AT&T: The Bell System's Second Act

I. Introduction & Episode Roadmap

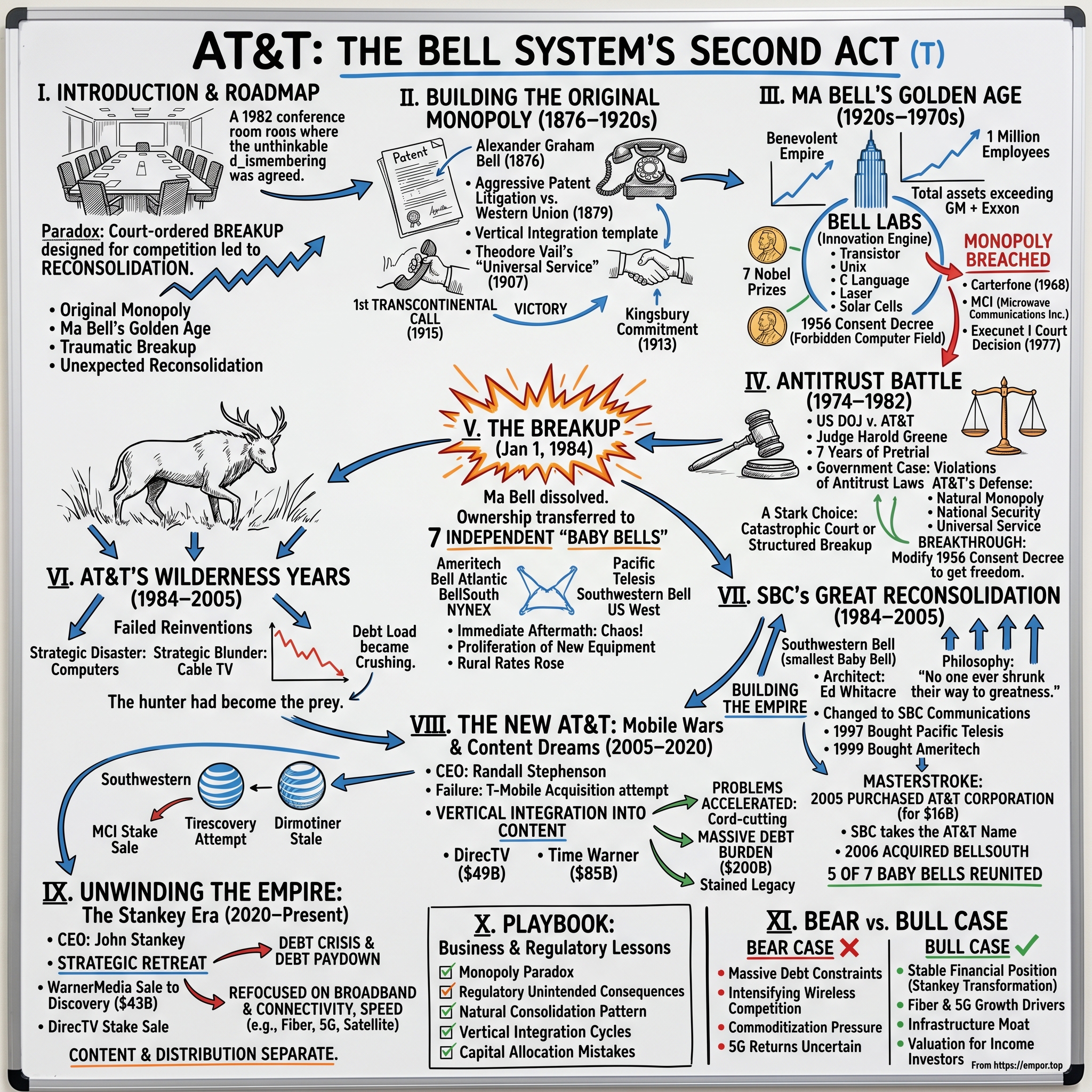

The conference room at 195 Broadway in Lower Manhattan fell silent on January 8, 1982. AT&T Chairman Charles Brown had just agreed to the unthinkable: voluntarily dismembering the most powerful corporation in American history. The company that had connected a nation, employed over one million people, and generated revenues exceeding $65 billion would cease to exist in its current form. Yet the most extraordinary part of this story wasn't the breakup itself—it was what happened next.

Twenty-three years later, in a Dallas boardroom, Ed Whitacre would sign papers that would make his company, Southwestern Bell—one of the seven "Baby Bells" born from AT&T's corpse—the new owner of AT&T itself. The child had consumed the parent. The monopoly that Judge Harold Greene had worked so hard to destroy had essentially reconstituted itself, like liquid metal reforming after being shattered.

This is the paradox at the heart of modern telecommunications: how a court-ordered breakup designed to foster competition ultimately led to reconsolidation. It's a story that begins with Alexander Graham Bell shouting "Mr. Watson, come here, I want to see you" into a crude apparatus in 1876, and continues today as AT&T battles for relevance in the age of 5G and streaming wars.

The fundamental question we're exploring isn't just how AT&T built, lost, and then rebuilt its empire. It's whether monopolies in network industries are inevitable—whether the physics of telecommunications naturally tends toward consolidation, regardless of what regulators, courts, or competitors attempt. As we watch today's tech giants face similar antitrust scrutiny, AT&T's century-and-a-half saga offers crucial lessons about the cycles of innovation, regulation, and corporate power.

This episode traces four distinct eras: the original monopoly's rise under Theodore Vail's vision of universal service; the golden age when Bell Labs invented the future while Ma Bell controlled the present; the traumatic breakup that was supposed to unleash competition; and the reconsolidation that nobody saw coming. Along the way, we'll meet visionaries, monopolists, trust-busters, and empire builders—all wrestling with the same question: who should control the nervous system of modern society?

II. The Bell Patent & Building the Original Monopoly (1876–1920s)

The patent that would create the world's most valuable monopoly was filed on Valentine's Day, 1876—just hours before Elisha Gray submitted his own telephone design. Alexander Graham Bell's lawyer had literally run to the patent office, arriving at the last possible moment. That two-hour difference would spawn decades of litigation and create a fortune worth hundreds of billions in today's dollars.

Bell himself was an unlikely monopolist. A teacher of the deaf who had stumbled upon voice transmission while working on acoustic telegraphs, he initially saw the telephone as a scientific curiosity. It was his future father-in-law, Gardiner Greene Hubbard, who recognized the commercial potential. Hubbard, a lawyer and entrepreneur who had previously battled Western Union's telegraph monopoly, understood that controlling a communications network meant controlling commerce itself.

The Bell Telephone Company, established in July 1877, faced immediate existential threats. Western Union, the Google of its day with 100,000 miles of telegraph wire and unlimited capital, launched its own telephone subsidiary in 1878 using Edison's superior transmitter and Gray's patents. Bell's company seemed doomed—until Hubbard's son-in-law pulled off one of the great legal coups in business history. Through aggressive patent litigation and a lucky break when Western Union became distracted by a hostile takeover attempt from Jay Gould, Bell negotiated a settlement in November 1879 that gave them Western Union's telephone patents and equipment in exchange for 20% of telephone rental receipts.

But the real genius move came in 1881 when Bell acquired controlling interest in Western Electric, Western Union's former equipment manufacturer. This vertical integration would become the template for the entire Bell System: control the patents, control the equipment, control the network. By 1885, the company had reorganized as American Telephone and Telegraph Company, signaling its continental ambitions. AT&T wasn't just going to connect neighborhoods—it would wire a nation.

The mastermind who transformed this collection of patents and wires into an empire was Theodore Newton Vail, who became AT&T's president in 1907 after a brief retirement. Vail understood something his competitors didn't: in a network business, monopoly wasn't just profitable—it was arguably better for consumers. His philosophy, "One System, One Policy, Universal Service," wasn't just a slogan but a social contract. AT&T would accept government regulation in exchange for monopoly status, using profits from business customers and long-distance calls to subsidize universal local service. The masterstroke came with the Kingsbury Commitment of December 19, 1913, when AT&T Vice President Nathan Kingsbury sent a letter to Attorney General James Clark McReynolds agreeing to divest Western Union, provide long-distance services to independent exchanges under certain conditions, and refrain from acquisitions if the Interstate Commerce Commission objected. This wasn't a defeat—it was Vail's greatest victory. The Wilson administration effectively gave its blessing to AT&T's dominance of the telephone industry, and in exchange for this government-sponsored monopoly, AT&T agreed to operate as a public utility, eventually providing high-quality phone service to the vast majority of Americans regardless of income or geography

The engineering triumph that demonstrated AT&T's continental ambitions came on January 25, 1915, when Alexander Graham Bell, now 67, spoke from New York to his former assistant Thomas Watson in San Francisco. The first transcontinental call required 2,500 tons of copper wire, 130,000 poles, and three vacuum-tube repeaters—a technology that AT&T had quietly acquired from inventor Lee de Forest. This wasn't just a publicity stunt; it was a declaration that AT&T could and would connect every corner of America.

By 1920, AT&T had methodically acquired or driven out of business nearly all significant competitors. The company controlled 10 million of the nation's 13 million telephones. Independent companies that survived did so only in rural areas AT&T deemed unprofitable, or by agreeing to interconnection arrangements that made them effectively vassals of the Bell System. The monopoly was complete, blessed by government and seemingly permanent. Nobody could imagine that this empire, built on patents and poles, would one day face threats from technologies that didn't yet exist.

III. Ma Bell's Golden Age & Growing Power (1920s–1970s)

The decade that Theodore Vail had anticipated—when AT&T would become not just America's telephone company but the world's largest corporation—arrived with spectacular force. By the 1970s it had nearly a million employees and was the largest company in the world, with total assets then exceeding the combined assets of General Motors, Exxon Corp., and Mobil Corp. At its peak in the 1950s and 1960s, it employed one million people and its revenue ranged between US$3 billion in 1950 ($42.6 billion in present-day terms) and $12 billion in 1966 ($120 billion in present-day terms). The Bell System had become a colossus beyond even Vail's imagination, touching every aspect of American life.

The regulated monopoly operated like a benevolent empire. AT&T maintained its social contract through an elaborate system of cross-subsidies—charging businesses and long-distance users above-cost rates to keep local residential service affordable. A call from New York to Los Angeles might cost $3 per minute (over $15 in today's dollars), but local service remained under $10 per month even in poor neighborhoods. This Robin Hood pricing wasn't charity; it was the quid pro quo for monopoly protection.

At the heart of this empire beat Bell Labs, the innovation engine that justified AT&T's existence as a monopoly. Located in Murray Hill, New Jersey, Bell Labs employed thousands of the world's brightest scientists and engineers, freed from commercial pressures to pursue pure research. The results were staggering: the transistor in 1947, which launched the computer age; the Unix operating system in 1969, which would power the internet; the C programming language in 1972, which became the lingua franca of software development; the laser, solar cells, cellular telephony concepts, and satellite communications.

Claude Shannon invented information theory there. Arno Penzias and Robert Wilson discovered the cosmic microwave background radiation, earning a Nobel Prize. Seven other Nobel Prizes would follow. Bell Labs wasn't just inventing products; it was inventing the future itself. The irony was that AT&T couldn't fully capitalize on most of these innovations due to regulatory constraints.

The 1956 consent decree had settled another antitrust threat but at a steep price: AT&T was prohibited from entering the computer business or any field outside regulated telecommunications. The company that invented the transistor couldn't make computers. The creator of Unix couldn't sell software. AT&T was forced to license its patents to others for nominal fees, seeding entire industries it couldn't enter.

By the 1960s, this restriction became increasingly absurd. Computers and telephones were converging—data needed to travel over phone lines, and computers needed to communicate. When businesses wanted to attach non-AT&T equipment to the phone network, like early modems or PBX systems, AT&T refused, citing network integrity. The Carterfone decision of 1968 forced AT&T to allow foreign attachments, cracking open the first fissure in the monopoly wall. The real threat came from an upstart called Microwave Communications Inc. (MCI), founded in 1963 by Jack Goeken to provide private line services between Chicago and St. Louis. MCI was founded as Microwave Communications, Inc. on October 3, 1963, with the initial business plan to build a series of microwave radio relay stations between Chicago, Illinois, and St. Louis, Missouri. What began as a modest plan to serve truckers with two-way radio became the battering ram that would break down Ma Bell's fortress.

MCI's breakthrough came through regulatory arbitrage and sheer audacity. After winning FCC approval in 1969 to provide private line services, the company was hemorrhaging money—losing working capital at the rate of $1 million a month between March 1973 and March 1975. Facing bankruptcy, MCI launched Execunet in 1974, a service that looked suspiciously like regular long-distance but was marketed as enhanced private line service.

AT&T immediately recognized the threat and appealed to the FCC, which ordered MCI to cease Execunet service. But in a landmark 1977 decision known as Execunet I, the U.S. Court of Appeals for the District of Columbia Circuit reversed, holding that the FCC must allow MCI and other companies to compete with AT&T in the market for regular long-distance service. The monopoly wall had been breached.

In AT&T's view, opening the long-distance market to competition was a serious threat to its business model—and, in particular, to the cross-subsidies that kept rates low for local callers, consumers in rural areas, and residential customers. The company fought desperately, but the convergence of technology and law was unstoppable. Computers needed to talk to each other over phone lines. Businesses wanted choice in equipment. The monopoly that had enabled universal service had become an obstacle to innovation.

IV. The Antitrust Battle & Judge Greene's Courtroom (1974–1982)

The United States Department of Justice filed United States v. AT&T in 1974, citing authority under the Sherman Antitrust Act. The lawsuit charged that AT&T had used its relationship with the local Bell companies to block competitors in both equipment and long-distance markets, leveraging its monopoly power in anticompetitive ways. After seven years of pretrial maneuvering, the case finally went to trial on January 15, 1981.

Judge Harold H. Greene, a refugee from Nazi Germany who had worked with Robert Kennedy on civil rights legislation, was assigned to the case and was determined to try the case as quickly and efficiently as possible. The judge's reaction to seeing the courthouse corridor crammed with boxes of cost studies was to quip, "I'm glad I only had Watergate".

The government's case was devastating. They presented evidence that AT&T had restricted competitors' access to the local network, discriminated in favor of Western Electric equipment, and overcharged for long-distance service to protect its monopoly profits. At the conclusion of the government's case, Judge Greene denied AT&T's motion to dismiss, concluding that "the testimony and the documentary evidence adduced by the government demonstrate that the Bell System has violated the antitrust laws in a number of ways over a lengthy period of time".

AT&T's defense rested on three pillars: natural monopoly economics, national security, and universal service. They argued that telecommunications was inherently a natural monopoly where competition would be wasteful and inefficient. They invoked Cold War anxieties, claiming that a unified Bell System was essential for national defense. Most emotionally, they warned that breakup would end universal service and raise local rates for millions of Americans.

But William Baxter, the new Assistant Attorney General for Antitrust appointed by Reagan, had a different vision. A Stanford law professor and free-market advocate, Baxter didn't want to destroy AT&T—he wanted to unleash it. His theory was elegant: separate the naturally monopolistic local exchanges from the potentially competitive long-distance and equipment markets. Let AT&T compete freely in computers and information services, but force it to give up the local bottleneck that gave it unfair advantages.

The negotiations intensified through late 1981. Charles Brown, AT&T's chairman, recognized that the company faced a stark choice: risk a catastrophic court decision that could dismember the company unpredictably, or negotiate a structured breakup on their own terms. AT&T itself recommended a divestiture structure in which it would be broken up into regional subsidiaries.

The breakthrough came with a creative legal maneuver. Rather than admitting guilt, AT&T would agree to modify the 1956 consent decree that had kept it out of computers. By divesting the local operating companies, AT&T would be freed from regulatory constraints to compete in the exploding information technology market. The company would keep long-distance, Western Electric, Bell Labs, and the Yellow Pages—what management saw as the crown jewels.

On January 8, 1982, Assistant Attorney General William F. Baxter and Charles L. Brown, chairman of AT&T, jointly announced settlement of the government's 1974 antitrust suit. When the agreement was announced to the press, most reported it as a victory for AT&T and a loss for the Justice Department. AT&T had kept its most profitable assets, divested itself of its least profitable ones, and escaped from the confines of the 1956 decree.

But Judge Greene wasn't finished. Judge Greene retained control over the proceedings under the Tunney Act, a federal law requiring court approval to ensure that antitrust consent decrees were in the public interest. Over the next eight months, he would reshape the agreement significantly, stripping AT&T of the Yellow Pages and giving the Baby Bells stronger footing to compete. The settlement was finalized on January 8, 1982, with some changes ordered by the decree court: the regional holding companies received the Bell trademark, Yellow Pages, and about half of Bell Labs.

V. The Breakup: January 1, 1984

At 12:01 AM on January 1, 1984, the Bell System ceased to exist. Effective January 1, 1984, ownership of the Bell System's many local operating companies were transferred into seven independent Regional Bell Operating Companies (RBOCs), or "Baby Bells". This divestiture reduced the book value of AT&T by approximately 70%. At the time of the breakup of the Bell System in the early 1980s, it had assets of $150 billion (equivalent to $450 billion in 2024) and employed over one million people.

The seven Baby Bells were geographic fiefdoms, each controlling local telephone service in their regions:

- Ameritech - The industrial Midwest (Illinois, Indiana, Michigan, Ohio, Wisconsin)

- Bell Atlantic - The Mid-Atlantic states (New Jersey, Pennsylvania, Delaware, Maryland, Virginia, West Virginia)

- BellSouth - The Southeast (North Carolina, South Carolina, Georgia, Florida, Alabama, Mississippi, Louisiana, Tennessee, Kentucky)

- NYNEX - New York and New England

- Pacific Telesis - California and Nevada

- Southwestern Bell - Texas, Missouri, Arkansas, Kansas, Oklahoma

- US West - The mountain and northwestern states

When the AT&T breakup ended in 1984, it retained only long-distance, Bell Labs, and Western Electric. Those companies, which were consolidated into seven regional operating companies (nicknamed "Baby Bells"), were permitted to keep the Bell name as a result of a decision by Judge Greene. Several of Judge Greene's modifications to the consent decree were favorable to the regional operators, such as allowing them to maintain the profitable Yellow Pages.

The immediate aftermath was chaos. Customers who had dealt with one company for generations suddenly faced a bewildering array of choices. Bills came from different companies. Equipment that had been leased now had to be purchased. Phone numbers that had been listed in one directory were scattered across multiple books. Corporate telecommunications managers scrambled to negotiate contracts with multiple vendors for services that had previously come from a single source.

The most obvious impact for consumers was the proliferation of new types of telephone equipment produced by myriad companies, including answering machines and designer handsets, while companies like Sprint and MCI offered competitive new options for long distance service. Radio Shack, once a tiny electronics retailer, became a billion-dollar company selling phones and answering machines. Japanese manufacturers flooded the market with innovative handsets. The plain black rotary phone, once the only option, became a museum piece almost overnight.

For businesses, the changes were seismic. The old certainties—one vendor, one network, one standard—evaporated. But with confusion came opportunity. New telecommunications companies sprouted like mushrooms after rain. Venture capitalists poured billions into startups promising to revolutionize business communications. The seeds of the internet boom were planted in the fertile chaos of divestiture.

Consumers, however, in addition to paying more for phone service, reported less satisfaction with the quality of their service and with customer service in the years after the breakup. Local rates, which AT&T's cross-subsidies had kept artificially low, began rising toward their true economic cost. Rural customers, who had benefited most from universal service policies, faced the steepest increases.

Rumors of the demise of the regional operating companies was premature, as they did well on their own, as a result not only of higher local phone rates but also the high prices they charged AT&T and other long-distance companies for local interconnection. The Baby Bells had inherited the most valuable asset: the last mile to customers' homes and businesses. Every long-distance call, whether from AT&T, MCI, or Sprint, had to traverse their networks at both ends. They charged handsomely for this access, turning what AT&T had seen as the least profitable part of the business into a gold mine.

The breakup also unleashed a wave of innovation that the old AT&T monopoly had suppressed. Cellular telephony, which Bell Labs had invented in the 1940s but AT&T had slow-walked for decades, suddenly exploded. Data communications, once restricted by AT&T's refusal to allow "foreign attachments," became a multibillion-dollar industry. The internet, which AT&T had dismissed as a toy for academics, would soon transform not just telecommunications but human civilization itself.

VI. AT&T's Wilderness Years & Failed Reinventions (1984–2005)

The new AT&T that emerged from divestiture was a company without a clear identity. Stripped of its local monopolies and facing fierce competition in long-distance, it thrashed about searching for a strategy. What followed was two decades of spectacular misadventures that would destroy hundreds of billions in shareholder value and reduce one of America's greatest companies to a shadow of its former self.

The first strategic disaster was the computer gambit. Finally freed from the 1956 consent decree's prohibition on entering the computer business, AT&T executives convinced themselves they could challenge IBM. The company already owned Unix, had world-class research capabilities, and understood networks better than anyone. What could go wrong?

Everything, as it turned out. AT&T's first personal computers, launched in 1984, were overpriced and underpowered. The company's sales force, accustomed to selling to telecom managers in regulated monopolies, had no idea how to compete in the cutthroat PC market. But rather than retreat, AT&T doubled down, acquiring NCR for $7.4 billion in 1991 in one of the most disastrous mergers in corporate history.

NCR's employees resented the takeover, customers fled, and the promised synergies never materialized. AT&T Computer Systems failed, and after misguided acquisitions such as NCR and AT&T Broadband, it was left with only its core long-distance business. By 1996, AT&T admitted defeat, spinning off NCR at a loss of billions. The computer strategy had been a complete failure.

Meanwhile, the company's core long-distance business was evaporating. The Baby Bells, initially barred from long-distance, successfully lobbied for entry into the market. New technologies like voice over IP made distance irrelevant. Wireless carriers offered buckets of minutes that included "free" long-distance. AT&T's revenues from its most profitable service began a death spiral that would never reverse.

Desperate for growth, AT&T lurched into its next strategic blunder: cable television. The theory seemed sound—cable networks could carry voice and data, creating a "triple play" of services. AT&T acquired TCI for $48 billion and MediaOne for $54 billion, substantially increasing the company's debt. CEO Michael Armstrong promised that AT&T would become the premier broadband company in America.

Instead, AT&T became a case study in acquisition failure. The cable systems were in worse shape than expected, requiring billions in upgrades. The cultures clashed—AT&T's bureaucratic style suffocated the entrepreneurial cable operators. Customer service, already poor, became abysmal. The debt load became crushing. By 2002, AT&T was forced to sell the cable assets to Comcast at a massive loss.

The management turmoil reflected the strategic confusion. CEOs came and went—Robert Allen, Michael Armstrong, David Dorman—each with a new vision that contradicted the last. The company that had once employed the best and brightest became known for bureaucracy and indecision. Bell Labs, once the crown jewel, was starved of funding and eventually spun off as part of Lucent Technologies in 1996.

By 2004, AT&T was a broken company. Its stock price had collapsed from over $60 in 1999 to under $20. Long-distance revenues were in free fall. The cable strategy had failed. The company that had once been larger than General Motors, Exxon, and Mobil combined was now worth less than any one of the Baby Bells it had spawned. The hunter had become the prey.

VII. SBC's Empire Building & The Great Reconsolidation (1984–2005)

While AT&T floundered, one Baby Bell was methodically executing a plan that would have seemed like fantasy in 1984: rebuilding the Bell System. Southwestern Bell, the smallest of the seven regional companies, would ultimately swallow its parent and five of its six siblings in the greatest consolidation story in American business.

The architect of this empire was Edward Earl Whitacre Jr., a Texan who had started his career climbing telephone poles and worked his way up through the ranks. Edward Whitacre—who started his telephone industry career doing repair work in Texas for Southwestern Bell—was named chair and chief executive of Southwestern Bell in 1990. He is credited with turning the smallest of the Baby Bells into what would become the largest telecommunications company in the world by 2007.

Whitacre understood something his peers didn't: in a network business, scale is everything. While other Baby Bell CEOs focused on protecting their regional fiefdoms, Whitacre went hunting. His philosophy was simple: "No one ever shrunk their way to greatness."

In 1995, Whitacre changed the Southwestern Bell name to SBC Communications Inc., a hint toward his grand scheme. The name change signaled that this was no longer just a regional phone company—it had national ambitions.

The consolidation began in 1997 when SBC Communications purchased Pacific Telesis in 1997 for $16.5 billion, creating an organization with about 100,000 employees, an annual net income of $3 billion, and revenue of about $23.5 billion. This gave SBC control of California, the largest state economy. SBC acquired fellow Baby Bells Pacific Telesis in 1997 and Ameritech in 1999, with the Ameritech acquisition adding the industrial Midwest to SBC's growing empire.

Each acquisition followed the same playbook: promise regulators that competition would be enhanced, then slash costs ruthlessly once approval was granted. Thousands of jobs were eliminated. Redundant networks were consolidated. The "synergies" that Wall Street loved translated into pink slips for workers and higher prices for customers.

But the masterstroke was yet to come. On January 31, 2005, SBC announced it would purchase AT&T Corporation for more than $16 billion, finalized on November 18, 2005. The child was literally buying its parent. The company that AT&T had been forced to divest was now acquiring AT&T itself.

The irony was delicious and disturbing in equal measure. Southwestern Bell Communications (SBC) bought two other Baby Bells, Ameritech and Pacific Telesis, and eventually became large enough that it purchased AT&T for $16 billion in 2005. The merged company took the better-known AT&T name and branding, with SBC taking on the AT&T name upon merger closure on November 18, 2005. SBC began trading as AT&T Inc. on December 1, 2005, but began re-branding as early as November 21 of the same year.

The reconsolidation didn't stop there. AT&T acquired BellSouth on December 29, 2006, consolidating ownership of Cingular Wireless. With BellSouth came the Southeast and complete control of Cingular Wireless, which had become the nation's largest wireless carrier. Five of the seven Baby Bells were now reunited under the AT&T banner.

Whitacre had pulled off the impossible: reassembling most of Ma Bell without triggering antitrust action. The regulators who had broken up AT&T in 1984 to promote competition had allowed it to reconstitute itself just two decades later. The difference was that this time, AT&T faced real competition from cable companies in broadband and from Verizon and others in wireless. The monopoly was gone, but the empire had returned.

VIII. The New AT&T: Mobile Wars & Content Dreams (2005–2020)

Randall Stephenson succeeded Edward Whitacre as CEO in April 2007, inheriting a reconsolidated AT&T that faced new challenges: the iPhone revolution, cord-cutting, and tech giants encroaching on telecommunications. Stephenson, an accountant who had risen through the ranks at Southwestern Bell, had a different vision than his predecessor. Where Whitacre had focused on reconsolidating the Baby Bells, Stephenson saw AT&T's future in content and convergence.

His first major crisis came with the failed T-Mobile acquisition attempt in 2011. Regulators opposed the $39 billion T-Mobile deal, which would have eliminated a major competitor. As a breakup fee for that deal, AT&T ended up providing T-Mobile with a seven-year roaming deal and billions in wireless spectrum. Those moves helped transform T-Mobile from a struggling competitor into a company that has grown faster than Verizon, AT&T and Sprint in recent years.

The T-Mobile failure haunted Stephenson, but he pressed forward with an even bolder strategy: vertical integration into content. AT&T acquired DirecTV for $49 billion in July 2015 and Time Warner for $85 billion in June 2018. AT&T has watched millions of satellite subscribers leave the service since closing the DirecTV deal in 2015.

The DirecTV acquisition was immediately problematic. Cord-cutting accelerated just as AT&T took ownership of the nation's largest satellite TV provider. Millions of subscribers fled to Netflix and other streaming services. What was supposed to be AT&T's entry into the triple play—voice, data, and video—became an albatross around its neck.

But Stephenson doubled down with the Time Warner acquisition, the fourth-largest deal in corporate history. Stephenson said the future of media entertainment is rapidly converging around three elements required to transform how video is distributed, paid for, consumed and created. Today, AT&T brings together: Premium Content: Broadly distributed, robust premium content portfolio that combines leading movies and shows from Warner Bros., HBO and Turner.

The deal faced intense regulatory scrutiny. The Trump administration's Department of Justice sued to block it, arguing that combining AT&T's distribution with Time Warner's content would harm competition. After a bruising trial, AT&T prevailed, but the victory was Pyrrhic. At the time Stephenson announced his departure, it was acknowledged that the acquisitions of DirectTV and Time Warner had by this point resulted in a massive debt burden of $200 billion for the company, forcing the company to cut back on its capital investments.

The streaming wars that Stephenson had anticipated arrived with a vengeance. Disney+, Apple TV+, and others launched with deep pockets and global ambitions. HBO Max, AT&T's answer to Netflix, struggled with technical problems, confusing branding (was it HBO, HBO Now, HBO Go, or HBO Max?), and a late entry into an increasingly crowded market.

By 2020, AT&T's acquisitions had resulted in a massive debt burden of $200 billion. The company that had once been the bluest of blue chips now carried more debt than many countries. Dividend cuts loomed. The stock price languished. Elliott Management, the activist investor, took a $3.2 billion stake and publicly excoriated management's strategy.

In December 2020, the Financial Times said Stephenson's "legacy has been stained by poor acquisitions". The empire-building that had defined AT&T since its reconsolidation had led it to the brink of disaster once again.

IX. Unwinding the Empire: The Stankey Era (2020–Present)

John Stankey replaced Randall Stephenson as CEO on July 1, 2020, inheriting a company drowning in debt and strategic confusion. A career AT&T executive who had started with Pacific Bell in 1985, Stankey had been Stephenson's lieutenant on both the DirecTV and Time Warner acquisitions. Now he faced the unenviable task of unwinding his predecessor's empire-building.

"Getting to this moment was one of the more difficult decisions of my life. I am sure you aren't surprised that it came with a fair amount of anxiety, disappointment, and concern relative to the changes it would trigger," Stankey would later write about dismantling the media empire.

The strategic retreat began immediately. In February 2021, Stankey oversaw the sale of a third of AT&T's stake in DirecTV to TPG Capital for $16.25 billion. When the AT&T breakup ended in 1984, it retained only long-distance, Bell Labs, and Western Electric—now AT&T was selling assets it had paid $48 billion to purchase just six years earlier.

The bigger bombshell came in May 2021 when Stankey oversaw WarnerMedia's sale to Discovery Inc. for $43 billion in cash. The company that AT&T had paid $85 billion for in 2018 was being spun off at roughly half that valuation. AT&T's decision to split out WarnerMedia comes less than three years after closing its $100 billion transaction, including debt, is an admission that putting a large content asset with a wireless phone company had few long-lasting synergies.

The debt crisis that had precipitated these sales was existential. AT&T aims to use the proceeds from the WarnerMedia spinoff to pay down net debt, which stood at $156.2 billion at the end of 2021. The company that had once been America's financial Gibraltar was now frantically selling assets to avoid a credit downgrade.

But Stankey's strategy went beyond mere asset sales. Stankey refocused AT&T on broadband and cellular availability, connectivity, and speed, including partnering with AST SpaceMobile to provide mobile phone service to remote areas via satellite. Under his leadership, AT&T expanded its network of fiber-optic cables, including to places it didn't already provide broadband, and entered a joint venture with BlackRock called Gigapower to build fiber-optic networks in metro areas around the country.

This return to core telecommunications represented a philosophical reversal as dramatic as any in corporate history. The convergence strategy that had driven two decades of dealmaking was dead. Content and distribution, it turned out, didn't need to be under the same roof. Netflix had no network. Verizon had no studio. The synergies that had justified hundreds of billions in acquisitions had proven illusory.

Stankey seriously started to consider extracting WarnerMedia from AT&T after activist hedge fund Elliott Management took a stake in the company in 2019 and publicly chastised management. At first, Elliott believed Stankey was part of the problem, assisting Stephenson in deals that moved AT&T away from its focus on wireless. But after expediting Stephenson's retirement and helping run a search for a new CEO, Elliott came to believe Stankey was actually the right man for the job. Stankey told Elliott privately he was his own man — not a Stephenson clone — and would come to his own viewpoints about the value of DirecTV and WarnerMedia.

The transformation under Stankey has been remarkable. The company that tried to be everything—phone company, cable operator, content creator, streaming service—is returning to its roots as a connectivity provider. The 5G rollout that had been delayed by media adventures is now the priority. Fiber expansion, not content creation, drives capital allocation.

X. Playbook: Business & Regulatory Lessons

The AT&T saga offers a masterclass in the paradoxes of monopoly, regulation, and corporate strategy. The same forces that created Ma Bell ultimately destroyed it, and the competitive market that was supposed to replace it gradually reconsolidated into an oligopoly barely distinguishable from what came before.

The Monopoly Paradox: AT&T's original monopoly was both a creation of government regulation and a victim of it. The Kingsbury Commitment gave AT&T protected status in exchange for universal service, but that same protection bred the complacency and rigidity that made the company vulnerable to technological disruption. The monopoly was supremely efficient at building and operating a unified network but terrible at innovation outside its narrow mandate.

The cross-subsidy model that made universal service possible—charging businesses and long-distance users more to subsidize residential service—created its own destruction. MCI and others could cherry-pick the profitable routes and customers, leaving AT&T with the universal service obligation but not the monopoly profits to fund it. In AT&T's view, opening the long-distance market to competition was a serious threat to its business model—and, in particular, to the cross-subsidies that kept rates low for local callers, consumers in rural areas, and residential customers.

Regulatory Capture and Unintended Consequences: The AT&T story demonstrates how regulation often achieves the opposite of its intent. The 1956 consent decree that kept AT&T out of computers seemed like consumer protection but actually delayed the computer revolution. The 1984 breakup that was supposed to create competition led to reconsolidation. The Telecommunications Act of 1996, meant to increase competition, enabled the Baby Bells to merge back together.

Regulators consistently fought the last war. They broke up AT&T's vertical integration just as vertical integration was becoming irrelevant. They worried about long-distance monopolies as distance became meaningless. They scrutinized mergers between phone companies while missing the rise of cable, wireless, and internet competitors.

The Reconsolidation Pattern: The AT&T story reveals a fundamental truth about network industries: they tend toward consolidation. The economics of building and maintaining networks create natural oligopolies. The same dynamics that created Ma Bell in the first place—network effects, economies of scale, high fixed costs—reasserted themselves after the breakup.

But the reconsolidated AT&T is fundamentally different from the original. It faces real competition from Verizon, T-Mobile, cable companies, and tech giants. It has no protected monopoly, no guaranteed returns, no cross-subsidy system. The new oligopoly is more dynamic, more innovative, and more fragile than the old monopoly.

Vertical Integration Cycles: AT&T's adventures in content demonstrate the cyclical nature of vertical integration in technology and media. The company spent $200 billion acquiring DirecTV and Time Warner, then sold them at massive losses just years later. The synergies that seemed obvious in PowerPoint presentations evaporated in practice.

This pattern repeats throughout tech history. AOL-Time Warner. Microsoft-Nokia. Google-Motorola. Companies consistently overestimate synergies and underestimate integration challenges. The urge to vertically integrate seems hardwired into executive psychology, resistant to the mountain of evidence against it.

Capital Allocation Lessons: AT&T's failed diversification offers textbook lessons in capital allocation. The company destroyed hundreds of billions in shareholder value through acquisitions that never made strategic sense. Management consistently chose empire-building over returns, growth over profitability, headlines over fundamentals.

The debt trap that resulted was predictable and preventable. At the time Stephenson announced his departure, it was acknowledged that the acquisitions of DirectTV and Time Warner had by this point resulted in a massive debt burden of $200 billion for the company. Debt that seems manageable in good times becomes crushing when growth slows or strategy fails. AT&T learned this lesson at enormous cost.

XI. Bear vs. Bull Case & Investment Analysis**

The Bear Case:**

The pessimistic view on AT&T centers on structural challenges that may be insurmountable. The company carries a massive debt burden that, while reduced from its peak, still constrains strategic flexibility. Competition in wireless is intensifying, with T-Mobile's "Uncarrier" strategy continuing to take share. Cable companies are entering wireless through MVNOs, adding pricing pressure.

The dividend, while attractive at around 5.13% yield as of late 2024, remains vulnerable. The board of directors today declared a quarterly dividend of $0.2775 per share on the company's common shares. While this provides income, the sustainability depends on free cash flow generation in an increasingly competitive market.

The 5G investment cycle requires massive capital expenditure with uncertain returns. Capital investment in the $22 to $22.5 billion range for 2025 represents a significant burden. Unlike previous network upgrades, 5G's killer applications remain unclear, and the monetization path is uncertain.

Technological disruption looms large. Starlink and other satellite providers threaten rural markets. Fixed wireless from Verizon and T-Mobile competes with fiber. Over-the-top services continue to erode traditional revenue streams. AT&T's core services face commoditization pressures that may prove irreversible.

The Bull Case:

The optimistic view sees AT&T as a transformed company trading at attractive valuations. Under Stankey's leadership, AT&T expanded its network of fiber-optic cables, including to places it didn't already provide broadband, and entered a joint venture with BlackRock called Gigapower to build fiber-optic networks in metro areas around the country. Consumer fiber broadband revenue growth in the mid-teens annually provides a clear growth driver.

The infrastructure advantage is real and durable. AT&T's fiber network and 5G deployment create competitive moats that new entrants cannot easily replicate. The company expects to reach approximately 50 million customer locations with its in-region fiber network by 2030. This physical infrastructure becomes more valuable as data consumption explodes.

Free cash flow generation remains robust. For 2024, the company reported strong fourth-quarter and full-year results that showcased solid momentum in gaining and retaining profitable 5G and fiber subscribers. Free cash flow in the low-to-mid $16 billion range for 2025 supports both the dividend and debt reduction.

Valuation appears compelling for income investors. AT&T's stock currently trades around $21.90 with a market capitalization of approximately $157.03 billion, offering significant upside if execution improves. Analysts project moderate to significant growth for AT&T stock, particularly through 2025 and beyond.

Current Financial Position:

As of 2025, AT&T has successfully stabilized its financial position after years of turmoil. For 2024, adjusted EPS of $2.26 demonstrates solid profitability. The company met all 2024 consolidated financial guidance and reiterates all financial and operational guidance for 2025 and beyond.

The strategic focus on core connectivity is paying dividends. Mobility service revenue growth in the 2% to 3% range annually provides steady growth. Consumer fiber broadband revenue growth in the mid-teens annually offers a higher growth vector. The combination provides balanced exposure to both stable and growth segments.

Debt reduction continues but remains a long journey. The sale of the remaining DirecTV stake to TPG, expected to close in mid-2025, will provide additional proceeds for debt paydown. Net debt, while still substantial, is on a clear downward trajectory.

XII. Epilogue: What AT&T Teaches Us About Tech Monopolies

As we witness today's battles over Big Tech monopolies—the multi-pronged antitrust attempts against Google and Facebook—AT&T's century-and-a-half saga offers sobering lessons. The parallels are unmistakable: dominant platforms, network effects, regulatory capture, and the eternal dance between innovation and control.

Facebook's attempts to use national security arguments and Section 230 concessions mirror AT&T's monopoly defense strategies from the 1970s. Google's control over search resembles AT&T's control over long-distance. Amazon's vertical integration echoes the Bell System's structure. The arguments are recycled; only the technology changes.

But AT&T's story suggests that breaking up tech giants may not achieve what regulators intend. The Bell System's breakup didn't create lasting competition—it created temporary chaos followed by reconsolidation. The Baby Bells that were supposed to compete instead merged back together. The monopoly that was destroyed in 1984 essentially reconstituted itself by 2005.

Why do breakups alone fail to ensure competition? Because the underlying economics of network businesses naturally tend toward consolidation. High fixed costs, network effects, and economies of scale create powerful incentives to merge. Competition may flourish briefly after a breakup, but market forces inevitably drive reconsolidation.

The real innovation in telecommunications came not from the breakup but from technological disruption. Wireless technology, the internet, and fiber optics changed the game more than any regulatory intervention. MCI didn't defeat AT&T through antitrust law—it won by exploiting technological arbitrage. Netflix didn't need regulators to break up cable companies—it simply offered a better product.

This suggests that regulating Big Tech through breakups may be fighting the last war. The next telecommunications revolution—whether 5G, satellite internet, or something not yet invented—will likely come from entrepreneurs and engineers, not lawyers and regulators. Innovation, not antitrust, remains the most powerful force against monopoly.

The cycle of disruption and consolidation appears inevitable in platform businesses. Today's disruptors become tomorrow's incumbents. The startups that challenge monopolies eventually become monopolies themselves. AT&T began as Bell's startup challenging Western Union's telegraph monopoly and became the monopoly it had fought.

Infrastructure versus services emerges as a key distinction. AT&T's troubles came when it confused owning pipes with creating content. The skills needed to build networks differ fundamentally from those needed to produce entertainment. Companies that try to do both often fail at both. The current AT&T, focused on connectivity rather than content, may have finally learned this lesson.

Perhaps the most important lesson from AT&T's odyssey is humility about predicting the future. In 1984, nobody imagined that the Baby Bells would reconsolidate. In 2000, nobody predicted that AT&T would be saved by wireless. In 2018, nobody foresaw that streaming would make Time Warner worthless to AT&T. The next revolution in telecommunications will likely surprise us all.

XIII. Recent News**

Q4 2024 and Full Year Results:** AT&T Inc. (NYSE: T) reported strong fourth-quarter and full-year results that showcased solid momentum in gaining and retaining profitable 5G and fiber subscribers. The Company met all 2024 consolidated financial guidance and reiterates all financial and operational guidance for 2025 and beyond that was shared at its recent Analyst & Investor Day.

Q1 2025 Performance: AT&T Inc. (NYSE: T) reported solid first-quarter results that again showcase its ability to grow the right way with high-quality, profitable 5G and fiber subscriber additions. Revenues for the first quarter totaled $30.6 billion versus $30.0 billion in the year-ago quarter, up 2.0%. Net income rose to $4.7 billion, and adjusted earnings per share came in at $0.51, compared to $0.48 a year ago. Adjusted EBITDA reached $11.5 billion and free cash flow increased to $3.1 billion.

Q2 2025 Results: Revenues for the second quarter totaled $30.8 billion, versus $29.8 billion in the year-ago quarter, up 3.5%. The company demonstrated continued momentum in both 5G and fiber subscriber additions.

Fiber Expansion Milestones: AT&T will acquire substantially all of Lumen's Mass Markets fiber internet business in a deal expected to close in the first half of 2026. AT&T (NYSE:T) (the Company) has reached an agreement to acquire substantially all of Lumen's (NYSE: LUMN) Mass Markets fiber business for $5.75 billion. AT&T now passes 29.5 million consumer and business locations with fiber.

Strategic Initiatives: The Company intends to invest $3.5 billion of these savings into its network to accelerate its fiber internet build-out to a pace of 4 million locations per year, a run-rate it expects to achieve by the end of 2026. As a result of this increased pace of organic fiber deployment, AT&T expects that by the end of 2030 it will reach approximately 50 million customer locations with its in-region fiber network and more than 60 million fiber locations when including the Lumen Mass Markets fiber assets it has agreed to acquire and plans to expand, its Gigapower joint venture, and agreements with other commercial open access providers.

5G Network Progress: AT&T's Mobility business remained a key growth driver, with 324,000 postpaid phone net adds in Q1 and service revenue rising 4.1% year over year to $16.7 billion. Total wireless revenue reached $21.6 billion, up 4.7%, thanks in part to a 6.9% increase in equipment sales and higher average revenue per user (ARPU), which grew 1.8% to $56.56.

DirecTV Sale Update: Additionally, the Company continues to expect the sale of its entire 70% stake in DIRECTV to TPG to close in mid-2025. This transaction will provide additional liquidity for debt reduction and strategic investments.

Management Commentary: "The strong results this quarter are the result of a four-plus-year period of hard work and consistent execution by our teams, which has positioned us well for a new era of growth," said John Stankey, AT&T CEO. "Our business fundamentals remain strong, and we are uniquely positioned to win in this dynamic and competitive market. We are growing the right way as customers continue to choose AT&T Fiber and 5G wireless for connectivity they can rely on, guaranteed or we'll make it right."

XIV. Links & References

Books on AT&T History and the Breakup: - "The Deal of the Century: The Breakup of AT&T" by Steve Coll - "The Master Switch" by Tim Wu - "Telephone: The First Hundred Years" by John Brooks - "The Rape of Ma Bell" by Constantine Raymond Kraus and Alfred W. Duerig

Key Court Documents and Regulatory Filings: - United States v. AT&T, 552 F.Supp. 131 (1982) - Modification of Final Judgment (1982) - FCC Execunet Decisions (1977-1978) - Telecommunications Act of 1996

Academic Papers on Telecommunications Economics: - "The Failure of Antitrust and Regulation to Establish Competition in Long-Distance Telephone Services" by Paul W. MacAvoy - "The Bell System Divestiture: A Note on the Sources of Regulatory Failure" by Richard H.K. Vietor - "Competition and Regulation in Telecommunications" by Jean-Jacques Laffont and Jean Tirole

Industry Analysis and Reports: - AT&T Investor Relations (investors.att.com) - FCC Communications Marketplace Reports - CTIA Wireless Industry Reports - Broadband Now Research

Historical Archives and Primary Sources: - AT&T Archives and History Center - Bell System Memorial (memorial.bellsystem.com) - Federal Communications Commission Historical Documents - Computer History Museum Bell Labs Collection

Relevant Podcasts and Documentaries: - Acquired.fm episodes on telecommunications - "The Telephone" documentary (American Experience) - "Pirates of Silicon Valley" (HBO) - "The Network" podcast series

Note: This analysis represents historical research and market observations, not investment advice. All financial decisions should be made in consultation with qualified financial advisors. Past performance does not guarantee future results.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube