SS&C Technologies: The Fintech Empire Built From a Basement

I. Introduction & Cold Open

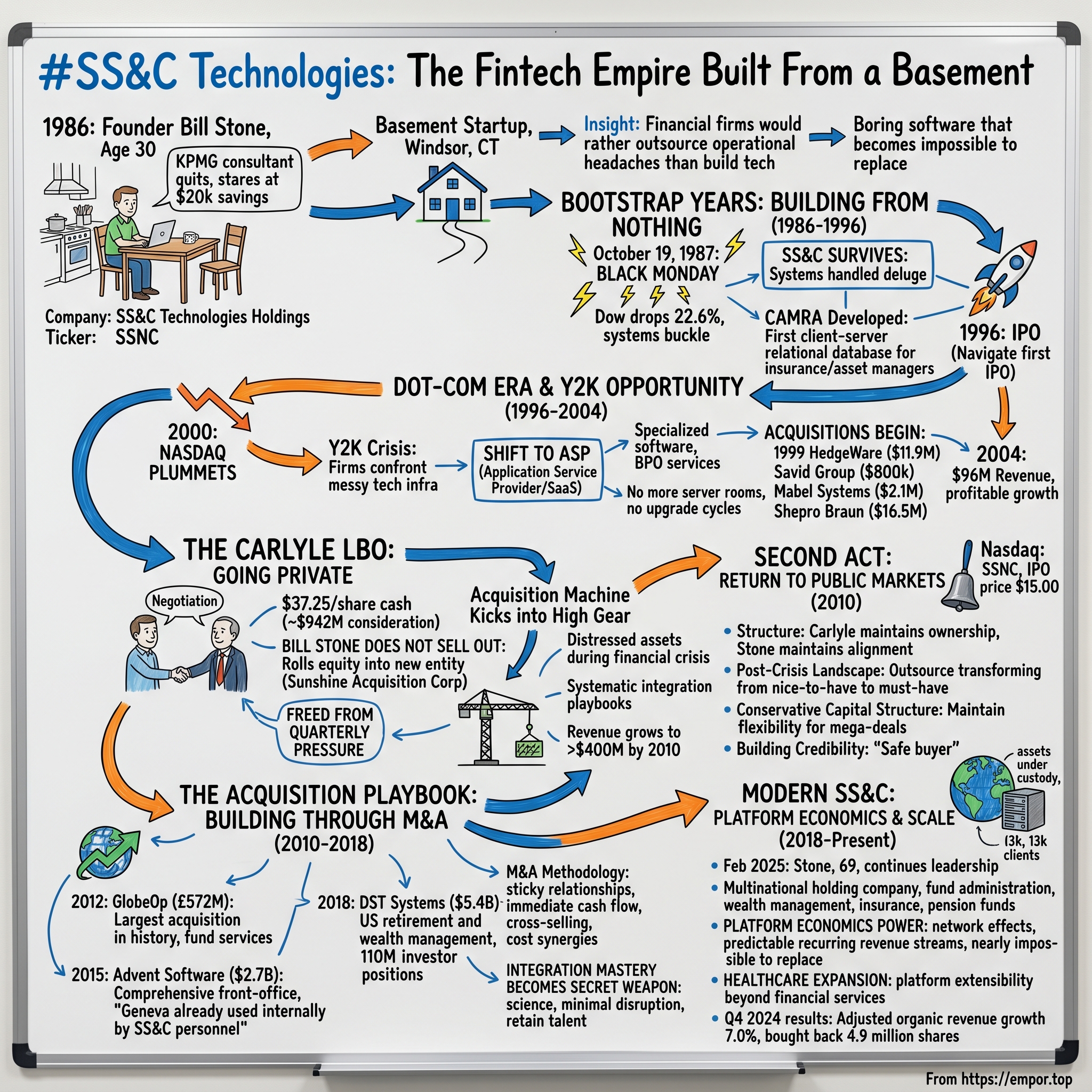

Picture this: It's 1986 in Windsor, Connecticut. A 30-year-old KPMG consultant named Bill Stone sits at his kitchen table, staring at $20,000 in savings—his entire net worth. He's about to make a decision that would terrify most people: quit his stable job and start a software company from his basement. No venture capital. No safety net. Just a conviction that Wall Street's back-office operations were ripe for disruption.

Fast forward to today. That basement startup, SS&C Technologies, processes over $1.69 trillion in assets under custody. Its software powers the operations of 13,000 clients worldwide, from hedge funds to pension plans. With $5.9 billion in annual revenue and a market cap hovering around $19 billion, SS&C has become the invisible infrastructure of global finance—the plumbing that makes modern investment management possible.

How does a bootstrapped company from Connecticut become Wall Street's back-office powerhouse? Through more than 50 acquisitions, two trips through public markets, a private equity buyout, and an almost maniacal focus on the unglamorous work that investment firms desperately need but never want to do themselves.

This is the story of how Bill Stone built a fintech empire by betting on a simple insight: as financial markets grew more complex, the firms managing money would rather outsource their operational headaches than build technology themselves. It's a bet that's paid off spectacularly—but the journey from basement startup to financial services behemoth reveals deeper lessons about timing, persistence, and the power of boring software that becomes impossible to replace.

II. Bill Stone & The Pre-Founding Story

The football captain from Evansville stared at the computer screen in the KPMG Hartford office. It was 1985, and Bill Stone had just been promoted to director—a significant achievement for someone only eight years out of college. But something gnawed at him.

Born and raised in Evansville, Indiana, Bill Stone graduated from Reitz Memorial High School in 1973 alongside his future wife Mary O'Daniel. In high school, Stone was captain of Reitz Memorial's football team—leadership qualities that would define his future approach to business. After high school, Stone attended Marquette University in Milwaukee, Wisconsin, receiving a Bachelor of Business Administration in 1977.

Stone began his career in 1977 at KPMG, a financial services consultancy and accounting firm, initially working out of St. Louis before transferring to Hartford, Connecticut. By 1985, he'd risen to director—impressive for someone barely 30. But watching his clients struggle with back-office operations, Stone saw opportunity where others saw tedium.

The financial services industry of the mid-1980s was undergoing seismic shifts. Personal computers were infiltrating trading floors. Lotus 1-2-3 was replacing paper ledgers. Yet most investment firms still ran their back offices like it was 1965—armies of clerks manually processing trades, calculating NAVs, and producing client statements. The software that did exist was either mainframe-based (expensive and inflexible) or cobbled together from spreadsheets (error-prone and unscalable).

Stone understood something fundamental: the PC revolution wasn't just about hardware getting cheaper. It was about democratizing computing power. A hedge fund with $50 million under management could now afford the same processing capability that once required a million-dollar mainframe. But they needed software designed for this new world—client-server architecture, relational databases, real-time processing.

In 1986 and at the age of 30, Founder and CEO Bill Stone quit his job to start SS&C from the basement of his house. The name stood for Securities Software & Consulting—straightforward, no-nonsense, exactly like its founder. The goal was simple - develop better technology and deliver superior service.

This wasn't a Silicon Valley story of venture capital and hockey stick growth projections. This was Connecticut—hedge fund country, insurance capital of America. Stone wasn't trying to change the world; he was trying to solve a specific problem for a specific set of customers he knew intimately from his KPMG days. The timing couldn't have been better: Wall Street was about to explode in complexity, and someone needed to handle the plumbing.

III. The Bootstrap Years: Building From Nothing (1986-1996)

The four employees huddled around a folding table in Stone's basement, watching the Dow Jones plummet. It was October 19, 1987—Black Monday. The Dow Jones Industrial Average dropped 22.6 percent in a single trading session, the largest one-day decline in stock market history. For a one-year-old startup selling financial software, this should have been a death sentence.

But Bill Stone saw opportunity in the chaos. As trading firms scrambled to process the unprecedented volume of transactions, their systems buckled. Manual processes that worked fine in calmer markets completely broke down. The firms that survived Black Monday weren't necessarily the smartest or the best capitalized—they were the ones with systems that could handle the deluge.

In 1986 and at the age of 30, Founder and CEO Bill Stone quit his job to start SS&C from the basement of his house. The goal was simple - develop better technology and deliver superior service. Stone started with just four employees, growing to 17 the next year, then doubling in 1988—remarkable growth considering the market trauma of October 1987.

The survival through Black Monday wasn't luck. Stone had positioned SS&C perfectly for the post-crash world. While competitors built monolithic mainframe systems, SS&C developed CAMRA—the first client-server, relational database investment accounting system for insurance companies and asset managers. This wasn't just incrementally better technology; it was a fundamental reimagining of how financial data should flow through an organization.

CAMRA represented a philosophical shift. Instead of forcing clients to adapt their workflows to the software, SS&C built software that adapted to how investment professionals actually worked. Real-time processing. Distributed architecture. SQL databases that let analysts actually query their own data without calling IT. Revolutionary concepts in 1988, but Stone understood that the future belonged to flexible, scalable systems.

The bootstrap mentality permeated everything. No venture capital meant every dollar mattered. Stone couldn't afford to build features nobody wanted or chase trendy technologies that didn't solve real problems. This constraint became SS&C's greatest strength—an obsessive focus on what clients actually needed, not what looked good in a demo.

By the early 1990s, SS&C had expanded beyond CAMRA into a comprehensive suite: LMS for loans, PORTIA for portfolio management, PAWS for private wealth. Each product followed the same philosophy—solve a specific problem exceptionally well, then integrate seamlessly with everything else. Clients could start with one module and expand as needed, creating switching costs that would become legendary in the industry.

The numbers tell the story of disciplined growth. From zero in 1986 to $18 million in revenues by the mid-1990s—all organic, all profitable, all without diluting Stone's ownership. This wasn't the hockey-stick growth that venture capitalists craved, but it was sustainable, predictable, and entirely under Stone's control.

SS&C Technologies went public in 1996 with Stone navigating the firm's initial public offering (IPO). The decision to go public wasn't about cashing out—Stone would maintain control and continue running the company for decades to come. It was about accessing capital for the next phase: acquisitions. The bootstrap years had proven the model worked. Now it was time to scale.

IV. The Dot-Com Era & Y2K Opportunity (1996-2004)

The conference room at SS&C's Windsor headquarters was silent except for the hum of servers. It was March 2000, and Bill Stone watched the NASDAQ plummet on the television screen—down 25% in a week. Around him, his executives waited for direction. Most of their clients were hemorrhaging value. Competitors were laying off staff by the hundreds. But Stone saw something different: opportunity.

"Y2K marks a significant change from the way financial services companies do business; they don't want to manage and build up back-office operations. ASP is where it's at and SS&C is prepared to take advantage of the trend." This wasn't just marketing speak—it was a fundamental insight about where the industry was heading.

The Y2K crisis had forced financial institutions to confront an uncomfortable truth: their technology infrastructure was a mess. Legacy systems built in COBOL, patched together over decades, nearly brought the global financial system to its knees. The remediation effort cost billions, and for what? To maintain systems that were already obsolete.

Enter the Application Service Provider (ASP) model—what we'd later call Software as a Service. Instead of installing software on-premise, clients could access SS&C's applications over the internet. No more server rooms. No more upgrade cycles. No more hiring armies of IT staff to maintain systems. For financial firms still traumatized by Y2K, the pitch was irresistible.

Stone had positioned SS&C perfectly for this shift. SS&C Technologies provided the financial services industry with a broad range of highly specialized software, business process outsourcing (BPO) services and application service provider (ASP) solutions. While dot-com darlings burned through venture capital building consumer websites nobody wanted, SS&C quietly built the infrastructure that actual businesses needed.

The acquisition strategy began modestly but strategically. In 1999, SS&C acquired HedgeWare for $11.9 million (later renamed AdvisorWare), expanding their hedge fund software and services offerings. The Savid Group followed for just $800,000, adding middle- and back-office derivatives accounting capabilities. Mabel Systems for $2.1 million brought European clients and presence. Shepro Braun for $16.5 million added comprehensive front-office capabilities to complement existing back-office solutions.

These weren't sexy acquisitions that would make headlines. But each one filled a specific gap in SS&C's product suite, added new clients, or expanded geographic reach. While the market obsessed over "eyeballs" and "stickiness," Stone focused on boring metrics like recurring revenue and customer retention.

For the year ended December 31, 2004, SS&C generated $19.0 million of net income, or $0.84 per share, on $95.9 million of total revenues. These weren't dot-com numbers—no hockey stick growth, no path to profitability promises. Just consistent, profitable growth while the rest of the tech world imploded.

The competitive landscape during this period was fascinating. Traditional enterprise software companies like Oracle and SAP largely ignored financial services verticals, viewing them as too specialized. Pure-play financial software companies were either going bankrupt or getting acquired at fire-sale prices. And the new breed of ASP providers were mostly focused on horizontal applications like CRM or email.

SS&C occupied a unique position: specialized enough to serve financial services deeply, but diversified enough across asset classes and functions to weather any single market downturn. SS&C provided comprehensive ASP/BPO services through its SS&C Direct operating unit for portfolio accounting, reporting and analysis functions, complete on- and offshore fund administration outsourcing services to hedge fund and other alternative investment managers.

The dot-com crash that devastated Silicon Valley barely touched SS&C. Their clients—hedge funds, private equity firms, insurance companies—needed their services more than ever as market volatility increased operational complexity. The shift from on-premise to ASP accelerated as CFOs, burned by massive Y2K spending, demanded operating expense models over capital expenditure.

By 2004, SS&C had emerged from the dot-com wreckage stronger than ever. Revenue had grown from $18 million in the mid-1990s to nearly $96 million. The company was profitable, growing, and perfectly positioned for what would come next: a transformative private equity deal that would supercharge their acquisition strategy.

V. The Carlyle LBO: Going Private (2005)

Bill Stone sat across from Bud Watts of Carlyle in a Manhattan conference room, July 2005. The offer was on the table: $37.25 per share in cash, representing a 15.7% premium over the average closing price of SS&C's stock for the last thirty trading days. The aggregate consideration to be paid to SS&C stockholders and option holders was approximately $942 million.

For most founder-CEOs, this would be the exit—take the money, maybe stay on for a transition period, then ride off into the sunset. But Stone had something different in mind. He wasn't selling out; he was buying in.

The genius of Stone's negotiation became clear in the deal structure. Immediately prior to the consummation of the transaction, William C. Stone, SS&C's Chairman of the Board and Chief Executive Officer, would be contributing certain of his shares of SS&C common stock in exchange for approximately 28% of the equity of Sunshine Acquisition Corporation. Stone wasn't cashing out—he was rolling his equity into the new entity, betting that SS&C's best days were ahead.

Why sell to private equity after building for 19 years? The public markets of 2005 didn't understand—or properly value—SS&C's model. Quarterly earnings calls focused on short-term metrics. Analysts questioned acquisition spending. The market wanted predictable 10% annual growth, not the lumpy but transformative expansion Stone envisioned.

Carlyle offered something different: patient capital and operational expertise. The Carlyle Group was a global private equity firm with $31 billion under management, investing in buyouts, venture capital, real estate and leveraged finance in Asia, Europe and North America. Since 1987, the firm had invested $14.3 billion of equity in 414 transactions for a total purchase price of $49.5 billion.

"The combination of Carlyle and SS&C will be a powerful force in financial technology and services. The public shareholders received a very full price for our shares and we are happy to have delivered excellent value to them," Stone commented. But the subtext was clear: freed from quarterly earnings pressure, SS&C could pursue a more aggressive acquisition strategy.

Bud Watts, Managing Director of The Carlyle Group, stated, "We'd like to thank the entire SS&C management team for their considerable efforts in making this transaction happen. We are pleased to have Bill Stone at the helm, and are excited about backing a strong management team with an outstanding track record and a clear strategy for long-term growth. We look forward to supporting the SS&C team as they continue to grow the business".

The financing structure revealed Carlyle's confidence: The acquisition would be financed through a combination of equity contributed by investment funds affiliated with The Carlyle Group and debt financing provided by affiliates of Wachovia, JPMorgan and Bank of America. This wasn't a strip-and-flip play—it was a growth investment.

During the private years (2005-2010), SS&C transformed from a software company that did some services into a full-stack financial technology platform. The acquisition machine kicked into high gear. Without the scrutiny of public markets, Stone could make bold bets on distressed assets during the financial crisis. Companies that would have been too risky for a public company to acquire became perfect targets for PE-backed SS&C.

The operational improvements were equally important. Carlyle brought discipline to SS&C's acquisition integration process. They developed playbooks for combining operations, migrating clients, and achieving cost synergies. What had been somewhat ad hoc became systematic and repeatable.

Revenue grew from roughly $96 million in 2004 to over $400 million by 2010. EBITDA margins expanded. The client base diversified. Most importantly, SS&C built the operational infrastructure to handle much larger acquisitions—capabilities that would prove essential in the coming decade.

On July 28, 2005, SS&C entered into a merger agreement with Sunshine Acquisition Corporation and its wholly owned subsidiary, Sunshine Merger Corporation. SS&C stock ceased to trade on the NASDAQ National Market at the close of market on November 23, 2005 and was delisted.

The Carlyle years weren't just about financial engineering. They were about building the muscles SS&C would need to become a consolidator. Stone learned how private equity thinks about value creation, debt capacity, and return hurdles. Carlyle learned that sometimes the best investment is backing a founder who refuses to let go.

VI. The Second Act: Return to Public Markets (2010)

March 31, 2010. The opening bell rang at the NASDAQ, and Bill Stone stood on the podium surrounded by SS&C executives. Five years after going private, SS&C was public again. SS&C Technologies Holdings, Inc. (Nasdaq: SSNC) announced the initial public offering of 10,725,000 shares of its common stock at a price to the public of $15.00 per share. The shares began trading on the NASDAQ Global Select Market under the ticker symbol "SSNC."

The timing was counterintuitive. The financial crisis of 2008 had devastated markets. IPO activity was near historic lows. But Stone saw what others missed: the crisis had created a once-in-a-generation consolidation opportunity in financial services technology.

Of the 10,725,000 shares being offered to the public, 8,225,000 shares were offered by SS&C and 2,500,000 by selling shareholders—primarily Carlyle. The structure revealed the alignment: Carlyle was taking some chips off the table but maintaining significant ownership. Stone wasn't selling a single share.

The transformation during the private years was remarkable. Revenue had grown from under $100 million to over $400 million. The company had completed multiple acquisitions, built out its service capabilities, and expanded globally. Most importantly, SS&C had developed the operational infrastructure to handle much larger deals.

Why return to public markets? The answer lay in the post-crisis landscape. Distressed financial services firms were shedding non-core technology assets. Standalone software companies couldn't access capital. Private equity owners needed exits. The consolidation opportunity was massive, but it required currency—public stock that could be used in acquisitions.

J.P. Morgan Securities Inc., Credit Suisse Securities (USA) LLC, Morgan Stanley & Co. Incorporated and Deutsche Bank Securities Inc. acted as joint book-running managers for the offering—a blue-chip underwriting syndicate that signaled institutional confidence in SS&C's strategy.

The public market reception was telling. Unlike the dot-com era IPOs that promised future profitability, SS&C was already highly profitable with strong cash flows and recurring revenue. This wasn't a growth story built on hope; it was an execution story built on a proven track record.

The financial crisis had fundamentally changed how financial institutions thought about technology. Before 2008, many firms believed technology was a competitive advantage worth building internally. After watching Lehman Brothers collapse and Bear Stearns get sold for pennies, priorities shifted. Survival trumped differentiation. Cost reduction became paramount. Outsourcing transformed from nice-to-have to must-have.

SS&C positioned itself perfectly for this shift. After some years as a private company, SS&C was taken public again in a second IPO in 2010 through a listing on Nasdaq under the symbol SSNC, emerging as the natural consolidator in a fragmented market. The company could offer distressed firms immediate cost savings through outsourcing while providing private equity owners an exit for their portfolio companies.

The capital structure post-IPO was conservative by design. Unlike many PE-backed IPOs that went public with massive debt loads, SS&C maintained flexibility for acquisitions. The balance sheet could support significant leverage when the right opportunity arose—a capability that would prove crucial for the mega-deals ahead.

From 2010 to 2012, SS&C operated in acquisition preparation mode. Small tuck-in deals continued, but Stone was hunting bigger game. The company built relationships with investment banks, developed detailed integration playbooks, and assembled a war chest for transformative acquisitions.

The market initially didn't fully appreciate SS&C's positioning. The stock traded sideways for much of 2010-2011 as investors tried to understand the model. Was it a software company? A services business? A roll-up story? The answer was yes to all three, but that complexity made it hard to value using traditional metrics.

Setting up for the next decade of M&A required more than just capital. SS&C needed to prove it could execute large-scale integrations without disrupting client operations. Every successful integration built credibility for the next, larger deal. The company was building a reputation as the safe buyer—the acquirer that employees wanted to work for and clients trusted to maintain service quality.

VII. The Acquisition Playbook: Building Through M&A (2010-2018)

The war room at SS&C headquarters, June 2012. Bill Stone stood before a whiteboard covered in numbers, integration timelines, and client retention projections. The target: GlobeOp Financial Services, a Luxembourg-based fund administrator. The price: £4.85 per share, approximately £572 million (roughly $814 million at the time). SS&C Technologies Holdings, Inc. announced its acquisition of GlobeOp Financial Services S.A. (GlobeOp), for £4.85 per share (approximately £572 million).

The acquisition is, by value, the largest in SS&C's history and significant for the fund services industry. But size wasn't the point—strategic fit was. GlobeOp provides independent fund services, specializing in middle and back office services and integrated risk-reporting to hedge funds, asset management firms and other sectors of the financial industry. This wasn't just buying revenue; it was buying expertise in fund administration that would transform SS&C's service capabilities.

The methodology behind SS&C's acquisition playbook had crystallized by this point. First, identify targets with sticky client relationships and recurring revenue. Second, pay a full price but structure the deal to ensure immediate cash flow coverage. Third, integrate operations while maintaining client service continuity. Fourth, cross-sell aggressively into the combined client base. Finally, achieve cost synergies through scale and operational efficiency.

The acquisition was funded by a new credit facility that also re-financed SS&C's existing credit facility. The new facility includes Term A loans of $325 million, Term B loans of $800 million and a Bridge loan of $31.6 million. The Term A Loans and the Bridge Loan will initially bear interest at LIBOR plus 2.75%. The Term B Loans will initially bear interest at LIBOR plus 4.00%, with LIBOR subject to a 1.00% floor. The financing structure revealed Stone's confidence in generating immediate cash flows from the acquisition.

Three years later came the transformative deal: Advent Software. Under the terms of the agreement, SS&C will purchase Advent for an enterprise value of approximately $2.7 billion in cash, equating to $44.25 per share plus assumption of debt. Advent has more than 4,300 customers including asset managers, hedge funds, fund administrators, prime brokers, family offices and wealth management advisory firms, located across more than 50 countries worldwide.

Bill Stone on the Advent acquisition: "It's a very full price, but it's worth it", citing the "literally hundreds" of opportunities to upsell existing clients. The strategic rationale was compelling: "Geneva already has 2,400 SS&C personnel using it everyday". SS&C knew Advent's products intimately because they were already using them internally.

SS&C plans to fund the acquisition and refinancing of existing debt with $3.0 billion of debt financing and cash on hand and approximately $400 million of equity. For the twelve months ended December 31, 2014, adjusted EBITDA for the combined pro forma entity is expected to be approximately $500 million with synergies. SS&C expects leverage to be approximately 5.3x net debt to last twelve months pro forma EBITDA at closing, and anticipates rapid deleveraging through the strong cash flow of the combined business.

The Advent deal showcased SS&C's evolution. The transaction represents a continuation of SS&C's proven growth strategy through acquisitions in the financial services software and software-enabled services industries, as evidenced by 40 acquisitions to date including GlobeOp in 2012 and DST Global Solutions in 2014. Each acquisition built on the previous ones, creating a compounding effect of capabilities and scale.

Then came the biggest deal yet: DST Systems in 2018. SS&C will acquire DST for $84 per share in cash for an enterprise value of $5.4 billion, including assumption of debt. The transaction significantly increases SS&C's scale, with approximately $3.9 billion in combined pro forma revenue and 13,000 clients. Additionally, the transaction expands SS&C's footprint into the US retirement and wealth management markets and adds 110+ million investor positions across DST's client base.

"SS&C will manage approximately 13,000 global clients and delivered pro forma 2017 revenue of approximately $3.9 billion. 'We are pleased to move forward as one company following the combination of two highly complementary market leaders,' said Bill Stone, Chairman and Chief Executive Officer of SS&C".

The DST acquisition represented peak execution of the SS&C playbook. As previously announced, SS&C expects the transaction to be immediately accretive to earnings per share before synergies and expects to achieve $175 million in cost savings by 2021. This wasn't hope—it was based on decades of integration experience.

Integration mastery became SS&C's secret weapon. While competitors struggled to combine operations without disrupting service, SS&C had it down to a science. Day one: maintain all client touchpoints. Week one: begin cross-training staff. Month one: identify redundant systems. Quarter one: start migrating clients to SS&C platforms. Year one: achieve initial cost synergies. The playbook was ruthlessly efficient yet surprisingly humane—SS&C retained key talent from acquired companies, often promoting them to run expanded divisions.

The acquisitions from 2010-2018 transformed SS&C from a $400 million revenue company to nearly $4 billion. But more importantly, they transformed SS&C from a software vendor into something unique: a full-stack financial technology platform that could handle any aspect of investment operations, from trade execution to investor reporting, from portfolio accounting to regulatory compliance.

VIII. The Modern SS&C: Platform Economics & Scale (2018-Present)

The conference room at SS&C's Windsor headquarters overlooks a campus that now spans multiple buildings—a far cry from Bill Stone's basement in 1986. It's February 2025, and Stone, now 69, reviews the latest earnings report. Q4 2024 GAAP revenue $1,529.7 million, up 8.4%, Fully Diluted GAAP Earnings Per Share $0.98, up 27.3%; Record Adjusted revenue $1,530.7 million, up 8.4%, Adjusted Diluted Earnings Per Share $1.58, up 25.4%.

Today's SS&C is a multinational holding company with offices in Americas, Europe, Asia, Africa and Australia, specializing in fund administration, wealth management, insurance and pension funds. Named to the Fortune 1000 list as a top U.S. company based on revenue, SS&C (NASDAQ: SSNC) is a trusted provider to more than 20,000 financial services and healthcare companies, with over 25,000 employees and operations in more than 40 countries.

The transformation from software vendor to platform powerhouse is complete. In 2020 SS&C Technologies reported in their balance sheet over $1.69 trillion in Assets Under Custody (AUC). The company has become what Stone always envisioned: the invisible infrastructure powering global finance.

"SS&C reported strong results for Q3 2024, with organic revenue up 6.4 percent, accompanied by $1.29 in adjusted earnings per share, up 10.1 percent," says Bill Stone, Chairman and Chief Executive Officer. "A few weeks ago we hosted over 1,000 clients, prospects, and partners in New Orleans for our annual SS&C Deliver Conference. We showcased SS&C's strengths in emerging technology, best practice operational solutions, and deep industry expertise. Feedback has been overwhelmingly positive and we look forward to another great event in Scottsdale, AZ in 2025."

Q4 2024 GAAP Revenue growth and Adjusted Revenue growth were 8.4 percent. Q4 Adjusted Organic Revenue Growth was 7.0 percent, Financial Services Recurring Revenue Growth was 7.4 percent. These aren't just numbers—they represent the compounding power of platform economics. Each new client makes the platform more valuable for existing clients. Each new capability creates cross-sell opportunities across thousands of relationships.

SS&C generated net cash from operating activities of $1,388.6 million for the twelve months ended December 31, 2024, up 14.3 percent compared to the same period in 2023. This cash generation machine funds continuous innovation and strategic acquisitions without diluting shareholders.

The subscription model advantage has fully materialized. Unlike traditional software companies that rely on lumpy license sales, SS&C's revenue streams are predictable and recurring. Clients pay monthly or quarterly fees for software access, processing services, and fund administration. Once embedded in a client's operations, SS&C becomes nearly impossible to replace.

Network effects in financial services software work differently than in consumer tech. It's not about viral growth or user-generated content. It's about data standardization, regulatory compliance, and operational integration. When a hedge fund uses SS&C for fund administration, their auditors, prime brokers, and investors all interface with SS&C systems. Each connection increases switching costs exponentially.

SS&C Technologies Holdings (NASDAQ: SSNC) is the world's largest hedge fund and private equity administrator, as well as the largest mutual fund transfer agency. SS&C's unique business model combines end-to-end expertise across financial services operations with software and solutions to service even the most demanding customers in the financial services and healthcare industries.

The modern SS&C operates at a scale that creates its own gravity. Small competitors can't match the R&D investment. Large competitors can't match the specialization. Private equity buyers can't find synergies because SS&C already operates at optimal efficiency.

Q4 2024 we bought back 4.9 million shares for $365.7 million, at an average price of $74.46 per share. This aggressive capital return reflects confidence in the business model. When you generate over a billion dollars in operating cash flow annually with minimal capital requirements, returning cash to shareholders becomes a strategic imperative.

Platform economics at SS&C's scale create virtuous cycles. More clients generate more data, which improves products, which attracts more clients. Higher volumes reduce per-unit costs, enabling competitive pricing while maintaining margins. Broader capabilities enable deeper client relationships, increasing lifetime value.

The healthcare expansion demonstrates the platform's extensibility beyond financial services. The same capabilities that process hedge fund transactions can handle healthcare claims. The same security infrastructure that protects financial data can safeguard patient information. The same workflow automation that streamlines fund administration can optimize hospital operations.

IX. Business Model & Competitive Moats

The elevator pitch for SS&C is deceptively simple: we handle the tedious, complex, mission-critical operations that financial firms need but don't want to do themselves. The reality is far more nuanced and powerful.

Switching costs at SS&C aren't just high—they're prohibitive. Consider what it takes to change fund administrators: migrating years of historical data, retraining hundreds of employees, updating investor reporting systems, notifying regulators, coordinating with auditors, and risking operational disruptions that could trigger investor redemptions. One SS&C client described switching providers as "like performing heart surgery on yourself while running a marathon."

The full-stack advantage compounds these switching costs. A hedge fund might start using SS&C for fund administration. Then they add Geneva for portfolio management. Then Eze for trading. Then Intralinks for investor communications. Each additional product creates new integration points and dependencies. Removing SS&C becomes not just difficult but existentially risky.

Recurring revenue dynamics in SS&C's model differ fundamentally from typical SaaS businesses. Software subscriptions might represent 30% of revenue. The remainder comes from processing fees, administration services, and transaction charges—all tied to client AUM and activity levels. When markets rise, SS&C's revenue rises. When trading volumes increase, SS&C's revenue increases. The company wins regardless of which firms succeed, as long as capital keeps flowing through financial markets.

Pricing power emerges from this irreplaceability. Annual price increases of 3-5% are standard, often buried in inflation adjustments or tied to new features. Clients grumble but pay because the switching costs dwarf the incremental expense. A 5% price increase on a $1 million annual contract is $50,000—substantial, but nothing compared to the millions required to switch providers.

SS&C Technologies Holdings (NASDAQ: SSNC) is the world's largest hedge fund and private equity administrator, as well as the largest mutual fund transfer agency. These aren't just titles—they represent market positions that become self-reinforcing. Being the largest means having the most experience with edge cases, the deepest regulatory expertise, and the broadest service capabilities.

Competition exists but struggles to gain traction. FIS and Fiserv focus more on banking and payments. Broadridge dominates proxy voting but lacks SS&C's fund administration depth. State Street has the custody business but treats technology as a cost center, not a profit center. Cloud-native startups like Carta nibble at the edges but lack the regulatory expertise and operational scale to handle institutional clients.

The real competitive moat isn't any single factor—it's the combination. High switching costs plus recurring revenue plus network effects plus regulatory expertise plus operational scale. Competitors might match one or two elements but replicating the entire ecosystem would require decades and billions of dollars with no guarantee of success.

SS&C's position resembles a medieval castle with multiple defensive rings. The outer wall is switching costs. The moat is network effects. The inner keep is operational excellence. The treasury is recurring cash flow. Attackers might breach one defense but face another equally formidable barrier.

This defensive position enables offensive strategies. SS&C can acquire competitors knowing their clients can't easily leave. They can invest in new capabilities knowing the payback period extends decades. They can weather economic downturns knowing recurring revenue provides stability. They can ignore activist investors because founder control and operational complexity deter intervention.

The healthcare expansion illustrates how these moats translate to new markets. The same switching costs that lock in hedge funds apply to hospital systems. The same regulatory expertise that handles SEC compliance works for HIPAA requirements. The same processing infrastructure that manages trades can handle claims. The moat isn't product-specific—it's capability-based.

X. Leadership & Culture: The Bill Stone Factor

William C. Stone founded SS&C in 1986 and has continuously served as Chairman of the Board of Directors and Chief Executive Officer. Mr. Stone took SS&C public in 1996 and private in 2005 with The Carlyle Group. Nearly four decades of continuous leadership—an anomaly in technology and almost unheard of in public companies.

Stone's leadership style reflects his Midwest roots and KPMG training: conservative financially, aggressive operationally. He doesn't do earnings calls well—his answers are terse, sometimes dismissive of analyst questions. But clients and employees describe a different person: engaged, detail-oriented, willing to dive into operational minutiae that most CEOs delegate.

The founder-CEO advantage in M&A cannot be overstated. Stone can make acquisition decisions in days that would take professional CEOs months. He knows every major system, every key client relationship, every integration challenge from personal experience. When evaluating targets, he doesn't need consultants or integration committees—he's supervised 50+ integrations personally.

Building culture through acquisitions typically destroys value. Most companies lose key talent, alienate clients, and dilute their culture with each deal. SS&C does the opposite. Acquired employees often describe joining SS&C as liberating—finally working for a company that understands their business and invests in their products. The culture isn't warm and fuzzy; it's competent and meritocratic.

In 2011, Stone announced a plan to bring 500 new jobs to his hometown, Evansville, Indiana, by 2014. The plan was seen as a boon to downtown Evansville and would add to SS&C Technologies' roster at the time of 1,400 employees around the globe. This wasn't charity—Evansville provided loyal, cost-effective talent away from expensive coastal markets.

In May 2018, Stone and his wife Mary donated $15 million toward a multi-institutional initiative in downtown Evansville, Stone Family Center for Health Sciences. The center was a collaborative effort among the University of Evansville, the University of Southern Indiana and Indiana University to support health sciences programs.

In December 2021, Bill and Mary Stone gifted $34.2 million to establish the Mary O'Daniel Stone and Bill Stone Center for Child and Adolescent Psychiatry at IU School of Medicine-Evansville. These aren't vanity projects—they're strategic investments in the community that provides SS&C's talent pipeline.

The succession question looms large. Stone is 69 with no announced retirement plans. The company has capable executives, but none with Stone's combination of technical knowledge, acquisition expertise, and client relationships. The most likely scenario: a gradual transition with Stone remaining Chairman while a successor handles operations, similar to Oracle's arrangement with Larry Ellison.

Stone's ownership stake—still substantial after decades of acquisitions and buybacks—aligns him with long-term value creation. He's never sold shares in a secondary offering, only in the PE exits where he immediately reinvested. This skin in the game affects every decision: acquisitions must create value, not just generate fees. Operations must be efficient, not just adequate.

The cultural impact of founder leadership extends beyond decision-making. Employees know Stone built the company from nothing, survived multiple crises, and chose to stay when he could have cashed out multiple times. This creates a different dynamic than hired-gun CEOs optimizing for their next role. People work for the mission, not just the paycheck.

XI. Playbook: Lessons for Operators & Investors

The SS&C story from bootstrap to IPO to PE to IPO again offers a masterclass in capital structure evolution. Each phase served a specific purpose: bootstrapping established product-market fit, first IPO provided acquisition currency, PE buyout enabled transformative M&A, second IPO created permanent capital. The lesson: capital structure should evolve with strategy, not constrain it.

M&A as core competency requires more than financial engineering. SS&C's integration playbook prioritizes retention over synergies, client service over cost cuts, and cultural fit over organizational charts. They keep acquired company names, maintain separate offices, and promote acquired executives. The counterintuitive insight: successful serial acquirers minimize integration, not maximize it.

The power of boring, mission-critical software cannot be overstated. SS&C's products don't win design awards or inspire TED talks. They process trades, calculate NAVs, and generate regulatory reports. But this mundane functionality becomes indispensable infrastructure. Investors seeking the next unicorn overlook these workhorses that generate decades of cash flow.

Vertical integration in financial services follows different rules than manufacturing. It's not about controlling supply chains but about owning client workflows. Each additional touchpoint—from trade execution to investor reporting—increases switching costs and cross-sell opportunities. The lesson: depth beats breadth in enterprise software.

When to sell, when to buy, when to go public requires situational awareness, not rigid rules. Stone sold to Carlyle when public markets undervalued SS&C but private markets had capital. He returned public when acquisition targets proliferated but required stock currency. He bought aggressively during crises when others retreated. The pattern: contrarian timing based on strategic logic, not market sentiment.

Building switching costs requires systematic effort, not lucky accidents. Every product decision at SS&C increases client dependency: proprietary data formats, custom integrations, specialized workflows. These "lock-in" features would be anti-patterns in consumer software but become competitive advantages in enterprise systems.

The recurring revenue transformation happened gradually, then suddenly. Early SS&C sold perpetual licenses with maintenance contracts. The shift to subscriptions took a decade, requiring investor education, sales force retraining, and temporary revenue impacts. But once complete, it transformed SS&C from a software company to a financial services utility.

For operators, the SS&C playbook offers clear lessons: Focus on unglamorous problems with expensive consequences. Build switching costs systematically. Acquire for capabilities, not just revenue. Maintain founder mentality regardless of size. Prioritize cash flow over growth metrics.

For investors, SS&C demonstrates the power of compounding in enterprise software. High retention rates, predictable price increases, and operational leverage create geometric returns over time. The companies that look expensive on P/E ratios might be cheap on customer lifetime value. The boring businesses that process mundane transactions might generate the most exciting returns.

XII. Bear & Bull Case Analysis

Bear Case:

The massive debt load from serial acquisitions creates vulnerability. With over $7 billion in gross debt, rising interest rates directly impact profitability. Each 100 basis point increase costs roughly $70 million annually—material for a company generating $1.3-1.5 billion in EBITDA. While cash flow covers interest payments comfortably today, a severe recession that reduces AUM and transaction volumes could stress coverage ratios.

Integration risks compound with each acquisition. SS&C has absorbed over 50 companies, each with different systems, cultures, and client expectations. While the track record is impressive, the law of large numbers suggests eventual integration failures. A botched integration that loses major clients could cascade through reference-ability and reputation.

Disruption from cloud-native competitors represents an existential threat. Companies like Carta, Addepar, and others build from scratch without legacy infrastructure. They offer modern interfaces, API-first architecture, and agile development that SS&C's monolithic systems can't match. Young firms starting today might choose these alternatives, slowly eroding SS&C's growth.

Regulatory changes could fundamentally alter the industry. Proposals for transaction taxes, carried interest changes, or hedge fund restrictions would reduce industry AUM and activity. Cryptocurrency and DeFi could bypass traditional fund structures entirely. SS&C prospers when traditional finance prospers—a symbiotic relationship that becomes parasitic if the host weakens.

Key person risk with Bill Stone is substantial and growing. At 69, Stone's continued involvement is uncertain. No clear successor exists with his combination of skills. The company's culture, acquisition strategy, and client relationships all center on Stone. His departure could trigger talent exodus, acquisition mistakes, and client defections.

Bull Case:

Dominant market position with high switching costs creates an almost unassailable moat. SS&C Technologies Holdings (NASDAQ: SSNC) is the world's largest hedge fund and private equity administrator, as well as the largest mutual fund transfer agency. This isn't just market share—it's market control. Competitors can't match the scale, expertise, or infrastructure. Clients can't leave without massive operational risk.

The proven M&A track record over decades demonstrates repeatable value creation. Fifty successful acquisitions isn't luck—it's systematic excellence. Each deal strengthens the platform, expands capabilities, and increases competitive advantages. The pipeline of potential targets remains robust as financial technology continues fragmenting.

Secular tailwind of financial services outsourcing accelerates post-COVID. Remote work proved operations can happen anywhere. Cost pressure forces efficiency. Regulatory complexity demands specialization. SS&C benefits from all these trends. The addressable market expands as firms outsource functions they previously handled internally.

Operating leverage at scale creates expanding margins. SS&C generated net cash from operating activities of $1,388.6 million for the twelve months ended December 31, 2024, up 14.3 percent compared to the same period in 2023. Incremental revenue drops directly to cash flow. The infrastructure investments are complete. Growth requires minimal capital.

Strong cash flow generation enables multiple paths to value creation. Debt paydown improves multiples. Share buybacks reduce count. Acquisitions add capabilities. Dividends reward patience. Management can optimize capital allocation based on market conditions, not financial constraints.

The balance of evidence tilts bullish but requires nuance. SS&C isn't a growth story that will double revenue annually. It's a compounding story where predictable growth, expanding margins, and intelligent capital allocation create steady wealth accumulation. The bears focus on dramatic risks that rarely materialize. The bulls recognize boring excellence that consistently delivers.

XIII. The Verdict & Future Outlook

SS&C got right what others missed: financial services firms want solutions, not software. They want outcomes, not tools. They want to focus on investing, not infrastructure. By providing complete solutions—software plus services plus expertise—SS&C became indispensable rather than merely useful.

The next frontiers—AI, blockchain, embedded finance—play to SS&C's strengths. AI requires massive data sets, which SS&C possesses. Blockchain needs integration with traditional systems, which SS&C controls. Embedded finance demands regulatory expertise, which SS&C has developed over decades. The company is positioned to absorb innovation rather than be disrupted by it.

Can the M&A machine continue? The arithmetic says yes. Thousands of financial technology companies exist globally. Private equity portfolios need exits. Founders want liquidity. SS&C has the currency (stock), capability (integration), and credibility (track record) to remain the natural buyer. The limitation isn't targets but digestive capacity.

Succession planning considerations will define the next chapter. Stone won't run SS&C forever, but his influence will persist through culture, strategy, and ownership structure. The most likely scenario: operational transition to professional management while Stone remains strategically involved. Think Berkshire Hathaway, not Apple—continuation of philosophy rather than radical transformation.

Building a fintech empire from scratch required four decades of disciplined execution. Stone didn't chase trends, pivot strategies, or optimize for exits. He identified a fundamental problem—financial services operational complexity—and solved it comprehensively. The empire emerged not from grand vision but from compound improvements.

The SS&C story ultimately demonstrates that in enterprise software, boring beats brilliant. Solving mundane problems for demanding customers creates more value than disrupting industries that don't want disruption. The next SS&C won't look like SS&C—it will solve different problems for different customers. But it will share the same characteristics: founder leadership, customer obsession, operational excellence, and patient capital.

For investors evaluating SS&C today, the question isn't whether the company will grow—it will. The question is whether the market will recognize the value of predictable compounding in an age obsessed with explosive growth. History suggests patient investors who understand the model will be rewarded. The impatient will sell to them.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube