Primoris Services Corporation: Building America's Infrastructure

I. Introduction & Episode Roadmap

The stretch of highway between Dallas and Houston pulses with the electricity of a nation transforming itself. Beneath the asphalt run fiber optic cables. Above the trees stretch transmission lines carrying power from wind farms and solar arrays to data centers hungry for electrons. And somewhere along that corridor, crews wearing hard hats and high-visibility vests are doing the actual work of building America's future—one trench, one tower, one solar panel at a time.

Founded in 1960, Primoris, through various subsidiaries, has grown to become one of the largest publicly traded specialty construction and infrastructure companies in the United States. But this is not a story about a company content to rest on its legacy. It's a story about transformation—about how a small California pipeline contractor metamorphosed into a $6+ billion revenue infrastructure powerhouse now positioned at the intersection of the most powerful secular trends reshaping the American economy.

The central question that will guide our exploration: How did a regional pipeline specialist navigate six decades of energy booms and busts, execute over a dozen acquisitions, survive an unusual early SPAC merger, and emerge as a critical player in the energy transition?

With a $3.09B market cap as of April 2025, and a trailing 12-month revenue of $6.37B, Primoris occupies a peculiar position in the market consciousness. Despite its scale—larger than many household names—it remains relatively obscure to generalist investors. Only a handful of sell-side analysts cover the stock. It lacks the glamour of a software company or the headline appeal of a consumer brand. Yet its work touches nearly every American daily: the natural gas heating their homes, the electricity powering their devices, the fiber carrying their data.

The themes that define Primoris today are themes that define the American economy: the energy transition from fossil fuels to renewables, the insatiable demand for data centers driven by artificial intelligence, the aging infrastructure requiring massive reinvestment, and the strategic importance of Master Service Agreements (MSAs) that transform project-based revenue into something approaching recurring revenue. Understanding Primoris means understanding how physical infrastructure—the least digital of businesses—has become essential to the most digital of futures.

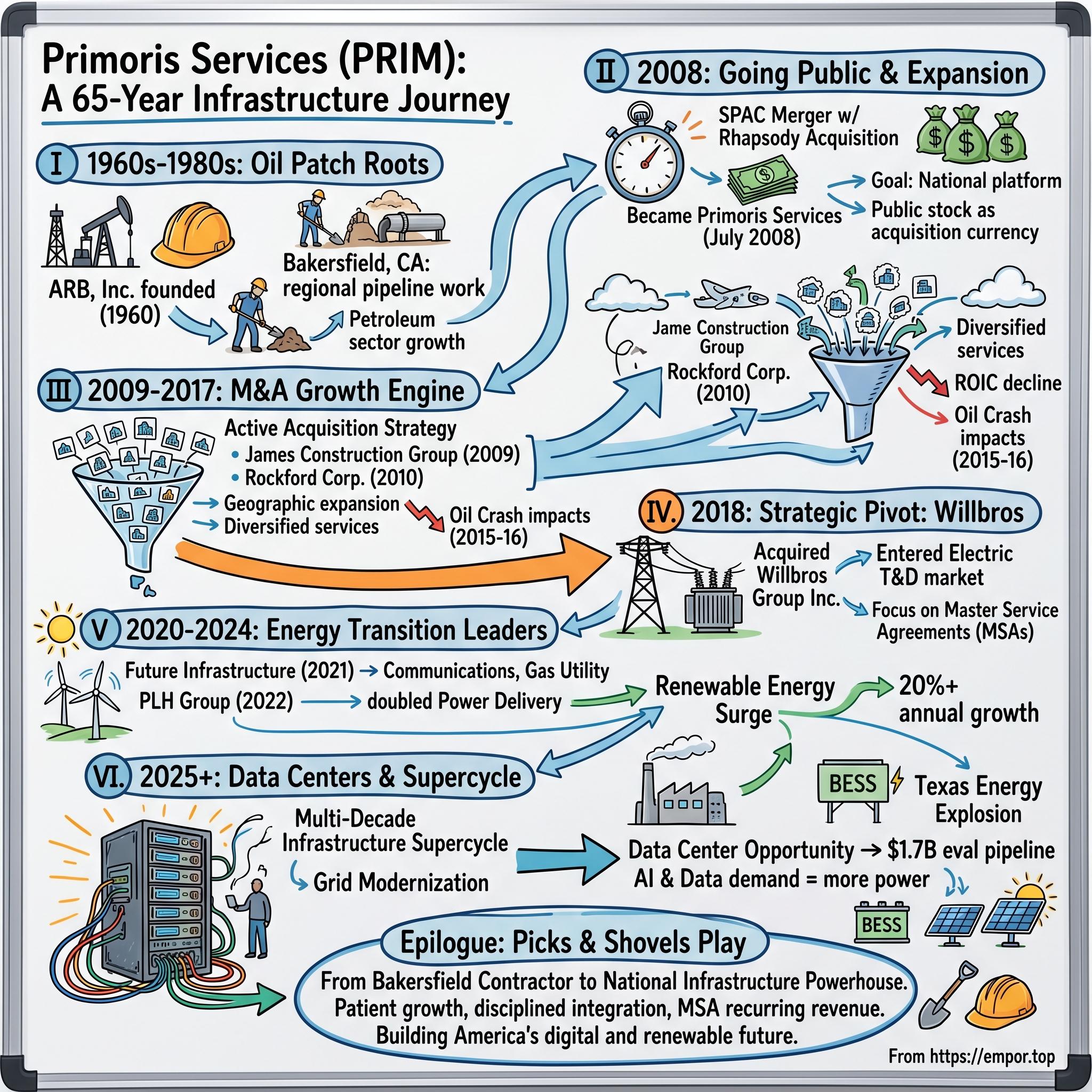

II. Origins: From Bakersfield to America's Pipelines (1960-2003)

In 1960, Bakersfield, California sat at the epicenter of American petroleum. The Kern County oil fields had been pumping crude since the 1890s, and by mid-century the region had developed its own culture—part Texas transplant, part California dreamer, with country music radio stations and roughnecks who could fix anything with diesel fuel and determination. It was here, in this gritty petroleum heartland, that the company that would become Primoris Services was born.

The company was founded as ARB, Inc. in Bakersfield, California in 1960, specializing in pipeline construction for the utilities and energy companies that dominated the region. The company emerged to address the expanding needs of the energy sector, initially focusing on constructing pipelines and related facilities for the oil and gas industry.

The business model was deceptively simple: California was growing, and growth required infrastructure. Natural gas pipelines needed to be laid. Water systems needed to be built. When cities expanded, someone had to dig the trenches and lay the pipe that made modern life possible. ARB positioned itself as that someone.

What made the early ARB distinctive was its focus on execution excellence in a fragmented industry. Pipeline construction is not glamorous work. It requires expertise in soil conditions, regulatory compliance, weather management, and the logistics of moving heavy equipment across terrain that doesn't want to cooperate. Small contractors could handle small jobs, but the growing scale of California's infrastructure needs favored contractors who could manage complexity.

The oil patch roots gave ARB something valuable: a workforce culture forged in an industry where mistakes could be catastrophic. Pipeline workers developed habits of safety and precision that would later prove essential when the company expanded into more complex work. The company grew steadily through California's boom decades, building relationships with utilities that would sustain it through downturns.

Since 1983, Brian Pratt served as the President, Chief Executive Officer and Chairman of the Board of Primoris and its predecessor, ARB, Inc. Prior to July 2008, Mr. Pratt was the majority owner of Primoris. Pratt represented the archetype of the owner-operator: a hands-on executive who knew the business from the trench level up, who could evaluate a project bid by feel as much as by spreadsheet, and who viewed the company as an extension of himself.

Pratt earned an undergraduate degree from California State Polytechnic University (Pomona) in 1974 and built his career in construction operations before taking the helm at ARB. His ownership stake aligned his interests perfectly with the company's performance—a governance structure that would become increasingly rare in corporate America but that gave ARB a certain focused clarity.

The company was organized as Primoris in Nevada in 2003, a reorganization that signaled ambitions beyond regional pipeline work. The name change was more than cosmetic. It represented a preparation for what would come next: transformation from a private regional contractor into a publicly traded national infrastructure platform.

For investors trying to understand Primoris's culture today, these origins matter. The company emerged from an industry where execution was everything, where relationships with utility customers could span decades, and where an owner-operator mentality prioritized long-term reputation over short-term financial engineering. This DNA would shape how Primoris approached its subsequent growth through acquisition.

III. Going Public: The SPAC Before SPACs Were Cool (2008)

In February 2008, as the first tremors of what would become the Global Financial Crisis rattled Wall Street, Primoris made a move that in retrospect looks either brilliantly prescient or audaciously risky: it decided to go public through a mechanism that wouldn't become widely known for another decade—the Special Purpose Acquisition Company.

In February 2008, Primoris Corporation (referred to as Former Primoris), a privately-held company, entered into an Agreement and Plan of Merger with Rhapsody Acquisition Corp. (Rhapsody), a publicly-held company. Rhapsody was founded as a special purpose acquisition company in 2006, and we became a public company in July 2008 when the merger was completed and Rhapsody changed its name to Primoris Services Corporation.

This was no ordinary transaction. In an era when SPACs were obscure vehicles used primarily by financial engineers seeking backdoor routes to public markets, Primoris saw an opportunity. The Merger was accounted for as a reverse acquisition. Under this method of accounting, Primoris was treated as the "acquired" company for financial reporting purposes. This determination was primarily based on the operations and management of Former Primoris comprising the ongoing operations and management of the Company after the Merger. In accordance with guidance applicable to these circumstances, the Merger was considered to be a capital transaction in substance.

The structure deserves examination because it reveals how Primoris thought about growth. Rather than pursuing a traditional IPO—with its roadshows, banker fees, and uncertainty about pricing—Primoris effectively took itself public through a reverse merger while preserving management control. Brian Pratt and his team knew the business far better than any investment banker could evaluate it in a typical IPO process.

On August 1, 2008, Rhapsody Acquisition Corp. announced that it has consummated its merger with privately held Primoris Corporation. Of Rhapsody's 6,300,000 shares outstanding, 4,889,503 (77.6%) were voted for the merger and 447,461 shares (7.1%) were voted against the merger and elected conversion rights.

The shareholder approval ratio—77.6% voting in favor—was strong for a SPAC deal. Those shareholders who voted against the merger and elected conversion rights received approximately $7.98 per share. The transaction mechanics included earnout provisions tied to EBITDA performance, creating alignment between the sellers and the public shareholders.

The Primoris stockholders received an aggregate of 24,094,800 shares of Rhapsody common stock at the closing of the merger plus the right to receive 2,500,000 shares of Rhapsody common stock for each of the fiscal years ending December 31, 2008 and 2009 during which Rhapsody achieved specified EBITDA milestones.

The timing—going public in July 2008, just months before Lehman Brothers collapsed—appears in retrospect either terribly unfortunate or strategically wise. On one hand, the company went public into a deteriorating market. On the other hand, it secured access to public capital markets before those markets effectively closed for most small companies. One of the company's primary reasons for going public was the desire to use its stock as acquisition currency—a strategic capability that would prove essential in the years ahead.

In 2008, it was incorporated as a public company in Delaware. The corporate restructuring gave Primoris the governance framework, financial reporting infrastructure, and stock currency it needed to execute its growth strategy. What had been a California pipeline contractor was now a publicly traded platform company.

IV. The Acquisition Engine Ignites (2008-2017)

With public stock as currency and access to credit markets, Primoris began executing a serial acquisition strategy that would fundamentally transform the company's scale and scope. The pace was aggressive, the ambition clear: become a national infrastructure platform by absorbing regional specialists.

From 2008-2014, the company completed a significant number of acquisitions that increased its invested capital from $48 million to $691 million—a compounded annual growth rate of 56%. This was not organic growth; this was transformation through aggregation.

On December 18, 2009, the company acquired James Construction Group, LLC, a privately-held Florida limited liability company. JCG is one of the largest general contractors based in the Gulf Coast states and is engaged in highway, industrial and environmental construction, primarily in Louisiana, Texas and Florida. The James acquisition pushed Primoris into new geographic markets and service lines—heavy civil work, highway construction—that complemented its core pipeline expertise.

In November 2010, Primoris purchased Rockford Corporation for $82.6 million, bolstering its expertise in pipeline construction and civil infrastructure projects, particularly in the western region.

The company acquired Sprint Pipeline Services, L.P. in 2012 and Q3 Contracting Inc., a gas pipeline service, in 2012 for $48.1 million in cash.

Since December 2009, Primoris has more than doubled its size and the Company's national footprint now extends from Florida, along the Gulf Coast, through California, into the Pacific Northwest and Canada.

The logic was compelling: infrastructure contracting is a fragmented industry where scale creates advantages. Larger contractors can bid on larger projects. They can spread overhead across a bigger revenue base. They can weather regional downturns by relying on work in other geographies. And they can negotiate better terms with equipment suppliers and insurers.

But rapid acquisition comes with risks, and Primoris experienced them fully. The integration challenge proved substantial, as the company struggled to absorb so many different cultures, systems, and operational approaches simultaneously. These acquisitions led to a significant decline in return on invested capital (ROIC), from 83% in 2008 to 11% in 2014.

That decline tells the story of acquisition indigestion. When ROIC falls dramatically during a period of aggressive growth, it usually means the acquirer is paying too much, integrating poorly, or both. Primoris was diluting its historically excellent returns by adding businesses that earned lower margins and required more capital.

Then came the oil crash. In 2015-2016, crude oil prices collapsed from over $100 per barrel to below $30. The shale revolution that had powered so much energy infrastructure investment suddenly reversed course. Pipeline projects were cancelled. Utility customers cut capital budgets. Primoris, with its oil patch heritage and significant exposure to energy infrastructure, felt the pain acutely.

The company's ROIC fell even further to 2% as the downturn exposed the cyclical risk embedded in its portfolio. What had been a growth engine became a survival challenge. Management had to shift focus from acquisition to integration, from expansion to optimization.

Invested capital increased by just 5-8% annually in 2015, 2016, and 2017. The pause in acquisition activity allowed Primoris to digest what it had swallowed, improve operational performance, and prepare for the next phase of growth.

V. Strategic Transformation: The Willbros Acquisition (2018)

If the early acquisitions built Primoris's geographic footprint, the 2018 acquisition of Willbros Group represented something different: a strategic pivot that would position the company for the energy transition.

In June 2018, Primoris Services Corporation completed its acquisition of Willbros Group, Inc. Willbros was a specialty energy infrastructure contractor that had struggled financially, making it available at an attractive price. Willbros had struggled financially in recent years. "The company began experiencing significant operating losses during the third quarter of 2017 on large lump-sum projects," Willbros President and CEO Michael Fournier explained at the time, referring to pipeline construction projects that faced substantial weather impacts through early 2018.

Under the terms of the all-cash agreement, Primoris paid $0.60 per share for all of the outstanding common stock of the Company, settled the existing debt obligations of the Company, and provided up to $20 million in bridge financing to support the Company's working capital liquidity needs through the closing date. The aggregate consideration was approximately $107.0 million, net of cash acquired.

The strategic rationale was clear: in 2018, Primoris got into the electrical transmission and distribution sector with its purchase of Willbros Group Inc. Upon completion of the transaction, Primoris expects the Willbros UTD business to become a new operating segment, Primoris UTD, which continues Primoris' strategic plan for growing its Master Service Agreement ("MSA") revenue base.

The Willbros Utility Transmission & Distribution (T&D) segment became a new segment for Primoris—a business with fundamentally different characteristics than pipeline construction. While pipelines are large, discrete projects with clear beginnings and endings, utility T&D work tends to be ongoing: maintenance, upgrades, storm restoration, line extensions. This work is often performed under multi-year MSAs that provide more predictable revenue streams.

"The T&D business provides Primoris with another avenue of growth, the Canadian operating centers expand our services into Western Canada, and the Oil & Gas Facilities business enhances offerings in our existing markets," said CEO David King.

The acquisition was expected to be accretive to revenues by approximately $660 million, add EBITDA of $25 million, total backlog of $400 million and around $7 million in annual cost savings in the first year. The UTD business had a strong backlog of primarily MSA revenue. While traditional transmission and distribution markets remained strong, there was also increased demand for renewables and overall strong increasing demand for electrical transmission and distribution.

Unlike previous acquisitions, this deal improved both ROIC and economic earnings. Primoris had learned from its earlier acquisition binge. Rather than simply buying revenue, it was buying strategic capabilities that enhanced its competitive position.

The timing proved fortuitous. The utility T&D market was on the cusp of a multi-decade investment cycle driven by grid modernization, renewable energy integration, and eventually the data center explosion. By entering this market in 2018, Primoris positioned itself to capture growth that many competitors would struggle to access.

The Willbros deal also demonstrated disciplined post-acquisition execution. Management paid down nearly a quarter of the debt associated with the acquisition by year-end and maintained focus on integration. Net income attributable to Primoris in fourth quarter 2018 was $32.4 million, a 44% increase over fourth quarter 2017.

VI. The Modern Era: Building the Energy Transition (2020-2024)

The COVID-19 pandemic disrupted countless industries, but infrastructure construction proved resilient—designated essential work continued even during lockdowns. More importantly, the pandemic accelerated trends that would benefit Primoris: remote work increased demand for data connectivity, government stimulus boosted infrastructure spending, and growing awareness of climate risk accelerated the energy transition.

Primoris responded with two transformative acquisitions that cemented its position as an energy transition infrastructure leader.

Future Infrastructure Holdings (2021)

In January 2021, Primoris Services Corporation closed its acquisition of Future Infrastructure Holdings, LLC in an all-cash transaction valued at $620 million.

Future Infrastructure is a leading provider of non-discretionary maintenance, repair, upgrade and installation services to the telecommunication, regulated gas utility and infrastructure end markets. For the last 12 months ended September 30, 2020, FIH generated total revenue of $342 million, total adjusted EBITDA of $66 million and adjusted EBITDA margin of 19 percent.

That 19% EBITDA margin stood out—significantly higher than Primoris's corporate average. The transaction directly aligns with Primoris' strategy to grow in large, higher growth, higher margin markets, and expands the Company's utility services capabilities.

Tom McCormick, President and Chief Executive Officer of Primoris, said, "This acquisition is fully aligned with our strategic and operational goals and represents a defining moment for Primoris. It moves us meaningfully into a market we have been targeting and does so in a way that establishes a new, robust platform while creating additional opportunities for our existing services."

The acquisition added communication infrastructure offerings and approximately 1,100 employees. The acquisition was funded using $120 million of cash on hand, a revolving advance of $100 million under existing credit facilities and proceeds from a new $400 million term loan.

PLH Group (2022)

In June 2022, Primoris announced that it had entered into a definitive merger agreement to acquire PLH Group, Inc. in an all-cash transaction valued at $470 million.

For the 12 months ended May 31, 2022, PLH generated total revenue of $733 million and total adjusted EBITDA of $54 million. Approximately 80 percent of PLH revenue is associated with Power Delivery and Gas Utility end markets.

"The addition of PLH is an important step in enhancing both the size and scale of our operations in the Power Delivery and Gas Utilities markets. This acquisition will help us capture substantial growth tailwinds as the U.S. transitions to greater dependence on both traditional and renewable energy sources," said Tom McCormick.

The PLH deal nearly doubled Primoris's Power Delivery business and increased the company's Utilities segment to over 50 percent of pro forma revenue. With a high proportion of PLH revenue based on master service agreements ("MSAs") and unit price contracts, the transaction also maintains Primoris' strategic emphasis on limiting contract risk.

The Renewable Energy Surge

When Primoris entered the ENR Top 600 Specialty Contractors list at No. 6 in 2020, its power segment accounted for just 1% of its $3 billion in revenue in 2019. On last year's Top 600 ranking, the firm reported power had grown to represent a quarter of its $4.4 billion in revenue in 2022.

In 2024, Primoris' Energy segment (including solar, battery storage, and gas projects) delivered 20.5% annual revenue growth, with renewables contributing $2.0 billion in annual revenue.

Primoris Renewable Energy is a leading power generation engineering, procurement, and construction (EPC) provider specializing in utility and commercial scale solar power, energy storage, solar repower, and operations and maintenance.

The company's ability to consistently generate double-digit gross margins on solar farm projects distinguished it from competitors who struggled with the execution complexity of utility-scale solar. For utility-scale solar, Primoris is usually looking at projects costing in the range of $80 million to $450 million. They generally target power generation projects valued between $200 million and $500 million. "We really want to stay in a niche because when you start getting into those big projects, you get into competition with the likes of Bechtel or Kiewit. We don't really want to be that big and take on that risk."

The financials speak for themselves: in 2024, Primoris reported $6.4 billion in revenue (up 11.4%), $180.9 million in net income (up 43.4%), and $508.3 million in net cash from operations—a 160% increase from 2023.

VII. The Business Model Deep Dive: Understanding Primoris Today

To understand Primoris's investment case, one must understand the mechanics of how specialty infrastructure contractors create value. The business looks deceptively simple from the outside: win contracts, deploy crews, complete projects, collect payment. But beneath this surface lies a complex interplay of risk management, labor economics, and customer relationships that determines which contractors thrive and which merely survive.

Two-Segment Structure

The company operates in two segments, Utilities and Energy. The Utilities segment offers installation and maintenance of new and existing natural gas and electric utility distribution and transmission systems, and communications systems. The Energy segment provides engineering, procurement, construction, and maintenance services for entities in the energy, renewable energy and energy storage, renewable fuels, and petroleum and petrochemical industries.

This two-segment structure reflects the fundamental duality of infrastructure markets: steady, predictable utility work that provides baseline cash flow, and larger energy projects that offer higher growth but more volatility.

The MSA Model: Recurring Revenue in Construction

The Master Service Agreement model represents Primoris's most significant strategic evolution. Traditional construction is project-based: you win a bid, complete the work, and then must win the next bid. This creates feast-or-famine dynamics and makes revenue difficult to predict.

MSAs change the equation. Under an MSA, a utility customer designates Primoris as an approved (or preferred or exclusive) contractor for specified types of work over a multi-year period. When the utility needs pipeline repair, line extension, or storm restoration, it calls Primoris rather than bidding the work competitively. The utility gets reliable service from a contractor who knows its systems and standards; Primoris gets recurring revenue with minimal bid costs.

On the MSA side, Primoris signed 120 MSAs in 2024 and another 15 in early 2025. On the gas utilities and electric utilities, it's pretty much all driven by MSA work.

A focus on multi-year master service agreements and an expanded presence in higher-margin, higher-growth markets such as utility-scale solar facility installations, renewable fuels, power delivery systems and communications infrastructure have increased the Company's potential for long-term growth.

Premier PV: Vertical Integration

Primoris launched Premier PV, an Arkansas-based subsidiary that manufactures electrical balance of systems (eBOS) equipment for utility-scale solar and battery energy storage projects.

Premier PV has reached over $55 million in backlog. Premier PV is a provider of electrical balance of systems (eBOS) solutions to the solar, battery energy storage systems, and operations and maintenance markets, with a focus on utility-scale applications. Its product offerings include combiner boxes, load break disconnects, splice boxes, wire harnesses, and jumpers and extenders.

This vertical integration serves dual purposes. First, it helps Primoris avoid supply chain disruptions that have plagued solar construction. Second, it captures margin that would otherwise flow to component suppliers. "Premier PV is not only a value-add for our Primoris clients, but is a standalone operation that can service a wide range of contractors, owners, and developers across the renewables landscape," said Stephen Jones, President of Primoris' Renewables business.

VIII. 2025 and Beyond: Data Centers, AI, and The Infrastructure Supercycle

The current moment represents what may be the most favorable demand environment in Primoris's history. Multiple secular trends are converging to drive unprecedented infrastructure investment.

Current Performance

For the second quarter of 2025, Primoris reported revenue of $1,890.7 million, up $327.0 million, or 20.9 percent, compared to the second quarter of 2024 driven by strong growth in the Energy segment.

Primoris achieved record quarterly revenue of $1.89 billion in Q2 2025, representing a 20.9% increase compared to the same period last year. More impressively, net income surged 70.2% year-over-year to $84.3 million, while diluted earnings per share rose 69.2% to $1.54.

Total Backlog reached just under $11.5 billion, an increase of approximately $100 million sequentially from Q1. EPS Guidance was increased to $4.40 to $4.60 per fully diluted share. Adjusted EPS Guidance was increased to $4.90 to $5.10 per fully diluted share.

The Data Center Opportunity

Primoris highlighted the evaluation process for about $1.7 billion of work related to data centers, which it expects to receive contracts for by the end of 2025. These projects include solutions across early-stage site preparation, power generation, utility infrastructure and fiber network construction.

The data center work is incremental to the base plan. The opportunities span transmission, substation, fiber, and generation.

The demand backdrop extends beyond data centers: utilities are embarking on extensive power delivery programs, while natural gas and solar generation projects—with a pipeline exceeding $2.5 billion—are adding further momentum.

The Texas Energy Explosion

Texas exemplifies the infrastructure supercycle. Peak demand could nearly double to 150 GW by 2030, ERCOT CEO Pablo Vegas told the Senate Committee on Business and Commerce. "It's a fairly significant step change from a demand perspective."

The grid operator is now tracking 205 gigawatts of large load interconnection requests. More than 70% of the 205 gigawatts of current large load interconnection requests are from data centers and another roughly 10% are from cryptocurrency mines.

The majority of new generation capacity is expected to come from the build-out of solar and battery storage systems (BESS), with solar expected to more than double between 2024 and 2029 and BESS projected to triple during the same period.

New Leadership

Primoris Services Corporation announced its Board of Directors has appointed Koti Vadlamudi President and Chief Executive Officer ("CEO") effective November 10, 2025. Mr. Vadlamudi will also be appointed to the Primoris Board on the effective date. He succeeds Interim President and CEO David King, who will continue to serve as Chairman of Primoris' Board of Directors.

Vadlamudi brings a 30-year career at Jacobs. Mr. Vadlamudi is recognized for his expertise in driving enterprise growth, acquisition integration, project delivery, client relationships, and operational leadership across complex, high-value programs.

The company's 2025 guidance of $203.3M to $214.3M in net income and $440M–$460M in Adjusted EBITDA is ambitious but achievable, given its backlog and execution track record.

IX. Playbook: Business & Strategic Lessons

Primoris's six-decade journey offers several lessons for investors evaluating infrastructure businesses.

The Acquisition Playbook

When searching for acquisitions, Primoris looks for targets that are contractors in core competencies where the company is expanding and that would bring something like new clients or territory. This discipline—acquire capabilities, not just revenue—distinguishes successful serial acquirers from those who destroy value through growth.

The company's acquisition history shows clear evolution: early deals focused on geographic expansion, later deals targeted strategic capabilities (T&D, communications, power delivery). The Willbros deal particularly demonstrated how buying a distressed asset at the right price can create value that transforms a company's trajectory.

Post-acquisition, Primoris emphasizes integration and deleveraging. The target for net leverage of 2.0x by 2024 (following PLH) reflected discipline that prevents acquisition-driven companies from becoming over-leveraged house of cards.

The MSA Strategy

The strategic shift toward MSA-based revenue represents a fundamental de-risking of the business model. Project-based construction creates binary outcomes: you either win the bid or you don't. MSA revenue flows more predictably, smoothing quarterly results and making long-term planning more feasible.

MSA backlog serves as a competitive moat. Once a utility has established Primoris as its approved contractor, switching costs are high. The utility's engineers know Primoris's capabilities. Primoris's crews know the utility's standards and systems. This institutional knowledge creates stickiness that pure price competition cannot easily disrupt.

Energy Transition Positioning

Primoris was early to utility-scale solar EPC and has maintained double-digit margins where competitors struggle. This positioning wasn't accidental—it reflected strategic recognition that the energy transition would require massive infrastructure investment and that contractors with solar expertise would be in short supply.

The company's flexibility to serve both renewable and traditional energy clients provides optionality. As natural gas generation expands (partially to back up intermittent renewables, partially to power data centers), Primoris can capture that work alongside its solar portfolio.

X. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

| Force | Assessment | Analysis |

|---|---|---|

| Threat of New Entrants | LOW-MEDIUM | High barriers exist: specialized equipment investments run to tens of millions, skilled labor takes years to develop, safety certifications require track records, and utility relationships span decades. However, regional contractors can enter local markets. |

| Bargaining Power of Suppliers | MEDIUM | Labor is the key input, and skilled construction workers have significant bargaining power in a tight market. Equipment suppliers have some power, but Primoris's scale and Premier PV vertical integration mitigate this. |

| Bargaining Power of Buyers | MEDIUM | Large utility customers have negotiating power, but MSA relationships create mutual dependency. Track record and safety ratings matter significantly—utilities won't switch contractors to save 5% if it means execution risk. |

| Threat of Substitutes | LOW | Physical infrastructure construction has no substitutes. You cannot digitize a pipeline or virtualize a transmission line. The energy transition creates more demand, not less. |

| Competitive Rivalry | MEDIUM-HIGH | North America is embarking on infrastructure expansion driven by grid modernization, renewable energy growth and data center expansion. Two prominent players are Primoris and Quanta Services, both deeply embedded in construction networks powering the continent's energy and utility systems. |

Hamilton's 7 Powers Analysis

| Power | Assessment | Analysis |

|---|---|---|

| Scale Economies | MODERATE | The company's industrial workforce is well-suited for infrastructure work, giving it flexibility to scale without major organizational shifts. Shared equipment, overhead spreading across larger revenue base. |

| Network Effects | WEAK | Limited network effects in construction services—each project stands alone. |

| Counter-Positioning | MODERATE | Early positioning in utility-scale solar EPC while legacy contractors hesitated; consistent double-digit gross margins on solar where many contractors struggle. |

| Switching Costs | STRONG | MSA relationships create significant customer stickiness; utility customers reluctant to switch proven contractors with safety records. |

| Branding | WEAK-MODERATE | B2B business limits brand power, but reputation with utilities matters significantly for long-term relationships. |

| Cornered Resource | MODERATE | Skilled labor force, specialized equipment fleet, and safety certifications are difficult to replicate quickly. |

| Process Power | MODERATE-STRONG | Demonstrated ability to consistently generate margins in solar EPC where competitors struggle; integration expertise from serial acquisitions. |

Key Competitive Advantage: The combination of MSA-based recurring revenue, utility-scale solar execution excellence, and serial acquisition integration capabilities creates a differentiated position in a fragmented industry.

Considering valuation, Primoris stock is currently trading at a discount compared with Quanta on a forward 12-month P/E ratio basis.

Although the mentioned market players often secure the largest projects, PRIM is competitive on specialized contracts and selective bidding, giving it an edge in profitability and execution in its chosen areas. Its ability to balance risk and remain agile helps it carve out a defensible position despite the scale advantage of EMCOR and Quanta Services.

XI. Bear Case vs. Bull Case

Bear Case

Acquisition Integration Risk: Concerns remain around Primoris's approach to mergers and acquisitions. Analysts stress that overextension or integration challenges could affect long-term profitability. As Primoris expands its footprint in emerging sectors, shifts in end market exposure could introduce new operational and execution risks.

Valuation Considerations: Current valuation multiples appear robust in the near term. This suggests that much of the company's anticipated growth may already be priced in. Shares of Primoris have rallied 66.5% in the past three months compared with the industry's growth of 27.1%. From a valuation standpoint, PRIM trades at a forward price-to-earnings ratio of 23.17, above the industry's average of 21.89.

Leadership Transition: Tom McCormick separated from the Company effective March 20, 2025. The Board conducted a search process to identify a permanent CEO, which included internal and external candidates. While Koti Vadlamudi has now been appointed, leadership transition introduces execution risk even as core business segments demonstrate solid momentum.

Policy Risk: Changes to renewable energy incentives (IRA modifications) could impact solar project economics.

Execution Risk: Large complex projects carry inherent execution risks—weather delays, labor shortages, supply chain disruptions.

Customer Concentration: Significant exposure to major utilities creates concentration risk.

Bull Case

Growth Momentum: Bullish sentiment highlights Primoris's robust growth in segments such as gas generation, renewable energy, and power delivery. These areas are seen as key drivers of margin expansion and improved valuation multiples.

Record Results: The second quarter revenue reached nearly $1.9 billion, marking a 20.9% increase from the previous year, driven by double-digit growth in both the Energy and Utilities segments. The Utilities segment gross profit surged by 52.3% to $97.5 million, with gross margins improving to 14.1% from 10.3% in the prior year.

Backlog Strength: A growing backlog continues to strengthen the company's long-term outlook. Total backlog stood at approximately $11.5 billion at the end of the second quarter of 2025. Growth was led by MSA backlog, which expanded more than $600 million, driven by higher power delivery activity within utilities.

Data Center Tailwind: The data center wave could become the company's next major growth engine. Regulatory complexity and infrastructure needs rising in tandem create an efficient lever for sustained earnings growth.

Multi-Decade Investment Cycle: Grid modernization, renewable buildout, data center expansion represent multi-decade investment cycles that provide secular demand tailwinds.

Valuation Relative to Peers: Primoris stock is currently trading at a discount compared with Quanta on a forward 12-month P/E ratio basis.

KPIs to Track

1. MSA Backlog Growth and Renewal Rates: The most important metric for assessing the durability of Primoris's business model. Growing MSA backlog indicates deepening customer relationships and recurring revenue. Renewal rates above 90% would indicate strong competitive positioning.

2. Energy Segment Gross Margins: Management targets 10-12% gross margins for the Energy segment. Consistent achievement or expansion of this range indicates pricing power and execution excellence. Utilities gross margin improved to 14.1% (vs. 10.3% prior year) through optimized project mix and productivity gains.

3. Net Debt/EBITDA Ratio: With a target of 2.0x, this metric indicates financial flexibility for future acquisitions while maintaining balance sheet strength. Net debt-to-EBITDA has fallen to 0.5x.

XII. Epilogue: The Infrastructure Hidden Champion

Shares of Primoris have rallied 66.5% in the past three months compared with the industry's growth of 27.1%. The market is beginning to recognize what long-term observers have understood: Primoris sits at the intersection of America's most important infrastructure trends.

The broader thesis is straightforward but powerful: America's infrastructure is aging, the energy transition requires massive investment, and data centers need unprecedented power. Every trend driving capital expenditure in the American economy—grid modernization, renewable energy deployment, AI infrastructure, reshoring of manufacturing—requires the physical construction work that Primoris provides.

In the parlance of gold rush investing, Primoris represents the "picks and shovels" play on multiple secular trends. Rather than betting on which renewable developer will succeed or which AI model will dominate, investors in Primoris bet on the certain fact that whoever wins will need infrastructure built.

The company's journey from Bakersfield pipeline contractor to national infrastructure platform illustrates a path rarely celebrated in American business: patient building, disciplined acquisition, and consistent execution in industries that lack the excitement of technology or consumer brands. Brian Pratt's owner-operator mentality evolved into institutional capabilities that can survive leadership transitions. MSA relationships built over decades provide competitive advantages that new entrants cannot quickly replicate.

Whether the energy transition accelerates or decelerates, whether data center growth meets projections or disappoints, whether Texas adds 50 gigawatts or 150 gigawatts—Primoris will be building something. And in a world fixated on the virtual, there remains profound value in companies that do the physical work of connecting American life.

The hard hats will keep appearing at job sites across the country. The trenches will keep getting dug. The lines will keep getting strung. And somewhere in Dallas, executives will keep allocating capital to capture the next wave of infrastructure demand, continuing a story that began in California's oil fields over six decades ago.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube