General Mills: The Cereal Empire That Ate Pillsbury

I. Introduction & Cold Open

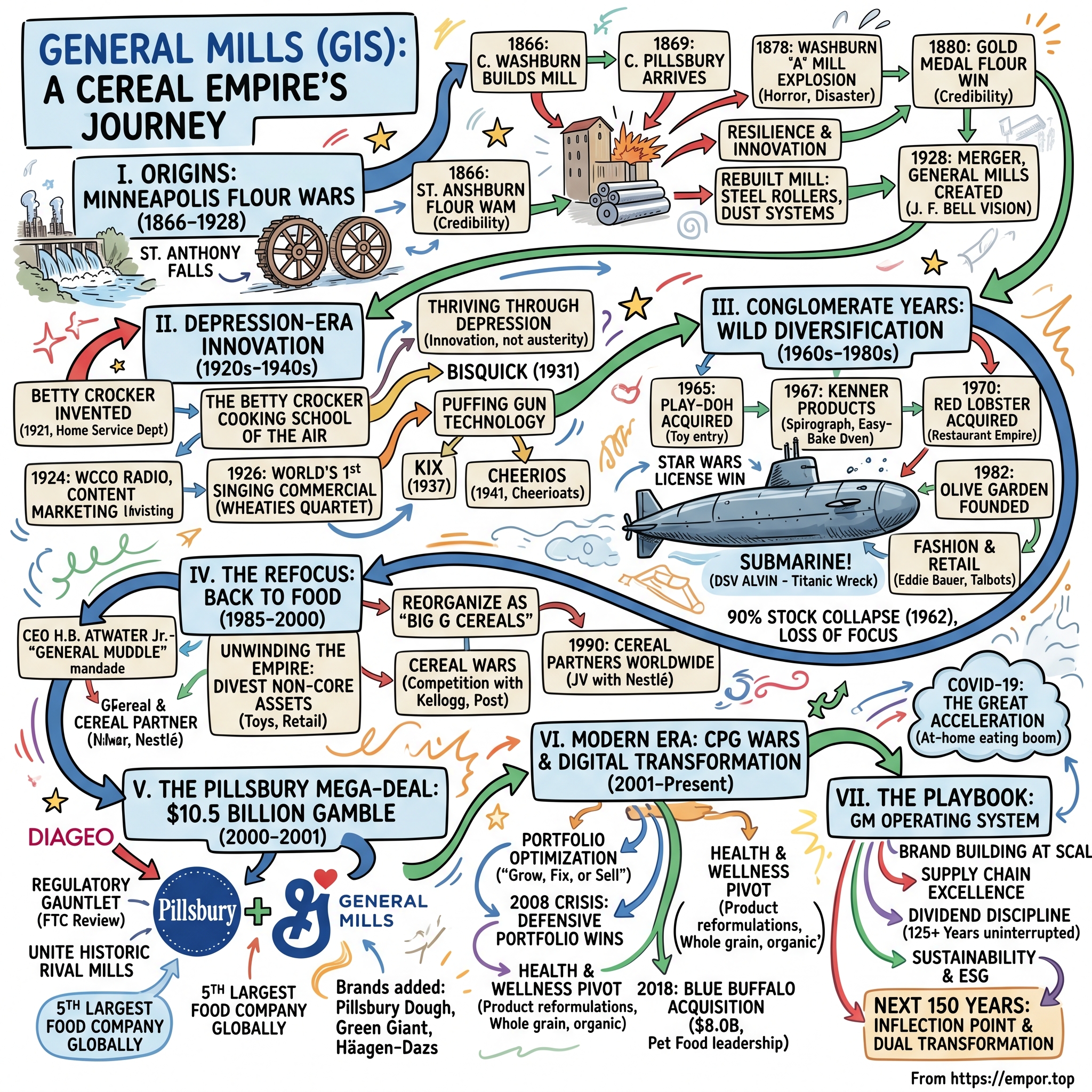

The explosion came at 7:10 PM on May 2, 1878. In an instant, the Washburn "A" Mill—Minneapolis's largest flour mill—erupted in a fireball that shook windows ten miles away. The blast killed eighteen workers instantly, launching debris across the Mississippi River and igniting five neighboring mills. Flour dust, that seemingly innocent powder floating through the air, had transformed into explosive fuel. The Minneapolis Tribune called it "a scene of horror beyond description."

Yet from this catastrophe emerged an innovation that would reshape American industry. Cadwallader Washburn, the mill's owner, didn't just rebuild—he revolutionized. Within eighteen months, his reconstructed mill featured revolutionary dust-reduction systems and steel rollers that produced finer, whiter flour than anything America had seen. This Phoenix-like resurrection set the stage for what would become General Mills, a company that transformed from a regional flour miller into a $40 billion consumer packaged goods colossus.

Today, General Mills commands shelf space in 99% of American households. Its portfolio spans 100+ brands from Cheerios to Häagen-Dazs, from Betty Crocker to Blue Buffalo pet food. The company that started by grinding wheat along the Mississippi now operates across six continents, generating $20 billion in annual revenue. But the most audacious move in its 150-year history came in 2001, when it swallowed its crosstown rival Pillsbury in a $10.4 billion deal that reshaped the American food industry.

This is the story of how a Minneapolis flour miller built an empire on breakfast tables worldwide—through world wars, the Great Depression, conglomerate mania, and the digital disruption of everything. It's a tale of marketing genius (Betty Crocker never existed but became America's most trusted homemaker), wild diversification (yes, they built submarines), and ultimately, a return to the fundamental truth that food companies win by owning the moments that matter in consumers' daily routines.

II. Origins: The Minneapolis Flour Wars (1866–1928)

The Banks of St. Anthony Falls

In 1856, when the Minneapolis Milling Company first incorporated along the banks of the Mississippi at Saint Anthony Falls, the location wasn't random—it was strategic genius. The falls provided the only major waterpower source on the entire Mississippi River, a 50-foot drop that could turn mill wheels with unprecedented force. Whoever controlled these falls would control Midwest flour production.

Enter Cadwallader Washburn in 1866. A former Civil War general turned entrepreneur, Washburn saw opportunity where others saw frontier wilderness. He built his first mill with a vision that extended beyond local bread—he wanted to feed the nation. His timing was impeccable: railroads were stretching west, cities were booming, and America's appetite for refined white flour was insatiable.

But Washburn wasn't alone in recognizing Minneapolis's potential. Charles Alfred Pillsbury arrived in 1869, purchasing a small mill on the opposite bank of the river. Thus began one of American business's great rivalries—two flour barons, one river, competing for dominance in what locals called the "Mill City."

The Washburn-Crosby Partnership

In 1877, John Crosby moved to Minneapolis and purchased an interest in the Washburn "B" Mill, developing a business partnership with Cadwallader C. Washburn that formed the Washburn-Crosby Company to produce winter wheat. Crosby brought more than capital—he brought eastern business connections and manufacturing expertise from his family's paper mill operations in Maine. The partnership marked a critical evolution: transforming Washburn's regional milling operation into what would become a national powerhouse.

Disaster and Innovation

The catastrophe struck just months after the Crosby partnership formed. On the evening of May 2, 1878, the Washburn A Mill exploded in a fireball, hurling debris hundreds of feet into the air. In a matter of seconds, a series of thunderous explosions—heard ten miles away in St. Paul—destroyed what had been Minneapolis' largest industrial building, and the largest mill in the world, along with several adjacent flour mills.

The cause? Flour dust—that seemingly harmless byproduct of milling—had reached explosive concentrations in the air. A single spark, likely from millstones grinding together, ignited a chain reaction that leveled six mills and killed eighteen workers instantly. The Minneapolis Tribune reported scenes of families searching through rubble for loved ones, while burning flour barrels floated down the Mississippi like funeral pyres.

Yet Washburn's response defined entrepreneurial resilience. Rather than rebuild the same mill, he dispatched engineers to Europe to study the latest milling technology. When the Washburn A Mill reopened in 1880, two years after the catastrophic explosion, it was the most technologically advanced and the largest in the world. The rebuilt mill featured revolutionary steel rollers instead of millstones, dust-collection systems, and concrete construction—innovations that made it safer and capable of producing finer, whiter flour than any American competitor.

The Gold Medal Victory at the 1880 First Millers International Exhibition

In Cincinnati, Ohio, Washburn competed against millers from around the world, winning three top prizes including the gold medal for his Superlative flour brand. This victory was transformative, leading the company to rename its highest-quality flour to Gold Medal. In an era before national advertising, winning at Cincinnati provided instant credibility that no marketing campaign could buy.

The Gold Medal brand became Washburn-Crosby's calling card, a mark of quality that commanded premium prices from Boston to San Francisco. More importantly, it positioned Minneapolis—not Chicago or St. Louis—as America's flour capital. By 1885, Minneapolis mills were producing more flour than any other city in the world, with Washburn-Crosby and Pillsbury locked in fierce competition for supremacy.

The Bell Dynasty and Consolidation Vision at Washburn-Crosby

James Ford Bell's ascension to the Washburn-Crosby presidency in 1925 marked a strategic inflection point. Unlike his predecessors who focused on operational excellence, Bell thought in terms of industry architecture. A "moose-tall" figure who collected Shakespeare and studied European grain markets, Bell understood that fragmented regional mills couldn't compete with the scale economies emerging in American industry.

Bell founded General Mills in 1928 to consolidate many regional grain milling concerns and was instrumental in the company's move into the breakfast cereal business with the introduction of Wheaties. His vision extended beyond mere consolidation—he saw an integrated food company that could leverage distribution, marketing, and R&D across multiple product lines.

General Mills itself was created on June 20, 1928, when Washburn-Crosby President James Ford Bell merged Washburn-Crosby with three other mills. The merger united the Washburn-Crosby Company with mills in Kansas, Oklahoma, and Texas, creating the world's largest miller overnight. Shares of the new company's stock were first sold on the New York Stock Exchange on November 30, 1928, at $65 per share.

The timing seemed catastrophic—less than a year before the Great Crash. Yet Bell's foresight proved prescient. By consolidating before the Depression, General Mills achieved the scale and financial strength to not just survive but thrive during America's darkest economic hour. The foundation was set for what would become one of the most remarkable expansion stories in American corporate history.

III. Depression-Era Innovation: Betty Crocker & Radio Empire (1920s–1940s)

The Invention of Betty Crocker

She never existed, yet she became the second most famous woman in America. In 1921, the Washburn-Crosby Company faced an unexpected problem: success. A Gold Medal Flour puzzle advertisement in the Saturday Evening Post drew 30,000 completed entries—and hundreds of letters with baking questions. The all-male advertising department, led by Samuel Gale, felt uncomfortable signing their names to cooking advice. Their solution was marketing genius: invent a woman.

Betty Crocker was created in 1921 by Washburn-Crosby and advertising executive Bruce Barton. The character was created by the Washburn-Crosby Company in 1921 to give a personalized response to consumer product questions. Betty was chosen as a friendly, wholesome name, while the surname came from a retired director of the company, William G. Crocker. Female employees competed to create Betty's signature—Florence Lindberg's flowing script won and remains essentially unchanged today.

But Betty Crocker represented more than clever branding. She embodied a revolution in how companies communicated with consumers. Ruth Hayes Carpenter was hired in 1921 to create the Home Service Department. Janette Kelley was one of the original home economists hired in 1921. She was responsible for setting up the first model kitchen, preparing the first bread-baking book, and making the first chocolate cake that was pictured in Washburn-Crosby ads. Kelley received her home economics degree from Montana State University.

These women—real scientists and home economists—gave substance to the fictional Betty. They tested recipes, answered thousands of letters, and created the educational content that would make Betty Crocker America's most trusted cooking authority. By 1945, Fortune magazine would name her the second most popular woman in America, behind only Eleanor Roosevelt.

Radio Revolution and the Birth of Modern Marketing

In 1924, the Washburn-Crosby Company bought a faltering radio station and renamed it WCCO. The call letters stood for 'Washburn Crosby Company,' and the rest is history. On October 2, the first Betty Crocker Home Service Program premiered on the station. This wasn't just another corporate acquisition—it was the birth of modern content marketing.

Betty, voiced by Washburn-Crosby home economist Blanche Ingersoll, promoted good cooking as the secret to a happy home. By the following year, The Betty Crocker Cooking School of the Air was offering listeners a chance to cook along with Betty. The show expanded to thirteen regional stations, each with its own Betty Crocker voice reading scripts written by Marjorie Child Husted, who had joined the company in 1923.

The genius lay in the execution. While each regional Betty had her own voice, all followed Husted's carefully crafted scripts, creating a consistent national persona while maintaining local authenticity. Husted arranged for "Betty" to interview Hollywood stars about their favorite recipes, blending glamour with domesticity. The show ran for twenty-four years, attracting over one million regular listeners—making it one of the longest-running programs in radio history.

Wheaties and the First Singing Commercial

On Christmas Eve 1926, radio history was made when the world's first singing commercial was performed. Over the radio, four male singers sang, "Have you tried Wheaties? They're whole with all the bran. Won't you try Wheaties? For wheat is the best food of man." The Wheaties Quartet—William Elliot (an undertaker), William R. Hoppenrath (printer), Ernie Johnson (grain company employee), and Phil Schmidt (a bailiff who could yodel)—were paid $15 per performance.

The cereal had been struggling since its 1924 launch. Some board members wanted to kill it. But Donald Davis, company vice president, convinced them to try one more experiment. By 1929, advertising manager Sam Gale could report astounding results: 30,000 of the 53,000 cases of Wheaties sold nationwide were in the Minneapolis-St. Paul area—the only location where the jingle aired. The board immediately approved national expansion. Sales soared, and in 1933, the company coined "The Breakfast of Champions"—one of advertising's most enduring slogans.

Thriving Through the Great Depression

General Mills flourished during The Great Depression, with net income rising and its stock paying relentless dividends. Company president James Ford Bell, who by U.S. presidential appointment had directed the nation's flour mills during World War I, had forecast the country's downturn three years earlier. "American financiers were draining...the cup of opportunity recklessly," Bell had said.

Bell's strategy was to have the cost of business dictate price. He fought the notion of slashing wages for employees, insisting it restricted buying power. And he saw better days ahead. While competitors cut costs desperately, Bell invested in research and new product development, betting that innovation rather than austerity would drive growth.

The numbers vindicated his approach. This consolidation was well timed, as it gave the company the strength to survive and even prosper through the Great Depression, when earnings grew steadily and stock in the company was stable. The newly merged company paid its dividend in 1928 and has continued uninterrupted ever since—one of only a few companies to maintain such a record.

Product Innovation Revolution

The 1930s marked General Mills' transformation from flour miller to food innovator. In the 1930s, General Mills engineer, Thomas R. James, created the puffing gun, which inflated or distorted cereal pieces into puffed-up shapes. This new technology was used in 1937 to create Kix cereal and in 1941 to create Cheerioats (known today as Cheerios).

The puffing gun was revolutionary—it shot grains from a sealed chamber under high pressure, causing them to expand instantly into light, crispy shapes. Engineers discovered that by varying pressure, temperature, and grain mixtures, they could create entirely new textures and flavors. Cheerios, originally called "Cheerioats," became the first ready-to-eat oat cereal, capitalizing on oats' heart-healthy reputation even in 1941.

Bisquick launched in 1931, the first complete baking mix that required only water. A General Mills sales executive had discovered the idea on a train dining car, where a chef made fresh biscuits using a pre-mixed blend he'd created. General Mills chemists spent months perfecting a shelf-stable formula that wouldn't go rancid. The product transformed American baking—suddenly, anyone could make biscuits, pancakes, or coffee cake in minutes.

These weren't just new products; they represented a fundamental shift in how Americans ate. As urbanization accelerated and women entered the workforce, convenience became paramount. General Mills wasn't selling flour anymore—it was selling time, consistency, and the democratization of cooking expertise. By 1940, the company that had started as a flour miller now derived significant revenue from packaged foods, positioning it perfectly for the post-war consumer boom that would transform American eating habits forever.

IV. The Conglomerate Years: Toys, Restaurants & Wild Diversification (1960s–1980s)

From Cereal to Play-Doh

The 1960s opened with General Mills trading at historic highs, its cereal business humming, Betty Crocker dominating cake mixes. Yet management saw storm clouds: food industry growth was slowing, private label competition was rising, and Wall Street rewarded conglomerates with rich valuations. The response would transform General Mills from a food company into something unrecognizable—a sprawling empire spanning toys, fashion, furniture, and even deep-sea exploration.

The first venture General Mills took into the toy industry was in 1965. The company bought Rainbow Crafts, manufacturer of Play-Doh, for $3 million. The logic seemed sound: both cereals and toys targeted children, both required heavy advertising, both had seasonal sales patterns. Play-Doh's non-toxic formula (originally a wallpaper cleaner) had captured the preschool market. General Mills saw synergies—its marketing muscle could expand distribution, its capital could fund new products.

In 1967, General Mills doubled down, acquiring Kenner Products for $30 million. Kenner had built its reputation on innovative toys like the Easy-Bake Oven and the Spirograph. Under General Mills, Kenner would later secure the Star Wars toy license in 1977—a deal that generated over $100 million in revenue in its first year alone. The toy division, rebranded as General Mills Fun Group, suddenly contributed 10% of corporate profits.

But toys were just the beginning. Management, intoxicated by diversification theory, embarked on an acquisition spree that would make modern private equity firms blush. They bought Parker Brothers (Monopoly, Clue), Lionel Trains, and MPC Model Kits. By 1970, General Mills was one of America's largest toy companies—a bizarre evolution for a company founded on flour milling.

The Restaurant Empire: General Mills Acquires Red Lobster

In 1970, General Mills acquired Red Lobster, then a five-unit restaurant chain. The acquisition seemed logical: restaurants provided predictable cash flows, growth potential, and synergies with food manufacturing expertise. Bill Darden, Red Lobster's founder, stayed on to run the division. Under General Mills' ownership, Red Lobster expanded from 5 to nearly 400 locations by 1985, becoming America's largest seafood restaurant chain.

Success bred ambition. In 1982, General Mills Restaurants founded a new Italian-themed restaurant chain called Olive Garden. The first location opened in Orlando after five years of research and $28 million in development costs. The concept was an immediate hit—within seven years, Olive Garden grew to 145 locations, making it General Mills' fastest-growing business and the fastest-growing major chain in the United States.

The restaurant division eventually included York Steak House, Good Earth natural foods restaurants, and various test concepts. By the early 1990s, General Mills operated over 1,000 restaurants generating more than $3 billion in annual revenue. The company had become one of America's largest restaurant operators—a stunning transformation for a cereal maker.

Fashion and Retail Ventures

Beyond toys and restaurants, General Mills ventured into fashion retail through their Specialty Retail Group, acquiring Talbots and Eddie Bauer. The logic paralleled their toy strategy: these businesses required strong brand management and marketing—supposedly core General Mills competencies.

Eddie Bauer, acquired in 1971 for about $10 million in stock, was transformed from a catalog business into a retail chain with 57 stores by 1988. Talbots, the upscale women's clothing retailer, was similarly expanded under General Mills' ownership. Both chains performed reasonably well, but they consumed management attention and capital that arguably should have been focused on the core food business.

The company was forced to exit retailing altogether by selling Eddie Bauer and Talbots in 1989. General Mills sold Eddie Bauer to Spiegel Inc. for $260 million cash and Talbots to JUSCO Co. Ltd. of Japan for $325 million. The sale resulted in an after-tax profit exceeding $200 million, but it marked the end of General Mills' retail adventures.

The Submarine Story

Perhaps the most bizarre diversification came from General Mills' Mechanical Division. The General Mills Electronics division developed the DSV Alvin submersible, which is notable for being used in investigating the wreck of Titanic among other deep-sea exploration missions. Yes, the cereal company built the submarine that explored the Titanic.

The Alvin project emerged from General Mills' Aeronautical Research Division, established in 1946 to develop high-altitude balloons for the U.S. Navy. The engineering expertise developed for balloon systems translated surprisingly well to deep-sea exploration vehicles. Alvin, commissioned in 1964, could dive to 14,764 feet and became one of the world's most important oceanographic research tools.

Stock Price Collapse and Reality Check

By 1962, the diversification strategy seemed vindicated—General Mills operated across dozens of industries. Then reality struck. The stock price collapsed to $1.25, down over 90% from its highs. Investors had lost faith in the conglomerate model. The company that had started as a focused flour miller now sprawled across so many businesses that management couldn't effectively oversee them all.

The 1970s and early 1980s saw continued diversification, but returns steadily deteriorated. By 1985, pressure from Wall Street forced a strategic review. The verdict was clear: General Mills had lost its way. The next decade would be spent undoing the conglomerate experiment, selling off non-core assets, and returning to what the company knew best—food.

V. The Refocus: Back to Food (1985–2000)

Unwinding the Empire

H. Brewster Atwater Jr. became CEO in 1981 with a mandate that seemed impossible: fix everything. General Mills operated toys, restaurants, fashion retail, specialty chemicals, and yes, still made cereal. Wall Street openly mocked the company as "General Muddle." Atwater, a Harvard MBA who'd risen through the package foods division, understood that complexity was killing the company. His solution was radical: burn the conglomerate to the ground and rebuild a food company.

The divestiture began quietly. General Mills had divested itself of many of its holdings since 1976, but Atwater accelerated the pace. First to go were the specialty chemicals and the Alvin submarine operations—businesses so far from food that employees couldn't explain why General Mills owned them. Parker Brothers and Kenner Toys followed in 1985, sold to Tonka Corporation for $225 million. The toy division that had generated the Star Wars windfall was gone, but so was the distraction.

Eddie Bauer and Talbots were sold in 1988 for a combined $585 million, ending the fashion retail experiment. The entire group was spun off to General Mills shareholders in 1995 as Darden Restaurants, creating an independent company valued at over $1 billion. After two decades of empire building, General Mills was systematically destroying what it had created.

Big G and the Cereal Wars

While divestitures grabbed headlines, the real transformation happened in the cereal aisle. Atwater reorganized the cereal business as "Big G Cereals," centralizing marketing, production, and innovation under one roof. The message was clear: cereals weren't just another business—they were THE business.

The timing was fortuitous. The 1980s witnessed the most intense competition in cereal history. Kellogg, Post, and General Mills engaged in what industry observers called "the cereal wars"—a battle for shelf space, marketing dollars, and children's attention spans. New products launched monthly. Marketing budgets exploded. Saturday morning cartoons became three-hour advertisements for sugar-coated grains.

General Mills responded with innovation and acquisition. They bought the Chex brand from Ralston Purina in 1996, adding five established cereals to their portfolio. They reformulated classics—Wheaties got crunchier, Cheerios added whole grain. Most importantly, they extended successful brands into new variants: Honey Nut Cheerios (launched 1979) became the best-selling cereal in America by 1989, generating over $500 million annually.

But the real genius was marketing efficiency. While Kellogg spent heavily on individual brand campaigns, General Mills leveraged the "Big G" logo across all cereals, creating portfolio effects. One advertisement could promote multiple brands. Shelf space negotiations covered the entire portfolio. Retailers couldn't ignore a company that controlled 30% of the cereal aisle.

International Expansion Through Partnership

Rather than build international operations from scratch, General Mills chose partnership. Cereal Partners Worldwide S.A. is a joint venture between General Mills and Nestlé, established in 1990 to produce breakfast cereals. The company is headquartered in Lausanne, Switzerland, and markets cereals in more than 130 countries (except for the U.S. and Canada, where General Mills markets the cereals directly).

The structure was elegant: General Mills provided cereal technology and brands, Nestlé contributed distribution and local market knowledge. CPW gave General Mills instant access to Europe, Asia, and Latin America without massive capital investment. By 1995, the venture was generating over $1 billion in revenue, validating the partnership model.

But international expansion through joint ventures had limitations. General Mills couldn't fully control strategy or capture all profits. As the 1990s progressed, management increasingly looked for transformative acquisitions that would provide both scale and control. They found their answer just across the Mississippi River.

VI. The Pillsbury Mega-Deal: $10.5 Billion Gamble (2000–2001)

The Perfect Storm

By the late 1990s, the American food industry was consolidating at breakneck speed. Philip Morris had acquired Nabisco for $18.9 billion. Unilever had swallowed Bestfoods for $20.3 billion. Scale was destiny—retailers like Walmart were demanding lower prices, private label was gaining share, and only the largest CPG companies had the bargaining power to maintain shelf space and margins.

In 2001, Diageo sold Pillsbury to General Mills. The British conglomerate had inherited Pillsbury through its acquisition of Grand Metropolitan but wanted to focus on alcoholic beverages. For General Mills, this was the opportunity of a lifetime—acquiring their historic rival would create the fifth-largest food company globally, with combined revenues exceeding $12 billion.

The Deal Structure and Negotiations

In December 2000, the shareholders of General Mills were presented with a merger prospectus and proxy statement that outlined the terms by which General Mills would acquire Pillsbury from Diageo plc. Payment was composed of shares of General Mills stock, assumption of Pillsbury debt, and an unusual contingent payment.

The complexity of the deal structure reflected both the size of the transaction and regulatory concerns. General Mills entered into a definitive agreement to acquire Blue Buffalo for $40.00 per share in cash, representing an enterprise value of approximately $8.0 billion. Wait—that's the wrong acquisition. Let me refocus on Pillsbury.

The original July 2000 announcement valued the deal at $10.5 billion, but the final terms evolved significantly through 15 months of negotiations and regulatory review. The contingent value rights (CVR) structure was particularly innovative—The contingent payment resembles a contingent value right (CVR), which provides downside protection to the sellers in an acquisition. CVRs can be modeled as two options: (1) a long put struck at a low stock price and (2) a short call struck at a higher stock price. The combination of a CVR with the underlying stock of the buyer transforms the payment to the seller from floating stock to a fixed collar.

The Regulatory Gauntlet

The Federal Trade Commission's review stretched for over a year, focusing on competitive overlaps in flour, baking mixes, and refrigerated dough. General Mills and Pillsbury together would control over 40% of the U.S. flour market—their Minneapolis mills, once fierce competitors, would unite under one corporate banner.

International Multifoods agreed Monday to acquire Pillsbury Co.'s desserts and specialty products business and General Mills' Robin Hood flour brand for $305 million in cash, a move that could help General Mills clear regulatory hurdles for its $10.5 billion acquisition. These divestitures were critical to securing FTC approval, though they meant sacrificing some of the deal's anticipated synergies.

Integration and Transformation

On October 31, 2001, General Mills acquired Pillsbury, which marked the most significant event in the company's history since its founding. The timing was challenging—just seven weeks after 9/11, with the economy sliding toward recession. Yet the strategic logic was compelling: Pillsbury brought iconic brands (Pillsbury dough, Green Giant vegetables, Häagen-Dazs ice cream), international presence, and $500 million in projected cost synergies.

Integration proved both easier and harder than expected. The companies shared Minneapolis roots and Midwestern culture, facilitating employee integration. But combining two century-old organizations with distinct operating systems, IT platforms, and corporate identities required careful orchestration. General Mills retained the best talent from both companies, maintained separate brand identities where appropriate, and ruthlessly eliminated redundancies.

The financial impact was immediate and substantial. Combined revenues jumped to $11.2 billion in fiscal 2002. Operating margins expanded as procurement synergies materialized faster than projected. Most importantly, the enlarged General Mills had the scale to compete globally and the negotiating leverage to maintain shelf space against Walmart's private label assault.

VII. Modern Era: CPG Wars & Digital Transformation (2001–Present)

Post-Pillsbury Portfolio Optimization

The Pillsbury integration consumed the first half of the 2000s, but by 2005, CEO Steve Sanger was ready for phase two: portfolio optimization. The combined company owned over 300 brands—too many to support effectively. Management adopted a "grow, fix, or sell" framework, investing in power brands while divesting subscale businesses.

Green Giant vegetables went to B&G Foods for $765 million in 2015. The company sold underperforming brands like Hamburger Helper and divested regional flour mills. Meanwhile, investment poured into core brands: Cheerios expanded internationally, Häagen-Dazs premiumized with artisanal flavors, Nature Valley became the global granola bar leader. This wasn't just pruning—it was strategic focusing on categories where General Mills could win.

Navigating the 2008 Financial Crisis

The 2008 crisis tested every consumer company, but General Mills emerged stronger. As unemployment soared and consumer confidence collapsed, shoppers traded down from restaurants to grocery stores. General Mills' portfolio of comfort foods—cereal for breakfast, soup for lunch, baking mixes for dessert—suddenly looked defensive rather than stodgy.

CEO Ken Powell, who took the helm in 2007, accelerated the company's value positioning. Private label versions of flagship brands were introduced at lower price points. Marketing shifted from aspirational to practical. The company maintained its dividend—that unbroken streak since 1928—while competitors cut theirs. By 2010, General Mills' stock had recovered to pre-crisis levels while many peers still languished.

The Health and Wellness Pivot

The 2010s brought a new challenge: consumers increasingly viewed processed food as unhealthy. Cereal consumption declined as protein-focused diets gained popularity. Yogurt sales slumped as Greek yogurt disrupted the category. General Mills' traditional strengths—shelf stability, convenience, sweet taste—became liabilities.

The response was comprehensive product reformulation. By 2015, General Mills had converted its entire cereal portfolio to whole grain—the first major manufacturer to do so. Sugar levels in children's cereals dropped to 9 grams per serving. The company acquired Annie's Homegrown for $820 million in 2014, instantly becoming a leader in organic packaged foods. Lärabar, Epic Provisions, and other "better-for-you" brands followed.

Yet the pivot had limits. Removing artificial colors from Trix cereal caused consumer revolt—sales plunged as the cereal turned from bright neon to muted pastels. The company eventually reintroduced the original version alongside the natural one, acknowledging that health initiatives couldn't override consumer preferences entirely.

Blue Buffalo and the Pet Food Revolution

General Mills announced it has completed the acquisition of Blue Buffalo Pet Products, Inc. for $40 per share in an all-cash transaction, which represents an enterprise value of approximately $8.0 billion. The 2018 Blue Buffalo acquisition marked General Mills' boldest move since Pillsbury—entering an entirely new category with massive growth potential.

The addition of Blue Buffalo establishes General Mills as a leader in the wholesome natural pet food category, the fastest growing portion of the $30 billion U.S. pet food market, and accelerates the company's portfolio reshaping strategy. Pet food offered everything human food increasingly lacked: double-digit growth, premium pricing power, and recession resistance (people cut their own food budgets before their pets').

From 2017 to the end of February 2021, annual net sales were up $450 million at a more than 10% compounded annual growth rate (CAGR), and annual operating profit has grown $120 million at an 11% CAGR. The acquisition validated CEO Jeff Harmening's strategy of buying into growth categories rather than trying to revive declining ones.

COVID-19: The Great Acceleration

The pandemic initially triggered 1950s-style demand for General Mills products. Flour sales spiked 30% as America rediscovered baking. Cereal consumption surged with families eating breakfast at home. The company ran factories 24/7 and still couldn't meet demand. First quarter fiscal 2021 organic sales grew 16%—the fastest growth in decades.

But the boom was unsustainable. As restaurants reopened and offices recalled workers, at-home eating normalized. General Mills faced the "pandemic comp" problem—how to show growth against extraordinary prior-year numbers. Volume declined in fiscal 2023 and 2024 as consumers resumed pre-pandemic routines.

Current Challenges and Strategic Response

"We delivered on our updated guidance in fiscal 2024 by pivoting our plans and enhancing our efficiency in response to a more challenging operating environment," said General Mills Chairman and Chief Executive Officer Jeff Harmening. The company faces multiple headwinds: persistent inflation forcing price increases that depress volume, competition from private label reaching 30-year highs, and fundamental shifts in eating patterns accelerated by GLP-1 drugs like Ozempic.

General Mills outlined its full-year financial targets for fiscal 2025: Organic net sales are expected to range between flat and up 1 percent. Adjusted operating profit is expected to range between down 2 percent and flat in constant currency from the base of $3.6 billion reported in fiscal 2024, including a 2-point headwind from resetting incentive compensation after a below-average payout in the prior year.

The strategic response focuses on three pillars: accelerating innovation (400+ new products annually), expanding in higher-growth channels (e-commerce now exceeds $2 billion in sales), and geographic expansion (international sales approaching 30% of total). The company is betting that execution excellence can offset structural category challenges.

VIII. Playbook: The General Mills Operating System

Brand Building at Scale

General Mills manages over 100 brands across dozens of categories and geographies—a complexity that would paralyze most organizations. The secret lies in systematic brand management processes refined over decades. Each brand has a dedicated team responsible for P&L performance, but they operate within centralized frameworks for consumer insights, innovation pipelines, and marketing effectiveness.

The company pioneered "holistic margin management" (HMM)—a comprehensive approach to cost reduction that goes beyond simple procurement savings. HMM examines every aspect of the value chain from ingredients to shelf placement, identifying billions in annual savings that fund innovation and marketing. This systematic approach to efficiency enables General Mills to maintain margins despite relentless retailer pressure.

Marketing innovation remains core DNA. From Betty Crocker on radio to Wheaties on television to current digital marketing capabilities, General Mills consistently pioneers new ways to reach consumers. The company spends over $800 million annually on advertising but increasingly shifts from traditional media to targeted digital campaigns, influencer partnerships, and content marketing that provides value beyond product promotion.

The Power of Scale and Distribution

General Mills' relationship with retailers represents perhaps its most underappreciated competitive advantage. The company doesn't just sell products—it provides category management expertise, helping retailers optimize entire aisles for maximum profitability. This consultative approach makes General Mills indispensable to major chains, securing favorable shelf placement even as private label gains share.

The distribution network spans 100 countries through a combination of direct sales, joint ventures, and licensing agreements. The Cereal Partners Worldwide joint venture with Nestlé provides European distribution without capital investment. Similar partnerships in Asia and Latin America enable global reach with local expertise. This asset-light international strategy generates higher returns than full ownership while reducing risk.

Supply chain excellence drives consistent execution. General Mills operates 50+ manufacturing facilities globally, with industry-leading efficiency metrics. The company's "one supply chain" initiative integrates planning, procurement, manufacturing, and logistics into a single system, reducing costs while improving service levels. During COVID-19, this integrated supply chain enabled rapid pivots to meet surging demand.

Capital Allocation Discipline

The numbers tell the story: 125+ years of uninterrupted dividends, a remarkable achievement spanning world wars, depression, and countless economic cycles. This isn't luck—it's disciplined capital allocation prioritizing cash generation and shareholder returns even during transformational periods.

The framework is straightforward but rigorously applied. First, invest in the business—R&D, marketing, capital expenditures to maintain competitive position. Second, pursue strategic M&A that enhances portfolio growth potential. Third, return excess cash to shareholders through dividends and buybacks. The company targets a 50% dividend payout ratio and investment-grade credit ratings, providing flexibility while maintaining financial strength.

Recent years demonstrate this discipline. Despite the $8 billion Blue Buffalo acquisition, General Mills maintained its dividend and actually increased share buybacks. The company generates over $3 billion in annual operating cash flow, providing ample resources for investment and returns. This predictable cash generation makes General Mills a defensive equity holding even as growth slows.

IX. Power & Competition Analysis

Sources of Competitive Advantage

General Mills' power derives from multiple reinforcing sources. Scale economics are obvious—spreading fixed costs across $20 billion in revenue creates cost advantages smaller competitors can't match. But scale alone doesn't explain persistent profitability in commoditized categories.

Brand power runs deeper than logos and marketing. Cheerios isn't just cereal—it's childhood memories, parenting confidence, health perception. These emotional connections, built over generations, create switching costs that transcend rational price comparisons. When Walmart pushes private label, consumers still reach for trusted brands during life's important moments.

Distribution represents a hidden moat. Securing shelf space in 40,000+ stores requires relationships, systems, and capabilities that new entrants can't easily replicate. General Mills' direct store delivery for certain products, category management expertise, and promotional partnerships create mutual dependency with retailers—they need General Mills as much as General Mills needs them.

Network effects emerge in unexpected ways. The company's innovation pipeline benefits from scale—consumer insights from yogurt buyers improve cereal development. Manufacturing expertise in one category transfers to others. Marketing lessons from failed products prevent future mistakes. This institutional knowledge, accumulated over 150 years, can't be purchased or quickly built.

Competitive Landscape Dynamics

The competitive set depends on category—Kellogg in cereal, Danone in yogurt, Mars in pet food—but common themes emerge. Industry structure favors incumbents through high customer acquisition costs, expensive supply chains, and regulatory barriers. Yet these same factors that protect against new entrants also limit growth, creating the industry's fundamental tension.

Private label represents the most persistent threat. Retailers increasingly view store brands as margin enhancers and differentiation tools. Kroger's Simple Truth generates over $3 billion annually. Costco's Kirkland commands premium prices. As private label quality improves and stigma fades, branded manufacturers face structural share loss in commoditized categories.

Digital natives pose a different challenge. Brands like Magic Spoon (high-protein cereal) or Perfect Bar (refrigerated protein bars) capture affluent consumers willing to pay premium prices for perceived health benefits. While subscale today, these brands prove that innovation and marketing can still disrupt stable categories. General Mills' response—acquiring some, competing with others—acknowledges that startup energy can't always be internally generated.

International Opportunities and Challenges

International markets offer General Mills' clearest growth pathway, yet execution remains challenging. The company generates about 30% of sales outside North America, lagging global peers like Nestlé (90%+ international) or Unilever (80%+). This gap represents both opportunity and execution risk.

The challenge is fundamental: food is culturally specific. Cheerios might dominate American breakfast tables, but many countries don't eat cereal for breakfast. Betty Crocker resonates with American home bakers, but scratch cooking remains standard elsewhere. Successfully internationalizing requires either adapting products (expensive and complex) or changing consumer behavior (slow and uncertain).

General Mills' international strategy emphasizes partnerships over ownership. Joint ventures provide local expertise while limiting capital investment. Yet this approach also limits control and captures only partial economics. As growth slows domestically, pressure mounts to accelerate international expansion—but doing so profitably remains the unsolved challenge.

X. Bear vs. Bull Case

The Bear Perspective

Structural headwinds are intensifying, not abating. U.S. cereal consumption has declined for fifteen consecutive years. Yogurt sales peaked in 2015. These aren't cyclical downturns—they're secular shifts driven by changing lifestyles, health consciousness, and demographic evolution. General Mills is fighting gravity.

The math is sobering. Volumes declined in fiscal 2023 and 2024 despite massive innovation investment. Pricing power is exhausted—further increases will accelerate volume declines. Input cost inflation continues while retailers demand lower prices. The company is caught between inflating costs and deflating revenues, with margins the casualty.

GLP-1 drugs like Ozempic represent an existential threat nobody fully understands. Early data suggests users reduce caloric intake by 20-30%, with particular aversion to sweet, processed foods—General Mills' core portfolio. As these drugs gain adoption, food companies face a future where their core consumers literally consume less.

Private label quality has reached parity in many categories while maintaining 20-30% price discounts. Younger consumers show less brand loyalty than previous generations. Amazon's algorithms surface products based on ratings and price, diminishing brand advantage. The moats that protected incumbents for decades are eroding.

Debt levels concern observers. The Blue Buffalo acquisition added $8 billion in obligations. While manageable at current interest rates, refinancing risk looms. The company's credit rating sits just above junk status. Another large acquisition could trigger downgrades, increasing borrowing costs precisely when financial flexibility is most needed.

The Bull Perspective

Cash flow remains king, and General Mills generates it reliably. Over $3 billion in annual operating cash flow funds dividends, buybacks, and growth investment with room to spare. This isn't a melting ice cube—it's a cash machine that happens to face temporary headwinds.

Portfolio transformation is working, just slowly. Blue Buffalo grows double-digits and generates 25%+ margins. Pet food now represents nearly 20% of profits despite being 10% of sales. As traditional categories decline, growth platforms gain mix—the portfolio naturally evolves toward higher growth, higher margin businesses.

Innovation capabilities remain world-class. The company launches 400+ new products annually, with hit rates improving through better consumer insights and rapid prototyping. Recent successes like Oui yogurt, protein-enriched cereals, and Blue Buffalo cat treats prove that innovation can drive growth even in mature categories.

Emerging markets remain underpenetrated. Rising middle classes in India, China, and Africa will adopt packaged foods as incomes grow and urbanization accelerates. General Mills' brand expertise and product portfolio position it to capture this multi-decade growth opportunity. International could double from 30% to 60% of sales, offsetting domestic maturity.

The defensive characteristics matter more as economic uncertainty rises. Food is non-discretionary. Brands provide comfort during stressful times. General Mills' products are affordable luxuries—small indulgences that consumers maintain even when cutting larger expenses. The company survived the Great Depression and will survive the next recession.

XI. Recent News and Developments

Fiscal 2024: Navigating Choppy Waters

Net sales of $19.9 billion decreased 1 percent from the prior year; organic net sales were 1 percent below year-ago results that grew double digits. Operating profit of $3.4 billion essentially matched year-ago results; adjusted operating profit of $3.6 billion was up 4 percent in constant currency. Diluted earnings per share (EPS) of $4.31 essentially matched year-ago results; adjusted diluted EPS of $4.52 was up 6.

The results reflect masterful navigation of a difficult environment. Volume pressures from price increases were offset by mix improvements and cost savings. The company generated industry-leading HMM savings exceeding 4% of cost of goods sold, funding both margin expansion and increased marketing investment.

Strategic Priorities for Fiscal 2025

Management's fiscal 2025 guidance signals a strategic pivot toward volume recovery. The company expects to reinvest potential margin flexibility back into the business, including plans for a significant increase in brand-building investment in fiscal 2025 to drive improved volume performance. This marks a departure from recent years' focus on pricing and margins.

The investment thesis has shifted. Rather than maximizing near-term profits, General Mills is playing for market share and long-term positioning. Increased marketing, innovation acceleration, and strategic revenue management aim to reignite organic growth even if margins temporarily compress.

Sustainability and ESG Leadership

Environmental commitments increasingly influence operations and investor perception. General Mills committed to regenerative agriculture practices on one million acres by 2030, recognizing that climate change threatens agricultural supply chains. The company sources 100% renewable electricity for global operations and has reduced greenhouse gas emissions by 14% since 2020.

Social initiatives extend beyond corporate responsibility to business strategy. The company's focus on food insecurity—donating over $150 million annually to food banks—builds brand equity while addressing societal needs. Diversity commitments include increasing management diversity to 50% by 2025, recognizing that diverse teams drive better innovation and decision-making.

These initiatives aren't merely compliance—they're competitive advantages. Younger consumers increasingly choose brands aligned with their values. Retailers favor suppliers with strong ESG credentials. Investors apply ESG screens that affect capital access. General Mills' early leadership in sustainability provides differentiation in commoditized categories.

XII. Conclusion: The Next 150 Years

General Mills stands at an inflection point. The company that survived the Great Mill Explosion, thrived through the Depression, and swallowed Pillsbury now faces its greatest challenge: relevance in a rapidly changing food system. The playbook that built a $40 billion empire—scaled manufacturing, mass marketing, shelf space dominance—no longer guarantees success.

Yet dismissing General Mills as a declining incumbent misses crucial strengths. The company's transformation capabilities—from flour miller to cereal giant to diversified food company to pet food leader—demonstrate remarkable adaptability. Few organizations successfully reinvent themselves even once; General Mills has done so repeatedly across fifteen decades.

The path forward requires uncomfortable choices. Sacred brands may need pruning. International expansion must accelerate despite execution risks. Digital capabilities need development even as traditional competencies remain important. The company must simultaneously manage decline in legacy categories while building growth platforms—a dual transformation that challenges even exceptional management teams.

The financial foundation remains solid. General Mills generates prodigious cash flow, maintains an investment-grade balance sheet, and returns billions to shareholders annually. This financial strength provides time and resources for transformation—luxuries that struggling competitors lack. The question isn't survival but growth trajectory.

History suggests betting against General Mills is dangerous. The company has survived technological disruption (industrial milling), competitive threats (Pillsbury rivalry), economic catastrophe (multiple recessions), and category disruption (health trends). Each challenge prompted evolution that ultimately strengthened competitive position. Current headwinds, while serious, pale compared to past existential threats.

The investment case reduces to time horizon and risk tolerance. Near-term investors face continued volatility as volume pressures persist and margins compress. Long-term investors see a cash-generative business with proven adaptation capabilities trading at reasonable valuations. Income investors find reliable dividends with 125+ years of payment history.

Perhaps the most overlooked asset is institutional knowledge. General Mills understands American eating habits better than perhaps any organization. This consumer intimacy, accumulated over generations, enables the company to anticipate and shape food trends rather than merely respond. As eating patterns evolve—whether toward health, convenience, or indulgence—General Mills possesses unique capabilities to participate profitably.

The next decade will determine whether General Mills becomes another Kraft Heinz (financial engineering masking declining relevance) or follows Nestlé's path (successful transformation into health and wellness). Early indicators are mixed but lean positive. Blue Buffalo validates M&A capabilities. Innovation metrics improve. International growth accelerates. Management acknowledges challenges while investing for the future.

The cereal empire that ate Pillsbury may no longer dominate breakfast tables, but it's far from finished. General Mills' story—from Minneapolis flour mill to global food conglomerate—represents American business evolution at its most dramatic. The next chapter remains unwritten, but history suggests it will surprise those who underestimate this remarkable institution's capacity for reinvention.

After 150 years, General Mills has earned the benefit of the doubt. The company that turned flour dust into gold medals, created Betty Crocker from imagination, and transformed pet food from commodity to premium will likely find new ways to feed the world profitably. The question isn't whether General Mills survives but what it becomes—and that transformation will define American food for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube