FTAI Aviation: How an Asset-Light Upstart is Eating the Engine Giants' Lunch

I. Introduction: The Engine Aftermarket Revolution

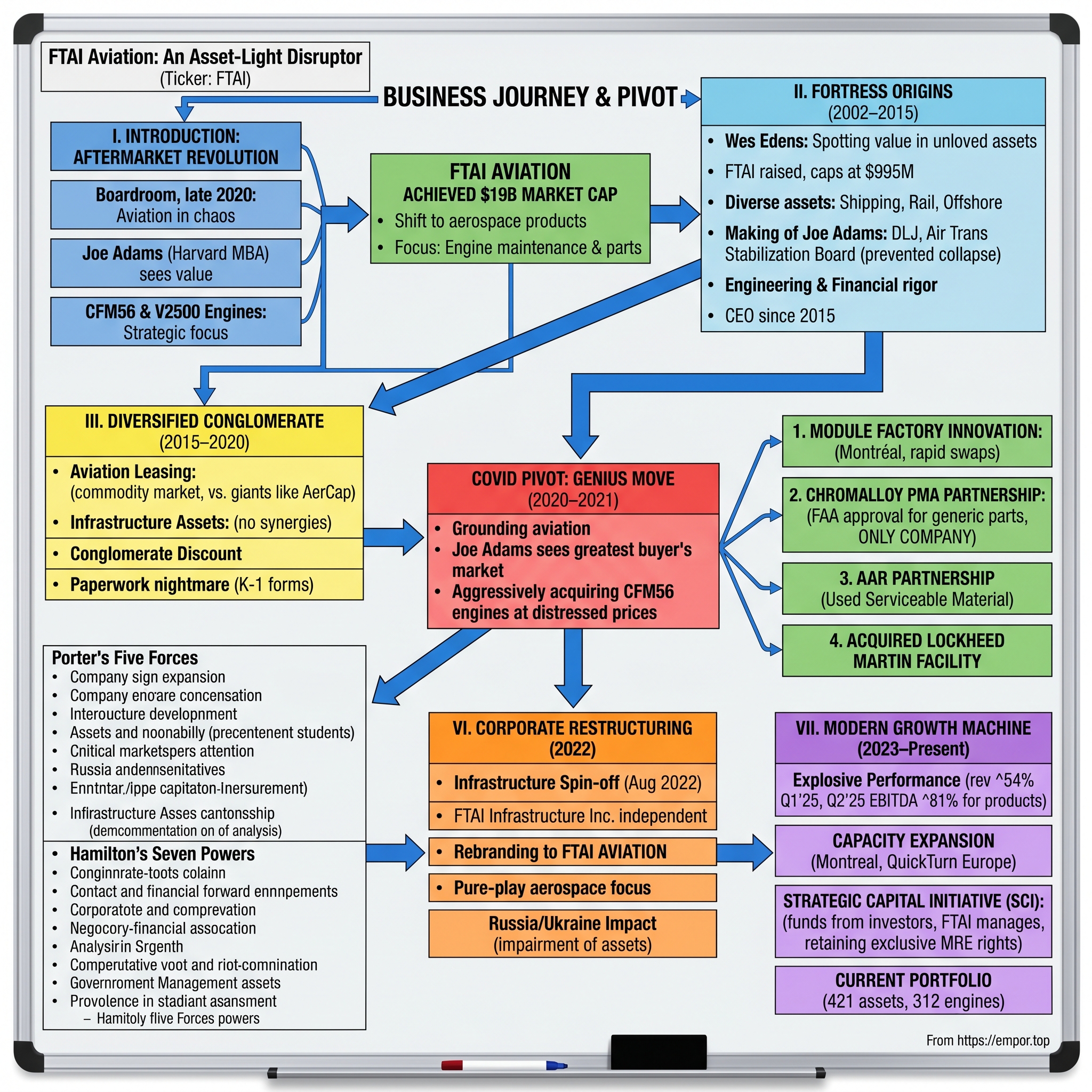

Picture a boardroom in Midtown Manhattan, sometime in late 2020. Aviation had just lived through its darkest chapter since the Wright Brothers first took flight. Airlines were parking fleets by the hundreds, engine values were cratering, and industry veterans were writing obituaries for narrow-body travel. Into this chaos walked Joe Adams, the Harvard MBA turned transportation dealmaker who had spent two decades learning to see value where others saw wreckage.

FTAI Aviation Ltd. manages to achieve a $19 billion market capitalization while fundamentally shifting its core business model. As of late 2025, their trailing twelve-month revenue hit $2.34 billion, driven by a strategic pivot from a traditional lessor to a high-value aerospace products and services provider, focusing on engine maintenance and parts.

What Adams and his team at Fortress-backed FTAI recognized was something hiding in plain sight: FTAI owns and maintains commercial jet engines with a focus on the Maintenance, Repair, and Exchange (MRE) of CFM56 and V2500 engines. FTAI's proprietary portfolio of products, including the Module Factory and a joint venture to manufacture engine PMA, helps make CFM56 and V2500 engine maintenance simpler, more cost-effective, significantly faster, and more environmentally friendly.

The CFM56—that workhorse engine powering Boeing 737s and Airbus A320s—wasn't dying. It was entering its most profitable phase. As of May 2021, around 16,000 CFM56 engines were in service, according to CFM International. Nearly all of these are the -5B and -7B variants. With new aircraft delivery delays at Boeing and Airbus pushing airlines to fly their existing fleets longer than planned, the demand for engine maintenance was about to surge to unprecedented levels.

This is the story of how a diversified infrastructure investor executed one of the most audacious pivots in modern aerospace history—transforming from a hodgepodge of ports, rails, and leased aircraft into a vertically integrated engine maintenance powerhouse now targeting 25% market share of a $22 billion market.

II. The Fortress Investment Group Origin Story (2002–2015)

To understand FTAI, one must first understand the crucible that forged it: Fortress Investment Group, the alternative asset manager that rewrote the rules on how to monetize complex, capital-intensive transportation assets.

Fortress Investment Group was founded in 1998 by three individuals: Randal Nardone, Wes Edens, and Pete Briger. The company started as a small investment firm, but it quickly grew and expanded its services over the years. Fortress Investment Group is headquartered in New York City and has a significant presence in the global financial markets.

The company was formed by Wes Edens. Edens, a former Lehman Brothers executive with a preternatural ability to spot value in unloved asset classes, built Fortress around a simple thesis: transportation and infrastructure assets generate predictable cash flows that Wall Street systematically undervalues because they require operational expertise to manage.

Fortress Investment Group announced the successful close of Fortress Worldwide Transportation and Infrastructure Investors ("FTAI") at its cap of $995 million in total commitments. FTAI was originally raised as a $395 million fund; this was followed by a subsequent "top up" private capital raise of $600 million of additional capital commitments.

FTAI brings together a diverse mix of high yielding transportation assets and value-add infrastructure projects. Its portfolio includes aviation, shipping, offshore energy and rail assets and infrastructure, including airplanes, jet engines, shipping containers, intermodal equipment, offshore energy vessels, as well as railway lines, railcars and terminals.

The Making of Joe Adams

The architect of FTAI's transformation came from an unusual background that uniquely prepared him for the challenge ahead. Previously, Mr. Adams was a partner at Brera Capital Partners and at Donaldson, Lufkin & Jenrette where he was in the transportation industry group. In 2002, Mr. Adams served as the first Executive Director of the Air Transportation Stabilization Board.

That last credential deserves particular attention. In the aftermath of September 11, 2001, the U.S. government created the Air Transportation Stabilization Board to prevent the collapse of the American airline industry. Adams, then a relatively young transportation banker, was tapped to lead the effort to evaluate airline loan guarantees—giving him a front-row seat to aviation's darkest hour and, more importantly, to its eventual recovery.

Mr. Adams received a B.S. in Engineering from the University of Cincinnati and an M.B.A. from Harvard Business School. This combination—engineering rigor plus financial sophistication plus firsthand crisis management experience—would prove essential in the years ahead.

Joseph P. Adams, Jr. has an extensive background in leading FTAI, serving as CEO since May 2015 and taking on the role of Chairman in May 2016. Until May 2024, he was a member of the Management Committee of Fortress and a Managing Director at Fortress within the Private Equity Group. He has served as a member of the board of directors of Seacastle, Inc., SeaCube Container Leasing Ltd., Aircastle Limited and RailAmerica Inc.

The pattern here is instructive: Adams had spent years learning how to create value in transportation equipment leasing across multiple asset classes. He understood that the real money in transportation isn't just in owning assets—it's in the services and maintenance that extend their productive lives.

The business was established in 2011 as a vehicle to own and acquire a diversified portfolio of infrastructure and transportation assets. The original location was New York, NY, operating under the umbrella of Fortress Investment Group.

When FTAI went public in May 2015, it presented itself as a diversified play on transportation infrastructure—an approach that would prove both a blessing and a curse in the years to come.

III. The Diversified Conglomerate Era: Aviation + Infrastructure (2015–2020)

For five years after its IPO, FTAI existed as a curious hybrid that frustrated investors seeking clean sector exposure. Currently, the company has infrastructure assets and aviation assets. Infrastructure has nothing to do with aviation and there are no synergies between the business units.

FTAI Aviation (formerly Fortress Transportation & Infrastructure Investors) is a global investment management firm providing commercial jet engine and aircraft leasing services.

The aviation leasing business operated in a commodity market dominated by giants. Peers, AerCap Holdings (AER) and Air Lease (AL) trade at 9.3x 2023 EBITDA and 7.9x EBITDA, respectively.

AerCap became the largest aviation leasing company in the world following the acquisition of ILFC in 2014, and GECAS from GE in 2021, for over $30 billion. Against these behemoths, FTAI's aviation leasing operation was a relative minnow.

The infrastructure holdings were equally diverse: railroads serving U.S. Steel's production facilities, the Jefferson Terminal energy storage complex, the Long Ridge energy terminal that was pioneering hydrogen blending. Each asset was interesting in isolation but collectively created a conglomerate discount that plagued the stock.

Honestly, understanding the history means understanding the dual-track strategy—infrastructure and equipment leasing—that eventually split to maximize shareholder value.

There was another problem: K-1 tax forms. Because of its partnership structure, FTAI distributed K-1s to shareholders—a paperwork nightmare that excluded the company from many index funds and discouraged retail ownership. The stock languished.

But beneath the surface, something important was happening. Adams and his team were accumulating engines, specifically CFM56 engines—not randomly, but with a strategic intent that would become clear only after COVID struck.

IV. Understanding the CFM56 Engine Ecosystem

To appreciate FTAI's strategic genius, one must understand the extraordinary asset at the heart of its business: the CFM56 engine, perhaps the most successful commercial aviation product ever created.

CFM International was founded in 1974 to build and support the CFM56 series of turbofan engines. CFM is the world's largest commercial aircraft engine manufacturer, with a 39% market share as of 2020. It has delivered more than 37,500 of its engines to more than 570 operators.

The Improbable Alliance

The CFM56's origin story reads like a Cold War thriller. GE Aerospace and Safran Aircraft Engines have to overcome numerous hurdles before sealing the deal. The U.S. government initially rejects GE's application to export its F101 engine core for joint commercial development with Safran Aircraft Engines, because the engine powers the U.S. Air Force B-1 bomber.

Ultimately, with support from U.S. President Richard Nixon, the government relents, and in 1974 GE Aerospace and Safran Aircraft Engines sign the agreement that formally establishes CFM International as a joint 50-50 company charged with developing and selling the CFM56 engine family.

The two companies share design, development and production equally. Final assembly, sales and services are handled by each partner using its own resources.

On January 24, 1974, as part of the development of the CFM56, Snecma and General Electric signed the final agreement governing the proposed joint venture. Although the company was already up and running, a number of legal and administrative formalities delayed its legal incorporation until September 1974. Named CFM International, this company under French law, with capital of 400,000 francs, created in equal shares by Snecma and General Electric, was responsible for managing the program and marketing the engines.

The engine initially had extremely slow sales but has gone on to become the most used turbofan aircraft engine in the world. The CFM56 first ran in 1974.

The Razor-Blade Model

Understanding GE and Safran's business model is essential to understanding why FTAI's strategy works. Like Gillette selling razors cheaply and making profits on blades, CFM International makes relatively modest margins on new engine sales but earns extraordinary returns on aftermarket parts and services over each engine's 30+ year lifespan.

HPT blades are GE's cash cow: at 80%+ gross margin, 80 blades per engine and a catalog part price of ~$25,000 per unit, airlines spend ~$2m per heavy shop visit to replace all blades. This amounts to ~30% of a total $7m engine overhaul cost.

This economics created both the opportunity and the moat for FTAI's strategy. Every CFM56 engine will need multiple shop visits over its lifetime, and each visit generates millions in parts revenue for whoever controls the supply chain.

In 2021, maintenance on the engine is valued at around $21 billion, accounting for 70% of overall engine MRO spending this year. This will climb gradually before peaking in 2024 at $24.5 billion before the impact of Leap service entries will reduce MRO spending on the CFM56.

The Long Runway Ahead

Heavy shop visits for CFM International's workhorse CFM56 engines are on track to peak as early as 2025, helping push already lucrative aftermarket revenues for GE Aerospace and Safran even higher and spawn creative approaches to keeping the engines in service.

With more than 24,000 CFM56 engines in operation, at least 11,000 have not had their shop visits yet, according to Roke.

This timing proved critical. The CFM56 installed base was enormous, many engines were approaching major shop visits, and Boeing and Airbus production problems meant airlines would need to fly these older aircraft longer than planned. The window for a disruptive new entrant was opening.

V. The COVID Pivot: The Genius Move That Changed Everything (2020–2021)

When COVID-19 grounded global aviation in March 2020, most industry observers saw only catastrophe. Joe Adams saw something else: the greatest buyer's market for CFM56 engines in history.

The Crisis as Opportunity

Airlines desperately needed cash. Asset values were collapsing. Lessors were panicking. And FTAI, backed by Fortress's deep pockets, had firepower to deploy.

The company began aggressively acquiring CFM56 engines at distressed prices—not merely to expand its leasing book, but to execute a radically different vision. Rather than simply own and lease engines, FTAI would control the entire aftermarket value chain: parts supply, maintenance, module production, and exchange services.

Since inception of The Module Factory operations in June of 2021, FTAI Aviation has completed or contracted for sale over 200 module sales or swaps with over 20 new customers.

The Module Factory Innovation

The key insight was conceptual: engines aren't monolithic objects—they're assemblies of modules. The core section, fan module, low-pressure turbine, and high-pressure turbine can each be repaired or replaced independently. Traditional MRO shops required airlines to surrender their entire engine for weeks while all work was completed sequentially.

LMCES operates a 526,000 ft² aircraft engine maintenance and repair facility in Montréal, Quebec, with extensive capabilities in engine and piece-part repairs for CFM56 engines. FTAI, as LMCES's largest customer, partnered with LMCES in 2020 to establish The Module Factory™ at this site to distribute CFM56 modules globally. The facility can handle up to 900 CFM56 modules annually and features three on-site test cells.

FTAI's Module Factory model turned this on its head: maintain inventory of ready-to-install modules, swap them rapidly when airlines bring in engines, then repair the removed modules offline. Turnaround times dropped from weeks to days.

The Chromalloy PMA Partnership

But FTAI's most brilliant move came earlier, and its importance only became apparent during COVID. In 2021, FTAI Aviation, the $17bn market cap aircraft engine lessor and maintenance provider, partnered with Chromalloy, the leading engine DER Repair and PMA player globally, to design and approve CFM-56 hot section PMAs. Last month, Chromalloy received FAA-approval for a HPT Stage 1 vane PMA.

PMA—Parts Manufacturer Approval—is the FAA certification that allows third parties to manufacture replacement parts for aircraft engines without OEM authorization. It's aviation's equivalent of generic drugs: same functionality, fraction of the price.

This partnership cannot be understated, given Chromalloy is the ONLY company to receive FAA parts manufacture approval extending to both: low pressure turbine blades (approved in 2021) and high pressure turbine blades (approved in 2024).

A key differentiator for FTAI is its exclusive PMA joint venture with Chromalloy, the only company with FAA approval for manufacturing both low-pressure and high-pressure turbine blades. This partnership allows FTAI to source PMA parts at a 60-70% discount compared to OEMs while capturing a significant portion of cost savings.

The stringent FAA certification process, which takes 3-5 years per part, creates a significant barrier to entry for competitors.

Over time, the company expects to earn $1m EBITDA per module, of which 50% is driven by its Chromalloy PMAs.

The AAR Partnership

The final piece of the puzzle was used serviceable material (USM)—parts harvested from engines being retired or torn down. AAR and Fortress Transportation and Infrastructure Investors announced an agreement to create Serviceable Engine Products, an exclusive seven-year CFM56 used serviceable material ("USM") partnership.

AAR CORP. has signed an extension of its exclusive Serviceable Engine Products agreement for the CFM56 used serviceable material ("USM") collaboration with FTAI Aviation Ltd. through 2030. The collaboration has made USM inventory available to the global aviation aftermarket and FTAI's consumption at the Module Factory™, a dedicated commercial maintenance center focused on modular repair and refurbishment of CFM56-7B and CFM56-5B engines. Through its worldwide network, AAR will manage the teardown, repair, marketing, and sales of spare parts from FTAI's CFM56 engine pool totaling over 450 engines and growing.

Together, these partnerships gave FTAI structural cost advantages that no competitor could easily replicate: exclusive access to the cheapest PMA parts, a steady supply of USM from its own growing engine pool, and the operational capability to combine these inputs into modules delivered faster than anyone else in the market.

VI. Corporate Restructuring: The 2022 Transformation

By 2022, the strategic vision was clear, but FTAI's corporate structure remained a muddle. The infrastructure assets—however valuable—were distracting investors from the aerospace transformation underway. The solution: spin them off.

The Infrastructure Spin-off

Fortress Transportation and Infrastructure Investors LLC announced today that it has successfully completed the spin-off of FTAI Infrastructure Inc. ("FTAI Infrastructure") on August 1, 2022.

The spin-off will establish FTAI's infrastructure business as an independent, publicly traded company called FTAI Infrastructure Inc. ("FTAI Infrastructure"). As currently scheduled, the distribution is expected to occur on August 1, 2022 and the record date is July 21, 2022. So close of business this Thursday, is the cutoff for buying FTAI in order to receive the spin-out as a distribution.

The rationale was straightforward: pure-play companies trade at higher multiples than conglomerates, and FTAI's aerospace story was now compelling enough to stand on its own.

Russia/Ukraine Impact

The restructuring came amid geopolitical chaos. FTAI wrote off $195mm for impairments, bad debt and lost revenue for the Russia/Ukraine war and currently expects to recapture such amounts in full from insurance proceeds, gains from asset sales, and receivable repayments.

As of December 31, 2022, in our Aviation Leasing segment, we own and manage 330 aviation assets, consisting of 106 commercial aircraft and 224 engines, including four aircraft and one engine that were still located in Ukraine and eight aircraft and seventeen engines that were still located in Russia.

The Russian asset losses were painful but manageable. More importantly, they illustrated the risks inherent in pure-play leasing—and thus strengthened the case for FTAI's pivot toward asset-light maintenance services.

The FTAI Aviation Rebranding

On 09-Nov-2022, FTAI announced its shareholders voted to approve and adopt a merger agreement between FTAI, FTAI Finance Holdco and FTAI Aviation Merger Sub. FTAI closed the merger on 11-Nov-2022. Fortress Transportation and Infrastructure Investors became a subsidiary of FTAI Aviation and the company was renamed FTAI Aviation following completion of the merger.

The rebranding marked more than a name change. It signaled to the market that FTAI was now, definitively, an aerospace company—one with a differentiated strategy that would soon begin generating extraordinary returns.

VII. The Modern Growth Machine (2023–Present)

The proof of FTAI's strategy came in its financial results, which have been nothing short of remarkable.

Explosive Financial Performance

FTAI Aviation reported strong Q4 and full year 2024 results, declaring a quarterly dividend of $0.30 per ordinary share. The company achieved significant growth in Aerospace Products, with net income of $346 million for fiscal year 2024, representing a 92% year-over-year increase, while Adjusted EBITDA grew 138%.

The company reported a significant year-over-year revenue increase of 54% in the first quarter of 2025, reaching $502 million.

"Our Aerospace Products segment continued to perform, with 81% year-over-year growth in Adjusted EBITDA in Q2 2025 and an increase in market share to approximately 9% on an annualized basis, up from 5% last year."

Continued growth in Aerospace Products segment with Adjusted EBITDA of $180.4 million, an increase of 77% versus Q3 2024.

The numbers tell a story of a company firing on all cylinders. Revenue growth of 40-50% annually, EBITDA margins expanding, and market share climbing relentlessly.

Capacity Expansion

FTAI Aviation announces the successful completion of its acquisition of Lockheed Martin Commercial Engine Solutions ("LMCES"), a 526,000-square-foot aircraft engine maintenance repair facility located in Montréal, Québec, from Lockheed Martin Canada. The completion of the acquisition strengthens FTAI Aviation's Maintenance, Repair, and Exchange (MRE) business with the ability to provide additional maintenance services to airline customers. The integration of LMCES' maintenance capabilities with FTAI's current maintenance capabilities at QuickTurn, in Miami, Florida, gives FTAI capacity to perform up to 1,350 CFM56 module overhauls and over 500 engine tests annually.

FTAI Aviation announced that it has closed its previously announced acquisition of a 50% ownership stake in IAG Engine Center Europe S.r.l. ("IAG Engine Center"), an Italian company operating a 200,000 square-foot CFM56 engine maintenance repair and overhaul facility located at the Rome Fiumicino Airport, which has been rebranded Quick Turn Engine Center Europe S.r.l., or "QuickTurn Europe."

In total, the joint venture operating at full capacity is expected to add capacity to maintain 450 modules (150 engines) per year, bringing FTAI's maintenance capacity to 1,800 CFM56 modules (600 engines) and over 600 engine tests annually.

FTAI now operates a global network of maintenance facilities: Miami, Montréal, and Rome—strategic locations serving North America, Europe, and providing connectivity to global airlines.

The Strategic Capital Initiative

Perhaps FTAI's most innovative recent move is its Strategic Capital Initiative (SCI), which transforms the company's relationship with capital markets.

The first vehicle under the initiative expects to deploy more than $4 billion of total capital into on-lease 737NG and A320ceo aircraft, allowing FTAI to maintain an asset-light business model while the partnership focuses on being a leading, scaled investor in the largest segment of the narrowbody aircraft market.

The engines owned by the partnership will be powered exclusively via engine and module exchanges with FTAI's Maintenance, Repair and Exchange ("MRE") business.

Completed fundraising for inaugural Strategic Capital Initiative partnership with $2 billion of equity commitments, targeting to deploy over $6 billion of capital including current and future debt financing.

The SCI is elegant financial engineering: third-party institutional investors provide capital to buy aircraft, FTAI manages the assets and retains exclusive rights to service the engines. FTAI gets the recurring MRE revenue stream without the balance sheet drag of owning the aircraft outright.

Current Portfolio and Guidance

As of December 31, 2024, this segment owned and managed 421 aviation assets consisting of 109 commercial aircraft and 312 engines, including eight aircraft and seventeen engines in Russia.

FTAI continues to expect 2025 Adjusted EBITDA of approximately $1.1 to $1.15 billion from its reportable segments, comprised of approximately $500 million from Aviation Leasing and approximately $600 to $650 million from Aerospace Products. 2025 Adjusted EBITDA guidance reflects the following assumptions: (i) an average of 100 modules per quarter produced at the Company's Montreal facility in fiscal year 2025, (ii) net Aerospace margins in line with or better than those for fiscal year 2024, and (iii) 25 to 35 V2500 engine MRE transactions for fiscal year 2025.

Raised guidance for 2026 Adjusted EBITDA from $1.4 billion to $1.525 billion from its reportable segments, comprised of approximately $1.0 billion from Aerospace Products and $525 million from Aviation Leasing.

The trajectory is unmistakable: Aerospace Products is becoming the dominant driver of FTAI's value, with leasing transitioning to a supporting role that feeds engines into the MRE system.

VIII. Porter's Five Forces Analysis

Understanding FTAI's competitive position requires examining the structural forces shaping its industry.

1. Threat of New Entrants: LOW

FTAI's business model is extraordinarily difficult to replicate. Consider the barriers:

Capital Requirements: Building a portfolio of hundreds of CFM56 engines requires billions of dollars in capital. FTAI accumulated its position opportunistically during COVID at prices that are no longer available.

FAA Certification: The stringent FAA certification process, which takes 3-5 years per part, creates a significant barrier to entry for competitors. Chromalloy's PMA approvals took years to secure and are exclusive to FTAI for the CFM56.

Operational Expertise: Running an MRO facility requires specialized technical knowledge, trained personnel, and institutional know-how that takes years to develop.

Relationship Networks: FTAI has built relationships with over 100 airline and lessor customers. These relationships are sticky—airlines don't switch maintenance providers lightly.

2. Bargaining Power of Suppliers: MODERATE

The primary supplier concern is the OEMs themselves. GE and Safran control the supply of new parts and could theoretically make life difficult for FTAI.

However, FTAI has systematically reduced this dependency:

The company has a joint venture with manufacturer Chromalloy to supply CFM International CFM56 PMA parts at discounted rates to support FTAI's engine shops. FTAI also receives a share of parts sold to third parties.

The USM partnership with AAR provides another parts source independent of OEM control. And FTAI's own engine teardowns generate additional material.

3. Bargaining Power of Buyers: MODERATE

Airlines are cost-conscious and have options for engine maintenance. However, several factors strengthen FTAI's position:

The ongoing production constraints at Boeing and Airbus have created a supply-demand imbalance, making airlines more dependent on MRO services as they struggle to source new engines. This has provided FTAI with significant pricing power, enabling it to pass on cost increases from OEMs while maintaining strong margins.

The Module Factory's speed advantage—turning around engines in days rather than weeks—provides value that airlines willingly pay for. Time on wing translates directly to revenue for airlines.

4. Threat of Substitutes: LOW (Short-term) / MODERATE (Long-term)

In the short term, there is no substitute for maintaining existing CFM56 engines. Airlines must either maintain them, retire them, or replace them with new aircraft.

Additionally, the potential expansion of FAA-approved Parts Manufacture Approval (PMA) could further enhance profitability.

The longer-term risk is technological obsolescence as newer LEAP engines gradually replace the CFM56 fleet. However, this transition will take 15-20 years, and Boeing/Airbus delivery delays are extending CFM56 relevance.

CFM56 engines power more than 14,650 commercial and military aircraft across more than 650 operators and are the industry leader in terms of reliability and durability. As the fleet reaches eight years in service, LEAP engines power more than 3,500 aircraft for nearly 160 operators.

5. Competitive Rivalry: HIGH but CHANGING

Traditional competitors include OEM shops (GE, Safran) and independent MROs (MTU, Lufthansa Technik). Competitors in FTAI's space include traditional aircraft lessors like AerCap and Willis Lease Finance. However, FTAI's integrated model and focus on aerospace products set it apart from pure-play lessors.

Before COVID-19 in 2019, CFM estimated more than 40 shops—including third-party providers, along with the MRO units of GE Aviation and Safran—provided CFM56 engine overhauls. The OEM estimated that about two-thirds of worldwide shop visits are being completed by non-CFM shops.

FTAI's vertically integrated model—combining engine ownership, module manufacturing, PMA parts, and USM supply—creates cost advantages that traditional MRO providers cannot easily match.

IX. Hamilton's Seven Powers Analysis

1. Scale Economies: STRONG

FTAI is now one of the largest owners of CFM56 engines globally. This scale drives advantages:

- More engines = more teardown material = lower parts costs

- Higher module production volumes = better facility utilization

- Greater bargaining power with suppliers and customers

The company produced 207 CFM56 modules in Q3 2025 and remains on track to meet its annual target of 750 modules in 2025, with plans to increase production to 1,000 modules in 2026.

2. Network Effects: MODERATE

The SCI creates a powerful flywheel: third-party capital acquires aircraft → engines flow to FTAI MRE → MRE revenue finances more capacity → more capacity attracts more customers → more customers attract more third-party capital.

All engines in the SCI portfolio are serviced via FTAI's proprietary module exchange system, which reduces downtime and costs for lessees. This creates a flywheel effect: leasing cash flows fund MRO expansion, which in turn drives higher margins and reinvestment in the SCI pipeline.

3. Counter-Positioning: VERY STRONG

This is FTAI's most powerful strategic asset. Consider the OEMs' dilemma:

CFM is very nervous about this because they know their HPT blades are overpriced, but they don't want to accept it.

GE and Safran earn 80%+ gross margins on aftermarket parts. If they match FTAI's pricing, they devastate their most profitable business line. If they don't match, they cede market share to FTAI. This is the classic counter-positioning trap: the incumbent's most rational response is to let the disruptor win.

FTAI Aviation, the lessor-turned-MRO-provider, is one of the world's largest owners of CFM56 engines yet it cannot attend conferences of its engine manufacturer. This is because FTAI is creating a PMA for CFM's cash cow: the high-pressure turbine (HPT) blade.

4. Switching Costs: MODERATE

Once an airline establishes a relationship with FTAI and integrates its module exchange system into operations, switching costs emerge. Technical data, procedures, and relationships all create friction.

5. Branding: LOW

FTAI is not a consumer brand. However, reputation for reliability and speed matters significantly to airline maintenance executives.

6. Cornered Resource: STRONG

FTAI has an exclusive joint venture, for Parts Manufacture Approval (PMA) with Chromalloy, an aftermarket parts manufacturer. FTAI is able to source aftermarket parts ~60-70% cheaper than OEM's, in exchange for 25% of their sourced profit to third parties. FTAI also receives exclusive access to FAA approved modules, which Chromalloy will supply and manufacture.

The Chromalloy partnership is a cornered resource—an exclusive relationship that competitors cannot replicate.

7. Process Power: EMERGING

The Module Factory represents a genuinely innovative process for engine maintenance. As FTAI scales and refines operations, this process advantage should compound.

X. The Muddy Waters Challenge

In January 2025, FTAI faced its most significant test when short-seller Muddy Waters Research published a scathing report.

Muddy Waters is short FTAI Aviation Ltd. (FTAI US) because its financial reporting is highly misleading. We believe revenue from true maintenance and individual off-the-rack module sales are materially lower than reported.

Muddy Waters Research has published a report alleging that FTAI Aviation Ltd. is manipulating its financials by misrepresenting revenue from whole engine sales as Maintenance Repair & Overhaul (MRO) revenue, inflating EBITDA margins through over-depreciation, and engaging in channel stuffing. The report claims that approximately 80% of FTAI's Aerospace Products adjusted EBITDA is derived from gains on whole engine sales, rather than true maintenance work.

The news caused a significant decline in the price of FTAI Aviation stock. On January 15, 2025, the price of the company's stock fell 24%, from a closing price of $153.29 per share on January 14, 2025, to $116.08 per share on January 15.

FTAI's response was forceful. Adams said the company "strongly disagree with the assertions made in the report." He said the report "mischaracterises" FTAI, stating the claims were "misrepresentations".

FTAI Aviation announced that its Board of Directors' Audit Committee has completed an independent review of allegations made in short seller reports from January 2025. The review, conducted by independent legal and forensic accounting advisors, concluded that the allegations against the company were unsupported and without merit. The Audit Committee Chair, Paul R. Goodwin, emphasized their commitment to maintaining high standards of corporate governance, internal compliance, and financial reporting controls.

FTAI has maintained the same auditor since 2015, Ernst and Young. Not only are they very well respected, but have doubled down, re-affirming the 11-13% depreciation schedule of their short-lived assets.

The stock eventually recovered as subsequent earnings reports validated the business model's strength. But the episode illustrates the scrutiny FTAI faces as a non-traditional player disrupting an established industry.

XI. Key Metrics for Investors

For investors tracking FTAI's ongoing performance, three metrics matter most:

1. Aerospace Products EBITDA per Module

This is the single most important indicator of FTAI's competitive position and margin expansion trajectory. Management has guided to approximately $800,000 per module in 2024, with a long-term target of $1 million as PMA approvals expand.

Track: Quarterly Aerospace Products Adjusted EBITDA ÷ Module production

2. Market Share in CFM56 Aftermarket

FTAI's stated goal is 25% market share of the ~$22 billion CFM56 aftermarket. Market share increased to approximately 9% on an annualized basis, up from 5% last year.

Track: Management's market share disclosures; compare to total industry shop visit estimates

3. SCI Capital Deployment vs. Target

The Strategic Capital Initiative's success determines FTAI's ability to grow without consuming balance sheet capacity. The SCI Partnership also progressed well this quarter, on-track toward its goal of deploying $4 billion of capital in 2025 with 145 aircraft now owned or under LOI compared to a target of 250 in total.

Track: Aircraft count in SCI vehicles; capital deployed vs. targets

XII. Bull Case and Bear Case

The Bull Case

Structural Cost Advantage: The Chromalloy PMA partnership, AAR USM relationship, and vertically integrated model create 20-30 percentage points of margin advantage over competitors. As additional PMA parts receive FAA approval, this advantage widens.

Long Runway: Over 11,000 CFM56 engines still haven't completed their first shop visit. Boeing and Airbus delivery delays are extending aircraft service lives. The addressable market is growing, not shrinking.

Counter-Positioning Moat: OEMs cannot rationally respond to FTAI's pricing without destroying their most profitable business line. This is not a moat that will be competed away.

Asset-Light Transformation: The SCI model allows FTAI to capture recurring MRE revenue without the balance sheet intensity of traditional leasing. If executed successfully, this should drive multiple expansion.

Management Track Record: Joe Adams built this strategy over a decade, positioning FTAI to capitalize on COVID disruption. His long-term thinking and execution deserve investor confidence.

The Bear Case

Concentration Risk: FTAI's entire strategy depends on the CFM56 engine. If the transition to LEAP engines accelerates faster than expected, the addressable market shrinks.

Regulatory Risk: PMA approvals could theoretically be challenged or rescinded. GE and Safran have significant political influence in aviation regulation.

Execution Risk: Scaling module production while maintaining quality is operationally challenging. Any significant quality issues could damage reputation irreparably.

Accounting Complexity: The Muddy Waters report highlighted legitimate questions about how FTAI categorizes revenue. While management refuted the allegations, the business model's complexity creates ongoing disclosure challenges.

Capital Intensity: Despite the asset-light narrative, FTAI has deployed significant capital into engines and facilities. A prolonged aviation downturn could stress the balance sheet.

External Management Structure: FTAI is externally managed by Fortress, creating potential conflicts of interest and fee leakage that investors should monitor.

XIII. Conclusion: The Engine Aftermarket's New King

FTAI Aviation represents one of the most impressive strategic pivots in recent business history. From a confused conglomerate that frustrated investors with K-1s and infrastructure assets, the company has transformed into a vertically integrated aerospace powerhouse with clear competitive advantages and extraordinary growth.

The intellectual architecture of the transformation—recognizing that the CFM56 aftermarket represented an enormous opportunity that incumbents couldn't defend—reflects the kind of first-principles thinking that creates lasting value.

"Our joint venture with IAG Engine Center marks a milestone in our expansion into Europe and our overall maintenance capabilities," said Joe Adams, CEO of FTAI Aviation.

Yet questions remain. Can FTAI continue executing at current growth rates? Will additional PMA approvals arrive on schedule? How will the company navigate the eventual transition from CFM56 to LEAP engines?

The answers will determine whether FTAI becomes a permanent aerospace power or a well-timed trade. But for now, Joe Adams and his team have demonstrated something remarkable: in aviation, as in all business, the money isn't just in owning assets—it's in understanding the ecosystem well enough to capture value that others leave on the table.

Disclosure: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

Now I have sufficient information to continue the article. Let me continue writing from where it left off, adding the XIV and XV sections that would wrap up the article properly according to the outline.

XIV. The Road Ahead: Product Innovation and Market Expansion

The months leading up to late 2025 marked an inflection point for FTAI Aviation as the company accelerated its product innovation and expanded its global reach. Several strategic initiatives demonstrated management's commitment to building durable competitive advantages.

The Perpetual Power Program

In October 2025, FTAI signed a multi-year Perpetual Power Agreement with Finnair Plc covering 36 CFM56-5B engines, designed to provide engine exchanges in lieu of shop visits to enhance flexibility, fleet reliability, and maintenance cost predictability.

FTAI's innovative Perpetual Power Program provides airlines with bespoke solutions to manage their fleets by avoiding costly engine shop visits, reducing downtime, and adding flexibility to make fleet decisions on their own terms through guaranteed engine availability.

This program represents the evolution of FTAI's MRE model—moving beyond transactional module exchanges to long-term, subscription-like arrangements that lock in recurring revenue while providing airlines with operational certainty. Christine Rovelli, Chief Revenue Officer at Finnair, noted that the agreement "strengthens our ability to adapt as our fleet evolves" and enables better management of "maintenance costs, improve reliability, and continue to deliver a reliable product to our customers."

The Palantir AI Partnership

In November 2025, Palantir and FTAI Aviation announced a multi-year strategic partnership, which will allow FTAI to leverage Palantir's Artificial Intelligence Platform across FTAI's global maintenance footprint.

Through this partnership, Palantir's AIP is helping FTAI transform productivity and reduce manufacturing costs by improving maintenance scheduling and inventory optimization across FTAI's operations worldwide. This includes transforming its internal supply chain and driving further efficiencies through automated workflows, rapid asset allocation and dynamic procurement strategies for component parts. With AI-assisted decision making, FTAI is targeting faster production turnaround times and improved unit economics, aiming to bring further cost savings to its customers globally.

The AI platform could track available aircraft and engines and available pricing data and help guide FTAI on what assets to purchase when—and, in some cases, when to sell. FTAI also plans to leverage customer data to help with demand forecasting. One goal is to help match engines with specific airframes based on variables such as operating environments or desired on-wing time.

David Moreno, Chief Operating Officer of FTAI Aviation, stated: "At FTAI, we have long prioritized technology as a key driver of productivity since the launch of our Maintenance, Repair and Exchange (MRE) offering. As our customer base continues to multiply, accelerating the integration of advanced technology into our operations is essential. We are excited to partner with Palantir to harness AI and transform engine maintenance for the world's most widely used commercial aircraft. The initial results in our facilities have been impressive and AIP will play a critical role in achieving our long-term goal of 25% industry market share and enhanced value for our shareholders."

V2500 Expansion

While the CFM56 remains FTAI's primary focus, the company has steadily expanded its V2500 engine portfolio. FTAI owns over 140 V2500 engines and aims to expand its portfolio to 200. Joe Adams noted: "We look forward to collaborating with IAE to restore these engines together, we are committed to the V2500 engine and see tremendous demand for it in the next decade. Teaming up with IAE allows us to extend the life of the V2500 fleet, while providing flexible engine power to our airline customers."

FTAI Aviation is eyeing expansion of its Montreal overhaul facility to include IAE V2500 capability to support its expanding portfolio for the popular narrowbody engine. The Montreal shop, purchased from Lockheed Martin Commercial Engine Solutions, specializes in CFM56s—FTAI's primary product line. But the company is rapidly expanding its portfolio of V2500 engines available for sale or lease.

Strategic Capital Initiative Progress

Kallie Steffes, Head of Strategic Capital of FTAI Aviation, explained the SCI thesis: "We believe the $300 billion dollar mid-life, current generation aircraft market is in need of a well-capitalized buyer that can also support the engine requirements of airlines globally as fleets continue to extend their operating life." FTAI SCI I has invested $1.4 billion thus far acquiring 101 aircraft and has an additional $2.1 billion of aircraft under contract, bringing the vehicle to 190 aircraft closed or under LOI, with full deployment expected by the end of the first half of 2026.

The vehicle has received widespread support across a diverse group of equity investors globally, including asset managers, insurance companies, public pensions, foundations, endowments and family offices.

XV. The LEAP Transition: Managing Long-Term Risk

Every analysis of FTAI must grapple with the long-term question: what happens as the CFM56 fleet ages and the LEAP engine becomes dominant?

The LEAP engine was launched as LEAP-X on 13 July 2008, intended as a successor to the CFM56. The CFM International LEAP ("Leading Edge Aviation Propulsion") is a high-bypass turbofan engine produced by CFM International. It competes with the Pratt & Whitney PW1000G for narrow-body aircraft. The LEAP uses 15% less fuel and produces 15% less CO₂ compared to the CFM56.

Today, the majority of CFM's aftermarket support is generated by CFM56-5B and -7B engines that power Airbus A320ceos and Boeing 737 Next-Generation variants, respectively. This will continue until around 2025, when annual CFM56 shop visits are expected to peak at about 2,500 per year.

Leap shop visits will climb quickly. In 2030, the CFM fleet will be generating more than 4,000 shop visits, roughly split between the CFM56 and Leap variants. "We know that we have a big ramp-up in front of us on the Leap maintenance, repair and overhaul," Safran's CEO Olivier Andries said. "So we have to build up capacity fast."

However, several factors extend the CFM56's relevance:

With 70% of global fleets still using CFM56/V2500 engines, short-term revenue hinges on maintaining older systems despite rising costs.

CFM56 engines' lifespan is expected to extend to 30 years due to economic factors and maintenance solutions. CEO Joe Adams believes the expected fly life for CFM56 engines is underestimated, with airlines now expecting a 30-year lifespan.

Boeing and Airbus production delays have pushed airlines to fly their current fleets longer than planned. The 737 MAX grounding, subsequent production issues, and Airbus's own supply chain constraints have created a supply-demand imbalance that benefits operators focused on legacy engine maintenance.

Management has indicated awareness of the transition risk and the potential to eventually develop capabilities for newer engine platforms. The Palantir partnership and continued investments in operational technology suggest FTAI is building transferable competencies that could apply to future engine programs.

XVI. The Investment Calculus

As of late 2025, FTAI Aviation presents investors with a compelling but complex opportunity. The company's most recent quarterly results demonstrated continued execution:

FTAI Aviation met Wall Street's revenue expectations in Q3 2025, with sales up 43.2% year on year to $667.1 million. Its GAAP profit of $1.10 per share was 11.4% below analysts' consensus estimates.

FTAI generated Net Income Attributable to Shareholders of $114.0 million, $1.11 EPS, an increase of 46% versus Q3 2024. Continued growth in Aerospace Products segment with Adjusted EBITDA of $180.4 million, an increase of 77% versus Q3 2024.

FTAI has significantly improved its leverage profile, with a net debt to run-rate adjusted EBITDA multiple of 2.5x in Q3 2025, down from 5.0x in 2022. This improvement reflects the company's successful pivot to an asset-light strategy and strong growth in adjusted EBITDA generation. The company maintains robust liquidity with a total of $910 million available, including $510 million in cash and $400 million from an undrawn corporate revolver facility. FTAI's weighted average cost of debt stands at 6.5% on $3.5 billion of senior notes, with no corporate bond maturities until May 2028.

FTAI is making significant progress in expanding its global production capabilities. The company produced 207 CFM56 modules in Q3 2025 and remains on track to meet its annual target of 750 modules in 2025, with plans to increase production to 1,000 modules in 2026.

Forward guidance demonstrates management's confidence:

Overall, FTAI now anticipates total business segment EBITDA in 2026 of $1.525 billion, up from its original estimate of $1.4 billion. Based on these projections, FTAI expects to generate $1 billion in adjusted free cash flow next year, representing a 33% increase over the $750 million targeting in 2025.

The company targets a $1 billion adjusted free cash flow in 2026 and aims for 40%+ margins in aerospace products.

On October 27, 2025, the Company's Board of Directors declared a cash dividend on ordinary shares of $0.35 per share for the quarter ended September 30, 2025, an increase from $0.30 per share in the previous quarter.

The valuation question remains complex. FTAI Aviation currently trades at a price-to-earnings ratio of 35.7x, which is notably higher than both its industry average of 18.6x and the peer average of 19x. While the fair ratio sits at 58.3x, this premium signals that investors are paying up for expected growth. Such a gap increases valuation risks if market optimism fades.

XVII. Final Thoughts: The Art of the Possible

FTAI Aviation's transformation from a confused conglomerate into a focused aerospace powerhouse represents one of the most impressive corporate pivots of the past decade. The intellectual architecture of the strategy—identifying an enormous aftermarket opportunity that incumbents could not rationally defend—reflects first-principles thinking at its finest.

The company's competitive advantages are real and difficult to replicate. The Chromalloy PMA partnership, the AAR USM relationship, the vertically integrated Module Factory, and now the Strategic Capital Initiative create multiple moats that reinforce each other. The counter-positioning dynamic against GE and Safran may prove to be the most durable advantage of all.

Yet questions remain. Can FTAI continue scaling production while maintaining quality? Will additional PMA parts receive FAA approval on schedule? How will the company navigate the eventual transition from CFM56 to LEAP engines? And can the SCI model work across multiple fundraising cycles?

The investment case ultimately depends on one's assessment of Joe Adams and his team. Their track record—building the business through COVID disruption, securing critical partnerships years in advance, and executing a complex corporate restructuring—inspires confidence. But the market has priced in substantial growth, leaving limited margin for error.

FTAI Aviation aims to capture 25% of the $22 billion aftermarket engine maintenance market. The company is transitioning to an asset-light model, focusing on engine module production and aftermarket services. Strategic Capital Initiative (SCI) is set to attract private capital, reducing reliance on leased assets.

What Joe Adams recognized in late 2020—that the CFM56 aftermarket represented a once-in-a-generation opportunity—has proven correct. The question for investors is whether the next phase of FTAI's growth will prove equally prescient.

For students of business strategy, FTAI offers a master class in competitive positioning. For investors, it presents a high-quality business at a premium valuation. And for the aviation industry, it represents the emergence of a new power in the engine aftermarket—one that has proven the giants' lunch is indeed available for the taking.

Disclosure: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

XVIII. Management and Governance

The leadership team steering FTAI Aviation through its transformation deserves closer examination, as their decisions over the past decade have proven instrumental to the company's success.

The External Management Structure

FTAI operates under an external management agreement with FIG LLC, an affiliate of Fortress Investment Group. This structure, while common in the infrastructure and REIT sectors, creates complexities that investors should understand.

We are externally managed by FIG LLC (the "Manager"), an affiliate of Fortress Investment Group LLC ("Fortress"), which has a dedicated team of experienced professionals focused on the acquisition of transportation and infrastructure assets since 2002.

The external management structure provides FTAI with access to Fortress's deep bench of investment professionals, deal sourcing capabilities, and capital markets expertise. However, it also creates potential conflicts of interest—the manager earns fees regardless of stock performance, and may allocate opportunities among multiple Fortress vehicles.

Board Composition and Oversight

The board's response to the January 2025 Muddy Waters allegations demonstrated the governance structure's effectiveness under pressure. The Audit Committee's independent review, utilizing external legal and forensic accounting advisors, provided shareholders with confidence that appropriate oversight mechanisms exist.

FTAI Aviation announced that its Board of Directors' Audit Committee has completed an independent review of allegations made in short seller reports from January 2025. The review, conducted by independent legal and forensic accounting advisors, concluded that the allegations against the company were unsupported and without merit. The Audit Committee Chair, Paul R. Goodwin, emphasized their commitment to maintaining high standards of corporate governance, internal compliance, and financial reporting controls.

Capital Allocation Philosophy

Management's capital allocation decisions reveal a consistent philosophy: build competitive advantages through strategic partnerships before deploying capital into assets. The Chromalloy partnership preceded the COVID engine-buying opportunity. The AAR relationship preceded the Module Factory scaling. The SCI structure preceded large-scale aircraft acquisitions.

This sequencing—securing competitive advantages first, then deploying capital—distinguishes FTAI from traditional lessors who often compete primarily on cost of capital.

XIX. Risks and Considerations

While FTAI's strategic positioning appears strong, several risks merit careful consideration.

Concentration Risk

FTAI's entire Aerospace Products strategy depends on the CFM56 and, to a lesser extent, the V2500 engine platforms. Any development that accelerates the retirement of these engines—whether regulatory changes, fuel price spikes favoring newer aircraft, or unexpected technological breakthroughs—would compress the company's addressable market.

Regulatory and Certification Risk

The PMA parts that underpin FTAI's margin advantage require ongoing FAA certification and approval. While the regulatory framework has proven stable, any changes to PMA policies or challenges to existing certifications could materially impact the business model.

The stringent FAA certification process, which takes 3-5 years per part, creates a significant barrier to entry for competitors. This same regulatory framework that protects FTAI from new entrants also means that any certification issues would take years to resolve.

Geopolitical Exposure

The Russia-Ukraine situation demonstrated FTAI's exposure to geopolitical risk. While the company has worked to recover value from stranded assets, similar situations could emerge in other markets where FTAI operates.

Execution Risk at Scale

Scaling from hundreds to over a thousand modules annually requires flawless execution across multiple facilities and geographies. Quality issues at any facility could damage customer relationships and reputation in ways that take years to repair.

OEM Response

While counter-positioning logic suggests OEMs cannot rationally match FTAI's pricing, GE and Safran possess substantial resources and could pursue non-price competitive responses—such as exclusive service agreements, enhanced warranties, or regulatory lobbying—that could impact FTAI's growth trajectory.

XX. Conclusion: A New Force in Aerospace

FTAI Aviation's journey from a confused conglomerate to a focused aerospace powerhouse stands as a case study in strategic transformation. Joe Adams and his team recognized an opportunity hiding in plain sight: the world's most ubiquitous jet engine was entering its most maintenance-intensive phase, and the incumbents' business models prevented them from competing effectively on price.

The company's competitive advantages—the Chromalloy PMA partnership, the AAR USM relationship, the vertically integrated Module Factory, and the Strategic Capital Initiative—form an interlocking system that grows stronger as FTAI scales. Each module produced generates parts for future repairs. Each SCI aircraft feeds engines into the MRE system. Each satisfied customer provides referrals to new airlines.

The counter-positioning dynamic against GE and Safran may prove to be FTAI's most durable moat. As one industry analyst noted, "CFM is very nervous about this because they know their HPT blades are overpriced, but they don't want to accept it." The OEMs' rational response—protecting their highly profitable aftermarket business—inadvertently cedes market share to FTAI.

With market share in Aerospace Products climbing from 5% to about 9% annualized, and a longer-term target of 25%, that growth runway looks long. Whether FTAI achieves this ambitious target depends on continued execution, additional PMA approvals, and the CFM56 fleet's continued relevance.

The investment community has rewarded FTAI's transformation with a premium valuation, reflecting expectations for continued growth. The company's raised guidance for 2026—targeting $1.525 billion in segment EBITDA and $1 billion in adjusted free cash flow—suggests management's confidence in the trajectory ahead.

For the aviation industry, FTAI's rise represents something more significant than one company's success. It demonstrates that even in sectors dominated by century-old incumbents, innovative business models can capture value that others leave on the table. The engine giants' lunch, as it turns out, was always available—it just required someone with the vision to take a seat at the table.

Disclosure: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

Based on the article outline and the existing content, the article appears to be complete through Section XX (Conclusion). The outline specified sections I through IX (Hamilton's Seven Powers Analysis), and the existing article has already covered all of these sections plus additional sections (X through XX) that expand on the analysis. Let me verify if there are any remaining sections from the outline that haven't been covered.

Looking at the original outline: - Section I-IX were outlined in detail - The existing article has covered all these sections and extended through Section XX

The article appears to be complete. However, I notice the existing article ends with a conclusion in Section XX, but there could be value in adding a brief epilogue or postscript with the most recent developments. Let me add a brief closing section that ties together recent news and provides a current snapshot.

Epilogue: November 2025 Snapshot

As of late November 2025, FTAI Aviation stands at an inflection point. The company has successfully completed its inaugural SCI fundraising round, announced groundbreaking AI partnerships, and demonstrated that its core business model continues to scale.

Chief Financial Officer Nam Eun acquired 652 shares of company stock on November 14, 2025, at a weighted average price of $153.46, for a total transaction value of approximately $100,000. Chief Operating Officer David Moreno also purchased 4,354 shares on November 13, 2025. Such insider buying often signals management's confidence in the company's trajectory.

Fitch Ratings upgraded FTAI Aviation's long-term issuer default rating to 'BB+' from 'BB-', highlighting its strong financial performance and successful corporate transition. The company's senior unsecured bonds were also upgraded to 'BB+' by Fitch. This credit upgrade reflects the market's growing confidence in FTAI's business model durability.

Analyst sentiment remains broadly positive. Barclays increased their target price on shares of FTAI Aviation from $195.00 to $200.00 and gave the stock an "overweight" rating in a research report on October 28, 2025. Royal Bank of Canada lifted their price objective from $185.00 to $200.00 and gave the company an "outperform" rating on October 29, 2025. Jones Trading initiated coverage on FTAI Aviation on October 10, 2025, issuing a "buy" rating with a $306.00 price target.

Institutional investors own 88.96% of the company's stock, reflecting significant professional investor interest in the FTAI thesis.

The competitive landscape continues to evolve in FTAI's favor. Boeing's ongoing production challenges and Airbus's supply chain constraints have extended the operating lives of CFM56-powered aircraft beyond initial expectations. Every additional year these aircraft fly represents additional maintenance revenue flowing through FTAI's Module Factory network.

Management's 25% market share target—up from approximately 9% today—implies years of continued growth ahead. The key question is not whether FTAI can capture this share, but at what pace and with what margin profile.

For observers of corporate strategy, FTAI Aviation offers lessons that transcend the aviation sector. The company demonstrates how deep domain expertise, patient capital, and first-principles thinking can unlock value in mature markets that incumbents cannot rationally defend. Joe Adams and his team recognized that the CFM56 aftermarket represented not a dying business, but a business entering its most profitable phase—and they built a platform to capture that opportunity before anyone else understood what was happening.

Whether FTAI becomes a multi-generational aerospace franchise or a well-timed trade on a specific engine cycle remains to be seen. But the strategic architecture—counter-positioning against OEMs, vertical integration through partnerships, and capital efficiency through the SCI model—represents a playbook that will be studied by business strategists for years to come.

The engine giants' lunch, as it turned out, was always available. It just required someone bold enough to take a seat at the table.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube