IKS Health: The "Clinical-Grade" Operating System for US Healthcare

I. Introduction: The Doctor's Dilemma

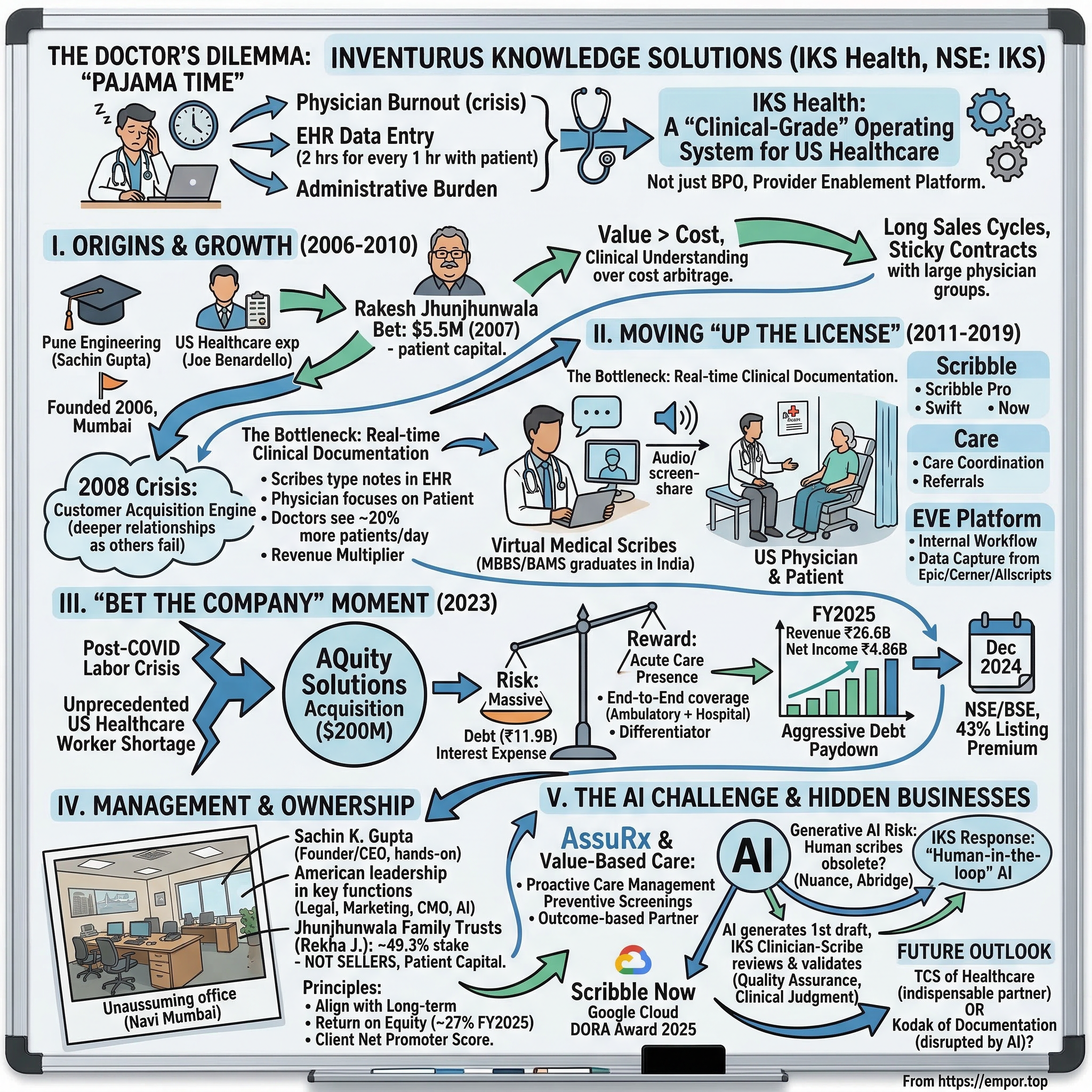

Picture this scene playing out right now in tens of thousands of American homes: it is 11 PM, the kids are asleep, and a physician is still hunched over a laptop in pajamas, typing furiously into an Electronic Health Record system. Not reviewing a tricky diagnosis. Not researching a new treatment protocol. Just typing. Documenting. Clicking through dropdown menus. Copying and pasting allergy lists. This ritual has a name in American medicine—"pajama time"—and it has become the defining pathology of the US healthcare system. Studies consistently show that for every hour a physician spends with a patient, roughly two hours go into EHR data entry and administrative tasks. The math is brutal: a doctor earning north of $300 per hour is spending the majority of their working life doing clerical work that a well-trained medical professional in another country could handle for a fraction of the cost.

The consequences are not abstract. Physician burnout in the United States has reached crisis levels. Surveys from the American Medical Association have found that over half of US physicians report symptoms of burnout, with administrative burden consistently cited as the number-one driver. Doctors are leaving practice early, reducing their hours, or abandoning medicine altogether. And here is the cruel irony: the very EHR systems that were supposed to modernize healthcare—think Epic, Cerner, Allscripts—became the instruments of this burnout. They were designed for billing compliance and data capture, not for the workflow of a clinician seeing thirty patients a day.

Into this crisis steps a company that most Indian retail investors had never heard of until late 2024: Inventurus Knowledge Solutions, trading on the NSE under the ticker IKS. The company operates commercially as IKS Health, and it describes itself not as a BPO—a label it has spent nearly two decades running from—but as a "Provider Enablement Platform." The distinction matters. A BPO takes a task, executes it offshore, and sends it back. IKS Health embeds itself inside the clinical workflow of American physician groups, health systems, and hospitals. Its people—many of them licensed doctors and pharmacists in India—sit inside the EHR alongside the American physician, typing notes in real time, managing prescriptions, coordinating care, and handling the billing that follows. The physician gets to do what they trained for: practice medicine. IKS handles everything else.

The scale is remarkable. From a small office in Mumbai founded in 2006, IKS Health now serves over 778 healthcare organizations and more than 150,000 clinicians across the United States. Its trailing twelve-month revenue as of December 2025 exceeded $350 million. It manages revenue cycle operations for US health systems collectively generating over $10 billion in patient revenue. And in December 2024, the company listed on the NSE and BSE at a price of ₹1,329 per share, only to open trading at ₹1,900—a 43% listing day premium that made it one of the most successful Indian IPOs of the year.

But the truly astonishing number in the IKS story does not appear in any prospectus. It sits on the cap table. In 2007, a young Sachin Gupta walked into the Nariman Point office of Rakesh Jhunjhunwala—India's legendary "Big Bull"—and pitched him on a healthcare services company targeting American doctors. Jhunjhunwala wrote a check for roughly $5.5 million. By the time IKS listed seventeen years later, that stake—held by the Jhunjhunwala family trusts after Rakesh's passing in 2022—was worth approximately $1.4 billion. It may be the single greatest uncelebrated investment in Jhunjhunwala's storied career, eclipsing even his famous Titan bet on a percentage-return basis. And the family has not sold a single share.

Understanding how a niche healthcare services company turned patient capital into a multi-billion-dollar platform requires going back to the beginning—to a moment when three co-founders saw something in the US healthcare system that almost nobody in India was paying attention to.

II. History: Origins and the "Non-BPO" BPO (2006–2010)

In September 2006, when Sachin K. Gupta incorporated Inventurus Knowledge Solutions in Maharashtra, the Indian outsourcing industry was at its most exuberant. Infosys, Wipro, and TCS were minting money hand over fist, and a new generation of BPO entrepreneurs was chasing every conceivable back-office function that could be shipped offshore. Medical transcription—converting American doctors' dictated notes into typed documents—was one of the hottest niches. Dozens of small Indian firms were grinding away on transcription, competing on price, and treating it as a commodity.

Gupta, who held an engineering degree in computer science from the University of Pune, saw the landscape differently. He had spent enough time studying the US healthcare system to understand a tectonic shift that was just beginning: the move from "Fee-for-Service" to "Fee-for-Value." Under the old model, a doctor got paid for every test ordered, every procedure performed, every patient seen. Under the emerging value-based model—accelerated by legislation like the Affordable Care Act—reimbursement would increasingly depend on patient outcomes, quality metrics, and documentation completeness. This meant that the administrative burden on physicians was not going to shrink. It was going to explode.

Together with co-founders Nitin Gupta and Joe Benardello—the latter an American healthcare executive born in 1967 who understood the US provider market intimately—Sachin set out to build something fundamentally different from the transcription sweatshops around him. The founding thesis was deceptively simple: do not compete on cost alone; compete on clinical understanding. Rather than hiring English-speaking generalists to type up medical notes, hire people who actually understood medicine. And rather than serving thousands of small clinics—the typical BPO playbook of maximizing volume—focus exclusively on large, multi-specialty physician groups where the relationships would be deep, the contracts would be sticky, and the revenue would be recurring.

This was a contrarian bet that sacrificed early growth for long-term defensibility. Large physician groups are notoriously difficult to sell to. The sales cycles are measured in quarters, not weeks. They demand references, security audits, HIPAA compliance certifications, and integration with their specific EHR systems. But once you are in, you are in. A large medical group does not switch its documentation and billing partner the way a consumer switches phone plans. The cost of transition—retraining doctors, reconfiguring EHR workflows, risking revenue cycle disruptions—creates enormous inertia.

The pivotal moment in IKS's early history came in 2007, when Sachin Gupta secured a meeting with Rakesh Jhunjhunwala at Rare Enterprises. Jhunjhunwala was not a typical venture capital investor. He did not think in terms of five-year fund horizons or exit multiples. He thought in decades. His greatest investments—Titan, CRISIL, Lupin—were all stories of patient compounding in businesses with durable competitive advantages. When Gupta pitched him on a healthcare services company that would take years to build but could become deeply embedded in the American healthcare infrastructure, Jhunjhunwala recognized the pattern. The $5.5 million check he wrote was not large by later standards, but it was transformational for a startup that needed to invest in technology, compliance, and talent long before revenue would justify the spending.

That capital proved critical almost immediately. When the 2008 financial crisis hit, US healthcare spending tightened sharply. Hospitals and physician groups slashed budgets, and many of the small Indian medical transcription firms that had proliferated in the boom years simply folded. They had been running on thin margins with no financial cushion. IKS, backed by Jhunjhunwala's patient capital, did not just survive—it used the downturn to deepen relationships with clients who were now more desperate than ever to cut costs without sacrificing quality. The crisis became a customer acquisition engine.

By 2010, IKS had established itself as a focused player serving large US physician groups with a combination of revenue cycle management, medical coding, and documentation services. It was still small—revenue was in the single-digit millions of dollars—but the foundation was laid. The company had learned to speak the language of American medicine: CPT codes, ICD-10 classifications, HEDIS quality measures, and the labyrinthine rules of Medicare and Medicaid reimbursement. It was not competing with Infosys or TCS for generic IT outsourcing contracts. It was building something that those giants could not easily replicate—a clinical-grade services platform that required deep domain expertise, not just labor arbitrage.

The question, though, was whether this niche positioning could scale. The answer would come from a radical innovation that IKS pioneered in the next decade—one that would transform it from a back-office service provider into a real-time clinical partner sitting inside the exam room.

III. The Middle Years: Moving "Up the License" (2011–2019)

Imagine a typical morning in a US primary care clinic around 2013. A physician walks into an exam room, greets the patient, and begins a conversation that will last perhaps fifteen minutes. During that conversation, the doctor needs to listen to the patient's symptoms, perform a physical examination, make diagnostic decisions, prescribe medications, order tests, and—here is the part that makes physicians grind their teeth—document everything in painstaking detail in the EHR. Every symptom mentioned. Every finding noted. Every medication reconciled. Every diagnosis coded. The documentation is not optional; it determines whether the practice gets paid, and whether the physician complies with an ever-growing web of regulatory requirements.

The doctors did not want to type. That was the insight that changed IKS Health's trajectory. Sachin Gupta and his team realized that the real bottleneck was not billing or coding—those were downstream activities that happened after the patient visit. The bottleneck was the clinical documentation itself, the real-time note-taking that consumed the physician's attention during the encounter. If you could solve that, everything else in the revenue cycle became easier.

IKS's answer was the virtual medical scribe. Here is how it worked: as the physician conducted a patient visit, an IKS-trained professional—sitting in an office in India, connected via a secure audio and screen-sharing link—would listen to the encounter in real time and type the clinical notes directly into the EHR. The doctor could focus entirely on the patient, maintaining eye contact, asking follow-up questions, and practicing medicine the way they had been trained to, while the scribe handled the documentation.

The genius of the model was in who IKS hired to do this work. Rather than using generic call-center employees, IKS recruited MBBS and BAMS graduates—individuals who had completed full medical degrees in India but, for various reasons, were seeking non-clinical corporate careers. India produces hundreds of thousands of medical graduates every year, far more than the clinical workforce can absorb. Many of these graduates, particularly from BAMS (Ayurvedic medicine) and BHMS (homeopathic medicine) programs, possessed strong medical knowledge and English fluency but faced limited clinical career prospects. IKS offered them something compelling: well-paying corporate jobs that used their medical training without requiring them to practice medicine.

This created a powerful arbitrage. A US physician's time was worth $300 or more per hour. An Indian medical graduate, even at competitive Indian salaries, cost a fraction of that. But the quality of the work was not a compromise—it was actually superior to what a non-medical scribe could produce. These were people who understood anatomy, pharmacology, and medical terminology at a professional level. They could anticipate what a physician was going to document, catch inconsistencies in clinical notes, and ensure that documentation supported the appropriate billing codes.

IKS productized this capability under branded service lines. Scribble became the umbrella for their virtual scribing offerings, eventually expanding into a suite: Scribble Pro provided EHR-integrated notes within four hours with comprehensive reconciliation by clinician-scribes and evaluation-and-management coding; Scribble Swift used trained associates to refine charts and add clinical information; and later, Scribble Now would incorporate ambient AI and speech recognition. Care became the brand for care coordination services—managing referrals, follow-ups, chronic disease monitoring, and the administrative infrastructure that surrounds patient care.

The impact on physician productivity was measurable and dramatic. A doctor working with IKS scribe support could typically see 20% more patients per day, because they were no longer spending half their time typing. For a medical practice, that translated directly into higher revenue—more patients seen, more encounters billed, better documentation supporting higher reimbursement rates. IKS was not just saving money for its clients; it was making them money. That changed the sales conversation entirely. This was not a cost center being outsourced. It was a revenue multiplier.

Behind the scenes, while the market saw a services company, management was quietly building something else: a technology platform. The IKS EVE platform began as an internal tool to manage workflow—routing audio feeds, integrating with EHR systems, tracking documentation quality. But over time, it evolved into a sophisticated data layer that captured structured information from millions of patient encounters. IKS teams were logging into Epic, Cerner, and Allscripts systems every day, and the platform was learning the patterns—which documentation triggered which billing codes, which quality measures were being missed, which patients were overdue for preventive screenings.

Think of it this way: if the US healthcare system is an airplane, the EHR is the cockpit instrument panel. IKS was not building a new instrument panel; it was building the autopilot system that sat on top of the existing instruments, reading them, interpreting them, and helping the pilot fly more efficiently. The platform was not visible to the outside world—IKS did not market itself as a technology company, and its revenue was still predominantly fee-for-service—but the data and workflow intelligence it was accumulating would become the foundation for everything that came next.

By 2019, IKS had grown its revenue to roughly ₹5.5 billion (approximately $70-75 million), was serving dozens of large US physician groups, and had built a workforce of several thousand clinical and administrative professionals. The company was profitable, cash-generative, and growing at over 30% annually. It was also, by design, nearly invisible. No flashy conference keynotes, no venture capital press releases, no LinkedIn thought leadership from the CEO. Sachin Gupta ran the company like a surgeon: quietly, precisely, and with an obsessive focus on the client relationship.

But invisibility has its costs. IKS was a mid-sized player in a massive market, and the US healthcare landscape was about to undergo a convulsion that would force it to make the biggest decision in its history.

IV. The "Bet the Company" Moment: The AQuity Acquisition (2023)

The COVID-19 pandemic did not just disrupt healthcare delivery—it permanently rewired the economics of the US healthcare workforce. When the pandemic hit in 2020, hospitals hemorrhaged money on emergency preparedness, while physician practices saw patient volumes collapse as elective care was postponed. Then came the recovery, and with it, an unprecedented labor crisis. Healthcare workers who had endured the trauma of COVID—the long shifts, the emotional toll, the burnout—left the profession in droves. The US Bureau of Labor Statistics recorded hundreds of thousands of healthcare workers quitting between 2021 and 2023. Those who stayed demanded higher wages. Travel nurse salaries doubled and tripled. Administrative staff became nearly impossible to hire and retain.

For IKS Health, the post-COVID labor crisis was simultaneously a tailwind and a constraint. The tailwind was obvious: American healthcare organizations, unable to hire domestically at any reasonable cost, became far more receptive to offshore clinical support. IKS's phone was ringing. The constraint was equally clear: IKS was strong in "ambulatory" care—the world of physician clinics, outpatient practices, and medical groups—but had limited presence in "acute" care, meaning hospitals and health systems. And it was the hospitals, with their massive scale and urgent staffing needs, that represented the largest untapped opportunity.

Enter AQuity Solutions. AQuity was a US-headquartered healthcare services company with a workforce of over 7,000 professionals and deep expertise in exactly the areas where IKS was weakest: acute care clinical documentation, hospital-based medical coding, and health system revenue cycle management. AQuity served major hospital networks and health systems, and its team included specialized clinical documentation improvement specialists who worked with hospital physicians—a different skill set from the ambulatory scribes that IKS had perfected.

In October 2023, IKS announced the acquisition of AQuity Solutions for $200 million—approximately ₹1,600 crore. To understand the magnitude of this bet, consider the context. Pre-acquisition, IKS had reported revenue of roughly ₹10.3 billion for FY2023 and was sitting on total assets of about ₹9.9 billion. The acquisition price was massive relative to the company's size. AQuity was generating annual revenue of over $100 million, which meant IKS was paying less than 2x revenue—a bargain compared to the 5-10x revenue multiples that health-tech SaaS companies commanded—but the absolute dollar amount required IKS to take on significant debt for the first time in its history.

The financing tells the story of the risk involved. IKS's balance sheet went from having virtually zero long-term debt in FY2023 to carrying over ₹11.9 billion in total debt by FY2024. The company's net debt went from negative (meaning it had more cash than debt) to approximately ₹11.7 billion. Interest expense, which had been negligible at ₹60 million in FY2023, ballooned to ₹611 million in FY2024. This was a company that had been run conservatively for seventeen years—cash-positive, debt-free, self-funded—suddenly leveraging its balance sheet to make a transformative bet.

The strategic logic, however, was compelling. The US healthcare market does not neatly divide into "clinics" and "hospitals." Large health systems increasingly operate both. A health network like Mass General Brigham or Duke Health—both IKS clients—runs outpatient clinics, urgent care centers, specialty practices, and acute care hospitals. They want a single partner who can handle documentation, coding, and revenue cycle across the entire continuum. Before the acquisition, IKS could serve the ambulatory side but had to hand off the hospital work. After the acquisition, it could offer end-to-end coverage. That capability became a powerful differentiator in competitive bids.

The integration was not trivial. AQuity brought over 7,000 employees, effectively doubling IKS's headcount to more than 14,000 globally. Merging two organizations with different cultures, technology stacks, and client management approaches is always fraught. But IKS had a structural advantage: both companies were already serving the same underlying customer (US healthcare providers) with similar service modalities (offshore clinical and administrative support). The integration was more about harmonizing workflows and cross-selling than about reconciling fundamentally different businesses.

The financial results validated the bet remarkably quickly. In FY2024 (the first full year including AQuity), IKS reported revenue of ₹18.2 billion—a 76% year-over-year increase. Even more importantly, EBITDA grew by 44%, suggesting that the acquisition was not just adding revenue but was being integrated without destroying margins. By FY2025, revenue reached ₹26.6 billion, another 47% jump, while net income grew 31% to ₹4.86 billion. The company was growing at a pace that suggested real operating leverage was emerging from the combined entity.

Perhaps the most telling indicator was the debt trajectory. After peaking in FY2024, total debt had already begun declining by FY2025, dropping from ₹13.1 billion to ₹8.6 billion. The company was generating enough cash flow to rapidly pay down the acquisition debt while continuing to invest in growth. Net debt fell from ₹11.7 billion to ₹6.8 billion in just one year. The "bet the company" moment was starting to look like one of the better-executed healthcare services acquisitions in recent Indian corporate history.

With the acquisition integrated and the IPO behind it, the question shifted from whether IKS could execute to whether it could sustain this trajectory—and that depended on the people running the show and the shareholders backing them.

V. Management and Ownership Structure

Walk into IKS Health's headquarters in Navi Mumbai's Mindspace SEZ—an unassuming office on the eighth floor of Buildings 5 and 6—and the first thing that strikes visitors is the absence of corporate theater. There is no marble-floored reception with a brand wall of accolades. No mission statement etched in glass. Sachin K. Gupta, the founder and CEO, operates from this office but spends a significant portion of his time in the United States, sitting across the table from the C-suite executives and medical directors of the health systems IKS serves. Born in 1976, Gupta is now forty-nine years old and has been running this company for nearly two decades—an unusually long tenure for a founder-CEO in the Indian technology services landscape.

What makes Gupta distinctive is that he never graduated to the ceremonial "Founder-Chairman" role. He remains the operating CEO, directly involved in client relationships, pricing negotiations, and strategic decisions. According to company filings, his compensation was ₹12.79 million—modest by Indian CEO standards, and minuscule compared to what his US healthcare-executive peers earn. This is not a founder cashing out through salary; his wealth creation is tied to his equity stake. He is also an active angel investor, with stakes in thirteen startups and board positions at three companies, suggesting a mind that stays engaged with the broader innovation ecosystem.

The leadership team reflects IKS's hybrid identity as an Indian-headquartered company serving exclusively American clients. Joe Benardello, the American co-founder, serves as Chief Growth Officer and Non-Executive Director, maintaining the US client relationships and market intelligence that have been critical since the founding. The CFO is Nithya Balasubramanian, born in 1984, who oversees the increasingly complex financial architecture of a company that now manages multi-currency revenues, acquisition debt, and public market reporting obligations. The Chief Medical Officer is Dr. Grace E. Terrell, who brings clinical credibility to client conversations. And in a signal of where the company sees its future, IKS appointed Ajai Sehgal as Chief AI Officer, a newly created role focused on enterprise-wide AI strategy.

The deeper you look at IKS's management, the more it resembles a US healthcare company that happens to be headquartered in India. The Chief Legal and Compliance Officer, Christi Braun, is American. The Chief Marketing Officer, Kathryn Weismantel, is American. The Chief Information Officer, Marty Serro, is American. The Chief Digital Officer, Hernan Giraldo, is American. This is not a token nod to the US market—it reflects the reality that IKS's entire client base, regulatory environment, and competitive landscape is American. The Indian operations provide the clinical and administrative workforce; the American leadership provides the market access, compliance expertise, and strategic direction.

But the most consequential name on the cap table is not any of the executives. It is Rekha Jhunjhunwala—the wife of the late Rakesh Jhunjhunwala—and the family trusts that hold approximately 49.3% of IKS's outstanding shares. The holding is distributed across three discretionary trusts—the Aryaman Jhunjhunwala Trust, the Aryavir Jhunjhunwala Trust, and the Nistha Jhunjhunwala Trust—each holding approximately 16.4%, with Rekha's direct holding at 0.2%. Utpal Sheth, who runs Rare Enterprises as its CEO, provides strategic oversight.

The significance of this ownership structure cannot be overstated. These are not financial investors looking for an exit. The Jhunjhunwala family treats IKS the same way it treats its holdings in Titan or Star Health—as multi-decade compounders to be held, not traded. They did not sell into the IPO (the offering was entirely an Offer for Sale from other shareholders, not the promoters). They have not sold since. This creates a powerful alignment with long-term shareholders but also means that the public float is lower than typical for a company of this market capitalization, which can create volatility in the stock during periods of heavy buying or selling.

The incentive structure within IKS reflects this long-term orientation. Management compensation emphasizes metrics like Return on Equity—which stood at approximately 27% in FY2025—and client retention rates rather than quarterly revenue beats. The company maintains an ESOP pool for senior leadership, tying executive wealth creation to the long-term stock performance rather than short-term bonuses. Client Net Promoter Score is tracked as a key management metric, which is unusual for a services company; most Indian IT services firms focus on utilization rates and billing hours, not on whether clients would recommend them.

The IKS IPO itself—which opened for subscription from December 12-16, 2024 and was oversubscribed 52.68 times—was entirely an Offer for Sale. The company did not raise any new capital. This means the IPO was a liquidity event for early investors, not a fundraising exercise. IKS did not need the money; it was already profitable, cash-generative, and had funded the AQuity acquisition through debt that it was actively paying down. The listing was about providing liquidity and establishing a public market currency, not about financing growth.

What investors are really buying when they buy IKS is not just the current business—it is the combination of a management team with deep domain expertise, a patient anchor shareholder who will not panic-sell in a downturn, and a culture that prioritizes clinical quality over growth-at-all-costs. Whether those qualities justify the valuation is a different question entirely—but the governance structure is unusually well-aligned for a company of this size and age.

VI. Hidden Businesses: The Tech Inside the Service

There is a question that surfaces in every investor conversation about IKS Health, and it usually goes something like this: "So they're basically a staffing company, right? They hire Indian doctors to type notes for American doctors. What's the moat?" It is a reasonable question, and the answer lies in two business capabilities that are not immediately visible from the outside but represent the company's most important strategic assets.

The first is AssuRx and IKS's broader push into value-based care. To understand why this matters, a brief detour into how American healthcare reimbursement works is necessary. Under the traditional "fee-for-service" model, a doctor gets paid for each service rendered—an office visit, a lab test, a procedure. Under value-based care contracts, which are growing rapidly, a provider organization receives a fixed payment per patient per month and is responsible for keeping that patient healthy. If the patient stays healthy, the provider keeps the surplus. If the patient gets sicker and requires expensive interventions, the provider absorbs the cost. This is a fundamental shift from "volume" to "value," and it requires an entirely different operational infrastructure.

IKS's AssuRx platform is built for this world. Think of it as a proactive care management layer. IKS teams—working through the data captured by the EVE platform—identify patients who are overdue for preventive screenings: mammograms, colonoscopies, diabetic eye exams, annual wellness visits. They then reach out to those patients, schedule the appointments, and ensure the documentation is completed so that the provider organization gets credit for meeting quality benchmarks. This sounds simple, but the operational complexity is enormous. It requires integrating with multiple EHR systems, tracking thousands of patients across dozens of quality measures, managing outreach across phone, text, and patient portals, and ensuring that every interaction is documented for compliance purposes.

Why does this matter strategically? Because it fundamentally changes the nature of IKS's relationship with its clients. When IKS was primarily doing medical scribing and coding, it was a vendor—a provider of defined services at an agreed-upon price. When IKS manages value-based care performance, it becomes a partner whose revenue is tied to patient outcomes. If IKS does its job well, the provider organization earns higher quality bonuses from Medicare and commercial insurers, and IKS shares in that upside. This creates alignment that makes the relationship even stickier than the switching costs alone would suggest.

The second hidden business is the AI layer—and this is where the IKS story gets truly interesting. The consensus narrative among skeptics is straightforward: generative AI will make human medical scribes obsolete. If an LLM can listen to a patient encounter and generate clinical notes automatically, why do you need thousands of Indian doctors doing the same thing? Companies like Nuance (owned by Microsoft), Abridge, and Suki AI are all building ambient AI scribing solutions that promise to eliminate the human from the documentation loop entirely.

IKS's response has been to lean into AI rather than hide from it. At the ViVE 2025 conference, the company launched Scribble Now, an ambient AI scribing product built on advanced speech recognition and generative AI that can produce high-quality clinical notes within minutes of a patient encounter. In parallel, IKS announced a novel generative AI platform built on Google Cloud technologies, using the Gemini family of models, designed as a multi-agent system that orchestrates clinical documentation, medical coding, order capture, claim submission, and prior authorization into a single automated workflow. According to company disclosures, AI agents within this system can autonomously handle up to 80% of routine, repetitive tasks.

But here is the critical insight: IKS is not trying to replace its humans with AI. It is trying to make each human dramatically more productive. The model is what the industry calls "human-in-the-loop" AI. The AI generates the first draft of a clinical note. An IKS clinician-scribe then reviews it, corrects any errors, adds nuanced clinical context that the AI may have missed, and ensures that the documentation supports appropriate billing codes and quality measures. The AI handles the heavy lifting; the human provides the quality assurance and clinical judgment.

This is not a theoretical framework—it is a practical response to a real limitation of current AI technology. Large language models are remarkably good at generating plausible-sounding medical text, but they are not yet reliable enough for the "last mile" of clinical documentation, where a single coding error can mean the difference between a claim being paid or denied, or where a missed diagnosis in the notes could have legal implications. IKS's bet is that it owns this last mile—the quality validation layer—and that AI will make its clinician-scribes more productive (handling more encounters per person) rather than making them obsolete.

The company earned recognition for this approach, winning the Google Cloud DORA Award 2025 for "Augmenting Human Expertise with AI" and top honors in the 2025 Black Book Research survey for AI-driven Revenue Cycle Management. Whether AI ultimately proves to be an existential threat or a productivity accelerator for IKS remains the single most important strategic question hanging over the company—but management is clearly not waiting to find out.

VII. Hamilton's 7 Powers Analysis

The strategic durability of any business ultimately comes down to whether it possesses sources of persistent differential advantage—what Hamilton Helmer, in his influential framework, calls the "7 Powers." For IKS Health, several of these powers are clearly present, while others are more contested.

Switching Costs represent IKS's most formidable power. Once a physician has been working with a dedicated IKS scribe for six months, a relationship forms that is both personal and operational. The scribe learns the doctor's speech patterns, their preferred documentation style, their clinical shortcuts and abbreviations. Taking away that scribe is, as one IKS client reportedly described it, "like taking away my right hand." But the switching costs go deeper than personal familiarity. IKS integrates directly into the client's EHR system—typically Epic, Cerner, or Allscripts. These integrations involve technical configuration, security protocols, user permissions, and workflow customization that take months to set up and test. Ripping them out and replacing them with a competitor's integration is a project that no health system IT department wants to undertake unless absolutely necessary. When IKS serves 778 healthcare organizations, each with its own EHR configuration, the aggregate switching cost across the client base creates a moat that is nearly impossible to replicate quickly.

Process Power is the second major source of advantage. IKS has built a proprietary knowledge management system that trains Indian medical graduates on US healthcare protocols—HIPAA compliance, American clinical terminology, EHR navigation, billing and coding rules—faster and more effectively than any competitor. This is not something you can see from the outside, but it represents nearly two decades of accumulated institutional knowledge. Every error that a scribe has ever made, every client complaint, every quality audit has been fed back into the training system. A new hire at IKS goes through a rigorous onboarding process that includes not just medical knowledge but also cultural training—understanding how American physicians communicate, the nuances of the US insurance system, and the regulatory landscape. This process power means that IKS can scale its workforce without proportionally degrading quality, which is the critical operational challenge for any services business.

Cornered Resource manifests in two ways. The first is capital: the Rare Enterprises backing gave IKS access to patient capital when competitors were starving for funding. This was not just money—it was the right kind of money, from an investor who understood that building a healthcare services platform takes a decade, not a venture fund cycle. The second cornered resource is talent. India produces an enormous surplus of medical graduates—MBBS, BAMS, BHMS—who are qualified, English-speaking, and seeking non-clinical career paths. IKS has built a recruiting pipeline and employer brand within this talent pool that gives it a structural advantage. Competitors trying to enter the space have to build this pipeline from scratch, and the best candidates are often already working at IKS or its established peers.

Counter-Positioning is the power that explains why US-based staffing firms have struggled to compete with IKS despite having geographic proximity to clients. An American medical scribe costs $15-25 per hour. An IKS clinician-scribe—who is often more qualified, holding an actual medical degree—costs a fraction of that. But the counter-positioning is not just about price. US staffing firms use generalists; IKS uses doctors. The quality differential means that IKS's documentation is more accurate, supports higher billing codes, and requires fewer revisions. US-based competitors cannot adopt IKS's model without cannibalizing their existing revenue streams and fundamentally restructuring their cost base—the classic counter-positioning dynamic.

Where IKS's powers are weaker is in Scale Economies (the healthcare services market is large enough to support multiple players without a winner-take-all dynamic), Network Effects (there are no direct network effects in clinical documentation services), and Branding (IKS operates behind the scenes; patients never know it exists). These are not fatal weaknesses—many excellent businesses lack all seven powers—but they do suggest that IKS's moat is built on operational execution and relationship stickiness rather than on the kind of structural advantages that create true monopolies.

For investors, the powers analysis reveals that IKS's competitive advantage is real but depends on continued operational excellence. The switching costs and process power are durable, but they require constant investment in technology, training, and client service. A complacent IKS could see its process power erode over time as competitors catch up. The company's long-term trajectory will be determined by whether it can keep deepening these powers—particularly through AI-augmented productivity—faster than the market evolves around it.

VIII. The Playbook: Lessons for Builders

The IKS story offers three strategic lessons that extend well beyond healthcare services, each of which challenges conventional wisdom in the Indian technology industry.

The first lesson is the power of services as a wedge for technology. In the startup world, there is an almost religious bias toward "product" companies and against "services" companies. Venture capitalists want to fund software platforms with 80% gross margins, not services businesses that scale linearly with headcount. IKS flipped this logic on its head. It started by doing the hard, manual, unglamorous work of medical documentation—the kind of work that no Silicon Valley startup wanted to touch because it did not look like a technology business. But by doing that work at scale, across hundreds of healthcare organizations, IKS accumulated something that no pure software startup could match: deep, real-world understanding of clinical workflows, billing patterns, and quality metrics.

That understanding became the foundation for its technology platform. The EVE platform, the AssuRx care management system, the Scribble AI suite—none of these could have been designed by engineers in a vacuum. They were built by people who had spent years inside the EHR, processing millions of patient encounters, and who understood where the real friction points were. The services business generated the revenue to fund the technology development, created the client relationships to test and deploy it, and provided the data to train it. By the time pure-technology competitors entered the market with ambient AI scribing products, IKS had already built the client trust, regulatory compliance infrastructure, and domain expertise that would take those competitors years to replicate.

This pattern—earning trust through services, then layering in technology to expand margins and deepen the moat—is one of the most underappreciated playbooks in the Indian technology industry. Companies like HCL Technologies used a version of it to move from hardware distribution to IT services to platform engineering. IKS is attempting the same trajectory in healthcare, and the FY2025 financial results—with revenue growing 47% while the company simultaneously reduced its debt burden—suggest the playbook is working.

The second lesson is about patient capital. The Rakesh Jhunjhunwala investment in IKS is not just a feel-good story about a legendary investor's foresight. It is a structural lesson about what kind of capital enables what kind of company. Healthcare services businesses are, by their nature, slow to build. The sales cycles are long. The regulatory hurdles are immense. The training infrastructure takes years to develop. A typical venture capital fund, with a 5-7 year horizon and pressure to generate interim markups, would have pushed IKS to grow faster than was prudent—to take on smaller clients for quick revenue, to cut corners on training, to skip the investment in technology that had no immediate revenue payoff. Jhunjhunwala's patient capital allowed IKS to make the right long-term decisions even when they looked like the wrong short-term decisions. The seventeen-year holding period between the initial investment and the IPO is almost unheard of in the Indian private equity and venture capital landscape.

The third lesson is about differentiation through domain depth. India's IT services industry is dominated by giants—TCS, Infosys, Wipro, HCL—that compete primarily on scale and cost. They serve every industry, every function, every geography. IKS chose the opposite approach: obsessive focus on a single vertical (US healthcare), a single function (provider enablement), and a single customer type (large physician groups and health systems). This focus allowed it to build the clinical-grade capabilities—the deep understanding of CPT codes, HEDIS measures, CMS regulations, and EHR workflows—that a horizontal IT services firm could never match. When a health system is choosing a documentation partner, the decision is not between IKS and TCS. It is between IKS and specialized competitors like R1 RCM, Optum, or AGS Health. IKS competes in a different arena entirely, where the language is medicine, not information technology.

IX. Valuation and the Bear vs. Bull Debate

Every investment thesis ultimately comes down to the balance between what could go right and what could go wrong. For IKS Health, both sides of the ledger are unusually vivid.

The bear case starts with the elephant in every room where IKS is discussed: generative AI risk. The ambient AI scribing market is evolving at breathtaking speed. Microsoft's Nuance DAX and Abridge together controlled roughly two-thirds of the estimated $600 million ambient AI scribe market as of late 2025. These are well-funded, technically sophisticated competitors building products designed to eliminate the human scribe entirely. If AI reaches a point where it can reliably generate clinical documentation without human review—not just a plausible first draft, but a final, billable, legally defensible clinical note—then IKS's core business model faces existential pressure. The company employs over 14,000 people, and a significant portion of them are doing work that AI companies are explicitly trying to automate. Management's argument that IKS owns the "last mile" of quality validation is credible today, but technology has a way of closing last-mile gaps faster than incumbents expect.

The second bear argument is US political risk. Healthcare outsourcing to India has never generated the same political backlash as, say, manufacturing outsourcing to China, but the risk is not zero. HIPAA—the Health Insurance Portability and Accountability Act—imposes stringent requirements on how patient data can be handled, stored, and transmitted. Any high-profile data breach involving offshore-processed patient records could trigger a regulatory crackdown that fundamentally alters the economics of IKS's model. Additionally, the periodic rise of protectionist sentiment in US politics—"bring jobs home" rhetoric—could result in legislative or regulatory barriers to offshore healthcare services. This is a low-probability but high-impact risk that has no hedge.

The third bear concern is Indian wage inflation. IKS's margin advantage depends on the cost differential between Indian clinical professionals and their US counterparts. Indian wages in the technology and services sectors have been rising steadily, and the competition for MBBS/BAMS graduates among healthcare BPOs, pharma companies, and clinical research organizations is intensifying. If Indian wages rise faster than IKS can increase its pricing to US clients—who are themselves under reimbursement pressure from Medicare and commercial insurers—margins will compress.

Analyzing through Porter's Five Forces, the competitive dynamics present a mixed picture. The threat of new entrants is moderate: the regulatory barriers (HIPAA, EHR integration, clinical training) are high, but the core service model is not patented and can be replicated with sufficient investment. Buyer power is significant: large US health systems have the leverage to negotiate pricing, and they increasingly consolidate their vendor relationships. Supplier power (i.e., the Indian clinical workforce) is currently low due to the surplus of medical graduates, but this could shift as demand grows. The threat of substitutes—primarily AI-driven automation—is the single greatest force acting on IKS's competitive position. Rivalry among existing players is moderate; IKS, R1 RCM, Optum, and AGS Health compete for large contracts, but the market is large enough that competitive intensity has not yet compressed margins to commodity levels.

The bull case is equally forceful. First, market depth: IKS has less than 5% market share in a total addressable market that exceeds $50 billion. The US healthcare administrative burden is not shrinking—if anything, it is growing as value-based care contracts add new layers of documentation and quality reporting requirements. Even in a world where AI automates a significant portion of scribing, the overall market for provider enablement services—coding, billing, care coordination, prior authorization, quality reporting—is expanding faster than any single technology can cannibalize it.

Second, operating leverage from the AQuity integration. The quarterly results through FY2026 tell a story of accelerating profitability. Q3 FY2026 (the quarter ending December 2025) showed revenue of ₹8.15 billion (24% year-over-year growth), EBITDA growth of 40%, and an EBITDA margin of 35%. PAT growth of 41% exceeded revenue growth, indicating real operating leverage as the combined entity achieves cost synergies and cross-sells services. The debt burden from the acquisition is being paid down aggressively, with total debt falling from ₹13.1 billion in FY2024 to ₹8.6 billion in FY2025 and continuing to decline.

Third, the moat of trust. Healthcare is not an industry where the low-cost provider automatically wins. When a US hospital system is entrusting patient records—the most sensitive category of personal data in American law—to an offshore partner, they want a "safe pair of hands." They want a company with a decade-plus track record, a Chief Compliance Officer who understands HIPAA inside out, and a technology infrastructure that has been audited, pen-tested, and certified. They want references from peers—from Mass General Brigham, from Duke Health, from Lehigh Valley Health Network. IKS has spent nearly twenty years building this trust. A well-funded startup with a better AI product still needs to earn that trust from scratch, and in healthcare, that process takes years, not months.

For investors tracking this company's trajectory, two KPIs matter more than any others: Revenue per Clinician Served (which measures whether IKS is deepening its wallet share within existing client relationships by cross-selling from scribing into coding, care coordination, and value-based care management) and EBITDA margin trajectory (which reveals whether AI-augmented productivity is genuinely improving the economics of the business or whether the company is simply growing revenue through headcount additions). These two metrics, tracked quarterly, will provide the clearest signal of whether IKS is successfully navigating the transition from a labor-intensive services model to a technology-enabled platform.

One material accounting consideration: the AQuity acquisition generated approximately ₹12 billion in goodwill and ₹4.8 billion in identifiable intangible assets on IKS's balance sheet. Together, these intangibles represent over 55% of total assets. Any impairment of this goodwill—triggered by underperformance of the acquired business relative to projections—would have a material impact on reported earnings and book value. Investors should monitor the company's annual goodwill impairment testing disclosures closely.

X. Outro

The question that will define IKS Health's next chapter is whether it becomes the TCS of healthcare—a company that leveraged India's talent advantage to build a global services empire that grew more valuable with each passing decade—or whether it becomes the Kodak of clinical documentation, a company that built a dominant position in a technology that was about to be disrupted.

The TCS analogy is instructive. When TCS started, critics dismissed it as a body shop—cheap Indian labor doing grunt work for Western companies. Over time, TCS moved up the value chain, built proprietary platforms, developed deep domain expertise, and created switching costs that made it indispensable to its clients. The "body shop" narrative never fully disappeared, but TCS proved that services businesses could compound wealth for decades if they continuously invested in capabilities that clients could not easily replicate.

IKS is at a similar inflection point. The critics today call it a "scribe shop"—cheap Indian doctors typing notes for American doctors. The company's response is to move up the value chain through AI augmentation, value-based care management, and platform technology. The AQuity acquisition was a bold move to achieve the scale necessary to invest in these capabilities. The Jhunjhunwala backing provides the patient capital necessary to see the transformation through. And the management team, with its deep roots in both Indian operations and American healthcare, understands the dual cultures it must navigate.

But the AI disruption risk is real, and it is moving fast. Microsoft, Google, Amazon, and a swarm of well-funded startups are all building products that target the exact workflow that IKS's 14,000 employees perform every day. IKS's bet—that it can ride the AI wave rather than be swamped by it, using technology to make its people more productive rather than replacing them—is rational and well-articulated. But it is still a bet. The next five years will determine whether IKS Health becomes a defining case study in how a services company successfully navigated the AI transition, or a cautionary tale about what happens when the wave moves faster than the surfer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube