Republic Services: The Empire Built on Trash

I. Introduction & Episode Roadmap

Picture this: A convoy of lime-green trucks rolls out before dawn across 41 states, their drivers navigating 2.5 million miles of routes every week. By the time most Americans wake up, these 17,000 vehicles have already begun their daily ritual—collecting, hauling, and processing 100 million tons of waste annually. This is Republic Services, a $78 billion colossus that has quietly built one of America's most resilient business empires on something everyone produces but nobody wants to think about: garbage.

The question that should fascinate any student of business is deceptively simple: How did a company spun off from an automotive conglomerate's waste division transform into America's second-largest environmental services empire, serving 13 million customers and generating over $14 billion in annual revenue?

The answer involves Wayne Huizenga's playbook from building Blockbuster and AutoNation, a perfectly-timed mega-merger during the 2008 financial crisis, and a strategic pivot from "waste hauler" to "environmental solutions provider" that would make any McKinsey consultant jealous. It's a story of consolidating a fragmented industry through 400+ acquisitions, achieving 18.62% return on equity in what most consider a commodity business, and somehow convincing Wall Street that a garbage company deserves a premium multiple.

This journey takes us from Republic's origins as a small waste disposal firm in 1981 through its transformation into an ESG darling that turns landfill gas into renewable energy and operates the nation's largest vocational fleet of clean energy vehicles. Along the way, we'll explore the economics of route density, the competitive moat of landfill ownership, and how regulatory complexity becomes a competitive advantage when you know how to wield it.

Four major themes emerge from Republic's ascent: the art of industry consolidation, the power of operational excellence in unglamorous businesses, the delicate balance between sustainability leadership and margin preservation, and the surprisingly sophisticated economics of trash collection. Each phase of Republic's evolution—from Huizenga's initial vision through today's environmental solutions expansion—reveals lessons about building enduring value in industries others overlook.

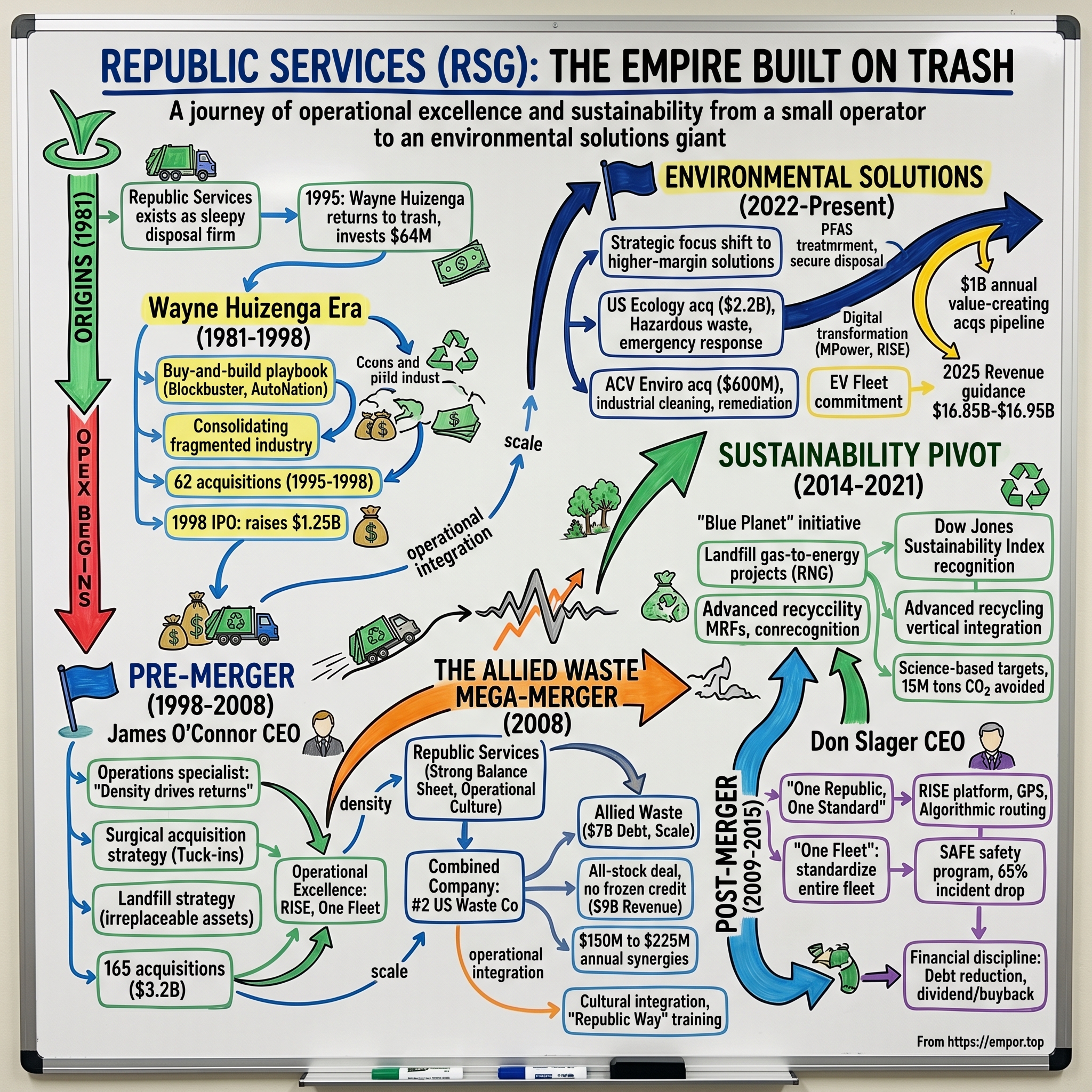

II. The Wayne Huizenga Era & Republic's Origins (1981–1998)

The conference room at the Fontainebleau Hotel in Miami Beach hummed with tension on a humid September morning in 1995. Wayne Huizenga, fresh off selling Blockbuster to Viacom for $8.4 billion, sat across from a group of investment bankers pitching him on various opportunities. At 57, most expected him to finally slow down. Instead, he stunned the room: "I want to buy garbage companies again."

The bankers exchanged glances. Huizenga had already built Waste Management from a $5 million company into a $19 billion giant before departing in 1984. Why return to trash? His answer was vintage Huizenga: "Because I understand it, the industry is fragmented again, and nobody else sees what I see."

Republic Services existed as a sleepy waste disposal subsidiary within Republic Industries, originally created in 1981. The company operated a handful of collection routes and landfills, generating modest returns for its automotive-focused parent. But Huizenga saw something others missed—the waste industry had re-fragmented after his departure from Waste Management, creating thousands of small operators ripe for consolidation.

In a move that would define Republic's trajectory, Huizenga invested $64 million of his personal fortune and raised an additional $168 million from investors who had followed him through Blockbuster and AutoNation. The funding structure was crucial: Huizenga maintained control while bringing in patient capital that understood his buy-and-build playbook. "Wayne didn't just bring money," recalled an early Republic executive. "He brought a system—standardized trucks, unified billing, route optimization software that was years ahead of what mom-and-pop haulers were using."

The AutoNation connection proved strategically brilliant. While Republic Industries focused on automotive retail, Huizenga quietly built Republic Services as a parallel venture within the same corporate structure. This gave him access to sophisticated financial engineering, shared services for back-office functions, and most importantly, credibility with Wall Street. Investment bankers who wouldn't return calls from a standalone waste company eagerly pitched deals to Wayne Huizenga's latest venture.

Between 1995 and 1998, Republic executed 62 acquisitions, expanding from 5 states to 21. Each deal followed the same template: identify family-owned haulers with strong local relationships but weak operational systems, pay fair multiples (typically 5-7x EBITDA), immediately implement Republic's standardized processes, and achieve 20-30% margin improvement within 18 months. The playbook was so consistent that Republic's integration team could absorb a new acquisition every three weeks.

The masterstroke came with timing the IPO. On July 1, 1998, Republic Services began trading on the NYSE under the symbol RSG, raising $1.25 billion at a $3.5 billion valuation. The prospectus pitched a simple story: the waste industry generates predictable cash flows, consolidation creates economies of scale, and Republic had the team and capital to roll up a fragmented market. First-day trading saw the stock pop 18%, validating Huizenga's vision.

What made Republic different from other roll-ups was operational discipline. While competitors focused solely on acquisitions, Huizenga insisted on standardization from day one. Every truck was painted the same shade of blue (later changed to signature lime green), every driver wore the same uniform, every customer received the same billing format. This might seem trivial, but it enabled Republic to achieve something remarkable: they could integrate acquisitions at one-third the cost and twice the speed of competitors.

The organizational structure Huizenga implemented deserves special attention. Rather than running Republic as a centralized empire, he created semi-autonomous regions with P&L responsibility while maintaining strict corporate standards for safety, fleet management, and customer service. Regional managers could make quick decisions on local acquisitions and pricing while benefiting from corporate purchasing power and operational expertise. This balance between local autonomy and corporate discipline would become Republic's secret weapon.

By late 1998, Republic had assembled a platform perfectly positioned for the next phase of growth. With 13,000 employees, 2,800 collection vehicles, and operations in 21 states, the company generated $1.5 billion in annual revenue. But Huizenga knew this was just the foundation. The real opportunity lay in competing head-to-head with his former company, Waste Management, and an emerging rival called Allied Waste. As he prepared to hand over the CEO reins to James O'Connor in December 1998, Huizenga left his successor with clear marching orders: "We've built the platform. Now go win the war."

III. Building Through M&A: The Pre-Merger Years (1998–2008)

James O'Connor's first morning as CEO in December 1998 began at 4:30 AM, riding along on a collection route in Phoenix. The driver, a 20-year veteran named Miguel, was stunned to see the new chief executive climbing into his cab. "You really want to see how we pick up trash?" Miguel asked. O'Connor's response set the tone for his tenure: "I want to understand every aspect of this business, starting with the most important job—yours."

O'Connor brought a different energy than Huizenga's dealmaking swagger. An operations specialist who had run Republic's largest region, he understood that winning in waste required more than just acquisitions—it demanded operational excellence at the route level. His philosophy was simple: "Density drives returns." Every decision, from acquisitions to customer contracts, would be evaluated through this lens.

The competitive landscape of the early 2000s resembled a three-way chess match. Waste Management remained the 800-pound gorilla with 30% market share, while Allied Waste had emerged as an aggressive consolidator targeting the same mid-sized operators Republic coveted. The remaining 50% of the market consisted of thousands of local and regional players, creating a land-grab dynamic where speed and execution determined winners.

Republic's acquisition strategy during this period was surgical rather than scattershot. While Allied pursued blockbuster deals that grabbed headlines, Republic focused on "tuck-in" acquisitions—buying competitors that operated adjacent to existing routes. A typical example: In 2001, Republic acquired Sanifill's Texas operations for $175 million, instantly adding 40% more density to its Dallas-Fort Worth routes. The math was compelling: adding customers to existing routes increased margins from 18% to 28% because trucks were already driving those streets.

The economics of garbage collection are beautifully simple yet operationally complex. A typical residential route might service 800 homes, generating $25 per month per home in revenue. The key variable is "picks per hour"—how many stops a driver can efficiently complete. By increasing route density from 15 to 20 picks per hour, Republic could boost EBITDA margins by 500 basis points. This might sound pedestrian, but across thousands of routes, it translated to hundreds of millions in additional profit.

Between 1999 and 2007, Republic completed 165 acquisitions totaling $3.2 billion in purchase price. But the real story wasn't the deal count—it was the integration playbook. Republic developed a 100-day integration plan so detailed that acquired companies often saw margin improvement before the deal officially closed. Safety training began on day one, fleet standardization within 30 days, billing system conversion by day 60, and full route optimization completed by day 100.

The landfill strategy deserves particular attention. While collection generates steady cash flow, landfill ownership creates the true moat in waste management. Republic systematically acquired strategic landfills, particularly those with 20+ years of remaining capacity near major metropolitan areas. By 2007, Republic owned or operated 95 active landfills with an average remaining life of 35 years. These assets not only provided disposal capacity for Republic's collection operations but also generated "tip fees" from competitors forced to use Republic's facilities.

Environmental regulations, rather than being a burden, became a competitive advantage. The EPA's Subtitle D regulations, implemented in the 1990s, required expensive upgrades to landfill liners, leachate collection systems, and groundwater monitoring. Smaller operators couldn't afford the compliance costs, accelerating consolidation. Republic invested over $500 million in environmental compliance between 2000 and 2007, turning regulatory requirements into barriers to entry.

The commercial and industrial segment became Republic's growth engine. While residential collection operated on thin margins due to municipal contract constraints, commercial customers offered better economics. Republic pioneered the "multi-year evergreen contract" structure—agreements that automatically renewed with built-in price escalators tied to CPI. By 2007, 75% of commercial revenues came from these contracts, providing predictable cash flow that Wall Street loved.

Technology investments during this period positioned Republic ahead of competitors. The company spent $150 million developing proprietary route optimization software that used GPS tracking and algorithmic planning to reduce miles driven by 15%. Driver tablets replaced paper manifests, customer service moved online, and predictive maintenance systems reduced fleet downtime by 20%. These weren't sexy innovations, but they generated real returns in a business where pennies per pick mattered.

The financial performance validated O'Connor's operational focus. Revenue grew from $1.5 billion in 1998 to $3.2 billion by 2007, while EBITDA margins expanded from 24% to 31%. Return on invested capital reached 12%, exceptional for a capital-intensive business. The stock price reflected this success, rising from $15 at IPO to $38 by late 2007, outperforming the S&P 500 by 250 basis points annually.

As 2008 approached, Republic had built itself into a formidable competitor—the clear number three player with 10% market share, strong free cash flow generation, and a proven operational model. But O'Connor knew that organic growth and tuck-in acquisitions could only take Republic so far. To truly compete with Waste Management, Republic needed scale. The opportunity would come sooner than expected, delivered by the most unlikely catalyst: the global financial crisis.

IV. The Allied Waste Mega-Merger (2008)

The Lehman Brothers building in Times Square still had lights on at 2 AM on September 15, 2008, as employees packed boxes and deleted files. Six blocks away, in a nondescript conference room at Wachtell, Lipton, Rosen & Katz, two teams of executives and bankers were pulling an all-nighter of their own. Republic Services and Allied Waste were racing to announce their $11 billion merger before markets opened—a deal that would create America's second-largest waste company precisely as the global financial system was collapsing.

"Everyone thought we were insane," recalled a Republic board member. "Credit markets were frozen, stocks were in freefall, and we were announcing the largest waste industry merger in history." But that was exactly the point. While others panicked, Republic and Allied saw opportunity in chaos.

The merger talks had actually begun six months earlier, in March 2008, when Allied CEO John Zillmer called O'Connor with a proposal. Allied, burdened with $7 billion in debt from its own aggressive acquisition spree, needed a partner. Republic, with its strong balance sheet and operational excellence, needed scale. The strategic logic was compelling: combined, they would operate in 40 states with $9 billion in revenue, creating a true competitor to Waste Management.

The deal structure revealed sophisticated financial engineering. Allied shareholders would receive 0.45 shares of Republic common stock for each Allied share, with Republic issuing approximately 196 million shares. This gave Allied shareholders 52% ownership of the combined company—technically making it a merger of equals, though everyone understood Republic's operational culture would dominate. The exchange ratio implied a 16% premium to Allied's pre-announcement price, modest by historical standards but appropriate given market conditions.

What made the timing brilliant rather than crazy was the financing structure. Because it was an all-stock deal, Republic didn't need to tap frozen credit markets. The combined company would have $7.5 billion in debt against $2.8 billion in EBITDA—a manageable 2.7x leverage ratio when competitors were struggling with 4-5x. Republic's investment-grade credit rating would extend to the combined entity, reducing Allied's borrowing costs by 200 basis points and generating $140 million in annual interest savings alone.

The integration planning was military in precision. Seventeen functional and cross-functional teams invested more than 12,000 hours mapping out every detail before the deal closed. Republic literally created a "war room" in Phoenix with walls covered in process maps, organizational charts, and integration timelines. Each of Allied's 370 locations was evaluated and assigned a "Day 1" plan. Every one of Allied's 23,000 employees received a welcome packet with their new reporting structure, benefits information, and Republic's operational standards.

The Department of Justice review added complexity but ultimately validated the merger's logic. After a six-month review, DOJ required divestitures in 13 markets where the combined company would have excessive concentration. Republic had anticipated this, identifying $250 million of non-core assets for sale even before regulatory demands. These divestitures actually improved the deal economics—Republic sold marginal routes to competitors at 8x EBITDA while the merger was priced at 6.5x.

The synergy targets seemed aggressive but proved conservative. Management promised $150 million in annual cost synergies by 2011. The actual number reached $225 million by 2010, a year ahead of schedule. The synergies came from multiple sources: $65 million from procurement savings (fuel, tires, insurance), $50 million from overhead elimination, $45 million from route optimization, $35 million from facility consolidation, and $30 million from IT systems integration.

Cultural integration posed the biggest challenge. Allied had grown through debt-fueled acquisitions with a decentralized, entrepreneurial culture. Republic operated with standardized processes and operational discipline. O'Connor's solution was elegant: keep the best of both. Republic adopted Allied's stronger positions in certain markets while implementing Republic's operational standards. Key Allied executives were retained but required to complete "Republic Way" training—a 90-day immersion in Republic's operating philosophy.

The fleet harmonization alone was a massive undertaking. The combined company operated 32,000 vehicles in dozen different colors with incompatible maintenance systems. Republic standardized on its lime-green livery and Mack/Peterbilt chassis, but the transition took three years and $400 million in capital investment. The payoff: maintenance costs dropped 18% and vehicle uptime increased to 94%.

By December 2008, when the merger officially closed, the macro environment had deteriorated further. Commercial construction—a key source of high-margin disposal volume—had virtually stopped. Recycling commodity prices collapsed 70% from their peaks. Municipal budgets were being slashed. Yet Republic's stock price held steady around $25 while competitors crashed. The market recognized that Republic had just executed one of the best-timed mergers in corporate history.

The combined company that emerged was formidable: 35,000 employees, 400 collection companies, 220 transfer stations, 190 active landfills, and 58 recycling centers. Annual revenue exceeded $9 billion with 30% EBITDA margins. Market share reached 18%, finally giving Republic the scale to compete effectively with Waste Management's 25% share. More importantly, Republic now had density in every major U.S. market—the foundation for sustainable competitive advantage.

The first earnings call post-merger set the tone for the next era. O'Connor's message was clear: "We didn't do this deal for size. We did it for density, operational excellence, and cash flow generation. Every decision we make will be evaluated through that lens." As 2009 dawned with the economy in recession, Republic would need every bit of that operational discipline to navigate the storm ahead.

V. Post-Merger Integration & Operational Excellence (2009–2015)

The morning of January 1, 2011, marked more than just New Year's Day at Republic Services. Don Slager, the company's longtime president and COO, stood before 300 field managers at the Phoenix headquarters. Behind him, a banner read "One Republic, One Standard." After James O'Connor's retirement following 12 years as CEO, Slager was taking the helm with a different vision: transform Republic from a holding company of acquisitions into a unified operating machine.

Slager embodied Republic's operational DNA. Starting as a regional manager in Michigan, he had spent 20 years perfecting the blocking and tackling of waste collection. His first act as CEO was telling: he mandated that every corporate executive spend one day per month in the field—riding routes, working at transfer stations, observing maintenance operations. "You can't manage what you don't understand," he declared. "And you can't understand this business from a spreadsheet."

The integration challenges from the Allied merger were staggering in scope. Republic operated 567 different IT systems, 45 different safety programs, and trucks running on 23 different maintenance schedules. Customer service calls were handled by 89 different call centers with no standard scripts. Some regions measured performance in revenue per truck, others in tons per route, making comparison impossible. Slager's mandate was ruthlessly simple: "One company, one system, one standard."

The technology transformation began with a $280 million investment in what Republic called "RISE"—Republic Integrated Service Excellence. Rather than buying off-the-shelf software, Republic built proprietary systems tailored to waste management's unique needs. Every truck received GPS tracking and onboard computers that captured real-time data on picks, weights, and route completion. This data fed into algorithmic route optimizers that reduced miles driven by 18% within two years.

The maintenance revolution deserves special attention. Republic's "One Fleet" initiative standardized the entire 17,000-vehicle fleet on just three chassis types and two body configurations. Parts inventory dropped from 45,000 SKUs to 12,000. Technician training was standardized across all 289 maintenance facilities. The result: vehicle uptime increased from 88% to 94%, while maintenance cost per mile dropped 22%. In an industry where trucks cost $350,000 each, keeping them running was worth hundreds of millions annually.

Safety became Slager's obsession, and for good reason—waste collection consistently ranks among America's most dangerous occupations. Republic implemented "SAFE" (Safety Awareness For Everyone), requiring every employee from CEO to helper to complete monthly safety training. Cameras were installed on every vehicle. Route observations increased from quarterly to weekly. The payoff was dramatic: OSHA recordable incidents dropped 65% between 2011 and 2015, saving $180 million in workers' compensation costs.

The customer service transformation was equally radical. Republic consolidated 89 call centers into three super-centers using cloud-based technology. Wait times dropped from 5 minutes to 90 seconds. First-call resolution increased from 67% to 89%. But the real innovation was proactive communication—using route GPS data to send customers automatic notifications about service delays or completions. Customer satisfaction scores rose 30 points while service costs dropped $45 million annually.

Republic's approach to recycling during this period revealed strategic sophistication. While competitors viewed recycling as a necessary evil with volatile commodity exposure, Republic saw opportunity. The company invested $500 million in state-of-the-art material recovery facilities (MRFs) with optical sorting technology that increased recovery rates from 65% to 85%. More importantly, Republic negotiated innovative contracts with municipalities that shared both upside and downside commodity risk, stabilizing margins even when recycling prices crashed.

The crown jewel of Republic's recycling investment was the North Las Vegas facility, opened in 2015. This $35 million, 110,000-square-foot plant could process two million pounds of recycled material daily—equivalent to 700,000 homes' worth of recycling. Solar panels generated enough energy to run the facility for two to three months annually. But the real innovation was automation: optical sorters, air classifiers, and magnetic separators reduced labor needs by 60% while improving sort quality.

Financial discipline under Slager was remarkable. Despite investing over $1 billion in technology and infrastructure, Republic actually reduced net debt from $7.5 billion to $6.8 billion between 2011 and 2015. Free cash flow generation averaged $1.1 billion annually—a 12% yield on the stock price. The company returned $3.2 billion to shareholders through dividends and buybacks while maintaining investment-grade credit ratings.

The operational improvements translated directly to financial performance. EBITDA margins expanded from 28% to 31% despite a challenging pricing environment. Return on invested capital increased from 8% to 11%. Most impressively, Republic generated these returns while growing revenue only 2% annually—proving that operational excellence could create value even without rapid growth.

By 2015, Republic had achieved something remarkable: it had successfully transformed from a roll-up of acquisitions into a unified operating company. Same-store revenue grew faster than inflation for 20 consecutive quarters. Customer retention reached 95%. Employee turnover dropped to 15%, exceptional in an industry averaging 25%. The company operated with the efficiency of a manufacturer but the local presence of a service business.

The transformation wasn't without costs. Republic's relentless standardization frustrated some longtime employees who preferred Allied's entrepreneurial culture. Several high-performing regional managers left for competitors. Some customers complained that Republic had become too corporate, losing the personal touch of local haulers. But the numbers validated Slager's approach: Republic's stock price rose from $25 to $42 between 2011 and 2015, generating 14% annual returns.

As 2015 ended, Slager faced a new challenge. Operational excellence had taken Republic as far as it could go. Margins were optimized, costs were controlled, and service quality was exceptional. But investors and stakeholders increasingly demanded something more: environmental leadership. The next phase of Republic's evolution would require balancing profitability with purpose—turning a waste company into a sustainability leader.

VI. The Sustainability Pivot & ESG Leadership (2014–2021)

The boardroom at Republic's Scottsdale headquarters was unusually tense on a February morning in 2014. Don Slager had just proposed something that would have been unthinkable five years earlier: committing Republic to aggressive sustainability targets that would require hundreds of millions in investment with uncertain returns. "We're a garbage company," one director pushed back. "Our job is to collect trash efficiently, not save the planet." Slager's response would define Republic's next chapter: "What if being a garbage company means we're uniquely positioned to lead on sustainability? We touch more materials destined for disposal than anyone except Waste Management. We can either be part of the problem or part of the solution."

The sustainability commitments Republic announced in 2014 were audacious for a traditional waste company. By 2018, Republic pledged to reduce fleet emissions by 3%, increase renewable energy generation from landfills by 50%, and achieve an injury rate 25% better than industry average. These might sound modest, but in the capital-intensive waste industry, they required fundamental operational changes and massive investment.

The "Blue Planet" initiative, launched in 2015, became Republic's sustainability brand. Rather than treating environmental goals as compliance costs, Republic positioned them as business opportunities. The logic was compelling: sustainable practices reduced operating costs (fuel efficiency), created new revenue streams (renewable natural gas), improved employee retention (safety focus), and attracted ESG-focused investors who would pay premium multiples.

Republic's landfill gas-to-energy program exemplified this approach. Decomposing waste in landfills produces methane, a greenhouse gas 28 times more potent than CO2. While competitors simply flared this gas to meet EPA requirements, Republic invested $200 million in capture systems that converted methane into renewable natural gas (RNG). By 2016, Republic operated 69 landfill gas projects generating enough renewable energy to power 400,000 homes annually.

The Dow Jones Sustainability Index recognition in 2016 validated Republic's transformation. Scoring in the 90th percentile, Republic became the only recycling and solid waste provider included in the DJSI World Index. This wasn't just a trophy for the PR department—it unlocked access to $12 trillion in ESG-focused investment capital and reduced Republic's cost of capital by an estimated 30 basis points.

The sustainability push created unexpected innovation. Republic's engineers developed a proprietary "well field optimization" system that increased landfill gas capture rates from 75% to 92%. This not only reduced emissions but generated an additional $45 million in annual RNG revenue. The company also pioneered "bioreactor landfills" that accelerated decomposition, allowing Republic to extract more gas faster while extending landfill life by 15%.

Employee safety, framed as human sustainability, became a cornerstone of the ESG strategy. Republic's "Mission to Zero" aimed for zero employee fatalities—ambitious in an industry averaging 30 deaths annually. The company invested $150 million in collision avoidance systems, backup cameras, and automated lifting mechanisms. Driver training increased from 40 to 80 hours annually. The result: Republic achieved two consecutive years with zero employee fatalities, unprecedented in waste management.

The circular economy presented both opportunity and challenge. Republic invested $300 million in advanced recycling infrastructure, including optical sorters that could identify and separate seven types of plastic. But China's 2018 "National Sword" policy, banning imports of contaminated recyclables, crashed commodity prices and threatened the economics of recycling. Republic's response was strategic: instead of abandoning recycling like some competitors, the company pushed for "producer responsibility" legislation requiring manufacturers to subsidize recycling costs.

The renewable natural gas joint venture with BP in 2021 marked Republic's most ambitious sustainability play. BP committed $500 million to develop RNG projects at Republic's landfills, with plans to produce 500 million cubic feet of RNG annually by 2025. The deal structure was innovative: BP provided capital and marketing expertise while Republic contributed landfill access and operational knowledge. Projected returns exceeded 15% IRR with 20-year contracted revenues.

Climate leadership created tension with profitability, particularly in fleet transformation. Electric garbage trucks cost $550,000 versus $350,000 for diesel equivalents, with unproven reliability and limited range. Republic's solution was pragmatic: test EVs in specific applications (residential routes under 40 miles) while investing in compressed natural gas (CNG) vehicles for longer routes. By 2021, 20% of Republic's fleet ran on alternative fuels, reducing emissions by 15% while maintaining operational efficiency.

The sustainability reporting revolution Republic led deserves recognition. While competitors published vague environmental commitments, Republic introduced science-based targets with quarterly progress updates. The company's 2020 sustainability report included 200 pages of detailed metrics, from water usage per ton collected to diversity statistics by job category. This transparency attracted ESG investors who now owned 35% of Republic's shares, up from 15% in 2014.

Financial performance during the sustainability pivot surprised skeptics. Between 2014 and 2021, Republic's EBITDA margins remained stable at 31% despite sustainability investments. Return on equity actually increased from 15% to 18% as ESG initiatives reduced operating costs and attracted premium pricing. The stock price rose from $42 to $110, generating 15% annual returns and outperforming the S&P 500 by 300 basis points.

The cultural transformation was equally significant. Employee engagement scores increased 20 points as workers took pride in Republic's environmental leadership. Recruitment improved dramatically—MIT and Stanford MBAs who would never consider working for a "garbage company" now viewed Republic as an environmental solutions provider. Customer retention in commercial segments reached 97% as businesses sought suppliers aligned with their own ESG goals.

By 2021, Republic had successfully repositioned itself from waste collector to sustainability leader. The company diverted 45 million tons from landfills through recycling and composting, generated 3,800 gigawatt-hours of renewable energy, and avoided 15 million metric tons of CO2 emissions. These weren't just statistics for annual reports—they represented a fundamental reimagining of what a waste company could be.

As Don Slager prepared to retire and hand leadership to Jon Vander Ark, Republic faced a new challenge. Sustainability credentials were now table stakes—every major waste company claimed environmental leadership. The next phase would require moving beyond traditional waste services into higher-margin environmental solutions. Republic's answer would be its boldest transformation yet.

VII. The Environmental Solutions Expansion (2022–Present)

Jon Vander Ark's first shareholder meeting as CEO in May 2021 opened with an unusual video: hazmat-suited technicians carefully extracting contaminated soil from a Superfund site, specialized trucks treating PFAS-contaminated water, and emergency response teams managing a chemical spill. "This," Vander Ark declared, "is Republic's next $5 billion opportunity. We're not just a waste company anymore—we're becoming America's partner for every environmental challenge."

Vander Ark brought a different perspective from his predecessors. An engineer by training who had run Republic's recycling division, he understood that traditional waste management was becoming commoditized. Municipal solid waste volumes were growing only 1% annually, recycling faced structural headwinds, and pricing power was limited by long-term contracts. Meanwhile, environmental remediation, hazardous waste management, and specialized treatment services were growing 8-10% annually with 40% EBITDA margins—double Republic's traditional business.

The US Ecology acquisition in May 2022 for $2.2 billion was Vander Ark's statement of intent. US Ecology wasn't just another waste hauler—it was a specialized environmental services provider with capabilities Republic had never possessed: 21 treatment and disposal facilities for hazardous waste, emergency response teams for chemical spills, and expertise in radioactive waste management. The price—14x EBITDA—raised eyebrows, but Vander Ark saw what others missed: access to a $15 billion addressable market growing twice as fast as traditional waste.

The integration of US Ecology revealed Republic's evolved M&A capability. Rather than forcing standardization like previous acquisitions, Republic maintained US Ecology's specialized teams and systems while providing capital and commercial support. Republic's 14,000 commercial customers became a sales channel for environmental services, while US Ecology's technical expertise enhanced Republic's capabilities. Within six months, cross-selling generated $50 million in new revenue—validating the strategic logic.

The ACV Enviro acquisition for $600 million further expanded Republic's environmental solutions footprint. ACV brought expertise in industrial cleaning, waste treatment, and site remediation across the Gulf Coast's petrochemical corridor. Combined with US Ecology, Republic now offered end-to-end environmental services: from emergency response through treatment and disposal. No other waste company could match this integrated capability.

Republic's polymer recycling initiative represented a different type of expansion—vertical integration into chemical recycling. The first Polymer Center, opened in 2023, used advanced pyrolysis technology to break down plastics into chemical feedstocks rather than mechanical recycling. This $95 million facility could process 100 million pounds of plastic annually, converting materials that traditional recycling couldn't handle into virgin-quality polymers. With plans for five facilities by 2027, Republic aimed to capture $500 million in high-margin revenue from brands desperate for recycled content.

The EV fleet transformation accelerated under Vander Ark, despite daunting economics. Republic committed to making 50% of all truck purchases electric by 2028—requiring $2 billion in capital investment. The math initially looked terrible: EV trucks cost 60% more than diesel, required charging infrastructure, and had unproven reliability. But Republic's analysis went deeper: including fuel savings, maintenance reduction, and regulatory credits, the total cost of ownership would reach parity by 2026. More importantly, major customers like Amazon and Microsoft were demanding zero-emission service providers.PFAS treatment emerged as Republic's newest frontier. With over 70 years of experience providing environmental solutions and significant federal funding available through the Infrastructure Investment and Jobs Act, Republic positioned itself as the industry leader with technology and expertise to address PFAS hazardous waste needs. The company developed comprehensive solutions including secure disposal at Subtitle C landfills in Grand View, Idaho and Beatty, Nevada, offering RCRA-compliant design with natural protections of remote desert locations with negative annual net precipitation. This capability positioned Republic uniquely as companies advertised their Subtitle C landfills as ideal PFAS disposal options, capturing premium pricing for managing these "forever chemicals" that traditional landfills couldn't safely handle. The digital transformation under Vander Ark represents the culmination of decades of operational evolution. Republic's MPower and RISE platforms have driven significant value—these digital tools have led to significant cost savings and incremental revenue, enhancing operational efficiency. The company's customer-centric approach yielded impressive results, with a strong customer retention rate of over 94% and favorable trends in net promoter scores.

Looking ahead to 2025, Republic's guidance reflects confidence in its diversified strategy. The company expects projected revenue between $16.850 billion and $16.950 billion and adjusted EPS ranging from $6.82 to $6.90. Sustainability investments are becoming material contributors, with polymer centers and RNG plants expected to contribute $70 million in incremental revenue and $35 million in EBITDA in 2025. The company plans to invest at least $1 billion in value-creating acquisitions, continuing its disciplined M&A approach that has defined its growth strategy for nearly three decades.

The transformation from a waste hauler to an environmental solutions provider is nearly complete. Republic now offers capabilities that would have been unimaginable in Huizenga's era: treating PFAS-contaminated materials, converting plastics into chemical feedstocks, and operating one of the nation's largest clean-energy vehicle fleets. As Vander Ark noted in the latest earnings call, Republic isn't just collecting garbage anymore—it's solving America's most complex environmental challenges while generating superior returns for shareholders.

VIII. Business Model & Competitive Advantages

Stand at the edge of Republic's Apex Regional Landfill in Las Vegas at sunrise, and you'll witness the choreography of modern waste management. A continuous stream of collection trucks, transfer trailers, and commercial vehicles navigate the 2,200-acre site with GPS-guided precision. Beneath this operational ballet lies one of corporate America's most underappreciated business models—a network effect so powerful that new entrants face essentially insurmountable barriers.

Republic operates 367 collection operations, 248 transfer stations, 75 recycling centers, and 208 active landfills. This isn't just infrastructure—it's an integrated ecosystem where each component reinforces the others. Collection routes feed transfer stations, which consolidate waste for efficient transport to company-owned landfills, which generate tipping fees from competitors lacking disposal capacity. The recycling centers and environmental solutions facilities add higher-margin revenue streams while serving the same customer base.

The economics of route density drive everything in waste management. Consider a typical residential neighborhood: Republic might serve 60% of homes on a street. Adding the remaining 40% doesn't require additional trucks or drivers—just more stops on existing routes. This incremental density can boost route profitability by 40-50%. Now multiply this effect across thousands of routes, and you understand why market share translates directly to margin expansion.

Landfill ownership represents Republic's most durable competitive moat. With environmental regulations making new landfill permits nearly impossible to obtain in most markets, Republic's 208 active sites with average remaining capacity of 35 years are essentially irreplaceable assets. These facilities not only provide guaranteed disposal capacity for Republic's collection operations but also generate high-margin tipping fees—typically $45-65 per ton—from competitors forced to use Republic's facilities. In markets where Republic owns the only permitted landfill within economic hauling distance, the company possesses pricing power that would make a software company jealous.

The contract structure in waste management creates remarkable revenue visibility. Commercial customers typically sign multi-year agreements with automatic renewal clauses and CPI-based price escalators. Municipal contracts often span 5-10 years with built-in rate adjustments. Even residential service, while technically month-to-month, exhibits 95%+ annual retention rates because switching providers requires effort for minimal potential savings. This contractual stickiness generates the predictable cash flows that enable Republic to invest confidently in long-term infrastructure.

Bill Gates's Cascade Investment emerged as Republic's largest shareholder, owning 35.1% of outstanding shares—a $27 billion stake that represents one of the portfolio's largest positions. Gates's investment thesis reflects Republic's unique characteristics: recession-resistant demand, inflation-protected pricing, and secular tailwinds from environmental regulations. Cascade has maintained or increased its position for over a decade, viewing Republic as a permanent holding rather than a trade.

Republic's capital allocation framework balances growth investment with shareholder returns. The company targets 10-12% of revenue for capital expenditures, primarily for fleet replacement and landfill development. Another 3-4% goes toward tuck-in acquisitions that enhance route density or add disposal capacity. The remaining free cash flow—typically $2+ billion annually—funds dividends (2.0% yield) and share repurchases. This disciplined approach has generated 18.62% return on equity while maintaining leverage around 2.5x EBITDA.

The operational leverage in Republic's model is subtle but powerful. Fixed costs—management, facilities, permits—are spread across growing revenue base. Variable costs are largely controllable: labor through route optimization, fuel through hedging and alternative vehicles, maintenance through fleet standardization. As revenue grows from price increases and modest volume gains, incremential margins can exceed 40%. This operating leverage explains how Republic expanded EBITDA margins from 24% to 31% despite relatively modest top-line growth.

Network effects manifest in multiple ways. Dense route networks enable Republic to offer more frequent service at lower cost. Control of disposal assets allows Republic to internalize the full waste value chain. Scale purchasing power reduces costs for everything from trucks to insurance. Digital investments—route optimization, customer portals, predictive maintenance—can be amortized across a massive operational base. These cumulative advantages create a widening moat that smaller competitors cannot replicate.

The competitive dynamics in waste management favor incumbents overwhelmingly. Starting a new waste company requires massive capital (trucks cost $350,000 each), regulatory approvals (often taking years), disposal access (controlled by incumbents), and route density (built over decades). Republic's returns on incremental capital consistently exceed 15% because the company is essentially adding revenue to a fixed-cost network already at scale.

Republic's business model elegance lies in its simplicity. Provide an essential service that everyone needs, build dense route networks that create cost advantages, control scarce disposal assets that competitors must access, and use predictable cash flows to compound shareholder value. It's a formula that has worked for decades and shows no signs of disruption. While Silicon Valley chases the next breakthrough, Republic quietly generates $2 billion in free cash flow by picking up garbage—proving that sometimes the best business models are hiding in plain sight.

IX. Playbook: Lessons from Building a Waste Empire

The Republic Services conference room in Phoenix displays a simple chart that executives show every visitor: industry structure in 1995 versus today. Three decades ago, waste management was fragmented across 10,000+ operators. Today, four companies control 55% of the market. Republic's transformation from bit player to the architect of this consolidation offers a masterclass in building dominance in unglamorous industries.

The roll-up strategy that built Republic wasn't about financial engineering—it was about operational integration. While failed roll-ups in other industries collapsed under acquisition debt and cultural conflicts, Republic developed a replicable integration playbook that turned acquisitions into earnings within 100 days. The key insight: standardize everything that doesn't touch the customer, but maintain local relationships and market knowledge. This balance allowed Republic to achieve the efficiency of scale while preserving the service quality of local operators.

Operational excellence in commodity businesses requires a different mindset than technology or consumer companies pursue. Republic couldn't differentiate on product—garbage is garbage—so it competed on reliability, efficiency, and cost. The company's maniacal focus on metrics like picks per hour, vehicle uptime, and route completion rates might seem mundane, but improving each metric by single-digit percentages translated to hundreds of millions in profit. Excellence came not from breakthrough innovation but from thousands of incremental improvements compounded over decades.

Republic's approach to regulatory complexity transformed a burden into competitive advantage. While smaller operators viewed environmental regulations as costly compliance requirements, Republic saw opportunity. The company invested ahead of regulatory requirements, turning compliance into barriers that prevented new competition. When EPA mandated new landfill liner standards, Republic had already upgraded its facilities. When emissions regulations tightened, Republic's fleet was already transitioning to cleaner fuels. This proactive approach not only avoided regulatory penalties but positioned Republic as the partner of choice for municipalities seeking compliant operators.

The transition from pure waste collection to environmental services required careful sequencing. Republic couldn't abandon its core business, which generated the cash flow funding transformation. Instead, the company layered new capabilities onto existing operations. Recycling facilities were added to transfer stations. Hazardous waste expertise was acquired and integrated with traditional collection. Renewable energy projects were developed at existing landfills. Each addition leveraged existing assets and relationships while expanding addressable markets.

Building sustainability credentials while maintaining margins challenged Republic to reframe environmental initiatives as business opportunities rather than cost centers. Landfill gas projects generated new revenue streams. Route optimization reduced fuel costs while cutting emissions. Safety programs decreased insurance expenses while improving Republic's employer brand. The lesson: sustainability and profitability aren't mutually exclusive if initiatives are designed with both objectives from inception.

The power of route density cannot be overstated in Republic's success. Every strategic decision—acquisitions, customer targeting, facility locations—was evaluated through the density lens. Republic would pay premium multiples for small competitors operating adjacent routes but pass on larger deals in new markets. This discipline, maintained over decades, created local monopolies within broader competitive markets. A Republic executive explained it simply: "We'd rather own 80% of Tucson than 20% of four cities."

Republic's cultural transformation from holding company to operating company required deliberate change management. The company couldn't simply mandate standardization—it had to demonstrate value to field operators accustomed to autonomy. Republic created "Pioneer Teams" of respected field managers who developed new processes, ensuring buy-in from peers. Corporate executives spent mandatory time in the field, building credibility with frontline employees. Change was positioned not as corporate interference but as sharing best practices across regions.

The M&A integration excellence that Republic developed became a sustainable competitive advantage. While competitors struggled to merge operations, Republic could evaluate, negotiate, and integrate acquisitions faster than rivals. The company maintained standing integration teams that could begin implementation within days of deal announcement. Republic's reputation for smooth integrations made it the buyer of choice for family-owned operators seeking exits—often accepting lower prices for the certainty of Republic's execution.

Technology adoption in Republic's traditional industry required careful change management. Rather than forcing digital transformation, Republic introduced technology that made employees' jobs easier. Route optimization meant drivers finished earlier. Predictive maintenance prevented breakdown frustrations. Customer portals reduced service calls. By focusing on employee benefits rather than cost reduction, Republic achieved technology adoption rates that exceeded software companies' benchmarks.

The durability of Republic's model offers lessons for building lasting enterprises. Rather than chasing growth, Republic focused on returns. Instead of pursuing glamorous markets, it dominated essential services. While competitors leveraged aggressively, Republic maintained financial discipline. The company's boring consistency—6% annual revenue growth, 30% EBITDA margins, 15% returns on capital—created more value than any moonshot strategy could achieve. Sometimes the best business strategy is doing the obvious exceptionally well, year after year, while others chase shiny objects.

X. Analysis & Investment Case

Republic Services achieved net income of $512 million, or $1.63 per diluted share, for Q4 2024, demonstrating the earnings power of America's second-largest waste management company. The investment case for Republic rests on three pillars: structural industry advantages, company-specific competitive positioning, and emerging environmental solutions opportunities that could transform the company's multiple.

The waste management industry structure creates an oligopoly with rational competition. Four companies—Waste Management, Republic, Waste Connections, and GFL Environmental—control over 55% of the $85 billion U.S. market. This concentration enables pricing discipline, with annual price increases consistently exceeding inflation. Unlike industries disrupted by technology, waste management's physical infrastructure requirements, regulatory complexity, and local market dynamics create insurmountable barriers to new entrants.

Republic achieved a 7.1% increase in total revenue and a 15.2% rise in adjusted EPS to $6.46 in 2024, with adjusted EBITDA margin expanding by 140 basis points to 31.1%. This margin expansion during a period of elevated inflation demonstrates pricing power and operational leverage. Return on equity at 18.62% significantly exceeds the cost of capital, indicating value creation even in a mature industry.

Republic's competitive positioning versus peers reveals both strengths and opportunities. Waste Management remains the largest player with superior scale, but Republic's operational metrics often exceed the industry leader. Republic's safety record, customer retention rates, and margin expansion have consistently outperformed. Waste Connections operates with a more decentralized model that achieves higher margins (32% vs Republic's 31%) but lacks Republic's systematic approach to technology and sustainability. GFL Environmental, the aggressive Canadian entrant, pursues growth through leverage that Republic has explicitly avoided.

The ESG tailwinds supporting Republic are strengthening. Corporate customers increasingly demand zero-waste solutions and renewable energy. Municipalities require operators that can meet stringent environmental standards. Investors allocate capital based on sustainability metrics where Republic excels. These trends create pricing premiums for environmentally-focused operators and barriers for traditional competitors. Republic's positioning as an environmental solutions provider rather than waste hauler captures these premiums.

The bear case for Republic centers on three concerns. First, recycling economics remain challenged, with commodity prices volatile and contamination rates rising. China's import ban destroyed the historical recycling model, forcing Republic to subsidize operations that previously generated profits. Second, competition for municipal contracts has intensified as cities seek cost savings, potentially pressuring margins. Third, technological disruption—autonomous vehicles, waste-to-energy innovations, zero-waste initiatives—could theoretically challenge Republic's model, though practical impacts remain distant.

The recycling challenge deserves deeper analysis. Republic processes 5 million tons of recyclables annually, but commodity revenues cover only 60-70% of processing costs. The company has responded by restructuring contracts to share commodity risk with municipalities and investing in technology that improves sort quality. Long-term, producer responsibility legislation could shift costs to manufacturers, but near-term headwinds persist.

The bull case for Republic rests on multiple expansion drivers. Essential service characteristics—everyone generates waste regardless of economic conditions—provide recession resistance that commands premium valuations. Pricing power from oligopolistic industry structure and long-term contracts with escalators ensures revenue growth exceeds inflation. The sustainability transition opens new high-margin revenue streams in environmental solutions, renewable energy, and circular economy services that justify higher multiples.

Republic trades at 11x EV/EBITDA versus historical averages of 10x and Waste Management at 12x. This discount seems unjustified given Republic's superior organic growth, margin expansion trajectory, and environmental solutions optionality. Applying Waste Management's multiple to Republic suggests 20% upside. If environmental solutions achieve management's targets, warranting a 13x multiple similar to environmental services peers, the upside exceeds 30%.

The capital allocation priorities enhance the investment case. Republic generates $2+ billion in annual free cash flow—a 6% yield on market cap. Management commits to returning substantially all free cash flow to shareholders through dividends (2% yield) and buybacks (4% of shares annually). This shareholder-friendly approach provides downside protection while maintaining growth investments.

Near-term catalysts could drive rerating. Integration of recent environmental solutions acquisitions should accelerate margin expansion. Polymer recycling facilities coming online in 2025-2026 will demonstrate circular economy capabilities. Renewable natural gas projects with BP will generate visible high-margin revenue growth. Producer responsibility legislation advancing in multiple states could transform recycling economics. Any of these could trigger multiple expansion.

The risk/reward for Republic appears favorable for long-term investors. Downside seems limited given essential service characteristics, strong free cash flow generation, and reasonable valuation. Upside from multiple expansion, environmental solutions growth, and continued operational improvements could generate 15%+ annual returns. While not without challenges, Republic offers a rare combination of defensive characteristics and growth optionality that warrants consideration in any portfolio.

XI. Epilogue & "What Would We Do?"

Imagine Republic Services in 2035. Autonomous collection vehicles navigate optimized routes while customers track service through augmented reality apps. Landfills have transformed into resource recovery centers where sophisticated sorting systems extract valuable materials and bioreactors generate renewable chemicals. Republic's environmental solutions division, larger than today's entire company, manages corporate sustainability programs end-to-end. The company that once just picked up trash has become America's circular economy infrastructure.

The future of waste presents a fundamental paradox: society increasingly demands zero waste while generating more refuse than ever. Americans produce 4.5 pounds of waste daily, up from 3.5 pounds in 1990, despite heightened environmental awareness. E-commerce drives packaging proliferation. Construction booms create demolition debris. The "zero waste" aspiration confronts the reality that modern life generates massive material flows requiring management. Republic's opportunity lies not in waste elimination but in waste transformation—converting liability into resource.

Technology disruption in waste management will likely enhance incumbents rather than displace them. Artificial intelligence optimizing collection routes saves millions but requires massive route networks to generate returns. Autonomous trucks reduce labor costs but demand capital that only scaled operators possess. Robotic sorting systems improve recycling economics but need volume throughput that only major facilities achieve. Unlike software where startups can disrupt giants, waste management's physical infrastructure and regulatory requirements favor established players adopting new technology.

If we were running Republic, we'd pursue three strategic initiatives. First, accelerate the environmental solutions expansion through larger acquisitions. The fragmented hazardous waste and industrial services markets offer consolidation opportunities at reasonable multiples. Republic's balance sheet could support $5-10 billion in strategic M&A while maintaining investment-grade ratings. Second, develop comprehensive circular economy solutions for major corporate customers. Partner with consumer brands to design packaging for recyclability, manage take-back programs, and guarantee recycled content supply. These integrated partnerships would generate stickier relationships and premium pricing. Third, aggressively pursue international expansion in developed markets with similar industry structures. Canada, Australia, and the UK offer oligopolistic markets where Republic's operational excellence would translate directly.

The international opportunity deserves emphasis. Republic's domestic focus contrasts with Waste Management's selective international presence and smaller peers' cross-border operations. Yet Republic's capabilities—operational excellence, technology systems, environmental solutions—would transfer seamlessly to markets with similar regulatory frameworks. A transformative acquisition in Canada or Australia could add 20% to Republic's revenue while maintaining return thresholds.

Climate regulations present upside optionality that markets underappreciate. Carbon pricing would make Republic's renewable natural gas more valuable. Extended producer responsibility would shift recycling costs to manufacturers. Landfill methane capture mandates would disadvantage smaller operators. Zero-emission vehicle requirements would favor Republic's early EV investments. Each regulation tightens Republic's competitive moat while creating new revenue opportunities.

The consolidation endgame in waste management points toward a 3-4 player oligopoly controlling 70%+ market share. Republic and Waste Management will likely acquire Waste Connections and GFL Environmental as founders retire or debt burdens force sales. Antitrust concerns seem manageable given local market fragmentation and essential service nature. The resulting industry structure—similar to railways or utilities—would enable consistent price increases, margin expansion, and shareholder returns for decades.

Republic's transformation from Huizenga's roll-up vehicle to environmental solutions leader demonstrates how traditional industries can reinvent themselves without abandoning core strengths. The company maintained operational discipline while adapting to societal demands for sustainability. It preserved shareholder returns while investing in transformation. Most importantly, Republic proved that companies in unglamorous industries can generate exceptional returns through execution rather than innovation.

The ultimate lesson from Republic's journey is that business success doesn't require breakthrough technology or category creation. Sometimes the best opportunities hide in essential services everyone needs but nobody wants to think about. Republic built an empire on trash by recognizing that waste isn't going away—it's only becoming more complex to manage. As environmental challenges intensify and regulations tighten, Republic's combination of operational excellence and environmental capabilities positions it to thrive for decades ahead.

Looking forward, Republic Services stands at an inflection point. The core waste business remains robust with predictable growth and strong returns. The environmental solutions expansion offers higher growth and margins. The sustainability transition creates competitive advantages and customer stickiness. For investors seeking defensive growth with ESG credentials, Republic offers a compelling proposition. The company that turned garbage into gold has plenty more value to create.

XII. Recent News

Jon Vander Ark, president and chief executive officer, noted: "We delivered another strong year of results in 2024, made possible by effectively executing our strategy designed to meet the needs of our customers and profitably grow the business. We exceeded expectations and generated double-digit growth in EBITDA, earnings and free cash flow, and expanded adjusted EBITDA margin by 140 basis points during the year"

Q4 2024 total revenue growth of 5.6 percent includes 4.3 percent organic growth and 1.3 percent growth from acquisitions. Core price on total revenue increased revenue by 6.1 percent. Core price on related business revenue increased revenue by 7.3 percent, which consisted of 9.1 percent in the open market and 4.5 percent in the restricted portion of the business

Excluding certain expenses and other items, on an adjusted basis, net income for the three months ended December 31, 2024, was $497 million, or $1.58 per diluted share, versus $446 million, or $1.41 per diluted share, for the comparable 2023 period

Republic generated Cash Flow from Operations of $3.94 Billion and Adjusted Free Cash Flow of $2.18 Billion in 2024

The Q4 2024 earnings demonstrated Republic's resilient business model despite macroeconomic headwinds. Organic volume on total revenue declined by 1.2% in the fourth quarter, primarily due to shedding underperforming contracts and softness in construction and manufacturing markets. However, pricing power remained intact, with core price increases more than offsetting volume declines.

Looking ahead to 2025, management provided confident guidance despite anticipated challenges. The company anticipates a headwind from recycled commodity prices, with a $20 million impact on EBITDA due to lower average prices compared to the previous year. Republic Services expects a modest margin expansion in 2025, with some headwinds from deal integration costs and the absence of CNG tax credits

The acquisition pipeline remains robust, with the company planning to invest at least $1 billion in value-creating acquisitions in 2025. This continued M&A activity, combined with operational improvements and sustainability initiatives, positions Republic for sustained growth despite near-term market softness.

XIII. Links & Resources

Official Resources: - Republic Services Investor Relations: investor.republicservices.com - Annual Reports & SEC Filings: investor.republicservices.com/financials - Sustainability Reports: republicservices.com/sustainability - Q4 2024 Earnings Presentation: investor.republicservices.com/events

Industry Analysis: - EPA Waste Management Data: epa.gov/facts-and-figures-about-materials-waste-and-recycling - National Waste & Recycling Association: wasterecycling.org - Solid Waste Association of North America: swana.org - Environmental Research & Education Foundation: erefdn.org

Books & Long-Form Reading: - "Waste: One Woman's Fight Against America's Dirty Secret" by Catherine Coleman Flowers - "Garbology: Our Dirty Love Affair with Trash" by Edward Humes - "The Waste Makers" by Vance Packard - "Junkyard Planet" by Adam Minter

Documentary Recommendations: - "Waste Land" (2010) - Examination of world's largest landfill - "Trashed" (2012) - Jeremy Irons investigation of global waste - "The Human Element" (2018) - Environmental impact documentary - "Plastic Wars" (2020 PBS Frontline) - Recycling industry investigation

Regulatory & Compliance Resources: - EPA RCRA Regulations: epa.gov/rcra - State Environmental Agencies: epa.gov/home/health-and-environmental-agencies-us-states-and-territories - OSHA Waste Industry Guidelines: osha.gov/waste - DOT Hazardous Materials Regulations: phmsa.dot.gov

Competitor Resources: - Waste Management (WM): investors.wm.com - Waste Connections (WCN): wasteconnections.com/investors - GFL Environmental: gflenv.com/investors - Casella Waste Systems: casella.com/investors

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube