Ventas: The Healthcare REIT That Defied Death and Defined an Industry

I. Introduction & Episode Teaser

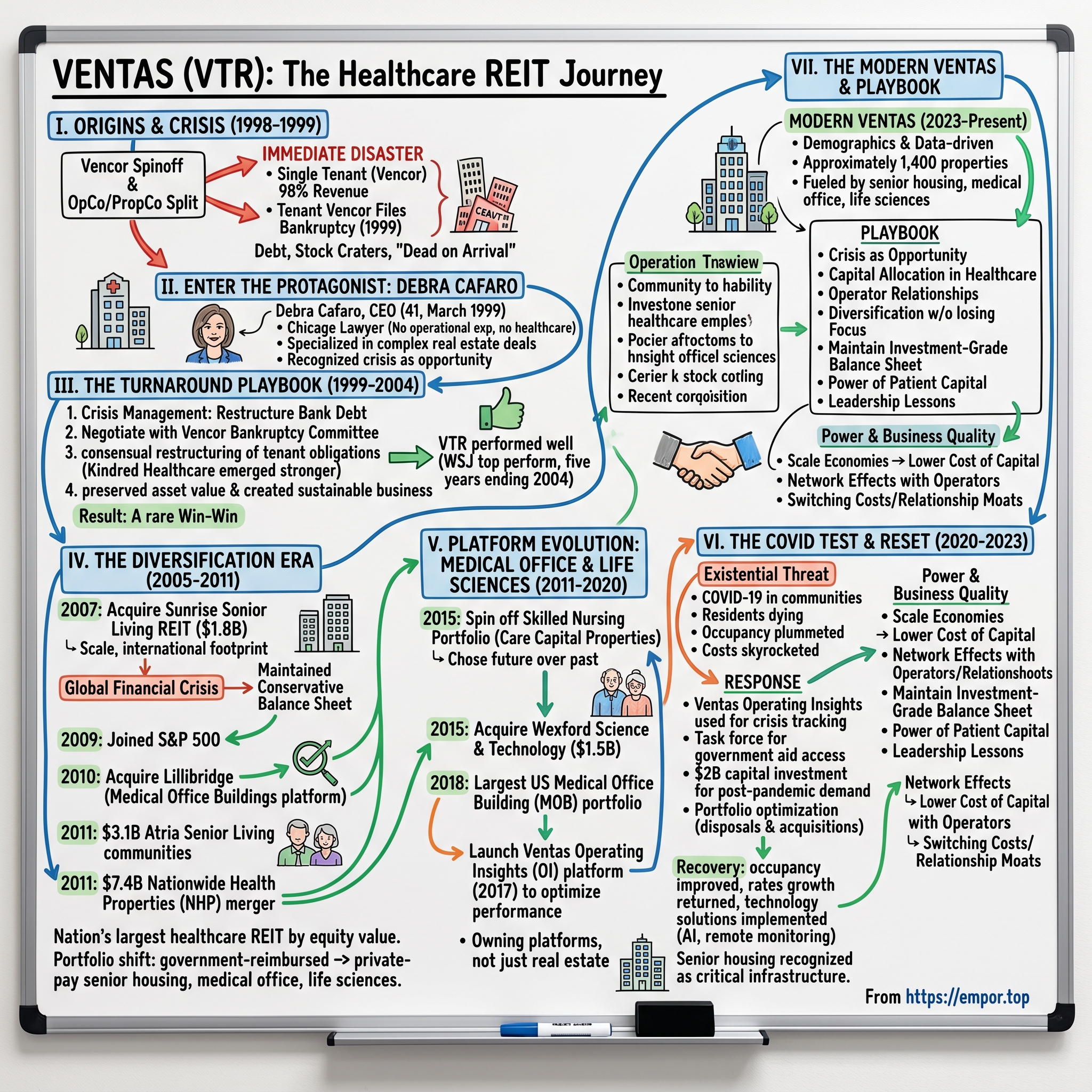

The conference room at 353 North Clark Street in Chicago was silent except for the hum of fluorescent lights. It was March 1999, and the lawyers around the table were doing what lawyers do best—documenting disaster. Ventas, barely a year old, was worth roughly $200 million in equity value, though even that seemed generous given the circumstances. The company's sole significant tenant, representing 98% of revenue, had just filed for bankruptcy protection. The banks were circling. Board members were exchanging glances that said what no one wanted to voice: this company was dead on arrival.

Twenty-five years later, that same company commands a market capitalization exceeding $30 billion, owns approximately 1,400 properties across three countries, and stands as one of the S&P 500's most remarkable turnaround stories. The transformation from near-death to healthcare real estate titan wasn't just about financial engineering or lucky timing—it was about recognizing that crisis creates opportunity, that healthcare real estate would become essential infrastructure, and that sometimes the best person to save a company is someone who's never worked in the industry before. As of August 2025, Ventas commands a market capitalization of $31.1 billion, a figure that seemed unimaginable to those lawyers in that Chicago conference room a quarter-century ago. The question isn't whether this transformation happened—the numbers speak for themselves. The question is how a company with no operating history, no management team, and essentially no tenant diversification became one of the most successful healthcare REITs in history.

This is the story of Ventas—a company that turned existential crisis into competitive advantage, transformed healthcare real estate from a niche asset class into essential infrastructure, and proved that sometimes the best qualification for running a specialized business is having no preconceptions about how it should be run. It's about Debra Cafaro, who became CEO at age 41 with zero healthcare experience and proceeded to deliver one of the greatest turnarounds in REIT history. And it's about understanding why, in an aging society, owning the real estate where healthcare happens might be one of the most important businesses of the 21st century.

The numbers tell part of the story: from near-bankruptcy to S&P 500 inclusion in just over a decade, from one problem tenant to approximately 1,400 properties across three countries, from survival mode to normalized FFO per share of $0.87 in Q2 2025. But the real story—the Acquired-style story—is about recognizing inflection points before they're obvious, building competitive moats in unexpected places, and understanding that in business, as in life, the biggest opportunities often come disguised as disasters.

II. Origins: The Vencor Spinoff & Immediate Crisis (1998-1999)

To understand Ventas, you first need to understand the healthcare industry's seismic shift in the late 1990s. Picture the American healthcare landscape in 1997: Medicare spending was spiraling out of control, skilled nursing facilities were printing money on government reimbursements, and healthcare REITs were Wall Street's darlings. Then Congress dropped a bomb called the Balanced Budget Act of 1997.

The Act slashed Medicare reimbursements to skilled nursing facilities by billions. What had been a goldmine suddenly became a minefield. Healthcare operators across the country began hemorrhaging cash. Among them was Vencor, Inc., one of the nation's largest long-term acute care hospital companies, founded by Kentucky entrepreneur Bruce Lunsford.

Lunsford had built Vencor into a healthcare giant through aggressive acquisition and a focus on high-acuity care. By 1998, the company operated hundreds of facilities nationwide. But the Balanced Budget Act hit Vencor like a sledgehammer. The company needed to restructure, and fast. The solution? Spin off the real estate into a separate REIT—a common financial engineering move that would theoretically unlock value and provide liquidity.

Thus, Ventas was born in 1998, not as a strategic vision but as a financial necessity. The spinoff was structured as a classic OpCo/PropCo split: Vencor would continue operating the facilities while Ventas would own the real estate and collect rent. Simple, clean, theoretically foolproof.

Except it wasn't.

The new REIT launched with a portfolio consisting almost entirely of skilled nursing and long-term acute care facilities—the exact properties getting crushed by Medicare cuts. Worse, it had devastating concentration risk: Vencor, its former parent, represented 98% of revenues. Ventas was less a diversified REIT than a single-tenant landlord with a tenant in critical condition.

Think about the absurdity of the situation: Ventas was created to help Vencor survive, but its own survival depended entirely on Vencor's health. It was like performing surgery to separate conjoined twins, only to discover they still shared the same heart.

The arrangement lasted less than a year. In September 1999, Vencor filed for Chapter 11 bankruptcy protection, one of the largest healthcare bankruptcies in U.S. history at the time. Overnight, Ventas went from being a newly minted REIT to a company whose sole major tenant couldn't pay rent. The stock price cratered. Credit facilities were in jeopardy. Board members were calling emergency meetings.

Most REITs in this situation would have followed their tenant into bankruptcy or been acquired for pennies on the dollar. The skilled nursing sector was radioactive—nobody wanted to touch these assets. The conventional wisdom was clear: healthcare real estate was too risky, government reimbursement too unpredictable, operator quality too variable.

But here's where the story takes an unexpected turn. The Ventas board didn't look for a healthcare executive to save the company. They didn't seek out a REIT veteran or a turnaround specialist from the industry. Instead, they made a call that would reshape not just Ventas but the entire healthcare REIT sector: they called a lawyer in Chicago who had never run a public company, never worked in healthcare, and never managed real estate.

They called Debra Cafaro.

III. Enter The Protagonist: Debra Cafaro's Recruitment

The phone rang in Debra Cafaro's Chicago office in early 1999. On the other end was Doug Crocker, a Ventas board member and one of her mentors from her days in real estate law. His pitch was straightforward and somewhat insane: "We need you to save this company."

Cafaro's journey to that phone call was anything but typical for a REIT CEO. Born in Pittsburgh to a working-class family, she was the daughter of a steel salesman and a homemaker. Her parents emphasized education as the path to opportunity—a classic American dream narrative that would prove more powerful than anyone imagined. She excelled academically, earning her undergraduate degree from Notre Dame before heading to the University of Chicago Law School, one of the nation's most rigorous legal programs.

For thirteen years, Cafaro had built a successful career as a real estate attorney, first at Barack Ferrazzano Kirschbaum & Nagelberg, then as a partner at Katten Muchin Rosenman. She specialized in complex real estate transactions, becoming known for her ability to structure deals that others couldn't figure out. Her clients included major real estate players, and she had developed a reputation as someone who could see around corners in complicated negotiations.

But being a successful lawyer and running a public company on the brink of collapse are vastly different challenges. When Crocker called, Cafaro was 41 years old, comfortable in her legal career, with no operational experience and no healthcare background. Taking the Ventas job meant leaving the partnership track, moving from advisor to principal, from negotiating deals to being responsible for them.

"I was asked by one of my mentors who was on the board at that time to join the company as its CEO to try to turn things around and save it," Cafaro would later recall. The understatement masks what must have been an agonizing decision. This wasn't joining a struggling company with upside potential—this was walking into a burning building while everyone else was running out.

Yet something about the challenge appealed to her. Perhaps it was the intellectual puzzle of it all—how do you save a company when its only tenant is bankrupt? Maybe it was the opportunity to prove that legal training, with its emphasis on structure, negotiation, and risk assessment, could translate to business leadership. Or possibly she saw what others missed: that existential challenges create opportunities for fundamental transformation.

Cafaro's working-class Pittsburgh roots mattered here. She understood what it meant to fight for everything, to not have a safety net, to bet on yourself when the odds were long. The steel industry had collapsed in Pittsburgh during her youth—she had seen entire communities wrestle with economic disruption. This wasn't her first encounter with institutional failure and the need for reinvention.

When she accepted the position in March 1999, becoming Ventas's President and CEO, the market's reaction was swift and skeptical. Who was this lawyer with no healthcare experience? How could someone who had never run a public company navigate the largest healthcare bankruptcy in history? The stock price, already depressed, showed no signs of recovery.

What the skeptics missed was that Cafaro brought exactly what Ventas needed at that moment. She didn't have preconceptions about how healthcare real estate "should" work. She wasn't wedded to industry conventional wisdom that was clearly failing. And most importantly, her legal training had taught her to think structurally about problems—to understand that sometimes the solution isn't fighting harder within the existing framework but changing the framework itself.

Her first day on the job, Cafaro walked into Ventas's sparse offices—the company had virtually no infrastructure, no management team, and no clear path forward. She had inherited a company with one major tenant in bankruptcy, banks threatening to call loans, and a board hoping for a miracle.

She would later describe her initial strategic thinking with characteristic clarity: "We had to preserve the value of the assets while restructuring the tenant's obligations. It wasn't about whether Vencor would pay rent—it was about creating a structure where they could pay rent and emerge stronger."

This wasn't the language of a traditional REIT executive focused on FFO and occupancy rates. This was the language of a deal lawyer who understood that in crisis, everything is negotiable, and the only thing that matters is finding a structure that lets all parties survive to fight another day.

IV. The Turnaround Playbook: Saving Ventas (1999-2004)

Cafaro's first hundred days as CEO read like a business school case study in crisis management, except no business school would recommend what she did. Instead of cutting costs and selling assets—the typical distressed company playbook—she went on offense, treating Vencor's bankruptcy not as a death sentence but as an opportunity to restructure the entire relationship.

The conventional approach would have been to play hardball: demand full rent payment, threaten eviction, and squeeze every dollar possible from the bankrupt tenant. That's what the lawyers recommended. That's what the banks expected. But Cafaro understood something crucial: dead tenants don't pay rent. Her goal wasn't to win a legal battle but to create a sustainable business.

"Her initial actions at Ventas were to restructure the bank debt and lead a global consensual restructuring of its main tenant, Vencor, so Vencor could emerge from bankruptcy," the company would later document. But this clinical description understates the complexity and audacity of what she accomplished.

First, she had to keep the banks at bay. Ventas's credit facilities had covenants that were about to be breached. Rather than wait for the inevitable default, Cafaro went directly to the lenders with a proposal: give us time to restructure Vencor's lease, and you'll get a stronger credit with better coverage. It was a negotiation she had to win—without bank support, Ventas was dead.

Simultaneously, she entered negotiations with Vencor's bankruptcy committee. Her proposition was counterintuitive: instead of trying to maintain the existing lease terms, she would accept lower rent in exchange for a structure that would allow Vencor (soon to be renamed Kindred Healthcare) to emerge from bankruptcy as a viable operator. The key insight: a healthy tenant paying sustainable rent was worth more than a dying tenant with unsustainable obligations.

The restructuring took months of around-the-clock negotiations. Cafaro personally led every major session, drawing on her legal background to navigate the Byzantine complexity of bankruptcy law while keeping focused on the business objective. She had to balance the interests of Ventas shareholders, Vencor's creditors, the bankruptcy court, and her own lenders—all while having essentially no leverage except the threat of mutual destruction.

During this period, Cafaro was also building a company from scratch. Ventas had been created as a shell to hold real estate; it had no real management infrastructure. She recruited a CFO, a head of asset management, and a skeletal team to actually run the business. Every hire was a bet—who would join a company that might not exist in six months?

The breakthrough came in 2001 when Kindred Healthcare successfully emerged from bankruptcy with a restructured lease agreement with Ventas. The new structure was elegant in its simplicity: lower base rent but with percentage rent tied to Kindred's performance, aligning interests and creating upside for both parties. Cafaro had engineered something rare in distressed situations—a true win-win.

But saving the company was just the first act. Cafaro's ambition extended far beyond survival. She recognized that Ventas's near-death experience had actually created an opportunity. The healthcare real estate sector was in chaos. Properties were trading at distressed prices. Many investors had sworn off healthcare real estate entirely. For someone with capital and courage, it was a generational buying opportunity.

Between 2001 and 2004, Cafaro began carefully acquiring properties, focusing initially on senior housing—a sector with better demographics and less government reimbursement risk than skilled nursing. Each acquisition was small, surgical, designed to reduce concentration risk while building expertise in new property types. She wasn't trying to build an empire overnight; she was laying the foundation for one.

The results spoke for themselves. According to The Wall Street Journal, Ventas was the ninth best performing publicly-traded company over the five-year period ending December 31, 2004. From the brink of bankruptcy to one of the market's top performers—it was a transformation that defied every expectation.

The strategic decision to stay in healthcare real estate, rather than diversifying into other property types, proved crucial. While others fled the sector, Cafaro saw its essential nature: people would always need healthcare, the population was aging, and healthcare delivery would increasingly move to outpatient settings. These weren't controversial insights, but acting on them while the sector was radioactive required conviction that few possessed.

By 2004, Ventas had stabilized its balance sheet, diversified its tenant base, and begun building what would become one of the premier healthcare real estate portfolios in the world. The company that almost died in 1999 was now positioned to thrive. The turnaround was complete. The growth story was just beginning.

V. The Diversification Era: Building Beyond Skilled Nursing (2005-2011)

The Ventas that entered 2005 bore little resemblance to the distressed spinoff of 1998. With a stabilized balance sheet and growing credibility in the capital markets, Cafaro faced a new challenge: how to build a scaled, diversified healthcare REIT that could weather any storm. Her answer would reshape not just Ventas but the entire healthcare REIT sector.

The first major move came in 2007 with the acquisition of Sunrise Senior Living REIT for $1.8 billion. This wasn't just another acquisition—it was a statement of intent. Sunrise gave Ventas instant scale in private-pay senior housing, premier properties in top markets, and crucially, its first international footprint with assets in Canada. The deal doubled Ventas's size overnight and shifted its center of gravity from government-reimbursed skilled nursing to private-pay senior housing.

But the Sunrise acquisition's timing seemed catastrophic. Within months of closing, Lehman Brothers collapsed, credit markets froze, and the global financial crisis threatened to undo everything Cafaro had built. Healthcare REITs were particularly vulnerable—they needed constant access to capital to grow, and suddenly capital was unavailable at any price.

Yet Cafaro's defensive positioning paid off brilliantly. While competitors struggled with excessive leverage and development commitments, Ventas had maintained a conservative balance sheet. Instead of playing defense during the crisis, Cafaro went shopping. As she would later explain, "Chaos creates opportunity for those who are prepared."

Throughout the financial crisis they managed to grow their staff, and by 2009 they had joined the S&P 500—a remarkable achievement for a company that had nearly disappeared a decade earlier. S&P 500 inclusion wasn't just symbolic; it opened Ventas to index funds and institutional investors who couldn't or wouldn't invest in smaller REITs.

The post-crisis period from 2010-2011 would prove to be Cafaro's masterpiece of capital allocation. With competitors weakened and sellers desperate for liquidity, Ventas embarked on an acquisition spree that would define its modern portfolio:

In 2010, Ventas completed its acquisition of Lillibridge Healthcare Services, obtaining not just 95 medical office buildings but also Lillibridge's development and management platform. This wasn't just about buying properties—it was about acquiring capabilities. Lillibridge brought relationships with major health systems and expertise in developing and managing medical office buildings adjacent to hospitals. The purchase price wasn't disclosed, but the strategic value was immense.

The Lillibridge deal marked a crucial evolution in Cafaro's thinking. Rather than just owning real estate, Ventas would own operating platforms that could create value beyond simple rent collection. It was a move toward vertical integration that would become a hallmark of the Ventas model.

Then came 2011, Ventas's annus mirabilis. In May, the company completed its $3.1 billion acquisition of 118 private-pay senior housing communities from Atria Senior Living Group. The Atria portfolio was trophy quality—large, purpose-built communities in affluent markets with strong demographics. These weren't your grandmother's nursing homes but rather resort-style communities for affluent seniors who could pay $5,000-$10,000 per month out of pocket.

But Cafaro wasn't done. In July 2011, Ventas announced its biggest deal yet: the $7.4 billion acquisition of Nationwide Health Properties (NHP) in an all-stock transaction. NHP was a publicly-traded healthcare REIT with a complementary portfolio of senior housing and medical office buildings. The merger created the nation's largest healthcare REIT by equity value, finally giving Ventas the scale to compete with anyone.

The NHP acquisition was particularly elegant in its structure. By using stock rather than cash, Cafaro maintained balance sheet flexibility while giving NHP shareholders upside in the combined company. The deal was immediately accretive to FFO, rare for a merger of equals, demonstrating the power of Ventas's lower cost of capital and superior operating platform.

The strategic shift from government reimbursement to private pay wasn't just about risk reduction—it was about recognizing a fundamental demographic truth. The baby boomers were aging, they were wealthier than any generation in history, and they would demand higher-quality senior housing than previous generations. Government reimbursement would always be subject to political pressure, but affluent seniors paying out of pocket represented a stable, growing revenue stream.

By the end of 2011, Ventas owned over 1,300 properties across 47 states and two Canadian provinces. The company that had started with complete tenant concentration now had over 400 tenants. The portfolio that had been entirely skilled nursing now included senior housing, medical office buildings, hospitals, and life science facilities. Annual revenues exceeded $2 billion.

The transformation was complete, but Cafaro wasn't satisfied with building just another large REIT. She wanted to build something different—a healthcare real estate platform that could create value through operations, not just ownership. That vision would drive the next phase of Ventas's evolution.

VI. The Platform Evolution: Medical Office & Life Sciences (2011-2020)

Standing before investors at the 2015 J.P. Morgan Healthcare Conference, Cafaro unveiled a vision that surprised even longtime Ventas watchers. The company would spin off its skilled nursing portfolio—the very assets that had birthed Ventas—and double down on medical office buildings and, remarkably, life science real estate. It was as if McDonald's had announced it was exiting hamburgers to focus on salads and sushi.

The spin-off of Care Capital Properties (CCP) in August 2015, containing 355 skilled nursing facilities, was more than portfolio optimization—it was an acknowledgment that healthcare real estate had fundamentally bifurcated. On one side: government-reimbursed, operationally intensive skilled nursing with declining margins. On the other: private-pay senior housing, medical office buildings, and life science facilities with growing demand and expanding margins. Cafaro chose the future over the past.

The $1.5 billion acquisition of Wexford Science & Technology that same year signaled Ventas's ambitions in research and innovation real estate. Wexford wasn't just a portfolio of buildings—it was a development platform specializing in creating innovation districts anchored by universities and medical centers. Properties like the Cambridge Innovation Center and research facilities at Johns Hopkins represented a new asset class for healthcare REITs: the physical infrastructure of medical innovation.

Why life sciences? Cafaro saw convergence everywhere she looked. Traditional boundaries between healthcare delivery, medical research, and technology development were dissolving. The same institutions that treated patients were developing new therapies. The medical office building next to a hospital might house both physician practices and clinical research organizations. By owning the real estate across this continuum, Ventas could capture value from healthcare's entire innovation ecosystem.

The medical office building (MOB) strategy was equally sophisticated. By 2018, Ventas had assembled the largest MOB portfolio in the United States, with over 700 properties primarily located on or adjacent to hospital campuses. These weren't commodity office buildings—they were specialized facilities with procedure rooms, imaging equipment, and infrastructure designed for healthcare delivery.

The MOB thesis rested on a powerful trend: the migration of healthcare from inpatient to outpatient settings. Procedures that once required hospital stays were moving to ambulatory surgery centers. Diagnostic imaging was shifting from hospitals to medical office buildings. Each migration created demand for specialized real estate that Ventas was uniquely positioned to provide.

International expansion accelerated during this period. The 2015 acquisition of a £145 million portfolio in the United Kingdom wasn't just about geographic diversification—it was about accessing the NHS system and understanding how single-payer healthcare created different real estate dynamics. Canadian expansion continued with senior housing acquisitions in Toronto, Vancouver, and Montreal, markets with demographics similar to the U.S. but different regulatory frameworks.

But Cafaro's masterstroke during this period was building operating platforms rather than just acquiring properties. The Lillibridge platform for medical office development. The Wexford platform for life science. Operating partnerships with premier senior housing operators like Atria and Sunrise. Each platform created capabilities that went beyond traditional REIT ownership.

Consider the Ventas Operating Insights (OI) platform, launched in 2017. By aggregating operational data from hundreds of senior housing communities, Ventas could benchmark performance, identify best practices, and help operators improve margins. This wasn't just about collecting rent—it was about actively improving the performance of the underlying businesses. The data showed results: Ventas-owned communities consistently outperformed market averages in occupancy and rate growth.

The numbers validated the strategy. By 2019, Ventas's enterprise value exceeded $40 billion. The company had investment-grade ratings from all major agencies. The dividend had grown for 15 consecutive years. Total shareholder returns had outperformed both the S&P 500 and REIT indices over virtually every time period.

Then came 2020, and with it, a crisis that would make the 2008 financial crisis look manageable by comparison. COVID-19 didn't just threaten the economy—it threatened the very facilities Ventas owned. Senior housing communities became ground zero for the pandemic. Medical office buildings emptied as elective procedures were canceled. Even life science facilities faced disruption as researchers were sent home.

The pandemic would test every assumption about healthcare real estate. It would challenge Cafaro's leadership as nothing had before. And it would ultimately prove that the platform Ventas had built was more resilient than anyone imagined.

VII. The COVID Test & Senior Housing Reset (2020-2023)

The email arrived at 2:47 AM on March 15, 2020. A senior housing operator in Washington State reported its first COVID-19 death. Within hours, similar messages flooded in from across the portfolio. The pandemic hadn't just arrived at Ventas's doorstep—it had kicked down the door and taken up residence in their properties.

For a company that owned approximately 850 senior housing communities, COVID-19 represented an existential threat unlike anything in its history. These weren't abstract financial assets but communities housing society's most vulnerable citizens. The human toll was devastating: residents dying, families unable to visit, staff stretched beyond breaking points. The financial impact was equally severe: occupancy plummeted as move-ins stopped and move-outs accelerated, operating costs skyrocketed with PPE and testing requirements, and some operators simply couldn't pay rent.

Cafaro's response revealed the difference between a traditional REIT and the platform Ventas had become. Rather than simply demanding rent and letting operators figure it out, Ventas mobilized its entire organization to support properties through the crisis. The company's Ventas Operating Insights platform, originally designed for performance optimization, was repurposed for crisis management—tracking infection rates, PPE supplies, and staffing levels across the portfolio in real-time.

The numbers were brutal. Senior housing occupancy, which had been running in the high 80s pre-pandemic, fell to the mid-70s by late 2020. Some communities saw occupancy drop below 60%. The SHOP (Senior Housing Operating Portfolio) segment, which Ventas operated directly rather than through triple-net leases, saw NOI decline by over 30% year-over-year at the pandemic's worst point.

Government intervention provided some relief but came with complications. The CARES Act and subsequent stimulus programs offered funding for healthcare providers, but navigating the bureaucracy required expertise many operators lacked. Ventas created a task force to help operators access every available dollar of government support, from Provider Relief Funds to Paycheck Protection Program loans.

The operational challenges were staggering. Communities needed to create isolation wings for COVID-positive residents, implement testing protocols that didn't exist six months earlier, and maintain staffing when healthcare workers were leaving the industry in droves. Labor costs spiked as operators competed for a shrinking pool of workers. Some communities were paying $150 per hour for agency nurses who had been making $40 pre-pandemic.

Yet amid the chaos, Cafaro saw opportunity—not to profit from crisis but to fundamentally reset the senior housing sector for sustainable growth. The pandemic had accelerated trends that were already emerging: the need for larger units with better ventilation, technology integration for telehealth and family communication, and operating models that could handle surge capacity.

Ventas launched a $2 billion capital investment program focused on repositioning properties for post-pandemic demand. This wasn't cosmetic renovation but fundamental reimagination: converting semi-private rooms to private, adding HVAC systems with hospital-grade filtration, and creating flexible spaces that could serve as dining rooms in normal times and isolation units during health emergencies.

The company also accelerated portfolio optimization, selling older properties that would require excessive capital to meet new market standards while acquiring newer communities with modern infrastructure. Between 2020 and 2022, Ventas disposed of nearly $3 billion in non-core assets while investing $1.5 billion in strategic acquisitions and development.

The recovery, when it came, was neither smooth nor uniform. By mid-2021, vaccines had arrived and senior housing began seeing increased demand from need-driven residents—those requiring assistance with daily living who couldn't delay move-in indefinitely. But the discretionary market—healthier seniors choosing lifestyle communities—remained weak through 2022.

Labor challenges persisted even as occupancy recovered. The senior housing sector had lost approximately 200,000 workers during the pandemic, and many weren't coming back. Ventas worked with operators to implement technology solutions—from automated medication dispensing to AI-powered fall detection—that could maintain quality while reducing labor intensity.

By early 2023, green shoots were everywhere. Occupancy had recovered to the low 80s and was climbing steadily. Rate growth had returned as operators pushed through price increases to offset higher labor costs. New supply, which had been a concern pre-pandemic, had essentially stopped as developers couldn't secure construction financing.

The pandemic's most lasting impact might be on how society values senior housing. What had been seen as discretionary became understood as essential. Families who had tried to care for elderly parents at home during lockdowns gained new appreciation for professional senior care. The federal government, which had largely ignored senior housing in favor of hospitals, began recognizing these communities as critical healthcare infrastructure.

The company expects 12-16% same-store cash NOI growth for its senior housing segment in 2025, a remarkable recovery from pandemic lows. The portfolio that survived COVID-19 was stronger, more technology-enabled, and better positioned for demographic tailwinds than the one that entered it.

VIII. The Modern Ventas: Demographics & Data (2023-Present)

Walking through a Ventas-owned life science building in Cambridge, Massachusetts, in 2024, you'd be forgiven for thinking you'd entered a tech company rather than a real estate firm. Digital displays show real-time occupancy data, AI algorithms optimize HVAC systems for each lab's specific needs, and the Ventas team can tell you not just who the tenants are but what clinical trials they're running and when they might need expansion space. This is healthcare real estate reimagined as a technology-enabled platform business.

With approximately 1,400 properties in North America and the United Kingdom, Ventas occupies an essential role in the longevity economy. The Company's growth is fueled by its approximately 850 senior housing communities, but the modern Ventas is about much more than just owning buildings.

The longevity economy thesis that Cafaro has championed represents one of the most powerful demographic megatrends in human history. By 2030, all baby boomers will be over 65. The 85+ population, which requires the most intensive healthcare services, is projected to triple by 2050. Healthcare spending as a percentage of GDP continues its inexorable climb. These aren't projections that depend on economic growth or technological breakthroughs—they're demographic certainties.

Ventas aims to deliver outsized performance by leveraging its operational expertise, data-driven insights from its Ventas OI platform, extensive relationships and strong financial position. The Ventas OI platform has evolved from a crisis management tool to a competitive advantage. By aggregating operational data from hundreds of communities, Ventas can identify which operators outperform, what drives their success, and how to replicate best practices across the portfolio.

The data reveals insights that challenge conventional wisdom. Communities with higher programming budgets don't necessarily achieve better occupancy—it's the quality and personalization of activities that matter. Labor costs correlate less with retention than you'd expect—operators who invest in culture and training keep staff despite paying market rates. Small design changes—wider hallways, better lighting, more gathering spaces—can improve both resident satisfaction and operational efficiency.

This data-driven approach extends to capital allocation. Ventas now uses predictive analytics to identify which markets will see the strongest senior housing demand based on demographic shifts, wealth patterns, and healthcare infrastructure. The model suggested Charlotte, Nashville, and Raleigh would outperform in 2024-2025—markets where Ventas had already positioned significant assets.

The life science portfolio has evolved beyond traditional lab space to encompass the entire innovation ecosystem. Ventas properties house everything from early-stage biotech startups to established pharmaceutical companies' research centers. The company's proximity to leading academic medical centers creates a network effect—researchers want to be near other researchers, creating clusters of innovation that drive demand and rental growth.

Current portfolio composition reflects this strategic evolution. As of 2025, senior housing represents approximately 60% of net operating income, medical office buildings contribute 25%, and research/innovation facilities account for 15%. This mix provides both stability (medical office with long-term leases) and growth (senior housing with annual rate increases and life science with mark-to-market opportunities).

The technology initiatives go beyond data analytics. Ventas is piloting ambient sensors in senior housing communities that can detect changes in residents' movement patterns, potentially identifying health issues before they become critical. Virtual reality programs help residents with dementia access memories and reduce anxiety. Telehealth platforms integrated into communities reduced unnecessary hospital transfers by 30% in pilot programs.

But perhaps the most important innovation is in capital structure and partnerships. Ventas has created joint ventures with sovereign wealth funds seeking long-term, stable healthcare exposure. It's partnered with technology companies to pilot new care delivery models. It's even exploring partnerships with Medicare Advantage plans that see senior housing as a way to reduce costly hospital admissions.

The financial performance validates the strategy. Net debt-to-further adjusted EBITDA improved to 5.6X in Q2 2025, demonstrating disciplined balance sheet management despite aggressive growth investments. The dividend, that crucial REIT metric, has been restored to pre-pandemic levels and continues growing.

Looking forward, Ventas is positioned at the intersection of multiple megatrends: demographic aging, healthcare system evolution, technological transformation, and the growing recognition of social determinants of health. The company that nearly died from concentration risk now benefits from diversification across property types, operators, and geographies while maintaining focus on the singular theme of healthcare real estate.

IX. Playbook: The Ventas Operating System

If you wanted to teach a masterclass in crisis management and business transformation, you could do worse than studying the Ventas playbook. The principles that Cafaro developed through trial by fire have become a repeatable system for creating value in healthcare real estate—a system that works precisely because it was forged in crisis rather than comfort.

Crisis as Opportunity: The first principle seems counterintuitive: run toward crisis, not away from it. When Vencor went bankrupt, when the financial crisis hit, when COVID-19 arrived, Ventas didn't just survive—it used each crisis to fundamentally strengthen its position. The key insight: crisis creates price discovery failures. Assets that are fundamentally sound become temporarily mispriced because investors can't distinguish between temporary disruption and permanent impairment.

Consider the 2009-2011 acquisition spree. While competitors were selling assets to shore up balance sheets, Ventas was buying at generational lows. The properties didn't suddenly become better when the crisis ended—they were always valuable. But it took courage and capital to act when others were paralyzed by fear.

Capital Allocation in Healthcare Real Estate: Cafaro's approach to capital allocation breaks from traditional REIT orthodoxy. Rather than focusing solely on immediate FFO accretion, Ventas evaluates investments across multiple dimensions: demographic exposure, operator quality, market dynamics, and platform value. A property might be dilutive to near-term FFO but accretive to long-term value if it provides entry to a new market or relationship with a premier operator.

The decision to pay up for trophy assets in gateway markets exemplifies this thinking. Yes, cap rates are lower in Boston or San Francisco, but these markets have barriers to entry, sophisticated healthcare systems, and wealthy demographics that support premium pricing. The IRR on these investments might not pencil out in a simple model, but the strategic value—the option value of being in these markets—justifies the premium.

The Importance of Operator Relationships: In healthcare real estate, you're not just buying buildings—you're buying into operating businesses. Ventas learned this lesson early and hard with Vencor. The best real estate with a failing operator is worth less than average real estate with an excellent operator.

This recognition drives Ventas's unusual approach to tenant relations. Rather than maintaining arm's length landlord-tenant dynamics, Ventas actively partners with operators to improve performance. The company shares data, provides capital for value-add investments, and even helps operators access government programs. It's a level of engagement that requires more resources but generates superior returns through higher occupancy, stronger rate growth, and lower tenant turnover.

Diversification Without Losing Focus: Ventas owns senior housing, medical office buildings, life science facilities, and hospitals across three countries. That could be a recipe for complexity-driven destruction. But Cafaro maintains focus through a simple filter: every asset must be essential to healthcare delivery or innovation.

This isn't diversification for its own sake but rather recognition that healthcare is becoming more distributed and integrated. The same patient might receive primary care in a medical office building, surgery in an ambulatory center, rehabilitation in a senior housing community, and participate in a clinical trial at a research facility. By owning real estate across this continuum, Ventas captures value wherever healthcare happens.

Building and Maintaining an Investment-Grade Balance Sheet: This might seem like basic blocking and tackling, but in the REIT world, it's a superpower. REITs are essentially spread businesses—they borrow at one rate and invest at a higher rate. The lower your cost of capital, the more investments pencil out. The more investments pencil out, the faster you can grow. The faster you grow, the lower your cost of capital becomes. It's a virtuous cycle, but only if you maintain discipline.

Ventas targets net debt to EBITDA of 5-6x, fixed charge coverage above 3x, and maintains multiple sources of liquidity. These aren't aggressive metrics—they're conservative by REIT standards. But this conservatism becomes a weapon during disruption. When credit markets freeze, Ventas can still access capital. When others are selling, Ventas can buy.

The Power of Patient Capital in Volatile Sectors: Healthcare real estate doesn't move in smooth lines. Regulatory changes, reimbursement adjustments, and pandemic disruptions create volatility that can destroy leveraged players. Ventas's response: embrace the volatility but maintain the balance sheet flexibility to survive the downturns.

This patience extends to development and redevelopment. Ventas will hold land for years waiting for the right development opportunity. It will spend millions repositioning properties for future demand rather than current conditions. These investments might not make sense on a quarterly earnings call, but they create enormous value over decade-long horizons.

Leadership Lessons: As the longest-serving female CEO of an S&P 500 company, Cafaro's leadership style offers lessons beyond real estate. She combines lawyer-like attention to detail with entrepreneurial risk-taking. She maintains intellectual humility—admitting what she doesn't know and hiring experts who do—while displaying unwavering conviction in her strategic vision.

Perhaps most importantly, she understands that in a people business like healthcare, culture matters as much as capital. Ventas's ability to attract and retain talent, to maintain operator relationships through crisis, and to build trust with investors stems from a culture that values integrity over expedience and long-term value over short-term gains.

X. Power & Business Quality Analysis

Warren Buffett famously quipped that he likes businesses with moats so wide you need a boat to cross them. In Ventas's case, the moats aren't immediately obvious—after all, anyone with capital can buy healthcare real estate. But dig deeper, and you discover competitive advantages that compound over time, creating barriers that become more formidable rather than less.

Scale Economies in Healthcare Real Estate: At first glance, real estate seems like a business without scale advantages. Each property operates independently, and owning 1,000 buildings doesn't make the 1,001st cheaper to buy. But healthcare real estate is different. Scale creates advantages in financing (lower cost of capital), operations (shared best practices across properties), and relationships (becoming a must-have partner for premier operators).

Consider Ventas's cost of capital advantage. As of today, Ventas market cap is 30.81B, making it one of the largest healthcare REITs globally. This scale provides access to investment-grade bond markets, reduces financing costs by 100-200 basis points versus smaller competitors, and creates a self-reinforcing cycle: lower cost of capital enables more acquisitions, which increases scale, which further reduces capital costs.

Network Effects with Operators: This is perhaps Ventas's most underappreciated moat. The company doesn't just have tenants—it has a network of operating partners who rely on Ventas for growth capital, operational expertise, and market intelligence. When Atria wants to expand into a new market, they call Ventas. When a health system needs to monetize real estate while maintaining operational control, Ventas gets the first look.

These relationships compound. Each successful partnership makes Ventas more attractive to other operators. The data and insights gained from one operator benefit others in the portfolio. The company becomes a platform that creates value for all participants, not just a landlord collecting rent.

Switching Costs and Relationship Moats: In traditional real estate, tenants can relatively easily move between buildings. Not so in healthcare. A senior housing community can't simply relocate—the residents, staff, and licenses are tied to specific locations. Medical office buildings are connected to hospitals through physical walkways and operational integration. Life science facilities have millions in specialized infrastructure that can't be moved.

But the real switching costs are relational. When Ventas owns the real estate for a health system's ambulatory network, they become embedded in that system's strategic planning. They understand the system's growth priorities, capital constraints, and competitive dynamics. Replacing Ventas would mean not just finding another landlord but rebuilding years of institutional knowledge and trust.

Capital as a Competitive Advantage: In healthcare real estate, capital isn't just money—it's a product. Operators need flexible capital solutions that traditional lenders can't provide. Ventas can offer sale-leasebacks, joint ventures, development financing, and complex structures that align interests while meeting regulatory requirements.

During COVID-19, this became crystal clear. While banks pulled back from senior housing lending, Ventas could provide capital to operators for working capital needs, property improvements, and expansion. This wasn't charity—it was strategic investment in relationships that will generate returns for decades.

The REIT Structure: Benefits and Constraints: The REIT structure forces discipline that ultimately becomes an advantage. The requirement to distribute 90% of taxable income means Ventas can't hoard cash for empire building. Every investment must compete for capital. Every acquisition must make sense not in some distant future but in the near term.

This constraint drives focus and efficiency. While non-REIT competitors might pursue vanity projects or strategic diversions, Ventas must maintain rigorous capital discipline. The result: higher returns on invested capital and more predictable performance through cycles.

Competitive Positioning vs. Welltower, Healthpeak, and Others: The healthcare REIT space has consolidated into three major players—Ventas, Welltower, and Healthpeak (formerly HCP)—plus several smaller specialists. Each has pursued slightly different strategies. Welltower has focused almost exclusively on senior housing and medical office. Healthpeak has diversified into lab space and eliminated skilled nursing entirely. Ventas sits in the middle—diversified across property types but maintaining meaningful exposure to each segment.

This positioning provides optionality. When senior housing struggles, life science carries the portfolio. When medical office cap rates compress, senior housing offers growth. Ventas doesn't have to be right about which healthcare real estate segment will outperform—it just has to be right about healthcare real estate as an asset class.

The competitive dynamics favor the big three. Smaller REITs lack the scale to compete for large portfolios. Private equity buyers face higher capital costs and shorter investment horizons. International buyers struggle with operational complexity. The result is an oligopoly where the major players compete intensely but rationally, maintaining discipline on pricing and avoiding mutually destructive behavior.

XI. Bear & Bull Case

Every investment thesis contains both dreams and nightmares. For Ventas, the bull case rests on demographic destiny while the bear case warns of structural disruption. Understanding both is essential for long-term investors.

Bear Case: The Structural Headwinds

Senior Housing Oversupply Concerns: The bear thesis starts with supply and demand imbalance. In many markets, senior housing construction in 2017-2019 exceeded absorption, creating oversupply that pressured occupancy and rate growth even before COVID-19. While new construction has slowed, the existing oversupply hasn't been fully absorbed. Bears argue this will cap pricing power for years.

Healthcare Reimbursement Pressures: Government budgets are strained, and healthcare costs are unsustainable. Medicare and Medicaid face long-term solvency challenges that will require benefit cuts or reimbursement reductions. While Ventas has shifted toward private-pay properties, approximately 20% of revenues still have government reimbursement exposure. Any significant cuts could pressure operator margins and ability to pay rent.

Rising Interest Rate Sensitivity: REITs are essentially leveraged spread businesses, and rising rates compress those spreads. Higher rates increase Ventas's cost of capital while making bonds more attractive relative to REIT dividends. The math is simple: if 10-year Treasuries yield 5% risk-free, why accept 3-4% yields from REITs with operational risk?

Operator Quality and Labor Challenges: Healthcare real estate is only as good as its operators, and operator quality varies wildly. Labor shortages in healthcare are structural, not cyclical. The U.S. faces a shortage of 200,000 nurses and millions of home health aides. Without staff, operators can't fill beds regardless of demand. Some operators will fail, forcing Ventas to find replacements or take over operations directly.

Technology Disruption to Care Delivery: The biggest bear case might be technological disruption of care delivery models. Telehealth reduces the need for medical office visits. Remote monitoring enables aging in place longer. AI-driven diagnostics might eliminate entire categories of outpatient procedures. If technology fundamentally changes where and how healthcare is delivered, current real estate could become obsolete.

Bull Case: The Unstoppable Forces

Unstoppable Demographic Wave: The bull case starts with math that cannot be disputed. Every day, 10,000 Americans turn 65. The 85+ population, which drives senior housing demand, will triple by 2050. These aren't projections dependent on immigration or birth rates—these people have already been born. The demand wave is coming regardless of economic conditions.

Exceptional Track Record: Market capitalization from $0.3 billion since her leadership began in 1999 to $26 billion as of December 31, 2024 represents one of the great value creation stories in REIT history. This isn't luck—it's a 25-year track record of navigating multiple crises, regulatory changes, and market cycles. Betting against Cafaro's ability to adapt seems historically unwise.

High Barriers to Entry in Key Markets: In gateway markets like Boston, San Francisco, and Manhattan, new healthcare real estate development is nearly impossible. Zoning restrictions, NIMBY opposition, and construction costs create insurmountable barriers. Ventas owns irreplaceable assets in these markets where demand will always exceed supply.

Essential Nature of Healthcare Real Estate: Healthcare isn't discretionary. People don't choose to age, get sick, or need medical care. While delivery models might evolve, the need for physical space—whether for senior housing, medical procedures, or research—remains essential. The bear case of technological disruption ignores that even telehealth originates from medical offices and AI research happens in life science facilities.

Track Record of Navigating Cycles: Perhaps the strongest bull argument is Ventas's proven ability to navigate disruption. The company survived its tenant's bankruptcy, thrived through the financial crisis, and emerged stronger from COVID-19. Each crisis provided opportunities to acquire assets cheaply and strengthen competitive position. If history is any guide, the next crisis will be no different.

The balanced view recognizes both perspectives have merit. Healthcare real estate faces real challenges—labor shortages, reimbursement pressure, and technological change. But it also benefits from inexorable demographic trends and essential service characteristics. For long-term investors, the question isn't whether challenges exist but whether Ventas's platform, leadership, and balance sheet can navigate them while capturing the enormous opportunity ahead.

XII. Recent News

The landscape of American healthcare real estate shifted seismically in the second quarter of 2025, and at the epicenter stood Ventas, reporting results that vindicated years of strategic positioning. Ventas delivered Q2 2025 earnings with 9% higher Normalized FFO and 18.3% revenue growth, driven by aging demographics and low supply in senior housing, with a 9% year-over-year increase in Normalized FFO to $0.87 per share and revenue climbing 18.3% to $1.42 billion.

The numbers told a story of operational excellence meeting demographic destiny. The company's Senior Housing Operating Portfolio (SHOP) reported a 13% year-over-year increase in Same-Store Cash NOI, driven by 8% cash operating revenue growth and a 130 basis point improvement in NOI margins. These weren't just incremental improvements—they represented the acceleration of a recovery that many thought would take years longer to materialize.

What made the quarter particularly noteworthy was the raised guidance. With raised 2025 guidance (Normalized FFO of $3.41–$3.46/share) and a 7% FFO growth projection, the company offers a compelling combination of operational discipline, demographic-driven demand, and financial strength. In an environment where many REITs were pulling back on investment, Ventas was accelerating.

The acquisition pipeline revealed even more ambition. Senior living REIT Ventas is said to be acquiring a six-community portfolio on New York's Long Island for $600 million, with the company during its second-quarter 2025 earnings call upping its investment guidance for 2025 to $2 billion. This wasn't defensive positioning—it was offensive capital deployment at a time when competitors were still licking COVID wounds.

The Brookdale relationship restructuring exemplified Cafaro's ability to turn potential conflicts into win-win outcomes. Ventas plans to convert 44 select large-scale senior housing communities to its Senior Housing Operating Portfolio (SHOP) platform, while providing a 38% cash rent increase on 65 properties, with these mutually beneficial agreements allowing for more certainty and successful execution. The deal transformed what could have been a contentious lease expiration into a strategic repositioning that benefited both parties.

Looking ahead, the company's positioning appears particularly prescient. Ventas will release its next earnings report on Oct 30, 2025, with full year normalized FFO guidance midpoint raised to $3.44 per share, representing an 8% year-over-year FFO per share growth. The consistent execution on guidance has become a Ventas hallmark, reinforcing investor confidence in management's ability to deliver on promises.

The broader transaction market dynamics favor Ventas's scale and capital access. REITs including Welltower and Ventas have increased their investment pace in senior living in 2025, with Ventas closing 2024 with more than $2 billion of investments made primarily in senior housing, with a further "line of sight" on a pipeline of $1 billion in future acquisitions. In a market where many potential buyers lack access to capital, Ventas's investment-grade balance sheet becomes a competitive weapon.

XIII. Links & References

Primary Sources: - Ventas Investor Relations: ir.ventasreit.com - SEC Filings (10-K, 10-Q, 8-K): sec.gov/edgar - Q2 2025 Earnings Presentation: Available at ir.ventasreit.com/financials/quarterly-results

Industry Research: - National Investment Center for Seniors Housing & Care (NIC): nic.org - American Seniors Housing Association (ASHA): seniorshousing.org - NAREIT Healthcare REIT Data: reit.com/data-research

Books & Long-Form Analysis: - "The Longevity Economy" by Joseph F. Coughlin - "Healthcare Real Estate: A Practitioner's Handbook" by Andrew J. Nelson - Harvard Business School Case Study: "Ventas Inc.: The REIT That Rose from the Ashes" (2019)

Key Interviews with Debra Cafaro: - CNBC Mad Money appearances (multiple dates) - Bloomberg Real Estate Forum keynotes - J.P. Morgan Healthcare Conference presentations - NAREIT REITweek keynotes

Regulatory & Demographic Studies: - U.S. Census Bureau: "An Aging Nation: Projected Number of Children and Older Adults" - CMS: "National Health Expenditure Projections 2023-2032" - Congressional Budget Office: "The 2024 Long-Term Budget Outlook" - Urban Land Institute: "Emerging Trends in Real Estate 2025"

Competitor Analysis: - Welltower Inc. (WELL): investor.welltower.com - Healthpeak Properties (DOC): ir.healthpeak.com - Omega Healthcare Investors (OHI): omegahealthcare.com/investor-relations

Industry Publications: - Senior Housing News: seniorhousingnews.com - McKnight's Senior Living: mcknightsseniorliving.com - Healthcare Real Estate Insights: healthcarerealestateinsights.com

The Ventas story isn't finished. At 67 years old, Debra Cafaro shows no signs of slowing down, and neither does the demographic wave driving demand for healthcare real estate. The company that almost died in 1999 has become essential infrastructure for an aging society. From a $200 million distressed spinoff to a $31 billion S&P 500 constituent, Ventas has proven that in business, as in life, the greatest opportunities often come disguised as insurmountable challenges.

The question for investors isn't whether healthcare real estate will matter in the coming decades—demographics guarantee it will. The question is whether Ventas, with its proven leadership, diversified platform, and battle-tested strategy, will continue to capture more than its fair share of this massive opportunity. History suggests betting against Cafaro and Ventas would be unwise. The future, shaped by 10,000 Americans turning 65 every day, suggests it would be foolish.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube