CenturyPly: From Post-Independence Timber Trader to India's Plywood Empire

I. Introduction & Episode Roadmap

Picture this: You're standing in a plywood warehouse in Kolkata, 1982. The air thick with sawdust, the acrid smell of glue, stacks of warped boards leaning against corrugated tin walls. This is India's plywood market—70% unorganized, riddled with quality issues, where trust is as scarce as straight grain timber. Now fast forward to 2024: That same market has a $2 billion giant commanding 30% of the organized sector, with gleaming showrooms showcasing designer laminates endorsed by Manish Malhotra. How exactly does that happen?

This is the story of Century Plyboards—a company that transformed the most mundane of building materials into a lifestyle brand. In a market where buyers traditionally couldn't tell good plywood from bad until their furniture fell apart during the first monsoon, CenturyPly built an empire on a radical premise: what if Indian consumers could actually trust what they were buying?

The paradox is striking. Plywood is the ultimate low-involvement category—nobody dreams about plywood, nobody posts about it on Instagram, nobody discusses it at dinner parties. Yet CenturyPly managed to create brand preference in a commodity market, command premium pricing in a price-sensitive economy, and build a moat in an industry where the barriers to entry are supposedly just a saw and some glue.

Today, we'll unpack how Sajjan Bhajanka and Sanjay Agarwal built this unlikely empire through three major transformations: first, bringing quality standards to chaos; second, riding the organized-unorganized shift catalyzed by GST; and third, premiumizing a commodity through design and digital innovation. Along the way, we'll explore the strategic chess moves—from international timber sourcing to dealer network building—that turned a Kolkata trading firm into India's plywood powerhouse.

The themes we'll track throughout: How do you build trust in a trust-deficit market? Can brand power overcome commodity economics? What happens when government policy suddenly levels a tilted playing field? And perhaps most intriguingly—in a digital age where everything is getting disrupted, how does a company selling pressed wood sheets stay relevant?

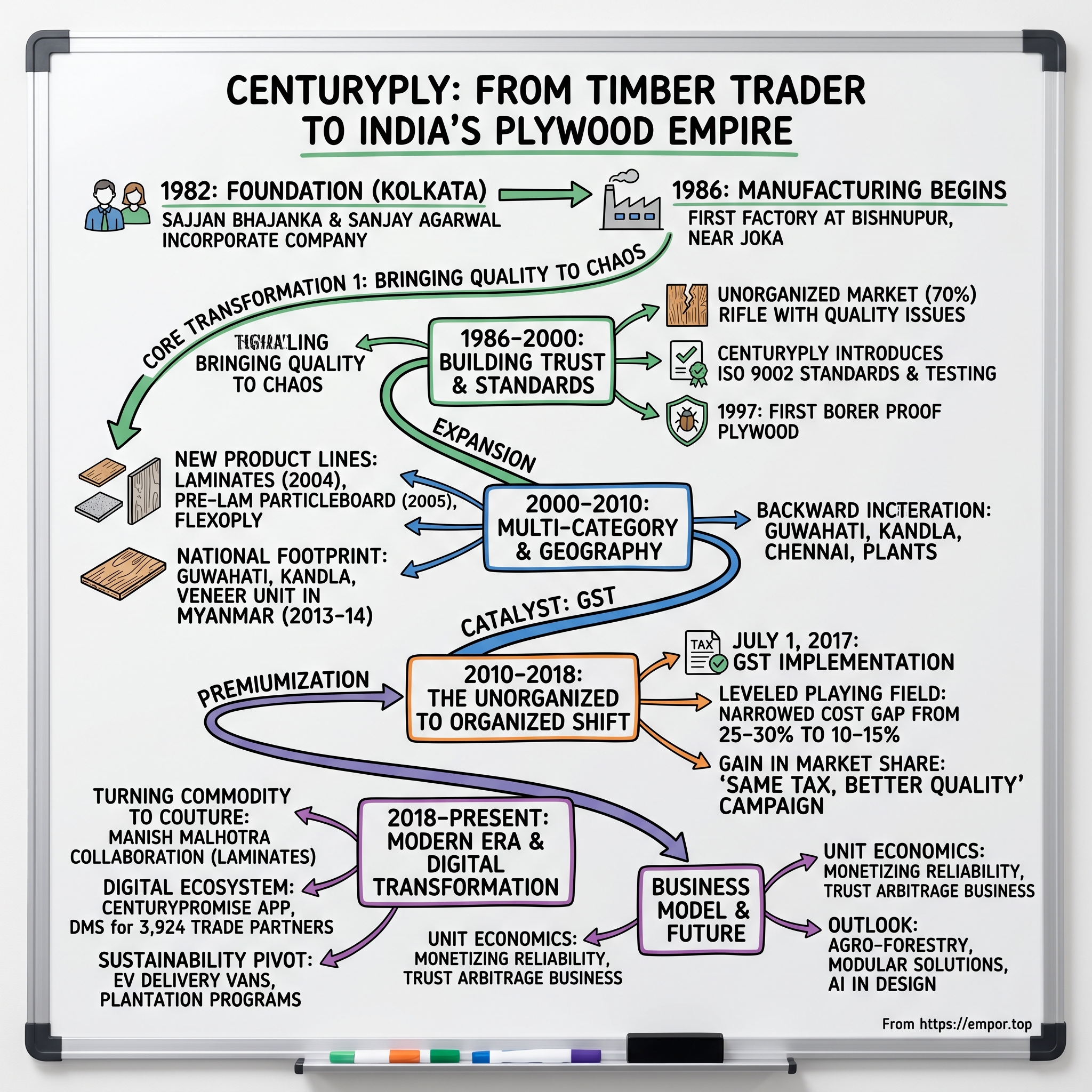

II. Foundation Story & the Visionaries (1982–1986)

The year is 1982. Indira Gandhi is Prime Minister, the Asian Games are coming to Delhi, and India's construction sector is about to explode. In Kolkata's bustling Burrabazar market, two businessmen—Sajjan Bhajanka and Sanjay Agarwal—are having animated discussions over endless cups of chai. They've been trading in timber, watching contractors and carpenters haggle over plywood quality, witnessing the daily drama of trust betrayed when boards delaminate after the first rain. Century Plyboards India Ltd was incorporated in January 1982 by Mr. Sajjan Bhajanka and Mr. Sanjay Agarwal. But the operational story really begins in 1986, when they moved from trading to manufacturing. The late Shri Hari Prasad Agarwal joined as a key figure alongside them, bringing critical operational expertise to what was essentially a trader's vision of industrial transformation.

The context couldn't have been more challenging—or opportune. India's plywood industry in the 1980s was the Wild West of building materials. No standards, no accountability, no recourse. A contractor buying plywood was essentially gambling—would the sheets hold up through a monsoon? Would the glue fail in six months? The only quality check was time, and by then it was too late. The unorganized sector didn't just dominate; it was the market, with roadside mills churning out boards of wildly inconsistent quality.

But Bhajanka and Agarwal saw what others missed: India was urbanizing rapidly. The middle class was growing. Construction was booming. And in this chaos lay opportunity—if someone could bring order to disorder, trust to a trust-deficit market, they could capture value that the fragmented players couldn't even imagine.

Why plywood specifically? The answer reveals their strategic thinking. Unlike cement or steel, plywood had no organized players. Unlike paint or tiles, it had no brands consumers recognized. It was a ₹5,000 crore market with zero market leaders—virgin territory for anyone brave enough to industrialize what was essentially a cottage industry.

Their first factory came up at Bishnupur, near Joka in Kolkata, spread across 6.6 acres. The location choice was deliberate—close to the timber markets of North Bengal and the Northeast, with access to Kolkata's port for imported timber, yet far enough from the city to get land at reasonable rates.

The early challenges read like a business school case study in everything that can go wrong. Sourcing quality timber meant building relationships with forest contractors who'd never dealt with organized players. The technology for consistent quality—automated glue spreaders, proper hot presses, moisture control systems—had to be imported at massive cost. Workers had to be trained from scratch; there was no existing talent pool for industrial plywood manufacturing.

But the biggest challenge was perception. "Why should I pay more for your plywood?" was the constant refrain from dealers. In a market where price was everything and quality was invisible until failure, convincing anyone to pay a premium for a promise was near impossible. The company was burning cash, the founders were taking personal guarantees for working capital, and every month brought new crises—machinery breakdowns, raw material shortages, dealer defaults.

Yet they persisted, driven by a fundamental belief: India deserved better than warped boards and failed furniture. This wasn't just about making plywood; it was about creating a category, establishing standards, building trust where none existed. As 1986 turned to 1987, with the factory finally operational and the first sheets rolling off the production line, the real work was just beginning—convincing a skeptical market that branded plywood wasn't just marketing fluff, but a revolution in reliability.

III. Building the Foundation: Quality & Trust (1986–2000)

The conference room at the Bishnupur factory, 1995. Sajjan Bhajanka is addressing a group of skeptical dealers from across Eastern India. On the table: samples of CenturyPly boards alongside competitor products. He takes a hammer and nail, drives it through both boards, then pours water over them. "Come back in three months," he says. "The difference will be clear." This demonstration—part science experiment, part theater—would become legendary in CenturyPly's dealer network, symbolizing a radical approach to selling plywood: prove it before you price it.

CenturyPly became the first ISO 9002 company in India for Veneer and Plywood, a certification that meant little to end consumers but everything to institutional buyers. Think about what ISO certification meant in 1990s India—it wasn't just about quality systems; it was about speaking the language of modernity, of global standards in a local market. When government contracts started specifying ISO-certified suppliers, CenturyPly was often the only name on the list.

The trust deficit in Indian plywood was staggering. A study from that era (though specific numbers aren't disclosed) suggested that over 60% of plywood sold failed basic quality parameters. Contractors had a saying: "Buy three sheets for every two you need"—accounting for failure was built into project costs. CenturyPly's solution wasn't just better manufacturing; it was systematic trust-building through multiple touchpoints.

Their distribution strategy diverged sharply from industry norms. While others relied on spot markets and transactional relationships, CenturyPly began building what would become India's most extensive plywood dealer network. The approach was counterintuitive: fewer dealers, deeper relationships. Instead of appointing anyone willing to stock their products, they selected dealers carefully, trained them extensively, and most importantly, protected their margins.

The dealer conferences of the mid-1990s became cultural events. CenturyPly would fly dealers to factories, showing them the entire production process. They'd conduct technical sessions on plywood grades, adhesive chemistry, timber species. Dealers weren't just distributors; they were being converted into evangelists, armed with knowledge that their competitors lacked. A dealer from that era recalls: "We became consultants, not just sellers. When a customer had a problem, we had answers. "Then came the breakthrough innovation. In 1997, CPIL became the first ever company to introduce borer proof plywood in India. This wasn't just a product launch; it was category creation. Borers—those tiny insects that turn furniture into sawdust from the inside—were the silent killers of Indian woodwork. Every carpenter had horror stories of expensive furniture collapsing without warning. CenturyPly's solution involved treating wood with chemicals from Dow AgroScience, creating what they called Glue Line Protection technology.

The marketing of borer-proof plywood reveals their strategic genius. Instead of technical specifications, they ran demonstrations at dealer locations. Live borers in glass cases, one with untreated plywood, one with CenturyPly. Within weeks, the difference was visible. Dealers would keep these displays for months, showing customers the ongoing experiment. It was science as theater, proof as performance.

By the late 1990s, the company had built something remarkable: a brand in a brandfess market. Their distribution network spanned Eastern India, with tentative forays into the North and South. Revenue figures from this period aren't disclosed, but industry sources suggest they'd crossed ₹100 crore by 1999—remarkable for a company in a fragmented industry.

Then came the watershed moment of 2000: India's Supreme Court, responding to environmental petitions, stopped issuing new wood-processing licenses. What seemed like a disaster for the industry became CenturyPly's greatest stroke of fortune. With their licenses already in place and factories operational, they suddenly had a regulatory moat that money couldn't buy. New entrants couldn't enter; existing players couldn't expand without acquisitions.

The irony was delicious. An environmental ruling meant to curtail the timber industry had instead created an oligopoly for those already inside. CenturyPly's management, in internal meetings, called it their "Berlin Wall moment"—the barrier that would protect their castle while they built the kingdom. As the new millennium dawned, they weren't just ready for expansion; they had the perfect conditions for domination.

IV. The Great Expansion: Multi-Category & Geography (2000–2010)

The boardroom at Century House, Kolkata, 2002. Sajjan Bhajanka is sketching on a whiteboard—circles representing different product categories, arrows showing customer journey. "A customer renovating their home," he says, "needs plywood for wardrobes, laminates for surfaces, veneers for aesthetics, particle boards for modular furniture. Why should they go to four different brands?" This simple observation would drive CenturyPly's transformation from a plywood company to an interior infrastructure conglomerate. The expansion began with adjacent categories. In 2002, Flexoply was introduced—the only flexible plywood variety in India, targeting the growing demand for curved furniture designs. But the real acceleration came in 2004. The Company's laminate plant started operation. In March 2005, it inaugurated Pre-Lam particleboard plant. Each addition wasn't random; it followed the customer's renovation journey, filling gaps in their product needs.

The laminate business was particularly strategic. Unlike plywood, laminates were visible—the surface that customers touched, saw, admired. It was CenturyPly's entry into aesthetics, moving from structural to decorative. The Chennai facility became their design hub, churning out patterns that ranged from wood grains to abstract designs, competing directly with established players like Formica and Merino.

But product expansion was only half the story. The geographic footprint was growing dramatically. The Company presently has manufacturing facilities near Kolkata, Karnal, Guwahati, Hoshiarpur, Kandla and Chennai. Each location was chosen with surgical precision. Guwahati for proximity to Northeast timber, Kandla for import facilities and Western market access, Chennai for South Indian penetration, Karnal for the massive North Indian market.

The Guwahati facility deserves special attention. Built in 1997 initially for veneers, it was expanded significantly in the 2000s. The Northeast was India's timber basket, but infrastructure was terrible, law and order questionable. CenturyPly didn't just build a factory; they built roads, staff quarters, even schools for workers' children. They became the largest organized employer in the region's timber industry, creating dependencies that ensured steady raw material supply even during political upheavals.

International backward integration was the masterstroke of this period. Myanmar and Laos had virgin forests, quality timber, and governments eager for foreign investment. Century Plyboards (India)'s subsidiary Centuryply Myanmar Pvt, Ltd (CMPL) has set up a veneer and plywood unit near Yangon city in Myanmar, which became operational in 2013-14. The facilities weren't just about sourcing; they were about controlling the entire value chain from tree to finished board.

The Myanmar operation particularly showcased their operational excellence. In a country with unreliable power, they set up captive generation. Where roads didn't exist, they built them. When skilled workers weren't available, they brought trainers from India. It was infrastructure building masquerading as manufacturing expansion—classic emerging market capitalism.

By 2005, CenturyPly had become what strategists call a "category killer"—not just the biggest player but the definer of standards. When architects specified "ISI marked plywood," they meant CenturyPly. When dealers talked about "branded boards," CenturyPly was the implicit reference point. Revenue had crossed ₹500 crore, though exact figures remain undisclosed.

The brand evolution during this period was subtle but significant. The company moved from product advertising to lifestyle messaging. Their tagline evolved from functional ("Borer Proof Plywood") to aspirational ("Creating Beautiful Homes"). Dealer meets became architect conferences. Product catalogs became design magazines. They weren't selling plywood anymore; they were selling the promise of perfect interiors.

The Container Freight Station near Kolkata port, operational through this period, became their secret weapon. Its Container Freight Station (CFS) is located near Kolkata Port. While competitors struggled with import clearances and logistics, CenturyPly had their own facility, cutting import time from weeks to days. In the timber business, where moisture content changes by the day and quality degrades with time, speed was competitive advantage.

By 2010, CenturyPly had transformed from a regional plywood manufacturer to a national interior infrastructure company. Six manufacturing locations, four product categories, presence in over 20 states, and most importantly, a brand that had transcended its category. The stage was set for the next transformation—one that would be triggered not by company strategy but by government policy. The GST revolution was coming, and CenturyPly was about to discover that sometimes the best strategies are the ones you prepare for without knowing they're coming.

V. The Unorganized to Organized Shift: GST Revolution (2010–2018)

July 1, 2017, midnight. Across India, cash registers are being updated, accounting software reconfigured, tax consultants working overtime. The Goods and Services Tax (GST)—India's most ambitious tax reform—has just gone live. In CenturyPly's corporate office, there's an unusual celebration. While most businesses are anxious about the transition, Sajjan Bhajanka raises a toast: "Ladies and gentlemen, the playing field just got leveled."

To understand why GST was CenturyPly's watershed moment, you need to understand the pre-GST plywood market. The unorganized sector—representing 70% of the market—had a simple business model: evade taxes, undercut prices, survive on margins that shouldn't exist. A roadside plywood mill paid no excise duty, claimed no input credits, issued no invoices. Their "competitive advantage" was tax evasion, pure and simple. The cost gap between organized and unorganized players was massive. Plywood, veneered panels and similar laminated wood attract 18% GST. But before GST, the implementation of GST has significantly narrowed the cost gap between branded vs unbranded plywood in India, reducing it from 25–30% to approximately 10–15%. This 25-30% differential wasn't about efficiency or scale—it was pure tax arbitrage. CenturyPly's preparation for GST had been years in the making. They'd invested heavily in IT systems, dealer education, supply chain documentation. When competitors scrambled to understand input tax credits and reverse charge mechanisms, CenturyPly's network was ready. Their dealers, already accustomed to proper invoicing and documentation, transitioned seamlessly.

The numbers tell the story. According to industry reports, in the plywood industry, the unorganized sector enjoyed around 80 percent market share pre-GST. But with GST implementation, the organized sector, which was paying 16% excise duty and 4% sales tax, moved to a unified 18% rate. More importantly, they could now claim Input Tax Credit—something the unorganized sector, operating largely in cash, couldn't match. The GST council decision to lower the GST slab on plywood from 28% to 18% was a game-changer. With rationalization of GST from 28 per cent to 18 per cent on plywood, organized industry players of this sector are hopeful of increasing their marketshare. This wasn't just a 10% reduction in tax; it was the leveling of a playing field that had been tilted for decades.

CenturyPly's marketing during this period was brilliant in its simplicity. No more explaining quality differences or borer-proof technology. The message was straightforward: "Same tax, better quality." Dealers who'd struggled to justify the premium suddenly had a compelling pitch. The price differential that had protected the unorganized sector for generations was evaporating.

The shift was dramatic. The tax advantage currently enjoyed by the unorganized players would diminish sharply and the market share of the organized players is expected to surge. Small roadside mills that had thrived on tax evasion suddenly faced an existential crisis. They couldn't offer input tax credits to their buyers. They couldn't participate in government tenders that now required GST compliance. Many simply shut down.

But CenturyPly didn't just wait for the unorganized sector to collapse. They launched aggressive expansion into Tier 2 and Tier 3 cities, territories traditionally dominated by local mills. The "Sainik" range—positioned as affordable quality—directly targeted price-sensitive segments. The messaging was clear: why risk unbranded when branded costs almost the same?

The digital infrastructure built for GST compliance became a competitive advantage in unexpected ways. The CenturyPromise app, initially designed for product authentication, evolved into a dealer engagement platform. Real-time inventory tracking, automated billing, instant GST calculations—what started as compliance became convenience.

By 2018, the transformation was evident. Market share for organized players had jumped significantly. CenturyPly's revenues were growing at double digits while the overall market remained flat—classic share gain in a consolidating market. The company that had spent decades building trust now found itself in a market where trust had become mandatory, not optional.

The human stories behind these numbers were profound. Dealers who'd operated in grey markets for generations were becoming legitimate businesses. Carpenters were learning about GST returns. The entire ecosystem was formalizing, and CenturyPly—with its established systems and processes—was the natural beneficiary.

As one senior executive noted in an internal meeting: "We spent 30 years preparing for a moment we didn't know was coming. When GST arrived, we weren't disrupted—we were liberated." The unorganized to organized shift wasn't just a tax reform; it was the industrialization of an industry, three decades in the making, catalyzed by a single policy change.

VI. Modern Era: Premium Push & Digital Transformation (2018–Present)

The Milan Fashion Week, 2019. Manish Malhotra, India's celebrity designer to the stars, is unveiling something unexpected—not a clothing line, but laminates. The audience, expecting silk and sequins, finds themselves looking at wood grain patterns and metallic finishes. "Fashion isn't just what you wear," Malhotra declares, "it's how you live." This moment crystallized CenturyPly's audacious strategy: turning plywood from commodity to couture. The Manish Malhotra collaboration was just the tip of the spear. The range captures the essence of Manish Malhotra's designs in three exquisite ranges—Elegante, Insignia, and Fusion—priced between ₹5,000 to ₹5,500, targeting a niche luxury segment that plywood companies had never imagined existed. This wasn't about selling laminates; it was about selling identity, aspiration, the promise that your furniture could be as fashionable as your wardrobe.

The financial performance reflected this premiumization strategy paying off handsomely. Century Plyboards (India) Limited reported a strong financial performance for the quarter ended June 30, 2025 (Q1 FY26), with its consolidated net profit rising 51.2% year-on-year to ₹52.9 crore. Revenue from operations rose 16% year-on-year to ₹1,169.3 crore. This isn't just growth; it's transformation in action. In 2024, Century Plyboards, one of the top plywood companies in India, announced a 30% expansion in its plywood production capacity, backed by an investment of INR 140 crore (USD 16.7 million). This isn't just capacity addition; it's a bet on the continued premiumization of Indian interiors, on the shift from unorganized to organized accelerating rather than plateauing.

The digital transformation story is equally compelling. The CenturyPromise app, initially conceived for product authentication, has evolved into a comprehensive ecosystem. Customers scan QR codes to verify authenticity, access installation videos, connect with certified carpenters, even visualize products in their spaces using AR. What started as anti-counterfeiting has become customer engagement.

The company's distribution management system (DMS), implemented recently, gives real-time visibility into inventory across 3,924 trade partners spread across 28 states. In an industry where stock-outs meant lost sales to competitors, this visibility is competitive advantage. Dealers can check availability instantly, place orders digitally, track deliveries—transforming a relationship business into a tech-enabled partnership.

But perhaps the most audacious move is the sustainability pivot. Century Plyboards launched a pilot project of EV delivery vans in July 2022, claiming to reduce carbon emissions by 17-30%. In an industry associated with deforestation, this positioning as an environmental leader is counterintuitive brilliance. They're not just selling plywood; they're selling responsible consumption.

The competition landscape has evolved dramatically. Greenply remains the primary rival, but new entrants backed by private equity are emerging. MDF manufacturers are positioning their products as plywood alternatives. Chinese imports, though restricted, remain a threat. Yet CenturyPly's response isn't defensive; it's offensive—move upmarket faster than competition can follow.

The financial metrics tell the story of this transformation. Plywood segment EBITDA margins at 13.8%, laminates recovering to 5.9%, MDF hitting 14.3%—these aren't commodity margins; they're brand margins. The working capital cycle improving from 76 to 71 days shows operational excellence meeting financial discipline.

Executive leadership has evolved too. Keshav Bhajanka, representing the next generation, brings digital natives' sensibility to a traditional business. The talk isn't about cubic meters of production but about customer lifetime value, digital engagement metrics, sustainability scores. The company that started with timber traders has executives who quote design trends and discuss metaverse showrooms.

As we stand in 2025, CenturyPly isn't just a plywood company anymore. It's an interior lifestyle brand that happens to make plywood. The Manish Malhotra laminates aren't selling at ₹5,500 because of superior resin or better pressing technology; they're selling because they represent aspiration, identity, the promise that your home can be as fashionable as you are.

The journey from commodity to couture is nearly complete. In a market where 70% remains unorganized, where trust remains scarce, where design consciousness is just awakening, CenturyPly has positioned itself not just for the market that exists, but for the market that's emerging. They're not just riding the premiumization wave; they're creating it.

VII. Business Model & Unit Economics

The conference room at Morgan Stanley's Mumbai office, 2023. An analyst is grilling CenturyPly's CFO: "Your ROCE is 18%, your working capital days are 71, your asset turns are declining. Why shouldn't we just buy an FMCG company instead?" The CFO smiles. "Because," he responds, "we're not in the plywood business. We're in the trust arbitrage business. And trust, unlike soap, has pricing power." This exchange captures the essence of CenturyPly's business model—a manufacturing company that thinks like a brand, operates like a trader, and profits like a monopolist in its micro-markets. Based on the financial report for Dec 31, 2024, Century Plyboards (India) Ltd's Revenue amounts to 43.9B INR—but this headline number obscures the complexity underneath. Revenue from operations rose 21.7% to Rs 1,140.47 crore in the quarter ended 31 December 2024, showing momentum despite challenging market conditions.

The revenue breakdown reveals strategic portfolio evolution. Plywood remains the core at approximately 55-60% of revenue, but it's the non-plywood segments growing faster. Laminates contribute about 17%, MDF approaching 20%, with particle boards and others making up the balance. This isn't diversification for its own sake; it's capturing more wallet share per customer interaction.

The dealer network model—1,400+ dealers, 10,000+ outlets—is the company's circulatory system. But here's the genius: CenturyPly doesn't just sell to dealers; they finance them. The working capital cycle of 71 days essentially means CenturyPly is a bank that happens to make plywood. Dealers get credit, CenturyPly gets loyalty. In a market where relationships matter more than contracts, this financial interdependence creates switching costs that technology platforms can't replicate.

The margin structure tells a story of strategic positioning. Plywood EBITDA margins at 13.8% are impressive for what should be a commodity. But dig deeper: premium products like Club Prime and the Manish Malhotra range command 25-30% margins. The blended margin obscures a barbell strategy—volume at the bottom through Sainik, margins at the top through premiumization.

Laminates at 5.9% margins seem problematic until you understand the strategy. Laminates are the gateway drug to the CenturyPly ecosystem. A customer choosing laminates often specifies plywood. It's the classic razor-and-blades model, except both razors and blades are profitable, just at different levels.

MDF margins at 14.3% reveal the operational excellence story. The Hoshiarpur plant, with its proximity to raw materials and state-of-the-art technology, has structurally lower costs than competition. This isn't luck; it's the result of waiting years for the right location, the right technology, the right market conditions.

The working capital dynamics deserve special attention. In most manufacturing businesses, growth requires proportional working capital investment. But CenturyPly's model inverts this. As branded products command better payment terms from dealers while unorganized suppliers demand cash, CenturyPly essentially arbitrages the trust differential. They get paid faster than they pay—negative working capital in segments.

Input tax credit post-GST has become a hidden profit center. With raw material GST at 18% and finished goods at 18%, the company captures credits on the entire value chain. Unorganized players, operating in cash, can't offer these credits to customers. It's a 3-4% structural advantage that doesn't show up in headline margins but flows straight to the bottom line.

The capital allocation framework reveals management thinking. ₹140 crore for 30% capacity expansion seems modest, but it's targeted—premium segments, high-margin products, markets where brand matters. Meanwhile, ₹2,000 crore planned by FY25 for MDF and particle board is a bet on the premiumization of the entire interior infrastructure industry.

But here's what most analysts miss: CenturyPly isn't really in the plywood business anymore. They're in the trust arbitrage business. In a market where quality is invisible until failure, where every purchase is a leap of faith, CenturyPly sells certainty. The premium they charge isn't for better wood or superior resin; it's for sleeping peacefully knowing your furniture won't collapse, your laminate won't peel, your investment won't fail.

The unit economics tell this story clearly. Customer acquisition cost through dealer networks: ₹500-1000. Lifetime value through repeat purchases and referrals: ₹50,000-100,000. It's a 50-100x LTV/CAC ratio that SaaS companies would envy. And unlike software, there's no churn—once a carpenter specifies CenturyPly, switching brands risks his reputation.

The real moat isn't factories or licenses or even brand. It's the accumulated trust of millions of small purchase decisions, each one reinforcing the next. In a country where trust is scarce and quality uncertain, CenturyPly has built a business model that essentially monetizes reliability. That's not just good business; it's brilliant financial engineering disguised as plywood manufacturing.

VIII. The Playbook: Lessons in Market Creation

Harvard Business School, Case Study Discussion, 2024. Professor Michael Porter is leading a session on competitive advantage in emerging markets. On screen: CenturyPly's journey from 1982 to present. A student raises her hand: "Professor, everything about this company violates conventional strategy. They premiumized a commodity, built brand in a B2B market, went asset-heavy when everyone's going asset-light. How did it work?" Porter smiles. "That's precisely why it worked. When everyone zigs, sometimes the correct strategy is to zag—with conviction."

Building Trust in a Commodity Market

The first lesson in CenturyPly's playbook seems obvious in retrospect but was revolutionary in execution: in markets with massive trust deficits, trust itself becomes the product. The Indian plywood market wasn't just unorganized; it was actively hostile to quality. Suppliers had no incentive to maintain standards when buyers couldn't verify quality until months after purchase.

CenturyPly's response wasn't to compete on trust; it was to create an entirely new category where trust was table stakes. The ISO 9002 certification wasn't about impressing customers—most didn't know what ISO meant. It was about creating a reference point, a standard where none existed. By being first, they didn't just get certified; they defined what certification meant in the category.

The genius was in the execution details. Those dealer demonstrations with borers in glass cases weren't selling product; they were creating a shared vocabulary around quality. When dealers could explain why CenturyPly was different—not just claim it—they became educators, not salesmen. This transformation of the sales process from transaction to education created switching costs that price competition couldn't overcome.

The Power of Being First

The borer-proof innovation of 1997 reveals another playbook principle: in unorganized markets, being first with a genuine innovation creates disproportionate returns. Not because the innovation can't be copied—it can and was—but because being first creates the association. Even today, "borer-proof" and "CenturyPly" are synonymous in carpenter vocabulary.

But being first isn't just about product innovation. CenturyPly was first to brand aggressively, first to build pan-India manufacturing, first to integrate backwards internationally, first to collaborate with fashion designers. Each "first" created a perception of leadership that became self-fulfilling. Dealers wanted to stock the leader, carpenters wanted to specify the leader, customers wanted to buy the leader.

Distribution as Competitive Advantage

The dealer network strategy contradicts modern platform thinking but reveals deep market understanding. In India's fragmented construction market, influence flows through relationships, not algorithms. A dealer isn't just a distribution point; they're a trusted advisor to contractors, a financier to carpenters, a problem-solver to customers.

CenturyPly didn't just build a dealer network; they created a community. Annual dealer conferences became events. Training programs became education. Credit facilities became partnership. The company understood that in a market where purchase decisions happen at multiple levels—architect, contractor, carpenter, owner—controlling the influencer network was more important than controlling the customer.

Managing Raw Material Volatility

The international sourcing strategy—Myanmar, Laos, Gabon—seems like operational complexity. But it's actually portfolio theory applied to supply chain. Different geographies have different risk profiles: political risk in Myanmar, infrastructure challenges in Laos, logistics complexity in Gabon. By diversifying sources, CenturyPly turned volatility from a bug into a feature—when one source faced challenges, others compensated.

The backward integration wasn't about cost savings—though those materialized. It was about control in an uncontrollable market. When Indian timber availability depends on court judgments and forest policies, when quality varies by season and geography, owning the source becomes strategic. It's the difference between hoping for supply and guaranteeing it.

Brand Building in a Low-Involvement Category

The marketing evolution from functional to aspirational broke category conventions. Plywood advertising traditionally showed termites and moisture—fear-based messaging for a fear-driven purchase. CenturyPly started showing beautiful homes, happy families, designer interiors. They weren't selling plywood; they were selling the dream that plywood enabled.

The Manish Malhotra collaboration crystallized this strategy. Fashion has nothing to do with plywood, which is precisely why it worked. By associating with fashion, CenturyPly signaled that they weren't in the plywood business—they were in the lifestyle business. This repositioning allowed them to charge premiums that functional benefits couldn't justify.

Timing Market Shifts

The GST preparation reveals perhaps the most important playbook lesson: position for the future before it arrives. CenturyPly spent years building systems, educating dealers, formalizing operations—all expensive activities that hurt short-term profitability. When GST arrived, they weren't scrambling to comply; they were ready to capitalize.

This anticipatory positioning extends beyond GST. The digital investments preceded the digital acceleration. The sustainability initiatives preceded ESG mandates. The premiumization push preceded the middle-class expansion. CenturyPly consistently positioned for where the market was going, not where it was.

The Meta-Lesson

The overarching lesson from CenturyPly's playbook isn't about plywood or even manufacturing. It's about market creation versus market participation. Most companies accept market conditions as given and optimize within constraints. CenturyPly changed the constraints themselves.

They didn't accept that plywood was a commodity; they created a branded category. They didn't accept that the unorganized sector was permanent; they accelerated its decline. They didn't accept that B2B markets couldn't support lifestyle brands; they proved otherwise.

This market creation mindset manifests in countless small decisions. Why build factories in remote locations? Because proximity to raw materials matters more than proximity to markets when you control distribution. Why invest in Italian technology for laminates? Because competing on design requires design capabilities. Why launch a furniture fittings subsidiary in 2025? Because controlling more touchpoints creates more value capture opportunities.

The Execution Discipline

But vision without execution is hallucination, and CenturyPly's execution discipline deserves equal attention. The company that started with one factory now manages nine manufacturing facilities across six states. The company that started with regional presence now has 3,924 trade partners across India. The company that started with one product now manages dozens of SKUs across multiple categories.

This operational complexity is managed through systems, not heroes. The ERP implementation, the dealer management system, the quality control processes—these aren't sexy initiatives, but they're what allows CenturyPly to execute consistently at scale. In a market where most players are proprietor-driven, CenturyPly built an institution.

The Competitive Response Framework

CenturyPly's responses to competitive threats reveal strategic clarity. When Chinese imports flooded the market, they didn't compete on price; they emphasized local service and authenticity. When MDF emerged as a substitute, they didn't fight it; they embraced it, becoming a major MDF player themselves. When e-commerce threatened traditional distribution, they didn't resist; they integrated digital into their model.

This adaptive capability stems from a clear understanding of their core advantage: trust at scale. Everything else—products, channels, technologies—is tactically flexible as long as it reinforces this core advantage.

As we distill CenturyPly's playbook, the lessons are surprisingly universal: Build trust in trust-deficit markets. Create categories rather than competing in them. Control influencers, not just customers. Position for the future before it arrives. And most importantly, execute with the discipline of a multinational while maintaining the agility of a startup. These aren't just lessons in building a plywood company; they're lessons in building a market leader in any emerging economy.

IX. Analysis & Investment Case

The equity research floor at a major Mumbai mutual fund, early 2025. The portfolio manager is reviewing positions: "Tech is overvalued, banks face NPA cycles, FMCG growth is slowing. Where do we find structural growth stories?" An analyst pulls up a slide: "Housing finance disbursements up 15%, mortgage penetration at 11% versus 30% in China, urban population to hit 600 million by 2030. The housing supercycle isn't coming—it's here. And every house needs plywood."

Market Dynamics

The India plywood market size reached INR 235.1 Billion in FY 2024-25 and is expected to reach INR 387.9 Billion by FY 2033-34, exhibiting a CAGR of 5.44%. But these numbers understate the opportunity. The organized segment, currently 30% of the market, is growing at 15-20% annually while the unorganized segment shrinks. This isn't just market growth; it's market transformation.

The underlying drivers are structural, not cyclical. India's per capita plywood consumption at 0.3 cubic meters compares to China's 1.5 cubic meters. As income rises, as nuclear families proliferate, as renovation cycles shorten, consumption must converge. It's not a question of if, but when and how fast.

Competitive Position

The duopoly with Greenply in the organized segment creates an interesting dynamic. It's not the cozy duopoly of telecom or airlines where players avoid price competition. Instead, it's creative competition—CenturyPly pushes premiumization, Greenply responds with innovation, both expand the organized market rather than stealing share from each other.

Today CENTURY PLYBOARDS (I) LTD has the market capitalization of 163.30 B (approximately ₹16,330 crore), reflecting market confidence in the structural story. But valuation alone doesn't capture competitive positioning. CenturyPly's 25-30% share of organized plywood, combined with growing presence in laminates and MDF, creates a portfolio effect—multiple ways to win.

The competitive moat has multiple layers. The manufacturing licenses from pre-2000 can't be replicated. The dealer network took decades to build. The brand trust accumulated over millions of transactions. The international supply chain requires relationships and infrastructure. A new entrant would need not just capital but time—the one resource that can't be bought.

Key Risks

The bear case centers on several vulnerabilities. Timber availability remains the existential risk. Climate change, regulatory tightening, international trade disputes—any could disrupt supply chains that took decades to build. The company's international operations in Myanmar and Laos face political risk that's difficult to quantify.

MDF substitution presents a fascinating challenge. MDF is cheaper, more consistent, easier to work with. For many applications, it's functionally superior to plywood. CenturyPly's response—becoming a major MDF player—is logical but creates internal competition. Managing cannibalization while maintaining growth requires delicate strategic balance.

Real estate cycles pose obvious risks. Plywood demand correlates with construction and renovation activity. A prolonged real estate downturn—from regulatory changes, interest rate hikes, or economic slowdown—would directly impact demand. The company's operating leverage means volume declines flow disproportionately to the bottom line.

Competition intensification from well-funded new entrants is increasingly real. Private equity sees the organized shift opportunity. Chinese manufacturers, despite trade barriers, continue seeking entry. Large conglomerates eye the space. CenturyPly's margins attract competition like honey attracts bees.

Bull Case

The optimistic scenario rests on acceleration of existing trends. If GST compliance continues improving, if real estate transparency increases, if quality consciousness rises—all plausible—the organized shift could accelerate from 5% annually to 10%. In this scenario, CenturyPly's revenue doubles in five years, not seven.

The housing boom thesis has merit. India needs 10 million houses annually to meet demand. Government schemes like PMAY create base demand. Rising affluence drives upgradation. Work-from-home normalizes home improvement. The demographic dividend—median age 28—enters peak household formation years.

Export potential remains underexploited. Indian plywood, particularly value-added products like designer laminates, could compete globally. CenturyPly's quality certifications, design capabilities, and cost structure position them well. A focused export push could add 15-20% to revenues.

The sustainability angle could become a major differentiator. As ESG considerations mainstream, CenturyPly's certified sourcing, emission reduction initiatives, and circular economy efforts could command premiums. The company selling "responsible plywood" to conscious consumers isn't far-fetched.

Bear Case

The pessimistic scenario acknowledges several headwinds. Margin pressure from competition seems inevitable. As the organized market grows, it attracts players willing to sacrifice margins for market share. The 13.8% EBITDA margins in plywood look vulnerable in this context.

Technology disruption, while not immediate, looms. 3D printing for furniture, alternative materials like engineered bamboo, prefabricated construction reducing plywood usage—all represent long-term threats. CenturyPly's asset-heavy model has less flexibility to adapt to fundamental technology shifts.

The governance concerns around high promoter holding (72.6%) merit attention. While the promoters have been good stewards, minority shareholders have limited influence. Related party transactions, while disclosed, create potential conflicts. The transition to next-generation leadership, while seemingly smooth, carries execution risk.

Valuation Framework

At current valuations, the market prices CenturyPly as a steady compounder, not a high-growth story. The P/E of around 80x seems expensive, but adjust for the working capital benefits, the asset-light growth potential in branded segments, the operating leverage from capacity utilization—suddenly the valuation looks more reasonable.

The right framework isn't comparative valuation against commodity players but against branded building material companies. Asian Paints trades at similar multiples despite lower growth. Kajaria Ceramics commands premium valuations with similar dynamics. In this context, CenturyPly looks fairly valued, not expensive.

The Investment Decision

The investment case ultimately depends on three beliefs: First, that India's housing market has multi-decade growth ahead. Second, that the organized shift in plywood is structural, not cyclical. Third, that CenturyPly's execution capabilities allow them to capture disproportionate value from these trends.

For long-term investors, CenturyPly offers exposure to India's consumption story through a differentiated angle. It's not FMCG, but has FMCG-like brand power. It's not real estate, but benefits from real estate growth. It's not technology, but uses technology for competitive advantage.

The risks are real—commodity exposure, cycle dependence, competition—but manageable through position sizing. For a diversified portfolio seeking structural growth stories in India, CenturyPly deserves consideration. Not as a core holding perhaps, but as a strategic allocation to a unique business model in a transforming market.

X. Future Outlook & Strategic Options

The strategy offsite at a resort in Uttarakhand, late 2024. CenturyPly's leadership team is debating the next decade. On one wall, photos from 1982—the first factory, the founding team, the original products. On another, mood boards of future homes—sustainable, modular, smart. Keshav Bhajanka poses the question: "We've won in plywood. We're winning in laminates and MDF. What's our third act? How does a 40-year-old company stay relevant for the next 40?"

Sustainability Challenges and Opportunities

The elephant in the room—or rather, the forest—is sustainability. A company built on cutting trees faces existential questions in a climate-conscious world. But CenturyPly's response reveals strategic sophistication: don't deny the challenge, embrace and transform it.

The agro-forestry initiatives, where farmers grow timber as a crop, create renewable supply while providing rural income. It's not CSR; it's creating a sustainable supply chain. The plantation programs in partnership with state governments ensure future raw material while earning carbon credits. The sawdust-to-energy plants turn waste into power. Sustainability becomes competitive advantage, not compliance burden.

The next frontier is circular economy integration. Plywood recycling, take-back programs, modular designs enabling reuse—all technically feasible, awaiting business model innovation. The company that figures out how to make circular plywood profitable doesn't just capture value; they create a new market.

International Expansion Possibilities

The international opportunity extends beyond timber sourcing. India's cost structure, combined with CenturyPly's quality standards, could compete globally. But smart expansion means choosing battles carefully.

Middle East markets, with their large Indian diaspora and similar climate conditions, offer natural entry points. African markets, where CenturyPly already has presence through Gabon operations, could be served with locally manufactured products. Southeast Asian markets present opportunities for premium products that local manufacturers don't address.

But the real opportunity might be in design and technology export rather than physical products. Licensing CenturyPly's designs, quality systems, and brand for local manufacturing could generate asset-light returns. The Manish Malhotra collaboration created IP that transcends geography.

Adjacent Categories

The recent incorporation of "Centuryply Furniture Fittings Limited" signals strategic intent. Furniture hardware—hinges, channels, handles—is a ₹15,000 crore market, 90% unorganized, with dynamics similar to plywood two decades ago. CenturyPly's playbook could replicate here.

Complete interior solutions represent the logical evolution. Instead of selling components, sell outcomes. The B2C furniture market, despite multiple attempts by various players, remains unconquered. But CenturyPly has unique advantages—material expertise, designer relationships, dealer networks. A curated furniture line using CenturyPly materials, sold through existing channels, could work where others failed.

The modular construction opportunity deserves attention. As construction industrializes, prefabricated components gain share. CenturyPly could move from supplying materials to supplying pre-fabricated wall panels, modular kitchens, bathroom pods. It's moving up the value chain while leveraging core competencies.

Technology Integration

AI in design isn't futuristic; it's present. Generative AI creating laminate patterns, machine learning optimizing cutting patterns, computer vision ensuring quality—all immediately applicable. CenturyPly's scale justifies investment; their margins support it.

The metaverse showroom sounds gimmicky but addresses real pain points. Customers could visualize products in their spaces, experiment with combinations, share designs with family—all before purchase. In a category where visualization drives decisions, virtual reality could become a powerful sales tool.

Blockchain for supply chain transparency addresses growing ESG concerns. Customers could trace their plywood from tree to installation, verifying sustainability claims. In premium segments where provenance matters, this transparency commands premiums.

But the most impactful technology might be mundane: advanced analytics for demand prediction, IoT for factory optimization, automation for cost reduction. These unsexy improvements compound over time, creating structural advantages that flashy innovations can't match.

The Next Decade Scenarios

Scenario 1: The Premium Play—CenturyPly continues moving upmarket, ceding volume segments to competition while dominating premium. Margins expand, capital efficiency improves, but growth moderates. The company becomes the "Asian Paints of plywood"—steady, profitable, predictable.

Scenario 2: The Platform Transformation—CenturyPly evolves from manufacturer to interior solutions platform, orchestrating ecosystem players. Manufacturing becomes one capability among many. Think Amazon for interiors, powered by CenturyPly's trust and distribution.

Scenario 3: The Consolidation Leader—As unorganized players struggle and subscale organized players lack resources, CenturyPly leads industry consolidation. Through acquisitions and partnerships, market share doubles. The company becomes to Indian plywood what Reliance is to telecom.

Scenario 4: The Sustainability Pioneer—Climate concerns accelerate, regulations tighten, consumer consciousness peaks. CenturyPly's early sustainability investments pay off massively. The company doesn't just survive the green transition; they lead it.

Strategic Imperatives

Regardless of scenario, certain imperatives emerge. First, maintain the core while exploring edges. Plywood cash flows fund experiments; experiments don't jeopardize plywood.

Second, build capabilities before they're needed. The digital investments, sustainability initiatives, design collaborations—all seemed premature when started. That's precisely why they created advantage.

Third, respect the distribution network while modernizing it. Dealers built CenturyPly; CenturyPly can't abandon them for e-commerce. But dealers must evolve too—becoming experience centers, not just warehouses.

Fourth, manage succession thoughtfully. The transition from founders to next generation is delicate. Preserving culture while enabling change, respecting history while embracing future—this balance determines whether CenturyPly remains relevant.

Can CenturyPly Maintain Leadership?

The question isn't whether CenturyPly can maintain leadership—they've proven that capability. The question is what leadership means in a transforming market. Leading in market share? Margins? Innovation? Sustainability? Stock performance?

The company's track record suggests they'll redefine leadership rather than just maintain it. Just as they transformed from traders to manufacturers, from regional to national, from commodity to brand—the next transformation is probably already underway, visible only in hindsight.

The biggest risk isn't competition or regulation or technology. It's success-induced complacency. When you've won in plywood, won in laminates, won against the unorganized sector—the hunger that drove those victories can diminish. Maintaining insurgent mindset with incumbent resources is the ultimate challenge.

As we look toward 2035, CenturyPly faces choices that will define its next chapter. The foundations are strong—brand, distribution, manufacturing excellence. The opportunities are clear—sustainability, technology, internationalization. The capabilities exist—capital, talent, relationships.

What remains to be seen is ambition. Will CenturyPly be satisfied being India's plywood leader, or will they reimagine what building materials mean in a digital, sustainable, experience-driven economy? The answer will determine whether CenturyPly's next 40 years are as transformative as its first 40.

The smart money bets on transformation. Companies that survive four decades in India don't do so by standing still. They evolve, adapt, reinvent. CenturyPly has proven this capability repeatedly. As India enters its infrastructure supercycle, as sustainability becomes imperative, as technology reshapes everything—CenturyPly is positioned not just to participate but to lead.

The future of CenturyPly isn't about plywood. It's about trust, solutions, experiences. The company that started by pressing wood sheets together might end up orchestrating India's interior transformation. That's not just growth; that's market creation at its finest. And if history is any guide, CenturyPly has both the vision and execution capability to pull it off.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube