Stanley Black & Decker: The Toolmakers Who Built America

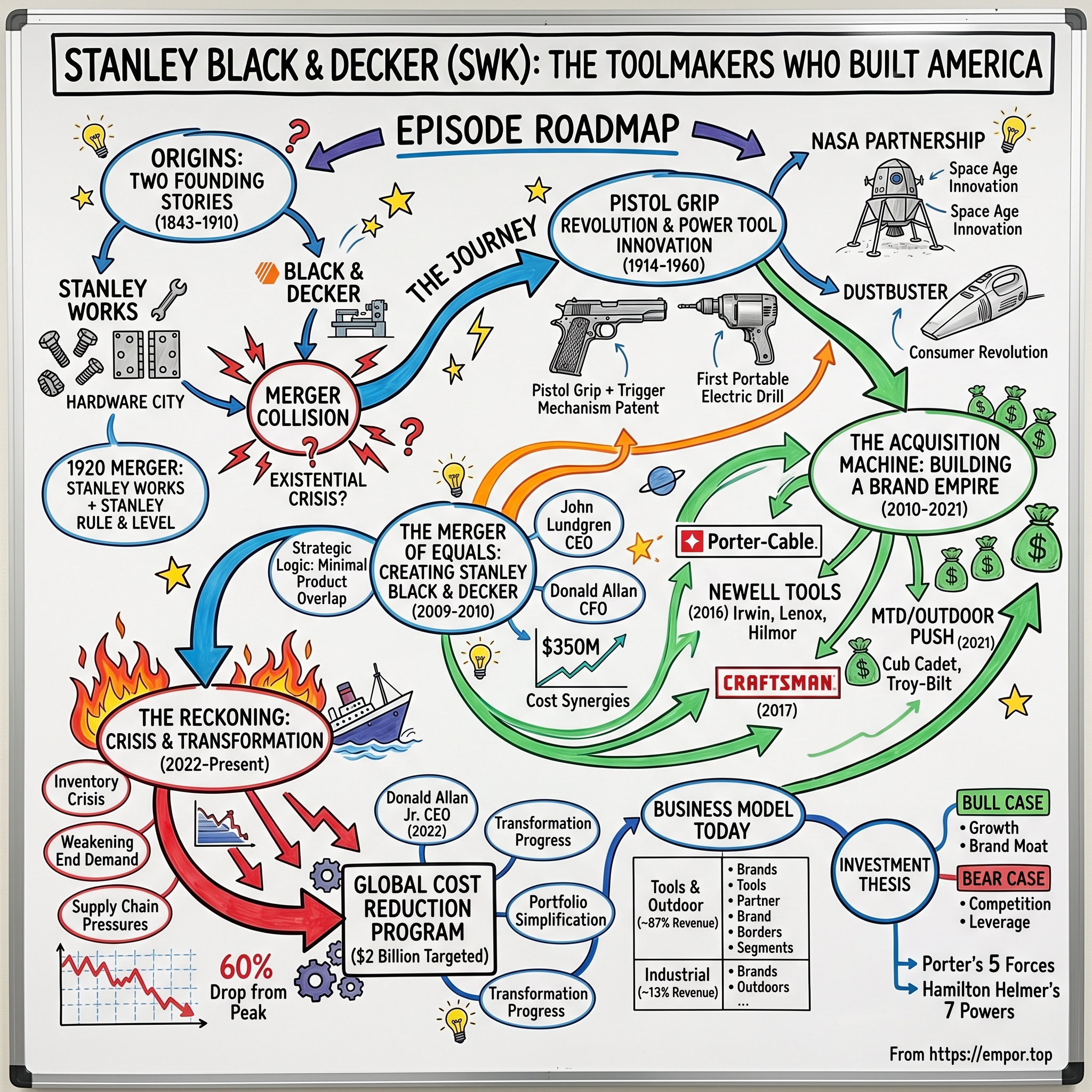

Introduction & Episode Roadmap

In the summer of 1916, in a cramped Baltimore machine shop, two twenty-something inventors contemplated a Colt .45 automatic pistol lying on a workbench. Duncan Black and Alonzo Decker weren't planning violence—they were solving an engineering problem that would reshape modern industry. The pistol's grip and trigger mechanism, they realized, offered the perfect ergonomic template for a new kind of portable electric drill. Within months, they had filed a patent that would become the foundation of the entire power tool industry.

Nearly 1,500 miles to the northeast, in New Britain, Connecticut, a company called The Stanley Works had been turning out wrought-iron bolts, hinges, and hand tools since 1843. For over seven decades, the Stanley name had become synonymous with reliable, durable hardware—the kind of products that built America's railroads, factories, and homes.

These two companies—one rooted in 19th-century Yankee craftsmanship, the other born from 20th-century electrical innovation—would eventually collide in one of the most significant industrial mergers in American history. On March 12, 2010, Stanley completed a merger with the Black & Decker Corporation. In connection with the Merger, Stanley changed its name to Stanley Black & Decker, Inc.

But the real story isn't just about two companies becoming one. It's about how an aggressive acquisition strategy created the world's largest tools company—and then nearly brought it to its knees. Since the inception of the program in mid-2022, the Global Cost Reduction Program has generated approximately $1.9 billion of the targeted $2.0 billion pre-tax run-rate cost savings. Stanley Black & Decker's journey from bolt manufactory to global industrial giant—and its subsequent $2 billion transformation—offers a masterclass in brand building, merger integration, and the dangers of acquisition-driven growth.

The central question this analysis explores: How did a 19th-century bolt maker and a 20th-century power tool pioneer merge to become the world's largest tools company—only to face an existential crisis requiring the most ambitious operational turnaround in the company's 180-year history?

Origins: Two Founding Stories (1843-1910)

The Stanley Works: Hardware City's Foundation

In 1843, the American economy was still emerging from the devastating Panic of 1837—a financial crisis that had wiped out countless businesses and fortunes. The company was founded in 1843 by Frederick T. Stanley, a 41-year-old merchant and manufacturer whose previous work experience included stints as a clerk on a Connecticut River steamboat and as an itinerant peddler in the South.

In 1831, Stanley, in partnership with his younger brother William Stanley, had opened a small facility in New Britain, Connecticut, for the manufacture of house trimmings and door locks. Though the business failed to survive the Panic of 1837, it seemed to have served as the prototype for a second manufacturing venture in New Britain—Stanley's Bolt Manufactory—which Frederick Stanley, again in concert with his brother, established in 1843.

Frederick Stanley embodied the New England Yankee work ethic. Stanley was born in Connecticut in 1802. One of seven children, he learned the New England Yankee work ethic at a young age while working on the family farm. By 1843, after brief stints in various manufacturing industries, Stanley co-founded the Stanley Bolt Manufactory, and later The Stanley Works in 1852.

The company's growth mirrored America's industrial expansion. Following the incorporation of The Stanley Works in 1852 with $30,000 in capital, Frederick T. Stanley oversaw rapid business expansion, with annual sales rising from $7,328 in 1853 to $21,371 in 1854 and approximately $53,000 by 1860. The firm transitioned from a modest bolt manufactory to a larger operation producing a broader array of builders' hardware, including T-hinges and wrought-iron straps.

New Britain, Connecticut, transformed into what locals proudly called "Hardware City," with Stanley at its industrial heart. Frederick Stanley's enterprise took many forms involving a variety of business partners before he established his wrought-iron bolt manufactory in 1843. His success in the bolt business soon encouraged Stanley to expand into forging other types of hardware such as hooks and hinges.

The pivotal moment came in 1920. The Stanley Works came to existence as a direct result of the 1920 merger of Stanley's Bolt Manufactory, founded by Frederick Trent Stanley in 1843, and the Stanley Rule and Level Company, founded by Frederick's cousin, Henry Stanley, in 1857. This merger united hardware manufacturing with precision hand tools, creating a diversified product portfolio that would define Stanley for the next century.

By the turn of the century, the name Stanley was a fixture, not only in New Britain but at hardware stores across the country. By the time of William Hart's passing in 1919, the company's sales had grown from a mere $7,000 a year to $11.3 million over the prior six decades. In 1920, Stanley Works purchased the business of Stanley Rule & Level, a New Britain business organized as a joint stock company in 1857. Stanley Rule & Level manufactured levels and squares and, perhaps most famously, the Bailey Plane. The success of the Bailey Plane allowed Stanley Rule & Level to branch out into the production of other hand tools, and by 1900, the company was the largest manufacturer of planes and related tools in America.

Black & Decker: The Power Tool Revolution

While Stanley built its empire on hand tools and hardware, a different kind of industrial revolution was brewing 200 miles south in Baltimore.

In 1910, "The Black & Decker Manufacturing Company" was founded by S. Duncan Black (1883–1951) and Alonzo G. Decker (1884–1956) as a small machine shop in Baltimore in September. Decker, who had only a seventh grade education, had met Black in 1906, when they were both 23-year-old workers at the Rowland Telegraph Company. With only $1,200 between them, one of their first jobs was designing machinery for making milk bottle caps and candy dipping.

The backstory of Black and Decker's partnership reads like an American dream narrative. In 1906, Black, a draftsman, and Decker, a tool and die maker, met as 23-year-old employees of the Rowland Telegraph Co. Four years later, Black sold his car for $600 and, with an equal amount from Decker, they opened a small machine shop in Baltimore. The initial focus of the new business was improving and manufacturing the inventions of others.

Black was educated at Baltimore Polytechnic Institute; Decker barely finished seventh grade. Yet together, they possessed complementary skills—Black the draftsman and designer, Decker the tool-and-die expert who could translate ideas into reality. Their machine shop survived its early years by doing contract manufacturing work—hardly glamorous, but profitable enough to keep the lights on while they dreamed of something bigger.

That something bigger came in 1916, born from an unlikely source of inspiration: a Colt .45 pistol.

The Pistol Grip Revolution & Power Tool Innovation (1914-1960)

The Invention That Changed Everything

The legend of Black & Decker's breakthrough has been told countless times, but it bears repeating for its sheer elegance. A century ago, the Black + Decker Manufacturing Co. (now Stanley Black + Decker) developed and filed a patent application for a ½-inch portable drill that one person could operate.

Electric drills existed before 1916, but they were monsters—heavy, stationary machines designed for industrial applications. In 1916 Black and Decker began to design and manufacture their own electric-powered tools. The German-made electric tools then available were heavy and difficult to operate, and, as a result, had not been commercially successful. Black and Decker designed a universal motor—the first for electric-tool use—which employed either alternating or direct current, and a trigger switch modeled after the mechanism in the Colt revolver. The first tool incorporating these innovative elements was a ½-inch portable drill with the innovative "pistol grip and trigger switch" that have remained standard for electric drills ever since.

The drill was comparatively light at 21 ½ pounds, and it was considered inexpensive at $230. In today's dollars, that would be roughly $6,500—still a significant investment, but revolutionary compared to the massive stationary equipment previously required.

In 1914, they devised a pistol grip and trigger switch enabling single-handed power control and began manufacturing their drill in 1916. In 1917, the company opened a 12,000-square-foot manufacturing plant in Towson, Maryland.

Virtually all of today's electric drills descend from the original portable hand-held drill patented in 1917 by S. Duncan Black and Alonzo Decker, whose invention spurred the growth of the modern power tool industry.

Scaling the Business

The timing proved fortuitous. Post-World War I America was experiencing a construction boom, and businesses were investing in labor-saving devices as wages rose. They began manufacturing their drill in 1916; the following year, the company opened a 12,000-square-foot manufacturing plant in Towson, Maryland. By 1920, Black & Decker surpassed $1 million in annual sales and soon had offices in eight U.S. cities and a factory in Canada.

The company they co-founded, Black & Decker, became a world leader as they continued to innovate, introducing the first line of power tools designed specifically for the "Do-It-Yourself" consumer market in 1946, and the first cordless power tool in 1961.

The company remained family-led for decades. Black held 14 patents. He served as president of the company from 1910 until his death in 1951, when Decker replaced him.

Wartime Production & Global Expansion

Both companies contributed to the American war effort. During World War II, Stanley Works received the Army-Navy "E" Award for excellence in war production.

Stanley's international expansion had begun decades earlier. Around 1937, Stanley acquired the British J. A. Chapman company, a British manufacturer of carpentry tools and other items (including bayonets during World War I) formerly located in Sheffield, from Norman Neill. This helped Stanley to enter the British market.

What investors should understand about this early history is the divergent but complementary DNA of these two companies. Stanley represented the old industrial economy—hand tools, hardware, physical craftsmanship. Black & Decker embodied the electrical age—innovation, power, the democratization of professional-grade capability. When they finally merged in 2010, the combination would theoretically create a complete tools ecosystem spanning hand and power tools, professional and consumer markets, domestic and international distribution.

Space Age Innovation & the Consumer Revolution (1960-1990)

NASA Partnership: Tools for the Moon

Few corporate partnerships have yielded more unexpected consumer spinoffs than Black & Decker's collaboration with NASA. NASA's scientists and engineers were particularly concerned about cords, which could easily entangle astronauts in the weightlessness of zero gravity. To solve that problem, NASA awarded Black & Decker—a household company name since 1914, when S. Duncan Black and Alonzo Decker invented the first hand-held electric drill—the contract to develop a cordless, rechargeable drill for extracting core samples from the moon.

For the NASA project, the company accelerated its research and development, experimenting with different kinds of batteries and even creating a computer program to help optimize power usage so astronauts would not have to stop their work to recharge. These new cordless tools included the B&D Moon Drill, first used during the Apollo 15 mission in 1971.

The technical requirements were extraordinary. The drill needed to operate in extreme temperatures, zero-atmosphere conditions, and extract rock samples from up to 10 feet below the lunar surface—all while being light enough for astronauts to handle in bulky spacesuits.

Portable self-contained drill capable of extracting core samples as much as 10 feet below the surface was needed for the astronauts. Black & Decker used a specially developed computer program to optimize the design of the drill's motor and insure minimal power consumption. Refinement of the original technology led to the development of a cordless miniature vacuum cleaner called the Dustbuster.

The DustBuster & Consumer Products

The Black & Decker DustBuster (now stylized as dustbuster) is a cordless vacuum cleaner that was introduced in January 1979. Mark Proett and Carroll Gantz are listed as the inventors on the utility and design patents, respectively, assigned to Black & Decker for a cordless vacuum cleaner.

The story of how space technology became a kitchen appliance illustrates Black & Decker's commercial genius. The Mod 4 series was introduced in 1974 but was generally not successful in the marketplace. However, in post-mortem consumer research, the Spot Vac was highly successful with women, who borrowed it from their husband's workbench in the basement to clean up minor spills in the kitchen and upstairs. This inspired the design of a new household product specifically for use upstairs by women.

Over a million Dustbusters were sold in its first year, four times that of the traditional handheld vacuum market. By 1985, B&D had the majority share of cordless vacuum cleaner market and the Dustbuster sold 7 million units annually.

Key Acquisitions Pre-Merger

The original company was started in 1924 in Leola, Pennsylvania by Raymond E. DeWalt, inventor of the radial arm saw. It grew quickly and was reorganized and reincorporated in 1947 as DeWalt Inc. American Machine & Foundry Co., Inc. bought the company in 1949, and sold it to Black & Decker in 1960.

DeWalt's acquisition would prove transformational—though not until decades later. In 1992, Black & Decker began a major effort to rebrand its professional quality and high-end power tools to DeWalt. In 1994, DeWalt took over the German woodworking power tool producer ELU, and used ELU's technology to expand their tool line.

The DeWalt repositioning represented brilliant brand management. Black & Decker was long associated with lighter weight consumer tools such as domestic appliances, and not the heavy duty equipment professional builders wanted. Towards the end of the 1980s, Michael Hammes, executive vice president and president of the company's power tools and home improvement group, introduced the "Acura concept," a notion Honda utilized to enter the upscale automobile market. Black & Decker found it useful to reintroduce a name with little appeal to many consumers in the market for construction tools.

In 1984, Black & Decker made another transformational move by acquiring General Electric's small-appliance business, extending its reach into household products beyond power tools.

For investors, this period established the brand-centric strategy that would define the company: own multiple brands positioned at different price points and customer segments, leverage shared manufacturing and distribution infrastructure, and continuously innovate across the portfolio.

The Merger of Equals: Creating Stanley Black & Decker (2009-2010)

The Setup: Two Complementary Giants

On November 2, 2009, in the depths of the Great Recession, Stanley and Black & Decker announced what they called a "merger of equals"—though as with most such descriptions, the reality was more nuanced.

While the deal is described as a merger, Stanley will retain a slight edge in ownership. Stanley shareholders will own 50.5% of the company, with Black & Decker shareholders owning 49.5%. The new board of directors will consist of nine members of Stanley's board, and six from Black & Decker.

Historically, this relationship is a romance that started 28 years ago. On three different occasions, the CEOs met to discuss the unique and complementary fit of the two companies, and had talked about a merger, but it didn't go anywhere for various reasons.

The strategic logic was compelling. Management believes the Merger is a transformative event bringing together two highly complementary companies, with iconic brands, rich histories and common distribution channels, yet with minimal product overlap. The Merger also enables a global offering in hand and power tools, as well as hardware, thus enhancing the Company's value proposition to customers.

Deal Structure & Leadership

Under the terms of the transaction, which has been approved by the boards of directors of both companies, Black & Decker shareholders will receive a fixed ratio of 1.275 shares of Stanley common stock for each share of Black & Decker common stock they own, representing an implied premium of 22.1% to Black & Decker's share price as of Friday, October 30, 2009. Upon closing, which is expected in the first half of 2010, Stanley shareholders will own approximately 50.5% of the equity of the combined company and Black & Decker shareholders will own approximately 49.5%. The nine members of the current Stanley Board of Directors will be joined by six new members from Black & Decker's Board of Directors. John F. Lundgren, Chairman and Chief Executive Officer of Stanley, will be President and Chief Executive Officer of the combined company. Nolan D. Archibald, Chairman, President, and Chief Executive Officer of Black & Decker, who has been CEO for 24 years, will be Executive Chairman.

After the exchange was completed, pre-merger Stanley shareowners retained ownership of 50.5% of the newly combined company. Based on the $57.86 closing price of Stanley common stock on March 12, 2010, the aggregate fair value of the consideration transferred to consummate the Merger was $4.657 billion.

The Strategic Rationale

The synergy projections were aggressive but grounded in operational reality. In addition to an anticipated $350 million in cost synergies, the companies note that there is virtually no overlap between the brands' product offerings. The merger will allow the combined company to have a presence in markets that would not have been possible for the individual brands.

John Lundgren, chairman and chief executive officer of Stanley, will be president and chief executive officer of the combined company. Nolan Archibald, chairman, president and chief executive officer of Black & Decker, who has been CEO for 24 years, will be executive chairman.

The deal included Donald Allan Jr. in a critical role. In addition to Messrs. Lundgren, Archibald, and Loree, Stanley Vice President and Chief Financial Officer Donald Allan, Jr. will be part of the executive team as Senior Vice President and Chief Financial Officer of the combined company. This continuity would prove crucial—Allan would eventually become CEO and lead the company through its greatest crisis.

Integration Execution

The integration exceeded expectations. Widely viewed as one of the most successful integrations in decades, the merger exceeded its original target of $350 million in cost synergies by 43 percent within three years and created a platform for growth that has tripled its share price.

The Merger also enables a global offering in hand and power tools, as well as hardware, thus enhancing the Company's value proposition to customers. Management believes the value unlocked by the anticipated $425 million in cost synergies, expected to be achieved by the end of 2012, will help fuel future growth and facilitate global cost leadership.

The merger created an $8.4 billion revenue behemoth with complementary product lines: Stanley's strength in hand tools, hardware, and security systems combined with Black & Decker's dominance in power tools and consumer appliances. The combined entity possessed iconic brands recognized worldwide, established distribution relationships with major retailers, and manufacturing scale that competitors would struggle to match.

For investors, the 2010 merger represented a textbook case of value creation through strategic combination—minimal product overlap, significant cost synergies, and complementary market positions. The question that would emerge over the following decade: could management resist the temptation to over-leverage this successful playbook?

The Acquisition Machine: Building a Brand Empire (2010-2021)

Post-Merger Acquisition Spree

If the 2010 merger demonstrated the power of strategic combination, the following decade would test the limits of acquisition-driven growth. Stanley Black & Decker became one of the most aggressive acquirers in American industry, systematically buying competitors, complementary businesses, and iconic brands.

The company's acquisition philosophy centered on brand collection. Rather than building brands organically, management pursued a strategy of acquiring established names with strong market positions and folding them into Stanley Black & Decker's operational infrastructure.

Key Strategic Acquisitions

Newell Tools (2016): Stanley Black & Decker announced in October that it acquired the Irwin, Lenox, and Hilmor tool brands for $1.95 billion from Newell Brands. This deal added premier industrial tool brands to the portfolio, particularly Lenox's dominance in saw blades.

The Craftsman Deal (2017): Perhaps no acquisition better illustrated management's brand-centric strategy than the rescue of Craftsman from dying Sears.

Agreement consists of $525 million cash payment at closing, $250 million at end of year three, and annual payments to Sears Holdings of between 2.5% and 3.5% on new Stanley Black & Decker sales of Craftsman products through year 15. Stanley Black & Decker to significantly increase availability and innovation of Craftsman products and add manufacturing jobs in the U.S. to support growth. EPS accretion to Stanley Black & Decker, excluding charges, of approximately $0.10-$0.15 per share in year one, increasing to approximately $0.35-$0.45 by year five and to approximately $0.70-$0.80 by year ten.

Today only approximately 10% of Craftsman-branded products are sold outside of Sears Holdings and the agreement will enable Stanley Black & Decker to significantly increase Craftsman sales in these untapped channels. "Craftsman is a legendary, American brand with tremendous consumer awareness built on a legacy of producing quality products at a great value," said Stanley Black & Decker President and CEO James M. Loree. "This agreement represents a significant opportunity to grow the market by increasing the availability of Craftsman products to consumers in previously underpenetrated channels."

The MTD/Outdoor Push

Management identified outdoor power equipment as the next growth frontier.

Stanley Black & Decker today announced that it has entered into a definitive agreement to acquire a 20 percent stake in MTD Products Inc ("MTD"), a privately held global manufacturer of outdoor power equipment, for $234 million in cash. Under the terms of the agreement, Stanley Black & Decker has the option to acquire the remaining 80 percent of MTD beginning on July 1, 2021. Stanley Black & Decker's President and CEO James M. Loree commented, "This investment in MTD increases our presence in the $20 billion global lawn and garden market in a financially and operationally prudent way."

Stanley Black & Decker today announced that it has successfully completed the acquisition of two leading companies in the growing outdoor power equipment industry, including purchasing the remaining 80 percent ownership stake in MTD Holdings Inc ("MTD") and the acquisition of Excel Industries ("Excel"). These transactions establish Stanley Black & Decker as a U.S. based global leader in outdoor products.

We welcome the 8,100 associates from MTD and Excel to Stanley Black & Decker and look forward to a seamless integration process. The purchase price for the two transactions totaled $1.9 billion inclusive of standard purchase price adjustments.

The MTD deal brought brands like Cub Cadet and Troy-Bilt into the fold, along with approximately $4 billion in annual outdoor equipment revenue. Management painted a compelling picture of leading the electrification of outdoor products—converting gas-powered lawn equipment to battery-powered alternatives using the same lithium-ion technology platform as DeWalt power tools.

By late 2021, Stanley Black & Decker appeared to be firing on all cylinders. The stock reached an all-time high of $187.73 in May 2021. Management projected adjusted earnings per share of $10.70-$10.90 for 2021. The future looked extraordinarily bright.

Then everything fell apart.

The Reckoning: Crisis & Transformation (2022-Present)

The Perfect Storm

2022 proved to be Stanley Black & Decker's annus horribilis. The convergence of multiple adverse forces created a crisis that management had neither anticipated nor adequately prepared for.

Unfortunately, what could go wrong, did go wrong in 2022. Instead of seeing easing supply chains and moderating raw materials prices, Stanley suffered ongoing pressures and rising prices. Management, in turn, slashed full-year earnings guidance throughout the year.

Having started the year expecting adjusted earnings per share of $12-$12.50 in 2022, management in its most recent guidance projected $4.15-$4.65. Meanwhile, Stanley and other tools companies are struggling to reduce inventory as sales (organic) declined 5% in the third quarter and are set to decline mid-to-high single digits for the full year. As discussed recently, Stanley and its industry peers need to improve the rate at which they turn over their inventory.

Shares in toolmaker, outdoor products, and industrial products company Stanley Black & Decker declined nearly 60% since the start of the bear market in early January of last year. A combination of supply chain pressures and weakening end demand put pressure on the stock in 2022.

The inventory situation proved particularly devastating. Stanley Black & Decker inventory for 2023 was $4.739B, a 19.15% decline from 2022. Stanley Black & Decker inventory for 2022 was $5.861B, a 8.14% increase from 2021.

The company had built up massive inventory levels during the pandemic-era DIY boom, anticipating sustained demand that evaporated as consumers shifted spending back to services and experiences. Rising interest rates crushed the housing market, further depressing tool purchases. The very same acquisitions that had been celebrated—MTD's outdoor equipment, new brand additions—became liabilities as the company struggled to integrate them amidst market turmoil.

The latest closing stock price for Stanley Black & Decker as of December 03, 2025 is 72.53. The all-time high Stanley Black & Decker stock closing price was 187.73 on May 10, 2021. The stock's collapse from peak to trough represented a loss of more than 60% of shareholder value.

The Global Cost Reduction Program

In July 2022, Donald Allan Jr. assumed the CEO role from James Loree, inheriting a company in crisis. Stanley Black & Decker has named Donald Allan, Jr., currently president and chief financial officer, the company's next chief executive officer, effective July 1. Allan will succeed James M. Loree, who has served as CEO since 2016.

Andrea J. Ayers, chair of the board of directors, commented: "Don Allan's appointment reflects the board's succession planning, and in naming him as our next CEO, we have chosen a world-class executive with exceptional experience and leadership skills. Since arriving at the Company in 1999, Don has been instrumental in driving the company's growth and transformation strategy. He is well respected throughout the organisation as well as among our valued customers and the investment community."

Allan launched what would become one of the most ambitious transformation programs in American industrial history. However, management isn't standing still. To address its disappointing supply chain and operational performance, it launched a plan to cut costs by a whopping $2 billion in three years, with $1 billion of the cuts to be implemented in 2023 alone.

The Company continued executing a series of initiatives that are expected to generate $1.5 billion of pre-tax run-rate cost savings by the end of 2024, growing to $2 billion by the end of 2025. Of the $2 billion savings, $1.5 billion is expected to be delivered through a supply chain transformation that leverages strategic sourcing, drives operational excellence, consolidates facilities and optimizes the distribution network, and reduces complexity of the product portfolio.

Transformation Progress

The execution has been remarkably disciplined. The Global Cost Reduction Program generated approximately $120 million of incremental pre-tax run-rate cost savings in the third quarter 2025. Since the inception of the program in mid-2022, it has generated approximately $1.9 billion of the targeted $2.0 billion pre-tax run-rate cost savings. These initiatives are designed to support continued margin enhancement as the Company remains focused on achieving its long term adjusted gross margin target of 35+%.

Chris Nelson, President and CEO: "We're on pace to hit a pretty significant milestone by the end of the year with achieving our $2 billion cost-out target that we set out as a target at the beginning of our transformation. We feel good about the progress we're making towards our margin goals at 35% plus, and we're able to see margin expansion in the quarter as well after a one-quarter step back due to tariffs. I thought that execution and getting back on the margin trajectory was encouraging."

Portfolio Simplification & Divestitures

Alongside cost reduction, management pursued aggressive portfolio simplification, divesting non-core businesses to focus on tools and outdoor products.

On December 8, 2021, Securitas AB announced that it had entered into an agreement to purchase Stanley Black & Decker's electronic security business unit for $3.2 billion.

The company also sold Stanley Access Technologies to Allegion for $900 million in 2022, and Since becoming CEO, Don has been a champion of portfolio simplification, including leading the divestitures of the Security, Attachment Tools, and Oil & Gas businesses and transforming Stanley Black & Decker into a more focused organization.

Chris Nelson noted: "We still have on our radar screen, obviously, the strengthening of the balance sheet. We have a stated objective of 2.5 times debt to EBITDA. We have been pretty public about the fact that we are likely to pursue a pruning action, most likely with our aerospace fastening business, to achieve that."

Leadership Transition

Stanley Black & Decker today announced that its Board of Directors has named Christopher Nelson as the Company's next President and Chief Executive Officer, effective October 1, 2025. Mr. Nelson currently serves as Stanley Black & Decker's Chief Operating Officer and Executive Vice President and President of the Tools & Outdoor business. He will succeed Donald Allan, Jr., who has served as CEO since July 2022.

Mr. Nelson is a seasoned leader with over 25 years of executive leadership, product development, innovation and growth transformation experience. He joined Stanley Black & Decker in 2023 as Chief Operating Officer and Executive Vice President and President of the Tools & Outdoor business. Since joining the Company, he has played a pivotal role in streamlining and optimizing the Company around its core businesses and strong portfolio of brands.

Nelson was President of Carrier's flagship heating, ventilation and air-conditioning segment, where he led the global commercial and residential product and service portfolio. Before joining Carrier, he held leadership roles with the U.S. Army, Johnson & Johnson and McKinsey & Company. Mr. Nelson holds a bachelor's degree from the University of Notre Dame and a master's degree in business from Cornell University.

The leadership transition represents a pivot from crisis management to growth orientation. Allan architected and executed the transformation; Nelson's mandate is to capitalize on the leaner, more focused organization.

Business Model & How It Works Today

Segment Overview

Founded in 1843 and headquartered in the USA, Stanley Black & Decker (NYSE: SWK) is a worldwide leader in Tools and Outdoor, operating manufacturing facilities globally. The Company's approximately 48,500 employees produce innovative end-user inspired power tools, hand tools, storage, digital jobsite solutions, outdoor and lifestyle products, and engineered fasteners to support the world's builders, tradespeople and DIYers. The Company's world class portfolio of trusted brands includes DEWALT®, CRAFTSMAN®, STANLEY®, BLACK+DECKER®, and Cub Cadet®.

The company now operates primarily through two segments:

Tools & Outdoor (~87% of revenue): This segment encompasses power tools, hand tools, storage, and outdoor power equipment. Key brands include DEWALT (professional), CRAFTSMAN (prosumer/tradesperson), STANLEY (hand tools), BLACK+DECKER (consumer), and the outdoor brands (Cub Cadet, Hustler, Troy-Bilt).

Industrial (~13% of revenue): This segment includes engineered fastening and infrastructure solutions. The aerospace fastening business serves automotive, aerospace, and industrial markets with highly engineered components.

Brand Portfolio Strategy

The brand architecture reflects deliberate positioning across price points and customer segments. Our brand-led, market-backed strategy starts with recognizing the needs of our end-users, predominantly the professionals who use our tools and equipment to make a living. With that understanding, we deploy our talented people and innovation capabilities to create solutions that directly address their needs. This approach drives our future growth strategy, led by a transformed, brand-oriented business that puts end-users and innovation first. From power and hand tools to storage and outdoor power equipment, our DEWALT®, CRAFTSMAN® and STANLEY® brands serve the people making our world by continuously improving our solutions and exceeding their expectations for safety and performance.

Stanley Black & Decker now owns DeWalt, Stanley, Black + Decker, Bostitch, Craftsman, Irwin, Lenox, Porter-Cable, and a half-dozen other brands.

DEWALT has emerged as the crown jewel. DEWALT Posts 7th Consecutive Quarter of Organic Growth. The brand's professional positioning, combined with continuous innovation (particularly in battery platform technology like POWERSTACK), has enabled it to gain market share even during the broader industry downturn.

Financial Profile

2024 Revenues of $15.4 Billion, Down 3% Versus Prior Year; Flat Organic Revenue Led by Growth in DEWALT as well as Aerospace Fasteners Offset by Infrastructure Divestiture and Currency.

Full Year Gross Margin Was 29.4%; Full Year Adjusted Gross Margin Was 30.0%. Fourth Quarter EPS Was $1.28 and Adjusted EPS Was $1.49; Full Year EPS Was $1.89 and Adjusted EPS Was $4.36.

Donald Allan, Jr., Stanley Black & Decker's President & CEO, commented, "Stanley Black & Decker delivered across its key focus areas in 2024 with continued gross margin expansion, strong free cash flow generation, strengthening our balance sheet as well as making new investments aimed at driving market share growth. Against a mixed macroeconomic backdrop, we are encouraged by the growth and share gain momentum in DEWALT and within portions of engineered fastening. As we continue on this journey, we are proud to have delivered on key financial milestones, including adjusted gross margin exceeding 31% in the fourth quarter along with strong cash generation."

Competitive Landscape

The global power tools market is consolidated among several major players. These key players hold a significant market share (78.3%), making the industry highly consolidated worldwide. Atlas Copco AB (Sweden), Emerson Electric Co. (U.S.), Enerpac Tool Group (U.S.), Hilti Corporation (Liechtenstein), Ingersoll Rand (U.S.), Koki Holdings Co. Ltd. (Japan), Makita Corporation (Japan), Robert Bosch GmBH (Germany), Stanley Black & Decker Inc. (U.S.), and Tectronic Industries Co. Ltd. (China) are the top players in the market.

Milwaukee Tool: Milwaukee Tool is a subsidiary of Techtronic Industries, a Hong Kong-based company. They are known for their heavy-duty power tools and accessories. Milwaukee Tool's focus on providing solutions for professional users gives them a competitive edge in the market.

Milwaukee, in particular, has emerged as a formidable competitor. Milwaukee Tool's exclusivity with Home Depot, Diablo's exclusivity with Home Depot, and Kobalt's exclusivity with Lowe's enable these brands to secure dedicated shelf space, promotional support, and consistent consumer exposure in targeted retail environments.

Investment Thesis: Bull Case, Bear Case, and Competitive Analysis

Bull Case

Transformation Nearing Completion: The Global Cost Reduction Program has delivered $1.9 billion of its $2 billion target, fundamentally restructuring the cost base. As these savings flow through to margins, the earnings power of the business should increase substantially even in a flat revenue environment.

Brand Portfolio Moat: Stanley Black & Decker President and CEO Donald Allan Jr. joins 'Mad Money' to discuss its portfolio of brands, describing it as "the best in the industry." The collection of DEWALT, CRAFTSMAN, STANLEY, and BLACK+DECKER represents decades of brand equity that would be extraordinarily expensive for competitors to replicate.

DEWALT Momentum: DEWALT Posts 8th Consecutive Quarter of Revenue Growth. The professional segment's consistent growth demonstrates the strength of the brand even in challenging market conditions.

Housing Cycle Recovery: The tools market is highly correlated with housing activity. When interest rates eventually decline and housing construction recovers, pent-up demand should benefit Stanley Black & Decker disproportionately given its market leadership.

Electrification Opportunity: The transition from gas-powered to battery-powered outdoor equipment represents a multi-decade secular tailwind. Stanley Black & Decker's platform approach—leveraging the same battery technology across power tools and outdoor equipment—creates ecosystem advantages.

Bear Case

Tariff Exposure: Second Quarter Revenues of $3.9 Billion, Down 2% Versus Prior Year due to a Slow Outdoor Buying Season and Tariff-Related Shipment Disruptions. Despite shifting production toward North America, the company remains exposed to trade policy volatility.

Competitive Intensity: Milwaukee Tool (TTI) has been aggressively gaining share in the professional segment. The exclusive retail partnerships (Milwaukee with Home Depot) create structural advantages that are difficult to overcome.

Leverage Concerns: We have a stated objective of 2.5 times debt to EBITDA. The balance sheet remains stretched, limiting strategic flexibility and requiring further asset sales.

Consumer/DIY Weakness: The pandemic-era DIY boom has normalized, and the consumer segment faces structural pressure from changing spending patterns. The BLACK+DECKER brand, while iconic, competes in a more commoditized segment.

Outdoor Integration Risk: The MTD acquisition, completed just before the crisis, has not yet delivered the synergies originally projected. The outdoor market faces its own competitive challenges from companies like Husqvarna and pure-play outdoor equipment manufacturers.

Porter's Five Forces Analysis

Threat of New Entrants (Low-Medium): High capital requirements, established distribution relationships, and brand loyalty create significant barriers. However, emerging battery platform competitors from Asia pose increasing threats.

Bargaining Power of Suppliers (Medium): While the company has scale advantages in procurement, critical components like lithium-ion batteries and semiconductors face periodic supply constraints.

Bargaining Power of Buyers (High): Retail concentration in Home Depot, Lowe's, and Amazon gives buyers significant leverage. Private label threats remain constant.

Threat of Substitutes (Low): Power tools and hand tools have limited substitutes for professional and DIY applications.

Industry Rivalry (High): Intense competition from Milwaukee/TTI, Bosch, Makita, and others. The industry has become increasingly promotional, pressuring margins.

Hamilton Helmer's 7 Powers Analysis

Brand (Strong): DEWALT and CRAFTSMAN possess genuine brand power—professional contractors actively seek out these brands, and the lifetime warranty proposition creates customer loyalty. This is the company's primary power source.

Scale Economics (Moderate): The company benefits from manufacturing scale and procurement leverage, but competitors like TTI have achieved comparable scale in key categories.

Switching Costs (Moderate): Battery platform ecosystems create some switching costs, but cross-compatibility and adapter technologies limit this power.

Network Effects (Weak): Limited network effects in the tools industry.

Counter-Positioning (Weak): The company's diversified approach doesn't represent true counter-positioning against focused competitors.

Process Power (Moderate): Manufacturing excellence and supply chain optimization represent potential process advantages, though competitors have similar capabilities.

Cornered Resource (Weak): No truly cornered resources beyond brand heritage.

Key Metrics to Watch

For investors tracking Stanley Black & Decker's ongoing performance, three metrics matter most:

1. Adjusted Gross Margin: The company's long-term target is 35%+ adjusted gross margin. Adjusted gross margin exceeding 31% in the fourth quarter represents meaningful progress but leaves significant room for improvement. This metric captures the success of the supply chain transformation and the company's ability to maintain pricing power.

2. DEWALT Organic Revenue Growth: As the company's most important brand, DEWALT's growth trajectory indicates whether the professional segment strategy is working. Continued organic growth above the market rate would suggest the brand is gaining share.

3. Free Cash Flow Conversion: Given balance sheet constraints, the company's ability to convert earnings into cash flow is critical for debt reduction and dividend sustainability. The company maintained its full-year 2025 guidance, projecting adjusted earnings per share of approximately $4.65 and free cash flow of around $600 million.

Regulatory and Accounting Considerations

Environmental Liabilities: Other, net included $148.4 million of charges, primarily related to environmental remediation reserve adjustments. Legacy manufacturing sites create ongoing environmental remediation obligations that periodically result in charges.

Tariff Policy Uncertainty: Trade policy remains a material risk factor. The company has accelerated supply chain reshoring but cannot fully insulate against tariff-related cost increases.

Goodwill and Intangible Assets: Given the company's acquisition history, the balance sheet carries significant goodwill and intangible assets that could face impairment if growth assumptions prove overly optimistic. The Company recognized $169.1 million of non-cash asset impairment charges in the third quarter of 2025.

Conclusion: The Next Chapter

Stanley Black & Decker's 180-year journey represents a fascinating case study in American industrial evolution. From Frederick Stanley's bolt manufactory to Duncan Black's pistol-grip drill, from the Apollo moon landings to the DustBuster, from the merger of equals to the $2 billion transformation—the company has demonstrated remarkable resilience and adaptability.

Mr. Nelson said, "I am honored to become President and CEO of Stanley Black & Decker, an iconic American company with a proud legacy and an incredibly bright future. Over the past two years, I have had the privilege of working closely with Don and the leadership team, gaining a deep understanding of the needs of our customers and end-users, as well as the unique opportunities ahead for our Company."

The transformation is nearly complete. "Our goal is to build a world class, branded industrial company by solving our end users' most pressing and complex challenges. We have nearly reached a critical milestone on this journey, with our multiyear global cost reduction program on track to achieve targeted 2025 and full-program savings. The proficiency we have developed through this transformation allows us to serve our customers and end users with greater effectiveness and improved profitability."

The company that emerges from this transformation is fundamentally different from the one that entered the crisis. Leaner operations, focused portfolio, and a brand-centric strategy position Stanley Black & Decker for its next chapter. Whether that chapter delivers value creation will depend on execution, market conditions, and the competitive dynamics of an industry that shows no signs of becoming less intense.

The toolmakers who built America face a new challenge: proving that in an era of rapid change and fierce competition, heritage brands and operational excellence can still compound value for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube