory, would produce more naval armor plate than any other facility in the country. The company's massive furnaces, rolling mills, and fabrication plants ran 24 hours a day, seven days a week. Each Liberty Ship required 7,000 tons of steel. Each ton of steel required 700 kilowatt-hours of electricity. The math was staggering—PP&L needed to double its generation capacity, and it needed to do it yesterday.

The company's response revealed the hidden strength of the utility consolidation model. Because PP&L had unified the regional grid, it could shift power instantly to where it was needed most. When Bethlehem Steel's blast furnaces fired up, drawing massive loads, the company could pull electricity from every corner of its system. Rural substations that served farms during the day could redirect power to factories at night. The integrated network Hall had envisioned twenty years earlier now proved its worth in national survival.

But redistribution wasn't enough. PP&L embarked on the largest construction program in its history. The Sunbury coal plant expanded from 100 megawatts to 400. New transmission lines—138,000 volts, then the highest voltage in commercial use—connected generation to load centers. The company pioneered the use of aluminum conductors instead of copper (which was needed for military purposes), fundamentally changing transmission line economics.

The real innovation came in 1942 with the creation of the Pennsylvania-New Jersey Interconnection (PNJ). PP&L joined with Philadelphia Electric and Public Service Electric & Gas of New Jersey to create America's first regional power pool. The three utilities connected their systems with a 220,000-volt transmission ring—a giant loop of high-voltage lines that allowed them to share generation capacity seamlessly. If one company's plants failed, the others could instantly provide backup power. It was mutual aid through engineering, and it would become the template for regional transmission organizations nationwide.

The PNJ represented something profound: utilities competing in their own territories but cooperating across boundaries. They shared reserves, coordinated maintenance schedules, and jointly planned new generation. The control center, built in a former department store in Allentown, looked like something from a science fiction movie—walls of analog meters, massive control panels, operators communicating via dedicated phone lines with every major plant and substation across three states.

When the war ended in 1945, everyone expected electricity demand to collapse as military production ceased. Instead, the opposite happened. Returning veterans started families, bought homes, and filled those homes with electrical appliances. The suburbs exploded across PP&L territory—Levittown-style developments in the Lehigh Valley, new communities spreading from Lancaster to Scranton. Each new home meant new load: electric ranges, water heaters, television sets, air conditioners.

PP&L's strategy during this period was brilliantly simple: build ahead of demand. The company operated on the assumption that if reliable, affordable electricity was available, growth would follow. They would extend transmission lines to empty fields, knowing that factories would come. They would upgrade distribution in rural areas, betting that farms would mechanize. They were usually right.

The 1950s acquisitions extended this strategy. When PP&L bought Scranton Electric Company in 1953, it wasn't just acquiring customers—it was consolidating the northern anchor of its territory. The Pennsylvania Water & Power Company acquisition in 1955 brought valuable hydroelectric resources along the Susquehanna River. Each deal followed the proven playbook: integrate operations, standardize equipment, reduce redundancy, lower costs.

But the real game-changer was nuclear power. In 1962, PP&L announced it would build a nuclear plant along the Susquehanna River near Berwick, Pennsylvania. The initial projections were intoxicating: a two-unit plant producing 2,000 megawatts of carbon-free electricity at a cost "too cheap to meter." The plant would cost $400 million and come online by 1972. Neither prediction would prove accurate.

The Susquehanna nuclear project became PP&L's Vietnam—a quagmire that consumed ever more resources while receding into the future. Initial site work began in 1970, but construction didn't seriously start until 1973. Then came Three Mile Island in 1979, just 80 miles south of Susquehanna. The partial meltdown at the Met-Ed plant didn't release significant radiation, but it fundamentally changed nuclear regulation. Every safety system had to be redesigned. Every procedure had to be rewritten. Every operator had to be retrained.

The numbers tell the story: The $400 million project ballooned to $4.1 billion. The 1972 completion date slipped to 1982 for Unit 1 and 1984 for Unit 2. At one point, 5,000 construction workers swarmed the site, making it Pennsylvania's largest construction project. PP&L had to issue billions in bonds, sending its debt-to-equity ratio soaring. Wall Street analysts questioned whether the company could survive if regulators didn't allow full cost recovery.

The regulatory battles were epic. Pennsylvania's Public Utility Commission had to decide how much of the nuclear cost overruns ratepayers should bear versus shareholders. Consumer advocates argued that PP&L's mismanagement shouldn't be rewarded with higher rates. PP&L countered that the delays were due to changing federal regulations beyond their control. The hearings went on for months, filling thousands of pages of testimony.

The resolution came in what industry insiders called "the Grand Bargain." Regulators allowed PP&L to recover most of the Susquehanna costs through rates, but stretched the recovery over 20 years to minimize immediate impact. In exchange, PP&L agreed to efficiency improvements and rate stability commitments. It was regulatory realpolitik—nobody was happy, but everyone could live with it.

Despite the trauma, Susquehanna eventually became one of PP&L's crown jewels. Once operational, the plant ran at capacity factors above 90%, generating enormous amounts of carbon-free electricity at very low marginal cost. The same nuclear plant that nearly bankrupted PP&L in the 1980s would generate billions in profits over its operating life. It was a lesson in utility economics: the capital costs are front-loaded and painful, but the operating benefits last for decades.

The 1970s also brought the energy crisis, with oil prices quadrupling overnight. PP&L's coal-heavy generation fleet suddenly looked prescient. While utilities dependent on oil-fired generation saw costs skyrocket, PP&L had access to cheap Pennsylvania coal. The company's financial performance diverged sharply from coastal utilities, attracting attention from investors looking for energy crisis winners.

This period also saw the emergence of environmental regulation. The Clean Air Act of 1970 required massive investments in pollution control equipment. PP&L spent hundreds of millions installing scrubbers, electrostatic precipitators, and other devices to reduce emissions. The company pioneered the use of low-sulfur coal from western mines, building unit trains that could transport entire trainloads of coal from Wyoming to Pennsylvania.

By 1980, PP&L had transformed from a regional utility into a major force in American electricity. The company operated 8,000 megawatts of generation capacity, up from 1,000 megawatts in 1945. Its transmission system had grown from 2,000 miles to 8,000 miles of high-voltage lines. It served 1.2 million customers across 10,000 square miles of Pennsylvania. The rural cooperative that had strung wires to farms now powered everything from steel mills to shopping malls.

But the biggest transformation was about to come. The comfortable world of regulated monopolies, guaranteed returns, and captive customers was ending. Deregulation was coming to the electricity industry, and PP&L would need to evolve from a utility into an energy company. The skills that had built a regional powerhouse—engineering excellence, regulatory relationships, operational efficiency—would no longer be enough. The company would need to learn to compete.

IV. Deregulation and Transformation (1990s-2000)

The October 1995 board meeting at PP&L headquarters was unlike any in the company's 75-year history. CEO William Hecht stood before a whiteboard covered with corporate structure diagrams that looked more like a technology company's org chart than a utility's. "Gentlemen," he said, "we're not just changing our strategy. We're changing our DNA." Within hours, the board would approve the most radical restructuring in PP&L's history: transforming from an integrated utility into a holding company with separate competitive and regulated businesses.

The forces driving this transformation had been building for years. The Public Utility Regulatory Policies Act of 1978 (PURPA) had cracked open the generation monopoly by requiring utilities to buy power from independent producers. The Energy Policy Act of 1992 went further, creating wholesale electricity markets where power could be traded like any commodity. But the real earthquake came from Pennsylvania itself. Governor Tom Ridge, elected in 1994, made electricity deregulation his signature initiative. Pennsylvania would have "customer choice"—consumers could buy electricity from any supplier, not just their local utility.

For PP&L, this wasn't just a regulatory change; it was an existential crisis. The company's entire business model—building power plants, recovering costs through regulated rates, earning a guaranteed return—was about to be blown up. Generation would become competitive. Transmission and distribution would remain regulated. Customers could leave for other suppliers. The comfortable monopoly was ending.

Hecht and his team didn't wait for deregulation to be imposed on them. Instead, they decided to get ahead of it, restructuring PP&L before the law required it. The strategy was bold: create a holding company (PP&L Resources, later renamed PPL Corporation) with separate subsidiaries for different businesses. Put generation assets into an unregulated subsidiary that would compete in wholesale markets. Keep transmission and distribution in a regulated utility. Create an energy marketing and trading operation. Build or buy generation assets in other states.

The financial engineering required was staggering. PP&L had to value and transfer billions in assets between regulated and unregulated entities. Debt had to be allocated. Tax structures had to be optimized. Accounting systems had to be completely rebuilt. The company hired investment bankers, consultants, and lawyers by the dozen. The restructuring costs alone exceeded $100 million.

But the real challenge was cultural. PP&L employees had spent their entire careers in a regulated monopoly where success meant operational excellence and regulatory compliance. Now, part of the company needed to think like traders, taking positions in volatile commodity markets. The generation business needed to maximize profits, not just keep the lights on. The retail business needed to actually market and sell, concepts foreign to a monopoly utility.

The company created "PPL University," an internal training program to teach employees about competitive markets. Engineers learned about futures and options. Plant operators studied supply and demand curves. Customer service representatives practiced sales techniques. It was a massive re-education program, transforming utility workers into energy entrepreneurs.

The 1998 Montana acquisition marked PP&L's coming-out party as a competitive generator. The company paid $1.6 billion for 13 power plants from Montana Power Company, adding 2,500 megawatts of generation in a single transaction. This wasn't adjacent Pennsylvania—this was 2,000 miles away, in a completely different electricity market. The plants included everything from hydroelectric dams on the Missouri River to coal plants serving copper mines.

Wall Street was skeptical. Why would a Pennsylvania utility buy Montana power plants? The answer revealed PP&L's new strategy: electricity was becoming a national commodity. With deregulation, power could be sold anywhere there was transmission capacity. Geographic diversification reduced risk. Different regions had different supply-demand dynamics. When prices were low in Pennsylvania, they might be high in Montana.

The Montana plants also came with something invaluable: trading rights and transmission access across the Western grid. PP&L suddenly had the ability to buy and sell power from Canada to Mexico, from the Pacific Coast to the Great Plains. The company built a trading floor in Allentown that looked like a Wall Street investment bank—dozens of traders watching multiple screens, buying and selling megawatts like shares of stock.

PP&L's early international ventures started modestly. In 1999, the company acquired distribution companies in Chile and El Salvador. These weren't huge investments—a few hundred million dollars total—but they were learning experiences. How do you operate a utility in a country where you don't speak the language? How do you manage currency risk? How do you navigate completely different regulatory regimes?

The Latin American investments taught PP&L valuable lessons, not all of them pleasant. In El Salvador, the company faced guerrilla attacks on transmission lines. In Chile, it discovered that "regulated returns" meant something very different when the regulator could change the rules retroactively. But the companies were profitable, and PP&L was learning how to be a multinational corporation.

Back in Pennsylvania, deregulation officially began on January 1, 2000. The date was carefully chosen—Y2K concerns meant everyone was focused on keeping systems running, not switching electricity suppliers. But PP&L was ready. The company had spent three years preparing, splitting its operations, training its people, and building new systems.

The immediate impact was chaotic. Electricity prices, which had been stable for decades, started fluctuating daily. Industrial customers quickly switched to alternative suppliers offering lower rates. Residential customers mostly stayed put, confused by the choices and skeptical of savings. PP&L's generation business saw profits soar as wholesale prices spiked during hot summers and cold winters. The regulated utility saw revenues decline as customers left.

The company name change in 2000—from PP&L Resources to PPL Corporation—was more than cosmetic. The ampersand and apostrophe were deliberate casualties, streamlining the brand for national and international expansion. PPL wasn't just Pennsylvania Power & Light anymore; it was an energy company that happened to be headquartered in Pennsylvania.

The creation of PPL EnergyPlus marked another evolution. This retail energy subsidiary sold electricity and natural gas to customers in deregulated markets across the country. PPL was now competing to win back its own former monopoly customers in Pennsylvania while simultaneously trying to poach customers from other utilities in Texas, Illinois, and other deregulated states.

The trading and marketing operation grew exponentially. PPL became one of the largest power marketers in America, trading billions of dollars in electricity and natural gas annually. The company pioneered structured products—long-term contracts with embedded options, weather derivatives, spark spread trades. The Allentown trading floor operated 24/7, with night shifts monitoring California markets and early morning crews tracking European prices.

But PPL learned that trading carried risks. The California electricity crisis of 2000-2001 saw wholesale prices spike to $1,000 per megawatt-hour, up from normal levels of $30-50. Some traders made fortunes; others went bankrupt. Enron's collapse in late 2001 sent shockwaves through energy markets. PPL had significant trading exposure to Enron and took nine-figure writedowns when the energy giant failed.

The Enron collapse changed everything. Suddenly, credit risk management became as important as market risk. PPL built sophisticated systems to monitor counterparty exposure. The company pulled back from speculative trading, focusing on hedging and optimization around its physical assets. The cowboys were reined in; risk management became paramount.

By 2000, PPL had successfully transformed from a traditional utility into a modern energy company. It operated unregulated generation in multiple states. It traded power across North America. It sold electricity at retail in competitive markets. It had international operations on three continents. The company that had started the decade as a Pennsylvania utility ended it as something entirely different—a prototype for the 21st-century energy company.

The transformation had been expensive and sometimes painful. Hundreds of millions had been spent on restructuring, systems, and training. Traditional utility employees had been forced to adapt or leave. The company had taken significant trading losses and learned hard lessons about risk. But PPL had successfully navigated the transition from monopoly to competition, positioning itself for the next phase of growth. The foundation was set for what would become the company's most ambitious expansion yet: the conquest of the British electricity market.

V. The International Expansion Era (2000-2015)

The PowerPoint slide that changed PPL's destiny appeared on the boardroom screen in March 2010. It showed a map of the United Kingdom overlaid with electricity distribution territories. "Ladies and gentlemen," CEO Jim Miller announced, "we have the opportunity to acquire E.ON's UK distribution business—2.5 million customers, the Midlands territory, for £3.5 billion." Within eighteen months, PPL would own not just that network but the entire Western Power Distribution portfolio, making it the largest electricity distributor in Britain. It was an acquisition so audacious that British newspapers ran headlines asking, "Who are these Americans buying our grid?"

The path to becoming a transatlantic utility had begun a decade earlier with those modest Latin American investments. But the UK represented something entirely different—a sophisticated, stable, first-world electricity market with predictable regulation and sterling-denominated returns. The British had invented the modern regulatory model that American states copied. Now an American utility was coming full circle, buying British networks using financial engineering that would have impressed the Empire's merchant bankers.

The Kentucky acquisition in 2010 was supposed to be PPL's big domestic play. For $7.6 billion, the company acquired Louisville Gas & Electric and Kentucky Utilities from E.ON, adding 1.2 million customers in Kentucky and Virginia. It was PPL's first major expansion outside Pennsylvania, doubling the company's regulated rate base. The utilities came with 8,000 megawatts of generation, mostly coal-fired plants sitting atop some of America's cheapest coal reserves.

But Miller and his team saw the Kentucky deal as more than just buying utilities—it was a gateway to E.ON's global portfolio. The German energy giant was retrenching, selling international assets to focus on Europe. During negotiations for Kentucky, PPL executives built relationships with E.ON's management. They learned about E.ON's UK operations. They studied the British regulatory model. They positioned themselves for what came next.

The UK electricity distribution business operated under a completely different model than American utilities. Instead of rate cases and cost-of-service regulation, the British used incentive-based regulation with eight-year price control periods. The regulator (Ofgem) set revenue allowances based on efficiency benchmarks. If you could operate below the benchmark costs, you kept the savings. If you exceeded them, shareholders absorbed the losses. It was regulation designed to mimic competitive markets.

For PPL, this was intoxicating. The company had spent a decade learning to optimize operations in competitive generation markets. Now they could apply those skills to regulated distribution, earning higher returns through superior efficiency. The UK assets were already well-run, but PPL believed American operational techniques—predictive maintenance, automated switching, mobile workforce management—could squeeze out additional savings.

The first UK acquisition closed in April 2011: Central Networks, serving 2.5 million customers across the Midlands, for £3.5 billion. But PPL wasn't done. Six months later, the company announced it would buy E.ON's remaining UK distribution business—South West England and Wales—for another £4.3 billion. Combined, PPL would own Western Power Distribution (WPD), serving 7.8 million customers across a territory stretching from the Welsh valleys to the Cornish coast to the suburbs of Birmingham.

The financing structure was a masterpiece of financial engineering. PPL issued $3 billion in equity, including common stock and equity units with forward contracts. It raised £2.5 billion in sterling-denominated debt at WPD, taking advantage of UK interest rates near historic lows. The company implemented complex hedging strategies to manage currency risk, using cross-currency swaps and forward contracts to lock in exchange rates.

The cultural integration challenge was immense. PPL sent American managers to run WPD but kept most British employees. The Americans had to learn that "redundancy" meant layoffs, "schemes" were plans, and tea breaks were sacred. The Brits had to adapt to American performance metrics, quarterly earnings calls, and a more aggressive approach to regulatory negotiations.

PPL applied its operational playbook systematically. The company invested £500 million annually in network upgrades, far exceeding regulatory requirements. Smart meters were deployed across the territory. Distribution automation allowed remote switching and fault isolation. The control room in Birmingham could monitor every substation, every major circuit, from a wall of screens that looked like mission control.

The regulatory strategy was equally sophisticated. PPL hired former Ofgem officials as consultants, built economic models to optimize regulatory submissions, and cultivated relationships with stakeholder groups. When the next price control period (RIIO-ED1) was set in 2014, WPD received one of the highest allowed returns among UK distributors. The company had learned to play the British regulatory game better than many British utilities.

Meanwhile, the Latin American ventures were quietly expanding. In Chile, PPL acquired additional distribution companies, growing to 650,000 customers. The company built small power plants in El Salvador, taking advantage of tax incentives for renewable energy. A team in Allentown managed these far-flung operations, conducting business in Spanish and Portuguese, navigating everything from volcanic eruptions to currency crises.

The international expansion transformed PPL's financial profile. By 2014, nearly 60% of the company's earnings came from outside Pennsylvania. Currency translation added a new line to quarterly reports. The company's investor presentations included primers on UK regulation and Latin American politics. Analysts had to model sterling-pound exchange rates and Chilean inflation.

But the international strategy was about to collide with dramatic changes in American energy markets. The shale gas revolution had crushed electricity prices, making PPL's merchant generation fleet—particularly the coal plants acquired in Montana and Pennsylvania—increasingly uneconomic. Environmental regulations were tightening, requiring billions in pollution control investments. Renewable energy was becoming competitive without subsidies. The merchant generation business that had driven PPL's deregulation strategy was becoming a millstone.

The solution was radical: exit generation entirely. On June 6, 2014, PPL announced it would spin off its competitive generation business into a new company called Talen Energy. The spinoff would include 15,000 megawatts of generation, the marketing and trading operations, and ironically, the very assets that had launched PPL's deregulation journey fifteen years earlier.

The Talen spinoff was complex. PPL shareholders received one share of Talen for every two shares of PPL. The companies had to divide assets, allocate debt, separate systems, and create entirely new management teams. Thousands of employees had to choose between staying with regulated PPL or joining competitive Talen. The transaction costs exceeded $200 million.

When the spinoff was completed on June 1, 2015, PPL emerged as a pure-play regulated utility for the first time since 1995. But it was a very different utility than the old Pennsylvania Power & Light. The company now operated in four American states and three foreign countries. It earned more from British customers than Pennsylvania ones. It had become, improbably, one of the few truly international utilities.

The transformation was remarkable. In just five years, PPL had invested over $20 billion in acquisitions, fundamentally reshaping its business. The company had gone from primarily domestic to majority international, from integrated utility to pure distribution, from Pennsylvania-focused to globally diversified. Revenue had doubled. The employee count had tripled. The market capitalization had grown from $12 billion to $20 billion.

But questions remained. Was the international diversification sustainable? Could an Allentown-based company effectively manage utilities in Wales? What happened when UK regulation changed or sterling weakened? PPL's stock traded at a discount to domestic utilities, which investors attributed to complexity and currency risk. The international empire PPL had built was impressive, but empires, as history shows, can be difficult to maintain.

VI. The Great Pivot: Back to America (2020-2022)

Vincent Sorgi's first all-hands meeting as CEO in June 2020 was unlike any in PPL's century-long history. Instead of gathering in the company's Allentown headquarters, 6,500 employees joined via videoconference from kitchen tables and home offices across four time zones. COVID-19 had shut down the world, but electricity still needed to flow. As Sorgi outlined his vision from a makeshift studio, he knew something his employees didn't yet: he was already planning to dismantle the international empire PPL had spent a decade building.

The pandemic had accelerated trends that were already troubling. Managing utilities across the Atlantic had always been challenging, but COVID made it nearly impossible. British managers couldn't travel to Allentown for strategy sessions. American executives couldn't visit UK operations. The eight-hour flights and five-hour time difference that had been inconveniences became barriers. When storms hit Wales, Pennsylvania executives monitored response efforts via WhatsApp at 3 AM.

But the strategic concerns ran deeper than logistics. PPL's stock had chronically underperformed pure-play domestic utilities. The company traded at 14-15 times earnings while American peers commanded 18-20 times. The "conglomerate discount" was real and persistent. Investors struggled to value a company with earnings in pounds sterling and dollars, with British price controls and American rate cases, with Kentucky coal plants and Welsh wind farms.

The UK regulatory environment was also shifting. Brexit created uncertainty about everything from labor laws to environmental standards. Ofgem was tightening price controls, reducing allowed returns from 7% to 4-5%. The Labour Party was threatening renationalization of utilities. Climate activists were pressuring for faster decarbonization. The stable, predictable UK market that had attracted PPL a decade earlier was becoming neither.

Sorgi assembled a small team in absolute secrecy to explore strategic alternatives. Code-named "Project Eagle," the analysis examined every option: selling pieces of WPD, buying more US utilities, going private, merging with another company. The models filled encrypted servers. The video conferences stretched past midnight. By October 2020, the conclusion was clear: PPL should exit the UK entirely and return to its American roots.

Finding a buyer for WPD wouldn't be easy. The business was valued at roughly £10 billion—one of the largest utility transactions in UK history. Only a handful of global infrastructure funds or utilities could write that check. The process needed to be confidential; if word leaked, it could destabilize operations, trigger labor actions, or invite political interference.

PPL hired Barclays and Wells Fargo as advisors, launching a formal sale process in November 2020. The code names multiplied—Project Eagle for the overall strategy, Project Thames for WPD, individual bidders assigned bird names. The data room contained 50,000 documents. Potential buyers signed non-disclosure agreements thicker than phone books. Management presentations ran 500 slides.

The bidding attracted global giants: infrastructure funds from Australia and Canada, sovereign wealth funds from the Middle East, European utilities looking to expand. Each had different plans for WPD. Some would lever it up and extract dividends. Others would merge it with existing UK operations. A few proposed breaking it apart, selling the pieces separately.

Then National Grid entered the process with a different proposition. The UK's largest utility didn't just want to buy WPD—it wanted to simultaneously sell its Rhode Island operations to PPL. It was a swap of almost unprecedented complexity: PPL would sell its UK business to a British company while buying an American business from that same British company. Two transactions, two currencies, two regulatory approvals, all needing to close simultaneously.

The strategic logic was compelling. National Grid wanted to consolidate its UK position, becoming the dominant player in British electricity distribution. PPL wanted to return to pure American focus while maintaining its growth trajectory. Rhode Island was perfect—a small but stable state with constructive regulation, adjacent to PPL's Pennsylvania territory, similar in size to what PPL was giving up in earnings.

The negotiations were brutal. Every dollar of value in Rhode Island affected the pound price for WPD. Tax structures had to be optimized in both countries. The timing had to be synchronized—if one deal closed without the other, someone would face massive currency exposure. The documentation eventually exceeded 10,000 pages.

On March 18, 2021, PPL announced the dual transactions. WPD would be sold to National Grid for £7.8 billion. The Narragansett Electric Company (Rhode Island's utility) would be acquired for $3.8 billion. The net proceeds to PPL, after taxes and fees, would be approximately $10.4 billion. The company's stock jumped 8% at the opening, the biggest single-day gain in years.

But the announcement was just the beginning. Both transactions required regulatory approval in multiple jurisdictions. The UK Competition and Markets Authority needed to approve National Grid's acquisition. The Rhode Island Public Utilities Commission had to bless PPL's purchase. The Federal Energy Regulatory Commission had to review both deals. Each regulator had different concerns, different processes, different timelines.

The currency hedging alone was a financial engineering marvel. PPL faced the risk that sterling might weaken between signing and closing, reducing dollar proceeds. The company executed a series of forward contracts and options, locking in an exchange rate of $1.36 per pound. The hedging cost hundreds of millions but provided certainty. When sterling actually strengthened to $1.42 by closing, PPL had left money on the table—but that was the price of prudence.

The Rhode Island regulatory process proved particularly contentious. Consumer advocates worried about an out-of-state utility taking over local operations. Environmental groups questioned PPL's climate commitments. Labor unions sought job guarantees. The state attorney general demanded concessions. PPL ultimately agreed to $200 million in customer bill credits, maintained local employment, and committed to aggressive renewable energy targets.

The UK closure came first, on June 14, 2021. In a ceremony conducted entirely via video conference, ownership of WPD transferred to National Grid. Seven thousand employees changed employers with the stroke of a pen. PPL's Union Jack was lowered from the Birmingham headquarters for the last time. The company that had been the largest American owner of UK utilities no longer owned a single British customer.

The financial impact was immediate and massive. PPL received $10.7 billion in cash—the largest influx in company history. Debt was paid down by $3.5 billion. The company announced a $1 billion share buyback program. The dividend was reset, declining from $1.66 to $0.80 per share annually, reflecting the smaller earnings base. But the payout ratio improved, and management promised 6-8% annual dividend growth going forward.

The Rhode Island acquisition closed on May 25, 2022, completing the transformation. Narragansett Electric was renamed Rhode Island Energy, serving 790,000 electric and 280,000 gas customers. PPL was now purely American again—Pennsylvania, Kentucky, and Rhode Island. No currency translation, no Brexit concerns, no 3 AM phone calls about Welsh weather.

The employees who had built PPL's international operations had mixed emotions. Some felt pride in what they'd accomplished—turning a Pennsylvania utility into a global player. Others felt disappointment that the international dream had ended. The UK team had delivered excellent returns; WPD was sold for nearly double what PPL paid. But the market had spoken: investors wanted simplicity, not complexity.

The strategic pivot was undeniably successful financially. PPL's valuation multiple expanded from 14 times to 17 times earnings, still below pure-play peers but significantly improved. The stock price rose 25% in the year following the announcement. The company's credit rating improved. Analyst coverage became more positive, with several upgrades citing the simplified structure.

Sorgi's post-transaction message to employees was revealing: "We didn't fail internationally. We succeeded. We bought assets, improved operations, earned strong returns, and sold at the right time. But the market has changed. Investors want focused, simple stories. Our story is now clear: we're an American utility investing in American infrastructure for American customers." It was corporate spin, perhaps, but also truth. PPL had executed one of the most successful round-trips in utility history.

VII. Modern PPL: The Pure-Play U.S. Utility (2022-Present)

The storm that tested PPL's new American strategy arrived on Christmas Eve 2022. An arctic blast descended on the eastern United States, sending temperatures plummeting to minus-20 degrees Fahrenheit in some areas. In PPL's territories across Pennsylvania, Kentucky, and Rhode Island, electricity demand spiked to near-record levels as heating systems worked overtime. Ice accumulated on power lines at rates meteorologists called "once in a generation." By dawn on Christmas Day, 350,000 PPL customers had lost power—the company's worst winter storm in decades.

What happened next demonstrated how profoundly PPL had transformed. The company's new Advanced Distribution Management System, installed just months earlier, automatically rerouted power to minimize outages. Artificial intelligence algorithms predicted which circuits would likely fail next, allowing crews to preemptively reinforce vulnerable points. Drones equipped with thermal cameras identified damaged equipment invisible to the human eye. Within 48 hours, 90% of customers had power restored—a recovery that would have taken a week using traditional methods.

This wasn't the PPL of even five years ago. The company that now serves 3.6 million customers with $7.9 billion in revenue has reinvented itself as a technology-forward utility. The $3.2 billion annual capital investment program—funded partly by the WPD sale proceeds—focuses relentlessly on grid modernization. Smart meters, distribution automation, and predictive analytics aren't pilot programs anymore; they're standard operations.

PPL Electric Utilities, the Pennsylvania subsidiary that started it all, has become the company's innovation laboratory. Based on strong year-to-date financial performance and continued execution of the business plan, the company is investing more than $3 billion in infrastructure improvements to make the grid more resilient to future storms and advance a safe, reliable, affordable and cleaner energy future. The service territory stretching from the Philadelphia suburbs through the Lehigh Valley to the Pocono Mountains serves as a real-world testbed for grid technologies that, if successful, roll out to Kentucky and Rhode Island.

The transformation is visible at the Allentown control center, rebuilt in 2023 with technology that would seem like science fiction to the operators of PP&L's original 1920s dispatch center. Wall-sized displays show real-time power flows across 50,000 miles of distribution lines. Machine learning algorithms process data from 2 million smart meters every 15 minutes, identifying potential problems before they cause outages. Operators can remotely control 10,000 switches and breakers, reconfiguring the grid in seconds rather than sending crews to manually operate equipment.

But the most dramatic changes are happening at the edge of the grid, where customers increasingly generate their own power. In Pennsylvania alone, PPL interconnected 15,000 rooftop solar systems in 2023, more than existed in the entire territory a decade ago. The company that once fought distributed generation now embraces it, viewing customer solar panels and batteries as grid assets rather than threats.

The Kentucky operations tell a different story—one of industrial transformation in the heart of coal country. Louisville Gas & Electric and Kentucky Utilities operate in a state where coal still provides 70% of electricity, where mining communities depend on coal jobs, where political leaders fiercely defend fossil fuels. Yet even here, change is accelerating. PPL's Kentucky Regulated segment's earnings from ongoing operations increased by $0.08 per share in the first nine months of 2024 compared with a year ago, with factors driving earnings including higher sales volumes primarily due to weather and lower operating costs.

PPL's Kentucky strategy threads a careful needle. The company is retiring aging coal plants—2,000 megawatts by 2028—but replacing them with natural gas and solar rather than abandoning thermal generation entirely. The Mill Creek coal plant in Louisville, commissioned in 1972, will close by 2027. But a new 640-megawatt natural gas plant is rising next door, providing reliable baseload power and jobs for many of the same workers.

The company has also become Kentucky's largest solar developer, with 1,000 megawatts of solar farms planned or under construction. These aren't rooftop panels but utility-scale installations covering thousands of acres. The Ragland Solar facility in Hardin County, when complete, will be Kentucky's largest solar installation at 200 megawatts. PPL carefully sites these projects in economically distressed areas, providing lease income to struggling farmers and tax revenue to rural counties.

Rhode Island Energy, the newest addition to PPL's portfolio, faces entirely different challenges. Acquired as Narragansett Electric Company and renamed Rhode Island Energy on May 25, 2022, it operates in one of America's most climate-conscious states. Rhode Island law mandates 100% renewable electricity by 2033. The state's Renewable Energy Standard requires increasing percentages of clean energy each year. Environmental groups scrutinize every decision.

PPL's Rhode Island Regulated segment reported earnings from ongoing operations in the first nine months of 2024 increased by $0.03 per share compared with a year ago, with factors driving earnings results primarily including higher distribution revenue from capital investments and higher transmission revenue, partially offset by higher interest expense.

The Rhode Island acquisition also brought PPL into the natural gas business for the first time outside Kentucky. The company now serves 280,000 gas customers in the Ocean State, delivering natural gas for heating and cooking. But even this traditional fossil fuel business is evolving. PPL is piloting renewable natural gas projects, capturing methane from landfills and wastewater treatment plants. The company is also preparing for a potential transition to hydrogen, which could use existing gas pipelines to deliver carbon-free fuel.

The regulatory environment across PPL's three states couldn't be more different, requiring sophisticated state-level strategies. Pennsylvania regulation remains traditional cost-of-service with periodic rate cases. Kentucky allows more automatic cost recovery through riders and trackers. Rhode Island uses performance-based rates with incentives for reliability and clean energy. PPL has learned to optimize within each framework, tailoring investment plans and rate designs to local preferences.

The capital allocation strategy post-WPD sale is disciplined but aggressive. The company increased its capital plan to $20 billion from 2025 through 2028, resulting in average annual rate base growth of 9.8% over the period. About 40% goes to Pennsylvania, 45% to Kentucky, and 15% to Rhode Island. The investments focus on three priorities: grid hardening against extreme weather, modernization to enable renewable integration, and traditional replacement of aging infrastructure.

The financial results validate the strategy. PPL announced 2024 reported earnings (GAAP) of $1.20 per share and achieved earnings from ongoing operations of $1.69 per share, while extending 6% to 8% annual EPS and dividend growth targets through at least 2028. The company expects to achieve earnings growth in the top half of its targeted range, driven by rate base expansion and operational efficiencies.

The technology investments are paying dividends beyond financial returns. PPL's System Average Interruption Duration Index (SAIDI)—the average outage time per customer—has improved 30% since 2020. Customer satisfaction scores have reached record highs. The company consistently ranks in the top quartile for reliability among major U.S. utilities.

But PPL faces new challenges that didn't exist in the monopoly era. Data centers are proliferating across the company's territories, with their massive and constant electricity demands. A single hyperscale data center can consume as much power as 50,000 homes. Electric vehicle adoption is accelerating, requiring upgraded distribution transformers and new rate designs. Cryptocurrency mining operations pop up in rural areas, stressing local grids designed for farm loads.

The clean energy transition presents both opportunities and threats. PPL must invest billions to interconnect renewable generation, upgrade transmission, and maintain reliability as baseload coal plants retire. But these investments expand the rate base, driving earnings growth. The Inflation Reduction Act provides tax credits and grants that reduce customer costs. The Infrastructure Investment and Jobs Act offers federal funding for grid modernization.

Climate change adds another layer of complexity. The Christmas 2022 storm was just one example of increasing extreme weather. PPL's territories face more frequent and severe storms, flooding, and temperature extremes. The company has spent $500 million on storm hardening since 2020—burying vulnerable lines, installing stronger poles, clearing vegetation more aggressively. But each major storm still costs $50-100 million in restoration expenses.

The workforce transformation is equally dramatic. PPL's 6,500 employees increasingly look like technology workers rather than traditional utility staff. The company has hired data scientists, cybersecurity experts, and software developers. Training programs teach lineworkers to operate drones and use augmented reality for equipment inspection. The average age of employees has dropped by five years as digital natives join the workforce.

Looking forward, PPL's strategy seems clear: remain a pure-play regulated utility, grow through capital investment rather than acquisitions, and lead the industry in grid modernization. As CEO Vincent Sorgi stated, "We continue to make significant progress in positioning PPL to create the utilities of the future — stronger, smarter, increasingly clean, and built for growth and success in a changing energy landscape. Our updated business plan reflects this strategy and will drive greater value for our customers, communities and shareowners".

VIII. Playbook: Business & Investing Lessons

The conference room in PPL's Allentown headquarters has witnessed a century of strategic decisions, but perhaps none more instructive than the 2021 board meeting where directors approved the WPD sale. CFO Joe Bergstein presented a single slide that crystallized decades of utility wisdom: "We bought WPD at 1.4x regulated asset value and sold at 1.8x. But our own stock trades at 1.2x. We're literally worth more dead than alive." That gap—between what strategic buyers pay for utility assets and what public markets value utility stocks—encapsulates the central challenge of utility investing.

The Value of Regulatory Relationships and Political Capital

PPL's history demonstrates that in the utility business, regulatory relationships are more valuable than physical assets. Power plants can be built, transmission lines can be strung, but constructive regulatory frameworks take decades to cultivate. The company's success in Pennsylvania stems from 100 years of trust-building with regulators, politicians, and consumer advocates. PPL executives serve on state economic development boards, sponsor community programs, and maintain relationships across the political spectrum.

The Kentucky acquisition succeeded partly because PPL inherited LG&E and KU's century-old regulatory relationships. The companies had never had a contentious rate case, maintaining what insiders call "the Kentucky compact"—utilities provide reliable service and economic development support; regulators provide reasonable returns and timely cost recovery. When PPL proposed billions in coal plant replacements, Kentucky regulators approved them with minimal controversy because of this accumulated trust.

Conversely, the Rhode Island acquisition required PPL to essentially purchase regulatory goodwill. The $200 million in bill credits, local employment guarantees, and renewable energy commitments weren't just transaction costs—they were investments in political capital that would pay dividends in future rate cases. Smart utilities understand that regulatory approval isn't bought in rate hearings; it's earned through years of reliable operation and community engagement.

When to Expand Internationally vs. Stay Domestic

PPL's round-trip to the UK offers a masterclass in international expansion timing. The company entered when conditions were perfect: stable UK regulation, favorable exchange rates, distressed sellers, and accessible financing. It exited when those conditions reversed: regulatory tightening, Brexit uncertainty, and premium valuations from strategic buyers.

The key insight is that international utility expansion only makes sense when you can arbitrage regulatory, financial, or operational differences. PPL could borrow in sterling at lower rates than UK utilities because of its strong US credit rating. It could apply American operational practices to British networks that had underinvested in technology. It could navigate UK regulation using skills honed in Pennsylvania rate cases.

But international expansion creates complexity that markets discount. Currency hedging costs money. Management attention divides. Regulatory expertise doesn't always translate. PPL's experience suggests international utility ventures should be viewed as long-term trades rather than permanent holdings—enter when valuations are low and regulation is favorable, exit when strategic buyers emerge and complexity discounts persist.

Capital Recycling: Selling High, Buying Strategic

The WPD-Rhode Island swap exemplifies sophisticated capital recycling. PPL sold a large, foreign, complex asset at premium multiples to a strategic buyer who valued it higher. It simultaneously bought a smaller, domestic, simpler asset at lower multiples that fit its core strategy. The transaction destroyed earnings per share in the short term but created value through multiple expansion and strategic focus.

This pattern repeats throughout PPL's history. The company bought Montana generation when power prices were low and sold (via Talen spinoff) when environmental regulations made coal uneconomic. It acquired UK distribution when pound sterling was strong and sold when Brexit created uncertainty. Each transaction followed the same principle: buy when you have an operational or financial advantage, sell when strategic value exceeds hold value.

The discipline to sell good assets is rare in utilities, where executives often become emotionally attached to properties they've improved. PPL's UK operations were excellently run, generating strong returns. But management recognized that excellence doesn't justify ownership if someone else values the asset more highly. The £7.8 billion National Grid paid exceeded any reasonable hold value PPL could generate.

Managing Through Deregulation and Re-regulation Cycles

PPL's journey through Pennsylvania deregulation offers lessons in regulatory cycle management. The company prepared for deregulation years before it arrived, restructuring operations and training employees for competitive markets. When deregulation came, PPL was positioned to profit from both the regulated utility and competitive generation businesses.

But PPL also recognized that full deregulation rarely lasts. Political winds shift, market failures occur, and regulation creeps back. The company maintained strong regulatory relationships even while operating competitive businesses. When Pennsylvania's deregulated retail market struggled, PPL was positioned to provide default service. When environmental regulations tightened, the company had the political capital to recover compliance costs.

The lesson is that utilities must build strategies robust to regulatory cycles. Pure deregulation plays (like merchant generation) face existential risk when regulation returns. Pure regulated strategies miss opportunities when markets liberalize. The winning approach maintains optionality—assets and capabilities that perform under multiple regulatory scenarios.

The Utility Consolidation Playbook

PPL's origin story from the 1920s established a consolidation playbook still valid today: identify fragmented markets, acquire subscale operators, integrate operations, standardize processes, and capture synergies through scale. This formula drove PPL's assembly of Pennsylvania territory, expansion into Kentucky, and acquisition of Rhode Island operations.

The key is that utility consolidation creates value through operational integration, not financial engineering. Combining two utilities doesn't automatically reduce costs—it requires systematic process improvement, technology standardization, and workforce optimization. PPL's success came from ruthlessly eliminating redundancy while maintaining service quality. Each acquisition followed the same integration plan, refined over decades.

Modern utility consolidation faces higher regulatory barriers but offers greater synergy potential through technology. Combining utilities allows spreading costs of expensive systems—advanced metering infrastructure, distribution management systems, customer platforms—across more customers. PPL's post-merger technology investments in Rhode Island leverage systems already developed for Pennsylvania and Kentucky.

Currency Hedging and International Risk Management

PPL's UK experience provides a doctorate-level course in currency risk management. The company employed every hedging instrument available: forward contracts, currency swaps, options, and natural hedges through sterling-denominated debt. The hedging strategy for the WPD sale alone involved dozens of transactions executed over months to lock in exchange rates while maintaining flexibility.

The lesson isn't just about technical hedging but about understanding what risks to take. PPL hedged transaction risk (exchange rates between signing and closing) but accepted translation risk (ongoing earnings in foreign currency). The company protected against catastrophic currency moves but accepted normal volatility. This selective hedging balanced risk management with cost.

The broader insight is that international utility investment requires sizing positions appropriately. PPL's UK operations grew to dominate earnings, making currency translation a major stock price driver. A smaller international position might have provided diversification without complexity. The right size depends on an investor's risk tolerance and the market's appetite for complexity.

Why Utilities Trade at Different Multiples in Different Jurisdictions

Perhaps the most valuable lesson from PPL's journey is understanding utility valuation disparities. The same electrons flowing through similar wires can be worth vastly different amounts depending on regulatory framework, growth prospects, and market structure. UK distribution utilities trade at higher multiples than US utilities because of longer regulatory periods and inflation indexation. Within the US, utilities in growth states trade at premiums to those in declining regions.

PPL exploited these disparities through geographic arbitrage—buying where multiples were low and selling where they were high. But the company also learned that multiple disparities persist for reasons. UK utilities trade at higher multiples but face tighter regulation. High-growth utilities command premiums but require constant capital investment. There's no free lunch, only different risk-return tradeoffs.

For investors, the lesson is to understand what drives utility multiples: regulatory framework quality, allowed returns versus interest rates, growth prospects, operational efficiency, and balance sheet strength. PPL's transformation demonstrates that changing these factors—through operational improvement, regulatory strategy, or portfolio reshaping—can drive multiple expansion even without earnings growth.

IX. Analysis & Bear vs. Bull Case

Bull Case: The Infrastructure Supercycle Beneficiary

The bull case for PPL starts with an observation that would have seemed like science fiction to the company's 1920 founders: America is about to electrify everything. Transportation, heating, industrial processes, even agriculture—all are shifting from fossil fuels to electricity. PPL sits at the intersection of this transformation, owning the wires that must carry all those new electrons.

The numbers are staggering. Electric vehicle adoption in PPL's territories is projected to increase electricity demand by 20% by 2035. Data centers, drawn to Pennsylvania's cheap power and Kentucky's available land, could add another 15%. Heat pump adoption in Rhode Island alone could double winter electricity demand. This isn't speculative—it's happening now. PPL processed interconnection requests for 5,000 megawatts of new load in 2024, more than the previous five years combined.

The company's increased capital plan to $20 billion from 2025 through 2028, resulting in average annual rate base growth of 9.8%, positions PPL to capture this growth. Unlike competitive businesses where growth requires winning market share, regulated utilities earn guaranteed returns on infrastructure investment. Every dollar PPL spends on grid upgrades, subject to regulatory approval, generates roughly 10 cents of annual earnings forever.

The regulatory environment has never been more constructive. The Inflation Reduction Act provides unprecedented federal support for grid modernization. States are mandating renewable energy transitions that require massive transmission investment. Regulators understand that reliability requires grid hardening against climate change. PPL operates in states with supportive regulation—Pennsylvania's infrastructure replacement programs, Kentucky's construction work in progress recovery, Rhode Island's performance incentives all allow timely cost recovery.

PPL's operational excellence multiplies these advantages. The company consistently ranks in the top quartile for reliability and customer satisfaction. Its technology investments—grid automation, predictive analytics, smart meters—reduce costs while improving service. This operational superiority translates to regulatory goodwill, enabling PPL to earn at the high end of allowed return ranges.

The financial position is equally strong. The WPD sale left PPL with one of the sector's best balance sheets. The company can fund its entire capital program without issuing equity, avoiding dilution. Credit ratings are solidly investment grade with positive outlooks. The 50% payout ratio leaves room for 6% to 8% annual EPS and dividend growth targets through at least 2028.

The simplification story resonates with investors. PPL is now a pure-play U.S. regulated utility—no currency translation, no international complexity, no commodity exposure. The business model is transparent: invest capital, earn regulated returns, grow the dividend. This simplicity should drive multiple expansion toward peer levels.

Climate change, paradoxically, helps PPL. Extreme weather drives infrastructure investment needs. Decarbonization mandates create growth opportunities. Federal funding supports grid modernization. The company's coal plant retirements, replaced with renewables and gas, improve environmental scores while expanding rate base. PPL is transforming from climate problem to climate solution.

The hidden option value lies in utility consolidation. PPL's operational capabilities and strong balance sheet position it as a potential acquirer. Dozens of small utilities in adjacent states could be targets. Each acquisition would bring scale efficiencies and regulatory diversification. The company that began through consolidation could grow through it again.

Bear Case: The Stranded Asset Trap

The bear case begins with a stark reality: PPL owns billions in assets that might become worthless. The company's Kentucky coal plants, natural gas infrastructure, and even parts of its transmission system face obsolescence risk as the energy transition accelerates. Stranded assets aren't theoretical—they're already happening. Pacific Gas & Electric's bankruptcy, driven partly by wildfire liability, shows how quickly utility assets can become liabilities.

PPL's Kentucky operations are particularly vulnerable. The state depends on coal for 70% of its electricity, but coal economics are deteriorating rapidly. Environmental regulations tighten annually. Renewable costs continue falling. Natural gas, touted as a bridge fuel, faces its own phase-out pressures. PPL is investing billions in gas plants that might operate for only 15-20 years instead of the traditional 40-50.

Regulatory risk looms larger than investors appreciate. PPL operates in three states with different political dynamics and regulatory philosophies. Pennsylvania's regulatory framework, stable for decades, faces pressure from consumer advocates demanding lower rates. Kentucky regulators, historically supportive, are questioning cost recovery as bills rise. Rhode Island's aggressive climate mandates could force accelerated asset retirements without full compensation.

The growth story might be overblown. Yes, electrification drives demand, but distributed generation erodes PPL's monopoly. Every rooftop solar panel, every battery storage system, every microgrid reduces dependence on utility infrastructure. PPL might spend billions upgrading grids only to see customers defect. The "death spiral"—where fixed costs spread across fewer kilowatt-hours, driving up rates and accelerating defection—remains a long-term threat.

Competition from distributed resources is accelerating. Tesla's Powerwall, residential solar, and community microgrids offer alternatives to utility power. Large customers increasingly self-generate, using utilities only for backup. Technology companies are developing peer-to-peer energy trading platforms that could bypass utilities entirely. PPL's monopoly, seemingly secure, faces technological disruption similar to what destroyed landline telephone companies.

Interest rate sensitivity creates near-term headwinds. Utilities are essentially bond substitutes—investors buy them for dividends, not growth. When interest rates rise, utility valuations fall. PPL trades at 17 times earnings partly because rates remain historically low. If rates normalize to 5-6%, utilities could trade at 12-14 times earnings, implying 20-30% downside.

The capital intensity trap worsens with time. PPL's $20 billion capital plan through 2028 sounds impressive, but it merely maintains the existing system while adapting to new requirements. Grid modernization, storm hardening, and renewable integration require constant investment. Unlike technology companies where capital spending eventually moderates, utility capital needs accelerate with age and complexity.

Physical climate risks are underpriced. PPL's territories face increasing extreme weather—ice storms, derechos, flooding, and polar vortexes. Each event costs tens of millions in restoration. Insurance covers some costs, but deductibles rise and coverage shrinks. The Christmas 2022 storm alone cost PPL $75 million. Climate change makes "100-year storms" annual events.

Cybersecurity presents existential risk. Utilities are prime targets for state-sponsored hackers and criminal ransomware. A successful attack could shut down power for millions, triggering massive liability. Colonial Pipeline paid $4.4 million in ransomware; a utility attack could cost billions. PPL spends heavily on cybersecurity, but attackers need to succeed only once.

The dividend sustainability question persists. PPL reset its dividend after the WPD sale, but growth requires constant capital market access. If equity markets close or debt becomes expensive, dividend growth stops. The company's 50% payout ratio provides cushion, but earnings depend on regulatory approvals that could be denied or delayed.

Customer affordability becomes politically toxic. Electricity bills in PPL territories have risen 30% since 2020. Further increases to fund capital investment face political resistance. Regulators must balance utility returns with customer impacts. As bills rise, political pressure for municipalization or rate freezes intensifies. PPL could win every regulatory battle but lose the political war.

The Verdict: Steady Accumulator with Hidden Risks

The truth lies between extremes. PPL is neither the infrastructure supercycle winner bulls envision nor the stranded asset disaster bears fear. It's a steady, well-managed utility navigating massive industry transformation with reasonable success probability.

The bull case fundamentals are solid: America needs massive grid investment, PPL operates in constructive regulatory environments, and the company executes well operationally. The 6-8% annual earnings and dividend growth targets through 2028 seem achievable given the capital program and regulatory support.

But the bear concerns are real: stranded asset risk in Kentucky, distributed generation threats, and climate change costs could materially impact returns. The company trades at reasonable valuations precisely because these risks exist. PPL isn't mispriced—it's fairly priced for a utility facing both opportunities and challenges.

For investors, PPL represents a classic regulated utility investment: moderate growth, decent dividend yield, and defensive characteristics, but with regulatory, technological, and environmental risks. It's suitable for income-focused investors who understand utility dynamics and can tolerate regulatory uncertainty. It's not for growth investors seeking the next doubling or conservative investors wanting risk-free returns.

The key variables to monitor are regulatory decisions (particularly Kentucky coal plant cost recovery), load growth (especially data centers and EVs), and distributed generation adoption rates. If regulation remains supportive and load grows faster than expected, PPL could deliver high-single-digit returns. If regulation tightens and distributed generation accelerates, returns could disappoint.

X. Epilogue & "What Would We Do?"

Standing in PPL's Allentown control room in 2025, watching operators manage electricity flows across three states, you can't help but marvel at the transformation. The company that began with eight small utilities merging around a boardroom table in 1920 now uses artificial intelligence to predict equipment failures before they happen. The business that once measured success by keeping lights on now optimizes for carbon reduction, grid resilience, and customer choice. Yet fundamentally, PPL remains what it always was: a vital piece of infrastructure connecting energy supply with demand.

If we were running PPL today, the strategy would focus on becoming the platform that enables rather than resists the energy transition. The traditional utility model—centralized generation flowing one-way to passive consumers—is already obsolete. The future grid is bidirectional, with millions of producers and consumers trading energy like packets on the internet. PPL shouldn't fight this future; it should build the infrastructure to enable it.

First priority: accelerate the transformation of distribution networks into energy platforms. This means moving beyond smart meters to true grid intelligence—every transformer, switch, and wire capable of real-time communication and control. PPL should position itself as the "operating system" for distributed energy, providing the standards, protocols, and physical infrastructure that allow seamless integration of solar panels, batteries, EVs, and other distributed resources. Think of it as becoming the iOS or Android of the energy world—earning returns not just from wires but from enabling transactions across those wires.