Sysco Corporation: The Hidden Giant Behind Every Restaurant Meal

I. Opening & The "Oh Wow" Moment

Picture this: You're sitting in your favorite restaurant—maybe it's a cozy neighborhood bistro, a bustling Chipotle, or the cafeteria at Google's headquarters. The waiter brings your perfectly seared salmon, the tortilla arrives warm and pliable, the tech workers grab their organic quinoa bowls. Behind every single one of these meals, there's a 76-billion-dollar company you've probably never thought about. Not the restaurant chain, not the food manufacturer, but the invisible middleman that makes modern dining possible: Sysco Corporation.

Here's the staggering reality—Sysco touches nearly every commercial kitchen in America. With $76 billion in annual revenue, 76,000 employees, and a fleet of 14,000 delivery trucks, they're larger than McDonald's, Starbucks, and Chipotle combined. Yet unless you work in foodservice, you've likely never encountered their brand. They don't advertise during the Super Bowl. They don't have storefronts. They exist in the shadows of loading docks at 4 AM, in the walk-in freezers of restaurants, in the complex logistics that ensure your local diner never runs out of eggs.

The story of how a Houston startup named after "systems and services" became the invisible backbone of American dining is one of the great untold business epics. It's a tale of consolidating a hopelessly fragmented industry, building unassailable scale advantages, and creating a distribution network so essential that even Amazon has struggled to compete. It's about turning the unglamorous business of moving frozen chicken and toilet paper into a fortress of competitive advantages.

Why does this story matter now? Because Sysco represents something profound about American capitalism—how operational excellence, not innovation or disruption, can build an empire. In an era obsessed with software eating the world, Sysco proves that sometimes the most valuable companies are those that perfect the mundane, that win through execution rather than invention. They've survived recessions, pandemics, and multiple attempts at disruption by simply being irreplaceable.

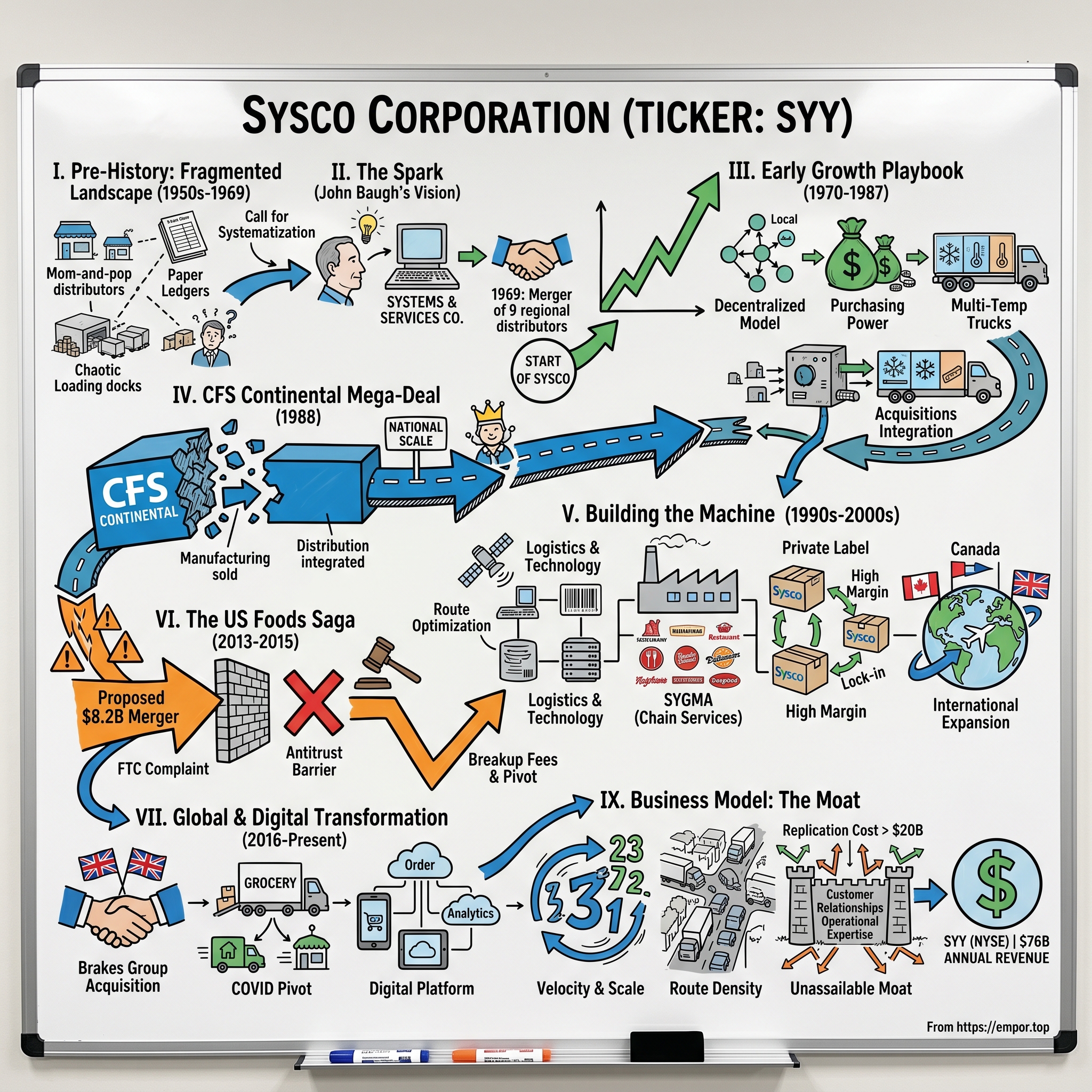

II. Pre-History: The Fragmented Food Distribution Landscape (1950s-1969)

The year is 1958, and John Baugh is standing in the warehouse of his Houston food distribution company, Zero Foods, watching chaos unfold. Orders scribbled on paper, trucks leaving half-empty, customers calling to complain about missing items. He'd left his comfortable job as a store manager at A&P—then America's grocery giant—to build something in the wild west of food distribution. What he saw wasn't just operational inefficiency; it was an entire industry crying out for systematization.

Post-World War II America was experiencing a dining revolution. Suburban expansion meant more restaurants. Women entering the workforce meant less home cooking. Fast food chains like McDonald's were standardizing the American palate. Restaurant sales exploded from $20 billion in 1950 to $43 billion by 1969. Yet the infrastructure feeding these restaurants was prehistoric—thousands of mom-and-pop distributors, each serving maybe 50-100 local establishments, operating with paper ledgers and handshake deals.

The typical 1960s food distributor was a family business started by someone who knew restaurants, not logistics. They'd buy from manufacturers, store products in a small warehouse, and deliver to local customers using a couple of trucks. Margins were thin—2-3%—and bankruptcy common. National manufacturers like Kraft and General Mills hated dealing with thousands of small distributors. Restaurant chains expanding beyond single markets faced a logistical nightmare of managing dozens of supplier relationships.

Baugh's epiphany came from an unlikely source: the nascent computer industry. IBM was evangelizing "systems thinking"—the idea that business processes could be standardized, measured, and optimized. What if food distribution wasn't just about moving boxes, but about creating a system? He started calling his vision the "Systems and Services Company"—later shortened to Sysco. The name itself was a manifesto: this wouldn't be "Joe's Food Distribution" but something bigger, more ambitious.

By 1968, Baugh had found eight other regional distributors who shared his vision. There was Herbert Irving running Global Frozen Foods in Houston, already doing $15 million in sales. The Crump family had built Thomas Foods in Cincinnati. Louisville Grocery Company dominated Kentucky. Each was successful regionally but understood the limitations of local scale. Together, they controlled about $115 million in combined revenue—significant, but still less than 1% of the food distribution market.

The merger negotiations took place in Houston's Warwick Hotel, with lawyers, accountants, and nine entrepreneurial families trying to create something unprecedented. The debates were fierce: Who would run the combined company? How much autonomy would each operation retain? Would brands be consolidated or kept separate? The breakthrough came when they agreed on a federated model—each company would maintain its local identity and relationships while gaining the purchasing power and best practices of the collective.

The genius wasn't just in combining nine companies; it was in the selection criteria. Each founding company dominated its local market, had modern facilities (by 1960s standards), and most importantly, had owners willing to stay and run their divisions. This wasn't a roll-up where founders cashed out—it was a confederation where entrepreneurs became owner-operators of something larger than themselves.

On December 30, 1969, the deal closed. Nine independent food distributors became Sysco Corporation, instantly creating the nation's largest foodservice distributor. The combined entity had 1,500 employees, operated from 16 locations, and served roughly 20,000 customers. Small by today's standards, but in the fragmented world of food distribution, it was revolutionary. As Baugh told the Houston Chronicle: "We're not just creating a company; we're creating an industry." The consolidation of American food distribution had begun.

III. Going Public & Early Growth Playbook (1970-1987)

March 3, 1970—barely two months after the merger closed—Sysco went public on the New York Stock Exchange, raising $6.5 million at $23 per share. The timing seemed insane. The stock market was in free fall, the economy teetering toward recession. But John Baugh understood something Wall Street didn't: food distribution was recession-resistant. People might stop buying cars, but they never stop eating. The IPO proceeds immediately went toward the company's first major acquisition—Arrow Foods, adding another $12 million in revenue. The growth machine was already humming.

The real innovation wasn't acquisition—it was Sysco's radically decentralized operating model. While competitors tried to impose top-down standardization, Sysco let each acquired company keep its local brand, management team, and customer relationships. The Houston headquarters, nicknamed "the corporate umbrella," focused only on three things: negotiating national purchasing agreements, sharing best practices, and allocating capital. Everything else—pricing, product selection, delivery routes—stayed local.

This philosophy crystallized in what insiders called "the Sysco Way." When they acquired Frost-Pack Distributing in 1971, they didn't send in corporate executioners. Instead, Frost-Pack's founder stayed as president, kept his sales team, and maintained relationships he'd built over decades. The only changes? Access to Sysco's purchasing power (cutting product costs by 3-5%), shared warehouse management systems, and capital for expansion. Within two years, Frost-Pack's revenues doubled.

Building the physical infrastructure required massive capital deployment. By 1975, Sysco operated 23 distribution centers covering 3.8 million square feet of warehouse space. Each facility represented a $5-10 million investment in refrigeration systems, loading docks, and automated inventory management—cutting-edge technology that smaller competitors couldn't afford. The truck fleet grew to 800 vehicles, each custom-designed with multi-temperature zones: frozen at -10°F, refrigerated at 35°F, and dry storage at room temperature.

Then came the 1976 disaster that nearly derailed everything. Sysco had aggressively expanded into canned goods, betting that inflation would drive prices higher. Instead, commodity prices crashed, leaving them with millions in overvalued inventory. The company posted its first quarterly loss. Stock price plummeted 40%. Business media declared the roll-up strategy dead. Inside headquarters, there was talk of breaking the company apart.

John Baugh's response revealed the leadership that would define Sysco's culture. Rather than panic cost-cutting, he doubled down on the core strategy. "We're not in the commodity speculation business," he told analysts. "We're in the service business." Sysco divested non-core manufacturing operations, implemented strict inventory controls, and refocused entirely on distribution. By 1977, profitability was restored. The lesson was seared into corporate DNA: stick to what you know.

The geographic expansion strategy that followed was methodical, almost military in precision. Sysco divided the U.S. into zones, identifying the largest independent distributor in each market. They'd approach with a standard offer: retain your management, keep your customers, gain our scale. Between 1977 and 1987, Sysco completed 25 acquisitions, adding names like Mid-Central Fish & Frozen Foods (Nebraska), Hardin's Food Systems (Missouri), and Pegler-Schwarz (Cleveland).

Each acquisition followed the same integration playbook. Week one: Sysco's IT team would arrive to install standardized inventory management systems. Month one: purchasing agreements renegotiated to Sysco's national contracts. Month three: best practices shared from other operations—optimal truck routing, warehouse layouts, customer credit management. Month six: full integration complete, but local brand and relationships intact. This systematic approach achieved a 90% success rate in acquisitions, extraordinary in an industry littered with integration failures.

By 1980, the numbers told the story: revenue hit $1.2 billion, up from $115 million at founding. Market share reached 3%—still small, but triple any competitor. The company served 100,000 customers from 43 distribution centers. Return on equity averaged 18%, remarkable for a capital-intensive, low-margin business. Wall Street finally understood what Baugh had seen a decade earlier: food distribution wasn't about food; it was about building an unbeatable logistics network.

The culmination came in 1987 when revenue crossed $4 billion. Sysco was now 35 times larger than at its founding, operating in 38 states, serving everyone from corner diners to hospital systems. But management knew they'd hit a ceiling. To truly dominate, they needed presence in every major market, especially the West Coast and Chicago. That would require their biggest bet yet—a transformational acquisition that would either secure their dominance or destroy everything they'd built.

IV. The CFS Continental Mega-Deal: Achieving National Scale (1988)

Bill Woodhouse, Sysco's CEO, sat across from the investment bankers at First Boston in January 1988, staring at numbers that made him dizzy. CFS Continental—the nation's third-largest food distributor—was for sale. Price tag: $750 million, nearly equal to Sysco's entire market cap. The bankers were blunt: "This deal will either make you the undisputed king of food distribution or bankrupt you trying." Woodhouse's response would define Sysco's next three decades: "Then we better not screw it up."

CFS Continental was a Frankenstein's monster of food businesses, assembled by Continental Grain Company through aggressive 1970s acquisitions. They had everything: distribution centers in Los Angeles, San Francisco, and Seattle (markets where Sysco was weak), massive operations in Chicago and Washington D.C., even manufacturing plants producing everything from salad dressing to frozen pizzas. Annual revenue: $2.4 billion. The problem? Continental Grain wanted out of food distribution to focus on commodities trading. Sysco had a narrow window before larger conglomerates circled.

The complexity was staggering. CFS Continental wasn't one company but 15 distinct operations, each with different systems, cultures, and profitability. The California operations alone included PYA Monarch (the West Coast's largest distributor), S.E. Rykoff (specializing in upscale restaurants), and Redwood Empire (dominating Northern California). The manufacturing assets—which Sysco didn't want—included 12 plants that would need separate buyers. Investment bankers estimated the integration would take five years and $100 million in additional capital.

Negotiations played out like a chess match in conference rooms from Houston to Chicago. Sysco needed financing that wouldn't dilute shareholders into oblivion. The solution: a complex structure involving $350 million in bank debt, $200 million in bonds, and $200 million from selling CFS's manufacturing divisions. But buyers for those manufacturing assets had to be lined up before the deal closed—if they couldn't sell the plants quickly, debt payments would crush cash flow.

The manufacturing divestiture became a deal within the deal. Woodhouse assigned a team to secretly negotiate with potential buyers while the main acquisition progressed. Within 60 days, they'd arranged to sell the salad dressing operation to Wish-Bone Foods for $58 million, the frozen pizza plants to Schwan's for $72 million, and various other facilities to regional manufacturers. Total proceeds: $250 million, covering a third of the purchase price. The precision was remarkable—contracts signed contingent on the main deal closing.

March 1988: After two months of 20-hour days, the deal closed. Overnight, Sysco added 4,500 employees, 16 distribution centers, and presence in 148 of America's top 150 markets. Combined revenue approached $7 billion—50% larger than the nearest competitor. But the real prize was strategic: the West Coast operations gave Sysco access to America's most innovative restaurant market, Chicago provided a gateway to the Midwest's chain restaurants, and D.C. opened doors to massive government contracts.

Integration began immediately, but followed Sysco's proven decentralized approach with a twist. Rather than maintaining all 15 separate CFS brands, they consolidated into regional powerhouses. PYA Monarch and S.E. Rykoff merged into Sysco Food Services of Los Angeles. The Chicago operations became Sysco Chicago. Each kept local management but gained Sysco's purchasing power—an instant 4-6% reduction in product costs that could be passed to customers or dropped to the bottom line.

The technology integration alone was a herculean effort. CFS Continental's operations ran on seven different computer systems, some dating to the 1960s. Sysco's IT team, now 200 strong, worked market by market to standardize on Sysco's proprietary inventory management system. They discovered unexpected treasures: CFS's route optimization software was superior to Sysco's, so they reverse-integrated it across the entire company, saving $15 million annually in fuel and labor costs. Customer impact was immediate and dramatic. A California restaurant chain that previously managed relationships with 15 different distributors could now work with a single Sysco representative. Product costs dropped 5-8% on average. Delivery reliability improved from 92% to 98%. The combined company's purchasing power extracted unprecedented concessions from manufacturers—Kraft, General Mills, and Tyson suddenly faced a customer buying $500 million worth of products annually.

By December 1988, nine months post-closing, the integration was declared complete—years ahead of schedule. Sysco raised an estimated $250 million from divesting CFS Continental manufacturing divisions, covering debt service while maintaining financial flexibility. Revenue for fiscal 1989 hit $6.9 billion. Operating margins improved to 3.2%, up from 2.8% pre-merger. The stock price doubled within 18 months as Wall Street recognized the strategic masterstroke.

The CFS Continental acquisition didn't just add scale—it transformed Sysco's DNA. They'd proven that massive, complex integrations could be executed flawlessly through disciplined process and decentralized execution. The playbook was set: identify large regional players, pay premium prices justified by synergies, integrate operations while preserving local relationships, and reinvest savings into further expansion. This wasn't just growth; it was systematic market consolidation executed with surgical precision.

V. Building the Machine: Technology, Logistics & Private Label (1990s-2000s)

The warehouse in Palmetto, Florida, hummed with an otherworldly efficiency in 1995. Forklifts guided by radio frequency scanners zipped through 400,000 square feet of precisely climate-controlled zones. Orders placed at midnight were picked, packed, and loaded by 3 AM. Trucks departed in synchronized waves, their routes optimized by algorithms that considered traffic patterns, delivery windows, and driver hours. This wasn't just a distribution center—it was Sysco's vision of the future, where technology transformed food distribution from labor-intensive chaos to automated precision.

The 1990s began with a strategic revelation. Bill Woodhouse's successor as CEO, Bill Lindig, recognized that Sysco's next phase of growth couldn't come from acquisitions alone. The company needed to serve two diverging markets: independent restaurants wanting personalized service and massive chains demanding standardized, low-cost distribution. The solution was organizational innovation—creating SYGMA Network in 1991 as a separate subsidiary focused exclusively on chain restaurants.

SYGMA represented a radical departure from Sysco's traditional model. While core Sysco operations delivered 5,000 different products to independent restaurants, SYGMA delivered 500 products to thousands of identical locations. A Wendy's in Atlanta needed exactly the same frozen patties as one in Phoenix. SYGMA's warehouses looked more like Amazon fulfillment centers than traditional food distributors—narrow SKU counts, high volumes, extreme automation. By 1995, SYGMA was delivering to 8,000 chain locations, generating $1.5 billion in revenue with margins half of traditional operations but volumes that more than compensated.

The "fold-out" strategy launched in 1999 represented another innovation in organic growth. Rather than acquiring companies to enter new markets, Sysco would "fold out" from existing operations—essentially opening satellite facilities in adjacent territories. A Nashville distribution center would open a smaller facility in Knoxville, leveraging existing supplier relationships and management expertise. This approach cost 70% less than acquisitions while achieving similar market penetration. Between 1999 and 2005, Sysco executed 15 fold-outs, adding $2 billion in revenue without dilution or integration risk.

Technology investment accelerated throughout the decade, with Sysco spending $100 million annually on IT infrastructure by 2000. The crown jewel was a proprietary inventory management system that tracked products from manufacturer to customer delivery. Every case of tomatoes had a barcode scanned at receiving, storage, picking, and delivery. This granular tracking enabled just-in-time inventory management, reducing working capital needs by 15% while improving fill rates to 98.5%. Competitors using paper-based systems simply couldn't match this efficiency.

Private label development became a strategic weapon. Sysco-branded products—everything from ketchup to cutting boards—offered restaurants quality comparable to national brands at 15-20% lower prices. But the real genius was psychological. A restaurant buying Sysco-brand products couldn't easily switch distributors; they'd have to change their entire supply chain. By 2000, private label represented 35% of Sysco's sales, generating 40% of gross profits. Each Sysco truck became a rolling advertisement for switching costs. The international expansion began modestly with Canadian acquisitions in the late 1990s, but the 2002 purchase of SERCA Foodservices for $278 million represented a watershed moment. SERCA, Canada's largest foodservice distributor with $1.4 billion in revenue and 80,000 customers, instantly made Sysco the dominant player north of the border. The integration proved seamless—SERCA's operations were virtually identical to Sysco's U.S. model, just with metric measurements and bilingual packaging. Within three years, Canadian operations were generating 15% returns on invested capital. The FreshPoint acquisition in 2000 represented another strategic masterstroke. FreshPoint Holdings, with annual sales of about $750 million, enhanced Sysco's existing $1 billion in fresh produce sales. Produce had always been challenging for distributors—highly perishable, fragmented supply base, volatile pricing. FreshPoint had cracked the code with specialized warehouses, expert buyers who understood seasonal variations, and relationships with thousands of farms. Post-acquisition, Sysco could offer restaurants a complete solution: proteins from their core business, produce from FreshPoint, all delivered on one truck.

The expansion of FreshPoint through subsequent acquisitions demonstrated Sysco's platform strategy. Since the acquisition of FreshPoint in 2000, Sysco committed to extending specialty produce offerings and distribution reach, adding regional specialists like Fowler & Huntting in Connecticut, Nashville Tomato, and dozens of other local produce experts. Each acquisition brought local relationships and expertise that would take decades to build organically.

By 2005, the transformation was complete. Revenue had grown from $7 billion post-CFS Continental to $30 billion. The company operated 150 distribution centers, employed 50,000 people, and served 400,000 customers. More importantly, Sysco had evolved from a food distributor to a comprehensive foodservice solutions provider. They could handle everything from a food truck needing basic supplies to a hospital system requiring specialized nutrition products to a new restaurant needing kitchen design services.

The numbers told the story of operational excellence. Inventory turns increased from 12 times annually in 1990 to 24 times by 2005. Delivery accuracy reached 99.2%. Customer retention exceeded 95% annually. These weren't flashy Silicon Valley metrics, but in the grinding, low-margin world of food distribution, they represented world-class execution. Sysco had built the machine—now they would attempt to make it unstoppable.

VI. The US Foods Saga: When Antitrust Kills a Deal (2013-2015)

December 9, 2013, started like any other Monday at Sysco headquarters until CEO Bill DeLaney called an all-hands meeting at 7 AM. The conference room screens displayed a number that made executives gasp: $8.2 billion. That was the enterprise value of the acquisition they were about to announce—US Foods, their closest competitor. DeLaney's words hung in the air: "We're about to create a foodservice giant that nobody can challenge. Or we're about to learn exactly where the government draws the line on market concentration. "The deal structure was audacious: $3.5 billion for US Foods, with total enterprise value including debt reaching $8.2 billion. US Foods, owned by private equity firms Clayton Dubilier & Rice and KKR since 2007, was the perfect target—national footprint, similar business model, overlapping but complementary customer base. Combined, the two companies would control 75% of the national market for broadline distribution services. DeLaney's pitch to investors was compelling: $600 million in annual synergies, elimination of redundant distribution centers, unprecedented purchasing power with manufacturers.

The initial market reaction was euphoric. Sysco's stock jumped 10% on the announcement. Analysts praised the strategic logic—in a scale business, more scale always wins. Customers were more nervous. Many restaurants deliberately split orders between Sysco and US Foods to maintain negotiating leverage. Now their two biggest suppliers would become one. But DeLaney assured them: "Competition will remain vigorous. There are still 15,000 distributors out there."

By February 2015, that confidence had evaporated. The Federal Trade Commission filed an administrative complaint charging that the merger would violate antitrust laws by significantly reducing competition nationwide and in 32 local markets. The FTC's case was devastating in its simplicity: Sysco and US Foods were the only broadline distributors with a truly national footprint, with numerous distribution centers spread throughout the country. Many hotel chains and group purchasing organizations considered them each other's closest competitor, and in some cases their only meaningful alternatives.

The companies scrambled to save the deal. In a desperate move, Sysco agreed to sell 11 US Foods facilities to Performance Food Group (PFG), attempting to create a new national competitor. The argument: PFG plus the divested assets would replace US Foods' competitive role. But the FTC charged that the proposed sale would neither enable PFG to replace US Foods as a competitor nor counteract the significant competitive harm. Internal documents proved fatal—the FTC uncovered materials from Sysco and US Foods suggesting that each company was the other's main competitor.

The courtroom battle in June 2015 was brutal. Sysco's lawyers argued the market included thousands of regional distributors, making the combined company's 25% share acceptable. The FTC countered that broadline distribution was a distinct market where only Sysco and US Foods could serve national customers. Judge Amit Mehta's questioning revealed his skepticism: "If there are truly 15,000 competitors, why do your own documents repeatedly refer to US Foods as your 'only real competition'?"

June 23, 2015, arrived with crushing finality. Judge Mehta ruled that the combined Sysco-US Foods would control 75% of the U.S. food service industry and would stifle competition. His opinion was scathing: the companies' own documents contradicted their legal arguments, the PFG divestiture was insufficient, and the merger would harm both national chains and local restaurants through reduced competition and likely price increases.

Six days later, Sysco threw in the towel. The termination triggered a $300 million break-up fee to US Foods and $12.5 million to PFG. Total costs including legal fees approached $500 million. DeLaney's statement was subdued: "We believed the merger was the right strategic decision for us, and we're disappointed with the outcome. But we're extremely well positioned to move forward".

The failure reverberated through the industry. Sysco had learned where the government drew the line—75% market share was too much, even in a fragmented industry. The company pivoted to a $3 billion share buyback program and renewed focus on organic growth. Competitors breathed easier, knowing the duopoly threat had passed. Restaurants maintained their dual-supplier strategies.

The US Foods saga became a case study in antitrust enforcement. It proved that even in industries with thousands of participants, mergers between the top two players face extreme scrutiny. For Sysco, it was a $500 million education in the limits of consolidation. The empire could grow, but not through swallowing its mirror image. They would need a different path to dominance.

VII. Global Expansion & The Digital Transformation (2016-Present)

The Brakes Group headquarters in Ashford, England, looked nothing like a typical Sysco facility when executives first visited in late 2015. Where Sysco distribution centers were sprawling horizontal complexes, Brakes operated from compact, multi-story urban warehouses. Where Sysco trucks made pre-dawn deliveries, Brakes vehicles navigated narrow medieval streets at all hours. Where Sysco served portions sized for American appetites, Brakes stocked metric quantities for European tastes. Yet CEO Bill DeLaney saw past the differences to the opportunity: "If we can't buy US Foods, we'll build a global empire instead. "The February 2016 announcement of the $3.1 billion Brakes acquisition stunned Wall Street. The transaction was valued at approximately $3.1 billion USD and included the repayment of approximately $2.3 billion of Brakes Group's financial debt. Investors questioned the logic—no operational synergies, unfamiliar markets, Brexit uncertainty looming. Sysco's stock dropped 6% on announcement day. But DeLaney saw what critics missed: In fiscal 2015, Brakes Group's revenues were nearly $5 billion (3.3 billion British pounds), a 6.5 percent increase from the previous fiscal year, and Europe's food-away-from-home market was growing faster than America's.

Brake Bros Limited became a subsidiary of Sysco Corporation on July 5, 2016, operating as a wholly-owned but independent entity. The integration strategy was radically different from Sysco's U.S. playbook. Rather than imposing American systems, Sysco let Brakes run autonomously under CEO Ken McMeikan. The only changes: access to Sysco's global purchasing agreements and sharing of best practices. Within 18 months, Brakes' operating margins improved by 150 basis points simply from better procurement terms on commodities like chicken and cooking oil.

The digital transformation, accelerated by necessity during COVID-19, represented Sysco's most dramatic evolution since computerization in the 1970s. When the pandemic struck in March 2020, restaurant sales collapsed 80% overnight. Sysco's revenue plummeted from $60 billion to $45 billion. The company furloughed 33% of its workforce. Stock price crashed to $30, down from $85. Analysts questioned whether the traditional distribution model would survive.

The response revealed organizational resilience built over five decades. Within weeks, Sysco pivoted to serve new channels—delivering restaurant-quality products directly to consumers stuck at home, supplying grocery stores facing unprecedented demand, creating "ghost kitchen" solutions for restaurants shifting to takeout-only models. The company accelerated its digital platform rollout, enabling customers to place orders via mobile apps, track deliveries in real-time, and access data analytics on purchasing patterns. The pandemic response revealed organizational depth. Sysco donated 30 million meals across eight countries as part of its community response strategy to the COVID-19 pandemic, valued at over $100 million. The company pivoted to providing logistics services to retail grocery customers, becoming a supplier to overwhelmed supermarkets, and enabling small restaurants to stand up home delivery operations. CEO Kevin Hourican, who had joined just weeks before the crisis, coined the internal mantra: "Don't let a good crisis go to waste."

By fiscal 2021, the recovery was underway. Revenue rebounded to $51 billion as restaurants reopened. But more importantly, Sysco emerged transformed. The digital platforms accelerated during COVID became permanent fixtures—60% of orders now came through digital channels versus 20% pre-pandemic. The company had proven it could serve retail grocery, ghost kitchens, and direct-to-consumer markets. International operations, particularly Brakes, proved more resilient than U.S. operations due to stronger government support for European restaurants.

The technology investments continued post-pandemic. Sysco deployed artificial intelligence for demand forecasting, reducing food waste by 15%. Autonomous trucks began pilot programs in Texas. The company acquired Edward Don & Company in 2023, a food service equipment distributor, adding kitchen design capabilities. Each innovation aimed at the same goal: making Sysco indispensable to customers beyond just food delivery.

Sustainability initiatives, once afterthoughts, became strategic priorities. Sysco committed to reducing carbon emissions by 27.5% by 2030, ordering 800 electric delivery trucks, and working with suppliers to reduce packaging waste. These weren't just corporate responsibility theater—commercial customers increasingly demanded sustainable supply chains, and Sysco positioned itself as the only distributor with the scale to deliver meaningful environmental impact.

By 2024, Sysco had fully recovered and then some. Revenue reached $76 billion, surpassing pre-pandemic levels. The company served 730,000 customer locations across 10 countries. Market capitalization exceeded $40 billion. The transformation from American food distributor to global foodservice solutions provider was complete. The empire that began with nine companies merging in a Houston hotel had become genuinely international, digitally enabled, and more dominant than ever.

VIII. Business Model Deep Dive: The Economics of Food Distribution

The numbers seem impossible at first glance. Sysco generates $76 billion in annual revenue but keeps only $1.7 billion in net income—a 2.2% margin that would bankrupt most businesses. A typical delivery generates just $35 in gross profit on a $1,000 order. The company turns inventory 24 times per year, meaning products sit in warehouses for just 15 days on average. These aren't the economics of a tech unicorn or luxury brand. They're the grinding mathematics of moving 45 billion pounds of food annually through the most complex logistics network in America.

Understanding Sysco's business model requires abandoning traditional thinking about profit margins. In food distribution, the game isn't about markup—it's about velocity, density, and scale. Every basis point of efficiency matters when you're operating on 2-3% net margins. A truck arriving 10 minutes late can turn a profitable route unprofitable. A 1% increase in fuel costs can erase millions in earnings. This is capitalism at its most Darwinian, where only the most operationally excellent survive.

The unit economics reveal the beauty hidden in apparent mediocrity. A typical Sysco truck carries 500 cases worth $15,000 in revenue, delivered to 8-10 stops. The gross margin on those cases averages 17%—about $2,550. From that, Sysco must cover the truck ($150,000 amortized daily), driver ($300/day in wages and benefits), fuel ($200/day), warehouse handling ($500), and allocated corporate overhead ($400). Net profit per truck per day: roughly $100. Multiply that by 14,000 trucks operating 250 days per year, and you reach $350 million. The rest comes from operational leverage—spreading fixed costs across growing volume.

Customer segmentation drives profitability variation invisible in aggregate numbers. Sysco divides customers into three tiers. "National accounts"—chains like Olive Garden or Marriott—generate 15% gross margins but massive volumes with predictable demand. "Regional chains" yield 18% margins with moderate complexity. "Street customers"—independent restaurants—produce 22% margins but require more service, credit risk, and sales support. The art lies in portfolio balance: too many national accounts crush margins, too many street customers explode costs.

Private label products represent the hidden profit engine. Sysco-branded items—from plastic forks to frozen shrimp—generate 25-30% gross margins versus 15% for manufacturer brands. But the real value isn't markup; it's customer lock-in. A restaurant standardizing on Sysco Brand ketchup faces switching costs beyond finding a new distributor—they must source alternative products, retrain staff, risk customer complaints about taste changes. This soft lock-in produces 95% annual customer retention rates, reducing sales costs and enabling route density.

The three-tier product strategy maximizes both margins and customer satisfaction. "Good" tier includes basic commodity products at competitive prices—15% margins but essential for customer acquisition. "Better" products offer superior quality at moderate premiums—20% margins targeting quality-conscious operators. "Best" includes premium imports and specialties—30% margins for high-end establishments. This tiering allows sales representatives to upsell while meeting diverse customer needs.

Route density economics explain why scale becomes self-reinforcing. Adding one customer to an existing route costs virtually nothing—the truck is already driving past. But that customer adds $125,000 in annual revenue at 17% gross margin. As density increases, delivery costs per case drop exponentially. In Manhattan, where Sysco might have 50 customers per square mile, delivery costs are 40% lower per case than rural markets with two customers per square mile. This density advantage is nearly impossible for smaller competitors to replicate.

Working capital management represents another hidden excellence. Sysco pays suppliers on 45-day terms but collects from customers in 30 days—effectively getting paid before paying bills. This negative working capital cycle generates $2 billion in float that funds operations without borrowing. During inflationary periods, this float becomes even more valuable as Sysco collects at today's prices while paying yesterday's costs.

Technology investments, while massive in absolute terms, generate extraordinary returns through tiny efficiency gains. A routing algorithm that reduces drive time by 3% saves $50 million annually. An inventory system preventing 0.5% of spoilage adds $30 million to the bottom line. A credit screening tool reducing bad debt by 10 basis points yields $20 million. These marginal gains compound—explaining why Sysco spends $500 million annually on technology while operating in an ostensibly low-tech industry.

The acquisition integration playbook demonstrates how Sysco transforms mediocre operators into profit machines. When acquiring a regional distributor, Sysco typically improves their operating margin from 2% to 4% within 18 months through: purchasing leverage (reducing product costs 4-5%), route optimization (cutting delivery expense 10%), technology systems (reducing administrative costs 20%), and credit management (eliminating 50% of bad debt). A $500 million revenue acquisition thus generates an additional $10 million in annual profit simply through operational improvement.

Capital allocation discipline ensures returns exceed cost of capital despite thin margins. Sysco targets 15% return on invested capital for new distribution centers, 20% for acquisitions, and 25% for technology investments. Projects failing to meet hurdles don't proceed, regardless of strategic arguments. This discipline has produced 18% average ROIC over the past decade—remarkable for a capital-intensive, low-margin business.

The moat appears narrow until you calculate replication costs. Building Sysco from scratch would require: $15 billion for 340 distribution centers, $3 billion for 14,000 trucks, $2 billion for technology infrastructure, $1 billion in working capital, and somehow convincing 400,000 restaurants to switch suppliers. The replacement cost exceeds $20 billion before considering customer relationships, supplier agreements, and operational expertise. The low margins that seem like weakness are actually the moat—they make the business uninvestable for anyone seeking quick returns.

IX. Power & Playbook Analysis

The conference room at Sysco headquarters displays a simple chart that explains everything: market share versus profitability by competitor. Sysco sits alone in the upper right quadrant—8% market share, 3% operating margin. US Foods occupies the next tier—4% share, 2% margin. Everyone else clusters in the bottom left—sub-1% share, break-even margins. This isn't coincidence or superior execution alone. It's the mathematical inevitability of scale economics in a high-fixed-cost business. Sysco has cracked the code that eluded thousands of food distributors: how to transform scale into an unassailable competitive advantage.

Scale economies manifest in ways invisible to casual observers. A manufacturer like Tyson Foods would rather negotiate one contract with Sysco for $500 million in annual chicken purchases than manage relationships with 100 regional distributors buying $5 million each. This purchasing power translates to 3-5% better pricing—massive in a low-margin business. But the real advantage is reliability: Tyson knows Sysco's check will clear, orders will be consistent, and logistics will be flawless. Smaller distributors can't match these terms because they lack the volume to matter.

Network effects, often associated with technology companies, operate powerfully in food distribution. As Sysco adds customers in a geographic area, route density improves, lowering per-delivery costs. Lower costs enable competitive pricing, attracting more customers. More customers justify expanded inventory, improving fill rates. Better fill rates increase customer satisfaction, reducing churn. This virtuous cycle explains why Sysco's market share in mature markets often exceeds 20%, while in newer markets it struggles to reach 5%.

Switching costs compound over time through dozens of small frictions. A restaurant changing from Sysco must: establish credit with a new distributor, retrain staff on new ordering systems, adjust recipes for different product specifications, manage the transition of standing orders, risk service disruption during changeover, and often accept higher prices or reduced selection. For a restaurant operating on 5% margins, these risks outweigh potential savings unless service completely fails. Result: 95% annual customer retention.

The decentralized operating model, seemingly chaotic, actually represents organizational genius. Each of Sysco's regional operations functions as a semi-autonomous business, with local presidents controlling pricing, inventory, and customer relationships. This structure enables rapid response to local competition while maintaining corporate scale advantages. When a regional competitor cuts prices, the local Sysco president can respond immediately without corporate approval. But when negotiating with Kraft Heinz, all regions benefit from combined volume.

The M&A playbook, refined over 150 acquisitions, turns integration from art to science. Due diligence focuses on cultural fit over financial metrics—Sysco walks away from financially attractive deals if management philosophy conflicts. Post-acquisition, Sysco implements its systems gradually: month one brings purchasing agreements, month three adds technology platforms, month six integrates logistics networks. Local management stays in place, maintaining customer relationships. This patient approach achieves 90% retention of acquired customers versus industry norms of 70%.

Geographic expansion follows a concentric circle strategy. Sysco doesn't enter new markets randomly but extends from existing strongholds. A Dallas distribution center might expand first to Fort Worth, then Oklahoma City, then Tulsa—each expansion leveraging existing infrastructure and relationships. This reduces risk and accelerates profitability compared to establishing beachheads in distant markets.

The multi-brand strategy preserves local relationships while achieving corporate scale. In Boston, customers order from "Hallsmith-Sysco," maintaining the trusted Hallsmith name acquired in 1988. In San Francisco, it's "Sysco San Francisco," acknowledging the local identity. This approach contrasts with roll-up strategies that impose corporate branding, alienating customers loyal to local suppliers.

Technology adoption proceeds through careful experimentation rather than wholesale transformation. Sysco tests innovations in single markets before system-wide rollout. Autonomous trucks pilot in Texas. AI-driven demand forecasting trials in California. Blockchain supply chain tracking experiments in Illinois. This measured approach prevents costly failures while ensuring proven technologies deploy rapidly.

The talent development system creates institutional knowledge that money can't buy. Sysco promotes from within religiously—most senior executives started as sales representatives or warehouse workers. This builds deep operational understanding and cultural continuity. A new MBA hire might understand financial models but won't grasp why Tuesday deliveries to Italian restaurants must arrive before 10 AM (because that's when sauce preparation begins).

Capital allocation maintains balance between growth and returns. Sysco could grow faster through aggressive acquisition or price cutting but maintains discipline. The company targets GDP-plus-2% organic growth, enabling market share gains without triggering destructive price wars. Acquisitions must be accretive within two years. Dividends grow steadily but leave room for reinvestment. This measured approach has produced 47 consecutive years of revenue growth—remarkable consistency in a cyclical industry.

The defensive moat proves most powerful during downturns. In recessions, small distributors fail as restaurants reduce orders and stretch payments. Sysco's balance sheet absorbs these shocks, often gaining share as competitors disappear. The 2008 financial crisis saw 15% of food distributors cease operations; Sysco's market share increased from 7% to 8%. COVID-19 repeated this pattern—Sysco survived while hundreds of regional players collapsed.

But the ultimate power lies in optionality. Sysco's infrastructure—warehouses, trucks, customer relationships—can distribute anything restaurants need. The company has expanded from food to equipment, supplies, and technology services. Future growth might come from meal kits, ghost kitchens, or categories not yet invented. The distribution network, built over 55 years, provides a platform for whatever foodservice becomes.

X. Bear Case, Bull Case & The Future

The bear case starts with a simple observation: Amazon Business grew from zero to $35 billion in revenue in six years, already approaching half of Sysco's size. The everything store's entry into B2B distribution sends chills through Sysco's Houston headquarters. Amazon offers 30 million SKUs versus Sysco's 500,000. Next-day delivery without minimum orders. Transparent pricing without sales representative negotiations. Technology-first operations versus Sysco's legacy systems. If Amazon can destroy retail, why not food distribution?

The numbers paint a sobering picture for bears. Restaurant industry growth has decelerated from 4% annually in the 2010s to 2% projected through 2030. Ghost kitchens and meal kit services bypass traditional distributors entirely. Labor costs are exploding—driver wages up 40% since 2019—while autonomous vehicles remain perpetually "five years away." Sysco's 14,000 trucks burn 200 million gallons of diesel annually; converting to electric requires $5 billion in capital expenditure. Meanwhile, private equity-backed regional competitors consolidate, creating super-regional threats with lower cost structures.

Technology disruption threatens from unexpected angles. Restaurant procurement platforms like ChefHero and BlueCart enable establishments to comparison shop across distributors in real-time, destroying pricing power. Direct-from-farm platforms eliminate distributors entirely for produce. Cloud kitchens vertically integrate supply chains, cutting out middlemen. Software companies like Toast embed procurement into point-of-sale systems, potentially disintermediating traditional sales relationships.

The capital intensity trap worsens over time. Sysco must invest $2 billion annually just to maintain current operations—new trucks, warehouse updates, technology modernization. Growth requires additional billions. Yet returns on invested capital have declined from 20% to 15% as competition intensifies. The company resembles a railroad in 1950—essential infrastructure but diminishing returns on massive capital requirements.

Environmental regulations pose existential challenges. California's Advanced Clean Trucks Rule requires 75% of delivery vehicles to be zero-emission by 2035. Similar regulations spread nationwide. But electric trucks with refrigeration units don't yet exist at commercial scale. Hydrogen alternatives remain experimental. Compliance could require $10 billion in fleet replacement—nearly two years of current free cash flow.

The bull case begins with market structure reality: food distribution isn't e-commerce. Amazon excels at shipping packages to patient consumers. Sysco delivers 500-pound orders to impatient chefs at 5 AM. Products range from frozen at -10°F to fresh at 35°F to hot at 140°F—requiring specialized trucks Amazon doesn't possess. Restaurants need credit terms, menu consultation, and emergency deliveries—services beyond Amazon's model. The company that disrupted bookstores struggles to deliver groceries profitably; foodservice distribution is exponentially more complex.

Market fragmentation ensures decades of consolidation opportunity. Sysco's 8% market share leaves 92% controlled by smaller players. Acquiring just 1% annually through tuck-in acquisitions adds $3 billion in revenue. International markets remain virtually untapped—Europe's food distribution market equals America's but remains even more fragmented. China's foodservice market, growing 10% annually, lacks professional distribution. Sysco could triple its size without increasing market share in any single geography.

The irreplaceable infrastructure moat strengthens over time. Building Sysco's distribution network today would cost $30 billion and take decades. No rational investor would attempt it given the returns. Meanwhile, Sysco's existing infrastructure becomes more valuable as urban real estate prices soar. A Los Angeles distribution center acquired for $10 million in 1980 now sits on land worth $100 million. This hidden real estate value—perhaps $5 billion nationally—provides downside protection while generating operational advantage.

Demographic tailwinds support long-term growth. Millennials and Gen Z spend 15% more on dining out than previous generations. Dual-income households lack time for cooking. Urban density makes kitchens smaller and restaurants more accessible. Food delivery apps expand restaurant accessibility. The "food away from home" share of consumption has grown from 25% in 1970 to 55% today, heading toward European levels of 65%. Even modest market growth, combined with share gains, produces attractive returns.

Technology amplifies rather than threatens Sysco's advantages. The company's scale justifies investments smaller players can't match—$500 million annually in digital platforms, analytics, and automation. These tools improve efficiency, enabling Sysco to profitably serve customers that lose money for subscale competitors. As technology becomes table stakes in distribution, only the largest players can afford to play.

The platform expansion opportunity dwarfs traditional distribution. Sysco's 730,000 customer relationships create distribution for adjacent services: equipment leasing, kitchen design, menu consulting, financial services. A restaurant spending $200,000 annually on food might spend another $100,000 on these services. Capturing 10% of this adjacent spend would add $15 billion in high-margin revenue. The company's recent acquisition of Edward Don & Company signals this strategic shift.

Resilience through diversification provides downside protection. International operations now generate 20% of profits, reducing U.S. exposure. Healthcare and education customers provide recession-resistant demand. Private label products create switching costs. The broadline model—distributing everything from food to toilet paper—ensures customer dependency. This diversification prevented collapse during COVID and positions Sysco for future shocks.

The future likely combines both narratives. Amazon and technology platforms will capture price-sensitive, low-service customers. Regional specialists will dominate high-touch niches. But Sysco's sweet spot—multi-unit chains requiring reliable, full-service distribution—remains defensible. The company might cede market share edges while strengthening its core.

The most probable scenario: Sysco evolves from pure distribution to comprehensive foodservice solutions. Physical distribution becomes the foundation for digital services, financial products, and operational consulting. Revenue growth slows but margins expand as services complement products. The company in 2040 might look as different from today as today's Sysco differs from the 1969 original—yet still dominate through scale, service, and systematic execution.

XI. Grading & Key Takeaways

Execution Grade: A-

Over 55 years, Sysco has delivered remarkably consistent execution in an inherently difficult business. Revenue grew from $115 million to $76 billion—a 12.5% compound annual growth rate. The company has increased its dividend for 54 consecutive years, a record matched by fewer than 20 American companies. Through recessions, inflation, pandemic, and competitive threats, Sysco adapted while maintaining strategic focus. The only execution blemish: the failed US Foods merger, costing $500 million and two years of distraction. Otherwise, the operational excellence borders on monotonous—which in food distribution represents the highest compliment.

Capital Allocation Grade: B+

Management has generally deployed capital intelligently, achieving 15-18% returns on invested capital despite operating in a capital-intensive, low-margin industry. The acquisition track record stands out—150+ successful integrations with minimal failures. Dividend policy balances growth investment with shareholder returns. The share buyback program, while substantial, came at reasonable valuations. The grade isn't higher because of occasional mistiming (buying at market peaks) and the US Foods debacle. But overall, Sysco has created tremendous value through disciplined capital deployment—turning $23 per share at IPO into today's $75 stock plus decades of dividends.

Management Quality Assessment: B+

Sysco's leadership demonstrates the power of promoting from within. Most CEOs started in operations, understanding the business intimately. The decentralized structure develops entrepreneurial leaders while maintaining corporate discipline. Succession planning works smoothly—no drama, no outside saviors, just competent executives stepping into well-defined roles. The culture emphasizes operational excellence over financial engineering. However, management sometimes lacks boldness—the company could have expanded internationally sooner, embraced technology faster, or pursued adjacent opportunities more aggressively. The conservatism that ensures survival may also limit potential.

Most Underappreciated Aspects

First, the network effects in food distribution remain invisible to most observers. Each additional customer makes Sysco more valuable to suppliers and more efficient in operations—a compounding advantage that accelerates over time. Second, the replacement cost of Sysco's infrastructure exceeds $30 billion, providing enormous downside protection. Even if the business model disrupted tomorrow, the real estate and logistics assets retain substantial value. Third, the international opportunity remains largely untapped. Sysco generates 80% of revenue domestically despite America representing just 25% of global foodservice spend.

The pricing power hidden within mundane operations deserves recognition. While headline inflation affects all distributors equally, Sysco's scale enables selective price increases that smaller competitors can't match. A 0.5% price increase on private label products, unnoticed by customers, generates $100 million in additional profit. This micro-pricing power, exercised across thousands of products and customers, creates substantial value over time.

Lessons for Founders and Investors

The Sysco story teaches that boring businesses can build extraordinary moats. Food distribution lacks the glamour of technology or innovation of pharmaceuticals, yet Sysco's competitive advantages prove more durable than most "disruptive" companies. The lesson: execution matters more than innovation in established industries. Systematic improvement, compounded over decades, creates insurmountable leads.

The power of consolidating fragmented industries through operational excellence rather than financial engineering provides a replicable playbook. Sysco didn't roll up food distribution through leveraged buyouts and cost-cutting. Instead, they improved acquired operations while maintaining local relationships. This patient approach took longer but created lasting value. Modern consolidators fixated on quick returns should study Sysco's 50-year journey.

The importance of culture in low-margin businesses cannot be overstated. When net margins are 2%, small differences in execution determine success or failure. Sysco's culture of operational excellence—where warehouse workers take pride in order accuracy and drivers view themselves as customer service representatives—creates advantages no competitor can purchase. Building such culture requires decades and can't be disrupted by technology or capital.

For investors, Sysco demonstrates that competitive advantages exist in unexpected places. The company lacks patents, network effects seem minimal, and switching costs appear low. Yet the combination of scale, service, and systems creates a moat that has widened for five decades. Understanding these subtle advantages requires deep industry knowledge—rewarding investors who look beyond financial statements.

The disciplined expansion into adjacent markets offers a template for mature companies seeking growth. Rather than desperate diversification into unrelated businesses, Sysco methodically expanded from food to supplies to equipment to services—each step leveraging existing customer relationships and operational capabilities. This patient approach might not excite growth investors but creates sustainable value.

Finally, Sysco proves that operational excellence can be a strategy. In an era obsessed with disruption and transformation, Sysco succeeds through relentless focus on basics: deliver on time, invoice accurately, maintain quality, serve customers. These mundane activities, performed slightly better than competitors every day for 55 years, compound into dominance. Sometimes the best strategy is simply executing the obvious better than anyone else.

The ultimate lesson may be that building an empire doesn't require genius insights or revolutionary technology. John Baugh's vision wasn't complicated—consolidate a fragmented industry through systematic operations and strategic acquisitions. The execution required patience, discipline, and focus most companies can't maintain. But for those who can, the rewards compound into something extraordinary: an invisible empire that feeds America, $35 of profit at a time.

XII. Recent News

Q3 2024 Earnings and Strategic MomentumThe company's fiscal 2025 performance demonstrates remarkable resilience and strategic momentum. In Q1 2025, sales increased 4.4% to $20.5 billion, with U.S. Foodservice volume increasing 2.7% and adjusted EPS increasing 1.9% to $1.09. The second quarter continued this trajectory, with sales growing 4.5% to $20.2 billion, U.S. Foodservice volume up 1.4%, and adjusted EPS increasing 4.5% to $0.93.

Management reiterated fiscal 2025 guidance, projecting sales growth of 4-5% and adjusted EPS growth of 6-7%. The confidence reflects strong performance across multiple segments despite headwinds. The International segment demonstrated exceptional strength with adjusted operating income growing 26.5%, driven by operational improvements and procurement synergies. SYGMA sales grew 10.6%, indicating robust chain restaurant demand.

Capital Returns and Financial Strength

Sysco increased its shareholder return program to approximately $2.25 billion in fiscal 2025, with share repurchases now expected at $1.25 billion alongside dividends of $1 billion. The company maintains a strong balance sheet with a net debt leverage ratio of 2.76 times and approximately $3.1 billion in total liquidity, providing flexibility for both growth investments and shareholder returns.Strategic Acquisitions and Expansion

Sysco announced in October 2023 its agreement to acquire Edward Don & Company, a leading distributor of foodservice equipment, supplies, and disposables generating approximately $1.3 billion in annual revenue. The acquisition was completed in November 2023 for approximately $970 million. Edward Don now operates as a standalone specialty division within Sysco led by Steve Don, complementing Sysco's Supplies on the Fly business and creating a specialty equipment and supplies platform.

This acquisition represents a strategic expansion beyond traditional food distribution into higher-margin equipment and supplies. Edward Don brings over 1.4 million square feet of distribution centers and office space in key U.S. geographies, a dedicated field sales team focused on equipment and supplies, and design and build capabilities. The move signals Sysco's commitment to becoming a comprehensive foodservice solutions provider rather than just a food distributor.Technology and AI Transformation

Sysco's Recipe for Growth strategy relies heavily on the company being a technology leader, implementing microservices, migrating to the cloud, and deploying artificial intelligence, with the goal of growing 1.5 times the size of the industry. The company has invested heavily in both traditional AI and generative AI capabilities to optimize operations across multiple dimensions.

In demand forecasting, Sysco employs machine learning algorithms to analyze historical sales data, market trends, and external factors to anticipate customer demand, optimizing inventory levels and reducing waste. AI-powered computer vision systems monitor inventory in real-time, identify stock discrepancies, and automate reordering processes, minimizing losses due to spoilage.

The company maintains nearly 2 million SKUs, using AI to make product recommendations by incorporating unstructured data like images and social media signals. Generative AI assists in call planning, menu curation, and customer segmentation, helping sales teams be more effective and resulting in bigger shopping carts and higher margins.

In supply chain operations, Sysco uses AI to manage inventory, optimize warehouse logistics, and route customer deliveries more efficiently, including intelligent substitutions when products are out of stock or deliveries are impacted by weather events.

XIII. Links & Resources

Official Company Resources - Investor Relations: investors.sysco.com - Annual Reports: SEC filings and 10-K documents available through investor portal - Quarterly Earnings: Live webcasts and presentations archived online - Corporate Website: www.sysco.com

Industry Research and Analysis - Foodservice Equipment Reports Magazine: Industry trends and dealer rankings - Restaurant Business Online: Foodservice distribution insights - CIO Magazine: Technology transformation case studies - MIT Sloan Management Review: Digital strategy analysis

Historical and Academic Resources - Harvard Business School Cases on Sysco's growth strategy - SEC EDGAR Database: Complete filing history since 1970 IPO - Company acquisition history and integration playbooks - Food Distribution Research Society publications

Technology and Innovation - Sysco Technology Careers Portal: Insights into digital transformation - Supply Chain Management Review: Logistics optimization studies - AI and automation implementation case studies - E-commerce platform development resources

Competitive Intelligence - US Foods investor materials for market comparison - Performance Food Group financial reports - Gordon Food Service market analysis - Regional distributor association publications

Books and Long-Form Analysis - "The Box: How the Shipping Container Made the World Smaller" - parallels in logistics revolution - "Scale: The Universal Laws of Growth" - understanding network effects in distribution - Industry trade publications on food distribution economics - Supply chain management textbooks featuring Sysco case studies

Final Thoughts: The Invisible Empire's Enduring Power

Sysco's story ultimately transcends food distribution. It's a masterclass in how operational excellence, patient capital allocation, and systematic execution can build an empire more durable than any built on innovation alone. In an era where venture capitalists chase unicorns and Wall Street rewards disruption, Sysco proves that sometimes the most valuable companies are those that perfect the mundane.

The company's 55-year journey from nine regional distributors to a $40 billion market capitalization demonstrates that competitive advantages don't require patents or network effects visible to casual observers. Sometimes, the moat is simply doing thousands of small things slightly better than anyone else, every single day, for decades. Each truck route optimized by 2%, each warehouse layout improved by inches, each customer relationship maintained through consistent service—these microscopic advantages compound into an insurmountable lead.

Looking forward, Sysco faces the classic innovator's dilemma in reverse. They're not the incumbent disrupted by innovation but the executor threatened by their own success. At 8% market share, they have room to grow through consolidation. But antitrust concerns, demonstrated by the failed US Foods merger, cap their domestic ambitions. International expansion offers promise but requires adapting their model to different cultures, regulations, and eating habits. Technology investments in AI and automation will improve efficiency but won't fundamentally change the physics of moving 45 billion pounds of food annually.

Yet Sysco's true genius lies not in solving these challenges but in not needing to solve them perfectly. Their business model—high volume, low margins, massive scale—creates a beautiful paradox. The very characteristics that make food distribution unattractive to new entrants (capital intensity, operational complexity, thin profits) become Sysco's protective moat. Would-be disruptors face a sobering reality: to compete with Sysco requires billions in capital, decades of relationship building, and acceptance of 2-3% margins. In Silicon Valley terms, it's the world's worst pitch.

The company that began as John Baugh's vision of systematizing chaos has achieved something remarkable: they've made themselves boring and essential simultaneously. Every restaurant owner knows Sysco's phone number. Every chef has opinions about their products. Every competitor benchmarks against their prices. Yet consumers remain blissfully unaware that their dining experiences depend on 14,000 trucks departing Sysco warehouses before dawn.

This invisibility is Sysco's greatest triumph. They've built an empire that operates in shadows, generates billions in profits from pennies per pound, and grows stronger with each passing year. While tech companies grab headlines and disruptors promise revolution, Sysco quietly feeds America, one delivery at a time. In the end, that's the lesson: empires aren't always built through innovation or disruption. Sometimes, they're built by showing up, every day, with exactly what customers need, exactly when they need it, for half a century and counting.

The Sysco story isn't finished. But after 55 years, $76 billion in revenue, and 730,000 customers served daily, one thing seems certain: whatever the future of food looks like, Sysco will be there to distribute it. The invisible empire, built on the unglamorous business of moving boxes, has proven more durable than anyone imagined when nine companies merged in a Houston hotel. And perhaps that's the ultimate business lesson—that true competitive advantage comes not from doing extraordinary things, but from doing ordinary things extraordinarily well, forever.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube