MYR Group: Powering America's Grid for 130 Years

The Quiet Giants of Energy Infrastructure

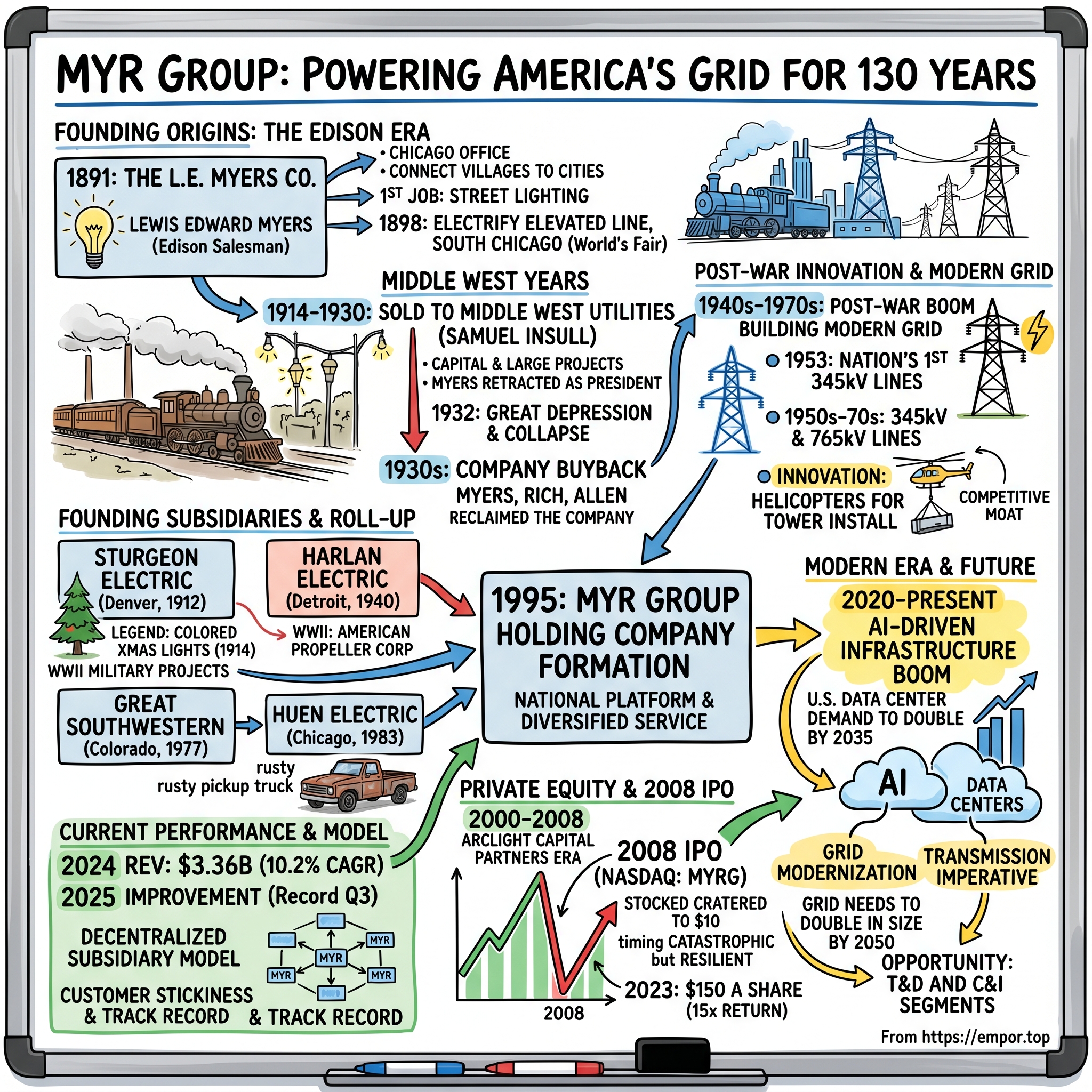

On a rain-soaked September morning in 2008, just days before the collapse of Lehman Brothers would plunge the world into financial chaos, a specialty electrical contractor from Colorado began trading on the NASDAQ. MYR Group's shares opened at $16—an inauspicious debut into what would become the worst financial crisis since the Great Depression. By December, the stock had cratered to $10. The timing seemed catastrophic.

From 2005 to 2007, ArcLight Capital Partners was the majority shareholder. In 2008, approximately 20 million shares in the company were registered with NASDAQ for resale. Trading started at $16 per share; by December the price had fallen to $10. In 2023 the stock reached $150 a share.

That's a 15x return through one of the most turbulent periods in American economic history—and a story that reveals something profound about infrastructure investing. While tech darlings rose and fell, while housing markets collapsed and recovered, while entire industries were disrupted and displaced, the business of keeping the lights on proved remarkably durable.

MYR Group Inc. is an American corporation that offers electrical construction services for transmission and distribution lines, substations, commercial and industrial buildings, and renewable energy. It is the parent company to 12 subsidiary electrical construction companies. It has approximately 8,500 employees and in 2022 had revenue of $3.01 billion. It is publicly traded on Nasdaq under the stock symbol MYRG. Its headquarters are in Thornton, Colorado.

But here's what makes MYR Group's story truly remarkable: The company's founder, Lewis Edward Myers, was a salesman for the American inventor Thomas Edison, who dreamed of making the new, modern convenience of electricity available and affordable to American homes and businesses.

That connection to Edison isn't just corporate mythology—it's a thread that runs through 130 years of American energy history. This is a story about how patient capital, disciplined execution, and positioning at the heart of critical infrastructure can compound wealth across generations. And with data centers now consuming more electricity than many nations, the AI revolution may be writing the next chapter of this century-old story.

I. Founding Origins: The Edison Era (1891–1940s)

The Lewis Edward Myers Story

Picture Chicago in 1891: a city pulsing with industrial ambition, the World's Fair on the horizon, and a revolutionary new technology—electricity—transforming every aspect of urban life. Lewis Edward Myers was working with Thomas Edison as a salesman in the late 1800s when he decided to harvest a dream that Edison had inspired—to power the approaching Twentieth Century. Building on his dream, Lewis E. Myers opened a small Chicago office in 1891, with the intent of connecting villages and towns to major cities along railroad lines in the Midwest.

Myers wasn't a scientist or engineer—he was a salesman. But working alongside Edison gave him a front-row seat to a technology that would reshape civilization. He saw something that many of his contemporaries missed: the opportunity wasn't in inventing electrical systems, it was in building them, in stringing wire across the American landscape, in the unglamorous but essential work of making electricity real for ordinary people.

In 1891, Myers founded The L.E. Myers Co. in Chicago, Illinois, and landed his first job, which was a street lighting project. Through creative financing and integrity, Myers was able to obtain material and pay his employees, thereby building the foundation for a long and successful business venture in electrical construction.

That first street lighting job established a pattern that would define the company for over a century: infrastructure work that sits at the intersection of technical complexity and essential public service. In 1898, Myers was awarded his first landmark project to electrify an elevated line in South Chicago to serve the 1893 World's Fair. Powering the Columbian Exposition—an event that introduced millions of Americans to electric light—would be the kind of prestige project that builds reputations across generations.

In the 1900s, much of Myers' early work was devoted to building the electrical infrastructure that brought electricity to the Midwest, and connected villages, towns and outlying areas to major cities along railroad lines. Building this new infrastructure was a crucial development in the industrialization of America; and with the growing demand for power, Myers' skills and experience were in high demand.

The Middle West Years: Ownership Drama

The first major turning point came in 1914, when Myers made a decision that would echo through the company's ownership history: Myers sold his company to Middle West Utilities; yet he and his organization were retained. He held the position of President until 1930.

Middle West Utilities was a sprawling utility holding company controlled by Samuel Insull—ironically, one of Edison's closest associates who had built Chicago Edison into the dominant utility in the Midwest. The acquisition brought capital and access to larger projects, but it also meant surrendering independence to a corporate parent with its own agenda.

During this period, Myers led the company through World War I and the Roaring Twenties: Throughout World War I, L.E. Myers began to diversify capabilities and focused efforts on "powering up" war-related industries. In the 1920s L.E. Myers embarked upon many significant pursuits that included hydroelectric projects throughout Wisconsin, Michigan, Kentucky and Texas; earning the reputation as an innovator and industry leader.

Then came the Great Depression—and with it, one of the most dramatic ownership transitions in the company's history. In the 1930s as the Great Depression began to take its toll, Myers, along with two other businessmen—Newton Rich and L.T. Allen—purchased L.E. Myers from Middle West Utilities; thus reclaiming the company.

This buyback is a fascinating piece of corporate history. Middle West Utilities collapsed spectacularly in 1932, taking Insull's empire down with it and destroying billions in shareholder wealth. Myers and his partners acquired the electrical contracting business from the wreckage—a founding narrative that speaks to the durability of infrastructure services even when their corporate parents fail.

The Other Founding Subsidiaries

The story of MYR Group isn't just the story of L.E. Myers. It's the story of regional electrical contractors across America, each building their own legacies before eventually combining into a national platform.

David Dwight (D.D.) Sturgeon founded Sturgeon Electric Company, Inc., opening a garden-level shop at 1026 14th Street in downtown Denver offering commercial and industrial electrical construction services. Throughout the years, D.D. Sturgeon continued to grow his company, earning a reputation as "the man you could depend on to get the job done."

Here's a charming piece of corporate lore: Legend tells that D.D. Sturgeon invented colored Christmas lights in 1914. To cheer his ailing son, Sturgeon dipped ordinary lightbulbs in paint, strung them on a cord, and hung them on a tree outside his home near his son's bedroom window. Word spread quickly, and folks came from miles away to view the lights outside the Sturgeons' home. Today, the company donates time and services for various outdoor lighting displays throughout Denver.

Whether apocryphal or not, the story captures something essential about these regional contractors: they were family businesses, rooted in communities, building personal relationships that would sustain client connections for generations.

In 1940, C. Allen Harlan founded Harlan Electric Company in Detroit, Michigan. The timing proved serendipitous. When the 1941 attack on Pearl Harbor thrust the country into World War II, the build-up of military capabilities began in earnest. Harlan Electric was awarded a contract with the American Propeller Corporation to perform the electrical scope for a new facility to support the wartime effort.

Sturgeon Electric worked on numerous military projects during WWII: electrical work at the Denver Ordnance Plant, Fort Carson, and Camp Hale for the ski troops of the 10th Mountain Division, and an extensive project for the Navy, installing electrical components into LCT boats. Sturgeon Electric received three Army-Navy "E" banners. Less than 4% of U.S. companies received even one "E" banner.

These wartime contributions established the regional contractors as essential partners in national defense infrastructure—a relationship that would persist through the Cold War and into the present day.

II. Post-War Innovation & Industry Leadership (1950s–1990s)

Building the Modern Grid

World War II transformed America's electrical infrastructure. Factories required unprecedented amounts of power. Defense installations needed reliable electricity. And when the war ended, the returning veterans and the baby boom they sparked created entirely new demands on the grid.

During World War II in the 1940s, L.E. Myers was instrumental in electrifying defense plants and wiring military installations to maintain an uninterrupted flow of power to factories and facilities across the country.

The death of Lewis Edward Myers in 1945 marked the end of the founder's era, but his company was positioned perfectly for the post-war boom. In 1953, L.E. Myers constructed the nation's first 345kV transmission lines for the Ohio Valley Electric Corporation.

This was more than a technical achievement—it was a preview of the future. Higher voltage transmission lines carry more power over longer distances with less loss. They enabled the construction of larger power plants in remote locations, connecting generation capacity to distant load centers. L.E. Myers' willingness to pioneer these technologies established the company as a partner for utilities pushing the boundaries of what was technically possible.

In the 1950s, 60s and 70s, L.E. Myers began constructing some of the first 345kV and 765kV transmission lines in this country and pioneered the use of helicopters for hauling and installing transmission towers.

The helicopter innovation deserves particular attention. Faced with the challenge of constructing transmission towers throughout the rugged terrain of Kentucky, in the 1950s L.E. Myers pioneered the use of helicopters to haul and install transmission towers in difficult locations.

This wasn't just clever engineering—it was a competitive moat. The ability to build infrastructure where others couldn't, to access terrain that would otherwise require expensive road construction, gave L.E. Myers access to projects that less capable contractors couldn't bid on.

New Players Enter the Field

Meanwhile, the 1970s and 1980s saw the emergence of additional regional contractors who would eventually join the MYR Group family:

Western Pacific Enterprises, Ltd. (WPE), MYR Group's Canadian subsidiary, began in 1973 in Coquitlam, British Columbia. Founders Dieter Fettback and Ernie Moore mortgaged their homes to start an electrical contracting company that has grown to one of the largest contracting firms in western Canada thanks to its founders' unwavering vision to deliver efficient and safe commercial, civil, and industrial assignments.

In 1977, Great Southwestern Construction Inc. opened its doors as a family-owned business founded by Bob Martinez in Castle Rock, Colorado. Great Southwestern earned its reputation as a trusted contractor by specializing in power delivery projects throughout the desert Southwest and Rocky Mountain region.

Huen Electric's humble beginnings date to 1983, when founders Mike Hughes and Jim McGovern launched the company in Chicago with nothing more than a rusty pickup truck, a small cache of tools, and a tiny office filled with a card table and chairs. By the early 1990s Huen Electric was performing electrical installations at many Chicago landmarks, including Wrigley Field, the Sears Tower, and the Navy Pier.

Each of these businesses developed deep expertise in their regional markets, built relationships with local utilities and general contractors, and established reputations for quality work. They represented exactly the kind of acquisition targets that would make a roll-up strategy viable.

III. The Holding Company Formation & First Public Life (1995–2000)

Creating MYR Group

By the early 1990s, the electrical contracting industry faced a crossroads. Regional contractors had reached the limits of organic growth. Utilities were consolidating and demanding contractors who could handle larger, more complex projects across multiple states. The opportunity was clear: combine the best regional players into a national platform.

By the 1990s, L.E. Myers' desire to expand operationally and geographically culminated with the acquisitions of Sturgeon Electric and Harlan Electric. In 1995, MYR Group Inc. was established as the holding company of L.E. Myers, Sturgeon Electric, and Harlan Electric and grew to one of the largest holding companies of specialty electrical contractors in the U.S. and Canada.

The first major transformative moment was the 1995 consolidation. By uniting regional powerhouses like L.E. Myers and Sturgeon Electric, MYR Group instantly gained a national footprint and a diversified service offering, which is definitely a huge competitive advantage.

The strategic logic was compelling. Each subsidiary brought different geographic coverage and technical specializations:

- L.E. Myers dominated the Midwest and Northeast, with deep expertise in high-voltage transmission

- Sturgeon Electric controlled the Rocky Mountain and Western markets, with strong commercial and industrial capabilities

- Harlan Electric served the Great Lakes region and had established relationships with automotive and industrial clients

Combined, they could pursue projects too large for any individual subsidiary, share equipment and personnel across regions during demand spikes, and present a unified face to national utility clients.

The NYSE Years & Utility Ownership

MYR Group was listed on the New York Stock Exchange from 1996 to 2000, when it was bought by GPU Inc., which was then bought by FirstEnergy Corp.

This utility ownership period represents an interesting chapter in the company's history. GPU Inc. was a major utility holding company operating in New Jersey and Pennsylvania. The logic of vertical integration—owning your contractor to guarantee capacity and control costs—appealed to utilities facing deregulation pressures and increasing infrastructure demands.

But the relationship proved awkward. Utilities competing for transmission projects found themselves hesitant to hire a contractor owned by a rival. The synergies that looked compelling on paper created conflicts in practice. When FirstEnergy acquired GPU in 2001, MYR Group found itself an orphaned subsidiary in a utility holding company with different strategic priorities.

The subsequent spin-off to private equity set the stage for the company's most important transformation.

IV. The Private Equity Transformation (2000–2008)

The ArcLight Era: A Critical Inflection Point

Founded in 2001, ArcLight Capital Partners is a leading private equity firm based in Boston, Massachusetts, with a focus on energy infrastructure investments. The firm has established itself as a pioneer in asset-based private equity, emphasizing investments in electric power, renewable energy, and strategic gas infrastructure. ArcLight's investment strategy centers on acquiring, developing, and operating energy assets that are critical to the ongoing energy transition.

ArcLight's acquisition of MYR Group wasn't a typical private equity play. Rather than loading the company with debt and cutting costs, ArcLight saw an opportunity to build a growth platform in essential energy infrastructure.

In the 2000s, MYR Group had multiple acquisitions and became a publicly-traded company on the NASDAQ under the symbol MYRG in 2008. In 2000, MYR Group acquired Great Southwestern Construction, Inc.

This acquisition expanded MYR Group's presence in the Southwest, adding capabilities in the fast-growing Arizona and Nevada markets where utility-scale solar would eventually become a major business line.

The 2008 IPO: Perfect Timing in Imperfect Markets

The timing of MYR Group's IPO appears, in retrospect, either brilliant or lucky—possibly both. The second was the 2008 IPO, which provided the liquid capital needed to accelerate growth through targeted acquisitions. This funding allowed them to aggressively pursue a strategy of acquiring specialized contractors.

The IPO launched into what would become the worst financial crisis since the Great Depression. Stock markets collapsed. Credit markets froze. Real estate values evaporated. But infrastructure spending—supported by government stimulus and essential utility maintenance—proved remarkably resilient.

The crisis validated MYR Group's business model in ways that wouldn't be fully appreciated for years. While housing contractors went bankrupt and commercial construction collapsed, electrical infrastructure work continued. Utilities couldn't defer maintenance on transmission lines. Industrial facilities needed power regardless of economic conditions. The "boring" nature of infrastructure services that made MYR Group unexciting to growth investors proved to be its greatest strength.

V. The Acquisitive Growth Era (2009–2022)

Building the Platform Through M&A

The post-crisis decade saw MYR Group execute a disciplined acquisition strategy, adding capabilities and geographic coverage while maintaining the operational autonomy of individual subsidiaries.

MYR Group subsidiaries completed several significant projects during this time—most notably, at the time, the $232 million "Northern Loop" of the Maine Power Reliability Program (MPRP), the largest energy infrastructure project in state history.

The Maine Power Reliability Program demonstrated MYR Group's ability to execute large-scale projects requiring coordination across multiple subsidiaries. It also established relationships with utilities in the Northeast that would generate recurring revenue for years.

The acquisition timeline reveals a methodical approach:

As growth is a key part of MYR Group's strategy, the company acquired Great Southwestern Construction, Inc. in 2000, E.S. Boulos Company and High Country Line Construction in 2015, Western Pacific Enterprises Ltd. in 2016, Huen Electric in 2018, and CSI Electrical Contractors in 2019.

Each acquisition served a specific strategic purpose:

E.S. Boulos Company (2015) strengthened the company's presence in New England, a market with aging infrastructure and strong utility investment plans. Edward S. Boulos was only 13 when he launched his electrical career in Portland, Maine. After founding the E.S. Boulos Company in 1920, the company expanded quickly, and by 1947, Boulos operated an expansive warehouse and elegant showroom.

High Country Line Construction (2015) provided specialized capabilities in transmission and substation construction. In 2013, MYR Group's youngest subsidiary at the time—High Country Line Construction, Inc.—opened its doors in Morgan, Utah. Founder Clay Thomson grew the company from the ground-up by providing a full-range of capabilities related to transmission, distribution, and substation construction. Now a forceful player on EPC projects throughout the western United States.

Western Pacific Enterprises (2016) expanded MYR Group into Canada, providing access to a stable infrastructure market with supportive regulatory environments and significant renewable energy development.

Huen Electric (2018) strengthened the company's Commercial & Industrial segment, particularly in healthcare and data center construction—markets that would prove increasingly important.

CSI Electrical Contractors (2019) added significant capacity in California, the largest state market for both utility-scale solar and commercial construction.

The Evolution to Clean Energy

In 2009, MYR Transmission Services, Inc. was established to better meet the needs of clients constructing large and complex transmission projects.

This subsidiary would eventually be rebranded to MYR Energy Services, reflecting the company's growing involvement in renewable energy projects. The energy transition created new business lines without disrupting traditional utility relationships—a positioning that many competitors struggled to achieve.

The company's involvement in clean energy spans solar, wind, energy storage, and the transmission infrastructure required to connect renewable generation to the grid. This diversification proved prescient as traditional fossil fuel generation began declining and utilities committed to decarbonization targets.

VI. The Modern Era: Data Centers, AI & Grid Modernization (2020–Present)

The AI-Driven Infrastructure Boom

Something unprecedented is happening to American electricity demand. After decades of flat or declining per-capita consumption, the United States is seeing the largest surge in power demand since air conditioning caught on in the 1960s. The culprit—or opportunity, depending on perspective—is artificial intelligence.

U.S. data centers consumed 183 terawatt-hours (TWh) of electricity in 2024, according to IEA estimates. That works out to more than 4% of the country's total electricity consumption last year—and is roughly equivalent to the annual electricity demand of the entire nation of Pakistan. By 2030, this figure is projected to grow by 133% to 426 TWh.

Electricity demand for data centers worldwide is projected to grow 16% in 2025 and to double by 2030, according to Gartner, Inc. Gartner analysts estimate worldwide data center electricity consumption will rise from 448 terawatt hours (TWh) in 2025 to 980 TWh by 2030.

If the facilities were a country they'd rank fourth in electricity use, behind only China, the US and India. In the US, power demand from data centers is set to double by 2035, to almost 9% of all demand, according to BNEF. Some predict it will be the biggest surge in US energy demand since air conditioning caught on in the 1960s. That comes as the grid is already struggling to update aging infrastructure and adapt to climate change.

For MYR Group, this represents both a direct opportunity in data center construction and an indirect one in the transmission infrastructure required to serve these power-hungry facilities.

MYR Group is strategically positioned to capitalize on the booming data center market, which is being driven by artificial intelligence and increased cloud services. According to the presentation, data centers could grow to consume 9% of U.S. electricity annually by 2030, creating significant opportunities for both the company's T&D and C&I segments. The company has already secured significant projects in this space, including a $90 million data center project awarded to Sturgeon Electric.

The Transmission Imperative

The AI boom is colliding with decades of underinvestment in transmission infrastructure. The result is a massive buildout that could sustain electrical contractors for a generation.

According to the presentation, the U.S. transmission system "will need to at least double in size by 2050," while data center growth is being "supercharged" by artificial intelligence applications.

MYR Group is well-positioned to benefit from several long-term industry trends, including increased T&D spending by investor-owned utilities, which invested $30 billion in transmission in 2023 and plan to invest approximately $158 billion between 2024 and 2027.

"As electricity demand climbs due to the onshoring of manufacturing, artificial intelligence, and electrification, the pace of transmission development isn't keeping up," said Christina Hayes, Executive Director of Americans for a Clean Energy Grid. The Department of Energy's 2024 National Transmission Planning Study implies the need to build roughly 5,000 miles of new high-capacity transmission per year in the U.S. to ensure grid reliability, support economic growth, and deliver low-cost power to customers. The 2024 buildout—less than a tenth of that target—underscores the scale of the challenge.

The gap between transmission needs and current construction creates a multi-decade runway for contractors with the capabilities to execute complex projects.

Current Performance

MYR Group reported full-year 2024 revenue of $3.36 billion, representing a decline from $3.64 billion in 2023, but maintaining a 10.2% compound annual growth rate (CAGR) from 2019 to 2024.

The 2024 results reflected challenges in the company's clean energy segment, where several large projects experienced cost overruns: For the full year of 2024, net income was $30.3 million, or $1.83 per diluted share, compared to $91.0 million, or $5.40 per diluted share, for the same period of 2023. Full-year 2024 EBITDA was $117.8 million, compared to $188.2 million for the full year of 2023.

However, 2025 results have shown significant improvement: For the third quarter of 2025, net income was $32.1 million, or $2.05 per diluted share, compared to $10.6 million, or $0.65 per diluted share, for the same period of 2024. Third-quarter 2025 EBITDA was $62.7 million.

MYR reported first nine months 2025 revenues of $2.68 billion, an increase of $151.8 million, compared to the first nine months of 2024. Specifically, our T&D segment reported revenues of $1.47 billion, an increase of $41.0 million, from the first nine months of 2024. Our C&I segment reported revenues of $1.21 billion, an increase of $110.9 million, from the first nine months of 2024.

Balance Sheet Strength & Capital Allocation

As of September 30, 2025, MYR's backlog was $2.66 billion, compared to $2.64 billion as of June 30, 2025. As of September 30, 2025, T&D backlog was $929.0 million, and C&I backlog was $1.73 billion. Total backlog as of September 30, 2025 increased $64.4 million, or 2.5 percent, from the $2.60 billion reported as of September 30, 2024.

As of September 30, 2025, MYR had $399.8 million of borrowing availability under its $490 million revolving credit facility.

The company has maintained conservative leverage that provides flexibility for acquisitions while preserving balance sheet strength: On July 30, 2025, the board approved a $75 million stock repurchase program, demonstrating confidence in the company's future prospects and commitment to returning capital to shareholders.

VII. Business Model Deep Dive

Two-Segment Structure

MYR Group is a holding company of leading, specialty electrical contractors providing services throughout the U.S. and Canada through two business segments: Transmission & Distribution (T&D) and Commercial & Industrial (C&I). MYR Group subsidiaries have the experience and expertise to complete electrical installations of any type and size. Through their T&D segment they provide services on electric transmission, distribution networks, substation facilities, clean energy projects and electric vehicle charging infrastructure. Their comprehensive T&D services include design, engineering, procurement, construction, upgrade, maintenance and repair services. T&D customers include investor-owned utilities, cooperatives, private developers, government-funded utilities, independent power producers, independent transmission companies, industrial facility owners and other contractors.

Through their C&I segment, they provide a broad range of services which include the design, installation, maintenance and repair of commercial and industrial wiring generally for airports, hospitals, data centers, hotels, stadiums, commercial and industrial facilities, clean energy projects, manufacturing plants, processing facilities, water/waste-water treatment facilities, mining facilities, intelligent transportation systems, roadway lighting, signalization and electric vehicle charging infrastructure. C&I customers include general contractors, commercial and industrial facility owners, government agencies and developers.

MYR Group operates through two primary business segments: Transmission & Distribution (T&D) and Commercial & Industrial (C&I). The T&D segment generated $1.90 billion in revenue for the LTM period ended June 30, 2025, with a backlog of $927 million.

The Holding Company Philosophy

MYR Group's organizational structure is itself a competitive advantage. Rather than integrating acquisitions into a monolithic corporation, the company maintains separate subsidiary identities:

MYR Group consists of the following subsidiaries: The L.E. Myers Co.; Sturgeon Electric Company, Inc.; Sturgeon Electric California, LLC; Harlan Electric Company; MYR Energy Services, Inc.

MYR Group is comprised of long-established and successful electrical contractors with the expertise, resources, and financial backing required to deliver many of the most challenging electrical infrastructure projects in the United States and Canada. We promote cross-collaboration and information sharing across our companies, which fosters innovative, optimized solutions specific to our projects. Our comprehensive offerings of industry-leading electrical construction services are coupled with superior customer service and value.

MYR Group Inc. operates as a holding company for a network of specialty electrical contractors, essentially acting as a critical infrastructure partner that designs, builds, and maintains the power grid and large-scale commercial facilities across the United States and Canada. The operational framework is built on a decentralized model, using a network of subsidiaries like CSI Electrical Contractors and Great Southwestern Construction, which allows them to maintain local expertise while leveraging the financial and resource strength of the parent company. This structure lets them bid and execute projects across a wide geographic footprint.

This decentralized approach preserves the local relationships that drive repeat business in electrical contracting while providing the scale benefits of a larger organization—access to capital, equipment sharing, and the ability to pursue larger projects through subsidiary collaboration.

Customer Relationships

The durability of MYR Group's customer relationships is remarkable. Utility clients have worked with the same MYR Group subsidiaries for decades—sometimes half a century or longer. These relationships are difficult for competitors to replicate because they're built on:

- Track record: Years of successful project execution create institutional trust

- Local knowledge: Understanding regional permitting requirements, landowner relations, and weather patterns

- Personal connections: Utility project managers often have multi-decade relationships with contractor superintendents

- Embedded systems: Alliance agreements and master service contracts create switching costs

VIII. Industry Landscape & Competitive Dynamics

Market Size & Growth

The U.S. electrical contractors market size was valued at USD 237.59 billion in 2023 and is expected to reach USD 256.65 billion by 2029, growing at a CAGR of 1.29% during the forecast period.

This modest overall market growth masks dramatic shifts in where spending is occurring. Traditional residential and commercial construction is growing slowly, but transmission infrastructure, data centers, and industrial facilities are seeing rapid expansion.

The market size of the Electricians industry in the United States has been growing at a CAGR of 3.7% between 2020 and 2025. The biggest companies operating in the Electricians industry in the United States are Quanta Services, Inc., Emcor Group, Inc. and Cleveland Electric. The company holding the most market share in the Electricians industry in the United States is Quanta Services, Inc. The level of competition is high and steady in the Electricians industry in the United States.

Competitive Landscape

Top 5 companies for U.S. electrical services industry are Quanta Services, EMCOR Group, APi Group, MYR Group, and MasTec holds 45% market share.

The competitive landscape reveals MYR Group's positioning as a mid-sized specialist in a fragmented market dominated by Quanta Services:

Quanta Services is a U.S. corporation that provides infrastructure services for the electric power, pipeline, industrial and communications industries. Its capabilities include planning, design, installation, program management, maintenance and repair of most types of network infrastructure. The company has grown organically since its founding, but it has also acquired over 150 companies in the electrical contracting industry. Quanta Services employs about 40,000. Measured as part of the S&P 500, its operating companies achieved combined revenues of about $24.9 billion (US) in 2024.

In 2024, Quanta Services achieved record revenues of $23.67 billion, up from $20.88 billion in 2023. With a backlog of $35.3 billion as of March 2025, the company is well-positioned to capitalize on the increasing demand for infrastructure solutions, including those driven by data center expansion for AI.

Quanta operates at a fundamentally different scale—roughly 7x MYR Group's revenue. But MYR Group competes effectively by:

- Focusing on markets where local relationships and specialized expertise matter more than scale

- Maintaining lower overhead costs through its decentralized structure

- Avoiding the acquisition integration challenges that larger roll-ups often face

- Targeting projects where quality execution matters more than price

Leading the pack, Texas-based Quanta Services recorded the highest revenue of any U.S. electrical contracting business in 2022, with nearly $17 billion in revenue. The next-closest contracting company was Colorado-based MYR Group, which recorded more than $3 billion in revenue in 2022. In a close third place was California-based electrical contractor Rosendin Electric.

The Labor Challenge

The electrical contracting industry is grappling with a severe and worsening shortage of skilled workers, with the Bureau of Labor Statistics projecting a need for 80,000 new electrician jobs annually through 2031.

Despite these efforts, the shortage remains critical. The electrical workforce is projected to shrink by 14% by 2030, while demand could increase by as much as 25% over the same time. This gap is particularly concerning given the growing demand for electricians in emerging sectors.

According to the National Electrical Contractors Association, nearly 30% of union electricians are at or close to retirement age. As people leave the profession, they create openings for new workers. According to the U.S. Bureau of Labor Statistics, there will be an increase in available electrician jobs of more than 84,000 over the decade.

That labor market conundrum threatens to stall the transition to renewable energy, which is crucial for meeting climate goals and reducing carbon emissions, as well as other booms where power needs are intense, including cryptocurrencies and artificial intelligence. It's a golden opportunity for tens of thousands of workers to enter a stable profession, with many open positions in the years ahead, and offering solid pay. "The electrification industry is alive and well, and will be in high demand for a decade-plus," said David Long, CEO of the National Electrical Contractors Association. "There's not an aspect of American life that will not be impacted by the work of electricians."

This labor shortage creates both risks and opportunities for established contractors. Companies with strong safety records, training programs, and employee benefits can attract workers away from competitors. But labor constraints can also limit revenue growth regardless of available project opportunities.

IX. Porter's Five Forces & Strategic Analysis

Threat of New Entrants: LOW

Electrical contracting exhibits meaningful barriers to entry:

- Licensing and bonding requirements: State and local regulations require extensive licensing, insurance, and financial bonding that new entrants must satisfy

- Safety track records: Utilities and large commercial clients evaluate safety performance over years before qualifying contractors for major work

- Equipment capital: Specialized equipment for transmission line work requires significant upfront investment

- Workforce development: Building a skilled workforce takes years of apprenticeship and training investment

- Relationship switching costs: Long-standing client relationships are difficult to replicate

Bargaining Power of Customers: MODERATE

Utility customers have significant purchasing power, but several factors limit their leverage:

- Limited pool of qualified contractors for complex projects

- Long-term alliance agreements create mutual dependency

- Switching costs include qualification processes and relationship rebuilding

- Safety and quality concerns outweigh pure price competition

Bargaining Power of Suppliers: LOW TO MODERATE

Electrical contractors are primarily labor-intensive businesses. Equipment and materials are commodities available from multiple suppliers. The main supply constraint is labor, where workers can command premium wages in tight markets.

Threat of Substitutes: LOW

There is no substitute for electrical infrastructure. Utilities cannot defer transmission line maintenance indefinitely. Data centers require electrical connections regardless of technological changes. The energy transition increases rather than decreases demand for electrical services.

Competitive Rivalry: MODERATE TO HIGH

The U.S. electrical contractors market is highly fragmented, with several vendors operating. Quanta Services, MYR Group, ArchKey Solutions, EMCOR Group, MasTec, and more have a sizeable local presence and major U.S.

The fragmented market creates intense competition for smaller projects but more favorable dynamics for large-scale work where fewer competitors have necessary capabilities.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Moderate. Size provides advantages in equipment utilization, purchasing, and overhead absorption, but local execution limits traditional scale economies.

Network Effects: Limited. Unlike platforms, electrical contracting doesn't exhibit network effects where more users increase value for others.

Counter-Positioning: Present. MYR Group's decentralized subsidiary model allows local responsiveness that larger, more integrated competitors struggle to match.

Switching Costs: Significant. Multi-decade customer relationships, alliance agreements, and qualification processes create meaningful switching costs.

Branding: Limited. Brand matters less than track record and personal relationships in B2B infrastructure services.

Cornered Resource: Moderate. The skilled workforce shortage means contractors with strong training programs and safety cultures have access to labor that competitors cannot easily replicate.

Process Power: Present. Decades of experience with complex transmission projects create execution capabilities that take years for competitors to develop.

X. Investment Considerations

Bull Case

Secular tailwinds are extraordinary: The convergence of grid modernization, AI-driven data center demand, renewable energy integration, and EV charging infrastructure creates multi-decade demand growth for electrical contractors. The explosion in interest in generative artificial intelligence has resulted in an arms race to develop the technology, which will require many high-density data centers as well as much more electricity to power them. Goldman Sachs Research forecasts global power demand from data centers will increase 50% by 2027 and by as much as 165% by the end of the decade.

Balance sheet strength enables opportunistic acquisitions: With significant credit facility availability and low leverage, MYR Group can pursue acquisitions during market dislocations when competitors may be constrained.

Customer stickiness protects margins: Long-term utility relationships and alliance agreements provide revenue visibility and limit competitive pressure on pricing.

Leadership continuity: Appointed President and Chief Executive Officer in January 2017, Rick brings more than 40 years of experience in the electrical construction industry. In this role, he assumes complete profit and loss responsibility for MYR Group and its subsidiaries and chairs the company's executive committee. MYR Group's performance reflects Rick's strong leadership as we strive to be the most efficient, high value provider to our clients.

Bear Case

Project execution risk: The 2024 results demonstrated how troubled projects can significantly impact profitability. Fixed-price contracts in particular expose the company to cost overruns.

Labor constraints limit growth: Even with strong demand, workforce shortages may cap revenue growth and pressure wages, compressing margins.

Quanta's scale advantage: The company's strategic shift, particularly the acquisition of Cupertino Electric, underscores its Quanta Services growth strategy to capitalize on the expanding digital infrastructure and energy transition trends. This move positions Quanta Services as a comprehensive provider for power transmission and distribution needs, enhancing its competitive advantages and market share. Quanta's aggressive acquisition strategy could put competitive pressure on MYR Group in key markets.

Data center demand uncertainty: Electricity companies across the U.S. are struggling to figure out how much demand will actually materialize from the artificial intelligence boom. "There is a question about whether or not all of the projections, if they're real," Willie Phillips, who served as chairman of the Federal Energy Regulatory Commission from 2023 until April 2025, told CNBC. "There are some regions who have projected huge increases, and they have readjusted those back."

Regulatory and permitting delays: Transmission project timelines are frequently extended by permitting challenges and local opposition, creating revenue timing uncertainty.

XI. Key Performance Indicators

For investors tracking MYR Group's ongoing performance, three metrics deserve primary attention:

1. Backlog and Book-to-Bill Ratio

Backlog represents contracted but not yet recognized revenue. The book-to-bill ratio (new orders divided by revenue) indicates whether the project pipeline is growing or shrinking. Current backlog of $2.66 billion represents approximately 9 months of revenue, providing reasonable visibility. A sustained book-to-bill above 1.0x suggests healthy demand; below 1.0x indicates potential revenue headwinds.

2. Gross Margin by Segment

Gross margin tracks pricing power and execution quality. MYR Group targets a T&D margin range of 7-10.5%. Margins below this range suggest project challenges, competitive pressure, or labor cost inflation outpacing contract pricing. The 2024 margin compression from troubled clean energy projects illustrates how execution issues directly impact profitability.

3. Revenue Mix: Data Centers and Clean Energy

The composition of revenue by end market reveals positioning for future growth. Increasing share from data centers and clean energy projects suggests successful capture of secular growth opportunities. Traditional utility T&D work provides stable baseline revenue but limited growth.

XII. Concluding Thoughts

Lewis Edward Myers probably couldn't have imagined that his street lighting business would, 130 years later, be building electrical infrastructure for artificial intelligence data centers. But there's a through-line from 1891 to today: the business of bringing electricity where it's needed remains essential, complex, and difficult to disrupt.

MYR Group occupies an interesting position in America's energy infrastructure. It's large enough to compete for major projects but small enough to maintain the local relationships that drive repeat business. It's exposed to exciting secular growth in data centers and clean energy while maintaining stable utility relationships that provide revenue visibility. It's conservatively financed but actively growing through acquisition.

The most recent and ongoing transformation is the company's performance in the 2025 fiscal year, driven by infrastructure investment and the clean energy transition. This is where the strategy pays off in hard numbers: Record Revenue: Q3 2025 revenue hit $950.40 million, a 7.0 percent year-over-year increase, showing robust demand.

The next decade will test whether MYR Group can capitalize on the extraordinary convergence of grid modernization, AI power demand, and energy transition spending. The company's century-long track record of adapting to new technologies—from street lights to 765kV transmission lines to utility-scale solar—provides some comfort that it can navigate the current transition as well.

For investors with a long-term horizon, infrastructure businesses like MYR Group offer something increasingly rare in public markets: durable competitive positions in essential services with visible growth tailwinds and manageable risks. The story that began with Edison's salesman in 1891 may have many chapters still to be written.

Myth vs. Reality

| Common Perception | Reality |

|---|---|

| "Boring utility contractor with limited growth" | Data center and clean energy exposure creates meaningful growth optionality |

| "Just a smaller Quanta Services" | Decentralized model and local relationships create different competitive position |

| "Commoditized labor-driven business" | 50+ year customer relationships and specialized capabilities create meaningful barriers |

| "AI power demand is hype" | Actual utility connection requests and construction spending confirm demand is real |

| "Infrastructure is recession-proof" | Generally resilient but not immune—2024 showed project execution can impact results |

This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube