Vodafone Idea (Vi): The "Too Big to Fail" Telecom Survivor

I. Introduction: The Hook

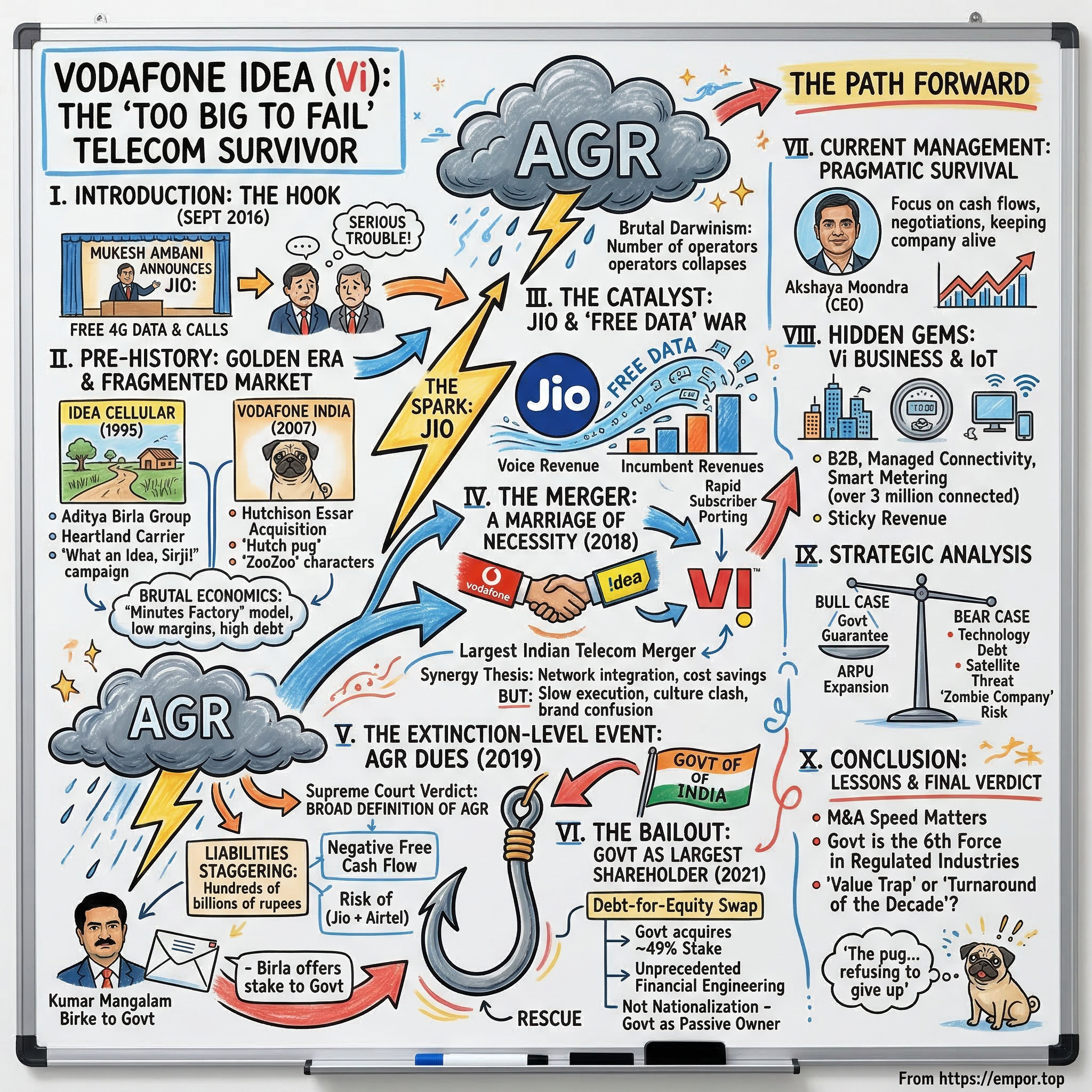

Picture this: It is September 2016, and in a gleaming convention center in Mumbai, Mukesh Ambani—the richest man in India—steps onto a stage and announces that Reliance Jio will give away free 4G data and voice calls to anyone who wants them. Free. Unlimited. Just come and get it. In the audience, telecom executives from a dozen companies feel their stomachs drop. In boardrooms at Vodafone India and Idea Cellular, two of the largest wireless operators in the country, executives exchange glances that say: We are in serious trouble.

What follows over the next decade is one of the most dramatic corporate survival stories in emerging-market history. It is a story about what happens when two giants merge not to conquer the world, but simply to survive a new predator. It is a story about a fifteen-year legal battle over three words—"Adjusted Gross Revenue"—that nearly bankrupted an entire industry. And it is a story about the Indian government making the extraordinary decision to become the largest shareholder in a private telecom company, not because it wanted to, but because the alternative—a two-player monopoly controlling the communications infrastructure for 1.4 billion people—was simply unacceptable.

Today, Vodafone Idea—rebranded simply as "Vi"—generates roughly 435 billion rupees in annual revenue, or about five billion dollars. It serves over 200 million mobile subscribers. But the most important number on its balance sheet is not revenue, or subscribers, or even its staggering two-trillion-rupee debt pile. The most important number is 49 percent—the approximate stake now held by the Government of India, making the sovereign the single largest shareholder in what was once a purely private enterprise. The government did not buy this stake. It did not nationalize the company. It acquired its ownership through one of the most creative pieces of financial engineering in Indian corporate history: converting unpaid interest on deferred government dues into equity shares.

The narrative arc here is extraordinary. From the glory days of the Hutch pug—that adorable dog that followed its owner everywhere in one of India's most beloved advertising campaigns—and the "What an Idea, Sirji!" tagline that became part of everyday Indian conversation, to the brink of liquidation, to an unprecedented government rescue. And buried within this story of near-death and resuscitation is something most analysts overlook: a quietly growing enterprise business called Vi Business that might actually be the jewel in the crown, generating sticky, high-margin revenue from corporate clients, smart meters, and IoT connectivity while the consumer mobile business wages its endless price war.

This is the story of Vodafone Idea: the telecom that was too big to fail, too broke to fix, and too important to ignore.

II. Pre-History: The Golden Era and the Fragmented Market

To understand what Vodafone Idea became, you have to understand what India's telecom market looked like before the great consolidation—and why it was both the most exciting and most chaotic wireless market on the planet.

Start with Idea Cellular. The company was born in 1995 as a joint venture involving the Aditya Birla Group, one of India's oldest and most diversified conglomerates. The Birla family had made their fortune in commodities—cement, aluminum, chemicals—the heavy industries that built modern India. Telecom was a departure, a bet on the country's coming digital revolution. But the Birlas brought something invaluable to the game: deep relationships across India's smaller cities and rural heartland. While competitors fought over Mumbai and Delhi, Idea Cellular quietly built dominance in states like Maharashtra, Gujarat, Madhya Pradesh, and Kerala. It was the "heartland carrier," the company that understood that India's telecom revolution would not be won in gleaming metros but in dusty district towns where a mobile phone was often the first piece of modern technology a family owned.

Idea's marketing was brilliant. The "What an Idea, Sirji!" campaign became a cultural phenomenon, positioning the brand as clever, accessible, and inherently Indian. The advertisements were witty—they showed how mobile connectivity could solve everyday Indian problems, from caste discrimination to election fraud. It was aspirational without being elitist, which perfectly matched Idea's customer base.

Then there was Vodafone India, which arrived via one of the most dramatic acquisitions in Asian corporate history. In 2007, Vodafone Group—the British telecom giant headquartered in Newbury, England—paid approximately eleven billion dollars to acquire a 67 percent stake in Hutchison Essar, the Indian wireless business controlled by Hong Kong billionaire Li Ka-shing. Eleven billion dollars for a company in a market where the average revenue per user was already among the lowest in the world. Vodafone was making the classic "bet on India" play: the country had a billion people, mobile penetration was still below 20 percent, and surely the sheer volume of subscribers would compensate for low per-user revenue. The Hutch brand was already beloved—that pug dog, trotting loyally after its owner through city streets and countryside, had become one of the most recognizable brand mascots in Indian advertising history. Vodafone wisely kept the emotional equity, transitioning from "Hutch" to "Vodafone" with the tagline "Change is good" while introducing its own global brand elements, including the iconic ZooZoo characters that debuted during the Indian Premier League cricket season and became instant viral sensations.

But what made the pre-Jio Indian telecom market truly unique was its extraordinary fragmentation. At its peak, India had more than a dozen licensed operators competing across 22 "circles"—the regulatory term for geographic service areas. In a single city, a consumer might choose between Airtel, Vodafone, Idea, BSNL, Reliance Communications, Tata Docomo, Uninor (later Telenor), Aircel, MTS, Videocon, and several others. The economics were brutal. Operators competed primarily on price, driving the cost of a voice call down to less than one paisa per second—a fraction of a US cent. The business model was what industry insiders called the "minutes factory": buy spectrum, build towers, push as many voice minutes through the pipes as possible, and hope that volume compensated for razor-thin margins. India became the cheapest mobile market in the world, which was wonderful for consumers but slowly corrosive for operators' balance sheets.

The warning signs were everywhere. Spectrum auctions in 2010 and 2014 forced operators to pay enormous sums to the government for airwave licenses—money borrowed at high interest rates, creating debt loads that assumed continued revenue growth. But revenue growth was already slowing because every new competitor drove prices lower. The market was a classic example of what happens when too much capital chases too little pricing power. By 2015, India's telecom industry was generating over a trillion rupees in revenue but barely covering its cost of capital. It was a powder keg waiting for a spark.

That spark had a name: Jio.

III. The Catalyst: Jio and the "Free Data" War

The story of Reliance Jio's entry into Indian telecom has been told many times, but it is worth dwelling on because the sheer audacity of what Mukesh Ambani did—and the devastating precision with which he did it—fundamentally altered the economics of an entire industry and set in motion the chain of events that would bring Vodafone and Idea to their knees.

Mukesh Ambani had been planning Jio for years. His father, the legendary Dhirubhai Ambani, had founded Reliance Industries as a textiles company in the 1960s and transformed it into India's largest private corporation through a combination of vision, political savvy, and ruthless execution. After Dhirubhai's death in 2002 and the bitter split between Mukesh and his brother Anil (who got the original Reliance Communications telecom business), Mukesh set about building his own telecom empire from scratch. He acquired broadband wireless access spectrum in 2010, then upgraded it to 4G LTE capability. While incumbents were still arguing about whether to invest in 3G or wait for 4G, Ambani spent over two trillion rupees—roughly 25 billion dollars—building an entirely greenfield 4G-only network that covered virtually the entire country.

On September 5, 2016, Jio launched commercially. The offer was staggering: free voice calls forever—not for a promotional period, but permanently. Free data for the first six months. When the promotional period ended, data prices were set at roughly one-tenth of what incumbents were charging. The logic was brutally simple and devastatingly effective. Ambani understood that in a market where voice revenue was already declining, the future belonged to data. By making voice free, he destroyed the primary revenue stream of every incumbent operator overnight. By pricing data at levels no competitor could match—subsidized by Reliance Industries' petrochemical profits—he ensured that customers would flock to Jio in the hundreds of millions.

And flock they did. Within six months, Jio had over 100 million subscribers. Within a year, it had over 130 million. These were not just new-to-mobile customers; they were existing subscribers who were porting their numbers from Airtel, Vodafone, and Idea, attracted by the combination of free voice, cheap data, and a brand-new 4G network that actually worked. The incumbents' 2G and 3G networks suddenly looked antique.

The impact on incumbent financials was immediate and catastrophic. In the quarter ending December 2016—just three months after Jio's launch—Idea Cellular's revenue fell 3.5 percent sequentially and its net profit turned into a net loss. Vodafone India's numbers were similarly grim. The "minutes factory" model that had sustained the industry for a decade was broken. Voice revenue, which had accounted for roughly 75 percent of industry revenue, collapsed as operators were forced to match Jio's free voice offering or watch their subscribers walk out the door. Data revenue grew, but not nearly fast enough to compensate—Jio had set data prices so low that even rapid volume growth could not offset the per-gigabyte price destruction.

In boardrooms across the industry, the calculus was stark. Competing with Jio required massive capital expenditure to build out 4G networks, acquire new spectrum, and match pricing that was below the cost of service for any operator that had to actually earn a return on capital. Jio could afford to lose money because it was backed by the cash flows of Reliance Industries' oil refining and petrochemicals businesses—the largest such operation in the world. For standalone telecom companies, there was no sugar daddy to cover the losses.

The industry's response was brutal Darwinism. Within two years of Jio's launch, the number of major operators in India collapsed from a dozen to effectively four. Reliance Communications—ironically, Anil Ambani's company—went bankrupt. Aircel filed for insolvency. Tata Docomo exited the consumer mobile business. Telenor sold its Indian operations to Airtel. MTS and Videocon disappeared. It was the fastest and most violent consolidation in global telecom history. An industry that had taken two decades to build was reshaped in twenty-four months.

For Vodafone India and Idea Cellular, the math was clear: neither company, standing alone, could survive the capex war against Jio while simultaneously servicing the enormous debt loads from previous spectrum auctions. If Porter's Five Forces analysis before Jio's entry showed rivalry as "high," after September 2016 it went to what one analyst memorably called "nuclear." The only path to survival was to combine—to merge the number two and number three operators into a single entity that might, just might, achieve the scale needed to compete. It was not a merger born of ambition. It was a merger born of desperation.

IV. The Merger: A Marriage of Necessity

On March 20, 2017—barely six months after Jio's commercial launch—Vodafone Group and the Aditya Birla Group announced what would become the largest telecom merger in Indian history. Vodafone India and Idea Cellular would combine to create the country's largest wireless operator by subscribers, with a combined customer base of approximately 400 million. The new entity would hold the most spectrum of any operator in India—1,850 MHz across all bands—and would operate in all 22 telecom circles. On paper, the deal was a masterstroke.

The synergy thesis was compelling. Management projected annual savings of roughly 840 billion rupees—over ten billion dollars—through network integration, tower sharing, elimination of duplicate operations, and optimized spectrum utilization. Two overlapping networks could be consolidated into one more efficient network. Two sets of corporate headquarters, two marketing departments, two billing systems could be merged. The combined entity would have the scale to negotiate better rates with equipment vendors, tower companies, and content providers.

The deal structure reflected the reality that this was a merger of equals in distress rather than an acquisition by a position of strength. Vodafone Group would hold approximately 45 percent of the merged entity, the Aditya Birla Group would hold roughly 26 percent, and the remainder would be held by public shareholders. Kumar Mangalam Birla, the chairman of the Aditya Birla Group, would serve as chairman of the new company. The board would be balanced between Vodafone and Birla nominees. The brand question—a surprisingly emotional issue in Indian telecom—was left unresolved initially, with both the Vodafone and Idea brands continuing to operate in parallel.

The merger received regulatory approval and officially closed on August 31, 2018. Idea Cellular Limited was renamed Vodafone Idea Limited. On paper, the number one Indian telecom operator had been born.

But paper and reality are different things, and the integration of Vodafone India and Idea Cellular turned into one of the most painful corporate mergers in Indian business history. The problems were manifold. First, there was the network challenge. Vodafone's network was strongest in urban areas—Mumbai, Delhi, Kolkata, Bangalore—where it had inherited Hutchison Essar's premium positioning. Idea's network was strongest in semi-urban and rural India—the heartland states where the Birla brand had deep roots. Combining these networks required rationalization of hundreds of thousands of cell sites, migration of subscribers between technology platforms, and harmonization of vastly different network architectures. In some circles, Vodafone ran on Ericsson equipment while Idea ran on Nokia. Integrating these was not just an engineering challenge but an organizational nightmare.

Second, there was the culture clash. Vodafone India was, at its core, a multinational corporation—it had global processes, international reporting requirements, and a management culture shaped by its British parent. Idea Cellular was an Indian conglomerate business—entrepreneurial, relationship-driven, with decision-making processes rooted in the Birla Group's century-old management traditions. These cultures did not blend easily. Key executives left during the integration, taking institutional knowledge with them. Employee morale suffered as people wondered which "side" would win the inevitable turf battles.

Third, and most damagingly, there was the brand confusion. For over a year after the merger closed, the company operated with two separate brands in the market—Vodafone and Idea—confusing customers and diluting marketing spend. It was not until September 2020 that the company finally unveiled the unified "Vi" brand, a full two years after the merger. By that point, the brand damage was done. Customers who might have stayed loyal to either Vodafone or Idea found it easier to switch to Jio or Airtel, which had clear, singular brand identities.

The opportunity cost of this protracted integration was enormous. While Vodafone Idea spent 2018 and 2019 focused inward—merging networks, consolidating operations, resolving cultural conflicts—Jio spent those same two years aggressively expanding its 4G footprint, launching JioFiber for home broadband, and building an ecosystem of digital services. Airtel, the other major survivor, used the same period to raise capital, invest in its 4G network, and position itself as the premium alternative to Jio. Vodafone Idea was running a three-legged race while its competitors sprinted.

The merged entity also inherited a crushing debt burden. Between them, Vodafone and Idea had accumulated enormous liabilities from spectrum auctions conducted in 2014, 2015, and 2016—auctions where operators had bid aggressively for airwave licenses, betting on revenue growth that Jio's entry had now made impossible. The combined company entered life with roughly 1.2 trillion rupees in debt, with annual interest costs that consumed a terrifying proportion of operating cash flow. Revenue was declining, costs were sticky, and the debt service burden was relentless. The merger had created scale, but scale without financial flexibility is just a bigger target.

The harsh verdict of history is this: the merger was necessary—without it, both companies would certainly have failed individually. But the execution was too slow, the integration too painful, and the strategic response to Jio too tentative. In the classic language of telecom M&A analysis, two turkeys had merged, but they had not produced an eagle. They had produced a larger, somewhat healthier turkey—one that could survive longer but still could not fly.

And then, just as the integration challenges were beginning to ease, the real crisis hit.

V. The Extinction-Level Event: AGR Dues

To understand the AGR crisis, you need to understand a fifteen-year legal battle over three words that nearly destroyed the Indian telecom industry: "Adjusted Gross Revenue."

When the Indian government first licensed private telecom operators in the 1990s, it established a revenue-sharing model. Operators would pay the government a percentage of their "Adjusted Gross Revenue" as license fees and spectrum usage charges. The concept seemed straightforward: take your gross revenue, subtract certain pass-through charges, and pay the government its cut. The problem was that the definition of "gross revenue" was ambiguous, and ambiguity in regulation is an invitation for litigation.

The telecom operators argued—reasonably, they believed—that AGR should include only revenue from core telecom services: voice calls, data usage, messaging. The government's Department of Telecommunications argued that AGR should include all revenue, including non-telecom income such as interest on deposits, dividend income, capital gains on asset sales, and revenue from ancillary businesses. The difference was enormous. Under the operators' interpretation, AGR was significantly lower, meaning they owed less in license fees. Under the government's interpretation, operators had been systematically underpaying for years, and the accumulated shortfall—plus interest and penalties—ran into the hundreds of billions of rupees.

The dispute wound through Indian courts for over a decade. In 2015, the Telecom Disputes Settlement Appellate Tribunal ruled partly in favor of the operators. The government appealed. The case reached the Supreme Court of India.

On October 24, 2019, the Supreme Court delivered its verdict. In a ruling that sent shockwaves through the industry, the court sided entirely with the government. AGR would be calculated using the government's broader definition, and operators owed the full amount of past dues—including interest, penalties, and interest on penalties—going back to the inception of their licenses. The numbers were staggering. Across the industry, the total liability was estimated at roughly 1.47 trillion rupees. For Vodafone Idea alone, the initial assessment was approximately 580 billion rupees—roughly seven billion dollars.

To put this in context: Vodafone Idea's annual revenue at the time was approximately 420 billion rupees. The company was being asked to pay more than an entire year's revenue in back dues, on top of its existing debt of over a trillion rupees, while generating negative free cash flow. It was, as one industry analyst described it, an "extinction-level event."

The company's response was a mix of legal maneuvering and public alarm. Vodafone Idea filed review petitions with the Supreme Court, arguing that the penalties were disproportionate and would force the company into insolvency. Kumar Mangalam Birla wrote to the government, effectively saying that the promoters—Vodafone Group and the Birla family—could not inject fresh equity into a company facing liabilities of this magnitude without some form of government relief. Vodafone Group's CEO Nick Read was even more blunt, telling investors in November 2019 that without government intervention, Vodafone Idea would not survive. The implicit threat was clear: if the government enforced the AGR ruling in full, India would go from three private telecom operators to two—Jio and Airtel—creating a de facto duopoly.

The Supreme Court, in January 2020, rejected the review petitions. There would be no judicial relief. The operators owed what they owed. The court did grant a ten-year payment timeline, but even spread over a decade, the annual payments were crippling for a company already bleeding cash.

What followed was a slow-motion crisis that stretched from 2020 through 2023. Vodafone Idea continued to lose subscribers—falling from roughly 300 million at the time of the merger to around 215 million by mid-2023—as customers churned to Jio and Airtel, networks that were investing in 4G expansion while Vi struggled to maintain its existing infrastructure. The company's EBITDA margin remained in the low-to-mid 40 percent range, which sounds healthy until you realize that essentially all of that EBITDA was consumed by interest payments on spectrum dues, AGR liabilities, and bank debt. Cash flow after debt service was deeply negative. The balance sheet showed negative net worth—the company technically owed more than it owned.

Kumar Mangalam Birla, in August 2021, offered to hand over his personal stake in Vodafone Idea to the government or any other entity that the government deemed suitable, rather than allow the company to die. It was an extraordinary gesture from one of India's most prominent industrialists—an admission that the situation had moved beyond what private capital could solve.

The government faced a genuine dilemma. Allowing Vodafone Idea to collapse would recover nothing on the AGR dues—you cannot collect from a corpse—and would leave 200 million mobile subscribers scrambling to find new providers. More strategically, it would create a telecom duopoly. India's 1.4 billion people would be served by just two private wireless operators: Jio, controlled by the Ambanis, and Airtel, controlled by the Mittals. In a sector as critical as telecommunications—the backbone of digital payments, e-governance, rural connectivity, and national security—a duopoly was a risk the government was unwilling to take.

The solution, when it came, was unprecedented.

VI. The Bailout: Government as the Largest Shareholder

In September 2021, the Indian government announced a telecom relief package that was remarkable in both its scope and its creative financial engineering. The package had several components: a four-year moratorium on spectrum and AGR dues payments, allowing operators to defer their obligations; redefinition of AGR going forward to exclude non-telecom revenue; reduction of the bank guarantee requirements; and—most critically—the option for operators to convert the interest accrued during the moratorium period into government equity.

This last provision was the game-changer. Rather than requiring Vodafone Idea to pay interest on its deferred dues in cash—cash it simply did not have—the government would accept equity shares instead. In effect, the government was converting its role from creditor to owner.

Vodafone Idea immediately opted for the equity conversion. In January 2022, the government converted approximately 160 billion rupees of accrued interest into equity, giving it a roughly 33 percent stake in the company. The conversion was done at the prevailing market price of approximately ten rupees per share, resulting in the issuance of billions of new shares to the government. Overnight, the President of India—acting on behalf of the sovereign—became the single largest shareholder in Vodafone Idea, surpassing both Vodafone Group and the Birla family.

It was, as many commentators noted, the strangest "nationalization" that was not actually a nationalization. The government had not seized the company. It had not installed its own management. It had not changed the board composition or operational strategy. It had simply converted a financial claim into an ownership stake—a swap of debt for equity that happened to make the sovereign the controlling shareholder. The government explicitly stated that it had no intention of managing the company and would treat its stake as a financial investment to be divested at an appropriate time.

But the initial relief package, while buying time, was not enough. Vodafone Idea still needed massive capital investment to upgrade its network to 4G (and eventually 5G) across its coverage area, and private investors were reluctant to put money into a company with negative net worth and a government as its largest shareholder. The company managed to raise approximately 180 billion rupees through a follow-on public offering in April 2024—a significant amount but still far short of the estimated 500-plus billion rupees needed for a full network overhaul.

The government's stake continued to grow through additional interest-to-equity conversions. By late 2025, the government's holding had risen to approximately 49 percent—just below the 50 percent threshold that would technically make it a government-owned enterprise and trigger a different set of regulatory and employment obligations. This was almost certainly by design: the government wanted control without the legal complications of majority ownership.

The turning point came in late 2025 when the government announced an expanded relief framework that effectively froze the growth of AGR and spectrum dues through a combination of payment staggering and interest rate adjustments, extending the repayment timeline through 2041. This gave Vodafone Idea what it most desperately needed: visibility on its future cash obligations and a plausible path to financial stability—or at least to continued existence.

The current capital structure is unlike anything in Indian corporate history. The Government of India holds roughly 49 percent. Vodafone Group holds approximately 22 percent—significantly diluted from its original 45 percent post-merger stake. The Aditya Birla Group holds roughly 15 percent. Public shareholders hold the remainder. The promoters—Birla and Vodafone—retain operational control through board representation and management appointments, but their economic interest is now a minority position. It is a structure that creates strange incentive dynamics: the promoters are managing a company in which the government is the dominant economic owner but the passive governance partner. The government is the largest shareholder in a company it does not want to own and would prefer to exit. And public shareholders are betting that this awkward equilibrium can somehow produce a return.

The "Protector" role of the state is perhaps the most important strategic reality for anyone analyzing Vodafone Idea today. The government's 49 percent stake means it has an overwhelming financial incentive to ensure the company survives—a bankruptcy would mean writing off its entire equity position. It also means the government has implicit veto power over any major strategic decision, even if it chooses not to exercise that power day-to-day. For competitors, the government's presence is both a constraint and a guarantee: Jio and Airtel know they cannot push pricing so aggressively that it kills Vi, because the government will intervene before that happens. In some ways, Vi's greatest competitive advantage is not its network or its brand—it is the fact that the sovereign cannot afford to let it fail.

VII. Current Management and Incentives

Understanding who runs Vodafone Idea—and what motivates them—is essential to understanding the company's trajectory. This is not a company led by visionary founders chasing exponential growth. It is a company led by pragmatic operators focused on a single objective: survival.

The CEO is Akshaya Moondra, who took the top job in August 2023 after serving as Chief Financial Officer since the merger. Moondra is the quintessential insider—he joined Idea Cellular in 2005 and has been with the combined entity through every crisis, every court ruling, every balance sheet restructuring. He is not a charismatic public figure in the mold of Mukesh Ambani or Sunil Bharti Mittal. He does not give keynote speeches about disrupting industries or changing the world. He is a financial engineer, a man whose career has been defined by managing cash flows under extreme duress, negotiating with creditors, and finding creative ways to keep the lights on when the math says they should have gone dark years ago. In a company where the margin between solvency and insolvency is measured in basis points, having a CFO-turned-CEO makes perfect sense. His job description, if written honestly, would read: "Keep this company alive long enough for the market to recover."

Moondra's incentive structure reflects this reality. Management compensation at Vodafone Idea is modest by industry standards—this is not a company that can afford lavish stock option packages or performance bonuses tied to growth metrics. The executive team's primary incentive is reputational and professional: successfully navigating a turnaround of this complexity would make their careers. The secondary incentive is more visceral: if Vodafone Idea fails, 200 million subscribers lose service and roughly 10,000 employees lose their jobs. The weight of that responsibility is a powerful motivator.

Above Moondra sits Kumar Mangalam Birla, who serves as non-executive chairman. Birla's role in the Vi story is a fascinating study in the obligations of Indian business dynasties. The Birla family has been at the center of Indian commerce for over a century—from jute mills in colonial Calcutta to the modern Aditya Birla Group's global operations in metals, cement, chemicals, fashion, and financial services. For Kumar Mangalam Birla, Vodafone Idea is not just a business investment; it is a matter of family and group reputation. The Birla name is on this company. When he offered to hand over his stake to the government in 2021, it was an act of both desperation and honor—an acknowledgment that the situation was beyond his control, combined with a refusal to simply walk away from the obligations.

Birla stepped back from active involvement after that 2021 letter but has since re-engaged as the company's prospects have stabilized. His "skin in the game" is less about the financial value of his diluted stake—which is modest relative to his overall wealth—and more about the reputational cost of being associated with a failure of this magnitude. The Aditya Birla Group's credibility in Indian business circles, its ability to raise capital for other ventures, and its standing with regulators and policymakers are all, to some degree, linked to the outcome at Vodafone Idea.

On the Vodafone Group side, the engagement has been more arm's-length. Vodafone Group, under CEO Margherita Della Valle, has been focused on its European operations and has treated its Indian stake as a legacy position to be managed rather than a growth investment to be nurtured. Vodafone Group has not injected fresh equity into Vi since the merger and has steadily reduced its involvement, though it retains board representation and certain governance rights. The relationship is cordial but distant—the parent has accepted that its Indian bet did not work out as planned and is now primarily interested in recovering whatever residual value it can, whenever an exit opportunity presents itself.

The shareholding dynamics create an unusual management challenge. The executives running the company day-to-day own very little stock personally. The government—the largest shareholder—has explicitly said it does not want to manage the company. The promoters retain control rights but have limited economic upside given their diluted stakes. The result is a management team whose primary incentive is operational turnaround to prevent the government from triggering additional equity conversions or, in an extreme scenario, exercising its effective veto power to install its own leadership. It is management by existential threat rather than by equity incentive—not ideal from a corporate governance textbook perspective, but perhaps appropriate for a company in Vi's extraordinary circumstances.

VIII. The Hidden Gems: Vi Business and IoT

Amid the relentless drumbeat of subscriber losses, balance sheet crises, and regulatory battles, something interesting has been happening quietly inside Vodafone Idea. The company has been building an enterprise business that, while still dwarfed by the consumer mobile operation in revenue terms, represents arguably the most strategically valuable asset in the entire company.

Vi Business—the company's B2B arm—serves thousands of corporate clients across India, from small and medium enterprises to some of the country's largest corporations. The business provides managed connectivity solutions, cloud-based services, cybersecurity offerings, and unified communications platforms. But the real differentiator is in the Internet of Things.

Consider smart metering. India is in the middle of the world's largest smart electricity meter deployment, a government initiative to replace 250 million conventional meters with smart meters that can be read remotely, detect theft, enable dynamic pricing, and reduce the staggering distribution losses that plague India's power sector. These smart meters need cellular connectivity—they need to send data back to utility control centers, receive firmware updates, and communicate with each other. Vi Business has emerged as one of the leading connectivity providers for this initiative, with over three million smart meters connected to its IoT platform and growing rapidly. Each connected meter generates a small but predictable monthly revenue stream—low individually, but at scale, with millions of meters, it adds up to meaningful and extraordinarily sticky revenue. A utility that has deployed three million Vi-connected smart meters is not going to switch providers because Jio drops its consumer data price by ten percent.

The IoT opportunity extends well beyond smart metering. Vi's IoT platform connects vehicle tracking systems for logistics companies, environmental sensors for manufacturing plants, point-of-sale terminals for retailers, and asset monitoring devices for infrastructure operators. The total addressable market for IoT connectivity in India is enormous and growing rapidly as the country digitizes its economy. Vi's advantage here is somewhat counterintuitive: its legacy 2G and 3G network, which is a liability in the consumer smartphone market, is actually well-suited for IoT applications that require wide-area coverage but only need to transmit small amounts of data. Many IoT devices operate perfectly well on 2G connections—they do not need to stream video or download apps; they just need to send a meter reading or a GPS coordinate every few minutes.

Vi Business also operates in the cloud and advertising technology spaces. Vi Ads, the company's digital advertising platform, leverages the anonymized behavioral data from its subscriber base to offer targeted advertising capabilities to brands—a business that generates revenue without requiring additional network investment. Partnerships with hyperscale cloud providers like Microsoft Azure and Amazon Web Services allow Vi to bundle connectivity with cloud services for enterprise clients, creating integrated solutions that are harder for competitors to replicate than simple mobile connections.

The significance of the enterprise business for Vodafone Idea's future cannot be overstated. Consumer mobile in India is a commodity business where competition is primarily on price, switching costs are minimal (mobile number portability makes it trivially easy to change providers), and customer loyalty is ephemeral. Enterprise and IoT, by contrast, offer higher margins, longer contract durations, and genuine switching costs. A corporation that has integrated Vi's managed network into its operations—connecting its branches, powering its IoT sensors, running its unified communications—faces significant cost and disruption in migrating to another provider. This stickiness is worth far more, per rupee of revenue, than any consumer mobile subscription.

The challenge is scale. Vi Business is still a relatively small part of the company's overall revenue, and growing it requires investment in sales teams, platforms, and partnerships at a time when capital is the company's scarcest resource. The enterprise business is also not immune to competition—Airtel has its own strong enterprise offering, and Jio is building one aggressively. But for investors looking for a reason to believe in Vodafone Idea's long-term viability beyond "the government will not let it die," the enterprise and IoT business is the most compelling answer.

IX. Strategic Analysis: 7 Powers and the Bull/Bear Case

Applying Hamilton Helmer's Seven Powers framework to Vodafone Idea reveals a company with a deeply mixed strategic position—some genuine advantages, some critical gaps, and a few factors that do not fit neatly into any standard framework because the government's role as shareholder-protector is, itself, a strategic anomaly.

Start with Cornered Resource. Vodafone Idea holds substantial spectrum across multiple bands—it is among the largest spectrum holders in India. Spectrum is the definition of a cornered resource: it is finite, government-allocated, and essential for providing wireless service. However, Vi's spectrum is heavily mortgaged—much of it was acquired through government auctions at prices that now look inflated relative to the revenue the company generates. Owning spectrum you cannot fully monetize because you lack the capital to build out the network is like owning a gold mine you cannot afford to dig. The resource is real, but its value depends on the company's ability to invest in infrastructure—which brings us back to the capital problem.

Switching Costs present a split picture. For consumer mobile subscribers, switching costs are essentially zero. India's mobile number portability regime means any subscriber can change providers while keeping their phone number, and the process takes just a few days. This is terrible for Vi, which has been losing consumer subscribers steadily for years. For enterprise clients, the picture is different. As discussed in the Vi Business section, corporate customers who have integrated Vi's managed connectivity, IoT platforms, and cloud services face meaningful switching costs—not just financial but operational. This is the strategic moat that the enterprise business provides, and it is the primary reason that business is so valuable relative to its current revenue contribution.

Scale Economies are where Vi fails most obviously. Jio operates the largest 4G network in India with over 480 million subscribers, giving it the lowest per-subscriber cost in the industry. Airtel, with over 370 million subscribers, is the clear number two. Vi, with roughly 215 million subscribers—and declining—has lost the scale advantage that the merger was supposed to deliver. In a capital-intensive business like telecom, per-subscriber costs decline dramatically with scale, meaning Vi is at a structural cost disadvantage against both larger competitors. Every subscriber that churns from Vi to Jio or Airtel makes this disadvantage worse—a vicious cycle that is difficult to break without significant new investment.

Counter-Positioning is perhaps the most painful lens. Jio counter-positioned against the entire incumbent industry by building a 4G-only network at a time when incumbents were burdened by legacy 2G/3G infrastructure. Vi is not the counter-positioner—it is the victim of counter-positioning. Its legacy network is a cost burden, not an advantage (except in the narrow IoT use case discussed earlier). There is no obvious way for Vi to counter-position against Jio or Airtel today.

Network Effects are limited. Telecom networks have interconnection obligations—a Vi subscriber can call a Jio subscriber seamlessly—which means there is no "network effect" benefit to being on the largest network, unlike social media platforms. Vi gains no advantage from having more subscribers than the minimum needed for financial viability.

Process Power and Brand Power are marginal. Vi's operational processes are not demonstrably superior to competitors, and the "Vi" brand, while recognized, does not command a meaningful premium over Jio or Airtel in consumer perception surveys. The legacy brand equity of both Vodafone and Idea was diluted by the protracted brand transition.

Now apply Porter's Five Forces. Rivalry among existing competitors is intense—three private operators plus state-owned BSNL competing primarily on price in the consumer segment. Threat of New Entrants is low—the capital requirements and regulatory barriers to entering Indian telecom are prohibitive, which is one structural positive for Vi. Bargaining Power of Suppliers (equipment vendors like Nokia, Ericsson, Samsung; tower companies like Indus Towers and American Tower) is moderate to high—Vi's weak financial position limits its negotiating leverage. Bargaining Power of Buyers is high—consumers face zero switching costs and are highly price-sensitive. Threat of Substitutes is emerging—Starlink and other satellite broadband providers represent a potential long-term threat, particularly in rural areas where Vi's network coverage is weakest.

But the most important force acting on Vodafone Idea does not appear in Porter's original framework: the government as regulator, shareholder, and implicit guarantor. The government sets spectrum pricing, determines license terms, defines AGR, and now owns 49 percent of the company. In a regulated industry like Indian telecom, the government is Porter's Sixth Force—and for Vi, it is simultaneously the greatest threat (as the entity that imposed the AGR liability) and the greatest protector (as the shareholder that cannot afford to let the company fail).

The Bull Case rests on three pillars. First, the government's implicit guarantee. With 49 percent ownership, the government has every incentive to ensure Vi survives—it will adjust regulations, defer payments, and provide relief as needed to prevent a duopoly. Second, industry-wide ARPU expansion. India's average revenue per user remains among the lowest in the world—roughly 180-190 rupees per month for Vi versus over 200 for Airtel and Jio. The entire Indian telecom industry needs ARPU to rise for the sector to be financially viable, and recent tariff increases by all three operators suggest this is beginning to happen. Every ten-rupee increase in ARPU translates to meaningful incremental revenue and EBITDA for Vi. Third, the enterprise and IoT business represents a genuine growth engine with structural advantages that the consumer business lacks.

The Bear Case is equally compelling. First, technology debt. Competing in the 5G era requires massive capital expenditure that Vi simply does not have. Jio and Airtel have been aggressively rolling out 5G networks since late 2022; Vi has barely started. As consumer applications increasingly demand 5G speeds—high-definition video, cloud gaming, augmented reality—Vi's lack of 5G coverage becomes an accelerating reason for subscribers to leave. Second, the satellite disruption threat. Starlink and Jio's own satellite broadband initiative could erode Vi's position in rural and semi-urban India, precisely the heartland markets that were Idea Cellular's original strength. Third, and most fundamentally, the "zombie company" risk. A company that exists primarily to service its debt obligations—where EBITDA is consumed by interest payments, leaving nothing for network investment or shareholder returns—is technically alive but strategically dead. The risk is that Vi enters a stable but terminal equilibrium: too important to kill, too weak to thrive.

For investors tracking Vodafone Idea's ongoing performance, two KPIs matter above all else. The first is ARPU (Average Revenue Per User). This single metric captures both the company's pricing power and the industry's trajectory toward financial sustainability. Rising ARPU means more revenue from the same subscriber base, improving margins and cash flow without requiring additional capital investment. The second is subscriber trajectory—specifically, whether the quarterly net subscriber additions (or losses) are stabilizing. Vi has been losing subscribers for years; a stabilization, and eventually a return to net additions, would signal that the network investments are working and the brand is regaining relevance. Everything else—5G rollout timing, enterprise revenue growth, debt service coverage—flows from these two numbers.

X. Conclusion: Lessons and the Final Verdict

The Vodafone Idea story offers two profound lessons for anyone who studies business, invests in emerging markets, or thinks about the intersection of industry and government.

The first lesson is about M&A execution. The merger of Vodafone India and Idea Cellular validated the old industry adage: two turkeys do not make an eagle. The deal was strategically necessary—both companies would have died alone. But the value of a merger is not in the signing ceremony; it is in the speed and quality of integration. Vodafone Idea took over two years to unify its brand, struggled for even longer to rationalize its network, and lost millions of subscribers during the transition. Meanwhile, competitors moved forward. The lesson is that in a fast-moving industry facing existential competitive pressure, the speed of integration matters more than the precision of spreadsheet synergies. A good plan executed quickly beats a perfect plan executed slowly—especially when your competitor is Mukesh Ambani.

The second lesson is about the role of government in regulated industries. In Western markets, telecom operators worry about antitrust regulators, spectrum policy, and net neutrality rules. In India, the government is not just a regulator—it is a spectrum licensor, a revenue-sharing partner, a creditor, a judicial adversary (in the AGR case), and now a 49 percent equity owner. The AGR crisis demonstrated that in regulated markets, your most important stakeholder is not your customer, your competitor, or your shareholder—it is the sovereign. The government created the problem (by litigating for the broader AGR definition), suffered the consequences (an industry in financial distress), and then created the solution (the equity conversion and relief package). Understanding this dynamic is essential for anyone investing in regulated industries in emerging markets. Porter identified five forces that shape industry competition. In India's telecom sector, the government is the sixth force—and it is more powerful than the other five combined.

The final question—whether Vodafone Idea is a "value trap" or the "turnaround of the decade"—depends on which of these realities you weight more heavily. The company has negative net worth, massive debt, declining subscribers, minimal 5G capability, and a management team whose primary achievement has been preventing bankruptcy. On the other hand, it has a sovereign backstop, a rising ARPU environment, a quietly compelling enterprise business, and a stock price that already reflects catastrophic expectations. The market capitalization as of early 2026 hovers around one trillion rupees—roughly twelve billion dollars for a company serving over 200 million subscribers with a growing IoT business and spectrum holdings worth multiples of the current enterprise value in a replacement-cost analysis.

What is certain is this: Vodafone Idea will not die quietly. The government's 49 percent stake ensures that. Whether it will actually thrive—whether the patient will move from the ICU to rehabilitation to genuine health—depends on execution, capital allocation, and the continued willingness of India's 200-million-plus Vi subscribers to stick with a carrier that is fighting every day to earn their loyalty.

The pug that followed its owner everywhere may have a new name now. But it is still following, still loyal, still refusing to give up. Whether that loyalty is rewarded remains the most fascinating open question in Indian telecom.

XI. Outro

For those interested in diving deeper, Vodafone Idea's investor day presentations, quarterly earnings calls, and the "Vi" rebranding case study offer rich material for understanding both the operational details and the brand strategy challenges of managing a turnaround at this scale. The company's filings with the Bombay Stock Exchange and National Stock Exchange contain detailed disclosures on AGR dues, spectrum obligations, and the government equity conversion mechanics that are essential reading for serious analysts. The Telecom Regulatory Authority of India's quarterly performance reports provide independent subscriber and revenue data that can be cross-referenced against the company's own disclosures.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube