Autodesk: The Desktop Revolution That Ate the Design World

I. Introduction & Episode Roadmap

Picture this: Every skyscraper piercing the Manhattan skyline, every Tesla rolling off the production line, every Pixar character bringing tears to your eyes—they all share a common digital DNA. Behind these creations sits a company that most consumers have never heard of, yet touches nearly every designed object in the modern world. Autodesk, with its $62 billion market capitalization and 7.5 million subscriptions, has become the invisible infrastructure of human creativity.

The numbers tell a remarkable story. From a $60,000 initial investment in 1982, Autodesk has grown to generate $5.47 billion in annual revenue, commanding a near-monopolistic position in computer-aided design software. But here's the question that should fascinate any student of business history: How did a group of sixteen programmers, meeting in John Walker's Marin County home, create one of the most durable software monopolies ever built?

This isn't just another software success story. It's a masterclass in platform economics, a case study in surviving multiple technology paradigm shifts, and perhaps most impressively, a blueprint for executing one of the most successful—and painful—business model transformations in enterprise software history. While Adobe gets the headlines for moving to subscriptions, Autodesk's journey from perpetual licenses to recurring revenue was arguably more complex, more risky, and ultimately more transformative.

The arc of Autodesk traces the entire evolution of the software industry. From shipping floppy disks to building cloud platforms, from DOS to AI-powered generative design, from selling to individual architects to powering entire construction ecosystems. Each transition could have killed the company. Instead, Autodesk emerged stronger, its moat deeper, its tentacles reaching further into the physical world's design process.

What makes this story particularly relevant today is that Autodesk sits at the intersection of several massive trends: the digitization of construction (a $10 trillion global industry still largely running on paper), the rise of digital twins and the metaverse, the sustainability revolution requiring smarter building design, and the AI transformation of creative work. Understanding how Autodesk got here—and where it's going—offers profound lessons for anyone building or investing in enterprise software.

We'll explore how AutoCAD became the MS-DOS of design software, why Carol Bartz's fourteen-year reign transformed a chaotic startup into a disciplined empire, how the company survived losing 18% of revenue during its subscription transition, and why Andrew Anagnost is betting billions that construction software is the next frontier. Along the way, we'll uncover the strategic decisions, near-death experiences, and brilliant moves that built this empire.

The Autodesk story challenges conventional Silicon Valley wisdom. It proves that sometimes the best businesses aren't built on network effects or viral growth, but on becoming so embedded in professional workflows that ripping you out would be like performing surgery on a beating heart. It shows that subscription transitions, while painful, can unlock extraordinary value. And perhaps most importantly, it demonstrates that in enterprise software, distribution and ecosystem can trump product innovation.

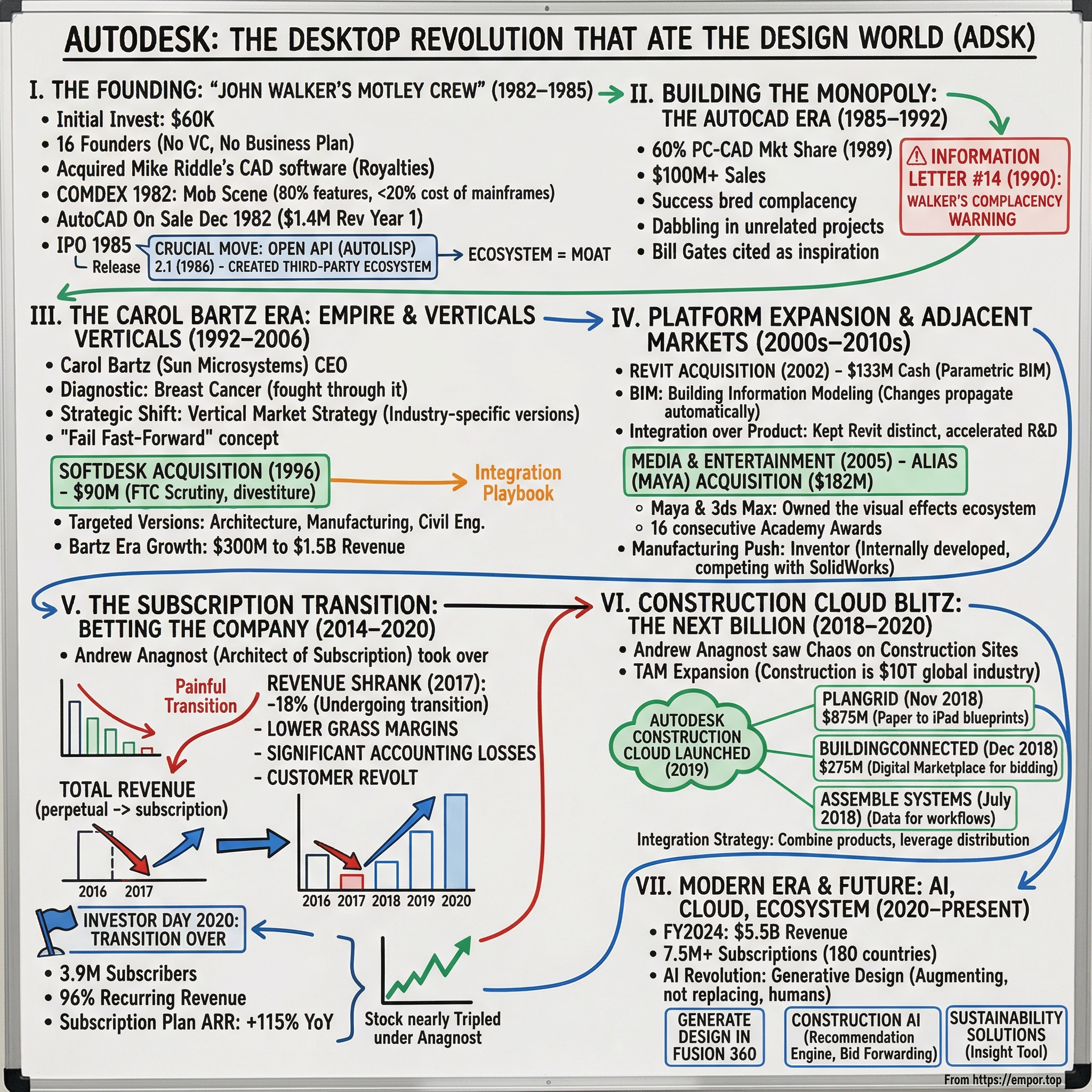

II. The Founding Story: John Walker's Motley Crew (1982–1985)

The conference room at the Marriott in Marin County wasn't exactly where you'd expect a revolution to begin. On April 26, 1982, sixteen programmers gathered around John Walker, each writing checks that would total $60,000. No venture capitalists. No business plan. Not even a clear product idea. Walker later described the founding meeting with characteristic honesty: "We had no idea what we were doing."

John Walker was an unlikely revolutionary. A programmer and writer with a philosophical bent, he'd already built and sold a successful company. But Walker saw something others missed: the personal computer revolution wasn't just about spreadsheets and word processing. It could democratize tools that had been locked away in million-dollar mainframes. His co-founder, Daniel Drake, brought the business acumen Walker freely admitted he lacked. Together with fourteen other programmers—including Hal Royaltun, Greg Lutz, and David Kalish—they formed what Walker called "the most unlikely collection of people to start a company. "Their most brilliant move wasn't what they built, but what they didn't build. In the early days, it was more of a collective of programmers working on five different projects. The group was developing an office automation system, a screen editor, a desktop organizer, and several other programs simultaneously. AutoCAD was almost an afterthought—a computer-aided design program that Michael Riddle had been trying unsuccessfully to sell.

The acquisition of Riddle's software reveals the scrappy nature of early Autodesk. AutoCAD was licensed from Mike Riddle, who was also a founder of the company. Unlike everyone else who joined the company, he did not contribute his software unencumbered: he had a royalty deal associated with it. This would later create complications, but at the time, it gave Autodesk a product they could ship quickly.

Then came COMDEX 1982 in Las Vegas—the moment everything changed. The turning point came half a year later when the company showed AutoCAD at the COMDEX trade show in Las Vegas in November 1982. By then, Riddle, who had signed a nonexclusive marketing agreement in return for royalty payments, had little further involvement with Walker's version of the software. With a starting price of just $1,000, AutoCAD delivered 80% of the capabilities of existing CAD systems—proprietary software running on expensive, proprietary systems—for less than 20% of the cost.

Walker expected polite interest. What he got was a mob scene. Architects, engineers, and designers crowded the booth, mesmerized by the possibility of CAD on a personal computer. Walker later said that he thought CAD was a niche field ("I mean, just compare the number of architects with the number of people that write documents"), but strong public reaction to AutoCAD at its debut at the 1982 Comdex in Las Vegas, and disinterest in the text editor that was Autodesk's other product there, caused the company to focus on CAD.

The numbers tell the story of a rocket ship taking off. AutoCAD went on sale in December 1982 and earned $1.4 million in revenue in its first year. Walker said in December 1984 that Autodesk was profitable from its first month and had not needed loans or outside investors. No venture capital. No burn rate. Just profitability from day one—a concept that seems almost quaint in today's Silicon Valley.

By 1985, the company was ready for its public debut. By then the company had about 10,000 AutoCAD systems installed; it was so successful that for a while Autodesk implied that AutoCAD was the company's name. The company continued to see itself as a general-purpose software company until new CEO Carol Bartz ended diversification outside computer-aided design in the early 1990s. Autodesk became a public company in 1985.

Walker's relationship with the company he founded was complex and increasingly strained. That year, Walker resigned as chairman and president of the company, continuing to work as a programmer. He would remain at Autodesk as a programmer, but his eccentric personality and philosophical approach to business increasingly clashed with the demands of running a public company.

The secret sauce that would make AutoCAD unstoppable came in Release 2.1 in 1986: AutoLISP. By opening up the platform to third-party developers, Autodesk created something more powerful than software—they created an ecosystem. Thousands of developers built specialized applications on top of AutoCAD, creating industry-specific solutions that made the software indispensable. It was the same playbook that would later make Windows, iOS, and Salesforce dominant, but Autodesk did it first in enterprise software.

III. Building the Monopoly: The AutoCAD Era (1985–1992)

The late 1980s at Autodesk resembled a gold rush more than a software company. In 1989, Autodesk's sales grew to over $100,000,000 after just four operational years. The company was printing money faster than they could figure out what to do with it. By 1989, AutoCAD commanded 60% of the PC-based CAD market—not just leading, but dominating in a way that would make today's platform monopolists envious. The open API strategy wasn't just smart—it was revolutionary for enterprise software in the 1980s. While competitors kept their systems closed, believing that controlling every aspect of the software was the path to profit, Autodesk understood that platforms beat products every time. By allowing third-party developers to build specialized applications on top of AutoCAD, they created thousands of mini-monopolies in vertical markets. An architect's practice management software, a mechanical engineer's stress analysis tool, a circuit designer's schematic capture system—all built on AutoCAD, all locking in their users even tighter.

But success bred complacency, and complacency bred chaos. By 1990, Autodesk had become what Walker himself would describe as directionless. The company was dabbling in everything from multimedia to molecular modeling, losing focus on its core CAD business. Products were tentatively separated into several different groups – AutoCAD, Multimedia, Retail, Molecular Modeling and Information – with a general manager responsible for each product family and a product manager responsible for each specific product.

Then came Information Letter 14, one of the most legendary internal memos in Silicon Valley history. In November 1990 Walker took a few months off to relax, read and think about the future of Autodesk. The result was Information Letter #14. An early version was circulated to several senior managers at the company, one of whom, unfortunately, allowed it to gain wider than intended distribution. Walker quickly finalized the document and Information Letter #14 was delivered to the company's senior management on April 1, 1991.

"Walker's primary concern was that Autodesk had been so successful that it had become complacent. His concern was: '…most companies that attain great value then lose it do so by failing to adapt when technological progress or the market demand they change.' He went on to apply this thought to Autodesk. 'When a company ceases to change at the rate demanded by the industry it exists within, it finds itself rapidly left behind.'"

The memo was brutal in its honesty. Walker argued that Autodesk was missing the Windows revolution, that the company had lost its technological edge, and that management wasn't listening to the engineers who saw disaster coming. Rightly or wrongly, there is a widely-held belief which I'm articulating because I share it, that management isn't hearing or doesn't believe what deeply worries people throughout the company, and isn't communicating to them the reasons for the course it is setting.

Bill Gates would later cite Walker's memo as inspiration for his own "Internet Tidal Wave" memo that redirected Microsoft toward the web. "A 1991 memo from Bill Gates (PDF): A source of inspiration to me is a memo by John Walker of Autodesk called 'Autodesk: The Final Days' (copies available from JulieG). It's brilliantly written and incredibly insightful. John hasn't been part of Autodesk management for three years and hasn't attended any management meetings for over two years, so he writes as an outsider questioning whether Autodesk is doing the right things. By talking about how a large company slows down, fails to invest enough and loses sight of what is important, and by using Microsoft as an example of how to do some things correctly he manages to touch on a lot of what's right and wrong with Microsoft today."

Walker's frustration peaked with what he saw as management's failure to understand the changing software landscape. The company was still thinking in terms of individual products when the world was moving to platforms. They were optimizing for short-term profits when they needed to be investing in long-term transformation.

By 1991, the situation had become untenable. The board realized that Autodesk needed adult supervision—someone who could harness the creative chaos and turn it into disciplined execution. John Walker would leave for Switzerland, eventually cutting all ties with the company in 1994. Walker moved to Switzerland in 1991. By 1994, when he resigned from the company, it was the sixth-largest personal computer software company in the world, primarily from the sales of AutoCAD. Walker owned more than 850,000 shares of Autodesk at the time of his departure, worth about $45.8 million at the time ($97,163,044 adjusted for inflation).

The stage was set for one of the most important CEO searches in enterprise software history.

IV. The Carol Bartz Era: From Chaos to Empire (1992–2006)

The woman who walked into Autodesk's headquarters in April 1992 didn't look like a savior. Carol Bartz, a veteran of Sun Microsystems, had never run a public company. She knew nothing about CAD software. And within days of starting, she received a diagnosis that would have sent most executives running: breast cancer.

She became CEO of Autodesk in 1992. According to Forbes, Bartz "transformed Autodesk from an aimless maker of PC software into a leader of computer-aided design software, targeting architects and builders." She is credited with instituting and promoting Autodesk's "3F" or "fail fast-forward" concept, also referred to as fail fast – the idea of moulding a company to risk failure in some missions, but to be resilient and move on quickly when failure occurs.

The board's reaction to her diagnosis revealed both the pressure she faced and the trust she'd already earned. "We just felt terrible for her, but we were sure we'd made the right choice, and she worked her way though it," said Hallam Dawson, chairman of IDI Associates and an 18-year member of Autodesk's board.

Bartz didn't just survive—she thrived through adversity. She underwent treatment while simultaneously performing one of the most dramatic corporate transformations in software history. Her approach was methodical, almost surgical. First, understand the business. Then, cut the cancer. Finally, rebuild stronger. Her listening tour was legendary. "I did a lot of listening. More important, I had a great group of people working for me that knew what they were doing and could teach this new, inexperienced-in-the-field CEO what the hell to talk about. I give them all the credit. If you don't go and find out how your customers are truly using the product, and listen very carefully to what they like and don't like — and they are very happy if you sit and shut your mouth for a while and not appear defensive — you learn so much."

One early conversation changed everything. "So, the first time I sat down with an architect, I asked him what he thought about CAD and Autodesk and the normal stuff and he goes, 'Well, I use AutoCAD, but I don't really like it because it's for the engineer.'" That single insight launched Autodesk's vertical strategy—creating industry-specific versions of AutoCAD that spoke the language of architects, mechanical engineers, and civil engineers rather than forcing them all to use generic CAD tools. The "fail fast-forward" philosophy became the cultural backbone of the new Autodesk. "In the late '80s and [early] '90s, Autodesk was essentially a one-product company: AutoCAD. [Whether you] were a mechanical engineer or a civil engineer or an architect or a construction company, you figured out how to make AutoCAD work for what you needed because we didn't do that for you," Bartz recalled. "That's when we had to kick into motion the fact that we have to try some things and we have try them fast and it's OK to fail. Try to figure out quickly that whatever you're trying isn't going to work and hopefully it moves you forward."

But the real test of Bartz's leadership came with Release 13. Autodesk was planning for AutoCAD Release 13, expected in the second half of 1994. It involved using HOOPS for the graphics interface, incorporating ACIS solids modeling in the basic product and changing the underlying architecture to a more object oriented methodology. Industry observers were skeptical: "The odds are also good that Release 13 will have its share of bugs due to all the new technology incorporated in it. Also, many of the older PCs users currently have installed may not support Release 13."

The skeptics were right. Release 13 was a disaster. Buggy, slow, and incompatible with many existing systems, it threatened to destroy customer trust that had taken a decade to build. But Bartz didn't panic. She mobilized the entire company around fixing the problems, personally calling major customers to apologize and promise solutions. The recovery with Release 14 wasn't just successful—it became a masterclass in crisis management.

The numbers during Bartz's tenure tell a story of relentless execution. During her 14-year tenure as the company's CEO, Autodesk net revenue substantially increased, and annual revenue rose from $300 million to $1.5 billion, with the stock price rising an average of 20 percent annually. Since Bartz took the helm in 1992, the company has diversified its product line and grown revenues from $285 million to $952 million in FY04.

Her strategic acquisitions reshaped the industry. In December 1996, Autodesk announced its plan to acquire Softdesk, a developer of architecture, engineering and construction software. The $90 million acquisition faced FTC scrutiny—Autodesk was the dominant provider of Windows-based CAD engines, accounting for nearly 70% of the installed base with approximately 1.4 million users. The Softdesk product, IntelliCADD, if brought to market, would have provided substantial direct competition to AutoCAD. The deal ultimately closed on March 31, 1997, after Softdesk divested IntelliCADD to maintain competition in the market.

With the purchase of Softdesk in 1997, Autodesk started to develop specialty versions of AutoCAD, targeted to broad industry segments, including architecture, civil engineering, and manufacturing. This wasn't just product development—it was market segmentation at its finest. Each vertical got its own language, its own workflows, its own ecosystem of third-party developers.

But Bartz's toughest battle was during the dot-com days, when Internet upstarts eclipsed the older software company. Although some investors called for her resignation, "she saw it through," said Gene Munster, a research analyst at Piper Jaffray. "She fixed the company." The internet boom and bust tested every software company, but Autodesk emerged stronger, having resisted the temptation to chase every shiny new trend.

By 2006, when Bartz stepped down to become executive chairman, she had transformed a chaotic collection of programmers into a disciplined, multi-billion dollar enterprise. "Nationally, she is probably the most successful female CEO," Munster said. "She was a big winner in a male-dominated world." More importantly for Autodesk's future, she had established the playbook for vertical market domination and acquisition integration that would define the company's next phase of growth.

V. The Platform Expansion: Acquisitions & Adjacent Markets (2000s–2010s)

The conference room at Autodesk headquarters in early 2002 witnessed a debate that would define the company's future. Should they acquire a small Massachusetts company called Revit Technology Corporation for $133 million? The price seemed steep for a company with minimal revenue. But what Revit had wasn't customers—it was a fundamentally different way of thinking about building design. In February 2002, Autodesk acquired Revit Technology Corporation, a developer of parametric building technology for building design, construction, and management. The acquisition completed on April 1, 2002, with Autodesk purchasing Revit Technology Corporation, a privately held company, for $133 million cash.

What made Revit revolutionary wasn't just 3D modeling—AutoCAD could do that. It was the concept of Building Information Modeling (BIM). Charles River Software was founded in Newton, Massachusetts, on October 31, 1997, by Leonid Raiz and Irwin Jungreis, key developers of PTC's Pro/Engineer software for mechanical design, with the intent of adapting parametric modeling - previously used in mechanical CAD - to the building industry. At the heart of Revit is a parametric change propagation engine that relied on a new technology, context-driven parametrics, that was more scalable than the variational and history-driven parametrics used in mechanical CAD software.

The genius of parametric modeling was simple: change a door dimension, and every drawing, schedule, and 3D view updates automatically. No more hunting through dozens of drawings to update a single change. No more coordination errors between disciplines. The term parametric building model was adopted to reflect the fact that changes to parameters drove the whole building model and associated documentation, not just individual components.

While RTC made a lot of noise, and its core parametric technology was innovative, it did not generate much revenue and, in fact, had few customers. But Carol Bartz and her team saw what others missed: this wasn't just a product acquisition—it was buying the future of building design. "The acquisition will extend our reach to new customers while expanding our existing building industry business," Bartz said at the time.

The integration of Revit into Autodesk's portfolio demonstrated the company's acquisition playbook at its finest. Rather than force Revit users to adopt AutoCAD workflows, Autodesk maintained Revit's Waltham, Massachusetts office and kept Dave Lemont, former CEO of Revit Technology Corporation, as vice president overseeing product development. They invested heavily in R&D, accelerating Revit's evolution while making it compatible with other Autodesk products. The expansion into Media & Entertainment revealed another dimension of Autodesk's platform strategy. In October 2005, Autodesk acquired Toronto-based Alias Systems Corporation for an estimated $182 million from Accel-KKR, and merged its animation business into its entertainment division. This acquisition brought Maya, the 3D animation software that had become the industry standard for visual effects, under the same roof as Autodesk's 3ds Max.

The industry was stunned. Maya and 3ds Max had been fierce competitors, each with passionate user bases. "Maya is way more widespread than Max. I fucking hate Max with passion, it's a giant piece of shit. Maya 4 lyfe," one user posted on forums at the time, capturing the tribal nature of the rivalry. Another countered: "EA uses Maya, everyone else worth a damn uses Max."

But Autodesk didn't force a merger. Instead, they continued developing both products, recognizing that different markets had different preferences. Film studios loved Maya. Game developers often preferred 3ds Max. Architectural visualization firms used both. By owning the entire ecosystem, Autodesk could serve everyone without forcing painful migrations.

By 2011, these products were used in films that won the Academy Award for Best Visual Effects for 16 consecutive years. Much of Avatar's visual effects were created with Autodesk media and entertainment software. Autodesk software enabled Avatar director James Cameron to aim a camera at actors wearing motion-capture suits in a studio and see them as characters in the fictional world of Pandora in the film.

The manufacturing push came through Inventor, Autodesk's internally developed parametric mechanical design CAD application. Rather than try to retrofit AutoCAD for mechanical engineering, Autodesk built Inventor from scratch to compete with SolidWorks and CATIA. This was Autodesk admitting that sometimes, even the mighty AutoCAD couldn't be everything to everyone.

Each acquisition and product launch followed the same playbook: identify a vertical market, acquire or build the best technology, integrate it with the Autodesk ecosystem, then dominate through superior distribution and support. The company wasn't just selling software anymore—it was selling entire workflows, complete ecosystems that made switching to competitors almost impossible.

The financial results validated the strategy. By the mid-2000s, Autodesk had successfully diversified beyond AutoCAD while maintaining its cash cow. The company had products in architecture (Revit), manufacturing (Inventor), media and entertainment (Maya, 3ds Max), and civil engineering (Civil 3D). Each vertical thought Autodesk understood them uniquely, not realizing they were all part of a carefully orchestrated platform play.

But the biggest transformation was yet to come. The software industry was about to undergo its most significant business model shift since the invention of shrink-wrapped software, and Autodesk would have to bet the entire company on navigating it successfully.

VI. The Subscription Transition: Betting the Company (2014–2020)

The boardroom at Autodesk in late 2013 felt like a war council. On one side of the table sat the financial reality: perpetual licenses generated massive upfront cash flow, customers were happy with the model, and Wall Street loved the predictability. On the other side sat the future: Adobe had just completed its transition to Creative Cloud subscriptions, younger competitors were all subscription-native, and customers increasingly expected continuous updates rather than big-bang releases.

Carl Bass, who had taken over as CEO in 2006, knew this was the defining decision of his tenure. "We can either disrupt ourselves, or someone else will disrupt us," he told the board. The question wasn't whether to move to subscriptions—it was how to do it without destroying the company in the process. January 31, 2016 marked the beginning of the end. Autodesk communicated that it will stop selling perpetual licenses of most individual products after January 31, 2016, with new licenses for these products available as subscriptions. By July 31, 2016, new commercial licenses of most Autodesk Design & Creation Suites and individual products would be available by subscription only.

The customer revolt was immediate and visceral. "Your return on your long-term investment in Autodesk software will be zero. Your reward for decades of loyalty to Autodesk will be to have your software costs blown through the roof. If you're not already making plans to abandon the Autodesk ship, you really need to do so now," one industry blogger wrote, capturing the rage of long-time customers who felt betrayed.

The financial impact was brutal. Autodesk has explained recent financial performance, which saw revenue decrease by 18%, as the result of "undergoing a business model transition in which it has discontinued most new perpetual license sales in favor of subscriptions and flexible license arrangements." During the transition, revenue, margins, EPS, deferred revenue and cash flow from operations were all impacted as more revenue was recognized ratably rather than up front. Andrew Anagnost took over as CEO in June 2017, after Carl Bass resigned following pressure from activist investors. As senior vice president of business strategy and marketing, he led the company's successful transition to a subscription business model, and drove adoption of Autodesk's cloud technologies. His appointment marked a crucial moment—the architect of the subscription strategy would now see it through to completion.

"The new normal is subscriptions," Anagnost said. "The software companies of the future are going to be subscription-based companies. It's the way we're going—there is more value, more power, and a vastly superior customer experience in the new subscription model than we currently have with the perpetual licensing model."

But the transition wasn't just about changing pricing models. In February 2016, Autodesk announced a restructuring that eliminated 10% of its workforce—925 positions—to align costs with the new business model. The company had to fundamentally reorganize around recurring revenue rather than big upfront sales.

The company also had to navigate the technical transition. Autodesk transitioned to AWS, implementing a hybrid cloud approach that allowed customers to work both locally and in the cloud. The migration wasn't just about moving software online—it was about reimagining workflows for a connected, collaborative world.

The financial journey through the transition was harrowing. Revenue shrunk in 2017 due to a huge decrease in perpetual license revenue, but subscription revenue soon caught up in 2018 and exceeded revenue in 2016. The transition necessitated many quarters of declining growth, lower gross margins, and significant accounting losses. However, the visibility into the progress of the transition and appeal of subscription models was rewarded by investors in the form of a higher valuation.

By 2020, Anagnost could declare victory. At the 2020 Investor Day, Autodesk declared that the transition was over. The company now had 3.9 million subscribers. During the quarter, Autodesk grew its subscription plan ARR (Annualized Recurring Revenue) by 115% year-over-year. Total ARR (subscription plus remaining maintenance) reached $2.3 billion. Recurring revenue as a percentage of total revenue hit 96%.

The stock market's verdict was clear: Autodesk's share price nearly tripled under Anagnost's leadership, and the company reached a market value of $41.1B, entering the Forbes Global 2000 and Fortune 500. What had seemed like corporate suicide in 2016 had become one of the most successful business model transformations in enterprise software history.

The subscription transition wasn't just about financial engineering. It fundamentally changed Autodesk's relationship with customers. Instead of selling software and hoping customers would upgrade every few years, Autodesk now had continuous engagement, continuous feedback, and continuous improvement. The company could push updates monthly instead of yearly, respond to customer needs faster, and build deeper relationships.

But perhaps most importantly, the subscription model positioned Autodesk perfectly for its next big bet: becoming the operating system for construction.

VII. The Construction Cloud Blitz: Building the Next Billion (2018–2020)

Standing in front of a construction site in San Francisco in 2018, Andrew Anagnost saw chaos disguised as order. Dozens of subcontractors, hundreds of workers, thousands of documents—all supposedly coordinated, but in reality held together by Excel spreadsheets, WhatsApp messages, and sheer determination. "Construction is the largest industry in the world that hasn't been digitized," he told his team. "And we're going to change that. "November 20, 2018: Autodesk announced plans to acquire PlanGrid for $875 million. The San Francisco startup helped move blueprints from paper to the iPad when it launched in 2011. For a company that had raised just $69 million, this represented one of the most successful exits in construction technology history.

Tracy Young, PlanGrid's CEO and co-founder, had experienced the pain firsthand. As an engineer working for a construction company, who was at one time responsible for making the paper copies, she recognized that the process could be improved by moving it into the digital realm. Her idea, which was kind of radical in 2011 when she started the company, was to move all that paper to the cloud and display it on an iPad.

"There is a huge opportunity to streamline all aspects of construction through digitization and automation. The acquisition of PlanGrid will accelerate our efforts to improve construction workflows for every stakeholder in the construction process," Anagnost said. PlanGrid currently had 400 employees, 12,000 customers and 120,000 paid users, and had been used on over a million construction projects worldwide.

Just a month later, on December 20, 2018, Autodesk announced it would acquire BuildingConnected for $275 million net of cash acquired, with the deal closing on January 31, 2019. BuildingConnected's network presented an opportunity to create a robust digital marketplace for construction goods and services, having built a network of more than 700,000 construction professionals, helping real estate owners and general contractors find and hire qualified contractors for their projects—the largest and most active digital network of construction professionals.

The strategic rationale was compelling. As CEO Dustin DeVan said, "Bid management is a critical step in preconstruction, since bidding is the genesis of construction projects". In addition to its leading bid-management platform, BuildingConnected offered TradeTapp, a subcontractor risk analysis platform, and Bid Board Pro, a platform that helped subcontractors manage and win more bids. BuildingConnected was the only bid-management platform that provided general contractors and owners with project-specific risk mitigation recommendations based on subcontractor qualification data, helping contractors efficiently vet and make more informed decisions when selecting subcontractors.

These weren't random acquisitions. Earlier in 2018, Autodesk had acquired Assemble Systems on July 3, 2018, though specific terms weren't disclosed, with Autodesk using a combination of cash and stock to finance the transaction. Assemble Systems provided a SaaS solution for general contractors that supported the construction phases of a project, enabling construction professionals to condition, query and connect the data to key workflows across bid management, estimating, scheduling, site management and finance.

The integration strategy revealed Autodesk's grand vision. BuildingConnected, along with Autodesk BIM 360, Revit, AutoCAD, and the acquisitions of PlanGrid and Assemble Systems, gave them a comprehensive construction offering and go-to-market capabilities. "Our tools empower all stakeholders with greater visibility and better information to make immediate decisions," said Jim Lynch, Vice President and General Manager, Autodesk Construction Solutions.

In 2019, Autodesk launched the Autodesk Construction Cloud, unifying these acquisitions into a comprehensive platform. The following year, they introduced Autodesk Build, combining PlanGrid's field management capabilities with BIM 360's project management tools. This wasn't just product integration—it was ecosystem construction at its finest.

The network effects were powerful. Every general contractor using BuildingConnected brought their subcontractors onto the platform. Every project managed in PlanGrid created data that made future projects more efficient. Every model created in Revit that flowed into construction made switching to competitors more painful.

By 2021, Autodesk's construction solutions were being used on projects worth more than $325 billion annually. The Construction Cloud had become the connective tissue between design and construction, between office and field, between general contractors and their entire supply chain. What had started as a series of acquisitions had become something more powerful: the operating system for construction.

VIII. Modern Era: AI, Cloud, and the Future of Design (2020–Present)

The pandemic should have been a disaster for a company dependent on construction and manufacturing. Instead, it accelerated every trend Autodesk had been betting on. Remote collaboration became mandatory. Digital workflows replaced paper processes overnight. AI went from nice-to-have to necessity.

By 2024, Autodesk's financial performance reflected this transformation. The company achieved $5.5 billion in revenue for fiscal 2024, with subscription plan ARR growing 12% year-over-year to reach $5.28 billion. The company's market capitalization exceeded $62 billion, making it one of the most valuable software companies in the world. With over 7.5 million subscriptions across 180 countries, Autodesk's reach was truly global.

The AI revolution at Autodesk wasn't about replacing designers—it was about augmenting them. Generative design in Fusion 360 allowed engineers to specify constraints and goals, then watch as AI generated thousands of design options, many resembling organic structures no human would have conceived. Autodesk's AI could optimize for weight, strength, material usage, and manufacturing method simultaneously, creating designs that were often 40% lighter and 20% stronger than human-designed alternatives.

In construction, Autodesk AI enhanced preconstruction workflows in BuildingConnected Pro, Bid Board Pro, and TradeTapp. BuildingConnected's Recommendation Engine helped teams quickly find the right subcontractors for projects by suggesting bidders based on location, trade expertise, and past performance. Bid Forwarding pulled key details from bid invitations received outside of BuildingConnected and organized them in Bid Board. TradeTapp's Financial Data Extraction used AI to turn PDF financial statements into structured data, giving a clearer view of a subcontractor's financial qualifications.

But new threats emerged from unexpected quarters. Figma, valued at $20 billion, democratized design for non-professionals. Canva made creating marketing materials as easy as posting on Instagram. These weren't direct competitors, but they represented a fundamental shift: design tools becoming consumer products rather than professional software.

More concerning were the AI-native startups. Companies like Midjourney and Stable Diffusion could generate photorealistic architectural renderings from text prompts. While they couldn't replace the precision of AutoCAD or the intelligence of Revit, they raised uncomfortable questions about the future value of traditional design tools.

Autodesk's response was multi-pronged. First, they doubled down on professional workflows, where precision, compliance, and collaboration mattered more than ease of use. Second, they integrated AI throughout their stack rather than treating it as a separate product. Third, they leveraged their data advantage—millions of designs, billions of design decisions—to train AI models that understood not just how to create, but how to create things that could actually be built.

The sustainability angle became increasingly important. Buildings account for 40% of global carbon emissions. Autodesk's tools could now simulate energy usage, optimize for carbon footprint, and ensure compliance with increasingly stringent environmental regulations. Their Insight tool could analyze millions of design options to find the most sustainable solution. This wasn't just good for the planet—it was becoming a requirement for winning projects.

International expansion presented both opportunities and challenges. While Autodesk dominated in North America and Europe, markets like China and India were still fragmented, with local competitors offering lower-priced alternatives. The company's strategy focused on partnering with local firms, offering localized versions of their software, and emphasizing the global collaboration capabilities of their cloud platform.

The metaverse and digital twin opportunity was perhaps the most intriguing. Every building designed in Revit was already a digital twin. Every product modeled in Fusion 360 existed in virtual space before physical space. As companies like Meta and Microsoft pushed virtual worlds, Autodesk was perfectly positioned to be the bridge between physical and digital reality.

By 2024, Autodesk wasn't just a CAD company anymore. It was a platform for imagining, designing, and making anything. From Hollywood blockbusters to electric vehicles, from skyscrapers to surgical implants, Autodesk software touched nearly every designed object in the modern world. The question wasn't whether Autodesk would remain relevant, but whether anyone could challenge their dominance in professional design software.

IX. Playbook: Business & Investing Lessons

The Platform Power Play: AutoCAD's genius wasn't in being the best CAD software—it was in becoming the platform everyone else built upon. By opening their APIs in 1986, Autodesk created thousands of co-dependent businesses. Every specialized add-on, every industry-specific tool, every custom workflow built on AutoCAD made switching costs astronomical. The lesson: In enterprise software, ecosystems beat products every time.

Subscription Transition Survival Guide: Autodesk's move from perpetual licenses to subscriptions offers a masterclass in managing Wall Street while transforming your business. They communicated metrics obsessively—ARR, subscriber count, retention rates—giving investors visibility even as traditional revenue plummeted. They set clear endpoints, declaring the transition complete in 2020. Most importantly, they had conviction: when activist investors pushed for faster change or abandonment, management held firm. The result? A 3x increase in valuation post-transition.

The Acquisition Integration Machine: Between 2011 and 2020, Autodesk acquired over 25 companies. Their integration playbook was consistent: maintain the acquired product for existing customers, gradually integrate features into the core platform, leverage Autodesk's distribution to accelerate growth, and retain key talent by giving them ownership of broader initiatives. The PlanGrid team didn't just run PlanGrid—they helped build the entire Construction Cloud.

Vertical Market Domination: Autodesk's evolution from generic CAD to industry-specific solutions demonstrates the power of vertical focus in horizontal platforms. Rather than build one product for everyone, they built specialized versions for architects (Revit), mechanical engineers (Inventor), and contractors (Construction Cloud). Each vertical thought Autodesk understood them uniquely, creating deeper loyalty than any horizontal competitor could match.

The Innovator's Dilemma Navigation: Autodesk survived multiple platform shifts that killed contemporaries. From DOS to Windows, desktop to cloud, perpetual to subscription, mouse-driven to AI-assisted—each transition could have been fatal. Their survival secret? They cannibalized themselves before others could. They launched cloud products while desktop was still growing. They pushed subscriptions while perpetual licenses printed money. Short-term pain, long-term survival.

Network Effects in B2B: BuildingConnected proved network effects aren't just for consumer apps. Every general contractor brought their subcontractors. Every subcontractor brought their suppliers. Every project created data that made the next project better. The network became so valuable that leaving meant losing access to opportunities, relationships, and intelligence. In B2B, networks might build slower, but they're stickier.

The Data Moat Strategy: Every design created in Autodesk software generates data. How engineers solve problems, how architects design spaces, how contractors sequence work. This data trains AI models that no competitor can replicate. OpenAI might have compute, Google might have algorithms, but Autodesk has decades of professional design decisions. In the AI era, domain-specific data is the ultimate moat.

X. Analysis & Bear vs. Bull Case

Bull Case:

The bulls see Autodesk as one of the most underappreciated monopolies in software. With 85% market share in many categories, switching costs measured in years of retraining, and workflows so embedded that removing them would paralyze entire industries, Autodesk's moat appears impregnable.

The subscription transition is now complete, unleashing powerful unit economics. With 96% recurring revenue and net revenue retention consistently above 100%, Autodesk has transformed from a cyclical software company to a predictable SaaS juggernaut. Free cash flow margins approaching 30% provide ample resources for R&D and acquisitions.

Construction cloud represents a massive TAM expansion opportunity. With construction being a $10 trillion global industry still largely running on paper and Excel, Autodesk's early leadership position could drive another decade of growth. The network effects from BuildingConnected's 700,000 professionals create a flywheel that accelerates with each new user.

AI leadership positions Autodesk perfectly for the next platform shift. While startups generate pretty pictures, Autodesk's AI understands building codes, manufacturing constraints, and physics. Their generative design doesn't just create—it creates things that work. As AI becomes table stakes in design software, Autodesk's data advantage becomes insurmountable.

The digital twin and sustainability megatrends play directly to Autodesk's strengths. Every smart city, every carbon-neutral building, every optimized supply chain needs digital modeling. Autodesk owns the tools that create these models. As physical and digital worlds converge, Autodesk becomes even more essential.

Bear Case:

The bears worry that Autodesk is a castle built on eroding foundations. The core AutoCAD business, while still profitable, faces declining growth as markets mature. Younger designers, raised on simpler tools, increasingly question why professional software needs to be so complex and expensive.

Disruption from below represents an existential threat. Just as Autodesk disrupted expensive workstations with PC software, new entrants like Onshape (cloud-native CAD) and Shapr3D (iPad-based modeling) are attacking from below with simpler, cheaper alternatives. These tools might not match Autodesk's capabilities today, but neither did AutoCAD match mainframe CAD in 1982.

Construction adoption might be slower than expected. Construction is a notoriously conservative industry with thin margins and high failure rates. Many contractors still prefer paper to pixels. The ROI on construction software, while real, takes time to materialize. Autodesk might be early to a party that starts later than expected.

International expansion faces significant headwinds. In China, cheaper alternatives like ZWCAD claim growing market share. In emerging markets, piracy remains rampant. As growth in developed markets slows, Autodesk's geographic expansion challenges become more pressing.

The commoditization of basic CAD functionality poses long-term risks. As open-source alternatives improve and cloud platforms make software development cheaper, the barriers to creating "good enough" CAD tools continue to fall. Autodesk's premium pricing might become harder to justify for basic use cases.

Valuation concerns persist at current multiples. Trading at over 11x revenue and 40x free cash flow, Autodesk is priced for perfection. Any stumble in execution, any delay in construction adoption, any successful disruption could trigger significant multiple compression.

Verdict:

The durability of Autodesk's moat versus the speed of disruption represents one of the most fascinating battles in enterprise software. The company's strengths—ecosystem lock-in, workflow integration, professional-grade capabilities—are real and powerful. But technology history is littered with "indispensable" companies that became dispensable overnight.

The most likely scenario is neither complete dominance nor sudden disruption, but gradual transformation. Autodesk will probably lose the low end of the market to simpler alternatives while moving upmarket to more complex, higher-value workflows. The construction cloud bet will likely pay off, but take longer than expected. AI will enhance rather than replace their products.

For investors, Autodesk represents a classic quality versus growth dilemma. The business is exceptional, the moat is real, but the growth rate is decelerating and the valuation is full. It's a wonderful company at a fair price, which in today's market might not be enough.

XI. Epilogue & "What Would We Do?"

The counterfactual that haunts Autodesk's history: What if they had moved to the cloud in 2008 instead of 2016? They had the technology, the customer relationships, and the balance sheet to survive the transition. Instead, they watched as younger companies built cloud-native solutions while Autodesk shipped DVDs. Those eight years of hesitation cost them momentum, allowed competitors to establish beachheads, and made the eventual transition far more painful than necessary.

If we were running Autodesk today, the strategic imperatives would be clear but execution would be complex. First, we'd accelerate the AI integration, but not as a separate product—as intelligence woven throughout every workflow. Every click, every design decision, every project outcome would train models that make the next user more productive. The goal isn't to replace designers but to make them superhuman.

Second, we'd double down on construction, but with a twist. Rather than just digitizing existing workflows, we'd reimagine construction from first principles. What if every building component came with embedded sensors? What if project management was predictive rather than reactive? What if payments were automated based on verified work completion? The construction industry is ready for transformation, not just digitization.

Third, we'd address the innovator's dilemma head-on by launching a separate, autonomous unit focused on democratizing design. Call it "Autodesk Elements"—simple, powerful, affordable tools for the next generation of creators. Yes, it would cannibalize some existing revenue. But better we disrupt ourselves than let others do it.

The M&A strategy would focus on three areas: AI capabilities (acquire the best research teams before big tech does), vertical depth (own more of the workflow in each industry), and geographic expansion (buy local leaders in markets where organic growth is slow). The BuildingConnected acquisition playbook—buy the network, not just the product—would guide our approach.

The biggest surprise from researching Autodesk's history is how many times the company nearly failed. Release 13 almost destroyed customer trust. The subscription transition led to an 18% revenue decline. Multiple CEO changes created strategic whiplash. Yet they survived and thrived through adaptability, customer obsession, and the sheer stickiness of embedded workflows.

For founders, Autodesk offers profound lessons. First, opening your platform to developers creates moats that pure product companies can't match. Second, serving professionals who bet their careers on your software creates pricing power that consumer companies can only dream of. Third, business model transitions are survivable if you have conviction and communicate clearly.

For investors, Autodesk demonstrates that boring can be beautiful. CAD software isn't sexy like social media or exciting like electric vehicles. But it's essential, sticky, and generates enormous cash flow. In a world obsessed with growth at any cost, Autodesk's profitable growth and successful transformation remind us that sustainable business models eventually win.

The Autodesk story isn't over. As the physical and digital worlds converge, as AI transforms creative work, as sustainability becomes non-negotiable, the company's next chapter could be even more remarkable than its first. The question isn't whether design software will remain relevant—it's whether Autodesk will continue to define what design software means.

Looking ahead, Autodesk sits at the intersection of multiple massive trends, each representing both opportunity and threat. The company that started by democratizing CAD must now navigate the democratization of AI, the platformization of everything, and the increasing demands for sustainable, efficient design. Their success will depend not on protecting their castle, but on continuing to expand it, one workflow, one industry, one user at a time.

The ultimate lesson from Autodesk's 42-year journey? In enterprise software, revolution happens slowly, then suddenly. The winners aren't always the most innovative or the fastest growing. Sometimes, they're simply the ones who become so essential to how work gets done that imagining life without them becomes impossible. Autodesk achieved that status. The question now is whether they can maintain it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube