Watts Water Technologies: The 150-Year Story of America's Hidden Water Infrastructure Giant

I. Introduction: The Boring Brilliance of Valves and Safety

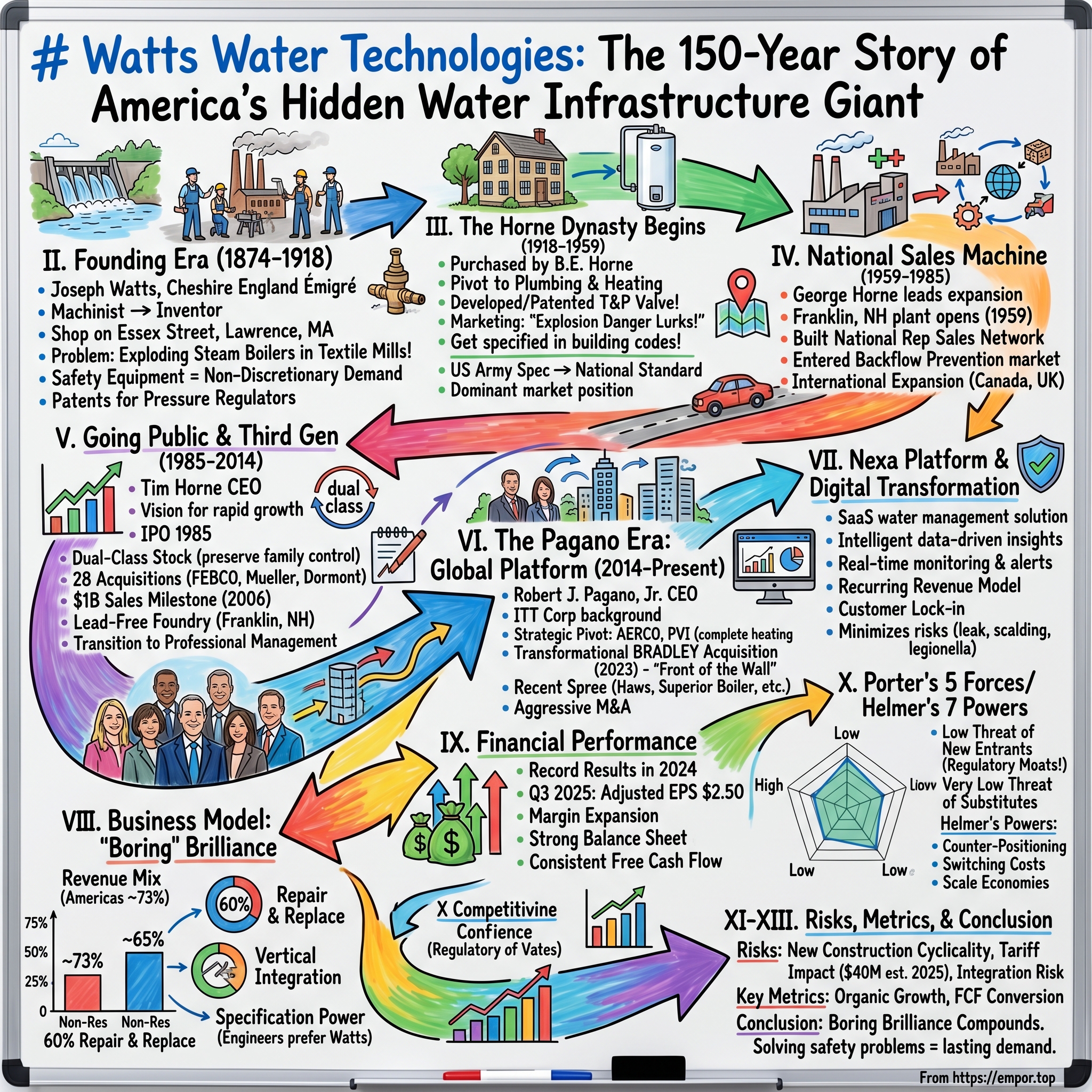

In August 2024, about 300 employees, retirees, suppliers, and local officials gathered at the corporate headquarters in North Andover, Massachusetts, to celebrate a milestone that few American manufacturing companies achieve: 150 years in continuous operation. The event was hosted by CEO Robert Pagano, but the emotional center belonged to Tim Horne, Director Emeritus, whose family had owned and operated the business for three generations. Horne regaled the audience with stories of his great grandfather breaking ground, mock home explosions and company growth.

The celebration captured something essential about Watts Water Technologies. Here is a company that makes products most people never think about—pressure regulators, temperature and pressure relief valves, backflow preventers—yet these products sit in virtually every building in America. They are the invisible infrastructure of water safety. And they have made Watts one of the most consistent wealth-compounding machines in the industrial sector.

As of Q4 2024, Watts held a global market share of 7.58% and achieved $2.25 billion in sales for the full year. The company's market cap reached approximately $9.4 billion as of November 2025, with market cap growth of over 37% in one year. Not bad for a company that started as a machine shop supplying parts to New England textile mills.

Watts Water Technologies, Inc. is an American manufacturing company based in North Andover, Massachusetts, that makes valve products for plumbing and heating, such as water pressure regulators and other valves. Watts is one of the largest manufacturers of water valves in the United States.

The hook for any investor is this: how does a 150-year-old company selling boring plumbing components become a premium-valuation juggernaut in the industrial sector? The answer lies in a combination of factors that any long-term investor should appreciate: regulatory moats built over decades, a family culture that prioritized long-term thinking over quarterly earnings, a repair-and-replace business model that generates demand regardless of economic cycles, and disciplined capital allocation that has transformed modest revenue growth into exceptional returns on invested capital.

This article will trace the arc of Watts from its founding during the New England textile boom through three generations of Horne family leadership, the transition to professional management under Bob Pagano, and the digital transformation that promises to turn a product company into a solutions platform. Along the way, we will examine the sources of Watts's competitive moat, the key metrics investors should track, and the strategic risks that could derail this quiet compounder.

II. Founding Era: Joseph Watts & The Textile Mills (1874-1918)

The Great Stone Dam and a 17-Year-Old Machinist

When Joseph Edwin Watts was 17 years old, he emigrated from Cheshire, England, to the newly built town of Lawrence, Massachusetts. The town was founded in 1845 by a group of industrialists and entrepreneurs whose idea was to build "The Great Stone Dam" across the Merrimack River to harness the river's immense water power for industrial textile production.

Lawrence in the mid-19th century was America's industrial frontier—a planned city designed specifically for manufacturing. The dam channeled the Merrimack's power into mills that produced cotton and woolen textiles at unprecedented scale. For a young machinist from England, it represented opportunity.

The first records of Joseph Watts's employment were in 1867 as a machinist at the Pacific Mills in Lawrence. He worked there until 1874, when he left to go into business for himself. From his shop on Essex Street, he contracted work supplying parts and fittings for machinery at the nearby textile mills.

The Problem of Exploding Boilers

The textile mills of 19th century New England had a deadly problem: steam boilers exploded. The industrial revolution ran on steam, but the technology for controlling steam pressure was primitive. Boiler explosions killed workers, destroyed equipment, and halted production. Insurance companies struggled with how to price the risk. Mill owners desperately needed reliable safety equipment.

Joseph Watts was a prodigious patent holder, innovating steam and water pressure regulators designed to stop catastrophic boiler failure and protect textile mill workers. While designed primarily for the textile industry, Joseph Watts' first pressure relief valve patent was hugely successful, finding widespread application and implementation.

By that time Watts had become more than a machinist and manufacturer. He was also an inventor, and between 1881 and his death in 1894, he received 18 patents for valves that proved essential to almost every manufacturing concern in the area.

First Lesson: Solving a Safety Problem Creates Lasting Demand

Watts's early success illustrates a pattern that would define the company for the next 150 years. Safety equipment is not discretionary. When a product prevents explosions and saves lives, customers don't haggle over price. Demand is inelastic because the alternative—catastrophic failure—is unthinkable.

As Laurie Leavy, senior manager of corporate communications, explained at the 150th anniversary: "Joseph Watts founded the company in Lawrence, and basically it was because there was pressure explosions in manufacturing sites and he wanted to save people's lives."

Joseph Watts died in 1894, but the company he founded continued under successive owners until it caught the attention of a local roofing contractor named Burchard Everett Horne.

III. The Horne Dynasty Begins (1918-1959)

B.E. Horne's $25,000 Bet

In 1918, Watts Regulator was purchased by Burchard Everett Horne (B.E. Horne). This transformed the company into a family-owned and operated business.

What started as a $15,000 investment with the purchase of the company from Joseph E. Watts. (Other sources cite $25,000, suggesting the purchase price was negotiated or the figures include different transaction costs.) Either way, it was a modest sum that would yield extraordinary returns over the following century.

By the time B.E. purchased the Watts Regulator Company, the textile industry, upon which the town of Lawrence had been founded, was in deep decline. The advent of steam power (as opposed to waterpower) meant that textile mills could be set up anywhere that fuel was available. Other technical advances, plus high labor costs and taxes in the North, drove the textile industry farther and farther south.

This was a pivotal moment. The textile industry that had given birth to Watts was dying. B.E. Horne recognized that the company needed to pivot from industrial steam applications to a new market: residential and commercial plumbing.

Robert Pickles had begun the diversification of the Watts Regulator Company, and B.E. Horne quickly capitalized on his emphasis on plumbing and heating uses for Watts valves.

The T&P Valve: An Innovation That Changed Everything

The 1920s brought a new danger to American homes. Gas-fired water heaters were becoming standard in middle-class households, but the safety technology hadn't kept pace. Water heaters were equipped with pressure-only relief valves, and yet they continued to explode.

The company's breakthrough came in the late 1920s, when B.E. Horne and an inventor named Chetwood Smith developed and patented a combination temperature and pressure relief valve, which came to be known as the T&P Valve. The valve was an important development in the safety of hot-water supply tank systems. Overheated hot-water tanks (without these safety valves) had periodically exploded, causing extensive property damage and even fatalities.

The insight was elegant: pressure alone wasn't the problem. When water overheats, it can turn to steam almost instantly, creating explosive pressure that overwhelms pressure-only valves. The T&P valve addressed both failure modes—releasing water when either temperature or pressure exceeded safe limits.

The Brilliant Marketing & Regulatory Strategy

Inventing a better safety device was only half the battle. B.E. Horne understood that the real moat would come from getting T&P valves specified in building codes. This meant educating regulators, plumbing inspectors, and insurance companies about why combination temperature and pressure valves were necessary.

George Horne (B.E.'s son) drove one of the company's earliest marketing campaigns: "Explosion Danger Lurks!", which demonstrated the dangers of unprotected water heaters in an effort to get T&P valves specified in safety codes.

Watts created a type of safety valve known as the temperature and pressure valve (T&P valve), which was used for safely venting hot-water supply tank systems, reducing the risk of explosion. By the time of World War II, the U.S. Army required Watts T&P valves on all army hot-water supply tanks.

The U.S. Army specification was a watershed moment. When the federal government specifies a product for military applications, it creates instant credibility. And military specifications often become the template for civilian building codes.

Today, most major water heater manufacturers use T&P Relief Valves manufactured by Watts—a dominant market position that traces directly back to B.E. Horne's regulatory strategy nearly a century ago.

Why "Educate the Regulators" Is a Timeless Playbook

The T&P valve story illustrates a business model that Hamilton Helmer might call "counter-positioning with regulatory capture." Watts didn't just make a better product; it created the standard by which all competitors would be judged. Once T&P valves were specified in building codes, the market was effectively locked in. Competitors could try to make cheaper or different valves, but they still had to meet the specifications that Watts helped write.

This is a powerful moat because it compounds over time. Every new building code revision, every update to safety standards, involves the same regulators and engineers who already know Watts products. The switching costs aren't technological—they're institutional.

IV. George Horne & The Building of a National Sales Machine (1959-1985)

Expansion and the Franklin Plant

Upon B.E. Horne's untimely passing, day-to-day control fell into the hands of George. Under a new generation of management the company changed, grew, and expanded. George drove the opening of the manufacturing plant in Franklin, NH in 1959.

The Franklin plant represented a bet on growth. By the late 1950s, the original Lawrence facility had grown overcrowded. The new 73,000-square-foot manufacturing plant in Franklin, New Hampshire provided room to scale. Today, that plant has undergone 16 expansions and grown to nearly triple its original square footage—a testament to the company's organic growth trajectory.

Building the Rep Network

George Horne's genius wasn't engineering—it was sales. He built the company's first national manufacturers' representative sales network, a distribution strategy that remains central to Watts's business model today.

Horne appointed his son George to head up marketing and sales for the company. In short order, George Horne was on the road, going from city to city, driving new sales, and marketing Watts products to the masses.

The manufacturers' rep model is notable because it avoids the channel conflict that plagues companies selling through big-box retail. Watts sells primarily through wholesale distributors and rep firms that serve contractors and engineers. This keeps pricing rational and protects margins.

Entering the Backflow Prevention Market

In the 1970's, George led Watts Regulator into backflow prevention and the waterworks industry. Backflow preventers have since become one of our most successful product lines.

Backflow preventers are devices that stop contaminated water from flowing backward into clean water supplies. Like T&P valves, they are code-mandated safety equipment—once installed, they create ongoing demand for testing, maintenance, and replacement.

The backflow prevention market exemplifies Watts's strategy of entering adjacent product categories where regulatory requirements create captive demand. By 2024, backflow preventers represented one of the company's most profitable product lines.

International Expansion

With George Horne at the helm, Watts Regulator expanded its domestic presence and entered the global market with manufacturing plants in Canada and the United Kingdom.

The international expansion of the 1960s and 1970s laid the groundwork for today's global footprint. Headquartered in North Andover, Watts is a global company with about 5,000 employees on five continents and $2 billion in revenue.

V. Going Public & Third Generation Leadership (1985-2014)

Tim Horne Takes the Helm

In 1976 Tim Horne became President of the company. When his father George retired in 1978, Tim became President and Chief Executive Officer (CEO).

Tim Horne represented the third generation of family leadership—a transition that often proves fatal for family businesses. The statistics are stark: fewer than 13% of family businesses survive to the third generation. Watts not only survived but thrived.

Tim's vision included expanding Watts into new markets with the development of entirely new product lines. His strategy paid off as sales rose from $39.5 million in 1978 to $100 million in 1984.

The IPO Decision

To build on this dramatic growth, Tim explored going public to raise investment capital and making major acquisitions. And so it would be, Watts Industries, Inc. was incorporated in Delaware in 1985 and went public around that same time.

The decision to go public was driven by Tim Horne's ambitious acquisition strategy. Between 1985 and 1995, Tim and his executive team made 28 acquisitions, including several international businesses, building Watts Industries into a significant global player.

The Dual-Class Stock Structure

When Watts went public, it implemented a dual-class stock structure that preserved family control while accessing public capital markets. Watts has two classes of common stock outstanding, Class A and Class B. The Class B common stock entitles its holders to ten votes for each share and the Class A common stock entitles its holders to one vote per share.

The dual-class structure allowed the Horne family to raise capital through public markets while retaining voting control. This meant Tim Horne could pursue his long-term acquisition strategy without worrying about short-term activist pressure.

Timothy P. Horne has filed a 13G/A form disclosing ownership of 6,004,290 shares of Watts Water Technologies Inc (WTS). This represents 17.9 percent ownership of the company.

The $1 Billion Milestone

After years of continued growth and strategic acquisitions, including FEBCO, Mueller Steam Specialty, and Dormont, Watts reached a corporate milestone: $1 billion in sales. This milestone was achieved in 2006, demonstrating the power of the company's acquisition-driven growth strategy.

The Lead-Free Revolution

In response to the Reduction of Lead in Drinking Water Act, Watts made the decision to open a dedicated 30,000 square foot lead free foundry at its Franklin, NH campus, positioning the company as a trusted source for lead free products. As a lead free pioneer, Watts also took a leadership role in educating the industry about lead free as a founding member of the "Get the Lead Out" Consortium.

The lead-free transition exemplifies how Watts turns regulatory change into competitive advantage. When new regulations mandate different products, companies that can move quickly and educate the market gain share. Watts's integrated manufacturing—including its own foundry—gave it the flexibility to reformulate products faster than competitors relying on outside suppliers.

Transition to Professional Management

The parent company's name was changed from Watts Industries to Watts Water Technologies, Inc. in 2003 to appropriately reflect our focus on water-related solutions. Under O'Keefe's leadership, Watts grew and expanded significantly with an annual revenue increase from $615 million (2002) to over $1.2 billion (2010) in addition to the acquisition of 23 companies-- increasing corporate revenues by approximately $400 million.

Patrick S. O'Keefe was appointed CEO in 2002, marking the transition from family management to professional leadership. He oversaw the transition of a successful family-owned business to a publicly-traded company with an international presence.

O'Keefe was succeeded by then COO David Coghlan in 2011. Coghlan helped the company lead the industry during the Lead Free plumbing transition in the U.S., strengthen business in EMEA, and expand in key growth markets. Coghlan left in early 2014 and Robert J. Pagano, Jr., was appointed President and CEO as he remains today.

VI. The Pagano Era: Transformation to a Global Platform (2014-Present)

The New CEO's Background

Robert J. Pagano, Jr. has been the CEO of Watts Water Technologies since May 2014 and became its Chairperson in February 2022. Before this, he worked at ITT Corporation for over 15 years, moving up the ranks to become the Senior Vice President and President of ITT Industrial Process.

Mr. Pagano originally joined ITT in 1997 and served in several additional management roles during his career at ITT, including as Vice President Finance, Corporate Controller, and President of Industrial Products.

He's a Certified Public Accountant and kicked off his career at KPMG, which shows his strong financial background.

Pagano's background is significant. He came from ITT Corporation, a diversified manufacturer that spun off Xylem (now a Watts competitor in the water technology space). His financial discipline and experience in industrial process businesses prepared him for the challenge of transforming Watts from a product company into a solutions provider.

Watts Water Technologies' CEO is Bob Pagano, appointed in May 2014, has a tenure of 11.58 years. His total yearly compensation is $9.05M, comprised of 11.9% salary and 88.1% bonuses, including company stock and options. He directly owns 0.59% of the company's shares, worth $54.02M.

Strategic Pivot to Heating and Water Heating

Prior to 2014, Watts had offered many of the components of a water-heating system, but not the boilers or water heaters themselves. All that changed in November 2014 with the acquisition of AERCO, a New York state-based manufacturer of high-efficiency commercial condensing boilers and water heaters.

In November 2016, Watts acquired PVI in Fort Worth, TX, a leading manufacturer of high-efficiency commercial water heaters for new construction and building retrofits in North America. PVI complemented the AERCO brand's leading position in high-efficiency boilers, thus strengthening Watts' ability to provide customers with complete heating and hot-water system solutions.

The AERCO and PVI acquisitions represented a strategic evolution: Watts was moving from components to complete systems. This is the classic "razors and blades" playbook applied to commercial water heating—sell the system, then capture the ongoing maintenance and replacement revenue.

Bradley Corporation Acquisition (2023)—Transformational Deal

Watts Water Technologies completed the previously announced acquisition of Bradley Corporation for $303 million, subject to customary adjustments. The net transaction value is approximately $268 million after adjusting for the estimated net present value of expected tax benefits of approximately $35 million.

The acquisition was funded with cash on hand and from Watts' existing revolving credit facility. Bradley is a trusted provider and manufacturer of commercial washroom and emergency safety products serving commercial (primarily institutional) and industrial end markets for over 100 years.

Bradley's complementary portfolio will enable us to provide our customers with innovative water solutions, as it adds front-of-the-wall applications to our differentiated back-of-the-wall portfolio.

The Bradley acquisition was transformational because it moved Watts into visible, branded products. Traditional Watts products are "back-of-wall"—hidden inside walls and mechanical rooms. Bradley products are "front-of-wall"—commercial washroom fixtures, emergency eyewash stations, and touchless faucets that building occupants actually see and use.

Bradley has annual net sales of approximately $200 million. At a net transaction value of $268 million, Watts paid less than 8x EBITDA after expected synergies—a reasonable multiple for a leading brand in a niche market.

Bryan Mullett, Bradley's Chairman and CEO, joined Watts as President of Bradley, a new platform within Watts' Americas region.

Recent Acquisition Spree (2023-2025)

Pagano has maintained an aggressive acquisition pace:

2023: - Completed the acquisition of Enware Australia to expand its global footprint in the APMEA region. - Acquired Josam Company, headquartered in Michigan City, IN, which specializes in designing and manufacturing drainage and plumbing products.

2025: - Completed the acquisition of I-CON Systems on January 2, 2025, which will enable expansion of digital offerings and provide growth opportunities in the correctional facility niche of the institutional market. - On June 13, 2025, Watts Water Technologies, Inc. acquired all the assets of Freije Treatment Systems, Inc., also known as "EasyWater" in an all-cash transaction. EasyWater, which is based in Fishers, Indiana, specializes in residential and commercial water treatment solutions, specifically in filtration and conditioning technologies which align with Watts Water's existing water quality portfolio. - Watts completed the acquisition of Superior Boiler, an industry leading designer and manufacturer of customized steam and hot water boilers and related ancillary equipment used in commercial, institutional and industrial applications. Superior offers a comprehensive portfolio that includes firetube, watertube and condensing boilers and has annualized sales of approximately $60 million. The acquisition was funded with cash on hand.

Haws Corporation (November 2025): In the third quarter, the company acquired Haws Corporation, a leading provider of emergency safety and hydration solutions. Management stated that the addition of Haws' innovative, specified products enhances the company's ability to deliver broader capabilities and solutions to customers.

The Haws acquisition will enhance the product portfolio and contribute approximately $60M in sales, but be modestly dilutive to margins in the first year; management expects to raise Haws' margins over several years to company averages.

VII. The Nexa Platform & Digital Transformation

From Products to Solutions

Watts Water Technologies, a global leader in plumbing, heating, and water quality technologies, introduced Nexa, the only truly intelligent water management solution on the market. Designed for facilities of all types, Nexa moves beyond "smart" technology by delivering proactive, data-driven insights that help facility managers take complete control of their water systems and gain actionable insights.

Nexa is a water management solution for commercial buildings that offers real-time monitoring, alerts and insights to prevent water-related incidents and reduce water and energy consumption. The system features sensing technology and a software platform designed to uncover hidden water system insights and risks, allowing facility managers to enhance building performance and occupant experience.

Watts Water Technologies announced the launch of Nexa, a SaaS water management solution expected to generate ongoing subscriptions.

How Nexa Works

Nexa technology is embedded in select water management assets from the Watts family of brands. Users access and manage that equipment via the Nexa dashboard. Adding additional pieces of Nexa equipment and/or Nexa sensing technology expands the ecosystem.

Developed by Watts, the Nexa platform provides real-time visibility into building water systems, empowering facility personnel to monitor and analyze water usage, temperature, pressure, and system health daily. With on-demand support from Watts' Customer Success Team, users can leverage Nexa's data to identify ways to mitigate risk, conserve water, reduce energy spend, and improve overall operational efficiency.

Nexa is system agnostic with many facilities experiencing a 3x return on their initial investment in the first year of usage. Nexa offers real-time monitoring, alerts, and insights to prevent costly water-related incidents and reduce water and energy consumption.

The Strategic Significance

Customers typically receive payback within the first year after installation. Access Nexa's powerful dashboard via the web app... Empower your team for as little as $150/month.

The transition from product company to solutions platform is strategically significant for several reasons:

-

Recurring Revenue: SaaS subscriptions create predictable, recurring revenue streams—a significant evolution from Watts's traditional transactional model.

-

Customer Lock-In: Once a building's water systems are monitored through Nexa, switching costs increase substantially. The accumulated data, customized alerts, and integration with Watts equipment create stickiness.

-

Cross-Sell Opportunities: Nexa provides visibility into water system performance, which naturally leads to recommendations for Watts products—creating a closed-loop sales channel.

-

Margin Expansion: Software carries higher gross margins than manufactured goods. As Nexa scales, it could meaningfully improve Watts's overall profitability.

With Nexa, many dangerous risks are minimized, including scalding, growth of legionella, and water leaks. Efficiency is optimized as facility managers or maintenance teams are armed with hard data for resource allocation and equipment performance. Even waste reduction is improved, enhancing a facility's sustainability.

VIII. Business Model Deep Dive: The "Boring" Brilliance

Revenue Mix & Geography

Watts operates through three geographic segments: - Americas: Approximately 73% of revenue - Europe: Approximately 22% of revenue - APMEA (Asia-Pacific, Middle East, Africa): Approximately 5% of revenue

By end market: - Approximately 65% Non-Residential (commercial, institutional, industrial) - Approximately 35% Residential

By channel: - Approximately 60% Repair & Replace - Approximately 40% New Construction

The Repair & Replace Moat

More than 70% of sales come from repair-and-replacement work, often mandated by changing building codes, safety regulations, or energy efficiency targets. This provides a base of recurring demand that has historically held up even during construction slowdowns.

This is the single most important fact about Watts's business model. The repair-and-replace dynamic creates something approaching annuity-like demand. Valves wear out. Codes change. Buildings age. New efficiency standards mandate upgrades. None of this depends on new construction activity.

Watts's business model includes a large repair/replace component, and the company has historically generated free cash flows that exceed 100% of its income.

Product Portfolio

Watts Water Technologies supplies systems, products and solutions that manage and conserve the flow of fluids and energy into, though, and out of buildings in the commercial, industrial, and residential markets. The company offers residential and commercial flow control and protection products, including backflow preventers, water pressure regulators, temperature and pressure relief valves, thermostatic mixing valves, leak detection and protection products, commercial washroom solutions, and emergency safety products and equipment for plumbing and hot water applications.

The breadth of the product portfolio is itself a competitive advantage. Engineers and contractors prefer dealing with fewer suppliers. Watts's comprehensive lineup—from rooftop drainage to basement valves—makes it a one-stop solution.

Switching Costs and Specification Power

Watts also benefits from being highly specified in projects. Engineers and contractors tend to standardize around its products, especially in institutional and commercial buildings where reliability is non-negotiable. Once specified, the switching costs are significant, not because of software, but because of risk and familiarity. Contractors know what works, and re-certifying a cheaper alternative isn't worth the liability.

This is a crucial insight. In building products, the spec sheet is everything. When an engineer specifies "Watts Series 009" backflow preventer, that's what gets installed. Contractors don't substitute cheaper alternatives because they bear the liability if something goes wrong.

Manufacturing Capabilities

Watts maintains vertically integrated manufacturing, including: - A state-of-the-art foundry dedicated exclusively to "lead-free" products under the U.S. Safe Drinking Water Act - Machining capabilities - Plastic extrusion - Injection molding - Assembly operations

Watts is vertically integrated to keep production near customers and reduce supply chain complexities.

Vertical integration provides quality control and flexibility—critical in a business where safety certifications and rapid product reformulations (such as the lead-free transition) can determine market position.

Distribution Strategy

Watts sells primarily through wholesale distributors and rep firms that serve contractors and engineers—not big-box retail. This keeps pricing rational and avoids margin pressure from channel conflict.

The company addresses a $20 billion total available market opportunity. End markets include: Residential, Multi-Family/Commercial, Institutional/Educational, Healthcare, Light/General Industrial, Hospitality - Hotel/Foodservice, Data Centers.

IX. Financial Performance & Capital Allocation

Record Results in 2024

Chief Executive Officer Robert J. Pagano Jr. commented, "We closed out 2024 with record results for the quarter and full year, including record operating income, adjusted earnings per share and full year sales."

Watts Water Technologies annual revenue for 2024 was $2.252B, a 9.53% increase from 2023. Watts Water Technologies annual revenue for 2023 was $2.056B, a 3.88% increase from 2022. Watts Water Technologies annual revenue for 2022 was $1.98B, a 9.41% increase from 2021.

Q3 2025 Performance

Watts Water Technologies reported third-quarter 2025 adjusted earnings per share (EPS) of $2.50 compared with $2.03 in the prior-year quarter. The company's quarterly net sales increased 13% year over year to $611.7 million. Organic sales were up 9% year over year due to favorable prices, volume and pull-forward demand.

Adjusted EBITDA was $128 million, with a margin of 20.9%, up 140 basis points. Year-to-date free cash flow was $216 million, compared to $204 million last year.

Margin Expansion Story

The margin expansion over the past decade has been remarkable. Management has consistently delivered operating leverage through: - Pricing power (safety-critical products command pricing authority) - Productivity initiatives (the "One Watts Performance System") - Mix shift toward higher-margin products - Acquisition synergies

This is a company that consistently turns modest revenue growth into outsized shareholder value, all while maintaining a balance sheet with minimal leverage and industry-leading returns on capital. Its core strength lies in doing one thing very well: providing water flow and safety solutions that are essential, regulated, and difficult to displace.

Balance Sheet Strength

The balance sheet remains strong. The quarter-end net debt-to-capitalization ratio was negative 15%, and net leverage is negative 0.5x. The solid cash flow and healthy balance sheet continue to give capital allocation optionality.

A negative net debt position is unusual for an industrial company pursuing acquisitions. It provides extraordinary flexibility—Watts can pursue opportunistic M&A without diluting shareholders or straining credit facilities.

Dividend Track Record

The company recently announced a quarterly dividend, which will be paid on December 15th. Stockholders of record on December 1st will be issued a dividend of $0.52 per share. This represents a $2.08 dividend on an annualized basis and a dividend yield of 0.8%. Watts Water Technologies's dividend payout ratio (DPR) is currently 21.47%.

The dividend yield is modest, but the payout ratio leaves ample room for continued increases while funding acquisitions and share repurchases.

2025 Outlook

Management remains cautiously optimistic about 2026 market conditions while acknowledging potential headwinds including tariff uncertainty, geopolitical challenges, and temporary margin dilution from the Haws acquisition. The company expects strong free cash flow in the fourth quarter and maintains its target of free cash flow conversion exceeding 100% of net income for the full year.

X. Competitive Positioning & Porter's 5 Forces Analysis

Industry Context

Watts's top 3 competitors are Pentair, Rheem, KSB SE Co KGaA. Pentair is the most similar to Watts. Rheem and KSB SE Co KGaA are also similar to Watts.

At approximately 25 times forward earnings, Watts Water trades at a notable premium to industrial peers like A. O. Smith (~20x), Pentair (~18x), and Xylem (~22x). On free cash flow, Watts is currently valued at approximately 23x, versus a 10-year average closer to 21x.

1. Threat of New Entrants: LOW

Several factors create substantial barriers to entry:

Regulatory Complexity: Safety valves and backflow preventers require extensive certifications (ASME, ANSI, CSA, UL, and various local code authorities). The certification process is expensive and time-consuming.

Specification Lock-In: Engineers specify products by brand name. Breaking into a market where "Watts" is synonymous with "T&P valve" requires years of relationship-building.

Manufacturing Scale: Vertical integration (including foundry operations) requires significant capital investment that new entrants may struggle to justify.

150 Years of Brand Equity: Watts's reputation has been built over a century and a half. That can't be replicated quickly.

2. Bargaining Power of Suppliers: LOW-MODERATE

Watts is vertically integrated to keep production near customers and reduce supply chain complexities.

The in-house foundry and manufacturing capabilities reduce dependency on external suppliers for critical components. For commodity inputs (brass, copper, plastics), Watts's scale provides negotiating leverage.

3. Bargaining Power of Buyers: LOW-MODERATE

Watts's customers are primarily wholesale distributors and contractors, not end consumers. Several factors limit buyer power:

- Products are specified by engineers and required by code—not discretionary purchases

- Quality failure risk (explosions, water damage, liability) discourages price-shopping

- Fragmented customer base (no single customer represents dominant volume)

4. Threat of Substitutes: VERY LOW

For code-mandated safety equipment, there are no functional substitutes. Buildings must have T&P valves, backflow preventers, and pressure regulators to pass inspection. The technology may evolve (smart valves vs. mechanical valves), but the product categories themselves are irreplaceable.

Watts operates in a highly regulated, non-cyclical water infrastructure segment with high barriers to entry and strong replacement demand.

5. Competitive Rivalry: MODERATE

The competitive landscape includes both global conglomerates and regional specialists. Major players include: - Pentair (most direct competitor) - Xylem - A. O. Smith - KSB SE - Mueller Water Products - Badger Meter

However, rivalry is moderated by: - Product differentiation through specification and brand reputation - Focus on different end markets and geographies - Rational pricing (no race to the bottom) - Growth through M&A rather than price wars

Hamilton Helmer's 7 Powers Framework

Applying Helmer's framework reveals several sources of durable competitive advantage:

Counter-Positioning: Watts's focus on code-specified safety products creates a business model that larger, more diversified competitors struggle to match. General industrial companies can't commit the same resources to regulatory relationships and specialized engineering.

Switching Costs: Once Watts products are specified and installed, switching is costly (re-engineering, re-certification, contractor retraining, liability risk).

Scale Economies: Watts's volume in core product categories (T&P valves, backflow preventers) provides manufacturing cost advantages that smaller competitors can't match.

Branding: In commercial/institutional markets, "Watts" carries trust that translates to specification preference.

Cornered Resource: The company's 150-year repository of engineering knowledge, patents, and regulatory relationships represents an intangible asset that competitors cannot simply buy.

XI. Key Risks and Investment Considerations

Macroeconomic Exposure

While repair-and-replace business provides stability, about 60% of Watts' business has historically been in less-cyclical repair/replace, but construction activity (residential and non-residential) has long been a key growth driver.

The 40% exposure to new construction makes Watts somewhat cyclical. A severe construction downturn would pressure revenue growth, though margins could hold up better than peers due to the repair-and-replace base.

European Market Weakness

Europe showed 15% organic decline due to OEM heat pump destocking and weak macros.

The European business has been a drag, particularly in heating OEM channels. Heat pump market volatility and European economic weakness present ongoing headwinds.

Tariff Risk

The earnings call transcript revealed that tariff impacts are estimated at $40 million for 2025, representing a significant challenge that management is working to mitigate.

Tariff uncertainty creates margin pressure and supply chain complexity. While Watts's domestic manufacturing provides some insulation, component sourcing remains exposed to trade policy.

Integration Risk

M&A dilution, if future acquisitions stretch the company's balance sheet or distract from core integration strengths.

The aggressive acquisition pace creates execution risk. Each acquisition brings integration challenges—systems, cultures, sales forces, supply chains. The company has historically integrated acquisitions well, but capacity constraints exist.

Valuation Premium

Despite a near fivefold stock price increase over the past decade, Watts Water's valuation multiples have remained surprisingly steady. Its forward P/E ratio currently hovers around 22x, just modestly above its 10-year median of 20x.

The premium valuation leaves limited margin for error. If organic growth disappoints or margin expansion stalls, multiple compression could amplify downside.

XII. Key Metrics to Track

For long-term investors, three metrics best capture Watts's ongoing performance:

1. Organic Revenue Growth

Strips out acquisition effects and currency to reveal underlying demand trends. Watch for: - Americas organic growth (largest segment, should lead) - Repair/replace vs. new construction mix - Price vs. volume contribution

2. Adjusted Operating Margin

The margin expansion story has been central to Watts's value creation. Tracking margin trajectory (including acquisition dilution and recovery) reveals execution quality.

3. Free Cash Flow Conversion

Watts's business model includes a large repair/replace component, and the company has historically generated free cash flows that exceed 100% of its income.

Cash conversion greater than 100% of net income indicates high-quality earnings and minimal working capital drag—essential for an acquisition-driven strategy.

XIII. The Investment Case: Bull vs. Bear

Bull Case

Secular Tailwinds: Aging water infrastructure, tightening safety codes, efficiency mandates, and water scarcity concerns create multi-decade demand tailwinds.

With global tailwinds in water infrastructure upgrades, decarbonization efforts, and tightening safety codes, Watts is positioned to benefit from both replacement cycles and regulatory-driven demand, without needing to stretch its capital base.

Digital Optionality: Nexa represents a potentially transformative shift to recurring SaaS revenue. Even modest success could meaningfully improve growth and margin profile.

Disciplined Capital Allocation: Strong balance sheet, smart acquisitions at reasonable multiples, and shareholder-friendly return policy.

Management Tenure: Pagano's 11+ year tenure provides continuity and institutional knowledge. The management team has successfully navigated multiple cycles.

Bear Case

Premium Valuation: At ~25x forward earnings, Watts trades at a notable premium to peers. Any stumble in execution could trigger multiple compression.

European Drag: The European segment faces structural challenges (heat pump market volatility, economic weakness) that may persist.

Tariff Uncertainty: Trade policy creates ongoing cost and supply chain uncertainty.

Integration Execution: The pace of acquisitions (Bradley, Josam, I-CON, EasyWater, Superior Boiler, Haws) creates integration bandwidth risk.

Myth vs. Reality

Myth: "Watts is just a boring valve company." Reality: Watts is a compounding machine with 70%+ repair/replace revenue, premium margins, and a digital transformation underway.

Myth: "Industrial companies can't sustain premium multiples." Reality: The company's valuation may seem elevated on a headline EV/EBITDA basis, but when considered alongside its near-perfect FCF conversion, superior ROIC, and low net debt, the premium reflects genuine quality.

Myth: "The water infrastructure thesis is priced in." Reality: Water infrastructure spending is a multi-decade cycle. Deferred maintenance, lead pipe replacement, and efficiency mandates create demand that hasn't fully materialized.

XIV. Conclusion: 150 Years and Counting

When Tim Horne addressed the 150th anniversary gathering in August 2024, he was speaking about more than corporate longevity. He was describing a particular kind of American business story—an immigrant founder, a family that stewarded the business for three generations, a successful transition to professional management, and a culture that prioritizes long-term value creation over short-term metrics.

CEO Bob Pagano observed at the anniversary: "I'm proud to be here today to celebrate our 150th – not many companies can say they've been around 150 years. 150 years — you have to adapt, you have to change, you have to do things differently. And Watts has done that."

The story of Watts Water Technologies offers several lessons for long-term investors:

First, solving safety problems creates durable demand. Joseph Watts built a business on preventing explosions; his successors extended that franchise to every critical water safety application in modern buildings.

Second, regulatory relationships compound over time. Burchard Horne's decision to educate regulators about T&P valves in the 1920s created a moat that competitors still haven't breached.

Third, repair-and-replace business models outperform across cycles. The 60-70% of Watts revenue tied to mandated maintenance and replacement provides ballast during construction downturns.

Fourth, family businesses can successfully transition to professional management—if the culture and incentives are right. Tim Horne's continued involvement as a major shareholder and Director Emeritus provides continuity while allowing professional managers to execute.

Fifth, boring businesses can be exceptional investments. Watts doesn't make headlines. Its products are hidden behind walls and under floors. But over 150 years, it has compounded wealth for shareholders while protecting millions of people from the dangers of uncontrolled water pressure and temperature.

As CEO Pagano frames it: "Everything we design is made to keep the Earth's most precious resource safer, cleaner, and more useful for our customers."

For investors seeking a durable industrial compounder with proven capital stewardship and niche dominance, Watts Water Technologies offers a quiet but compelling case—150 years of evidence that boring brilliance compounds.

Material Considerations: Investors should note that Tim Horne remains a significant shareholder with approximately 17.9% ownership. The dual-class stock structure concentrates voting control. European segment performance remains challenged. Tariff impacts for 2025 are estimated at $40 million. Recent acquisitions (Haws, Superior Boiler, EasyWater) will be dilutive to margins in year one as integration progresses.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube