WESCO International: Building, Connecting, Powering, and Protecting the World

I. Introduction: The Invisible Giant Behind the Wires

In the gleaming corridors of a hyperscale data center somewhere in Virginia, engineers scramble to install racks of NVIDIA AI accelerators. In a remote stretch of West Texas, utility crews string new transmission lines to connect wind farms to the grid. On a construction site in downtown Chicago, electricians pull miles of copper wire through conduit, racing against a deadline.

What do these scenes have in common? Behind each of them, orchestrating the flow of millions of SKUs across a complex global supply chain, stands WESCO International—a $22 billion Fortune 200 company that most Americans have never heard of.

WESCO International, Inc. is a publicly traded American holding company for WESCO Distribution, an electrical distribution and services company based in Pittsburgh, Pennsylvania. The company provides electrical, industrial, communications, maintenance, repair, and operating (MRO), original equipment manufacturer (OEM) products, construction materials, and shipping. In 2023, its total revenue was approximately $22 billion. The company employs approximately 20,000 employees and 30,000 suppliers to serve more than 150,000 active customers worldwide.

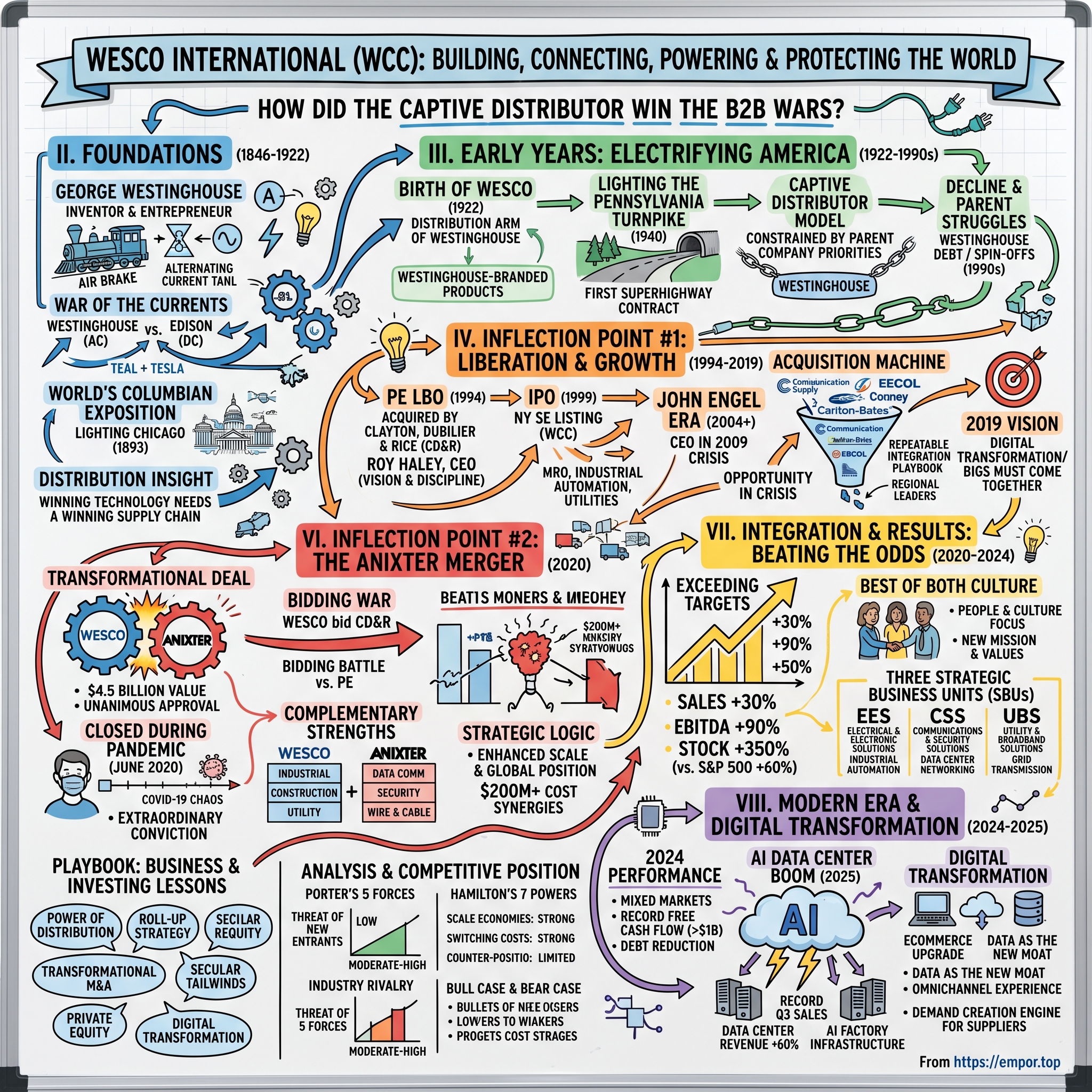

The central question that animates this story is deliciously ironic: How did the distribution arm of the company that lost the "War of the Currents" to Edison eventually win the B2B distribution wars more than a century later?

The answer involves visionary inventors, private equity transformations, a bold merger executed during a pandemic, and a strategic bet on the AI infrastructure boom that is reshaping the modern economy. The global supply chain solutions powerhouse acquired Anixter International, a leading worldwide distributor of network and security solutions, in June 2020 against the backdrop of the COVID-19 pandemic. And together, they form a Fortune 200 company, operating in more than 50 countries worldwide with a blue-chip customer base that includes more than half of global Fortune 500 companies.

This is the story of WESCO—a hundred-year journey from the workshop of George Westinghouse to the digital supply chains that power artificial intelligence factories. It's a tale of distribution as a moat, roll-up strategies in fragmented industries, and the unsexy businesses that build civilization.

II. The George Westinghouse Foundation & Origins (1846-1922)

The Man Who Lit America

George Westinghouse was born in 1846 in the village of Central Bridge, New York, the son of Emeline (Vedder) and George Westinghouse Sr., a farmer and machine shop owner. The Westinghouse ancestors came from Westphalia in Germany.

From his earliest years, young George displayed an unusual gift for machinery and entrepreneurship. From his youth, Westinghouse displayed a talent for machinery and business. He was encouraged by his father and was assigned tasks in the Westinghouse Company workshop. The company produced farm equipment such as the Westinghouse Farm Engine.

After serving in the Union Army during the Civil War, Westinghouse returned to tinkering. By his early 20s, Westinghouse had already invented several devices, but it was his deep concern for railroad safety that propelled him toward his first great breakthrough—the air brake. At the time, railroads relied on brakemen manually turning wheels to stop speeding trains—a dangerous, slow, and often deadly process. Westinghouse saw a better way: harnessing compressed air. In 1869, at just 22 years old, he patented the Westinghouse Air Brake.

This invention alone would have secured his place in industrial history. But Westinghouse was just getting started.

The War of the Currents

By the mid-1880s, Thomas Edison had become the world's most famous inventor, with his Pearl Street Station providing direct current (DC) power to lower Manhattan. But Westinghouse saw a fundamental flaw in Edison's system: Westinghouse investigated Edison's scheme, but decided that it was too inefficient to be scaled up to a large size. Edison's power network was based on low-voltage DC, which meant large currents and serious power losses. Several European inventors were working on "alternating current (AC)" power distribution. An AC power system allowed voltages to be "stepped up" by a transformer for distribution, reducing power losses, and then "stepped down" by a transformer for use.

His firm faith in the alternating-current system led to the founding of the Westinghouse Electric Company in 1886, which was in bold opposition to the well-entrenched backers of the direct-current system, led by Thomas Edison. But in a span of just 10 years, the value of the alternating-current system had been convincingly demonstrated.

What followed became known as the "War of the Currents"—one of the most dramatic business battles in American history. Westinghouse's promotion of AC power distribution led him into a bitter confrontation with Edison and his DC power system. The feud became known as "the War of Currents." Edison claimed that high voltage systems were inherently dangerous; Westinghouse replied that the risks could be managed and were outweighed by the benefits. Edison tried to have legislation enacted in several states to limit power transmission voltages to 800 volts, but failed.

Edison's campaign against AC turned increasingly desperate—and macabre. Edison waged a public smear campaign, claiming AC was too dangerous, even sponsoring public electrocutions of animals. Meanwhile, Westinghouse, alongside Nikola Tesla, quietly proved that AC could transmit power long distances efficiently and safely.

The partnership with Serbian inventor Nikola Tesla proved decisive. Westinghouse saw the potential for electricity and formed the Westinghouse Electric Company in 1884, later known as the Westinghouse Electric & Manufacturing Company. He obtained exclusive rights to Nikola Tesla's patents for a polyphase system of alternating current in 1888, persuading the inventor to join the Westinghouse Electric Company.

The war's turning point came when Westinghouse outbid Edison to light the World's Columbian Exposition in Chicago. For the first time, millions witnessed the incredible potential of AC power—bright, clean, and efficient. Soon after, Westinghouse secured the contract to build the Niagara Falls Power Project, delivering hydroelectric power to Buffalo, New York—a feat that cemented AC as the future of electricity.

The War of Currents ended in 1892 when financier J.P. Morgan forced Edison General Electric to switch to AC power and then pushed Edison out of the company he had founded. Edison General Electric company was merged with the Thomson-Houston Electric Company to form General Electric.

Westinghouse had won the technological war. But ironically, the company bearing his name would eventually need to separate from its parent to achieve its greatest success. Westinghouse died on March 12, 1914, in New York City at age 67. He never saw the distribution company that would carry his legacy into the 21st century.

The Distribution Insight: Why Supply Chain Mattered

In fact, as early as the late 1880s, immediately after founding Westinghouse Electric and Manufacturing Company, George Westinghouse worked with regional agents of a new 'Westinghouse Electric Supply company' to provide natural gas and electrical power to cities, rail lines, and roads from coast to coast. Competition was fierce, and these distribution representatives worked hard on the front lines of the business to help customers understand the possibilities of emerging technologies.

This insight—that winning technology needs a winning supply chain—would prove prophetic. A century before "supply chain" became a buzzword, Westinghouse understood that the best products in the world were worthless without an effective system to get them into customers' hands.

III. Early Years: Electrifying America (1922-1990s)

Birth of the Distribution Arm

1922: Wesco founded as the distribution arm of the pioneering Westinghouse Electric and Manufacturing Company, with a focus on Westinghouse branded lighting and electrical products. 1929: WESCO opens its headquarters in New York City, with operations across 19 cities across the US and revenues of $60 million. 1934: Westinghouse Commercial Investment Company consolidates all Westinghouse distributors into the new Westinghouse Electric Supply Company (WESCO).

The timing was fortuitous. Post-World War I America was hungry for electricity. Cities were being wired, factories were electrifying their production lines, and the consumer appliance revolution was beginning. WESCO positioned itself at the center of this transformation, serving as the critical link between Westinghouse's manufacturing prowess and the contractors, utilities, and industrial customers who needed electrical supplies.

Lighting America's First Superhighways

From its foundation as the distribution arm of Westinghouse, WESCO was positioned to be a leader in the supply of electrical and lighting products. In 1940, WESCO was contracted to light seven tunnels across the Pennsylvania turnpike, the first of its kind "Superhighway". Not long after, WESCO expanded its portfolio to include consumer products including televisions, air conditioners, refrigerators, and laundry machines, as well as new electrical wiring and heating systems.

The Pennsylvania Turnpike contract exemplified WESCO's early value proposition: not just selling products, but providing complete solutions for complex infrastructure projects. This consultative approach—helping customers solve problems rather than simply taking orders—would become a defining characteristic of the company's culture.

The Captive Distributor Model

For seven decades, WESCO operated as a "captive distributor"—essentially a sales and distribution subsidiary of its parent company. This arrangement had clear advantages: guaranteed product access, brand alignment, and a built-in customer base. But it also created limitations.

Throughout the 1900s, Wesco entered and subsequently exited the consumer electronics, transit, bottling, and nuclear plant distribution markets. It was sold to a private equity firm in 1994 and then went public in 1999, and numerous acquisitions have since been made to fill the gaps in Wesco's geographical and product coverage.

As a captive distributor, WESCO was constrained by Westinghouse's strategic priorities. When the parent company expanded into consumer electronics, WESCO followed. When Westinghouse contracted, WESCO contracted. The business lacked the autonomy to pursue its own growth strategies, diversify its supplier base, or respond independently to market opportunities.

By the early 1990s, Westinghouse Electric Corporation itself was struggling. With its enormous new debt load, the company sought to trim its operations once again. In 1992, Westinghouse exited the rough and tumble financial service business and also announced plans to sell its office furniture, residential real estate, electric-supply, and electric distribution and control subsidiaries. In 1993, Westinghouse sold its electric distribution and control unit to Eaton Corp. for $1.1 billion.

WESCO's moment of liberation was approaching.

IV. Inflection Point #1: Private Equity Liberation (1994-1999)

The Clayton, Dubilier & Rice Acquisition

In early 1994, a private equity transaction would fundamentally transform WESCO's destiny. On February 1, 1994, private equity firm Clayton Dubilier & Rice acquired distribution company WESCO from Westinghouse Electric for 330M USD.

WESCO became a separate private company after a leveraged buyout in 1994. "At the time of the LBO, the company had US$1.5 billion in sales, and was losing money."

This transaction marked far more than a change in ownership. For the first time in 72 years, WESCO was free to chart its own course. Clayton, Dubilier & Rice (CD&R) was not just any private equity firm—it had pioneered the concept of "operational value creation" in PE investing. From its inception, CD&R's founders (Joseph Rice, Martin Dubilier, and Eugene Clayton) believed that bringing experienced corporate leaders into deals would differentiate the firm. In the 1980s, CD&R began recruiting former CEOs and industry veterans to work alongside its investment professionals—a novel approach that "pioneered the concept of operating partners" in private equity.

Roy Haley Takes Command

1994: Roy Haley becomes Chief Executive Officer of WESCO, with a vision to significantly expand its product portfolio and a focus on industrial automation, utility and MRO. 1995: WESCO enters the manufactured structures industry.

Prior to joining WESCO in February 1994, he was President and Chief Operating Officer of American General Corporation, one of the nation's largest consumer financial services organizations. Haley is a Trustee of Carnegie Mellon University and received his undergraduate degree from Massachusetts Institute of Technology.

Haley brought an unusual combination of skills to WESCO: an MIT engineering background that gave him credibility with technical customers, and financial services experience that brought discipline to working capital management. Under his leadership, WESCO transformed from a money-losing captive distributor into a lean, growth-oriented acquisition machine.

The strategic shift was immediate and dramatic. No longer limited to Westinghouse products, WESCO could partner with any manufacturer whose products its customers needed. The company expanded aggressively into industrial automation, utility sectors, and MRO (maintenance, repair, and operations) markets—categories where recurring revenue and customer stickiness were highest.

The Cypress Group Era and IPO

In 1994, the private equity firm Clayton, Dubilier & Rice (CD&R) purchased Westinghouse Electrical Supply Company and created Wesco Distribution Inc. In June 1998, CD&R sold Wesco to The Cypress Group for USD 1.1 billion, which formed WESCO International Inc., the current owner of Wesco Distribution.

The 3.3x multiple return in just four years demonstrated the value creation potential that CD&R had unlocked. But more importantly, the acquisition by The Cypress Group set the stage for the company's transformation into a publicly traded enterprise.

In the same year, Wesco acquired the Bruckner Supply Company Inc., a provider of integrated supply management solutions and MRO products to Fortune 500 customers. On May 12, 1999, Wesco held its initial public offering on the New York Stock Exchange.

WESCO was formed via a private equity sponsored leveraged buy-out in 1994 and became a publicly-traded NYSE listed company in 1999.

The IPO at $18 per share marked WESCO's coming-of-age. By 1999, the company had transformed from a captive subsidiary losing money to an independent, publicly traded distributor with strong growth momentum and a proven acquisition playbook.

V. The John Engel Era & The Acquisition Machine (2004-2019)

A New Leader for a New Century

"Wesco went public in 1999, an IPO, and when I joined in 2004 as COO, we had about US$3 billion a year in sales." Engel spent five years in that role before becoming CEO in 2009.

John Engel's arrival at WESCO marked the beginning of the company's most transformative era. With a Bachelor of Science in Mechanical Engineering from Villanova University and an MBA from the University of Rochester, Engel holds a Bachelor of Science degree in Mechanical Engineering from Villanova University and a Master of Business Administration from the University of Rochester. Engel combined technical depth with strategic vision.

"The year 2009 was a challenging time because it was the great global recession," he points out. "That's when the board made the decision to move forward and gave me the opportunity and the honor to lead the company as CEO." Shortly thereafter, in 2011, Engel was appointed Chairman of the Board of Directors.

John Engel says his tenure as CEO at Wesco International has been bookended by crises. After joining Wesco in 2004 as COO, he stepped into the CEO role in 2009 during the Great Recession.

Taking the helm during the worst economic downturn since the Great Depression would have been daunting for any executive. But Engel saw opportunity in crisis. While competitors retrenched, he positioned WESCO to emerge stronger through disciplined execution and strategic acquisitions.

Building the Empire Through Acquisitions

In 2005, Wesco acquired the Carlton-Bates Company, a provider of original equipment products and supply solutions to industrial customers. In the same year, Forbes magazine named Wesco as one of their 400 Best Big Companies, an honor which was received again in 2006, 2007, and 2009. In 2006, Wesco acquired the Communication Supply Corporation, a national distributor of data communications products for enterprise and data center customers.

The acquisition of Communication Supply Corporation in 2006 proved particularly prescient—it gave WESCO early exposure to data center and enterprise networking markets that would later drive explosive growth.

In 2012, Wesco acquired EECOL Electric Corp. In June 2012, the company acquired Conney Safety Products, LLC. In 2014, Wesco acquired Hazmasters Inc. In 2015, Wesco acquired Hill Country Electric Supply, Aelux, and Needham Electric Supply. In 2016, Wesco acquired Atlanta Electrical Distributors, LLC.

Each acquisition followed a disciplined playbook: identify regional leaders or niche specialists, integrate them quickly, leverage WESCO's scale for procurement savings, and cross-sell into expanded product categories. The company developed a repeatable integration process that minimized disruption while maximizing synergies.

In 2019, Wesco acquired OSRAM's Sylvania Lighting Solutions (SLS), now known as Wesco Energy Solutions.

The 2019 Vision: Setting the Stage for Transformation

By 2019, Engel had built WESCO into an $8 billion enterprise through organic growth and more than 20 acquisitions. But he knew the company needed to think bigger. At the company's 2019 Investor Day, Engel made two provocative statements that would soon reshape the industry.

First, he declared that WESCO was committed to leading the digital transformation of the distribution industry. Second—and more provocatively—he announced that "our part of the value chain was very fragmented and the bigs had to come together."

The message was unmistakable: WESCO was hunting for transformational deals.

VI. Inflection Point #2: The Anixter Merger—Transformational Deal of 2020

Anixter: A Worthy Dance Partner

Founded in 1957 by brothers Alan and William Anixter, this Skokie-based company grew into one of the country's leading wholesalers of wire. In 1986, when annual sales stood at about $600 million, Anixter was purchased for about $500 million by the Itel Corp., a large holding company controlled by legendary investor Sam Zell.

Sam chaired Anixter through 34 years of growth that established the enterprise as a global industry leader, increasing revenues from $650 million to $8.8 billion expanding from three to fifty countries. Anixter was sold to WESCO International in 2020 for $4.5 billion.

In 1985, Zell acquired Itel Corporation, a diversified transportation and logistics company, shortly after it emerged from bankruptcy. In 1986, he acquired Anixter, remaining in charge until it was sold in 2020.

Under Zell's stewardship, Anixter had developed expertise in precisely the areas where WESCO was weaker: communications infrastructure, network security, and wire & cable. The companies' strengths were remarkably complementary.

The Bidding War with Private Equity

In late 2019, Anixter announced that it had agreed to be acquired by Clayton, Dubilier & Rice—ironically, the same firm that had transformed WESCO twenty-five years earlier. Monday's closing comes six months after the two distributors initially announced the merger agreement, which followed a multi-month bidding battle between WESCO and private equity firm Clayton, Dubilier & Rice. CD&R originally bid $81 per share in an acquisition agreement announced Oct. 30, 2019. That offer was later amended higher before WESCO proposed its own offer just before Christmas, and Anixter fielded another round of bids from those two companies before announcing Jan. 9 that it preferred WESCO's latest offer.

Anixter, a leading global distributor of Network & Security Solutions, Electrical & Electronic Solutions, and Utility Power Solutions, announced that their boards of directors have unanimously approved a definitive merger agreement under which WESCO will acquire Anixter in a transaction valued at approximately $4.5 billion. Anixter's prior agreement to be acquired by Clayton, Dubilier & Rice, LLC ("CD&R") has been terminated, following CD&R's waiver of its matching rights under the agreement.

Engel and his team moved aggressively during Anixter's "go-shop" period—the window that allowed the target company to solicit competing offers even after signing a merger agreement. WESCO's strategic rationale proved more compelling than private equity's financial engineering.

Closing During COVID-19

PITTSBURGH, June 22, 2020 /PRNewswire/ -- WESCO International, Inc. (NYSE: WCC), a leading provider of business-to-business (B2B) distribution, logistics services and supply chain solutions, announced it has completed its merger with Anixter International Inc., creating a premier, industry-leading global B2B distribution and supply chain solutions company. Upon completion of the merger, Anixter became a wholly owned subsidiary of WESCO International.

The timing could not have been more challenging. The COVID-19 pandemic had thrown global supply chains into chaos, shut down construction projects, and created unprecedented uncertainty. Many deal teams would have walked away or demanded massive price reductions.

While the coronavirus outbreak has had a significant impact on the financial markets, it is important to understand that WESCO has committed financing in-place to complete the transaction, and we remain on track to successfully complete the merger in the second or third quarter of this year.

WESCO's decision to push forward required extraordinary conviction. But Engel understood that the pandemic's disruption was temporary, while the strategic value of combining two industry leaders was permanent.

The Strategic Logic

The combined company has a comprehensive and balanced portfolio that unites WESCO's capabilities in industrial, construction, and utility with Anixter's expertise in data communications, security, and wire and cable. Bringing together the companies' complementary products, services, technologies, and solutions creates significant cross-selling opportunities, strengthening the customer value proposition as well as supplier relationships.

The company listed the following as its strategic and financial rationale at the closing of the merger: It enhances scale and global position: The combined company generated pro forma 2019 revenue of more than $17 billion.

WESCO expects to realize annualized run-rate cost synergies of over $200 million by the end of year three through efficiencies in corporate and regional overhead, optimization of the branch and distribution center network, and productivity in field operations and the supply chain.

VII. Integration & Results: Beating the Odds (2020-2024)

Exceeding Every Expectation

We exceeded all our initial operational synergy targets set at the time of the Anixter acquisition. Through the end of last year, our sales grew 30 percent compared to 2019. Our EBITDA grew 90 percent. We expanded our EBITDA margin by 240 basis points, and our stock today is trading above $180. From June 2020 through the end of 2023, our total shareholder return was north of 350 percent, compared to 60 percent for the S&P 500 during the same period.

These results were extraordinary by any measure. The 350% total shareholder return versus 60% for the S&P 500 represented one of the most successful large-scale industrial mergers of the pandemic era.

The Secret to Integration Success

Many mergers of equals do not go well, yet you succeeded and created a new company in the process. How did you beat the odds? John Engel: I think it was the focus on the people and the culture. There have been many deals throughout business history that made tremendous sense at a strategic level, but they failed because of a culture mismatch.

"When we put the two companies together, we took the best from each, providing a foundation for us to be the leading, most comprehensive supply chain solutions provider to our customers around the world," CEO, President and Chair John Engel tells The CEO Magazine. "Together, we established a new mission, a new vision and a harmonized set of values. Our mission is to build, connect, power and protect the world. And our vision is to be the best tech-enabled supply chain solutions provider across the globe, with an emphasis on being tech-enabled."

Rather than forcing one company's culture onto the other, WESCO adopted a "best of both" approach—evaluating every process, system, and team structure to determine which approach delivered superior results. This methodology required humility and rigorous analysis, but it earned buy-in from employees of both legacy organizations.

The Three Strategic Business Units

The integration yielded a new organizational structure with three strategic business units, each addressing distinct end markets:

Electrical & Electronic Solutions (EES): Serves industrial, construction, and commercial customers with electrical infrastructure products, automation solutions, and lighting systems.

Communications & Security Solutions (CSS): Delivers networking, security, and structured cabling solutions to data centers, enterprises, and commercial buildings. This unit has become WESCO's highest-growth segment, driven by AI infrastructure demand.

Utility & Broadband Solutions (UBS): Serves investor-owned utilities, public power systems, and telecommunications providers with transmission and distribution equipment.

This three-pillar structure provides diversification across end markets while allowing each unit to develop deep expertise in its domain.

VIII. Modern Era & Digital Transformation (2024-2025)

2024 Performance: Navigating Mixed Markets

In 2024 the company made a revenue of $21.81 Billion USD a decrease over the revenue in the year 2023 that were of $22.38 Billion USD. The year represented a period of consolidation following the exceptional post-merger growth, with mixed conditions across end markets.

We are pleased with our return to sales growth in the fourth quarter sparked by more than 70% growth year-over-year in our global Data Center business, 20% growth in Broadband Solutions, and renewed positive sales momentum in Electrical and Electronic Solutions. This was partially offset by a slowdown with industrial customers and the expected continued weakness in our utility business in the fourth quarter.

Mr. Engel continued, "Our continued focus on effective working capital management yielded strong benefits again in the fourth quarter and contributed to record free cash flow generation of over $1 billion in 2024, or 154% of adjusted net income. Financial leverage remained stable at 2.9x trailing twelve-month adjusted EBITDA as we reduced our net debt by $431 million and repurchased $425 million of shares last year.

2025: The AI Data Center Boom

For its fiscal Q3 ending Sept. 30, Wesco sales climbed 12.9% to $6.2 billion. That's up from $5.49 billion a year earlier. Organic sales, excluding currency and acquisition effects, increased 12.1%.

AI infrastructure remained the centerpiece of that acceleration. Data center revenue hit an all-time high of $1.2 billion. That's up roughly 60% from a year earlier and represents about 19% of company sales. The Communications and Security Solutions segment supplies networking, fiber and security systems for so-called "white-space" data center environments.

WESCO International Inc (NYSE:WCC) reported record quarterly sales in its third quarter 2025 results, exceeding analyst expectations and prompting a significant upward revision to its full-year outlook. The company's presentation, delivered on October 30, 2025, highlighted accelerating sales momentum across all business segments, with particularly strong performance in data center solutions. The market responded positively to the results, with WESCO's stock jumping 10.66% to $228.29 following the announcement.

The Digital Transformation Imperative

Wesco has already invested $270 million in this digital transformation initiative, focusing on upgrading its ecommerce platform, modernizing its supply chain, and enhancing digital tools.

"We've streamlined backend systems and now provide 24/7 support for customers and suppliers through agile methodologies," said chief digital and information officer Akash Khurana. "By the end of next year, we expect to complete the initial phases of our transformation, significantly enhancing our omnichannel experience."

The company's push into digital transformation is also gathering speed. Engel said Wesco remains "firmly focused on executing our cross-selling initiatives and enterprise-wide margin improvement program" while advancing its "technology-driven business transformation." All three business units are now running early versions of the company's new digital platform. Wesco designed it to streamline pricing, procurement and project management across global operations. Broader deployment is slated to scale in 2026.

Data as the New Moat

"We are the demand creation engine and the front end of the new product development process for our supplier partners," Engel explains. "We hold unique customer data and are unmatched in capability in that regard. Our secret sauce is the ability to unlock the power of that big data and use it to provide insights for our suppliers and develop even more effective and efficient solutions for our customers. As we digitally transform our company, our ability to unlock that power grows exponentially."

This perspective positions WESCO not merely as a physical distributor of products, but as an information company that happens to move physical goods. The company's visibility into purchase patterns across 150,000 customers creates insights that neither manufacturers nor competitors can replicate.

The AI Factory Opportunity

That's why NVIDIA is building AI factory architecture, and why Wesco, as a strategic partner, is delivering real-world industrial systems that transform unstructured data and electrical power into scalable intelligence for next generation data centers. These AI factories are the digital supply chains that power AI models, which interpret, classify, generate and act on signals from the physical and digital world.

More than a hardware distributor or solution aggregator, Wesco serves as the delivery arm for real AI infrastructure, managing everything from sourcing and staging to secure transport, rack integration, structured cabling, liquid cooling implementation and software bring-up. Our teams execute globally, with regionally distributed logistics and engineering capacity to operate at the scale and speed required for enterprise transformation, providing control, transparency and performance ownership.

Wesco's recent acquisition of Ascent, finalized in December 2024, adds a fast-growing business to its portfolio. Ascent specializes in providing recurring management services to data centers and is growing at an impressive 30% annually. This acquisition strengthens Wesco's position as a premier partner in data center solutions, leveraging Ascent's recurring revenue model to drive long-term stability.

IX. Playbook: Business & Investing Lessons

Lesson 1: The Power of Distribution in Industrial Markets

The WESCO story demolishes the myth that distribution is a commodity business destined for disintermediation. In B2B markets with fragmented customers, complex products, and value-added service requirements, distributors create irreplaceable value.

Manufacturers lack the local presence, inventory depth, and customer relationships to serve thousands of contractors, industrial plants, and utilities directly. Customers lack the procurement sophistication to manage relationships with thousands of suppliers. The distributor sits in the middle, creating value for both sides.

The key insight: distribution businesses with genuine switching costs, technical expertise, and service differentiation can sustain attractive returns even as Amazon Business expands into adjacent categories.

Lesson 2: Roll-up Strategy Execution

WESCO's twenty-plus acquisitions under Engel demonstrate the characteristics of successful roll-up strategies:

Target selection discipline: Focus on geographic gaps, product category extensions, or capability additions—never acquisitions for scale alone.

Integration rigor: Develop repeatable playbooks that preserve customer relationships while capturing synergies quickly.

Cultural alignment: Prioritize targets where management philosophy and customer orientation match the acquirer's values.

Retention focus: Keep the best people from acquired companies by offering growth opportunities, not just retention bonuses.

Lesson 3: Transformational M&A Timing

The Anixter merger demonstrated the courage required for transformational deals. Executing a $4.5 billion acquisition during a pandemic, with financing markets stressed and economic outlook uncertain, required extraordinary conviction.

But the reward for that conviction was substantial: the opportunity to acquire a strategic asset at prices that would never be available in normal conditions, while competitors hesitated.

Lesson 4: Private Equity as a Training Ground

WESCO's liberation by Clayton, Dubilier & Rice in 1994 provides a case study in how private equity can create lasting value. CD&R didn't just financial engineer the business—they installed operational leadership, developed acquisition capabilities, and created the foundation for decades of growth.

The lesson for investors: companies that emerge from disciplined private equity ownership often carry valuable institutional knowledge about operational excellence and capital discipline.

Lesson 5: Secular Tailwinds Trump Cyclical Headwinds

We're well-positioned to deliver outsized growth due to the secular trends of AI-driven data centers, increased power generation, electrification, automation, and reshoring.

WESCO's current positioning illustrates the importance of aligning with secular trends that will persist regardless of economic cycles. Data center buildout, grid modernization, electrification, and reshoring represent multi-decade investment themes that provide structural growth tailwinds.

Lesson 6: Digital Transformation in Traditional Industries

"Here, one plus one is equal to three plus. In putting these two companies together, we have transformed Wesco. And we intend to digitally transform our part of the value chain and the entire B2B industry. This is really a story of market leadership and the value we can create for all of our stakeholders."

Traditional industries often provide the best digital transformation opportunities precisely because starting points are so low. A distributor that invests in advanced analytics, e-commerce capabilities, and supply chain visibility can create substantial competitive advantages against rivals still operating with legacy systems.

X. Analysis: Competitive Position & Strategic Assessment

Porter's Five Forces Analysis

| Force | Assessment | Analysis |

|---|---|---|

| Threat of New Entrants | LOW | Wesco operates ten fully automated distribution centers and 500 branches in North American and international markets. Scale economics, 30,000 supplier relationships, and working capital requirements create formidable barriers. |

| Supplier Power | MODERATE | Relationships with 30,000 suppliers reduce dependence, but major manufacturers like Hubbell, Schneider, and Siemens retain leverage. Some suppliers, like Hubbell, operate as both partners and competitors, creating a dynamic where Wesco must balance collaboration with competition. |

| Buyer Power | MODERATE | Wesco customers include commercial and industrial businesses, contractors, government agencies, institutions, telecommunications providers, and utilities. Diverse customer base limits individual buyer power, but large contractors and utilities can negotiate. |

| Threat of Substitutes | LOW-MODERATE | Direct-from-manufacturer sales are an alternative, but most customers prefer value-added services, inventory management, and product breadth. Amazon Business represents an emerging but currently limited threat. |

| Industry Rivalry | MODERATE-HIGH | Hubbell (Electrical Equipment), Sonepar USA, MRC Global, Fastenal, and Applied Industrial Technologies are some of the 12 competitors of Wesco International. Consolidation trend favors largest players. |

Hamilton's 7 Powers Analysis

| Power | Assessment | Analysis |

|---|---|---|

| Scale Economies | ✅ STRONG | Distribution centers, IT systems, and procurement leverage create meaningful cost advantages. Largest players achieve 100+ basis points of margin advantage. |

| Network Economies | ⚠️ MODERATE | Geographic density creates value—more branches mean faster delivery. Supplier relationships strengthen with more customer touchpoints. |

| Counter-Positioning | ❌ LIMITED | Large incumbents can replicate the model. Amazon Business poses potential disruptive threat, though B2B penetration remains nascent. |

| Switching Costs | ✅ STRONG | Wesco collaborates with over 50,000 suppliers globally, with approximately 65% of its purchases concentrated among 360+ preferred suppliers. These partnerships allow Wesco to maintain a diverse and competitive inventory while benefiting from volume-based cost efficiencies. Integrated supply chain solutions and custom inventory management create high switching costs. |

| Branding | ⚠️ MODERATE | B2B branding matters less than consumer, but trust and reliability drive long-term relationships. |

| Cornered Resource | ⚠️ MODERATE | Customer data and supplier relationships represent difficult-to-replicate assets, but not truly exclusive resources. |

| Process Power | ✅ STRONG | Integration capabilities, supply chain expertise, and digital transformation investments represent accumulated know-how that competitors cannot easily replicate. |

Competitive Landscape

Sonepar is a global leader in the B2B distribution of electrical products. In 2023, Sonepar reported sales of €33.3 billion, highlighting its substantial global presence and competitive strength. Rexel is another major worldwide distributor of electrical supplies. Rexel competes with WESCO through its extensive product offerings and established distribution networks.

The electrical distribution market remains fragmented globally, but consolidation accelerates among the largest players. WESCO's post-merger position as the #1 or #2 player in most North American categories provides meaningful competitive advantages:

- Procurement leverage: Larger purchase volumes enable better pricing from suppliers

- Customer stickiness: One-stop-shop capability reduces customer procurement complexity

- Talent attraction: Scale enables investment in digital capabilities that attract top talent

- M&A optionality: Financial capacity to continue tuck-in acquisitions

Key Performance Indicators to Monitor

For long-term investors tracking WESCO, three KPIs deserve particular attention:

1. Organic Sales Growth: The clearest indicator of market share gains and demand trends. Track by segment to identify relative strength across EES, CSS, and UBS.

2. Adjusted EBITDA Margin: The best measure of operational execution. Target range of 7-8% adjusted EBITDA margin indicates healthy pricing discipline and cost control.

3. Free Cash Flow Conversion: As a working-capital-intensive business, WESCO's ability to convert earnings into cash flow determines its capacity for debt reduction, acquisitions, and shareholder returns. Target of 100%+ adjusted net income conversion demonstrates disciplined working capital management.

XI. Bull Case & Bear Case

Bull Case: The AI Infrastructure Play Nobody Talks About

The bull case for WESCO rests on several compelling dynamics:

Data Center Supercycle: The standout performer for WESCO has been its data center vertical. In Q1 2025, this segment experienced a remarkable 70% growth, now accounting for 14% of total revenues. This significant expansion indicates WESCO's increasing share-of-wallet in the data center market and positions the company well to capitalize on the ongoing digital transformation trends across industries.

The AI infrastructure buildout represents a generational investment cycle. WESCO's positioning in networking, structured cabling, and data center services creates direct exposure to this theme with lower valuation multiple than pure-play AI infrastructure companies.

Grid Modernization: The global push for electric vehicles (EVs), renewable energy, and grid modernization creates consistent demand for Wesco's utility and electrical solutions.

Electrification of transportation, renewable energy integration, and aging grid infrastructure require trillions of dollars in electrical infrastructure investment over the coming decades.

Margin Expansion Potential: Post-merger integration is complete, digital transformation investments are scaling, and procurement leverage continues to improve. Management has articulated a pathway to sustained margin expansion through operational excellence initiatives.

Capital Allocation Discipline: Strong free cash flow generation supports continued debt reduction, share repurchases, and dividend growth while maintaining acquisition optionality.

Bear Case: Cyclical Exposure and Competitive Threats

The bear case centers on structural and cyclical concerns:

Economic Sensitivity: Electrical distribution is inherently tied to construction activity, industrial production, and utility capital spending. A significant economic downturn would pressure volumes across all three segments.

Amazon Business Threat: While current B2B penetration remains limited, Amazon's entry into industrial distribution represents a long-term disruptive risk. The company's logistics capabilities and customer data could eventually challenge traditional distributor value propositions.

Margin Pressure: Competition from well-capitalized global players like Sonepar and Rexel, combined with customer demands for price transparency, could constrain margin expansion despite scale advantages.

Integration Execution Risk: While Anixter integration succeeded, continued tuck-in acquisitions carry execution risk. A poorly integrated acquisition could distract management and damage customer relationships.

Data Center Concentration: As data center sales approach 20% of revenue, WESCO becomes increasingly exposed to the capital spending decisions of hyperscale cloud providers. Any pullback in AI infrastructure investment would disproportionately impact growth.

XII. Conclusion: The Next Century Begins

George Westinghouse would likely marvel at what his distribution arm has become. The man who defeated Edison in the War of the Currents built his legacy on a simple insight: transformational technology needs transformational distribution to reach customers who can use it.

A century later, WESCO embodies that insight more fully than ever. Our mission is to build, connect, power and protect the world. That mission statement captures both the company's industrial heritage and its positioning for the digital future.

The AI data center buildout, grid modernization, electrification, and reshoring represent investment themes that will unfold over decades. WESCO sits at the intersection of all of them—not as a technology company commanding premium multiples, but as an essential infrastructure provider generating cash flows and compounding value.

In 2025, we expect organic sales to grow 2.5% to 6.5% and operating margin to expand, as all three business units are expected to deliver profitable growth. We expect to generate $600 to $800 million of free cash flow and I am pleased to announce that we plan to increase our common stock dividend by 10% again this year to $1.82 per share while continuing our share buyback program.

The story of WESCO demonstrates that distribution businesses, properly executed, can create substantial long-term value. The company that started as Westinghouse's captive sales arm has become a Fortune 200 enterprise defining the future of B2B supply chains.

In the end, the company that lost the War of the Currents won something more durable: a distribution network that would outlast its parent by decades and continue building, connecting, powering, and protecting the world for generations to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube