United Parcel Service: From Seattle Messenger Boys to Global Logistics Giant

I. Introduction & Episode Teaser

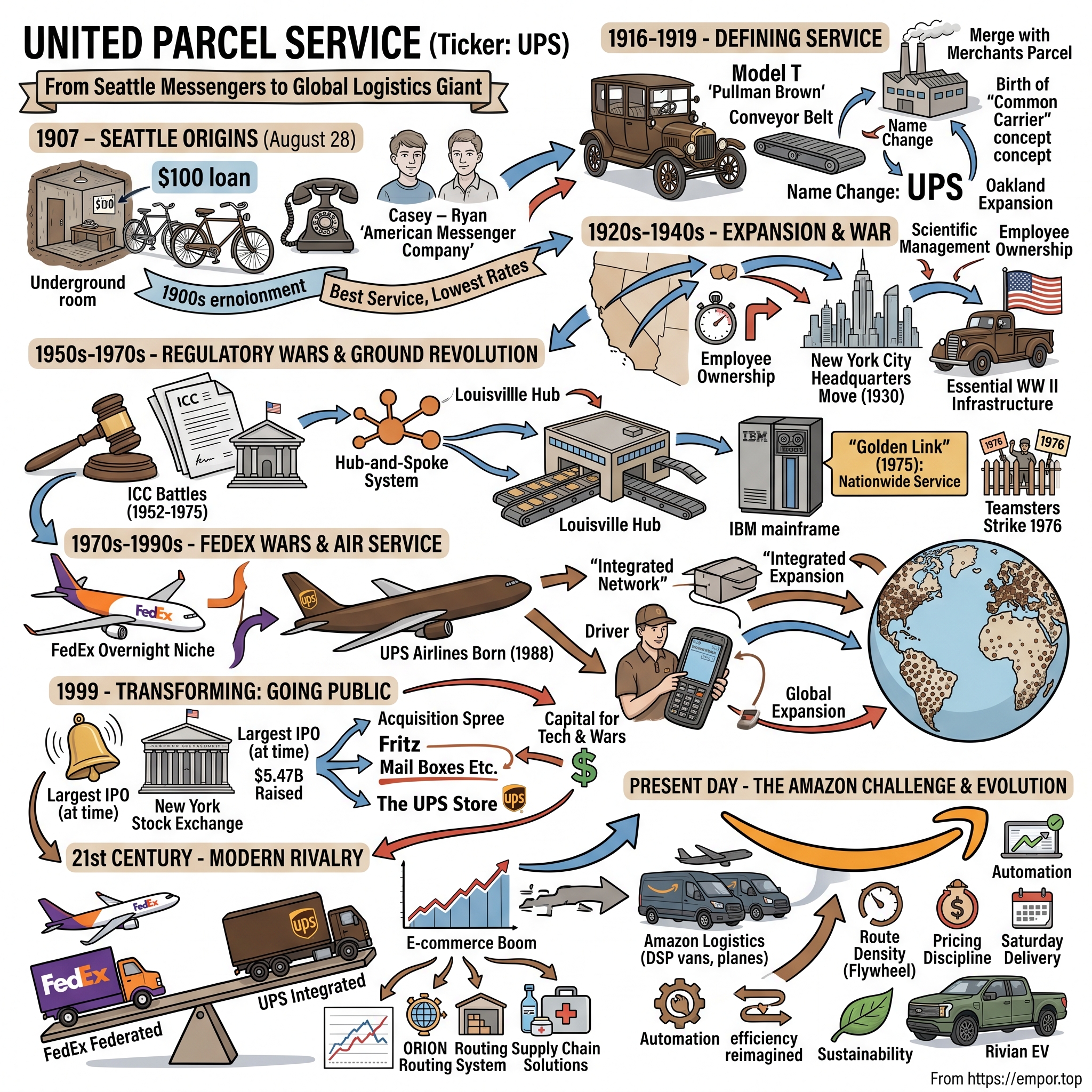

Picture this: August 28, 1907, beneath a Seattle saloon, in a cramped 6-by-17-foot basement that reeked of stale beer and damp wood. Two teenagers—James Casey, 19, and Claude Ryan, 18—are counting out borrowed bills on a makeshift desk. They have exactly $100 in debt capital, two bicycles, and a telephone. Their business plan? Run messages and packages across Seattle faster than anyone else.

Casey's hands are already calloused from six years of working odd jobs since his father died in the Alaskan gold fields. He's been the family breadwinner since age 11. Ryan's the talker, the one who convinced a local shop owner to loan them the hundred bucks. Together, they're about to build what becomes the world's largest package delivery company—a business that will one day generate $100 billion in annual revenue and deliver 6.5 billion packages a year.

The puzzle at the heart of this story isn't just how two broke teenagers built UPS into a global logistics colossus worth over $150 billion. It's how they created something even more valuable: a culture so distinctive and durable that it survived 117 years, multiple technological revolutions, and the rise of competitors who moved faster, flew higher, and spent more. While Federal Express would later capture imaginations with overnight delivery and Amazon would threaten to eat the entire industry, UPS kept doing what it always did—showing up, every day, in those brown trucks, delivering more packages on the ground than anyone else on Earth.

This is a story about operational excellence taken to an almost religious extreme. About strategic patience in an impatient world. About how network effects compound over a century. And ultimately, about how the least sexy business model in tech-obsessed capitalism—moving physical boxes from A to B—became one of the most defensible moats in business history.

The roadmap ahead takes us from that Seattle basement through the regulatory battles that nearly killed the company, into the overnight delivery wars with FedEx that defined modern logistics, through a late-in-life IPO that shocked Wall Street, and into today's three-way knife fight with Amazon and FedEx for the future of e-commerce delivery. Along the way, we'll discover why UPS drivers only make right turns, how the company accidentally invented modern venture capital, and why a business founded on bicycle delivery might be perfectly positioned for the age of autonomous vehicles.

II. The Casey & Ryan Origins: American Messenger Company (1907-1919)

James Edward Casey never intended to revolutionize global commerce. He just needed to eat. When his father died in 1897 during the Klondike gold rush—another Irish immigrant chasing fortune in frozen Alaska—eleven-year-old Jim became the man of the house. His mother, Annie, took in washing. Jim delivered groceries before school, worked at a department store after school, and spent weekends running messages for a telegraph company. By nineteen, he'd saved enough to dream bigger than subsistence.

The American Messenger Company, founded with Claude Ryan on August 28, 1907, wasn't Casey's first entrepreneurial venture—he'd already failed at a messenger service in Nevada. But Seattle in 1907 was different. The city was exploding from the Alaska gold rush aftermath, growing from 80,000 to 240,000 people in a single decade. Department stores were booming. Telephones existed but were rare—only 9% of Seattle homes had one. If you wanted to send a message, order from a store, or move a package across town, you needed a messenger.

Casey and Ryan's innovation wasn't the messenger service itself—Seattle had dozens of competitors. Their edge was treating it like a profession, not a hustle. Every messenger wore a uniform (unheard of at the time). Casey wrote a code of conduct that banned whistling, mandated courtesy, and required messengers to call customers "Mr." or "Mrs." regardless of social station. "Best service and lowest rates" became their motto, but Casey always emphasized the order—service first, then price.

The operation ran with military precision from that saloon basement. Casey worked the phones and dispatched riders. Ryan recruited messengers and handled the books. They guaranteed one-hour delivery anywhere in Seattle's business district for a nickel. But here's what separated them from every other messenger service: they hired carefully, promoted from within, and shared profits with employees. Casey believed that "owned managers make the best managers"—a philosophy that would shape UPS for the next century.

By 1913, the American Messenger Company had grown from two bicycles to six motorcycles and a Model T Ford—their first motorized delivery vehicle. That Ford wasn't just transportation; it was a statement. While competitors stuck to bikes and horses, Casey saw that the automobile would reshape American cities. He was already thinking beyond messages to packages, beyond Seattle to the nation.

The pivotal moment came in 1916 when Casey absorbed his main rival, Evert McCabe's Merchants Parcel Delivery. McCabe had been focusing on department store deliveries—a higher-margin business than messages. The merger created a company with 50 employees, four cars, and five motorcycles. More importantly, it gave Casey a vision: What if, instead of stores maintaining their own delivery fleets, one company handled all their packages? The efficiency gains would be enormous. Stores could focus on selling; Casey's company would handle the logistics.

This was the birth of the "common carrier" concept that would define UPS. Unlike contract carriers who worked exclusively for specific clients, a common carrier served everyone equally. It was a radical democratization of logistics—whether you were Nordstrom or a corner shop, you got the same brown truck, same uniformed driver, same reliable service.

In 1919, Casey made two decisions that transformed a regional messenger service into a national ambition. First, he changed the name to United Parcel Service—"United" suggesting a network that would eventually span the country, "Parcel" indicating the focus had shifted from messages to packages, and "Service" because that's what Casey believed they were really selling. Second, he expanded to Oakland, California, proving the model could work beyond Seattle.

But perhaps Casey's most enduring decision came in 1916: painting the trucks brown. The color was chosen for practical reasons—brown hid dirt and projected professionalism—but it became something more. "Pullman brown," as Casey called it (after the luxurious Pullman railroad cars), would become one of the most recognizable corporate colors in the world. A century later, UPS would trademark the exact shade and the phrase "What can Brown do for you?"

As the 1910s ended, United Parcel Service had 180 employees, operated in three cities, and had established the three pillars that would support it for the next century: obsessive operational efficiency, employee ownership culture, and the common carrier model. Casey was just getting started. The boy who'd lost his father to gold rush dreams was building something more valuable than gold—a network that would become essential infrastructure for American capitalism.

III. Building the Machine: Common Carrier & West Coast Expansion (1920s-1940s)

Charlie Soderstrom had a problem. The young UPS executive stood in a Los Angeles warehouse in 1922, staring at mountains of packages from competing department stores—Bullock's, Robinson's, The Broadway. Each store ran its own delivery trucks, most half-empty, crisscrossing the same neighborhoods. The inefficiency was maddening. Soderstrom had been sent from Seattle to expand UPS's newfound common carrier model, but Los Angeles retailers weren't buying it. Why outsource delivery when you'd always done it yourself?

Then Soderstrom had an idea that would define UPS's growth strategy for the next century: he didn't pitch efficiency or cost savings. He pitched reliability. "Give us your packages for one month," he told skeptical store managers. "If we miss a single delivery window, you pay nothing." It was a massive gamble—one that required UPS to be operationally perfect from day one in a new city. They pulled it off. Within six months, most major LA retailers had abandoned their private fleets for UPS's brown trucks.

The Los Angeles expansion marked UPS's evolution from a regional player to something more ambitious. In 1924, they unveiled an innovation that seems quaint now but was revolutionary then: a conveyor belt system for sorting packages. Designed by Casey and his engineers, the system could process 5,000 packages per hour—ten times faster than manual sorting. Competitors mocked it as over-engineering for a "simple delivery business." They didn't understand that Casey wasn't building a delivery business; he was building a machine.

The machine had human components too. In 1927, Casey instituted something radical: he gave stock to all employees, from drivers to clerks. Not options, not bonuses—actual equity. By 1930, employees owned 10% of the company. The ownership structure created an unusual dynamic. UPS employees didn't just work for the company; they were the company. This would have profound implications when labor unions came calling in the 1930s.

But the biggest strategic decision of the 1920s was also the most controversial inside UPS: the move from Seattle to New York City. Casey saw that the future of American commerce was shifting east. The retailers, manufacturers, and financial markets that would drive package volume were concentrated between Boston and Washington. In 1930, against the protests of Seattle old-timers who'd built the company, Casey moved headquarters to Manhattan and launched service in New York City.

New York was a different beast. The density was unprecedented—more packages per block than entire Seattle neighborhoods. The traffic was brutal. The competition was fierce. But Casey had a secret weapon: data. While competitors relied on intuition and experience, UPS time-studied every aspect of delivery. How long to walk from truck to doorway? 17 seconds on average. How to organize packages in the truck for maximum efficiency? By delivery sequence, heaviest on bottom. What was the optimal number of stops per route? 120-150, depending on density.

This obsession with measurement and optimization—what would later be called "scientific management"—reached absurd levels. UPS engineers calculated that left turns wasted time waiting for traffic, so they designed routes that were primarily right turns. They determined that drivers walking fast but not running optimized both speed and safety. They even standardized how drivers should hold their key rings (on the pinky finger, to avoid fumbling).

The Great Depression should have killed UPS. Package volumes plummeted 40% between 1929 and 1933. Competitors folded weekly. But Casey refused to lay off employees or cut wages. Instead, he used the downturn to invest. While others retreated, UPS expanded into Philadelphia, Chicago, and San Francisco. They modernized their fleet, standardized their processes, and deepened relationships with retailers desperate for any edge. When the economy recovered, UPS had doubled its market share.

World War II brought different challenges. Gas rationing crippled delivery operations. Young men who formed the backbone of the driver force were drafted. The government commandeered trucks for military use. Yet somehow, UPS thrived. They contracted with the military to deliver supplies to bases. They hired women as drivers for the first time—though Casey insisted they wear brown skirts, not pants. Most importantly, they became essential infrastructure for the war economy, moving everything from ration cards to aircraft parts.

By 1945, UPS operated in 16 major cities, employed 5,000 people, and had developed three competitive advantages that would prove insurmountable: First, network density—they had more pickup and delivery points than anyone else, creating a virtuous cycle where more volume meant more efficient routes. Second, operational excellence—their time-motion studies and standardized processes delivered 99.5% reliability when competitors averaged 95%. Third, and most importantly, culture—the combination of employee ownership, promote-from-within policies, and Casey's original service ethos created a workforce that saw themselves as partners, not workers.

The post-war boom was about to begin. Americans were moving to suburbs, buying cars, and shopping more than ever. The interstate highway system would soon connect every corner of the country. Television would create national brands requiring national distribution. Everything was aligned for explosive growth. But first, UPS would have to fight a two-decade regulatory war that would determine whether they could serve the entire country—or remain trapped in a handful of cities forever.

IV. The Ground Game Revolution: Territory Expansion (1950s-1970s)

The hearing room at the Interstate Commerce Commission was packed on a humid Washington morning in 1952. UPS lawyer Paul Grund stood before three stone-faced commissioners who held the company's future in their hands. For forty-five years, UPS had been confined to operating within individual cities. They could deliver packages throughout Los Angeles or Chicago, but couldn't carry a package between them. The regulatory walls that protected local trucking companies and railroads were about to face their first serious challenge.

"Gentlemen," Grund began, "American businesses are becoming national. Sears has 700 stores. JCPenney has 1,600. Yet our delivery system remains fragmented by city limits drawn in the horse-and-buggy era." One commissioner interrupted: "Mr. Grund, are you suggesting we should destroy thousands of small trucking companies so one Seattle company can monopolize package delivery?" The question hung in the air. It would take UPS twenty-three more years to fully answer it.

The regulatory battle that consumed UPS from 1952 to 1975 was fought state by state, sometimes city by city. Each expansion required proving to regulators that existing carriers were inadequate—without explicitly saying competitors were incompetent. It was a delicate dance. In Indiana, UPS spent three years and $500,000 in legal fees to win the right to deliver between Indianapolis and Fort Wayne—a mere 126 miles.

But Casey and his successor, George Smith, understood something regulators didn't: the future of retail was suburban shopping malls, not downtown department stores. By the 1950s, Americans were fleeing cities for suburbs, and stores were following. The old model of department store delivery trucks serving dense urban neighborhoods was breaking down. Suburban customers drove to malls, shopped at multiple stores, then wanted purchases delivered to far-flung addresses. Only a common carrier with massive scale could do this efficiently.

While lawyers fought regulators, UPS engineers were building the operational infrastructure for nationwide service. The breakthrough came in 1959 with the hub-and-spoke system, borrowed from the airline industry but adapted for ground transport. Instead of direct routes between every city pair (which would require thousands of routes), packages would flow through central hubs where they'd be sorted and redirected. Louisville, Kentucky, was chosen for the first major hub—central location, minimal weather delays, and politicians eager for jobs.

The hub system was a gamble. It meant packages would travel farther—a package from Cincinnati to Columbus might go through Louisville first, adding 300 miles. But the efficiency gains were staggering. A hub processing 100,000 packages nightly could sort them into precise delivery routes with 99.9% accuracy. The system also enabled next-day ground delivery within 500-mile radiuses—not as fast as air, but at one-fifth the cost.

Technology became UPS's secret weapon in the expansion wars. In 1961, they installed their first mainframe computer—an IBM 1401 that cost $800,000 (about $8 million today). Competitors scoffed at the expense. What did package delivery need with computers? But UPS used it to optimize everything: routing, scheduling, capacity planning, even predicting seasonal volume surges. By 1970, they were processing 1 million packages daily with lower error rates than companies handling a tenth that volume.

The real breakthrough came through an unlikely source: Sears and JCPenney, America's largest retailers. In 1971, both companies were paying UPS roughly $50 million annually—massive sums that gave them negotiating leverage. They demanded 15% rate cuts, threatening to switch to Roadway Package System if UPS didn't comply. CEO Harold Oberkotter made a decision that stunned Wall Street observers: he said no. On December 1, 1971, Sears and JCPenney pulled their volume—overnight, UPS lost 12% of its revenue.

The board panicked. Employees worried about layoffs. But Oberkotter saw opportunity. Without the low-margin department store volume, UPS could focus on higher-margin commercial deliveries. They aggressively courted smaller retailers who'd been neglected. Within eighteen months, they'd replaced the lost volume with more profitable business. Sears and JCPenney, meanwhile, discovered that Roadway couldn't match UPS's reliability. By 1974, both came crawling back—at UPS's original rates.

The regulatory dam finally broke in 1975. After twenty-three years of legal battles, UPS won "the Golden Link"—authorization to serve all 48 contiguous states. The final piece came when Nevada approved interstate service, connecting Pacific Coast operations with the Midwest and East. For the first time, a single company could pick up a package anywhere in America and deliver it anywhere else via ground transport.

But victory came with a price. The Teamsters union, which had organized UPS drivers city by city since the 1930s, now had leverage over the entire network. In August 1976, they flexed that muscle with a wildcat strike in Michigan that spread to fifteen states. For two weeks, 40% of UPS's volume stopped moving. The company settled quickly, granting wage increases and pension improvements that would cost $100 million annually.

The 1970s ended with UPS in a paradoxical position. They'd achieved Casey's dream of nationwide ground service, handling 8 million packages daily with 99% on-time delivery. They were generating $3 billion in annual revenue with margins that made Wall Street salivate. But storm clouds were gathering. A Memphis entrepreneur named Fred Smith had launched Federal Express in 1973, promising overnight delivery anywhere in America. The Interstate Commerce Commission was moving toward deregulation, which would unleash hundreds of new competitors. And somewhere in Seattle, a young executive named Jeff Bezos was about to graduate from Princeton with ideas about selling books online.

The ground game that UPS had perfected over seven decades was about to be disrupted by the air.

V. The FedEx Wars Begin: Air Service & Competition (1970s-1990s)

Fred Smith was everything Jim Casey wasn't. Yale-educated, inherited wealth, a decorated Marine pilot from Vietnam who looked like he'd stepped out of a Brooks Brothers catalog. In 1973, while UPS was still fighting for ground rights in Nebraska, Smith launched Federal Express with a radical proposition: anything, anywhere in America, absolutely positively overnight. His purple and orange planes, flying into Memphis each night like a choreographed invasion, captured imaginations in a way brown trucks never could.

UPS executives initially dismissed FedEx as a "niche player for emergency documents." By 1978, when FedEx was moving 35,000 packages nightly and had gone public with a $500 million valuation, that dismissal looked like dangerous complacency. Customers who'd never questioned UPS's two-to-five day ground delivery suddenly wondered why everything couldn't arrive tomorrow. IBM started FedExing computer parts. Law firms FedExed contracts. Even consumers FedExed birthday gifts they'd forgotten to send earlier.

The mathematics of air delivery horrified UPS's engineering culture. Flying packages cost ten times more than driving them. FedEx was losing money on most shipments, subsidized by venture capital and public markets. It violated everything Casey had taught about sustainable, profitable growth. But George Lamb, who'd become CEO in 1980, understood that this wasn't about mathematics—it was about perception. UPS was becoming your father's delivery company while FedEx was the future.

The internal debate about entering air delivery split UPS down the middle. Old-timers argued it would cannibalize their profitable ground business. Finance worried about the capital requirements—planes cost $50 million each. Operations questioned whether their culture of methodical precision could adapt to the speed of air logistics. But the deciding factor came from an unexpected source: their own customers. In 1982, IBM threatened to move all its volume to FedEx unless UPS offered overnight service. That was 3% of total revenue walking out the door.

UPS's entry into air delivery was characteristic: methodical, comprehensive, and about five years late. Rather than lease planes like FedEx, they decided to buy and operate their own fleet. Instead of using independent contractors for pickup and delivery, they'd use their existing driver force. Most ambitiously, they wouldn't just match FedEx's overnight service—they'd integrate air and ground into a seamless network where customers could choose speed versus price for each shipment.

The regulatory battle for air rights made the ground expansion look simple. The FAA had strict rules about cargo airlines, most written when planes carried mail bags, not millions of packages. UPS needed approval to fly at night (when most cargo moved), to operate their own meteorology department (critical for routing decisions), and to build sort facilities at airports (where real estate was precious). It took six years and $50 million in legal fees, but in 1988, UPS Airlines was born with 15 planes and routes to 50 cities.

The operational challenge was even greater. UPS's Louisville hub, designed for trucks, had to be reimagined for aircraft. The solution was "Worldport"—a facility that would eventually span 5.2 million square feet (equivalent to 90 football fields) and process 416,000 packages per hour. Packages arrived on planes, were sorted through 155 miles of conveyor belts, and departed on other planes—all within a two-hour window from 11 PM to 2 AM. The margin for error was zero; one delayed plane could cascade through the entire network.

But the real innovation was information technology. While FedEx had popularized package tracking with their Cosmos system, UPS went deeper. Their new Delivery Information Acquisition Device (DIAD)—a handheld computer carried by every driver—captured signatures electronically and uploaded them to mainframes in real-time. Customers could track packages, but more importantly, UPS could track drivers. They knew every stop, every delay, every deviation from the optimal route. It was Big Brother in brown, and drivers hated it initially.

The international expansion that followed was Casey's vision on steroids. In 1985, UPS entered six European countries simultaneously. By 1989, they were in 175 countries. The strategy was classic UPS: they didn't try to build local delivery networks from scratch. Instead, they acquired local companies, painted their trucks brown, and plugged them into the global network. In Germany, they bought Seeland. In France, Prost. In Italy, Alimondo. Each acquisition brought local knowledge and relationships that would've taken decades to build organically.

The competitive dynamics with FedEx evolved from war to détente to something resembling a duopoly. By 1990, they'd divided the market almost philosophically: FedEx owned overnight—70% market share for next-day air. UPS dominated ground—60% share for two-to-five day delivery. Both were printing money. FedEx had 25% operating margins on overnight packages. UPS had 15% margins on vastly higher ground volume. Wall Street loved both companies, but for different reasons—FedEx for growth, UPS for consistency.

Then came the 1997 Teamsters strike that nearly broke UPS. For fifteen days in August, 185,000 drivers, sorters, and loaders walked off the job. It was the largest strike in America since the 1970s. Packages piled up in facilities. Customers fled to FedEx and other competitors. The company was losing $300 million weekly. When settlement came—with wage increases, pension improvements, and a promise to convert part-time jobs to full-time—it cost UPS $4 billion over five years.

But the strike's real cost was strategic. While UPS was paralyzed, FedEx grabbed market share that took years to recover. More importantly, it exposed UPS's vulnerability to labor disruption in a way that spooked major customers. Amazon, just three years old and shipping 20,000 packages daily, started diversifying carriers. Walmart began building its own logistics network. The strike didn't kill UPS, but it ended their monopolistic grip on ground delivery.

As the 1990s ended, UPS faced an existential question: remain private and employee-owned as Casey intended, or go public and access capital markets for the wars ahead? The dot-com boom was creating competitors with seemingly infinite venture capital. FedEx was using its public currency for acquisitions. Amazon was growing 300% annually. The decision would've horrified Casey, but his successors saw no choice. After 92 years as a private partnership, United Parcel Service was going public.

VI. Going Public: The 1999 IPO & Transformation

Jim Kelly stood at the New York Stock Exchange podium at 9:30 AM on November 10, 1999, preparing to ring the opening bell. The UPS CEO, a 35-year company veteran who'd started as a driver in New Jersey, was about to do something Jim Casey had explicitly opposed: sell the company to Wall Street. Around him, 500 UPS employees—all shareholders about to become millionaires—erupted in cheers as their company began trading under the symbol "UPS."

The numbers were staggering. UPS offered 109.4 million shares at $50, raising $5.47 billion in the largest IPO in American history at that time. Within minutes, the stock shot up to $65. By day's end, it settled at $68.25—a 36% first-day pop that created $14 billion in paper wealth. The company that had survived 92 years on retained earnings and employee ownership was suddenly worth $81 billion, making it America's 35th largest corporation overnight.

Why go public after nearly a century of private operation? The board's internal debates, later revealed in SEC filings, showed three driving factors. First, employee liquidity—UPS had 30,000 employee-shareholders, many nearing retirement, holding stock they couldn't easily sell. The internal buyback program was straining under $2 billion in annual redemptions. Second, acquisition currency—FedEx had used its stock to buy 15 companies in five years while UPS watched helplessly. Third, and most pressing, the dot-com revolution was creating competitors with valuations that defied logic. Webvan was worth $8 billion despite losing money on every delivery. Amazon's logistics ambitions were obvious. UPS needed public currency to compete.

But going public meant revealing secrets UPS had guarded for decades. The S-1 filing was a masterclass in operational excellence that stunned Wall Street analysts. UPS delivered 99.1% of packages on time. Their ground network had 62% operating margins in some regions. They spent $1 billion annually on technology—more than most tech companies. They owned 152,000 vehicles, 536 aircraft, and employed 344,000 people. The numbers revealed a business that was less delivery company and more logistics machine.

The dual-class share structure was quintessentially UPS—complex, protective, and designed for the long term. Class A shares (sold to the public) got one vote each. Class B shares (held by employees and retirees) got ten votes each. This meant public shareholders owned 10% economically but controlled only 1% of voting power. Wall Street grumbled, but not loudly—they were too busy calculating the profits from a business generating $27 billion in revenue with 15% margins.

The IPO proceeds unleashed an acquisition spree that transformed UPS from a package carrier to a supply chain conglomerate. Within eighteen months, they bought: Fritz Companies ($450 million) for freight forwarding, First International Bank ($180 million) for trade finance, Mail Boxes Etc. ($191 million) for retail presence, and Challenge Air ($117 million) for heavy cargo. Each acquisition added capabilities that would've taken decades to build internally. The brown trucks were now just the visible tip of a vast logistics iceberg.

The Mail Boxes Etc. acquisition deserves special attention for its strategic brilliance. Overnight, UPS gained 3,000 retail locations in strip malls across America. They rebranded them "The UPS Store" and suddenly had more customer touchpoints than FedEx and the US Postal Service combined. The stores became miniature fulfillment centers where consumers could ship packages, receive deliveries, and access services like printing and packaging. It was physical retail infrastructure just as e-commerce was about to explode.

The cultural transformation was equally dramatic. For 92 years, promotion came from within—every executive had driven a truck or sorted packages. Now UPS hired outsiders: Chief Information Officer from Delta Airlines, Chief Marketing Officer from Coca-Cola, heads of strategy from McKinsey. The old-timers called them "aliens." The aliens called the old-timers "lifers." The tension was palpable at Louisville headquarters, where executives who'd spent decades perfecting ground delivery now reported to MBAs who'd never delivered a package.

Technology investment accelerated post-IPO. UPS spent $11 billion on IT infrastructure between 2000 and 2005—more than they'd spent in the previous century. They built data centers that tracked 15 million packages daily in real-time. They deployed algorithms that optimized delivery routes down to individual turns. They created APIs that let customers integrate UPS tracking into their own systems. Amazon became their largest technology partner, with systems so intertwined that UPS knew about Amazon orders before packages were even packed.

The relationship with Amazon was complicated from the start. By 2002, Amazon represented 5% of UPS's volume—enough to matter, not enough to control. But Jeff Bezos was already planning Amazon Logistics. In meetings, he'd openly tell UPS executives that Amazon would eventually deliver its own packages. UPS executives thought he was bluffing—the capital requirements were astronomical. They'd learn otherwise, but not for another decade.

Wall Street's reaction to UPS as a public company evolved from enthusiasm to respect to something approaching awe. The stock rose 50% in its first two years despite the dot-com crash. Analysts discovered what employees had known for decades: UPS was a compounding machine. Volume grew with GDP. Prices increased with inflation plus a bit more. Margins expanded through efficiency gains. The math was beautiful—high single-digit revenue growth, low double-digit earnings growth, massive free cash flow.

But public ownership brought scrutiny UPS had never faced. Environmental groups attacked their carbon footprint—150,000 diesel trucks burning 400 million gallons annually. Labor unions used quarterly earnings calls to pressure management during negotiations. Activists questioned why a company with $5 billion in annual profits paid drivers $20 an hour while the CEO made $10 million. The brown trucks that had operated in relative anonymity for a century were suddenly symbols in larger debates about capitalism, labor, and climate change.

The IPO transformed UPS, but perhaps not in ways Jim Casey would've expected—or appreciated. The company was richer, more powerful, and more technologically sophisticated than he could've imagined. But it was also more complex, more conflicted, and more vulnerable to forces beyond its control. The employee-owners who'd built the company now owned less than 30% of shares. The patient capital that had funded seven decades of steady growth was replaced by quarterly earnings pressure.

As 1999 turned to 2000, UPS stood at an inflection point. They were public but still culturally private. They dominated ground delivery but lagged in overnight service. They were technology leaders but faced a customer—Amazon—that would soon become a competitor. The next decade would determine whether brown could do for e-commerce what it had done for catalog retail—or whether the company that had survived the Depression, world war, and deregulation would finally meet its match in the everything store from Seattle.

VII. The Modern Rivalry: UPS vs. FedEx in the 21st Century

The conference room at UPS's Atlanta headquarters (they'd moved from Connecticut in 1994) was silent except for the hum of air conditioning. It was June 2003, and CEO Mike Eskew was showing his board a slide they didn't want to see. For the first time in history, FedEx had passed UPS in market capitalization—$22 billion to $20 billion. The company that Fred Smith had started from nothing in 1973 was now worth more than the 96-year-old giant that had invented the industry.

The numbers told a story of two companies evolving in opposite directions. FedEx had built a portfolio of separate operating companies—FedEx Express for overnight, FedEx Ground for economy delivery, FedEx Freight for large shipments, FedEx Office (formerly Kinko's) for retail. Each operated independently with its own drivers, trucks, and systems. It was federated, flexible, and fast-moving. UPS, true to its roots, ran everything through one integrated network. Same drivers delivered air and ground. Same trucks handled packages and freight. Same systems tracked everything. It was efficient but inflexible.

The operational philosophies created starkly different economics. FedEx Express, focused on high-margin overnight delivery, generated 35% operating margins on some routes. But FedEx Ground, using independent contractors instead of employees, had 8% margins—half of UPS's ground business. The integrated UPS network meant a driver might deliver overnight packages in the morning (high margin) and ground packages in the afternoon (medium margin), averaging out to solid but unspectacular 12-15% margins overall.

The real battle was for e-commerce volume, which was exploding beyond anyone's projections. In 2000, online sales were $27 billion—1% of retail. By 2005, they'd reached $90 billion. By 2010, $170 billion. Every percentage point of retail that moved online meant millions more packages. But e-commerce logistics were different from traditional shipping. Consumers expected free delivery (meaning retailers squeezed carriers on price), real-time tracking (requiring massive IT investment), and increasingly, same-day or next-day delivery (destroying the efficiency of traditional hub-and-spoke networks).

UPS's response was typically methodical. They created UPS Supply Chain Solutions, offering complete logistics outsourcing—warehousing, fulfillment, returns processing. The pitch to retailers was compelling: why build your own distribution network when UPS had already spent $50 billion building theirs? High-end retailers bit first. Nike used UPS to manage inventory across 50,000 retail locations. Toshiba had UPS technicians repair laptops at Louisville Worldport, turning returns around in 24 hours instead of weeks.

FedEx countered with speed. In 2009, they launched SameDay City, promising delivery within hours in 25 metropolitan areas. It was absurdly expensive—$50 to deliver a single package across Los Angeles—but it grabbed headlines and positioned FedEx as the innovation leader. They acquired Kinko's for $2.4 billion, rebranding it FedEx Office and creating 1,200 retail locations that doubled as micro-fulfillment centers. They partnered with the US Postal Service for last-mile delivery to rural addresses, something UPS's driver union prohibited.

The international expansion strategies diverged even more dramatically. UPS bought existing networks and painted them brown—TNT's European operations for $1.8 billion, Lynx Express in UK for $55 million. They wanted control, consistency, and integration with their global network. FedEx partnered instead of acquiring, working with local carriers who maintained independence. By 2010, UPS operated its own planes and trucks in 200 countries. FedEx operated directly in 90 countries but could deliver to 220 through partners.

China became the ultimate battleground. UPS got there first, securing direct flight rights to Beijing and Shanghai in 2001. They built a $180 million hub in Shanghai, hired 5,000 local employees, and painted hundreds of trucks brown. FedEx arrived later but moved faster, acquiring China's DTW Group for $400 million and gaining immediate access to 500 cities. By 2015, both companies were moving 20 million packages annually between China and the US, fighting for every percentage point of the exploding cross-border e-commerce market.

Technology became the differentiation battlefield. UPS's ORION (On-Road Integrated Optimization and Navigation) system, deployed in 2013 after ten years and $1 billion in development, was a masterpiece of operations research. It calculated optimal delivery routes for 55,000 drivers daily, considering package volume, promised delivery times, traffic patterns, and even UPS's preference for right-hand turns. The system saved 100 million miles annually—equivalent to $400 million in fuel and labor costs.

FedEx responded with SenseAware—sensors that tracked not just package location but temperature, humidity, light exposure, and shock. For pharmaceutical companies shipping vaccines or museums transporting art, it was revolutionary. The sensors cost $120 per shipment but enabled FedEx to charge premium prices for "white glove" logistics. It was classic FedEx—high tech, high margin, and focused on customers who valued service over price.

The 2016 holiday season exposed both companies' vulnerabilities. E-commerce volume surged 40% year-over-year, overwhelming every carrier. UPS had packages piled in parking lots. FedEx rented U-Hauls for deliveries. Both imposed holiday surcharges and volume caps on major retailers. Amazon, shipping 1 billion packages that year, was furious. The everything store's response would reshape the industry: they'd build their own delivery network.

Labor relations continued to differentiate the rivals. UPS's 260,000 unionized drivers earned $35 per hour plus benefits—total compensation approaching $75,000 annually. It was expensive but created remarkable retention; average driver tenure exceeded 16 years. FedEx Ground's 60,000 independent contractors earned whatever they could net after expenses, typically $40,000-50,000. It was cheaper but created constant churn and quality issues. When FedEx contractors sued for employee classification, the company spent $450 million settling claims.

The financial performance divergence was striking. By 2019, UPS generated $74 billion in revenue with $6.5 billion in operating profit—margins of 8.8%. FedEx generated $69 billion in revenue with $4.4 billion in operating profit—margins of 6.4%. But FedEx grew revenue 8% annually versus UPS's 5%. Wall Street was split: growth investors preferred FedEx's trajectory, value investors preferred UPS's profitability. Both stocks had tripled since 2010, performing in remarkable lockstep despite different strategies.

The pandemic stress-tested both models to breaking point. E-commerce surged 50% in 2020. B2B shipping collapsed 30%. International trade froze then exploded. UPS's integrated network proved more resilient—they could shift capacity from struggling B2B to booming residential delivery. FedEx's federated model created problems—Express had empty planes while Ground was overwhelmed. But FedEx adapted faster, implementing surcharges and capacity limits that protected margins. Both companies had their most profitable year ever in 2020, even as they struggled to maintain service levels.

As the rivalry entered its fifth decade, the differences were crystallizing. UPS remained the operational excellence machine—efficient, reliable, methodical. Every package through one network, every process optimized, every cost scrutinized. FedEx was the innovation engine—flexible, fast-moving, willing to experiment. Multiple networks for different needs, new services launched constantly, failures accepted as learning experiences.

The irony was that both strategies worked. In a logistics market approaching $500 billion globally, there was room for both philosophies. UPS dominated ground delivery with 60% share. FedEx controlled overnight with 50% share. Both printed money in international express. Neither could kill the other despite forty years of trying. It was the perfect capitalist competition—two giants locked in eternal struggle, pushing each other to improve, with customers benefiting from the rivalry.

But both companies now faced a common threat that dwarfed their rivalry: Amazon was no longer just a customer. The everything store was becoming the everything logistics company. And unlike the UPS-FedEx war, this wouldn't be a battle between equals.

VIII. The Amazon Challenge & Strategic Evolution (2010s-Present)

Dave Clark had worked at Amazon for thirteen years when Jeff Bezos gave him an impossible mission in 2012: build a delivery network that could compete with UPS and FedEx. Clark, who'd started in an Amazon warehouse and risen to VP of Operations, looked at the numbers and almost laughed. UPS had 100,000 vehicles and 500 planes built over a century. FedEx had 180,000 vehicles and 650 planes built over four decades. Amazon had... ambition and a willingness to lose money that defied conventional business logic.

The relationship between Amazon and UPS had always been symbiotic but tense. In 2010, Amazon represented 4% of UPS's revenue—about $2 billion annually. By 2013, it was 7% and growing 30% per year. UPS executives faced an impossible dilemma: Amazon was their largest customer and biggest threat simultaneously. Every package UPS delivered for Amazon generated profit but also funded Amazon's logistics buildout. It was like selling bullets to someone who'd eventually shoot you with them.

The breaking point came during Christmas 2013. Amazon had promised millions of customers delivery by December 24th. On December 23rd, a perfect storm hit: ice storms, volume 20% above projections, and UPS's Louisville hub overwhelmed. Hundreds of thousands of packages didn't arrive until after Christmas. Amazon issued apologies and refunds. But privately, Bezos was done relying on third parties for his company's most critical customer promise.

Amazon Logistics launched quietly in 2014 with a simple proposition to independent contractors: deliver packages for $18-25 per hour using your own vehicle. No uniforms, no benefits, no long-term commitments. It was the Uber model applied to delivery—algorithmic dispatch, flexible labor, zero assets. UPS executives mocked it as "unsustainable" and "unscalable." They were thinking like a logistics company. Amazon was thinking like a technology platform.

The numbers scaled faster than anyone anticipated. 2014: 20 million packages delivered by Amazon Logistics. 2015: 100 million. 2016: 500 million. 2017: 1 billion. By 2018, Amazon was delivering 2.5 billion packages annually—20% of their volume. They'd built 75 fulfillment centers, 25 sort centers, and 50 delivery stations. They'd recruited 100,000 independent drivers. And they were just getting started.

UPS's response was schizophrenic. Publicly, CEO David Abney insisted Amazon was "a valued partner" and that "cooperative competition" would benefit everyone. Privately, UPS was transforming its entire operation to reduce Amazon dependence. They automated sort facilities, reducing labor costs 30%. They implemented dimensional pricing, charging for package size not just weight, which hit Amazon's inefficiently packed boxes hard. Most significantly, they diversified their customer base, focusing on healthcare, automotive, and high-value B2B shipping that Amazon couldn't easily replicate.

The Saturday delivery decision epitomized UPS's strategic dilemma. For 96 years, UPS had delivered Monday through Friday only. Weekend delivery was expensive—overtime pay, lower route density, disrupted hub operations. But Amazon was conditioning consumers to expect seven-day delivery. In 2017, UPS capitulated, launching Saturday delivery in 15 cities. By 2019, they'd expanded to 90% of the US population. The cost: $500 million annually. The alternative: losing e-commerce entirely to Amazon and FedEx.

Amazon's logistics innovations kept coming in waves. Amazon Air launched in 2016 with 40 leased Boeing 767s. By 2021, they had 85 planes flying to 70 destinations. They didn't need UPS's 500-plane fleet; they just needed enough capacity to handle surge volume and negotiate leverage. Amazon Delivery Service Partners followed in 2018—$10,000 got entrepreneurs a turnkey delivery business with Amazon-branded vans, uniforms, and guaranteed volume. Within three years, 3,000 DSPs were operating 100,000 vans.

The technology gap was even more threatening. Amazon's delivery app gave drivers turn-by-turn navigation, package-specific instructions, and real-time customer communication. Their AI optimized routes considering traffic, weather, and driver experience. Machine learning predicted package volume down to neighborhood level. Computer vision automated package sorting. Robotics handled warehouse operations. UPS had better operations; Amazon had better algorithms.

UPS acquired Coyote Logistics in 2015 for $1.8 billion, entering the freight brokerage market. The logic was compelling: e-commerce meant more small packages to consumers, but those products first moved as freight from manufacturers to fulfillment centers. Controlling both legs meant more revenue per item and better supply chain visibility. Coyote's technology platform connected 10,000 trucking companies with 35,000 shippers, generating $2 billion in annual revenue.

The labor challenge intensified throughout the decade. UPS drivers, represented by the Teamsters, earned $40 per hour by 2020—total compensation exceeding $100,000 annually with benefits. Amazon DSP drivers earned $16-20 per hour with minimal benefits. The cost differential was unsustainable, but UPS's union contract ran through 2023. When negotiations began in April 2023, 340,000 Teamsters held the US supply chain hostage. The settlement, reached hours before a strike deadline, gave drivers $49 per hour by 2027—a 30% increase that would cost UPS $30 billion over five years.

The pandemic accelerated every trend. E-commerce exploded from 11% of retail in 2019 to 19% in 2020. UPS's volume surged 21% in a single year. But Amazon grew even faster, delivering 4.2 billion packages in 2020—one-third of their total volume. They'd become the third-largest delivery company in America by package count, trailing only USPS and themselves as UPS's customer. The student hadn't just caught the teacher; they were rewriting the curriculum.

Sustainability became a new battlefield. UPS announced 10,000 electric vehicles by 2025, $750 million in alternative fuel infrastructure, and carbon neutrality by 2050. Amazon ordered 100,000 electric vans from Rivian, built solar farms powering fulfillment centers, and pledged net-zero carbon by 2040—ten years ahead of UPS. Both companies knew that corporate customers increasingly demanded green logistics. The brown trucks going electric wasn't environmental virtue signaling; it was competitive necessity.

International expansion strategies diverged completely. UPS continued buying established networks—spending $5 billion attempting to acquire TNT Express (ultimately blocked by EU regulators). Amazon built from scratch, launching local delivery networks in UK, Germany, Japan, and India. They didn't need global coverage; they just needed to control delivery in markets where they had significant e-commerce share. By 2023, Amazon Logistics operated in 20 countries—small compared to UPS's 220, but covering 80% of Amazon's international volume.

The strategic evolution wasn't just about competing with Amazon; it was about becoming more like them. UPS launched UPS Flight Forward, using drones for medical deliveries. They created UPS Capital, offering supply chain financing. They built digital platforms letting small businesses access enterprise-grade logistics. They acquired Roadie, a crowdsourced same-day delivery platform. The brown truck company was transforming into a technology-enabled supply chain solutions provider.

By 2023, the landscape had fundamentally shifted. Amazon delivered 5.9 billion packages annually—more than UPS's US volume. They'd spent $100 billion building logistics infrastructure in a decade—more than UPS's market capitalization. But paradoxically, UPS was thriving. Revenue reached $100 billion. Operating margins improved to 13%. The stock hit all-time highs. How? By doing what Casey had always preached: focusing on service, efficiency, and reliability while others chased growth at any cost.

The Amazon challenge had forced UPS to evolve more in ten years than the previous thirty. They'd automated operations, diversified services, modernized technology, and expanded internationally. They'd learned to compete with a customer, partner with a rival, and transform a century-old culture. Most importantly, they'd proven that operational excellence still mattered in an age of algorithmic disruption.

But the war wasn't over. Amazon's logistics buildout continued at $10 billion annually. Autonomous vehicles promised to eliminate driver costs. Drone delivery threatened dense urban routes. Artificial intelligence could optimize networks beyond human comprehension. The next decade would determine whether UPS's hundred-year head start was an insurmountable moat or merely a temporary advantage in the face of unlimited capital and technological disruption.

IX. Playbook: The UPS Business Model & Lessons

Let's break down the DNA of the UPS machine—a business model so robust it survived horse-drawn carriages to autonomous vehicles, yet so simple Jim Casey could sketch it on a napkin. After 117 years, thousands of competitors, and multiple technological revolutions, the core economics remain remarkably intact: pick up packages, sort them efficiently, deliver them reliably, repeat 22 million times daily.

Network Effects and Density Economics

The genius of UPS isn't complexity—it's density. Every additional package in a neighborhood makes every other package cheaper to deliver. A driver stopping at one house can hit three neighbors for marginal seconds more. This creates a beautiful flywheel: more volume enables lower prices, which attracts more volume, which increases density, which improves margins. Between international and domestic package revenue, domestic package delivery generated more money, bringing in 60.3 billion U.S. dollars, compared to international delivery which brought in 19.5 billion U.S. dollars.

Consider the mathematics: A UPS driver makes 120-150 stops daily. Adding one package to an existing route costs virtually nothing—the truck's already there. But a competitor starting fresh needs sufficient volume to justify that route. Until they reach critical density (roughly 100 stops per route), they're bleeding money. This is why Amazon, despite unlimited capital, still uses UPS for 20% of deliveries in rural areas. The density economics are unassailable.

The hub-and-spoke architecture amplifies these effects. Louisville's Worldport processes 416,000 packages hourly through 155 miles of conveyor belts. The facility cost $2 billion to build, but the per-package cost approaches zero at volume. A competitor needs similar infrastructure to match UPS's efficiency, but can't justify the investment without UPS's volume—a classic chicken-and-egg problem that protects incumbents.

The Power of Operational Excellence

UPS's operational precision borders on obsessive. Drivers follow computerized routes that minimize left turns (saving 10 million gallons of fuel annually). Package cars are loaded in exact delivery sequence. Keys go on the pinky finger to avoid fumbling. These micro-optimizations compound into macro advantages: 99% on-time delivery when competitors average 95%.

The ORION routing system epitomizes this philosophy. Ten years and $1 billion in development to save 100 million miles annually—roughly $400 million in cost savings. The ROI seems pedestrian until you realize ORION also improved delivery consistency, reduced driver stress, and created data that feeds machine learning models. Operational excellence isn't just about efficiency; it's about building capabilities that become competitive moats.

Culture as Competitive Advantage

Every UPS CEO started at the bottom—driving trucks, sorting packages, or loading planes. This isn't tradition; it's strategy. Executives who've done the work understand the work. They make better decisions because they've lived the consequences of bad ones. When CEO David Abney negotiated with the Teamsters in 2018, he could reference his own experience as a part-time loader in Mississippi. That credibility matters when 340,000 unionized employees can shut down your network.

The employee ownership culture Casey created survives today, though diluted. Drivers earning $100,000 annually with full benefits don't just deliver packages—they protect the brand. When a UPS driver helps carry groceries for an elderly customer or waits to ensure a child gets inside safely, they're not following protocol—they're acting like owners. FedEx's contractor model can't replicate this, no matter how sophisticated their technology.

Patient Capital and Long-Term Thinking

UPS stayed private for 92 years, allowing multi-decade bets impossible for public companies. The regulatory battle for interstate commerce took 23 years and millions in legal fees. The international expansion required buying and integrating dozens of companies over 30 years. The technology transformation consumed $50 billion over two decades. These investments had negative ROI for years before paying off spectacularly.

Even as a public company, the dual-class share structure preserves long-term thinking. When activists pushed for breaking up the company in 2015—separating high-margin international from lower-margin domestic—management could resist because employees controlled voting rights. The integrated network might be suboptimal for margins, but it's optimal for resilience and customer service.

Managing Labor Relations

UPS's relationship with the Teamsters is often portrayed as a weakness—unionized labor costs 40% more than FedEx's contractors. But it's actually a strategic choice with hidden benefits. Union drivers stay for careers (average tenure: 16 years), accumulating route knowledge and customer relationships impossible to replicate. The union contract provides labor stability—no sudden driver shortages that plague Amazon and FedEx. And counterintuitively, high labor costs force operational excellence; when drivers cost $100,000 annually, you optimize everything else.

The 2023 contract negotiation showcased this dynamic. UPS agreed to $30 billion in wage increases over five years—seemingly catastrophic for margins. But they simultaneously announced $5 billion in automation investment that would reduce sort facility headcount by 30%. The high labor costs justify automation investments that improve long-term competitiveness. It's expensive stability that enables transformation.

The Integrated vs. Federated Model Debate

UPS runs one network for everything—air, ground, international, freight. It's massively complex but creates synergies. A sales rep selling ground delivery can upsell international shipping. Technology investments benefit all services. Customer relationships deepen across products. The downside: when something breaks, everything breaks. The 1997 strike paralyzed all services simultaneously.

FedEx's federated model—separate operations for different services—provides flexibility and resilience. FedEx Ground can experiment with contractor models without affecting FedEx Express employees. Each unit optimizes for its specific market. But coordination suffers. Customers deal with different systems, drivers, and service levels. Costs duplicate across organizations. The model works but lacks UPS's economies of scale.

Pricing Power and Duopoly Dynamics

UPS annual revenue for 2023 was $90.958B, a 9.35% decline from 2022. Despite this decline from peak pandemic volumes, UPS maintained pricing discipline. They consciously shed low-margin volume (down 15% in packages) while increasing revenue per package by 8%. This pricing power comes from the duopoly structure—when customers have only two real options for critical logistics, both can maintain margins.

The duopoly exhibits fascinating game theory dynamics. Neither UPS nor FedEx wants a price war that destroys margins for both. So they compete on service, technology, and capacity—not price. When one raises rates 5.9% (as both did for 2024), the other matches within days. This rational competition creates a pricing umbrella that smaller players can't puncture because they lack network scale.

Technology as Enabler vs. Disruptor

UPS views technology as operational enhancement, not transformation. ORION optimizes existing routes. DIAD devices digitize existing processes. Even drone delivery augments, rather than replaces, traditional delivery. This conservative approach seems outdated compared to Amazon's moon shots, but it's proven remarkably effective. UPS gets consistent ROI from technology investments because they're solving known problems, not inventing new businesses.

The risk is discontinuous change. If autonomous vehicles eliminate driver costs (40% of operating expenses), UPS's entire model breaks. If drone delivery becomes viable for residential packages (60% of volume), the route density advantages evaporate. If 3D printing eliminates package shipping for manufactured goods (20% of volume), the network becomes stranded assets. UPS is betting these changes will be evolutionary, allowing adaptation. History suggests they're right, but history doesn't always repeat.

The UPS playbook ultimately reduces to this: Build network density through operational excellence. Reinvest profits into capabilities that deepen moats. Maintain culture through employee ownership and promotion from within. Think in decades while executing in minutes. It's not sexy, but it's generated $500 billion in cumulative revenue over a century. In a world obsessed with disruption, there's something profound about a business model that treats innovation as incremental improvement rather than revolution. Casey would recognize today's UPS—the brown trucks, the uniformed drivers, the obsession with service. That continuity, in an era of constant change, might be the greatest competitive advantage of all.

X. Analysis & Investment Case

The investment case for UPS boils down to a fundamental question: Is this a melting ice cube in the age of Amazon, or a mispriced compounder temporarily out of favor? The trailing PE ratio is 12.95 and the forward PE ratio is 13.11. This stock pays an annual dividend of $6.56, which amounts to a dividend yield of 7.54%. At these valuations, the market is pricing UPS like a declining industrial, not the critical infrastructure backbone of global commerce.

Competitive Positioning: The Duopoly Endures

As the world's largest parcel delivery company, UPS manages a massive fleet of more than 500 planes and 100,000 vehicles, along with many hundreds of sorting facilities, to deliver an average of about 22 million packages per day to residences and businesses across the globe. UPS' domestic US package operations generate around 65% of total revenue, while international package makes up 20%. This scale creates insurmountable barriers for new entrants. Amazon spent $100 billion building logistics infrastructure and still relies on UPS for rural deliveries where density economics dominate.

The competitive landscape has stabilized into three distinct tiers. UPS and FedEx control the premium segment—time-definite, high-value, business-critical shipments. Amazon dominates consumer e-commerce in dense urban markets. Regional players and the USPS fill niches. This structure is remarkably stable because each player's economics reinforce their position. UPS can't match Amazon's willingness to lose money on last-mile delivery, but Amazon can't replicate UPS's B2B relationships or international network.

Moats: Network Density and Switching Costs

The network density moat deepens daily. Every package added to a route improves margins. Every new pickup location makes the network more valuable to shippers. This isn't Silicon Valley-style network effects where users attract users—it's physical world network effects where packages attract packages. The difference: digital networks can be disrupted by better algorithms, but physical networks require decades and billions to replicate.

Switching costs are understated but substantial. Large shippers have systems integrated with UPS's APIs, tracking numbers printed on packaging, negotiated rates based on volume commitments, and employees trained on UPS procedures. When Sears tried switching from UPS to Roadway in 1971, the operational chaos forced them back within 18 months. Today's integration is exponentially deeper—ERP systems, warehouse management software, customer service platforms all built around UPS's infrastructure.

The stock's EV/EBITDA ratio is 8.36, with an EV/FCF ratio of 27.26. The company has a current ratio of 1.32, with a Debt / Equity ratio of 1.83. Return on equity (ROE) is 34.91% and return on invested capital (ROIC) is 11.14%. These metrics reveal a capital-intensive business generating exceptional returns—exactly the profile that creates competitive moats. High ROIC with high capital requirements means competitors need both massive investment and operational excellence to compete.

Risks: Labor, Amazon, and Structural Decline

The bear case is straightforward and sobering. Labor costs are structurally higher than competitors and rising—the 2023 Teamsters agreement adds $30 billion in costs through 2027. Amazon Logistics is growing 30% annually and will eventually turn from partner to pure competitor. E-commerce growth is slowing from pandemic peaks. Autonomous vehicles could eliminate UPS's largest cost advantage—experienced drivers who know every shortcut and customer preference.

The structural decline argument deserves scrutiny. UPS annual revenue for 2023 was $90.958B, a 9.35% decline from 2022. Bulls argue this reflects normalization from unsustainable pandemic volumes. Bears see the beginning of long-term share loss to Amazon. The truth likely lies between—UPS is ceding low-margin residential volume while defending high-margin B2B shipping.

Economic sensitivity remains acute. UPS is essentially a leveraged bet on economic activity—when GDP grows 2%, package volume grows 4%. When recession hits, the leverage works in reverse. The next downturn will test whether UPS's cost structure, inflated by union agreements, can flex sufficiently to maintain profitability.

The Future of Logistics: Transformation Vectors

Three technological shifts could transform UPS's economics. Autonomous vehicles would eliminate driver costs (40% of expenses) but require massive capital investment and regulatory approval—advantage incumbents with capital access. Drone delivery could serve rural areas more efficiently, but payload limitations and weather sensitivity limit applicability. Most intriguingly, AI-driven route optimization could improve efficiency 20-30% beyond current levels—and UPS has the data to train these models better than anyone except possibly Amazon.

Sustainability initiatives, often dismissed as ESG theater, actually strengthen competitive position. UPS's order of 10,000 electric vehicles and commitment to carbon neutrality by 2050 anticipates regulatory requirements and customer demands. More importantly, electric vehicles have lower operating costs after the initial investment—another advantage for capital-rich incumbents over capital-constrained challengers.

Bull Case: The Mispriced Compounder

Price-To-Earnings vs Peers: UPS is good value based on its Price-To-Earnings Ratio (12.8x) compared to the peer average (17.3x). Price-To-Earnings vs Industry: UPS is good value based on its Price-To-Earnings Ratio (12.8x) compared to the Global Logistics industry average (15.4x). Price-To-Earnings vs Fair Ratio: UPS is good value based on its Price-To-Earnings Ratio (12.8x) compared to the estimated Fair Price-To-Earnings Ratio (17.5x).

The bull case rests on mean reversion and operational leverage. If UPS returns to historical margins (13-15% vs current 10%), earnings double without revenue growth. The path exists: automate sorting facilities, optimize routes with AI, shift mix toward higher-margin services. The 2027 labor contract provides cost certainty, allowing management to plan transformation investments.

International expansion remains underpenetrated. Cross-border e-commerce is growing 20% annually. UPS's international infrastructure, built over 40 years, can't be replicated quickly. As global trade fragments into regional blocs, companies need logistics partners who can navigate complexity—advantage UPS.

The dividend alone makes a compelling case. This stock pays an annual dividend of $6.56, which amounts to a dividend yield of 7.54%. At this yield, investors get paid handsomely to wait for operational improvements. The dividend is covered by free cash flow even at current depressed margins, suggesting sustainability despite the high payout ratio.

Bear Case: The Melting Ice Cube

The bear case sees structural decline accelerating. Amazon will eventually insource all profitable volume, leaving UPS with unprofitable rural routes and declining B2B shipping. Shippers will diversify away from the UPS/FedEx duopoly to reduce pricing power. Regional competitors using gig-economy labor models will cherry-pick profitable routes.

Labor costs create a death spiral—high costs require high prices, high prices drive volume to competitors, lower volume reduces route density, lower density increases unit costs. The 2023 Teamsters agreement locked in cost inflation just as pricing power peaks. When the next recession hits, UPS won't be able to cut costs sufficiently, leading to sustained losses that force dividend cuts and asset sales.

Technology disruption accelerates the decline. 3D printing eliminates manufacturing shipments. Autonomous vehicles commoditize delivery. Digital documents replace physical packages. What remains is low-margin, price-sensitive e-commerce delivery—exactly where Amazon has structural advantages.

The Verdict: Asymmetric Risk-Reward

The average price target for UPS is $112.11, which is 28.76% higher than the current price. The consensus rating is "Buy". The market's pessimism has created an unusual situation: a dominant oligopolist with irreplaceable infrastructure trading at distressed valuations. This typically occurs when linear extrapolation of current trends suggests terminal decline. But logistics isn't winner-take-all like social networks. There's room for multiple players because shippers want redundancy, capabilities vary by segment, and physical infrastructure creates regional advantages.

The investment case ultimately depends on time horizon and risk tolerance. For traders, UPS is a falling knife in a slowing economy. For long-term investors, it's a rare opportunity to buy critical infrastructure at pessimistic valuations. The dividend provides downside protection while operational improvements and mean reversion offer multi-bagger upside.

History suggests betting against UPS is dangerous. The company has survived technological disruption (trucks replacing horses), regulatory change (deregulation), competitive threats (FedEx, Amazon), and economic catastrophe (Depression, Financial Crisis, COVID). Each time, the bears extrapolated demise. Each time, UPS adapted and emerged stronger. The brown trucks keep rolling because the need they serve—moving physical goods efficiently—is fundamental to modern civilization.

The risk isn't that UPS disappears—it's that it becomes a slow-growing utility earning regulated returns. But at current valuations, even that scenario generates acceptable returns. And if management executes the transformation plan—automating operations, optimizing networks, expanding internationally—the stock could triple while paying dividends throughout. In a market obsessed with finding the next Amazon, the opportunity might be in buying the infrastructure Amazon still depends on, priced like it's going bankrupt when it's merely transitioning.

XI. Epilogue: What Would Jim Casey Think?

Standing in Louisville's Worldport at 1 AM, watching 416,000 packages flow through 155 miles of conveyor belts in perfect synchronization, you can't help but wonder what nineteen-year-old Jim Casey would make of his creation. The boy who borrowed $100 to start a bicycle messenger service built something that now moves 6.5 billion packages annually, employs half a million people, and generates $90 billion in revenue. The basement beneath the Seattle saloon has become a global network spanning 220 countries.

Casey would recognize the principles, even if the scale would stagger him. "Best service and lowest rates"—still the philosophy, though "service" now means real-time tracking and guaranteed delivery windows, while "rates" are dynamically priced by algorithms considering fifteen variables. The brown trucks he chose for their professional appearance have become so iconic that UPS trademarked the color. The employee ownership he championed survives, though diluted by public markets Casey opposed.

But Casey would marvel at what his principles, applied consistently over 117 years, accomplished. The culture of operational excellence he instilled—measuring everything, optimizing constantly, respecting process—created a learning organization that survived the transition from horses to trucks to planes to drones. The employee-first philosophy produced generations of managers who started as drivers, creating institutional knowledge no competitor can replicate. The patient capital approach built infrastructure whose replacement cost exceeds $200 billion.

The enduring principles seem almost quaint in today's business environment: Service before profits. Employees as partners. Steady expansion over explosive growth. Operational excellence over financial engineering. Yet these principles created one of America's most successful businesses, surviving every economic downturn, technological disruption, and competitive threat for over a century.

What UPS got right that others didn't was understanding that logistics isn't about moving packages—it's about trust. When a small business ships a product, they're trusting UPS with their reputation. When a hospital receives medical supplies, they're trusting UPS with lives. When grandparents send presents to grandchildren, they're trusting UPS with relationships. That trust, built package by package over 117 years, can't be algorithm-ed away or disrupted by venture capital.

Casey's greatest insight was that sustainable competitive advantage comes from doing simple things extraordinarily well, repeatedly, at scale. Not from revolutionary technology or brilliant strategy, but from hundreds of small optimizations compounding over decades. Right-hand turns saving seconds. Package cars loaded in delivery sequence. Drivers who know every dog on their route. These micro-advantages, multiplied by 22 million daily deliveries, create macro moats.

The Next 100 Years: Challenges and Opportunities

The challenges facing UPS would be familiar to Casey—labor tensions, technological change, aggressive competitors, economic uncertainty. The solutions would be familiar too: invest in operations, take care of employees, focus on service, think long-term. The specifics change—autonomous vehicles instead of automobiles, Amazon instead of Sears—but the fundamentals endure.

The next century's opportunities are hiding in plain sight. Global e-commerce will grow from $5 trillion to $50 trillion. Someone has to move those packages. Healthcare logistics, already 10% of revenue, will explode as populations age and medicines become personalized. Supply chain complexity, driven by reshoring and trade fragmentation, favors sophisticated operators over simple carriers. Sustainability requirements will advantage companies with capital for electric fleets and renewable infrastructure.

But the real opportunity is what it's always been: being the physical world's most trusted logistics provider when everyone else is chasing digital dreams. As augmented reality, artificial intelligence, and quantum computing capture imaginations and investment, someone still needs to move atoms from point A to point B. That's not sexy, but it's essential. And essentiality, Casey understood, is the ultimate moat.

The biggest risk isn't disruption—it's forgetting what made UPS great. The temptation to chase Amazon's growth, copy FedEx's innovations, or appease Wall Street's quarterly demands could erode the patient, methodical, service-obsessed culture that created the company. When UPS tries to be something other than UPS, it fails. When it focuses on being the best version of itself, it dominates.

Final Reflections on Building an Enduring Business

UPS's story offers lessons that transcend logistics. First, competitive advantage can come from excellence in execution rather than breakthrough innovation. Second, culture and values, consistently applied over decades, create moats that technology and capital can't replicate. Third, serving essential needs with reliability and integrity builds businesses that survive centuries, not just cycles.

In an era obsessed with disruption, UPS proves the power of consistency. While competitors pivoted, acquired, and restructured, UPS kept delivering packages, optimizing routes, and training drivers. The cumulative effect of millions of small improvements created something extraordinary—a business that's both dinosaur and dynamo, tradition-bound yet constantly evolving, simple in concept but complex in execution.

Jim Casey died in 1983 at ninety-five, having seen his company grow from two bicycles to a global giant. His last public statement captured the ethos he'd built: "We have become successful by always looking ahead, not back, and by always trying to do better tomorrow what we did well today." It's not a motto that would excite venture capitalists or make TED Talk highlights. But it built a business that's survived everything the world could throw at it for 117 years.

The brown trucks will keep rolling because they must. Whatever the future brings—autonomous vehicles, drone swarms, teleportation—someone needs to bridge the gap between digital commerce and physical delivery. That someone will likely be the company that's been doing it since before airplanes existed, adapting to each new technology while maintaining the timeless principles of service, efficiency, and integrity that Jim Casey sketched out in a Seattle basement in 1907.

Looking ahead, the question isn't whether UPS will survive—it's what form that survival takes. The optimistic scenario sees UPS as the physical backbone of global commerce, leveraging its infrastructure and expertise to capture value as middleman between digital and physical worlds. The pessimistic scenario sees a regulated utility, earning modest returns on massive infrastructure, essential but uninspiring. Either way, the brown trucks keep delivering, as they have through depressions and booms, wars and peace, disruption and stability.

Casey would probably smile at the current moment—the company he founded with $100 is worth $75 billion, employs 500,000 people, and moves 6% of global GDP. Not bad for a messenger service started by two teenagers who just wanted to provide "best service and lowest rates." That simple mission, pursued relentlessly for over a century, built something that transcends business—a trust network connecting the world's commerce, one package at a time.

XII. Recent News### Strategic Pivot Announcement (January 2025)

Today the company announces the following set of strategic actions: first, it has reached an agreement in principle with its largest customer to lower its volume by more than 50% by the second half of 2026; second, effective January 1, 2025, the company has insourced 100% of its UPS SurePost product; and third, in connection with these efforts, the company is reconfiguring its U.S. network, and launching multi-year "efficiency reimagined" initiatives to drive approximately $1.0 billion in savings through an end-to-end process redesign. This bombshell announcement represents UPS's most dramatic strategic shift since going public—essentially divorcing Amazon while simultaneously restructuring the entire US network.

The Amazon volume reduction, while shocking in magnitude, is strategically logical. Low-margin residential deliveries were diluting profitability and creating operational complexity. By cutting Amazon volume in half, UPS can focus on higher-margin B2B and healthcare logistics while reducing strain on the network during peak seasons.

Q4 2024 and Full Year Results

UPS today announced fourth-quarter 2024 consolidated revenues of $25.3 billion, a 1.5% increase from the fourth quarter of 2023. Consolidated operating profit was $2.9 billion, up 18.1% compared to the fourth quarter of 2023, and up 11.2% on a non-GAAP adjusted basis. Diluted earnings per share were $2.01 for the quarter; non-GAAP adjusted diluted earnings per share were $2.75, 11.3% above the same period in 2024.