HCA Healthcare: The Rise, Fall, and Redemption of America's Hospital Empire

I. Introduction & Episode Roadmap

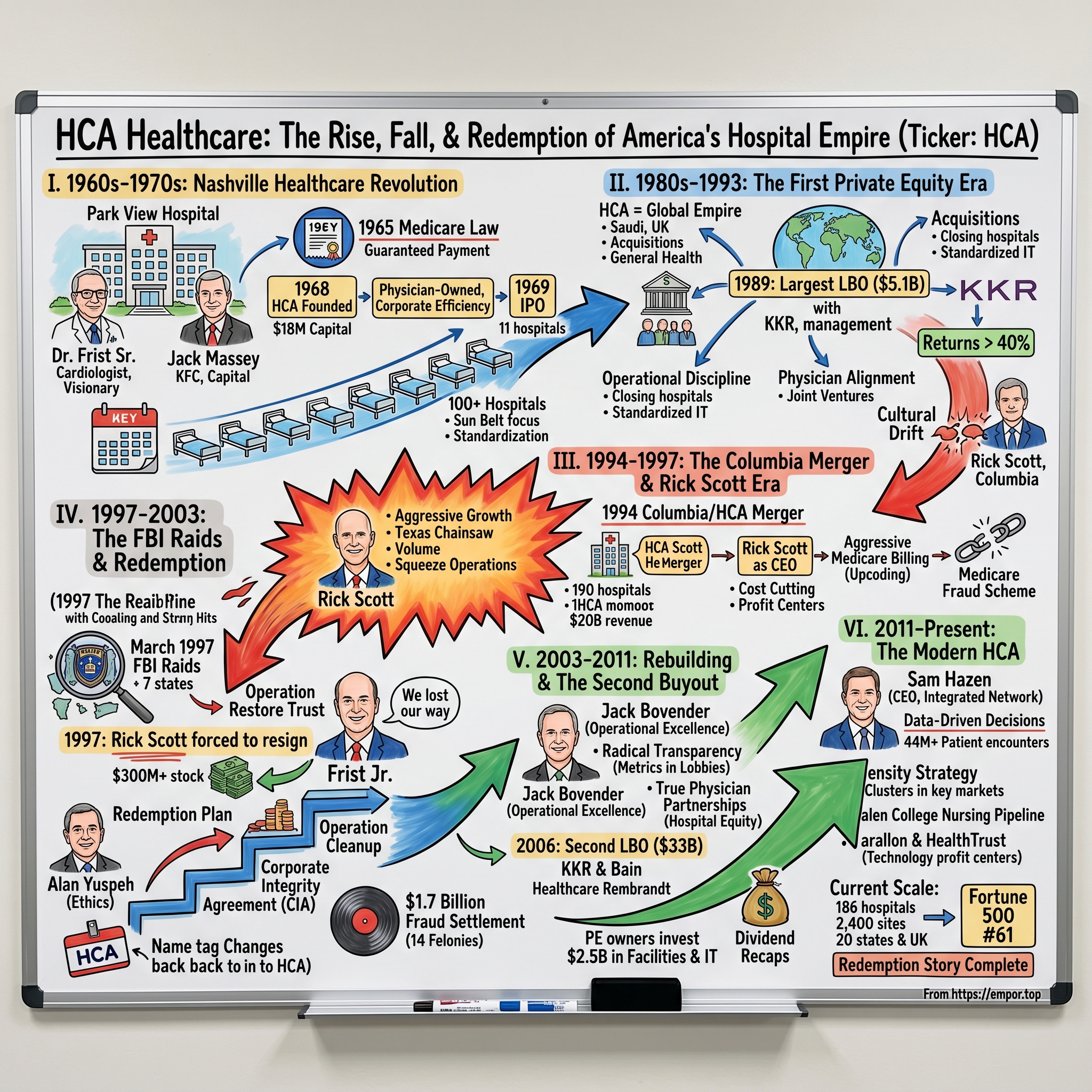

The fluorescent lights hummed in the Nashville boardroom on a humid July morning in 1997. Thomas F. Frist Jr., the genteel Tennessee physician-turned-executive who had built HCA into a healthcare colossus, sat across from Rick Scott, the brash Texan who had engineered its transformation into Columbia/HCA—then the world's largest hospital company. Between them lay FBI subpoenas, search warrants, and the wreckage of what would become the largest healthcare fraud investigation in U.S. history. Within hours, Scott would be forced to resign, and Frist would begin one of corporate America's most remarkable redemption stories.

Today, HCA Healthcare stands as a $300 billion market cap giant, operating 186 hospitals and approximately 2,400 sites of care across 20 states and the United Kingdom. With 2024 revenues of $70.6 billion and a position at #61 on the Fortune 500, it's easy to forget that this company once paid $1.7 billion in fraud settlements and pleaded guilty to 14 felonies. The journey from Nashville startup to corporate pariah to Wall Street darling isn't just a business story—it's a uniquely American tale of ambition, hubris, and reinvention.

What makes HCA's story particularly fascinating is how it mirrors the evolution of American healthcare itself: from the physician-entrepreneurs of the 1960s who saw opportunity in the newly created Medicare system, through the go-go consolidation of the 1980s, the private equity engineering of the 2000s, to today's data-driven, scale-obsessed healthcare delivery model. At every turn, HCA has been both protagonist and antagonist, innovator and cautionary tale.

The cast of characters reads like a Southern Gothic novel meets Wall Street thriller. There's Thomas F. Frist Sr., the cardiologist who founded Nashville's Park View Hospital with a vision of physician-owned care. His son, Thomas Jr., the HCA architect who would see his life's work nearly destroyed, only to resurrect it. Jack Massey, the Kentucky Fried Chicken magnate who provided the initial capital and business acumen. Rick Scott, the healthcare outsider whose aggressive tactics built an empire—and nearly destroyed it—before his second act as Florida's governor and U.S. Senator. And the private equity titans at KKR and Bain Capital, who engineered the largest leveraged buyout in history at the time, turning a billion-dollar investment into a three-billion-dollar payday.

This is a story about the power of consolidation in fragmented industries, the delicate dance between profit and purpose in healthcare, and how a company can transform scandal into success. It's about understanding that in American healthcare, scale isn't just an advantage—it's survival. And perhaps most importantly, it's about how the same forces that created modern American healthcare's problems also created its most successful players.

II. Origins: The Nashville Healthcare Revolution (1960s–1970s)

Picture Nashville in 1960: not yet "Music City USA," but a mid-sized Southern city on the cusp of transformation. Elvis had just returned from the Army, the interstate highway system was carving new paths through Tennessee, and a quiet revolution was beginning in a modest hospital on Charlotte Avenue. Dr. Thomas F. Frist Sr., a 49-year-old cardiologist with wire-rimmed glasses and the bearing of a Southern gentleman, was about to plant the seed that would grow into America's hospital empire.

Frist Sr. wasn't your typical physician. While his colleagues focused on their practices, he obsessed over the business of healthcare delivery. He'd founded Park View Hospital with $50,000 of his own money and a radical idea: physicians should own and operate hospitals, not just practice in them. "Doctors know what patients need," he'd tell anyone who'd listen, his soft Tennessee drawl masking fierce ambition. "Why should we let administrators make all the decisions?"

But Frist Sr. knew he needed more than medical expertise. Enter Jack C. Massey, a character straight from American business folklore. Massey had already made one fortune turning Harland Sanders' fried chicken recipe into Kentucky Fried Chicken, selling his stake for $35 million in 1964 (roughly $340 million today). Now in his mid-60s, with silver hair and the easy confidence of a man who'd bet big and won, Massey was hunting for his next venture. When mutual friends introduced him to the Frists at a Nashville country club in 1968, the chemistry was immediate.

The timing couldn't have been more perfect. Three years earlier, Lyndon Johnson had signed Medicare and Medicaid into law, instantly creating a guaranteed payment stream for hospital services. What had been a risky, capital-intensive business suddenly looked like a gold mine. "Medicare changed everything," Thomas Frist Jr. would later recall. "Overnight, millions of Americans had healthcare coverage. The demand was there—we just needed to build the supply."

On November 20, 1968, Hospital Corporation of America was born with $18 million in capital—Massey putting up the lion's share, the Frists contributing Park View Hospital and their expertise. Their vision was audacious: create a chain of hospitals run with the efficiency of a corporation but the care standards of a physician's practice. They would standardize operations, centralize purchasing, and most importantly, give doctors equity stakes to align incentives.

The early days were a blur of 18-hour workdays and red-eye flights. Frist Jr., then just 30 years old, became the chief dealmaker, crisscrossing the South in a twin-engine Cessna, visiting struggling hospitals in places like Dothan, Alabama, and Savannah, Georgia. His pitch was simple but compelling: "Join us, and you'll have the capital to buy new equipment, the scale to negotiate with suppliers, and the expertise to navigate Medicare billing. Stay independent, and you'll be competing against us."

The company's initial public offering in March 1969 was a watershed moment. HCA hit the New York Stock Exchange with 11 hospitals under management, raising $18 million at $12 per share. By year's end, they'd grown to 26 hospitals with 3,000 beds. Wall Street was mesmerized. Here was a company bringing corporate discipline to the notoriously inefficient hospital sector, with Medicare essentially guaranteeing demand.

But it wasn't just about financial engineering. The Frists insisted on maintaining clinical quality—a principle that would later distinguish them from more aggressive competitors. They created one of the industry's first standardized quality monitoring systems, tracking everything from infection rates to patient satisfaction scores across all facilities. "We're not just buying hospitals," Frist Sr. would say. "We're creating a system of care."

By 1973, HCA operated 50 hospitals. The playbook was working: acquire underperforming hospitals in growing Sun Belt markets, implement standardized operations, recruit physician partners with equity incentives, and leverage scale for purchasing power. They were particularly clever about site selection, focusing on suburbs and smaller cities where they could dominate market share rather than competing in crowded urban centers.

The cultural DNA established in these early years would prove crucial decades later. Unlike the wheeler-dealers who would flood the hospital industry in the 1980s, the Frists maintained a physician-first culture. Board meetings began with discussions of patient care metrics before moving to financials. Executives were required to spend time in hospitals, not just corporate offices. This "Nashville way"—genteel, physician-centric, quality-focused—would clash dramatically with other approaches, setting the stage for both triumph and catastrophe.

By the decade's end, HCA had grown to over 100 hospitals, becoming the undisputed king of the nascent for-profit hospital industry. They'd proven that healthcare could be both a business and a calling, that scale and quality weren't mutually exclusive. But success attracted competition, and the gentlemanly world of Nashville healthcare was about to collide with the bare-knuckled capitalism of the 1980s. The empire-building phase was about to begin, and with it would come temptations that would test everything the Frists had built.

III. The First Private Equity Era & Empire Building (1980s–1993)

The oak-paneled partners' meeting room at Kohlberg Kravis Roberts in New York felt worlds away from Nashville's hospital corridors. It was September 1988, and Henry Kravis, the leveraged buyout king who would soon orchestrate the RJR Nabisco takeover, leaned forward as Thomas Frist Jr. laid out his audacious proposal: take HCA private in what would be one of the largest leveraged buyouts in history. "The market doesn't understand our value," Frist argued, his usually measured Tennessee drawl quickening with conviction. "We're trading at eight times earnings while our assets alone are worth twice our market cap."

But we're getting ahead of ourselves. To understand how a physician-founded hospital company became a private equity play, we need to rewind to the early 1980s, when HCA transformed from a regional player into a global healthcare empire.

By 1983, HCA operated 376 hospitals—not just in the American South, but in seven countries including Saudi Arabia, Brazil, and the United Kingdom. The international expansion was Frist Jr.'s baby, driven by his belief that American hospital management expertise could be exported globally. In Jeddah, HCA ran the King Faisal Specialist Hospital, a gleaming facility serving Saudi royalty. In London, they operated Wellington Hospital, catering to Harley Street physicians and their wealthy patients. The company had become, improbably, one of Tennessee's first multinationals.

The domestic expansion was equally aggressive. Between 1980 and 1985, HCA acquired three major competitors: General Care Corporation, General Health Services, and Hospital Affiliates International. Each deal brought not just hospitals but entire management teams, IT systems, and corporate cultures that had to be integrated. The General Health Services acquisition alone added 42 hospitals overnight. By 1987, HCA had ballooned to 463 facilities—255 owned, 208 managed—making it by far the world's largest hospital company.

But size brought problems. The company had become unwieldy, with regional fiefdoms developing their own cultures and practices. Profit margins, once industry-leading at 15%, had compressed to under 10%. Wall Street, initially enamored with the growth story, began questioning whether bigger was actually better. HCA's stock languished in the $30s, implying a valuation that Frist Jr. found insulting. "We owned prime real estate in growing markets, had irreplaceable hospital licenses, and generated predictable cash flows," he'd later reflect. "Yet we were valued like a declining industrial company."

The solution came from an unexpected source: the hostile takeover attempt of Hospital Corporation International by Riley Bechtel in early 1987. Though unsuccessful, it awakened Frist Jr. to HCA's vulnerability. If he didn't take the company private, someone else might do it hostile. He began quietly assembling a buyout group, bringing in Morgan Stanley, and eventually KKR, though Kravis would later reduce his stake as he focused on RJR Nabisco.

The HealthTrust spinoff in 1987—creating a separate 104-hospital company—was both a defensive move and a preview of coming attractions. It reduced HCA's size, making a buyout more manageable, while also demonstrating that value could be unlocked through financial engineering. HealthTrust immediately traded at a premium to its implied value within HCA, proving Frist's point about the conglomerate discount.

On February 1, 1989, the hammer fell: HCA would go private in a $5.1 billion leveraged buyout, with management owning 18%, employees 10%, and the rest split among institutional investors. The deal valued HCA at $51 per share, a 65% premium to its recent trading price. Frist Jr. personally invested $50 million, mortgaging everything he owned. "This wasn't just a financial transaction," he'd say. "We were betting our careers, our reputations, our families' futures on making this work."

The private HCA of 1989-1992 was a case study in operational discipline. Free from quarterly earnings pressure, management made tough decisions: closing underperforming hospitals, renegotiating supplier contracts, and most controversially, laying off 5,000 corporate staff. They sold 74 hospitals for $1.7 billion, using proceeds to pay down debt. IT systems were standardized, purchasing was centralized, and clinical protocols were harmonized across the chain.

But the real innovation was in physician alignment. Frist Jr. pioneered joint ventures where doctors owned minority stakes in hospital service lines—surgery centers, imaging facilities, cancer centers. This gave physicians skin in the game while keeping majority control with HCA. "We turned potential competitors into partners," explained Jack Bovender, then running HCA's Eastern division. "A surgeon who owns 20% of our surgery center isn't going to send cases to the hospital across town."

The financial results were spectacular. EBITDA margins expanded from 14% to 19%. Debt was reduced from $5.1 billion to $3.2 billion. When HCA returned to public markets in February 1992 at $22 per share (adjusted for subsequent splits), the company was valued at $3.1 billion. Early investors saw returns exceeding 40% annually. Frist Jr.'s $50 million stake was worth $180 million.

Yet something was lost in the financial engineering. The physician-first culture that Frist Sr. had instilled was fraying. Young MBAs from consulting firms and investment banks were replacing hospital administrators who'd risen through clinical ranks. Performance metrics focused increasingly on financial rather than clinical outcomes. "We'd become very good at making money," one longtime executive recalled. "But we'd lost sight of why we existed."

This cultural drift would soon collide with a force of nature named Rick Scott, whose Columbia Hospital Corporation was revolutionizing—or destroying, depending on whom you asked—everything the Frists had built. The stage was set for a merger that would create the world's largest healthcare company and precipitate the industry's largest scandal. The Nashville way was about to meet the Texas chainsaw, and the results would reshape American healthcare forever.

IV. The Columbia Merger & Rick Scott Era (1994–1997)

Rick Scott didn't look like a healthcare revolutionary when he walked into Richard Rainwater's Fort Worth office in 1987. With his intense blue eyes, marathon runner's build, and the coiled energy of a middleweight boxer, the 34-year-old looked more like what he was—a corporate lawyer from a hardscrabble Illinois background who'd never run anything larger than a legal brief. But Rainwater, the billionaire investor who'd helped grow the Bass family fortune from $50 million to $5 billion, saw something others missed: hunger.

"How much are you worth?" Rainwater asked bluntly during their first meeting. Scott didn't flinch: "About $500,000, mostly from my law practice." Rainwater leaned back in his chair. "I'm going to make you rich, but first, you're going to make me richer. Healthcare is broken. The hospitals are run by doctors who can't manage money or administrators who don't understand medicine. Someone who understands both finance and operations could build an empire."

By April 1988, Scott and Rainwater had each ponied up $125,000 to form Columbia Hospital Corporation, purchasing two struggling El Paso hospitals for $60 million in mostly borrowed money. Where the Frists had built HCA through physician partnerships and gradual expansion, Scott attacked the industry like General Sherman marching through Georgia. His philosophy was brutal in its simplicity: cut costs, increase volume, and squeeze every dollar from operations.

Scott's first innovations seemed minor but proved revolutionary. He eliminated executive parking spaces—if the CEO could walk from the back of the lot, so could everyone else. He standardized everything from surgical gloves to financial software across facilities. But his masterstroke was turning department heads into entrepreneurs. Each unit—emergency, surgery, radiology—became a profit center with bonuses tied to financial performance. A lab director who previously worried about test accuracy now obsessed over turnaround times and profit margins.

The results were immediate and stunning. Those two El Paso hospitals went from losing $4 million annually to generating $40 million in EBITDA within 18 months. Scott used the cash flow to leverage more acquisitions, growing Columbia to 11 hospitals by 1990, then 44 by 1993. His CFO, Tom Vincen, a former Arthur Andersen partner, developed innovative financing structures that maximized leverage while maintaining investment-grade ratings. They were doing HCA-style roll-ups but at triple the speed and half the cost.

The Galen acquisition in September 1993 announced Scott's arrival as a major player. Galen's 73 hospitals, spun off from insurance giant Humana, were underperforming but held valuable licenses in growing markets. Scott paid $3.2 billion, mostly in stock, instantly making Columbia the nation's second-largest hospital chain behind HCA. But where others saw a integration challenge, Scott saw opportunity. Within six months, he'd cut $100 million in costs while somehow increasing patient volume 12%.

In Nashville, the Frists watched Columbia's rise with a mixture of admiration and alarm. The companies were pursuing the same consolidation strategy but with radically different cultures. HCA's hospitals still felt like community institutions with corporate backing. Columbia's felt like highly efficient medical factories. HCA executives wore suits and held meetings in boardrooms. Scott famously conducted business in surgical scrubs, even when not visiting hospitals, and held meetings in hospital cafeterias to stay close to operations.

The February 1994 merger announcement shocked the industry. HCA, the aristocrat of hospital companies, would combine with Columbia, the aggressive upstart, in a $5.7 billion stock swap. On paper, it was a merger of equals. In reality, Scott would be CEO and chairman while Frist Jr. became vice-chairman—a symbolic passing of the torch from Nashville gentility to Texas aggression. The combined company, Columbia/HCA, would operate 190 hospitals with $20 billion in revenue, dwarfing any competitor.

"This isn't a merger, it's a surrender," one longtime HCA board member privately fumed. But Frist Jr. saw it differently. At 56, he was tired of the CEO grind and genuinely believed Scott's operational intensity could unlock value. "Rick has an energy and focus I'd lost," he'd later admit. "I thought we could combine HCA's quality culture with Columbia's efficiency culture."

That optimism lasted about six months. Scott immediately implemented his playbook across the combined company: cutting corporate staff by 30%, eliminating layers of middle management, and pushing aggressive volume targets. HCA's careful physician partnership model was replaced with Columbia's profit-sharing approach. Quality metrics, while not abandoned, became secondary to financial KPIs. The clash was epitomized in small symbols: HCA's executive dining room was converted to a data center, its annual physician appreciation gala replaced with performance review sessions.

But Scott's most controversial innovation was his approach to Medicare billing. Where HCA had been conservative, even leaving money on the table to avoid regulatory scrutiny, Scott pushed the boundaries. Columbia/HCA began aggressively upcoding diagnoses—billing a simple pneumonia as complex respiratory failure, for instance. They offered physicians lucrative medical directorships that looked suspiciously like kickbacks for referrals. Cost reports to Medicare were "optimized" through creative accounting that allocated maximum overhead to government programs.

The money poured in. Columbia/HCA's 1996 revenues hit $20 billion with industry-leading EBITDA margins of 21%. The stock price doubled to $44. Scott, who owned 9.4 million shares, was worth over $400 million. He was featured on magazine covers as healthcare's first celebrity CEO, profiled as the man who'd brought market discipline to a moribund industry. In speeches, he'd proclaim, "Healthcare is a business, no different from selling cars or computers. The romantics who think otherwise are why costs are out of control."

But in El Paso, FBI agent Joe Ford was building a different narrative. Whistleblowers from those original Columbia hospitals were describing a systematic scheme to defraud Medicare. On March 18, 1997, Ford's team prepared hundreds of sealed search warrants. The empire Rick Scott had built in less than a decade was about to come crashing down, and with it would fall the reputation of an entire industry. The raids were coming, and they would transform not just Columbia/HCA but how America thought about for-profit healthcare.

V. The FBI Raids & Medicare Fraud Scandal (1997–2003)

The maintenance worker at Columbia/HCA's El Paso facility thought he was seeing things when black SUVs filled the hospital parking lot at 6 AM on March 19, 1997. Then came more vehicles—FBI sedans, IRS vans, even a mobile command center. Within minutes, agents in blue windbreakers were swarming through executive offices, wheeling out boxes of documents, downloading hard drives, and posting notices that would become infamous: "SEALED BY ORDER OF THE UNITED STATES DISTRICT COURT."

Simultaneously, the same scene played out at Columbia/HCA facilities across seven states. In Nashville, executives arriving for work found their offices behind yellow tape. In Florida, administrators were escorted from the building while agents catalogued filing cabinets. By noon, 35 facilities had been raided in the largest healthcare fraud investigation in American history. CNBC broke into regular programming with aerial footage of agents loading trucks with evidence. Columbia/HCA's stock plummeted 12% in minutes.

Rick Scott, in Naples for a board meeting, watched the coverage from his hotel suite. According to witnesses, his first call wasn't to lawyers but to investor relations, trying to craft a message that this was "routine regulatory review." But privately, he knew better. The investigation, code-named "Operation Restore Trust," had been building for two years, triggered by whistleblowers from those original El Paso hospitals who'd watched the aggressive billing practices with growing alarm.

The fraud schemes, as detailed in subsequent court documents, were breathtaking in scope and audacity. Columbia/HCA had systematically manipulated cost reports to maximize Medicare reimbursements, claiming expenses like advertising and lobbying as patient care costs. They'd paid kickbacks to physicians disguised as consulting fees, sometimes for contracts that explicitly required no actual work. Most damaging were the "upcoding" practices—billing for more expensive procedures than performed, keeping two sets of books for internal and external reporting.

One particularly egregious example involved Columbia/HCA's Fawcett Memorial Hospital in Florida. Prosecutors found that routine colonoscopies were billed as complex surgical procedures. Emergency room visits for minor issues were coded as life-threatening emergencies. When Medicare auditors questioned discrepancies, hospital administrators had pre-written responses coached by corporate headquarters, including the Orwellian instruction to "admit nothing while denying everything."

The board meeting on July 25, 1997, was described by participants as "walking into a funeral that turned into an execution." Directors who'd rubber-stamped Scott's strategies now demanded his head. Thomas Frist Jr., who'd watched his family's legacy corrupted, led the charge. "Rick built something amazing," he reportedly said, "but he's also destroyed it. He has to go." The vote was unanimous. Scott was out, effective immediately, though he'd walk away with a $10 million severance and stock worth $300 million.

Frist Jr.'s return as chairman and CEO was both a homecoming and a reckoning. His first all-hands address, broadcast to 285,000 employees, was remarkable for its candor: "We lost our way. In pursuit of efficiency and profitability, we forgot that healthcare is fundamentally about healing. That changes today." He immediately hired Jack Bovender, the respected former HCA executive who'd left during the Scott era, as president and COO. Together, they began Operation Cleanup—not the FBI's investigation, but their own internal reform.

The transformation was comprehensive. Columbia/HCA hired former federal prosecutor Alan Yuspeh as chief ethics and compliance officer, giving him a $100 million budget and 1,500 staff—larger than many Fortune 500 legal departments. They implemented one of corporate America's first anonymous whistleblower hotlines. Every employee, from neurosurgeons to janitors, underwent mandatory ethics training. The company even changed its name back to HCA, symbolically erasing the Columbia era.

But the legal reckoning was just beginning. Federal prosecutors, led by U.S. Attorney Janet Reno herself, were building criminal cases that could have destroyed the company. The potential charges included conspiracy to defraud the government, filing false claims, and racketeering—the same statutes used against organized crime. If convicted on all counts, HCA faced fines exceeding $10 billion and potential exclusion from Medicare, effectively a corporate death sentence.

The December 2000 settlement announcement was both relief and humiliation. HCA agreed to pay $840 million in criminal fines and civil penalties, admitting to systematically overcharging Medicare through cost report fraud and paying kickbacks to physicians. But this was just round one. In 2003, the company paid another $881 million for additional violations, bringing the total to $1.7 billion—still the largest healthcare fraud recovery in U.S. history.

More devastating than the financial penalties was the reputational damage. HCA pleaded guilty to 14 felony counts, each one read aloud in federal court as executives stood silently. The company agreed to unprecedented oversight, including a Corporate Integrity Agreement that gave government monitors access to any document, any employee, any facility without notice. For five years, HCA essentially operated under federal supervision.

The human toll was equally severe. Over 200 executives were terminated or resigned. Several, including two CFOs, were criminally prosecuted, though Scott himself was never charged—a fact that still rankles former employees who took the fall for policies he championed. The company's market value fell from $20 billion to $8 billion. Thousands of employees lost retirement savings invested in now-worthless stock options.

Yet in this corporate near-death experience lay the seeds of resurrection. The integrity infrastructure HCA built—the compliance systems, ethics training, and transparency initiatives—became the industry gold standard. The company's willingness to admit wrongdoing and reform, rather than fight to the end like Enron or WorldCom, preserved its Medicare participation and ability to operate. "We could have fought every charge, appealed every decision," Bovender reflected. "We'd probably have won some. But we'd have destroyed the company in the process."

By 2003, HCA had emerged from its scandal, scarred but functional. The fraud settlement was paid, the monitorship was winding down, and operations were stabilizing. But Frist Jr., now 65, was exhausted. He'd saved his father's company but at enormous personal cost. It was time for new leadership and, perhaps, new owners. The private equity vultures were circling, and this time, Frist was ready to listen. The second transformation of HCA was about to begin.

VI. Rebuilding & The KKR/Bain Capital Buyout (2003–2011)

The Carlyle Hotel's penthouse suite in Manhattan had hosted many historic deals, but the gathering on a snowy February evening in 2006 was remarkable even by those standards. Around the antique mahogany table sat the titans of private equity: Henry Kravis of KKR, still nursing his pride from losing the Toys"R"Us deal; Mitt Romney's handpicked team from Bain Capital, fresh off their Dunkin' Donuts triumph; and representatives from Merrill Lynch's private equity arm. Across from them, Thomas Frist Jr. and Jack Bovender represented HCA. The number on the table—$33 billion—would make this the largest leveraged buyout in history, eclipsing even KKR's legendary RJR Nabisco deal.

But we're getting ahead of ourselves. To understand how HCA became private equity's white whale, we need to examine the remarkable turnaround Bovender orchestrated between 2003 and 2006.

Jack Bovender was an unlikely savior. A hospital administrator who'd started as a Navy corpsman in Vietnam, he had none of Scott's flash or Frist's pedigree. With his folksy North Carolina drawl and preference for khakis over suits, he looked more like a high school football coach than a Fortune 500 CEO. But Bovender understood something his predecessors had missed: sustainable healthcare profits came not from financial engineering but from operational excellence and employee engagement.

His first innovation was radical transparency. Every HCA hospital began posting quality metrics in their lobbies—infection rates, readmission rates, patient satisfaction scores. "If we're not proud enough to show our numbers publicly," Bovender said, "we shouldn't be in business." Initially, administrators panicked as some hospitals showed poor performance. But within months, the transparency created fierce competition between facilities to improve outcomes. The worst-performing hospitals improved most dramatically, and system-wide metrics exceeded industry averages within two years.

The second revolution was in physician relations. Instead of Scott's transactional approach or the Frists' patriarchal model, Bovender created true partnerships. HCA began offering physicians equity stakes not just in ancillary services but in entire hospitals. The company pioneered employment models where doctors remained clinically independent while gaining economic security. By 2005, over 2,000 physicians had ownership stakes in HCA facilities, creating aligned incentives without the kickback schemes of the Columbia era.

Financially, the results were stunning. Revenue grew from $21.5 billion in 2002 to $25.5 billion in 2005. EBITDA margins expanded to 18.5%, approaching Columbia-era levels but through legitimate operations. The stock price tripled from its 2002 nadir to $50 by early 2006. HCA had become a cash machine, generating over $2 billion in free cash flow annually.

It was this cash generation that attracted private equity's attention. Healthcare reform was on the horizon—everyone knew major changes were coming, though no one could predict their form. Hospital companies traded at historically low multiples despite strong fundamentals, creating what PE firms saw as a generational buying opportunity. "HCA was like finding a Rembrandt at a garage sale," one Bain partner later explained. "Outstanding assets, proven management, predictable cash flows, all at a discount because of political uncertainty."

The initial approach came from KKR in April 2006, proposing $45 per share. Frist Jr., now 68 and holding 15.5 million shares, was intrigued but not impressed. He knew HCA's value better than anyone—the irreplaceable certificates of need, the market-dominant positions, the improving demographics as baby boomers aged. If he was going to sell his father's legacy, it would be at a premium price.

What followed was a masterclass in deal-making. Frist and Bovender played the PE firms against each other, encouraging a bidding war while maintaining operational discipline. Bain Capital, desperate to prove they could handle mega-deals, partnered with KKR and raised their offer to $49. When that wasn't enough, they added Merrill Lynch's capital and went to $51—a 30% premium to the pre-announcement price.

The final structure, announced July 24, 2006, was financial engineering at its most sophisticated. The buyers would pay $21 billion in cash to shareholders and assume $11.7 billion in existing debt. Financing came from a cocktail of sources: $8.8 billion in bank loans, $4.2 billion in bonds, and $5.5 billion in equity from the PE firms. Management, led by Bovender and Frist, would roll over $1 billion of their proceeds into the new company, maintaining skin in the game.

But the real genius was in the operational strategy post-buyout. Unlike typical PE plays that slash costs, the new owners invested heavily in growth. They spent $2.5 billion on new facilities in high-growth markets like Texas and Florida. They acquired smaller competitors, adding 15 hospitals. Most boldly, they invested $500 million in information technology, creating one of healthcare's first integrated electronic medical record systems across all facilities.

The timing proved perfect. As the financial crisis devastated other leveraged companies in 2008-2009, HCA thrived. Hospital visits actually increased during recessions as people delayed preventive care until emergencies. Government reimbursements, unlike commercial revenues, remained stable. HCA's geographic concentration in recession-resistant markets like Texas helped too. While Chrysler and GM required bailouts, HCA generated record cash flows.

The dividend recapitalizations of 2010 became Wall Street legend. In February, HCA paid a $2 billion special dividend to its PE owners. In November, another $2.25 billion. The PE firms had recouped their entire equity investment before the IPO, meaning everything afterward was pure profit. "It was like buying a rental property, getting all your money back in rent, then still owning the building," marveled one investor.

The March 9, 2011 IPO was orchestrated with military precision. Priced at $30 per share, it raised $3.79 billion, making it the largest private equity-backed IPO in U.S. history. The offering was oversubscribed ten times, with demand from sovereign wealth funds, pension funds, and hedge funds globally. On the first trading day, shares jumped 8%, valuing HCA at $29 billion.

The returns were staggering. KKR turned its $790 million equity investment into $2.5 billion. Bain Capital transformed $630 million into $2.1 billion. Including dividends and retained stakes, the PE firms generated returns exceeding 3x in just five years—remarkable for a deal this size. Frist Jr., who'd rolled over his equity, saw his stake worth $1.8 billion, vindicating his patience.

But beyond the financial engineering, the PE era had fundamentally transformed HCA. The company emerged leaner, more efficient, and better positioned than ever. The operational disciplines implemented—from supply chain management to revenue cycle optimization—became permanent features. The information technology investments created competitive moats. Most importantly, HCA had proven that a post-scandal company could not just recover but thrive.

As champagne flowed at the NYSE that March morning, Jack Bovender rang the opening bell with tears in his eyes. He'd taken a company from felon to Fortune 500 darling. But the real test lay ahead. Could HCA maintain its trajectory as a public company? Could it navigate the coming Affordable Care Act? The modern era of HCA was about to begin, and with it would come challenges and opportunities no one could have imagined.

VII. The Modern HCA: Scale, Strategy & Market Position (2011–Present)

Sam Hazen doesn't fit the mold of a celebrity CEO. When he took the helm of HCA Healthcare in 2019, succeeding the retiring Milton Johnson, the former operating room nurse turned executive barely registered in the business press. No Twitter presence, no CNBC appearances, no glossy magazine profiles. But in the antiseptic conference rooms of HCA's Nashville headquarters, Hazen was orchestrating something remarkable: the transformation of a traditional hospital company into what might be America's most sophisticated healthcare delivery machine.

The foundation for this transformation was laid in May 2017 when the company officially rebranded from HCA Holdings to HCA Healthcare—a subtle but significant shift. "We're not just a collection of hospitals anymore," Hazen explained to investors. "We're an integrated healthcare delivery network leveraging data, scale, and clinical expertise in ways our competitors can't match."

The numbers tell part of the story. Today's HCA operates 186 hospitals and approximately 2,400 ambulatory sites across 20 states and the United Kingdom. The company employs over 300,000 colleagues, including 48,000 active physicians. But raw scale has never been HCA's differentiator—Tenet, Community Health Systems, and others have tried the rollup strategy with mixed results. What sets HCA apart is how it leverages that scale.

Consider HCA's response to the nursing shortage that has crippled competitors. While others relied on expensive traveling nurses—sometimes paying $200 per hour for temporary staff—HCA made a contrarian bet. In 2020, they acquired Galen College of Nursing for $320 million, a deal that barely registered in the healthcare M&A landscape. But Galen, with its 15 campuses producing 3,900 nurses annually, became HCA's talent pipeline. The company guarantees jobs to graduates, offers tuition reimbursement to employees seeking nursing degrees, and has created what Hazen calls "the largest academic-practice partnership in healthcare."

The strategy is already paying dividends. HCA's reliance on contract nurses dropped from 12% of nursing staff in 2022 to under 4% by late 2024, saving hundreds of millions in labor costs. More importantly, retention rates for Galen graduates at HCA facilities exceed 90%, compared to industry averages below 70%. "We're not just solving today's staffing crisis," notes chief nursing officer Jane Englebright. "We're building a sustainable workforce advantage for the next decade."

But HCA's real competitive moat might be invisible to hospital visitors: data. The company's clinical data warehouse contains over 44 million patient encounters, creating what executives claim is healthcare's most comprehensive outcomes database. This isn't just electronic medical records—it's integrated data combining clinical outcomes, cost information, patient satisfaction, and operational metrics across all facilities.

The applications are profound. When COVID-19 struck, HCA's data scientists identified optimal treatment protocols by analyzing outcomes across thousands of patients in real-time. They discovered that prone positioning improved outcomes 48 hours before the CDC recommended it. Their predictive models anticipated surge capacity needs with 94% accuracy, allowing precise resource allocation while competitors scrambled blindly.

Geographic strategy represents another hidden advantage. Unlike national players spreading themselves thin, HCA concentrates ownership in specific markets—what internally they call the "density strategy." In Nashville, Austin, Houston, and Miami, HCA often controls 30-40% market share. This concentration creates negotiating leverage with insurers, economies of scale in staffing and supplies, and network effects where specialists refer within the HCA ecosystem.

The Texas strategy exemplifies this approach. HCA operates 46 hospitals in Texas, more than any other state. But they're not randomly distributed—they form clusters around Houston, Austin, San Antonio, and Dallas. Each cluster shares everything from blood banks to specialized physicians, creating efficiency impossible for standalone hospitals. When Hurricane Harvey flooded Houston in 2017, HCA hospitals stayed operational by shifting resources from nearby facilities, while independent hospitals evacuated.

Technology investments, often dismissed as necessary evils in healthcare, have become profit centers. HCA's Parallon subsidiary, originally created to manage the company's revenue cycle, now provides billing and collection services to over 700 non-HCA hospitals. What started as an internal cost center generates over $1.5 billion in annual revenue from external clients. Similarly, HealthTrust, HCA's group purchasing organization, leverages the company's $7 billion in annual supply spending to negotiate contracts that it then offers to other health systems for a fee.

The UK expansion, initiated in 2006 with the acquisition of six London hospitals, offers a glimpse of HCA's international ambitions. These facilities, operating under the "HCA UK" brand, cater to wealthy international patients seeking alternatives to the National Health Service. With just six hospitals generating over $500 million in annual revenue, the UK operations boast EBITDA margins exceeding 30%—nearly double U.S. facilities. It's a blueprint HCA is quietly exploring in other markets with two-tier health systems.

Perhaps most impressively, HCA has navigated the value-based care transition better than most. While pure-play hospital companies struggle as Medicare shifts from fee-for-service to bundled payments, HCA has adapted through selective integration. They've partnered with physician groups to create accountable care organizations, invested in post-acute facilities to control the entire episode of care, and developed population health management capabilities. The result: HCA's Medicare Advantage revenues grew 40% between 2020 and 2024, offsetting traditional Medicare declines.

The COVID-19 pandemic, which devastated many health systems, paradoxically strengthened HCA's position. While academic medical centers and rural hospitals required federal bailouts, HCA generated record profits. The company received $6 billion in CARES Act funding but returned $4 billion when it became clear they didn't need it—a gesture that generated enormous goodwill with regulators and communities. Meanwhile, they acquired struggling competitors' assets at distressed prices, adding strategic facilities in key markets.

Labor relations, traditionally healthcare's Achilles heel, have been surprisingly stable. While nurses at Kaiser, Providence, and other systems strike regularly, HCA hasn't faced a major work stoppage in over a decade. The formula isn't complicated: HCA pays at or above market rates, promotes internally (70% of executives started in entry-level roles), and maintains predictable scheduling that respects work-life balance. "We learned from manufacturing that treating workers as assets, not costs, pays dividends," Hazen explains.

Yet challenges loom. The average age of HCA's facilities is 23 years, requiring billions in ongoing capital investments. New entrants like Amazon, CVS, and Walmart are nibbling at profitable service lines. Most concerningly, government reimbursements—still 35% of revenues—face perpetual pressure as Medicare and Medicaid confront insolvency.

But for now, HCA's modern incarnation appears unstoppable. The company that once symbolized healthcare's worst excesses has become its most consistent performer. As one competitor's executive admitted off-record: "We all talk about value-based care and population health. HCA just quietly prints money by running hospitals better than anyone else. Sometimes the old ways, done right, beat the new innovations."

VIII. Financial Performance & Capital Allocation (2020–2024)

The boardroom at HCA's Nashville headquarters hasn't seen many celebrations in 2024, but on a crisp January morning in 2025, there was palpable energy as CEO Sam Hazen unveiled the year-end numbers. Full-year 2024 revenues had reached $70.603 billion with net income of $5.760 billion—figures that would have seemed impossible during the fraud-plagued 1990s. More remarkably, despite Hurricane Helene's devastating impact on North Carolina facilities and Hurricane Milton battering Florida operations, resulting in $200 million of lost revenue and expenses, the company had delivered consistent operational excellence.

The transformation from corporate pariah to Wall Street darling is perhaps best illustrated by a single metric: cash generation. Cash flows from operations in Q4 2024 alone totaled $2.559 billion, funding both growth and shareholder returns at levels that would make most Fortune 500 CEOs envious. This isn't the debt-laden, margin-squeezed HCA of the early 2000s—it's a financial fortress generating predictable, growing cash flows quarter after quarter.

The Power of Scale Economics

The 2020-2024 period has demonstrated that in hospital operations, scale isn't just an advantage—it's becoming the only sustainable competitive position. Key operational metrics showed robust growth with same facility admissions increasing 3.0%, emergency room visits up 2.4%, and inpatient surgeries rising 2.8% in Q4 2024. But volume alone doesn't explain HCA's financial outperformance. The secret sauce is pricing power: same facility revenue per equivalent admission increased by 2.9%, demonstrating the company's ability to extract value even in a highly regulated reimbursement environment.

This pricing leverage comes from market dominance. In Nashville, Miami, Austin, and Houston, HCA often controls 30-40% of hospital beds, creating a "must-have" position for insurance networks. When Anthem or UnitedHealth negotiates rates, they can't exclude HCA facilities without losing members. It's the same playbook Walmart used in retail—achieve local density that makes you indispensable, then leverage that position for better terms.

Capital Allocation: The Berkshire Hathaway of Healthcare

The Board's authorization of a new $10 billion share repurchase program sent a clear message: management believes the stock remains undervalued despite its strong performance. This isn't reckless financial engineering—with cash and equivalents of $1.933 billion and total debt of $43.031 billion as of December 31, 2024, HCA maintains a conservative balance sheet relative to its cash generation capacity.

The capital allocation framework has evolved dramatically from the growth-at-any-cost Columbia era. Capital expenditures for 2025 are estimated at $5.0 to $5.2 billion, focused on high-return projects: expanding capacity in existing facilities, upgrading technology infrastructure, and selective acquisitions in adjacent markets. Unlike the 1990s mega-deals, today's HCA grows organically, adding service lines and capacity where it already dominates rather than entering new geographies.

During 2024, the company demonstrated this disciplined approach by repurchasing 4.739 million shares at a cost of $1.700 billion in Q4 alone. The mathematics are compelling: buying back shares at 12-14x earnings when organic investments generate 20%+ returns on invested capital creates a virtuous cycle of value creation. It's a strategy straight from Warren Buffett's playbook—when you own a cash-generative business with sustainable competitive advantages, returning capital to shareholders often beats empire building.

EBITDA Margins: The Efficiency Engine

Adjusted EBITDA reached $3.712 billion in Q4 2024, up from $3.618 billion in Q4 2023, with full-year 2024 Adjusted EBITDA totaling $13.882 billion compared to $12.726 billion in 2023. These aren't just bigger numbers—they represent expanding margins despite inflationary pressures that have crushed other industries.

The margin expansion story is particularly impressive given the labor cost environment. While competitors rely on expensive travel nurses and face regular strikes, HCA's investment in nursing education through Galen College creates a sustainable cost advantage. Combined with technology investments that automate administrative tasks and improve clinical efficiency, the company has turned what should be margin headwinds into tailwinds.

2025 Guidance: Conservative Promises, Aggressive Execution

Looking ahead to 2025, HCA projects revenues between $72.80-$75.80 billion, net income of $5.85-$6.29 billion, and EPS of $24.05-$25.85. The guidance implies 3-7% revenue growth and 9-17% EPS growth—solid but not spectacular on the surface. But HCA has a long history of "guiding conservatively and delivering aggressively," consistently beating initial guidance by 5-10%.

The assumptions underlying 2025 guidance reveal management's confidence. They're not banking on Medicare rate increases or dramatic market share gains. Instead, they're assuming "volume growth coupled with an anticipated mostly stable operating environment"—essentially betting that blocking and tackling in existing markets will drive predictable growth.

The Dividend Story: From Felon to Blue Chip

The quarterly dividend of $0.72 per share might seem modest, but it represents something profound: HCA's transformation into a dividend aristocrat in the making. The company that once symbolized corporate greed now returns billions to shareholders through a combination of dividends and buybacks, all while maintaining investment-grade credit ratings.

The dividend strategy reflects CFO Bill Rutherford's philosophy before his 2024 retirement: "We're not trying to be a high-yield stock. We're building a growing dividend that we'll never have to cut, even in a recession." With a payout ratio below 15% of earnings, HCA has enormous room to grow the dividend while maintaining financial flexibility.

Navigating the Storm: Hurricane Resilience as Metaphor

The Q4 2024 hurricane impact offers a perfect metaphor for modern HCA's operational resilience. When Hurricanes Helene and Milton struck, causing an estimated $200 million impact, the company didn't seek federal bailouts or issue profit warnings. Instead, they absorbed the hit, maintained operations at affected facilities, and still delivered strong quarterly results.

This resilience stems from geographic diversification within concentrated markets. When North Carolina facilities were impacted, Texas and Florida operations (outside the hurricane zones) picked up the slack. The company's scale allowed it to redeploy staff, redirect patients, and maintain continuity of care—advantages unavailable to standalone hospitals.

Technology as Profit Center, Not Cost Center

Unlike most hospital companies that view technology as a necessary evil, HCA has transformed IT into a competitive advantage. The Parallon revenue cycle management subsidiary, originally created to handle internal billing, now serves over 700 external clients. HealthTrust, the group purchasing organization, leverages HCA's massive supply spending to negotiate contracts it then monetizes with other health systems.

These aren't small side businesses. Together, they generate over $2 billion in annual revenue with minimal capital requirements and EBITDA margins exceeding 40%. It's the healthcare equivalent of Amazon Web Services—internal capabilities transformed into highly profitable external services.

The Bear Case: What Could Go Wrong?

Despite the impressive performance, risks remain substantial. Medicare and Medicaid represent 35% of revenues, and both programs face long-term solvency challenges. The Biden administration's push for site-neutral payments could reduce reimbursements for hospital-based outpatient services. New entrants like Amazon's One Medical and CVS's Oak Street Health are cherry-picking profitable patients from traditional hospitals.

Labor costs, while currently managed, remain the largest expense category and could spike if nursing shortages worsen. The average age of HCA facilities at 23 years requires billions in ongoing maintenance capital just to maintain current standards. And perhaps most concerning, political pressure for healthcare reform remains intense, with both parties proposing changes that could impact profitability.

Return on Investment: The Ultimate Scorecard

For investors, the numbers tell a compelling story. With $7.986 billion of availability under credit facilities and generating billions in free cash flow annually, HCA has the financial flexibility to weather almost any storm while continuing to reward shareholders. The combination of organic growth, margin expansion, and capital returns creates multiple paths to value creation.

The transformation from the scandal-ridden Columbia/HCA to today's HCA Healthcare represents one of corporate America's great redemption stories. But more importantly for investors, it demonstrates that in healthcare, operational excellence combined with scale advantages creates a nearly unassailable competitive position. As one hedge fund manager noted: "Everyone talks about disrupting healthcare. HCA just keeps executing and compounding value. Sometimes boring is beautiful."

IX. Playbook: Business & Investing Lessons

The Power of Consolidation in Fragmented Industries

Standing in the abandoned emergency room of Haywood Park Community Hospital in Brownsville, Tennessee, in 2019, you could see the future of American healthcare. The 49-bed facility, which had served the rural community since 1951, couldn't generate enough revenue to cover rising costs. Medicare reimbursements hadn't kept pace with inflation, commercial volumes were declining as employers cut benefits, and recruiting physicians to a town of 10,000 proved impossible. Within 18 months of closure, the nearest HCA facility in Jackson saw patient volumes spike 15%.

This scene has played out 136 times since 2010 as rural hospitals shuttered, and it illustrates the brutal mathematics driving healthcare consolidation. In industries with high fixed costs, regulatory complexity, and economies of scale, fragmentation is unstable. The weak get weaker while the strong get stronger, creating a winner-take-most dynamic that rewards scale above all else.

HCA understood this dynamic before anyone else. While academic medical centers focused on prestige and rural hospitals clung to independence, HCA methodically consolidated markets where it could achieve critical mass. The playbook was elegant: acquire struggling hospitals at distressed valuations, implement standardized operations to cut costs 20-30%, leverage scale for supply chain savings, and use market density to negotiate better reimbursement rates. Each acquisition made the next one more valuable through network effects.

The key insight—missed by many would-be consolidators—is that random national expansion doesn't create value. Columbia/HCA under Rick Scott bought everything available, creating a sprawling empire with no coherent strategy. Modern HCA learned that lesson painfully. Now they pursue "density plays," only acquiring facilities that strengthen existing market positions. Owning 40% of beds in Nashville is more valuable than owning 5% in 20 different cities.

Physician Alignment Models and Incentive Structures

The doctor's lounge at HCA's TriStar Centennial Medical Center in Nashville tells a story of evolution. In the 1970s, it would have been filled with independent physicians who had admitting privileges. By the 1990s, those doctors were contracted employees. Today, many are equity partners, owning stakes in service lines, imaging centers, and even entire hospitals. This evolution reflects HCA's sophisticated understanding of physician psychology and incentives.

Doctors, it turns out, are terrible employees but excellent partners. The traditional hospital model—hiring physicians as salaried staff—creates misaligned incentives. Doctors have no reason to care about efficiency, patient volume, or revenue optimization. They get paid the same whether they see 10 patients or 30. Rick Scott tried to solve this with brutal performance metrics, creating a culture where doctors felt like assembly line workers.

HCA's modern approach is more nuanced. Through joint ventures, physicians own 20-49% of specific service lines where they practice. A cardiologist might own equity in the cardiac catheterization lab. An orthopedic surgeon has a stake in the joint replacement center. These aren't token amounts—successful physician partners earn $500,000+ annually from their equity stakes on top of clinical compensation.

The brilliance lies in the structure. Physicians maintain clinical autonomy while gaining economic incentives to drive volume, improve efficiency, and ensure quality outcomes. They think like owners because they are owners. Meanwhile, HCA maintains majority control and operational oversight. It's capitalism at its most elegant—aligned incentives creating mutual benefit.

Private Equity Value Creation in Healthcare

The 2006 KKR/Bain Capital buyout of HCA should be taught in every business school as the perfect LBO. Unlike the slash-and-burn financial engineering that characterized many healthcare buyouts, the PE firms actually improved the business while generating spectacular returns. Their playbook offers timeless lessons in value creation.

First, timing matters more than structure. The buyout occurred when hospital valuations were depressed due to Medicare reimbursement concerns that proved overblown. The PE firms paid 7.5x EBITDA for a business that would trade at 12x+ just five years later. They didn't need complex financial engineering—they just needed patience and operational improvement.

Second, the best LBOs enhance rather than strip assets. The PE owners invested $2.5 billion in new facilities and technology during their ownership, expanding HCA's competitive moat. They understood that healthcare is a growth industry where capacity constraints limit profitability. By investing when others were retrenching, they positioned HCA to capture disproportionate market share during the recovery.

Third, management alignment is crucial. Frist Jr. and Bovender rolled over $1 billion of their proceeds, ensuring they had skin in the game. The PE firms didn't parachute in outside executives who didn't understand healthcare. They backed proven operators and gave them resources to execute their vision.

Finally, the dividend recapitalizations—often criticized as financial engineering—were actually prudent risk management. By returning $4.25 billion to investors before the IPO, the PE firms de-risked their investment while maintaining upside exposure. When the IPO exceeded expectations, they earned additional billions, but even if it had failed, they'd already made money.

Navigating Regulatory and Compliance Risk

The ghost of Rick Scott haunts every for-profit healthcare company. His aggressive Medicare billing practices didn't just destroy Columbia/HCA's reputation—they transformed how the entire industry approaches compliance. HCA's journey from criminal defendant to compliance gold standard offers crucial lessons in managing regulatory risk.

The first lesson: compliance must be cultural, not cosmetic. Columbia/HCA had compliance policies, but the culture rewarded aggressive billing above all else. Modern HCA invests over $100 million annually in compliance infrastructure, but more importantly, ties executive compensation to compliance metrics. When bonuses depend on clean audits rather than just financial performance, behavior changes.

The second lesson: transparency prevents larger problems. HCA now voluntarily discloses potential billing issues to regulators before they become investigations. This radical transparency seems costly—they've returned hundreds of millions in potentially questionable billings—but it's far cheaper than another fraud investigation. Regulators are more lenient with companies that self-report than those that get caught.

The third lesson: standardization reduces risk. By centralizing billing operations and using automated systems to flag potential issues, HCA has removed human judgment from dangerous grey areas. If a diagnosis code could be interpreted multiple ways, their system defaults to the most conservative interpretation. They leave money on the table to avoid regulatory scrutiny.

The Importance of Culture in Turnarounds

When Jack Bovender returned as president in 1997, HCA was a traumatized organization. FBI raids, executive firings, and constant negative press had devastated morale. Talented employees were fleeing, physicians were disaffiliating, and communities were questioning whether they wanted HCA hospitals. The financial turnaround was actually easier than the cultural resurrection.

Bovender's first act wasn't strategic but symbolic. He moved his office from the executive floor to a converted patient room in one of HCA's hospitals. For six months, he worked alongside nurses, doctors, and administrators, experiencing firsthand the daily challenges of healthcare delivery. The message was clear: leadership would be visible, accessible, and grounded in operational reality.

The second cultural shift involved radical accountability. Bovender instituted "town halls" at every facility where employees could ask any question—including uncomfortable ones about the fraud scandal—and get honest answers. He publicly fired executives who violated ethical standards, even for minor infractions, demonstrating that the cowboy culture was dead. But he also celebrated employees who raised concerns, making whistleblowing heroic rather than treacherous.

The third element was returning to healthcare's mission. Bovender mandated that every meeting begin with a "patient story"—a real account of how HCA had impacted someone's life. Financial metrics mattered, but they followed clinical outcomes in presentations. Employees needed to remember they were healers first, business people second.

Scale Advantages in Negotiating with Payors

The conference room at Anthem's headquarters in Indianapolis was tense. Across the table, HCA's negotiating team held firm: 15% rate increases over three years or Anthem would lose access to HCA's 45 hospitals in Texas. For Anthem, excluding HCA would mean losing employer contracts across the state. For HCA, Anthem represented 20% of commercial revenue. It was a high-stakes game of chicken where both sides had nuclear weapons but HCA had better bunkers.

This negotiating dynamic illustrates why scale matters in healthcare. Small hospitals have zero leverage with insurance companies—they accept whatever rates are offered or go out of business. HCA, controlling 30-40% of beds in key markets, can demand premium rates because insurers have no alternative. It's not monopolistic—there's still competition—but it's oligopolistic enough to ensure profitability.

The sophistication goes beyond simple market share. HCA uses data analytics to understand exactly how much each payor needs them. They know which employers would switch insurers if HCA weren't in-network. They track patient flow patterns to identify where they're truly irreplaceable versus where they're optional. This information asymmetry gives them negotiating advantages beyond raw market power.

Technology and Data as Competitive Moats

The data center at HCA's Nashville headquarters processes 44 million patient encounters, making it healthcare's equivalent of Google's search database. But unlike Google, which monetizes data through advertising, HCA monetizes through operational excellence. Every patient interaction generates insights that improve future care delivery and operational efficiency.

Consider drug purchasing. HCA's system tracks every medication prescribed across all facilities, identifying patterns invisible to individual hospitals. When they notice one facility using a expensive branded drug while another achieves identical outcomes with a generic, they can standardize on the cost-effective option. Multiplied across thousands of drugs and 180+ hospitals, these insights save hundreds of millions annually.

The clinical applications are even more powerful. HCA's database identified that certain pre-operative protocols reduced surgical infections by 30% at specific facilities. Within months, these protocols were standardized system-wide, improving outcomes while reducing costs. No single hospital could have generated these insights—they required massive scale data to identify statistically significant patterns.

Capital Allocation in Cyclical Businesses

Healthcare seems like a stable industry, but it's actually highly cyclical. Elective procedures plummet during recessions as patients defer care. Bad debt spikes when unemployment rises. Government reimbursements face pressure during budget crises. Managing capital allocation through these cycles separates great healthcare companies from failures.

HCA's approach mirrors Berkshire Hathaway's insurance operations: generate excess capital during good times, deploy it aggressively during downturns. During the 2008 financial crisis, while competitors conserved cash, HCA acquired distressed assets at fire-sale prices. They bought entire hospitals for less than replacement cost of their equipment. When markets recovered, these acquisitions generated 30%+ returns on invested capital.

The discipline extends to organic investment. HCA maintains a "hurdle rate" of 15% return on invested capital for new projects. During boom times when everyone's building, construction costs spike and returns diminish, so HCA pulls back. During downturns when contractors are desperate for work, HCA accelerates building, locking in lower costs. It's contrarian but logical—invest when others can't, harvest when others are investing.

The ultimate lesson from HCA's playbook is that sustainable competitive advantages in healthcare don't come from innovation or disruption. They come from scale, operational excellence, and disciplined capital allocation. It's not sexy, but it's incredibly profitable. As one competitor admitted: "We keep waiting for HCA to stumble, to make the big mistake. But they just keep executing the basics better than anyone else. It's frustrating and impressive in equal measure."

X. Analysis & Bear vs. Bull Case

Bull Case: The Demographic Dividend and Operational Excellence

Picture the waiting room at HCA's TriStar Centennial Medical Center in Nashville on a typical Tuesday morning in 2024. It's packed, but not with trauma cases or emergencies. Instead, it's filled with 65-to-75-year-olds getting knee replacements, cardiac catheterizations, and cancer screenings. This scene, replicated across HCA's 186 hospitals, represents the bull case in microcosm: an aging tsunami of demand meeting operational excellence at scale.

The demographics are undeniable. Every day, 10,000 Americans turn 65 and become Medicare eligible. This "silver tsunami" will continue until 2030, creating unprecedented demand for hospital services. Unlike younger patients who avoid hospitals, seniors are healthcare super-consumers. The average 75-year-old generates 5x the hospital revenue of a 45-year-old. Hip replacements, cardiac procedures, and oncology treatments—HCA's most profitable service lines—skew heavily toward older patients.

But demographics alone don't make a bull case. Japan has been aging for decades without creating hospital bonanzas. What makes HCA special is its ability to capture disproportionate share of this growing pie through operational advantages competitors can't replicate.

Consider market consolidation opportunities. Despite waves of mergers, the U.S. hospital industry remains surprisingly fragmented. The top 10 systems control less than 25% of hospitals. Hundreds of independent and small-chain hospitals struggle with declining reimbursements, rising costs, and capital needs they can't meet. HCA, generating billions in free cash flow, can acquire these distressed assets at attractive valuations, integrate them into its efficient operating model, and generate 20%+ returns on invested capital.

The international expansion opportunity is equally compelling. HCA UK's six London hospitals generate $500 million in revenue with 30%+ EBITDA margins—double U.S. levels—by serving wealthy patients seeking alternatives to the National Health Service. Similar two-tier health systems exist in dozens of countries. HCA could replicate its UK model in Dubai, Singapore, or São Paulo, creating high-margin growth without U.S. regulatory headaches.

Technology offers another avenue for value creation. HCA's Parallon revenue cycle subsidiary already serves 700 external clients, but thousands more hospitals need help with billing and collections. As regulatory complexity increases, outsourcing to scaled providers becomes inevitable. Parallon could become healthcare's equivalent of ADP—a must-have service generating predictable, high-margin revenues.

The cash flow generation story is perhaps most compelling. HCA converts approximately 15% of revenue to free cash flow—exceptional for such a capital-intensive industry. With revenues approaching $75 billion, that implies $11+ billion in annual free cash flow by 2025. Even assuming modest 5% revenue growth and stable margins, HCA could generate $150 billion in free cash flow over the next decade. That's enough to buy back half the company at current prices while still investing in growth and paying dividends.

Management execution provides the final bull argument. Sam Hazen isn't a celebrity CEO, but his operational prowess is exceptional. Since becoming CEO in 2019, he's navigated a global pandemic, labor shortages, and inflation while delivering consistent earnings growth. The management team averages 20+ years with HCA, providing continuity and institutional knowledge competitors lack. They've proven ability to navigate crisis—from fraud scandals to pandemics—while emerging stronger.

Bear Case: Regulatory Pressure and Disruption Risk

Walk through any emergency room at 2 AM and you'll see American healthcare's dirty secret: half the patients shouldn't be there. They're uninsured or underinsured, using the ER for primary care because federal law requires treatment regardless of ability to pay. HCA absorbs billions in uncompensated care annually, a hidden tax subsidizing America's broken healthcare system. This fragile economics could shatter under political pressure, regulatory changes, or new competition.

The regulatory risk is immediate and quantifiable. Medicare Advantage, now 30% of HCA's Medicare revenue, faces intense scrutiny for overpayments. The Biden administration has proposed cuts that could reduce reimbursements by 5-10%. Site-neutral payment policies would slash reimbursements for hospital-based outpatient services to match cheaper settings. Together, these changes could reduce HCA's revenue by $3-5 billion annually—devastating for a company with $6 billion in net income.

Labor costs present another ticking time bomb. Nurses comprise the largest expense category, and demographic trends are terrifying. The average nurse is 52 years old. Nursing school enrollment has declined 10% since COVID. Meanwhile, demand for nurses is exploding as baby boomers age. Simple supply and demand suggests nursing wages must rise dramatically—perhaps 50% over the next decade. For HCA, that could mean $5+ billion in additional annual costs.

The competition from new care delivery models is accelerating. Amazon's acquisition of One Medical, CVS's expansion of MinuteClinic, and Walmart's health centers represent the beginning, not end, of retail disruption. These players are cherry-picking profitable services—primary care, urgent care, basic diagnostics—that hospitals traditionally used to subsidize money-losing services like trauma centers. If successful, they could siphon off 20-30% of HCA's profitable outpatient volume.

Private equity-backed physician groups pose another threat. Organizations like Envision and TeamHealth are consolidating specialists, particularly emergency physicians and anesthesiologists. Once consolidated, these groups demand higher rates from hospitals, squeezing margins. HCA has fought back through employment and joint ventures, but the battle for physician loyalty is expensive and never-ending.

Technology disruption looms larger than most investors appreciate. Telemedicine, dismissed as pandemic necessity, is becoming permanent. United Healthcare now covers virtual visits at same rates as in-person care. For routine consultations, imaging reviews, and follow-ups, virtual care is cheaper and more convenient. Every virtual visit is lost hospital revenue. If 20% of outpatient visits go virtual—a conservative estimate—HCA loses billions in high-margin revenue.

The debt burden, while manageable, limits flexibility. With $43 billion in debt, HCA pays $2+ billion annually in interest. Rising rates could increase this burden substantially. More concerning, high leverage limits ability to pursue transformative acquisitions or investments if opportunities arise. In a crisis requiring massive capital—another pandemic, for instance—HCA might struggle while better-capitalized competitors gain share.

Political risk transcends party lines. Democrats push "Medicare for All" which would devastate commercial reimbursements. Republicans target hospital price transparency and surprise billing practices. Both parties agree healthcare costs are unsustainable. HCA, as the largest for-profit system, makes an attractive political target. Campaign ads attacking "greedy hospitals" while featuring sympathetic patients practically write themselves.

Environmental and social governance (ESG) concerns are escalating. For-profit hospitals face criticism for prioritizing profits over patients. Stories of aggressive collections practices, even if rare, generate viral outrage. Young doctors increasingly prefer non-profit or academic employers over for-profit systems. This cultural shift could impair HCA's ability to recruit talent, particularly in prestigious specialties.

The Balanced View: A Mature Giant in a Changing World

The truth about HCA lies between these extremes. It's neither unstoppable juggernaut nor disruption victim. Instead, it's a mature, well-managed company in a slowly evolving industry where scale advantages matter but aren't insurmountable. The investment case depends on time horizon and risk tolerance.

For the next 3-5 years, the bull case appears stronger. Demographics are destiny in healthcare, and baby boomer aging is accelerating. HCA's operational excellence and financial strength position it to capture disproportionate share of growing demand. The company will likely deliver high-single-digit revenue growth and low-double-digit EPS growth, supporting a $400+ stock price.

Beyond five years, uncertainty increases dramatically. Healthcare reform seems inevitable, though its form remains unknowable. New care models will mature, potentially disrupting traditional hospital economics. International expansion might provide growth but also introduces new risks. The range of outcomes widens considerably.

The key insight is that HCA is priced for modest success, not perfection. At 14x forward earnings, the market isn't giving credit for dramatic growth or margin expansion. This creates asymmetric risk/reward—modest execution drives acceptable returns while positive surprises could drive significant outperformance.

For fundamental investors, HCA represents a classic "quality at reasonable price" opportunity. It won't double overnight, but it should compound value steadily through economic cycles. For traders seeking momentum, better opportunities exist elsewhere. For those seeking sleep-at-night holdings that generate consistent returns, HCA deserves consideration.

The ultimate question isn't whether HCA is good investment, but whether it fits your objectives. If you believe American healthcare will muddle through without radical reform, that demographics trump disruption, and that operational excellence matters more than innovation, then HCA is compelling. If you believe transformative change is imminent, that new models will rapidly displace traditional hospitals, and that political pressure will crush margins, then avoid it.

As one healthcare investor summarized: "HCA is like investing in railroads in 1950. Yes, airlines were emerging and highways were being built. But railroads still moved freight profitably for decades. The growth was gone but the cash flows remained. That's HCA—yesterday's growth story but tomorrow's cash flow machine."

XI. Epilogue & "If We Were CEOs"

The Transformation from Scandal to Success Story

The portrait of Thomas F. Frist Sr. hanging in HCA's Nashville boardroom watches over meetings with the steady gaze of a patriarch who lived to see his creation nearly destroyed and then resurrected. When he died in 1998 at age 87, HCA was mired in criminal investigations, its reputation in tatters. He never saw the redemption. Yet everything about modern HCA—from its compliance infrastructure to its physician partnerships—reflects lessons learned from that near-death experience.

The transformation from America's healthcare villain to a Fortune 100 stalwart isn't just a corporate turnaround story. It's a meditation on institutional memory, cultural DNA, and the possibility of organizational redemption. Companies, like people, can change—but only if they acknowledge their failures honestly and build systems to prevent recurrence.

Today's HCA employees, most of whom joined after the scandal, learn about the fraud case during orientation. Not as ancient history but as cautionary tale. The ethics training doesn't just cover rules but explores the psychological dynamics that led good people to make bad decisions. How competitive pressure corrodes judgment. How small compromises compound into massive frauds. How culture eats compliance for breakfast.

This institutional scarring has proven paradoxically valuable. While competitors chase growth at any cost, HCA maintains disciplined restraint born from experience. They've seen where aggressive tactics lead. They've paid the price—literally and figuratively. This corporate PTSD creates a conservative culture that values sustainability over short-term gains.

Lessons on Corporate Redemption and Culture Change

The rehabilitation required three essential elements that any organization seeking redemption should study. First, acknowledgment without equivocation. HCA didn't blame rogue employees or claim persecution. They admitted systematic wrongdoing, accepted responsibility, and committed to change. This honesty, painful as it was, provided foundation for rebuilding trust.