Indian Energy Exchange (IEX): The Story of India's Power Market Pioneer

I. Introduction & Episode Roadmap

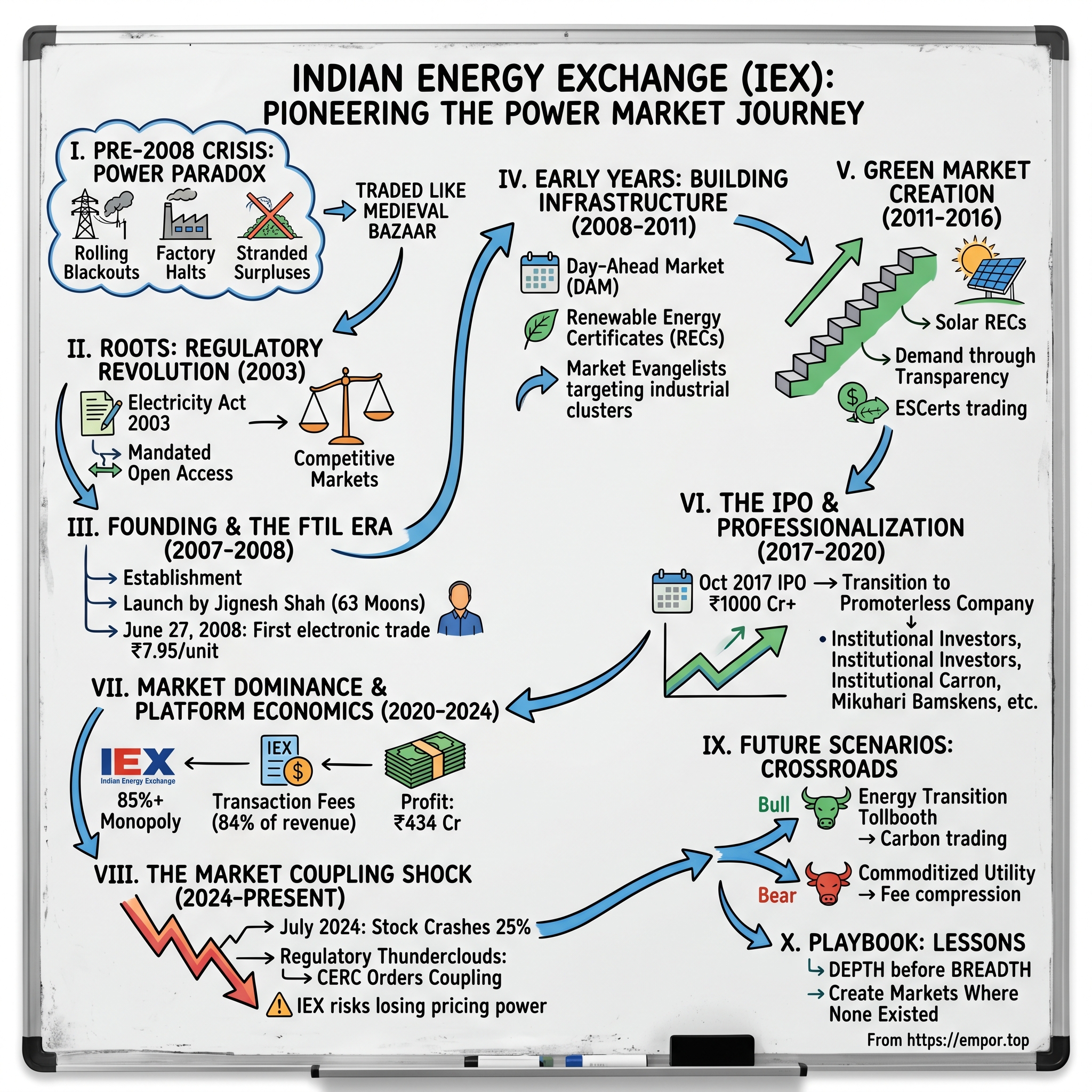

Picture this: It's 3 AM on a sweltering June night in 2008. Across India, millions of air conditioners struggle against rolling blackouts. Factory managers in Gujarat frantically call power traders, desperately seeking electricity to keep production lines running. Meanwhile, a wind farm in Tamil Nadu sits idle, its surplus power trapped behind interstate transmission barriers with no buyers in sight. This was India's power paradox—acute shortages alongside stranded surpluses, a $100 billion sector operating like a medieval bazaar.

At exactly 10:00 AM on June 27, 2008, something revolutionary happened. A bell rang at a small office in New Delhi's Pragati Maidan, and India's first electronic power trade executed on the Indian Energy Exchange. Price: ₹7.95 per unit. Volume: 20 million units. In that moment, electricity—the lifeblood of modern civilization—became a transparently traded commodity in India for the first time.

Today, IEX commands an 85% monopoly over India's power exchange market, facilitating over 100 billion units of electricity trades annually. With 8,100+ participants across every state and union territory, it has become the nerve center of India's power market, setting prices that affect everything from your monthly electricity bill to the viability of billion-dollar power plants. The company sports a market cap of ₹12,312 crore, generates ₹552 crore in revenue with ₹434 crore in profit—all while being virtually debt-free and delivering a stunning 40.5% ROE.

But here's the twist that makes this story fascinating: Just when IEX seemed to have built an unassailable moat, regulatory thunderclouds gathered. In July 2024, the stock crashed 25% in a single day when India's power regulator announced "market coupling"—a mechanism that could obliterate IEX's pricing power and transform it from a monopoly into a commodity processor by 2026.

This raises the central question of our story: Is IEX India's CME—a permanent toll booth on an essential market that will compound wealth for decades? Or is it a regulatory creation that, having solved the problem it was built to solve, now faces its own obsolescence? The answer requires us to journey back to India's post-liberalization power crisis, through controversial beginnings involving financial scandals, into the creation of entirely new markets, and ultimately to a crossroads that will determine whether this exchange remains a crown jewel or becomes a cautionary tale about building monopolies on regulatory quicksand.

II. Origins: Post-Liberalization Power Crisis & The Regulatory Revolution

The lights flickered again in the textile mill. It was 2003 in Coimbatore, and factory owner Krishnamurthy had just lost another batch of fabric to yet another unscheduled power cut—the third that week. His generators kicked in with their familiar diesel roar, but the damage was done. Thread tangled on idle looms, dyes separated in vats, and workers stood helplessly as another day's production turned to waste. Across India, this scene repeated thousands of times daily—a nation's industrial ambitions held hostage by its crumbling power infrastructure.

This was India's electricity paradox at the turn of the millennium. The average manufacturing plant was losing 5-10% of annual revenues to power shortages, while states like Uttar Pradesh experienced chronically high and variable shortages. The crisis would culminate spectacularly in 2012 when India suffered the largest power failure in history—a cascading blackout that plunged 600 million people into darkness.

The roots of this crisis stretched back decades. India's power sector before 2003 resembled a Soviet-style command economy trapped in a democracy. State Electricity Boards (SEBs) controlled generation, transmission, and distribution as vertically integrated monopolies. These behemoths operated with the efficiency of government departments because that's essentially what they were—political instruments for dispensing subsidized power to farmers and vote banks, while industrial consumers paid inflated tariffs to cross-subsidize the losses.

The numbers painted a grim picture. By the early 2000s, India faced power deficits ranging from 7% to 11% on average, with peak shortages touching 15-20% in industrial states. The technical and commercial losses—a euphemism for theft and inefficiency—exceeded 40% in some states. SEBs collectively hemorrhaged over ₹26,000 crore annually, trapped in a death spiral of underpricing, undercollection, and underinvestment.

Then came the Electricity Act of 2003—India's power sector equivalent of the Big Bang. The Indian parliament enacted this landmark legislation following the Electricity Regulatory Commissions Act of 1998 and the Electricity Bill of 2001. For the first time, the Act recognized electricity trading as a distinct licensed activity, separate from generation and distribution. It mandated open access, allowing large consumers to bypass their local distribution companies and buy power directly from any generator. Most crucially, it tasked the newly empowered Central Electricity Regulatory Commission (CERC) with developing competitive markets.

But how do you create a market for electrons—an invisible, instantaneous commodity that can't be stored and must be perfectly balanced every microsecond? Traditional bilateral contracts between generators and distribution companies were opaque, inefficient, and riddled with political interference. Interstate sales faced Byzantine regulations and transmission bottlenecks. Price discovery happened in smoke-filled rooms, if at all.

Enter the concept of a power exchange. In 2005, as India's software engineers were conquering Silicon Valley, a different group of technologists had an audacious idea: What if we could trade electricity like stocks? Financial Technologies India Limited (FTIL), the company that had revolutionized commodity trading with MCX, spotted an opportunity. Along with their application to CERC, they painted a vision of an electronic marketplace where power could be bought and sold transparently, with prices discovered through real-time supply and demand.

The skeptics were legion. "Electricity isn't wheat or cotton," scoffed the traditionalists. "You can't warehouse it. You can't ship it across oceans. The physics alone make it impossible." State utilities worried about losing their monopolistic control. Private traders feared disintermediation. Even reform advocates questioned whether India's creaky grid could handle the technical complexity of real-time power trading.

But FTIL's founder Jignesh Shah, a serial disruptor who had already built MCX into India's largest commodity exchange, wasn't deterred. He understood something fundamental: In a country where information asymmetry was power, transparency was revolution. The same principle that had worked in commodities could work in electricity. All they needed was regulatory blessing and the technology to make it happen.

The technology challenge was formidable. Unlike financial markets where settlement could happen days later, electricity markets required instantaneous physical delivery. Every trade had to factor in transmission constraints, grid stability, and the laws of physics. The exchange needed to coordinate with multiple load dispatch centers, transmission utilities, and system operators in real-time. One software glitch could literally black out cities.

Meanwhile, the human challenge was equally daunting. Convincing hidebound utilities to trade on an electronic platform required changing mindsets forged over decades. The exchange needed to build trust in a sector where contract sanctity was often theoretical and payment delays were measured in years, not days.

As 2007 drew to a close, the stage was set for one of India's most ambitious market experiments. The power deficit was worsening, reaching crisis proportions. Industrial growth was throttled by electricity shortages. The government was desperate for solutions. And in a nondescript office in Mumbai, a team of engineers and traders were putting finishing touches on a platform that would either revolutionize India's power sector or become another footnote in the graveyard of well-intentioned reforms.

The answer would come sooner than anyone expected, and it would change everything about how India's economy accessed its most fundamental input: power itself.

III. The Founding Story: Financial Technologies & The Controversial Birth (2007-2008)

The monsoon of 2007 brought more than rain to Mumbai's financial district. On March 26, in an unremarkable office building in Andheri, paperwork was being filed for what would become India's most important market infrastructure company after the stock exchanges. Nobody present that day—not the lawyers, not the regulators, not even the promoters—fully grasped they were birthing an institution that would fundamentally rewire how a $100 billion industry operated.

The man behind this audacious venture was Jignesh Shah, the enfant terrible of India's exchange ecosystem. Shah, often referred to as the "Exchange King," was a prominent Indian entrepreneur who rose to fame as the founder of Financial Technologies India Ltd (FTIL). His vision for transforming India's financial landscape led him to create several exchanges, including the wildly successful Multi Commodity Exchange (MCX). By 2007, Shah had built FTIL into a financial technology powerhouse, operating nine exchanges across India and internationally. He understood exchanges weren't just trading venues—they were network-effect machines that printed money once liquidity reached critical mass.

On March 26, 2007, IEX was established in Maharashtra. On April 17, 2007, the Company received a certificate of establishment. The co-promoter alongside FTIL was PTC India Financial Services, providing crucial domain expertise in power trading. But this wasn't Shah's first attempt at cracking the power market. The concept of power exchange in India had its genesis in the year of 2005, post which, Financial Technologies Limited and Multi Commodity Exchange together yielded an application for setting up the nation's first power exchange.

What followed was a masterclass in regulatory navigation. While competitors got bogged down in bureaucratic quicksand, Shah's team moved with Silicon Valley velocity. They hired the best power sector experts money could buy, poached talent from European power exchanges, and built technology infrastructure that could handle the unique physics of electricity trading. Unlike commodities that could sit in warehouses, every electron traded had to be delivered instantaneously, with millisecond precision, across a grid that barely functioned on good days.

The technical architecture was revolutionary for India. The exchange had to interface with five regional load dispatch centers, coordinate with dozens of transmission utilities, and ensure that every trade was physically feasible given transmission constraints. One bug in the algorithm could trigger cascading blackouts. The margin for error was zero.

But technology was only half the battle. The human challenge was equally daunting. State Electricity Boards viewed the exchange as an existential threat to their monopolistic fiefdoms. Private generators worried about price transparency destroying their bilateral contract premiums. Industrial consumers, desperate for reliable power, were skeptical that an electronic platform could deliver where decades of government promises had failed.

Shah's solution was quintessentially Indian: overwhelming force combined with strategic compromise. He deployed armies of relationship managers across the country, conducting hundreds of training sessions, literally teaching utility engineers how to use computers for trading. When Tamil Nadu's power utility refused to participate, Shah personally camped in Chennai for weeks, meeting everyone from the Energy Secretary to the Chief Minister's advisors.

The regulatory approval process became a high-stakes chess match. CERC, under pressure from various lobbies, kept moving the goalposts. Requirements changed monthly—new financial guarantees, additional technical specifications, more stringent audit requirements. Each delay cost millions and gave competitors time to catch up. But Shah had one advantage: he knew how to play this game. He'd already shepherded MCX through similar regulatory mazes.

On June 9, 2008, CERC finally granted approval. IEX started its operations on 27 June 2008. The exchange launched with 58 members—a mix of state utilities, private generators, and industrial consumers. The initial daily volume was a modest 20 million units, a rounding error in India's total power consumption. But Shah understood something his critics didn't: in platform businesses, the hardest trades are the first ones. After that, network effects take over.

The launch timing was fortuitous. India's power deficit had reached crisis proportions. Industrial production was suffering. The economy was booming but electricity supply wasn't keeping pace. The exchange offered something revolutionary: transparent price discovery. For the first time, anyone could see the real-time value of electricity across India. No more backroom deals. No more political favoritism. Just supply meeting demand at a market-clearing price.

But even as IEX celebrated its successful launch, storm clouds were gathering around its promoter. Shah's empire—built on financial innovation and regulatory arbitrage—was developing cracks. His other ventures, particularly the National Spot Exchange Limited (NSEL), were engaging in practices that would soon explode into one of India's biggest financial scandals.

The NSEL scam began to unravel in July 2013 when the exchange defaulted on payments totaling ₹5,574 crore. The scam came to light in August 2013, when Jignesh Shah-led group company National Spot Exchange Ltd (NSEL) faced a payment crisis, with nearly 18,000 investors losing millions. The crisis would ultimately lead to Shah's arrest in 2014 and force FTIL (renamed 63 Moons Technologies) to divest its entire stake in IEX.

This forced divestment would prove to be IEX's liberation. Pursuant to divestment by them of the Equity Shares of IEX, they currently hold no Equity Shares in the company. Currently, IEX is a professionally managed company and does not have an identifiable promoter in terms of the SEBI ICDR Regulations. Free from the shadow of its controversial founder, IEX could finally emerge as an institution rather than an entrepreneur's plaything.

The irony was delicious. Shah, who had birthed IEX to disrupt India's power sector, would watch from the sidelines as his creation grew into a monopoly he could no longer control. The exchange he founded as a vehicle for financial engineering had transformed into critical national infrastructure. And unlike NSEL, which collapsed in scandal, IEX would thrive precisely because it had escaped its creator's orbit before the implosion.

As 2008 drew to a close, IEX had processed over 2 billion units of electricity, established price benchmarks across five regions, and proven that transparent markets could function in India's complicated political economy. The foundation was laid. Now came the hard part: building liquidity in a market where trust was scarce, defaults were common, and the product being traded literally couldn't be stored. The next phase would test whether IEX was just another flash-in-the-pan financial innovation or something more fundamental—a new architecture for how India's economy accessed its most critical input.

IV. Early Years: Building the Market Infrastructure (2008-2011)

The first year was brutal. Every morning at 6 AM, Satish Kumar, IEX's first operations head, would arrive at the exchange's modest office in Pragati Maidan to find the same sight: empty order books. The screens that should have been flickering with buy and sell orders displayed mostly zeroes. In 2008, trading in the Day-Ahead Market (DAM) began on its exchange with 58 participants. Around 20 million units volume cleared in DAM daily. Those 20 million units represented less than 1% of India's daily power consumption—a rounding error in a market that desperately needed transparency.

The chicken-and-egg problem was existential. Sellers wouldn't list power without buyers. Buyers wouldn't participate without reliable sellers. And both needed liquidity to get fair prices. Traditional power traders, who made fortunes from information asymmetry, actively discouraged their clients from using the exchange. "Why pay exchange fees when I can get you power directly?" they'd whisper, conveniently omitting their hidden markups that often exceeded 30%.

IEX's solution was guerrilla warfare. They identified the most power-starved industrial clusters—textile mills in Coimbatore, steel plants in Jharkhand, cement factories in Rajasthan—and deployed teams of "market evangelists." These weren't typical salespeople but power engineers who spoke the language of load factors and transmission losses. They'd sit with factory managers, pull out Excel sheets, and demonstrate exactly how much money the exchange could save them.

The breakthrough came from an unexpected source: captive power plants. These private generators, built by industries for self-consumption, often had surplus capacity they couldn't sell due to regulatory restrictions. In 2009, the IEX enrolled first open access customers and established Term-Ahead Market. Open access was the game-changer—it allowed large consumers to bypass their local distribution companies and buy directly from any generator through the exchange.

But implementing open access was like performing surgery with a sledgehammer. Each state had different rules, different charges, different forms. Karnataka demanded bank guarantees. Maharashtra required no-objection certificates from local utilities. Gujarat simply refused to process applications. IEX's legal team filed over 200 regulatory petitions in the first two years, challenging every arbitrary restriction, every illegal fee, every bureaucratic roadblock.

The technology infrastructure evolved rapidly. The initial platform, designed for maybe 100 trades daily, was suddenly handling thousands. In 2010, Trading in the term-ahead market (TAM) and the first industrial consumer was registered on the company's exchange. The average monthly cleared volume on its exchange exceeded 500 million units (MU). That 500 MU milestone—a 25-fold increase from launch—validated the model. But it also exposed weaknesses. The matching algorithm, borrowed from financial markets, didn't account for transmission constraints. Trades would match electronically but fail physically when grid operators couldn't wheel the power.

The solution required rebuilding the entire trading engine. IEX hired a team of PhDs from IIT Delhi to develop algorithms that incorporated real-time grid data. Every trade now checked available transmission capacity, calculated losses, and ensured physical delivery was possible. It was like building a GPS system that not only showed you the route but also guaranteed the road existed.

In November 2009, IEX won Best E-Enabled Customer Platform at the second annual India Power Awards for developing what was described as "a robust platform for energy trading. Awards were nice, but survival required volumes. The exchange burned through cash—technology upgrades, regulatory compliance, market development. The investors were getting nervous. Where was the hockey stick growth that platforms were supposed to deliver?

The answer came from an unlikely product: Renewable Energy Certificates. In 2011, the first non-solar Renewable energy certificates (RECs) were first traded on its exchange. RECs were a regulatory creation—a mechanism to help states meet renewable energy obligations without actually building renewable plants. They could buy certificates from states with surplus renewable generation. It was carbon credits for the power sector.

IEX saw opportunity where others saw complexity. RECs required a completely different settlement mechanism—monthly trading sessions instead of daily, different participant categories, separate clearing processes. The exchange built an entirely new vertical, hiring renewable energy experts, conducting hundreds of training sessions, literally educating the market about a product that didn't exist six months earlier.

The REC market exploded. Within months, IEX was trading millions of certificates, generating fees that finally pushed the exchange toward profitability. More importantly, it proved IEX could innovate beyond simple power trading. The exchange wasn't just a marketplace—it was becoming a laboratory for new financial products in the energy sector.

By 2011's end, daily volumes regularly exceeded 100 million units. By 2010, the average monthly cleared volume on the exchange had crossed 500 million units (MU) of electricity, signifying the growing trust and reliance on IEX as a robust platform for trading power. Industrial consumers who'd initially participated reluctantly were now logging in multiple times daily, optimizing their power portfolios like fund managers managing stocks. State utilities, initially hostile, were quietly using the exchange to manage shortfalls without political embarrassment.

The foundation was set, but IEX was still a startup in a market dominated by giants. The real test would come when the exchange tried to extend beyond spot trading into the complex world of green energy—a market that didn't yet exist but would soon become larger than the power market itself. The next phase would determine whether IEX was just a successful experiment or the future of India's energy economy.

V. The RECs Revolution & Green Market Creation (2011-2016)

The meeting room at CERC's headquarters was tense. It was February 2012, and IEX's management team sat across from skeptical regulators who'd just proposed something radical: solar RECs. The renewable energy certificate market, barely a year old, was already fracturing. Central Electricity Regulatory Commission introduced REC mechanism to ease the purchase of renewable energy by the state utilities and obligated entities. REC framework seeks to create a national level market for renewable generators to recover their cost. But solar developers complained they couldn't compete with cheaper wind projects in the unified REC market. They wanted their own certificates, their own pricing, their own rules.

For IEX, this wasn't just another product launch—it was a test of whether the exchange could evolve from a simple trading platform into a market architect. The challenge was staggering: create a bifurcated market that maintained liquidity in both segments, develop separate clearing mechanisms, and convince market participants to trade in what was essentially a market for regulatory compliance, not economic necessity.

The deeper problem was that the main reason for lower demand is the lack of interest shown by obligated entities in meeting their RPO (Renewable Purchase Obligation). States had renewable energy targets on paper, but enforcement was toothless. Distribution companies, already bleeding money, saw RECs as an unnecessary expense. Why buy certificates when you could simply ignore the regulations and face minimal consequences?

IEX's strategy was counterintuitive: instead of waiting for enforcement, they'd create demand through transparency. The exchange began publishing monthly "shame lists"—states and utilities failing to meet renewable obligations, complete with deficit calculations. They hosted conferences where compliant states could publicly pressure laggards. They turned regulatory compliance into a reputational game.

The technology architecture for RECs required complete reimagination. Unlike electricity, which was delivered instantaneously, One REC (Renewable Energy Certificate) represents 1 MWh of energy generated from renewable sources. These certificates had to be tracked from generation to retirement, potentially over years. IEX built India's first blockchain-inspired ledger system (before blockchain was mainstream), creating an immutable record of every certificate's journey.

But the real innovation came in market design. Bidding timing for REC at Power Exchanges are between 13:00 Hrs to 15:00 Hrs. Matching methodology is based on double-sided closed bidding auction with Price-Prorata base allocation. This concentrated trading window created urgency and liquidity—participants couldn't wait for better prices because trading only happened once a month.

The early results were mixed. In 2012, the first solar REC trade executed at ₹13,400 per certificate—nearly ten times the price of regular RECs. Critics called it a subsidy scam. Supporters argued it was necessary to jumpstart India's solar revolution. The truth, as always, lay somewhere in between.

By 2013, cracks appeared in the REC edifice. As on date there is an inventory of 1.22 crore unsold RECs. In the last fiscal (2014-15), just about 30.6 lakh RECs were traded on the exchange whereas 96 lakh such certificates were available. The market was drowning in supply. Renewable generators who'd built capacity expecting to sell RECs at ₹3,000 were suddenly facing prices below ₹1,000. Many faced bankruptcy.

IEX found itself in an impossible position. As the market operator, they couldn't influence prices. But as the ecosystem's de facto leader, everyone expected them to solve the crisis. The exchange's response was surgical: they lobbied for floor prices to protect generators while advocating for stricter RPO enforcement to boost demand. It was a delicate balance—too much intervention would destroy market credibility, too little would kill the market entirely.

In August 2016, three ISO certifications achieved (quality, information security, environmental management). These certifications weren't just bureaucratic checkboxes—they were trust signals to international investors increasingly interested in India's green energy market. The exchange was positioning itself not just as a trading venue but as the institutional foundation for India's energy transition.

September 2017 marked another milestone: Energy Saving Certificates trading begins. ESCerts represented energy saved, not generated—a conceptual leap that required educating an entirely new participant base. Heavy industries that had never traded anything were suddenly buying and selling certificates representing their efficiency improvements. The exchange had to build specialized desks just to handle queries from cement plants confused about market orders.

The green market evolution revealed a fundamental truth about IEX: its real product wasn't trading technology but market education. The exchange employed more trainers than traders, conducted more workshops than trades. They were teaching India's old economy to speak the language of environmental markets—a cultural transformation disguised as financial innovation.

Throughout this period, IEX's business model evolved subtly but significantly. Risk management through the requisite margin, including any additional margin as specified for the respective trading segment or the type of contract became a crucial revenue stream. The exchange wasn't just facilitating trades—it was becoming a quasi-bank, holding margins, managing credit risk, earning float income.

By 2016's end, the green market had grown from an experiment to IEX's second-largest revenue driver. The exchange was trading millions of RECs monthly, had created entirely new certificate categories, and was consulting with other countries on replicating India's model. What started as regulatory compliance had evolved into genuine market creation.

But success brought scrutiny. Competitors questioned IEX's dominance. Regulators worried about systemic risk. And a new generation of renewable developers, born in the age of grid parity, questioned whether certificates were even necessary anymore. The stage was set for IEX's next transformation: from private pioneer to public institution. The IPO would test whether markets valued innovation or just monopoly.

VI. The IPO & Professionalization Era (2017-2020)

The boardroom at the Taj Mahal Hotel was electric with tension. It was October 8, 2017, the night before IEX's IPO opened, and CEO Rajesh Sinha faced his harshest critics yet: institutional investors who controlled billions. "Your entire business exists at regulatory whim," challenged a fund manager from Singapore. "Tomorrow, CERC could cap your fees and destroy your margins. Why should we pay 44 times earnings for that risk?"

Indian Energy Exchange IPO opens on October 9, 2017, and closes on October 11, 2017. Indian Energy Exchange IPO is a main-board IPO of 60,65,009 equity shares of the face value of ₹10 aggregating up to ₹1,000.73 Crores. The issue is priced at ₹1650 per share. The pricing was aggressive—at the upper end of possibilities, valuing the company at over ₹5,000 crore. For context, this put IEX's market cap dangerously close to established exchanges like BSE and MCX, despite having a fraction of their history.

The IPO structure itself told a story. The IPO will see sale of 6,065,009 equity shares by existing shareholders including Tata Power Company Ltd, Aditya Birla Group's private equity arm, Madison India Capital and Renuka Ramnath-led Multiples Alternate Asset Management Pvt Ltd. Besides, AF Holdings, Kiran Vyapar Ltd, Golden Oak (Mauritius) Ltd and IEX's former chief executive Jayant Deo would offload shares in the public issue. This was purely an offer for sale—not a penny would go to the company. The smart money was cashing out.

But the backstory was even more intriguing. The company was promoted by Financial Technologies (India) Ltd ("FTIL")(now known as 63 Moons Technologies Ltd) and PTC India Financial Services Ltd ("PFS"). Pursuant to divestment by them of the Equity Shares of IEX, they currently hold no Equity Shares in the company. Currently, IEX is a professionally managed company and does not have an identifiable promoter in terms of the SEBI ICDR Regulations and the Companies Act, 2013.

This "promoterless" structure was both IEX's biggest strength and weakness. Without a controlling shareholder, the exchange could claim true independence—critical for regulatory credibility. But it also meant no deep-pocketed sponsor to navigate crises, no visionary founder to drive innovation. The company would sink or swim based purely on professional management and market dynamics.

The roadshow had been grueling. Sinha and his team visited 15 cities across 7 countries in 20 days, presenting to over 200 institutional investors. The pitch was simple but powerful: India's power consumption would double by 2030, renewable energy would explode, and every electron would eventually trade through an exchange. IEX, with its 98% market share, would be the toll booth on India's energy superhighway.

Skeptics raised uncomfortable questions. Competition from Power Exchange India Limited (PXIL) was intensifying. Regulatory changes could destroy margins overnight. The business model—charging tiny fees on massive volumes—had no pricing power. One aggressive hedge fund manager calculated that if trading fees dropped from 2 paise to 1 paise per unit, profits would evaporate entirely.

IEX's response was to emphasize the network effects. With 98% market share, every new participant had to trade on IEX because that's where liquidity existed. The switching costs weren't just technological but behavioral—thousands of traders trained on IEX's platform, familiar with its conventions, trusting its settlement. It was the same moat that protected stock exchanges globally.

The subscription data revealed market sentiment. Indian Energy Exchange IPO subscription was 2.28 X. IPO subscription refers to applications received in an IPO by each quota, i.e., QIB, Retail, and NII. The lukewarm response—barely oversubscribed—reflected institutional wariness. This wasn't a hot tech IPO but infrastructure dressed up as technology.

The shares got listed on BSE, NSE on Oct 23, 2017. The company made its market debut with listing on the bourses at ₹1,500 apiece on October 23, 2017, a discount of over 9% compared to its IPO price of ₹1,650 per share. Indian Energy Exchange IPO listed at a listing price of 1626.45 against the offer price of 1650.00. The listing day disappointment—a 9% discount to IPO price—seemed to validate the skeptics. Retail investors who'd bet on listing gains were underwater immediately.

But beneath the surface, a transformation was underway. The IPO proceeds, though not going to the company, had achieved something crucial: it professionalized IEX's shareholder base. Hence, IEX does not have any identifiable promoter and is owned by 63 investors and power companies - DCB Power Ventures holds 15% stake, 2 funds of Multiples PE hold combined 12.8% while 10% is held by TVS Shriram Fund. The dispersed ownership created genuine independence from any single stakeholder's agenda.

On April 19, 2021, it commenced Cross-border Electricity Trade with Nepal, Bangladesh, and Bhutan to build a regional power market. This international expansion, barely mentioned during the IPO, would prove transformative. IEX wasn't just building an Indian exchange but positioning itself as the hub for South Asian power trading.

March 2018: MOU with Japan Electric Power Exchange for international collaboration marked another milestone. The Japanese, masters of efficient power markets, saw IEX as their gateway to understanding emerging market dynamics. The knowledge transfer was bidirectional—IEX learned sophisticated risk management while JEPX gained insights into managing infrastructure constraints.

The real validation came from operations. Daily volumes crossed 200 million units regularly. New products launched successfully—15-minute contracts for real-time balancing, specialized renewable energy contracts, even exotic weather derivatives. The exchange that started with simple day-ahead contracts now offered over 50 different products.

By 2020, as the pandemic disrupted everything, IEX's importance became undeniable. With factories shutting and reopening unpredictably, the ability to buy power in real-time became critical. The exchange's systems, upgraded continuously since IPO, handled record volumes without a single failure. When the grid itself struggled, IEX's platform remained rock solid.

The IPO, initially seen as expensive, began looking prescient. The stock, after languishing below issue price for months, began a steady climb. By 2020, it had doubled from listing price, vindicating early believers. The company had successfully transitioned from entrepreneurial experiment to institutional infrastructure—a rare feat in Indian markets.

But the biggest test lay ahead. The pandemic had accelerated energy transition globally. Renewable energy was approaching grid parity. Battery storage was becoming viable. Prosumers—consumers who also produced power—were proliferating. The entire architecture of power markets was evolving, and IEX would need to evolve with it or risk obsolescence. The next phase would determine whether the exchange could maintain its monopoly in a rapidly democratizing energy landscape.

VII. Market Dominance & The Platform Economics (2020-2024)

The war room at IEX's Noida headquarters buzzed with controlled chaos. It was March 2021, and CEO Satyanarayan Goel watched as trading volumes hit an all-time high—312 million units in a single day. On the giant screens, real-time maps showed electricity flowing across India like blood through veins, each transaction processed in microseconds, each settlement guaranteed. This was platform economics at its purest: zero marginal cost, infinite scalability, and a monopoly that seemed unassailable.

The company is India's premier electricity exchange with an 85% market share as of 9MFY25, offering a nationwide, automated trading platform for the physical delivery of electricity, renewable power, renewable energy certificates, and energy-saving certificates. But beneath this dominance lay a more complex reality. IEX's market share declined from 92% in FY22 to 85% in FY23. This was due to the entry of new players in the power exchange market. The monopoly was eroding, slowly but perceptibly.

The financial numbers told a story of exceptional unit economics. Market Cap: ₹12,508 Crore, Revenue: ₹552 Cr, Profit: ₹434 Cr. The profit margins were staggering—nearly 80% of revenue flowing straight to the bottom line. Company is almost debt free. Company has a good return on equity (ROE) track record: 3 Years ROE 38.7% Company has been maintaining a healthy dividend payout of 53.4%. This wasn't just a business; it was a money-printing machine.

The revenue model was elegantly simple yet devastatingly effective. Transaction fees comprised 84% of revenue—tiny charges on massive volumes. Annual subscription fees added another 5%. The rest came from ancillary services like data feeds and technology licensing. Every participant paid something, but the amounts were so small relative to the value created that nobody complained. It was the perfect toll booth—unavoidable, affordable, essential.

2020-2022 marked IEX's international expansion phase. On April 19, 2021, it commenced Cross-border Electricity Trade with Nepal, Bangladesh, and Bhutan to build a regional power market. This wasn't just about volumes; it was about becoming the hub for South Asian energy trading. Nepal's hydropower could now flow to Bangladesh's factories through IEX's platform. India wasn't just importing and exporting electricity—it was becoming the market maker for an entire region.

The launch of Indian Gas Exchange (IGX) in 2020 represented another dimension of platform extension. Natural gas, like electricity, suffered from opaque pricing and inefficient distribution. IGX applied the same principles—transparent pricing, guaranteed settlement, anonymous trading—to create India's first gas trading platform. Within two years, it was handling billions of cubic meters monthly.

IGX launched the Gas Index of India (GIXI) in December 2022. This wasn't just a pricing benchmark but a financial instrument that could spawn derivatives, hedging products, and entirely new markets. IEX was evolving from a trading platform to a market infrastructure company, creating the indexes and benchmarks that would define energy pricing for decades.

The technology evolution during this period was remarkable. Real-Time Market, launched in 2020, required trades to be matched and settled every 15 minutes—96 auctions daily, each with millisecond precision. The complexity was mind-boggling: accounting for transmission constraints across five regional grids, calculating losses in real-time, ensuring financial settlement while electricity was still flowing. One software bug could cascade into nationwide blackouts.

It introduced a Mixed-Integer Linear Programming (MILP) based trading algorithm, which makes it easy to introduce complex bids on the Exchange platform to meet the requirements of a changing market scenario. This wasn't just an algorithm upgrade—it was a fundamental reimagining of how electricity markets could work. Participants could now submit complex bids with multiple conditions, time preferences, and location constraints. The system would optimize across thousands of variables to find the perfect market-clearing solution.

The platform's network effects had become self-reinforcing. Its ecosystem comprises over 8,100 stakeholders located across 28 states and 8 union territories. Buyers and Sellers have the option to join as Full Members, Trader Members, or Clients. Every new participant increased liquidity, which attracted more participants, which increased liquidity further. It was the virtuous cycle that every platform business dreams of achieving.

But success brought scrutiny. IEX operates under the regulatory framework of CERC, which sets the rules and tariffs for the power sector. However, CERC's role and authority have been challenged by some state regulators and utilities, who have opposed some of CERC's orders and policies. The very regulator that created IEX could also destroy it with a single order.

Competition was intensifying. Power Exchange India Limited (PXIL) and the new Hindustan Power Exchange (HPX) were chipping away at IEX's monopoly. They offered lower fees, better technology, aggressive customer acquisition. IEX's response was to compete on ecosystem rather than price—offering more products, better analytics, superior liquidity. But the days of automatic 98% market share were over.

The financial performance reflected these challenges. IEX's revenue declined by 5.8% year-on-year in FY 2023 due to lower volumes traded in the day-ahead market (DAM) amid surplus power availability in the country. However, IEX's net profit increased by 3.27% year-on-year in FY 2023 due to higher margins from new products such as RTM, GEM, IGX, LDCs, etc. The company was maintaining profitability through product innovation even as its core market matured.

2023 brought new innovations. IEX launched the Term Ahead Market contracts, which enabled customers to hedge risk against volatility in spot prices. It launched Green Monthly contracts and introduced Green Hydro contracts. It launched Long-Duration Contracts and commenced trade in the High Price Day Ahead Market (HP-DAM). Further, it commenced Tertiary Reserve Ancillary Services (TRAS) Market Segment from the delivery date of 1st June 2023. Each product addressed specific market needs, expanding IEX's relevance beyond simple spot trading.

The International Carbon Exchange, launched as a subsidiary, represented IEX's boldest bet yet. The exchange established a subsidiary, International Carbon Exchange, to facilitate trading in the voluntary carbon market. The goal of this subsidiary is to reduce global greenhouse gas emissions by 45% by 2030 and help achieve the target of limiting global warming to 1.5 degrees. Carbon trading could eventually dwarf electricity trading, and IEX was positioning itself at the center of this emerging market.

By 2024, IEX had evolved far beyond its origins. Net profit of Indian Energy Exchange rose 25.16% to Rs 120.70 crore in the quarter ended June 2025 as against Rs 96.44 crore during the previous quarter ended June 2024. Sales rose 14.72% to Rs 141.75 crore in the quarter ended June 2025. The company was growing again, but the growth was harder-earned, coming from new products and markets rather than monopolistic dominance.

The moat remained formidable: regulatory barriers that took years to navigate, network effects that made switching costly, technological infrastructure that couldn't be easily replicated. But moats, as Warren Buffett often warned, could become prisons if the castle they protected became irrelevant. And in July 2024, IEX would discover exactly how quickly a regulatory moat could become a regulatory noose.

VIII. The Market Coupling Shock & Regulatory Disruption (2024-Present)

The emergency board meeting convened at 9 PM on July 23, 2024. CEO Satyanarayan Goel's face on the video screen showed the strain of the past six hours. The leaked CERC order had already circulated among institutional investors. Tomorrow would be carnage. "Gentlemen," he began, "in twelve hours, we will lose approximately 30% of our market value. The question is not whether we survive the day, but whether we survive the decade."

Market coupling is an economic model used in energy markets to create a single, uniform price for electricity across different trading platforms or exchanges. The concept sounds benign, even progressive. But for IEX, it represented an existential threat to everything the company had built over sixteen years. The implementation of a market coupling model could reduce the IEX's dominance in price discovery and affect its market share, as currently, the Indian Energy Exchange is the country's most prominent platform for electricity spot price discovery.

The market's reaction was swift and brutal. IEX shares plunged 10% to lock at their lower circuit of ₹169.10 on July 24, 2025, following a major regulatory shift by the Central Electricity Regulatory Commission (CERC), which approved the implementation of market coupling for India's power exchanges. Within minutes of opening, over 4 crore sell orders flooded the system. The stock that had touched ₹244 just weeks earlier was in freefall.

On Thursday, July 24, 2025, shares of Indian Energy Exchange Ltd. (IEX) crashed by 28%, reaching a 52-week low of ₹135.30. This sharp decline followed the announcement from the Central Electricity Regulatory Commission (CERC) about the implementation of market coupling in India's electricity sector, starting with the Day-Ahead Market (DAM) in January 2026.

The technical details of market coupling revealed why investors panicked. The Day-Ahead Market (DAM) will transition to a round‑robin market-coupling model by January 2026. The Term-Ahead Market (TAM) and Real-Time Market (RTM) will be integrated later, following pilot studies and consultations. Under the new system, power exchanges will take turns acting as the market coupling operator.

But the real damage wasn't operational—it was strategic. IEX has long enjoyed a monopoly in power trading, with a market share of 84.2% as of FY25.This is because of high liquidity and volume on IEX which .led to efficient price discovery. Most of the volumes on IEX, about 90%, come from the Day-Ahead Market (DAM). The very segment being coupled was IEX's cash cow.

The implications cascaded through every aspect of the business model. IEX will lose control over price discovery. Smaller exchanges like PXIL and HPX will get access to the same pricing. Under market coupling, power exchanges like IEX will no longer independently match bids and set prices. Instead, their role will be reduced to a platform for collecting bids, while pricing and allocation will be centrally managed by the designated MCO.

Analyst reactions ranged from cautious to catastrophic. Bernstein slashed its IEX target to ₹122, citing loss of competitive edge. UBS, however, remains bullish with a ₹285 target, highlighting strong balance sheet and optionality from new segments like long-duration contracts and green energy trading.

The pilot study results, buried in regulatory filings, painted a mixed picture. In case of DAM coupling, the overall welfare increases by ₹38 Cr (0.3%), overall volume cleared increases by 52 MU (0.2%), negligible impact on price due to skewed liquidity and welfare increases in every session in line with the objective of coupling. The benefits were marginal—a 0.3% welfare gain hardly justified destroying a functioning market.

Grid-India's resistance added another layer of complexity. Grid-India, vide its letter dated 13 February 2024, raised some concerns on the strict timelines provided for implementing the shadow pilot of market coupling and also requested for constituting a Committee be constituted for harmonization of bid structure and other related issues. The Commission granted an extension to Grid-India to develop and deploy the necessary software as required for running the shadow pilot.

Management's response was measured but unconvincing. In hastily arranged investor calls, executives emphasized diversification—green markets, carbon trading, long-duration contracts. But everyone knew these were drops in the ocean compared to DAM revenues. The company that had spent years perfecting one product was suddenly scrambling to find alternatives.

The technical indicators screamed oversold. RSI (Relative Strength Index): 14–17 range — extremely oversold. DMI (Directional Movement Index): Strong negative crossover. Pattern Breakdown: Confirmed double-top near ₹185. Support Zones: No confirmed floor until ₹118–₹122 levels.

Some saw opportunity in the chaos. "The stock has been punished for regulatory risk, but the fundamentals and volumes are still robust," says Sameer Shah, energy analyst at ICICIdirect. The contrarians argued that market coupling wouldn't destroy IEX, just transform it. Europe's power exchanges thrived under coupling. Why couldn't India's?

The answer lay in timing and market structure. Europe implemented coupling after markets matured, with multiple strong exchanges. India was coupling a market where one player held 85% share—a recipe for disruption, not evolution. Coupling presents a unique opportunity to form a bigger connected liquid and efficient marketplace to overcome many of the limitations of a fragmented market that currently has only 7% liquidity, multiple segments, a very low price cap, and aggressive bidding by the supply side in the face of unfulfilled demand.

The international precedents offered little comfort. In Europe, dominant exchanges saw market share erosion of 20-30% post-coupling. Transaction fees compressed by 40-50%. Recovery took years, and some never regained their monopolistic margins. IEX faced the same trajectory, compressed into an 18-month implementation window.

By August 2024, the dust had settled somewhat. The stock found a floor around ₹140, down 40% from its peak. Volume hadn't collapsed—traders still needed to trade, and IEX still had the best technology and liquidity. But the valuation multiple had permanently reset. The market no longer priced IEX as a monopoly but as a utility—stable, essential, but unexciting.

The company's response evolved from denial to adaptation. New products launched weekly. International partnerships accelerated. The carbon exchange, previously a side project, became a strategic priority. Management spoke of becoming a "multi-asset energy exchange," though nobody quite knew what that meant.

As 2024 drew to a close, IEX stood at a crossroads. The Ministry of Power (MoP) directed CERC to initiate the market coupling process across multiple electricity exchanges. The regulatory die was cast. January 2026 would bring either renaissance or relegation. The exchange that had created India's power market now had to recreate itself, or risk becoming just another casualty of regulatory progress.

IX. Business Model Deep Dive & Unit Economics

The numbers tell a story that most investors miss. IEX isn't a trading company—it's a toll booth disguised as technology. Market Cap: 12,508 Crore (down -24.5% in 1 year), Revenue: 552 Cr, Profit: 434 Cr. That profit margin—78.6%—is higher than Google's, approaching Visa's territory. This isn't normal. This is what happens when you own the only bridge across a river everyone needs to cross.

The revenue model is deceptively simple. Transaction fees generate 84% of revenue—typically 2 paise per unit traded. On a ₹4 per unit electricity price, that's a 0.5% take rate. Sounds tiny, but when you're processing 100 billion units annually, those paise add up to hundreds of crores. It's the same model that made NYSE and CME into money machines: charge tiny fees on massive volumes with zero marginal cost.

Annual subscription fees contribute another 5%—₹10-50 lakhs depending on participant category. This recurring revenue, though small, is crucial. It creates switching costs. Once a utility invests in training staff, integrating systems, and establishing credit lines, they're locked in. The subscription fee becomes irrelevant compared to the operational disruption of switching.

But here's where it gets interesting: the actual cost of processing a trade is essentially zero. Whether IEX handles 100 trades or 100,000, the technology cost is identical. The servers run anyway. The algorithms execute anyway. Each additional trade is pure profit. This is platform economics at its most extreme.

Company is almost debt free. Company has a good return on equity (ROE) track record: 3 Years ROE 38.7% Company has been maintaining a healthy dividend payout of 53.4%. The capital structure is pristine—no debt because there's nothing to finance. Unlike manufacturing or even software companies, IEX doesn't need working capital. Trades settle in T+1, but IEX never touches the money. It's just a clearinghouse, taking its fee while banks handle the actual cash.

The regulatory moat manifests in the numbers. Starting a competing exchange requires CERC approval—a 2-3 year process minimum. Then you need technology infrastructure (₹50-100 crore), regulatory capital (₹25 crore), and operational capabilities. But even with all that, you're competing against IEX's liquidity. It's like starting a social network to compete with Facebook—technically possible, practically futile.

Working capital dynamics reveal the model's elegance. IEX operates with negative working capital—it collects fees before paying any expenses. Member deposits and margins sit on the balance sheet, generating float income. The company essentially runs on other people's money while earning interest on their deposits. Warren Buffett would approve.

The technology spend is surprisingly modest—₹30-40 crore annually, less than 8% of revenue. This isn't a tech company constantly rebuilding its platform. The core matching engine, once built, requires only incremental updates. The real technology moat isn't sophistication but reliability. IEX's systems have 99.99% uptime—one minute of downtime could cascade into grid instability.

Employee costs tell another story. With just 100-odd employees generating ₹550 crore revenue, revenue per employee exceeds ₹5 crore—higher than most investment banks. These aren't just employees; they're specialists in an arcane field where expertise takes years to develop. The talent moat is real—you can't just hire power trading experts off the street.

The customer concentration risk is both weakness and strength. Top 10 members contribute 40% of volumes, but these are mostly state utilities and large generators who have nowhere else to go. They need IEX more than IEX needs any individual member. It's mutual dependence, but IEX holds the leverage.

Pricing power appears limited—fees are regulated by CERC. But the real pricing power comes from volume growth and product expansion. Each new product—RECs, ESCerts, carbon credits—comes with its own fee structure. IEX doesn't raise prices; it adds toll booths.

The cash generation is relentless. Free cash flow exceeds 90% of net profit. There's no inventory to finance, no receivables to chase (prepaid model), no factories to build. The cash piles up faster than the company can deploy it, hence the massive dividends and buybacks. It's a wonderful problem to have.

But unit economics also reveal vulnerability. If transaction fees dropped from 2 paise to 1 paisa—a regulatory possibility—profits would halve instantly. There's no cost structure to cut, no efficiency to gain. The operating leverage that creates 78% margins also means any revenue decline flows straight to the bottom line.

The green market economics differ substantially. REC trading generates higher fees (₹50-100 per certificate) but lower volumes. The margins are better, but the market is volatile—dependent entirely on regulatory enforcement of renewable obligations. It's a high-margin, high-risk complement to the stable electricity business.

International expansion changes the economics minimally. Cross-border trading with Nepal and Bangladesh adds complexity without commensurate revenue. These markets are tiny—Nepal's entire grid is smaller than Delhi's. It's strategically important for positioning but financially immaterial.

The platform network effects compound over time. Each new participant increases liquidity, which attracts more participants, which increases liquidity further. But these effects have limits. At 85% market share, there are few participants left to capture. Growth must come from market expansion, not share gains.

Competition economics are fascinating. PXIL and HPX lose money trying to compete, subsidizing trades to gain share. IEX could match their prices and still be profitable, but doesn't need to. Liquidity trumps pricing in exchange competition. Traders will pay more for better execution, and better execution comes from deeper liquidity.

The ESG angle adds a new dimension. As India pushes renewable energy, IEX becomes the settlement mechanism for the energy transition. Every solar plant, wind farm, and battery storage system will eventually trade through IEX's platform. The company isn't just riding the energy transition; it's enabling it.

Looking forward, the unit economics face three scenarios. Bull case: Market coupling fails, volumes double by 2030, new products contribute 30% of revenue. Base case: Coupling reduces margins 20%, volume growth offset compression, international expansion contributes 10%. Bear case: Coupling destroys pricing power, competition intensifies, margins compress to 40%.

The numbers suggest IEX is simultaneously the best and worst business in India. Best because the economics are extraordinary—monopolistic margins, negative working capital, infinite scalability. Worst because it all depends on regulatory whim. One CERC order could transform this money machine into a regulated utility. That's the paradox investors must wrestle with—extraordinary economics built on regulatory quicksand.

X. Playbook: Lessons in Market Creation & Platform Building

The IEX story isn't about electricity—it's about the alchemy of turning chaos into order, opacity into transparency, fragmentation into liquidity. The playbook reads like a masterclass in platform economics, but with uniquely Indian characteristics. Here are the lessons that transcend power trading and apply to any attempt at market creation in emerging economies.

Lesson 1: Create Markets Where None Existed—The Infrastructure Approach

IEX didn't just build a trading platform; it built an entire market infrastructure from scratch. Before 2008, India's power "market" was a collection of bilateral deals, political favors, and information asymmetries. There was no price discovery, no transparency, no liquidity. IEX had to simultaneously create supply, demand, and the mechanisms to match them.

The key insight: In emerging markets, you can't assume market infrastructure exists. You have to build the roads before selling the cars. IEX spent its first three years not just facilitating trades but educating participants, lobbying for regulations, building settlement systems, and creating the very concept of transparent power pricing. They weren't a platform company; they were market missionaries.

Lesson 2: Regulatory Capture vs. Regulatory Alignment

The conventional Silicon Valley wisdom says "move fast and break things." In regulated markets, that's a recipe for destruction. IEX succeeded not by disrupting regulations but by aligning perfectly with regulatory intent. CERC wanted transparent markets; IEX delivered transparency. The government wanted renewable energy integration; IEX created REC markets.

But there's a fine line between alignment and capture. IEX never captured the regulator—that would have created backlash. Instead, they became indispensable to regulatory objectives. Every government goal—rural electrification, renewable targets, regional integration—ran through IEX's platform. They made themselves too useful to disrupt.

Lesson 3: Building Trust in Low-Trust Environments

India's power sector was a cesspool of defaults, political interference, and broken promises. State utilities routinely didn't pay generators. Generators routinely didn't deliver promised power. In this environment, asking participants to trade anonymously on an electronic platform required enormous trust.

IEX built trust through technology and process, not relationships. Prepaid margins eliminated counterparty risk. T+1 settlement removed payment uncertainty. ISO certifications provided third-party validation. The platform became more trustworthy than bilateral relationships because it removed human discretion from the equation. In low-trust markets, automate trust.

Lesson 4: Network Effects in B2B Marketplaces

Consumer platforms get network effects from millions of users. B2B platforms must create network effects with hundreds. IEX achieved this through forced scarcity and clustering. By limiting membership initially, they created exclusivity. By focusing on specific regions and products, they achieved critical mass quickly.

The playbook: Don't try to be everything to everyone immediately. Create dense networks in narrow verticals, then expand. IEX started with day-ahead power in five states. Only after achieving liquidity there did they add products and geographies. Depth before breadth—always.

Lesson 5: The Danger of Regulatory Dependency

IEX's greatest strength became its greatest weakness. Complete dependence on regulatory frameworks meant a single order could destroy the business model. The market coupling announcement proved this vulnerability. Companies building in regulated markets must constantly diversify their regulatory exposure.

The solution isn't avoiding regulation but creating multiple regulatory dependencies. IEX's expansion into gas, carbon, and international markets wasn't just growth—it was regulatory hedging. Each new market meant new regulators, new rules, new protection against any single regulatory change.

Lesson 6: Why Timing Matters—India's Power Deficit to Surplus Journey

IEX launched at the perfect moment—when India's power deficit was acute but infrastructure was improving. Too early, and the grid couldn't handle electronic trading. Too late, and bilateral relationships would have ossified. The window for market creation is narrow and unforgiving.

The pattern repeats across markets: ride the transition, not the steady state. India's transition from power deficit to surplus, from coal to renewable, from regulated to market—each transition created opportunity. Platforms succeed not by serving stable markets but by facilitating transitions.

Lesson 7: Platform vs. Exchange—What's the Real Business?

IEX calls itself an exchange, but it's really three businesses. First, a trading platform charging transaction fees. Second, a data business selling market intelligence. Third, a trust business guaranteeing settlement. The trading generates volume, data generates margins, trust generates moat.

Most platforms make this mistake—defining themselves by their most visible function rather than their most valuable one. IEX's real product isn't electricity trading; it's trust in an untrustworthy market. Everything else—the technology, regulations, network effects—just enables that core value proposition.

The Meta-Lesson: Market Creation as Nation Building

IEX's story transcends business—it's about institution building in emerging markets. The exchange didn't just facilitate trades; it changed how India's economy accessed its most fundamental input. Every factory that didn't shut down due to power shortage, every renewable plant that found buyers for its electricity, every fair price discovered—these ripple effects matter more than profits.

The playbook for market creators in emerging economies: Don't just build platforms; build institutions. Don't just facilitate transactions; create trust. Don't just serve markets; create them. And always remember—in emerging markets, the absence of infrastructure isn't a bug; it's the biggest feature.

The Unwritten Rules

Beyond the formal playbook lie unwritten rules that determined IEX's trajectory:

- Political Economy Matters More Than Economics: Understanding who benefits and who loses from transparency matters more than efficiency gains

- Technology Is Necessary But Not Sufficient: The matching algorithm was simple; the stakeholder management was complex

- Monopolies Are Temporary: Every moat eventually becomes a bridge for competitors

- Regulation Giveth and Regulation Taketh Away: Live by regulatory fiat, die by regulatory fiat

- The Real Competition Isn't Other Exchanges: It's the old way of doing things

Looking forward, the IEX playbook will be tested by new market creators—in agriculture, healthcare, logistics. Each will face the same challenges: creating liquidity from nothing, building trust where none exists, navigating regulatory mazes. Those who succeed will follow IEX's path—not by copying its model but by understanding its principles.

XI. Bear vs. Bull Case & Future Scenarios

The investment case for IEX splits violently between believers and skeptics, between those who see an indispensable institution and those who see a regulatory accident waiting to happen. Both sides have compelling arguments, backed by data, precedent, and logic. The truth, as always, likely lies in the messiness between extremes.

Bull Case: The Energy Transition Tollbooth

The bulls begin with arithmetic. India's power consumption, currently at 1,400 TWh annually, must double by 2030 to support GDP growth targets. Every electron of that growth will need price discovery. Even if IEX's market share halves, volumes would still double. The math is inescapable—India needs more power, and power needs markets.

The renewable revolution multiplies this opportunity. India targets 500 GW of renewable capacity by 2030, up from 150 GW today. But renewables are intermittent—solar doesn't work at night, wind doesn't blow on demand. This intermittency creates volatility, and volatility creates trading opportunities. The more renewable the grid becomes, the more valuable real-time markets become. IEX isn't threatened by the energy transition; it's the primary beneficiary.

Green markets offer exponential growth potential. Carbon trading, still nascent, could become larger than power trading within a decade. Global carbon markets already exceed $1 trillion annually. India's carbon pricing mechanism, once implemented, will need an exchange. IEX has the infrastructure, relationships, and regulatory approvals to dominate this market from day one.

Regional integration presents another mega-opportunity. South Asia's combined power market exceeds $200 billion. Nepal's hydropower, Bangladesh's gas, Bhutan's renewables, Sri Lanka's solar—all need markets to find optimal prices. IEX has already started cross-border trading. As regional grids integrate, IEX becomes the natural hub for South Asian energy trading. Think of it as the Singapore Exchange for South Asian power.

New products keep expanding the addressable market. Derivatives on power prices, weather hedging instruments, battery storage certificates, green hydrogen trading—each product adds revenue streams with minimal marginal cost. The platform economics mean 80% margins on every new product. IEX doesn't need to dominate each market, just participate.

The technology moat deepens daily. While competitors struggle with basic matching, IEX is implementing machine learning for price prediction, blockchain for settlement, and quantum computing for optimization. The R&D gap widens because IEX can invest 10% of revenue in technology while competitors lose money on operations.

Structural advantages remain intact even post-coupling. Market coupling only affects price discovery, not settlement, clearing, or technology. IEX still owns the best infrastructure, deepest relationships, and most trusted brand. Customers won't switch platforms just because prices are uniform—execution, reliability, and service still matter.

Financial flexibility enables aggressive growth. With ₹1,000 crore cash, zero debt, and ₹400 crore annual free cash flow, IEX can acquire competitors, invest in new markets, or return capital to shareholders. The balance sheet provides optionality that stressed competitors lack.

Bear Case: The Regulatory Guillotine

The bears counter with history. Every exchange monopoly eventually gets disrupted by regulation. NYSE dominated U.S. equities until decimalization and Reg NMS destroyed its model. European power exchanges saw margins compress 50% post-coupling. London Stock Exchange lost its monopoly to alternative venues. Regulatory intervention is not a risk—it's a certainty.

Market coupling fundamentally breaks IEX's business model. When price discovery becomes centralized, exchanges become commoditized. Why trade on IEX at higher fees when PXIL offers the same price at lower cost? The race to the bottom in fees is inevitable. European exchanges saw transaction fees drop 60% within three years of coupling.

Competition from unexpected sources looms. PXIL and HPX are obvious threats, but the real danger comes from adjacent players. Stock exchanges like NSE have technology, capital, and regulatory relationships. Large utilities might create captive exchanges. International players like ICE or CME might enter India. The competitive landscape will transform from monopoly to melee.

Technology disruption could eliminate exchanges entirely. Blockchain enables peer-to-peer energy trading without intermediaries. Prosumers with solar panels and batteries can trade directly with neighbors. Smart contracts can handle settlement automatically. The entire exchange model—centralized matching and clearing—might become obsolete within a decade.

Regulatory overhang creates permanent uncertainty. Even if market coupling is delayed, the threat remains. Every CERC meeting, every Ministry of Power announcement, every regulatory consultation creates volatility. Institutional investors hate regulatory uncertainty more than actual regulation. The multiple will remain depressed regardless of fundamental performance.

Market saturation limits growth potential. At 85% market share, where does growth come from? The power market grows at GDP rates—5-7% annually. New products like carbon credits are years from meaningful revenue. International expansion faces local competition and regulatory barriers. The growth story is largely played out.

ESG backlash could impact volumes. As renewable energy reaches grid parity, the need for RECs diminishes. Why buy certificates when renewable power is cheaper than coal? The entire certificate market—currently 15% of revenue—could evaporate as renewables become economically superior, not just environmentally preferable.

Concentration risk amplifies any disruption. IEX depends entirely on Indian power markets. One bad monsoon affecting hydropower, one gas shortage affecting generation, one grid failure affecting confidence—any disruption cascades through the business. Geographic and product concentration creates fragility.

Scenario Analysis: Three Futures

Scenario 1: The Monopoly Persists (30% probability) Market coupling gets delayed indefinitely due to technical challenges. IEX maintains 70%+ market share through superior execution. New products contribute 40% of revenue by 2030. Stock trades at 50x earnings, market cap exceeds ₹50,000 crore. This requires everything going right—regulatory forbearance, competitor incompetence, flawless execution.

Scenario 2: Managed Decline (50% probability) Market coupling launches in 2026 but takes years to fully implement. IEX market share gradually erodes to 50% by 2030. Margins compress from 78% to 60%. Growth comes from market expansion and new products offsetting share loss. Stock trades at 25x earnings, market cap stabilizes around ₹15,000 crore. This is the muddle-through scenario—neither triumph nor disaster.

Scenario 3: Disruption and Transformation (20% probability) Market coupling succeeds immediately, competition intensifies, blockchain disrupts the model. IEX market share collapses to 30%, margins compress to 40%. Company pivots to technology licensing and international markets. Stock trades at 15x earnings, market cap drops to ₹8,000 crore. This requires multiple negative events—aggressive regulation, successful competition, technology disruption.

The Investment Decision

The bull-bear debate ultimately reduces to a single question: Is IEX a monopoly or a utility? Monopolies deserve premium valuations because they control pricing. Utilities deserve modest valuations because they're regulated returns on capital. IEX is transitioning from monopoly to utility, but the speed and extent of that transition remains uncertain.

For growth investors, IEX is probably dead money. The explosive growth phase is over. Regulatory overhang caps multiple expansion. Better opportunities exist in pure-play renewable energy or technology companies.

For value investors, IEX might be interesting below ₹120. At that price, you're paying 20x depressed earnings for a business with structural advantages, even in the worst case. The dividend yield provides income while waiting for clarity.

For strategic investors, IEX is a call option on India's energy transition. If carbon markets explode, if regional integration accelerates, if new products succeed—the upside is multiples of current valuation. But it's a long-term, high-risk bet on regulatory and market evolution.

The meta-lesson: IEX exemplifies the opportunities and challenges of investing in regulated markets. The returns can be extraordinary when regulation creates monopolies. The losses can be devastating when regulation destroys them. Understanding regulatory dynamics matters more than understanding business fundamentals. In IEX's case, the next CERC order matters more than the next earnings report.

XII. Epilogue & Reflection

Standing at the crossroads of 2025, IEX presents a paradox that transcends simple categorization. Is it India's CME—a permanent fixture in the financial architecture that will compound wealth for generations? Or is it something more troubling, a castle built on regulatory sand, one government order away from irrelevance? The answer might be that it's both, neither, and something entirely different—a new species of business that emerging markets are creating as they leapfrog developed market evolution.

The comparison to CME is seductive but ultimately misleading. CME emerged in mature markets with established legal frameworks, property rights, and centuries of trading tradition. IEX created its market from nothing, in a country where electricity was politics, not commodity. CME serves sophisticated financial players hedging complex risks. IEX serves a nation trying to keep the lights on. The contexts are so different that comparison becomes meaningless.

The Enron parallel—minus the fraud—is more intriguing. Enron pioneered energy trading, created markets, innovated products, then imploded when ambition exceeded reality. IEX shares Enron's market-making DNA but not its hubris. Where Enron leveraged aggressively, IEX remains debt-free. Where Enron obscured reality, IEX provides transparency. Yet both companies faced the same fundamental question: What happens when you succeed too well at solving the problem you were created to solve?

The Paradox of Essential Infrastructure as a Listed Company

Here lies IEX's deepest contradiction. It's simultaneously critical infrastructure and a profit-maximizing corporation. Every basis point of margin IEX earns is a cost to India's economy. Every monopolistic advantage IEX maintains is an inefficiency in power markets. The very success that rewards shareholders imposes costs on society.

This tension is irreconcilable. Listed companies must maximize shareholder value. Critical infrastructure must maximize social welfare. IEX must do both, creating a schizophrenia that manifests in every strategic decision. Should they lower fees to increase volumes and help the economy? Or maintain fees to preserve margins and reward investors? There's no right answer, only trade-offs.

The market coupling decision crystallizes this paradox. From a social perspective, coupling creates efficiency, transparency, and fair pricing—unquestionable goods. From a shareholder perspective, coupling destroys competitive advantage, reduces margins, and increases risk—unquestionable bads. CERC chose social welfare over shareholder value, as regulators should. But it highlights the fundamental instability of IEX's position.

What Happens When You Solve the Problem You Were Created to Solve?

IEX was created to solve India's power market dysfunction—opacity, inefficiency, shortages. By most measures, it succeeded brilliantly. Price discovery is transparent. Markets are liquid. Shortages have become surpluses. The patient is cured. So what happens to the doctor?

This is the innovator's curse in regulated markets. Success eliminates the need for your existence. IEX's monopoly was tolerated because markets needed creation. Now that markets exist, why tolerate monopoly? The very efficiency IEX created enables competition that threatens its existence.

The parallel extends beyond IEX. Uber solved urban transportation, then faced regulatory backlash. Facebook connected the world, then faced content moderation demands. Amazon revolutionized commerce, then faced antitrust scrutiny. Success at scale attracts scrutiny that threatens the scale that enabled success. It's a recursive loop that traps successful platforms.

Lessons for Founders Building in Regulated Markets

For entrepreneurs watching IEX's journey, several lessons emerge:

First, regulatory alignment is everything, until it isn't. IEX perfectly aligned with CERC's objectives for fifteen years. That alignment created the monopoly. But regulations evolve, objectives change, and yesterday's alignment becomes today's obstacle. Build regulatory flexibility into your model from day one.

Second, monopolies in regulated markets are borrowed, not owned. The government giveth, and the government taketh away. Price accordingly. Value accordingly. And always have a plan for when monopoly ends.

Third, solve real problems, not regulatory arbitrage. IEX succeeded because it genuinely improved power markets, not because it exploited regulatory loopholes. When regulations changed, the fundamental value proposition remained. Build substance, not scaffolding.

Fourth, diversification is survival. IEX's expansion into gas, carbon, and international markets wasn't growth strategy—it was existential hedging. In regulated markets, single points of failure are death sentences.

Fifth, technology moats are temporary, regulatory moats are illusory, but trust moats can be permanent. IEX's real asset isn't its matching algorithm or CERC approval—it's the trust of 8,000 participants who rely on it daily. Trust compounds. Protect it above profits.

The Future of Energy Markets in a Renewable, Distributed World