Welltower: Building America's Healthcare Infrastructure REIT

I. Introduction & Episode Roadmap

The year is 2025, and in a nondescript office building in Toledo, Ohio, executives at Welltower are reviewing a portfolio that would have seemed like science fiction just five decades ago: over 3,000 properties spanning three countries, housing hundreds of thousands of seniors, generating nearly $8 billion in annual revenue. This isn't just real estate—it's the physical infrastructure of American aging, a $100 billion empire built on a simple yet profound insight: as America grays, someone needs to own the buildings where aging happens.

Consider this staggering reality: every single day, 10,000 Americans turn 65. That's one person every eight seconds, a demographic tsunami that began in 2011 when the first baby boomers hit retirement age and won't crest until 2030. By 2040, the population of Americans over 85—those most likely to need senior housing—will triple. This isn't a trend or a cycle; it's a mathematical certainty as inexorable as compound interest.

Welltower, ranked 534th on the Fortune 500, has positioned itself as the dominant landlord to this aging nation. But here's what makes this story fascinating: the company didn't start as a healthcare visionary or a real estate mogul's vanity project. It began in 1970 as a quirky financial innovation called a REIT—a Real Estate Investment Trust—at a time when most Americans had never heard the term and healthcare real estate barely existed as an asset class.

The journey from Health Care Fund, a small Toledo startup, to Welltower, the S&P 500's healthcare real estate giant, is a masterclass in three converging forces that define modern American capitalism: the financialization of real estate through REITs, the industrialization of healthcare delivery, and the demographic destiny of an aging population. It's also a story of timing—how a company founded just five years after Medicare's creation would ride every major wave in American healthcare for the next half-century.

What makes Welltower particularly compelling isn't just its scale—though owning properties worth more than the GDP of Iceland certainly commands attention. It's how the company has evolved from a passive landlord collecting rent checks to what CEO Shankh Mitra calls a "wellness infrastructure company," using data science, operational expertise, and capital allocation to fundamentally reshape how Americans age. This transformation required navigating financial crises, a global pandemic that nearly destroyed the senior housing industry, and multiple leadership transitions that each redefined what the company could become.

The REIT structure itself deserves examination. Created by Congress in 1960 to democratize real estate investing, REITs must distribute 90% of taxable income as dividends, creating a unique business model that trades operational flexibility for tax efficiency and forces extreme discipline in capital allocation. For Welltower, this structure has been both a constraint and a superpower—limiting retained earnings but creating a cost of capital advantage that has fueled five decades of growth.

This episode explores how three visionary leaders—George Chapman, Thomas DeRosa, and Shankh Mitra—each reimagined what a healthcare REIT could be, transforming Welltower from a nursing home landlord into a vertically integrated platform that influences how millions of Americans experience aging. We'll examine the company's biggest bets, including the $4.4 billion ProMedica acquisition, the pandemic-era pivot that nearly broke the company before making it stronger, and the current AI and data science revolution that's creating new competitive moats.

But this isn't just a story about financial engineering and demographic charts. It's about the intersection of capital and care, where Wall Street metrics meet human dignity, and where the quality of real estate directly impacts the quality of life for society's most vulnerable. As we'll see, Welltower's evolution mirrors America's ongoing struggle to care for its aging population—a challenge that grows more urgent with each passing day, each retiring boomer, each family searching for a safe, dignified place for mom or dad to spend their final years.

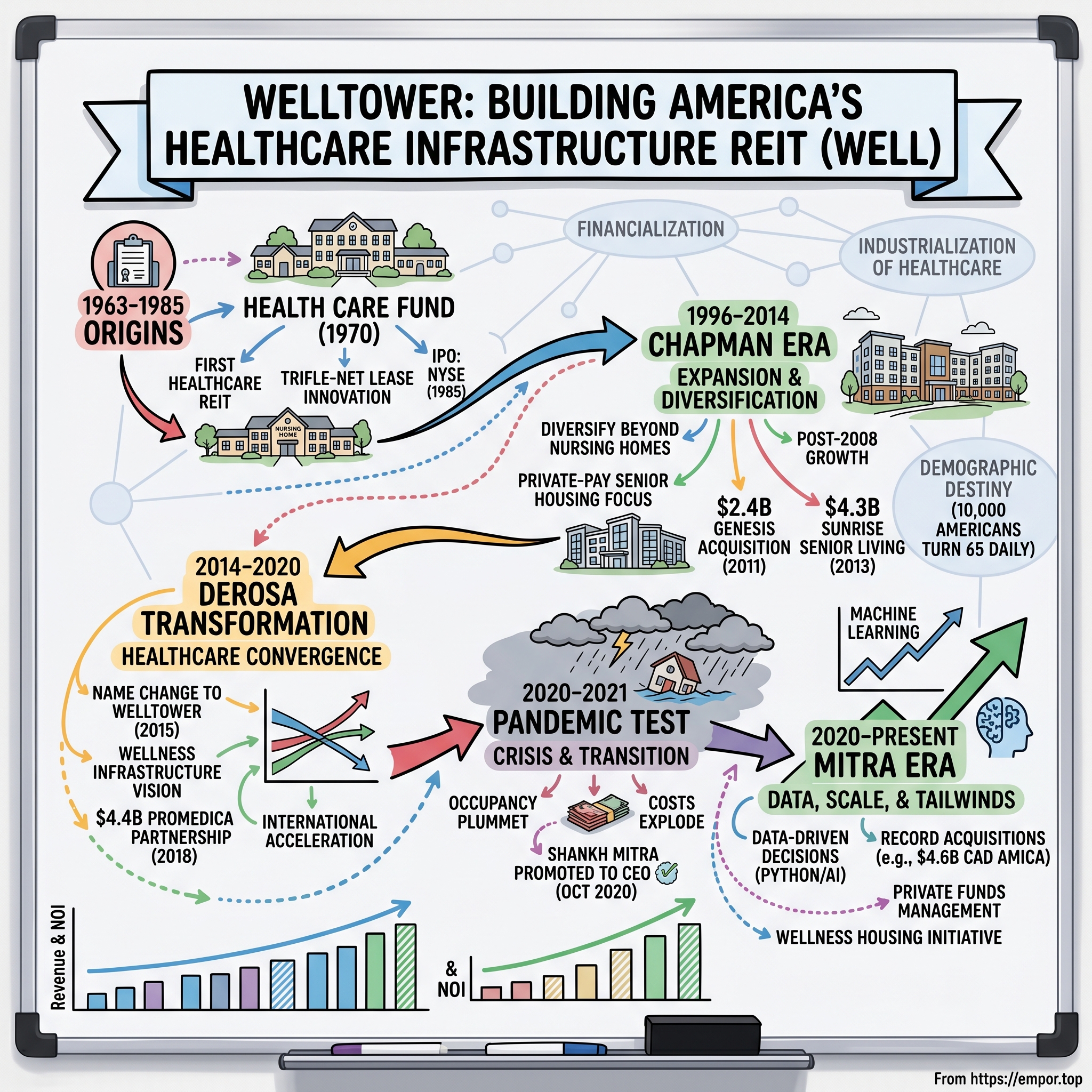

II. Origins: The First Healthcare REIT (1963-1985)

The fluorescent lights hummed in the cramped Lima, Ohio office as Bruce Thompson spread architectural drawings across a folding table. It was 1963, and Thompson, barely 30, was explaining to local investors why building nursing homes wasn't just a social good—it was about to become a goldmine. Two years later, Lyndon Johnson would sign Medicare and Medicaid into law, transforming healthcare from a private family burden into a government-backed entitlement. Thompson saw it coming.

But Thompson faced a problem that every real estate developer knows: buildings are expensive, capital is scarce, and banks don't like lending to unproven sectors. Nursing homes in 1963 occupied a strange netherworld—not quite hospitals, not quite apartments, serving a population that society preferred to ignore. The few facilities that existed were often converted mansions or repurposed buildings, chronically underfunded and understaffed. Thompson believed he could do better, but he needed a financial innovation to match his operational vision.

Enter the REIT—a creation of the Real Estate Investment Trust Act of 1960, itself a product of President Eisenhower's belief that ordinary Americans should be able to invest in large-scale real estate just as they could buy shares in General Motors. The structure was elegant: pool investor capital, buy real estate, distribute 90% of taxable income as dividends, pay no corporate taxes. It democratized real estate investing while creating a powerful tax-advantaged vehicle for patient capital. By 1970, Thompson had spent seven years building and operating nursing homes, learning the business from the ground up. Now he was ready for the next leap. In 1970, Bruce G. Thompson, Frederic D. Wolfe, and Fritz Wolfe founded Health Care Fund, becoming the first healthcare REIT. The partnership was quintessentially midwestern—Thompson, a Lima lawyer turned nursing home developer, and Fritz Wolfe, whose family owned Lima Lumber Company and had built its first nursing home in 1963. Thompson and Wolfe had been Yale roommates, a connection that would prove crucial as they navigated the uncharted waters of healthcare real estate finance.

The timing was exquisite. Medicare and Medicaid, enacted in 1965, had created a government-backed payment system for elderly care, transforming nursing homes from charity cases into profitable enterprises. The Hill-Burton Act was pouring federal money into hospital construction. Demographics were destiny—the parents of baby boomers were aging, life expectancy was rising, and families were increasingly unable to care for elderly relatives at home. Thompson and Wolfe weren't just building nursing homes; they were constructing the physical infrastructure of a new social contract.

But growth was glacial at first. As a REIT has to sell stock in order to grow, and investors in 1970 didn't understand healthcare real estate. Was it like apartments? Office buildings? Hospitals? The answer was none of the above—it was a new asset class with its own risk profile, operational complexity, and growth trajectory. By the end of the decade, the firm's assets had grown to more than $25 million—respectable but hardly revolutionary.

The innovation wasn't just financial; it was operational. Health Care Fund pioneered the triple-net lease structure for healthcare properties, where tenants paid not just rent but also taxes, insurance, and maintenance. This transformed the REIT from an active operator into a passive landlord, reducing operational risk while maintaining steady cash flows. It was a model perfectly suited to the REIT structure's requirement to distribute 90% of taxable income—predictable, scalable, and capital-efficient. The transition to public markets marked the company's next evolution. In 1985, Health Care Fund changed its name to Health Care REIT and completed its initial public offering on the New York Stock Exchange, becoming one of the first publicly traded healthcare REITs. The IPO wasn't a blockbuster—healthcare REITs were still an oddity, and institutional investors preferred traditional real estate sectors. But it gave the company access to public capital markets and the liquidity that would prove crucial for future growth.

As former Welltower CEO George Chapman would later reflect, "Bruce, together with Fritz, were leaders not only in health care, but in long-term care. They formed the first REIT that was fully dedicated to health-care properties. They paved the way for many other health-care REITs to come".

The genius of Thompson and Wolfe's model became clear only in retrospect. They had created a financial structure that aligned perfectly with the economics of healthcare real estate: long-term, stable cash flows from essential services backed by government reimbursement and demographic tailwinds. While others saw nursing homes as a social service, they saw them as an infrastructure play on American aging. By 1985, Health Care REIT owned properties across multiple states, had survived the volatile 1970s economy, and had proven that healthcare real estate could be a legitimate institutional asset class. The foundation was set for explosive growth.

III. Building the Foundation: Chapman Era (1996-2014)

George Chapman arrived at Health Care REIT in 1983 as a young executive with a background in traditional real estate, not healthcare. By 1996, when he ascended to CEO, the company had grown steadily but remained a niche player with a market cap under $500 million. Chapman would transform it into a $20 billion behemoth, but his first challenge was more fundamental: convincing Wall Street that a healthcare REIT wasn't an oxymoron. Chapman joined the company in 1992 as executive vice president and general counsel, recruited to succeed the founders. When he took the CEO role in 1996, Health Care REIT had a market capitalization of just $394 million. By his retirement in 2014, that number would reach $15.5 billion—a 39-fold increase that outpaced the S&P 500 by a factor of ten.

His strategy was deceptively simple: diversify beyond nursing homes. Throughout the late 1990s and early 2000s, Chapman systematically expanded the portfolio to include senior housing communities, medical office buildings, and other healthcare-related properties. This wasn't just geographic diversification—it was a fundamental reimagining of what healthcare real estate could encompass. Where the founders had focused on government-reimbursed skilled nursing, Chapman saw opportunity in private-pay senior housing, where residents paid out of pocket for higher-quality accommodations and services.

The shift to private-pay was prescient. Medicare and Medicaid reimbursements were increasingly under pressure, subject to political whims and budget constraints. But affluent seniors would pay premium prices for quality housing with healthcare services—a demographic sweet spot that combined the baby boomers' wealth accumulation with their desire to age differently than their parents. Chapman was building for customers who didn't yet exist but were demographically inevitable.

Then came 2008. The financial crisis that destroyed Lehman Brothers and nearly took down the global banking system hit REITs particularly hard. Property values plummeted, credit markets froze, and Health Care REIT's stock fell from over $50 to under $25. For a REIT dependent on capital markets for growth, it was an existential threat. But Chapman saw opportunity where others saw catastrophe.

Healthcare real estate, he argued, was fundamentally different from office towers or shopping malls. People don't stop aging in a recession. Seniors still need care. Hospitals still operate. While other REITs slashed dividends and sold properties at fire-sale prices, Health Care REIT maintained its dividend and went shopping. The company's defensive characteristics—long-term leases, essential services, demographic tailwinds—made it attractive to investors seeking safety in chaos.

The company's biggest coup during the Chapman era came in 2011 with the $2.4 billion acquisition of Genesis HealthCare's real estate portfolio—147 properties including post-acute, skilled nursing, and assisted living facilities across 11 states. It was a massive bet on the post-acute care sector just as hospitals were being incentivized to reduce readmissions and length of stay. Chapman understood that as hospitals discharged patients "quicker and sicker," demand for transitional care facilities would soar.

But Chapman's masterstroke was the 2013 acquisition of Sunrise Senior Living's real estate for $4.3 billion—125 properties in prime urban markets across the U.S., Canada, and the UK. Sunrise was the Ritz-Carlton of senior housing, with properties in affluent areas like McLean, Virginia, and Beverly Hills. The deal transformed Health Care REIT from a domestic player into a global platform, while dramatically upgrading the quality and demographics of its portfolio.

Chapman also pioneered new partnership structures that went beyond traditional triple-net leases. The RIDEA structure (named after the REIT Investment Diversification and Empowerment Act of 2007) allowed REITs to participate in the operating income of senior housing properties, not just collect rent. It was riskier—operating income is more volatile than rent—but offered higher returns and better alignment with operators. Chapman was transforming Health Care REIT from a passive landlord into an active participant in healthcare delivery.

By 2014, when Chapman announced his retirement at age 66, Health Care REIT owned properties worth $25 billion across three countries. The company had survived the financial crisis, consolidated a fragmented industry, and positioned itself for the coming demographic wave. As Chapman handed the reins to Thomas DeRosa, he left behind not just a larger company but a fundamentally different one—diversified, international, and operationally sophisticated. The foundation builder had completed his work.

IV. The DeRosa Transformation: Healthcare Convergence (2014-2020)

Thomas DeRosa stepped into the CEO role at Health Care REIT in April 2014 with a radically different vision. Where Chapman had built through acquisition and diversification, DeRosa saw integration and transformation. His first major decision signaled the ambition: in 2015, Health Care REIT would become Welltower, shedding its functional but forgettable name for something that suggested wellness, aspiration, and vertical reach. "We're not a healthcare REIT," DeRosa declared in his first major presentation as CEO. "We're a wellness infrastructure company." It was more than semantics—it was a fundamental reconceptualization of the business. Where traditional REITs owned buildings and collected rent, DeRosa envisioned Welltower as an active participant in healthcare transformation, using real estate as a platform for care delivery innovation.

DeRosa brought a different background than his predecessors. A former CFO of The Rouse Company and investment banker at Deutsche Bank, he understood capital markets but also operational excellence. His thesis was simple but profound: as healthcare shifted from acute care hospitals to outpatient settings, from treatment to prevention, from institutional to residential, whoever owned the real estate where this transformation happened would capture enormous value.

The strategy manifested in increasingly sophisticated partnerships. The 2014 joint venture with Revera to acquire Sunrise Senior Living's management company wasn't just about real estate—it was about controlling the operating platform. Welltower now had influence over how properties were managed, how care was delivered, how technology was deployed. The REIT was becoming something unprecedented: a hybrid between landlord and healthcare company.

DeRosa's boldest move came in 2018 with the $4.4 billion acquisition of Quality Care Properties and HCR ManorCare, done in partnership with ProMedica Health System. This wasn't just Welltower buying nursing homes—it was the company partnering with a major health system to reimagine post-acute care. ProMedica would operate the facilities, using its clinical expertise to improve outcomes and reduce readmissions. Welltower would own the real estate and share in the operational upside. It was the physical manifestation of DeRosa's wellness infrastructure vision.

The international expansion accelerated under DeRosa. Welltower acquired premium properties in London's healthcare district, partnered with the Canada Pension Plan Investment Board for major acquisitions, and built a UK portfolio worth billions. The company wasn't just following demographic trends—it was betting that healthcare convergence was a global phenomenon, that aging populations in Toronto and London would need the same infrastructure innovation as those in Toledo.

DeRosa also pioneered the use of data and technology in ways REITs traditionally hadn't. Welltower began tracking operational metrics daily across its portfolio—occupancy, length of stay, acuity levels, staffing ratios. The company used this data to identify best practices, optimize operations, and even predict which properties would outperform. As DeRosa explained to investors, "We're in touch on a daily basis with what is happening at the property level of our portfolio."

The company's relationship with operators evolved from landlord-tenant to strategic partnership. Welltower would share data, provide capital for technology investments, facilitate best practice sharing across operators. The company hosted innovation summits where operators could learn about telemedicine, sensor technology, predictive analytics. DeRosa was transforming Welltower from a passive capital provider into an active catalyst for industry transformation.

By early 2020, DeRosa's transformation seemed complete. Welltower had divested most of its skilled nursing exposure, upgraded to premium private-pay properties, built deep health system relationships, and created operational capabilities that rivaled those of healthcare companies. The stock had more than doubled during his tenure. Revenue had grown from $2.5 billion to over $5 billion. The company had been added to the S&P 500.

Then, in March 2020, everything changed. COVID-19 arrived in American nursing homes and senior living communities with devastating force. Occupancy plummeted as families pulled residents out and new move-ins froze. Operating costs soared as facilities scrambled for PPE and testing. Death rates in senior care facilities dominated headlines. For a company that had just pivoted toward operational participation through RIDEA structures, the timing couldn't have been worse. DeRosa's wellness infrastructure vision was about to face its ultimate test.

V. The Pandemic Test & Leadership Transition (2020-2021)

The call came at 2 AM on March 13, 2020. A Welltower property in Seattle—ground zero for COVID in America—had reported its first positive case. Within hours, the senior leadership team was assembled via video conference, staring at screens from their home offices as they grappled with an unprecedented crisis. Senior housing occupancy, which had been running at 87%, would plummet to 72% within months. Some properties saw occupancy fall below 60%. For a business model predicated on high fixed costs and stable occupancy, it was catastrophic. DeRosa issued statements of confidence: "There is no perfect playbook to manage through a pandemic," he wrote in March 2020. But behind the scenes, the situation was dire. Operating costs in senior housing were exploding—PPE that once cost pennies now cost dollars, staffing agencies were charging triple rates, and testing infrastructure had to be built from scratch. Meanwhile, families were pulling residents out, and new admissions had essentially stopped. Some properties were bleeding $50,000 per month in operating losses.

Enter Shankh Mitra. The board had promoted him to Vice Chair and Chief Operating Officer in April 2020 with the explicit intention that he would succeed DeRosa. By October, the transition was complete. Mitra, 44 at the time, brought a radically different profile than his predecessors. An Indian immigrant with an engineering degree from Jadavpur University and an MBA from Columbia focused on value investing, he had spent his career at hedge funds including Millennium Management, not in real estate operations.

Mitra's leadership philosophy centers on data-driven decision-making, and the mentoring of early career professionals. He is deeply passionate about capital allocation, predictive analytics in the area of statistical learning and machine learning. This wasn't corporate speak—it was his genuine obsession. Where DeRosa had talked about wellness infrastructure, Mitra talked about machine learning models and predictive analytics. Where Chapman had been a dealmaker, Mitra was a quant.

His first moves were surgical. Welltower sold over $1.3 billion in underperforming properties within months, using the proceeds to shore up the balance sheet. The company maintained $5.3 billion in liquidity—enough to survive even if occupancy stayed depressed for years. But Mitra wasn't planning to just survive; he was positioning for a generational buying opportunity.

The data science approach proved crucial during the pandemic. Welltower built models to predict which properties would recover fastest based on local vaccination rates, demographic mix, competitive supply, and dozens of other variables. The company could identify which operators were managing the crisis well and which were floundering. This granular, property-level intelligence allowed Welltower to make decisions that seemed counterintuitive—investing heavily in some markets while others were retreating.

Friends and colleagues will tell you that I'm a crisis leader. Mitra embraced the role. He instituted daily calls with major operators, not to micromanage but to share data and best practices. Welltower became a clearinghouse for operational intelligence—which properties had successfully implemented rapid testing, which staffing strategies were working, how to message to families about safety protocols. The REIT was acting less like a landlord and more like a management consultant.

The company also leveraged its scale in unprecedented ways. Welltower negotiated bulk purchases of PPE for its operators, used its relationships with CVS and Walgreens to prioritize vaccine distribution to its properties, and even worked with academic institutions to develop testing protocols. The company that had started as a passive landlord was now actively managing a public health crisis across thousands of properties.

By mid-2021, the strategy was working. Senior housing occupancy bottomed at 72% and began climbing. The properties Welltower had identified as likely to recover first were indeed outperforming. Operating margins, while still compressed, were improving. Most importantly, the competitive landscape had been transformed. Thousands of mom-and-pop senior living facilities had closed permanently. New construction had essentially stopped. When demand returned—and demographics guaranteed it would—supply would be constrained for years.

The pandemic had been a near-death experience for the senior housing industry. But for Welltower, it was also a catalyst for transformation. The crisis had accelerated trends that might have taken a decade to play out: consolidation of ownership, professionalization of operations, integration with healthcare systems, adoption of technology. Mitra hadn't just navigated the crisis; he had used it to fundamentally reposition the company. As he told investors in late 2021, "We've laid down a very solid foundation... The foundations are there for meaningful growth."

VI. The Mitra Era: Data, Scale, and Demographic Tailwinds (2020-Present)

The Bloomberg terminal glowed in Shankh Mitra's home office at 5 AM on a Tuesday morning in February 2022. While most CEOs might be reviewing quarterly reports or preparing for board meetings, Mitra was writing Python code, tweaking a machine learning model that predicted move-in probability based on web traffic patterns, local COVID case rates, and competitive pricing dynamics. This wasn't a hobby—it was how he ran Welltower. By 2022, as the pandemic receded and occupancy began recovering, Mitra's data-driven approach was bearing fruit. Senior housing occupancy climbed back above 80%, then 85%. But more importantly, Welltower's properties were recovering faster than competitors'. The company's same-store NOI growth hit 23% year-over-year—not just pandemic recovery but genuine outperformance. For eight consecutive quarters, growth exceeded 20%, a streak unmatched in REIT history.

The acquisition machine roared back to life, but with a difference. Under Mitra, every deal was underwritten not just on current performance but on predictive models incorporating dozens of variables. The company could identify properties where small operational improvements would yield outsized returns. A property might be struggling with 75% occupancy, but Welltower's models might show that with better digital marketing, optimized pricing, and operational tweaks, it could reach 90% within 18 months.

The pace was staggering. In 2024 alone, Welltower completed $6.1 billion in acquisitions—a company record. The crown jewel came in 2025 with the $4.6 billion CAD acquisition of Amica Senior Lifestyles from the Ontario Teachers' Pension Plan. Amica operated 38 ultra-luxury communities in Canada's most affluent markets—Toronto's Yorkville, Vancouver's West End, Victoria's Oak Bay. These weren't nursing homes; they were the Four Seasons of senior living, with average revenue per occupied room exceeding $12,000 CAD per month.

The Amica portfolio included communities in "highly affluent neighborhoods" in Toronto, Vancouver and Victoria, Canada and spanned the care continuum from independent living to memory care, with an average length of stay between three and four years. The deal showcased Mitra's strategic vision: focus on affluent markets with high barriers to entry, partner with best-in-class operators, and use data to optimize performance.

But Mitra's most innovative move was launching Welltower's private funds management business in January 2025. The company announced its first fund, which has the ability to source up to $2 billion to invest in stable or near-stable seniors housing properties, with NorthStar Healthcare's 40-community portfolio becoming one of its first acquisitions for $900 million. This wasn't just about raising third-party capital; it was about creating a platform that could move faster and more aggressively than the public REIT structure allowed.

The fund structure solved multiple problems. It provided dry powder for acquisitions without diluting public shareholders. It allowed Welltower to take on transitional assets that might temporarily depress REIT metrics. Most importantly, it positioned the company as an asset manager, not just an owner—earning fees on other people's capital while maintaining operational control.

Mitra's approach to operations was equally revolutionary. Welltower built what he called a "data platform" that tracked everything: how long prospects spent on property websites, which amenities correlated with higher occupancy, how staffing ratios affected resident satisfaction. The company could predict with startling accuracy which residents were at risk of moving out, which prospects were most likely to move in, even which properties would see COVID outbreaks based on community transmission rates.

This wasn't just data for data's sake. Welltower used these insights to help operators improve performance. If the models showed that properties with dog parks had 3% higher occupancy, Welltower would fund dog park construction. If certain digital marketing keywords drove better-qualified leads, that information was shared across the portfolio. The REIT was becoming a learning machine, getting smarter with every data point.

The wellness housing initiative represented Mitra's vision for Welltower's future. Recognizing that the 55-65 demographic wanted different things than traditional senior housing offered, the company began developing active adult communities with fitness centers, co-working spaces, and lifestyle programming. These weren't retirement homes but wellness communities that happened to offer healthcare services. It was a bet that baby boomers would redefine aging just as they had redefined every other life stage.

Financial performance under Mitra has been extraordinary. Revenue grew from $6.47 billion in 2023 to $7.85 billion in 2024, while same-store NOI growth for the senior housing operating portfolio was 23%, marking the eighth consecutive quarter of over 20% growth. The stock price, which had languished in the $60s during the pandemic, soared past $100. Market capitalization exceeded $100 billion, making Welltower one of the largest REITs in the world.

But perhaps Mitra's greatest achievement was transforming Welltower's culture. The company recruited data scientists from tech companies, healthcare analysts from consulting firms, and operators from hospitality brands. The Toledo headquarters, once a traditional corporate office, now resembled a Silicon Valley campus with open workspaces, collaboration zones, and walls covered in data visualizations. Mitra himself continued coding, hosting "Python Fridays" where employees could learn programming together.

As 2025 progresses, Welltower stands as a fundamentally different company than the one founded 55 years ago. It's part REIT, part private equity firm, part data company, part healthcare operator. Under Mitra's leadership, it has become what he envisioned: a platform that uses real estate as the foundation for healthcare transformation, powered by data, scaled through technology, and positioned to capture the enormous value creation opportunity of American aging.

VII. Business Model Deep Dive: The REIT Advantage

To understand Welltower's dominance, you must first understand the elegant brutality of the REIT structure. Imagine running a business where you're legally required to distribute 90% of your taxable income every year. No war chest for downturns. No retained earnings for growth. Every quarter, nearly every dollar that comes in must go out. It's a model that would terrify most CEOs, yet it's precisely this constraint that has made Welltower so formidable.

The company's business model centers on acquiring, developing, and managing high-quality healthcare properties that generate stable rental income. Welltower's portfolio includes senior housing communities, skilled nursing facilities, outpatient medical buildings, and life science properties. But the real sophistication lies in how the company structures these investments.

The triple-net lease, Welltower's original model, remains the simplest: the tenant pays rent plus all operating expenses, taxes, and maintenance. It's pure real estate—predictable, stable, boring. For a medical office building leased to Cleveland Clinic for 15 years, this structure makes perfect sense. The rent check arrives every month, escalates annually, and Welltower's involvement is minimal. These leases typically generate 6-7% unlevered returns—not exciting, but reliable as gravity.

The RIDEA structure, enabled by legislation in 2007, transformed the industry. Instead of being a passive landlord, Welltower could now participate in the operational performance of senior housing. The company doesn't operate properties directly—that would violate REIT rules—but partners with operators in joint ventures, sharing both risks and rewards. When occupancy rises from 85% to 90%, Welltower captures that upside. When a pandemic hits and occupancy plummets, Welltower feels the pain.

Consider the math on a typical RIDEA property: A 200-unit senior living community might generate $15 million in revenue at 90% occupancy, with operating expenses of $10 million, yielding $5 million in net operating income. Under a triple-net lease, Welltower might collect $3 million in annual rent regardless of performance. Under RIDEA, Welltower owns 95% of the property and receives 95% of that $5 million NOI. If the operator improves occupancy to 95% and raises rents 5%, NOI might jump to $6.5 million—and Welltower captures 95% of that increase.

But RIDEA also means risk. During COVID, when occupancy fell to 75% and operating costs spiked, that same property might have generated only $1 million in NOI—or even operated at a loss. Triple-net tenants still paid rent (mostly), but RIDEA properties hemorrhaged cash. It's operational leverage in its purest form—magnifying both gains and losses.

The capital allocation framework is where Mitra's influence is most evident. Every investment decision runs through predictive models that consider not just current returns but probabilistic outcomes across multiple scenarios. A property might offer a 7% going-in yield, but if Welltower's models show a 60% probability of achieving 9% within three years through operational improvements, it becomes attractive. Conversely, a 10% yield in a declining market with high supply risk might be rejected.

The cost of capital advantage is crucial. As an investment-grade REIT with access to public markets, Welltower can raise capital more cheaply than almost any competitor. When 10-year Treasury rates are 4%, Welltower might issue debt at 5%, while a private owner might pay 7% or more. This 200-basis-point advantage might seem small, but when deployed across billions in assets, it creates an insurmountable competitive moat.

Portfolio composition tells the strategic story. As of Q1 2024, Senior Housing Operating represents 60% of revenue at $1.04 billion, Outpatient Medical 25% at $227.3 million, Triple-net 15% at $219.9 million, with smaller contributions from health systems and long-term care. This isn't random; it's carefully optimized for risk-adjusted returns. Senior housing offers the highest growth but most volatility. Medical office provides stability and credit quality. Triple-net acts as ballast during turbulent times.

The operator ecosystem is perhaps Welltower's most underappreciated asset. The company doesn't just have tenants; it has partners. Sunrise Senior Living, Brookdale, Atria—these aren't just names on leases but deeply integrated relationships. Welltower shares data, provides capital for improvements, facilitates best practice sharing. When Sunrise discovers a new memory care protocol that reduces falls by 20%, that knowledge spreads across Welltower's portfolio. It's network effects in physical form.

The alignment mechanisms are sophisticated. In RIDEA structures, operators typically own 5-10% of the property, ensuring skin in the game. Performance incentives are tied not just to occupancy but to resident satisfaction, staff retention, and clinical outcomes. Welltower has even pioneered "waterfall" structures where operator economics improve as properties hit performance hurdles—turning operators into true partners in value creation.

Technology integration adds another layer. Welltower's properties increasingly feature smart building systems that track everything from HVAC efficiency to resident movement patterns (with permission). This data feeds back into operational decisions: if residents in memory care units are most active between 10 AM and noon, that's when activities are scheduled. If certain room configurations correlate with fewer falls, future developments incorporate those designs.

The development pipeline, while smaller than acquisitions, showcases the model's evolution. Welltower doesn't develop speculatively; every project has an identified operator and often pre-leasing before breaking ground. The company targets 8-10% development yields versus 5-6% for acquisitions—compensation for taking development risk. But even here, risk is minimized through phased developments, modular construction, and partnerships with experienced developers.

The international dimension adds complexity but also opportunity. UK and Canadian properties operate under different regulatory regimes, reimbursement models, and cultural expectations. But they share demographic tailwinds and supply constraints. Welltower applies its operational playbook while adapting to local conditions—memory care protocols might be universal, but dining programs reflect local preferences.

What makes this model so powerful isn't any single element but how they reinforce each other. Scale provides data. Data improves operations. Better operations attract top operators. Top operators enable RIDEA structures. RIDEA structures generate higher returns. Higher returns lower cost of capital. Lower cost of capital enables more acquisitions. More acquisitions increase scale. It's a virtuous cycle that accelerates with each revolution.

The REIT structure itself, that requirement to distribute 90% of taxable income, becomes an advantage. It forces discipline—no empire building, no unrelated diversification, no hoarding cash. Every dollar must be productively deployed or returned to shareholders. It creates trust with investors who know management can't waste money even if they wanted to. And it provides tax efficiency—Welltower pays no corporate taxes, while investors pay taxes only on distributions they receive.

VIII. Competitive Landscape & Market Position

The conference room at Ventas headquarters in Chicago hummed with tension. It was February 2024, and CEO Debra Cafaro was reviewing Welltower's latest acquisition announcement—another $500 million portfolio grabbed at what seemed like an impossible cap rate. "How do they keep winning these deals?" an analyst asked. The answer wasn't just capital or relationships. It was that Welltower had become something none of its competitors had managed: a platform company that transcended real estate.

Welltower operates in the healthcare REIT sector, competing primarily with other specialized healthcare real estate companies. Its main competitors include Ventas (VTR), Healthpeak Properties (DOC), Omega Healthcare Investors (OHI), and Medical Properties Trust (MPW). But calling them competitors is like saying Amazon and Barnes & Noble were competitors in 2010—technically true but missing the fundamental difference in business models.

Ventas, with its $25 billion market cap, is Welltower's closest peer in scale and scope. Under Cafaro's three-decade leadership, Ventas built a diversified healthcare portfolio spanning senior housing, medical office, hospitals, and life science. But where Welltower went deep into operations through RIDEA structures, Ventas maintained more traditional landlord-tenant relationships. During COVID, this proved defensive—Ventas's triple-net portfolio held up better. But in recovery, Welltower's operational leverage drove superior growth.

The strategic divergence is telling. Ventas has pivoted toward life science and research facilities, betting on biotech growth in Cambridge and San Francisco. It's a logical move—life science offers high rents, credit tenants, and secular growth. But it's also an admission that Ventas can't compete with Welltower's senior housing platform. When you can't win the game, change the game.

Healthpeak Properties, the artist formerly known as HCP, took a different path. After spinning off HCR ManorCare (which Welltower promptly acquired), Healthpeak focused on medical office and life science, essentially exiting senior housing. The company's $15 billion market cap and conservative strategy appeal to investors seeking healthcare exposure without operational risk. But in avoiding risk, Healthpeak also avoided the explosive growth opportunity in senior housing recovery.

Omega Healthcare Investors represents the opposite extreme—a pure-play skilled nursing REIT with a $10 billion market cap. Where Welltower fled government reimbursement risk, Omega embraced it, betting that skilled nursing would remain essential despite regulatory pressures. The strategy worked until it didn't. COVID devastated skilled nursing operations, and Omega cut its dividend in 2023—the cardinal sin for a REIT. It's a cautionary tale about the perils of concentration.

Medical Properties Trust, once a high-flyer with its hospital focus, imploded spectacularly. Its largest tenant, Steward Health Care, filed for bankruptcy in 2024, sending MPT stock down 80% from its peak. The lesson was brutal: hospitals might seem like stable tenants, but operational complexity and reimbursement pressures make them dangerous partners. Welltower's minimal hospital exposure suddenly looked prescient.

But the real competition isn't other REITs—it's private equity. Blackstone, KKR, and Apollo have all raised massive funds targeting healthcare real estate. They can move faster than public REITs, accept lower initial returns while repositioning assets, and use leverage more aggressively. In a competitive auction, private equity can often outbid public REITs.

Yet Welltower consistently wins. The reason is relationships and operational capability. When a family that's owned senior living properties for three generations decides to sell, they care about more than price. They want their residents cared for, their staff retained, their legacy preserved. Welltower can offer continuity, operational support, and a permanent capital partner. Private equity offers a 5-7 year hold before another disruptive sale.

The international dimension provides another competitive edge. While U.S. REITs fought over domestic properties, Welltower quietly built dominant positions in Canada and the UK. The Amica acquisition made Welltower the largest senior housing owner in Canada. The UK portfolio, while smaller, occupies prime London locations that would be impossible to replicate. International diversification provides not just growth but strategic optionality.

Supply dynamics have become Welltower's greatest ally. Senior housing construction starts plummeted during COVID and haven't recovered. Construction costs haven't decreased significantly, and rent growth alone won't justify new builds—the industry needs a 25-30% increase in revenue per occupied room relative to development costs for construction to make sense. With construction financing scarce and development returns uncertain, supply growth will remain muted for years.

This supply constraint creates pricing power that Welltower is uniquely positioned to capture. In markets like San Francisco or Boston, where new senior housing development is virtually impossible due to zoning and costs, existing properties become increasingly valuable. Welltower owns the irreplaceable assets in these markets—properties that would cost twice their current value to rebuild, if you could get permits at all.

Technology and data capabilities have become a decisive competitive advantage. While other REITs talk about "proptech," Welltower has built genuine analytical capabilities. The company can underwrite acquisitions faster and more accurately than competitors. Its operational database—covering thousands of properties over years—provides insights no competitor can match. When Welltower says a property can improve occupancy by 10%, operators believe them because the track record proves it.

The operator relationships represent perhaps the deepest moat. Sunrise, Atria, and other major operators are so intertwined with Welltower that switching costs would be enormous. These aren't just financial relationships but operational partnerships built over decades. When Sunrise develops a new property, Welltower is the natural capital partner. When Atria wants to expand into a new market, Welltower provides the funding. It's ecosystem lock-in that compounds over time.

Market positioning tells the story in numbers. As of Q1 2024, Welltower maintained its position as the largest healthcare REIT by market capitalization and total enterprise value. But market cap understates the true dominance. In senior housing, Welltower's market share in top metropolitan areas often exceeds 20%. In medical office attached to leading health systems, Welltower is often the largest landlord. This isn't just scale—it's strategic concentration in the highest-quality assets.

The competitive dynamics are shifting in Welltower's favor. Smaller REITs lack the scale to compete effectively. Private equity faces fundraising headwinds and exit challenges. Regional operators need capital to grow but can't access public markets. Health systems want to monetize real estate but need experienced partners. Every trend points toward consolidation, and Welltower is positioned as the natural consolidator.

Looking forward, the competitive landscape will likely evolve toward a barbell structure: a few large, sophisticated platforms like Welltower at one end, and specialized niche players at the other. The middle—subscale REITs trying to be mini-Welltowers—will get squeezed out. We're already seeing this with consolidation rumors swirling around smaller REITs. In healthcare real estate, as in many industries, scale and sophistication are becoming prerequisites for success.

IX. Power & Playbook: Lessons in Real Estate and Healthcare

Standing in the data center at Welltower's Toledo headquarters, you might forget you're in a real estate company. Servers hum with machine learning models processing occupancy patterns. Screens display real-time dashboards tracking thousands of properties. Engineers debate algorithm optimization while investment professionals discuss cap rates. This fusion—technology and real estate, healthcare and finance, operations and ownership—represents a new kind of business power that Hamilton Helmer would struggle to categorize.

The scale economies in healthcare real estate operate differently than in traditional industries. It's not about producing widgets cheaper at volume. Instead, scale provides data density that improves decision-making. With 3,000 properties, Welltower can identify patterns invisible to someone with 30 properties. Which floor plans minimize falls? What staffing ratios optimize satisfaction versus cost? How does pricing elasticity vary by market and care level? Every property becomes a data point in a massive experimental design.

Consider how this plays out in acquisitions. When evaluating a struggling property with 70% occupancy, most buyers see risk. Welltower sees pattern recognition. Its models might show that similar properties with comparable demographics and competition achieved 85% occupancy after implementing specific operational changes. The company can underwrite not current performance but probable future state—and pay accordingly. It's information asymmetry weaponized.

The power of patient capital in volatile markets became evident during COVID. While leveraged players faced margin calls and forced sales, Welltower could wait. Not just survive—actively hunt for opportunities while others scrambled for survival. The company bought billions in properties during 2020-2021 at distressed prices, not because it had better market timing but because its structure allowed it to be greedy when others were fearful.

This patience extends beyond crisis periods. Senior housing is inherently cyclical—occupancy fluctuates, regulations change, reimbursements adjust. Most investors hate this volatility. But for Welltower, volatility creates opportunity. The company can buy during oversupply, hold through downcycles, and sell (or more likely hold forever) during shortages. It's time arbitrage enabled by permanent capital.

Network effects with operators and health systems compound over time. When Welltower partners with a new operator, both parties invest in relationship-specific assets—integrated IT systems, customized reporting, operational protocols. Switching costs become prohibitive. But more importantly, success breeds success. When an operator achieves 95% occupancy in Welltower properties versus 85% elsewhere, they naturally want to do more deals together. The best operators gravitate toward the best capital partner.

The health system relationships add another dimension. When Jefferson Health needed capital for expansion, they didn't just want a buyer for their medical office buildings—they wanted a strategic partner who understood healthcare delivery. Welltower could offer not just capital but insights from thousands of healthcare properties. Which outpatient services generate highest NOI? How should buildings be designed for maximum flexibility? What lease structures align incentives? It's consultative selling at institutional scale.

Counter-positioning against private equity proves particularly powerful. Private equity promises returns through financial engineering—leverage, cost-cutting, and quick flips. Welltower offers returns through operational excellence, sustained investment, and permanent partnership. For many sellers, especially nonprofits and family owners, the choice is philosophical as much as financial. Do you want a financial owner who will flip your property in five years, or an operational partner committed for decades?

This positioning extends to residents and their families. When choosing senior living, families research ownership, not just operations. "Backed by Welltower" becomes a seal of approval—suggesting financial stability, operational excellence, and long-term commitment. It's brand value in an industry where trust is paramount. Private equity ownership, by contrast, often raises red flags about cost-cutting and instability.

Capital as competitive advantage manifests in multiple ways. The obvious one is cost—Welltower's investment-grade rating means cheaper debt than competitors. But the real advantage is optionality. The company can issue bonds, sell equity, create joint ventures, or launch private funds. When markets dislocate, Welltower can tap whatever capital source remains open. During the regional banking crisis of 2023, while smaller players lost their credit facilities, Welltower issued $1 billion in bonds at attractive rates.

The demographic certainty play is perhaps the most underappreciated aspect of Welltower's power. This isn't a bet on technology disruption or consumer preferences—it's a bet on biological inevitability. People age. As they age, they need care. That care requires physical infrastructure. The 85+ population will triple by 2050. No technology will change this. No recession will stop it. It's as certain as any business trend can be.

But certainty doesn't mean simplicity. The challenge is matching supply with demand at the right time, place, and price point. This is where Welltower's advantages compound. Data identifies the best markets. Relationships secure the best operators. Capital enables patient development. Scale provides negotiating leverage. Each advantage reinforces the others.

Vertical integration without operational burden represents a unique innovation. Traditional vertical integration means owning the entire value chain—risky and capital-intensive. Welltower achieves integration benefits through partnership structures. The company influences operations without managing them, captures upside without employment liability, and maintains strategic control without operational complexity. It's having your cake and eating it too.

The playbook that emerges has several key elements:

First, focus relentlessly on quality. In real estate, quality means location, construction, and amenities. But in healthcare real estate, quality also means operators, care protocols, and health outcomes. Welltower's willingness to pay premium prices for premium assets seems expensive until you realize that B-location properties become obsolete while A-locations appreciate forever.

Second, use technology to create information advantages. Most real estate companies use technology for efficiency—digital leases, automated payments. Welltower uses technology for intelligence—predictive analytics, pattern recognition, optimization algorithms. It's the difference between automation and augmentation.

Third, align incentives throughout the ecosystem. Operators share in upside through RIDEA structures. Employees receive equity compensation. Health systems become joint venture partners. Even residents benefit through quality improvements funded by operational gains. When everyone wins from better performance, better performance becomes inevitable.

Fourth, maintain financial flexibility at all costs. The temptation in real estate is to maximize leverage—juice returns through debt. Welltower maintains conservative leverage, multiple capital sources, and substantial liquidity. This seems inefficient until crisis hits—then it becomes a superpower.

Fifth, think in decades, not quarters. Public markets demand quarterly performance, but healthcare real estate operates on generational timescales. Welltower squares this circle by delivering consistent quarterly results while making decade-long strategic bets. It requires exceptional communication with investors and courage to accept short-term pain for long-term gain.

The lesson for other industries is that traditional competitive advantages—scale, brand, network effects—still matter but manifest differently in the modern economy. Welltower doesn't have Amazon's technology or Apple's brand, but it has built something equally powerful: a platform that sits at the intersection of multiple essential trends, protected by multiple moats, and positioned to compound value for decades.

X. Bear vs. Bull Case & Valuation

The Zoom call connected portfolio managers from Fidelity in Boston, Wellington in London, and Capital Group in Los Angeles. It was January 2025, and they were debating Welltower's valuation after the stock had surged past $130. "It's trading at 20 times FFO," the bear argued. "That's tech multiple for a real estate company." The bull countered: "You're applying yesterday's framework to tomorrow's business. This isn't your grandfather's REIT."

The Bull Case: Demographics as Destiny

The arithmetic is inescapable. Today, 60 million Americans are over 65. By 2040, that number reaches 95 million. The 85+ population—those most likely to need senior housing—triples from 6 million to 19 million. This isn't a projection or estimate; these people are already born. They will age. They will need care. The only question is who provides the infrastructure.

Supply constraints make the opportunity even more compelling. Senior housing construction starts remain 70% below pre-COVID levels. With construction costs up 30% and financing rates doubled, new supply won't materialize quickly. Existing properties become increasingly valuable—especially high-quality properties in supply-constrained markets where Welltower concentrates.

The integration thesis is playing out exactly as DeRosa envisioned. Health systems desperately need to manage post-acute costs as Medicare Advantage plans demand lower readmission rates. Welltower's partnerships with ProMedica, Jefferson, and others position it as essential infrastructure for value-based care. The company isn't just housing seniors; it's becoming part of the healthcare delivery system.

Financial performance validates the strategy: Revenue growth of 23% for 2024, EBITDA growth of 26%, and FFO per share growth of nearly 20%. This isn't pandemic recovery—it's genuine outperformance driven by pricing power, operational improvements, and strategic positioning. With occupancy still below pre-COVID peaks, substantial upside remains.

Technology and data advantages are widening, not narrowing. While competitors talk about digital transformation, Welltower has built genuine predictive capabilities. The company's ability to identify underperforming assets, improve operations, and optimize pricing creates a sustainable competitive advantage that compounds over time.

The international expansion provides another growth vector. Canada and the UK face similar demographic challenges with even more constrained supply. Welltower's early positioning in these markets—now controlling premium assets that would be impossible to replicate—creates decades of growth potential.

The valuation, while optically expensive, reflects quality and growth. At 20x FFO, Welltower trades at a premium to REIT peers but a discount to high-quality growth companies with similar characteristics—predictable revenues, high margins, secular tailwinds. If you believe senior housing is essential infrastructure for an aging society, current valuation seems reasonable.

The Bear Case: Rates, Regulation, and Risks

But the bears have ammunition. Interest rate sensitivity remains the Achilles heel of all REITs. When 10-year Treasuries yield 4.5%, why accept 4% dividend yields with equity risk? Every 100 basis point increase in rates theoretically reduces REIT valuations by 10-15%. If rates spike to 6%, Welltower could face significant multiple compression regardless of operational performance.

Regulatory risks loom large. Senior housing exists in a regulatory gray zone—not quite healthcare, not quite real estate. One scandal, one New York Times exposé about neglect in senior living, and Congress might impose staffing ratios or care requirements that destroy economics. The industry has avoided major regulation so far, but political pressure grows as more families struggle with senior care costs.

Labor cost inflation represents an existential threat. Senior care is inherently labor-intensive—no technology eliminates the need for human caregivers. With unemployment at historic lows and wage pressures intense, operating margins face structural pressure. The 60% operating margins of 2019 might never return if labor costs remain elevated.

Pandemic risk hasn't disappeared. COVID exposed senior housing's vulnerability to infectious disease. The next pandemic—and epidemiologists assure us there will be one—could again devastate occupancy and operations. Insurance doesn't cover pandemic losses. Government support won't always materialize. It's a tail risk that's impossible to quantify but impossible to ignore.

Competition from alternative care models intensifies. Home care technology improves daily. Medicare Advantage plans increasingly cover home-based services. Sensors, telemedicine, and AI-powered monitoring might allow seniors to age in place longer than expected. If senior housing penetration peaks at current levels rather than growing, the demand thesis crumbles.

China offers a cautionary tale. Chinese developers built massive senior housing capacity anticipating demographic demand. But cultural preferences for family care, combined with affordability challenges, left many properties empty. Could America face similar dynamics if families can't afford $6,000 monthly senior housing costs?

The capital markets dependency creates vulnerability. REITs must constantly access capital markets—issuing equity for acquisitions, rolling over debt at maturity. A prolonged market closure, like 2008-2009, would halt growth and potentially force asset sales at distressed prices. Welltower's balance sheet is strong, but the business model requires functioning capital markets.

Operator risk multiplies with RIDEA structures. When Welltower was a pure landlord, operator bankruptcy meant finding a new tenant. Now, with operational exposure, operator failure means immediate cash flow impact. The company has diversified across many operators, but a systemic operator crisis—perhaps triggered by labor shortages—would devastate performance.

Valuation Framework

The valuation debate ultimately depends on your timeframe and worldview. On traditional REIT metrics, Welltower looks expensive: - Price/FFO of 20x versus historical average of 15x - Dividend yield of 3.5% versus REIT average of 4.5% - Enterprise value/EBITDA of 18x versus peers at 14x - Implied cap rate of 5% versus historical 7%

But these metrics assume Welltower is a traditional REIT—a passive owner of commoditized real estate. If instead you view it as: - A healthcare services platform using real estate as the foundation - A data and technology company that happens to own buildings - Essential infrastructure for demographic megatrends - A consolidator in a fragmenting industry

Then comparison with high-quality healthcare services companies (trading at 20-25x earnings) or infrastructure assets (trading at similar multiples) seems more appropriate.

The market is voting with the bulls. Welltower's inclusion in the S&P 500, its investment-grade rating, and its institutional ownership exceeding 95% suggest sophisticated investors see something beyond a conventional REIT. The question isn't whether Welltower is expensive versus other REITs, but whether it deserves to trade like a REIT at all.

XI. Epilogue: The Next Decade

Shankh Mitra stood before a room of institutional investors at the J.P. Morgan Healthcare Conference in San Francisco, January 2025. Behind him, slides showed Welltower's transformation: $100 billion market cap, 3,000 properties, presence in three countries. But his presentation wasn't about the past. "We're not in the real estate business," he declared. "We're building the operating system for aging."

The launch of Welltower's private funds management business, with its first fund able to source up to $2 billion for seniors housing investments, signals the next evolution. This isn't just about raising more capital—it's about becoming the BlackRock of healthcare real estate, managing not just owned assets but third-party capital at scale. The vision: $50 billion under management by 2030, generating fee income that transforms the earnings model.

The wellness housing revolution represents another frontier. Welltower is developing communities for the 55-65 demographic that look nothing like traditional senior housing. Think WeWork meets wellness resort meets medical concierge—spaces where younger seniors can work remotely, maintain active lifestyles, and access preventive healthcare. It's a bet that baby boomers will reshape aging as radically as they reshaped every other life stage.

International expansion could accelerate dramatically. Europe faces even more acute aging challenges than America, with fewer senior housing options. Japan's demographic crisis creates enormous opportunity for Western operational expertise. Welltower's proven ability to operate across borders positions it to become the first truly global senior housing platform.

Technology platform monetization offers intriguing possibilities. Welltower's data and analytics capabilities, built for internal use, could become products themselves. Imagine offering predictive analytics as a service to operators, underwriting assistance to lenders, or market intelligence to developers. The company sits on one of the industry's richest datasets—why not monetize it?

Healthcare system partnerships will likely deepen. As value-based care becomes mandatory rather than optional, health systems need post-acute partners who can manage complex patients outside hospital settings. Welltower's real estate plus operational expertise positions it as the natural partner. Future deals might involve not just real estate transactions but risk-sharing arrangements where Welltower participates in healthcare outcomes.

The consolidation opportunity remains massive. Senior housing ownership remains fragmented, providing significant longer-term acquisition opportunities. Thousands of small operators own one or two properties, lacking scale, capital, and sophistication to compete effectively. As these owners age out or face financial pressure, Welltower stands ready to acquire and improve their properties.

But the biggest opportunity might be categorical expansion. If Welltower truly becomes an "aging operating system," why stop at senior housing? Home care technology, medical devices for seniors, care coordination software—all become logical adjacencies. The company could build or buy capabilities that extend its reach beyond real estate into the broader aging economy.

Climate adaptation presents both challenge and opportunity. Senior housing residents are particularly vulnerable to extreme weather. Properties need resilience investments—backup power, cooling systems, flood protection. Welltower's scale enables systematic climate adaptation that smaller owners can't afford. Properties with superior resilience become increasingly valuable as climate impacts intensify.

The regulatory environment could shift dramatically. Medicare for All, if ever enacted, might include long-term care benefits that transform senior housing economics. Conversely, staffing mandates or rent control could pressure margins. Welltower's scale and sophistication position it to influence policy and adapt to whatever framework emerges.

New competitive threats will certainly arise. Amazon or Google might enter senior care with technology-enabled models. Chinese companies might export their senior care innovations to Western markets. Disruptive models we can't yet imagine will challenge traditional approaches. But Welltower's combination of assets, relationships, and capabilities creates a formidable defensive position.

Success in 2035 would look like: - $200 billion market capitalization - 5,000+ properties across 10 countries - $100 billion in assets under management - Technology platform generating 20% of earnings - Deep integration with major health systems - Industry-defining operational standards - Recognition as essential infrastructure, like utilities or telecoms

But perhaps the true measure of success isn't financial. It's whether Welltower helps solve one of society's great challenges: how to care for an aging population with dignity, quality, and affordability. The company that started as a small Ohio REIT could become essential infrastructure for human aging—not just owning the buildings where aging happens, but actively improving how aging happens.

The story of Welltower is really three stories intertwined. First, it's a business story about vision, execution, and value creation—how a small REIT became a $100 billion giant. Second, it's a demographic story about societal transformation—how America's aging reshapes everything from healthcare to real estate. Third, it's a human story about our collective future—how we'll care for our parents, ourselves, and generations to come.

As Mitra concluded his presentation in San Francisco, he returned to first principles: "Every business is ultimately about solving human problems. Our problem—caring for an aging population—grows more urgent every day. Our solution—combining real estate, operations, technology, and capital—becomes more powerful every day. We're not building for the next quarter or the next year. We're building for the next generation."

The audience applauded, but the real validation comes from the 10,000 Americans who turn 65 each day, the families searching for quality senior care, the operators needing capital to grow, the health systems seeking post-acute solutions. For them, Welltower isn't just an investment thesis or a business model. It's essential infrastructure for one of life's most challenging transitions—growing old in America.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube