APi Group: The "Industrial Jarden" Building the World's Fire Safety Empire

I. Introduction & Episode Roadmap

Picture this scene: a commercial building in any major American city, maybe a hospital in Minneapolis, a data center in Phoenix, or an office tower in Manhattan. Hidden behind walls and above ceilings runs an invisible network of pipes, sensors, and sprinkler heads—fire protection systems that most occupants will never think about until they're needed. Once a year, sometimes more often, a technician arrives with a clipboard and testing equipment. This inspection isn't optional; it's mandated by law. If the system fails inspection, the building can't be occupied until it's fixed.

That statutory mandate—the legal requirement that fire safety systems be inspected, maintained, and repaired—is perhaps the most powerful economic moat in American business services. And sitting atop the industry built around this regulatory necessity is APi Group Corporation, a $7 billion company that quietly became the largest provider of life and safety services globally.

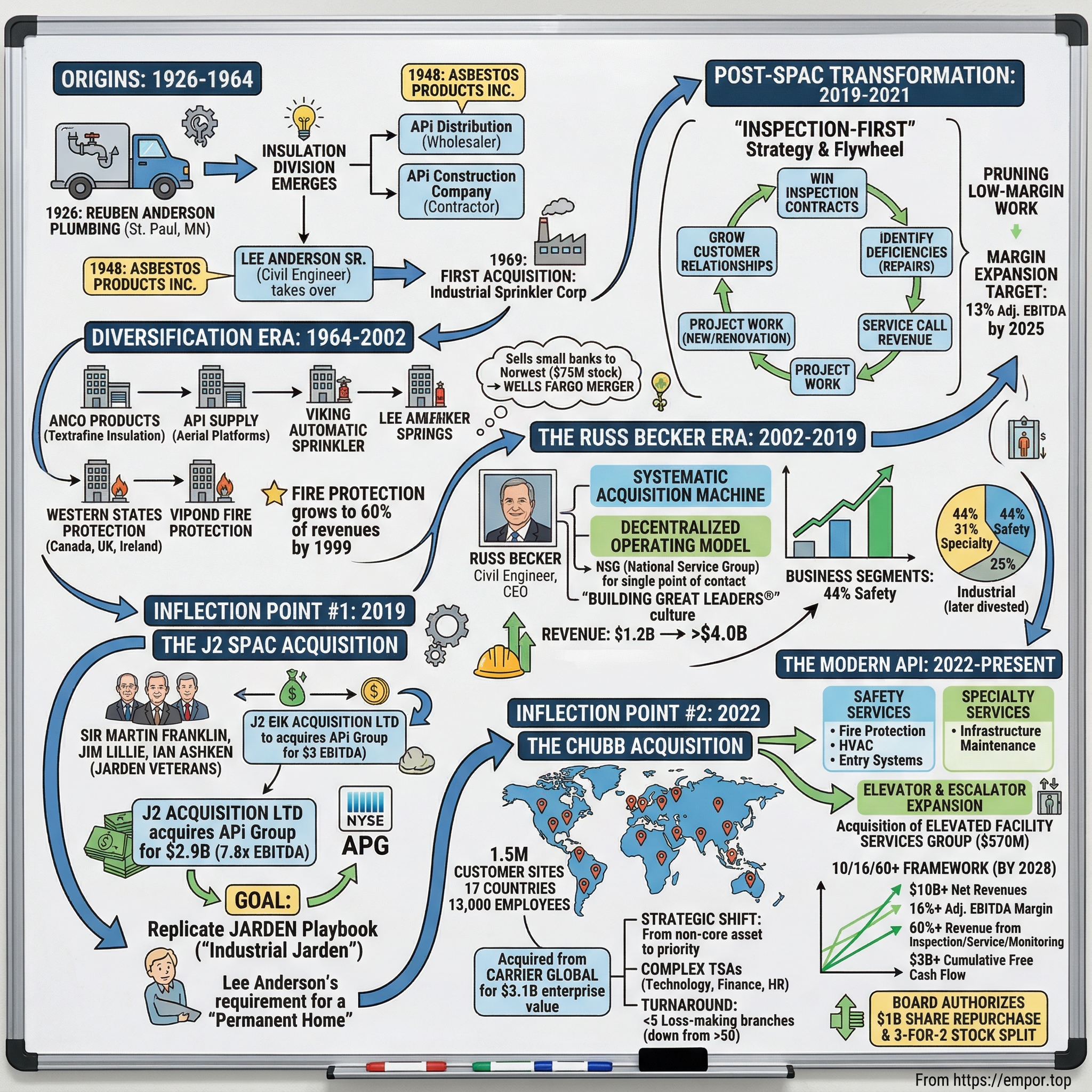

The company was formerly known as J2 Acquisition Limited and changed its name to APi Group Corporation in October 2019. APi Group Corporation was founded in 1926 and is headquartered in New Brighton, Minnesota. What began as a small plumbing company in St. Paul has evolved through nearly a century of family stewardship, serial acquisitions, and a transformative SPAC deal into something remarkable: a business services empire that generates recession-resistant cash flows by performing work that building owners must purchase by law.

The central question of APi's story is this: How did a small Minnesota plumbing company from 1926 become the world's largest life safety services provider through a unique marriage of serial acquirers and a SPAC? The answer involves three generations of Andersons, a civil engineer turned CEO who completed over 90 acquisitions, and the reunion of three Jarden Corporation veterans who saw in APi the opportunity to repeat one of the greatest value creation stories in consumer products history.

APi Group annual revenue for 2024 was $7.018 billion, a 1.3% increase from 2023. But raw revenue numbers don't capture what makes this company fascinating. The story is in how it generates that revenue: through inspection contracts that automatically renew, through service calls triggered by mandatory compliance schedules, and through project work earned as a byproduct of ongoing customer relationships.

The themes threading through APi's century-long journey apply far beyond fire safety services: the power of serial acquisition strategies in fragmented industries, the value of statutorily-mandated recurring revenue, the importance of inspection-first business models that create downstream opportunities, and the art of transforming thousands of small, regional players into a coordinated national platform.

II. Origins: From Plumbing to Insulation (1926–1964)

The streets of St. Paul, Minnesota in 1926 were a world away from the modern fire safety industry. Warren Harding had recently died in office, the Great Gatsby had just been published, and a plumber named Reuben Anderson was building a small contracting business in the Twin Cities.

The founding of APi Group traces back to 1926 when Reuben Anderson started a small plumbing company in St Paul, Minnesota. Over time, his company grew, and a division focused on insulation contracting and distribution emerged. The company operated under the name Reuben L. Anderson-Cherne, a mechanical contracting firm serving the growing industrial base of the upper Midwest.

The choice of insulation as a specialty wasn't accidental. By the late 1920s the company also had branched out into asbestos and pipe insulation and the distribution of insulation materials. The industrial facilities of the era—paper mills, food processing plants, manufacturing operations—required extensive thermal insulation to operate efficiently. Reuben Anderson positioned his company to serve these needs.

The separation of the insulation business from the plumbing operations came in 1948, when this division was incorporated as a separate company. In 1948 the insulation-related activities were spun off into a separate firm known as Asbestos Products. This firm included divisions that eventually would develop into the subsidiaries APi Distribution, a wholesaler of insulation products for industry, and APi Construction Company, an insulation contractor for the utility, energy generation, petroleum, and paper industries.

For nearly three decades, Anderson operated Asbestos Products as an independent sister company to his plumbing firm. The business grew steadily but unremarkably, serving industrial customers across Minnesota and the surrounding states.

The critical transition came in 1964. Lee Reuben Anderson Sr. (born June 22, 1939) is an American businessman and philanthropist. He was the owner and chairman of the Minnesota-based API Group Inc., a holding company for numerous construction and fire-protection firms.

Lee Anderson's background shaped everything that followed. Anderson, an only child, was born in Minneapolis, Minn., and attended the private Breck School, then in St. Paul. A lifelong outdoorsman, he spent much of his boyhood at the family home in the Brainerd lakes area north of the Twin Cities. At the urging of his father, a successful plumbing contractor, he enrolled at the United States Military Academy at West Point and played football and basketball. After he graduated in 1961 with a B.S. in civil engineering, Anderson served in the U.S. Army at Luke Air Force Base in Phoenix, Arizona, where he oversaw materials procurement and construction services and was promoted to first lieutenant.

In 1964, Anderson returned to the Twin Cities and took over A.P.I. Inc. (originally Asbestos Products International), an insulation contractor founded in 1926 as a division of his father's plumbing business. After he purchased an industrial fire sprinkler company in 1969, Anderson continued to acquire other firms, primarily in the construction and fire-protection fields.

The West Point training and Army logistics experience gave Lee Anderson something that would prove invaluable: a systematic approach to building organizations and a long-term perspective on value creation. Family-owned businesses operate differently from public companies—they can think in decades rather than quarters, build relationships rather than optimize for short-term metrics, and take calculated risks knowing that patient capital stands behind them.

The post-war American construction boom provided the perfect context for Anderson's ambitions. As America built highways, suburbs, shopping centers, and industrial parks, specialty contractors thrived by solving specific problems that general contractors couldn't. Insulation, electrical work, plumbing, fire protection—each required specialized knowledge, licensed technicians, and local relationships.

The question that would define APi's next fifty years was taking shape: Could these fragmented specialty services be consolidated into something larger?

III. The Diversification Era: Building a Portfolio Company (1964–2002)

Lee Anderson didn't waste time. Anderson's first acquisition was the 1969 purchase of the Industrial Sprinkler Corporation, a fire protection company located in St. Paul that had been founded 15 years earlier. This was followed by the purchase of Anco Products, Inc. in 1972. Anco was a young firm in Elkhart, Indiana, engaged in the production of flexible heating and cooling air ducts. The company also made the Textrafine brand of insulation, a resilient long-fiber insulation used in cryogenic tanks for the storage of liquefied natural gas.

The 1969 acquisition of Industrial Sprinkler Corporation proved prophetic. Fire protection would eventually become the core of APi's business, but in the early years it was just one piece of a diversifying portfolio. Another subsidiary, APi Supply, Inc., was established in St. Paul in 1977 as a sales and rental firm for aerial work platforms—machines used to lift loads high into the air—including scissorlifts and boom lifts from manufacturers such as Snorkel, JLG, SkyJack, Workforce, and Upright. In 1981 APi bought Industrial Contractors, Inc. (ICI) of Bismarck, North Dakota.

The acquisition pace accelerated through the 1990s. The Jamar Company, Viking Automatic Sprinkler, and APi Supply Company were acquired. Western States Fire Protection and two steel fabrication companies were acquired. VFP Fire Systems and Vipond Fire Protection of Canada were acquired. About a dozen fire protection acquisitions expanded the company's reach in Canada, the United Kingdom, and the western United States.

The pattern emerging was deliberate: acquire local champions in specialty services, maintain their identity and operational independence, provide resources and capital for growth, and let entrepreneurial managers continue running their businesses. By 1999 fire protection had grown to account for 60 percent of APi's revenues, up from 30 percent five years earlier.

The growing conglomerate was renamed APi Group Inc. in 1997. The name change reflected a shift from the legacy insulation business (Asbestos Products International) to a broader portfolio of construction and fire protection services.

International expansion came with the Vipond acquisitions. Vipond was further enhanced in 1999 with the acquisition of Cronin Fire Equipment of Ottawa, Alsask Fire Equipment of Regina, Saskatchewan, and Firestop of Belfast, Ireland.

The business Lee Anderson was building had characteristics that would prove extraordinarily valuable: Fire protection, including installation of sprinkler systems and wildfire suppression, accounts for more than half the company's business. Other subsidiaries are active in insulation and electrical contracting, plumbing, boiler maintenance, heating and ventilation, garage door installation, asbestos abatement, building security systems, steel fabrication, distribution of construction materials, the manufacture of air ducts, and the rental of aerial work platforms. Most of the APi Group's construction and contracting-related subsidiaries are located in Minnesota and surrounding states, but the company's fire protection holdings extend as far as Texas, California, Canada, and the United Kingdom.

APi bought US Fire Protection and Alliance Fire Protection, both based near Chicago, in 2000. Late in 2003 APi bought Windy City Fire Protection of Chicago and merged it into Alliance Fire Protection.

Lee Anderson also demonstrated business acumen beyond APi. In the late 1970s, Anderson also began to purchase small banks in central and northern Minnesota. In 1997, he sold his banking assets to Norwest Corporation for a reported $75 million in stock. Norwest's subsequent merger with Wells Fargo, in 1998, greatly enhanced the value of the shares Anderson had acquired in the original trade.

The sale of banking assets to Norwest revealed something important about Lee Anderson: he understood how to create and realize value across multiple decades. The patient accumulation of small banks, followed by a well-timed sale to a strategic acquirer, followed by the benefits of a subsequent merger—this was sophisticated capital allocation dressed in Midwestern humility.

By 2002, APi had become one of the largest specialty contractors in North America, with operations spanning fire protection, insulation, electrical, and infrastructure services. But the company remained private and largely unknown outside the construction industry. Lee Anderson was approaching his mid-sixties, and the question of succession loomed.

The answer came from within APi's own ranks: a civil engineer who had joined the Jamar Company subsidiary in 1995.

IV. The Russ Becker Era Begins (2002–2019): Building the Acquisition Machine

Russell Becker's path to the CEO office wasn't typical for a construction services company. Russell (Russ) Becker completed his bachelor's (1989) and master's (1991) degrees in civil engineering at Michigan Tech. He is the Chief Executive Officer and President of APi Group, one of the largest providers of specialty services in North America and the largest provider of life safety services in the world.

Russ began his career as a field engineer with Cherne Contracting. He moved on to become a project manager for Ryan Companies during the construction of the Greenfield Recycled Paper Mill project for Liberty Paper. Upon completion of his project, he joined APi Group's subsidiary, The Jamar Company, in Duluth, Minnesota.

The path from Jamar to the CEO office was remarkably swift. Russell A. Becker currently works at APi Group, Inc., as President & Chief Executive Officer from 2002... Mr. Becker also formerly worked at Children's Health Care, as Chairman, Liberty Diversified International, Inc., as Director, Dunwoody College of Technology, as Trustee, Ryan Cos. Us, Inc., as Project Manager from 1993 to 1995, The Jamar Co., as President from 1998 to 2002, and Cherne Contracting Corp., as Field Engineer from 1991 to 1993.

He has built his career through progressive leadership roles within the company and its subsidiaries. Beginning his tenure at APG in 2002 as President and Chief Operating Officer, he was promoted to Chief Executive Officer in 2004.

Mr. Becker joined APi Group, Inc. in 2002 as President and Chief Operating Officer and became CEO in 2004. Mr. Becker has continued to serve as CEO of APi Group Corporation following its acquisition of APi Group, Inc. in October 2019.

The transition from Lee Anderson's leadership to Russ Becker's marked a shift from founder-led entrepreneurship to systematic operational excellence. Anderson had built APi through relationship-based acquisitions and patient capital allocation. Becker would transform those foundations into a disciplined acquisition machine.

APGs operating model has allowed them to grow revenues from $1.2B to over $4.0B during the past 10 years. The growth came through a combination of organic expansion and relentless acquisition activity.

We believe that one of our core pillars of success is our distinct leadership development culture – driven by our purpose of Building Great Leaders®. Our commitment to investing in leadership development at all levels of the organization has created an empowered, entrepreneurial atmosphere that facilitates organizational sharing of knowledge and best practices and enables the development of cross-brand solutions and innovation.

The "Building Great Leaders" philosophy became central to APi's identity. Our enduring purpose is Building Great Leaders® – and we're proud to provide all team members with diverse opportunities for leadership development. No matter what your role is, we'll equip you with personalized tools, resources, and support to ignite your potential and accelerate your unique career journey. Building Great Leaders® is our mission, and the name of the internally-created development program we designed to make it happen.

"As Leaders, we recognize that our success happens only when our Branches and Field Leaders are successful. All of our people are foundational to creating value."

This decentralized operating philosophy was strategic, not accidental. APi competes in local markets where relationships, reputation, and responsiveness matter enormously. A fire protection contractor in Denver doesn't win work because headquarters in Minnesota says so—they win because local leaders have built trust with building owners, general contractors, and facility managers over years or decades.

But decentralization creates its own challenges: inconsistent quality, difficulty capturing scale benefits, and the risk that acquired companies don't actually integrate into the broader platform. APi's answer was what it calls the National Service Group (NSG), which provides customers with a single point of contact for multi-location needs while maintaining local delivery.

Unlike non-pure play comps and other mom and pop specialty contractors, APi Group has a wide range of blue chip customers and serves a diverse set of end markets limiting their contract risk (no contract accounts for >5% of revenues). They also have an outstanding reputation given their near 100 year history and track record, leading them to low contract loss rates (less than 1.5% of revenues) and plenty of repeat business.

The business model evolution during the Becker era increasingly emphasized service revenue over project revenue. Fire protection installations are lumpy and competitive; ongoing inspection and maintenance contracts are recurring and sticky. Today, APi operates three segments, Safety Services, Specialty Services, and Industrial Services responsible for 44%, 31% and 25% of revenues. (Note: The Industrial Services segment was later divested or restructured as part of the post-SPAC transformation.)

By 2019, APi had grown to approximately $4 billion in revenue. Lee Anderson was 80 years old and ready to transition. The question was: who would buy APi, and on what terms?

In part, I attribute the low acquisition multiple to Lee Anderson's desire to find a permanent home for APi as he wanted to retire at the age of 80 and see his baby taken care of and not chopped up or flipped by private equity. He wasn't making his decision based on the highest price he could get, but based on a relationship with the future owner and trust they wouldn't rip apart what he spent so long building.

Anderson's requirements eliminated most potential buyers. Private equity firms would eventually flip the company. Strategic acquirers might break it apart. A traditional IPO would expose the company to quarterly earnings pressure and activist investors. What Anderson needed was a buyer who would commit to APi's decentralized culture, keep management in place, and provide patient capital for continued growth.

Enter Martin Franklin.

V. INFLECTION POINT #1: The J2 SPAC Acquisition (2019)—Enter Martin Franklin

To understand why the APi-J2 deal made sense, you first need to understand Martin Franklin. Sir Martin Ellis Franklin, KGCN (born 31 October 1964) is a British American, Miami-based businessman. He is the founder and chairman of Element Solutions Inc.; co-founder and co-chairman of Nomad Foods Limited, and co-founder and former chairman of Jarden Corporation, which was sold to Newell Brands in 2016.

Martin Ellis Franklin was born on 31 October 1964 in London, England. His father, Sir Roland Franklin, was a merchant banker who undertook hostile takeovers with Sir James Goldsmith. Franklin emigrated to the United States with his family at the age of fifteen, settling in Harrison, New York.

The family history matters. James Goldsmith was one of the legendary corporate raiders of the 1980s, and Roland Franklin was his partner in transactions that reshaped British industry. Martin Franklin grew up watching his father identify undervalued companies, acquire them (sometimes hostilely), and unlock value through operational improvements and strategic repositioning.

But the younger Franklin chose a different path. "It was much less fulfilling to breakup a company. And when you're building something, everybody is sort of rooting for you. The investment community is rooting for you, employees are rooting for you. The establishments is rooting for you. And when I started on that path of building Benson Eyecare, it was just — all the energy was positive energy."

Franklin's masterwork was Jarden Corporation. Alltrista was renamed Jarden Corporation and Franklin served as its chairman and chief executive from 2001 to 2011, and as its executive chairman from 2011 to 2016 when James E Lillie became Jarden's CEO. Under Franklin's leadership, Jarden grew from approximately $300 million in revenues to more than $10 billion, having over 120 global brands and 35,000 employees before it was acquired by Newell Brands.

From 2001-2016, investors in Jarden stock received an overall return of 5,353% or 32% IRR over 15 years, culminating in the sale of the business to Newell Brands.

The Jarden model was straightforward in principle but fiendishly difficult in execution: acquire underperforming consumer products companies, maintain their brand identities, provide capital and operational expertise, let local management run day-to-day operations, and deploy cash flows into additional acquisitions. The company accumulated brands like Mr. Coffee, Crock-Pot, Coleman, Rawlings, and Ball Mason jars into a diversified portfolio that generated consistent cash flows.

"The triumph of Jarden was built on a decentralized model that combined the economies of scale of a large corporation with 'the entrepreneurial freedom to build their businesses as they saw fit.'"

Sound familiar? The parallels between Jarden's approach to consumer brands and APi's approach to fire protection companies were striking. Both emphasized decentralized operations with entrepreneurial local leadership. Both focused on acquiring market-leading positions in fragmented industries. Both generated strong cash flows from established customer relationships.

After Jarden's sale to Newell Brands in 2016, Franklin found himself wealthy but restless. The Newell integration went poorly (the combined company struggled, and Franklin ultimately waged a proxy fight against its board), and Franklin wanted another vehicle for deploying capital.

In October 2017, Franklin, Ashken, and Lillie launched J2 Acquisition Limited, a $1.25 billion acquisition vehicle listed on the London Stock Exchange. J2 acquired APi Group, Inc., a market-leading business services provider of safety, specialty, and industrial services, for $2.9 billion, in 2019, at which time the company changed its name to APi Group Corporation. The company moved its listing to the NYSE, under the symbol APG, in April 2020.

The J2 team reunited the core Jarden leadership: Martin Franklin, Jim Lillie (who had been Jarden's CEO from 2011-2016), and Ian Ashken (who had been CFO). They explicitly sought to replicate the Jarden playbook in a new industry.

Management has called APi the 'industrial version of Jarden' and feels as though the opportunity set could be even larger.

On October 2, 2019, J2 Acquisition Corp, a SPAC run by Martin Franklin, Jim Lillie and Ian Asken, signed an agreement to acquire APi for $2.9 billion, 7.8x LTM June 2019 Adjusted EBITDA of $371 million net of tax benefits.

Importantly, Franklin and his partners co-invested approximately $100 million of their own money in the deal at the same price as the SPAC holders.

This co-investment was unusual and important. Most SPAC sponsors receive shares at below-market prices as compensation for finding deals, creating misaligned incentives. Franklin's team put substantial personal capital at risk alongside public shareholders, aligning their interests with other investors.

Why was the acquisition multiple so attractive? The SPAC gave him instant liquidity vs an IPO or sponsor sale both of which would allow him only to get out over time. Lee Anderson valued certainty, continuity, and a relationship with buyers who would respect what he'd built. Franklin's track record at Jarden, combined with the commitment to maintain APi's culture and keep Becker as CEO, made J2 the right buyer at an attractive price.

The deal structure also demonstrated Franklin's sophistication. By using a London-listed SPAC and then moving the listing to NYSE after completion, he navigated the mechanics of taking APi public while giving the company access to U.S. capital markets and a broader investor base.

For investors, the APi acquisition represented a rare opportunity: a high-quality, cash-generative business with proven management, acquired by operators with an exceptional track record, at a valuation below comparable transactions. The question was whether Franklin and team could apply the Jarden playbook to industrial services as successfully as they had to consumer products.

VI. The Post-SPAC Transformation: Margin Expansion & Quality Focus (2019–2021)

The immediate post-SPAC period revealed the changes Franklin's team intended to make. APi under the Andersons had grown aggressively but not always profitably. Some acquired businesses operated at thin or negative margins. The company's decentralized culture had allowed underperforming units to persist.

The new strategic priorities were clear: margin expansion through portfolio pruning, increased focus on recurring inspection and service revenue, and disciplined project selection to avoid low-margin work.

As I look across our global operation, I am confident in our leaders' ability to continue to deliver double-digit core inspection organic growth and continued margin expansion across the business as we drive towards our 2025 target of 13% (or more) Adjusted EBITDA margin. As we look to 2024 and beyond, we have great confidence in the business, our ability to deliver consistent organic growth globally, while simultaneously increasing our discipline on project selection and pruning low margin revenue opportunities.

The "inspection-first" strategy became the central organizing principle. Fire protection systems require annual inspections to maintain compliance. These inspections generate recurring revenue on predictable schedules. More importantly, inspections identify deficiencies that must be repaired—creating service revenue. And service relationships lead to project work when customers build new facilities or renovate existing ones.

The flywheel works like this: Win inspection contracts → identify repair and maintenance needs → earn project work → grow relationships → increase retention → repeat. Companies that start with project work (competitive bidding for new construction) often struggle to break into the more profitable inspection and service work. Companies that start with inspection contracts naturally earn the right to do service and project work.

In 2020 and early 2021, APi began establishing its European platform through acquisitions. The company acquired SK FireSafety Group and other businesses that provided a beachhead for international expansion, contributing approximately $200 million in revenue with adjusted EBITDA margins around 13%.

The transformation from a private, growth-focused company to a public, margin-focused company wasn't without tension. Some managers who had thrived under the old regime struggled with the new emphasis on profitability. But the results validated the approach: margins expanded, cash flow improved, and the stock price appreciated.

The company was also building firepower for its next move—a transformational acquisition that would make APi the undisputed global leader in life safety services.

VII. INFLECTION POINT #2: The Chubb Acquisition—Becoming the Global Leader (2022)

On July 27, 2021, APi announced an agreement to acquire the Chubb fire and security business from Carrier Global Corporation. APi Group Corporation completed its previously announced acquisition of the Chubb fire and security business ("Chubb") from Carrier Global Corporation (NYSE: CARR) for an enterprise value of $3.1 billion, which is comprised of $2.9 billion cash and approximately $200 million of assumed liabilities and other adjustments.

Headquartered in the United Kingdom, Chubb has approximately 13,000 employees globally and a sales and services network spanning 17 countries serving more than 1.5 million customer sites in Asia Pacific, Canada and Europe. The business is a globally recognized fire safety and security services provider, offering customers complete and reliable services from design and installation to monitoring and on-going maintenance and recurring services.

The deal closed on January 3, 2022, transforming APi's geographic footprint and scale. We begin 2022 as the world's leading life safety services provider.

Why did Carrier sell? The sale enables Carrier to focus on its core businesses and to re-allocate the net proceeds consistent with its stated capital allocation priorities, including funding organic and inorganic growth, a growing and sustainable dividend, and share repurchases while maintaining a solid investment grade credit rating.

This "non-core asset" dynamic is central to understanding the deal. Carrier, spun out of United Technologies in 2020, was focused on HVAC and refrigeration. Fire and security services, while profitable, didn't fit Carrier's strategic priorities. When a business is non-core to its parent, it typically receives less investment, less management attention, and less strategic focus than it would as someone's primary business.

APi's thesis was straightforward: "As the Chubb business shifts from being a non-core asset to one that is a paramount strategic priority within APi, we believe the business will move faster and more efficiently, globally leveraging the expertise and ability of our combined 26,000 dedicated and talented team members."

Co-Chair James E. Lillie added: "The completion of the acquisition of Chubb is an exciting milestone as we continue our evolution and growth as a public company. The acquisition creates another new chapter for APi, while also continuing our original investment thesis in creating value as the global leader in life safety services concentrating the majority of the business on statutorily-mandated, recurring service revenue."

The financing structure was complex but manageable. The transaction will be funded through a combination of cash on hand, a combined $800 million investment in perpetual preferred equity from Blackstone and Viking Global Investors and debt. Barclays and Citi provided committed financing. APi Group Corporation has obtained financing commitments aggregating $1.8 billion in the form of a term loan of $1.4 billion and senior unsecured notes of $400 million to be used to finance the acquisition.

Bringing in Blackstone and Viking Global as preferred equity investors demonstrated APi's access to sophisticated capital. The perpetual preferred structure provided flexible financing without the near-term repayment requirements of traditional debt.

The integration challenge was substantial. Chubb operated in 17 countries with different regulatory environments, different labor practices, and different customer expectations. Many Chubb branches were operating at subpar margins—or worse. We expect that we will continue our 1:1, or better, cost-benefit ratio and spend up to $125 million in total to capture these savings. We expect to conclude these value capture efforts by year-end 2025.

In 2022, APi Group, a North American provider of safety and building-related services, acquired Chubb Fire & Security Ltd., a global fire safety and security solutions provider headquartered in the UK. As part of the acquisition, APi Group negotiated an extensive set of transitional services agreements (TSAs) that covered technology, finance, tax, treasury, and HR services for an initial 12-month period. To separate from Chubb's parent company, the deployment required a greenfield tech estate and a new network that could accommodate Chubb's geographically diverse organization. To avoid TSA penalties and ensure timely fulfillment of the separation agreement, APi Group needed an implementation partner that had the technology and M&A expertise to hit the ground running, and fast.

The turnaround has progressed substantially. Management has indicated that the international business entered 2025 with fewer than five loss-making branches, down from over 50 at the time of acquisition. This dramatic improvement in branch-level profitability validates the thesis that Chubb's underperformance was a function of neglect rather than fundamental business quality.

VIII. The Modern APi: Two Segments, One Machine (2022–Present)

Today's APi operates primarily through two reporting segments: Safety Services and Specialty Services.

Safety Services comprises the core fire and life safety business that defines APi's identity. The segment offers end-to-end integrated occupancy systems including fire protection solutions, HVAC, and entry systems—covering design, installation, inspection, and service. Life Safety (approximately 88% of segment revenues) provides design, contract, inspection, monitoring, and other services for life safety systems such as fire sprinklers, alarms and extinguishers across multiple geographies. HVAC Mechanical (approximately 12% of segment revenues) includes controls technology, entry systems, HVAC systems service and maintenance, and plumbing engineering.

Specialty Services refers to infrastructure services and specialized industrial plant services, including maintenance and repair of critical infrastructure such as electric, gas, water, sewer, and telecommunications infrastructure.

Reported net revenues increased by 13.0% (4.7% organic) driven by acquisitions, strong growth in inspection, service and monitoring revenues and pricing improvements, partially offset by a decline in project revenues in the HVAC business. Reported and adjusted gross margin increased 200 and 60 basis points, respectively, compared to prior year period driven by planned disciplined project and customer selection, pricing improvements, value capture initiatives and an improved business mix of inspection, services and monitoring revenues. Reported segment earnings increased by 18.5% (18.9% on a fixed currency basis) compared to prior year period. Segment earnings margin was 16.0%, a fourth quarter record and a 70 basis point increase compared to prior year period, primarily due to the increase in adjusted gross margins.

The most recent quarterly results show continued momentum. In its latest earnings report, APi Group Corporation announced record-breaking financial results for the third quarter of 2025, with net revenues reaching $2.1 billion, marking a 14.2% increase from the previous year. The company also reported a significant rise in net income and adjusted EBITDA, demonstrating robust financial health and operational efficiency.

Adjusted net income for Q3 2025 was $174 million, with adjusted diluted EPS of $0.41, up 20.6% year-over-year. Adjusted free cash flow for Q3 was $248 million, with conversion at 88.3% and year-to-date at $434 million.

The expansion into elevators represents APi's most significant recent strategic move. Minnesota-headquartered APi Group Corp. on June 5 announced the completion of its previously announced acquisition of Tampa, Florida-headquartered Elevated Facility Services Group for approximately US$570 million from a fund managed by L Squared Capital Partners. APi said the acquisition establishes "a new statutorily mandated service platform in the highly attractive elevator and escalator services space." It is expected to shift APi's business mix toward 60% of revenues from inspection, service and monitoring.

Elevated Business Overview: $570 million cash consideration, subject to working capital and other standard adjustments. Establishes new platform in the highly attractive elevator and escalator services space. Expected to contribute approximately $220 million in annual revenue at a ~20% Adjusted EBITDA margin.

Becker continued, "We believe there is a long runway of opportunity for Elevated to grow organically and through acquisition. The strength of our balance sheet today and our track record executing complementary bolt-on M&A over the last 20 years makes APi the perfect owner to help Elevated accelerate its growth in the fragmented elevator and escalator services market."

The strategic logic is compelling: elevator inspections, like fire system inspections, are mandated by regulation. Building owners must have their elevators inspected and maintained by licensed technicians. The U.S. elevator services market is approximately $10 billion and highly fragmented, presenting similar consolidation opportunities to what APi found in fire protection decades ago.

At its May 2025 Investor Day, APi unveiled new long-term financial targets that superseded the previous "13/60/80" framework. APi introduced the 10/16/60+ shareholder value creation framework, highlighted by $10B+ of net revenues and adjusted EBITDA margin of 16%+ by 2028. At today's event, APi plans to provide updates to its strategic plan and introduce the following long-term 10/16/60+ financial targets: $10+ billion in net revenues by 2028, with mid-single-digit organic growth, 16%+ adjusted EBITDA margin by 2028, 60%+ of net revenues from inspection, service and monitoring, and $3.0+ billion in cumulative adjusted free cash flow through 2028.

"All 29,000 of our leaders rallied behind our 13/60/80 targets, and I can't wait to see our businesses embrace our new framework and goals. We believe our proven operating model, built on an inspection and service-first strategy, purpose-driven leadership, and a disciplined approach to capital allocation, positions APi for sustained organic growth, margin expansion and value-accretive M&A."

In a strategic move, APi Group's board authorized a new $1 billion share repurchase program, replacing the previous authorization. In addition to the financial targets, APi announced a three-for-two stock split, with the dividend of additional shares scheduled for June 30, 2025, for shareholders of record as of June 16, 2025. Post-split, APi anticipates having approximately 415 million shares of common stock outstanding.

The stock split and share repurchase authorization signal management's confidence in the company's prospects. The 10/16/60+ framework represents a significant step up from previous targets, implying continued margin expansion through mix shift toward higher-margin inspection and service revenue.

IX. Understanding the Fire & Life Safety Industry

To appreciate APi's competitive position, investors must understand the industry dynamics that create such attractive economics.

The global fire & life safety services market was valued at USD 11.75 billion in 2023 and is projected to reach USD 15.16 billion by 2029, growing at a CAGR of 4.35% during the forecast period.

Different market research firms cite different figures depending on how they define the market scope. The global fire and life safety protection services market was valued at USD 148.5 billion in 2024 and is projected to grow from USD 155.5 billion in 2025 to USD 232.5 billion by 2034, registering a CAGR of 4.6%, according to Global Market Insights Inc.

The United States Fire and Life Safety Protections Services Market size was valued at USD 47.39 Billion in 2024 and is projected to reach USD 78.91 Billion by 2033, growing at a CAGR of 5.83% during the forecast period (2025-2033).

U.S. fire & life safety market is worth $15 billion and fast-growing (>9% annual growth rate). Building codes and safety regulations mandate recurring inspections and repairs leading to predictable future revenue. Building activity across commercial, industrial, and residential sectors has grown consistently over the past 10 years.

The key insight is the dominance of testing, inspection, repair, and maintenance work. By Service: The testing, inspection, repair, & maintenance segment holds the largest market share of over 51%. The segment sees significant growth as it focuses on the regular testing, inspection, repair, & maintenance of installed fire and life safety systems to ensure its functionality and compliance with regulatory standards.

This is what makes the industry so attractive: more than half of all revenue comes from recurring, mandated work rather than discretionary new construction. Building owners don't choose whether to have their fire systems inspected—local fire marshals and building codes require it. The only question is which contractor performs the work.

The top companies in the market are APi Group Corp, Pye-Barker Fire & Safety, Johnson Controls, Siemens, and Honeywell, contributing around approximately 35% of the market in 2024.

The fragmentation opportunity remains significant. Even as the largest player globally, APi captures a relatively small share of the overall market. As Becker has noted, in most major metropolitan markets in the U.S., APi has less than 10% market share—and often less than 5%. This fragmentation provides a long runway for continued consolidation.

The industry is fragmented, meaning there are many companies with relatively small shares of the industry's overall revenue, which is attractive to investors looking to grow platform investments through acquisitions.

Regulatory tailwinds support continued growth. Building codes continue to tighten, requiring more sophisticated fire detection and suppression systems. The installed base of fire safety equipment continues to grow as new buildings are constructed. And existing systems require regular inspection and eventual replacement as they age.

The market is growing significantly due to various factors, including integrating smart technologies, emphasizing life safety & emergency preparedness, and shifting towards managed and integrated services. The global fire & life safety services market is further propelled by a shift towards managed and integrated services, increasing burn rate, development of smart cities and infrastructure projects, growing demand from educational institutions, and industrial expansion.

The competitive dynamics favor established players with inspection relationships. Key competitors include EMCOR Group, Johnson Controls, Fluor Corporation, CentiMark Corporation, and Aegion Corporation. APi Group's strengths include its diverse service portfolio, established brand reputation, decentralized structure, and strong financial performance. Johnson Controls offers a wide range of products and services related to building efficiency, fire safety, and security.

The principal competitors vary by geography and service type. In North America, APi faces competition from Pye-Barker Fire & Safety, which has pursued an aggressive acquisition strategy similar to APi's. In Europe and globally, Johnson Controls and Honeywell have significant market positions, though they focus more heavily on products than services.

X. The Business Model Deep Dive: Why APi is Different

The "inspection-first" flywheel is the conceptual heart of APi's competitive advantage. Understanding how it works explains why the business generates such attractive economics.

Traditional contracting follows a simple flow: a building owner or general contractor puts a project out for competitive bid, contractors submit proposals, the lowest qualified bidder wins. Margins are thin, relationships are transactional, and competitive advantage is limited.

APi's model inverts this dynamic. By winning inspection contracts first, APi earns the right to be selective on project work. A building owner who has trusted APi to inspect their fire system for years is far more likely to award the service call when deficiencies are found. And when that owner builds a new facility or renovates an existing one, they're more likely to specify APi for the installation.

Russ Becker, APi's President and Chief Executive Officer stated: "Our record results in 2024 once again demonstrate the strength of our recurring revenue, services-focused business model and the ongoing execution of our strategy by our teammates. We begin 2025 with positive momentum and the demand for the services we offer is strong across our global platform. We remain relentlessly focused on growing inspection, service and monitoring revenue."

The company has achieved remarkable consistency in inspection revenue growth. Reported net revenues increased by 5.8% (1.3% organic) driven by acquisitions, strong growth in inspection, service, and monitoring revenues, and pricing improvements. Management has noted that the company achieved double-digit growth in inspection revenues in its U.S. Life Safety business for multiple consecutive quarters.

The recurring revenue characteristics provide stability. Russell Becker highlighted the company's focus on increasing inspection, service, and monitoring revenues to 60% of total net revenues, which provides resilience against economic fluctuations. He also noted the company's variable cost model, which allows for quick adjustments if needed.

The decentralized operating model enables local responsiveness while capturing scale benefits. APG's core strategy is simple: acquire small established owner-operated life safety businesses, provide them with the support and resources of the mothership and let them operate with autonomy.

M&A remains a core competency. The company has completed over 100 acquisitions during Russell Becker's tenure. Russell Becker indicated plans to spend approximately $250 million on bolt-on M&A, focusing on fire, life safety, security, and elevator and escalator spaces.

Our pipeline remains robust and continues to grow, now including fire protection, electronic security, and elevator services opportunities globally. Most importantly, our value proposition as a forever home for their team continues to resonate with sellers.

The "forever home" positioning is strategically important. Selling business owners care about more than price—they want assurance that their employees will be treated well and their company's identity will be preserved. APi's track record of maintaining acquired company cultures and promoting from within makes it an attractive acquirer, potentially allowing better acquisition terms than competitors.

XI. Bull Case and Bear Case: Framework Analysis

Bull Case

Regulatory Moat: Fire safety inspections are mandated by law and cannot be eliminated through competitive pressure or economic downturn. Building owners must have their systems inspected regardless of market conditions. This provides recession-resistant baseline revenue.

Inspection-to-Service Flywheel: The inspection relationship generates service opportunities, which generate project opportunities, which strengthen inspection relationships. This virtuous cycle creates customer stickiness and cross-selling opportunities that pure project contractors cannot replicate.

Fragmentation Opportunity: Even as the market leader, APi holds single-digit market share in most metropolitan areas. The runway for acquisitive growth extends for decades given thousands of small, regional competitors.

Proven Serial Acquirer: Management has completed 100+ acquisitions with strong track records of integration. The decentralized model allows acquired companies to maintain their cultures while benefiting from APi's scale.

Elevator Expansion: The Elevated acquisition opens a $10+ billion addressable market with similar regulatory dynamics and fragmentation characteristics to fire protection.

Franklin Involvement: Martin Franklin's track record at Jarden (32% IRR over 15 years) provides confidence in capital allocation discipline. His continued involvement signals alignment with long-term shareholder value creation.

Bear Case

Integration Execution: The Chubb integration required fixing dozens of unprofitable branches and separating complex technology systems. Future large acquisitions could present similar challenges.

Labor Intensity: Fire protection services require skilled technicians who must be recruited, trained, and retained. Labor cost inflation and competition for talent could compress margins.

Economic Sensitivity: While inspection revenue is stable, project revenue (still a significant portion of the business) is tied to construction activity. A severe recession would pressure results.

Debt Load: The Chubb acquisition was funded partially with debt. While leverage has declined, interest expense remains meaningful in a higher-rate environment.

Competitive Intensification: Pye-Barker and other consolidators are pursuing similar strategies, potentially bidding up acquisition prices and competing more aggressively for talent and customers.

Regulatory Risk: While unlikely, changes to fire codes or inspection requirements could affect demand. Also, local authorities having jurisdiction can change contractors, though this is rare.

Porter's Five Forces Analysis

Threat of New Entrants (Low): Fire protection requires licensed technicians, established customer relationships, and local market knowledge. New entrants struggle to compete against incumbents with decades of history.

Bargaining Power of Suppliers (Moderate): Equipment manufacturers like Tyco, Honeywell, and others have some pricing power, but service companies can switch suppliers and pass along cost increases to customers.

Bargaining Power of Customers (Low to Moderate): Building owners must have inspections performed—they can't simply choose not to buy. Large national accounts have some negotiating leverage, but switching costs are meaningful.

Threat of Substitutes (Very Low): There are no substitutes for fire protection systems or mandated inspections. Building owners cannot opt out.

Competitive Rivalry (Moderate): While fragmented, competitors include sophisticated players like Johnson Controls and aggressive consolidators like Pye-Barker. Competition for talent and acquisitions is real.

Hamilton Helmer's Seven Powers Framework

Process Power: APi's inspection-first flywheel and decentralized operating model create embedded processes that are difficult to replicate. Competitors can copy the strategy but not easily build the relationships and systems.

Scale Economies: National coverage enables APi to serve multi-location customers efficiently while maintaining local responsiveness. The National Service Group provides coordination that smaller players cannot match.

Switching Costs: Once APi performs inspections and develops documentation on a building's systems, switching to another contractor requires rebuilding institutional knowledge. Long-term relationships make switching costly and risky for building owners.

Counter-Positioning: APi's willingness to prioritize inspection relationships over higher-margin project work creates a business model that project-focused competitors struggle to replicate—doing so would cannibalize their existing business.

Brand: Chubb has 200+ years of heritage; APi's individual brands have deep local market recognition. Brand value manifests in customer trust and employee recruitment.

XII. Key Performance Indicators for Investors

Given APi's business model, we believe investors should focus on the following KPIs:

1. Inspection/Service/Monitoring Revenue Growth and Mix

This is the most important metric to track. Management targets 60%+ of revenue from inspection, service, and monitoring work. Higher mix means more recurring revenue, better margins, and greater recession resistance. Quarterly disclosure of organic inspection revenue growth provides the best signal of business health.

2. Adjusted EBITDA Margin Trajectory

APi has established clear margin targets: 13% in 2025, 16%+ by 2028. Progress toward these targets validates the transformation thesis. Margin expansion should come from mix shift (more inspection/service), operational improvements (particularly in Chubb), and pricing discipline.

Tracking Note

Investors should compare actual results against the 10/16/60+ framework announced at the May 2025 Investor Day: - $10+ billion net revenues by 2028 - 16%+ adjusted EBITDA margin by 2028 - 60%+ of revenues from inspection, service and monitoring - $3.0+ billion cumulative adjusted free cash flow through 2028

Consistent achievement against these targets would validate the investment thesis; material misses would require reassessment.

XIII. Risks and Regulatory Considerations

Accounting Judgments: APi uses significant non-GAAP adjustments including adjustments for acquisitions, restructuring, and one-time items. Investors should track the gap between GAAP and adjusted metrics over time to ensure adjustments don't become structural.

Goodwill Risk: Serial acquirers accumulate significant goodwill on their balance sheets. A material acquisition failure could result in impairment charges, though APi's track record has been strong.

Contract Labor Dependence: A substantial portion of APi's workforce consists of skilled tradespeople whose availability affects the company's ability to service demand. Labor shortages in the construction trades are a persistent industry challenge.

International Currency Exposure: The Chubb acquisition added significant non-U.S. revenue, creating currency translation risk. The company operates in 17 countries with exposure to Euro, British Pound, and various Asia-Pacific currencies.

No Material Legal/Regulatory Overhangs Identified: As of the current filing review, no material pending litigation or regulatory actions appear to threaten the business model. Fire safety regulations are generally tightening rather than loosening, supporting demand growth.

XIV. Conclusion: The Long View

APi Group's journey from a 1926 St. Paul plumbing company to the world's largest life safety services provider reflects a series of patient decisions compounded over time. Reuben Anderson built a foundation. Lee Anderson diversified into fire protection and proved the acquisition model. Russ Becker systematized the acquisition machine and professionalized operations. Martin Franklin and team brought public market discipline and capital allocation expertise.

The business APi has built possesses characteristics that value-oriented investors should find attractive: recurring revenue mandated by regulation, a fragmented industry structure that enables continued consolidation, strong customer relationships that create switching costs, and a proven operating model that can be applied to adjacent verticals like elevator services.

The 10/16/60+ framework provides a clear roadmap: grow revenues to $10 billion through mid-single-digit organic growth and bolt-on M&A, expand margins to 16%+ through mix shift and operational improvements, and generate $3+ billion in cumulative free cash flow for reinvestment.

In summary, we move through the fourth quarter and into 2026 with great momentum. Our inspection, service, and monitoring business continues to expand, our backlog is at a record high, our balance sheet remains strong, and we are confident in our leaders' ability to execute our strategy and deliver against our 2025 targets and our 10-16-60 plus shareholder value creation framework.

The "Industrial Jarden" label that management embraces is both aspirational and instructive. Jarden created extraordinary shareholder value through disciplined acquisition and decentralized management in consumer products. APi aims to do the same in fire and life safety services, but with an even more defensible moat: regulatory mandates that make demand essentially non-discretionary.

Nearly a century after Reuben Anderson started his plumbing business, APi Group inspects fire systems in hospitals, data centers, schools, and office buildings across five continents. The technicians who perform that work rarely make headlines, but they provide a service that building occupants depend on—and that investors can count on regardless of economic conditions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube