Twilio: The API That Ate Communications

I. Introduction & Episode Roadmap

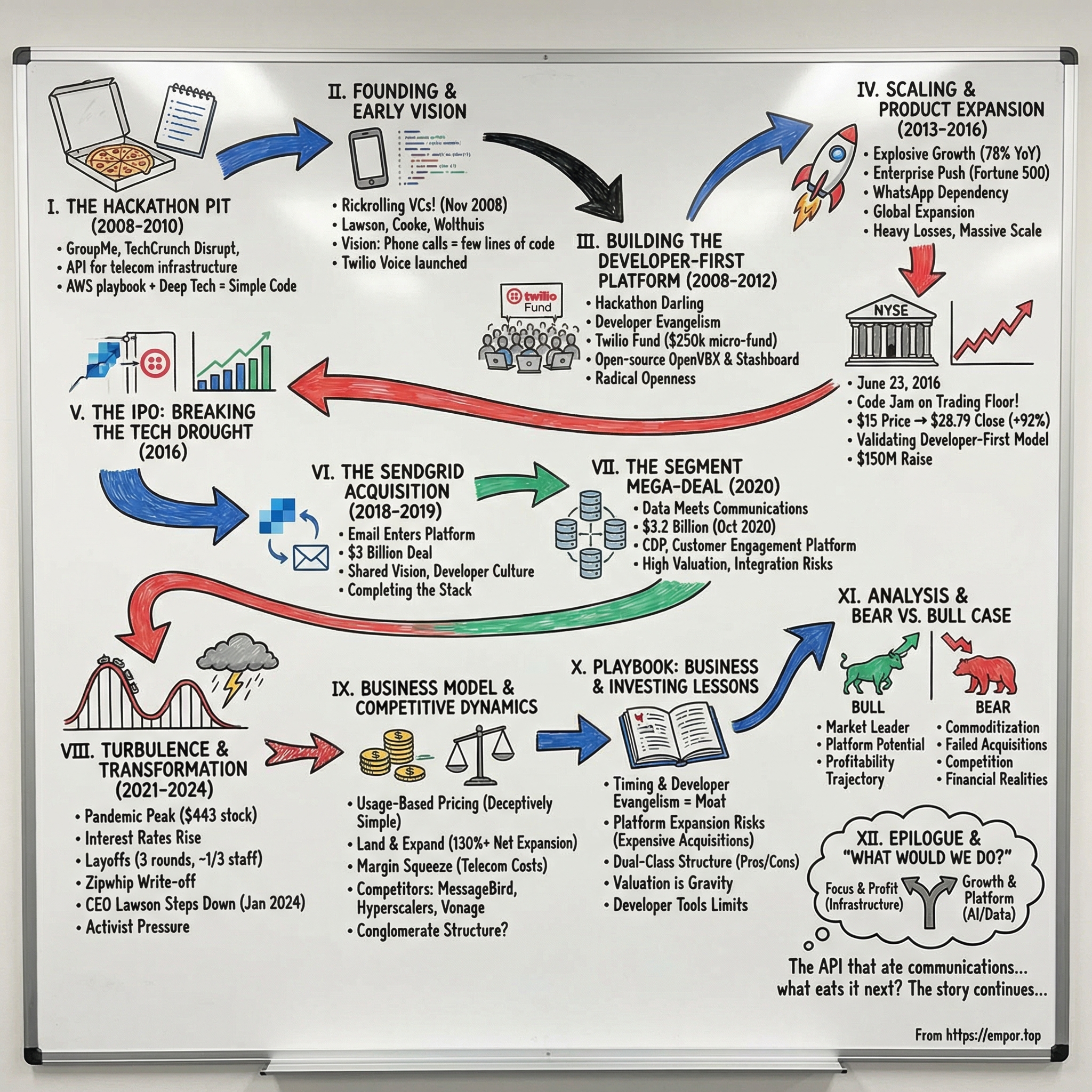

Picture this: It's May 2010 at TechCrunch Disrupt in New York. A young team is frantically coding in the hackathon pit, building what would become GroupMe—a group messaging app that would sell to Skype for $85 million just 370 days later. Their secret weapon? A few lines of code connecting to an obscure Seattle startup's API that magically handled all the complex telecom infrastructure. That startup was Twilio, and those few lines of code represented a seismic shift in how software would interact with the physical world of telecommunications.

Today, Twilio stands as a $15 billion cloud communications platform, powering everything from Uber's driver notifications to Airbnb's host messages, from Netflix's user authentication to countless COVID-19 contact tracing systems. The company processes billions of interactions annually, yet most consumers have never heard its name. It's the ultimate infrastructure play—invisible to end users but indispensable to developers.

The story begins with three engineers—Jeff Lawson, Evan Cooke, and John Wolthuis—who saw telecommunications stuck in the hardware age while the rest of technology was racing toward the cloud. Lawson, a serial entrepreneur and Amazon Web Services alumnus, brought the AWS playbook of turning infrastructure into APIs. Cooke brought deep technical expertise in distributed systems. Wolthuis brought the telecommunications know-how. Together, they asked a simple question that would reshape an industry: What if making a phone call was as easy as writing a few lines of code?

This is the story of how Twilio transformed from a hackathon darling into a public company roller coaster, navigating the treacherous waters of hypergrowth, massive acquisitions, and the eternal tension between developer love and Wall Street expectations. It's a tale of brilliant timing—riding the mobile wave, the cloud revolution, and the API economy—but also of painful reckonings when growth-at-all-costs collided with market reality.

II. The Founding Story & Early Vision

The scene was Silicon Valley's ultimate initiation rite: a prank that would define a startup's character. On a November evening in 2008, TechCrunch founder Michael Arrington's phone rang. When he answered, expecting a routine call, Rick Astley's "Never Gonna Give You Up" blared through the speaker. He'd been rickrolled via phone, courtesy of a new startup called Twilio, initiated by venture capitalist Dave McClure who was dining with the founders that night.

The rickroll app was an internal project meant to test Twilio's new voice API—never intended for public consumption—but word slipped out during that fateful dinner with McClure, who immediately weaponized it against Arrington. Viral press ensued, transforming what could have been another forgettable startup launch into Silicon Valley legend. The prank perfectly encapsulated Twilio's DNA: technically sophisticated yet playfully accessible, enterprise-grade infrastructure wrapped in developer whimsy.

Behind this cheeky demo stood three engineers who'd spent years wrestling with telecommunications' archaic complexity. Jeff Lawson, Evan Cooke, and John Wolthuis founded Twilio in 2008, initially based in both Seattle, Washington, and San Francisco, California. Lawson brought the vision and the Amazon Web Services playbook—he'd been one of the first product managers for AWS, watching Jeff Bezos transform infrastructure into APIs. Lawson and his two co-founders were all developers, and they were essentially building something they had needed in their prior lives—Lawson had started three companies before Twilio and could imagine cases where he would have needed this at every single company.

The origin story reads like entrepreneurial archeology. Lawson had previously started Versity (an online note-taking marketplace in college), joined StubHub as founding CTO (building it from first line of code to launch in six weeks), and even attempted a skateboard shop that doubled as a tech workspace. What he discovered was a missing thread: conviction. He found it in communications—in every one of his three previous companies, communications was a core part of their business, but it was incredibly cumbersome to set up.

On November 20, 2008, just days after the rickroll incident, Twilio officially launched Twilio Voice, an API to make and receive phone calls completely hosted in the cloud. The timing seemed insane—Lehman Brothers had collapsed two months earlier, the financial system was in freefall, and VCs were telling portfolio companies to prepare for nuclear winter. But Twilio's founders saw opportunity in chaos: while others retreated, they would build the communications infrastructure for the next generation of companies that would emerge from the rubble.

The product's radical simplicity shocked developers accustomed to telecommunications' byzantine complexity. Twilio commoditized phone services by making them accessible through intuitive commands—primarily five commonly used phone actions (Say, Play, Record, Dial, and Gather), each behaving exactly as expected. That rickroll app? Here's the code—basic stuff that managed to replicate GrandCentral's core functionality in only around 15 lines.

III. Building the Developer-First Platform (2008–2012)

The magic happened at 3 AM in a Manhattan warehouse. May 22, 2010, TechCrunch Disrupt Hackathon, New York. While 300 hackers fueled by pizza and Red Bull coded through the night, two friends—Jared Hecht from Tumblr and Steve Martocci from Gilt Groupe—were solving a problem that had annoyed Hecht's fiancée days earlier. Her friends were trying to coordinate a trip via email chain, but when it came time to mobilize in real-time, the chain broke down. Not everyone had smartphones, lag times killed momentum. SMS seemed like the most intuitive solution.

When they arrived they were greeted by Danielle Morrill from Twilio who was encouraging hackers to use their API. 18 hours later they had a working prototype. The best part? They started using their product immediately—Hecht went to Kinko's to print business cards and stayed in touch with the group the entire time. Steve and Hecht remember walking the halls at 3 in the morning telling each other that if all went well they wouldn't be working at Gilt and Tumblr the next week—this would be their full-time job.

What happened next became Silicon Valley legend. During TechCrunch Disrupt proper, Steve's high school friend started telling everyone about GroupMe. Steve was so overwhelmed with requests for demos that his phone died. He found an empty table on Startup Alley, plugged into an outlet, and whipped out his computer and phone. He was stationed as if he were a contestant at TCD, and for the rest of TCD he had a continuous line of people requesting demos.

This was the power of Twilio's developer evangelism strategy in action. Twilio's text messaging API was released in February 2010, and SMS shortcodes were released in public beta in July 2011. The company wasn't just building APIs—it was building a movement. Following the success of TechCrunch Disrupt, seed accelerator 500 Startups announced the Twilio Fund, a $250,000 "micro-fund" to provide seed money to startups using Twilio in September 2010.

The fund represented something unprecedented: a platform company investing directly in its ecosystem before achieving significant scale itself. Via Twilio Fund, they offered investments of $10,000 in up to 10 companies for a 1% stake in the company. Dave McClure, who had rickrolled Arrington less than two years earlier, now managed this micro-fund alongside his broader 500 Startups portfolio.

The early funding rounds tell a story of patient capital betting on a developer-first vision that VCs initially dismissed. Twilio received its first round of seed funding in March 2009 for an undisclosed amount from Mitch Kapor, The Founders Fund, Dave McClure, David G. Cohen, Chris Sacca, Manu Kumar, from K9 Ventures, and Jeff Fluhr. Twilio's first A round of funding was led by Union Square Ventures for $3.7 million and its second B round of funding, for $12 million, was led by Bessemer Venture Partners.

The company's approach to building its platform was radically open. In June 2010, Twilio launched OpenVBX, an open-source product that lets business users configure phone numbers to receive and route phone calls. One month later, Twilio engineer Kyle Conroy released Stashboard, an open-source status dashboard written in Python that any API or software service can use to display whether their service is functioning properly.

IV. Scaling and Product Expansion (2013–2016)

The year 2013 marked Twilio's transition from scrappy startup to serious contender. The numbers told a story of explosive growth: revenue had grown from $49.9 million in 2013 to $88.8 million in 2014, a 78% increase that caught the attention of Silicon Valley's biggest players. But beneath these headline figures lay a more remarkable metric—the company's Dollar-Based Net Expansion Rate, which was 155% for the year ended December 31, 2015. This meant existing customers were spending 55% more year-over-year, a testament to the land-and-expand model working at scale.

In June 2013, Twilio announced the completion of a $70 million Series D round of funding. New investors include Redpoint Ventures, who led the round with existing investor Bessemer Venture Partners, and Draper Fisher Jurvetson (DFJ). The round brought heavyweight Scott Raney from Redpoint to Twilio's board—a partner who had backed cloud computing winners like Heroku and Stripe.

Jeff Lawson's statement accompanying the funding revealed both confidence and ambition: "For each of the past three years, Twilio experienced more than 100 percent revenue growth as we helped developers and corporations realize they can tap the power of the cloud for voice and messaging services". The telecommunications industry represented hundreds of billions of dollars, and Twilio was positioning itself as the software layer that would eat this massive market.

The product expansion during this period was relentless. In the past year, Twilio expanded its presence globally and is now available in more than 40 countries. The company introduced a range of new capabilities and products including new Android and iOS development kits for the company's Twilio Client product, WebRTC integration for improved voice calling from within web browsers, SIP from Twilio that enables enterprises to more easily integrate existing on-premises solutions with Twilio's cloud-based platform, multi-user account management, and much more. In addition, the company inked partnerships with Amazon Web Services, Google Cloud Platform, Microsoft Azure, Japanese service provider KDDI Web Communications and others.

The enterprise push represented a crucial evolution in Twilio's go-to-market strategy. While developers remained the entry point, the company increasingly found itself in conversations with Fortune 500 CTOs and CIOs. The value proposition was compelling: instead of ripping and replacing legacy telecom infrastructure, enterprises could gradually modernize by routing specific use cases through Twilio's APIs.

In 2013, 2014 and 2015 and the three months ended March 31, 2016, WhatsApp accounted for 11%, 13%, 17% and 15% of our revenue, respectively. WhatsApp uses our Programmable Voice products and Programmable Messaging products in its applications to verify new and existing users on its service. We have seen year-over-year growth in WhatsApp's use of our products since 2013 as its service has expanded and as it has increased the use of our products within its applications.

This WhatsApp dependency represented both validation and vulnerability—validation that the world's fastest-growing messaging app trusted Twilio for critical infrastructure, vulnerability in the concentration risk. The company's S-1 filing would later reveal the delicate balance: growing fast enough to dilute any single customer's impact while maintaining the quality that kept WhatsApp and others loyal.

The momentum continued building through 2015. 2015 was marked by a $130 million E round from Fidelity, T Rowe Price, Altimeter Capital Management, Arrowpoint Partners, and Amazon and Salesforce. The presence of crossover investors like Fidelity and T. Rowe Price signaled something important: public market investors were already circling, preparing for what seemed like an inevitable IPO.

For the years ended December 31, 2013, 2014 and 2015 and the three months ended March 31, 2016, our revenue was $49.9 million, $88.8 million, $166.9 million and $59.3 million, respectively. The trajectory was undeniable—88% growth from 2014 to 2015—but so were the losses. The company had incurred net losses of $26.9 million, $26.8 million, $35.5 million and $6.5 million in 2013, 2014 and 2015 and the three months ended March 31, 2016, respectively.

By early 2016, Twilio had reached escape velocity. The platform processed billions of interactions annually, powered everything from Uber's driver communications to Airbnb's host messaging, and had become indispensable infrastructure for the on-demand economy. The stage was set for one of the most anticipated tech IPOs in years.

V. The IPO: Breaking the Tech Drought (2016)

June 23, 2016. The New York Stock Exchange trading floor buzzed with an energy that had been absent for months. For the first time all year, a venture-backed technology company was going public. The drought was over. Twilio's initial public offering marks the first U.S. venture-backed tech IPO of 2016, entering a market frozen by uncertainty—the Brexit referendum vote was literally happening that same day.

Jeff Lawson rang the opening bell wearing his trademark red track jacket—the same one Twilio gave to winning hackathon developers. Behind him stood engineers, not bankers. In a brilliant piece of theater, Twilio held a "code jam" (a NYSE-safe version of a Hackathon) with three developers on the trading floor. While traders scrambled to execute orders, developers were literally coding on the exchange floor, building apps with Twilio's APIs. The symbolism was perfect: software eating the world, live from capitalism's cathedral.

Twilio priced its initial public offering at $15 per share, which would value the company at around $1.23 billion. The pricing came above the already-raised range of $12 to $14, signaling strong institutional demand. But nothing could have prepared the market for what happened next.

The stock opened at $23.99, rising to close at $28.79 per share—a 92% surge on the first day, valuing the company at nearly $2.4 billion. The pop was so dramatic that CNBC anchors kept double-checking the numbers on air. This wasn't supposed to happen in 2016. The narrative had been set: tech unicorns were overvalued, the IPO window was closed, and public markets had no appetite for money-losing growth companies.

Yet here was Twilio, reporting a net loss of $35.5 million on $166.9 million in revenue in 2015, commanding a valuation of 14 times its prior year's revenue. The market's message was clear: they believed in the developer-first model, the platform strategy, and the massive telecommunications market waiting to be disrupted.

The dual-class share structure that Lawson and the board had insisted upon gave them the runway to think long-term. The company had two classes of common stock, Class A common stock and Class B common stock. The rights of the holders were identical, except voting and conversion rights. Each share of Class A common stock was entitled to one vote. Each share of Class B common stock was entitled to 10 votes and was convertible at any time into one share of Class A common stock.

Bessemer Venture Partners owned the largest chunk of the company at 28.5 percent per its last IPO filing, validating their early bet when others thought developers would never be a real market. The firm's persistence through multiple rounds had paid off spectacularly.

Lawson's comments that day revealed both humility and ambition: "We see this as the beginning of a very long journey to improve the world's communications with the power of software. We truly see every company can benefit from better communications. Whether that is retailers better communicating with their customers ... whether it's travel, whether it's real estate".

The stellar debut had broader implications for Silicon Valley. Anxiety had gripped many startups that had hit unicorn status given the complete lack of tech IPOs for 2016. The hope, for many startups, was that Twilio would re-open the tech IPO window with a strong showing. If that happened, it might convince investors that many startups that had hit frothy valuations have come back in line with reality.

The stellar first-day performance of Twilio was a huge sigh of relief for Silicon Valley. After SecureWorks' disappointing debut earlier in the year—the first tech IPO of 2016 saw shares open at $13.89, below the $14 IPO price before ending their first day flat—Twilio proved that the right company with the right model could still excite public investors.

The IPO raised $150 million for the company, creating a war chest for expansion just as the cloud communications market was exploding. More importantly, it validated a decade of betting on developers, proving that a bottom-up, API-first approach could build a public company worth billions.

VI. The SendGrid Acquisition: Email Enters the Platform (2018–2019)

The email arrived late on a Sunday night in October 2018. Jeff Lawson was sitting at home when his phone buzzed with a message from SendGrid CEO Sameer Dholakia. Following a ski trip full of cloud and business software leaders sharing a common investor, Bessemer Venture Partners, SendGrid CEO Sameer Dholakia and Lawson came to an agreement. The conversation that had been percolating for over a year was finally ready to reach its conclusion.

Twilio announced its plan to acquire the API-centric email platform SendGrid for about $2 billion in an all-stock transaction. At face value, it was Twilio's largest acquisition to date. But the strategic implications ran far deeper than the price tag suggested. Twilio had made bids for SendGrid since 2017, but all were rejected by Dholakia because he thought the "offers [were not] good enough" and would rather continue with their planned IPO.

The missing piece of Twilio's communications stack had always been email. This is the claimed "missing channel from Twilio" that Twilio CEO Jeff Lawson says the company has been trying to avoid. The irony wasn't lost on industry observers—Twilio had revolutionized voice and SMS but had deliberately steered clear of email, the oldest digital communication channel. Now they were paying top dollar to fill that gap.

The two companies share the same vision, the same model, and the same values, Lawson said in the announcement. This wasn't corporate speak—the parallels were uncanny. Both companies were developer-first, API-driven, and had built massive businesses by abstracting away infrastructure complexity. In 2009, Techstars Ventures was one of the earliest investors in Twilio. And at the same time, SendGrid (Techstars Class 4, Boulder 2009) was going through the original location of the Techstars mentorship-driven accelerator program.

SendGrid's metrics were staggering: A leader in email deliverability, SendGrid has processed over 45 billion emails each month for internet and mobile-based customers as well as more traditional enterprises. Over 74,000 SendGrid customers like Spotify, Uber, and Airbnb send over 45 billion emails every month. Many of these were already Twilio customers—the cross-selling opportunity was obvious.

The market's initial reaction was mixed. Shares of Twilio fell more than 4 percent in extended trading after the announcement, while SendGrid stock jumped 17%. Some investors questioned the premium—At closing, each outstanding share of SendGrid common stock will be converted into the right to receive 0.485 shares of Twilio Class A common stock, which represents a per share price for SendGrid common stock of $36.92 based on the closing price of Twilio Class A common stock on October 15, 2018. The exchange ratio represents a 14% premium over the average exchange ratio for the ten calendar days ending, October 15, 2018.

But Lawson saw beyond the numbers. "Increasingly, our customers are asking us to solve all of their strategic communications challenges — regardless of channel. Email is a vital communications channel for companies around the world, and so it was important to us to include this capability in our platform," Twilio CEO Jeff Lawson said in a statement.

The cultural fit was remarkable. SendGrid made history in November 2017 when they became the first company from any accelerator program to IPO. Like Twilio, they had built a developer-first culture, an usage-based business model, and a platform that powered critical infrastructure for the internet's biggest companies.

By the time the deal closed in February 2019, the valuation had risen even further. This transaction is valued at approximately $3 billion. Based on the closing price of Twilio Class A common stock on Jan. 31, 2019 and the exchange ratio of 0.485 shares of Twilio Class A common stock per share of SendGrid common stock, SendGrid stockholders received approximately $53.99 of aggregate value per share of SendGrid common stock.

The integration strategy was textbook Silicon Valley: SendGrid will operate as a wholly owned subsidiary of Twilio and will continue to be led by SendGrid CEO Sameer Dholakia, reporting to Lawson. No heavy-handed integration, no culture clash—just two developer-first companies continuing to do what they did best, now under one roof.

Together, we serve more than 140,000 active customer accounts and power more than 600 billion annualized interactions each year, the companies announced. The combined entity now offered developers a single, best-in-class platform to manage all of their important communication channels -- voice, messaging, video, and now email as well.

The strategic rationale proved prescient. With SendGrid, developers and businesses can use Twilio to reach their customers over any channel - voice, SMS, Facebook Messenger, WhatsApp, video, and now email. Across a wide variety of customer touchpoints, companies can now trust one platform to deliver the right communication, on the right channel, without having to setup different vendors for each approach.

VII. The Segment Mega-Deal: Data Meets Communications (2020)

The rumors started swirling on a Friday afternoon in October 2020. Friday afternoon brought an unconfirmed Forbes report that communications platform Twilio is buying CDP Segment for $3.2 billion. By Monday morning, it was official: This transaction is valued at approximately $3.2 billion in Twilio Class A common stock, on a fully diluted and cash free, debt free basis.

The deal represented a watershed moment for both the Customer Data Platform (CDP) category and Twilio's strategic evolution. CDP has become the buzzword-du-jour in marketing technology (martech) circles — much to the dismay of my colleague Jon Reed who named it most tedious acronym of 2019 — but it aims to solve a very real problem for enterprises seeking to build digital engagement with customers.

"Together, Twilio and Segment have an incredible opportunity to build the customer engagement platform of the future," said Peter Reinhardt, Segment's co-founder and CEO. "We created Segment to help businesses set themselves apart in the digital age and deliver rich, connected customer experiences built on high-quality data. By joining forces and applying our customer data platform to Twilio's engagement cloud, we'll be able to make the entire customer experience seamless from end-to-end."

The strategic logic was compelling. As Twilio Co-founder and CEO Jeff Lawson said today: We help companies take their investments in the myriad apps that they've bought and actually take the data that exists in silos for most companies. They bought a bunch of apps, typically SaaS apps, to power their business. They may have an app for marketing, they may have an app for sales, and they may have an app for customer support. They have myriad apps across the enterprise and it's the data silos that result from having bought all those apps that is the enemy of great customer engagement ... We want to empower developers with the best infrastructure, [to] break down what historically have been monolithic systems into more flexible, agile bu

The developer DNA ran deep in both companies. A further differentiation, its co-Founder and CEO Peter Reinhardt said today, is that whereas many in the sector start from a marketing-first workflow, Segment has always focused on solving data and infrastructure problems for developers who can then build the tools that marketers and customer support teams need. That developer focus is one that it shares with Twilio, he adds: The way that we approached the customer data platform market was much more by focusing on the developer and the developer experience. We launched an open source library, and the vast majority of our buyers are actually folks on the engineering or IT side, or folks who report jointly into IT or engineering. There's actually a lot of philosophical, spiritual, joint go-to-market alignment between Twilio and Segment. We've actually looked up to Twilio for many years in terms of how they've approached developer evangelism.

The numbers painted a picture of massive scale and ambition. Segment's ability to process events at scale (roughly 500 billion a month) amplifies Twilio's focus on customer engagement, helping developers connect with customer data across multiple sources. The combined company would serve a massive market: The transaction will accelerate Twilio's growth with a combined total addressable market of $79 billion, bringing Twilio one step closer to achieving the company's vision of becoming the world's leading customer engagement p

The valuation metrics revealed both the opportunity and the risk. Segment's current revenue isn't known, although one published estimate put it at $180 million for 2019. That sounds a bit high for a company with 450 employees at the time, but let's go with it and assume $200 million for 2020 revenue. This has Twilio is paying 16x revenue, which is less than the 20x that Salesforce paid for Mulesoft ($6.5 billion on roughly $300 million) but in line with the 15x that Adobe paid for Marketo ($4.7 billion on $320 m

In a deal worth $3.2B in 2020, Twilio paid a forward multiple of 15.9x for Segment. No other company among its closest competitors has achieved an exit of this scale, or landed a valuation near it. Tealium (last valued at $1.2B in February 2021) claimed over $100M ARR in 2020 — or a 12x multiple.

The competitive dynamics were shifting rapidly. Further, the market once solely dominated by pure-play CDPs now also features the arrival of CDPs from Microsoft, Adobe, SAS, Salesforce, Informatica, Oracle and SAP, the latter announcing its CDP just this week. The big clouds (Oracle, Adobe, Salesforce, Microsoft, SAP) all chose to build their CDPs internally, but Twilio is much smaller and lacks the resources to do the same in a timely fashion. (Even the big clouds struggled, of course). On the other hand, Twilio's surging stock price makes acquisition much easier. So buying a CDP they can deploy immediately gains them time and a mature product.

The vision went beyond just adding another product. Questioned by Wall St analysts about the deal today, Lawson agreed that there are immediate use cases in combining Segment's data with Twilio's SendGrid email platform, acquired two years ago. But he was keen to talk up more sophisticated use cases, in particular combining Segment with the Twilio Flex contact center platform and using machine learning to analyze customer data and propose the best action: Which channel to use? What message to send? Which will actually result in more repeat purchases or more customer satisfaction? These are all places where data coming from myriad places can help companies make better decisions and automated systems and machine learning systems [can] drive better outcomes. That occurs across many of the touch points, not just marketing or not just contact center, but really it's everywhere.

The deal positioned Twilio as a new challenger to incumbent giants. With its acquisition of CDP pureplay Segment, Twilio cements its position as the API-centric platform to challenge the traditional CRM giants on customer engagement ... Communications platform vendor Twilio today confirmed that it is buying Segment, the leading pureplay vendor in the emerging customer data platform (CDP) space. The move will create a new challenger to incumbent customer relationship and engagement vendors including Salesforce, Adobe and Microsoft when the all-stock transaction closes later this year.

But some observers saw it differently. The reason is that Segment is more Pipe than Platform when it comes to CDP. They were even less of a business solution and much more of a developer toolkit. Finally, they were focused on integrating a 360 view of digital data but were not built to include other customer data sources such as offline, loyalty or call center data. These are all fundamental aspects of their product and business that made them a very different "CDP" from, say, ActionIQ.

The pandemic context added urgency to the deal. This move also demonstrates the impact of accelerated digital transformation in a COVID-19 world, where organizations require more access to data-driven tools to grow and compete. Both Twilio and Segment have seen greater opportunity as businesses shift to a digital-first model in the wake of the pandemic – and that shows no sign of slowing down.

Looking back, the acquisition would prove both prescient and problematic. The Segment acquisition feels especially extravagant considering Twilio's market cap has dropped from $45B to under $13B since the deal was announced. The strategic vision of unifying data and communications was sound, but executing on that vision while managing Wall Street's expectations would prove to be Twilio's greatest challenge yet.

VIII. Turbulence and Transformation (2021–2024)

The pandemic changed everything. Twilio's stock reached its all-time high closing price of $443.49 on February 18, 2021, a valuation that would prove to be the peak of irrational exuberance. The company seemed unstoppable—revenue was accelerating, every business needed digital communications, and the land-grab for customer engagement platforms was in full swing. In May 2021, Twilio announced the acquisition of Zipwhip for approximately $850 million in an approximately equal blend of cash and stock, betting big on toll-free messaging as businesses scrambled to connect with customers stuck at home.

But the sugar high couldn't last. Interest rates began rising, growth stocks cratered, and suddenly Wall Street's patience for money-losing companies evaporated. The reckoning was swift and brutal. In September 2022, Twilio cut around 11% of its staff, followed just months later in February 2023 by another 17% of its workforce—approximately 1,500 employees shown the door in the second round alone.

The layoffs revealed deeper structural issues. Jeff Lawson's email to employees pulled no punches: "We've gotten too big, especially in Communications." The company that had prided itself on developer love and employee perks was suddenly canceling cherished benefits. The company ended benefits such as book and wellness allowances as well as Twilio Recharge—a four-week paid sabbatical that employees would get every three years, with Lawson admitting it "was ill-timed given our profitability goals".

By December 2023, the cuts continued. After laying off 11% of staff in September 2022 and 17% in February 2023, Twilio announced another 5% workforce reduction. The company had now shed nearly a third of its workforce in just over a year. Each round came with promises that this would be the last, only to be followed by another restructuring months later.

The activist investors smelled blood in the water. Anson Funds and Legion Partners began circling, demanding radical changes. Anson Funds said that Twilio should sell the entire company or at least divest the data and applications division. The pressure mounted through 2023, with activists arguing that Twilio's conglomerate structure was destroying value—the communications business was profitable but weighed down by money-losing ventures in data and applications.

On January 8, 2024, Jeff Lawson announced he would step down as CEO and board member, replaced by Khozema Shipchandler, a longtime Twilio executive who had served as CFO and COO. Lawson also stepped down from Twilio's board, where he had served as chairman. The founder's exit after 15 years marked the end of an era. In his farewell, Lawson struck a bittersweet tone: "We launched Twilio in 2008 with a to-do list written on the back of a pizza box and 15 years later, Twilio's platform handles over 1.7 trillion interactions a year on behalf of more than 306,000 customers across the globe. I'm proud to have led the company from zero to over $4 billion in annualized revenue, and now generating a 19% free cash flow margin".

The new CEO immediately signaled a shift in priorities. Shipchandler suggested the company would take a harder look at "underperforming" businesses, in line with what activists had been agitating for. The message was clear: the era of growth-at-all-costs was definitively over.

Meanwhile, the strategic bets made during the boom times were unraveling. The Zipwhip acquisition, celebrated as a masterstroke in 2021, turned into an embarrassment. Twilio culled its Zipwhip solution despite only acquiring the software in May 2021 for $850M, with software services running until November 30, 2023. In just 18 months, Twilio had essentially written off nearly a billion dollars, unable to even provide a migration path for Zipwhip's 30,000 customers.

The restructuring continued into late 2023 and early 2024. "We've made tremendous progress in Communications, even overachieving on our goals; however, we've underachieved on growth in TD&A. So we're taking some steps to create a more effective GTM motion for Flex and recalibrate our investments in Segment", Lawson explained in one of his final acts as CEO. The Segment acquisition, once heralded as transformative, was now being "recalibrated"—corporate speak for admitting it hadn't worked as planned.

IX. Business Model & Competitive Dynamics

The Twilio business model is deceptively simple: charge developers for every API call, every message sent, every minute connected. This usage-based pricing created perfect alignment—startups could start small, paying pennies while prototyping, then scale to millions as they grew. No contracts, no minimums, just pay for what you use. It was the AWS playbook applied to communications.

The numbers tell the story of this model's power. Twilio's Dollar-Based Net Expansion Rate—the metric that measures how much existing customers increase their spending—consistently exceeded 130% for years. This meant that once Twilio landed a customer, that customer would typically more than double their spending within 18 months. The land-and-expand strategy worked brilliantly: hook developers with free credits at hackathons, then watch usage explode as their apps scaled.

But the model had a dark side. Twilio's gross margins hovered around 50-55%, far below typical software companies that enjoyed 70-80% margins. The reason was simple: Twilio wasn't really a software company—it was a reseller of telecommunications capacity with a software layer on top. Every SMS sent, every call made required Twilio to pay carriers. As competition intensified, these wholesale costs became an albatross.

The competitive landscape evolved dramatically from Twilio's early days. What started as Twilio versus legacy telecom quickly morphed into a multi-front war. MessageBird raised massive rounds and competed aggressively on price, even stealing Uber as a customer. Bandwidth went public and targeted the enterprise directly. Vonage, acquired by Ericsson, leveraged its telecom relationships. And most ominously, the hyperscalers—AWS, Azure, and Google Cloud—began offering communications APIs as loss leaders to drive cloud consumption.

The platform evolution strategy seemed logical: move from horizontal infrastructure (APIs) to vertical solutions (applications) to full-stack platforms. SendGrid added email. Segment added data. Flex added contact center. The vision was compelling—become the operating system for customer engagement, the single platform where businesses managed every customer interaction.

But each expansion brought new challenges. Email had different economics than SMS—lower margins, more competition from free alternatives. Customer data platforms required selling to different buyers—data teams rather than developers. Contact center software meant competing with established players like Genesys and Five9 who had decades of enterprise relationships.

The developer-first go-to-market that had been Twilio's superpower became a limitation. Developers could adopt Twilio's APIs without executive approval, spreading virally through organizations. But Segment required C-suite buy-in and complex integration projects. Flex needed to displace existing contact center infrastructure. The sales cycles lengthened, the deal sizes grew, but so did the cost of sales.

Network effects, theoretically Twilio's moat, proved weaker than expected. Yes, more developers using Twilio made the platform more valuable—more tutorials, more integrations, more community support. But unlike true network effect businesses, each Twilio customer operated independently. Uber using Twilio didn't make it more valuable for Airbnb. The switching costs that should have locked in customers were undermined by the ease of multi-vendor strategies and the commoditization of basic communications APIs.

The margin challenge became existential as growth slowed. In hypergrowth, investors ignored profitability, focusing on revenue expansion and market share. But as growth decelerated, the math became unavoidable. Twilio was buying revenue through acquisitions, paying sales teams increasingly large commissions to hit numbers, and competing on price in commoditized segments. Stock-based compensation alone regularly exceeded $200 million per year, a hidden cost that crushed real profitability.

The two-business structure announced in 2023—Twilio Communications and Twilio Data & Applications—was admission that the unified platform vision hadn't materialized. Communications was profitable but growing slowly. Data & Applications was losing money with unclear product-market fit. Activists saw what management wouldn't admit: these were different businesses with different customers, economics, and competitive dynamics, artificially bundled together.

X. Playbook: Business & Investing Lessons

The Twilio story offers a masterclass in both the promise and perils of platform building in the API economy. The first lesson is timing: Twilio succeeded not because it invented communications APIs, but because it arrived at the perfect intersection of cloud adoption, smartphone proliferation, and developer empowerment. The iPhone SDK had just launched, AWS was gaining momentum, and suddenly every company needed mobile communications. Timing the platform shift mattered more than technical superiority.

The power of developer evangelism cannot be overstated. While competitors built sales teams, Twilio built a movement. They turned infrastructure into culture—red track jackets became status symbols, hackathon victories became customer acquisition events. The $250,000 Twilio Fund wasn't about financial returns; it was about creating thousands of founders who would evangelize Twilio for life. The lesson: in platform businesses, community is your competitive moat.

But the platform expansion playbook revealed hard truths. Acquiring your way to platform completeness—SendGrid for $3 billion, Segment for $3.2 billion, Zipwhip for $850 million—is expensive and risky. Each acquisition brought integration challenges, cultural conflicts, and dilution of focus. The lesson isn't that acquisitions don't work, but that they must be existential improvements to the core platform, not adjacencies that might create cross-sell opportunities.

The dual-class share structure that gave Lawson control proved both blessing and curse. It enabled long-term thinking, allowing Twilio to invest in developer experience over short-term profits. But it also insulated management from market feedback, allowing strategic drift to continue unchecked. When activists finally forced change, the stock had already fallen 70% from its peak. The governance lesson: founder control works until it doesn't, and the market always gets the last vote.

Managing hypergrowth exposed a paradox: the capabilities that enable rapid scaling often prevent profitable scaling. Twilio's culture of shipping fast and iterating worked brilliantly for APIs but failed for enterprise software. The muscle memory of giving developers free credits translated poorly to selling six-figure Segment contracts. Growing from $100 million to $1 billion revenue required different skills than growing from $1 billion to $4 billion. The playbook had to be rewritten mid-flight, and many companies crash during that transition.

The most sobering lesson concerns valuation and expectations. At its peak, Twilio traded at over 30 times revenue, priced for perfection in a world where perfection is impossible. The acquisition spree made sense at those valuations—using inflated stock as currency to buy growth. But when multiples compressed, Twilio was left holding expensive assets that couldn't generate returns to justify their cost. The investing lesson: valuation is gravity, and what goes up far above fundamentals must come down.

The developer tools gold rush that Twilio pioneered created massive wealth but also revealed the sector's limitations. Unlike consumer platforms with winner-take-all dynamics, developer tools face constant competition, technical commoditization, and limited pricing power. The successful ones—Stripe, Datadog, MongoDB—found ways to expand beyond developers to business buyers. Those that remained developer-only often hit growth ceilings.

XI. Analysis & Bear vs. Bull Case

The bull case for Twilio rests on three pillars: market position, platform potential, and profitability progress. Twilio remains the clear leader in cloud communications APIs, processing over 1.7 trillion interactions annually. Despite competitive pressure, no rival matches Twilio's scale, reliability, or developer mindshare. The core communications business generates substantial cash flow, proving the underlying model works when properly managed.

The integrated platform story, while delayed, isn't dead. Twilio now owns critical components—communications, email, and customer data—that enterprises desperately need unified. The shift to first-party data, privacy regulations, and real-time personalization all play to Twilio's strengths. If management can execute on integration, the whole could be worth far more than the sum of parts. Early CustomerAI innovations suggest the platform vision might finally be crystallizing.

Bulls point to the massive market opportunity ahead. Digital transformation isn't slowing—every business must become a digital business, and digital businesses need programmable communications. The $79 billion total addressable market Twilio claims might be conservative. As AI transforms customer engagement, Twilio's infrastructure becomes more valuable, not less. The company processing the interactions has the data to train the models that will power the next generation of customer experiences.

The profitability trajectory offers hope. After years of losses, Twilio is generating meaningful free cash flow. The restructuring, while painful, rationalized the cost structure. The new CEO brings operational discipline from GE, not Silicon Valley growth-at-all-costs mentality. If Twilio can maintain 20%+ growth while expanding margins, the stock could re-rate dramatically from current levels.

The bear case is equally compelling. The core communications business faces inevitable commoditization. What Twilio does—routing messages and calls through carrier networks—isn't technically defensible. Carriers themselves are launching APIs, hyperscalers offer communications as loss leaders, and open-source alternatives proliferate. Pricing pressure will only intensify, making margin expansion nearly impossible in the core business.

The acquisition strategy has demonstrably failed. Twilio paid $7 billion for SendGrid, Segment, and Zipwhip—more than half its current market cap. Zipwhip was shut down after 18 months. Segment hasn't achieved projected growth. SendGrid faces brutal competition from Amazon SES and other email providers. The company destroyed billions in shareholder value chasing a platform vision that may be fundamentally flawed.

Competition is coming from every angle. Microsoft Teams, Zoom, and Slack are building communications capabilities directly into collaboration platforms. Salesforce, Adobe, and Oracle offer integrated customer engagement stacks. Startups attack specific verticals with purpose-built solutions. Twilio's position as horizontal infrastructure provider becomes less relevant as communications gets embedded everywhere.

The financial realities are sobering. Stock-based compensation remains massive, obscuring true profitability. Revenue growth has decelerated from 60%+ to 15%, but the company still trades at premium multiples. Customer concentration risk persists—losing a major customer like WhatsApp would be devastating. The balance sheet, once a strength, has been weakened by acquisitions and restructuring costs.

Bears argue the fundamental business model is broken. Twilio is essentially a middleman between developers and carriers, capturing a spread that will inevitably compress. Unlike true software companies with zero marginal costs, Twilio pays for every interaction. As volumes grow, so do costs. The usage-based model that enabled viral growth also caps margins and creates revenue volatility.

The cultural damage from multiple layoffs cannot be ignored. Twilio's greatest asset was its developer community and employee evangelism. Three rounds of layoffs, broken promises, and eliminated benefits have shattered that culture. The best talent has left for startups or FAANG companies. The company that once defined developer-first culture now feels like any other struggling tech company.

XII. Epilogue & "What Would We Do?"

Standing at the crossroads of 2025, Twilio faces an existential question: Is it a communications infrastructure company that should optimize for profitability, or a customer engagement platform that must invest for growth? The answer determines everything—strategy, valuation, even survival.

If we were running Twilio, the first move would be radical simplification. The platform vision, while intellectually compelling, has proven too complex to execute. Separate the businesses cleanly: Communications as a profitable, dividend-paying infrastructure company; Data & Applications as a growth-oriented software business. Let each find its natural owners and valuations. The conglomerate structure serves no one well.

The communications business should embrace its destiny as the AWS of communications—reliable, scalable, profitable infrastructure that developers trust. Stop chasing enterprise deals that require armies of salespeople. Return to the roots: simple APIs, transparent pricing, exceptional reliability. Let competitors fight over complex enterprise features while Twilio owns the developer workflow. This business could generate 30% EBITDA margins and return cash to shareholders.

The data and applications business needs a different playbook entirely. Segment has potential but requires focus—pick either being the best CDP for developers or the easiest for marketers, not both. Flex should be sold or spun off; contact centers are a different business with different dynamics. The email business via SendGrid makes sense but needs aggressive investment in deliverability and anti-spam technology to differentiate from commoditized alternatives.

Internationally, Twilio has barely scratched the surface. While the US market is mature, digital transformation in Asia, Africa, and Latin America is just beginning. But expansion requires local partnerships, regulatory navigation, and patient capital—not the quarter-to-quarter management that public markets demand. Perhaps Twilio needs to go private, restructure away from public scrutiny, and emerge leaner and more focused.

The AI opportunity is real but requires careful positioning. Twilio shouldn't compete with OpenAI or Anthropic on models but should own the orchestration layer—routing conversations, managing context, ensuring compliance. Every AI agent will need to communicate via voice, SMS, or email. Twilio should be the pipes that AI flows through, not another AI platform in an increasingly crowded field.

Most critically, Twilio must rebuild its developer community. The layoffs and strategic zigzags have damaged trust. Launch a new developer fund, not for equity investments but for pure grants to builders. Bring back the hackathon culture. Make the red track jacket mean something again. Without developer love, Twilio is just another vendor.

The future of developer-first businesses remains bright despite Twilio's struggles. The API economy is still early—most business processes haven't been programmed yet. The winners will be companies that maintain technical excellence while building business model innovations. Stripe added lending, Shopify added fulfillment, Square added banking. The lesson isn't to avoid platform expansion but to expand into areas that strengthen the core network effect.

Looking ahead, communications platform versus customer engagement platform is a false choice. The winners will be invisible infrastructure that powers visible experiences. Twilio's APIs should disappear into the background, so reliable and simple that developers never think about them. The platform should be everywhere and nowhere—embedded in every customer interaction but never the focus of attention.

The API economy that Twilio pioneered has fundamentally changed how software gets built. No longer do developers rebuild infrastructure from scratch; they compose solutions from specialized services. This shift from monolithic to modular is irreversible. Twilio's challenge isn't that the vision was wrong but that execution faltered under the pressure of public market expectations.

What would we do? We'd take Twilio private, split it into focused businesses, rebuild developer trust, and prepare for the next platform shift. Because despite current challenges, the need Twilio addresses—programmable communications in a digital world—will only grow. The company that turned phone calls into code still has chapters to write. Whether those chapters form a comeback story or a cautionary tale depends on decisions being made in San Francisco boardrooms today.

The Twilio story isn't over. Like many technology pioneers—IBM, Microsoft, Oracle—the company faces a difficult transition from explosive growth to sustainable profitability. Some navigate this successfully, emerging stronger and more focused. Others become acquisition targets or slowly fade into irrelevance. Twilio stands at that inflection point, its fate uncertain but its impact on the technology industry indelible.

Jeff Lawson's pizza box to-do list launched more than a company; it launched a movement that transformed how businesses communicate with customers. Thousands of companies exist because Twilio made communications programmable. Millions of developers learned that infrastructure could be beautiful. And an entire industry learned that developer experience matters more than enterprise features.

That legacy endures regardless of stock price or acquisition outcomes. Twilio proved that APIs could build billion-dollar businesses, that developers were a market worth serving, and that infrastructure could be revolutionary. In the end, that might be the most important lesson: sometimes the companies that don't survive intact leave the biggest impact. They change the game so fundamentally that their innovations become invisible, embedded in everything that comes after.

The API that ate communications may ultimately be eaten itself. But the DNA of developer-first thinking, usage-based pricing, and infrastructure-as-code that Twilio pioneered will replicate through generations of companies to come. That's the ultimate platform play—becoming so fundamental that you transcend your own existence.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube