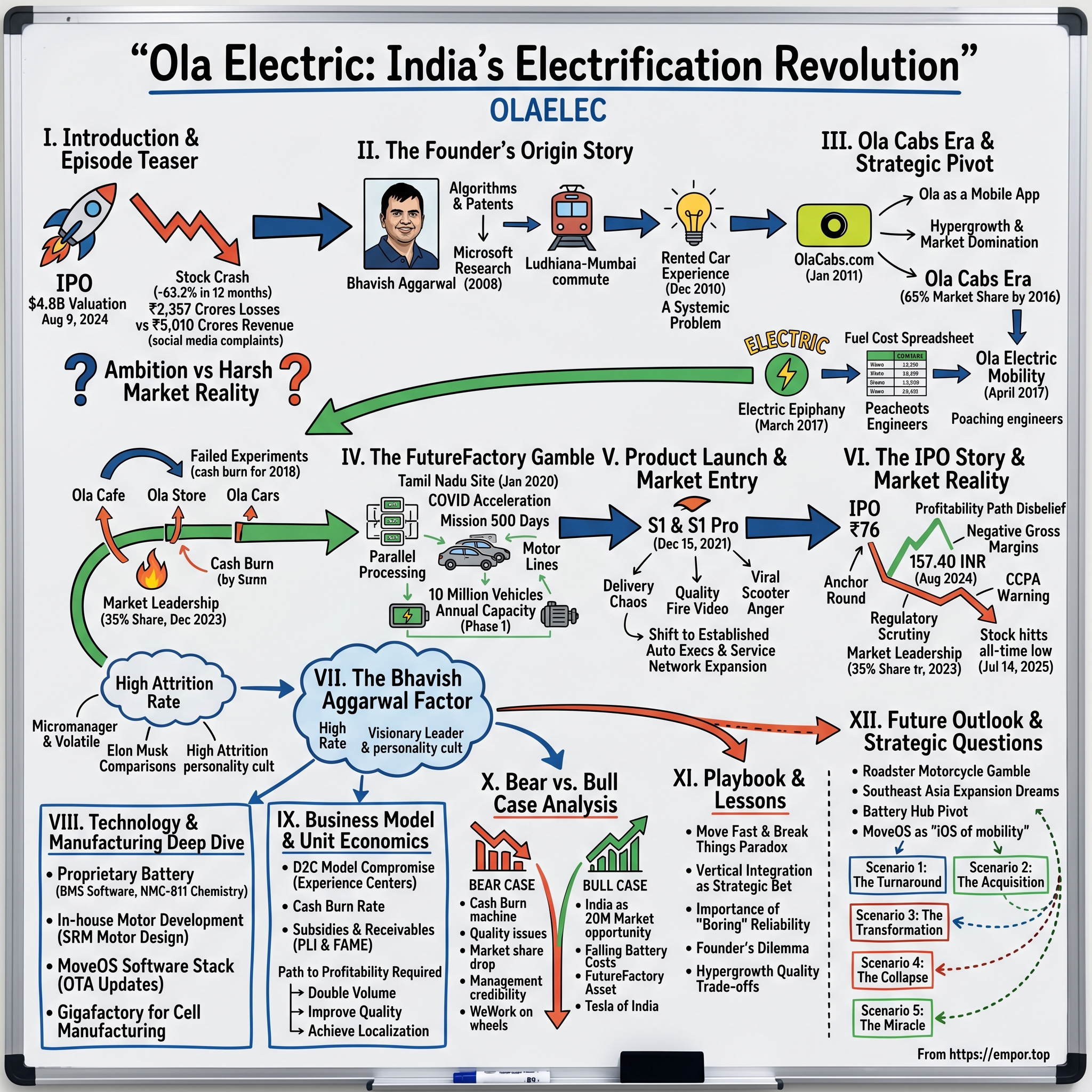

Ola Electric: India's Electrification Revolution

I. Introduction & Episode Teaser

Picture this: August 9, 2024. The trading floor at the National Stock Exchange erupts as Ola Electric Mobility makes its debut. Within hours, the company that started delivering its first scooter just 32 months earlier commands a $4.8 billion valuation. Bhavish Aggarwal, standing at 39 years old with his signature stubble and intense gaze, has just orchestrated one of India's most ambitious IPOs of the year. The euphoria is palpable—India's answer to Tesla, they call it.

Fast forward twelve months. That same stock has hemorrhaged 63.2% of its value. The company that promised to revolutionize Indian mobility burns through cash at an alarming rate—₹2,357 crores in losses against ₹5,010 crores in revenue. Customer complaints flood social media. Videos of Ola scooters catching fire go viral. The narrative has shifted from disruption to dysfunction.

Yet here's what makes this story irresistible: Ola Electric still commands 19.6% of India's electric two-wheeler market. It operates the country's largest integrated EV manufacturing facility. And Bhavish Aggarwal, now worth $2.3 billion, remains utterly convinced he's building the mobility company of the future.

This is the story of how a ride-hailing entrepreneur who once battled Uber decided to take on Hero, Bajaj, and TVS—companies that have dominated Indian roads for generations. It's about the audacity to build a vertically integrated hardware company in a country where most startups stick to software. It's about betting billions that India's 250 million two-wheeler owners are ready to go electric, even when the evidence suggests otherwise. The most fascinating aspect of this tale isn't the technology or the billions raised—it's the sheer velocity of change. Ola Electric receives Rs 73.7 crore incentives under PLI-Auto scheme, becoming the first 2W auto maker in India to qualify. The company that didn't exist as a separate entity until 2017 now operates manufacturing facilities that rival those of companies founded before India's independence.

What we're about to explore is a case study in extreme ambition meeting harsh market reality. It's about what happens when Silicon Valley's "move fast and break things" ethos collides with the unforgiving physics of hardware manufacturing. It's about testing whether India's 280 million two-wheeler riders are ready to abandon the familiar rumble of combustion engines for the silent whir of electric motors.

The numbers tell one story: a company that grew revenue from ₹373 crores in FY22 to ₹5,010 crores in FY24—a 13x expansion in just two years. But the market tells another: a stock that has lost nearly two-thirds of its value since listing, reflecting deep skepticism about whether Ola can deliver on its promises.

This is not just Ola's story. It's India's story—a nation attempting to leapfrog from fossil fuels to electric mobility, from importing technology to manufacturing it, from following global trends to setting them. The outcome will reshape not just Ola's future, but potentially the trajectory of mobility across the developing world.

II. The Founder's Origin Story

The train from Ludhiana to Mumbai takes 28 hours. In 2003, a young Bhavish Aggarwal made this journey countless times, shuttling between his hometown in Punjab and IIT Bombay where he was pursuing computer science. His father sold medical equipment; his mother was a homemaker. Nothing in his middle-class upbringing suggested he would one day command a $2.3 billion fortune or pick public fights with India's most established industrialists.

At IIT Bombay, Aggarwal wasn't the typical entrepreneur-in-waiting. He was the studious type—focused on algorithms, data structures, and systems design. His batchmates remember him as intense, argumentative, and possessed of an almost uncomfortable level of self-confidence. "Bhavish would argue about everything," recalls a classmate. "Whether it was the optimal way to write code or which mess food was better, he had an opinion and would defend it to death."

After graduating in 2008, Aggarwal joined Microsoft Research India in Bangalore—a coveted position for any IIT graduate. Here, he wasn't building apps or websites; he was working on fundamental computer science problems. Between 2008 and 2010, he filed two patents and published three research papers on information retrieval and machine learning. His supervisors noted his exceptional ability to identify patterns in complex data sets—a skill that would later prove invaluable in building Ola's matching algorithms.

But the defining moment came during a weekend trip in December 2010. Aggarwal had rented a car to travel from Bangalore to Bandipur, a wildlife sanctuary 220 kilometers away. Halfway through the journey, the driver stopped the car and demanded more money, threatening to abandon Aggarwal and his companions on the highway unless they paid up. When Aggarwal refused, the driver made good on his threat.

Standing on that empty highway, furious and humiliated, Aggarwal didn't just see a personal inconvenience—he saw a systemic problem. India's taxi and car rental industry was fragmented, unreliable, and ripe for disruption. The country had 1.5 million taxis but no way to reliably book one. Drivers had no steady income; passengers had no recourse for bad service.

Within weeks of returning to Bangalore, Aggarwal quit Microsoft Research. His colleagues thought he'd lost his mind. Why leave a prestigious research position to start a taxi company? His parents were horrified. They hadn't sent him to IIT to become a travel agent.

Aggarwal partnered with Ankit Bhati, his IIT Bombay batchmate who was working at IIT Kanpur. Together, they started OlaCabs.com in January 2011 with ₹3 lakhs—money borrowed from credit cards and friends. The initial model wasn't ride-hailing as we know it today. It was a website where users could book taxis for outstation trips and airport transfers. They signed up a handful of travel agencies and small fleet owners, taking a commission on each booking.

The early days were brutal. Aggarwal would spend mornings cold-calling travel agencies, afternoons debugging the website, and nights handling customer complaints. He personally answered every customer service call, often apologizing for delays and cancellations. The company's "office" was a small apartment in Bangalore's Koramangala neighborhood, where the founders lived and worked.

The breakthrough came when they realized smartphones could change everything. By late 2011, Android phones were becoming affordable in India. Aggarwal saw an opportunity: what if passengers could book a taxi with one tap? What if drivers could accept rides without calling a dispatch center? The entire middleman layer could be eliminated.

They rebuilt Ola as a mobile app, launching it in November 2011. The initial version was buggy and crashed frequently. They had signed up just 20 drivers. On the first day, they got three bookings. Aggarwal personally called each customer to ensure the ride went smoothly.

But something was different about Aggarwal's approach compared to other startup founders of that era. While others focused on capturing the English-speaking, upper-middle-class market, Aggarwal insisted on building for "Bharat"—the real India. The app was designed to work on low-end Android phones. It supported multiple Indian languages. Drivers didn't need to be literate; the interface used voice commands and visual cues.

By early 2012, Ola was completing 100 rides per day. That's when the venture capitalists started calling. Tiger Global, which had backed Flipkart, saw parallels in Ola's trajectory. They invested $5 million in Series A funding. Suddenly, Aggarwal had the resources to think bigger.

What followed was a period of hypergrowth that would define Aggarwal's management philosophy: move fast, dominate the market, figure out the details later. Ola expanded from Bangalore to Mumbai, Delhi, Chennai, and Pune within six months. They launched Ola Auto for autorickshaw bookings—something Uber wouldn't do for years. They introduced Ola Money, a digital wallet, when most Indians still used cash.

The most audacious moment came in 2014 when SoftBank's Masayoshi Son visited India. Son was famous for making investment decisions within minutes of meeting founders. Aggarwal had 30 minutes to pitch. He didn't talk about unit economics or profitability paths. Instead, he painted a vision of 200 million Indians using Ola every day, of transforming how a nation moved.

Son invested $210 million.

With SoftBank's backing, Aggarwal went to war with Uber, which had entered India in 2013. What followed was one of the most intense corporate battles in Indian startup history. Both companies burned through hundreds of millions subsidizing rides. Drivers were offered bonuses that sometimes exceeded their actual earnings. Passengers paid ₹10 for rides that cost ₹100.

But Aggarwal wasn't just copying Uber's playbook. He was innovating for Indian conditions. Ola allowed cash payments when Uber was credit-card only. Ola partnered with autorickshaw unions while Uber focused on cars. Ola launched "Ola Play," letting passengers control music and temperature—features designed for India's harsh climate.

By 2016, Ola had captured 65% of India's ride-hailing market. Merger talks with Uber fell through when Aggarwal refused to cede control. He wanted to build an Indian champion, not sell out to a foreign competitor.

It was during this period that Aggarwal's management style became legendary—and not always in a good way. Former employees describe a culture of extreme intensity. Aggarwal would call meetings at midnight and expect instant responses to emails sent at 3 AM. He once reportedly threw a pen at an executive who couldn't answer a question about driver acquisition costs. Another time, he tore up a presentation in front of the entire leadership team because the font was wrong.

Yet people stayed because Aggarwal had an unusual ability to make them believe they were part of something historic. "He would tell us we weren't just building a company," recalls an early employee. "We were building the future of Indian transportation."

By 2017, Ola was valued at $7 billion and operated in 110 Indian cities. But Aggarwal was already restless. The ride-hailing market was maturing. Growth was slowing. He needed a new mountain to climb.

That's when he noticed something interesting in Ola's data. The company's biggest expense wasn't driver incentives or marketing—it was fuel. If Ola could eliminate fuel costs by switching to electric vehicles, unit economics would transform overnight. Moreover, the Indian government was pushing electrification through subsidies and policy support.

In early 2017, Aggarwal quietly registered a new subsidiary: Ola Electric Mobility Private Limited. Few people noticed. Even fewer understood that this side project would soon consume Aggarwal entirely, leading him to bet everything on becoming India's Elon Musk.

The boy from Ludhiana who once stood stranded on a highway had built one of India's most valuable startups. But that was just the warm-up act. The real audacity was about to begin.

III. The Ola Cabs Era & Strategic Pivot

By 2015, Ola's Bangalore headquarters resembled a war room more than a corporate office. Giant screens displayed real-time ride data from 110 cities. Red dots indicated driver shortages; green showed surplus. Bhavish Aggarwal would stand in front of these screens for hours, personally directing surge pricing and driver allocation like a general commanding troops.

The company was burning $30 million monthly fighting Uber. But Aggarwal saw this as necessary martyrdom. "You can't build an empire without casualties," he told investors during a particularly brutal quarter when losses exceeded $100 million. The strategy was working—Ola completed 1 million rides daily by 2016, compared to Uber's 400,000.

Yet success in ride-hailing masked deeper anxieties. Aggarwal knew that winning against Uber was just surviving, not thriving. He needed Ola to become something more—an ecosystem, a platform, perhaps even a conglomerate. This thinking led to a series of experiments between 2015 and 2017 that would teach him crucial lessons about focus and failure.

First came Ola Cafe in 2015—food delivery with a twist. Meals would be prepared in Ola-operated kitchens and delivered through their cab network. The logic seemed impeccable: utilize idle driver time, leverage existing logistics infrastructure. Within three months, it was clear the model didn't work. Food delivery required different workflows, packaging expertise, and kitchen operations. Ola shut it down, taking a ₹50 crore writeoff.

Next was Ola Store, launched in early 2016—a hyperlocal delivery service for groceries and essentials. Again, the idea appeared synergistic. Ola had the drivers, the technology, and the customer base. But they were competing against focused players like BigBasket and Grofers who understood inventory management and perishables. After burning through ₹200 crores in nine months, Aggarwal pulled the plug.

The most expensive failure was Ola Cars, a used car marketplace launched in late 2016. The thesis: Ola drivers were constantly buying and selling vehicles, so why not intermediate these transactions? The company invested heavily in inspection centers and warranty programs. But used car sales required deep expertise in pricing, quality assessment, and financing—competencies Ola didn't possess. The division was quietly shut down in 2017 after losses exceeded ₹300 crores.

These failures weren't just financial setbacks. They were psychological blows to Aggarwal's self-image as an infallible entrepreneur. Board meetings became tense. SoftBank's representatives questioned whether Ola was losing focus. Tiger Global worried about the cash burn rate. There were whispers about bringing in a professional CEO.

It was during this period of introspection that Aggarwal had his electric epiphany. In March 2017, he was reviewing Ola's unit economics with his CFO. The numbers were sobering. Despite dominant market share, Ola was still losing money on every ride when fully loaded costs were considered. The biggest variable cost after driver incentives? Fuel.

Aggarwal pulled up a spreadsheet and started modeling. What if every Ola vehicle was electric? Fuel costs would drop by 70%. Maintenance expenses would halve. The environmental narrative would attract conscious consumers and ESG-focused investors. The government was offering subsidies through the FAME scheme. The math was compelling.

But there was a problem: electric vehicles suitable for ride-hailing didn't exist in India. The few available models were expensive imports or underwhelming conversions of existing vehicles. If Ola wanted electric vehicles, they would have to make them.

The board thought he was insane. Manufacturing vehicles was a completely different business from operating a ride-hailing platform. It required massive capital investment, deep technical expertise, and patience—not exactly Aggarwal's strongest virtue. But Aggarwal saw it differently. This wasn't diversification; it was vertical integration. Amazon sold books before building AWS. Apple sold computers before making phones.

In April 2017, Aggarwal quietly registered Ola Electric Mobility as a subsidiary. He didn't announce it publicly. He wanted time to build without scrutiny. He poached engineers from Mahindra, TVS, and Bajaj. He hired battery experts from LG Chem and Samsung SDI. He brought in manufacturing specialists from Maruti and Hyundai.

The initial plan was modest: develop an electric autorickshaw for Ola's fleet. Autorickshaws were simpler than cars, cheaper to produce, and represented 40% of Ola's rides. If they could crack this market, they would have proof of concept for larger vehicles.

But Aggarwal's ambitions quickly expanded. During a trip to China in late 2017, he visited BYD and Nio facilities. He saw production lines churning out thousands of electric vehicles daily. He met battery scientists working on next-generation chemistries. He realized India was already a decade behind.

Upon returning, Aggarwal made a decision that would define Ola Electric's trajectory: they wouldn't just assemble vehicles from imported components. They would build everything—batteries, motors, controllers, software—from scratch. It was an audacious goal for a company that hadn't produced a single vehicle.

The funding requirements were staggering. Aggarwal estimated they needed $500 million just to build a factory. Another $300 million for R&D. Plus working capital for operations. The numbers would make even SoftBank pause.

So Aggarwal employed a classic startup strategy: sell the vision before building the product. In December 2017, he announced that Ola would deploy 10,000 electric vehicles across India by 2018. The vehicles didn't exist. The charging infrastructure wasn't ready. But the announcement generated headlines and attracted investor interest.

Tiger Global and Matrix Partners led a $56 million funding round for Ola Electric in early 2018. The money was specifically earmarked for EV development, separate from Ola's ride-hailing operations. This structural separation would prove crucial later when Ola Electric sought independent funding.

The pivot accelerated in 2019 when Aggarwal made another strategic decision: forget autorickshaws, focus on scooters. The logic was data-driven. India sold 20 million two-wheelers annually versus 3 million cars. The average Indian family bought a scooter before a car. The market was dominated by combustion engines with no serious electric alternatives.

But the real catalyst came from an unexpected source: COVID-19.

When India went into lockdown in March 2020, Ola's ride-hailing business collapsed overnight. Daily rides dropped from 2 million to near zero. The company had to lay off 1,400 employees. Revenue evaporated. Survival was uncertain.

For most founders, this would be a crisis. For Aggarwal, it was an opportunity. With ride-hailing in suspended animation, he could focus entirely on Ola Electric. He moved to Tamil Nadu where Ola was building its factory. He spent 18-hour days on the construction site, personally supervising everything from foundation laying to equipment installation.

The pandemic also changed consumer behavior in ways that favored electric vehicles. People wanted personal mobility over shared transportation. Fuel prices were rising. Environmental consciousness was growing. The government announced additional EV subsidies as part of economic stimulus.

By late 2020, Aggarwal was ready to reveal what Ola Electric had been building. Not just a scooter, but an entire ecosystem—manufacturing facility, charging network, service infrastructure. The ride-hailing entrepreneur was about to become an industrialist.

The transformation was remarkable. The same person who couldn't make food delivery work was now attempting something orders of magnitude more complex. But perhaps those failures had taught him valuable lessons. This time, he wouldn't diversify prematurely. This time, he would go deep rather than broad. This time, he would build something that couldn't be easily replicated.

As 2020 drew to a close, Ola Electric had raised over $300 million, construction of the FutureFactory was underway, and prototypes were being tested. The pivot from bytes to batteries was complete. Now came the hard part: actually delivering on the promises.

IV. The FutureFactory Gamble

The land in Pochampalli, Tamil Nadu, stretched for 500 acres—roughly the size of 380 football fields. When Bhavish Aggarwal first visited the site in January 2020, it was barren red earth, scattered with thorny bushes and grazing goats. Local farmers thought he was crazy to pay ₹500 crores for what they considered wasteland. Within 18 months, it would become India's largest integrated electric two-wheeler manufacturing facility.

Aggarwal didn't just want to build a factory; he wanted to build a statement. The facility would be called "FutureFactory"—a name that betrayed his Silicon Valley influences while signaling ambition beyond mere manufacturing. The architectural plans, created by British firm Foster + Partners (who designed Apple Park), featured sweeping curves, solar panel canopies, and floor-to-ceiling windows. This wasn't going to look like the typical Indian automotive plant.

The timing seemed insane. India was entering its strictest COVID lockdown in March 2020, just as construction was supposed to begin. International borders were closed, preventing foreign equipment suppliers from visiting. Supply chains were shattered. Labor was fleeing cities for villages. Any rational entrepreneur would have paused.

Instead, Aggarwal accelerated. He moved into a makeshift office on the construction site, living in a modified shipping container. He instituted "Mission 500"—500 days to go from groundbreaking to mass production. Executives who suggested this timeline was impossible were replaced. "Impossible is a state of mind," Aggarwal would say, echoing Elon Musk's famous philosophy.

The construction approach was unprecedented in Indian manufacturing. Typically, factories are built sequentially—complete the building, install equipment, test systems, begin production. Aggarwal demanded parallel processing. While foundations were being poured in one section, equipment was being installed in another, and production trials were happening in a third. It was chaos, but organized chaos.

The numbers were staggering. The factory would have 10 production lines capable of producing 10 million vehicles annually at full capacity—making it the world's largest two-wheeler facility by output. The investment: ₹2,400 crores, funded through a combination of equity capital and debt. The Tamil Nadu government, eager to establish the state as an EV hub, offered land at subsidized rates and promised infrastructure support.

But building the physical factory was just one challenge. The bigger problem was technology. Unlike traditional scooter manufacturers who source components from suppliers, Ola Electric decided to manufacture critical parts in-house. This meant building capabilities in battery pack assembly, motor winding, controller programming, and frame welding—each requiring different expertise and equipment.

The battery pack assembly line was the crown jewel. Ola imported automated equipment from South Korea and Germany—robotic arms that could spot-weld connections with microscopic precision, testing chambers that simulated years of usage in hours. The investment in this single line exceeded ₹300 crores. But it gave Ola complete control over their most critical component.

The motor manufacturing presented different challenges. Traditional scooter motors are simple mechanical devices. Electric motors require precise electromagnetic engineering. Ola's engineers developed a new permanent magnet synchronous motor design that claimed industry-leading efficiency. But translating lab prototypes to mass production proved nightmarish. Early units overheated. Magnets demagnetized. Controllers failed.

Aggarwal's response was typical: throw more resources at the problem. He hired 200 engineers in three months, poaching talent from Bosch, Continental, and Valeo. He set up an R&D center in Bangalore with equipment worth ₹100 crores. He instituted daily 7 AM review meetings where engineers had to present solutions or face his wrath.

The frame and body manufacturing was outsourced to vendors initially, but Aggarwal wasn't satisfied with quality. In a decision that stunned industry observers, he decided to bring this in-house too. This meant installing massive stamping presses, welding robots, and paint shops—infrastructure typically requiring decades of expertise to operate efficiently.

By December 2020, the factory structure was complete, and equipment installation was underway. But Aggarwal made another audacious decision: instead of starting with one model and gradually expanding, Ola would launch with two variants simultaneously—the S1 and S1 Pro. This meant parallel development of different battery configurations, software systems, and production processes.

The software dimension was equally ambitious. Unlike traditional scooters that are purely mechanical, Ola's vehicles would be "computers on wheels." They would have touchscreens, over-the-air updates, navigation systems, and connectivity features. This required building an entire software stack from scratch—operating system, application layer, cloud infrastructure.

Aggarwal created a 500-person software team split between Bangalore and San Francisco. They worked on everything from battery management algorithms to rider analytics. The development philosophy was pure Silicon Valley: ship fast, fix later. This would later prove problematic when software bugs caused vehicles to malfunction.

The manufacturing philosophy was inspired by Tesla's "alien dreadnought" concept—extreme automation with minimal human intervention. The assembly line featured 3,000 robots performing tasks from battery insertion to quality inspection. The theoretical production rate: one scooter every two seconds. The reality would prove messier.

In August 2021, with the factory barely operational, Aggarwal announced that Ola would begin deliveries in October—just two months away. Industry veterans were incredulous. It typically takes 2-3 years to stabilize a new production line. Ola was attempting it in months.

The first production runs were disasters. Rejection rates exceeded 40%. Batteries didn't fit properly. Software crashed randomly. Paint quality was inconsistent. The production line, designed for 10,000 units daily, was producing barely 100 acceptable units.

But Aggarwal refused to delay the launch. He instituted 24-hour production shifts. Engineers slept on the factory floor, debugging problems in real-time. Quality standards were "adjusted" to meet delivery commitments. It was a high-wire act that would have consequences.

The factory's design included provisions for future expansion. Phase 2 would add battery cell manufacturing—currently, Ola imports cells from LG and assembles them into packs. This would require another ₹5,000 crore investment but would give Ola complete vertical integration. Phase 3 envisioned car manufacturing, though these plans remain conceptual.

The workforce challenges were immense. Pochampalli is rural Tamil Nadu, not exactly a hub of automotive talent. Ola had to recruit workers from surrounding villages, many of whom had never worked in manufacturing. The training program was intensive—six weeks of classroom instruction followed by on-the-job training. Still, error rates remained high.

The supply chain complexity was staggering. Ola worked with 150 suppliers across 10 countries. Components had to arrive just-in-time to avoid inventory costs. But COVID disruptions made scheduling impossible. Semiconductor shortages delayed controller deliveries. Shipping containers were stuck in ports. Aggarwal's solution: stockpile everything, capital efficiency be damned.

By December 2021, the FutureFactory was operational enough to begin customer deliveries. The first scooter rolled off the production line in a ceremony attended by Tamil Nadu's Chief Minister. Aggarwal, in typical fashion, rode it himself, performing wheelies for the cameras.

The gamble appeared to have paid off. Ola had built India's most advanced EV manufacturing facility in record time. The factory could theoretically produce more electric scooters than the rest of India combined. The vertical integration gave Ola control over quality and costs.

But the real test wasn't building the factory—it was operating it efficiently. Manufacturing isn't like software where bugs can be fixed with updates. Physical products have to work perfectly from day one. Customers who pay ₹1 lakh for a scooter expect reliability, not beta testing.

As 2022 began, the FutureFactory was producing 1,000 units daily, far below its 10,000-unit capacity. Quality issues persisted. Costs were higher than projected. The automated systems required constant manual intervention. The alien dreadnought was more like an expensive experiment.

Yet Aggarwal remained undaunted. In interviews, he compared the FutureFactory to Tesla's Fremont facility—initial struggles followed by eventual dominance. He pointed to production improvements: rejection rates down from 40% to 15%, daily output rising steadily, software updates fixing early issues.

The factory had consumed over ₹3,000 crores in capital expenditure by early 2022, with another ₹2,000 crores planned for expansion. For context, Hero MotoCorp's annual capex is around ₹700 crores. Ola was betting the farm on manufacturing excellence—a bet that would either establish them as India's EV champion or become a cautionary tale about hubris in hardware.

V. Product Launch & Market Entry

December 15, 2021. The Ola Experience Center in Bangalore's Indiranagar neighborhood was packed with customers, journalists, and social media influencers. After 16 months of promises, delays, and relentless marketing, the first Ola S1 Pro was finally being delivered to a retail customer. Bhavish Aggarwal personally handed over the keys to a software engineer named Rakesh, who had paid ₹1.3 lakhs for the privilege of owning vehicle number 001.

Within three hours, Rakesh's S1 Pro was trending on Twitter—but not for reasons Ola wanted. The scooter's touchscreen had frozen while riding. The regenerative braking engaged unexpectedly, nearly causing an accident. The mobile app couldn't connect to the vehicle. Rakesh's thread documenting these issues garnered 50,000 retweets. The dream launch had become a nightmare.

The S1 Pro was supposed to be revolutionary. It featured a 3.97 kWh battery promising 181 kilometers of range—more than any competitor. The top speed of 116 kmph made it the fastest electric scooter in India. The 7-inch touchscreen dashboard offered navigation, music playback, and even cruise control. The price of ₹1.3 lakhs positioned it as a premium product competing with petrol-powered 125cc scooters.

But the market entry strategy was even more audacious than the product itself. Ola decided to completely bypass traditional dealerships. Customers would book online, configure their scooters digitally, and receive home delivery. Service would be provided through company-owned centers. It was the Tesla model transplanted to India.

The initial booking process in September 2021 demonstrated both the opportunity and the chaos. Ola opened reservations for just ₹499, promising delivery within 60 days. The response was overwhelming—100,000 bookings in 24 hours. The website crashed repeatedly. Payment gateways failed. Customers who successfully booked received no confirmation for days.

Aggarwal spun this chaos as success. "We've received overwhelming response from customers," he tweeted, sharing graphs of booking momentum. But internally, panic was setting in. The factory could produce maybe 500 units daily. At that rate, fulfilling 100,000 orders would take seven months. And that assumed everything worked perfectly—which it didn't.The product issues were catastrophic. The first batch of scooters delivered to 100 customers in Bengaluru and Chennai faced unsatisfactory performance and poor build quality. One customer reported that in less than 6km, his S1 Pro started making screeching noises and lights began malfunctioning. The product felt rushed into production with power delivery requiring significant fine-tuning, and many headline features were still in beta or even alpha testing stages.

The root cause was Aggarwal's insistence on launching before the product was ready. Engineers had flagged critical issues: the battery management system needed months more testing, the touchscreen software was buggy, the regenerative braking calibration was inconsistent. But Aggarwal overruled them all. "We'll fix it with OTA updates," became the standard response—forgetting that hardware problems can't be solved with software patches.

The delivery chaos compounded customer frustration. Ola promised deliveries within 60 days but took six months or more for many customers. The company blamed semiconductor shortages, logistics issues, and "overwhelming demand." But the real problem was production. The FutureFactory, designed for 10,000 units daily, was producing barely 100 acceptable units initially.

When scooters finally arrived, the problems multiplied. Range claims of 181 kilometers translated to 80-90 kilometers in real-world conditions. The cruise control feature didn't exist despite being advertised. The mobile app connectivity failed randomly. Some scooters simply refused to start, leaving owners stranded.

The service infrastructure wasn't ready either. Ola had promised doorstep service—technicians would come to customers' homes for repairs. But they had fewer than 50 trained technicians nationwide. Customers waited weeks for basic issues to be addressed. Spare parts weren't available. The company-owned service centers were overwhelmed.

Social media became a battlefield. Twitter was flooded with complaints tagged #OlaScamster. YouTube reviews turned increasingly negative. A particularly damaging video showed an S1 Pro catching fire while charging—it garnered 2 million views in 48 hours. Competitors' marketing teams amplified these issues, sensing opportunity in Ola's struggles.

Aggarwal's response was characteristic: attack mode. He personally replied to critics on Twitter, often aggressively. He accused traditional manufacturers of spreading "FUD" (fear, uncertainty, doubt). He shared selective data showing improving quality metrics while ignoring fundamental problems. When a customer posted about his scooter breaking down, Aggarwal replied that the customer was "riding it wrong."

But the market reality couldn't be tweeted away. By March 2022, Ola's order cancellations exceeded new bookings. Customers who had paid full amounts months earlier demanded refunds. The company instituted a "no questions asked" refund policy, hemorrhaging cash as thousands canceled orders.

The pricing strategy added another layer of complexity. The S1 Pro was priced at ₹1.3 lakhs before subsidies, dropping to ₹1.1 lakhs with FAME incentives in certain states. But these subsidies required meeting specific localization requirements. When auditors found that Ola's claimed localization percentages were inflated, subsidy disbursements were delayed, forcing the company to absorb the discount.

To salvage the situation, Ola launched the S1 in September 2022—a cheaper variant with a 3 kWh battery priced at ₹99,999. The strategy was to capture price-sensitive customers while fixing quality issues on the premium model. But this created SKU complexity the factory wasn't prepared for, further complicating production.

The software updates promised to fix everything became a joke. MoveOS 2 was supposed to address connectivity issues but created new problems with battery percentage display. MoveOS 3 promised navigation but drained the battery faster. Each update felt like one step forward, two steps back.

By mid-2022, Ola made strategic pivots. They slowed production to focus on quality. They hired experienced automotive executives from Maruti and Hyundai to professionalize operations. They expanded the service network, adding 200 centers in six months. They instituted stricter quality control, accepting higher rejection rates.

The product portfolio expanded rapidly—perhaps too rapidly. In August 2023, Ola announced the S1 Air at ₹79,999 and the S1 X series starting at ₹69,999. Each new model was positioned to capture different market segments: urban commuters, college students, delivery riders. But this proliferation strained an already struggling production system.

The direct-to-consumer model, initially seen as revolutionary, proved problematic. Without dealerships to handle customer issues locally, every problem escalated to corporate. The experience centers, designed as Apple Store-like showcases, became complaint centers where angry customers demanded answers.

Competition intensified as established players launched their electric offerings. TVS iQube, Bajaj Chetak, and Hero Vida arrived with less ambitious specifications but better reliability. They leveraged existing dealer networks and service infrastructure. Their message was clear: boring but dependable beats exciting but unreliable.

Yet somehow, despite all these issues, Ola maintained market leadership. By December 2023, they had delivered over 300,000 scooters. The company claimed a 35% market share in electric two-wheelers. How? Partly through aggressive pricing, partly through constant marketing, but mostly through the reality that even flawed electric scooters were cheaper to operate than petrol vehicles as fuel prices soared.

The December 2023 launch of the S1 X+ at ₹89,999 marked a turning point. This model incorporated lessons from two years of customer feedback. The software was more stable. The build quality improved. The range claims became realistic. Customer reviews, while not glowing, turned less hostile.

But the reputational damage was done. Ola Electric became synonymous with overpromising and underdelivering. The brand that was supposed to represent India's EV future instead became a cautionary tale about the perils of rushing hardware to market.

As 2024 began, Ola faced a choice: continue the hypergrowth strategy that had brought them market leadership but also massive losses, or slow down to focus on profitability and quality. The upcoming IPO would force this decision. Public market investors wouldn't tolerate the "growth at all costs" mentality that private investors had funded.

The product launch had achieved its primary goal: establishing Ola as a serious player in electric vehicles. But it had also revealed the enormous gap between software-style iteration and hardware manufacturing excellence. In Aggarwal's race to disrupt the industry, he had perhaps disrupted his own company more than anyone else.

VI. The IPO Story & Market Reality

The Bombay Stock Exchange trading floor buzzed with unusual energy on August 9, 2024. Ola Electric's IPO—priced at ₹76 per share—opened for trading at ₹79.60, a modest 4.7% premium. Within minutes, the stock rocketed to ₹91, valuing the company at nearly $5 billion. Bhavish Aggarwal, watching from the NSE building, allowed himself a rare smile. The company that didn't exist seven years ago was now worth more than Ashok Leyland, a 76-year-old automotive giant.

The IPO process had begun 18 months earlier in hushed boardrooms and late-night strategy sessions. Ola Electric needed capital—desperately. The company had burned through over ₹6,000 crores since inception. The FutureFactory expansion required another ₹3,000 crores. Battery cell manufacturing ambitions demanded ₹5,000 crores more. Private investors were growing weary of endless funding rounds.

The timing seemed perfect. India's stock markets were hitting record highs. Retail investors were hungry for new-economy stocks. The EV narrative was compelling—climate change, government support, technological disruption. Investment bankers from Goldman Sachs and Kotak Mahindra painted a picture of Ola as "India's Tesla," potentially worth $20 billion by 2030.

But preparing for the IPO revealed uncomfortable truths. The company's financials were a disaster zone. FY23 revenue of ₹2,631 crores came with losses of ₹1,472 crores. FY24 looked better—₹5,010 crores in revenue—but losses had ballooned to ₹2,357 crores. The company was losing ₹47 for every ₹100 earned.

The draft red herring prospectus (DRHP) filed in December 2023 required careful crafting. How do you explain to investors that you're losing money on every scooter sold? The answer: focus on the future. The document emphasized market leadership, vertical integration advantages, and the massive TAM (Total Addressable Market) of 20 million two-wheelers annually.

The risk factors section ran 50 pages. "We have a history of net losses and may continue to incur losses," read one understated warning. Others were more specific: dependency on government subsidies, quality control challenges, concentrated manufacturing risk, competitive threats, and the ominous "our Founder and Chairman's behavior could adversely impact our reputation."

That last risk factor deserved its own prospectus. Aggarwal's Twitter feuds had become legendary. He had publicly fought with comedian Kunal Kamra over service issues, with automotive journalists over reviews, and with anyone who questioned Ola's quality. Investment bankers begged him to stay quiet during the IPO process. He agreed, then immediately tweeted about "legacy manufacturers spreading lies."

The valuation exercise was contentious. Ola wanted $8 billion—a multiple of 1.6x forward revenues. Bankers suggested $5-6 billion was more realistic. Comparable companies like Ather Energy were valued at 0.8x revenues. Even loss-making EV companies globally traded at 1-2x revenues. But Aggarwal insisted Ola deserved a premium for market leadership and vertical integration.

The anchor investor roadshow in July 2024 was grueling. Aggarwal and CFO Harish Abichandani met 200 institutional investors across Mumbai, Singapore, London, and New York. The questions were brutal. Why were gross margins negative? When would the company turn profitable? How sustainable was the market share given quality issues? What happened if subsidies disappeared?

Aggarwal's answers walked a tightrope between confidence and credibility. Gross margins would turn positive by Q3 FY25 through scale and cost reduction. Profitability would come by FY27. Market share would stabilize around 30-35%. Subsidies were helpful but not essential—the fundamental economics worked without them.

Foreign investors were skeptical. EV companies globally were struggling. Arrival had gone bankrupt. Canoo and Lordstown Motors were on life support. Even established players like Rivian were burning cash rapidly. Why would Ola be different?

The answer, Aggarwal argued, was India. The country's two-wheeler market was 20x larger than its car market. Fuel prices were rising faster than electricity costs. The government was committed to electrification. Unlike Western markets where EVs competed with efficient gasoline vehicles, Indian two-wheelers were inherently inefficient—perfect for disruption.

Domestic institutions were more receptive. They understood India's consumption story, the aspiration for personal mobility, the environmental pressures. Several mutual funds committed to anchor investments. But they demanded a valuation haircut. The final anchor round raised ₹2,763 crores at ₹72-76 per share—a $4.5 billion valuation, far below Aggarwal's aspirations.

The retail portion of the IPO opened on August 2, 2024. The response was mixed. While institutional investors oversubscribed their portion 5x, retail subscription was just 1.5x. The grey market premium—unofficial trading before listing—was barely 5%. The market was interested but not excited.

The IPO raised ₹6,146 crores—₹5,500 crores in fresh capital and ₹646 crores as offer-for-sale from existing investors. Notably, SoftBank didn't sell, signaling long-term confidence. Tiger Global sold partially, booking partial profits on their early investment.

The listing day started well. The stock opened strong, traded actively, and closed at ₹85—a 12% premium. Media coverage was overwhelmingly positive. "Ola Sparks EV Revolution," screamed headlines. Aggarwal did victory laps on television, promising to make India the "EV capital of the world."

But reality set in quickly. Within a week, the stock dropped to ₹78, barely above the issue price. The first quarterly results as a public company, announced in November 2024, were disappointing. Revenue grew just 15% quarter-on-quarter. Losses remained stubbornly high. Worse, the company revealed that 25,000 scooters were sitting in inventory due to "quality hold"—they needed repairs before delivery. The aftermath was brutal. Ola Electric Mobility share prices hit an all-time low on March 3, down more than 60% from its peak. OLAELEC reached its all-time high on Aug 20, 2024 with the price of 157.40 INR, and its all-time low was 39.60 INR and was reached on Jul 14, 2025. The company that had promised to revolutionize Indian mobility was now trading at less than half its IPO price.

The market's verdict was harsh but clear. By the quarter ending December 2024, Ola Electric Mobility posted a net loss of 5.64 billion rupees ($65 million), up from 3.8 billion ($44 million) a year ago. Revenue growth had stalled. Market share was eroding. The IPO proceeds of ₹5,500 crores were being consumed at an alarming rate.

Institutional investors who had bought during the anchor round faced massive losses. Mutual funds that had positioned Ola as a play on India's EV future were forced to mark down their holdings. Retail investors who had bought on listing day, dreaming of Tesla-like returns, watched their investments evaporate.

The regulatory scrutiny intensified post-IPO. In October 2024, India's consumer rights enforcement agency sent Ola a warning letter, seeking a legal explanation for the 10,664 consumer complaints. SEBI questioned the company's disclosure practices. Tax authorities examined the PLI subsidy claims. Being public meant every misstep was magnified.

The talent exodus accelerated. In the last quarter of 2024, a slew of executives left the company, including the chief technical officer, chief marketing officer, chief people officer, chief business officer, and head of sales. In April the same year, Ola Electric's CEO resigned just three months after he took the reins, and its chief financial officer departed the next month. The revolving door of senior management created strategic paralysis.

Sales momentum collapsed. Only 8,647 Ola scooters were registered in February this year, down from nearly 34,000 a year ago. Competition from Bajaj, TVS, and new entrants like Ather Energy intensified. Customers who might have taken a chance on Ola when it was the only option now had alternatives from trusted brands.

The response from management was predictable: reorganization and cost-cutting. To stem its losses, Ola is cutting 1,000 jobs across procurement, fulfillment, customer relations, and charging infrastructure. But this created a vicious cycle—fewer employees meant worse service, which meant fewer sales, which required more cost-cutting.

The quarterly earnings calls became exercises in damage control. Analysts questioned everything: Why were warranties provisions so high? When would battery costs decline? How sustainable was the claimed market share? Aggarwal's responses grew increasingly defensive, often blaming "short-term market dynamics" and "competitive pressures."

The governance issues that investors had flagged during the IPO process materialized. Aggarwal's 47% voting control through differential voting rights meant minority shareholders had little say. Board meetings reportedly involved more dictation than discussion. Independent directors resigned citing "personal reasons"—code for irreconcilable differences.

By mid-2025, the stock had become a battleground between believers and skeptics. Day traders loved the volatility—the stock could swing 10% in a single session. Long-term investors, however, were fleeing. The promise of becoming "India's Tesla" seemed increasingly hollow as Tesla itself struggled globally.

The FY25 results, announced in May 2025, provided no relief. Sales declined 9.90% to Rs 4514.00 crore in the year ended March 2025 as against Rs 5010.00 crore during the previous year ended March 2024. The company guided for lower revenues in FY26, citing "market headwinds" and "strategic recalibration."

The IPO that was supposed to validate Ola Electric's business model had instead exposed its fundamental weaknesses. Public market investors, unlike private VCs, demanded profits, not promises. They wanted consistent execution, not constant pivots. They valued boring reliability over exciting dysfunction.

As the first anniversary of the IPO approached in August 2025, Ola Electric's market capitalization stood at roughly ₹18,000 crores—a destruction of over ₹30,000 crores in shareholder value. The boy from Ludhiana who had built two unicorns was learning that public markets were far less forgiving than private investors.

The IPO story wasn't over—companies can recover from difficult debuts. But it had fundamentally changed Ola Electric's trajectory. The luxury of long-term thinking was gone, replaced by quarterly pressures. The ability to pivot rapidly was constrained by public disclosure requirements. The founder's cult of personality was being questioned by governance advocates.

For Aggarwal, the IPO had been both a triumph and a trap. He had achieved the rare feat of taking a company public within seven years of founding. But he was now accountable to thousands of shareholders who cared more about returns than revolution. The question was whether he could adapt to these new realities or whether Ola Electric would become another cautionary tale of premature public listing.

VII. The Bhavish Aggarwal Factor

The WhatsApp message arrived at 2:47 AM on a Tuesday in March 2023. "Why is production only at 73% of target? Meeting in 30 minutes. Factory floor." Every senior manager at Ola Electric knew what this meant—Bhavish Aggarwal was in one of his moods. By 3:20 AM, bleary-eyed executives stood in a semicircle as Aggarwal interrogated each one. When the head of quality control couldn't immediately explain a 0.3% increase in defect rates, Aggarwal grabbed the production report from his hands, tore it in half, and threw it on the floor. "This is what I think of excuses," he said, before walking away.

This wasn't unusual. This was Tuesday.

Understanding Ola Electric requires understanding Bhavish Aggarwal—his brilliance, his brutality, and his bizarre ability to inspire loyalty despite behavior that would be considered abusive in most corporate settings. At 39, he had built two unicorns, commanded a $2.3 billion fortune, and been named to Time's 100 Most Influential People in 2018. He was also, by numerous accounts, one of the most difficult bosses in Indian corporate history.

The numbers tell one story: under Aggarwal's leadership, Ola Electric captured market leadership in an industry that didn't exist five years ago. The human cost tells another: the company's attrition rate hit 47.48% in FY2023, meaning nearly half the workforce left within a year. For context, the Indian IT industry—notorious for high turnover—averages 15-20%.

Former employees describe a culture of fear mixed with exhilaration. "Working for Bhavish was like being in an abusive relationship with someone brilliant," says a former VP who requested anonymity. "He would humiliate you in public, then pull you aside and share a vision so compelling you'd forget the humiliation. Until the next time."

The stories are legendary within Indian startup circles. There was the time Aggarwal made the entire leadership team stand for a two-hour meeting because someone had been late. The incident where he threw a laptop across the room when shown a competitor's product. The famous "pen incident" where he allegedly threw a pen at an executive's face during a disagreement about pricing strategy.

Yet people stayed—at least initially. Why? Because Aggarwal possessed an unusual combination of traits that made him both insufferable and irresistible as a leader. He had a photographic memory for numbers, able to recall obscure metrics from meetings months ago. He worked 18-hour days and expected the same from others. Most importantly, he had an almost mystical ability to make people believe they were part of something historic.

"Bhavish doesn't sell you a job, he sells you a mission," explains a current employee who has survived three years at Ola Electric. "He makes you feel like you're not just building scooters, you're transforming how a billion people move. That's intoxicating, especially for young engineers who want to change the world."

The Elon Musk comparisons were inevitable and somewhat warranted. Both were micromanagers who involved themselves in minute technical details. Both had volatile personalities and Twitter addictions. Both promised to revolutionize transportation. But while Musk's eccentricities were often dismissed as "genius quirks" in Silicon Valley, Aggarwal operated in India's more hierarchical corporate culture where such behavior was simultaneously more shocking and more tolerated.

Aggarwal's management philosophy, if it could be called that, was simple: extreme pressure produces extreme results. He believed that comfortable employees produced mediocre products. Every interaction was a test. Every meeting was a trial. Every decision was a battle. This approach had worked in building Ola Cabs—the existential fight with Uber required wartime leadership. But manufacturing scooters wasn't war; it was precision engineering requiring patience and systematic improvement.

The social media feuds became increasingly problematic post-IPO. When comedian Kunal Kamra posted about his malfunctioning Ola scooter, Aggarwal personally attacked him on Twitter, calling him a "failed comedian" and suggesting he didn't know how to ride properly. When an automotive journalist wrote a critical review, Aggarwal accused him of being paid by competitors. These weren't CEO communications; they were tantrums.

The board tried to intervene. Independent directors suggested hiring a professional CEO while Aggarwal focused on vision and strategy. PR consultants begged him to hire a social media manager. Investors privately expressed concerns about reputational risk. Aggarwal's response was typical: he knew better than everyone else.

His personal wealth—$2.3 billion according to Forbes—insulated him from consequences. When board members pushed too hard, he reminded them of his 47% voting control. When investors complained, he pointed to market share numbers. When employees quit, he said they weren't "mission-aligned" anyway. The money had made him untouchable and he knew it.

But there was another side to Aggarwal that explained his continued influence. He lived modestly despite his wealth, driving an Ola scooter to work and living in a relatively simple apartment. He was vegetarian, teetotal, and devoted to his parents who still lived in Ludhiana. He could be surprisingly generous, personally funding education for employees' children and medical treatments for their families.

He also had moments of genuine vision that reminded everyone why they followed him. During a 2023 town hall, he spoke for two hours without notes about India's energy future, weaving together insights about battery chemistry, grid infrastructure, and demographic trends into a compelling narrative about why Ola Electric would inevitably succeed. Employees left energized, forgetting the previous week's humiliations.

The cultivation of a personality cult was deliberate. Aggarwal's face was everywhere in Ola offices—on posters, screensavers, even coffee mugs. Company communications referred to him as "Bhavish" never "Mr. Aggarwal," creating false intimacy. His birthday was celebrated like a festival with mandatory attendance. New employees underwent "Bhavish orientation" where they learned his preferences, his triggers, and most importantly, how to survive his scrutiny.

The inner circle consisted of roughly a dozen executives who had proven their loyalty through years of abuse. They were handsomely compensated—salaries often 50% above market rates plus substantial equity. More importantly, they had learned to navigate Aggarwal's moods, knowing when to push back and when to submit. They formed a protective buffer between Aggarwal and the rest of the organization.

But even the inner circle wasn't immune. In 2024, Aggarwal's longtime CFO—who had been with him since Ola Cabs—resigned after Aggarwal publicly berated him during an investor call for not answering a question quickly enough. The CTO, recruited from Tesla, lasted eight months before leaving, reportedly telling colleagues that "Elon was difficult, but Bhavish is impossible."

The impact on company culture was toxic. Employees learned to hide problems rather than surface them. Meetings became theatrical performances where everyone tried to say what Aggarwal wanted to hear. Innovation slowed because people were afraid to take risks that might trigger his wrath. The company that was supposed to out-innovate established players was becoming paralyzed by its founder's personality.

International expansion plans were complicated by Aggarwal's reputation. European partners who Googled him found articles about his Twitter feuds and management style. Potential overseas hires declined offers after speaking to former employees. One European battery supplier reportedly refused to work with Ola Electric specifically because of concerns about Aggarwal's behavior.

The comparison to other Indian entrepreneurs was stark. While Byju Raveendran of Byju's was known for aggressive expansion and Vijay Shekhar Sharma of Paytm for his volatility, Aggarwal combined the worst traits of both with an added layer of personal cruelty. Even in India's founder-friendly ecosystem, he was an outlier.

Yet the question remained: could Ola Electric succeed despite Aggarwal, or was his driven personality essential to its existence? The company wouldn't exist without his vision and drive. But his behavior was now actively hampering its growth. It was the classic founder's dilemma, amplified by a personality that seemed almost designed to create chaos.

As 2025 progressed, the board faced an impossible choice. Removing Aggarwal would likely cause a collapse in employee morale and investor confidence—he was Ola Electric in many ways. But keeping him meant continued dysfunction, talent exodus, and reputational damage. There was no good answer, only degrees of bad ones.

The tragedy was that Aggarwal's technical vision was often brilliant. His insights about battery technology, his understanding of Indian consumer behavior, his strategic thinking about vertical integration—all were genuinely impressive. But these gifts were overshadowed by a personality that seemed incapable of normal human interaction.

In the end, the Bhavish Aggarwal factor was both Ola Electric's greatest asset and its biggest liability. He was the visionary who imagined an electric future for India and the tyrant who made that future harder to achieve. He was proof that in startups, founder psychology matters as much as business models—perhaps more.

VIII. Technology & Manufacturing Deep Dive

Inside the clean room at Ola's Bangalore R&D facility, six engineers huddle around a dismantled battery pack, its 6,720 individual cells arranged in perfect geometric patterns like a high-voltage honeycomb. The lead engineer, poached from Samsung SDI eighteen months ago, points to a specific weld point that failed during thermal runaway testing. "This," she says, "is why Tesla recalled 400,000 vehicles. And this is what keeps me awake at night."

The technical challenges Ola Electric faced weren't just about building scooters—they were about mastering technologies that had taken established manufacturers decades to perfect, then integrating them in ways nobody had attempted before. The ambition was staggering: develop proprietary battery management systems, design motors without rare earth elements, create over-the-air update capabilities for two-wheelers, and manufacture everything at a scale that would make unit economics work.

The battery pack was the heart of the challenge. Unlike cars where batteries can be floor-mounted, scooters required packaging cells in irregular spaces while maintaining center of gravity. Ola's solution was a custom 4680 cell configuration—larger cylindrical cells that Tesla had popularized but nobody had adapted for two-wheelers. The advantages were clear: 30% better energy density, improved thermal management, and lower manufacturing costs. The execution was nightmarish.

The first problem was sourcing. Ola initially partnered with LG Energy Solution for cells, but supply constraints forced them to dual-source from Contemporary Amperex Technology (CATL). But cells from different manufacturers had slightly different characteristics—different internal resistance, different degradation curves, different thermal profiles. The battery management system had to accommodate these variations while maintaining consistent performance.

The BMS itself was a marvel of engineering paranoia. It monitored individual cell voltages 1,000 times per second, predicted failure patterns using machine learning, and could isolate problematic cells before they affected the pack. The software contained over 2 million lines of code—more than a modern fighter jet. But complexity meant bugs, and bugs in battery systems meant fires.

The thermal management system was equally sophisticated. Unlike air-cooled systems used by competitors, Ola developed a phase-change material cooling system. Special waxes absorbed heat during high-load conditions, then dissipated it slowly during idle periods. This passive system added no moving parts while extending battery life by an estimated 40%. But the waxes were expensive and manufacturing them consistently proved difficult.

The motor development told a different story of ambition meeting reality. Aggarwal had mandated developing motors without rare earth permanent magnets—both for cost reasons and to avoid supply chain dependencies on China. The engineering team designed a switched reluctance motor that used electromagnetic fields rather than permanent magnets. The design was theoretically superior: cheaper, more reliable, better torque characteristics.

But switched reluctance motors were notoriously difficult to control. They required precise timing of electromagnetic pulses, sophisticated control algorithms, and extensive calibration. Early prototypes sounded like angry washing machines. The vibration was so severe that test riders complained of numbness in their hands. It took 18 months and ₹200 crores in R&D to achieve acceptable refinement.

The manufacturing process for these motors was equally complex. The stator winding required robots capable of sub-millimeter precision, winding copper wire at specific tensions to achieve optimal electromagnetic fields. The rotor laminations had to be stacked with tolerances of 10 microns—thinner than human hair. Any deviation affected efficiency, creating heat that degraded performance.

The vehicle control unit (VCU) was Ola's attempt to create a "brain" for their scooters. Unlike traditional vehicles with distributed control systems, Ola centralized everything into a single unit. The VCU managed motor control, battery management, connectivity, user interface, and safety systems. It was running a custom Linux-based operating system that Ola developed from scratch.

This centralization had advantages: faster response times, better integration, easier updates. But it also created a single point of failure. When the VCU crashed—which happened frequently in early models—the entire scooter became inoperable. Riders reported scooters suddenly dying in traffic, displays freezing, and random acceleration or braking. Each incident was a software emergency requiring immediate patches.

The over-the-air update capability was supposed to be Ola's killer feature. Like Tesla, they could fix problems and add features remotely. MoveOS, their operating system, supported everything from performance tuning to adding new sound effects. But OTA updates for vehicles were far more complex than smartphones. You couldn't update a scooter doing 60 kmph on a highway.

The update process required sophisticated state management. The scooter had to verify it was stationary, adequately charged, and in a safe location. The update had to be atomic—either completely successful or rolled back entirely. Any corruption could brick the vehicle. Early updates had a 15% failure rate, leaving customers with dead scooters until technicians could manually reflash the firmware.

The manufacturing integration at FutureFactory was where all these technologies converged—or collided. The assembly line had to handle battery packs from two suppliers, motors with different calibration requirements, and VCUs running different software versions. The MES (Manufacturing Execution System) tracking all this was a custom-built monster that frequently crashed under load.

The quality control systems were particularly sophisticated. Every scooter underwent 147 automated tests before leaving the factory. Cameras using computer vision checked paint quality. Dynamometers tested motor performance. Thermal cameras monitored battery temperatures during charge cycles. X-ray machines verified weld integrity. The data generated was enormous—each scooter produced 3GB of quality data.

But sophisticated didn't mean effective. The automated systems had high false-positive rates, flagging good scooters as defective. They also missed subtle issues that experienced technicians would catch—unusual sounds, slight vibrations, minor alignment issues. Ola had to add human quality inspectors, defeating the purpose of automation.

The cell manufacturing ambitions represented the next level of complexity. Ola announced plans to produce lithium-ion cells at their Gigafactory, targeting 5GWh capacity initially, expanding to 20GWh. This would require mastering electrode coating, cell assembly, formation cycling, and aging—processes that companies like Panasonic had spent decades perfecting.

The chemistry chosen was NMC-811 (80% nickel, 10% manganese, 10% cobalt)—offering high energy density but notorious for thermal instability. The manufacturing process required clean rooms with humidity below 1%, precise coating thicknesses measured in microns, and formation cycling taking weeks. The capital investment was staggering: ₹5,000 crores for initial capacity.

But cell manufacturing wasn't just about equipment—it was about expertise. The global talent pool for cell manufacturing was tiny, mostly concentrated in East Asia. Ola hired aggressively, offering 3x salaries to Korean and Japanese engineers. But cultural integration proved difficult. The methodical approach of experienced cell engineers clashed with Ola's "move fast" culture.

The software stack complexity continued to grow. Beyond the vehicle software, Ola built cloud infrastructure to manage fleet data, customer apps for iOS and Android, dealer management systems, service center software, and charging network management platforms. Each system had to integrate seamlessly while handling millions of transactions daily.

The connectivity features added another layer of complexity. Each scooter had an embedded SIM card, GPS module, and Bluetooth connectivity. They generated continuous telemetry: location, speed, battery status, error codes, usage patterns. This data streamed to Ola's servers, requiring massive infrastructure to process and store. The monthly AWS bill exceeded ₹15 crores.

The R&D operations spread across three continents added coordination challenges. The Bangalore center focused on software and electronics. The UK facility, acquired from a defunct EV startup, worked on next-generation motors. The California office, staffed with ex-Tesla engineers, developed autonomous features that seemed wildly premature for scooters.

The patent portfolio grew rapidly but chaotically. Ola filed over 200 patents covering everything from battery pack designs to handlebar interfaces. But many were defensive patents with little commercial value. The legal team struggled to identify which innovations were genuinely protectable versus obvious iterations of existing technology.

By 2025, Ola Electric had built impressive technical capabilities. They had developed proprietary technologies across the entire vehicle stack. They had created manufacturing processes that, while imperfect, were uniquely theirs. They had assembled a team of world-class engineers working on cutting-edge problems.

But the question remained: was all this complexity necessary? Competitors like Ather Energy built successful products using off-the-shelf components and proven technologies. TVS and Bajaj leveraged their existing capabilities rather than reinventing everything. Ola's vertical integration and technical ambition were either visionary or foolish—only time would tell.

The technology story of Ola Electric was ultimately about the tension between ambition and execution. Every technical decision—from cell chemistry to motor design—represented a bet that complexity could be managed, that integration would create advantages, that software could solve hardware problems. These bets had made Ola Electric both the most technically advanced and most technically troubled EV company in India.

IX. Business Model & Unit Economics

The spreadsheet on the CFO's laptop told a story of beautiful theory murdered by ugly reality. Each row represented an Ola S1 Pro scooter, columns tracking costs from raw materials to delivery. The bottom line was damning: Ola lost ₹23,000 on every vehicle sold, even after accounting for government subsidies. The path to profitability required selling 400,000 units annually at 35% gross margins. They were currently at 150,000 units and negative 18% margins.

The direct-to-consumer model that Aggarwal championed was supposed to be Ola's competitive advantage. By eliminating dealerships, they would save 15-20% in distribution costs. Customers would configure vehicles online, receive home delivery, and access service through company-owned centers. It was the Tesla model, applied to Indian two-wheelers. The math seemed irrefutable.

But math didn't account for Indian market realities. Customers wanted to touch, feel, and test-ride vehicles before purchasing. They expected immediate delivery, not three-month waiting periods. They wanted local service, not appointments at distant company centers. The D2C model that worked for ₹1,000 smartphones didn't translate to ₹100,000 scooters.

The experience center strategy was the expensive compromise. Ola built 935 centers across India—showrooms where customers could see vehicles but not buy them. Each center cost ₹50 lakhs to establish and ₹5 lakhs monthly to operate. With average footfall of 100 visitors daily and conversion rates of 2%, each center generated maybe 60 sales monthly. The unit economics were abysmal.

The service infrastructure was even more problematic. 414 service centers sounded impressive until you realized Hero MotoCorp had 6,000. Each Ola center required specialized equipment for EV diagnostics, trained technicians, and inventory of proprietary parts. The average service center handled 20 vehicles daily but had capacity for 50, meaning 60% idle capacity.

The working capital requirements were staggering. Unlike traditional manufacturers who pushed inventory to dealers, Ola held everything. At any time, they had ₹800 crores tied up in finished goods inventory, ₹400 crores in raw materials, and ₹300 crores in work-in-progress. The cash conversion cycle was 120 days—they paid suppliers in 30 days but collected from customers in 150 days average.

The PLI (Production Linked Incentive) scheme was supposed to bridge the profitability gap. The government offered ₹15,000 per vehicle for achieving 50% localization. But calculating localization was complex. Did software developed in India count? What about batteries assembled locally but using imported cells? Ola claimed 72% localization; auditors calculated 43%. The difference meant ₹200 crores in disputed subsidies.

The FAME-II subsidies added another layer of complexity. Customers received ₹15,000-25,000 discounts depending on battery capacity and state. But Ola had to front this money and claim reimbursement from the government. Processing took 6-9 months, creating massive receivables. At one point, ₹600 crores was stuck in subsidy claims, earning no interest while Ola paid 12% on working capital loans.

The pricing strategy was schizophrenic. The S1 Pro launched at ₹1.3 lakhs, dropped to ₹1.1 lakhs within months, then rose to ₹1.47 lakhs when subsidies reduced. Each price change required honoring previous bookings at old prices, creating margin chaos. The sales team never knew what margin they were working with.

The warranty provisions were a hidden time bomb. Ola offered 3-year unlimited kilometer warranties, later extended to 8 years on batteries. Based on initial quality issues, actuaries calculated warranty costs at ₹8,000 per vehicle. But Ola provisioned only ₹3,000, arguing quality was improving. The under-provisioning meant future quarters would face massive warranty charges.

The battery replacement economics were particularly concerning. Batteries degraded 2-3% annually, meaning significant capacity loss by year 5. Replacement cost was ₹45,000, but Ola couldn't charge customers that much. They offered replacement at ₹25,000, eating ₹20,000 losses. With 300,000 vehicles on road, even 10% requiring battery replacement meant ₹600 crore losses.

The software and services revenue stream—Aggarwal's vision for recurring income—hadn't materialized. MoveOS+ subscription at ₹5,000 annually offered navigation, advanced analytics, and priority support. Only 3% of customers subscribed. The charging network, supposed to generate ₹100 monthly per user, was free because competitors offered free charging.

The corporate sales channel showed promise but required different economics. Fleet operators like Zomato and Swiggy wanted bulk discounts, extended credit terms, and on-site service. Margins dropped to 5%, payment terms extended to 180 days, and service costs doubled. Volume was attractive—orders of 1,000+ vehicles—but profitability was worse than retail.

The export opportunity seemed attractive with 70% higher prices in European markets. But homologation costs were prohibitive—₹50 crores per market for certification. Shipping added ₹15,000 per unit. Service infrastructure required local partnerships. After full costs, export margins were actually lower than domestic sales.

The financial projections presented to investors required aggressive assumptions. FY26 guidance of 325,000-375,000 vehicles assumed 150% growth despite increasing competition. The 35-40% gross margin target required battery costs falling 30% and steel prices remaining flat. The ₹4,200-4,700 crore revenue projection assumed average selling prices rising despite market pressures for lower prices.

The cash burn rate was alarming. Despite raising ₹6,000 crores at IPO, Ola burned ₹800 crores quarterly on operations, ₹400 crores on capex, and ₹200 crores on R&D. At current burn rate, they had 15 months of runway. Another fundraise seemed inevitable, but at what valuation?

The comparison with competitors was unflattering. Ather Energy achieved 15% gross margins with half Ola's scale. TVS iQube generated positive EBITDA within 18 months of launch. Bajaj Chetak, despite lower volumes, had better unit economics through dealer networks and shared manufacturing infrastructure.

The vertical integration that was supposed to drive margins was instead destroying them. Making batteries in-house saved ₹5,000 per vehicle but required ₹2,000 crores in capex. Manufacturing motors saved ₹3,000 but added ₹15,000 in overhead allocation. The FutureFactory running at 30% capacity meant massive fixed cost absorption problems.

The path to profitability required four things simultaneously: doubling volumes, improving quality to reduce warranty costs, achieving actual (not claimed) localization for subsidies, and somehow maintaining prices despite competition. Each was difficult individually; achieving all four seemed impossible.

The tragic irony was that the business model wasn't fundamentally flawed. Direct-to-consumer could work with better execution. Vertical integration made sense at scale. Software services had potential with better products. But Ola had tried to do everything simultaneously, resulting in nothing working properly.

By mid-2025, the board was forcing hard conversations. Should they abandon D2C and partner with dealers? Outsource manufacturing to reduce capital intensity? Focus on one product instead of eight? Each option meant admitting failure in some dimension, something Aggarwal was constitutionally incapable of doing.

The business model story of Ola Electric was ultimately about the difference between Silicon Valley economics and manufacturing economics. In software, you could lose money on each user but make it up on volume because marginal costs were zero. In hardware, losing money on each unit meant volume made things worse. Ola was learning this lesson the expensive way.

X. Bear vs. Bull Case Analysis

The Morgan Stanley analyst pulled up two slides, side by side. On the left, titled "The Bear Case," Ola Electric's stock price target: ₹15, implying 65% downside. On the right, "The Bull Case," target: ₹180, suggesting 300% upside. "Rarely," she told the investment committee, "have I seen a company where reasonable people can disagree so fundamentally about value."

The Bear Case: A House of Cards

The bear thesis was straightforward: Ola Electric was a cash-burning machine masquerading as a technology company, led by an erratic founder, selling defective products in a market that didn't actually want them. Every metric that mattered was deteriorating.

Start with the cash burn. At ₹800 crores quarterly operating losses, Ola would need another capital raise within 12-18 months. But who would fund them? The stock was down 63% from IPO. Private investors who bought at $7 billion valuation were underwater. Any new round would be deeply dilutive, perhaps at a valuation below the IPO price—a devastating signal.

The quality issues weren't improving despite claims otherwise. Internal documents leaked to analysts showed warranty claims rising, not falling. The claimed 2% failure rate was actually closer to 15% when including software issues. Each recalled vehicle cost ₹12,000 to fix. With 400,000 vehicles on roads, even minor recalls could cost hundreds of crores.