TopBuild: The Insulation Empire Hidden in Plain Sight

Introduction: The Case for "Boring" Businesses

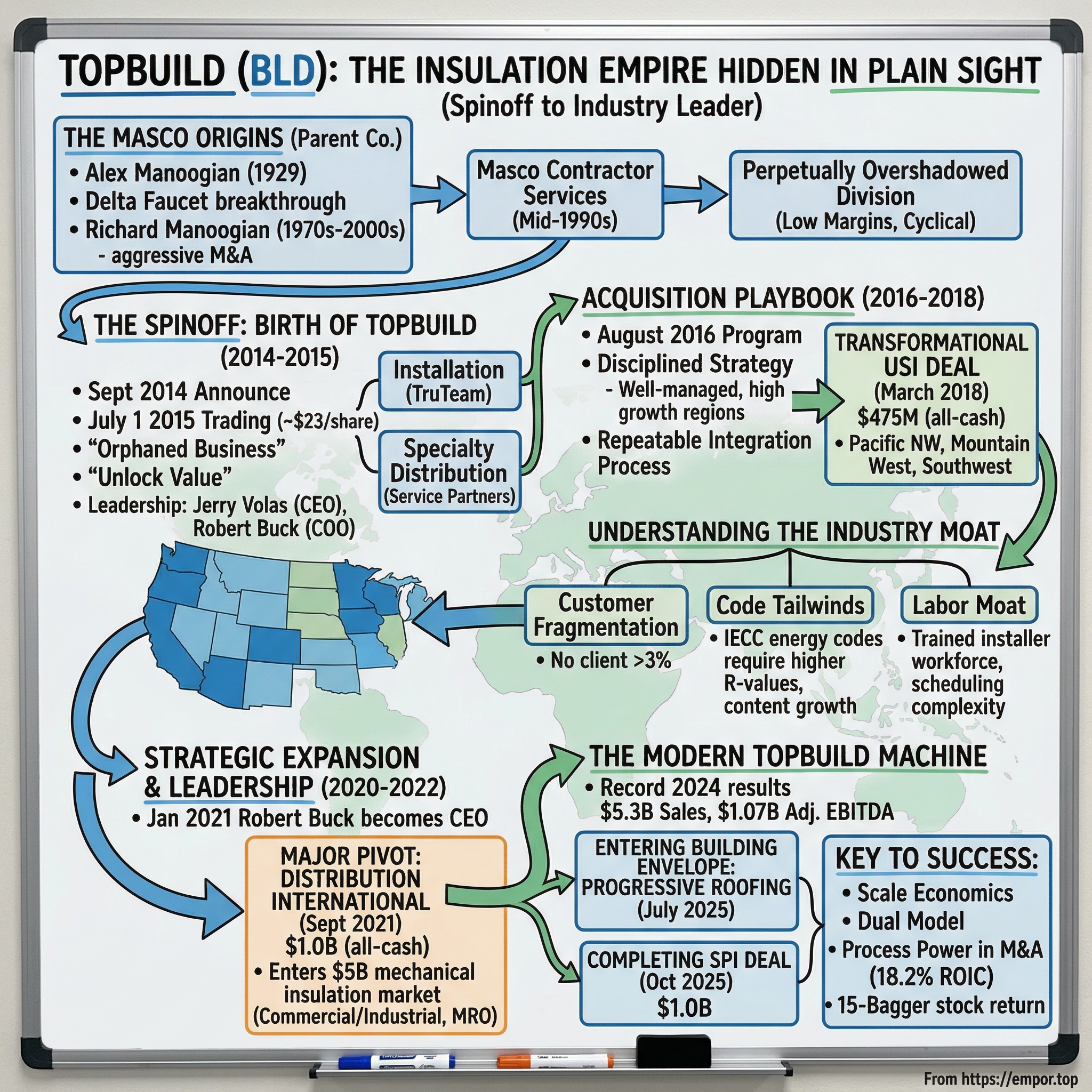

On a sweltering summer day in 2015, an unremarkable corporate transaction took place that few investors noticed. Masco Corporation, the Taylor, Michigan conglomerate known for Delta faucets and Behr paints, quietly spun off its insulation installation services division—the "ugly duckling" of its portfolio—into an independent company called TopBuild. The stock began trading on July 1 at roughly $23 per share.

A decade later, that orphaned business has compounded into one of the construction industry's most remarkable success stories. TopBuild achieved record 2024 results: sales of $5.3 billion and adjusted EBITDA of $1.07 billion. The stock trades above $400, representing approximately a 15-bagger from its spinoff price. The market capitalization hovers around $12.5 billion.

The central question for investors is deceptively simple: How does a company selling and installing insulation—one of the most commoditized products in construction—become one of the best-performing stocks of the past decade?

The answer illuminates several timeless investing themes: the hidden value in corporate spinoffs, the compounding power of disciplined roll-up strategies, and the rare ability to ride secular tailwinds while building genuine competitive advantages. TopBuild Corp., headquartered in Daytona Beach, Florida, is a leading installer and specialty distributor of insulation and related building material products to the construction industry in the United States and Canada.

TopBuild operates in two segments, Installation and Specialty Distribution. It provides insulation products and accessories, glass and windows, rain gutters, garage doors, fireplaces, roofing materials, closet shelving, and other products. The company also offers insulation installation services for fiberglass batts and rolls, blown-in loose fill fiberglass, polyurethane spray foam, and blown-in loose fill cellulose applications.

What makes this story remarkable is not just the financial returns, but how TopBuild achieved them in a market that institutional investors typically dismiss as too fragmented, too cyclical, and too unglamorous to analyze carefully.

Part I: Parent Company Origins — The Masco Story

To understand TopBuild's genesis, one must first understand the empire from which it emerged. Masco Corporation is an American manufacturer of products for the home improvement and new home construction markets. Comprising more than 20 companies, the Masco conglomerate operates nearly 60 manufacturing facilities in the United States and over 20 in other parts of the world. Since 1969 it trades on the NYSE. Under the leadership of Richard Manoogian, the company grew exponentially and subsequently joined the Fortune 500 list of largest U.S. corporations.

The Masco story begins in 1929 with Alex Manoogian, an Armenian immigrant who founded a small machine screw products company in Detroit. The company's breakthrough came in the 1950s when Alex designed the Delta faucet—one of the first single-handle hot/cold faucets. In 1952, Manoogian began redesigning the single-handle washerless faucet. The faucet he created was one of the first single-handle hot/cold faucets; it is now known as Delta. Delta's television advertisements were a first for any faucet, and made the product a successful seller. Masco went on to capture the mass market as sales moved from plumbing wholesalers to retail stores. These steps of production and marketing of the Delta faucet began in 1954, and four years later Delta Faucet's annual sales exceeded a million dollars.

Under Richard Manoogian, Alex's son, the company pursued an aggressive diversification strategy. Masco Screw Products grew into the Masco Corporation, a large corporate holding company for numerous acquisitions. Small, family-run businesses were bought out by Masco Corporation with cash and stock in the parent corporation. Between 1997 and 2002, Richard Manoogian, who succeeded his father as chief executive, acquired 42 companies valued at a total of $10 billion.

This acquisition spree included entry into the services business in the mid-1990s. At that point in time three different Masco Companies existed: Masco Corp., Masco Tech., and TriMas Corp. Two years later, Masco entered the services business. Masco Contractor Services became the company's vehicle for building a nationwide insulation installation platform, eventually growing into one of the largest installers in the United States.

But within the broader Masco portfolio, the insulation services business was perpetually overshadowed. Masco Corporation is one of the world's leading manufacturers of branded building products, as well as a leading provider of services that include the installation of insulation and other building products. The manufacturing businesses—faucets, cabinets, paints—generated higher margins and were easier for investors to understand. The installation services division was labor-intensive, tied to volatile housing starts, and seemed to lack the brand equity of Delta or Behr.

For years, this division remained a footnote in Masco's investor presentations. The conglomerate discount weighed on both businesses: Masco's branded manufacturing wasn't valued as a pure-play, and the insulation business was too small and different to attract dedicated coverage. It was, in the parlance of value investors, a classic "sum of the parts" situation waiting to be unlocked.

The economics told the story. Masco's core manufacturing businesses derived approximately 71% of revenues from repair and remodeling—a less cyclical and higher-margin business than new construction. The insulation services business, by contrast, was heavily tied to the health of new housing starts, which had only recently recovered from the devastating 2008-2009 financial crisis. Management increasingly viewed the division as a strategic mismatch.

Part II: The Spinoff — Birth of TopBuild (2014-2015)

In September 2014, Masco made the announcement that would change everything. The spin-off, which was previously announced in September of 2014, is expected to be complete in mid-2015.

The strategic rationale was transparent: after spinning off the installation services business, the "new" Masco would generate approximately 82% of its pro-forma revenues from repair and remodeling, allowing the better business to be better appreciated by the market as a pure R&R proxy. The services division could pursue its own destiny, develop its own investor base, and execute a strategy tailored to its unique economics.

The company that would emerge from the spin-off of Masco's Installation and Other Services businesses will be named TopBuild Corp. and will be listed on the New York Stock Exchange under the ticker symbol BLD.

The mechanics of the separation were straightforward. After market close on June 30, 2015, Masco Corporation distributed to its stockholders one share of TopBuild common stock for every nine shares of Masco common stock held at time of close of business on the record date of June 19, 2015.

TopBuild Corp. (NYSE: BLD), the leading installer and distributor of insulation products to the United States construction industry, announced the successful completion of its spin-off from Masco Corporation (NYSE: MAS) into an independent, publicly‑traded company. TopBuild is comprised of the former Masco Contractor Services business, now called TruTeam, a nationwide installer of insulation, and Service Partners, a nationwide distributor of residential insulation products and related accessories. TopBuild reported revenue of $1.5 billion in 2014, which represents a compound annual growth rate of 12% since 2012.

The founding leadership team was drawn from Masco veterans who knew the business intimately. Upon completion, TopBuild's management team will include: Jerry Volas, Chief Executive Officer; Robert Buck, President and Chief Operating Officer; and John Peterson, Chief Financial Officer.

Jerry Volas, the inaugural CEO, had spent over three decades at Masco. Prior to his tenure at TopBuild Corp, Mr. Volas was employed by Masco Corporation, one of the world's leading manufacturers of brand-name products for the home improvement and new home construction industries, in various positions of increasing responsibility, between 1982 and June 2015. These roles include Group Executive responsible for almost all of Masco's operating companies between February 2005 and June 2015; President of Liberty Hardware, a Masco operating company, between April 2001 and February 2005; as a Group Controller supporting a variety of Masco operating companies between January 1996 and April 2001. In addition, Mr. Volas held progressive financial roles including Vice President/Controller at BrassCraft Manufacturing Company, a Masco operating company, between May 1982 to January 1996. He is a Certified Public Accountant. He received a Bachelor of Business Administration degree from the University of Michigan.

Volas understood both the opportunities and challenges of the newly independent company. On day one, TopBuild had significant scale: TopBuild provides insulation installation services nationwide through its Contractor Services business, TruTeam, which has over 190 installation branches located in 43 states. TopBuild also distributes insulation nationwide through its Service Partners business from over 70 distribution centers located in 35 states. In addition to insulation products, TopBuild also installs or distributes other building products, including rain gutters, garage doors, fireplaces, shower enclosures, closet shelving and roofing.

"Today we begin a new chapter in the exciting TopBuild story by becoming a separately traded public company. As the leading installer and distributor of insulation products in the United States, we serve residential and commercial builders of all sizes from coast to coast. Our geographic presence and industry leading service positions us extremely well to drive shareholder value," said Jerry Volas, TopBuild's Chief Executive Officer. He continued, "Being part of Masco for the past 20 years has provided TopBuild with the people, processes and systems to prosper as a separate company. On behalf of our 8,000 associates nationwide, I would like to thank everyone at Masco who has contributed to our success. We welcome Masco's shareholders as our own and we look forward to continued success."

But separation came with obligations. Masco received a $200 million dividend from the spinoff, which TopBuild paid by taking on term loan debt. The new company emerged with a clean balance sheet by industry standards, but also with immediate pressure to demonstrate that it could stand alone.

The market's initial reception was tepid. Spinoffs often experience selling pressure as index funds rebalance and parent company shareholders exit positions in unfamiliar businesses. TopBuild traded sideways for months as investors digested the new company's story.

What few recognized at the time was that independence would unleash management's ability to deploy capital aggressively—a capability that had been constrained within the larger Masco bureaucracy. The acquisition playbook that would transform TopBuild was about to begin.

Part III: Understanding the Insulation Industry

Before diving into TopBuild's strategic evolution, one must understand the peculiar economics of insulation installation—a business that defies easy categorization.

Insulation is simultaneously one of the most commoditized and most essential products in construction. The materials themselves—fiberglass batts, blown-in cellulose, spray polyurethane foam—are largely undifferentiated. Three major manufacturers (Owens Corning, Johns Manville, and Knauf) dominate supply. Yet the installation process is intensely local, relationship-driven, and service-oriented.

TopBuild also distributes building and mechanical insulation, insulation accessories, and other building product materials for the residential, commercial, and industrial end markets. The company serves single-family homebuilders, single-family custom builders, multi-family builders, commercial general contractors, remodelers, and individual homeowners.

TopBuild operates through a dual business model that provides both competitive advantages and natural diversification. The company operates in two segments, Installation and Specialty Distribution. It provides insulation products and accessories, glass and windows, rain gutters, garage doors, fireplaces, roofing materials, closet shelving, and other products.

The Installation Segment (TruTeam)

The installation business is fundamentally about managing labor—coordinating crews of trained installers across hundreds of local markets to serve homebuilders on tight construction schedules. Every new single-family home requires insulation. The installer must coordinate with the builder's construction timeline, arriving after framing is complete but before drywall goes up—a window that may be only days.

This scheduling complexity creates meaningful switching costs. Once a homebuilder establishes a relationship with an installer who delivers on time and performs quality work, there's genuine reluctance to change. A missed insulation appointment can delay an entire construction schedule by weeks. The value of reliability far exceeds any marginal material cost savings.

The Specialty Distribution Segment (Service Partners and Distribution International)

The distribution business operates differently. Service Partners and the later-acquired Distribution International act as intermediaries between insulation manufacturers and the contractors who install it. They maintain inventory, provide credit, and offer technical expertise that smaller contractors cannot source directly from manufacturers.

This segment has historically generated lower margins than installation but provides important strategic benefits: it creates additional touchpoints with customers, generates insights into local market conditions, and reduces overall business volatility by diversifying the customer base beyond homebuilders.

Customer Fragmentation as Competitive Advantage

One of TopBuild's most important structural characteristics is customer diversification. Unlike many building products companies dependent on a handful of national homebuilders, TopBuild's revenue is remarkably distributed. No single customer accounts for more than 3% of total sales. The top ten customers combined represent approximately 10% of revenues.

This fragmentation means TopBuild doesn't face concentrated buyer power. It also means that gaining market share requires winning thousands of local relationships—a process that favors scale and persistence over disruptive innovation.

The Code Tailwind

Perhaps the most important secular driver for insulation demand is the inexorable tightening of building energy codes. The International Code Council develops model residential energy codes every three years, referred to as the International Energy Conservation Code (IECC). The model code currently in effect is the 2021 IECC. Model codes are adopted by most states and municipalities and frequently amended.

The International Code Council (ICC) published the 2024 International Energy Conservation Code (IECC) on Aug. 14. The IECC is a model code that sets minimum requirements for energy efficiency for residential and commercial buildings. It is the most adopted energy code in the country and is recognized as the national model energy code for low-rise residential buildings in federal law. ICC publishes a new edition every three years for states and municipalities to adopt, amend and enforce in their jurisdictions.

The residential provisions — covering one- and two-family homes and multifamily dwellings up to three stories — are expected to be about 7% more efficient. The commercial provisions — covering buildings four stories and higher — are expected to be about 10% more efficient.

Each code revision tends to increase required R-values (the measure of insulation's thermal resistance), driving greater insulation content per home. What once required a few inches of fiberglass may now require spray foam, multiple insulation types, or significantly thicker materials. This content growth provides a structural tailwind independent of housing volume.

Part IV: The Acquisition Playbook Begins (2016-2018)

In August 2016, roughly a year after independence, TopBuild launched the acquisition program that would define its next decade. Jerry Volas, Chief Executive Officer of TopBuild, stated, "Since implementing our acquisition program in August 2016, we have completed nine transactions and have established a successful track record of integrating them onto our systems and supply chain. We've also closely adhered to our strategy of seeking well managed companies with experienced operators, well-trained installers, solid customer bases and a footprint that expands our presence in high growth geographies."

The strategy was elegantly simple but difficult to execute: acquire smaller regional installers, integrate them onto TopBuild's systems and supply chain, extract synergies, and reinvest the cash flow into more acquisitions. The fragmented nature of the industry—with hundreds of regional players and few scaled competitors—provided abundant targets.

But the playbook required discipline. Unlike some roll-up strategies that chase growth at any price, TopBuild established clear acquisition criteria from the start. The company sought well-managed businesses with experienced operators, trained installer workforces, solid customer relationships, and geographic footprints that expanded TopBuild's presence in high-growth markets. Management explicitly avoided "fixer-uppers" requiring operational turnarounds.

The integration process became a core competency. TopBuild developed repeatable playbooks for onboarding acquired companies onto its IT systems, supply chain contracts, and operational best practices. This institutional capability created compounding advantages: each acquisition made the next one easier and faster to integrate.

The USI Acquisition: A Transformational Deal

In March 2018, TopBuild announced the deal that would prove the scalability of its acquisition machine. TopBuild Corp. (NYSE:BLD) has entered into an agreement to acquire United Subcontractors, Inc. ("USI") in an all-cash transaction valued at $475 million.

Compass Lexecon was retained by counsel for TopBuild to evaluate the competitive effects of its $475 million acquisition of United Subcontractors Inc. (USI). The parties owned and operated the #1 and #3 nationwide insulation installation services companies in the U.S., with a combined total of 200 service branch locations.

USI was no small tuck-in—it was a transformational deal that would nearly double TopBuild's employee count and significantly expand its geographic footprint. USI (excluding the construction services business) is a leading provider of insulation installation and distribution services to the residential and commercial construction markets. USI has a diversified product and service offering, including fiberglass, spray foam and window and glass installation. USI has 38 locations in 13 states, including high growth regions in the Pacific Northwest, Mountain West, Southwest and Southeast.

The deal economics reflected TopBuild's disciplined approach. On a December 31, 2017 pro forma basis, inclusive of expected run rate synergies of $15 million, the combined company would have had revenue of $2.3 billion, adjusted EBITDA of $259 million, almost 10,000 employees and close to 300 installation and distribution locations. The Company funded this transaction through a previously announced 5.625% $400.0 million Senior Notes offering and a $100.0 million term loan. At the close of the transaction, the Company's net debt to pro forma adjusted EBITDA implies a multiple of 2.8 times pre-synergies, or 2.6 times post-synergies.

Critically, Compass Lexecon compiled a database of insulation installation competitors that was submitted to the FTC, showing the parties faced a substantial number of local competitors in metro areas where TopBuild and USI had one or more service locations that overlapped. The FTC cleared the transaction without conditions without a second request.

The regulatory clearance without a second request demonstrated something important: despite combining the #1 and #3 national players, the insulation installation market remained highly fragmented with strong local competition. TopBuild could continue consolidating without antitrust constraints.

Part V: Distribution International & Commercial/Industrial Expansion (2021-2022)

If USI proved TopBuild could execute large transactions in its core residential market, the next strategic pivot demonstrated the company's ambition to transcend residential housing cycles entirely.

In September 2021, TopBuild announced its most strategic acquisition to date. TopBuild Corp. (NYSE:BLD) has entered into an agreement to acquire Distribution International ("DI") from global private equity firm Advent International in an all-cash transaction valued at $1.0 billion. TopBuild expects to finance the acquisition using a combination of debt financing and cash on hand and to close the transaction in the fourth quarter of 2021. Robert Buck, President and Chief Executive Officer of TopBuild, stated, "The acquisition of Distribution International is highly strategic for TopBuild. It aligns with our strategy of seeking well managed companies with experienced, talented teams with expertise in our core business of insulation and adjacent products. DI provides us with a direct entry and immediate leadership position in the $5 billion mechanical insulation market which is a highly attractive and complementary new growth platform for TopBuild."

Founded in 1986, DI is the leading specialty distributor of mechanical insulation solutions for the industrial and commercial end-markets. DI has grown significantly through both market share gains and acquisitions, having completed 11 transactions over the past six years. DI has 84 branches across the United States and 17 branches in Canada. For the trailing 12 months ended June 30, 2021, DI generated pro-forma revenue of approximately $747 million, approximately half of which was tied to its MRO business and the other half related to new construction activity.

The strategic significance cannot be overstated. Distribution International served a completely different end market: mechanical insulation for pipes, HVAC systems, and industrial equipment in commercial and industrial facilities. This business had fundamentally different demand drivers than residential construction. Approximately half of DI's revenue came from maintenance, repair, and operations (MRO)—recurring revenue streams driven by the age and condition of existing buildings rather than new construction cycles.

Robert Buck stated, "Following the closing of this transaction, TopBuild will be the leader of energy saving insulation solutions in all three major end-markets: residential, commercial, and industrial. Increasingly stricter energy codes, and the desire for energy efficient solutions and reductions in carbon footprint are driving demand, and we expect they will continue to be important growth drivers for our Company."

The transaction closed in October 2021. TopBuild Corp. (NYSE:BLD), a leading installer and specialty distributor of insulation and building material products, has successfully completed its previously announced acquisition of Distribution International ("DI") from Advent International, in an all cash transaction valued at $1.0 billion.

On a June 30, 2021 pro forma basis, the combined company had trailing twelve-month revenue of $3.93 billion and adjusted EBITDA of $647 million. As of June 30, 2021, on a pro forma basis, the Company's net debt to adjusted EBITDA implies a multiple of 2.5 times pre-synergies.

This acquisition fundamentally transformed TopBuild's business mix. The Specialty Distribution segment—which had represented roughly 33% of TopBuild revenue before DI—would grow to represent over 40% of the combined company. More importantly, the commercial and industrial exposure provided a natural hedge against residential housing volatility.

The talent acquisition proved equally valuable. Joey joined TopBuild in 2021 when the Company acquired Distribution International. He was promoted to Executive Vice President of Distribution International in March 2022, and to Chief Operating Officer of TopBuild in October 2022. Prior to the acquisition, Joey was Senior Vice President of Specialty Products as well as Distribution International's East Division. Joey began his professional career in sales and marketing at Procter & Gamble in 1990. He then led Goodyear Tire and Rubber company's North American consumer brand and marketing functions before joining Knauf Insulation in 2009 where he served as VP of Marketing and subsequently in various executive leadership roles. Joey earned a Bachelor's degree in Management from the University of Alabama.

Part VI: Leadership Succession and Operational Excellence

At the end of 2020, TopBuild executed a seamless CEO transition that would set the stage for its next phase of growth.

TopBuild Corp. (NYSE:BLD), a leading installer and distributor of insulation and building material products and its Board of Directors announced that Jerry Volas, 65, will retire as Chief Executive Officer and member of the Board of Directors effective December 31, 2020. Robert Buck, 50, who has served as President and Chief Operating Officer since June 2015, will assume the role of CEO and director upon Volas' retirement. TopBuild Board Chair Alec Covington said, "Jerry has done a terrific job leading TopBuild through its spin-off from Masco (NYSE:MAS) in 2015 and overseeing its tremendous revenue growth and profitability during this period. On behalf of the Board, we thank Jerry for his dedication to TopBuild and wish him the very best upon his well-earned retirement."

Buck assumed the position of Chief Executive Officer on January 1, 2021 after serving as President and Chief Operating Officer since the Company's spin-off from Masco Corporation in June 2015.

Robert Buck's background made him ideally suited for the role. Buck joined TopBuild in 2009 when it was Masco Contractor Services (MCS), serving as the division's President and Chief Executive Officer. He assumed his current role at TopBuild in June 2015 when the company was spun-off from Masco. Buck began his career with Masco Corporation in 1997 at Liberty Hardware where he spent eight years in several operations leadership roles and worked extensively in international operations.

He became Executive Vice President in 2005 and helped lead the merger of another Masco company with Liberty Hardware before being promoted to the office of President in 2007. Robert earned a Master's degree in Business Administration from the University of North Carolina at Greensboro.

Robert Buck stated, "I am honored to be named the next CEO of TopBuild and want to thank both Jerry and the Board for the confidence they have placed in me to lead this strong organization. Jerry and I have worked together for many years, and I welcome working with him through this transition period as we continue to grow our business. Over the past four and a half years we've built a strong organization with a very broad and deep bench of talent. Our strategic plan will remain in place and our team will continue its laser focus on driving profitable growth."

The succession exemplified TopBuild's thoughtful approach to leadership development. Buck had been preparing for this role for five years as COO, deeply involved in every major acquisition and strategic decision. The transition created no disruption to operations or strategy.

Under Buck's leadership, TopBuild has accelerated its acquisition cadence while maintaining integration discipline. M&A is a core strength of TopBuild, which has a proven track record of creating significant value, having successfully completed 45 acquisitions since the spin-off in 2015 and generating an 18.2% return on invested capital as of December 31, 2024.

Part VII: The Modern TopBuild Machine (2022-2025)

By 2024, TopBuild had transformed from a mid-cap spinoff into a diversified building products platform with genuine scale advantages.

TopBuild provides insulation installation services nationwide through its Installation segment which has approximately 250 branches located across the United States. It distributes building and mechanical insulation, insulation accessories and other building product materials for the residential, commercial, and industrial end markets through its Specialty Distribution business.

2024: Record Results Amid Housing Uncertainty

TopBuild Corp. (NYSE:BLD) reported solid fourth quarter and full-year 2024 results, with Q4 sales growing 2.0% to $1.31 billion, driven by a 6.6% improvement in Specialty Distribution. The company achieved a gross margin of 29.9% and adjusted EBITDA margin of 19.7% in Q4. For the full year 2024, TopBuild reached record sales of $5.3 billion and adjusted EBITDA of $1.07 billion. The company completed 8 acquisitions totaling $153.1 million in annual sales and returned $966.4 million to stockholders by repurchasing approximately 2.5 million shares.

TopBuild Corp (BLD) achieved its ninth consecutive year of growth and profit expansion in 2024.

The capital allocation philosophy reflects TopBuild's maturation as a compounder. Looking ahead to 2025, TopBuild anticipates sales between $5.05 to $5.35 billion and adjusted EBITDA ranging from $925 million to $1.075 billion. The company announced a new $1 billion share repurchase authorization, bringing total repurchase availability to $1.2 billion. Management emphasized that acquisitions remain the top priority for deploying capital, citing a robust M&A pipeline.

2025: Expanding the Building Envelope

In July 2025, TopBuild made another transformative move—this time into an entirely new category. TopBuild Corp. (NYSE:BLD), a leading installer and specialty distributor of insulation and related building material products to the construction industry in the United States and Canada, announced that it has entered into an agreement to acquire Progressive Roofing, a portfolio company of Bow River Capital, for $810 million in cash. This represents approximately 9.1x Progressive's earnings before interest, taxes, depreciation and amortization (EBITDA) for the trailing twelve months ended March 31, 2025, and a multiple of 8.6x EBITDA post-synergies, considering $5M in synergies. The transaction is expected to be immediately accretive to adjusted earnings per share.

Founded in 1978, Progressive Roofing is a leader in commercial roofing installation services in the United States, with a comprehensive offering that includes re-roofing, recurring maintenance services, and new construction. The company serves attractive commercial verticals, including education, technology, industrial, healthcare and government. Progressive generated $438 million in revenue and $89 million in EBITDA for the trailing 12 months ended March 31, 2025. Approximately 70% of the company's revenue is related to non-discretionary re-roofing and maintenance, while approximately 30% is from new construction. Based in Phoenix, Progressive employs more than 1,700 people across 12 branches.

"Entering the large and growing Commercial Roofing business through the acquisition of Progressive Roofing is a natural next step for TopBuild. The acquisition of Progressive, one of the largest commercial roofing installers in the United States, will enable us to offer commercial customers more comprehensive building envelope installation solutions," said Robert Buck, President and Chief Executive Officer of TopBuild.

The total addressable market for commercial roofing installation services is approximately $75 billion and is highly fragmented. TopBuild and Progressive Roofing both have proven M&A track records, with robust acquisition processes in place.

This acquisition extends TopBuild's strategy in multiple dimensions: it enters a new category (roofing), maintains focus on installation services where TopBuild has demonstrated expertise, and further reduces residential housing exposure. With 70% of Progressive's revenue from non-discretionary re-roofing and maintenance, the business provides natural counter-cyclicality.

The SPI Deal: Perseverance Pays Off

In October 2025, TopBuild completed a deal years in the making. TopBuild Corp. (NYSE:BLD), a leading installer of insulation and commercial roofing and a specialty distributor of insulation and related building material products to the construction industry in the United States and Canada, announced that it successfully acquired Specialty Products and Insulation (SPI), a leading specialty distributor and fabricator of mechanical insulation solutions for the commercial, industrial and residential end markets in North America, for $1.0 billion in cash. The acquisition closed on October 7 and was funded with cash on hand, including proceeds from the September senior notes issuance. The acquisition excludes SPI's metal building insulation ("MBI") business. SPI generated approximately $700 million in revenue and $75 million in EBITDA for the trailing twelve months ended June 30, 2025. The transaction represents approximately 12.4x SPI's EBITDA for the trailing twelve months ended June 30, 2025, inclusive of tax benefits.

The SPI story illustrates TopBuild's disciplined approach to M&A. A deal was announced in July 2023, but in May 2024 the acquisition was called off as the two companies were unable to agree a valuation for the metal building insulation part of SPI's business.

TopBuild Corp. announced its decision today to abandon its proposed $960 million acquisition of its rival, SPI Parent Holding Company (SPI). The abandonment comes after the department's competition concerns. The Justice Department issued the following statement from Assistant Attorney General Jonathan Kanter of the Antitrust Division: "TopBuild's proposed acquisition of SPI would have harmed competition across the United States by combining two of the largest providers of important building insulation products and eliminating fierce head-to-head competition between them."

Rather than force through an unfavorable deal, TopBuild walked away. A year later, with the metal building insulation business carved out, the companies reached terms that satisfied both parties and regulators.

Robert Buck, President and Chief Executive Officer of TopBuild, stated, "The SPI acquisition is highly strategic for TopBuild. The addition of SPI's resources and capabilities further enhances our customer value proposition while its complementary fabrication footprint strengthens and expands our presence across North America. The transaction also drives our growth in non-cyclical revenue streams given that approximately 55% of SPI's revenue relates to recurring maintenance and repair."

Part VIII: Business Model Deep Dive — Why This Works

TopBuild's sustained success stems from a combination of structural advantages that compound over time.

Scale Economics in a Fragmented Market

TopBuild's position as one of the largest single purchasers of insulation in North America creates meaningful negotiating leverage with manufacturers. This translates into better pricing, preferential allocation during supply constraints, and access to technical support that smaller competitors cannot match.

But scale provides benefits beyond purchasing power. The company's 250+ installation branches and 150+ distribution locations create logistics advantages—the ability to move crews and materials efficiently across regions to match demand. A local installer with three trucks cannot replicate this flexibility.

The Labor Moat

In an industry where human capital is the primary asset, TopBuild's ability to attract, train, and retain skilled installers represents a genuine competitive advantage. Installation quality matters—improperly installed insulation fails code inspections, causes callbacks, and damages relationships with builders. The training infrastructure required to maintain consistent quality across thousands of installers is difficult for smaller competitors to replicate.

When TopBuild acquires regional installers, it gains not just customers and contracts but experienced installer crews with local relationships. This tacit knowledge—understanding which builders value speed versus quality, navigating local permitting processes, managing seasonal workforce fluctuations—cannot be purchased separately.

The Dual Model Advantage

TopBuild's ownership of both installation (TruTeam) and distribution (Service Partners, Distribution International) creates strategic optionality that pure-play competitors lack. The company can serve customers who want turnkey installation services and those who prefer to purchase materials and install themselves. It captures margin at different points in the value chain depending on market conditions.

Perhaps more importantly, the distribution business provides visibility into market trends. When a regional distributor sees installation contractors increasing orders, it provides early signal of local construction activity. This intelligence informs both operational planning and acquisition targeting.

Process Power in Integration

Robert Buck added, "The identification and integration of acquisitions is a TopBuild core competency as evidenced by our successful M&A track record over the past six years. During this period, we have acquired 26 companies that are contributing over $820 million of annual revenue and creating tremendous value for our stakeholders. We are confident DI will be another outstanding addition to our Company."

The company has developed repeatable playbooks for post-acquisition integration covering IT systems migration, supply chain optimization, best practice sharing, and cultural onboarding. Each acquisition makes the next one easier and faster to integrate—a classic example of learning curve advantages.

Part IX: Competitive Landscape and Industry Dynamics

TopBuild operates in a market with a unique competitive structure: two scaled national players and hundreds of regional competitors.

TopBuild and Installed Building Products share approximately 70% of the US insulation installation market but rarely compete head-on as they operate in different regions.

Installed Building Products (IBP): The Principal Competitor

Installed Building Products, Inc., together with its subsidiaries, engages in the installation of insulation, waterproofing, fire-stopping, fireproofing, garage doors, rain gutters, window blinds, shower doors, closet shelving and mirrors, and other products in the United States. It operates through Installation, Distribution, and Manufacturing operation segments.

Installed Building Products, Inc. (IBP) The company commenced operations in 1997. Installed Building Products stands as a major national player in the building products installation sector, second only to TopBuild in overall scale based on 2024 estimates.

IBP has pursued a similar roll-up strategy, acquiring regional installers and building national scale. The founder's son Jeff Edwards began working in the business in the 1990s and recognised a huge scaling opportunity. He started buying similar family-owned insulation installer firms around the country, gained procurement discounts from suppliers as the group grew larger, and then used the excess profitability to reinvest into further acquisitions and drive more scale efficiencies. Starting with just one branch some 50 years ago, IBP now represents around 30% of the total US insulation installation industry. The business now has considerable scale and distribution advantages.

However, the competitive dynamic between TopBuild and IBP is more nuanced than typical duopoly markets. Because insulation installation is inherently local—crews must travel to job sites—the two companies rarely compete directly for the same projects. Their service territories largely complement rather than overlap.

The Fragmented Remainder

TopBuild Corp. (BLD) holds approximately 19% market share and is the largest in terms of market share, with significant scale in both installation (TruTeam) and distribution (Service Partners). Regional/Local Installers represent approximately 70% of the market with deep local market relationships and operational agility within specific geographies.

The remaining 30% of the market consists of hundreds of regional and local installers—family businesses, single-location operators, and regional chains. This fragmentation provides the consolidation opportunity that both TopBuild and IBP continue to pursue.

Part X: Competitive Analysis — Porter's Five Forces

1. Threat of New Entrants: LOW

Establishing a national insulation installation platform requires significant time and capital. TopBuild's 250+ branches took decades to build through organic growth and acquisitions. New entrants cannot simply purchase this infrastructure—it must be assembled one relationship, one acquisition, one trained installer at a time.

More importantly, relationships with national homebuilders are extremely sticky. Builders value reliability and consistency across multiple markets. A new entrant cannot credibly promise national service capability without first building the local infrastructure.

2. Bargaining Power of Suppliers: MODERATE

Insulation manufacturing is concentrated among three major suppliers: Owens Corning, Johns Manville (a Berkshire Hathaway company), and Knauf. This concentration would normally create supplier power.

However, TopBuild's scale as one of the largest single purchasers provides countervailing leverage. Manufacturers cannot afford to lose TopBuild as a customer without significantly impacting their own volumes. The relationship is characterized by mutual dependence rather than supplier dominance.

Additionally, TopBuild's product-agnostic approach—installing fiberglass, spray foam, and cellulose—provides optionality to shift between insulation types based on pricing and availability.

3. Bargaining Power of Buyers: LOW-MODERATE

Customer fragmentation limits buyer power. With no single customer exceeding 3% of revenue, TopBuild does not face concentrated negotiating pressure from major accounts.

However, large production homebuilders do negotiate volume arrangements and can pressure pricing in their markets. TopBuild manages this through service differentiation—reliability, quality, and scheduling flexibility—rather than competing purely on price.

4. Threat of Substitutes: VERY LOW

Insulation is code-required in virtually all new construction. Buildings cannot be legally occupied without meeting minimum insulation requirements. This regulatory mandate creates inelastic demand—builders cannot simply choose to forgo insulation.

Different insulation types (fiberglass, spray foam, cellulose) do compete, but TopBuild installs all varieties. The company is agnostic to which product wins market share within the insulation category.

5. Industry Rivalry: MODERATE

Competition occurs primarily at the local level, where TopBuild and IBP rarely overlap. Price competition does exist but is tempered by service differentiation and the importance of reliability in construction scheduling.

The highly fragmented competitor base actually reduces rivalry intensity—small regional players cannot match the pricing or service capabilities of scaled national platforms.

Part XI: Strategic Analysis — Hamilton's 7 Powers

1. Scale Economies: STRONG

TopBuild demonstrates classic scale economies across multiple dimensions: - Purchasing power with insulation manufacturers drives unit cost advantages - National logistics network optimizes crew deployment and material distribution - Corporate overhead is amortized across a larger revenue base - IT systems and integration capabilities serve all branches equally

As the largest player in a fragmented market, TopBuild's scale advantages compound with each acquisition.

2. Network Economies: MODERATE

TopBuild is not a traditional network business—installers serving a home in Phoenix don't directly benefit from installers serving a home in Atlanta. However, the branch network does create density advantages: more branches mean shorter drive times, faster response to customer requests, and better crew utilization.

The distribution network also exhibits mild network characteristics—more branches mean broader product availability and faster delivery for customers across the service area.

3. Counter-Positioning: MODERATE

TopBuild's combined installation and distribution model creates some counter-positioning versus pure-play competitors. Insulation manufacturers (Owens Corning) could theoretically forward-integrate into installation but would create channel conflict with their existing contractor customers. Pure-play distributors lack the installation capabilities that provide TopBuild's service differentiation.

4. Switching Costs: MODERATE

For homebuilders, switching installers creates operational risk. Established relationships include understanding of scheduling expectations, quality standards, and local permitting requirements. A new installer might deliver equivalent product but requires time to understand each builder's specific needs.

These switching costs are not contractual but operational—real enough to create meaningful customer inertia.

5. Branding: WEAK

TruTeam and Service Partners are trade brands with limited consumer recognition. Homebuyers do not choose their home's insulation installer—they trust the builder to make appropriate selections. Brand matters primarily to construction industry professionals rather than end consumers.

6. Cornered Resource: MODERATE

TopBuild's most valuable cornered resource is its experienced installer workforce. Skilled insulation installers require training and develop expertise over years. When TopBuild acquires a regional competitor, the installed base of trained employees represents a resource that cannot be easily replicated.

Local market knowledge—which subcontractors are reliable, which builders value speed versus quality, how to navigate local regulations—constitutes tacit knowledge that transfers with acquisitions.

7. Process Power: STRONG

TopBuild's acquisition integration playbook represents genuine process power. "Our performance in 2024 was driven by consistent execution within our unique operating model and the entire TopBuild team's relentless pursuit of operational excellence and focus on driving improvements."

The company has refined this capability over 45+ acquisitions, developing institutional knowledge about what works in post-merger integration. Competitors pursuing similar roll-up strategies must learn these lessons through costly trial and error.

Part XII: Secular Tailwinds and Growth Drivers

TopBuild benefits from multiple secular trends that provide structural demand growth independent of housing cycle fluctuations.

Energy Code Tightening

The residential provisions — covering one- and two-family homes and multifamily dwellings up to three stories — are expected to be about 7% more efficient. The commercial provisions — covering buildings four stories and higher — are expected to be about 10% more efficient.

Each code cycle increases required insulation R-values, driving greater insulation content per building. This "content growth" provides volume increases even in flat housing markets.

Climate and Sustainability Focus

The Inflation Reduction Act and broader sustainability initiatives are driving increased attention to building energy efficiency. Insulation is one of the most cost-effective ways to reduce building energy consumption and carbon footprint. As climate concerns intensify, demand for higher-performance building envelopes should accelerate.

Commercial and Industrial Exposure

Approximately 87% of SPI's revenue is related to commercial and industrial end markets.

TopBuild's expansion into mechanical insulation through Distribution International and SPI reduces dependence on residential housing cycles. Commercial and industrial buildings require insulation for pipes, HVAC systems, and process equipment—demand driven by different factors than residential construction.

Retrofit and Maintenance Opportunities

Approximately 55% of SPI's revenue is driven by recurring maintenance and repair, improving TopBuild's exposure to non-cyclical revenue.

The installed base of buildings requiring insulation maintenance, upgrades, and repairs represents a large and growing addressable market largely insulated from new construction cycles.

Part XIII: Key Risks and Bear Case Considerations

Housing Cycle Exposure

Despite diversification efforts, TopBuild remains significantly exposed to residential new construction. Total housing starts for 2024 were 1.36 million, a 3.9% decline from the 1.42 million total from 2023. Single-family starts in 2024 totaled 1.01 million, up 6.5% from the previous year. Multifamily starts ended the year down 25% from 2023.

Elevated mortgage rates and housing affordability challenges continue to pressure residential construction. An extended housing downturn would negatively impact TopBuild's Installation segment.

Acquisition Integration Risk

TopBuild's growth strategy depends on continued successful acquisition execution. The company has an excellent track record, but integration challenges can emerge—particularly with larger deals or entry into new categories like commercial roofing.

Labor Market Pressures

The installer workforce is challenging to recruit and retain. Immigration policy changes could impact labor availability, particularly in markets with significant immigrant installer populations. Labor cost inflation could pressure margins.

Supplier Concentration

Reliance on three major insulation manufacturers creates supply chain risk. Manufacturing disruptions, pricing actions, or capacity constraints at major suppliers could impact TopBuild's cost structure and service capabilities.

Interest Rate Sensitivity

Higher interest rates impact TopBuild through two channels: increased borrowing costs on acquisition financing and reduced housing demand from rate-sensitive homebuyers. The company has managed leverage conservatively, but extended high-rate environments create headwinds.

Part XIV: Key Performance Indicators for Investors

For long-term investors monitoring TopBuild, three metrics provide the clearest signal of business health:

1. Same-Branch Sales Growth

This metric strips out the impact of acquisitions to reveal organic growth in existing operations. Positive same-branch growth indicates market share gains, pricing power, and healthy underlying demand. Negative readings suggest competitive pressure or market weakness.

Same-branch sales growth provides the clearest view of whether TopBuild is winning in its existing markets versus simply growing through acquisitions.

2. Adjusted EBITDA Margin

TopBuild also improved adjusted EBITDA margin by 10 basis points to 19.7%.

Margin trends reveal whether TopBuild is extracting synergies from acquisitions and maintaining operational discipline. Expanding margins indicate successful integration and scale benefits. Contracting margins may signal pricing pressure, labor cost inflation, or integration challenges.

3. Return on Invested Capital (ROIC)

M&A is a core strength of TopBuild, which has a proven track record of creating significant value, having successfully completed 45 acquisitions since the spin-off in 2015 and generating an 18.2% return on invested capital as of December 31, 2024.

ROIC measures whether TopBuild is creating value with its acquisition-driven growth strategy. An 18.2% ROIC indicates that capital deployed in acquisitions is generating returns well above the cost of capital—a sign of disciplined deal execution and successful integration.

Declining ROIC might indicate that TopBuild is paying higher multiples for acquisitions, experiencing integration challenges, or facing diminishing returns as the consolidation opportunity matures.

Part XV: Bull Case vs. Bear Case

Bull Case

Continued Consolidation Runway

The insulation installation market remains highly fragmented. Regional/Local Installers represent approximately 70% of the market. TopBuild has demonstrated the ability to acquire and integrate regional players successfully. The consolidation opportunity extends for years, if not decades.

Diversification Reduces Cyclicality

The Distribution International and SPI acquisitions significantly increased commercial and industrial exposure. The Progressive Roofing deal adds non-discretionary maintenance revenue. As these businesses grow as a percentage of total revenue, TopBuild's earnings stability should improve.

Energy Efficiency Tailwinds

Building energy codes will continue tightening. Climate concerns will drive increased demand for building efficiency investments. TopBuild is well-positioned to benefit from these secular trends regardless of housing cycle fluctuations.

Capital Allocation Excellence

Management has demonstrated exceptional capital allocation discipline—pursuing accretive acquisitions, maintaining reasonable leverage, and returning excess capital through buybacks. TopBuild's Board authorized the repurchase of up to $1.0 billion of the Company's outstanding common stock. The new authorization is in addition to the $188.1 million remaining from the prior authorization, bringing total availability for share repurchases to $1.2 billion.

Bear Case

Housing Downturn Exposure

Despite diversification, residential new construction remains approximately 40-50% of TopBuild's business. An extended housing recession would materially impact earnings. Elevated mortgage rates and affordability challenges create near-term headwinds.

Acquisition Multiple Expansion

As TopBuild and IBP consolidate the industry, acquisition targets may demand higher valuations. If TopBuild must pay increasing multiples for deals, ROIC will decline even with successful integration.

Integration Challenges in New Categories

The Progressive Roofing acquisition takes TopBuild into an adjacent but different industry. Commercial roofing has different competitive dynamics, labor requirements, and customer relationships. Integration risk is elevated compared to core insulation acquisitions.

Margin Pressure

Labor cost inflation, supplier pricing actions, and competitive pressure could compress margins. The company's 19-20% adjusted EBITDA margins leave limited room for absorption.

Conclusion: The Power of Boring

TopBuild's journey from orphaned spinoff to industry leader illustrates several enduring investment principles.

First, corporate spinoffs create opportunity. When Masco separated its insulation services division in 2015, it was shedding a business that didn't fit its portfolio narrative. But that orphaned business—freed from conglomerate bureaucracy and equipped with focused management—could pursue a strategy tailored to its unique economics.

Second, disciplined roll-up strategies work in fragmented industries. TopBuild has executed 45+ acquisitions while maintaining integration discipline and generating 18%+ returns on invested capital. The key differentiator is not the strategy itself—many companies pursue roll-ups—but the execution rigor and institutional capability TopBuild has built.

Third, boring businesses can be beautiful investments. Insulation installation lacks the glamour of technology or healthcare innovation. It doesn't generate viral press coverage or spark investor enthusiasm at cocktail parties. But the product is essential, the demand is code-driven, and the competitive dynamics favor scaled, disciplined operators.

TopBuild Corp achieved its ninth consecutive year of growth and profit expansion in 2024.

The company that began as Masco's unwanted services division now stands as the dominant force in North American insulation installation and distribution—a position that took decades to build and would take competitors decades to replicate.

For investors willing to look past the unglamorous exterior, TopBuild represents the kind of high-quality compounder that value creation is built upon: strong competitive positioning, disciplined capital allocation, capable management, and secular tailwinds that should persist for years to come.

The insulation in your walls may be hidden—but the investment opportunity has been hiding in plain sight.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube