Williams-Sonoma: From Sonoma Kitchen Shop to Omni-Channel Home Empire

I. Introduction & Episode Setup

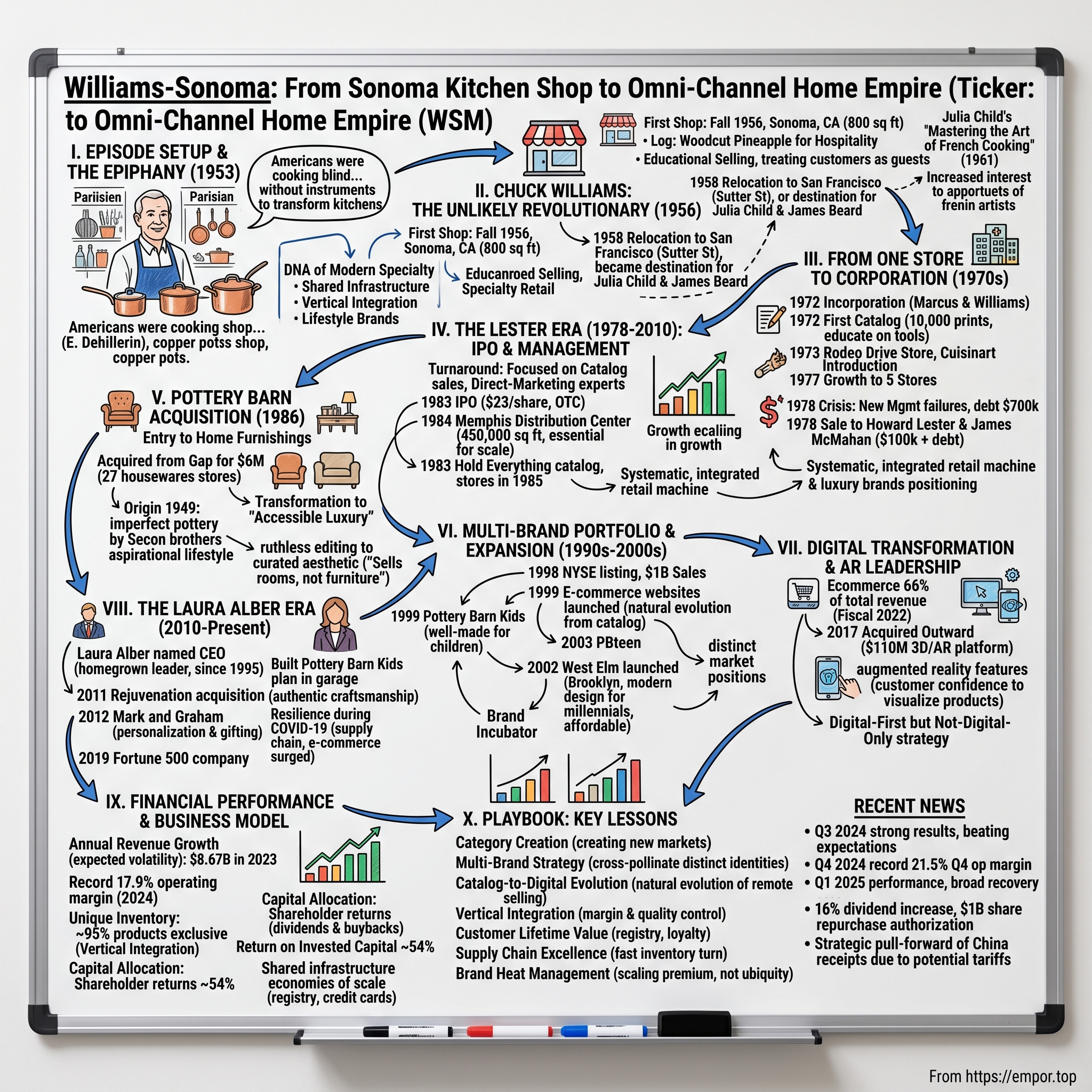

Picture this: It's 1953, and a middle-aged hardware store owner from Sonoma, California, walks into E. Dehillerin, a legendary cookware shop tucked away in Les Halles market in Paris. Chuck Williams, a self-taught cook who'd been making do with cast-iron skillets and basic American cookware, suddenly finds himself surrounded by gleaming copper pots, carbon-steel knives, and specialized baking molds that most Americans had never seen. In that moment, standing among the professional chefs selecting their tools with the same care a violinist chooses a bow, Williams realized something profound: Americans were cooking blind, without access to the very instruments that could transform their kitchens from places of drudgery into theaters of creativity.

That Parisian epiphany would eventually birth Williams-Sonoma, today an $8 billion omni-channel home furnishings empire that commands premium positioning across multiple lifestyle brands. But the path from a single 800-square-foot shop selling French copper pots to Fortune 500 company wasn't just about riding America's culinary awakening—it was about creating it.

This is a story of category creation at its finest, where a passionate merchant didn't just identify a market gap but cultivated an entirely new consumer desire. It's about how a company built for catalog sales in the 1970s became a digital commerce powerhouse generating 64% of revenue online. And perhaps most impressively, it's about maintaining premium brand heat while scaling to nearly 600 stores and $7.75 billion in revenue.

The key themes we'll explore aren't just historical curiosities—they're the DNA of modern specialty retail: how to build multiple distinct brands on shared infrastructure, why vertical integration matters more than ever in the age of Amazon, and what it really means to create a lifestyle brand before venture capitalists turned it into a cliché. Along the way, we'll see how Williams-Sonoma navigated multiple recessions, the dot-com bubble, the housing crisis, and a global pandemic—each time emerging stronger and more profitable than before.

II. Chuck Williams: The Unlikely Retail Revolutionary

Charles Edward "Chuck" Williams didn't set out to revolutionize American cooking. Born in 1915 in northern Florida during World War I, he lived through the Depression, worked as an auto mechanic, and served in World War II before settling in Sonoma, California in 1947. Like many veterans seeking a fresh start in post-war America, he opened a hardware store—a practical business in a growing town where returning GIs were building homes and starting families.

But Williams harbored a secret passion that set him apart from other hardware store owners: he loved to cook and, more importantly, he loved to eat. Not just eat, but to truly savor food in the European tradition. His dinner parties became legendary among Sonoma's small creative community—elaborate affairs where Williams would spend days preparing multiple courses, treating cooking as an art form rather than a chore. Yet he was constantly frustrated by his tools. American cookware in the 1950s was utilitarian at best—heavy cast iron, thin aluminum pans that burned everything, and a complete absence of specialized equipment.

The transformation began with that 1953 trip to Paris. Williams had saved enough money to travel to Europe, ostensibly for vacation but really to eat. He spent weeks wandering through French markets, dining in bistros, and watching how Europeans approached food—not as fuel but as one of life's great pleasures. When he discovered E. Dehillerin, it was like a classical musician finding a Stradivarius after years of playing on a student violin. Here were copper pots that conducted heat evenly, knives that held their edge, madeleine molds, soufflé dishes, and a hundred other tools he'd never seen in America. Williams brought a suitcase full of samples back from Paris and began quietly stocking them in his hardware store. In 1954 he purchased a hardware store in downtown Sonoma with the intention of converting it into a store specializing in French cookware. It was a gradual transformation—hammers and nails slowly giving way to copper pots and wooden spoons. Within two years the shovels and electrical tape had been replaced with copper pans and chef's knives—and the first Williams-Sonoma store was born.

Chuck opened his first shop in Sonoma, CA in the Fall of 1956. The store was tiny—just 800 square feet—but Williams approached it with the precision of a craftsman. He covered the floor with black and white checkerboard tiles, painted the walls a bright yellow that he'd seen in pictures, and built custom shelving to display individual pots and pans. He crafted a simple logo with the words "Williams" and "Sonoma" in block letters over a woodcut illustration of a pineapple – a symbol of hospitality.

The early customers were a mix of curious locals and serious cooks from San Francisco who'd heard rumors about this strange little shop selling French cookware. Williams treated each visitor like a guest in his home, spending hours explaining the difference between copper and cast iron, demonstrating proper knife techniques, sharing recipes. He grossed $35,000 the first year. Not bad for a hardware store owner selling fancy pots, but Williams sensed he was onto something bigger. In 1958, Williams relocated the store to San Francisco, finding a 3,000-square-foot space on Sutter Street, just blocks from Union Square. The store quickly became a destination with culinary figures such as Julia Child and James Beard becoming customers of the flagship location. This was no longer just a quirky shop for Sonoma weekenders—it was ground zero for America's culinary revolution.

The timing couldn't have been better. In 1961, Julia Child published "Mastering the Art of French Cooking," and suddenly millions of Americans wanted to cook like the French. Julia Child's landmark 1961 cookbook, "Mastering the Art of French Cooking," and her cooking show on television sent even more cooks interested in French cuisine to Williams-Sonoma. Williams had anticipated this cultural shift by five years, positioning himself as the sole purveyor of the very tools Child was demonstrating on television.

But Williams wasn't just riding a trend—he was actively shaping American taste. He introduced products methodically, educating customers about each item's purpose and provenance. A whisk wasn't just a whisk; it was a specific tool for specific tasks, and Williams could spend an hour explaining the differences between balloon whisks for egg whites and flat whisks for roux. He treated his customers as students and collaborators in a grand culinary experiment.

III. From One Store to Corporation: The 1970s Expansion

By the early 1970s, Williams-Sonoma had become a pilgrimage site for serious cooks, but Chuck Williams was approaching 60 and running the business largely by himself—building shelves, doing the books, fixing plumbing, traveling to Europe, ordering merchandise, wrapping packages, even sweeping the sidewalk. The store on Sutter Street had expanded to twice its original size, and demand was overwhelming. Something had to give. Enter Edward Marcus, a friend and regular customer who ran the Neiman Marcus catalog operation. In 1972, Marcus approached Williams with a proposition: either sell the company or expand it properly. Williams decided to expand, and in 1972, Marcus and Williams formed a corporation, Williams-Sonoma, Inc. Williams continued to handle the purchasing and merchandising, while Marcus brought in a team of executives to guide the company's business end.

The incorporation marked a crucial turning point. In 1972, Chuck produced the first catalog for the Williams-Sonoma store. The idea had come from Jackie Mallorca, a customer and copywriter for a local San Francisco advertising agency, who approached Chuck with the concept. "Jackie was intrigued with what I was doing. She came in one day and said, 'You need a catalog and I can create one for you.' I think she wanted to prove to herself that she could do it, and prove to us that it could be a real business. Well, she was right, and she continued to work on the catalog right up to just a few years ago."

The first catalog was modest—black and white, fitting into a business-sized envelope with an initial printing of 10,000. But it represented something revolutionary: the ability to bring Williams-Sonoma's curated selection to customers nationwide. Each catalog wasn't just a list of products; it was an education in French cooking, with detailed descriptions of how to use each tool and why it mattered.

The second Williams Sonoma store opened on Rodeo Drive in Beverly Hills in 1973. The rent was high, but right from the beginning the store was very successful. The Beverly Hills location proved that Williams-Sonoma could work beyond San Francisco, attracting Hollywood's elite and Los Angeles food enthusiasts. The same year, Williams Sonoma introduced the Cuisinart food processor to the American market through its stores and catalog. This single product introduction would generate millions in sales and establish Williams-Sonoma as the place where Americans discovered the next essential kitchen tool.

By 1977, the Williams-Sonoma chain had grown to five stores—San Francisco, Beverly Hills, Palo Alto, Costa Mesa, and Carmel. The catalog operation had moved from Chuck's basement to a proper distribution center in Emeryville. Everything seemed to be going perfectly. Then came 1978.The crisis came swiftly. After Edward Marcus died in 1977, the new management team he'd brought in drove the company into the ground. With $4.9 million in sales, the company carried a debt of $700,000 and posted a net loss of $173,000. "[The new management] proceeded to run it the wrong way," Williams told the San Francisco Business Times, "In a year's time, the company was in financial difficulty. I decided to sell. If it was going to have these kinds of financial problems, I didn't want it. I'd never had those kinds of problems before. I'd never borrowed money. For years, I never had credit because I paid cash."

In 1978, Williams sold the company for $100,000 to W. Howard Lester, a former IBM salesman and founder of several computer services firms, and his partner, James McMahan. Lester said, "I felt like I could run it better," and together with his partner James McMahan bought the company for $100,000 and the assumption of $700,000 in debt, at that point the company was generating around $4 million in annual revenue.

Howard Lester was the opposite of Chuck Williams in almost every way. Where Williams was a craftsman and aesthete, Lester was a systems thinker and entrepreneur. Born in Durant, Oklahoma in 1935, Lester had built and sold a computer software company before age 40. He was looking for his next venture when a friend told him about this quirky cookware company in San Francisco that was bleeding cash but had incredible customer loyalty.

IV. The Lester Era Begins: IPO and Professional Management

Lester spent weeks "looking at every detail and talking to every employee" at Williams-Sonoma. What he saw was a financially shaky business with $4 million in revenue and $700,000 in debt. "It had no systems, no idea of inventory, and that was something I did know about," he says. But he also saw something Williams and Marcus had built that couldn't be replicated: authentic brand heat and a cult following among affluent consumers.

The turnaround began immediately. Rather than jump into the capital-intensive business of building stores, Lester focused on growing catalog sales by hiring direct-marketing experts. He went on buying trips to Europe with Williams, learning the business while respecting the founder's eye for product. He also traveled across the U.S. visiting kitchen stores, noting that "they were run more as a hobby than a business."

Lester's first major strategic decision was to take the company public. Williams-Sonoma, Inc., had its initial public offering in July 1983. One million shares were offered on the OTC Market at $23 a share. Lester retained about 22 percent of the company; Williams, who continued to lead the company's catalog division, held about 1.9 percent of the company's stock.

The IPO capital allowed for critical infrastructure investments. The company established a new 450,000-square-foot distribution and warehouse facility in Memphis, Tennessee, which opened in 1984. This wasn't glamorous work, but it was essential for scaling a catalog business that was shipping millions of packages annually. Lester understood something fundamental: you could have the best products in the world, but if you couldn't deliver them efficiently and profitably, you didn't have a business.

The early public years weren't without stumbles. The company introduced two new catalogs—one featuring table settings and another with exotic cookware—both of which flopped. The Memphis facility's startup costs hammered profits. Earnings fell to $445,000 in 1983 from $1.5 million in 1982. By 1984, with sales reaching nearly $52 million, earnings had sunk to a mere $38,000.But Lester wasn't panicking. By 1985, sales climbed to $68 million, earning the company a net of $2.4 million. At the end of 1985, the company was generating over $51 million in sales. The turnaround came from focusing on what worked: the core Williams-Sonoma brand and careful expansion of proven concepts.

One of those concepts was Hold Everything, which launched as a catalog in 1983. The "Hold Everything" brand began as a Williams Sonoma catalog introduced in 1983. The catalog's success caused the company to begin opening retail stores using the brand name in 1985. The inspiration came from a visit Chuck Williams made to a Dallas warehouse store that specialized in storage containers and organizational products. By 1985, a retail version opened in Corte Madera, a quiet, upscale suburb north of San Francisco.

Lester was building something systematic—not just a collection of stores but an integrated retail machine. He hired experts to teach him about real estate, cherry-picking locations as fastidiously as Chuck selected copper pots. When mall owners tried to put Williams-Sonoma stores by the food court, he refused. Williams-Sonoma belonged with the luxury brands. The company emphasized not inventory levels but customer metrics like "How many did we fail to satisfy yesterday?"

V. The Pottery Barn Acquisition: Entering Home Furnishings (1986)

In September 1986, Williams-Sonoma made a move that would transform the company from a kitchen specialist into a full home furnishings empire: it acquired Pottery Barn from Gap for $6 million. The acquisition included Pottery Barn's 27 housewares stores located in California, Connecticut, New Jersey, and New York.

To understand the significance of this acquisition, you need to know Pottery Barn's origin story. The Pottery Barn was co-founded in 1949 by Paul Secon and his brother Morris in Chelsea, Manhattan. Paul discovered three barns full of pottery from the factory of Glidden Parker in Alfred, New York, who had stored extras and seconds up the road from the business, hence the inspiration of the chain's name.

The Secon brothers were the antithesis of Williams-Sonoma's premium positioning. They literally drove a station wagon full of discontinued and slightly damaged ceramics from upstate New York to Manhattan and opened a 12-foot-wide store selling "nicked and slightly misshapen platters, plates, pitchers, cups and saucers." After The New Yorker published an article about the store in 1952, customers flocked to buy these imperfect but charming pieces.

By the time Gap acquired Pottery Barn in 1984, it had grown to multiple locations but lost its way. Gap, focused on apparel, didn't know what to do with a home furnishings chain. The stores were cluttered, unfocused, selling everything from dinnerware to random furniture pieces without any coherent vision. Gap was ready to dump it, and Lester saw opportunity where others saw a mess.

Its mail-order catalog was first published in 1987. This wasn't just adding another channel—it was completely reimagining what Pottery Barn could be. Lester and his team transformed it from a quirky discount chain into something revolutionary for the late 1980s: an aspirational lifestyle brand at accessible prices.

The transformation required ruthless editing. Out went the hodgepodge of random housewares. In came a carefully curated aesthetic that suggested how you could live, not just what you could buy. The new Pottery Barn didn't sell furniture; it sold rooms. It didn't offer bedding; it provided the foundation for your personal sanctuary. Every catalog spread, every store display, told a story about a life well-lived—casual but elegant, comfortable but sophisticated.

This was the birth of "accessible luxury"—a positioning that would become the template for countless retailers. Pottery Barn suggested you could have the lifestyle of the wealthy without the trust fund. It was democratic aspiration, and it perfectly captured the mood of the late 1980s boom years.

VI. Multi-Brand Portfolio Strategy: The 1990s-2000s

The Pottery Barn success proved something crucial: Williams-Sonoma, Inc. wasn't just a specialty retailer—it was a brand incubator. The company had figured out how to identify underperforming concepts, apply operational excellence and sophisticated merchandising, and create distinct market positions. This realization drove the aggressive expansion of the 1990s and 2000s.

The experiments began with Hold Everything and Gardener's Eden in the 1980s. Hold Everything worked; Gardener's Eden, acquired in 1982, struggled with seasonality but provided valuable lessons about catalog merchandising. These early forays taught the company that success required more than operational efficiency—each brand needed a distinct reason for being. The breakthrough moment came in 1998 when the company was listed on the New York Stock Exchange and sales reached $1 billion for the first time. This wasn't just a financial milestone—it signaled Williams-Sonoma's transformation from specialty retailer to lifestyle brand powerhouse. The move from NASDAQ to NYSE reflected institutional confidence that this wasn't a niche player but a major force in American retail.

The following year, 1999, marked another watershed: Williams-Sonoma launched its e-commerce websites. While competitors treated online as an experiment or threat, Williams-Sonoma saw it as the natural evolution of their catalog heritage. They already knew how to sell without physical interaction, how to convey quality through images and words, how to build trust remotely. The digital transition that would devastate traditional retailers came naturally to a company built on mail-order.

The company also launched Pottery Barn Kids in 1999, a spin-off that seemed obvious in retrospect but was revolutionary at the time. Children's furniture had been either cheap and disposable or precious and impractical. Pottery Barn Kids split the difference: well-made pieces that could survive actual children but looked good enough for design-conscious parents. It wasn't just selling furniture; it was selling the idea that children's spaces deserved the same aesthetic consideration as adult rooms. The Pottery Barn brand further expanded with the launch of PBteen in early 2003, targeting the overlooked demographic between kids and adults. The concept grew from Pottery Barn Kids customers requesting products that would grow with their children. It was another example of Williams-Sonoma's ability to identify white space in the market and create brands to fill it.

But the most significant new brand launch was West Elm. The West Elm brand was launched in 2002 with the release of a catalog; the following year, the brand opened its first store. West Elm was founded in April 2002 with the launch of a catalog, with the concept of "great design at affordable price points," followed by the first store in the Dumbo district of Brooklyn, New York later that year.

West Elm represented something entirely new for Williams-Sonoma: modern design for millennials. While Pottery Barn served suburban families and Williams-Sonoma catered to serious cooks, West Elm targeted urban dwellers who wanted mid-century modern aesthetics without the mid-century prices. Born in Brooklyn in 2002, West Elm is a design-led brand dedicated to helping people create spaces they love. The brand offered modern, stylish furniture at reasonable prices, with a focus on clean lines and global influences.

The international expansion began modestly. In October 2001, the company opened its first international stores in Toronto, Ontario, Canada. But this was just testing the waters for what would become a global presence through a combination of owned stores and franchise partnerships in the Middle East, Australia, and eventually the UK.

VII. Digital Transformation & E-Commerce Leadership

By the late 1990s, Williams-Sonoma was ready to embrace the internet. In 1999, the company launched its first e-commerce site. This wasn't a defensive move against Amazon or a reluctant acknowledgment of changing times—it was the natural evolution of a company that had always understood remote selling.

Think about it: Williams-Sonoma had been converting catalog browsers into buyers for nearly three decades. They knew how to photograph products to convey quality, how to write descriptions that created desire, how to build trust without physical interaction. The skills that made them catalog champions translated perfectly to digital commerce.

The digital transformation accelerated through the 2000s. Each brand got its own e-commerce site, allowing for distinct positioning while sharing backend infrastructure. The company invested heavily in photography and content creation, understanding that online shopping for home furnishings required exceptional visual merchandising. The numbers tell the story: Williams-Sonoma ecommerce sales accounted for 66% of total revenue across all brands in fiscal 2022. Digital sales represent 64.3% of total company revenue as of 2023. This isn't just a successful digital transition—it's one of the most complete transformations in retail history.

The secret sauce was treating digital not as a separate channel but as the natural evolution of their direct-to-consumer heritage. They understood that online shopping for furniture and home goods required solving unique problems: How do you convey quality without touch? How do you help customers visualize products in their space? How do you build confidence in big-ticket purchases made sight unseen?

In 2017, Williams-Sonoma acquired Outward, a 3-D imaging and augmented reality platform for the home furnishings and decor industry. This $110 million acquisition wasn't about jumping on a tech trend—it was about solving a fundamental e-commerce challenge. More than 1,500 SKUs, or more than 80% of Pottery Barn's core assortment of products, including sofas, sections, tables, consoles, chairs and lighting, are available in 3-D in the app.

The augmented reality feature allows customers to virtually place furniture in their rooms, solving the visualization problem that had long plagued online furniture retail. As their CMO explained, "[Augmented reality] gives them the confidence that they are making the right purchase, and it eliminates the second-guessing and enhances the inspiration".

But technology was just one piece. Williams-Sonoma also pioneered what they call "digital-first but not digital-only" strategy. Stores became showrooms and fulfillment centers. The catalog evolved into content marketing. Every touchpoint reinforced the others in an omni-channel symphony that few retailers have matched.

VIII. The Laura Alber Era: Modern Leadership (2010-Present)

In May 2010, Lester retired, and Laura Alber was named CEO of the umbrella organization. Alber joined the company in 1995. She was active in building the Pottery Barn catalog and the development and launch of Pottery Barn Kids and PBteen. The transition marked a generational shift—from the entrepreneur who'd bought and built the company to a homegrown leader who'd risen through the ranks.

Laura J. Alber (born 1968) is an American businesswoman who in 2010 became the CEO of Williams-Sonoma, Inc. Her path to the corner office was anything but conventional. After graduation from Penn, Alber drove to California with no plan and took a series of odd jobs until taking an entry-level job at Gap Inc. Alber joined Williams-Sonoma in 1995 as a senior buyer in the Pottery Barn subsidiary brand.

What set Alber apart was her entrepreneurial mindset within the corporate structure. After being pregnant with her first daughter, Alber said she was inspired to create Pottery Barn Kids, providing home furnishings for children's spaces. "In my entire career, being pregnant was the time I was most creative," Alber said. "I had so much energy, I could practically lift the car." She wrote the business plan herself, recruited other women from the company, and prototyped the concept in the Williams-Sonoma parking garage.

Alber has spearheaded WSI's innovation and expansion into new markets, including the introduction of Pottery Barn Kids, Pottery Barn Teen, West Elm, Mark & Graham, Rejuvenation, and GreenRow. But her most significant achievement may be the digital transformation. During her tenure, Williams-Sonoma launched its first app — "Recipe of the Day" — and partnered with YouTube to offer shoppable online videos. By 2014, under Alber's leadership, Williams-Sonoma became one of the largest U.S. e-tailers, selling about half of its $5 billion annual sales online.

In November 2011, the company acquired Portland, Oregon-based Rejuvenation, a manufacturer and direct marketer of light fixtures and hardware with stores in Portland, Seattle, and Los Angeles. The $65 million acquisition brought authentic craftsmanship and American-made manufacturing capabilities in-house, adding a brand focused on period-authentic lighting and house parts—a natural complement to the portfolio that appealed to renovation enthusiasts and historic home owners.

The company launched a lifestyle brand offering personalized products, Mark and Graham, in November 2012. This wasn't just another brand extension but a strategic move into personalization and gifting—high-margin categories that leveraged Williams-Sonoma's operational excellence while requiring minimal inventory risk. The brand specializes in personalized gifts and monogrammed products, from leather goods to home accessories, capturing the growing consumer desire for customized products.

Under Alber's leadership, the company demonstrated remarkable resilience during COVID-19. While other retailers shuttered stores and filed for bankruptcy, Williams-Sonoma saw the pandemic as an accelerant for trends already in motion. With people spending more time at home, demand for home furnishings exploded. The company's digital infrastructure, built over two decades, handled the surge seamlessly. E-commerce sales jumped 49% in 2020, and rather than pulling back, Alber doubled down on investments in supply chain and technology.

The pandemic revealed the strength of Williams-Sonoma's model. While competitors struggled with inventory and fulfillment, the company's vertically integrated supply chain and sophisticated demand planning systems kept products flowing. The company emerged from the pandemic stronger, with record margins and a stock price that quintupled from its March 2020 lows.

In 2019, Williams-Sonoma, Inc., was named as a Fortune 500 company for the first time in its history, ranking 466th with revenues of $5.67 billion. This wasn't just a vanity metric—it represented the company's evolution from specialty retailer to major American corporation, validating decades of strategic brand building and operational excellence.

IX. Financial Performance & Business Model Analysis

The financial trajectory of Williams-Sonoma tells a story of consistent execution and margin expansion that would make any MBA salivate. Revenue evolution shows remarkable growth with expected volatility: Williams Sonoma's annual revenue for 2021 was $6.78 billion, a 15.01% increase from 2020. Williams Sonoma's annual revenue for 2022 was $8.25 billion, a 21.56% increase from 2021. Williams Sonoma's annual revenue for 2023 was $8.67 billion, a 5.2% increase from 2022. Williams Sonoma's annual revenue for Jan 28, 2024 was $7.75 billion, a 10.65% decrease from 2023.

But revenue tells only part of the story. The company achieved a record annual operating margin of 17.9% for 2024, with full-year earnings per share of $8.50. These aren't just good numbers for retail—they're exceptional for any industry. Consider that most specialty retailers operate with single-digit margins. Williams-Sonoma's ability to command nearly 18% operating margins reflects pricing power, operational efficiency, and a business model that's fundamentally different from traditional retail.

The secret lies in the company's unique approach to inventory and merchandising. Unlike traditional retailers who buy from vendors and mark up products, Williams-Sonoma designs much of what it sells. Approximately 95% of products are exclusive to their brands, either designed in-house or through exclusive vendor partnerships. This vertical integration allows for better margins, quality control, and differentiation—you literally can't find these products anywhere else.

Capital allocation under Alber has been textbook efficient. The company consistently returns cash to shareholders through dividends and aggressive buybacks, having repurchased over $3 billion in stock over the past decade. Yet they've maintained flexibility for strategic acquisitions and organic growth investments. The balance is deliberate: reward shareholders while investing in capabilities that extend competitive advantages.

Return on Invested Capital sits at an eye-popping 54%, a metric that would make Warren Buffett blush. This isn't financial engineering—it's the result of a capital-light model where vendors hold inventory, stores serve as showrooms more than warehouses, and digital sales require minimal physical infrastructure. The company has essentially figured out how to generate luxury goods margins with minimal capital intensity.

The brand portfolio economics reveal sophisticated synergies. Each brand maintains distinct positioning—Williams-Sonoma for serious cooks, Pottery Barn for family living, West Elm for modern design—but they share everything behind the scenes: distribution centers, technology platforms, customer databases, even credit card processing. This shared infrastructure means the incremental cost of adding a new brand or channel is minimal, while the revenue opportunity is substantial.

The membership and credit card programs, while less visible than products, drive significant value. The Key Rewards program and co-branded credit cards create customer stickiness and provide rich data for personalization. Customers who join these programs spend 2-3x more than non-members, and the data insights allow for sophisticated lifecycle marketing that drives higher lifetime values.

X. Playbook: Key Business Lessons

Category Creation: Williams-Sonoma didn't just sell French cookware—it created the entire category of specialty culinary retail in America. Chuck Williams understood that you don't just identify demand; sometimes you have to create it through education and evangelism. Every product introduction was a teaching moment, every catalog a curriculum. The lesson: the biggest opportunities often lie in markets that don't yet exist.

Multi-Brand Strategy: Each brand in the portfolio serves a distinct customer need and life stage, but they share operational DNA. This isn't the conglomerate model of unrelated businesses but carefully orchestrated brand architecture. Pottery Barn customers graduate to West Elm. Williams-Sonoma shoppers discover Pottery Barn Kids when they have children. The brands cross-pollinate while maintaining distinct identities—a delicate balance few retailers achieve.

Catalog-to-Digital Evolution: The seamless transition from mail-order to e-commerce dominance wasn't luck—it was the natural evolution of core competencies. The skills required for successful catalog retail—product photography, compelling copywriting, remote selling, efficient fulfillment—translate directly to digital commerce. Williams-Sonoma didn't have to learn e-commerce; they'd been doing it since 1972, just with different delivery mechanisms.

Vertical Integration: From sourcing to last-mile delivery, Williams-Sonoma controls more of its value chain than most retailers. They design products, manage production with vendors, operate their own distribution centers, and increasingly handle final delivery. This integration provides margin advantages, quality control, and agility that pure retailers can't match. When supply chains broke during COVID, Williams-Sonoma's direct vendor relationships and controlled logistics kept products flowing.

Customer Lifetime Value: The registry strategy is genius in its simplicity. Capture customers at major life events—weddings, babies, new homes—and you capture them for life. The registry creates switching costs (why start over somewhere else?), provides rich data about life stages, and generates natural repeat purchase occasions. Add in credit cards and loyalty programs, and you have customers worth thousands in lifetime value.

Supply Chain Excellence: Operational efficiency isn't sexy, but it's the foundation of sustainable competitive advantage. Williams-Sonoma's supply chain sophistication—from demand planning to inventory management to fulfillment—allows them to maintain high service levels with minimal working capital. They turn inventory faster than competitors while maintaining higher margins. This operational excellence becomes a moat that's nearly impossible to replicate.

Brand Heat Management: Perhaps the most delicate balance is maintaining premium positioning while scaling. Most brands lose their edge as they grow—exclusivity dies with ubiquity. Williams-Sonoma has managed to keep each brand feeling special while operating nearly 600 stores and generating $7.75 billion in revenue. The secret is careful distribution, consistent quality, and never chasing volume at the expense of brand integrity.

XI. Bear vs. Bull Case

Bear Case:

The housing market sensitivity cannot be ignored. Williams-Sonoma's fortunes are tied to home sales, renovations, and consumer confidence in making large discretionary purchases. When mortgage rates spike or housing transactions slow, Williams-Sonoma feels it immediately. The company's beta to housing is both a blessing in good times and a curse in downturns.

Amazon and direct-to-consumer competition intensify daily. Every venture-backed DTC brand targets segments of Williams-Sonoma's market—Casper for mattresses, Article for furniture, Made In for cookware. While none match Williams-Sonoma's scale or brand portfolio, death by a thousand cuts remains a risk. Amazon's private label ambitions in home furnishings pose a particular threat to the mid-market positioning of West Elm.

Tariff exposure and supply chain vulnerabilities persist despite operational excellence. With significant sourcing from Asia, particularly Vietnam and China, trade policy changes can impact margins overnight. The company has diversified sourcing and built buffer inventory, but geopolitical risks remain elevated in an increasingly fractured global trade environment.

The mature retail market offers limited store growth potential. Unlike fast-growing categories or emerging markets, home furnishings in developed countries grows roughly with GDP. Williams-Sonoma must take share in a zero-sum game, and their already-strong position limits runway. New store productivity has declined, forcing growth to come from same-store sales and digital—harder battles than geographic expansion.

High valuation multiples relative to growth create downside risk. Trading at premium multiples to retail peers assumes continued execution excellence. Any stumble—a failed brand launch, supply chain disruption, or digital platform issue—could trigger multiple compression that amplifies fundamental challenges.

Bull Case:

Best-in-class operating margins in specialty retail deserve premium valuations. The 17.9% operating margin isn't a peak-cycle anomaly but the result of structural advantages that should persist. Few retailers at any scale achieve these margins, and fewer still maintain them across cycles. This isn't just operational efficiency but pricing power from brand strength and product differentiation.

Dominant market position in premium home furnishings creates competitive advantages that compound over time. Scale economics in sourcing, technology, and marketing create barriers to entry. Would-be competitors must invest billions to replicate Williams-Sonoma's infrastructure, and even then would lack the brand heritage and customer relationships built over decades.

The strong brand portfolio with distinct positioning provides multiple growth vectors. While individual brands may face challenges, the portfolio provides diversification and optionality. West Elm can take share in modern furniture while Williams-Sonoma maintains culinary leadership. New brand launches like Rejuvenation can target niche markets without diluting core brands.

Digital capabilities and data advantage compound with each transaction. Twenty-plus years of e-commerce experience and customer data create personalization capabilities competitors can't match. The company knows what customers buy, when they move, when they have children—insights that drive marketing efficiency and product development. This data moat widens daily.

Capital-light model with strong cash generation supports shareholder returns regardless of growth rates. Even in flat revenue scenarios, Williams-Sonoma generates substantial free cash flow. The combination of high margins, minimal capital requirements, and strong cash conversion means the company can return billions to shareholders while investing in the business.

Management execution track record inspires confidence. Laura Alber and her team have navigated multiple crises, from the financial crisis to COVID, emerging stronger each time. They've consistently exceeded guidance, expanded margins, and returned capital efficiently. In retail, where execution is everything, this track record matters.

XII. Power Analysis & Competitive Moats

Brand Power: Premium positioning across multiple categories creates pricing power and customer loyalty that transcends rational purchase decisions. When customers buy Williams-Sonoma, they're not just buying cookware—they're buying into a lifestyle, a self-image, a statement about their values and aspirations. This emotional connection, built over decades, can't be replicated with venture capital or aggressive marketing.

Scale Economies: Shared infrastructure across brands creates cost advantages that improve with size. Every additional brand or product leverages the same distribution centers, technology platforms, and corporate functions. This operating leverage means incremental revenue drops to the bottom line at higher rates than competitors. The scale economics are particularly powerful in digital marketing, where customer acquisition costs can be amortized across multiple brands and purchase occasions.

Network Effects: While subtle, network effects exist through registry and social commerce elements. As more couples register at Williams-Sonoma brands, it becomes the default choice for gift-givers. The company's design services create communities of customers who share ideas and inspiration. These network dynamics are weaker than pure technology platforms but stronger than traditional retail.

Switching Costs: Design services and customer relationships create meaningful switching costs. Once customers have worked with Williams-Sonoma design consultants, received trade discounts, or integrated products into their homes, switching becomes costly in time and money. The registry ecosystem locks in customers at crucial life moments. Credit card rewards and loyalty points add financial switching costs.

Counter-positioning: Premium quality versus mass market competitors creates a defensible position. Williams-Sonoma doesn't compete on price—they compete on quality, service, and experience. This positioning means Walmart or Amazon can't directly attack without undermining their own value propositions. It's the classic strategy of forcing competitors to choose between their existing model and yours.

XIII. Final Thoughts & Legacy

Chuck Williams' lasting impact on American culinary culture extends far beyond retail. He didn't just sell products; he changed how Americans think about cooking and eating. Before Williams-Sonoma, cooking was often drudgery. After, it became a creative outlet, a social activity, a form of self-expression. Walk into any serious home kitchen today and you'll see Williams' influence—from the copper pots to the stand mixers to the very idea that cooking tools matter.

The blueprint for specialty retail success that Williams-Sonoma created remains the gold standard. Start with authentic passion and expertise. Build trust through education and curation. Expand thoughtfully into adjacent categories. Maintain premium positioning while scaling. Invest in infrastructure before you need it. Treat digital as core, not auxiliary. These lessons seem obvious now because Williams-Sonoma made them so.

What the future holds—AI, personalization, sustainability—will test the model but not break it. AI-powered personalization could make the Williams-Sonoma shopping experience even more compelling, with product recommendations and room designs tailored to individual taste and budgets. Sustainability initiatives, from sourcing to circular economy programs, align with customer values and regulatory requirements. The company's vertical integration and direct vendor relationships position it well for supply chain transparency demands.

The key takeaways for entrepreneurs and investors are timeless. First, category creation beats competition—it's better to define a new market than fight in an existing one. Second, operational excellence compounds—small advantages in efficiency and execution become insurmountable over time. Third, brand power is real—emotional connections drive pricing power that defies economic logic. Fourth, culture matters—Williams-Sonoma maintained its merchant DNA through multiple ownership changes and massive scale. Finally, patience pays—this is a 70-year story of compound growth, not a venture-scale rocket ship.

Williams-Sonoma stands as proof that in retail, as in cooking, the best results come from quality ingredients, careful preparation, and patience. Chuck Williams knew that a good meal couldn't be rushed, and neither could a great company. From that first shop in Sonoma to today's omni-channel empire, Williams-Sonoma has stayed true to its founding insight: Americans will pay for quality and expertise when it enhances their daily lives.

The company enters its eighth decade stronger than ever, with the highest margins in its history, a proven digital model, and brands that resonate across generations. Whatever challenges lie ahead—recession, competition, changing consumer preferences—Williams-Sonoma has the operational excellence, financial strength, and brand power to adapt and thrive. In an industry littered with fallen giants and disrupted incumbents, Williams-Sonoma remains the exception: a specialty retailer that specialized in survival, growth, and generating exceptional returns for those patient enough to own it.

XIV. Recent News

Based on the most recent earnings results and strategic updates, here are the key recent developments for Williams-Sonoma:

XIV. Recent News

Q3 2024 Earnings Performance Williams-Sonoma reported strong third-quarter 2024 results, with diluted EPS growth of 7.1% to $1.96, beating analyst expectations. The company raised its full-year guidance, expecting revenues to be in the range of down 3% to down 1.5% and operating margin to be between 17.8% and 18.2%. Despite Pottery Barn experiencing a negative 7.5% comp in Q3, reflecting ongoing difficulties in the furniture market, the company demonstrated resilience through operational excellence and margin expansion.

Q4 2024 and Full-Year Results The company finished fiscal 2024 strong with Q4 comparable brand revenue up 3.1% and a record Q4 operating margin of 21.5%. The company achieved a record annual operating margin of 17.9% for 2024, with full-year earnings per share of $8.50. B2B revenue exceeded $1 billion with a 12% comp in Q4, highlighting the success of this strategic growth initiative.

Q1 2025 Performance Williams-Sonoma started fiscal 2025 strong with Q1 comparable brand revenue up 3.4% and an operating margin of 16.8%, with diluted EPS of $1.85. CEO Laura Alber noted that "all brands running positive comps" in the quarter, signaling broad-based recovery.

Strategic Initiatives and Capital Allocation The Board of Directors authorized a 16% increase in the company's quarterly cash dividend to $0.66 per common share. The quarterly dividend is payable on May 24, 2025. "After another strong performance in 2024, we are proud to increase our quarterly dividend by 16%," said Laura Alber.

The company announced an additional share repurchase authorization of $1 billion and maintains a strong cash position with $827 million and no debt. Included in year-end inventory levels is a strategic pull forward of China receipts to reduce the potential impact of higher tariffs in fiscal year 2025. Share repurchases in 2024 totaled $807 million or 4.6% of outstanding shares.

Brand Performance and Innovation Pottery Barn Q4 comp was negative 0.5%, while Pottery Barn Children's posted positive 3.5%. West Elm showed strong momentum with positive 4.2% comp, and the Williams-Sonoma brand delivered positive 5.7% comp in Q4. The company continues to leverage collaborations and partnerships to drive growth, with CEO Alber highlighting successful partnerships like Monique Lhuillier in Pottery Barn and Stanley Tucci in Williams Sonoma.

Market Conditions and Outlook The housing market remains a challenge, with no significant improvement expected in 2025. Tariffs on China, Mexico, and Canada, as well as on metals and aluminum, are expected to impact operating margins. Despite these headwinds, Williams-Sonoma remains focused on three key priorities: returning to growth, elevating world-class customer service, and driving earnings. The company is confident it will continue to outperform peers through its ability to gain market share, strength in proprietary design, competitive advantage of digital-first strategy, ongoing strength of growth initiatives, and resilient balance sheet.

Stock Performance and Market Recognition As of January 2024, Williams-Sonoma share prices were up over 65% in the previous year, and over four times that in the previous five years. In June 2024, the company announced a two-for-one stock split. Following the strong Q3 2024 earnings report, Williams-Sonoma's stock jumped more than 30% in trading to an all-time high of just over $175, among the biggest single-day leaps in the brand's 40-year history as a public company.

XV. Links & Resources

Company Resources

- Investor Relations: ir.williams-sonomainc.com

- Annual Reports & SEC Filings: Available through investor relations portal

- Earnings Call Transcripts: Quarterly earnings calls archived on investor site

- Corporate Website: williams-sonomainc.com

Key Books & Long-Form Resources

- "Williams-Sonoma Cookbook: The Essential Recipe Collection" - Chronicles the culinary influence of the brand

- "Chuck Williams: Creator of Williams-Sonoma" - Biography of the founder

- Harvard Business School Case Studies on Williams-Sonoma's digital transformation

- Stanford Graduate School of Business analysis of multi-brand portfolio strategy

Industry Analysis

- National Retail Federation: Industry reports on home furnishings sector

- Home Furnishings Association: Market trends and consumer behavior studies

- Statista: Comprehensive statistics on Williams-Sonoma and home furnishings market

- IBISWorld: Detailed industry reports on specialty retail and e-commerce

Competitor Information

- RH (Restoration Hardware): Direct premium competitor analysis

- Wayfair: E-commerce comparison and market share data

- Crate & Barrel: Private company competitive positioning

- Amazon Home: Mass market disruption analysis

- IKEA: Global furniture market dynamics

Financial Analysis Platforms

- Seeking Alpha: Earnings analysis and investor commentary

- Morningstar: Independent research and valuation metrics

- S&P Capital IQ: Professional-grade financial analysis

- Bloomberg Terminal: Real-time data and analytics (subscription required)

Trade Publications

- Home Textiles Today: Industry news and trends

- Furniture Today: Market analysis and company profiles

- Business of Home: Design industry insights

- RetailWire: Retail strategy discussions

Academic Research

- "The Evolution of Specialty Retail" - Journal of Retailing

- "Digital Transformation in Traditional Retail" - MIT Sloan Management Review

- "Brand Portfolio Management" - Harvard Business Review

- "Omni-Channel Excellence" - Wharton Research Papers

This analysis represents a comprehensive examination of Williams-Sonoma's journey from a single Sonoma kitchen shop to an $8 billion omni-channel empire. The company's story exemplifies American entrepreneurship, operational excellence, and the power of brand building over seven decades. As Williams-Sonoma enters its next chapter, it carries forward Chuck Williams' original insight: quality, expertise, and passion for the home will always find a market among discerning consumers.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube