Sterling Infrastructure: From Struggling Highway Builder to AI's Invisible Backbone

II. Origins: A Michigan Contractor Goes to Texas (1955–1990)

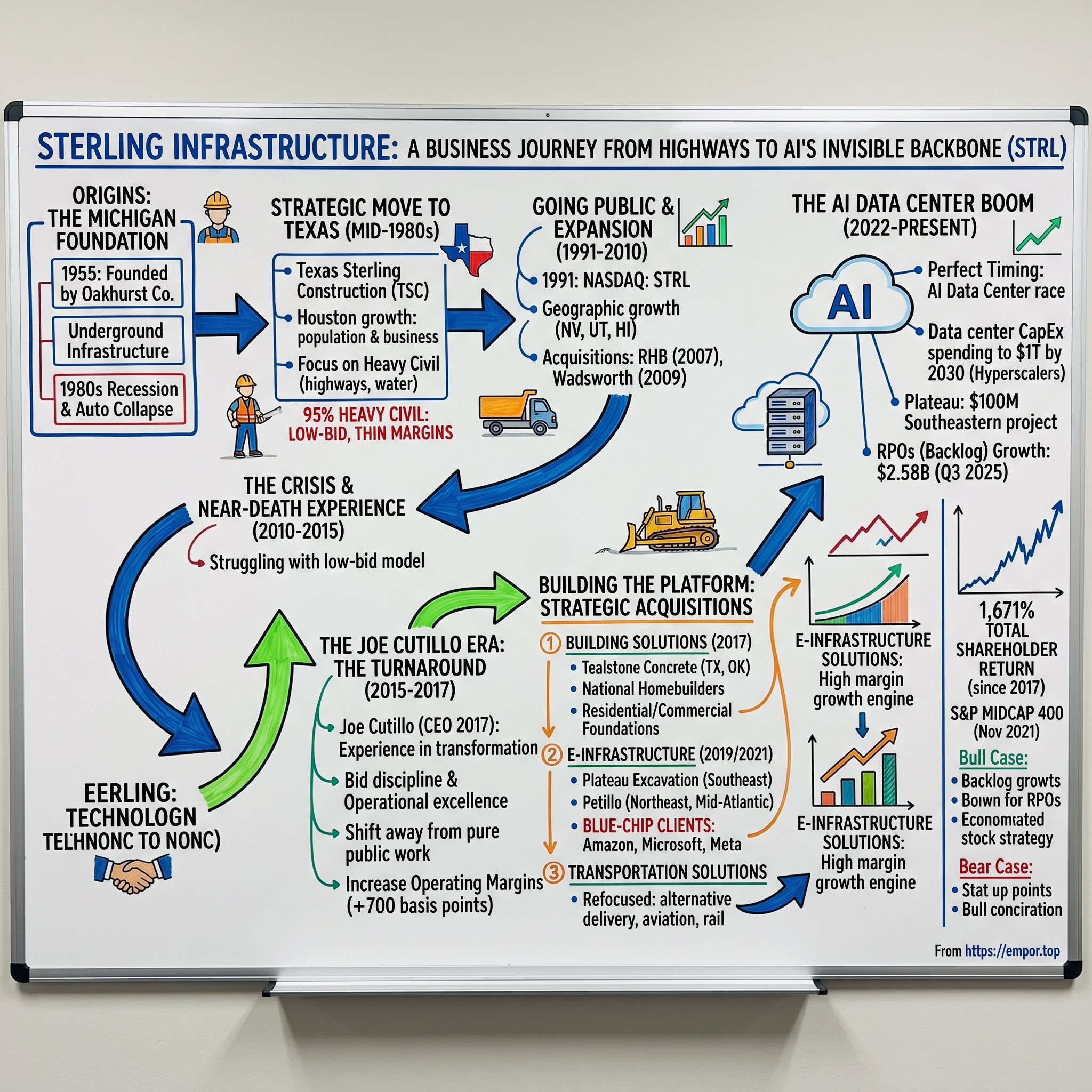

The Sterling story begins not in the Lone Star State but in the manufacturing heartland of Michigan. Originally founded by two brothers in 1955 as the Oakhurst Company, Inc., the business was born into the post-war construction boom when America was building highways, subdivisions, and the physical infrastructure of suburban prosperity.

Sterling Construction Company was founded in 1955 in Sterling Heights, Michigan. As an underground infrastructure company, Sterling steadily gained market share over the next two decades, growing to become one of Michigan's most experienced, reliable, and well-known contractors. That success continued until the early 1980s when Sterling faced the harsh impacts of a significantly diminished building market in Michigan.

The Michigan recession of the early 1980s—brought on by the collapse of the American auto industry—proved to be a crucible that would ultimately reshape the company's destiny. With Detroit's Big Three hemorrhaging market share to Japanese imports and Michigan's construction market drying up, Sterling's leadership faced a stark choice: adapt or perish.

Determined and opportunistic, Sterling's leadership relocated the company to a more active construction market in Houston, Texas and became Texas Sterling Construction Co. (TSC). It wasn't long after TSC settled in the great state of Texas that the company began to experience success once again.

The move to Texas proved prescient. Houston in the mid-1980s was emerging from its own oil bust, but the region's fundamental growth dynamics—population influx, pro-business regulatory environment, and massive infrastructure needs—created fertile ground for a construction company with midwestern work ethic and technical expertise.

Texas Sterling Construction (TSC) is a leading heavy civil construction company that specializes in the building and reconstruction of transportation and water infrastructure. TSC has provided construction services in Texas since 1978 with offices in the Dallas-Fort Worth area, San Antonio, and Houston.

Throughout the 1980s and into the 1990s, TSC built its reputation on highway projects, storm drainage systems, and water infrastructure—the unglamorous but essential backbone of Texas's rapid growth. The company developed deep relationships with the Texas Department of Transportation and municipal agencies across the state, winning contracts through the traditional low-bid process that defined public construction work.

In 1990, TSC made the decision to expand their civil services by adding a paving division to its operations. By the end of the decade, TSC was being awarded large highway paving and bridge projects for the Texas Department of Transportation. The unwavering determination and commitment to building and delivering quality projects on schedule and below budget earned TSC a reputation as a premier contractor in the Houston area.

This foundation—technical competence, relationship-driven growth, and a culture of on-time delivery—would prove essential decades later when Sterling pivoted to serve a very different type of customer. But first, the company would have to navigate the public markets and confront the brutal economics of heavy civil construction.

III. Going Public & Early Geographic Expansion (1991–2010)

In 1991, Sterling Construction Company went public, trading on the NASDAQ under the ticker symbol "STRL." This move provided the capital necessary for the company to expand beyond its Texas roots. Throughout the 1990s and early 2000s, Sterling pursued a strategy of geographic expansion and diversification, acquiring several regional construction companies to establish a presence in new markets across the United States.

The IPO marked a turning point. With access to public market capital, Sterling could pursue acquisitions that would have been impossible for a purely private, family-owned contractor. The company's strategy was straightforward: find regional construction firms with strong local relationships, acquire them, and integrate them into a growing network that could bid on larger projects across multiple states.

Key milestones included acquiring Road and Highway Builders, LLC for $53 million in 2007, expanding operations into Nevada and Hawaii, and acquiring Ralph L. Wadsworth Construction Company, LLC for $64 million in 2009, entering the Utah market.

These acquisitions followed a predictable playbook. Sterling would identify well-run regional contractors with established client relationships and track records of profitable execution. The targets were typically family-owned businesses whose founders were approaching retirement or seeking liquidity. Sterling offered a combination of cash and stock, allowing sellers to participate in the combined company's growth while securing immediate value.

The geographic logic was sound: Nevada and Utah offered exposure to fast-growing western markets, while Hawaii provided a specialized niche where few mainland contractors had expertise. Ralph L. Wadsworth in particular brought expertise in alternative delivery methods—design-build and construction manager/general contractor (CM/GC) contracts—that would prove increasingly valuable as state DOTs sought more collaborative relationships with contractors.

In 1996, the company expanded to the Dallas market and in 2002, set up an office in San Antonio. Capitalizing on continued growth and success, TSC became listed as a publicly traded company on the American Stock Exchange in 2004, under the name Sterling Construction Company Inc.

Yet beneath the surface of geographic expansion, Sterling struggled with the fundamental economics of heavy civil construction. The industry operated on razor-thin margins, with public contracts typically awarded to the lowest bidder. This competitive dynamic meant that any project could become unprofitable if costs exceeded estimates—and in construction, cost overruns were endemic.

The challenges were structural. Public infrastructure projects faced funding uncertainty tied to legislative appropriations. Weather delays, material price volatility, and labor shortages could devastate margins on fixed-price contracts. And the cyclicality of government spending meant that boom years were inevitably followed by budget crunches.

Formerly known as Oakhurst Company, the organization adopted the Sterling Construction Company name in 2001 before becoming Sterling Infrastructure. The name change reflected management's aspiration to build something more than a collection of regional highway contractors. But making that aspiration reality would require confronting years of accumulated challenges.

For investors, Sterling in this era offered a classic value trap: cheap on traditional metrics but perpetually failing to compound value. The stock meandered, reflecting the company's middling returns on capital and lack of differentiated competitive position. Something fundamental would have to change.

IV. The Crisis & Near-Death Experience (2010–2015)

The 2008 financial crisis didn't hit Sterling Infrastructure immediately, but its effects cascaded through the construction industry over the following years. State budgets collapsed as tax revenues plummeted, and federal stimulus provided only temporary relief. By 2014-2015, Sterling was facing what industry veterans would later describe as an existential moment.

In 2015, the company committed to transforming their organization from a business that was 95% Heavy Civil to a results-driven, growth-minded efficient machine. That phrase—"95% Heavy Civil"—captures the strategic trap Sterling had constructed over decades of expansion. The company was almost entirely dependent on government infrastructure spending, bidding competitively against other contractors for work with margins that, at best, covered costs and provided modest profits.

The Board noted the need to "plan and execute the turnaround that is currently underway" as Sterling faced "some significant challenges." The Board Chairman stated that he was grateful for the CEO's continued commitment as Sterling navigated these turbulent waters.

The problems were both cyclical and structural. Cyclically, government infrastructure spending had not recovered from post-crisis austerity. Structurally, Sterling's low-bid business model generated minimal pricing power, leaving the company vulnerable to every cost increase it couldn't pass through. Project selection discipline had been poor, with the company sometimes winning work that turned unprofitable during execution.

Paul Varello, who stepped into the CEO role in February 2015, found a company in need of fundamental surgery. "When I stepped into the CEO role in February of 2015, Sterling was undergoing significant operational and cash flow challenges," said Mr. Varello. "Together with Joe Cutillo, Ron Ballschmiede, our Chief Financial Officer, and Con Wadsworth, our Chief Operating Officer, we have made significant improvements in operating performance, increased margins and backlog and completed a major acquisition."

The turnaround thesis was emerging: Sterling needed to escape the low-bid commodity trap by moving up the value chain into work where relationships, capabilities, and reliability mattered more than price alone. It needed to diversify away from pure public-sector exposure. And it needed operational discipline to improve margins on existing work while avoiding the money-losing projects that had plagued the company.

What Sterling required was someone who could see beyond the current business model—someone with experience transforming commodity businesses into differentiated platforms. In October 2015, the company found that person.

V. The Joe Cutillo Era Begins: Turnaround & Transformation (2015–2017)

Joe Cutillo didn't look like a typical heavy civil construction executive. Joe Cutillo has served as the Chief Executive Officer of Sterling Infrastructure, Inc. since 2017 and brings 30 years of experience leading complex, transformational change to the role. Before joining Sterling in 2015, Mr. Cutillo served as President and Chief Executive Officer of Inland Pipe Rehabilitation LLC, a $200 million private equity-backed trenchless pipe rehabilitation company, from 2008 to 2015. Prior to this, he held leadership roles at Contech Construction Products, Ingersoll-Rand Corp, and General Electric.

That background—General Electric, Ingersoll-Rand, private equity-backed specialty contractors—meant Cutillo understood both operational excellence and strategic repositioning. At Inland Pipe Rehabilitation, he grew the business from a start-up acquisition to the second largest trenchless rehabilitation pipe business in the U.S. He knew how to take a niche specialty service and build it into a market leader.

He joined the Company in October 2015 as Vice President, Strategy & Business Development. In May 2016, he was promoted to Executive Vice President and Chief Business Development Officer. In February 2017, he was promoted to President of the Company and in April 2017 he was promoted to Chief Executive Officer.

His rapid rise through Sterling's ranks reflected the urgency of the turnaround and the board's confidence in his strategic vision. That vision was multi-pronged:

Back in 2016, we initiated a turnaround and began transforming the company from a heavy civil construction business to a diversified infrastructure service provider. We applied our core capabilities to end markets with long-term sustainable growth drivers, including the data center build out, onshoring of manufacturing and major U.S. infrastructure investment. We started our transformation with the turnaround of our Transportation Solutions business, which at the time was doing a lot of low-bid (and low margin) heavy highway work, and moved that business into higher-margin offerings including alternative delivery, aviation, and rail. Through this process, we increased operating margins in this business by over 700 basis points.

Seven hundred basis points of margin improvement—from roughly 5% operating margins to nearly 12%—represents a fundamental transformation in business quality. Cutillo achieved this through relentless bid discipline, refusing work that didn't meet margin thresholds regardless of how hungry the sales team was for revenue. He shifted the mix toward alternative delivery projects where Sterling's capabilities commanded premium pricing. And he invested in aviation and rail expertise where competition was less intense than in highway construction.

Since 2016, Sterling has improved bid discipline to reduce the likelihood of underperforming project margins. This sounds simple but requires cultural change throughout an organization. Construction companies are culturally predisposed to chase volume—the instinct to "keep the crews busy" leads to accepting marginal work that destroys value. Breaking that instinct required new metrics, new incentives, and relentless communication about the strategy.

"While we still have much to accomplish to meet our goals, I firmly believe that Sterling is a business with tremendous potential to generate value for our shareholders as we continue to execute on our strategic growth initiatives. It is an honor for me to lead and serve Sterling's 1,900 employees, and I consider it a privilege to have worked side-by-side with Paul, our Board of Directors, and a very talented leadership team."

The transformation of the Transportation business was necessary but not sufficient. Cutillo's bigger insight was that Sterling's core capabilities—project execution, equipment management, client relationships—could be applied to adjacent markets with better structural economics. The question was which adjacent markets, and how to enter them.

VI. Building the Platform: Strategic Acquisitions (2017–2022)

The Cutillo playbook had three pillars. First, fix the core Transportation business through bid discipline and mix shift. Second, identify adjacent markets with superior structural economics—higher margins, better growth, less cyclicality. Third, enter those markets through programmatic acquisitions of best-in-class operators, preserving their entrepreneurial cultures while providing Sterling's capital and scale.

Sterling is committed to a programmatic acquisition strategy; one that creates new platforms within higher-margin, specialty end markets that serve to broaden its portfolio of products, services and customers. Sterling has pursued platform acquisitions which are accretive to our financial results and with gross margin profiles at or above 15%.

That 15% gross margin threshold was the filter. Traditional highway work often generated gross margins in the high single digits. Cutillo wanted businesses that could produce double-digit gross margins because they operated in markets where relationships and capabilities mattered more than price.

Tealstone (2017) - Building Solutions:

Sterling announced that it has completed the previously announced acquisition of Tealstone Construction ("Tealstone"), a leading Texas-based concrete construction company, for approximately $85 million. It serves commercial contractors and multi-family developers, as well as national homebuilders in Texas and Oklahoma.

Tealstone Residential Concrete and Tealstone Commercial are located in Denton, TX. The residential division builds foundations for single family homes throughout the Dallas-FT Worth, Houston and Phoenix area. The commercial division builds foundations for multi-family homes and projects such as parking structures and commercial developments throughout Texas. Tealstone serves the nation's top builders in the fastest-growing markets.

Tealstone represented Sterling's entry into Building Solutions—specifically, concrete foundations for residential and commercial construction. The logic was compelling: Tealstone had established relationships with the nation's largest homebuilders, who valued reliability and quality over penny-pinching on foundations. Housing construction was growing rapidly in Texas, Florida, and Arizona, and Tealstone's expertise was highly portable to these markets.

Joe Cutillo stated, "We view the acquisition of Tealstone as the next step in transforming the Company. In addition to its revenue and income, it is key to advancing our strategy of expanding into adjacent markets. The strong talent of the Tealstone management team and the relationships they have established with their customers will allow for growth opportunities with their existing customers into our other markets."

Plateau Excavation (2019) - E-Infrastructure:

If Tealstone was important, Plateau Excavation was transformative. Over the past three decades, Plateau Excavation has been a part of the phenomenal commercial, residential and industrial growth of Georgia and the entire Southeast region.

"Sterling's acquisition of Plateau aligns directly with our strategic growth plan as it meets our key criteria of expansion into adjacent markets, diversification of revenue sources and customer base, and enhancement of our overall margin mix while reducing our risk," said Joe Cutillo. "Plateau is a transformational acquisition in that it not only complements our core heavy civil construction and commercial concrete businesses, but also gives Sterling access to new geographies and rapidly growing end markets."

Plateau's full-year 2018 revenues were approximately $290 million. Excluding transaction related costs, the acquisition is expected to be accretive to Sterling's gross and EBITDA margins, earnings per share and free cash flow beginning in the fourth quarter of 2019.

Plateau's importance lay in its customer base and capabilities. The company had become the contractor of choice for large-scale site development serving e-commerce distribution centers, data centers, and industrial facilities in the Southeast. These were projects for Amazon, Microsoft, Facebook, and their developers—companies that valued on-time delivery above all else and were willing to pay premium prices for contractors who could execute.

Petillo (2021) - E-Infrastructure:

Sterling closed on the acquisition of Petillo Incorporated and its related operating entities on December 30, 2021. Petillo is a leading specialty site development solution provider in the Northeast and Mid-Atlantic. Founded in 1994 by owner and CEO Michael Petillo, Petillo has seen compound revenue growth from 2017 to 2021 of 29% through continued expansion of its geographic footprint, customer base and service offerings.

"Their entrepreneurial spirit focused on delivering customer-centric solutions coupled with their geographic footprint will enable us to service our key blue-chip e-commerce customers up and down the entire East Coast with even more offerings than we had before. Petillo's capabilities along with our current Plateau capabilities will not only create one of the largest specialty site development companies in the U.S. but will also add broader capabilities and service offerings to both end markets."

Petillo's 2021 revenues and income from operations were expected to be approximately $212 million and $29 million, respectively. The aggregate consideration of $195 million paid on the Closing Date consisted of $175 million of cash and 759,447 shares of Sterling common shares valued at $20 million.

With Petillo, Sterling gained coverage of the entire East Coast—from the data center corridor of Northern Virginia through the logistics hubs of New Jersey and into the emerging data center markets of the Mid-Atlantic. The combination of Plateau and Petillo created a dominant footprint in exactly the markets where hyperscaler capital expenditure was accelerating.

Since 2017, the Company has created its E-Infrastructure Solutions and Building Solutions segments with the significant acquisitions of Plateau, Petillo and Tealstone, with gross margin profiles at or above 15%.

The acquisition strategy was remarkably consistent: buy best-in-class operators, pay fair prices, preserve entrepreneurial cultures, and let the acquired companies continue serving customers while benefiting from Sterling's capital and scale. It was the opposite of the strip-and-flip private equity playbook—Sterling was building for the long term.

VII. The Rebrand & Three-Segment Structure (2021–2022)

By 2021, the transformation was evident in Sterling's financial statements, but the company's name and identity hadn't caught up. In 2021, the company rebranded from Sterling Construction Company to Sterling Infrastructure, Inc., reflecting its evolution into a comprehensive infrastructure solutions provider with capabilities spanning transportation, e-infrastructure, and building solutions. This strategic repositioning has allowed Sterling to capitalize on growing infrastructure needs across various sectors, particularly in high-growth areas such as data centers and e-commerce facilities.

The company was formerly known as Sterling Construction Company, Inc. and changed its name to Sterling Infrastructure, Inc. in June 2022.

The three-segment structure that emerged tells the story of Sterling's transformation:

The E-Infrastructure Solutions segment provides site development services for the blue-chip end users in the e-commerce distribution center, data center, manufacturing, warehousing, and power generation sectors.

The Transportation Solutions segment is involved in the development of infrastructure and rehabilitation projects for highways, roads, bridges, airports, ports, rail, and storm drainage systems for the departments of transportation, regional transit, airport, port, water, and railroads authorities.

The Building Solutions segment provides residential and commercial concrete foundations for single-family and multi-family homes, parking structures, elevated slabs, other concrete work for developers and general contractors.

The structural elegance of this portfolio is worth appreciating. E-Infrastructure provides secular growth tied to the digitization of the economy and the reshoring of manufacturing. Transportation provides steady cash flows from government infrastructure spending—cyclical, but counter-cyclical to private construction. Building Solutions provides exposure to housing demand while leveraging relationships with national homebuilders.

Once primarily a highway and bridge construction company, Sterling is now an infrastructure solutions provider with a portfolio of diversified, value-added services and an expanded footprint in high-growth end markets.

Whether it's bidding on a new project, extending customer services, or planning for future infrastructure endeavors, Sterling's fiscal approach is always predicated on rock-solid, well-founded strategy and an unwavering commitment to building trust and delivering value for our investors, customers, and society at large. Fearless and forward-thinking, we are driven by a passion for progress.

The operating model emphasized subsidiary autonomy within a disciplined capital allocation framework. Sterling benefits from a roster of companies with unmatched quality, sound management, and proven performance. Our subsidiaries have the autonomy they need to make decisions at the local level and the freedom to respond to the market's ever-changing needs.

This decentralized approach preserved the entrepreneurial cultures that made acquisition targets successful in the first place. Local managers maintained client relationships, made hiring decisions, and managed projects. Corporate provided capital allocation, strategic guidance, and shared services. It was a classic holding company model adapted for the construction industry.

VIII. The AI Data Center Boom: Perfect Timing (2022–Present)

Sometimes in business, preparation meets opportunity in ways that generate returns far exceeding what any strategy could have planned. Sterling's decade-long transformation positioned it perfectly for a boom that would reshape the global economy: the explosion of artificial intelligence.

Artificial intelligence has developed rapidly in recent years, with tech companies investing billions of dollars in data centers to help train and run AI models. The expansion of data centers has raised questions on several fronts, including the effect these facilities may have on energy and the environment as the United States seeks an edge in the global AI race.

Data center spending is projected to surpass $1 trillion by end of decade. Fueled by the race for AI supremacy, the global data center infrastructure market is on course to surpass $1 trillion in annual spending by 2030. This growth is being propelled by the world's largest technology companies. In 2024, spending reached $290 billion, with growth set to accelerate in 2025. Of the $290 billion, Alphabet, Microsoft, Amazon, and Meta invested nearly $200 billion in CapEx, a figure expected to climb by over 40% in 2025 as they rush to build the computational power needed to train and deploy next-generation AI models.

Total annual U.S. electricity consumption hit a record high in 2024, and that ceiling could rise if data centers continue expanding at their current pace. U.S. data centers consumed 183 terawatt-hours (TWh) of electricity in 2024, according to IEA estimates. That works out to more than 4% of the country's total electricity consumption last year – and is roughly equivalent to the annual electricity demand of the entire nation of Pakistan. By 2030, this figure is projected to grow by 133% to 426 TWh.

Sterling's E-Infrastructure segment was already built to serve data center customers when AI created unprecedented demand growth. "The data center market remains extremely robust as our customers work to build the infrastructure to support future data demand including the needs of artificial intelligence (AI) and other emerging technologies," stated Joe Cutillo.

Sterling announced that Plateau Excavation, a Sterling subsidiary, has been awarded a data center project in the southeastern U.S. with a value of approximately $100 million. The project scope covers 280 acres and includes 125,000 linear feet of underground infrastructure installation. Work was expected to begin in the second quarter of 2024.

Sterling Infrastructure is a key player in E-Infrastructure, supporting data centers and e-commerce giants like Amazon, Microsoft, and Meta.

The financial impact has been extraordinary. E-Infrastructure revenue was $937 million in 2023, 48% of Sterling's total last year. However, E-Infrastructure operating income was $141 million, 62% of the total. This fast-growing segment thus also happens to be far and away the most profitable part of this construction business. Growth and higher profit margins over time can equate to big stock gains.

Our most exciting segment is E-infrastructure which is focused on data centers, which now represent over 40% of our segment backlog, as well as manufacturing and e-commerce distribution. On the manufacturing front we are engaged in battery plants, solar panel plants, and small manufacturing facilities and are anticipating a wave of chip plants, pharma, and food processing facilities in the next few years. The shift toward domestic manufacturing was spurred by COVID-19 highlighting supply chain vulnerabilities, and signifies a move towards supply chain security over cost.

Why has Sterling succeeded in this market? The answer lies in the nature of data center construction. These are not commodity projects awarded to the lowest bidder. They are mission-critical facilities where on-time delivery can be worth billions to customers whose AI training schedules depend on infrastructure availability.

In our E-infrastructure projects, we are an insurance policy for our clients. Meeting deadlines is critical, especially when our site development work is part of a larger multi-billion dollar project. A two-week delay on our end could result in a six-month delay for the entire project. Our ability to deliver on time ensures that clients continue to choose us for subsequent projects.

The company has positioned itself at the center of long-term demand drivers like data centers, e-commerce distribution and critical transportation projects, areas where reliability and speed often matter more than lowest cost. Sterling's E-Infrastructure Solutions segment has become its strongest growth engine, with backlog climbing 44% year over year at the end of the second quarter. Mission-critical projects, particularly data centers, now represent a majority of its pipeline. Management notes that its ability to complete large-scale, multi-phase projects on or ahead of schedule has translated into both repeat business and pricing power.

IX. Recent Performance & S&P MidCap 400 (2024–2025)

The numbers tell a story of accelerating momentum. In 2024, Sterling Infrastructure's revenue was $2.12 billion, an increase of 7.28% compared to the previous year's $1.97 billion. Earnings were $257.46 million, an increase of 85.68%.

Q3 2025 saw revenues of $689.0 million. Revenues increased 32% excluding RHB from the prior year quarter. The CEC acquisition contributed $41.4 million to revenue in the quarter. Gross margin of 24.7%, up from 21.9%. Net income of $92.1 million, or $2.97 per diluted share, increases of 50% and 51%, respectively, and a new third quarter record.

The E-Infrastructure Solutions segment, which focuses on data centers, semiconductor fabrication, and e-commerce distribution centers, delivered exceptional results with revenue growing 58% over the prior year (42% excluding the CEC acquisition).

Sterling's remaining performance obligations (RPOs), also referred to as backlog, reached $2,575.4 million as of September 30, 2025, representing a substantial increase from $1,693.2 million at the end of 2024. This growth was primarily driven by the E-Infrastructure Solutions segment, which saw its backlog increase from $1,032.1 million to $1,808.2 million during this period. The acquisition of CEC contributed significantly to this backlog expansion, adding $475 million to signed backlog and $335 million to unsigned awards. Importantly, the company noted that current backlog figures don't include approximately three-quarters of a billion dollars of future phases of work associated with current projects.

The most recent strategic move—the CEC acquisition—extended Sterling's capabilities further into the data center value chain. Sterling announced that it has completed its previously announced acquisition of Irving, Texas-based CEC Facilities Group, LLC, et al. ("CEC"), a leading specialty electrical and mechanical contractor.

Sterling announced that it has signed a definitive agreement to purchase substantially all of the assets of Irving, Texas-based CEC Facilities Group, LLC ("CEC") a leading specialty electrical and mechanical contractor. The upfront purchase price at closing totals $505 million, consisting of $450 million in cash (subject to certain adjustments) and $55 million in Sterling Common Stock. Additionally, CEC has an earn out opportunity contingent upon achieving certain operating income targets through December 31, 2029.

As part of Sterling's E-Infrastructure Solutions segment, CEC will continue to provide advanced electrical and mechanical services for mission-critical projects, including data centers, semiconductor facilities, manufacturing, and large-scale infrastructure. CEC Facilities Group, LLC is a specialty contractor delivering electrical, mechanical, technology, and infrastructure solutions for some of the nation's most demanding projects.

The market has recognized Sterling's transformation. Sterling Infrastructure Inc. will replace Light & Wonder Inc. in the S&P MidCap 400, and Red Rock Resorts Inc. will replace Sterling Infrastructure in the S&P SmallCap 600 effective prior to the opening of trading on Thursday, November 13.

Moving from the SmallCap 600 to the MidCap 400 is more than symbolic. It forces index funds tracking the S&P MidCap 400 to purchase Sterling shares while those tracking the SmallCap 600 must sell. More importantly, it signals that Sterling has graduated from small-cap status into a more mature company with greater institutional following and analyst coverage.

Sterling announced that its Board of Directors authorized a new stock repurchase program. Under the new program, which becomes effective today, Sterling may repurchase up to $400 million of its outstanding common stock over the next 24 months. The new program replaces the Company's previous repurchase program, which was set to expire on December 5, 2025. "This expanded share repurchase authorization reflects our continued confidence in Sterling's outlook," stated Joe Cutillo. "With our strong balance sheet and cash flow, we are well-positioned to pursue a balanced capital allocation strategy that supports our investments in organic growth and strategic acquisitions, while returning capital to shareholders."

X. The Business Model Deep Dive

Sterling's business model is deceptively simple: build infrastructure that other companies need to operate. But the sophistication lies in customer selection, project execution, and capital allocation.

The majority of the revenue is generated from E-Infrastructure Solutions. This represents a dramatic shift from the company that was "95% Heavy Civil" less than a decade ago. The segment evolution reflects a fundamental change in customer mix, margin profile, and growth trajectory.

The customer relationship model differs dramatically across segments. In Transportation Solutions, Sterling serves government agencies through competitive bidding, though the company has shifted toward alternative delivery methods that reward capability over pure price. In Building Solutions, relationships with national homebuilders provide recurring work as builders develop new subdivisions. But E-Infrastructure is where Sterling's model shines brightest.

Meeting deadlines is critical, especially when our site development work is part of a larger multi-billion dollar project. A two-week delay on our end could result in a six-month delay for the entire project. Our ability to deliver on time ensures that clients continue to choose us for subsequent projects.

This dynamic creates a virtuous cycle. Sterling delivers a data center site on time. The hyperscaler or developer remembers. When the next project comes up—perhaps in a new geography—Sterling gets called first. The relationship deepens, leading to multi-phase projects where Sterling handles successive expansions of a campus.

There are two main aspects to our acquisition strategy. First, we look at the geography of the U.S. and identify large data center and manufacturing growth markets where we currently do not have a presence. We have been successful in redirecting some of our transportation business and assets to support other markets. For example, a large data center customer asked us to do a project in Idaho.

The geographic expansion is customer-driven rather than speculative. When hyperscaler customers enter new markets, they bring Sterling with them, valuing the proven relationship over the unknown quantity of a local competitor.

Myth vs. Reality: Sterling as a "Data Center Play"

| Myth | Reality |

|---|---|

| Sterling is just riding AI hype | Sterling built its E-Infrastructure platform through acquisitions starting in 2017, well before AI became a mainstream investment theme |

| The company depends entirely on data centers | Data centers are the largest category but E-Infrastructure also serves e-commerce, manufacturing, and power generation; Transportation and Building provide diversification |

| Competition will commoditize margins | On-time execution creates switching costs; hyperscalers value relationship continuity over marginal price savings |

| The business is capital-intensive | Construction equipment can be redeployed across projects; Sterling has generated strong free cash flow relative to growth |

XI. Competitive Positioning & Strategic Analysis

Porter's Five Forces Analysis:

Sterling Infrastructure operates in a fragmented industry with competition varying across its three business segments. In the Transportation Solutions segment, Sterling competes with large national and regional heavy civil construction companies such as Granite Construction (GVA), Tutor Perini (TPC), and Primoris Services (PRIM). These competitors typically bid on similar public infrastructure projects, including highways, bridges, and airports. In the E-Infrastructure Solutions segment, which has become Sterling's fastest-growing and highest-margin business, the company faces competition from specialized site development contractors such as MasTec (MTZ) and Quanta Services (PWR). This segment has benefited significantly from the boom in data center construction and e-commerce facility development, with Sterling establishing itself as a preferred partner for major technology companies and developers.

| Force | Assessment | Explanation |

|---|---|---|

| Threat of New Entrants | LOW-MODERATE | Large-scale site development requires significant capital, specialized equipment, experienced workforce, and track record with blue-chip clients. Sterling has become one of the largest and most technologically advanced site infrastructure contractors in the Southeast. New entrants cannot easily replicate decades of relationships and execution track record. |

| Bargaining Power of Suppliers | MODERATE | Materials (concrete, equipment, aggregates) are commoditized but construction labor remains tight. Sterling's scale provides some purchasing power, but labor constraints affect the entire industry. |

| Bargaining Power of Buyers | MODERATE | Blue-chip customers (hyperscalers like Amazon, Microsoft, Meta) have significant leverage, but when Sterling secures large projects, superior performance makes them the first choice for future phases. The value of on-time delivery exceeds marginal price differences. |

| Threat of Substitutes | LOW | Physical infrastructure must be built. No substitute exists for site development, foundations, and civil works. Data centers, highways, and homes all require physical construction. |

| Competitive Rivalry | HIGH | Granite Construction, Tutor Perini, Actividades de Construcción y Servicios, Kiewit, and Kier Group are some of the 84 competitors of Sterling Infrastructure. However, Sterling has differentiated through specialization, customer relationships, and execution track record. |

Another relevant peer is Tutor Perini (TPC), which competes in complex infrastructure and building projects. Tutor Perini has struggled with project delays and cost overruns, which have weighed on earnings consistency. This comparison highlights Sterling's operational discipline—the company has avoided the large project disputes and margin volatility that plague some competitors.

Hamilton Helmer's 7 Powers Framework:

| Power | Present? | Explanation |

|---|---|---|

| Scale Economies | ✓ MODERATE | A higher-value business mix, together with disciplined expense management, positions Sterling as one of the largest specialty site development companies in the Northeastern and Mid-Atlantic U.S. Scale enables equipment sharing, purchasing power, and geographic flexibility. |

| Network Effects | ✗ LIMITED | Construction lacks network effects in the traditional sense, though relationship networks with repeat customers create some switching costs. |

| Counter-Positioning | ✓ STRONG | Traditional heavy civil contractors optimized for low-bid public work cannot easily pivot to relationship-driven private work without cannibalizing existing business models. Sterling's transformation took years. |

| Switching Costs | ✓ MODERATE | On a project basis, customers can switch. But for multi-phase campus developments, switching contractors creates coordination risk, schedule risk, and relationship friction that exceed cost savings. |

| Branding | ✓ MODERATE | Sterling has built a reputation for on-time delivery with hyperscaler customers. This "insurance policy" positioning creates demand-side advantages. |

| Cornered Resource | ✓ MODERATE | Specialized crews, equipment, and project management expertise in data center site development are not easily replicated. Management teams from acquired companies provide institutional knowledge. |

| Process Power | ✓ STRONG | Sterling has strategically positioned itself to focus on higher-margin, specialized infrastructure work rather than competing solely on price in traditional heavy civil construction. This strategy has allowed the company to achieve industry-leading margins compared to many of its peers. |

XII. Bull Case, Bear Case & Investment Considerations

The Bull Case:

The data center buildout is still in early innings. Digital Realty CEO Andy Power described today's AI expansion as "a full-fledged technology race," emphasizing that the industry is still in the "very early innings." If AI adoption continues accelerating, hyperscaler capital expenditure will continue growing, and Sterling's E-Infrastructure backlog will expand further.

In 2024, private investment in US data centers reached a record high. Meanwhile, electric and gas utilities are forecasting a record increase in capex. It is expected to jump 22% year over year to US$212 billion in 2025 across 47 utilities.

By 2028, we expect Sterling to be significantly larger, with more than double our current profitability. The natural tailwinds in our markets and continued acquisition growth will drive this trajectory. The demand for data centers will continue to grow, fueled by AI and increased data requirements. We also anticipate having a fourth segment. For example, one of the areas we have explored is the power grid, which is a multi-trillion-dollar market needing significant upgrades. The U.S. grid and power supply are far behind current demands, and this gap will only widen with the increasing load from electric vehicles, data centers, and manufacturing plants.

Sterling's customer relationships create a moat. When hyperscalers expand to new regions, they bring trusted contractors with them. This geographic expansion opportunity is largely organic—following existing customers into new markets rather than speculatively entering markets and building relationships from scratch.

The reshoring trend provides additional tailwinds. Manufacturing returning to the U.S.—whether semiconductor fabs, battery plants, or pharmaceutical facilities—requires the same site development capabilities Sterling has honed for data centers.

The Bear Case:

The AI investment cycle could slow. If AI models hit capability ceilings, if enterprise adoption disappoints, or if hyperscaler CFOs face pressure to demonstrate ROI on massive capital expenditures, data center construction could decelerate faster than current backlog suggests.

Construction is an inherently cyclical business. Since it's reliant on big tech businesses continuing to ramp up data center and other specialty property development, Sterling could be just one bad year away from losing its high-flying construction stock status. Such is life for highly cyclical companies.

Competition could intensify. As data center construction becomes more attractive, larger contractors like Quanta Services and MasTec are investing in capabilities. While Sterling is making strides in data centers and e-infrastructure, it competes with industry heavyweights such as Quanta Services PWR and MasTec MTZ. Both Quanta Services and MasTec are well-positioned in the digital and clean energy buildout, giving them strong footholds in overlapping markets. Quanta Services brings scale and expertise in utility and grid modernization. MasTec continues to expand aggressively into telecommunications and renewable infrastructure.

Building Solutions faces headwinds from housing affordability challenges. The Building Solutions segment faced challenges due to a slowdown in the housing market, impacting prospective homebuyers' affordability. While E-Infrastructure is growing rapidly, weakness in Building Solutions could offset some gains.

Valuation has expanded dramatically. This year alone, the stock has soared 99.2%, capping off an eye-popping 5-year gain of 1930.2%. Much of the transformation story is now reflected in the stock price. Future returns depend on continued execution and sustained end-market demand rather than multiple expansion.

Key Risks to Monitor:

-

Hyperscaler capex trends: Watch Amazon, Microsoft, Google, and Meta capital expenditure guidance. Any deceleration in data center investment would affect Sterling's E-Infrastructure pipeline.

-

Project execution: Construction margins depend on disciplined execution. Any high-profile project failures or cost overruns could damage both profitability and reputation.

-

Labor availability: Skilled construction labor remains tight. Wage inflation or inability to staff projects could compress margins.

-

Interest rates and housing: Building Solutions depends partly on housing construction, which is sensitive to mortgage rates. Prolonged high rates could extend weakness in this segment.

Key KPIs to Track:

-

E-Infrastructure Backlog Growth: The most important leading indicator for Sterling's highest-margin segment. Watch not just signed backlog but also "unsigned awards" and "future phases" that indicate pipeline visibility.

-

Gross Profit Margin: Sterling's transformation is reflected in margins expanding from single digits to over 20%. Any margin compression would signal competitive or execution challenges.

XIII. Conclusion: AI's Hidden Infrastructure Play

Sterling Infrastructure's transformation from struggling highway contractor to essential AI infrastructure provider represents one of the more remarkable corporate reinventions in recent American business history. Sterling has successfully positioned itself as a leading provider of infrastructure services across three key solution areas. The company's strategic transformation, initiated in 2015, has created a strong, diversified platform with multi-year secular growth drivers.

The company illustrates a timeless business truth: the most valuable opportunities often lie not in building the headline-grabbing technology but in providing the picks and shovels. Hyperscalers racing to build AI capabilities need physical infrastructure—data centers, power connections, site work—before they can deploy a single GPU. Sterling has positioned itself as an indispensable partner in this buildout.

"We build and service the infrastructure that enables our economy to run, our people to move and our country to grow." That CEO quote captures Sterling's value proposition: not glamorous but essential, not headline-grabbing but fundamental to how the modern economy operates.

Sterling's transformation into a high-performing platform is delivering real results. With a disciplined strategy, targeted growth, and a strong balance sheet, the company is not just building infrastructure—it's creating shareholder value.

The question for investors is whether the transformation is complete or whether Sterling can continue compounding value. Management believes significant runway remains. Sterling is playing a critical role in building the manufacturing production coming back to the U.S., the data infrastructure that enables artificial intelligence (AI) and other emerging technologies, critical transportation infrastructure, and the homes we live in. This infrastructure is the foundation of the America of tomorrow.

Whether that vision materializes depends on factors both within Sterling's control (execution, capital allocation, acquisition discipline) and outside it (AI adoption trajectories, interest rates, competitive dynamics). What's undeniable is that Sterling has transformed itself from a commodity business grinding out thin margins into a differentiated platform positioned at the intersection of multiple secular growth trends.

That transformation—from near-death experience to S&P MidCap 400 member, from 95% Heavy Civil to AI's invisible backbone—stands as a case study in strategic repositioning, disciplined acquisition, and the value of preparation meeting opportunity.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube