Altria Group: The Evolution of American Tobacco

I. Introduction & Episode Roadmap

Picture Richmond, Virginia, on a humid August morning in 2018. Inside Altria's gleaming headquarters, CEO Howard Willard is about to make the biggest bet in the company's 170-year history. On his desk: a term sheet to invest $12.8 billion—nearly a third of Altria's market cap—in a five-year-old e-cigarette startup called JUUL. The board has approved it. The bankers are ready. In four months, this decision will look brilliant. In four years, it will become one of the most spectacular corporate failures in American business history.

But we're getting ahead of ourselves.

Altria Group stands as one of the most paradoxical companies in American capitalism. It's simultaneously one of the most hated and most profitable enterprises ever created. Its flagship product, Marlboro, commands an astounding 42% of the U.S. cigarette market in 2024—a dominance that would make even tech monopolists envious. The company generated $24 billion in revenue last year and returned billions to shareholders through dividends and buybacks, maintaining its aristocrat status with 54 consecutive years of dividend increases.

Yet this is also a company whose core product kills half its customers when used as intended. A company that spent decades denying what it knew about addiction and cancer. A company that today openly states its mission is to "move beyond smoking"—essentially planning for the obsolescence of the very product that generates most of its profits.

The central question isn't just how a London tobacco shop founded in 1847 became one of America's most valuable companies. It's how this enterprise navigated—and continues navigating—an existential paradox: managing terminal decline while generating extraordinary returns, transforming from pariah to... well, still pariah, but a remarkably profitable one.

This is a story about American capitalism at its most complex. About the tension between shareholder returns and public health. About how a company can be simultaneously dying and thriving. About transformation, resilience, and the lengths corporations go to survive.

We'll trace Altria's journey from Philip Morris's humble London shop through the Marlboro Man's conquest of America, the great conglomerate experiment with Kraft and Miller Beer, the spin-off decade that created today's focused tobacco company, and the ongoing scramble to find growth in a world increasingly hostile to smoking. We'll dissect the JUUL catastrophe—how chasing the future cost $12.8 billion. And we'll examine what Altria's evolution tells us about corporate adaptation, regulatory capture, and the future of vice industries in modern capitalism.

Buckle up. This isn't just a business story—it's a mirror reflecting some of the most uncomfortable truths about American enterprise.

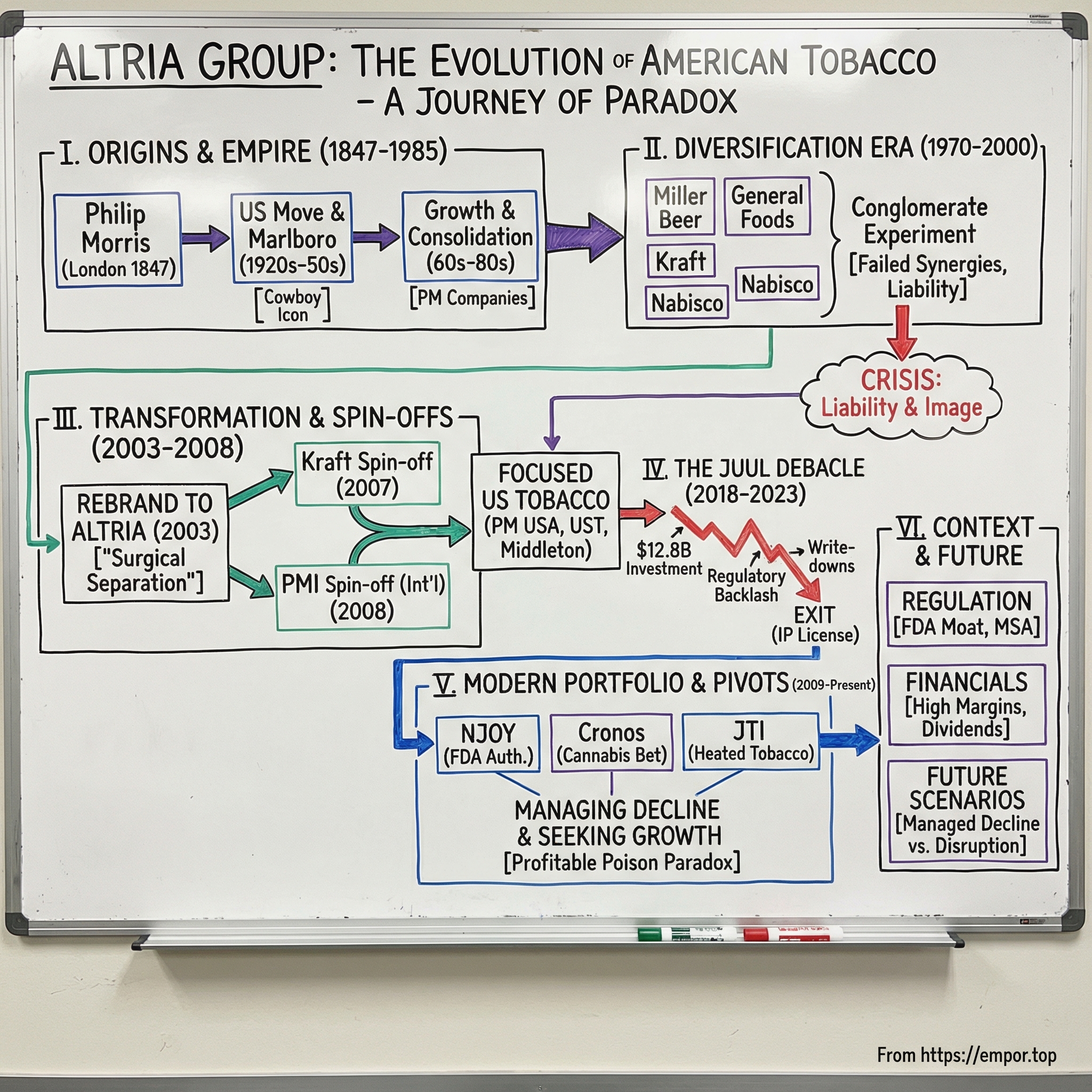

II. The Philip Morris Origins & Early Empire Building (1847–1985)

The London fog was particularly thick on Bond Street in 1847 when Philip Morris, a tobacconist and importer, opened his modest shop. Morris had no grand ambitions of empire—he simply wanted to serve the city's gentlemen with quality tobacco from Turkey and Egypt. He would have been astounded to learn that his name would one day be synonymous with the most valuable cigarette brand in history.

Morris died in 1873, leaving his widow Margaret and brother Leopold to manage the business. They struggled. By 1894, the family sold to William Curtis Thomson and his family, who owned it until 1901. The company bounced between owners like a Victorian orphan—each trying to extract value from the prestigious address and established clientele but lacking the vision for true scale.

Everything changed in 1902 when Gustav Eckmeyer, an importer who'd built a small tobacco empire, consolidated ownership. But even Eckmeyer was thinking small—premium cigarettes for London's elite. The real transformation came from an unlikely source: America's hunger for cigarettes and a group of ambitious businessmen who saw opportunity where others saw only a quaint British brand.

In 1919, a group of American investors led by Reuben M. Ellis incorporated Philip Morris & Co. Ltd. in Virginia. This wasn't just a geographic move—it was a complete reimagining of what the company could be. While the London operation continued making hand-rolled cigarettes for British aristocrats, the American venture began mass production. They introduced Marlboro in 1924 as a women's cigarette—"Mild as May" with a red filter tip to hide lipstick stains. Yes, Marlboro started as a ladies' brand. The irony is delicious.

The company limped through the Depression and World War II as a minor player. By 1954, Philip Morris had just 1% of the U.S. cigarette market. Lucky Strike, Camel, and Chesterfield dominated. Reader's Digest had just published "Cancer by the Carton," linking smoking to lung cancer. The industry was in crisis. Philip Morris needed a miracle.

Enter Leo Burnett, the advertising genius who'd created Tony the Tiger and the Jolly Green Giant. In 1954, Philip Morris hired Burnett to reposition Marlboro. The women's cigarette had failed. The health scare meant filtered cigarettes were suddenly in demand (filters implied safety, even if they didn't deliver it). Burnett's insight was brilliant and cynical: make Marlboro the most masculine cigarette ever created.

The Marlboro Man debuted in 1955—first as various rugged archetypes (sailors, athletes, cowboys), but by 1963, it was all cowboys, all the time. The campaign was psychological warfare at its finest. Worried about cancer? Here's a filter. Worried filters make you look weak? Here's a cowboy. The tagline—"Come to where the flavor is. Come to Marlboro Country"—sold not just cigarettes but an entire identity.

The transformation was staggering. Marlboro sales increased 3,000% within a year of the campaign launch. By 1972, Marlboro was the world's best-selling cigarette. The cowboy had conquered America.

But Philip Morris's true genius wasn't just marketing—it was operational excellence married to ruthless expansion. Under CEO George Weissman (1978-1984), the company perfected what insiders called "the Philip Morris way": obsessive focus on manufacturing efficiency, aggressive pricing strategies, and relentless market share capture. They pioneered "buy-downs"—paying retailers for prime shelf space. They perfected the art of line extensions—Marlboro Lights, Marlboro 100s, Marlboro Menthol. Each variant captured a different segment while reinforcing the master brand.

By 1983, Philip Morris surpassed R.J. Reynolds to become America's largest cigarette company. Marlboro alone commanded 22% market share and climbing. The company generated $1.5 billion in operating income from U.S. tobacco operations—margins that made other industries weep with envy.

In 1985, as Marlboro's dominance seemed unassailable, Philip Morris Companies was incorporated as a holding company structure. This wasn't just administrative reshuffling—it was preparation for what CEO Hamish Maxwell called "the next chapter." The tobacco cash cow was producing billions, but storm clouds were gathering. Smoking rates had peaked in 1964. Health advocates were mobilizing. Lawsuits were multiplying.

The question facing Philip Morris wasn't whether to diversify but how fast and how far. The answer would transform a cigarette company into one of the world's largest consumer goods conglomerates—and set the stage for one of corporate America's most audacious experiments in empire building.

III. The Diversification Era: Beyond Tobacco (1970–2000)

The Miller Brewing Company boardroom in Milwaukee was in chaos in June 1969. The 114-year-old brewery was bleeding cash, losing market share to Anheuser-Busch and Schlitz, and the controlling family was fighting over whether to sell. Into this mess walked John Murphy, Philip Morris's shrewd head of acquisitions, with a simple pitch: "Cigarettes and beer—they're both about marketing lifestyle products to blue-collar Americans. We know how to do this better than anyone."

Philip Morris acquired 53% of Miller in 1970 for $130 million, gaining full control by 1972. Wall Street was baffled. Why would a cigarette company buy a failing brewery? CEO George Weissman had a theory he called "transferable excellence"—the marketing magic that built Marlboro could work anywhere. He was about to test it at unprecedented scale.

The Miller transformation was Philip Morris's proof of concept. They brought in John Murphy as president and unleashed the Marlboro playbook: segment the market, advertise aggressively, innovate relentlessly. Miller Lite launched in 1975 with the "Tastes Great, Less Filling" campaign—turning diet beer from a punchline into a phenomenon. Miller High Life was repositioned from "The Champagne of Beers" (aristocratic, stuffy) to "Miller Time" (blue-collar reward after hard work). Sound familiar? It should—it was Marlboro Country with foam.

By 1978, Miller had rocketed from seventh to second place in U.S. beer sales. Revenue quintupled. The experiment had worked spectacularly. But Weissman and his successor Hamish Maxwell weren't satisfied with beer. They wanted an empire.

The shopping spree that followed was breathtaking in scope and ambition. In 1985, Philip Morris acquired General Foods for $5.6 billion—at the time, the largest non-oil acquisition in U.S. history. Suddenly, they owned Maxwell House coffee, Jell-O, Oscar Mayer hot dogs, and Birds Eye frozen vegetables. The rationale was elegant: stable cash flows, recession-resistant products, and brands that could benefit from Philip Morris's marketing muscle.

But Maxwell wasn't done. In 1988, he orchestrated the hostile takeover of Kraft Inc. for $12.9 billion, wrestling it away from RJR Nabisco in one of the most dramatic takeover battles of the decade. Now Philip Morris owned Kraft cheese, Miracle Whip, and Philadelphia cream cheese. The tobacco company had become America's largest consumer packaged goods company almost overnight.

The pièce de résistance came in 2000 with the $18.9 billion acquisition of Nabisco from RJR Reynolds—a delicious irony, buying the snack division from their cigarette rival. Oreos, Ritz crackers, Planters nuts—icons of American snacking now answered to the makers of Marlboro.

By 2000, Philip Morris Companies was a behemoth generating $80 billion in annual revenue. Tobacco contributed less than 40% of sales (though still 60% of profits—those margins remained untouchable). CEO Geoffrey Bible could truthfully claim Philip Morris was a "balanced consumer products company." Seven of the top 10 grocery brands in America were Philip Morris products. Your morning probably started with Maxwell House coffee and ended with a Kraft Singles grilled cheese.

The strategy seemed brilliant. As cigarette volumes declined 1-2% annually, food revenues grew 3-4%. The conglomerate structure provided what executives called "liability diversification"—harder to demonize a company that made both Marlboros and Oreos. The stable food earnings could cushion tobacco's volatility. Cross-selling opportunities abounded—Philip Morris's relationships with convenience stores and supermarkets could push food products, while food salespeople could secure better cigarette placements.

But beneath the surface, cracks were forming. The synergies never materialized—turns out selling cheese and selling cigarettes required completely different capabilities. Food company executives resented being tainted by tobacco association. Kraft struggled to recruit top talent who didn't want Philip Morris on their resume. Institutional investors interested in food stocks wouldn't touch Philip Morris because of ESG concerns.

Most critically, the liability protection proved illusory. Plaintiffs' attorneys argued the food assets made Philip Morris a deeper pocket worth pursuing. Juries seemed more willing to punish a company profiting from Oreos while selling cigarettes to kids. The stock traded at a "tobacco discount"—the combined company was worth less than its parts.

By 2001, new CEO Louis Camilleri faced reality: the conglomerate experiment had failed. Philip Morris stock traded at just 8 times earnings while pure-play food companies commanded 15-20 times. The company was literally worth more dead than alive. The great unbundling was inevitable.

But first, Camilleri had one more transformation to attempt—one that would fundamentally alter not just the company's structure but its very identity.

IV. The Altria Transformation & Spin-Offs (2003–2008)

The focus groups were brutal. It was late 2002, and Philip Morris had hired Wirthlin Worldwide to test new corporate names. In room after room across America, consumers reacted to "Philip Morris" with visceral disgust. "Death merchants," one participant spat. "Child killers," said another. The brand name that had existed since 1847 had become toxic—literally and figuratively.

CEO Louis Camilleri watched from behind one-way glass as his head of investor relations, Nick Rolli, presented the challenge to the board: "Gentlemen, our corporate name has negative brand equity. It actively destroys value. We need to change it, and we need to change it now."

The name change wasn't just cosmetic—it was existential. Lawsuits were mounting. The Department of Justice's RICO case was proceeding. States were demanding billions in healthcare cost reimbursements. Most urgently, the company needed to separate its food businesses, but no banker would underwrite a Kraft IPO with Philip Morris's name attached. As one board member put it: "We're trying to sell wholesome American food with a scarlet letter branded on our forehead."

After testing hundreds of names, they landed on Altria—derived from the Latin "altus" meaning high, suggesting high performance and reaching higher. Critics immediately mocked it as meaningless corporate babble. The advocacy group Campaign for Tobacco-Free Kids called it "putting lipstick on a pig." But Camilleri didn't care about critics. He cared about creating what he privately called "a surgical separation between past and future."

On January 27, 2003, Philip Morris Companies officially became Altria Group. The press conference was surreal—Camilleri standing before a new logo (a colorful square meant to represent innovation) insisting this represented "a new chapter" while everyone knew it was the same cigarettes, same executives, same Richmond headquarters. The stock price didn't budge. Investors weren't fooled by Latin linguistics.

But the name change unlocked the chess moves Camilleri really wanted to make. Within months, Altria announced plans to spin off Kraft. The food giant went public in June 2001 (before the name change), but Altria still owned 84%. Investment bankers from Goldman Sachs and Morgan Stanley suddenly became enthusiastic about underwriting a secondary offering for "Altria's food subsidiary"—something they'd never touch from "Philip Morris's food division."

The Kraft spin-off, completed in March 2007, was financial engineering at its finest. Altria distributed its remaining 88.1% stake to shareholders—a $32 billion value transfer accomplished tax-free. Kraft shareholders received 0.692024 shares for each Altria share owned. Overnight, Altria shareholders became owners of the world's second-largest food company, completely separated from tobacco liability.

The Kraft separation was just the appetizer. The main course was Philip Morris International (PMI)—the crown jewel that sold Marlboro and other brands in 180 countries outside the U.S. International operations generated $45 billion in revenue and faced fewer regulatory threats than the U.S. business. Growth markets in Asia and Eastern Europe were actually expanding smoking populations.

But keeping PMI inside Altria was destroying value. International investors wouldn't buy Altria because of U.S. litigation risk. U.S. litigation plaintiffs saw PMI's deep pockets as a target. The businesses needed different strategies—PMI pursuing growth in emerging markets while Altria managed decline in America.

On March 28, 2008, Altria completed the PMI spin-off, distributing one PMI share for every Altria share owned. The separation created $180 billion in combined market value—PMI worth $110 billion, Altria worth $70 billion. It was the largest spin-off in U.S. corporate history.

The mechanics were elegant, but the human drama was messier. Thousands of employees had to choose—stay with declining but profitable Altria U.S. or join growing but uncertain PMI international. Entire departments were literally split down the middle. The Marlboro brand team was carved up like a divorced couple's assets—U.S. rights to Altria, rest of world to PMI.

In a symbolic gesture that spoke volumes, Altria also moved its headquarters from New York City to Richmond, Virginia in 2008. The Park Avenue address had represented Philip Morris's aspirations to be a sophisticated global conglomerate. Richmond represented acceptance of what Altria really was—a Southern tobacco company. As CFO Dave Beran told investors: "We're not running from our heritage anymore. We're embracing it."

Post-spin-off Altria was a radically simpler company. Revenue dropped from $80 billion to $18 billion. Employee count fell from 175,000 to 10,000. But margins expanded. The stock price, freed from the conglomerate discount, surged 40% within a year. The company that emerged was leaner, meaner, and unapologetic about its mission: extract maximum value from the declining U.S. cigarette market while searching for what comes next.

The transformation complete, new CEO Mike Szymanczyk surveyed his streamlined empire. Altria now consisted of Philip Morris USA (cigarettes), John Middleton (cigars), U.S. Smokeless Tobacco (Copenhagen, Skoal), and a wine business inherited from UST. It was purely focused on U.S. tobacco and alcohol—vice products for American adults.

"We're not trying to be all things to all people anymore," Szymanczyk told analysts in 2009. "We're the best at what we do, and what we do is sell tobacco products to American adults who choose to use them."

That clarity of purpose would soon be tested by the most seductive opportunity—and devastating failure—in Altria's modern history.

V. The JUUL Debacle: A $12.8 Billion Lesson (2018–2023)

The Altria boardroom was electric with possibility on December 19, 2018. CEO Howard Willard had just walked the directors through his masterstroke: Altria would invest $12.8 billion for a 35% stake in JUUL Labs, valuing the e-cigarette startup at $38 billion. Board member Tom Farrell, usually conservative, was effusive: "This could save the company." Another director added: "We're buying the future."

The numbers were intoxicating. JUUL had captured 75% of the U.S. e-cigarette market in just three years. Sales were growing 800% annually. The product had achieved something Altria's own e-cigarette efforts never could—it made vaping cool. At Stanford and Harvard, "JUULing" had become a verb. The sleek USB-stick design and high-nicotine pods had cracked the code that had eluded Big Tobacco for a decade: creating an alternative that smokers actually preferred.

Willard's presentation was compelling. Traditional cigarette volumes were declining 4-5% annually—accelerating from historical 1-2% declines. Altria's own e-cigarette brand, MarkTen, was a disaster, losing $150 million annually with just 2% market share. Meanwhile, JUUL's revenue had exploded from $200 million in 2017 to a projected $2 billion in 2018. Internal Altria surveys showed 30% of Marlboro smokers had tried JUUL—and 40% of those had significantly reduced cigarette consumption.

"Gentlemen," Willard told the board, "we can either watch JUUL cannibalize our business, or we can own a piece of the disruption. This is our Kodak moment—and we're choosing to embrace digital photography."

The deal terms were extraordinary. Beyond the $12.8 billion investment, Altria would provide JUUL with shelf space in 230,000 retail locations, insert JUUL coupons into Marlboro packs, and convert its entire e-cigarette sales force to selling JUUL. In exchange, Altria got 35% ownership, board seats, and a non-compete agreement—JUUL couldn't develop competing products without Altria's permission.

Wall Street was divided. Bulls saw it as brilliant—paying 6.5 times revenue for a company growing 800% annually. Bears called it desperate—massively overpaying for an unproven technology facing regulatory scrutiny. But one detail should have raised red flags: JUUL's founders and employees would receive $2 billion in bonuses from the deal, with the average employee getting a $1.3 million windfall. They were cashing out at the top.

The honeymoon lasted exactly 48 hours. On December 21, Surgeon General Jerome Adams declared youth vaping an epidemic, specifically calling out JUUL. The FDA announced it was considering banning flavored e-cigarettes. Parents groups organized protests at Altria's headquarters. The headlines were brutal: "Big Tobacco Targets Teens Again."

The timing couldn't have been worse. Unknown to Altria's board, FDA Commissioner Scott Gottlieb had been building a case against JUUL for months. Internal FDA documents (later revealed through FOIA requests) showed the agency had evidence of JUUL's youth marketing, including presentations at schools without parental permission and social media campaigns clearly targeting teenagers. A Stanford study found 25% of U.S. high schoolers had used JUUL in the past month.

By February 2019, the situation was spiraling. The FTC filed an administrative complaint alleging the Altria-JUUL deal violated antitrust laws by eliminating competition. The argument was devastating in its simplicity: Altria shut down its competing e-cigarette products as a condition of the JUUL investment, reducing consumer choice and innovation.

Then came the body blows. In September 2019, the Trump administration announced plans to ban flavored e-cigarettes. JUUL preemptively pulled all flavored pods from shelves. Revenue projections collapsed from $3.4 billion to $1.3 billion. International expansion plans evaporated as countries from India to China banned JUUL products.

On October 31, 2019—just 10 months after the investment—Altria took its first write-down: $4.5 billion. CFO Billy Gifford tried to maintain calm on the earnings call: "We remain confident in the long-term value creation opportunity." But privately, executives were panicking. JUUL's valuation had fallen to $24 billion, meaning Altria's stake had lost 35% of its value.

The write-downs became a quarterly ritual of corporate humiliation. January 2020: another $4.1 billion hit as JUUL's valuation fell to $12 billion. March 2021: $2.6 billion more as lawsuits from parents and state attorneys general mounted. By July 2022, Altria valued its JUUL stake at just $450 million—a 96% loss from the original investment.

The human toll was equally devastating. Howard Willard, the architect of the JUUL deal, announced his retirement in April 2020, officially for health reasons but widely seen as accountability for the debacle. JUUL itself imploded—laying off 75% of staff, pulling out of international markets, replacing its entire executive team. The founders who'd collected billion-dollar paydays disappeared from public view.

Internal Altria documents revealed through litigation painted a damning picture of the due diligence process. The board had spent just three weeks evaluating the deal. Key concerns raised by junior analysts—youth usage rates, regulatory risks, patent challenges from Reynolds—were minimized in presentations to senior management. One email from a risk assessment team warned: "JUUL's growth is unsustainable and built on teenage adoption." It was never forwarded to the board.

The final indignity came in March 2023. With JUUL facing bankruptcy and a potential FDA product ban, Altria exchanged its remaining stake for a non-cash consideration: global licensing rights to JUUL's heated tobacco intellectual property. Translation: Altria traded its $12.8 billion investment for some patents of dubious value. The company that was supposed to save Altria had become worthless paper.

In the aftermath, new CEO Billy Gifford was remarkably candid: "We rushed into JUUL because we were afraid of being left behind. We confused momentum with sustainability. We failed our shareholders." The lesson was worth $12.8 billion: in highly regulated industries, the hottest opportunity is often the riskiest bet.

VI. Modern Portfolio & Strategic Pivots (2009–Present)

Billy Gifford's first all-hands meeting as CEO in May 2020 was sobering. Standing before a virtual audience—COVID had emptied Altria's Richmond headquarters—he didn't mince words: "We just incinerated $12.8 billion chasing someone else's innovation. That ends now. We're going back to what we do best: acquiring established assets and optimizing the hell out of them."

The strategy pivot was already underway, actually predating the JUUL disaster. In 2009, Altria had acquired UST Inc. for $11.7 billion—a deal that looked expensive at 4.5 times revenue but proved prescient. UST brought Copenhagen and Skoal, commanding 50% of the U.S. smokeless tobacco market. Unlike JUUL's phantom profits, UST generated $400 million in immediate EBITDA with 45% margins. Within five years, Altria had grown UST's operating income by 40% through price optimization and cost synergies.

The UST deal also brought an unexpected bonus: Ste. Michelle Wine Estates, producer of Chateau Ste. Michelle and 14 Hands wines. Initially seen as a non-core asset to divest, the wine business proved surprisingly synergistic. The same distributors selling cigarettes to convenience stores could place wine. The same age-verification systems worked for both products. By 2020, wine was generating $700 million in revenue with 20% margins.

The 2007 acquisition of John Middleton Co. for $2.9 billion followed a similar playbook—buying the maker of Black & Mild cigars, America's top-selling brand. Middleton dominated the mass-market machine-made cigar segment with 30% share. Altria applied its pricing algorithm, raised prices 6% annually while volumes stayed flat, and doubled operating income within seven years.

But the most intriguing bet came in March 2019—ironically, while JUUL was imploding. Altria invested $1.8 billion for a 45% stake in Cronos Group, a Canadian cannabis company. The thesis was elegant: when federal legalization comes (not if, when), Altria would have first-mover advantage in distribution, regulation navigation, and product development. Cannabis was tobacco's natural successor—a combustible plant product with age restrictions, state-by-state regulation, and social acceptance challenges.

The Cronos investment looked smarter with each passing year. While U.S. legalization remained stalled, Altria quietly developed capabilities: cannabinoid extraction techniques, dosing standardization, brand development. They treated it like a call option on federal legalization worth 2% of market cap—minimal downside, massive upside if cannabis followed alcohol's post-Prohibition trajectory.

The crown jewel of Altria's portfolio remained its 10% stake in Anheuser-Busch InBev, worth $12 billion by 2024. This wasn't an investment Altria made—it inherited the stake when AB InBev acquired SABMiller, which had previously bought Miller Brewing from Altria. The stake threw off $600 million in annual dividends while providing a window into another vice industry's evolution. As one board member noted: "It's like having a Harvard case study that pays us to read it."

The real innovation came in 2023 with the $2.75 billion acquisition of NJOY Holdings, owner of the only e-cigarette products authorized by the FDA. Unlike JUUL's regulatory nightmare, NJOY had methodically pursued FDA approval through the Premarket Tobacco Application process, submitting 14,000 pages of scientific evidence. The FDA authorization was a regulatory moat—competitors would need years and millions to replicate it.

NJOY represented Altria's new philosophy: boring but profitable. No teenage TikTok influencers. No mango flavors. Just FDA-compliant devices sold through age-verified channels to adult smokers. CEO Billy Gifford called it "innovation through regulation"—using the FDA approval process as a competitive advantage rather than fighting it.

The joint venture with Japan Tobacco International for heated tobacco products followed similar logic. Announced in 2023, Altria would distribute JTI's Ploom heated tobacco device in the U.S., leveraging its 230,000 retail points of distribution. Heated tobacco occupied a sweet spot—less harmful than cigarettes (according to FDA statements) but more familiar than e-cigarettes to older smokers. The economics were attractive: similar margins to cigarettes but growing volumes in markets like Japan.

By 2024, Altria's "beyond smoking" portfolio generated $3 billion in revenue—still dwarfed by the $20 billion from traditional cigarettes but growing while cigarettes declined. The company's vision, articulated in every investor presentation, was to "responsibly lead the transition of adult smokers to a smoke-free future."

Critics called this greenwashing—Philip Morris trying to rehabilitate its image while still selling Marlboros. But the numbers suggested genuine transformation. Altria was investing $500 million annually in reduced-risk product R&D. Smoke-free products would represent 50% of revenue by 2035, according to internal projections.

The modern Altria was a contradiction resolved: a company simultaneously harvesting a dying business and planting seeds for what comes next. As Gifford told investors: "We're not running from our past, but we're not imprisoned by it either."

VII. Regulatory Battles & Legal Reckoning

Judge Gladys Kessler's 1,683-page ruling read like a corporate crime novel. It was August 17, 2006, and the federal judge had just found Philip Morris and Altria guilty of violating the Racketeer Influenced and Corrupt Organizations Act—RICO, the law designed to prosecute the Mafia. Her opening line was devastating: "Over the course of more than 50 years, defendants lied, misrepresented, and deceived the American public about the devastating health effects of smoking."

The ruling was the culmination of the largest civil litigation in U.S. history. The Department of Justice had sued in 1999, seeking $280 billion in ill-gotten gains. The trial featured 84 witnesses over nine months. The evidence was damning: internal documents showing Philip Morris knew nicotine was addictive in the 1960s while publicly denying it until 1999. Memos discussing targeting "younger adult smokers" (code for teenagers). Scientists ordered to destroy research showing harmful effects.

Kessler's remedies were almost quaint compared to what the DOJ wanted. No monetary penalties (an appeals court had ruled them out). Instead, Altria had to publish "corrective statements" admitting their deceptions. Remove "light" and "mild" descriptors from cigarettes. Fund a $10 million public education campaign. The stock price actually rose 2% on the news—investors had feared much worse.

But Kessler's ruling was just one battle in a regulatory war that had raged since the 1960s and fundamentally shaped Altria's evolution. The Master Settlement Agreement of 1998 remained the defining moment—46 states settling lawsuits for $206 billion over 25 years, the largest civil settlement in U.S. history. Altria's share: $100 billion, or roughly $4 billion annually indexed to inflation.

The MSA was paradoxically both devastating and protective for Altria. The payments were massive—roughly 50 cents per pack sold. But the agreement also created barriers to entry. New cigarette companies had to either join the settlement (accepting the same payment obligations) or post massive bonds. Marketing restrictions—no billboards, no sports sponsorships, no cartoon characters—actually helped Altria by freezing market share. Marlboro's dominance was essentially locked in.

The Family Smoking Prevention and Tobacco Control Act of 2009 gave the FDA authority to regulate tobacco—something the agency had sought since the 1990s. Altria shocked everyone by supporting the legislation. Internal strategy documents revealed why: FDA regulation would create a "high barrier to entry" for competitors and provide "predictability and clarity" for business planning. Better the devil you know.

FDA regulation proved both burden and opportunity. The Premarket Tobacco Application process required manufacturers to prove new products were "appropriate for public health"—a standard that cost millions to meet. By 2024, Altria had submitted over 3 million pages of scientific documentation for various products. But this also created a moat. Smaller competitors couldn't afford the regulatory burden. Chinese imports were blocked. The vaping free-for-all that enabled JUUL's rise wouldn't happen again.

The corrective statements, finally published in 2018 after 11 years of appeals, were surreal corporate theater. Full-page ads in major newspapers with Altria's logo stating: "Smoking kills, on average, 1,200 Americans. Every day." "Nicotine is addictive." "Cigarettes cause cancer." The ads ran on prime-time television for a year. Altria's brand team called it "the most expensive anti-marketing campaign in history."

State and local regulations created a patchwork of challenges. California banned flavored tobacco in 2022. New York City set minimum prices at $13 per pack. Chicago prohibited sales within 500 feet of schools. Each regulation required Altria to rejigger distribution, pricing, and product mix. The regulatory team grew to 400 employees, larger than many companies' entire workforce.

The litigation never stopped. As of 2024, Altria faced roughly 2,000 product liability lawsuits. Most were individual cases alleging smoking caused specific diseases. The Engle progeny cases in Florida—thousands of individual lawsuits stemming from a class action—resulted in several hundred-million-dollar verdicts. But Altria's legal strategy was attrition: appeal everything, settle nothing publicly, make litigation so expensive that lawyers thought twice.

The regulatory landscape shaped every strategic decision. The JUUL investment failed partly because Altria misread FDA intentions. The NJOY acquisition succeeded because it came with FDA authorization. The move into cannabis was contingent on federal legalization. Even pricing decisions were regulated—the MSA payments meant Altria needed 6-8% annual price increases just to maintain margins.

Yet Altria had also mastered the art of regulatory influence. The company spent $6.6 million on federal lobbying in 2023, employing 80 lobbyists including 50 former government officials. They donated to both parties—$2.3 million in the 2024 cycle split 60/40 Republican/Democrat. The goal wasn't to eliminate regulation but shape it. As one lobbyist explained: "We don't fight regulation anymore. We write it."

The result was a regulatory equilibrium that, perversely, protected Altria's position. High barriers to entry. Predictable restrictions. Manageable litigation costs. The company that had fought regulation for decades had become dependent on it. The cage had become a castle.

VIII. Financial Performance & Market Dynamics

The numbers tell a story of beautiful decline. Altria's 2024 earnings call featured CEO Billy Gifford delivering what had become a familiar refrain: volumes down, prices up, profits growing. Cigarette shipments fell 9.5% in Q4 2024, accelerating from the 4-5% historical decline rate. Yet net revenues grew to $24 billion. Adjusted earnings per share rose 3.4% to $5.12. The stock yielded 7.5%. For a dying business, Altria was remarkably profitable at dying.

The math behind this paradox was elegant. In 2024, Altria sold roughly 85 billion cigarette sticks in the U.S., down from 135 billion a decade ago. But the average price per pack had risen from $6.50 to $11.50. Simple arithmetic: lose 37% of volume, raise prices 77%, grow revenue 11%. The pricing power was extraordinary—name another product where demand is this inelastic.

The secret was Marlboro's dominance and what economists called "consumer capture." Marlboro commanded 42% market share in 2024, up from 38% a decade ago despite being the premium-priced brand. During recessions, smokers traded down from Marlboro to discount brands. During recoveries, they traded back up. But they rarely quit. The average Marlboro smoker had used the brand for 15 years. Switching costs—psychological, not economic—were enormous.

Altria's capital allocation was a masterclass in financial engineering. The company generated roughly $8 billion in operating cash flow annually. Capital expenditures were minimal—$200 million to maintain factories that were largely depreciated. That left $7.8 billion in free cash flow, roughly a 15% yield on the $52 billion market cap.

The dividend policy was almost algorithmic: target 80% payout ratio of adjusted earnings. In 2024, Altria paid $7.2 billion in dividends, a 7.5% yield. The company had raised its dividend for 54 consecutive years, achieving "Dividend King" status. For income investors, Altria was irreplaceable—what other large-cap stock offered a 7.5% yield with 5% annual growth?

Share buybacks consumed another $2-3 billion annually. Since 2010, Altria had repurchased 30% of shares outstanding, each retirement making remaining shares more valuable. The January 2025 announcement of a new $1 billion buyback program was almost ritualistic—the 15th consecutive program. The mechanics of margin expansion were surgical. Altria maintained an adjusted operating companies income margin of 60.3% in 2024—among the highest of any large-cap company. Every 1% price increase on unchanged volume added roughly $200 million to operating income. Cost cuts were continuous: factory automation, SKU rationalization, overhead reduction. The Richmond manufacturing complex that employed 5,000 in 1990 now operated with 800 workers producing similar volumes.

But the industry headwinds were intensifying. U.S. adult smoking rates had fallen from 42% in the 1960s to less than 13% by 2024. The decline was accelerating among younger cohorts—only 5% of adults under 30 smoked regularly. The average smoker was 47 years old and aging. Simple demographics meant the customer base was literally dying off.

Competition dynamics had evolved into a strange equilibrium. Reynolds American (Camel, Newport) maintained 30% market share as the perpetual second player. Imperial Brands (Winston, Kool) held 8%. A long tail of discount brands captured 20%. But nobody seriously challenged Marlboro's premium positioning. The industry had learned from decades of price wars that racing to the bottom destroyed value for everyone.

The illicit market was the wildcard growing more dangerous each year. High taxes—averaging $3.50 per pack between federal and state levies—created arbitrage opportunities. Cigarettes bought in low-tax Virginia for $5 were smuggled to New York and sold for $10. Chinese counterfeit Marlboros flooded urban markets. Native American reservations sold tax-free cigarettes online. The ATF estimated 15% of U.S. cigarette consumption was illicit—untaxed, unregulated, and eating into legal volumes.

Altria's response was predictable: lobby for enforcement, not lower taxes. The company spent millions supporting anti-smuggling task forces and authentication technology. Every pack of Marlboro got digital tax stamps trackable through the supply chain. But enforcement was like squeezing water—pressure in one area just moved the problem elsewhere.

The investment case for Altria had become almost philosophical. Bulls saw a cash machine with years of runway—even declining 5% annually, the business would generate $100 billion in cumulative free cash flow over the next 15 years. At a 7.5% dividend yield, investors were paid handsomely to wait. The company's ventures into cannabis and reduced-risk products provided optionality.

Bears saw terminal decline accelerating. ESG mandates meant institutional investors were forced sellers—Altria was excluded from most sustainability indices. Retail investors were aging alongside the customer base. Who would own the stock in 10 years when smoking rates hit 5%? The end game was visible, just a matter of timing.

CFO Sal Mancuso addressed this directly on the Q4 2024 call: "Our company's leading brands and talented teams enabled our core tobacco businesses to deliver solid income growth and margin expansion while we strategically invested in our future." Translation: we're managing decline profitably while searching for what's next.

The numbers for 2025 guidance told the story: adjusted diluted EPS expected in the range of $5.22 to $5.37, implying 2-5% growth. Not spectacular, but for a company selling a dying product, remarkably resilient. The market valued Altria at 10 times earnings—a distressed multiple for a business generating 15% free cash flow yields.

IX. Playbook: Business & Investing Lessons

The Altria story reads like a masterclass in managing contradictions. How do you optimize a business everyone wants to disappear? How do you innovate when regulation prohibits most innovation? How do you attract talent to an industry considered evil? The playbook Altria developed—through spectacular failures and unlikely successes—offers lessons that extend far beyond tobacco.

Lesson 1: The Art of Profitable Decline

Most businesses facing structural decline follow a predictable death spiral: cut investment, lose market share, slash prices, destroy margins, eventual bankruptcy. Altria inverted this. They raised prices faster than volumes declined. They increased marketing efficiency rather than marketing spend. They consolidated production into fewer, more efficient facilities. The result: a business losing 5% of customers annually but growing profits 3%.

The key insight was that declining markets often become more profitable, not less. Competition exits. Price discipline improves. Customer acquisition costs drop to zero—you're not trying to grow, just retain. The customers who remain are the most loyal, least price-sensitive cohort. Marlboro smokers paying $11 per pack in 2024 would have paid $15. They're not shopping on price; they're buying identity.

Lesson 2: Diversification's False Promise

The Kraft/Miller era taught Altria that unrelated diversification usually destroys value. The stated synergies never materialized. Managing food required completely different capabilities than managing tobacco. The conglomerate structure didn't provide liability protection—plaintiffs just saw deeper pockets. The complexity tax was enormous: multiple reporting segments, competing capital allocation priorities, diluted management focus.

But related diversification—smokeless tobacco, cigars, e-cigarettes, cannabis—made strategic sense. These businesses leveraged Altria's core competencies: navigating vice product regulation, managing age-verified distribution, building adult consumer brands. The lesson: diversify along your capabilities, not away from your controversies.

Lesson 3: Regulatory Capture as Competitive Advantage

Altria's relationship with regulation evolved from opposition to embrace. FDA oversight, once seen as existential threat, became a competitive moat. The PMTA process requiring millions in documentation prevented new entrants. Marketing restrictions froze market share in Altria's favor. Even the Master Settlement Agreement, while costly, essentially cartellized the industry.

The playbook: don't fight regulation, shape it. Hire former regulators. Support "reasonable" restrictions that you can afford but competitors can't. Make compliance a core competency. Turn the regulatory burden into a barrier to entry. It's cynical but effective.

Lesson 4: Capital Allocation in Terminal Decline

Altria's capital allocation was algorithmic: 80% payout ratio, buybacks with excess cash, minimal capex, selective M&A. This wasn't financial engineering—it was acknowledgment of reality. A declining business shouldn't retain capital it can't deploy at high returns. Better to return it to shareholders who can reallocate elsewhere.

The JUUL debacle violated this discipline—paying growth multiples (6.5x revenue) for an unproven business in a declining industry. The lesson was expensive but clear: in declining industries, pay declining industry multiples. Never pay for growth you're structurally unable to achieve.

Lesson 5: Brand Power in Commodity Markets

Cigarettes are functionally identical—tobacco wrapped in paper. Yet Marlboro commands 30% price premiums over identical products. This wasn't just marketing genius; it was decades of consistent positioning. The Marlboro Man never evolved, never repositioned, never chased trends. In a world of constant change, Marlboro's consistency became its strength.

The lesson: in commodity markets, brand is the only moat. But brand requires decades to build and seconds to destroy. Altria never tried to make Marlboro "cool" for millennials or "healthy" with organic tobacco. They kept selling the same aspiration to the same demographic until that demographic aged out.

Lesson 6: The Acquisition Paradox

Altria's acquisition track record was bipolar. Disciplined acquisitions of established businesses (UST, John Middleton) created billions in value. Speculative acquisitions of "the future" (JUUL) destroyed billions. The pattern was clear: Altria succeeded buying mature assets it could optimize, failed buying growth assets it couldn't understand.

The insight: know your circle of competence. Altria understood manufacturing efficiency, distribution optimization, and pricing power. They didn't understand Silicon Valley, teenage social dynamics, or viral marketing. The JUUL deal was Altria trying to buy capabilities rather than develop them—always dangerous, often fatal.

Lesson 7: Managing Stakeholder Hostility

Altria operated in an environment where politicians denounced them, media demonized them, and activists protested them. Yet the company survived and thrived. How? By focusing on stakeholders who mattered: shareholders, employees, retail partners, and yes, adult consumers who chose their products.

They stopped fighting unwinnable PR battles. No more corporate image campaigns. No more defending smoking. Instead, radical transparency: acknowledge the harm, support reasonable regulation, focus on harm reduction. It wasn't redemption, but it was sustainable.

Lesson 8: The Innovation Trap

Traditional companies facing disruption often make the same mistake: overpaying for innovation they don't understand. Altria's MarkTen e-cigarette was a classic example—me-too product, late to market, lacking differentiation. The JUUL acquisition was overcompensation—if we can't build it, buy it at any price.

The better approach, demonstrated by the NJOY acquisition and JTI partnership, was pragmatic: buy proven technology with regulatory approval at reasonable valuations. Innovation in regulated industries isn't about being first; it's about being compliant.

The Meta-Lesson: Some Problems Can't Be Solved

Altria's fundamental challenge—selling a product that kills its customers—has no solution. No amount of diversification, innovation, or financial engineering changes this reality. The company's journey suggests that some business problems must be managed, not solved. The goal isn't transformation but optimization within constraints.

For investors, Altria represents a philosophical question: is it ethical to profit from addiction? The market has answered with a persistent discount—Altria trades at half the multiple of consumer staples peers. This discount is the price of controversy, and it's probably permanent.

Yet Altria's playbook—managing decline, navigating regulation, optimizing capital allocation—offers lessons for any business facing structural challenges. From newspapers to cable TV to internal combustion engines, declining industries are everywhere. Altria's trajectory suggests that decline, properly managed, can be surprisingly profitable.

X. Bull vs. Bear Case & Future Scenarios

The investment debate around Altria has crystallized into two irreconcilable worldviews. Bulls see a cash-generating machine with years of runway. Bears see a melting ice cube accelerating toward zero. Both are right—it's a matter of timeframe.

The Bull Case: Slow Decline, Fast Cash

The optimistic thesis rests on simple math. Even with volumes declining 5-7% annually, pricing power of 6-8% delivers positive revenue growth. Margins remain robust at 60%. The business generates $8 billion in free cash flow on a $52 billion market cap—a 15% yield. Where else can investors find that?

The dividend sustainability is compelling. At $7.2 billion annually, dividends are covered 1.1x by free cash flow. Even if profits decline 20%, the dividend remains safe. The 54-year streak of increases—Dividend King status—suggests management prioritizes shareholder returns above all else. For income investors in a low-yield world, Altria is irreplaceable.

The reduced-risk product transition provides optionality. NJOY's FDA authorization is a regulatory moat competitors will take years to match. The heated tobacco joint venture with JTI leverages proven technology successful in Japan. Cannabis legalization, whenever it comes, transforms Cronos from a $750 million experiment into a multi-billion-dollar opportunity. These aren't pie-in-the-sky ventures—they're calculated bets with asymmetric upside.

Valuation provides a margin of safety. At 10 times earnings, Altria trades at half the market multiple. Any positive surprise—slower volume declines, successful product launches, cannabis legalization—triggers multiple expansion. The stock doesn't need miracles, just stability.

The competitive dynamics favor the incumbent. Marlboro's 42% share continues growing as smaller brands exit. Reynolds seems content as the profitable number two. Private label cigarettes can't compete on brand equity. The illicit market, while growing, remains fragmented and risky for consumers. Altria's position has never been stronger.

The Bear Case: Accelerating Obsolescence

The pessimistic view sees multiple inflection points approaching simultaneously. Volume declines are accelerating—from 4% historically to 7-9% recently. Price increases are hitting elasticity limits. At $12+ per pack, even addicted consumers are quitting or switching to illicit products. The revenue algorithm is breaking.

Demographics are destiny. The average smoker is 47 and aging. Young adult smoking rates have collapsed to 5%. In 10 years, half of today's customers will be dead or quit. There's no replacement generation. The customer base is literally dying.

ESG pressures are intensifying. Major institutions are prohibited from owning tobacco stocks. Sovereign wealth funds divest. Index funds face pressure to exclude Altria. The shareholder base is shrinking to retail investors and specialized value funds. Who owns this stock in 2035?

Regulatory risks remain existential. Menthol bans would eliminate 30% of industry volumes overnight. Nicotine caps would destroy the addictive potential. Plain packaging would commoditize brands. Any of these—increasingly likely under progressive administrations—would devastate the investment thesis.

The innovation efforts are failing. JUUL was a $12.8 billion disaster. MarkTen failed. NJOY has captured just 6% share despite FDA authorization. Heated tobacco remains niche. Cannabis is perpetually "two years from legalization." The transformation beyond smoking isn't happening fast enough.

Litigation never ends. Individual lawsuits generate periodic hundred-million-dollar verdicts. Class actions seek billions. The industry paid $206 billion in the Master Settlement Agreement but that didn't end liability—it established precedent that tobacco companies can and should pay for health consequences.

Scenario Analysis: Three Futures

Scenario 1: Managed Decline (60% probability) Volumes decline 5-6% annually. Prices increase 6-7%. Margins compress gradually. Free cash flow shrinks from $8 billion to $5 billion over five years. The dividend grows low-single-digits then flatlines. The stock delivers 8-10% annual returns from dividends plus modest buybacks. Boring but acceptable for income investors.

Scenario 2: Accelerated Disruption (30% probability) A combination of regulatory shocks—menthol ban, nicotine caps, federal excise tax increases—accelerates volume declines to 10-12% annually. Pricing power evaporates as consumers hit affordability limits. Margins compress from 60% to 45%. The dividend gets cut for the first time in 50 years. The stock falls 40-50% as income investors flee. Value traps don't get more classic than this.

Scenario 3: Successful Transformation (10% probability) Reduced-risk products achieve breakthrough adoption. NJOY captures 20% of the vaping market. Heated tobacco takes 10% share from cigarettes. Cannabis legalization unlocks a $20 billion market where Altria's distribution provides competitive advantage. The company successfully migrates from cigarettes to next-generation products. The stock re-rates from 10x to 15x earnings as ESG concerns moderate. Total returns exceed 20% annually.

The Time Horizon Dilemma

The bull-bear debate ultimately reduces to timeframe. Over the next 2-3 years, Altria probably delivers acceptable returns through dividends and buybacks. Over 10-15 years, the business faces existential challenges that financial engineering can't solve. The question for investors: is the near-term income worth the long-term risk?

Risk-reward depends on individual circumstances. For a retiree needing income, Altria's 7.5% yield with modest growth might be attractive despite long-term challenges. For a young investor with decades ahead, owning a declining industry seems irrational regardless of current yield.

The market's judgment—a persistent 50% discount to consumer staples peers—suggests skepticism about the long term while acknowledging near-term cash generation. This discount is probably permanent. Altria will never trade at Coca-Cola multiples regardless of execution.

XI. Epilogue & Reflections

Standing in Altria's Richmond headquarters, you can almost feel the weight of history. The executive floor displays artifacts from 170 years of tobacco commerce: Philip Morris's original London shop sign, vintage Marlboro advertisements, the contract purchasing Miller Brewing. But the most telling detail is what's not displayed—no cigarettes, no ashtrays, no evidence of the product that built this empire. It's as if Altria is embarrassed by its own success.

This cognitive dissonance defines modern Altria. The company proclaims its vision to "move beyond smoking" while generating 85% of profits from cigarettes. Executives speak of "harm reduction" while selling products that kill 480,000 Americans annually. The headquarters is smoke-free while manufacturing billions of cigarettes. The contradictions aren't bugs; they're features of operating in late-stage capitalism's most conflicted industry.

The Paradox of Profitable Poison

Altria represents capitalism's shadow—the uncomfortable truth that markets don't distinguish between value creation and value destruction. The company has generated over $500 billion in shareholder returns since 1970. It's created thousands of jobs, paid billions in taxes, supported communities. By traditional business metrics, Altria is an American success story.

Yet this success is built on addiction and death. The 7 trillion cigarettes Altria has sold killed approximately 10 million Americans—more than all U.S. wars combined. The $100 billion paid in the Master Settlement Agreement barely covers a fraction of healthcare costs. The human toll is incalculable.

This paradox has no resolution. Markets reward Altria for efficiently delivering nicotine. Society condemns Altria for the consequences. Both responses are rational within their frameworks. The tension reveals something profound about capitalism: it's an amoral optimizer, brilliant at delivering what people want, indifferent to whether wants align with welfare.

The Transformation That Wasn't

Altria's attempted transformation—from cigarettes to food to reduced-risk products—is a case study in organizational inertia. Despite decades of trying, cigarettes remain 85% of profits. Every diversification either failed (JUUL) or was divested (Kraft, Miller). The company that started as a tobacco company remains a tobacco company.

Why? Path dependence is powerful. Altria's capabilities—regulatory navigation, excise tax management, adult-only distribution—are tobacco-specific. Their brand equity is in Marlboro, not innovation. Their culture, despite modernization efforts, was formed by decades of selling cigarettes. Asking Altria to transform beyond tobacco is like asking a fish to climb a tree.

The lesson for corporate transformation: core capabilities are harder to change than strategies. Altria could articulate visions of smoke-free futures, but their organizational DNA was programmed for cigarettes. True transformation requires changing capabilities, not just intentions.

The Future of Vice Industries

Altria's trajectory previews the future of vice industries in developed democracies. Gambling, alcohol, cannabis, and even sugar face similar dynamics: legal but discouraged, profitable but controversial, demanded but demonized. The playbook Altria developed—regulatory compliance, targeted marketing, premium pricing, shareholder focus—will be replicated.

Cannabis is following tobacco's arc in real-time. Initial enthusiasm (medical benefits!) gives way to concern (teenage use!). Regulation tightens. Taxes increase. Marketing restrictions multiply. In 20 years, cannabis companies will face the same challenges as Altria today: managing decline in developed markets while chasing growth in emerging ones.

The investment implications are clear. Vice industries offer high current returns but face terminal decline. They're trades, not investments. Own them for income, not growth. Expect multiple compression, not expansion. And always, always have an exit strategy.

What Altria Tells Us About American Capitalism

The Altria story is quintessentially American—entrepreneurial origins, explosive growth, regulatory battles, financial engineering, and gradual decline. It mirrors America's own trajectory: industrial dominance followed by financialization followed by managed decline.

Like America, Altria succeeded through marketing genius rather than product superiority. Marlboro conquered the world not because it was a better cigarette but because it sold a better story. American soft power worked the same way—selling dreams, not just products.

Like America, Altria's response to decline was financial engineering rather than fundamental reform. Buybacks, dividends, and M&A replaced innovation. Financial returns masked operational deterioration. The core business atrophied while the stock price climbed.

Like America, Altria faces an uncertain future where past advantages become present liabilities. Regulatory capture that once protected now constrains. Brand equity built over decades erodes in years. The playbook that created success prevents transformation.

Final Thoughts: The Banality of Corporate Evil

Hannah Arendt wrote about the "banality of evil"—how ordinary people doing ordinary things can produce extraordinary harm. Altria embodies corporate banality of evil. It's not run by villains but by MBAs optimizing spreadsheets. Employees don't celebrate addiction; they celebrate quarterly earnings. The board doesn't plot teenage nicotine dependence; they approve marketing budgets.

This banality makes Altria more disturbing than cartoonish corporate villainy. It's evil diffused through bureaucracy, diluted across shareholders, disguised as fiduciary duty. No one feels responsible because everyone is just doing their job.

Yet condemning Altria requires confronting uncomfortable questions. If selling cigarettes is evil, what about selling alcohol? Sugar? Firearms? Where's the line? Who draws it? And if we ban everything harmful, what's left of freedom?

Altria exists because 30 million Americans choose to smoke despite knowing the risks. In a free society, that choice, however destructive, must be permitted. Altria is the institutional expression of that freedom—ugly, necessary, profitable.

The company will likely continue its profitable decline for decades. Cigarettes will never disappear entirely—prohibition doesn't work. But smoking will become increasingly marginal, like chewing tobacco or snuff. Altria will extract value until the end, returning cash to shareholders who will redeploy it elsewhere.

Future business historians will study Altria as we study the East India Company or Standard Oil—enterprises that dominated their eras then disappeared. They'll marvel at the cash flows, puzzle over the moral questions, and draw lessons about capitalism's contradictions.

But one lesson will stand above others: in business, as in life, some problems can't be solved, only managed. Altria managed the unsolvable problem of selling death profitably for 170 years. That's not admirable, but it is remarkable. And in the annals of American business, remarkably profitable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube