IES Holdings: From Bankruptcy to Billions — The Quiet Compounder Powering America's Data Centers

Introduction & Episode Roadmap

Picture this: It's August 2020, and America is in the grip of a pandemic. Most executives are hunkering down, slashing budgets, and praying for survival. But in Houston, Texas, a veteran hedge fund manager named Jeffrey Gendell is making a move that would seem either brilliant or reckless. He's stepping out of the shadows—where he'd quietly amassed a 57% stake in a company most investors had never heard of—to become CEO of IES Holdings, a scrappy electrical contractor with a checkered past.

The company now boasts a market capitalization of $7.01 billion with trailing twelve-month revenue of $3.25 billion. Yet walk into any investment conference, mention IES Holdings, and you'll likely get blank stares. This is a company that has compounded shareholder wealth at an extraordinary rate while flying almost completely under the radar.

The IES Holdings story contains every ingredient that makes for a compelling business case study: a spectacular failure, a distressed investor playing the long game, a hidden tax asset worth hundreds of millions, a decentralized conglomerate structure, and—critically—being in exactly the right position when AI-fueled data center demand exploded across America.

Today, IES designs and installs integrated electrical and technology systems and provides infrastructure products and services to a variety of end markets. But to understand how this company became one of the best-performing stocks of the 2020s, we need to rewind to the go-go days of the late 1990s, when roll-up strategies were all the rage and a group of Houston entrepreneurs thought they could consolidate America's fragmented electrical contracting industry.

The questions we'll explore: When does a roll-up strategy work, and when does it blow up spectacularly? What happens when an activist investor becomes an operator? How did a bankrupt company emerge with a hidden asset that would shield hundreds of millions in future profits from taxation? And how do you catch a generational wave—like AI infrastructure—at precisely the right moment?

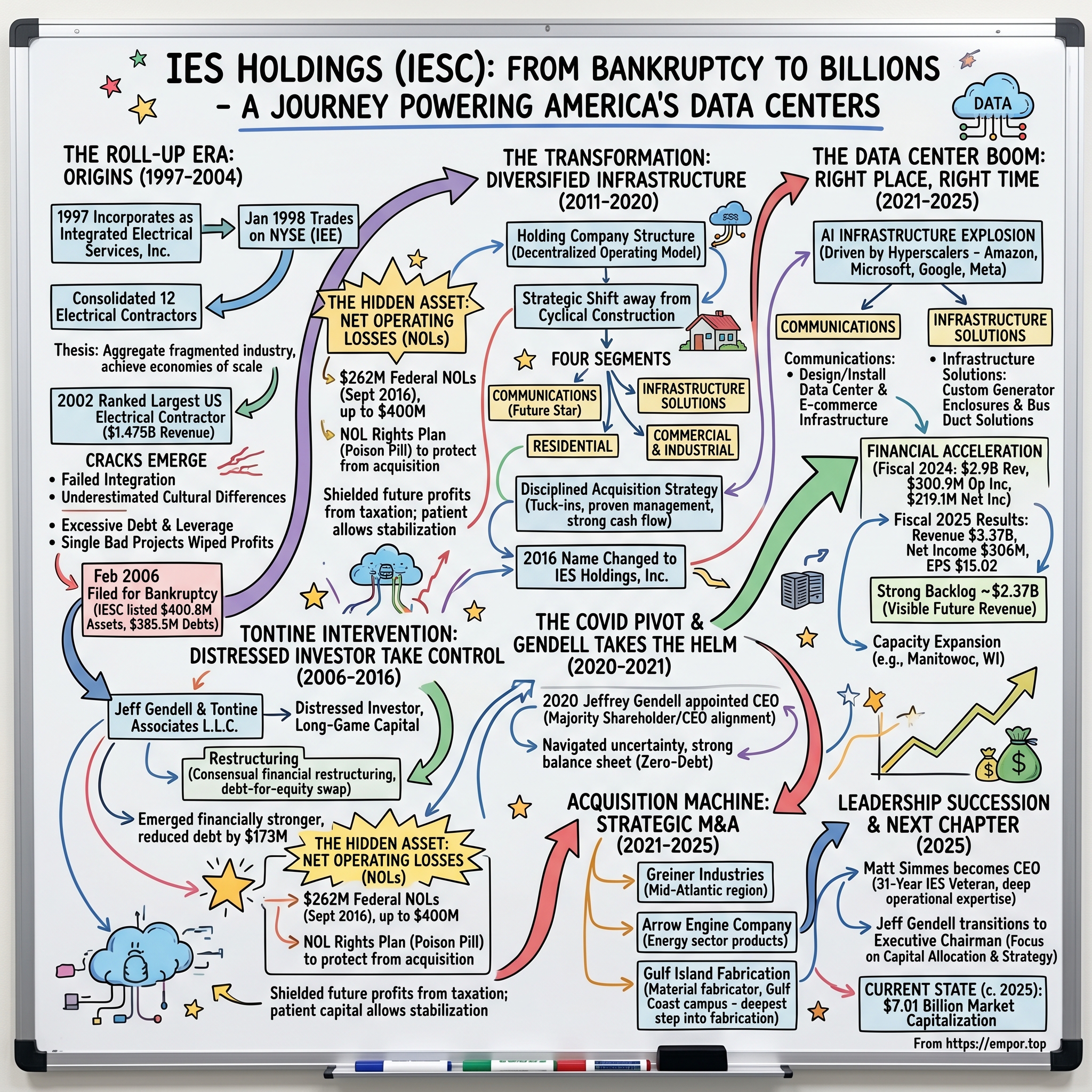

The Roll-Up Era: Origins & The Original Thesis (1997-2004)

The Birth of a "Platform Company"

The late 1990s were intoxicating times for financial engineers. The playbook was simple: find a fragmented industry, acquire a bunch of small players, slap them together under a corporate umbrella, promise "synergies," and watch the multiple expansion work its magic. It worked in waste management. It worked in funeral homes. It worked in staffing. Why not electrical contracting?

IES Holdings, Inc. was founded in 1997 as Integrated Electrical Services, Inc. through the consolidation of 12 electrical contractors. The company was established with the vision of creating a national platform of electrical contractors to serve the construction industry.

The thesis wasn't crazy. Electrical contracting in America was—and still is—incredibly fragmented. Thousands of small, family-owned firms compete for work across commercial, industrial, and residential markets. Local relationships matter enormously, but there are genuine economies of scale in back-office functions, equipment procurement, and surety bonding.

June 26, 1997 incorporates as Integrated Electrical Services Incorporated. January 27, 1998, Integrated Electrical Services began trading with the symbol (IEE) on the New York Stock Exchange.

The IPO raised capital for an aggressive acquisition spree. The company gobbled up electrical contractors across the country at a frenetic pace, using a combination of cash and stock to fund the buying binge.

Rise to Industry Dominance

By any traditional metric, the strategy appeared to be working spectacularly. In 2002 Integrated Electrical Services was ranked as the largest electrical contractor in the United States, with $1.475 billion in revenue. In just five years, IES had grown from a collection of 12 contractors to the nation's undisputed leader in its field.

But beneath the impressive revenue figures lurked serious problems. Roll-up companies live or die by their ability to integrate acquisitions, maintain discipline on pricing, and generate enough cash flow to service the debt they take on to fund growth. IES struggled on all three fronts.

The Cracks Emerge

Years later, in 2004, the company had some accounting issues which, combined with excessive leverage, led to IESC filing for bankruptcy in February 2006.

What went wrong? The classic roll-up failure modes: overpaying for acquisitions in the heat of a competitive bidding war; underestimating the difficulty of integrating disparate company cultures; failing to realize that "synergies" in a people-intensive, project-based business don't materialize as easily as they do on a spreadsheet.

The electrical contracting business is brutal. Projects are bid competitively, margins are thin, and a single bad project can wipe out a year's profits. The decentralized nature of the business—where relationships with local builders and developers are everything—fought against the centralizing logic of the roll-up model.

IES listed $400.8 million in assets and $385.5 million in debts in its petition, and it claimed about $1.1 billion in revenue for the fiscal year ending Sept. 30, 2005. The company that had once been the nation's largest electrical contractor was now fighting for survival.

For investors, the cautionary tale was clear: roll-ups can create enormous value when executed with discipline, but the temptation to grow for growth's sake—to chase revenue rather than profits—can lead to catastrophe.

The Tontine Intervention: A Distressed Investor Takes Control (2006-2016)

Enter Jeff Gendell

Every great turnaround story needs a protagonist willing to take a contrarian bet when everyone else is running for the exits. For IES Holdings, that person was Jeffrey Gendell.

He is the founder and managing member of Tontine Associates, L.L.C., which, together with its affiliates (collectively, "Tontine"), is a private investment management firm and the majority shareholder. Mr. Gendell formed Tontine in 1995 and manages all of the investment decisions at the firm, where he has built an extensive record in public and private investing across industries.

Gendell wasn't your typical activist investor looking for a quick flip. Prior to forming Tontine, Mr. Gendell held senior investment management positions at several other private investment firms, including Odyssey Partners, L.P., and began his career in investment banking over 35 years ago at Smith Barney, Harris Upham & Co. where he was involved in capital markets, corporate finance and M&A activity. He holds a Bachelor's degree from Duke University and a Masters of Business Administration from the Wharton School of the University of Pennsylvania.

This wasn't a vulture fund looking to strip assets—it was a patient capital allocator who saw value where others saw only distress.

The Restructuring

The case was filed pursuant to an agreement with institutions that hold approximately 61% of the company's approximately $173 million outstanding, 9 3/8% senior subordinated notes due 2009 to support a consensual financial restructuring of the company through a pre-arranged chapter 11 plan of reorganization.

Jeffrey Gendell's Tontine Partners, a very successful hedge fund in the late 1990s until 2008, held a significant percentage of IESC's bonds that he exchanged into stock when the company exited bankruptcy.

The restructuring was designed to be fast and surgical. By allowing IES to exchange 100% of the senior subordinated notes for new equity, "our plan will reduce the company's debt balance by approximately $173 million and allow IES to emerge as a financially stronger, more efficient company."

On May 12, 2006, Integrated Electrical Services, Inc. and all of its domestic business units consummated the Plan of Reorganization and exited from Chapter 11. In just three months—lightning speed for a bankruptcy—IES had shed $173 million in debt and emerged with a clean balance sheet.

But the real genius of Gendell's play wasn't just the debt-for-equity swap. It was what came along with it.

The Hidden Asset: NOLs as Strategic Weapons

When companies lose money, those losses don't simply evaporate. Under U.S. tax law, they become Net Operating Loss carryforwards (NOLs)—assets that can be used to offset future taxable income, effectively allowing a company to pay zero federal taxes until the NOLs are exhausted.

As of September 30, 2016, we have approximately $262.0 million of federal NOLs that are available to use to offset taxable income. At various points, the company's NOL balance approached $400 million.

Think about what this means in practice: every dollar of pre-tax profit that IES generated would flow straight to the bottom line without the 21% (or higher, in earlier years) federal tax bite. For a company emerging from bankruptcy with a long runway of future profitability, this was equivalent to a secret weapon.

The NOL Rights Plan was intended to preserve the availability of IES's federal net operating loss carryforwards by deterring an acquisition of the Company's stock in excess of a threshold amount that could trigger an "ownership change" within the meaning of the Internal Revenue Code.

IES implemented a "poison pill" specifically to protect these NOLs. Any potential acquirer would have to weigh whether triggering an ownership change—and potentially losing the NOL shield—was worth it. This gave IES breathing room to execute its turnaround without fear of being absorbed by a competitor.

Building for the Long Term

Gendell has served as a director and as Chairman of the Board since November 2016. For a decade after the bankruptcy emergence, Gendell played a supporting role—a patient, influential board member rather than an operator. He allowed management to stabilize the business while he focused on capital allocation and strategic direction.

This patience is unusual in a world of activist investors demanding immediate results. Gendell understood something crucial: the electrical contracting business required operational expertise that a hedge fund manager couldn't simply parachute in and provide. The turnaround would take time.

The Transformation: From Electrician to Diversified Infrastructure Company (2011-2020)

The Holding Company Structure

The original IES model—a single integrated electrical contractor—had failed. What emerged from the ashes was something fundamentally different: a holding company structure that recognized the inherent diversity of the business.

The strategic shift towards diversification through targeted acquisitions, particularly after 2010, has reshaped IES. Moving purposefully into areas like infrastructure solutions, communications technology, and specialized industrial services broadened its market reach and reduced reliance on cyclical construction markets.

The company employs a decentralized operating model, empowering local management teams within its numerous subsidiaries to manage projects and customer relationships effectively. This structure allows for responsiveness and tailored solutions specific to regional market needs.

The Four-Segment Model

IES reorganized itself into four distinct business segments, each targeting different end markets:

IES Holdings Inc owns and manages subsidiaries that design and installs integrated electrical and technology systems and provide infrastructure products and services. It has four business segments; Communications, Residential, Infrastructure Solutions, and Commercial & Industrial.

Communications: The segment that would become IES's star performer designs, builds, and maintains communications infrastructure within data centers, corporate buildings, e-commerce distribution centers, and high-tech manufacturing facilities.

Residential: Provides electrical installations to single-family housing and multi-family apartments, along with HVAC and plumbing services in certain markets.

Infrastructure Solutions: Manufactures custom-engineered products like generator enclosures and bus duct solutions, and provides electro-mechanical repair services.

Commercial & Industrial: Offers electrical and mechanical design, construction, and maintenance services for office buildings, manufacturing facilities, data centers, and renewable energy projects.

Disciplined Acquisition Strategy

The roll-up mentality was dead. In its place emerged a more disciplined approach to M&A.

IESC's corporate strategy is one built on improving its existing businesses and completing tuck-in acquisitions. Put simply, IESC employs a 'rollup' strategy, using a nuanced approach when considering acquisition targets. The company seeks to invest in or acquire businesses with the following characteristics: Proven management with a willingness to continue post-acquisition. Low technological and/or product obsolescence risk. Established market position and sustainable competitive advantages. Strong cash flow characteristics.

This wasn't the frenzied, growth-at-any-cost acquisition spree of the 1990s. Each deal was evaluated on its own merits. Management teams were kept in place. The corporate office's job was capital allocation and strategic oversight—not micromanaging local operations.

Rebranding for a New Era

In 2016, the company officially changed its name from Integrated Electrical Services to IES Holdings, Inc. to better reflect its expanded scope of operations beyond traditional electrical services. The rebranding signaled to the market that this was no longer just an electrical contractor—it was a diversified infrastructure company with multiple growth vectors.

The holding company structure allowed each subsidiary to maintain its own identity and customer relationships while benefiting from IES's balance sheet strength and capital allocation expertise. It was a model borrowed from the likes of Danaher and Berkshire Hathaway—decentralized operations with centralized capital allocation.

The COVID Pivot & Gendell Takes the Helm (2020-2021)

The Leadership Transition

The year 2020 brought unprecedented challenges and an unexpected leadership change. IES Holdings, Inc. announced today that Jeffrey L. Gendell has been appointed as Interim Chief Executive Officer, succeeding Gary S. Matthews, who has resigned as Chief Executive Officer to pursue other interests.

After fourteen years of patient oversight as a board member and shareholder, Gendell was stepping directly into the operator's seat—right in the middle of a global pandemic.

Despite the ongoing economic uncertainty related to COVID-19, I remain optimistic about the Company's outlook and believe that our strong balance sheet and cash flow generation help position the Company to both manage through future economic disruptions and execute on our long-term growth strategy.

From Investor to Operator

Gendell's dual role—majority shareholder AND CEO—created an alignment of interests rarely seen in public markets. Every decision he made as CEO would directly impact his largest investment. There was no misalignment between management incentives and shareholder returns.

IES Holdings is a founder-led company (founder holds 55% of the company) that stands apart from the typical promotional playbook—rather than flashy marketing, it quietly prioritizes operational excellence and shareholder alignment.

Mr. Gendell served as Chief Executive Officer from October 1, 2020 to June 30, 2025, and Interim Chief Executive Officer from July 31, 2020 to September 30, 2020.

A Strong Foundation for Growth

While the pandemic created uncertainty, IES's diversification across end markets provided resilience. Residential construction remained strong as Americans fled cities for suburbs. Data center construction continued unabated as the pandemic accelerated digital transformation. Infrastructure projects received government support.

The company's zero-debt balance sheet—built through years of conservative financial management—meant IES could play offense while competitors scrambled to manage liquidity. When opportunities emerged, IES had the firepower to act.

The Data Center Boom: Right Place, Right Time (2021-2025)

AI Infrastructure Demand Explodes

If you had to pick the single most important driver of IES Holdings' transformation from obscure contractor to market darling, it would be one word: data centers.

IESC's Communications business is largely cyclical and highly levered to communications infrastructure spending. Growth this segment is mainly driven by demand increases for computing and storage resources in the U.S. Put another way, this segment's growth stems from the continued build-out of new and maintenance of existing data centers in the United States.

When ChatGPT launched in November 2022, it triggered an arms race among hyperscalers—Amazon, Microsoft, Google, Meta—to build out AI computing infrastructure. Every new AI model required more graphics processing units (GPUs), more servers, more cooling systems, and critically, more electrical infrastructure to power it all.

Our Communications segment's revenue was $299.2 million in the third quarter of fiscal 2025, an increase of $106.9 million or 56% compared with the third quarter of fiscal 2024. The strong demand across the business at the beginning of fiscal 2025 has continued to accelerate, particularly in the data center market. In addition, our high-tech manufacturing and distribution center end markets remain strong.

Financial Performance Acceleration

The numbers tell the story of a company hitting its stride at precisely the right moment.

IES Holdings reported strong financial results for fiscal 2024. Fourth quarter revenue increased 20% to $776 million, with operating income up 41% to $75 million. For the full fiscal year 2024, revenue grew 21% to $2.9 billion, while operating income jumped 88% to $300.9 million. Net income attributable to IES reached $219.1 million, a 102% increase from 2023.

The acceleration continued into fiscal 2025. IES Holdings, Inc. reported strong financial results for the fourth quarter and fiscal year ending September 30, 2025, highlighting a revenue increase of 16% to $898 million in Q4 and a 17% rise to $3.37 billion over the fiscal year. Operating income in Q4 increased by 39% to $104.3 million, while net income surged 61% to $101.8 million. For the full year, net income attributable to IES rose by 40% to $306 million, resulting in a diluted earnings per share of $15.02.

The Communications Segment Leads the Way

Reflecting the increase in revenue, successful project execution, and improved margins on projects well-suited to our skilled workforce, the segment's operating income increased to $47.8 million for the third quarter of fiscal 2025, compared with $21.0 million for the third quarter of fiscal 2024.

The Communications segment wasn't just growing revenue—it was generating exceptional operating leverage. As volume increased, fixed costs were spread over a larger revenue base, and pricing power improved as data center operators scrambled for capacity.

The Communications segment saw a significant increase in revenue by 46.9%, driven by strong demand from data center customers and high-tech manufacturing.

Infrastructure Solutions Joins the Party

The Infrastructure Solutions segment also caught the data center wave. Our Infrastructure Solutions segment's revenue was $129.5 million in the third quarter of fiscal 2025, an increase of $27.5 million or 27% compared with the third quarter of fiscal 2024, driven by continued strong demand in our custom engineered solutions business, primarily in the data center end market, as well as expansion of our field services offerings. Operating income for the third quarter of fiscal 2025 was $32.6 million, compared with $19.8 million for the third quarter of fiscal 2024. The year-over-year profit improvement was driven primarily by a combination of higher volumes, improved pricing and operating efficiencies at our facilities.

The custom generator enclosures and bus duct solutions manufactured by the Infrastructure Solutions segment were essential components for data center power distribution—another example of IES being in the right place at the right time.

Strong Backlog Provides Visibility

Remaining performance obligations and backlog indicate strong future revenue potential, with approximately $1.69 billion and $2.37 billion, respectively.

A backlog approaching $2.4 billion provides significant visibility into future revenue streams. Data center projects are large, complex, and often span multiple quarters—giving IES a clearer line of sight to future performance than many project-based businesses enjoy.

Expanding Capacity to Meet Demand

During the third quarter of fiscal 2025, we continued our focus on growth, entering into an agreement to purchase an industrial fabrication operation in Manitowoc, Wisconsin to expand capacity for our custom engineered solutions business.

When demand exceeds capacity, successful companies invest to meet it. IES has been methodically expanding manufacturing footprint and workforce to capture the data center opportunity.

The Acquisition Machine: Strategic M&A (2021-2025)

Disciplined Deal-Making

The disciplined acquisition approach established after the bankruptcy has continued to guide IES's M&A strategy. Rather than empire-building for its own sake, the company focuses on strategic fit and return on capital.

Greiner Industries: Entering the Mid-Atlantic

IES Holdings, Inc. announced today that it has acquired Greiner Industries, Inc., a Mount Joy, PA-based structural steel fabrication and services company. The acquisition also includes the purchase of Greiner's facilities, which cover 450,000-square feet of manufacturing space on a 60-acre campus. Greiner, with 2023 revenue of approximately $58 million, will become part of IES's Infrastructure Solutions segment and continue to operate under the Greiner name.

Jeff Gendell, Chairman and Chief Executive Officer, said, "The acquisition of Greiner strategically expands our geographic footprint into the attractive Mid-Atlantic market, while adding several products and services. Greiner, founded by Frank Greiner in 1976, has a long track record of completing large-scale, complex projects and providing specialized industrial services that are highly complementary with our Infrastructure Solutions segment."

The Greiner deal exemplified the IES playbook: acquire a family-owned business with strong local relationships, keep management in place, and provide capital and strategic support for growth.

Arrow Engine Company

IES Holdings acquired Arrow Engine Company in January 2025, a Tulsa-based provider of engines, generator sets, compressors, and replacement parts for the natural gas production market.

The Arrow acquisition expanded IES's product portfolio into equipment serving the energy sector—diversifying beyond the data center focus while adding another stream of recurring revenue from parts and service.

Gulf Island Fabrication: A Major Step Forward

IES Holdings, Inc. and Gulf Island Fabrication, Inc. today announced that they have entered into a definitive agreement, providing for the acquisition of Gulf Island, a leading steel fabricator and service provider to the industrial, energy and government sectors, by IES. Under the terms of the agreement, IES will pay $12.00 in cash per Gulf Island share, or an aggregate equity value of approximately $192 million. The transaction has been approved by the boards of directors of both companies and is currently expected to close in the quarter ending March 31, 2026.

Strategically located Gulf Coast fabrication campus: Gulf Island's Houma, Louisiana facility, which consists of a 450,000-square foot fabrication and operations facility on 160 acres, offers a strategic complement to IES's footprint.

The planned acquisition of Gulf Island Fabrication looks more material: it pushes IES further into fabrication-intensive work tied to U.S. infrastructure, which could deepen its opportunity set but also raise integration and project risk.

The Gulf Island deal represents IES's largest acquisition in years and signals ambitions to expand deeper into fabrication-intensive infrastructure work. While this creates opportunity, investors should monitor integration execution and project risk carefully.

Leadership Succession & The Next Chapter (2025)

Matt Simmes Takes the Helm

IES Holdings, Inc. announced today that the Company completed its previously-announced executive succession plan, with Matt Simmes becoming the Company's President and Chief Executive Officer and Jeff Gendell transitioning from Chairman of the Board and Chief Executive Officer to Executive Chairman of the Board.

Simmes, who has been with IES for over 31 years and previously served as President and Chief Operating Officer, will retain his position as President and join the Board of Directors. Gendell, who has been with the company since 2016 and CEO since 2020, will transition to the role of Executive Chairman while continuing to guide the Board and work closely with Simmes.

A 31-Year IES Veteran

From January 2017 to December 2021, Mr. Simmes served as President of IES Communications. Mr. Simmes joined Federal Communications Group (FCG) as a field technician in 1993. FCG grew to become one of the nation's largest providers of structured cabling and low-voltage systems, where Mr. Simmes served in various positions, including Project Manager and Branch Manager. In 1999, IES acquired FCG; in 2005 Mr. Simmes assumed the role of Vice President of Operations and in 2017 became the President of IES Communications.

Simmes's journey from field technician to CEO encapsulates what IES values: deep operational expertise, long-term commitment, and a bottom-up understanding of the business.

Continuity with Fresh Energy

"I am grateful for the opportunity to lead IES into its next chapter," said Mr. Simmes. "Under Jeff's leadership, IES has established a strong record of growth, and I am committed to building on that legacy to deliver value for our shareholders, customers, and employees." Mr. Gendell added, "I am incredibly proud of all that Matt and I have accomplished together, and as Executive Chairman, I look forward to working with Matt and the senior leadership team as they drive the Company's continued success."

The Company has grown significantly over the last five years, and Matt's organizational leadership experience and deep knowledge of our businesses position him well for this role. With Matt leading the Company as CEO, I will continue to focus on the strategic issues that are critical to IES's long-term success, including organic growth, acquisitions and capital allocation.

The transition represents continuity rather than disruption. Gendell remains deeply involved as Executive Chairman, focusing on capital allocation and strategic direction, while Simmes handles day-to-day operations. For investors, this orderly succession reduces key-person risk while maintaining the strategic vision that has driven IES's success.

Business Deep Dive: The Four Segments

Communications (The Star Performer)

The Communications segment has emerged as IES's most dynamic growth engine. Communications segment revenue grew 41% to $273.1M in Q2 2025.

What makes this segment particularly attractive:

-

High-growth end market: Data centers represent one of the fastest-growing infrastructure categories globally, driven by AI, cloud computing, and digital transformation.

-

Technical complexity: Designing and installing communications infrastructure within mission-critical data centers requires specialized expertise that creates barriers to entry.

-

Recurring relationship model: Once IES establishes a relationship with a hyperscaler or co-location provider, subsequent projects flow naturally.

-

Pricing power: Capacity constraints across the industry have allowed well-positioned contractors to improve margins.

Infrastructure Solutions

Infrastructure Solutions revenue increased by 42.0%, supported by strong demand and expanded capacity in custom engineered solutions.

The Infrastructure Solutions segment manufactures custom-engineered products that power data centers and industrial facilities—generator enclosures, bus duct solutions, and specialized electrical equipment. This segment benefits from the same data center tailwinds as Communications but operates with a manufacturing rather than service model.

The acquisition of Greiner Industries in 2024 expanded this segment's geographic reach and added structural steel fabrication capabilities. The pending Gulf Island acquisition will further enhance manufacturing capacity.

Commercial & Industrial

Results for the third quarter of fiscal 2025 reflect increased activity in the education and healthcare end markets, expansion of one of our operations in the Midwest market, and continued solid demand and strong execution in the data center end market.

The Commercial & Industrial segment provides electrical and mechanical services to a diversified customer base including office buildings, manufacturing facilities, healthcare systems, and educational institutions. While not growing as rapidly as Communications, this segment provides stable cash flow and diversification.

Residential (The Cyclical Challenge)

Our Residential segment's revenue was $346.1 million in the third quarter of fiscal 2025, a decrease of $31.5 million or 8% compared with the third quarter of fiscal 2024, as a result of the continued softness in the housing market.

Despite overall revenue growth, the Residential segment reported a 6% decrease in revenue compared to the previous fiscal year, attributed to softer demand in the housing market and related affordability issues. Increased costs in the Residential segment, including price reductions passed from large home builders, negatively impacted operating income.

The Residential segment faces headwinds from high mortgage rates and housing affordability challenges. This cyclical pressure creates near-term drag but also positions the segment for recovery when housing markets normalize. IES has been diversifying within Residential by adding HVAC and plumbing services—reducing pure dependence on new housing starts.

Competitive Landscape

Industry Position

Major competitors include EMCOR Group (EME), Quanta Services (PWR), and MYR Group (MYRG). These companies compete for commercial, industrial, and infrastructure projects, with differentiation based on technical expertise, project management capabilities, safety records, and pricing.

IES operates in a competitive but fragmented market. Quanta Services & EMCOR Group: ~12% market share each, dominating the infrastructure sector, with market caps of $46 billion and $21 billion respectively. Both companies have delivered exceptional returns, multiplying an initial investment by orders of magnitude. MasTec: ~8% market share, with strengths in renewable energy. IESC: With ~2% market share, IESC has significant room for growth and opportunities to capture additional market share through strategic initiatives and acquisitions.

Market Fragmentation Creates Opportunity

The U.S. electrical contractors market is highly fragmented, with several vendors operating. Quanta Services, MYR Group, ArchKey Solutions, EMCOR Group, MasTec, and more have a sizeable local presence and major U.S. electrical contractors market vendors.

The fragmented nature of the market creates ongoing M&A opportunities for well-capitalized players like IES. Family-owned contractors reaching succession events often prefer to sell to a company like IES that maintains their brand and keeps management in place.

Relative Valuation

Despite its strong performance, IES trades at reasonable valuations relative to peers. EMCOR Group has a net margin of 7.51% compared to IES Holdings's net margin of 7.31%. IES Holdings's return on equity of 37.95% beat EMCOR Group's return on equity of 35.99%.

IES has delivered peer-leading returns on equity while maintaining a clean balance sheet—a combination that deserves investor attention.

Strategic Analysis: Competitive Moat Assessment

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

Significant barriers protect IES's market position: - Skilled labor represents a critical bottleneck; electricians require years of apprenticeship and certifications - Customer relationships in construction are built over decades - Bonding and insurance requirements favor established players with strong balance sheets - Scale advantages in procurement and project management - However, local markets remain accessible to entrepreneurial competitors

2. Bargaining Power of Suppliers: LOW

IES maintains favorable supplier dynamics: - Electrical components are largely commoditized - Multiple suppliers compete for business - IES's scale creates procurement advantages across segments - Supplier switching costs are low

3. Bargaining Power of Buyers: MEDIUM

Buyer dynamics vary by segment: - Large hyperscalers (data center operators) have significant negotiating leverage - However, specialized expertise and capacity constraints limit alternatives - Residential builders have moderate power but value reliability - Strong customer relationships create meaningful switching costs - Technical specifications often favor established contractors

4. Threat of Substitutes: LOW

Electrical infrastructure has no real substitutes: - Physical electrical systems are required regardless of technology changes - Data centers need power infrastructure no matter how efficient chips become - Trend toward electrification increases rather than decreases demand - No technology disruption on the horizon threatens the core business

5. Competitive Rivalry: MEDIUM-HIGH

Competition is intense but manageable: - Highly fragmented industry creates competition but also acquisition opportunities - Differentiation based on expertise, relationships, and track record - Price competition on commodity work; value selling on complex projects - Geographic and segment diversification reduces competitive pressure

Hamilton Helmer's Seven Powers Assessment

Process Power: IES demonstrates process power through its decentralized operating model that enables local market responsiveness while maintaining corporate-level capital allocation discipline. Years of post-bankruptcy refinement have created operational excellence that would be difficult for competitors to replicate quickly.

Scale Economies: Present but limited—the electrical contracting business doesn't exhibit the winner-take-all dynamics of software businesses, but IES benefits from procurement scale, bonding capacity, and overhead absorption across a larger revenue base.

Switching Costs: Meaningful in complex projects where contractor knowledge of customer facilities, processes, and requirements creates value that would be lost by switching.

Cornered Resource: IES's ~60% ownership by Tontine/Gendell creates alignment of interests unavailable to dispersedly-owned competitors. The company's remaining NOL assets (though now largely utilized) provided a tax advantage unavailable to profitable competitors.

Bull Case vs. Bear Case

The Bull Case

Secular Tailwinds: AI infrastructure spending represents a generational investment cycle. Hyperscalers have committed hundreds of billions to data center buildout, and IES is positioned to capture a meaningful share of the electrical infrastructure spend.

Operational Excellence: Under Gendell's leadership, IES has demonstrated disciplined capital allocation, conservative financial management (zero debt), and improved operational execution across segments.

Acquisition Runway: With a clean balance sheet and strong cash generation, IES can continue acquiring family-owned contractors at reasonable multiples, driving both organic and inorganic growth.

Management Alignment: 60% insider ownership creates alignment rarely seen in public markets. Management is invested alongside shareholders.

Margin Expansion: As data center projects scale, operating leverage should drive continued margin improvement in the Communications and Infrastructure Solutions segments.

The Bear Case

Cyclical Exposure: The residential segment remains exposed to housing cycles, and even the hot data center market could face a correction if hyperscaler spending slows.

Customer Concentration: Large data center projects can create customer concentration risk; project delays or cancellations could impact near-term results.

Integration Risk: The Gulf Island acquisition moves IES into heavier fabrication work with potentially different margin and risk profiles.

Valuation Expansion: Much of IES's stock appreciation reflects multiple expansion; further gains require continued execution rather than re-rating.

Labor Constraints: Skilled electrician shortages could constrain growth and pressure wages across the industry.

Key Person Risk: While partially mitigated by the succession plan, Gendell's continued involvement remains important to the investment thesis.

Key Performance Indicators for Investors

For investors tracking IES Holdings' ongoing performance, three KPIs stand out as most critical:

1. Communications Segment Growth Rate & Operating Margin

The Communications segment represents IES's primary growth engine and data center exposure. Tracking year-over-year revenue growth and operating margin trends provides the clearest signal of whether the AI infrastructure thesis remains intact. Watch for: revenue growth above 20% indicating continued strong demand; operating margins expanding as scale benefits materialize; any commentary on project delays or customer concentration.

2. Backlog/Remaining Performance Obligations

The company's backlog (non-GAAP) and remaining performance obligations (GAAP) provide forward visibility into revenue. A growing backlog suggests healthy demand and successful project bidding; a declining backlog could signal slowing demand or competitive pressure on pricing. The backlog-to-revenue ratio indicates how many quarters of revenue are already committed.

3. Return on Invested Capital (ROIC)

Given IES's acquisition-driven strategy, ROIC measures whether capital allocation is creating value. A rising ROIC indicates that acquisitions and organic investments are generating returns above the cost of capital; a declining ROIC would suggest deteriorating acquisition discipline or competitive pressure on margins.

The IES Holdings Playbook: Lessons for Investors

The IES Holdings story offers several lessons for long-term investors:

1. Roll-ups can work—but discipline matters: The first iteration of IES failed because growth became the goal rather than profitable growth. The post-bankruptcy IES succeeded by maintaining acquisition discipline, keeping target company management, and focusing on cash flow rather than revenue.

2. Distressed situations create hidden assets: The NOL carryforwards that emerged from bankruptcy represented hundreds of millions in tax savings—an asset invisible to most investors but tremendously valuable to a patient owner.

3. Alignment of interests matters: Gendell's majority ownership and transition to CEO created an alignment of interests that drove disciplined decision-making. When the person making capital allocation decisions has the most to gain or lose, incentives work.

4. Being in the right place at the right time isn't luck—it's preparation: IES didn't pivot to data centers in 2023; it had been building Communications segment capabilities for years. When AI demand exploded, IES was positioned to capture it.

5. Decentralized structures can outperform in people businesses: The holding company model—local operators empowered to serve customers with corporate support for capital and strategy—works particularly well in relationship-driven, project-based businesses.

From bankruptcy in 2006 to a $7 billion market cap in 2025, IES Holdings has delivered one of the most remarkable corporate transformations of the past two decades. For investors, the question now is whether the next chapter can match the last—and whether the data center boom has room to run.

The quiet compounder has spoken through its results. The market is finally listening.

Note: This analysis is for informational purposes only and should not be considered investment advice. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube