SPX Technologies: The Phoenix of American Industrial Engineering

I. Introduction & Episode Roadmap

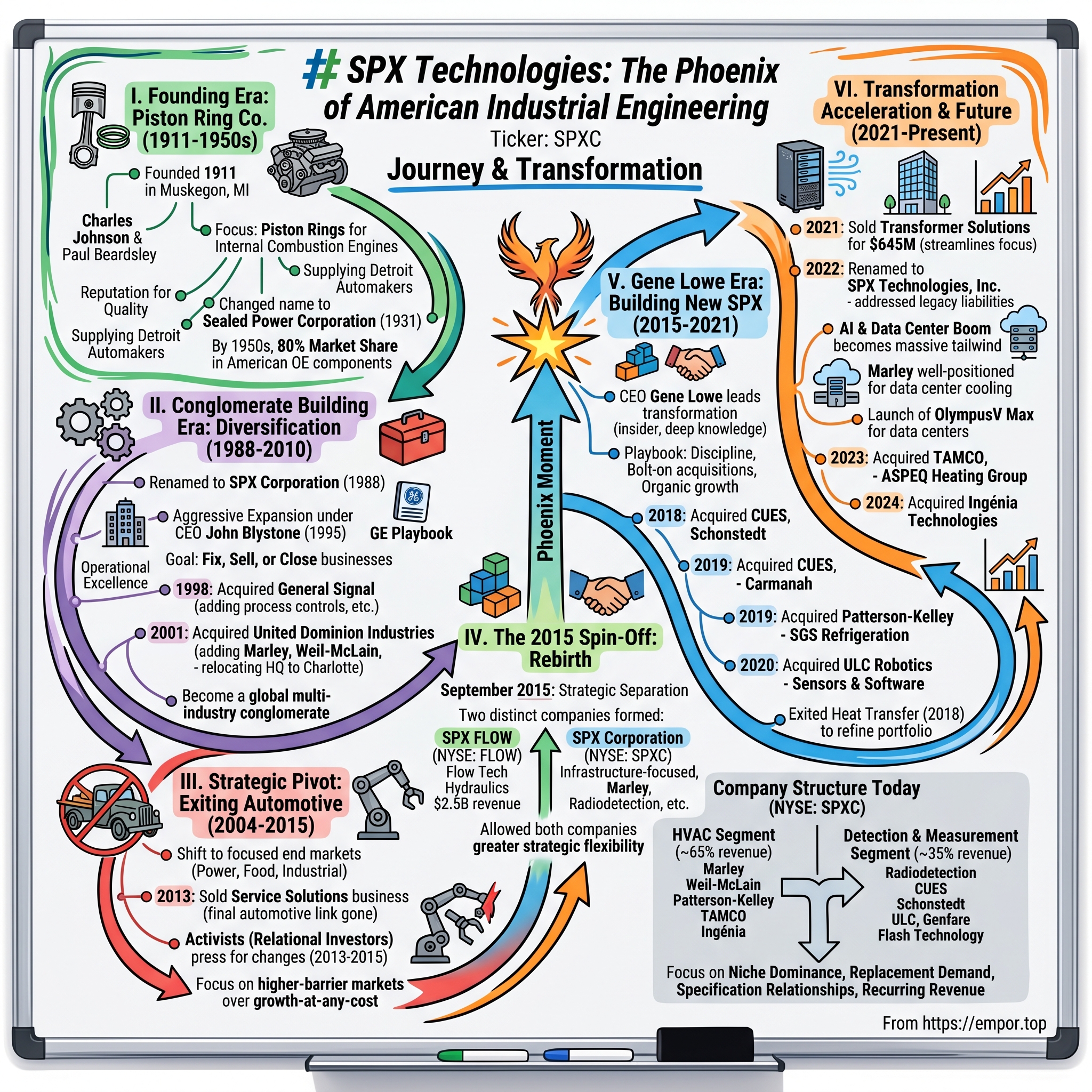

Picture a winter evening in 1911, Muskegon, Michigan—a small industrial city hugging the shores of Lake Michigan, thick with smoke from sawmills and the rhythmic hammering of machine shops. Two entrepreneurs, Charles E. Johnson and Paul R. Beardsley, huddle over blueprints in a cramped workshop, obsessing over one of the internal combustion engine's most critical components: the humble piston ring. What they built that December would survive two world wars, power 80% of American automobiles, morph into a sprawling conglomerate, nearly collapse under its own complexity, and ultimately emerge as one of the most compelling transformation stories in American industrial history.

With more than $2 billion in annual revenue and over 4,400 employees in 16 countries, SPX offers a wide array of highly engineered infrastructure products with strong brands. The company trades on the NYSE under the ticker SPXC, sporting a market capitalization of approximately $10-11 billion—a remarkable valuation for what began as a modest piston ring shop on the shores of the Great Lakes.

The central question every investor should be asking: How did a 113-year-old piston ring company transform into a focused, high-margin infrastructure play that delivered 70% annual EPS growth during certain periods? And more importantly, is the transformation durable?

Gene Lowe, President and CEO, remarked, "I am very pleased with our full-year 2024 results, including Adjusted EBITDA growth of 36% and Adjusted EPS growth of 29%, which was near the top end of our guidance range." These are not the numbers of a stodgy industrial dinosaur—they're the metrics of a company operating at the intersection of infrastructure modernization and technological disruption.

The SPX story unfolds in distinct acts: the automotive origin myth, the GE-influenced conglomerate expansion under John Blystone, the activist pressure and strategic pivot, the critical 2015 spin-off that created two separate companies, and finally the Gene Lowe era of disciplined acquisition and operational excellence. Expansion in data center cooling solutions, highlighted by the new OlympusV Max launch, which addresses the rapidly growing demand for energy-efficient, large-scale data center infrastructure, positions SPX to meaningfully expand its addressable market and top-line growth as hyperscale projects accelerate into 2026.

The company now operates in two segments: HVAC (approximately 65% of revenue) and Detection & Measurement. The HVAC segment encompasses the legendary Marley cooling tower brand—a name that has dominated evaporative cooling for over a century—alongside Weil-McLain boilers, Patterson-Kelley commercial heating equipment, and a growing engineered air movement platform. Detection & Measurement includes underground utility locators (Radiodetection), pipeline inspection robotics (CUES, ULC Robotics), transit fare systems (Genfare), and communication technologies serving defense and maritime markets.

What makes SPX particularly interesting for long-term fundamental investors is the convergence of three powerful tailwinds: the data center construction boom driven by AI infrastructure requirements, aging North American infrastructure requiring inspection and replacement, and the continued push for energy-efficient building systems. Management has positioned the company directly in the path of these secular trends while maintaining the operational discipline that transforms revenue growth into outsized earnings expansion.

II. Founding Era: The Piston Ring Company (1911-1950s)

The story begins in the waning months of 1911, when the automobile was still a novelty—a loud, unreliable contraption that terrified horses and excited the imaginations of tinkerers and dreamers across America. SPX was founded on December 20, 1911 in Muskegon, Michigan, as the Piston Ring Company by Charles E. Johnson and Paul R. Beardsley.

What did Johnson and Beardsley see that others missed? The piston ring was a seemingly mundane component—a small metal ring fitted into grooves around a piston to seal the combustion chamber, prevent oil from entering the cylinder, and manage heat transfer. But in an era of rapidly proliferating automobile designs, each engine required precisely engineered rings. The company was entirely devoted to the production of piston rings of leading engine builders.

In 1912, the Piston Ring Company officially opened for business in Muskegon, Michigan. The company designed and manufactured original equipment components for Detroit's largest car companies and quickly earned a reputation for quality products serving the rapidly developing automobile industry.

Muskegon was a strategic choice. The city sat within the gravitational pull of Detroit's emerging automotive ecosystem while maintaining the lower costs and skilled labor pool of Michigan's industrial heartland. The founders understood something crucial about the automotive supply chain: the car companies themselves were assemblers, not manufacturers. They needed reliable suppliers who could deliver precision-engineered components at scale.

The First World War provided an unexpected catalyst. As America's industrial capacity pivoted toward the war effort, engine technology advanced rapidly—and with it, the demand for higher-performance piston rings capable of withstanding greater pressures and temperatures. The Piston Ring Company emerged from the war years with enhanced capabilities and deeper relationships with engine manufacturers.

After acquiring the Accuralite Company in 1931, the company changed its name to "Sealed Power Corporation" and started manufacturing piston rings, pistons and cylinder sleeves for military applications.

The Accuralite acquisition represented more than product diversification—it signaled a strategic evolution from component supplier to systems provider. Rather than simply making piston rings, Sealed Power now offered the complete piston assembly: rings, pistons, and cylinder sleeves. This vertical integration created stickier customer relationships and higher margins.

The Second World War amplified these trends exponentially. America's wartime industrial mobilization required precision engine components for everything from tanks to aircraft to naval vessels. Sealed Power's military contracts funded massive capacity expansion and technology development that would pay dividends for decades.

By the 1950s, the company had distributors in every state and in more than 40 countries. At the time, Sealed Power products were used as original equipment in more than 80 percent of American-made cars and trucks.

Think about that number: 80% market share in original equipment piston components for American vehicles. This wasn't just a successful company—it was an essential node in the American industrial ecosystem. General Motors, Ford, Chrysler—they all depended on Sealed Power. The company had achieved something rare in industrial markets: specification dominance. Engineers designing new engines specified Sealed Power components because that's what they knew worked.

But by the late 1950s, the seeds of future challenges were already germinating. The U.S. automotive industry was consolidating, Japanese competitors were emerging, and the original equipment market was becoming brutally competitive. Sealed Power's leadership began looking beyond piston rings for growth.

III. Conglomerate Building Era: Diversification & Acquisitions (1988-2010)

The transformation from Sealed Power Corporation to SPX Corporation represents one of the most aggressive—and ultimately problematic—diversification strategies in American industrial history. By 1988, and after a number of strategic acquisitions to further diversify the company into a replacement parts and specialty service tool manufacturer, the company changed its name to SPX Corporation.

The name change signified a fundamental reimagination of the company's identity. SPX wasn't just a piston ring maker anymore—it was a diversified industrial platform. But what did "SPX" even mean? The letters weren't an acronym for anything specific; they were chosen to signal a break from the automotive-focused past while retaining the "SP" from Sealed Power as a subtle nod to heritage.

When he was hired as chairman and CEO of SPX Corp. in December 1995, John Blystone knew that turning around the troubled Muskegon, MI-based producer of specialty tools and original equipment components to the automotive industry would be no joyride. After building a solid reputation selling specialty tools and diagnostic equipment to auto dealers and mechanics, SPX had faltered, piling on new divisions and several hundred million dollars of high-yield, long-term debt.

Enter John Blystone—a General Electric-trained executive who would fundamentally reshape SPX's trajectory. To head SPX, Blystone left a promising career at GE, which he joined in 1978. Except for three years at Tenneco, he learned sales and marketing at the foot of Jack Welch's spinning wheel. "Welch did things back in the early 1980s that people are starting to do now," Blystone asserts.

Blystone arrived at SPX with the playbook that had made Welch famous: fix, sell, or close underperforming businesses; aggressively pursue acquisitions in attractive markets; drive operational excellence through rigorous process management; and reward performance while ruthlessly culling underperformers.

Among the first divestments, in a clear signal of a new era, was the company's Sealed Power Division, its founding business, which was sold to Dana Corporation in early 1997 for $223 million. Other early moves in the Blystone era were the consolidation of divisions to save costs and the elimination of 1,100 jobs by mid-1997.

This was a watershed moment. The company sold its founding business—the very reason SPX existed—because Blystone determined that automotive components offered insufficient growth potential. The message to employees, investors, and competitors was unmistakable: nothing was sacred, and everything was on the table.

What followed was an acquisition spree of remarkable ambition. 1998: General Signal Corporation, maker of products for the process control, electrical control, and industrial technology industries, is acquired for $2.3 billion.

The General Signal deal was transformative. In one stroke, SPX acquired significant positions in industrial process controls, power generation equipment, and sensing technologies. The company was no longer a diversified automotive supplier—it was a multi-industry conglomerate.

In May 2001 SPX completed the acquisition of United Dominion Industries Limited in an all-stock transaction valued at about $1.9 billion, including the assumption of $876 million in debt. Based in Charlotte, North Carolina, United Dominion was a diversified manufacturer of flow technology, engineered machinery, test instruments, and other products. The firm had annual sales of about $2.4 billion.

The United Dominion acquisition doubled SPX's revenue to over $4 billion and brought the Marley cooling tower brand, Weil-McLain boilers, and numerous other industrial brands into the portfolio. The company announced that it would relocate its company headquarters from Muskegon to Charlotte, North Carolina. In a press release, Blystone explained the reasoning: "In choosing Charlotte, we considered total corporate costs, labor pool, access to metropolitan airports that offer better domestic and international flights, affordable housing, employment opportunities for dual income families and overall quality of life."

By the mid-2000s, SPX had become exactly what Blystone envisioned: a sprawling, diversified industrial conglomerate with operations spanning continents and end markets. Revenues exceeded $5 billion. The company operated in automotive diagnostics, cooling towers, transformers, food processing equipment, fluid handling, and dozens of other categories.

But the strategy's weaknesses were becoming apparent. Managing such diverse operations required extraordinary management bandwidth. Capital allocation decisions became increasingly complex—how do you compare investment opportunities across fundamentally different industries? And investors struggled to value the company, applying the dreaded "conglomerate discount" because they couldn't easily analyze the constituent businesses.

Blystone joined SPX in December 1995. During his nine years leading the company, he helped transform SPX from a small automotive supplier into a global multi-industry company. When Blystone departed in 2004, he left behind a company fundamentally different from the one he inherited—but also one wrestling with the strategic contradictions inherent to conglomerate structures.

IV. Strategic Pivot: Exiting Automotive (2004-2015)

The years following Blystone's departure marked a period of strategic soul-searching for SPX. The company's leadership recognized that the conglomerate model, while successful in building scale, had created structural challenges that hampered value creation.

Beginning in 2004, the company started to shift to a narrower focus on key end markets related to power and energy, food and beverage, and industrial process infrastructure. As a result, SPX Corporation sold off several businesses and re-invested in strategic acquisitions that helped anchor its growth in those end markets.

This wasn't a sudden about-face but rather a gradual recognition that the "do-a-little-of-everything" approach had run its course. The company began trimming non-core businesses while doubling down on markets where it had genuine competitive advantages.

This strategy resulted in SPX exiting the automotive industry entirely with the sale of its Service Solutions business in 2013.

The Service Solutions sale to Robert Bosch GmbH deserves particular attention. This business—automotive diagnostic equipment, repair tools, and related services—was highly profitable and represented SPX's last remaining connection to its automotive roots. Selling it generated approximately $1.15 billion in cash, but more importantly, it signaled a complete strategic break from the company's founding industry.

The automotive exit illustrates a crucial principle in corporate strategy: sometimes the best decisions are the ones that seem to contradict a company's identity. SPX had been an automotive company for 100 years. Its heritage, its culture, its organizational DNA were automotive. Walking away from that heritage required extraordinary conviction.

But the rationale was sound. The automotive aftermarket was consolidating rapidly, with margins compressing as large distributors gained bargaining power. Meanwhile, SPX's infrastructure-focused businesses—cooling towers, transformers, detection equipment—operated in markets with higher barriers to entry, better pricing power, and more attractive long-term growth prospects.

By 2013, activist investors had taken notice of SPX's strategic ambiguity. In February 2013, Relational Investors acquired a 8.8% stake in SPX Flow's former parent company, SPX Corporation, and claimed that "the company's shares and profit suffered from its 'growth-at-any-cost strategy' and 'excessive prices' paid for acquisitions." This followed SPX Corporation's failed takeover bid for competitor Gardner Denver, which had a larger market capitalization than SPX Corporation at that time.

Relational Investors eventually increased its stake in SPX Corporation to as high as 15.7% in 2015, which is likely to have been the catalyst for the spin-off of SPX Flow.

Activist pressure forced management to confront uncomfortable questions: Why was this collection of businesses more valuable together than apart? What synergies actually existed between cooling towers and food processing equipment? Was the complexity of managing dozens of disparate businesses destroying value rather than creating it?

The honest answer was that SPX had become a holding company masquerading as an operating company. The only thread connecting its businesses was ownership structure, not operational synergy. This realization set the stage for the most consequential decision in the company's modern history.

V. The 2015 Spin-Off: The Rebirth Moment

September 26, 2015. Mark this date. It represents the inflection point that transformed a struggling conglomerate into the focused, high-performing company that exists today.

CHARLOTTE, N.C., Sept. 28, 2015 /PRNewswire/ -- SPX FLOW, Inc. (NYSE:FLOW) announced today that it has completed its spin-off from its former parent company and its stock will begin "regular way" trading today on the New York Stock Exchange under the symbol "FLOW".

The spin-off was designed with surgical precision. "Today marks a significant milestone in the long history of our Company and also the beginning of a new chapter as we work to grow, advance and redefine SPX Corporation," said Mr. O'Leary. "Going forward, we will have greater strategic flexibility and will also have an increased ability to attract an investor base suited to our Company's specific operational and financial characteristics."

The transaction separated SPX into two distinct publicly traded entities:

SPX FLOW (NYSE: FLOW): Inherited the Flow Technology reportable segment and Hydraulic Technologies business—essentially the food and beverage processing equipment, power and energy flow solutions, and industrial flow products. This business had approximately $2.5 billion in annual revenues and 8,000 employees.

SPX Corporation (NYSE: SPXC): Retained the thermal equipment and services segment, power transformers, Radiodetection, Genfare, and communications businesses—the infrastructure-focused operations that would become the foundation of today's company.

The strategic logic was compelling: each company could now pursue its own optimal strategy without being constrained by the needs of dissimilar businesses. SPX FLOW could focus on food and beverage processing, where growth opportunities were tied to emerging market consumption patterns. The "new" SPX could concentrate on North American infrastructure, where aging installed bases and regulatory requirements created steady replacement demand.

SPX Corporation is led by non-executive Chairman, Patrick O'Leary and President and Chief Executive Officer, Gene Lowe. "Today marks a significant milestone in the long history of our Company and also the beginning of a new chapter as we work to grow, advance and redefine SPX Corporation," said Mr. O'Leary. "Going forward, we will have greater strategic flexibility and will also have an increased ability to attract an investor base suited to our Company's specific operational and financial characteristics."

Gene Lowe's appointment as CEO was critical. Unlike Blystone, who came from outside to revolutionize a troubled company, Lowe was an insider who understood SPX's culture, capabilities, and competitive positioning at a deep level.

Gene joined SPX in 2008, holding multiple strategic leadership positions, most recently as the president of SPX's Thermal Equipment and Services segment. His tenure at SPX also includes roles leading the Evaporative Cooling business and the marketing, strategy, and business development functions within the Thermal segment where he focused on driving differentiation through technology innovation and operational initiatives.

His previous roles at SPX include Segment President and Vice President of Global Business Development, showcasing his depth of knowledge in thermal equipment and cooling solutions. Gene's educational background includes an MBA from Dartmouth College and a BS in Management Science from Virginia Tech. He is also a board member for Federal Signal Corporation and the Virginia Tech APEX Center for Entrepreneurs.

Lowe's background in cooling technology proved particularly valuable. He understood that Marley wasn't just a brand—it was an installed base of relationships with engineers, contractors, and facility managers who specified Marley products because they trusted the quality and knew the service network would support them.

The immediate post-spin-off period was challenging. The "new" SPX inherited significant exposure to power generation equipment—a cyclical business facing headwinds from the shift away from coal-fired power plants. But Lowe and his team used this period to further refine the portfolio, shedding businesses that didn't fit the emerging strategic vision while acquiring capabilities that strengthened core platforms.

For investors, the spin-off represents a case study in value creation through corporate simplification. The conglomerate structure had obscured the genuine excellence of certain SPX businesses while diluting management focus across too many priorities. Separation allowed each company to tell its own story, attract its own investor base, and pursue its own capital allocation priorities.

VI. Gene Lowe Era: Building the New SPX (2015-2021)

The first years following the spin-off required Gene Lowe to make difficult choices about which businesses deserved investment and which should be divested. The overarching principle: concentrate resources on businesses with leading market positions, high barriers to entry, and attractive long-term growth prospects.

After splitting from SPX Flow, SPX acquired both CUES Inc., a pipeline inspection manufacturer, and Schonstedt Instrument Co., a manufacturer and distributor of magnetic locator products, in 2018. In December of that year, SPX announced that it would also acquire the marine and aviation warning-light corporation Carmanah Technologies. In 2019, the corporation acquired SGS Refrigeration Inc., a manufacturer and supplier of industrial refrigeration products, following its ongoing partnership since 2015. Patterson-Kelley was acquired that same year to join SPX's HVAC solutions division.

Each acquisition followed a consistent playbook:

-

Target businesses with leading positions in niche markets: CUES dominated municipal pipeline inspection; Schonstedt was the standard for magnetic utility locators; Patterson-Kelley held strong positions in commercial boilers.

-

Acquire at reasonable valuations: Management consistently emphasized acquisition multiples averaging around 11x EBITDA, which they worked to improve to 9x through integration and operational improvements.

-

Drive synergies through the SPX business system: Standardized processes, shared best practices, and centralized procurement created value beyond what targets could achieve independently.

-

Invest in organic growth post-acquisition: Rather than strip-mining acquisitions for cost savings, SPX invested in product development and capacity expansion to accelerate growth.

In September 2020, SPX acquired ULC Robotics Inc., a developer of robotics systems and inspection technology for natural gas networks, in a $135 million deal. Sensors & Software Inc. was also acquired by SPX in November 2020.

The ULC Robotics acquisition was particularly strategic. As utility companies faced mounting pressure to ensure pipeline safety—driven by high-profile gas explosions and tightening regulatory scrutiny—demand for robotic inspection systems was accelerating. SPX was building an integrated platform for infrastructure inspection: underground locators, pipeline cameras, and now robotic inspection systems.

But Lowe also proved willing to exit businesses that no longer fit the strategic vision. In July 2018, SPX announced it was exiting the Heat Transfer business within its Engineered Solutions segment. This decision shed exposure to the challenged power generation market while generating capital for reinvestment in higher-growth opportunities.

The financial results during this period validated the strategic approach. Management noted that from 2017-2020, SPX's earnings per share grew approximately 70% per year. While this rate inevitably moderated as the company scaled, it demonstrated that focused execution on a coherent strategy could generate extraordinary shareholder returns.

Lowe's leadership style differs markedly from the Blystone era. Where Blystone was the aggressive deal-maker constantly seeking transformational acquisitions, Lowe operates more like a patient capital allocator, building platform businesses through disciplined bolt-on acquisitions while investing heavily in organic growth initiatives. With a career that spans over three decades, he has developed a keen understanding of market dynamics and strategic planning.

VII. Transformation Acceleration (2021-2024)

The period from 2021 through 2024 marked an acceleration of SPX's transformation, as management completed the exit from legacy power generation exposure while aggressively building out the HVAC and Detection & Measurement platforms.

In 2021, SPX sold its Transformer Solutions business, which manufactured power and distribution transformers, to Prolec GE for $645 million, with the transaction closing on October 4. This move streamlined operations by concentrating on HVAC and detection and measurement technologies, eliminating exposure to the more cyclical power transformer market.

The Transformer Solutions divestiture was the final piece of the portfolio rationalization puzzle. Power transformers were project-based, highly cyclical, and capital-intensive—characteristics that conflicted with SPX's emerging focus on recurring revenue streams and steady demand. The $645 million proceeds provided substantial firepower for acquisitions in core growth areas.

The company also took decisive action to address legacy liabilities. In late 2022, SPX completed the divestiture of its asbestos portfolio, significantly reducing legacy liability exposure that had weighed on investor sentiment for years.

In 2022, SPX reorganized its corporate structure through a tax-free merger, transitioning from SPX Corporation to SPX Technologies, Inc. as the publicly traded holding company, which facilitated more efficient management and future acquisitions.

The name change to SPX Technologies was more than cosmetic. It signaled that the company viewed itself as a technology-enabled infrastructure provider, not a traditional industrial company. The cooling towers, boilers, and detection equipment SPX sold increasingly incorporated sophisticated sensors, controls, and connectivity features that differentiated them from commodity products.

The acquisition pace accelerated significantly:

In April 2023, SPX Technologies acquired privately held TAMCO for approximately CA$170 million (approximately US$125 million) in cash. Headquartered in Smiths Falls, Ontario, Canada, TAMCO is a market leader in motorized and non-motorized dampers that control airflow in large-scale specialty applications in commercial, industrial, and institutional markets. TAMCO, which has operations in Canada and the US, is well-known for its eco-friendly solutions, which provide very low levels of air leakage in critical thermal applications, such as data centers and healthcare facilities. TAMCO is now a part of SPX Technologies' HVAC segment and expands the Company's position in Engineered Air Movement solutions. TAMCO has annual revenue of more than US$50 million, and its margins and anticipated revenue growth rate are higher than the HVAC segment average.

"We are very excited about welcoming TAMCO to the SPX Technologies team," said Gene Lowe. "TAMCO's well-respected brand and attractive niche-engineered products are a strong fit within our Engineered Air Movement business. We see multiple opportunities to create value and accelerate our growth by leveraging our combined product offerings, distribution channels, and SPX Technologies' business system. This is our 12th acquisition since 2018, and further validates our strategy of building high-quality, market-leading platforms, and creating foundations for further growth in closely adjacent end markets."

TAMCO was particularly strategic because it strengthened SPX's position in data center infrastructure—a market poised for explosive growth.

In June 2023, SPX completed the acquisition of ASPEQ Heating Group, significantly expanding its portfolio of electrical heating products. For the full year of 2024, HVAC segment revenue increased 21.6%, including a 9.7% increase in organic revenue, a 12.0% inorganic increase from the Ingénia, ASPEQ and TAMCO acquisitions, and a 0.1% unfavorable impact related to currency fluctuation.

In early 2024, SPX acquired Ingénia Technologies, a Canadian manufacturer of custom commercial air handling units, for approximately $300 million. In February 2024, SPX expanded its Heating Ventilation and Air-Conditioning business by acquiring, Ingenia Technologies, a Canadian manufacturer of custom commercial air handling units, headquartered in Mirabel, Quebec. The acquisition amounting to $300 million included cash and associated real estate in its valuation.

The 2024 full-year results demonstrated the success of this strategy:

Q4 GAAP EPS reached $1.19 (up 78% YoY) while full-year GAAP EPS hit $4.29 (up 38% YoY). The company's full-year GAAP net income surged 123% to $200.5 million.

Key financial metrics for 2024 include a 13.9% increase in revenue to $1.98 billion and a 38.9% rise in operating income to $308.3 million.

VIII. The Data Center Tailwind & Future Growth (2024-Present)

The convergence of artificial intelligence, cloud computing, and digital infrastructure has created perhaps the most powerful secular tailwind in SPX Technologies' history. Data centers—the massive facilities housing the servers that power the digital economy—require enormous cooling capacity to manage the heat generated by thousands of processors running continuously.

The global data center cooling market is on a meteoric trajectory, projected to grow at a 12% annual rate through 2030. With AI-driven infrastructure demands surging and hyperscale data center deployments accelerating, companies positioned to address this need are poised for outsized gains.

SPX's Marley brand is extraordinarily well-positioned to capture this opportunity. Marley combines a century of experience in cooling technologies with a broad product portfolio, making us the go-to consultative partner for modern data center customers.

Data center revenue was about 7% of total company revenue or 10% of HVAC, in line with expectations. Expected to maintain similar share or slightly higher in 2025.

The introduction of OlympusV Max represents SPX's most ambitious data center cooling solution to date. Expansion in data center cooling solutions, highlighted by the new OlympusV Max launch, which addresses the rapidly growing demand for energy-efficient, large-scale data center infrastructure, positions SPX to meaningfully expand its addressable market and top-line growth as hyperscale projects accelerate into 2026. This is expected to support both revenue and margin improvement due to product differentiation and high-engineering requirements.

CEO Gene Lowe highlighted the company's progress on key initiatives during the earnings call, stating, "We're on track to achieve our objective of booking $50 million of Olympus Max orders in 2025 for revenue in 2026." He also emphasized the company's growth targets, noting, "We very clearly say we want 15% growth every year. This year, we're penciling in around 20%."

SPX has invested aggressively in manufacturing capacity to support data center growth. SPX Cooling Tech, a full-service cooling tower and air-cooled heat exchanger manufacturer, announced that it plans to open a manufacturing facility in Springfield, creating more than 60 new jobs as part of a capital plan focused on incremental capacity of SPX Cooling Tech products manufactured in the U.S. "For over a century, Marley has been the preeminent manufacturer of cooling solutions for industries that have formed the foundation of our communities," said Sean McClenaghan, President of Global Cooling for SPX Cooling Tech. "To prepare for the next generation of growth, we're pleased to announce that SPX Cooling Tech, with the assistance of the Department of Economic Development, is opening this new manufacturing facility in Springfield. The site will support the increased investment in data centers, semiconductor fabrication facilities, and battery and EV infrastructure throughout North America."

The new 100,000-square-feet, SPX-operated facility is projected to be operational within six months, and is expected to employ approximately 60 team members.

The Q3 2025 results demonstrated continued momentum:

Revenue of $592.8 million, up 22.6% GAAP income from continuing operations of $63.1 million, up 24.0% GAAP EPS of $1.29, up 19.4% Adjusted EPS of $1.84, up 32.4% Adjusted EBITDA of $136.1 million, up 30.9%

"We grew third quarter adjusted EPS by 32% and drove significant profit and margin growth in both segments," management stated, emphasizing strategic execution as a core driver of the quarter's success. The company reported revenue of $592.8 million, a 22.6% year-on-year increase, beating analyst estimates of $579.8 million.

2025 revenue guidance raised to $2.225–$2.275B, with adjusted EBITDA expected at $495–$515M (up ~20% at midpoint) and adjusted EPS at $6.65–$6.80 (up ~21% at midpoint).

Management has also strengthened the balance sheet to support continued growth:

SPX successfully raised $575 million through an equity offering and increased its revolving credit facility capacity by $500 million. This strategic move has resulted in over $1 billion of additional liquidity, with no dilutive impact on the 2025 EPS, further strengthening the company's financial flexibility.

IX. The Business Model Deep Dive

SPX Technologies operates what might be called a "niche dominance" business model—targeting specific infrastructure categories where engineering expertise, brand reputation, and installed base relationships create sustainable competitive advantages.

The company's two segments serve fundamentally different but equally attractive markets:

HVAC Segment (~65% of revenue): This segment encompasses cooling products (Marley cooling towers, Recold fluid coolers, SGS refrigeration), heating products (Weil-McLain boilers, Patterson-Kelley commercial heating, ASPEQ electrical heating), and engineered air movement (Cincinnati Fan, TAMCO, Ingénia).

The Marley NC Everest offers significant advantages for data centers, including up to 50% greater cooling capacity, higher energy savings, fewer components, and lower maintenance costs. With up to 58% more cooling capacity than other preassembled cooling towers and the ability to be installed up to 80% faster than field-erected cooling towers, the Marley MD Everest is an ideal solution for data centers.

Weil-McLain® is a leading North American brand of hydronic comfort heating systems for residential, commercial and institutional buildings, since 1881. Contractors, engineers, architects, homeowners and facility managers rely on Weil-McLain boilers for their comfort heating needs. Installed in homes, offices, schools, restaurants, hotels and other facilities throughout North America, the Weil-McLain brand is among the most trusted and often used in the building industry.

Detection & Measurement Segment (~35% of revenue): This segment offers underground pipe and cable locators (Radiodetection, Schonstedt), inspection and rehabilitation equipment (CUES, Pearpoint), robotic systems (ULC Technologies), transportation systems (Genfare fare collection), communication technologies (TCI, ECS), and obstruction lighting products (Flash Technology, ITL, Sabik Marine, Sealite, Avlite).

The economic characteristics of these businesses are highly attractive:

High Replacement Demand: Much of SPX's revenue comes from replacing aging equipment rather than new construction. Cooling towers have finite lifespans; boilers eventually fail; underground locators wear out. This creates steady, predictable demand largely independent of economic cycles.

Specification Relationships: Consulting engineers who design building systems specify brands based on performance, reliability, and their own experience. Once a specification is written around Marley or Weil-McLain, it's difficult for competitors to win the job. These "spec" relationships create a powerful barrier to entry.

Service and Aftermarket Revenue: Installed equipment requires ongoing maintenance, parts replacement, and eventual upgrade. This aftermarket revenue carries higher margins than original equipment sales and creates deeper customer relationships.

The M&A playbook deserves particular attention. Management has been remarkably transparent about their acquisition approach:

Acquisitions typically occur at approximately 11x EBITDA, which management then works to reduce to approximately 9x through integration and operational improvements. The targets are businesses averaging around 20% EBITDA margins that are accretive to growth rates. Since 2018, SPX has completed over 20 acquisitions, with peak activity occurring in 2018, 2021, and 2025.

Management confirmed $50M Olympus Max bookings target for 2025 (revenue in 2026) and emphasized capacity expansions at TAMCO/Ingénia to meet data center/HVAC demand surges. EBITDA doubling targets by 2027-2028 remain intact, with disciplined M&A strategy (avg. 11x multiples) and strong 2026 visibility in data centers, healthcare, and industrial markets.

X. Brand Portfolio & Competitive Position

SPX Technologies' competitive position rests fundamentally on its portfolio of heritage brands—names that carry weight with engineers, contractors, and facility managers who make specification and purchasing decisions.

Marley: The crown jewel of the HVAC segment. SPX Cooling Technologies, Inc., is commemorating the 100-year anniversary of its Marley brand, a name synonymous with the development and advancement of energy-efficient and sustainable evaporative cooling towers and components.

It all started with two young engineers and manufacturer's representatives named L. T. Mart and Chester Smiley, who founded Power Plant Equipment Company in Kansas City in 1922. L. T. Mart, a mechanical engineer, was considered the inventor of the group. Together, Mart and Smiley developed and patented new spray nozzles and spray pond inventions, so innovation has been a core of the business from the beginning. When Mart and Smiley needed an original name for the business, they combined elements of their last names, and the Marley brand was born in 1924. In 1928, Smiley continued his role as a manufacturer's representative, while Mart retained the patents and all products carrying the Marley name, then incorporated the business as The Marley Company.

Over the past 100 years, the Marley spirit of entrepreneurialism and invention has fueled the organization. Today, SPX Cooling Technologies holds more than 200 U.S. patents for evaporative cooling systems and components.

Weil-McLain: The anchor of the heating platform. Founded in 1881 in Chicago by Isadora and Benjamin Weil, Weil-McLain was originally Weil Brothers. In 1918, the Weil brothers acquired a main supplier, J.H. McLain Company, and the Weil-McLain brand was born. Manufacturing in Michigan City, Indiana for over 100 years, we have grown to be the largest U.S manufacturer of cast-iron boilers under the Weil-McLain® brand.

Radiodetection: The leading brand in underground utility locating equipment. This business benefits from regulatory requirements that utilities and contractors locate underground infrastructure before excavation—a mandate that creates steady, non-discretionary demand.

CUES: The dominant brand in pipeline inspection equipment, serving municipalities responsible for maintaining sewer and water infrastructure. With much of America's underground infrastructure aging beyond its design life, inspection demand continues to grow.

Genfare: A leading provider of fare collection systems for public transit. While not as large as other platforms, Genfare benefits from long-term contracts with transit agencies and the complexity of integrating fare systems with other transit operations.

The competitive landscape varies by business, but SPX generally competes against specialized competitors in each niche rather than diversified industrial giants. Key competitors include Evapco and Baltimore Aircoil in cooling towers, Burnham and Lochinvar in boilers, Vivax-Metrotech and 3M Dynatel in underground locators, and Cubic Transportation in fare collection.

XI. Strategic Analysis: Porter's Five Forces

Threat of New Entrants: LOW

Building a credible competitor to Marley or Weil-McLain would require decades of brand-building, massive capital investment in manufacturing capacity, development of sales and service networks, and earning the trust of specification engineers. The switching costs for customers are meaningful—once a facility is designed around particular equipment, changing suppliers requires expensive modifications. The regulatory certifications and testing required for safety-critical equipment like boilers create additional barriers.

Bargaining Power of Suppliers: MODERATE

SPX purchases steel, copper, and various manufactured components from numerous suppliers. While commodity price fluctuations affect costs, the diversified supplier base limits any single supplier's leverage. SPX has pursued vertical integration in critical components where possible, further reducing supplier power.

Bargaining Power of Buyers: MODERATE

The dynamics differ significantly across customer segments. Large commercial customers and contractors can negotiate on price, but the specification-driven nature of the business limits price sensitivity for many applications. When a cooling tower is specified for a data center project, the customer's primary concern is performance and reliability, not extracting the lowest possible price. The replacement market also favors SPX—when a Weil-McLain boiler fails, replacing it with another Weil-McLain is typically the path of least resistance.

Threat of Substitutes: LOW

The Marley OlympusV Adiabatic Series balances the water-saving benefits of an air-cooled heat rejection system with the energy efficiency of a water-cooled solution to provide flexible cooling for data systems.

Cooling towers and HVAC systems represent fundamental infrastructure requirements. While technology evolves—adiabatic cooling offers advantages over traditional evaporative cooling in water-scarce regions—SPX leads this evolution rather than being disrupted by it. Detection and measurement equipment similarly faces limited substitution threat; you simply cannot locate underground utilities without specialized equipment.

Competitive Rivalry: MODERATE

Markets are fragmented with numerous niche players, which actually benefits SPX's consolidation strategy. Competition exists but tends to be rational—competitors don't engage in destructive price wars because sophisticated buyers value quality and reliability. SPX's acquisition program consolidates market position over time.

XII. Strategic Analysis: Hamilton's Seven Powers Framework

1. Scale Economies: PRESENT (Moderate)

With more than $2 billion in annual revenue and over 4,400 employees in 16 countries, SPX achieves meaningful scale advantages in manufacturing, procurement, and sales coverage. The Springfield facility expansion demonstrates continued investment in scale.

2. Network Effects: WEAK

Limited direct network effects exist in industrial equipment. Some indirect effects emerge through the ecosystem of contractors, engineers, and service providers familiar with SPX specifications and products.

3. Counter-Positioning: STRONG (Historical)

The 2015 spin-off represented classic counter-positioning. Legacy conglomerates struggled to match the focused pure-play strategy. SPX FLOW continued with a complex portfolio while "New SPX" concentrated resources on infrastructure—a simpler, more compelling value proposition.

4. Switching Costs: STRONG

Engineered-to-order products create deep customer relationships. Training and familiarity with service/maintenance procedures lock in contractors. Specification relationships with consulting engineers create embedded switching costs. The replacement nature of much demand reinforces incumbent advantages.

5. Branding: STRONG

Marley, Weil-McLain, and Radiodetection represent brands that engineers trust and specify. This year marked a century for the world-renowned evaporative cooling tower brand, Marley. And after 100 years, the Marley brand and the company that produces and services the well-known products, SPX Cooling Tech, show no signs of slowing down.

6. Cornered Resource: MODERATE

SPX possesses unique accumulated engineering expertise in cooling tower design, boiler metallurgy, and detection technology developed over decades. The patent portfolio (200+ U.S. patents in cooling alone) provides some protection, though patents in industrial equipment are more defensive than dominant.

7. Process Power: EMERGING

The "SPX Business System"—the company's approach to operational excellence, continuous improvement, and acquisition integration—represents developing process power. Management consistently emphasizes this system as a source of competitive advantage.

XIII. Bull Case: Infrastructure Renaissance Meets Disciplined Execution

The optimistic thesis for SPX Technologies rests on several reinforcing factors:

1. Data Center Secular Growth: The explosion in AI workloads requires massive cooling infrastructure. The global data center cooling market is on a meteoric trajectory, projected to grow at a 12% annual rate through 2030. With AI-driven infrastructure demands surging and hyperscale data center deployments accelerating, companies positioned to address this need are poised for outsized gains.

Marley's century of cooling expertise, established relationships with data center operators, and new products like OlympusV Max position SPX to capture disproportionate share of this growth.

2. Infrastructure Replacement Cycle: America's built environment is aging. Cooling towers installed 30 years ago are reaching end-of-life. Boiler systems in schools and hospitals require replacement. Underground utility infrastructure needs inspection and rehabilitation. SPX's portfolio aligns precisely with these replacement needs.

3. M&A Value Creation: For investors, SPX's demonstrated ability to identify, acquire, and successfully integrate specialized businesses while maintaining financial discipline represents a significant competitive advantage in creating long-term shareholder value through both revenue growth and margin expansion.

4. Margin Expansion Runway: As acquisitions mature and operational improvements compound, margins should continue expanding. The 2024 results showed record HVAC segment margins, suggesting the flywheel is working.

5. Management Alignment: Gene Lowe's decade-plus tenure and deep understanding of the business creates strategic continuity. The leadership team has demonstrated both patience and decisiveness in portfolio optimization.

XIV. Bear Case: Valuation, Execution Risk, and Cyclical Exposure

Skeptics raise legitimate concerns:

1. Premium Valuation: SPX Technologies is currently trading at a price-to-earnings ratio of 45.6x, which is much higher than both its peer group average of 26.7x and the industry average of 23.7x. Its market price also sits well above the fair ratio of 29.3x, suggesting investors are paying a sizable premium for growth.

The market clearly expects continued strong performance. Any stumble—missed guidance, acquisition integration problems, demand slowdown—could trigger significant multiple compression.

2. Acquisition Integration Risk: Integration risks associated with recent acquisitions remain meaningful. The rapid pace of acquisitions requires flawless execution; even one bad deal could destroy years of value creation.

3. Data Center Concentration: Slower growth in commercial building and hotel markets, which could affect the HVAC segment. If the data center boom moderates while traditional commercial construction remains weak, the HVAC segment could face headwinds.

4. Capital Structure After Equity Raise: Potential dilution from the $575 million stock offering, despite the company's assertion that it would not impact 2025 EPS. Long-term dilution effects may be more meaningful than near-term EPS protection suggests.

5. Macroeconomic Sensitivity: Despite the replacement-driven nature of much demand, commercial construction activity influences new equipment sales. A significant recession could pressure results more than management's messaging suggests.

XV. Key Performance Indicators for Investors

For long-term fundamental investors tracking SPX Technologies, three KPIs deserve particular attention:

1. Organic Revenue Growth: This metric strips out acquired growth to reveal underlying demand trends. Management targets 15% total annual growth; the organic component indicates whether existing businesses are capturing market share and expanding with end markets. The Q3 2025 organic growth of 14.3% demonstrates strong underlying momentum.

2. HVAC Segment Margin: This is the profit engine of the company. Segment income margin guidance for 2025: HVAC 24.25%–24.75%. Tracking this margin reveals whether pricing power, operational improvements, and mix shifts are flowing through to profitability. Record margins in recent quarters suggest the business system is working; any sustained margin pressure would warrant attention.

3. Acquisition Pace and Integration Success: Given that M&A is central to the growth strategy, investors should monitor both deal volume and post-acquisition performance. Are acquired businesses meeting or exceeding expectations? Are integration timelines and synergy capture on track? Management's target of improving acquired businesses from 11x to 9x EBITDA multiples provides a benchmark for evaluating acquisition effectiveness.

XVI. Regulatory and Risk Considerations

Investors should be aware of several material considerations:

Environmental Regulations: Cooling towers and HVAC equipment face evolving regulations around water usage, energy efficiency, and refrigerant emissions. While SPX generally positions itself as a provider of sustainable solutions, regulatory changes could require product modifications or create compliance costs.

Tariff Exposure: With international operations and global supply chains, tariff policy affects SPX. Management has noted the importance of monitoring tariff situations, though the recent reshoring trend may benefit domestic manufacturing capacity.

Legacy Liabilities: While SPX completed the divestiture of its asbestos portfolio, historical industrial operations can generate long-tail liabilities. Investors should monitor any developments in legacy environmental or product liability matters.

Customer Concentration: The data center market involves a relatively small number of hyperscale operators. While demand is robust, significant exposure to any single customer creates concentration risk.

XVII. Conclusion: The Phoenix Narrative

SPX Technologies represents one of American industry's most compelling transformation stories. A company founded to make piston rings for Model T engines has reinvented itself as an infrastructure technology provider at the heart of the digital economy's physical foundation.

The journey from Sealed Power Corporation to SPX Corporation to SPX Technologies traces the arc of American industry itself: the rise of mass production, the conglomerate era, the activist-driven breakup of sprawling enterprises, and the emergence of focused, technology-enabled industrial platforms.

Today we celebrate ten years as SPX Technologies. Gene Lowe's decade leading the transformed company has validated the 2015 strategic bet. The focused portfolio, disciplined M&A approach, and relentless operational improvement have generated extraordinary shareholder returns.

For investors, the central question is whether this performance can continue. The bull case is compelling: secular tailwinds in data center cooling, infrastructure replacement, and sustainability; proven acquisition capabilities; and heritage brands with genuine competitive moats. The bear case focuses on valuation, execution risk, and the challenge of maintaining growth rates as the company scales.

What seems indisputable is that SPX Technologies has earned attention as a case study in corporate transformation. The company that began making piston rings on the shores of Lake Michigan now cools the servers that power artificial intelligence. That's a phoenix story worth understanding.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube