Ashok Leyland: The Hinduja Group's Bet on India's Highways

I. Introduction & Episode Roadmap

Somewhere on the Chennai–Bengaluru corridor tonight, a driver is nursing a fully-loaded tipper up a gradient with the engine note that anyone who has driven Indian highways knows instinctively — the low, unhurried thrum of a Leyland. He is not thinking about EBITDA margins or promoter pledges. He is thinking about diesel prices, tyre wear, and whether the workshop in Hosur has the part he needs. Multiply that driver by a few hundred thousand and you have the actual business: not a stock, but a rolling fleet of steel that moves roughly the majority of what India eats, builds, and burns.

The company that built his truck is India's second-largest commercial vehicle manufacturer, and in the financial year ended March 2026 it had the best twelve months in its seventy-eight-year existence. Standalone revenue reached ₹44,007 crore, up about 14% year on year; profit after tax came in at ₹3,566 crore; and commercial vehicle volumes hit 220,437 units — the highest the company has ever recorded, comfortably past its pre-pandemic FY19 peak of 197,366 units.12 As of early August 2026, the market values the whole thing at roughly ₹1.02 lakh crore.3

Here is the tension worth two hours of your attention. This is a cyclical, capital-intensive, low-differentiation industrial business — trucks are trucks — owned and controlled by a family conglomerate whose roots are in trading and merchant banking, not manufacturing. The Hinduja Group did not build Ashok Leyland. It bought control of it, gradually, through offshore holding vehicles, and then made it the group's most visible industrial asset in India.

That ownership structure is the source of both the company's patience and its most uncomfortable governance question: in March 2026, the promoter entity that holds the controlling stake pledged 106.5 crore Ashok Leyland shares — 18.13% of the company's entire equity — as collateral for a US$1.445 billion margin loan raised alongside other Hinduja entities.4

Meanwhile, the operating business has been doing something genuinely interesting. The truck core got more profitable. And around it, a set of adjacent businesses — buses, defence vehicles, engines and gensets, spare parts, light commercial vehicles, and an electric-vehicle subsidiary that spent years bleeding cash in Yorkshire before finding profitability in Tamil Nadu — grew fast enough that management now describes non-truck revenue as roughly half the top line.5

So the questions this piece will try to answer, and to test rather than assume. Why does Ashok Leyland win against Tata Motors, Mahindra & Mahindra, and VE Commercial Vehicles — and where is that advantage thinner than the company's own narrative suggests? Is the margin improvement of the last three years structural, or is it what every operating-leverage-heavy manufacturer looks like at the top of a demand cycle? Is the electric pivot, having already failed expensively once in the United Kingdom, a lesson learned or the same bet with a cheaper address? And what does a minority shareholder actually own when the controlling shareholder has borrowed against nearly half its stake?

The route this piece takes:

-

How a post-independence, British-licensed assembler became a vertically integrated engine manufacturer — and why a broken partnership in 1975 turned out to be the most valuable thing that ever happened to it.

-

How a trading family bought control from London, in stages, across two decades, and what the absence of disclosure around those transactions should tell a modern investor.

-

What the commercial vehicle business actually is: the freight economics, the financing chain, the regulatory shocks, and the service-network moat that keeps the industry structure remarkably stable.

-

Why the businesses that are not trucks — buses, defence, engines, spare parts, and light commercial vehicles — have become the more interesting half of the story, and what would falsify that claim.

-

The electric vehicle arc, from a Yorkshire factory that could not reach scale to a Tamil Nadu subsidiary that turned profitable, and the battery investment that will test whether the lesson was actually learned.

-

The management record on its own terms: guidance discipline, capital allocation, and how misses have been explained.

-

And the pledge — the thing that has nothing to do with trucks and everything to do with what a minority shareholder actually owns.

The story starts, as many Indian industrial stories do, with a Prime Minister asking businessmen for a favour.

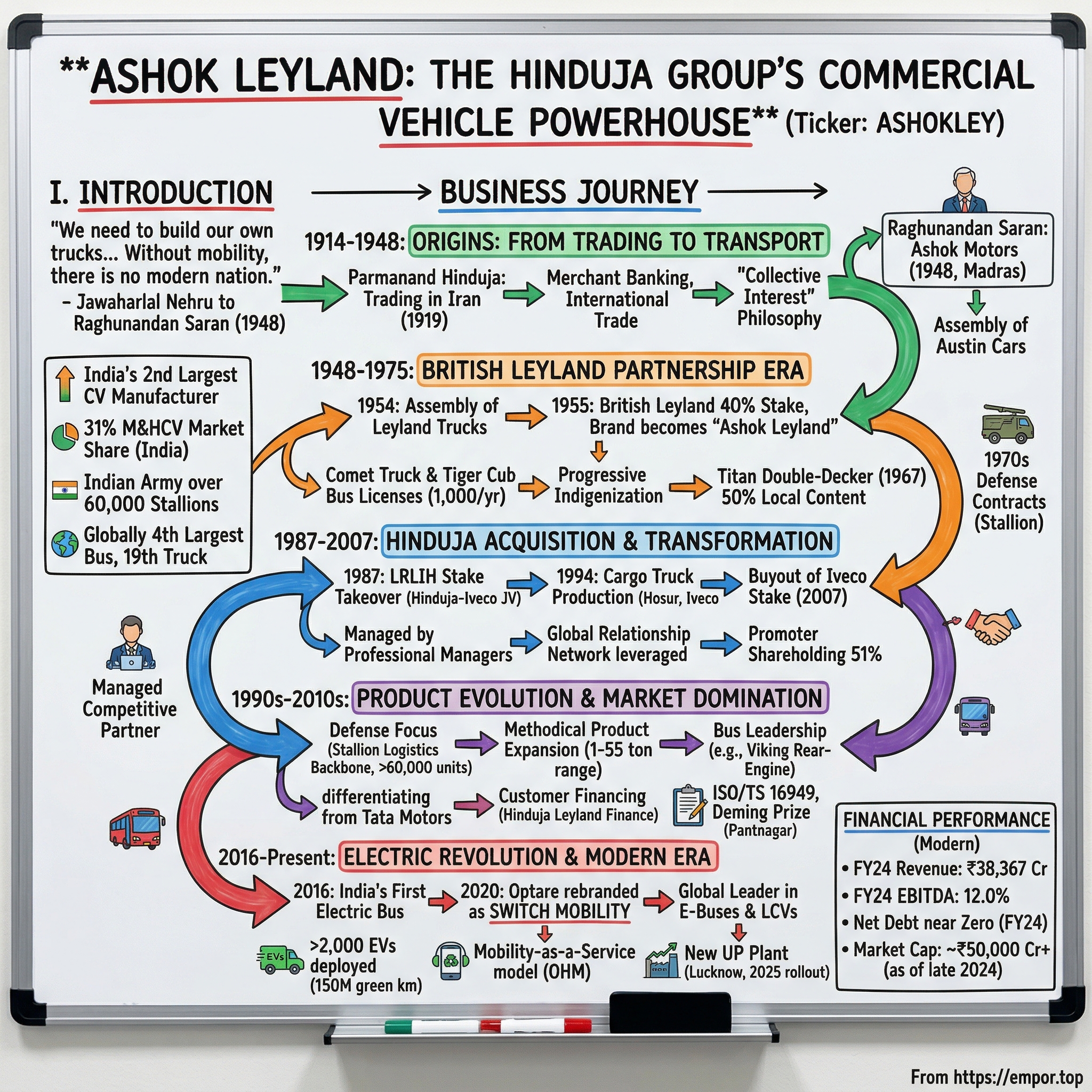

II. Origins: License Raj to Highway Backbone (1948–1987)

In the first years after independence, India had almost no capacity to build a motor vehicle. It had assembly sheds, importers, and a great many ambitions. Jawaharlal Nehru's government wanted a domestic manufacturing base, and it asked the country's trading families to supply one. One of the people who answered was Raghunandan Saran, the son of a Delhi car dealer, who founded Ashok Motors in 1948 in collaboration with Britain's Austin Motor Company.6 He named it after his son, Ashok — an unusually personal act of branding for what was framed publicly as a nation-building venture.

The early product was not trucks. Ashok Motors assembled Austin cars. The pivot to commercial vehicles came through a collaboration with Leyland Motors of the United Kingdom, agreed around 1950, which gave the Indian company rights to import, assemble, and progressively manufacture Leyland trucks. In 1955 the company was renamed Ashok Leyland, with equity participation from the British partner.67 The Leyland Comet truck and the Tiger Cub bus chassis became the physical foundation of Indian road freight and public transport — vehicles that, in modified form, stayed in production for decades because they were rugged, repairable, and cheap to keep alive.

It is worth being precise about the economic environment, because it explains institutional habits that persist today. Under the licensing regime that governed Indian industry until the early 1990s, the binding constraint was not customer demand or competitive pricing. It was permission. Capacity was allocated by government. The number of players was fixed by policy rather than by competitive attrition.

In a system like that, the skill that compounds is not product innovation — it is relationship management with the state and with large institutional buyers. Ashok Leyland's DNA was formed in that environment, and you can still see it in the shape of the business: a dominant position supplying state transport undertakings with buses, and a defence vehicles franchise built on decades of continuous supply to the Indian Army.

Two products from that era deserve a moment, because they explain the company's later positioning. The Comet was a medium-duty truck designed for British road conditions and adapted, painfully and repeatedly, for Indian ones — overloading that would be criminal in Europe was routine here, road surfaces were worse, and maintenance was performed by roadside mechanics with improvised tools. Everything Ashok Leyland learned about durability under abuse it learned in that adaptation.

The Tiger Cub bus chassis, meanwhile, went into state transport fleets across southern India and created the institutional relationships that still underpin the bus franchise seventy years later. Neither product was technologically remarkable. Both were nearly impossible to kill, and in a market where the customer's economics depend on uptime rather than refinement, that is the correct design brief.

The British collaboration ended in 1975, and this turned out to matter more than the collaboration itself. Cut off from a technology parent, the company had no option but to indigenise — to develop its own engine and driveline capability rather than license it. That forced march into in-house engineering is why Ashok Leyland today manufactures its own engines rather than buying them, a vertical integration choice that shapes its cost structure and its ability to redeploy the same engine platform into gensets, marine applications, and defence vehicles. Necessity in 1975 became optionality in 2026.

By the mid-1980s, the picture was of a competent, regionally-anchored, southern Indian truck maker with a protected franchise, a strong bus position, and a shareholder — the British parent, by then folded into the wreckage of the UK motor industry — that was itself in crisis. The asset was about to change hands, and the buyers would not be industrialists at all.

III. The Hinduja Takeover: Building a Flagship (1987–2007)

Picture the Hinduja brothers in the late 1980s: four sons of a Sindhi trader from Shikarpur, operating out of London, Geneva, and Mumbai, with a business built on commodity trading, film distribution in Iran, oil, and finance. They were rich, globally networked, politically well-connected, and — in the Indian industrial imagination — not manufacturers. Trading families were assumed to lack the patience for a business where you sink capital into tooling and wait a decade to earn it back.

In 1987, the overseas holding company that controlled Ashok Leyland — Land Rover Leyland International Holdings, an artefact of the British parent's own restructuring — was taken over by a joint venture between the Hinduja Group and Iveco, the truck arm of Italy's Fiat Group. That holding vehicle's stake in Ashok Leyland was 40% at the time; it was raised to 51% in 1994.78 Note the structure carefully, because it recurs: the Hindujas did not buy Ashok Leyland shares directly. They bought the offshore holding company that owned the shares. Control was exercised one layer removed from the Indian listed entity — the same architecture that, decades later, would make a promoter-level margin loan a live question for minority shareholders.

Why did a trading and merchant-banking group want a heavy industrial asset it had no operating experience in? Three reasons, in descending order of romance. First, legitimacy: in India, owning a nation-building manufacturer confers a kind of standing that a trading balance sheet cannot buy. Second, cash: a truck company at the right point in the cycle throws off real operating cash flow, which is useful to a group that likes optionality. Third, timing: India's economy was four years from liberalisation, and the people best positioned to read that shift were exactly the globally-networked families who had spent decades watching capital move across borders.

The Iveco partnership itself was the industrial half of the bargain — European engineering credibility, access to technology, a route to global platforms. It lasted nineteen years and then ended undramatically. In July 2006, Iveco agreed to sell its 30% holding in Machen Iveco Holding, the parent through which the partners held 51% of Ashok Leyland and 59% of Ennore Foundries, to the Hinduja Group for cash at closing. The joint statement from G.P. Hinduja and Iveco's Paolo Monferino was the corporate equivalent of a handshake at the door: both sides declared themselves "proud of the rapid strides made by Ashok Leyland in product and process technologies over the last two decades."8 The transaction completed in 2007, and from that point the Hindujas held control outright.

Here is a data gap worth flagging rather than papering over: the consideration for that 2006–07 transaction was not disclosed, and no public benchmark multiple exists for the 1987 acquisition either.8 Both deals sit in an era before Indian and European disclosure norms required the kind of forensic detail investors now take for granted. It is instructive to contrast this with Tata Motors' acquisition of Jaguar Land Rover from the same decade — a transaction whose price, financing structure, and strategic logic were argued over in public in real time, and whose consequences investors could therefore track. The Hindujas' consolidation of Ashok Leyland was, by comparison, almost invisible.

That is not evidence of wrongdoing. It is evidence that the ownership history of this company was never subjected to the scrutiny that a modern buyer of the stock might assume.

The two decades between the entry and the buyout were also the two decades in which India changed underneath the company. The 1991 liberalisation dismantled the licensing regime that had guaranteed Ashok Leyland's protected niche. Capacity restrictions went away; so did the guarantee of demand. Imports became conceivable. Foreign manufacturers began evaluating India seriously.

For a company whose entire operating culture had been built around allocation rather than competition, this was an existential adjustment, and it took most of the 1990s to work through — a decade in which the company had to learn, more or less from scratch, how to sell rather than how to be allocated. The Hinduja ownership through that period was, by the standards of the era, competent and unglamorous: capacity was expanded, product development continued, and the company avoided the fate of several Indian industrial names that simply did not survive the transition to open competition.

What the timing did deliver was luck. Full control arrived just as India entered its mid-2000s infrastructure and freight boom, and Ashok Leyland became the flagship listed vehicle of the Hinduja Group — the asset the family is known for, and the one the market prices most closely.9 That status cuts both ways. A flagship attracts capital and management talent. It is also the most liquid, most pledgeable collateral in a conglomerate's portfolio, which becomes a problem for minority shareholders precisely when the rest of the conglomerate needs money.

Before we get to that, we need to understand what the flagship actually does for a living — and why trucks are one of the most brutally honest businesses in the world.

IV. The Core Engine: Commercial Vehicle Industry Structure & Where Ashok Leyland Sits

There is a chart that every commercial vehicle analyst in India keeps somewhere close, and it looks like a cardiogram. Indian medium and heavy commercial vehicle volumes do not grow steadily. They surge for three or four years, collapse by thirty or forty percent, and then surge again. The FY19 peak, the pandemic trough, the FY23–FY26 recovery — this is not a secular growth industry with cyclical noise. It is a cyclical industry with a slow secular drift underneath it.

Why the cycle exists. A truck is a capital good bought by a business to generate freight income. Fleet operators buy when three things line up: freight rates are firm, financing is available and affordable, and there is visible construction, mining, or infrastructure activity to haul. When any one of those breaks, orders do not slow — they stop.

Layered on top are regulatory shocks that reshape demand overnight: axle-load norm changes that instantly increase the carrying capacity of the existing fleet and destroy a year of replacement demand, emission-standard transitions that pull purchases forward and then leave a hole, and scrappage policy that can create demand where none existed. None of these are forecastable with confidence, and all of them move volumes more than product quality does in any given year.

Why it is punishing. Truck manufacturing is fixed-cost heavy. Plants, tooling, engine lines, and a national service network all have to be paid for whether volumes are at peak or trough. That is operating leverage, and it is symmetrical. When volumes rise 13%, as Ashok Leyland's did in FY26, margins expand faster than revenue. When volumes fall 30%, margins do not merely compress — they can vanish. Any investor evaluating this company's recent margin record has to hold that symmetry in mind.

Who actually pays for the truck. It is easy to miss that almost nobody buys an Indian commercial vehicle with cash. The overwhelming majority are financed, often by non-banking finance companies rather than banks, and often to borrowers whose credit history is thin. This has two consequences that outsiders consistently underestimate.

First, the effective price of a truck to the customer is not the sticker price — it is the monthly instalment, which means changes in interest rates and loan-to-value norms move demand as forcefully as changes in vehicle price. A hundred basis points of policy tightening can do more damage to order books than a competitor's new model launch.

Second, the manufacturer with the deepest financing relationships can keep selling when credit tightens, because the financier will underwrite marginal borrowers that others will not. This is the structural reason Tata Motors' financing depth is a genuine competitive asset rather than a footnote, and the reason Ashok Leyland's association with Hinduja Leyland Finance matters more in a bad year than in a good one. A truck company's true competitor set includes balance sheets, not just factories.

Where the players sit. Tata Motors' commercial vehicle business is the incumbent giant, described in industry coverage as India's largest truck and bus maker with roughly 45% share across the medium and heavy commercial vehicle segment.10 Ashok Leyland is the persistent number two: domestic M&HCV market share of 30.8% in FY26, and — importantly — number one in buses with 34.1% share.2 Mahindra & Mahindra is the challenger from below, strong in light commercial vehicles and occasionally overtaking Tata in monthly total CV readings. VE Commercial Vehicles, the Eicher–Volvo joint venture, is smaller but technologically credible, particularly in fuel efficiency and in the light-and-medium duty band.

The interesting structural fact in Ashok Leyland's FY26 numbers is not the M&HCV share, which has been stable above thirty percent for years. It is the light commercial vehicle line. LCV volumes reached 74,322 units in FY26, and VAHAN-registered LCV market share hit an all-time high of 12.7%, up 80 basis points year on year.12 LCVs are a different business from heavy trucks: shorter replacement cycles, more retail and first-time buyers, tighter linkage to consumption and e-commerce logistics than to infrastructure capex. Building share there is genuine diversification of the demand driver, not just extra volume. It is also the segment where Ashok Leyland is structurally weakest against Tata and Mahindra, which is precisely why an 80-basis-point gain matters more than it sounds.

A Porter's Five Forces read, honestly applied. Barriers to entry are high but not because of technology — a competent Chinese or Korean truck maker could engineer an Indian-spec vehicle. The barrier is the service network. A fleet operator will not buy a truck he cannot get repaired in a small town at 2 a.m., and building that coverage takes a decade and a great deal of capital that earns nothing directly.

Buyer power is high and concentrated: large fleet operators negotiate hard, and state transport undertakings buy buses through tenders where price is the dominant criterion. Supplier power is moderate and improving in the manufacturer's favour, since in-house engine manufacturing removes the single largest bought-out component from the negotiation.

Rivalry is intense and share shifts month to month on discounting. Substitution risk is low in the near term — dedicated rail freight corridors take decades to bite, and electrification of long-haul trucking remains a distant proposition in India.

A Hamilton Helmer read. Of the seven powers, the ones with real evidence behind them here are scale economies and, partially, switching costs. Scale shows up in the service and dealer network and in the engine plants — Ashok Leyland manufactures across a global footprint of roughly nine plants, and the fixed cost of that network is spread over more units than any competitor except Tata.9

Switching costs are real but asymmetric: a fleet operator running two hundred Leyland trucks has trained mechanics, parts inventory, and driver familiarity, all of which raise the cost of switching brands. A first-time single-truck buyer has none of that, which is why the LCV segment is contested so ferociously. Branding power exists but is modest — this is not a business where a badge commands a price premium. Counter-positioning, cornered resource, network economies, and process power are not, on the available evidence, meaningfully present.

Myth versus reality. Three consensus beliefs about this company deserve testing.

Myth one: Ashok Leyland is a south Indian regional player gradually going national. This was true for a long time and is now substantially outdated. The company's share position is national in M&HCV, it leads the country in buses, and its fastest share gains in FY26 came in light commercial vehicles, a segment that is intrinsically distributed rather than regional.2 The reality is more interesting than the myth: the remaining regional skew is in service density rather than sales, and network depth in northern and eastern India is where incremental competitive investment has the highest return.

Myth two: the M&HCV cycle is now smoothed by GST, scrappage policy, and infrastructure spending, so the old boom-bust pattern is over. Each of those factors is real and each has moderated the amplitude somewhat. But every one of them is itself a policy variable, which means the cycle has not been eliminated so much as its driver has partly shifted from private freight economics to government capital expenditure decisions. Trading one cyclical driver for another is not the same as becoming non-cyclical, and government capex is not obviously more stable than freight rates over a five-year horizon.

Myth three: electrification is an existential threat to the diesel truck franchise this decade. It is not, at least not in heavy long-haul. The physics and economics of moving forty tonnes several hundred kilometres on batteries, in a country whose highway charging infrastructure is nascent, keep long-haul diesel dominant for years. Where electrification genuinely bites first is exactly where Ashok Leyland has chosen to play: urban buses on fixed routes returning to a depot each night, and last-mile light commercial vehicles. The real risk from electrification is not demand destruction — it is margin compression, because an electric vehicle has fewer serviceable parts, which over time erodes the aftermarket annuity that makes the network economically self-sustaining.

So how does Ashok Leyland actually win? Four mechanisms, each with evidence and each with a limit.

Premiumisation: management has consistently attributed margin gains to a richer product mix, and the FY26 result — EBITDA of ₹5,732 crore at a 13.0% margin, up from 12.7% — is consistent with that claim, though not proof of it.1 The limit is that mix improvement is finite; you can only sell the customer a higher-specification truck once.

Network depth: the aftermarket business, which is spare parts sold through that same network, generated ₹4,450 crore of revenue in FY26, growing 12%.2 That is a high-margin annuity that only exists because the network exists.

Institutional relationships: buses and defence, discussed in the next section.

Cost position: in-house engines, value engineering, and e-sourcing savings, which management cited specifically on the Q4 FY26 call as the offset to material costs that had climbed to 71.4% of fourth-quarter revenue.11

And how does it lose? Tata's scale advantage is not going away, and Tata's captive financing depth gives it a lever in downturns that Ashok Leyland matches only partially through its associate financier. More fundamentally, the margin story has a test it has not yet taken.

Consider the sequence: FY24 EBITDA margin 12.0%, FY25 12.7%, FY26 13.0%.121 That is genuine, consistent improvement. But look one level down. The fourth quarter of FY25 delivered an EBITDA margin just above 15% — the company's high-water mark — while the fourth quarter of FY26 came in at 14.6%, on 19% higher revenue.11 Peak quarterly profitability did not advance; it slipped slightly, even as volumes hit records. That is what commodity cost pressure looks like when it meets a business with limited pricing power, and management's response — price increases of 1% to 1.5% implemented in the first quarter of FY27 to recover steel costs — is the honest tell.11

The analytical conclusion is narrower than the headline. Ashok Leyland has demonstrably improved its through-cycle cost structure and mix. It has not yet demonstrated that a "mid-teens" margin survives a volume decline, because it has not faced one under this management. The evidence supports "better business than it was in 2019." It does not yet support "no longer cyclical."

Which brings us to the part of the story where the company has been trying to change the question entirely.

V. Diversification: When Non-Truck Became Half the Business

If you had walked into Ashok Leyland's Ennore plant in 2015 and asked what the company sold, the answer would have been trucks, with buses as a strong second and everything else a rounding error. Walk in today and the answer is more complicated, and the complication is the most under-appreciated part of the equity story.

By the second quarter of FY26, management was describing non-truck businesses — spare parts, defence, power solutions, and light commercial vehicles — as contributing roughly half of revenue, with double-digit growth across all four and, notably, higher margins than trucks.5 That last clause is the one that matters. Diversification that dilutes margin is empire-building. Diversification into higher-margin adjacencies that share the same engineering base and the same distribution is something else.

Buses: the quiet franchise. Ashok Leyland has held the number one position in Indian buses for years, and retained it in FY26 at 34.1% domestic share.2 Buses are a strange business — dominated by state transport undertaking tenders, with long procurement cycles, political pricing, and payment terms that would make a private-sector CFO weep. But the same chassis engineering, the same plants, and the same relationships that win a Tamil Nadu STU order also win a school bus fleet, a staff transport contract, and — as we will see — an electric bus tender. The bus franchise is the platform on which the electric bet was built.

Defence: from side business to genuine growth engine. For decades Ashok Leyland's defence work was a steady, unglamorous supply relationship: Stallion trucks, the 4x4 and 6x6 workhorses that move Indian Army logistics, produced continuously since the 1990s. Then it started compounding.

In March 2025, the defence business booked multiple orders worth approximately ₹700 crore from the Indian Army for Stallion vehicles and mobility platforms.13 By the third quarter of FY26, defence revenue was growing 84% year on year — the fastest-growing line in the company.14 For the full year, the business crossed ₹1,200 crore with over 20% annual growth and an executable order book above ₹1,500 crore, and Executive Chairman Dheeraj Hinduja told investors that the "Defence order pipeline is at its all-time high."12

In June 2026, management laid out the longer ambition: autonomous variants of the Stallion platform, and a stated addressable defence mobility market of roughly ₹11,000 crore.15 Exports of Stallion variants have gone to Saudi Arabia, Sudan, Thailand, and markets across SAARC and Africa, which is consistent with the company's broader export record — international volumes of 18,082 units in FY26, up 18.5%.2

How should an investor read this? Positively, but with proportion. Defence at ₹1,200 crore is under 3% of standalone revenue. It cannot move the consolidated P&L yet. What it can do is change the quality of earnings: defence orders are contracted, multi-year, less correlated to freight cycles, and typically carry better margins than a discounted fleet truck sale. A company whose fastest-growing segment is also its least cyclical is a company whose future downturns should be shallower than its past ones. That is a real claim, and it is testable — watch what happens to defence revenue the next time M&HCV volumes fall.

Power Solutions: the moat nobody talks about. The engines Ashok Leyland was forced to develop after 1975 do not only go into trucks. They go into diesel gensets, industrial equipment, marine applications, and — in a niche that deserves more attention than it gets — industrial air compressors, where the company holds an estimated domestic share above 75%.

The power solutions business grew 45% year on year in the third quarter of FY26 and crossed ₹1,000 crore of revenue for the second consecutive year in FY26, up 18.8%.142 This is a small business with unusual characteristics: high share in a fragmented niche, sold to industrial buyers who value reliability and service over price, and built entirely on engineering the company already owns. It is the clearest example in the portfolio of an adjacency that costs almost nothing incremental to serve.

Spare parts: the annuity hiding in plain sight. Of all the non-truck lines, the aftermarket is the least discussed and arguably the most economically attractive. A commercial vehicle in India stays on the road for well over a decade, often two, and every one of those years it consumes filters, brake components, clutch plates, and eventually reconditioned engines. The manufacturer that sold the truck has a structural advantage in selling those parts — genuine-part availability through an owned network, warranty linkage, and a captive installed base that grows every year the company sells vehicles.

The economics are the inverse of the truck business. Parts demand is driven by the existing fleet rather than by new purchases, which means it holds up during exactly the periods when new vehicle sales collapse. Margins are structurally higher than on the vehicle itself. Working capital is lighter. And the revenue is annuity-like rather than lumpy.

At ₹4,450 crore in FY26, growing 12%, this is a business roughly four times the size of the defence franchise, and it is the single clearest counter-cyclical stabiliser inside the company.2 It is also, unavoidably, the line most exposed to electrification over a long horizon, since an electric drivetrain simply has fewer wearing parts to replace. That tension — a counter-cyclical annuity today that the company's own electric strategy erodes tomorrow — is one of the more elegant strategic contradictions in the file, and management has not addressed it publicly in any detail.

Financial services: useful, but not the story. Hinduja Leyland Finance, the group's vehicle financier, ended FY26 with assets under management of ₹59,531 crore, up 24%, and profit after tax of ₹491 crore; Hinduja Housing Finance added ₹15,937 crore of AUM.1 For Ashok Leyland, the financier's relevance is as a demand-support tool — a captive-adjacent channel that can keep trucks moving to small operators when banks tighten. It is genuinely useful in downturns. It is also a related-party arrangement inside a family group, and its economics accrue mostly outside the listed manufacturer. Investors should treat it as a distribution asset, not a valuation driver.

The proportionality test. None of these businesses individually rivals the truck core in rupee terms. Trucks and their aftermarket still determine whether the year is good. But the combined growth rate of the non-truck portfolio is materially outpacing the core, and the mix shift is arithmetically inevitable if that persists. The metric that will settle the argument is not revenue mix — it is profit mix, which the company does not break out with enough granularity for an outsider to compute. Until it does, "half the business is non-truck" is a claim about the top line, and investors should hold it at that level of confidence.

The most expensive diversification attempt, though, was none of these. It was the one that went to Yorkshire.

VI. The Electric Pivot: Switch Mobility's Long, Costly Road

In 2016, Ashok Leyland did two things that looked, at the time, like credible early bets on where commercial vehicles were heading: it showed India's first indigenously developed electric bus, and it demonstrated a Euro 6-compliant truck years before Indian regulation required anything close. The intent was real. The execution took a decade and one very expensive detour.

The detour was Optare, the Leeds-based bus manufacturer that Ashok Leyland had acquired a controlling interest in years earlier. In 2020, Optare was rebranded Switch Mobility and repositioned as the group's global electric vehicle platform — a UK-anchored business that would sell electric buses into Britain and Europe while a sister entity, Switch Mobility Automotive, addressed India. On paper the logic was elegant. Europe was decarbonising public transport on an aggressive regulatory timetable; the UK had engineering talent and an existing bus franchise; India would supply cost. In practice, the thesis required European transit authorities to order electric buses at a pace and volume that would give a mid-sized manufacturer scale.

They did not. Switch Mobility lost money year after year. And in March 2025, the reckoning arrived in the form of an exchange filing that is worth reading closely for what it does and does not say: Switch Mobility Limited had initiated a consultation process with employees that could lead to the cessation of manufacturing and assembly operations at its Sherburn-in-Elmet facility.1617 The stated reasons were continuing economic uncertainty in the UK and Europe and a slower-than-expected transition to electric vehicles in public transport.18 Existing orders would be fulfilled and service support maintained through the Rotherham and Thurrock sites; future UK and European demand would be met from Ashok Leyland's manufacturing in India and the United Arab Emirates.16

Strip away the language and this was a strategic reversal. A company that had spent five years positioning a UK manufacturing base as the centre of its global EV ambition concluded that it could not reach economies of scale there. The candid version, which management came close to saying, is that the demand forecast was wrong. The less candid framing — that market conditions changed — is technically true but analytically weak: electric bus adoption in Europe did grow, just not fast enough or profitably enough for a sub-scale entrant competing against far larger European and Chinese manufacturers. This is the single most useful data point in the whole file on management's forecasting record, and investors should keep it on the table.

Then something unexpected happened. The India business, which had been the junior partner in the original structure, worked. In FY26, Switch delivered 1,530 electric buses — a 238% increase — and 1,606 electric light commercial vehicles, up 56%. Revenue roughly doubled to ₹1,807 crore, and the business swung to a profit after tax of ₹104 crore against a loss of ₹62 crore the previous year.1 That is the first full year of net profitability in the entity's history, and it removes a multi-year cash drag from consolidated results.19

Why did India work where Britain didn't? Three reasons, and only one of them is management skill. First, demand: Indian state transport undertakings began procuring electric buses at scale under central and state programmes, creating tender volume that simply did not exist in equivalent form in the UK. Second, cost: an electric bus assembled in India against Indian labour and component costs has a fundamentally different breakeven point. Third — and this is the credit management deserves — distribution. Switch India was selling into the same STU relationships that Ashok Leyland's diesel bus business had been cultivating for fifty years. It was not entering a market; it was electrifying an existing one. The UK operation had no equivalent incumbency to lean on.

There is a mechanical detail here that materially changes the risk profile, and it deserves explaining because it is unfamiliar to most equity investors. Indian electric bus procurement has largely moved away from outright purchase toward contracting models in which the manufacturer or an operator supplies buses and is paid per kilometre operated over a contract of a decade or more. Think of it as the difference between selling someone a printer and selling them a per-page printing service.

The upside is a long, contracted, annuity-like revenue stream with visibility that a diesel bus sale never had. The downside is that the manufacturer carries the asset, the battery degradation risk, and the counterparty risk of a state transport undertaking's ability to pay, for years.

It converts a working-capital business into something closer to an infrastructure business, and it means that reported profitability in any single year says less about the venture's economics than the eventual realised return over the full contract life. One profitable year at Switch is genuinely good news. It is not yet proof that the contract economics work across a full asset cycle, and investors should hold both thoughts simultaneously.

The next bet. Having learned that lesson, the company then made a considerably larger one. In early September 2025, Ashok Leyland announced a partnership with 中创新航 CALB, the Chinese battery technology group, to localise battery manufacturing in India — a plan framed publicly at over ₹5,000 crore of investment across seven to ten years, with some coverage citing an eventual ceiling closer to ₹10,000 crore.202122 The structure is worth understanding, because it is where the discipline question lives.

Think of a battery system as three layers, like a Russian doll. The innermost layer is the cell — the actual electrochemistry, enormously capital-intensive, technologically demanding, and the layer where Chinese manufacturers have a decisive global lead. The middle layer is the pack — cells wired together with structural housing, cooling, and safety systems. The outer layer is the battery management system, the software and electronics that decide how the pack charges, discharges, and protects itself. Pack assembly is comparatively cheap to enter and delivers most of the near-term localisation benefit. Cell manufacturing is where the money and the risk are.

Ashok Leyland started at the outer layer. The first phase is a battery pack facility, with reported first-tranche investment of ₹400–500 crore, ground broken at the SIPCOT industrial park in Pillaipakkam, roughly 43 kilometres from Chennai, on 11 March 2026, with Tamil Nadu Chief Minister M.K. Stalin unveiling the foundation plaque.2324 Production is targeted for 2027.24

Notably, CALB is not investing directly in the venture — a structure that keeps the arrangement a technology partnership rather than a Chinese equity investment, avoiding the regulatory friction that Chinese FDI attracts in India.21 On the Q4 FY26 call, management confirmed the battery business sits inside Ashok Leyland rather than in a separate subsidiary, meaning the spend flows through the parent's capital expenditure, and said construction would begin within eight to ten weeks with production expected in the second quarter of the following year.11 Full-year FY27 capital expenditure guidance was set at ₹750–1,000 crore.11

The credibility test. Is the phased structure — small first tranche, cell manufacturing deferred, scaling contingent on demand — a lesson learned from Sherburn, or the same optimism with better packaging? The honest answer is that the structure is materially more disciplined than the UK bet was, and the thesis is not yet proven.

What is genuinely different: the first commitment is roughly a tenth of one year's operating cash flow, it sits adjacent to a customer base the company already owns, and the demand it serves is partly captive — Switch's own buses and LCVs need packs.

What is not different: the eventual ₹5,000–10,000 crore ambition depends on Indian commercial EV adoption arriving on schedule, which is precisely the class of forecast the company got wrong in Europe. Investors should treat the ₹400–500 crore as a real decision and the ₹5,000 crore as an intention, and should watch whether the second tranche is committed before or after demand shows up.

The person who has to make that call has been in the job for three and a half years, and his record so far is better than his hardest test.

VII. The Shenu Agarwal Era: Management, Incentives & Capital Allocation

When Shenu Agarwal was named Managing Director and Chief Executive Officer of Ashok Leyland, effective 8 December 2022, the appointment raised eyebrows for a specific reason: he did not come from trucks.2526 He came from Escorts Kubota, where he had been President and had run the agri-machinery business for more than seven years — tractors, not tippers. The company's own announcement framed his contribution there as ushering in "contemporary global standards of design, quality, and manufacturing."26

That background turns out to explain a great deal about how he has run the company. Tractors are sold to individual farmers through dense rural dealer networks, where after-sales service and financing availability determine repeat purchase far more than horsepower does. It is a business about distribution intensity and product-line segmentation, not about winning big fleet tenders. Agarwal brought that lens to a truck company, and the strategic vocabulary he has used consistently since arriving — premiumisation, network expansion, cost optimisation, digital enablement — is essentially a distribution-and-mix playbook applied to commercial vehicles.

What the record shows. The margin trajectory under his tenure is the headline: from roughly 11% EBITDA in FY23 through 12.0% in FY24, 12.7% in FY25, and 13.0% in FY26, against a stated medium-term ambition of mid-teens.121 Profit after tax rose from ₹2,618 crore in FY24 to ₹3,303 crore in FY25 — a 26% increase — and then to ₹3,566 crore in FY26, a slower 8% gain that included a ₹308 crore charge related to India's new Labour Codes.271 Ex-that charge, the underlying progression was stronger, and operating profit before tax grew 22% to ₹5,163 crore — a gap between headline and operating growth that investors should note rather than ignore, because one-time charges have a habit of recurring in different costumes.1

Capital allocation is where the behaviour gets legible. FY25 was the shareholder-return year: two interim dividends totalling ₹6.25 per share — 625% of the ₹1 face value, comprising ₹2 declared in November 2024 and ₹4.25 in May 2025 — alongside a 1:1 bonus issue announced with the FY25 results and issued on 17 July 2025.272 In FY26, with the share count doubled, total interim dividends came to ₹3.50 per share, which on the pre-bonus base is the equivalent of ₹7.00 — a real increase, not a maintained payout dressed up.12

Simultaneously, the balance sheet strengthened dramatically. Standalone net cash rose from ₹4,242 crore at the end of FY25 to ₹5,899 crore at the end of FY26, an improvement of over ₹1,650 crore even after paying dividends and spending ₹1,050 crore of capital expenditure during the year.111 Agarwal himself pointed to the "record cash surplus of nearly ₹6,000 Cr" as the thing that enables future investment.1 It is a fair point, and it is also the strongest evidence available that the operating improvement is converting to cash rather than sitting in working capital — a distinction that matters enormously in a business where receivables from state transport undertakings can be creative.

Narrative consistency, tested. One of the more useful exercises with any management team is to line up what they said across several calls and look for drift. Here, the language has been unusually stable. The four-pillar margin story has been repeated across FY25 and FY26 calls without meaningful revision.

In September 2025, Agarwal publicly forecast that Indian commercial vehicle sales would cross the pre-pandemic peak in FY26 — a specific, falsifiable prediction that the FY26 volume record subsequently validated at least for the company's own book.28 Guidance for FY27 has been set at 5–7% growth for the Indian M&HCV segment, supported by the infrastructure pipeline and replacement cycle — a deliberately modest number after a 13% volume year.29 Setting conservative guidance after a record is a mildly good sign; it is the opposite of the pattern where a management team extrapolates a peak.

Where the record is weaker. On Switch Mobility's UK retreat, the explanation offered leaned on external conditions — economic uncertainty and slower EV adoption — rather than on an admission that the original capacity and demand assumptions were wrong.18 Both things can be true, but the framing consistently placed causation outside the company. Investors evaluating whether the battery investment reflects genuine learning should note that the process changed more than the explanation did.

Similarly, on the Q4 FY26 call, when material costs rose to 71.4% of revenue, the response emphasised value engineering and e-sourcing savings and pricing actions — concrete answers, to be fair, but answers about mitigation rather than about why the cost pressure was not anticipated.11

The other half of the leadership equation. Ashok Leyland is not run by its CEO alone. Dheeraj Hinduja serves as Executive Chairman — an active role rather than a ceremonial one, and the channel through which the controlling family's strategic preferences enter the company. It was the Chairman, not the CEO, who framed the defence pipeline as being at an all-time high in the FY26 commentary.1 The FY26 annual report placed a resolution on the Executive Chairman's re-appointment before the 77th Annual General Meeting scheduled for 14 August 2026.2

For investors, the practical implication of an executive-chairman structure in a promoter-controlled company is that the board's independent directors carry a heavier burden than usual, because the two most senior executive roles are not independent of each other in the way a separated chair-and-CEO model provides.

Incentive alignment is the structural caveat. Agarwal is a professional manager, not a controlling shareholder. The controlling stake sits with Hinduja Automotive Limited, and executive compensation and key performance indicators are disclosed in the annual report's remuneration section rather than being inferable from equity ownership.30 This is not unusual and not inherently negative — professional management with conservative guidance and rising dividends is a reasonable configuration. But it does mean that when the interests of the controlling family and the interests of minority shareholders diverge, the CEO is not the person who resolves it.

Which is exactly what the next section is about.

VIII. Governance Stress Test: The Hinduja Pledge

On 25 March 2025, a routine-looking disclosure hit the exchanges. Hinduja Automotive Limited, the promoter entity through which the family controls Ashok Leyland, had pledged 30 crore shares — approximately 10.21% of the company's paid-up capital, worth roughly ₹6,400 crore at prevailing prices — with lenders.31 The following day, a further pledge of similar size was created, taking the aggregate encumbrance to 25.59% of the company.31 By that point, roughly 42.5% of Hinduja Automotive's total holding in Ashok Leyland was pledged. The stock fell on the news, though the move was tangled up with broader concerns about the Hinduja Group and separately-timed news on US automotive tariffs.32

Then, a year later, the picture changed shape rather than disappearing. On 27 March 2026, a margin loan agreement was executed with a consortium of global banks — J.P. Morgan Securities, Barclays Bank, Citibank, and Deutsche Bank — for a term facility of up to US$1.445 billion. Hinduja Automotive pledged 106.5 crore Ashok Leyland shares, representing 18.13% of the company's total equity, with Catalyst Trusteeship Limited as onshore security agent and no voting rights transferred. The co-borrowers included QH Hungary Holdings, IndusInd International Holdings, and other Hinduja entities.4

What this actually means, in plain terms. A share pledge is a margin loan against stock. The promoter borrows money and posts Ashok Leyland shares as collateral. If the share price falls far enough, the lender can demand additional collateral or, in the extreme, sell the shares. The risk to a minority shareholder is not that the company is doing anything wrong — Ashok Leyland's operations are entirely unaffected — but that a forced sale by the controlling shareholder would flood the market with stock and, in the worst case, destabilise control of a company they own a piece of.

Three observations, in order of importance.

First, the purpose of the borrowing matters, and it is not about Ashok Leyland. The co-borrower list is the tell. IndusInd International Holdings is the Hinduja vehicle that acquired Reliance Capital — a large, capital-hungry financial services transaction entirely separate from the truck business. In other words, the listed manufacturer's most liquid asset is being used as collateral to fund the group's ambitions elsewhere. That is precisely the flagship-asset dynamic flagged earlier: being the group's best asset is not an unambiguous good for the people who own the other half of it.

Second, the March 2026 transaction is a refinancing, not a de-pledging. The prior encumbrance was released and a new, differently-sized one created against a larger, longer-dated facility with a syndicate of top-tier international banks.4 The optimistic read is that global banks conducted diligence and were willing to lend at scale, which is a form of external validation of both the collateral and the borrower. The skeptical read is that the pledge has now been institutionalised as a permanent feature of the capital structure rather than a temporary bridge.

The percentage figure fell from 25.59% to 18.13%, but note that the share count doubled in between due to the bonus issue, so comparing percentages across that boundary requires care — the absolute number of shares encumbered rose.

Third, the disclosure quality is adequate but the strategic communication is not. The encumbrance filings are made and are public. What is absent from the public record is any management statement of a de-pledging timeline, a target encumbrance level, or a commitment about future pledges. Promoters are not obliged to provide one. But the absence is itself information: it suggests the arrangement is expected to persist. A separate declaration from Hinduja Foundries Holding Limited, another promoter entity, confirmed no new encumbrances were created by it during FY26 beyond those previously disclosed — useful, but narrow in scope.33

What a minority shareholder can actually monitor. This is worth being practical about, because the temptation is either to ignore the pledge entirely or to treat it as a reason to dismiss the company. Neither is right. Three observable signals exist, and all three are free.

The quarterly shareholding pattern discloses encumbrance as a percentage of promoter holding and of total capital. A rising trend without a corresponding rise in the group's disclosed funding needs would be the warning. A falling trend, sustained across several quarters, would be genuine de-risking rather than refinancing.

Second, the price level matters mechanically. Margin loans carry maintenance thresholds, which means the risk is not linear — it is negligible above a certain share price and abruptly material below it. Since the specific covenant levels are not disclosed, outsiders cannot calculate the trigger, which is itself a limitation worth acknowledging rather than modelling around.

Third, watch the borrower's other obligations. The co-borrowers are financial-sector entities whose own capital requirements are visible through their own disclosures. Stress there transmits here.

Balance. Promoter pledging is common in Indian family conglomerates and is not evidence of distress or impropriety by itself. Plenty of well-run companies have pledged promoter stakes for years without incident. The lenders here are among the most conservative institutions in the world, and they lent against a business generating record cash. But the honest framing for a minority shareholder is this: you are exposed to the credit quality of a private, unlisted holding structure whose financials you cannot see, whose other obligations you cannot size, and whose collateral is the very stock you own. That is a real risk premium, and it should not be argued away.

It is also, in a sense, the price of the thing that made this company what it is.

IX. Playbook: Lessons from a Cyclical, Conglomerate-Backed Industrial

Step back from the quarter-to-quarter and five patterns emerge that generalise well beyond one Indian truck maker.

Patient capital is not automatically wise capital. The Hinduja Group's long ownership horizon funded genuinely good things: the indigenisation of engineering, a two-decade buildout of manufacturing and network capacity, and a willingness to invest through downturns that a quarterly-reporting management under activist pressure might not have sustained. The same patience funded a UK electric bus operation for years past the point where the numbers were sending a clear signal.

Long-term capital removes the discipline of the market's impatience, which is a benefit when the market is wrong and a cost when it is right. The distinguishing variable is not time horizon but whether the owner has a mechanism for admitting error. Sherburn suggests the mechanism exists but operates slowly.

Operating leverage is a promise you make to the future. Every fixed cost added in an up-cycle is a claim on cash in the down-cycle. Ashok Leyland's margin gains from FY23 to FY26 were achieved during a period of rising volumes, which flatters any manufacturer. The company's own history is the best evidence: this is a business that has previously seen volumes halve. The question for the next few years is not whether margins can rise further — it is what they do at 70% of FY26 volumes. Management's mid-teens ambition is a claim about the peak; the number investors should care about is the trough.

Adjacent diversification works; distant diversification usually doesn't. Compare the two experiments. Defence and power solutions used the same engines, the same plants, the same engineering, and — critically — customer relationships the company already had. Both grew fast and profitably with minimal incremental capital.

The UK electric bus venture required new customers, new regulatory relationships, new cost structures, and a new competitive set, in a geography where the company had no incumbency. It failed. The EV bet only started working when it was pulled back toward the core — Indian manufacturing, Indian cost base, Indian bus customers the company had served for decades. The lesson is not "don't diversify." It is that the transferable asset in an industrial business is usually distribution and relationships, not technology, and diversification that travels along those rails succeeds far more often than diversification that abandons them.

Service networks are the moat that doesn't show up on a balance sheet. In a market where three manufacturers can build a functionally similar truck at a similar cost, the differentiator is what happens after the sale. The aftermarket parts business is the financial expression of that network, and its steady growth is the evidence. It also explains why entry barriers in Indian commercial vehicles have held for decades despite the absence of any real technological secret: a new entrant can copy the truck in two years and cannot copy the workshop coverage in ten.

The corollary is that any erosion of network density — dealer closures, service quality decline, parts availability problems — would be a leading indicator of competitive trouble long before market share moved.

A record year is the worst moment to extrapolate, and the best moment to check the balance sheet. There is a version of this story that reads the FY26 results as the beginning of a re-rating. There is another that reads them as the top. The useful discipline is to separate the two things a peak year actually produces.

One is an earnings number, which is the least durable output of a cyclical business and the one most likely to be extrapolated by mistake. The other is a balance sheet position — cash built, debt retired, capacity paid for out of operating cash flow — which is durable precisely because it survives the cycle turning.

On that second measure Ashok Leyland's FY26 was more impressive than the profit headline suggests: the company funded its capital expenditure and raised its dividend while still adding materially to net cash. A company that enters a downturn with cash and no refinancing pressure has options that a leveraged competitor does not, and those options — countercyclical capacity investment, distressed dealer support, share gain through a bad year — are how cyclical businesses compound over decades rather than merely oscillate.

The uncomfortable footnote is that this logic applies to the operating company, not to the entity that controls it. The strength sits one level below where the leverage sits.

With the frameworks established, it is worth laying out both sides of the argument as sharply as possible.

X. Bull vs. Bear Case

The bull case, stated at its strongest.

The core proposition is that Ashok Leyland in 2026 is a structurally better business than the one that existed in 2019, and the market is still partly pricing it as the old one. Four supports.

Margin improvement is now multi-year and multi-source, moving from 12.0% to 12.7% to 13.0% at the full-year level across FY24 to FY26, with the improvement attributed to mix, network, and cost programmes rather than to a single favourable input.121 Crucially, the improvement was accompanied by cash generation, not just accounting profit — net cash grew by more than ₹1,650 crore in FY26 while the company paid dividends and invested.1

The demand base is broadening. Light commercial vehicles at a record 12.7% share and 74,322 units, exports at a record 18,082 units, defence growing over 20% with an all-time-high pipeline, power solutions past ₹1,000 crore, and spare parts at ₹4,450 crore together represent a set of revenue streams whose cycles do not perfectly correlate with heavy truck demand.12 A business with four uncorrelated growth engines deserves a different multiple from a business with one.

The electric drag is gone. Switch's swing from a ₹62 crore loss to a ₹104 crore profit removes a persistent cash consumer and converts it into an option — with a real order book, a manufacturing footprint, and a battery localisation programme that starts small.1 Early-mover position in Indian electric buses, built on incumbent STU relationships, is a genuinely defensible starting point.

And capital allocation behaviour has been shareholder-friendly and consistent: rising dividends, a bonus issue, conservative forward guidance after a record year, and capital expenditure of ₹750–1,000 crore guided for FY27 that is comfortably covered by operating cash flow.1129

The bear case, stated at its strongest.

FY26 has all the characteristics of a cycle peak: record volumes, record revenue, record profit, record cash, and management guiding to 5–7% industry growth from that base.29 Indian M&HCV cycles do not plateau gracefully. If volumes decline meaningfully, the operating leverage that manufactured the margin story runs in reverse, and it does so quickly. The evidence that the improvement is structural rather than cyclical does not yet exist, because the test has not been administered.

The competitive position is stable but not improving where it counts most. Tata Motors retains a decisively larger share of the medium and heavy segment and a financing apparatus with more depth.10 Ashok Leyland's M&HCV share has hovered around thirty percent for years — respectable, defended, and not expanding. In a business where scale drives cost, being permanently second is a permanent handicap. Mahindra's LCV momentum caps the segment where Ashok Leyland is gaining, and VE Commercial Vehicles keeps technological pressure on efficiency claims.

The already-visible margin ceiling is a warning. Fourth-quarter FY26 profitability came in below fourth-quarter FY25 despite substantially higher revenue, because material costs rose and the response was a 1–1.5% price increase implemented after the fact.11 That is the signature of a business with limited pricing power operating in a commodity-exposed cost structure. Mid-teens margins through a cycle are a hypothesis, not a demonstrated capability.

The battery commitment is the same class of risk that already cost real money. Sherburn was a bet on the pace of electric adoption in a market management did not control. The ₹5,000–10,000 crore battery ambition, and particularly any eventual move into cell manufacturing, is a bet on the pace of electric adoption in commercial vehicles in India.2022 The first tranche is disciplined. The plan is not, if it is executed in full on an ambitious timeline.

And the governance overhang is unresolved and structurally permanent-looking. An 18.13% encumbrance on the company's equity, held as collateral for group-level borrowing whose purposes lie entirely outside the truck business, with no stated path to release, is a risk that a minority shareholder cannot hedge, diligence, or influence.4

Scoring the powers against the peer set. Held up against Tata Motors, Mahindra, and VE Commercial Vehicles, the picture is of a company with one clear advantage, one clear disadvantage, and a lot of parity.

The clear advantage is buses and institutional relationships. No competitor matches the depth of Ashok Leyland's state transport undertaking and defence franchises, and both are relationship-based rather than product-based, which makes them slow to erode. That advantage is now compounding into electric buses, where the incumbent relationship converted directly into an order book.

The clear disadvantage is scale within the heavy truck segment itself, where a competitor roughly half again as large amortises development and network costs over more units and finances more of its own sales.10 Scale differences of that magnitude do not close through better execution; they close only through a competitor's mistake or a structural market shift.

Everything else is parity. Product capability, emissions technology, dealer coverage in core markets, and cost position are all close enough that share moves on discounting and availability rather than on capability. This is why the industry structure has been so stable for so long, and it is also why margin, not share, is the correct scorecard for this company. Share gains bought with discounts are worth less than margin held at flat share.

The activist stress test. What would a skeptical investor push hardest on? Three things.

First, disclosure: the company reports revenue mix by segment but not enough profitability detail for outsiders to verify the claim that non-truck businesses carry higher margins — a segmental profit disclosure would settle the single most important question in the equity story, and its absence is a choice.

Second, related-party architecture: the financing associate, the technology arm, and the various Hinduja entities create a web where value can leak in either direction, and minority shareholders are dependent on the audit committee to police it. This is not an allegation of anything; it is an observation that the structure requires trust in a governance process rather than in a disclosure.

Third, the pledge: an activist would demand a stated de-pledging schedule as a condition of supporting management resolutions, and would point out that the company's own record cash surplus does nothing to address a liability that sits one level above it.

Where the balance actually falls. The honest resolution is that the bull case and the bear case are not in conflict about facts — they are in conflict about the durability of the same facts. Both sides agree the business improved. The bull believes the improvement is architectural; the bear believes it is cyclical with an architectural veneer. That argument will be settled by data, not by narrative, and the data will arrive when volumes fall.

XI. Risk Radar

Demand cyclicality is the dominant risk, and everything else is second. Commercial vehicle replacement demand is a derivative of freight rates, infrastructure capital expenditure, and construction and mining activity. When India's infrastructure spend decelerates or freight rates soften, fleet operators defer purchases immediately — a truck bought this year can almost always be bought next year instead. Because manufacturing costs are largely fixed, a volume decline compresses margin faster than it compresses revenue. This is not a hypothetical; it is the mechanism that has driven every previous downturn in this industry. Ashok Leyland's guidance of 5–7% industry growth for FY27 assumes the cycle extends.29

Execution risk in the electric transition is concentrated and time-sensitive. The Pillaipakkam battery pack facility targets production in 2027, with cell manufacturing contemplated in later phases.2324 The economics of that investment depend on Indian electric bus and electric light commercial vehicle volumes scaling roughly on the timeline management projects. If adoption lags — because charging infrastructure buildout is slower than expected, because state procurement budgets tighten, or because battery prices fall so fast that a domestic pack plant loses its cost rationale against imports — the capital is stranded in a facility with limited alternative use.

Note the specific asymmetry: falling global battery prices are good for Switch's vehicle business and bad for the case for making packs domestically.

Input cost and pricing power. Steel and other commodity inputs flow into the cost base with a lag and can only be recovered through price increases that the competitive structure limits. The FY26 fourth quarter demonstrated the mechanism clearly — material cost at 71.4% of revenue, with price recovery implemented only in the following quarter.11 In a soft demand environment, that recovery becomes far harder to push through.

Geopolitical and trade exposure. The 2025 round of US tariff actions on automobiles contributed to sentiment pressure on Indian auto stocks including Ashok Leyland, even where direct exposure was limited.32 More directly relevant, the demand uncertainty in UK and European public transport was the proximate cause of the Sherburn decision.18 Export volumes at a record 18,082 units are concentrated in GCC, African, and South Asian markets, which carry their own currency, payment, and political risks.2

And the CALB partnership involves a Chinese technology counterparty in a policy environment where India–China investment relations remain politically sensitive — the structure deliberately avoids Chinese equity participation, but technology dependence is still a dependency.21

Refinancing and governance risk at the promoter level. The US$1.445 billion facility is a group-level obligation, not the company's, but its collateral is the company's stock.4 Rising global rates, a fall in the share price, or stress elsewhere in the Hinduja portfolio would each transmit into this equity through the collateral channel rather than through the P&L. Shareholding pattern filings, which disclose encumbrance levels quarterly, are the monitoring mechanism available to outside investors.

Competitive intensity. Tata Motors' scale and Mahindra's light commercial vehicle momentum together cap the realistic ceiling on both pricing and share gains.10 The risk is not dramatic share loss — the market structure has been stable for years — but rather that competitive pressure quietly consumes the mix and cost gains that management is booking as structural margin improvement.

Second-layer items worth a brief note rather than a section. Three smaller things belong on the radar without being inflated.

On accounting judgment: FY26 profit absorbed a one-time provision related to India's new Labour Codes, which is a genuine estimate rather than a settled liability, and comparable charges may recur across Indian manufacturers as the codes are implemented state by state.1 It is a legitimate charge, not an aggressive one, but it is a reminder that headline profit growth and operating profit growth diverged this year for a reason.

On regulatory and climate exposure: the FY26 annual report disclosed renewable energy use rising to 77% of consumption and operational carbon emissions down over 61% since FY19.2 For a diesel engine manufacturer, the operational footprint is the smaller half of the exposure — the product footprint is what future emissions regulation will price, and that is a cost the whole industry will carry together rather than a company-specific disadvantage.

On concentration: the defence franchise, valuable as it is, has one dominant customer whose procurement timing is political and lumpy. A quarter of weak defence revenue is more likely to reflect an order cycle than a lost position, and investors should avoid over-reading either direction in any single period.

XII. Future Outlook & What to Watch

As of August 2026, the company sits at an unusual juncture: its best-ever operating year is behind it, its guidance for the current year is deliberately modest, and the two largest open questions — battery capital discipline and promoter leverage — will both be answered by disclosure rather than by operations.

The battery scaling decision. The pack facility is under construction with a first tranche of ₹400–500 crore.24 The decision that matters is the second one: whether the company commits to cell manufacturing, at what scale, and on what evidence. A move into cells would multiply the capital at risk by an order of magnitude and would put Ashok Leyland into direct competition with global cell manufacturers operating at vastly greater scale. Watch whether the trigger for that commitment is stated in terms of demand thresholds or in terms of a timeline. The former would be genuine discipline; the latter would rhyme uncomfortably with Sherburn.

Margin through a full cycle. The mid-teens EBITDA ambition remains management's stated medium-term target. The meaningful observation will not come from another record quarter. It will come from the first quarter in which volumes decline year on year, and what margin does in that quarter. Until that observation exists, the structural-versus-cyclical debate is unresolvable.

Defence scaling and programme wins. The executable order book above ₹1,500 crore and the stated ₹11,000 crore addressable mobility opportunity give a clear framework for tracking.115 The specific things worth watching are conversion of the pipeline into contracted orders, any award in the autonomous platform programmes management has discussed, and whether export defence volumes broaden beyond the existing Middle East, African, and South Asian markets.

The pledge trajectory. Each quarterly shareholding pattern filing discloses promoter encumbrance. The direction of that number over the next several quarters — and whether management or the promoter ever articulates a target — is the single cleanest read on whether the March 2026 refinancing was a bridge or a permanent structure.

Capital allocation as a behavioural signal. With capital expenditure guided at ₹750–1,000 crore against a materially larger cash pile, the company has more capacity than it currently has committed uses for.11 That surplus creates a choice, and the choice is informative.

Continued dividend growth and organic investment would be consistent with the discipline management has claimed. A large acquisition, a step-up in the battery commitment ahead of demand evidence, or an increase in intra-group exposure would each say something different. Watching which of those happens is more informative than any guidance statement, because capital allocation is the one form of communication a management team cannot fake.

The three KPIs that matter most. Cutting through everything above, an investor tracking this company over the next several years needs remarkably few numbers.

First, EBITDA margin measured against volume direction. Not the margin in isolation — the margin paired with whether volumes rose or fell that period. A margin holding above the low teens in a quarter of declining volumes would be the strongest possible evidence that the cost structure genuinely changed. A margin falling back toward single digits on a volume decline would settle the question the other way.

Second, the non-truck share of profit, not revenue. Management's claim is that the diversified businesses carry higher margins than trucks. Revenue mix is disclosed; profit mix is not, with the granularity required. As segmental disclosure improves — or as investors can infer it from defence, power solutions, and aftermarket growth rates against consolidated margin — this becomes the test of whether diversification is creating value or merely adding activity.

Third, Switch Mobility's order-to-delivery conversion and standalone profitability. One profitable year does not establish durability, particularly in a business that depends on government procurement timelines. The specific things to track are whether the order book converts into delivered units on schedule and whether profitability persists as the mix shifts from buses toward light commercial vehicles, where competition is far more intense.

XIII. Recent News

The most recent reported period is the fourth quarter and full year of FY26, announced on 28 May 2026, which delivered the record results detailed throughout this piece — including a fourth-quarter profit of ₹1,405 crore, up 13%, and consolidated fourth-quarter revenue of ₹17,246 crore.341 The FY26 annual report was subsequently filed, disclosing research and development spending of ₹635 crore, or 1.44% of turnover, and confirming the company's 77th Annual General Meeting for 14 August 2026, with a resolution on the re-appointment of the Executive Chairman on the agenda.2

Quarterly results for the first quarter of FY27, covering the June 2026 quarter, are scheduled for release on 14 August 2026 — four days after the date of this writing.29 Ahead of that, monthly volume data showed continued double-digit growth in June 2026 across the Indian commercial vehicle sector, with both Tata Motors' CV business and Ashok Leyland shares responding positively to the volume prints.35 Management's stated expectation for the full year remains 5–7% growth in the domestic M&HCV segment, supported by the infrastructure pipeline and replacement cycle.29

On the battery programme, the position as of August 2026 is that the location question has been settled — Pillaipakkam, Tamil Nadu — construction has commenced, and the production target remains 2027 for pack manufacturing, with cell manufacturing explicitly described as a later phase.2411 No decision on cell manufacturing capacity or location has been disclosed.

On the promoter share pledge, the most recent development remains the March 2026 refinancing into the US$1.445 billion margin loan facility, with 18.13% of the company's equity encumbered.4 No de-pledging timeline has been disclosed.

On defence, the FY26 order book above ₹1,500 crore and the all-time-high pipeline described by the Executive Chairman are the latest disclosed positions, with management having outlined the autonomous Stallion programme and the broader ₹11,000 crore addressable market in June 2026.115 No new contract award has been announced since the FY26 results.

The near-term calendar is therefore unusually dense. Within the same week, the company will report a quarter, hold its annual general meeting, and put its Executive Chairman's re-appointment to a shareholder vote.229 For an investor working through the questions this piece has raised, that combination is the next real information event — the first-quarter numbers will speak to whether the demand cycle is extending as guided, and the meeting is the venue where the governance questions can be asked out loud.

References

-

Ashok Leyland reports record volumes, revenue and profitability in Q4 and FY26 — Autoguideindia, 2026 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Ashok Leyland Files FY26 Annual Report: Record Revenue, Volumes and EV Milestones — ScanX, 2026 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Catalyst Trusteeship pledge on 106.5 crore Ashok Leyland shares — ScanX, 2026-03-27 ↩↩↩↩↩↩

-

A look at Ashok Leyland's 75 year old journey in India — Autocar Professional ↩↩

-

Hinduja Group acquires Iveco's stake in Ashok Leyland — Iveco press release, 2006-07-24 ↩↩↩

-

How Tata Motors commercial vehicle stacks up against M&M, Ashok Leyland, Eicher Motors — Upstox ↩↩↩↩

-

Ashok Leyland Ltd (BOM:500477) Q4 2026 Earnings Call Highlights — GuruFocus via Yahoo Finance, 2026-05-28 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Ashok Leyland Q4 results FY24: net profit rises 16.73% — Business Standard, 2024-05-24 ↩↩↩

-

Ashok Leyland's defence business bags orders worth Rs 700 cr from Indian Army — Business Standard, 2025-03-28 ↩

-

Ashok Leyland Q3 FY26 result: Net profit rises to ₹796 crore, revenue increases 22% YoY — Upstox, 2026-02-11 ↩↩

-

Ashok Leyland bets on autonomous Stallion and ₹11,000 crore defence market — Business Standard, 2026-06-12 ↩↩↩

-

Switch considers potential ceasing of UK manufacturing operations, will double down on India EV market — Ashok Leyland press release, 2025-03 ↩↩

-

Switch Mobility to stop manufacturing in UK (Sherburn) — Sustainable Bus, 2025 ↩

-

Demand dip: Switch Mobility UK decides to shut down its Sherburn plant — Business Standard, 2025-03-26 ↩↩↩

-

Ashok Leyland Accelerates EV Push as Switch Mobility Turns Profitable — Truck Bus India, 2025-11-15 ↩

-

Ashok Leyland Plans ₹5,000 Crore Battery Investment with Chinese Partner CALB — Autocar Professional, 2025-09 ↩↩

-

India: Ashok Leyland partners with CALB to localise batteries — electrive.com, 2025-09-04 ↩↩↩

-

Ashok Leyland Q2 profit hits record ₹820 cr, plans ₹10k-cr battery unit — Business Standard, 2025-11-12 ↩↩

-