Clean Harbors: North America's Hazardous Waste Empire

How a Four-Person Tank Cleaning Business Became a Fortune 500 Environmental Services Powerhouse

I. Introduction: The Quiet Giant Behind America's Cleanups

Picture the chaos following the September 11, 2001 attacks at Ground Zero. Significant clouds of dust filled the air for hundreds of city blocks, bringing with them ash, debris, and harmful particles such as asbestos. As one of the first companies to respond to the site, Clean Harbors got to work setting up decontamination stations for essential workers. Since the Sept. 11 response, Clean Harbors' reputation as the go-to provider for emergency response in North America has only grown—to include the anthrax attacks, Hurricanes Katrina and Rita, the Deepwater Horizon spill, the Kalamazoo River spill, the 2015 avian flu outbreak, and the COVID-19 decontamination efforts.

This is Clean Harbors, Inc. (NYSE: CLH)—a company most investors have never heard of, yet one that sits at the intersection of environmental regulation, industrial necessity, and an extraordinarily defensible competitive moat.

The company posted full-year 2024 revenues of $5.89 billion, driven by 11% growth in its Environmental Services segment, generating full-year net income of $402.3 million. The company now ranks 586th on the Fortune 500—a remarkable journey from its origins as a four-person tank cleaning operation in suburban Boston.

How did Alan McKim build this from nothing? And why does Clean Harbors possess what may be one of the most defensible competitive positions in American industry?

The company operates 870 locations in 630 properties across the U.S. and Canada, including a network of over 100 waste disposal facilities—incinerators, landfills (seven hazardous waste landfills and two non-hazardous waste landfills), and treatment, storage and disposal facilities. Combined, Clean Harbors' ten incinerators represent more than 600,000 tons of incineration capacity per year, or 60% of the total available commercial incineration capacity in North America.

That statistic alone—sixty percent of North America's commercial hazardous waste incineration capacity—tells you nearly everything you need to know about Clean Harbors' competitive position. But understanding how the company got here requires traveling back to 1980, to a young entrepreneur with a single truck and a vision most considered unremarkable.

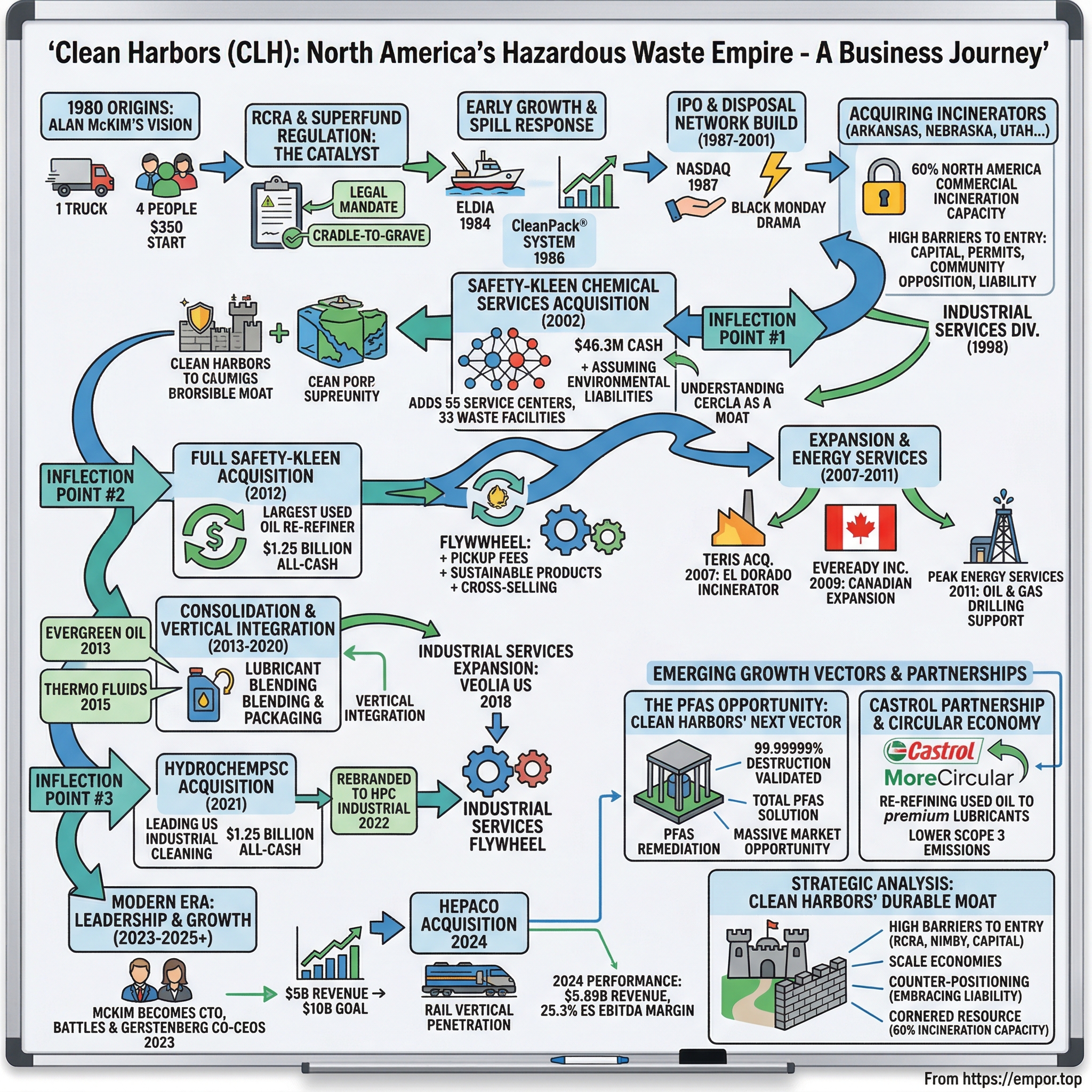

II. The Origin Story: Alan McKim's Vision (1980–1987)

The Founding Context

As detailed in his autobiography, McKim started Clean Harbors in 1980 with just $350, naming it after his love of Boston Harbor. The company, with only a handful of employees at its inception, was initially geared toward cleaning up oil spills and tanks. He quickly found three inexpensive vacuum trucks through a bankruptcy auction and went to work.

McKim started Clean Harbors in 1980 after spending his first few working years at a small oil clean-up company, Jet-Line. The timing proved fortuitous—though not immediately obvious.

Clean Harbors was founded on March 24, 1980, by Alan McKim in Brockton, Massachusetts, initially operating as a four-person tank cleaning business with a single truck, focused on servicing petroleum industry clients by removing hazardous residues from oil tanks. This venture emerged in the wake of heightened environmental awareness and regulations following the 1978 Love Canal disaster, which exposed groundwater contamination from chemical waste and spurred the passage of the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA) in December 1980.

The Regulatory Tailwind: RCRA and Superfund

To understand Clean Harbors' trajectory, one must first understand the regulatory environment that created the entire hazardous waste management industry.

The Resource Conservation and Recovery Act (RCRA) and the Comprehensive Environmental Response, Compensation and Liability Act (CERCLA) govern the Section's work to address contamination of the nation's lands, groundwater, waterways and their sediments. Passed in 1976, RCRA—intended as a "cradle-to-grave" regulatory scheme—was enacted to control the handling of hazardous waste from its creation through any storage, treatment, transportation, and ultimate disposal.

The Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), commonly known as Superfund, was enacted by Congress on December 11, 1980. This law created a tax on the chemical and petroleum industries and provided broad Federal authority to respond directly to releases or threatened releases of hazardous substances that may endanger public health or the environment. Over five years, $1.6 billion was collected and the tax went to a trust fund for cleaning up abandoned or uncontrolled hazardous waste sites.

Arguably the most notable provisions of the RCRA statute are included in Subtitle C, which directs EPA to establish controls on the management of hazardous wastes from their point of generation, through their transportation and treatment, storage and/or disposal. Because RCRA requires controls on hazardous waste generators, transporters, and treatment, storage and disposal facilities, the overall regulatory framework has become known as the "cradle to grave" system.

This regulatory architecture created something unprecedented: a legal mandate that companies properly handle hazardous materials, combined with severe liability for improper disposal. The combination effectively created a captive customer base—industrial companies that could face crippling lawsuits and criminal penalties if they failed to properly manage their hazardous waste.

McKim started his business right as this regulatory regime took hold, positioning Clean Harbors to ride a wave of compliance-driven demand.

Early Growth Trajectory

The growth was immediate and sustained. By the end of its second year, Clean Harbors had grown to 18 employees and $1.5 million in revenues. By year three, revenue had increased to $4.2 million with 34 employees. Revenues continued climbing, approaching $50 million by 1986.

First Major Emergency Response

Clean Harbors' first major project came in 1984 when it removed 130,000 gallons of fuel oil from the tanker Eldia, which became the largest ship to have been beached off Cape Cod. This emergency response work established the company's reputation for rapid mobilization and complex environmental remediation—capabilities that would prove invaluable in building relationships with major industrial clients.

Building the Service Model

The company's core offerings expanded to include emergency spill response, industrial cleaning and maintenance, laboratory chemical packing via its proprietary CleanPack® system introduced in 1986, and used oil re-refining.

The CleanPack® service deserves attention as an early example of McKim's strategic thinking. Rather than simply competing on price for commodity services, Clean Harbors developed proprietary service methodologies that created switching costs and recurring revenue streams. A university or research facility that standardized on CleanPack® for laboratory chemical disposal wasn't likely to switch vendors casually—the training, procedures, and relationships became embedded in operations.

Over the years, Clean Harbors took a dominant position in its industry nationwide. Through it all, McKim has been a relatively low-key leader, rarely the subject of publicity.

This low-key approach proved strategically valuable. While flashier companies attracted media attention and regulatory scrutiny, McKim quietly built infrastructure and customer relationships that would prove nearly impossible to replicate.

III. Going Public & Building the Disposal Network (1987–2001)

The IPO Drama: Black Monday and the Path Forward

In 1986, founder McKim began receiving queries from parties interested in funding Clean Harbors. A venture capitalist asked if he would consider selling part of the company to raise money, while an investment banker asked if he would think about taking the company public. McKim considered both private placement and going public. By that time, Clean Harbors had more than $11 million in debt. McKim himself was personally liable for much of this. McKim was also interested in sharing profits with his employees by letting them own stock. McKim eventually decided to take both routes, first selling 18 percent of the company to Boston-area venture capitalists, and then taking Clean Harbors public.

But the road to going public turned out to be bumpier than McKim expected. McKim laid plans in the spring of 1987 to take Clean Harbors public in the early fall.

The timing could not have been worse.

On October 19, 1987, the stock market slid, an enormous "correction" to the bull market memorialized as Meltdown Monday. From an August high of close to 3,000, the Dow Jones Industrial Average fell to 1,739. Clean Harbors' underwriters were nervous about the IPO, and discussed postponing the offering or canceling it. Ultimately, Clean Harbors and its underwriters decided to go ahead with the IPO, but to offer one million shares instead of 1.5 million, and at $9 instead of $15. This would bring in only $9 million instead of the hoped-for $22 million. The company went public on the NASDAQ on November 24.

Black Monday was a global, severe and largely unexpected stock market crash on Monday, October 19, 1987. Worldwide losses were estimated at US$1.71 trillion. Black Monday dramatically reduced both the number of companies planning to go public and the amount of cash available for other firms to raise in the equity market. On Black Monday, 229 businesses had filed papers with the SEC declaring their intention to issue public stock for the first time; about 45 percent abandoned those plans within nine months after the crash.

Clean Harbors was one of the companies that chose to proceed—a decision that demonstrated McKim's risk tolerance and long-term orientation.

Yet six months later, Clean Harbors' stock had risen from $9 to more than $15. The company then made a secondary offering later in 1987, and that year paid off some $12 million in debt. Founder Alan McKim retained about 60 percent ownership of Clean Harbors.

Strategic Asset Acquisitions: Building the Moat

With public market capital, Clean Harbors began the acquisition strategy that would define its next four decades.

In 1989, Clean Harbors purchased Chem Clear, Inc., an industrial aqueous waste treatment company. This acquisition firmly established Clean Harbors as a waste disposal provider, and the 1995 purchase of an incinerator in Kimball, Nebraska, expanded resources in this area.

Going public set the stage for expansion. Clean Harbors, still solely an environmental services company, purchased Occupational Safety and Health Administration (OSHA) Resource Conservation and Recovery Act (RCRA) certified hazardous waste incinerators in Arkansas, Nebraska, Ontario, Quebec, Texas and Utah, which it continues to own and operate to this day.

This incinerator acquisition strategy represents one of the most underappreciated aspects of Clean Harbors' business model. Hazardous waste incinerators require:

- Extraordinary capital investment — High-temperature incineration facilities cost hundreds of millions to construct

- Multi-year permitting processes — Obtaining RCRA permits requires years of environmental studies and public hearings

- Community acceptance — "Not in my backyard" opposition makes new facilities nearly impossible to site

- Technical expertise — Operating within EPA emissions limits requires specialized knowledge

- Ongoing regulatory compliance — Facilities face continuous EPA oversight

By the mid-1990s, the regulatory and community opposition environment had made building new hazardous waste incinerators essentially impossible. Clean Harbors recognized this early and aggressively acquired existing permitted facilities, creating a moat that new competitors simply cannot cross.

Building Industrial Services Division

In 1998, Clean Harbors formed its Industrial Services division. Their industrial personnel perform cleaning and maintenance services that require fast turnaround, such as hydro-blasting, liquid and dry vacuuming, sodium bicarbonate blasting, steam cleaning, and chemical cleaning of equipment and systems.

This division created a strategic flywheel: industrial cleaning services generate hazardous waste that flows to Clean Harbors' own disposal facilities. The company captures margin on the cleaning work and again on the disposal, while competitors who only offer one service cannot match the integrated value proposition.

Early Regulatory & Operational Challenges

The path wasn't without obstacles. Early challenges included navigating complex environmental compliance and liabilities under RCRA and CERCLA. The company faced a 1991 permit denial for a proposed incinerator in Massachusetts due to local community opposition and regulatory hurdles. Clean Harbors also assumed Superfund-related remediation responsibilities at various sites inherited through acquisitions and operations.

These obstacles tested the company's resilience but ultimately reinforced its foundational model of integrated hazardous waste management. More importantly, the community opposition that blocked Clean Harbors' Massachusetts expansion simultaneously prevented competitors from building competing facilities—solidifying existing asset positions.

IV. Inflection Point #1: The Safety-Kleen Chemical Services Acquisition (2002)

The Safety-Kleen Story & Bankruptcy

Safety-Kleen was started in the late 1950s and early 1960s when Ben Palmer invented the parts washer which he decided to lease to customers and service by removing and replenishing the solvent in the machines. In 1968, the Safety-Kleen business was acquired by Chicago Rawhide, and under the leadership of Don Brinckman Safety-Kleen became a publicly traded company and enjoyed tremendous growth and business success over 30 years, eventually joining the Fortune 500.

In 1954, Ben Palmer invented the PartsWasher. Deemed the "Safety-Kleen" washer, it was a success from the start. Palmer believed that spelling the name as "Kleen" instead of "Clean" would garner attention and that it did. In early 1960s, Palmer decided not to sell his machine, but rather to lease it to the customer and provide services such as removing and replenishing the used solvent. This practice is still maintained today through the Safety-Kleen service structure.

The Safety-Kleen model was elegant: rather than selling parts washers, the company leased them and serviced them regularly, collecting the used solvent and replenishing with fresh. This created recurring revenue, customer relationships, and a waste stream that Safety-Kleen could manage.

Unfortunately, success led to overexpansion. The company filed for bankruptcy in 2000 after an ill-fated merger and accounting irregularities.

The Transformational Deal

Clean Harbors saw opportunity in Safety-Kleen's distress.

In 2002, Clean Harbors acquired the assets of the Chemical Services Division of Safety-Kleen. This purchase added 55 service centers, 33 waste management facilities, and 4,400 employees to Clean Harbors' existing resources.

The deal structure was remarkable: Clean Harbors purchased these assets for $46.3 million in cash plus the assumption of approximately $265 million in environmental liabilities. This acquisition tripled the company's size at the time and marked its initial foray into waste recycling and broader chemical services.

Why would Clean Harbors assume hundreds of millions in environmental liabilities? Because McKim understood something crucial: environmental liabilities at waste management facilities aren't bugs—they're features. The same CERCLA liability framework that created customer demand for Clean Harbors' services also made competitors wary of acquiring disposal assets. By demonstrating expertise in managing these liabilities, Clean Harbors could acquire assets at prices that reflected seller anxiety rather than intrinsic value.

Integration Challenges & Lessons

The integration proved challenging. Revenue for 2003 was less than expected, at around $600 million. By that time, Clean Harbors appeared to be recovering from the shock of digesting such a large acquisition. The company claimed its fourth quarter of 2004 was its best ever, and it finished the year with a 5 percent increase in revenue over the year previous, to $643.2 million.

This experience informed Clean Harbors' subsequent acquisition playbook: acquire distressed assets at favorable prices, invest in integration, and extract synergies over a multi-year horizon. The pattern would repeat numerous times over the following decades.

V. Expansion Era: Energy Services & Canadian Growth (2007–2011)

Teris Acquisition (2007)

In 2007, Clean Harbors acquired Teris, LLC, along with its 550 employees, several field locations, an incineration facility in El Dorado, Arkansas, and a treatment, storage, and disposal facility.

The El Dorado facility proved particularly valuable. North America's most advanced incinerator is now keeping the air cleaner for all of us. The new incinerator at the El Dorado, Arkansas facility meets new source MACT emission standards, which are ten times more stringent for metals and particulate matter.

Eveready Inc.: The Canadian Expansion (2009)

In 2009, Clean Harbors acquired Eveready Inc., a Canadian company providing industrial maintenance and production, lodging, and seismic services. With the addition of more than 2,100 employees, 79 locations, and a service fleet of over 2,400 trucks and trailers, this purchase expanded energy and industrial service offerings and geographic reach.

The Eveready acquisition for approximately $387 million represented Clean Harbors' entry into the oil and gas services sector. Early investments from Clean Harbors' founding until 2009 were primarily in the environmental services, waste management and industrial services areas. It made its first major acquisition in the oil and gas area in 2009 and has since further expanded in that sector through organic growth and acquisitions.

Peak Energy Services (2011)

In 2011, Clean Harbors acquired Peak Energy Services, adding the ability to support oil and gas drilling operations through surface rentals and specialized liquid, solid, and sludge processing. The acquisition, for approximately CAD $202 million, added specialized oilfield services primarily in Western Canada.

The energy services expansion represented a calculated bet. Oil and gas operations generate significant hazardous waste streams, and by offering integrated services—industrial cleaning plus waste disposal—Clean Harbors could capture multiple margin layers while deepening customer relationships.

VI. Inflection Point #2: The Full Safety-Kleen Acquisition (2012)

The Deal Structure

A decade after acquiring Safety-Kleen's Chemical Services Division, Clean Harbors returned for the rest.

Clean Harbors announced it has signed a definitive agreement to acquire Safety-Kleen, Inc., the largest re-refiner and recycler of used oil in North America and a leading provider of parts cleaning and environmental services. Under the terms of the agreement, Clean Harbors would purchase Safety-Kleen in an all-cash transaction valued at $1.25 billion.

Clean Harbors financed the all-cash transaction valued at $1.25 billion through the combination of $289 million of existing cash, $370 million in net proceeds from its recently completed follow-on offering of common stock and $591 million in net proceeds from its recently completed senior notes offering.

Strategic Rationale

"The acquisition of Safety-Kleen aligns perfectly with our strategy of expanding our Environmental Services business in North America," said Alan S. McKim. "Safety-Kleen brings well-established leadership positions in several important markets, including parts cleaning, small quantity waste generators and used oil recycling. We expect the transaction to drive a substantial increase in waste volumes into our waste disposal treatment network. Safety-Kleen services more than 200,000 customer locations – we are looking forward to the substantial cross-selling opportunities we anticipate across our combined customer base."

Scale and Synergies

In 2012, Clean Harbors completed the largest acquisition in its history with the purchase of Safety-Kleen, a leading North American used oil recycling and re-refining, parts cleaning, and environmental solutions company. The acquisition added approximately 4,200 employees serving more than 200,000 customer locations across the United States, Canada, and Puerto Rico.

In December 2012, Safety-Kleen was purchased by Clean Harbors, Inc., forming the largest environmental services company in North America, approaching $4 billion in annual revenue.

For 2012, revenues were projected at $3.72 billion to $3.77 billion. The Company expected combined 2013 adjusted EBITDA to be in the range of $605 million to $620 million, including approximately $30 million of acquisition-related synergies.

The Re-Refining Model

Clean Harbors also owns Safety-Kleen, the largest re-refiner and recycler of used oil in North America. The Safety-Kleen subsidiary produces around 150 million gallons of base oil annually.

The used oil re-refining business deserves special attention. When a mechanic changes oil in a vehicle, that used oil contains valuable base oil that can be recovered through re-refining. Safety-Kleen created a collection network spanning 200,000+ customer locations—auto shops, fleet maintenance facilities, manufacturers—that generates recurring pickup revenue while providing feedstock for re-refining operations.

This creates another flywheel: the collection network generates fees, the re-refined oil sells as a sustainable product, and the customer relationships enable cross-selling of other Clean Harbors services.

VII. Consolidation & Vertical Integration (2013–2020)

Used Oil Infrastructure Build-Out

In 2013, Clean Harbors acquired Evergreen Oil, a California-based company specializing in the recovery and re-refining of used oil. In 2015, the company acquired Thermo Fluids, Inc., further expanding used oil collection and recycling capabilities and strengthening presence in the western United States.

From 2014 through 2017, Clean Harbors continued investing in used oil collection, re-refining, and lubricant blending and packaging by acquiring and building capabilities to distribute finished lubricants.

This represented vertical integration: rather than simply collecting and re-refining used oil, Clean Harbors began blending and packaging finished lubricant products. The company could now capture margin at every stage—collection, re-refining, blending, and distribution.

Industrial Services Expansion

The 2017 acquisition of Lonestar West for CAD $44 million introduced advanced hydro excavation services and extended operations into the Canadian market. In 2018, Clean Harbors acquired Veolia North America's U.S. industrial cleaning business for $120 million, enhancing its scale and capabilities in industrial services.

By this point, Clean Harbors' strategy had become clear: build the most comprehensive environmental and industrial services platform in North America, with integrated disposal capacity that competitors cannot replicate.

VIII. Inflection Point #3: HydroChemPSC Acquisition (2021)

The Deal

On October 8, 2021, Clean Harbors announced the completion of its acquisition of HydroChemPSC ("HPC"), a leading U.S. provider of industrial cleaning, specialty maintenance and utilities services. Clean Harbors purchased HPC from an affiliate of Littlejohn & Co., LLC, for $1.25 billion in an all-cash transaction. The acquisition was financed through a combination of existing cash and proceeds from Clean Harbors' new 2021 Incremental Term Loan financing that was completed in conjunction with the transaction. The 2021 Incremental Term Loans were issued in the aggregate principal amount of $1.0 billion at a rate of Libor +200 basis points.

Scale and Strategic Fit

With more than 5,000 employees and 240 service locations throughout the country, HPC serves a broad range of end markets including refining, chemical and utilities.

For 2021, as a standalone company, HPC estimated that it would generate revenues of approximately $744 million and Adjusted EBITDA of approximately $115 million. Clean Harbors expects to achieve cost synergies of $40 million from the acquisition after the first full year of operations.

"HPC is an established leader in Industrial Services, with proprietary technology and a dedicated manufacturing center to fabricate its own tools. The addition of HPC's experienced team, considerable assets and customer base create significant strategic benefits to Clean Harbors beyond just expanding the size and scale of our operations," said Alan S. McKim.

Rebranding

In 2022, HydroChemPSC was rebranded as HPC Industrial, integrating the acquisition into Clean Harbors' broader industrial services platform.

The HPC acquisition reinforced the strategic flywheel: industrial cleaning services at refineries and chemical plants generate hazardous waste streams that flow to Clean Harbors' disposal network. The integrated offering creates customer lock-in while generating multi-layer margins.

IX. Modern Era: HEPACO & Current Operations (2023–2025)

Leadership Transition

Mr. McKim, who founded Clean Harbors in 1980, became Executive Chairman and Chief Technology Officer of the Company in March 2023 as part of a planned transition. Before that, he served as Chairman of the Board of Directors and Chief Executive Officer of the Company since its inception.

McKim's transition to CTO this spring came alongside the appointment of two longtime Clean Harbors executives as co-CEOs: Chief Operations Officer Eric Gerstenberg and Chief Financial Officer Mike Battles. "Succession" jokes aside, both the step-down to CTO and the co-CEO appointments are increasingly popular in the corporate world. Oracle founder Larry Ellison appointed co-CEOs as his replacements when he stepped down from that company's top job in 2014, to become CTO.

Battles, who joined the company in 2013 as Senior Vice President, Corporate Controller, and Chief Accounting Officer, had served as Executive Vice President and Chief Financial Officer since 2016 prior to his promotion. Gerstenberg, with the company since 2005, was previously Chief Operating Officer for eight years, overseeing operational aspects of environmental and industrial services. This co-CEO structure was designed to leverage their complementary expertise in finance and operations to drive continued growth.

The company grew to $5 billion in annual revenue over four decades. But McKim hopes it can double that number again, to $10 billion, over the next five years under the guidance of Gerstenberg and Battles. "Although I feel like I have the energy today, it just made sense when we hit that $5 billion mark to take a step back."

McKim is also vice chair of Northeastern University's Board of Trustees, half the namesake of the D'Amore-McKim School of Business, and the founder, chairman and former CEO of Clean Harbors. He combined "tech" and "waste cleanup" throughout his career. In the book's preface, McKim recounts waking up to a text message informing him that Clean Harbors had fallen victim to a ransomware attack.

McKim is a member of the board of trustees at Northeastern University and on September 12, 2012, he joined Richard D'Amore to donate $60 million to the College of Business Administration. It was the 4th largest donation to a business school in US history. In honour of the donation, Northeastern renamed its business school to the D'Amore-McKim School of Business.

HEPACO Acquisition (2024)

On March 25, 2024, Clean Harbors announced the completion of its acquisition of HEPACO, a leading environmental provider of field and emergency response services in the Eastern United States. Clean Harbors purchased HEPACO from Gryphon Investors for $400 million in cash. The acquisition was financed through proceeds from a recently completed $500 million expansion of the Company's Term Loan facility.

On an adjusted basis, HEPACO generated full-year 2023 EBITDA of approximately $36 million on $270 million of revenue. Clean Harbors expects the acquisition to generate cost synergies of approximately $20 million after the first full year of operations, which equates to a post-synergy acquisition multiple of 7.1 times.

Headquartered in Charlotte, North Carolina, HEPACO has approximately 1,000 employees and 900 vehicles at 40 regional locations in 17 states.

Private equity firm Gryphon acquired HEPACO in 2016 and more than tripled its revenue since then. HEPACO, which is an acronym for Hazardous Environmental Products Abatement Company, has completed seven add-on acquisitions with Gryphon Investors.

"One thing that HEPACO has really brought to the table is their penetration in the rail vertical. They've had some great relationships with some of the largest railroads and have got a great team that responds to not only events, but ongoing services for the rail industry," said Gerstenberg.

Current Operations and Financial Performance

"Our fourth-quarter results were in line with our expectations as our Environmental Services (ES) segment capped a record 2024 with a robust performance, including the 11th consecutive quarter of year-over-year margin growth," said Mike Battles, Co-Chief Executive Officer. "The segment benefited from steady demand, strong waste collection volumes, a healthy flow of project work and favorable pricing. For the full year the segment saw 11% top-line growth and annual Adjusted EBITDA margin exceeded 25%."

Adjusted EBITDA margin in the ES segment expanded by 90 basis points to 25.3% on the strength of 11% revenue growth combined with a 15% increase in Adjusted EBITDA. Beyond financial performance, the company achieved significant operational milestones in 2024, including more than 20,000 emergency response events.

X. The PFAS Opportunity: Clean Harbors' Next Growth Vector

The PFAS Challenge

Polyfluoroalkyl substances (PFAS) or "forever chemicals" are linked to harmful health effects in humans and animals. These chemicals, used in everything from non-stick cookware to firefighting foam, have contaminated groundwater across the country and present a massive remediation challenge.

The EPA and other federal and state regulatory authorities have begun establishing frameworks to protect human health from the impacts of these compounds. The first major step at the federal level was the creation in 2024 of a drinking water standard. Further steps are needed to establish rules for soil remediation and acceptable methods for PFAS destruction.

Clean Harbors' Positioning

Clean Harbors announced the successful results of its latest PFAS study, which affirms that its commercial high-temperature, RCRA-permitted incineration facilities can reliably and safely destroy multiple forms of PFAS (per- and poly-fluorinated alkyl substances), the "forever chemicals" that pose significant human health risks. The testing protocols were an extension of the initial tests the Company conducted in 2021 and 2022 using U.S. Environmental Protection Agency (EPA) standards. The latest study was specifically designed to demonstrate that Clean Harbors' high-temperature combustion process—ranging from 2,000-2,200 degrees Fahrenheit—could achieve destruction of PFAS compounds while testing for the EPA's stringent new OTM-50 and 0010 emission standards.

Clean Harbors conducted a PFAS incineration study in conjunction with the EPA and DOD in November of 2024. Results, which were reviewed by third-party experts, were issued in September of 2025 and included: Clean Harbors' RCRA-permitted, high-temperature incineration ensures safe and permanent thermal destruction of PFAS in its various forms. Destruction can be achieved cost effectively at commercial scale as well as 99.9999% effective in thermal destruction.

The most recent test found that Clean Harbors' facility could destroy up to 99.9999% of PFAS chemicals in certain materials, achieving air emissions more than two orders of magnitude lower than the strictest ambient air quality standard. Clean Harbors Co-CEO Eric Gerstenberg testified at a U.S. Senate Environment and Public Works committee hearing.

"Given that customers are facing PFAS in multiple forms, we introduced our 'Total PFAS Solution' in 2024 consisting of eight core elements and providing customers with a range of services to meet all their needs, from analysis to water filtration to remediation to disposal. Today, Clean Harbors remains the only company that can offer an end-to-end, single-source answer for any PFAS need, and at a commercially scalable level."

"We're doing about $50 million to $70 million of PFAS-related work through our network from all the different opportunities," Gerstenberg said, adding that the PFAS pipeline is growing between 15% to 20% each quarter "as we go into 2025."

The Market Opportunity

"Given that customers are facing PFAS in multiple forms, we introduced our 'Total PFAS Solution' in 2024. Today, Clean Harbors remains the only company that can offer an end-to-end, single-source answer for any PFAS need, and at a commercially scalable level," said Battles. "Based on the results of this latest rigorous study, we continue to view our end-to-end solution and thermal destruction at our RCRA-permitted facilities as the safest and most viable option for addressing and eliminating PFAS, which in total represents a massive market opportunity in the years ahead."

XI. The Castrol Partnership and Circular Economy

Used Oil Re-Refining at Scale

Castrol®, the global lubricant brand, announced the launch of 'Castrol MoreCircular', designed to reduce the carbon footprint of business lubricants in the United States. 'Castrol MoreCircular' encompasses the entire process of collecting used oil from business customers, re-refining it and integrating re-refined base oil into premium lubricants for supply to businesses. 'Castrol MoreCircular' has been created in collaboration with Safety-Kleen, an environmental services subsidiary of Clean Harbors Inc. Following successful market trials, Safety-Kleen and Castrol signed a multi-year collaboration agreement.

"Safety-Kleen is proud to partner with Castrol, a recognized industry leader, to help to bring increased circularity to the United States lubricants industry," said Brian Weber, President of Safety-Kleen Sustainability Solutions. "We are North America's largest collector of used oil with more than 200 branch locations that safely and compliantly collect more than 250 million gallons annually."

Of the more than one billion gallons of used oil generated annually in the United States, only around 20% are currently re-refined back to base oils. With the launch of 'MoreCircular,' Castrol is moving towards embracing circularity.

The used oil is re-processed, enabling around 70% of it to be recovered as base oil. Re-refined base oil is combined with Castrol's cutting-edge technology to blend premium lubricants, resulting in an estimated 20-40% lower carbon footprint compared to Castrol's traditional products.

This partnership represents a sustainability premium opportunity. As corporations face pressure to reduce Scope 3 emissions (emissions from their supply chain), lower-carbon-footprint lubricants become attractive—potentially commanding premium pricing while aligning with ESG mandates.

XII. Strategic Analysis: Why Clean Harbors Has a Durable Moat

Porter's Five Forces Analysis

Threat of New Entrants: VERY LOW

The barriers to entry in hazardous waste disposal are perhaps the highest of any industry in America:

- Regulatory barriers: Obtaining RCRA permits for new hazardous waste facilities requires years of environmental studies, public hearings, and regulatory approvals

- Community opposition: "Not in my backyard" (NIMBY) activism makes siting new facilities virtually impossible

- Capital intensity: Building a permitted hazardous waste incinerator costs hundreds of millions of dollars

- Technical expertise: Operating within EPA emissions limits requires specialized knowledge accumulated over decades

- Liability concerns: CERCLA liability deters capital from entering the space

Clean Harbors' ownership of incinerators, landfills, and wastewater treatment facilities gives it operational control and cost advantages that many competitors cannot match.

Supplier Power: LOW

Clean Harbors' scale allows it to negotiate favorable terms with equipment manufacturers, fuel suppliers, and chemical vendors. The company's proprietary equipment manufacturing capability (inherited from HPC) further reduces supplier dependency.

Buyer Power: MODERATE

Large industrial customers have some negotiating leverage, but switching costs are high: - Established compliance relationships and documentation - Proprietary service methodologies (CleanPack®, etc.) - Integration with customer ERP systems - Liability concerns from disrupting established waste chains

The regulatory requirement for proper hazardous waste disposal also makes this spend non-discretionary—customers cannot simply stop generating hazardous waste.

Threat of Substitutes: VERY LOW

There are few substitutes for proper hazardous waste disposal. Companies can reduce waste generation at the margin, but industrial processes inherently create hazardous byproducts that require professional management.

Competitive Rivalry: MODERATE

The Hazardous Waste Management Market is expected to reach USD 52.94 billion in 2025 and grow at a CAGR of 6.54% to reach USD 72.66 billion by 2030. Veolia Environnement SA, Waste Management Inc., Clean Harbors Inc., Suez SA and Republic Services Inc. are the major companies operating in this market.

The Hazardous Waste Management Market is moderately concentrated. Industry consolidation is advancing as vertically integrated leaders seek economies of scope.

While competition exists, Clean Harbors' integrated model—collection, transportation, treatment, disposal, and recycling—creates advantages that point-solution competitors cannot match.

Hamilton Helmer's 7 Powers Framework

1. Scale Economies: STRONG

Clean Harbors' fixed-cost infrastructure—incinerators, landfills, treatment facilities—delivers improving unit economics as volume grows. Competitors without similar scale face structural cost disadvantages.

2. Network Effects: MODERATE

The company's 870 locations create a network effect: more collection points mean faster service and lower transportation costs, which attracts more customers, which justifies more collection points. The Safety-Kleen parts washer network (200,000+ customer locations) is particularly powerful.

3. Counter-Positioning: STRONG

Clean Harbors' willingness to assume environmental liabilities represents counter-positioning. Competitors view these liabilities as risks to avoid; Clean Harbors views them as moat-building opportunities. This difference in perspective allows Clean Harbors to acquire assets at attractive prices while competitors hesitate.

4. Switching Costs: MODERATE TO STRONG

Established compliance relationships, proprietary service methodologies, and integrated waste management programs create meaningful switching costs. A refinery that has standardized on Clean Harbors for industrial cleaning, waste disposal, and emergency response faces significant disruption from changing vendors.

5. Branding: MODERATE

In hazardous waste management, brand reputation centers on reliability, compliance, and safety. Clean Harbors' track record at high-profile events (9/11, Deepwater Horizon) provides credibility that newer competitors lack.

6. Cornered Resource: VERY STRONG

With over 60 percent of North America's incineration capacity, Clean Harbors' five facilities in the United States and Canada guarantee they can meet any requirement from any customer.

This is Clean Harbors' most powerful competitive advantage. The permitted incineration and landfill capacity cannot be replicated—regulatory and community opposition make building new facilities essentially impossible. This capacity is quite literally a cornered resource.

7. Process Power: MODERATE

Decades of operational experience have created process advantages in complex remediation projects. The company's emergency response capabilities—honed through countless disasters—represent institutional knowledge that cannot be easily replicated.

Competitive Comparison

Enviri has viewed the hazardous waste business as a platform for investment since it acquired Clean Earth, as well as Stericycle's Environmental Solutions business, in 2019 and 2020, respectively. The segment's competitors include U.S. Ecology, which Republic Services acquired in 2022; Clean Harbors; Veolia; and Reworld. But Enviri noted in its annual report that Clean Earth operates in "a very fragmented, regionally-driven market."

Clean Harbors' primary competitors include:

- Veolia: Global environmental services giant with strong European presence but more limited North American hazardous waste infrastructure

- Republic Services: Focused on municipal solid waste with hazardous waste capabilities through U.S. Ecology acquisition

- Waste Management: Largest waste company in North America but primarily focused on non-hazardous municipal and commercial waste

- Reworld (formerly Covanta): Strong in waste-to-energy but limited hazardous waste disposal capacity

None of these competitors can match Clean Harbors' integrated hazardous waste disposal capacity—particularly its 60% share of commercial incineration capacity.

XIII. Bull and Bear Cases

The Bull Case

1. PFAS Remediation Represents a Multi-Decade Opportunity

PFAS contamination is widespread—present in groundwater, soil, and biosolids across the country. As EPA regulations tighten, the remediation market could be worth tens of billions of dollars. Clean Harbors has validated PFAS destruction capability and operates the only commercial-scale solution.

2. Regulatory Moat Deepens Over Time

Every year that passes without new hazardous waste incinerators being built strengthens Clean Harbors' competitive position. Community opposition to new facilities shows no signs of abating.

3. Infrastructure Investment and Manufacturing Reshoring

As manufacturing returns to North America and infrastructure spending accelerates, hazardous waste generation should grow, increasing demand for Clean Harbors' disposal capacity.

4. Sustainability Premium

The Castrol partnership demonstrates potential for sustainability-driven premium pricing. As corporations face pressure to reduce emissions, Clean Harbors' re-refining and circular economy offerings become more valuable.

5. Acquisition Optionality

Clean Harbors' balance sheet and cash flow generation provide optionality for continued acquisitions, with management demonstrating consistent discipline in deal evaluation and integration.

The Bear Case

1. Energy Sector Exposure

The Safety-Kleen Sustainability Solutions segment depends partly on base oil and lubricant pricing, which correlates with energy markets. Electric vehicle adoption could reduce used motor oil volumes over time, though the transition timeline remains uncertain.

2. Regulatory Risk Cuts Both Ways

While regulation creates demand, it also creates compliance risk. Changes in EPA policy could affect permit requirements, disposal methods, or liability frameworks.

3. Integration Execution Risk

Clean Harbors has made numerous acquisitions, each requiring successful integration. While the company's track record is strong, execution missteps could affect returns.

4. Economic Cyclicality

Industrial services demand correlates with manufacturing and refining activity. Economic downturns reduce waste generation and pricing power.

5. Environmental Liability Tail Risk

The company has assumed significant environmental liabilities through acquisitions. While management has demonstrated expertise in managing these liabilities, unexpected issues could emerge.

XIV. Key Performance Indicators to Watch

For investors monitoring Clean Harbors, three KPIs merit particular attention:

1. Environmental Services Segment Adjusted EBITDA Margin

This metric captures pricing power, operating efficiency, and disposal capacity utilization. Adjusted EBITDA margin in the ES segment expanded by 90 basis points to 25.3%. Continued margin expansion signals pricing power and operating leverage; compression could indicate competitive pressure or capacity oversupply.

2. Incinerator Utilization Rate

Incinerator utilization was 79%, down from 80% due to weather-related outages and planned maintenance. This rate indicates demand for Clean Harbors' most irreplaceable asset. Sustained high utilization supports pricing; declining utilization could signal demand weakness.

3. PFAS Revenue Run-Rate Growth

Management has disclosed that PFAS-related work generates $50-70 million annually with 15-20% quarterly pipeline growth. Tracking this growth rate provides visibility into the emerging PFAS remediation opportunity and Clean Harbors' market share gains.

XV. Conclusion: The Quiet Compounding Machine

Clean Harbors represents something rare in modern markets: a company with genuine structural competitive advantages, operated by a founder who has demonstrated discipline over four decades, positioned in an industry with regulatory tailwinds and secular demand drivers.

The company grew to $5 billion in annual revenue over four decades. McKim hopes it can double that number again, to $10 billion, over the next five years.

Whether that ambitious goal is achieved, Clean Harbors' fundamental value proposition remains intact: industrial America generates hazardous waste that must be properly managed, Clean Harbors owns 60% of the incineration capacity required to destroy that waste, and building competing capacity is essentially impossible.

Clean Harbors was instrumental in recovering New York's World Trade Center site after 9/11, cleaning up the 2010 Deepwater Horizon oil spill, and medically decontaminating tens of thousands of sites during the height of the COVID-19 pandemic. Taking decisive action is in the company's DNA.

From a four-person tank cleaning business in Brockton, Massachusetts, to a Fortune 500 environmental services powerhouse, Clean Harbors has demonstrated that unsexy businesses—properly executed over long time horizons—can generate extraordinary shareholder value. The company's infrastructure cannot be replicated, its regulatory moat deepens annually, and its integrated service model creates customer lock-in that supports pricing power.

For investors seeking exposure to critical industrial infrastructure with regulatory-protected margins, Clean Harbors offers a distinctive value proposition. The company's future growth—driven by PFAS remediation, sustainability initiatives, and continued market consolidation—may prove as impressive as its already remarkable past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube