CreditAccess Grameen: India's Microfinance Giant and the Quest for Financial Inclusion

I. Cold Open & Stage Setting

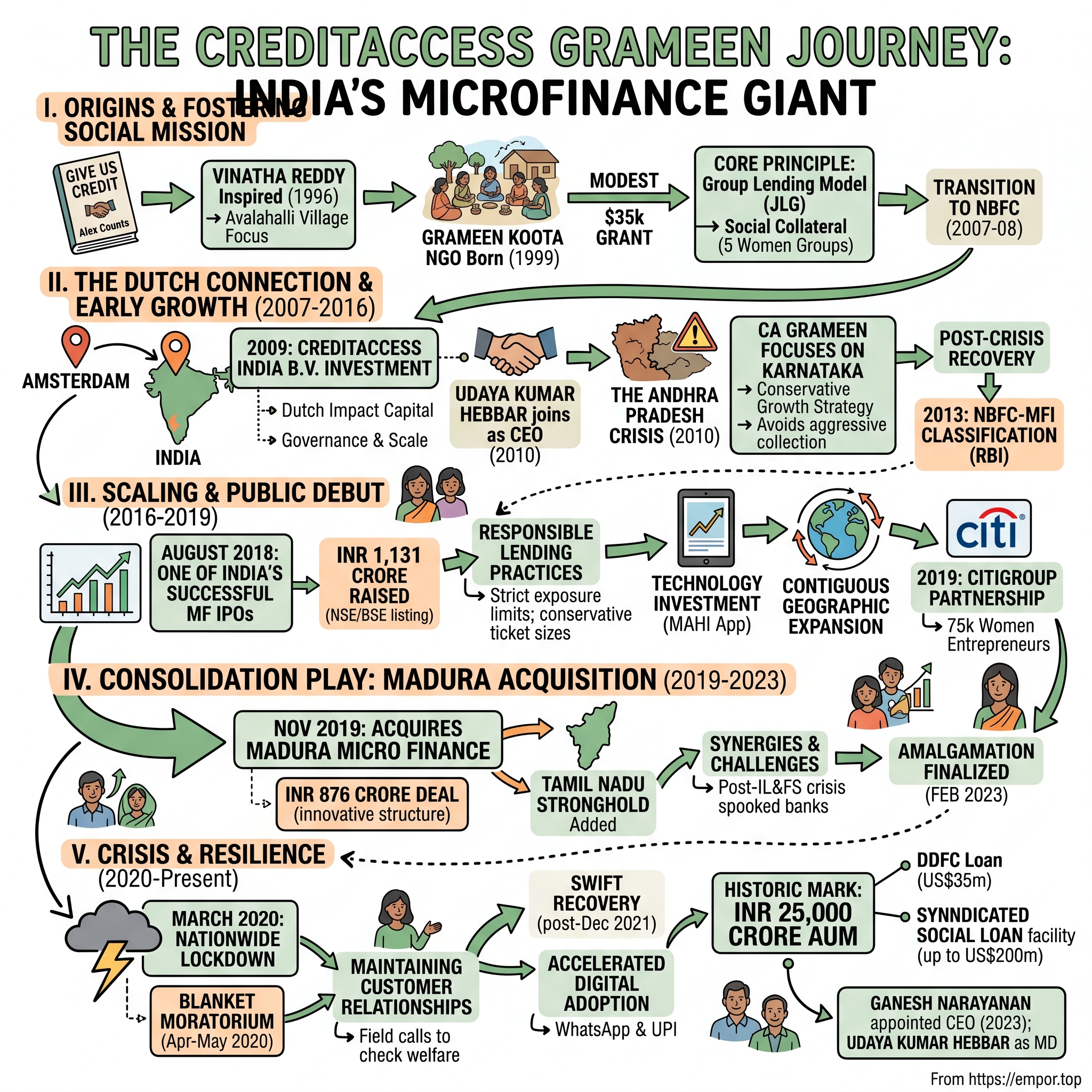

The trading floor at the National Stock Exchange erupted in applause on August 23, 2018. CreditAccess Grameen Limited, a company that started with a $35,000 grant and a dog-eared copy of a book about Bangladesh's rural poor, had just raised ₹1,131 crore in one of India's most successful microfinance IPOs. The stock opened at ₹538, a 17% premium to its issue price—a remarkable vote of confidence for a company operating in India's most challenging financial frontier.

Picture this: In the villages of Karnataka, Tamil Nadu, and Maharashtra, millions of women gather weekly in small groups, sitting cross-legged on concrete floors or under banyan trees, carefully counting out small bills. These are the customers of CreditAccess Grameen—women who've never seen the inside of a bank, whose financial dreams were once limited to the village moneylender's usurious rates. Today, with a 6% market share of India's microfinance sector, CreditAccess Grameen serves over 4.6 million such borrowers through 2,063 branches across 423 districts.

The central question isn't just how a small NGO inspired by Muhammad Yunus's Grameen Bank became India's largest NBFC-MFI. It's how they cracked the code that eluded centuries of formal banking: making tiny loans to the poorest profitable, scalable, and transformative. It's a story of Dutch capital meeting Indian opportunity, of social mission colliding with commercial reality, and of building trust where none existed before.

What follows is the definitive account of CreditAccess Grameen's journey—from its idealistic origins through crisis and transformation, to its current position as a ₹20,797 crore market cap giant generating ₹5,703 crore in annual revenue. We'll explore the decisions, the near-death experiences, the strategic pivots, and the relentless focus on India's financial inclusion that shaped this remarkable institution.

II. The Genesis Story: From Book to Bank (1996-2007)

In December 1996, in a modest office in Bangalore, Vinatha M. Reddy sat reading a worn copy of "Give Us Credit" by Alex Counts. The book chronicled Muhammad Yunus's revolutionary work with Bangladesh's rural poor—how tiny loans without collateral could lift entire villages out of poverty. Vinatha, inspired by the book, visualized what would become CreditAccess Grameen. For someone who'd been running the T. Muniswamappa Trust and witnessing rural poverty firsthand in her native Avalahalli village, this wasn't just academic interest—it was a calling.

Vinatha had spent considerable time in Avalahalli at her grandmother's house, surrounded by agricultural laborers, quarry workers, and daily wage earners. The memory of their poverty and especially the condition of children from these underprivileged homes stayed with her. She had already started a rural Montessori school called "Gurukul" in Avalahalli from a trust set up by her grandmother, but she knew education alone wasn't enough. The poor needed capital, not charity. Reddy managed to obtain a US$35,000 grant from the Grameen Foundation to create a replica in India, and with this modest seed capital, Grameen Koota was born in 1999. The name itself—"Koota" meaning gathering in Kannada—reflected the core principle of bringing people together for collective empowerment.

The Grameen Bank model that Vinatha sought to replicate was revolutionary in its simplicity. Muhammad Yunus had launched it in 1976 as a research project to study how to design a credit delivery system to provide banking services to the rural poor. The bank was founded on the principle that loans are better than charity for reducing poverty, offering credit to traditionally underserved groups including the poor, women, illiterate, and unemployed people through a group lending system with weekly-instalment payments.

The genius of the model lay in its Joint Liability Group (JLG) mechanism—social collateral replacing financial collateral. Five women would form a group, mutually guaranteeing each other's loans. If one defaulted, the others couldn't access further credit. This peer pressure mechanism, combined with small loan amounts and frequent repayments, created recovery rates of 95.58%—unheard of in traditional banking to the poor.

But adapting the Bangladeshi model to Indian conditions required significant modifications. India's social structures, regulatory environment, and economic realities differed markedly from Bangladesh. Vinatha and her early team, including co-founder Suresh Krishna, spent months studying villages around Avalahalli, understanding local dynamics, caste equations, and economic patterns. They realized that while the core JLG principle could work, the operational model needed to be distinctly Indian.

Vinatha Reddy and Suresh Krishna nurtured the institution as an NGO and transitioned it to an NBFC in 2007-08. This transition was crucial—as an NGO, Grameen Koota faced severe limitations in raising capital and scaling operations. The regulatory framework for NBFCs, while more stringent, offered a path to sustainable growth and access to commercial funding.

The company was renamed Grameen Financial Services Private Limited in October 2007, marking not just a name change but a fundamental shift in ambition. What started as a social experiment inspired by a book was now positioning itself to become a serious financial institution. The early days had proven the concept—poor women would repay loans, the JLG model worked in Indian villages, and there was massive unmet demand for credit. Now came the challenge of scale.

III. The CreditAccess Era: Dutch Capital Meets Indian Opportunity (2007-2016)

In 2009, CreditAccess India B.V., a Dutch microfinance investment vehicle backed by over 250 shareholders, made its biggest investment from Amsterdam's Herengracht district—funding an Indian NBFC that had just transformed from an NGO. The Dutch-based Asia-focused microfinance major has invested INR 968 crore in CA Grameen since 2009.

The Dutch connection wasn't accidental. The Netherlands had emerged as a global hub for impact investing, with institutions like Triodos Bank and FMO pioneering socially responsible finance. CreditAccess India B.V., founded by Italian entrepreneur Paolo Brichetti, represented this ethos—combining European capital with Asian opportunity. Brichetti, who had previously co-founded MicroFinanza Rating, understood that Indian microfinance needed more than capital; it needed governance, systems, and scale.

Udaya Kumar Hebbar joined as CEO in 2010, and has acquired a larger role as MD and CEO since 2016. Hebbar's appointment marked a turning point. A veteran banker with deep understanding of rural credit markets, he brought operational rigor that would prove crucial during the turbulent years ahead. His first task: navigating the worst crisis in Indian microfinance history. The year 2010 would test every principle CreditAccess Grameen stood for. More than 200 poor, debt-ridden residents of Andhra Pradesh killed themselves in late 2010, according to media reports compiled by the government of the south Indian state. The state blamed microfinance companies for fueling a frenzy of overindebtedness and then pressuring borrowers so relentlessly that some took their own lives.

SKS Microfinance, which became the largest microfinance institution in the country and had been central to the Andhra Crisis, became the first Indian microfinance entity to go public with its initial public offering (IPO) in 2010. The IPO, which raised around $350 million, became a lightning rod for criticism—how could an institution claiming to serve the poor make millions for its investors?

On October 15, the government of Andhra Pradesh issued an ordinance aimed at protecting women who "are being exploited by private microfinance institutions through usurious interest rates and coercive means." The ordinance effectively brought microfinance operations to a grinding halt in the state, triggering a nationwide liquidity crisis.

For CreditAccess Grameen, operating primarily in Karnataka but with growing presence in neighboring states, the crisis was both a threat and an opportunity. While competitors collapsed—recovery rates plummeted from over 95% to below 10% in Andhra Pradesh—CreditAccess's focus on Karnataka and more conservative growth strategy proved prescient. Hebbar's steady hand during this period was crucial. Rather than panic or overreact, the company doubled down on its core principles: maintain strong relationships with borrowers, ensure transparent practices, and avoid the aggressive collection tactics that had brought the industry into disrepute.

The crisis led to comprehensive regulatory reform. The Reserve Bank of India created a new category—NBFC-MFI (Non-Banking Financial Company - Microfinance Institution)—with specific regulations on interest rates, loan sizes, and collection practices. CreditAccess Grameen was among the first to receive this classification in 2013, legitimizing its operations and providing a clear regulatory framework for growth.

The Dutch investors' patience during this tumultuous period proved critical. While other foreign investors fled, CreditAccess India B.V. not only maintained but increased its commitment. More than 250 shareholders in the holding company have been supporting with more than adequate growth equity for the past 15 years in the form of patient capital. This wasn't just financial support—it was a vote of confidence in the fundamental model and management team.

By 2014, as the industry recovered, CreditAccess Grameen had emerged stronger. The customer base and portfolio had grown from 83,000 borrowers and INR 46 crore at the end of FY 2007 to 5.2 lakh borrowers and INR 810 crore. The company had successfully navigated the worst crisis in Indian microfinance history, proving its resilience and setting the stage for its next phase of growth.

IV. Going Public: The IPO and Growth Story (2016-2019)

The Mumbai trading floor buzzed with anticipation on August 8, 2018. Investment bankers from Kotak Mahindra, ICICI Securities, and IIFL Holdings crowded around terminals as CreditAccess Grameen's IPO opened for subscription. Within three days, the issue was oversubscribed 1.04 times, with qualified institutional buyers showing particular enthusiasm at 1.21 times subscription. The pricing—₹418-422 per share—valued the company at approximately ₹6,600 crore, making it one of the largest microfinance IPOs in Indian history.

But the road to this moment had been anything but smooth. Preparing for public markets meant transforming every aspect of the organization. Governance structures that had served a closely-held company needed complete overhaul. The board was reconstituted with independent directors bringing deep expertise in banking, risk management, and regulatory compliance. Financial reporting systems were upgraded to meet the stringent requirements of quarterly disclosures. Most importantly, the company had to articulate its story to a market still scarred by the 2010 crisis—how was CreditAccess Grameen different from SKS?

The answer lay in what the company called "responsible lending." Unlike the aggressive growth-at-any-cost model that had precipitated the AP crisis, CreditAccess Grameen emphasized sustainable expansion. Average ticket sizes remained conservative—around ₹25,000 per loan. The company maintained strict exposure limits, ensuring no borrower could take loans from more than two NBFC-MFIs. Field officers were incentivized not just on disbursements but on portfolio quality, aligning their interests with long-term sustainability rather than short-term growth.

In August 2018, the company was listed on National Stock Exchange and Bombay Stock Exchange with INR 1,131 crore-IPO. The proceeds weren't just for expansion—they were strategic. A significant portion went toward technology infrastructure, recognizing that the future of microfinance would be digital. The company launched its MAHI app, enabling field officers to process loans, collect repayments, and manage customer relationships through tablets, dramatically improving efficiency and data accuracy.

Geographic expansion followed a contiguous district strategy—rather than jumping to far-flung states chasing growth, the company expanded into neighboring districts where it could leverage existing infrastructure and knowledge. By 2019, operations had expanded from Karnataka into Tamil Nadu, Maharashtra, Madhya Pradesh, and Chhattisgarh, always maintaining the discipline of understanding local dynamics before scaling.

In September 2019, Citigroup partnered with CA Grameen to finance 75,000 Women Entrepreneurs in India. This wasn't just another funding arrangement—it represented validation from one of the world's largest banks that CreditAccess Grameen's model was both sustainable and scalable. The partnership focused specifically on women entrepreneurs, recognizing that female borrowers had consistently shown better repayment rates and more prudent use of capital.

Product diversification became a key strategy post-IPO. While income generation loans remained the core product, the company introduced home improvement loans, emergency loans, and individual loans under the "Unnati" brand for graduated borrowers who had successfully completed multiple group loan cycles. This lifecycle approach recognized that customers' needs evolved, and the company needed to evolve with them.

The competitive landscape during this period was intense but rational. Bandhan Bank and Ujjivan Small Finance Bank, former MFIs that had converted to banks, competed for the same customer base but with the advantage of being able to offer savings products. New-age fintechs promised instant loans through mobile apps. Yet CreditAccess Grameen's physical presence—loan officers who knew their customers personally, weekly center meetings that provided social support beyond just financial transactions—proved surprisingly resilient.

Market reception told the story. From the IPO price of ₹422, the stock climbed steadily, reaching ₹900 by early 2019. Institutional investors, particularly foreign portfolio investors, accumulated significant positions, attracted by the company's consistent execution and the massive underpenetrated market opportunity. With credit penetration in rural India still below 10%, the growth runway seemed infinite.

But Udaya Kumar Hebbar and his team knew that going public meant playing a different game. Quarterly earnings calls, analyst meetings, and constant scrutiny required a new level of transparency and communication. The company established a dedicated investor relations function, regularly engaging with the investment community to explain the nuances of microfinance—why NPAs might spike during harvest season, how demonetization impacted collections, why geographic concentration was actually a strength rather than a weakness.

By 2019, CreditAccess Grameen had firmly established itself as the largest NBFC-MFI in India. But management's ambitions went beyond organic growth. The fragmented microfinance sector, still recovering from the 2010 crisis, was ripe for consolidation. Several smaller MFIs struggled with capital adequacy and operational efficiency. It was in this context that an opportunity emerged that would transform CreditAccess Grameen's trajectory—the acquisition of Madura Micro Finance.

V. The Madura Acquisition: Consolidation Play (2019-2023)

The Chennai boardroom was tense in August 2018. Tara Thiagarajan, founder and chairperson of Madura Micro Finance, faced a difficult decision. Federal Bank, after months of advanced negotiations to acquire Madura, had suddenly gone cold. The IL&FS crisis that erupted in September 2018 had spooked banks across India. Federal Bank, with an exposure of ₹210 crore to IL&FS and still recovering from Kerala's devastating floods that affected 47% of its branches, had lost its appetite for NBFC acquisitions.

Madura, the 11th largest NBFC-MFI in the country with gross loan portfolio of Rs 2,053 crore, 11.1 lakh borrowers and 430 branches as on September 30, 2019, needed a strategic partner. The company had built a strong presence in Tamil Nadu but faced capital constraints for further growth. More importantly, the microfinance sector was consolidating rapidly—scale was becoming crucial for survival.

Enter CreditAccess Grameen. Udaya Kumar Hebbar and his team saw in Madura not just a portfolio acquisition but a strategic complement. While CreditAccess was strong in Karnataka and expanding northward, Madura dominated Tamil Nadu—a state where CreditAccess had limited presence. The customer profiles were similar, the operational models compatible, and most importantly, both companies shared a commitment to responsible lending.

CreditAccess Grameen acquired Madura Micro Finance at the deal of INR 876 crore in November 2019. The structure was innovative—a two-step process where CAGL would first acquire up to 76.2% stake for Rs 666.4 crore in cash from existing shareholders including Tara Thiagarajan, A.V. Thomas and Co. Ltd., and Elevar Equity Mauritius. In the second stage, MMFL would be merged into CAGL through a scheme of arrangement, with residual shareholders receiving CAGL shares at a swap ratio of 158 CAGL shares for every 100 MMFL shares.

The valuation—₹1,208 per share—reflected Madura's quality. Despite being smaller than CreditAccess, Madura had built robust technology platforms and pioneered the use of analytics in microfinance. Their field staff, mostly former borrowers themselves, had deep community connections. Tara Thiagarajan would continue as an advisor to the board, ensuring continuity and knowledge transfer.

Integration, however, proved more complex than anticipated. Two different core banking systems, distinct organizational cultures, and overlapping geographies in border districts required careful management. The companies operated as separate entities initially, with integration proceeding methodically. Branch staff needed retraining, loan products required harmonization, and perhaps most delicately, the Madura brand—well-established in Tamil Nadu—needed to be gradually transitioned to Grameen Koota.

Then COVID-19 struck. Just as the acquisition was closing in March 2020, India went into lockdown. Collection activities ceased overnight. Borrowers, mostly daily wage earners, lost their livelihoods. The RBI announced a moratorium on loan repayments. For a company that had just leveraged itself for a major acquisition, the timing couldn't have been worse.

Yet the crisis also accelerated integration. With physical operations suspended, both teams focused on building unified digital infrastructure. The combined entity's larger balance sheet provided a buffer that neither company alone might have had. CA Grameen also invested INR 150 crore through subordinated debt in Madura Micro Finance in December 2021, providing additional capital support during the recovery phase.

The National Company Law Tribunal (NCLT) finally approved the amalgamation in February 2023. By then, the benefits were clear. The combined entity had a loan portfolio approaching ₹15,000 crore, serving over 37 lakh borrowers through 1,300+ branches across 13 states and one union territory. Geographic diversification reduced concentration risk. Madura's technology capabilities enhanced CreditAccess's digital transformation. Most importantly, the acquisition had proven EPS accretive from inception, validating the strategic rationale.

The Madura acquisition marked CreditAccess Grameen's evolution from a regional player to a true national champion. It demonstrated the company's ability to execute complex M&A, integrate operations during a crisis, and emerge stronger. For an industry still fragmented with over 80 NBFC-MFIs, it set a template for consolidation that others would follow.

VI. Business Model Deep Dive: Serving the Underserved

Picture a Tuesday morning in Tumkur district, Karnataka. Under a peepal tree, 20 women sit in a circle, each clutching a small passbook. They're members of a Joint Liability Group, meeting for their weekly center meeting. The loan officer, tablet in hand, calls out names. "Lakshmi—₹200." She counts out two hundred-rupee notes, hands them over. "Pushpa—₹200." The process continues, methodical and transparent. In 45 minutes, the meeting concludes, loans are collected, new loan applications discussed, and the women disperse to their daily work—running petty shops, rolling beedis, tending livestock.

This scene, replicated across 2,063 branches serving 4.6 million borrowers, represents the core of CreditAccess Grameen's business model. But beneath this simplicity lies sophisticated financial engineering, behavioral psychology, and operational excellence that makes lending to the poorest not just possible but profitable.

The product portfolio starts with income generation loans—the bread and butter constituting 85% of the portfolio. These loans, averaging ₹25,000-₹30,000, finance micro-enterprises: a woman buying inventory for her vegetable stall, another purchasing a sewing machine, a third investing in a cow. The genius lies not in the product but the structure. Loans are disbursed to individuals but guaranteed by the group. Weekly repayments of ₹200-₹500 align with cash flows of daily wage earners. No collateral is required—social pressure replaces physical security.

The Joint Liability Group mechanism deserves deeper examination. Five women, typically from the same neighborhood but not relatives, form a group. They undergo a five-day training program covering not just loan terms but basic financial literacy—how to calculate interest, maintain accounts, plan cash flows. The training serves a dual purpose: education and assessment. Loan officers observe group dynamics, identifying natural leaders and potential defaulters.

When one member struggles with repayment, others don't immediately pay on her behalf. Instead, they provide bridge financing—small interest-free loans from their savings. They visit her home, understand her problems, sometimes even help with her business. This peer support mechanism, invisible in financial statements, drives recovery rates above 95%—better than many secured retail loans.

Product evolution reflects customer lifecycle needs. After successfully completing 2-3 loan cycles, borrowers graduate to larger individual loans under the "Unnati" brand. Home improvement loans help upgrade from thatch to tin roofs. Emergency loans provide liquidity during medical crises. Two-wheeler loans enable better mobility for business. Each product is designed with specific use cases, repayment patterns, and risk profiles.

The 2,063 branches follow a hub-and-spoke model. A branch typically serves 2,000-2,500 borrowers within a 20-kilometer radius. Location selection is crucial—accessible to villages but situated in semi-urban areas with basic infrastructure. Each branch has 6-8 loan officers, each managing 400-500 borrowers organized into 20-25 centers. This density enables weekly collection while keeping travel costs manageable.

Technology adoption has been transformative. The MAHI app, deployed on tablets, enables loan officers to process applications, record collections, and access customer history in real-time. Biometric authentication prevents fraud. GPS tracking ensures field visits happen. But technology complements rather than replaces human interaction. The weekly center meeting remains sacred—it's where trust is built, problems identified early, and the social fabric that underpins the model is maintained.

Unit economics reveal the model's elegance. Interest rates, at 22-26% annually, seem high but are competitive with alternatives—moneylenders charging 60-120% or gold loans at similar rates but requiring collateral. Operating expenses, at 11-12% of assets under management, are higher than banks but necessary given the high-touch model. Credit costs of 1-2% reflect strong underwriting and collection. This leaves a healthy net interest margin of 12-13%, generating ROE of 20%+ even with conservative leverage of 5-6x.

Risk management happens at multiple levels. At origination, credit bureau checks prevent over-leveraging—no loans to customers already borrowing from two MFIs. During disbursement, loans go directly to bank accounts, eliminating cash handling risks. In collections, the weekly frequency means problems surface quickly—missing one payment triggers immediate follow-up. The group mechanism provides first-loss protection. Geographic and sector diversification prevent concentration risks.

The social impact, while hard to quantify, is profound. Independent studies show borrowers' household incomes increasing 20-30% within two years. Children's education levels improve—loan officers track school enrollment as a lead indicator of household stability. Women's agency within households strengthens as they control capital. Villages with MFI presence show higher levels of formal financial inclusion—bank accounts, insurance penetration, digital payments adoption.

But challenges persist. Competition has intensified—customers now have multiple options, reducing loyalty. Digital lenders promise instant loans without meetings, appealing to younger borrowers. Rising operating costs—fuel, wages, compliance—pressure margins. Most fundamentally, the model's dependence on physical meetings and cash collections seems anachronistic in an increasingly digital India.

CreditAccess Grameen's response has been measured evolution rather than revolution. Digital collections through UPI are encouraged but not mandated. The MAHI app streamlines operations but doesn't eliminate human interaction. New products like micro-business loans and education loans expand the addressable market. The core insight remains: for millions of India's poor, credit is not just about money—it's about dignity, community, and hope. Any business model that forgets this human dimension, no matter how technologically sophisticated, will fail.

VII. Modern Era: Scale, Innovation, and New Frontiers (2020-Present)

March 24, 2020: Prime Minister Modi announced a complete nationwide lockdown in India. For CreditAccess Grameen's 40 lakh borrowers and 10,000+ employees, life changed instantly. Weekly center meetings—the cornerstone of the microfinance model—became impossible overnight. Collections ceased. Field officers couldn't visit villages. The carefully constructed edifice of group lending seemed to crumble in hours.

Creditaccess Grameen Ltd's Management decided to give a blanket moratorium to all its borrowers for the month of April & May 2020. This wasn't just operational necessity—it was recognition that their borrowers, mostly daily wage earners, had lost their livelihoods overnight. Because of this blanket moratorium an amount of ₹466.2 Cr of interest is accrued during the moratorium period.

The financial impact was severe. In Q1 FY2022, the company posted a 73% fall in net profit, reflecting the accumulated stress of the moratorium period. But what distinguished CreditAccess Grameen's response was its focus on maintaining customer relationships despite physical distance. Field officers made phone calls to every borrower, checking on their welfare, explaining the moratorium, and maintaining the human connection that underpinned the model.

Recovery, when it came, was swifter than expected. By December 2021, disbursements reached pre-Covid levels. The rural economy, less affected by lockdowns than urban areas, bounced back as agricultural activities continued. More importantly, the trust built over decades held firm—borrowers who could repay did so voluntarily, even without the pressure of weekly meetings.

The crisis accelerated digital transformation. UPI-based collections, previously a minor channel, became essential. The company launched WhatsApp-based customer service, enabling borrowers to check balances and make payments remotely. Field officers were equipped with better tablets and trained on video calling for virtual center meetings. What might have taken years of gradual change happened in months.

Strategic initiatives during this period positioned the company for post-pandemic growth. U.S. International Development Finance Corporation, the US Government's development finance institution signed a loan agreement of US$35 million with CA Grameen in November 2022. This wasn't just capital—it was validation from a US government institution of the company's resilience and impact.

In June 2023, CA Grameen signed a syndicated social loan facility of up to US$200 million, the first in the microfinance industry and the fourth in the country. The "social loan" designation was significant—linking interest rates to social impact metrics like women empowerment and financial inclusion. This innovative structure aligned investor returns with development outcomes, pioneering a new model for impact financing.

Leadership transition marked a new chapter. Ganesh Narayanan was appointed as the CEO with effect from August 1, 2023, while Udaya Kumar Hebbar continues to oversee the firm as MD. Narayanan, with extensive experience in retail banking and financial inclusion, brought fresh perspective while Hebbar's continuity ensured institutional memory. This dual leadership structure—combining new ideas with deep experience—reflected the company's evolution from founder-led to institutionally managed.

CreditAccess Grameen Touches Historic Mark of INR 25,000 Crore AUM, a milestone that seemed impossible during the dark days of 2020. The company also received multiple accolades including 'Microfinance Organisation of the Year Award' and featured in the Top 5 of Fortune India Next 500 list.

Product innovation accelerated post-COVID. Recognizing that the pandemic had created new financial needs, the company launched emergency medical loans, education loans for digital devices, and micro-enterprise loans for businesses pivoting to new models. The traditional income generation loan evolved to include working capital for e-commerce ventures, recognizing that even rural entrepreneurs were going digital.

Geographic expansion continued strategically. Rather than chasing growth in new states, the company deepened penetration in existing markets. District coverage increased from 300 to 423, but more importantly, the company increased wallet share with existing customers through cross-selling insurance, pension products, and gold loans through partnerships.

Technology infrastructure saw massive investment. A new data warehouse enabled real-time analytics on portfolio performance. Machine learning models improved credit scoring, reducing turnaround time for loan approvals from days to hours. API integrations with banks streamlined disbursements and collections. Yet the company resisted the temptation to become fully digital—maintaining that for their customer segment, human interaction remained irreplaceable.

By 2024, the transformation was complete. From a company that nearly ground to a halt during lockdown, CreditAccess Grameen emerged as a digital-physical hybrid, combining high-tech operations with high-touch customer service. Market Cap reached ₹20,788 Cr with Revenue of ₹5,703 Cr, making it one of India's most valuable financial inclusion companies.

The modern era also brought new challenges. Regulatory scrutiny intensified, with the RBI concerned about over-leveraging in the microfinance sector. Competition from small finance banks and fintech lenders increased. Rising interest rates pressured margins. Most fundamentally, the question emerged: as India develops and financial inclusion improves, what's the future of microfinance?

CreditAccess Grameen's answer has been evolution rather than revolution. The company sees itself transitioning from pure microfinance to comprehensive financial services for the underserved. This means not just credit but savings, insurance, payments, and advisory services. It means serving not just rural women but their families' entire financial needs. It means being not just a lender but a trusted financial partner for India's next billion.

Competitive Dynamics & Industry Analysis

The Indian microfinance landscape resembles a battlefield where different armies—NBFC-MFIs, Small Finance Banks, commercial banks, and fintechs—compete for the same territory: India's 400 million underbanked population. In the financial year 2023, the portfolio outstanding or the value of microfinance loans in India was around 3.55 trillion, representing a massive opportunity that attracts diverse players with different strategies, capabilities, and ambitions.

CreditAccess Grameen, with its 6% market share, stands as the largest pure-play NBFC-MFI. But this leadership position masks intense competitive dynamics. Bandhan Bank and Ujjivan Small Finance Bank, former MFIs that converted to banks, now compete with the advantage of offering full banking services—savings accounts, fixed deposits, remittances—creating sticky customer relationships that pure MFIs can't match. Their cost of funds, at 6-7%, is significantly lower than NBFC-MFIs' 10-12%, enabling them to offer more competitive rates while maintaining margins.

The Small Finance Bank model represents an existential question for CreditAccess Grameen. Should they pursue a banking license? The benefits are clear: lower funding costs, ability to mobilize deposits, fuller customer relationships. But the costs are equally significant: higher regulatory requirements, mandatory priority sector lending beyond microfinance, the complexity of managing deposit operations. Management's decision to remain an NBFC-MFI reflects a strategic choice—focus on what they do best rather than dilute efforts across multiple business lines.

Traditional banks pose a different challenge. State Bank of India, HDFC Bank, and ICICI Bank have all launched microfinance verticals or partnered with MFIs through co-lending arrangements. In November 2024, Muthoot Microfin, a Kochi-based microfinance institution, commenced loan disbursals under a new co-lending partnership with the State Bank of India (SBI). SBI has sanctioned a ₹500 crore limit, to be disbursed in ₹100 crore tranches. These partnerships allow banks to meet priority sector lending requirements while leveraging MFIs' last-mile connectivity. For MFIs, it provides cheaper capital but at the cost of becoming essentially origination agents rather than principals.

The fintech disruption is perhaps most intriguing. Companies like PayTM, PhonePe, and Google Pay aren't traditional lenders but payment platforms that have accumulated vast user bases and transaction data. They're now leveraging this to offer instant micro-loans—₹1,000 to ₹10,000—approved in seconds through algorithms analyzing payment history. No field officers, no center meetings, no physical infrastructure. For younger, digitally-savvy borrowers, this convenience is compelling.

Yet CreditAccess Grameen's response reveals the limitations of pure digital models in microfinance. Their typical borrower—a 40-year-old woman in rural Karnataka with limited literacy—values the weekly center meeting not just for financial transactions but for social interaction, mutual support, and financial education. The loan officer who knows her family situation, understands seasonal income fluctuations, and can provide flexibility during crises offers value that no algorithm can replicate.

Regional players add another layer of competition. In Tamil Nadu, Equitas and Belstar compete fiercely. In Maharashtra, Annapurna Finance dominates certain districts. In the Northeast, Arohan Financial Services has deep roots. These regional specialists often have better cultural understanding, political connections, and operational efficiency in their territories. CreditAccess Grameen's strategy of contiguous expansion—moving into neighboring districts rather than distant states—reflects recognition that local knowledge matters more than national scale.

The competitive intensity varies dramatically by geography. In Andhra Pradesh and Telangana, still recovering from the 2010 crisis, competition is muted with strict regulatory oversight. In Tamil Nadu, with the highest microfinance penetration in India, competition is fierce with multiple lenders chasing the same borrowers. In newer markets like Uttar Pradesh and Bihar, with vast unserved populations, there's room for multiple players to grow without direct competition.

Pricing has become a key battleground. The Reserve Bank of India (RBI) has established a uniform household loan limit of Rs 300,000 for loans to be classified as microfinance. In addition, to qualify for an NBFC-MFI license, entities must have a minimum of 75% of their assets dedicated to microfinance activities. Moreover, the cap on NBFCs (Non-Banking Financial Companies) has been raised to 25% of their assets, an increase from the previous limit of 10%. Within these regulatory boundaries, interest rates range from 18% to 26%. CreditAccess Grameen, at 22-24%, sits in the middle—higher than bank-backed MFIs but lower than smaller NBFCs. This positioning reflects a strategic choice: compete on service quality rather than price alone.

Product innovation has become crucial for differentiation. While the basic income generation loan remains commoditized, companies are innovating at the edges. CreditAccess Grameen's Unnati individual loans for graduated borrowers compete with similar products from Ujjivan and Bandhan. Emergency loans, education loans, and home improvement loans are now offered by most players. The real differentiation comes from execution—speed of disbursement, flexibility in repayment, quality of customer service.

Technology adoption varies widely across competitors. New-age fintechs are fully digital by design. Small Finance Banks have invested heavily in core banking systems and digital channels. Traditional MFIs like CreditAccess Grameen are in transition—digitizing back-end operations while maintaining high-touch front-end delivery. This hybrid model may prove optimal, combining operational efficiency with the human relationships that drive microfinance success.

The role of promoters adds another dimension to competition. Annapurna Finance, BSS Microfinance Limited, Asirvad Microfinance Limited, Bandhan Bank and CreditAccess Grameen Limited are the major companies operating in this market. CreditAccess Grameen's Dutch promoter, CreditAccess India B.V., brings patient capital and international best practices. Bandhan's transformation from MFI to bank was driven by founder Chandra Shekhar Ghosh's vision. Ujjivan's Samit Ghosh brought banking expertise from his days at HDFC Bank. These leadership differences shape strategic choices and competitive positioning.

Looking ahead, consolidation seems inevitable. India micro lending market is projected to witness a CAGR of 12.21% during the forecast period FY2025-FY2032, growing from USD 18.32 billion in FY2024 to USD 46.04 billion in FY2032. But this growth will likely be captured by fewer, larger players. Smaller MFIs lacking capital or operational scale will be acquired or exit. Regional players will need to choose between remaining niche or seeking strategic partners. Digital attackers will force traditional players to accelerate technology adoption.

For CreditAccess Grameen, maintaining leadership requires a delicate balance. They must digitize without losing the human touch that defines their model. They must grow without sacrificing portfolio quality. They must compete on multiple fronts—against banks with cheaper funding, fintechs with better technology, and regional players with local expertise. Success will come not from winning every battle but from choosing which battles to fight.

IX. Playbook: Lessons in Financial Inclusion

After studying CreditAccess Grameen's 25-year journey, several strategic lessons emerge that transcend microfinance and apply to any business serving base-of-pyramid markets. These aren't theoretical frameworks but battle-tested principles forged through crises, refined through growth, and validated by sustainable success.

Building Trust in Low-Trust Environments

The fundamental challenge in microfinance isn't capital or technology—it's trust. CreditAccess Grameen's borrowers have often been exploited by moneylenders, ignored by banks, and disappointed by government schemes. Building trust required consistency over decades. Weekly meetings happen rain or shine. Loan officers stay in territories for years, becoming part of the community fabric. Promises made during good times are kept during crises. This trust, once earned, becomes a moat competitors can't cross regardless of pricing or technology.

The Power of Patient Capital

The Dutch investors' 15-year commitment through multiple crises exemplifies patient capital's importance. Unlike venture capital seeking quick exits or private equity demanding immediate returns, CreditAccess India B.V. understood that financial inclusion is a marathon, not a sprint. This patience allowed management to make long-term decisions—investing in technology during profitable periods, maintaining conservative growth during boom times, supporting borrowers during crises—that short-term oriented competitors couldn't match.

Managing Political and Regulatory Risk

The AP crisis of 2010 taught the industry that microfinance operates at the intersection of commerce and politics. Success requires not just regulatory compliance but active engagement with all stakeholders. CreditAccess Grameen's approach—maintaining transparent pricing, avoiding aggressive collection practices, engaging proactively with regulators, building relationships with local administration—turned potential adversaries into allies. The lesson: in politically sensitive sectors, reputation risk management is as important as credit risk management.

Balancing Social Mission with Commercial Viability

The tension between social impact and profitability defines microfinance. Lean too far toward social mission, and the business becomes unsustainable, unable to raise capital or scale operations. Lean too far toward profitability, and mission drift occurs, culminating in crises like AP 2010. CreditAccess Grameen's balance—maintaining 20%+ ROE while serving the poorest—wasn't achieved through compromise but through operational excellence that made serving the poor profitable.

Technology Adoption in Low-Tech Environments

The digitization challenge in microfinance isn't technical but behavioral. Borrowers comfortable with cash need compelling reasons to adopt digital payments. Loan officers used to paper processes resist tablet-based systems. CreditAccess Grameen's approach—gradual adoption, maintaining parallel systems, incentivizing rather than mandating change—reflects understanding that technology adoption is a human change management challenge, not an IT implementation project.

Crisis Management: From AP to COVID

Every crisis teaches different lessons. The AP crisis taught the importance of geographic diversification and regulatory engagement. Demonetization highlighted the need for digital payment infrastructure. COVID demonstrated the value of strong balance sheets and customer relationships. CreditAccess Grameen's crisis playbook—immediate customer support, transparent communication with stakeholders, conservative provisioning, accelerated innovation—turned each crisis into an opportunity for competitive differentiation.

The Consolidation Playbook

The Madura acquisition provides a template for successful M&A in microfinance. Due diligence goes beyond financial metrics to cultural compatibility and operational synergies. Integration proceeds gradually, maintaining separate brands and systems initially while building unified processes. Customer retention takes priority over cost synergies. Most importantly, acquisition isn't about eliminating competition but building scale for competitive advantage against new entrants.

Talent Management in Rural Markets

Recruiting and retaining quality staff in rural locations remains challenging. CreditAccess Grameen's solution combines competitive compensation with career development paths that don't require relocation to cities. Local hiring ensures cultural fit and reduces attrition. Investment in training—not just initial but continuous—builds capabilities while demonstrating commitment to employees. The promotion of field staff to management positions provides aspirational role models.

Risk Management Through Diversification

Concentration risk—geographic, sectoral, or product—has destroyed many MFIs. CreditAccess Grameen's measured diversification across states, loan products, and customer segments provides resilience without losing focus. The key insight: diversification should follow operational capability, not precede it. Entering new markets or launching new products before building requisite capabilities invites disaster.

The Network Effect in Microfinance

Unlike digital platforms where network effects are obvious, microfinance network effects are subtle but powerful. Each successful borrower becomes a reference for others. Each center meeting strengthens social bonds that improve repayment. Each village with successful groups attracts neighboring villages. This organic growth, slower than aggressive expansion but more sustainable, builds density that improves economics and resilience.

Innovation Through Incremental Evolution

Revolutionary innovation rarely works in microfinance—borrowers and field staff resist dramatic change. CreditAccess Grameen's innovation model emphasizes incremental improvements: slightly larger loan sizes for successful borrowers, gradual introduction of individual loans, slow adoption of digital payments. This evolution, while appearing conservative, cumulatively transforms the business while maintaining stability.

Managing Stakeholder Complexity

Microfinance institutions serve multiple stakeholders with often conflicting interests. Borrowers want lower rates and flexible terms. Investors seek returns. Regulators demand compliance. Communities expect social development. Government wants financial inclusion. Managing these competing demands requires clear prioritization—borrowers first, sustainability second, growth third—and consistent communication that explains how serving one stakeholder ultimately benefits all.

The Importance of Middle Management

In organizations with thousands of field staff serving millions of customers, middle management—branch managers, area managers, regional heads—determines success. They translate strategy into execution, maintain culture during rapid growth, and serve as the communication link between field and headquarters. CreditAccess Grameen's investment in middle management development, often overlooked by competitors focused on technology or top leadership, provides operational excellence that technology alone can't deliver.

Creating Shared Value

The most sustainable businesses in base-of-pyramid markets create value for all participants. Borrowers build businesses and improve lives. Employees have stable careers with growth opportunities. Investors earn reasonable returns. Communities see economic development. Government achieves policy objectives. This shared value creation, where success isn't zero-sum but mutually reinforcing, provides the foundation for long-term success.

These lessons, learned through success and failure, growth and crisis, provide a playbook not just for microfinance but for any business seeking to serve underserved markets profitably and sustainably. The key insight: building businesses for the poor requires not charity or subsidy but operational excellence, patient capital, and unwavering focus on creating value for customers who have been ignored by traditional business models.

X. Bear & Bull Case Analysis

The investment case for CreditAccess Grameen presents a classic emerging market dichotomy—enormous opportunity shadowed by significant risks. Understanding both the bull and bear cases requires examining not just the company but the entire ecosystem of Indian financial inclusion.

Bull Case: The Underpenetrated Opportunity

India's credit-to-GDP ratio stands at approximately 55%, compared to 150%+ in developed markets and even 100%+ in other major emerging markets. Within this underpenetrated market, rural credit penetration is below 10%. With 600 million Indians still lacking access to formal credit, the addressable market is massive and growing.

Demographics provide a powerful tailwind. India adds 12 million people to the working-age population annually. Rural incomes are growing at 7-8% annually, faster than urban income growth. Increasing smartphone penetration—now exceeding 600 million users—enables digital financial services delivery to previously unreachable customers. The formalization of the economy through GST and digital payments creates credit histories for previously invisible borrowers.

CreditAccess Grameen's market leadership position provides substantial competitive advantages. Scale economics in microfinance are powerful—larger operations mean lower cost per borrower, better technology leverage, and stronger negotiating power with lenders. The company's conservative underwriting and strong risk management have created a portfolio that has weathered multiple crises. Geographic diversification across 16 states provides resilience against localized shocks.

The Madura acquisition demonstrates management's ability to execute complex transactions and integrate operations successfully. This capability becomes crucial as the industry consolidates, with smaller players lacking scale or capital adequacy becoming acquisition targets. CreditAccess Grameen's strong balance sheet and access to capital position it as a natural consolidator.

Technology investments are beginning to pay dividends. Digital collections reduce operational costs while improving convenience for borrowers. Data analytics enhance credit underwriting and early warning systems. API integrations with banks and payment systems streamline operations. While maintaining the high-touch model that differentiates microfinance, these digital capabilities improve efficiency and scalability.

Regulatory evolution favors established players. The RBI's progressive regulations have created a level playing field while weeding out weak players. Regulatory emphasis on customer protection and responsible lending aligns with CreditAccess Grameen's operational philosophy. The potential for differentiated bank licenses or payment bank licenses could provide additional growth avenues.

The social impact angle increasingly matters to investors. ESG-focused funds seek investments that generate both financial returns and social impact. CreditAccess Grameen's focus on women empowerment, financial inclusion, and rural development perfectly fits these mandates. The $200 million social loan facility demonstrates access to new capital pools linked to impact metrics.

Bear Case: Structural and Cyclical Headwinds

Company has low interest coverage ratio. This fundamental concern reflects the high leverage inherent in the NBFC model. With debt-to-equity ratios of 5-6x, even small increases in funding costs or credit losses can significantly impact profitability. Rising interest rates globally and in India pressure margins from both sides—increasing funding costs while limiting ability to raise lending rates due to regulatory caps and competitive pressure.

Asset quality concerns persist despite current low NPAs. Microfinance loans are unsecured, relying entirely on social collateral and borrower willingness to pay. Economic shocks—whether local (drought, floods) or systemic (demonetization, COVID)—immediately impact repayment. The lack of physical collateral means recovery from defaulted loans is minimal. Historical precedents from AP 2010 and demonetization show how quickly asset quality can deteriorate.

Political risk remains elevated. Microfinance operates at the intersection of commerce and social policy, making it vulnerable to populist politics. Loan waivers, interest rate caps, or operational restrictions can be imposed suddenly by state governments. The AP crisis demonstrated how political intervention can destroy the entire sector in a state overnight. With elections cyclic and poverty a political issue, this risk never fully dissipates.

Competition from multiple angles pressures the business model. Small Finance Banks offer full banking services with lower funding costs. Fintech lenders provide instant digital loans without operational infrastructure. Traditional banks use co-lending to cherry-pick better customers. Government schemes provide subsidized credit to the same target segments. This competition pressures both market share and margins.

Concentration risks persist despite diversification efforts. Rural markets depend heavily on agriculture, making the portfolio vulnerable to monsoons and crop prices. Women borrowers, while showing better repayment behavior, may be more vulnerable during economic stress. Geographic expansion into new states brings execution risk and unfamiliar operating environments.

The traditional microfinance model faces existential questions. Younger borrowers prefer digital channels over physical meetings. Rising operational costs—wages, fuel, real estate—pressure the high-touch service model. The weekly meeting structure seems anachronistic in an increasingly digital India. If the fundamental service delivery model becomes obsolete, massive infrastructure investments become stranded assets.

Regulatory tightening could constrain growth. The RBI, concerned about over-leveraging and customer protection, could impose stricter regulations. Limits on lending rates, number of loans per borrower, or total exposure could reduce profitability. Requirements for higher capital adequacy or provisioning would reduce ROE. The regulatory pendulum, having swung toward liberalization, could swing back toward restriction.

Valuation concerns merit attention. Trading at 3x book value, the stock prices in perfect execution and continued growth. Any disappointment in growth rates, asset quality, or profitability could trigger significant multiple compression. The promoter's potential exit, with CreditAccess India B.V. reportedly seeking buyers, creates overhang and uncertainty about future strategy and governance.

Macro-economic headwinds pose risks. India's rural economy, despite long-term growth potential, faces near-term challenges. Agricultural distress from climate change impacts crop yields and farmer incomes. Rural unemployment remains elevated post-COVID. Input cost inflation pressures small business profitability. These factors could impact both loan demand and repayment capacity.

Balancing the Cases

The bull and bear cases aren't mutually exclusive—many of the bearish concerns are risks to be managed rather than certainties to be avoided. The massive market opportunity is real, but capturing it requires navigating political, regulatory, competitive, and operational challenges. CreditAccess Grameen's track record suggests capability to manage these challenges, but past performance doesn't guarantee future success.

For investors, the key question isn't whether risks exist—they clearly do—but whether the company's competitive position, operational capabilities, and market opportunity justify these risks. The answer depends on investment horizon, risk tolerance, and belief in India's financial inclusion story. Long-term investors believing in India's development trajectory may find the bull case compelling despite near-term headwinds. Short-term investors or those concerned about regulatory and political risks may find the bear case more persuasive.

XI. Looking Forward: The Next Chapter

Standing at the threshold of 2025, CreditAccess Grameen faces an inflection point. The company that started with $35,000 and a dream of replicating Grameen Bank in India now stands as a ₹20,000+ crore market cap institution. But the next chapter won't be written by simply extrapolating past success. The convergence of technological disruption, regulatory evolution, competitive dynamics, and changing customer expectations demands strategic choices that will define the company's next decade.

The Path to 1 Crore Customers

Management's stated ambition of reaching 10 million (1 crore) customers from the current 4.6 million represents more than doubling in size. But linear scaling won't work—adding more branches and loan officers in the traditional model would face diminishing returns and operational complexity. The path requires a fundamental reimagination of service delivery.

The hybrid model emerging combines physical presence with digital delivery. Branch infrastructure evolves from transaction processing centers to relationship management hubs. Loan officers transform from cash collectors to financial advisors. Weekly meetings continue but incorporate digital tools—tablets for documentation, apps for financial literacy, WhatsApp groups for communication. This evolution maintains the human connection while improving efficiency.

Customer segmentation becomes crucial. The traditional JLG model continues serving core customers—rural women with limited digital literacy. But new products target different segments: individual loans for graduated borrowers, education loans for next-generation customers, micro-enterprise loans for small businesses. Each segment requires different service models, risk assessment methods, and engagement strategies.

Digital Lending and the Phygital Model

The term "phygital"—physical plus digital—captures CreditAccess Grameen's strategic direction. Pure digital models struggle with customer acquisition costs and trust deficits in rural markets. Pure physical models face cost pressures and efficiency constraints. The phygital model leverages the best of both worlds.

Digital loan origination through the MAHI app reduces turnaround time from days to hours. But loan officers still conduct physical verification and assess character—crucial for unsecured lending. Digital collections through UPI provide convenience and cost savings. But center meetings continue for relationship building and problem resolution. Digital financial literacy through videos and apps supplements but doesn't replace face-to-face education.

The technology stack evolution focuses on three areas. Front-end applications improve customer and employee experience. Middle-layer analytics enhance credit decisioning and risk management. Back-end infrastructure ensures scalability and reliability. APIs enable ecosystem partnerships—credit bureaus for underwriting, banks for disbursement, payment platforms for collection.

But technology adoption faces behavioral challenges. Customers comfortable with cash need incentives to adopt digital payments. Field staff fear technology will replace them. Middle management lacks digital skills. Overcoming these requires change management as much as technology implementation—training programs, incentive alignment, gradual transition with parallel systems.

Small Finance Bank: The Strategic Question

The potential conversion to a Small Finance Bank represents the biggest strategic decision ahead. The benefits are compelling: ability to mobilize deposits reducing funding costs, full banking relationships increasing customer stickiness, payment services generating fee income, regulatory parity with competing SFBs.

But challenges are equally significant. Banking licenses come with obligations—priority sector lending requirements, branch opening mandates, complex compliance requirements. Deposit mobilization requires different capabilities—liability sales forces, treasury management, ALM expertise. Technology infrastructure for core banking costs hundreds of crores. Most fundamentally, banking is a different business from lending, requiring different skills, systems, and strategies.

The regulatory pathway exists—the RBI has guidelines for NBFC-MFI to SFB conversion. But meeting eligibility criteria—track record, capital adequacy, governance standards—is just the beginning. The transformation process takes 18-24 months, during which normal business must continue while building new capabilities.

Management's cautious approach reflects these complexities. Rather than rushing into banking, they're building capabilities gradually. Payment services through partnerships provide experience without regulatory burden. Deposit-like products such as gold loans create liability relationships. Technology infrastructure upgrades prepare for eventual banking systems. This measured approach preserves optionality while avoiding premature commitment.

International Expansion Possibilities

CreditAccess Grameen's promoter operates across Asia—Indonesia, Philippines, Vietnam. This network provides potential international expansion opportunities. The microfinance model, with local adaptations, works across emerging markets. Management expertise in building and scaling operations could transfer internationally.

But international expansion in microfinance faces unique challenges. Unlike technology businesses that scale globally through digital platforms, microfinance requires local presence, regulatory approvals, and cultural understanding. Each market has different competitive dynamics, regulatory frameworks, and customer behaviors. Currency risks, political risks, and operational complexity multiply with geography.

A more likely scenario involves knowledge transfer rather than direct expansion. Sharing best practices with sister companies, providing technical assistance to other markets, or licensing technology platforms generates value without operational risk. This approach leverages expertise while maintaining focus on the massive Indian opportunity.

Climate Finance and Sustainable Lending

Climate change disproportionately impacts CreditAccess Grameen's borrowers—rural communities dependent on agriculture. Droughts affect crop yields and repayment capacity. Floods destroy small businesses. Rising temperatures reduce agricultural productivity. This creates both risks and opportunities.

Climate adaptation financing emerges as a new product category. Loans for drought-resistant seeds, water conservation infrastructure, or climate-resilient livelihoods address customer needs while managing portfolio risk. Partnerships with agricultural technology companies provide access to weather insurance, soil testing, or precision agriculture tools.

Green financing attracts new capital sources. Development finance institutions prioritize climate-related lending. Impact investors seek environmental alongside social returns. The $200 million social loan facility demonstrates appetite for such structures. Future capital raising could increasingly link to environmental metrics—loans for clean energy, sustainable agriculture, or climate adaptation.

But implementation requires new capabilities. Assessing environmental impact of loans, monitoring climate risks, and measuring adaptation outcomes demand different skills than traditional microfinance. Partnerships with climate experts, technology providers, and development organizations become essential.

Artificial Intelligence and the Future of Credit

AI and machine learning promise to revolutionize credit decisioning. Alternative data sources—mobile phone usage, social media behavior, digital payments history—could assess creditworthiness without traditional financial histories. Pattern recognition could identify fraud or predict default before traditional indicators. Natural language processing could automate customer service and financial education.

CreditAccess Grameen's data advantage—millions of customers with years of repayment history—provides training data for AI models. But implementation faces practical challenges. Rural customers often share phones or have limited digital footprints. Regulatory requirements for explainable AI conflict with black-box algorithms. Most fundamentally, the human judgment that underpins successful microfinance—assessing character, understanding circumstances, providing flexibility—resists automation.

The likely evolution involves AI augmenting rather than replacing human decision-making. Algorithms flag risks for human review. Pattern recognition identifies cross-selling opportunities. Chatbots handle routine queries while humans manage complex issues. This human-in-the-loop approach combines artificial intelligence with emotional intelligence.

The Next Decade's Trajectory

Looking ahead to 2035, CreditAccess Grameen's evolution seems clear in direction if uncertain in specifics. The company will be more digital but not purely digital, maintaining physical presence while leveraging technology. Product portfolios will expand beyond traditional microfinance to comprehensive financial services. Geographic presence will deepen in existing markets rather than expanding to new countries.

The competitive landscape will consolidate around 5-10 large players, with CreditAccess Grameen among the leaders. Technology platforms and partnerships will matter as much as branch networks. Regulatory frameworks will mature, providing clarity and stability. Customer expectations will evolve, demanding convenience alongside relationship.

Success requires balancing multiple transitions simultaneously—digital transformation while maintaining human touch, geographic expansion while deepening existing markets, product diversification while maintaining core focus, growth while managing risk. This balance, difficult to achieve, represents the key challenge and opportunity.

The fundamental mission—financial inclusion for India's underserved—remains unchanged. But the methods, models, and mechanisms will evolve dramatically. The company that emerges will be as different from today's CreditAccess Grameen as today's institution differs from the NGO that started in Avalahalli village. Yet the thread connecting past, present, and future remains constant: the belief that access to credit, responsibly provided, can transform lives and communities.

For investors, employees, customers, and stakeholders, this evolution presents both opportunity and uncertainty. The market opportunity remains massive, the competitive position strong, and the management capable. But execution risks abound, competition intensifies, and disruption accelerates. Success isn't guaranteed but remains achievable for those who navigate carefully, adapt quickly, and remain focused on the ultimate mission—enriching lives through financial inclusion.

XII. Recent News

The microfinance sector entered turbulent waters in late 2024, and CreditAccess Grameen found itself navigating unprecedented challenges that tested its operational resilience and strategic adaptability. Shares of CreditAccess Grameen hit 34-month low of Rs 750.05, tanking 18% after the company reported a loss of Rs 99.5 crore in Q3FY25, led by higher provision at Rs 752 crore, compared to a net profit of Rs 353.42 crore in Q3FY24.

This dramatic reversal wasn't isolated to CreditAccess Grameen but reflected broader sectoral stress. The microfinance industry faced a perfect storm of challenges: over-leveraging in certain pockets, competitive intensity leading to relaxed underwriting standards, and economic stress in rural markets affecting repayment capacity. The company stated that "early risk recognition, conservative provisioning, and accelerated write-offs resulted in a loss of Rs 99.5 crore in Q3FY25" but would "safeguard profitability over the coming quarters".

Collection efficiency in X bucket was over 99.2% in December 2024 and further improved in January 2025, though Q3 FY25 profits were impacted, the company still delivered ROA of 2.3% and ROE of 9.4% for 9M FY25. This improvement in collection efficiency provided early signs of recovery, though management remained cautious about declaring victory prematurely.

The company's response demonstrated both prudence and confidence. Management forecasts 7-8% loan portfolio growth for FY25 with ROA of 2.3-2.4% and ROE of 9.5-10.0%, anticipating asset quality to normalise by Q1 FY26 and profitability by Q2 FY26, with preliminary FY26 outlook suggesting AUM growth of 18-20%.

Strategic initiatives continued despite operational challenges. In November 2024, CreditAccess Grameen secured €25M from DEG and Rs 170 Cr from Citi via co-financing, demonstrating continued access to international capital markets despite sectoral headwinds. In September 2024, the company elevated Nilesh Dalvi to CFO, strengthening its finance function during a critical period.

The financial position remained robust despite quarterly losses. The company maintained robust liquidity of Rs 2,035.7 crore, 7.6% of total assets enhanced to ~10% in October 2024, with healthy capital position showing CRAR of 26.1% and credit ratings of AA-/Stable from CRISIL, ICRA & India Ratings.

Operational metrics showed resilience. GLP grew by 11.8% YoY from Rs 22,488 crore to Rs 25,133 crore, with borrower base growing 7.2% YoY from 46.03 lakh to 49.33 lakh across 2,031 branches. The historic milestone of touching INR 25,000 Crore AUM was achieved despite challenging conditions.

Recognition continued even during difficult times. The company received the 'Microfinance Organisation of the Year Award', featured in the Top 5 of Fortune India Next 500 list, and was conferred "Best Small NBFC" 2023 at Mint BFSI Summit & Awards.

Guidance for FY25 was revised downwards for the second time, with growth at 7-8%, credit cost at 6.7-6.9%, and RoA at 2.3-2.4%. This conservative guidance reflected management's preference for under-promising and over-delivering rather than maintaining aggressive targets during uncertain times.

Analyst perspectives remained mixed but cautiously optimistic. MOFSL believes sectoral pain will continue for 2-3 more quarters as stress needs to be provided for and written off, though improvement in collections gives hope that needs monitoring over 3-4 months before confirming trend reversal. While management remains confident about peaking out of stress, more signs of revival are expected before recovery in valuations, with relative superior quarterly performance potentially keeping valuation in a broad range near-term.

The stock performance reflected market concerns. The market price declined 55% from its 52-week high of Rs 1,659.95 hit on February 12, 2024, creating potential opportunity for long-term investors believing in the recovery thesis but also reflecting genuine concerns about near-term challenges.

Looking forward, the company's trajectory depends on multiple factors converging positively. Rural economic recovery, normalized monsoons, stabilization of competitive intensity, and successful execution of credit risk management strategies will determine whether Q3FY25 represents the trough or merely a waystation in a longer adjustment period. Management's track record through previous crises—AP 2010, demonetization, COVID-19—suggests capability to navigate current challenges, but each crisis is unique and past performance doesn't guarantee future success.

XIII. Links & Resources

Company Resources: - Annual Reports: creditaccessgrameen.in/investors/financials-and-investor-presentations/annual-reports/ - Investor Presentations: creditaccessgrameen.in/investors/financials-and-investor-presentations/investor-presentations/ - Financial Results: creditaccessgrameen.in/investors/financials-and-investor-presentations/financial-results/ - Press Releases: creditaccessgrameen.in/media/press-releases/ - Corporate Governance: creditaccessgrameen.in/investors/corporate-governance/

Regulatory Documents: - RBI NBFC-MFI Guidelines: rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=9827 - RBI Master Directions for NBFC: rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=11846 - SEBI Listing Regulations: sebi.gov.in/legal/regulations/ - NCLT Orders on Amalgamation: nclt.gov.in/

Industry Reports: - MFIN India Microfinance Review: mfinindia.org/publications - Sa-Dhan Bharat Microfinance Report: sa-dhan.net/resources/publications/ - World Bank Financial Inclusion Data: worldbank.org/en/topic/financialinclusion - CGAP Research on Microfinance: cgap.org/research

Academic Resources: - "Give Us Credit" by Alex Counts (Grameen Foundation) - "Creating a World Without Poverty" by Muhammad Yunus - "Banker to the Poor" by Muhammad Yunus - "The Economics of Microfinance" by Beatriz Armendáriz and Jonathan Morduch - Journal of Microfinance / ESR Review - Small Enterprise Development Journal

Market Data & Analysis: - NSE India: nseindia.com/get-quotes/equity?symbol=CREDITACC - BSE India: bseindia.com/stock-share-price/creditaccess-grameen-ltd/creditacc/543427/ - Screener.in: screener.in/company/CREDITACC/ - Trendlyne: trendlyne.com/equity/543427/CREDITACC/ - MoneyControl: moneycontrol.com/india/stockpricequote/nbfc/creditaccessgrameenlimited/CGL02

Competitor Analysis: - Bandhan Bank: bandhanbank.com/investor-relations - Ujjivan Small Finance Bank: ujjivansfb.in/investor-relations - Spandana Sphoorty: spandanasphoorty.com/investors/ - Fusion Microfinance: fusionmicrofinance.com/investor-relations/ - Equitas Holdings: equitas.in/investor-relations/

Research Reports: - ICICI Direct Research - Motilal Oswal Research - IIFL Securities Research - Kotak Institutional Equities - HDFC Securities Research

Development Finance Resources: - U.S. International Development Finance Corporation: dfc.gov - DEG (German Investment Corporation): deginvest.de - FMO (Dutch Development Bank): fmo.nl - IFC (World Bank Group): ifc.org - ADB Microfinance Resources: adb.org/sectors/finance/microfinance

Technology & Innovation: - CGAP Technology for Microfinance: cgap.org/topics/digital-financial-services - Microsave Reports on Digital Finance: microsave.net/ - Better Than Cash Alliance: betterthancash.org/ - GSMA Mobile Money: gsma.com/mobilemoney/

Impact Measurement: - Social Performance Task Force: sptf.info/ - IRIS+ Impact Metrics: iris.thegiin.org/ - MIX Market Data: themix.org/ - Microfinance Transparency: mftransparency.org/

News & Media Coverage: - The Economic Times BFSI: economictimes.indiatimes.com/industry/banking/finance - Business Standard Finance: business-standard.com/finance - The Hindu BusinessLine: thehindubusinessline.com/money-and-banking/ - BloombergQuint: bloombergquint.com/ - CNBC TV18: cnbctv18.com/finance/

Podcasts & Video Resources: - Acquired.fm Episodes on Financial Services - Masters of Scale Episodes on Financial Inclusion - How I Built This - Muhammad Yunus Episode - CNBC Making it Big - CreditAccess Grameen Feature - Company Earnings Call Recordings

Books for Further Reading: - "Portfolios of the Poor" by Collins, Morduch, Rutherford, and Ruthven - "The Fortune at the Bottom of the Pyramid" by C.K. Prahalad - "Due Diligence: An M&A Value Creation Approach" by William J. Gole - "Microfinance Handbook" by Joanna Ledgerwood (World Bank) - "Financial Inclusion in India: Policies and Programmes" by C. Rangarajan

Conclusion: The Unfinished Revolution

CreditAccess Grameen's story represents far more than a single company's journey—it embodies India's ongoing revolution in financial inclusion. From Vinatha Reddy's $35,000 beginning to today's ₹20,000+ crore institution, the trajectory traces not just corporate growth but social transformation. Millions of women who once depended on usurious moneylenders now access formal credit, build businesses, and imagine different futures for their children.

Yet calling this revolution complete would be premature. The recent quarterly loss and sectoral stress remind us that microfinance remains a fragile bridge between poverty and prosperity. The business of lending to the poor without collateral depends on trust, social cohesion, and economic stability—all vulnerable to disruption. The 2010 AP crisis, demonetization, COVID-19, and now the 2024 sectoral stress each tested different aspects of this model, revealing both resilience and vulnerability.

The strategic choices ahead—whether to pursue a banking license, how aggressively to digitize, where to expand geographically—will determine whether CreditAccess Grameen remains relevant in India's rapidly evolving financial landscape. The company that succeeded by bringing Grameen Bank's group lending model to India must now navigate a world where smartphones are ubiquitous, digital payments commonplace, and customer expectations transformed.

Competition has evolved from other MFIs to a complex ecosystem including Small Finance Banks with full service offerings, fintech companies with algorithmic lending, and traditional banks awakening to the opportunity at the bottom of the pyramid. Maintaining leadership requires not just operational excellence but strategic vision—understanding which battles to fight and which to concede.

The fundamental tension between social mission and commercial viability remains unresolved. Every basis point reduction in interest rates helps borrowers but pressures margins. Every relaxation in underwriting standards increases financial inclusion but risks portfolio quality. Every geographic expansion serves more poor but dilutes operational focus. Managing these trade-offs requires wisdom that financial models alone cannot provide.

International investors watching CreditAccess Grameen see more than an Indian NBFC—they see a test case for whether commercial microfinance can deliver both financial returns and social impact at scale. The Dutch promoter's patient capital over 15 years proved this possible, but whether public market investors will show similar patience during sectoral downturns remains uncertain.

For India's policymakers, CreditAccess Grameen represents both achievement and challenge. The company has demonstrated that private capital can serve public purpose, reaching customers government programs struggled to serve sustainably. Yet concentration of microfinance in certain states, over-leveraging in some segments, and periodic crises requiring regulatory intervention highlight the model's limitations.