Medpace Holdings: The Quiet Compounder of Clinical Trials

I. Introduction & Episode Roadmap

The Cincinnati skyline doesn't typically conjure images of biotech innovation. This is a city known for Procter & Gamble, Kroger, and the perpetually hopeful Cincinnati Reds—not exactly Silicon Valley or the Boston biotech corridor. Yet here, in the Madisonville neighborhood on the city's eastern flank, sits a gleaming campus that has quietly become one of the most important addresses in global drug development.

Medpace Holdings, Inc. is a global clinical research organization (CRO) based in Cincinnati, Ohio, employing approximately 6,000 people. Operating under a full-service model, the company also offers global central laboratory, imaging core laboratory, and bioanalytical laboratory services, as well as a Phase I unit located on its headquarters and clinical research campus in Cincinnati, Ohio.

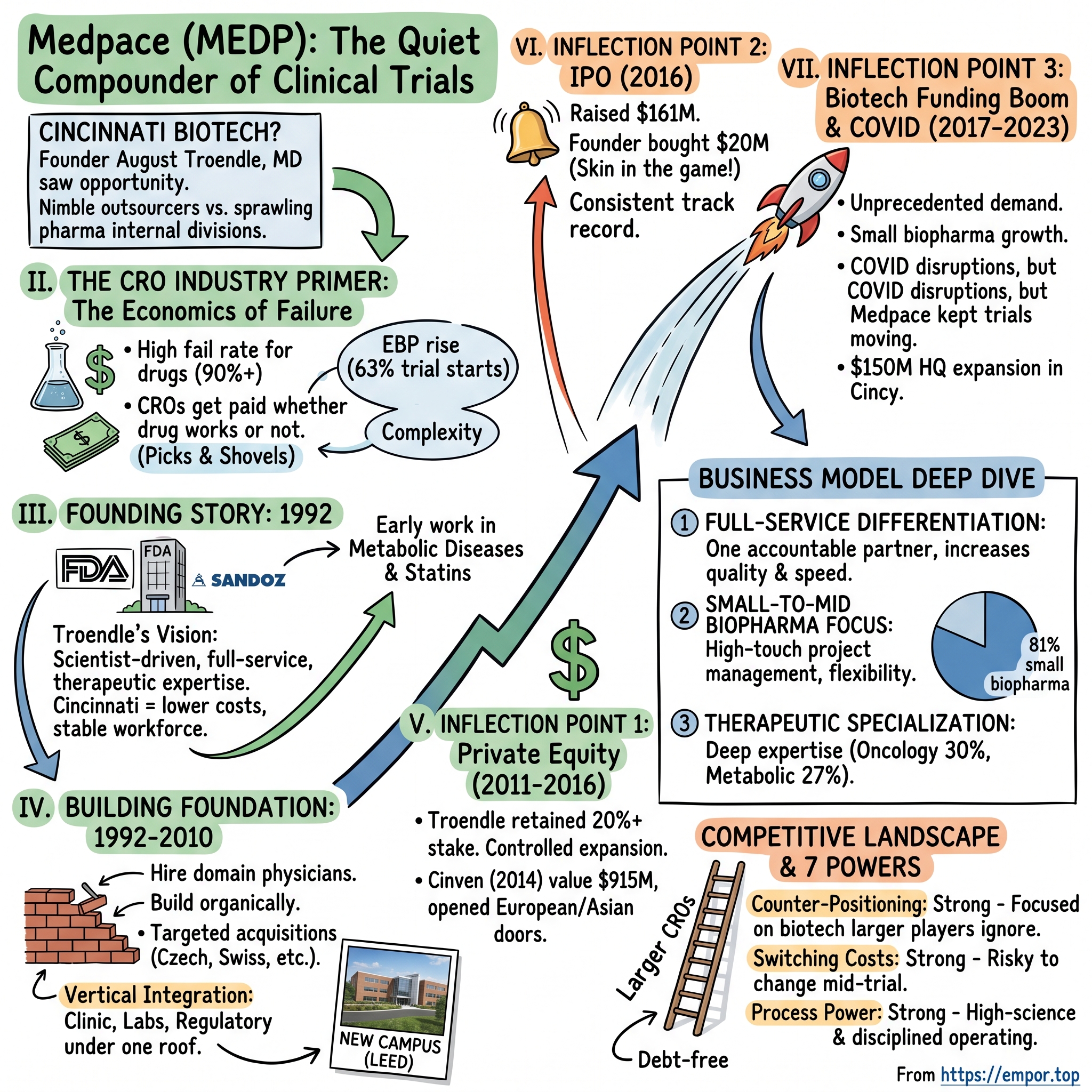

This isn't a story about a flashy unicorn or a founder with a TED Talk. It's the story of a physician-entrepreneur who saw something that others missed: that the future of drug development would belong not to the pharmaceutical giants with sprawling internal research divisions, but to nimble outsourcers who could execute faster, cheaper, and with sharper scientific expertise.

The "picks and shovels" thesis is well-worn in investing circles, but Medpace represents perhaps its purest expression in healthcare. Rather than attempting to pick individual winners among the myriad of pharma and biotech companies developing new drugs, investors can gain exposure to the overall growth of the industry by investing in companies that provide essential services to all participants. Medpace is a scientifically-driven, global, full-service clinical contract research organization (CRO) providing Phase I-IV clinical development services to the biotechnology, pharmaceutical and medical device industries. Medpace's mission is to accelerate the global development of safe and effective medical therapeutics through its high-science and disciplined operating approach that leverages regulatory and therapeutic expertise across all major areas including oncology, cardiology, metabolic disease, endocrinology, central nervous system and anti-viral and anti-infective.

The central question this analysis addresses is deceptively simple: How did a Cincinnati-based company founded by an FDA physician become a $16+ billion market cap powerhouse while larger CROs merged and consolidated? The answer lies in founder August Troendle's counter-intuitive strategy, his obsessive focus on operational excellence, and his willingness to stay disciplined while others chased scale at any cost.

Revenue of $659.9 million in the third quarter of 2025 increased 23.7% from revenue of $533.3 million for the comparable prior-year period, representing a backlog conversion rate of 23.0%. Net new business awards were $789.6 million in the third quarter of 2025, representing an increase of 47.9%—numbers that would make any growth investor's heart race.

What follows is the complete story of how Medpace went from a one-man operation in 1992 to a company that processes billions in clinical trial work annually, all while remaining headquartered in the same Midwest city where it started.

II. The CRO Industry Primer: Why This Business Exists

To understand Medpace's brilliance, you first need to understand the economics of failure—specifically, the economics of drug development failure.

Picture a pharmaceutical company in 1980. It employs thousands of researchers, maintains its own clinical trial operations, navigates regulatory submissions internally, and does everything from molecule discovery to FDA approval under one roof. This vertically integrated model made sense when drug pipelines were simpler and regulatory requirements less onerous. But by the 1990s, cracks were showing.

The math became punishing. Out of every 100 drugs that enter clinical trials, approximately 9.7 will eventually receive regulatory approval. That's a 90%+ failure rate—and the capital-intensive endeavor falls entirely on the biotech and pharma companies funding these trials. However, CROs are not only capital-light enterprises, but they generate revenue on the full 100% of drugs entering clinical trials, regardless of which ones ultimately succeed.

This asymmetry is the entire foundation of the CRO business model. The CRO gets paid whether the drug works or not. They're selling picks and shovels during a gold rush where most prospectors go home empty-handed.

The global contract research organization (CRO) services market, valued at US$79.10 billion in 2024, stood at US$84.61 billion in 2025 and is projected to advance at a resilient CAGR of 8.3% from 2025 to 2030, culminating in a forecasted valuation of US$125.95 billion by the end of the period.

What drove this explosive growth? Several converging forces.

First, the outsourcing megatrend became a secular tailwind for the CRO industry. In the U.S. alone, the pharmaceutical R&D market was estimated at approximately $125 billion recently, with about $65 billion of that being outsourced. This percentage continues to climb as companies—both large and small—recognize that maintaining internal clinical trial infrastructure is neither efficient nor cost-effective.

Second, the rise of biotech changed the competitive equation entirely. Small pharma firms are outsourcing more as R&D costs rise. EBPs now account for 63% of trial starts, up from 56% in 2019. These emerging biopharma companies often have brilliant science but zero infrastructure. They can't afford to build out internal clinical operations for a single drug candidate—they need partners.

Third, trials themselves became more complex. Multi-national, multi-site trials with sophisticated endpoints require expertise that most companies simply cannot develop internally. Factors such as the increasing complexity & the growing volume of trials; the rising focus on patient-centric clinical trials such as Decentralized Clinical trials (DCTs); and the flexibility of services offered by CROs are supporting the growth of this market. Moreover, the upcoming therapeutic drugs patent cliff is fueling pharmaceutical companies to invest heavily in R&D activities and outsource their clinical trials to CROs.

CROs like Medpace can speed up trial timelines by up to 30% compared to in-house trials, reducing drug development costs that often exceed $1 billion. When you're racing against patent clocks and burning through venture capital, speed isn't just convenient—it's existential.

For long-term investors, the CRO industry represents a fascinating combination of defensive characteristics and growth potential. Clinical trials run for years, sometimes decades, and CROs enjoy years of uninterrupted recurring revenue. There are four phases of clinical trials before a drug is approved, and while each is put out to tender, the incumbent from the prior phase has a clear advantage. This creates a sticky revenue base that compounds over time.

III. Founding Story: The FDA Physician's Vision (1992)

Before there was Medpace, there was a young physician named August Troendle sitting in a cramped government office at the FDA, reviewing applications for lipid-lowering therapies. It was 1986, and the statin revolution was just beginning. Troendle wasn't just processing paperwork—he was watching the future of cardiovascular medicine unfold from the inside.

From 1986 to 1987, Mr. Troendle worked as a Medical Review Officer in the Division of Metabolic and Endocrine Drug Products at the FDA. Before founding Medpace, Mr. Troendle served as Assistant Director, Associate Director and Senior Associate Director from 1987 to 1992 at Sandoz (Novartis), where he was responsible for the clinical development of lipid altering agents.

This career trajectory—FDA regulator to pharmaceutical executive—gave Troendle a dual perspective that would prove invaluable. He understood how regulators thought, what they looked for, where submissions failed. He also understood the pharmaceutical company side: the pressures, the inefficiencies, the frustrations of clinical development.

Mr. Troendle received his Medical Degree from the University of Maryland, School of Medicine and his Master of Business Administration from Boston University. We believe Mr. Troendle brings to our Board valuable perspective and experience as our Chief Executive Officer, and as a former member of a large pharmaceutical company and the FDA, as well as extensive knowledge of the CRO and biopharmaceutical industries.

By 1992, Troendle saw something others didn't. At Sandoz, he had witnessed firsthand how pharmaceutical companies struggled with clinical trial execution. The internal bureaucracies were enormous. Decision-making was slow. Scientific expertise was diluted across too many therapeutic areas. And crucially, smaller biotech companies—the ones developing some of the most innovative therapies—had no internal capabilities whatsoever.

August Troendle founded Medpace in Cincinnati, Ohio, in 1992 as Medical Research Services. Troendle first became interested in the CRO sector after working in both the regulatory and pharmaceutical area. He began his career as a reviewer with the FDA, specializing in the development of lipid lowering therapies to treat high cholesterol.

Why Cincinnati? This question has puzzled many over the years. The biotech industry's gravitational centers have always been Boston, San Francisco, and San Diego. Cincinnati wasn't even in the conversation. But Troendle wasn't trying to be convenient for venture capitalists or close to academic research centers. He was building an operations company, and Cincinnati offered something the coastal hubs couldn't: reasonable costs, a stable workforce, and—crucially—lower turnover.

Dr. Troendle's leadership was driven by a core belief – that a streamlined, efficient clinical trial process could significantly expedite the development of life-saving therapies. He envisioned Medpace as a partner, not just a service provider, for companies striving to bring innovative treatments to patients in need.

With a team of industry physicians, Jonathan Issacsohn and Evan Stein completed many early studies while at Medpace and Medpace Reference Laboratories on the use of statin therapies for the treatment of hypercholesterolemia. Another Medpace physician, David Orloff was regarded as an industry opinion leader in the study of metabolic diseases – most specifically diabetes and obesity.

These early hires established what would become Medpace's defining characteristic: deep therapeutic expertise. While other CROs were generalists, Medpace doubled down on metabolic diseases—statins, diabetes, obesity. The company knew this space better than anyone, and that knowledge became a competitive moat.

Dr. August Troendle, a noted medical doctor and scientist in the study of lipid altering agents, saw an opportunity in 1992 to offer a more innovative way to conduct clinical trials on behalf of biopharmaceutical customers (sponsors). As a former Medical Review Officer with the FDA – Dr. Troendle's personal achievements span both the scientific, regulatory, and the business arena. His vision for a physician-driven, full-service CRO with expertise in specific therapeutic areas spurred him on to found Medpace – capitalizing on an unmet need in the life science sector with a better way to design and deliver innovative process in clinical studies.

The Cincinnati decision would pay dividends for decades. While coastal CROs battled for talent in overheated labor markets, Medpace built a loyal workforce in a city where a job at a world-class healthcare company meant something. This wasn't just good fortune—it was strategic foresight from a founder who understood that operational excellence requires workforce stability.

IV. The Early Years: Building the Foundation (1992-2010)

The first decade of Medpace's existence was unremarkable by venture capital standards. There were no splashy fundraising rounds, no IPO attempts, no breathless press releases. August Troendle was doing something deeply unfashionable: building a real business, slowly and methodically.

The early focus on metabolic diseases and statin therapies wasn't accidental. Troendle understood his competitive advantage—his FDA experience in lipid-lowering drugs—and he exploited it relentlessly. He previously worked for Sandoz (Novartis) where he was responsible for the clinical development of lipid altering agents. His past experience as a Medical Review Officer in the Division of Metabolic and Endocrine Drug Products at the FDA gives him insight into the regulatory environment for development of drugs in the metabolic and cardiovascular fields.

As the company grew, it expanded into adjacent therapeutic areas—always with the same approach. Hire physicians with deep domain expertise. Build capabilities organically. Never sacrifice scientific depth for scale. This philosophy stands in stark contrast to how most CROs grew during this period, through aggressive acquisitions that often diluted expertise.

The strategic acquisitions Medpace did make were surgical—designed to build geographic reach and specific capabilities, not just top-line growth:

2007 – Medpace acquires Monax in the Czech Republic · 2009 – Medpace acquires PharmaBrains AG in Switzerland · 2010 – Medpace acquires Symbios, a medical device consultancy in Minneapolis, Minnesota · 2010 – Medpace acquires Medical Consulting Dr. Schlichtiger, GmbH, in Germany · 2012 – Medpace acquires MediTech BV, a medical device consultancy in the Netherlands.

Notice the pattern: small, targeted acquisitions in specific geographies or capabilities. The Czech Republic deal gave Medpace a foothold in Eastern European clinical trial sites. The Swiss acquisition added regulatory expertise in the European market. The medical device consultancies expanded the company's addressable market beyond pharmaceuticals.

Medpace Holdings, Inc. is a global clinical research organization (CRO) based in Cincinnati, Ohio, employing approximately 6,000 people. Operating under a full-service model, the company also offers global central laboratory, imaging core laboratory, and bioanalytical laboratory services, as well as a Phase I unit located on its headquarters and clinical research campus in Cincinnati, Ohio.

By the end of the 2000s, Medpace had built something unusual in the CRO industry: a vertically integrated platform where clinical operations, laboratories, and regulatory expertise all resided under one roof. This full-service model would become the company's primary differentiator as it scaled.

Medpace completed construction on a new campus in 2012 in Madisonville, a neighborhood on the eastern side of Cincinnati. The project encompassed revitalizing an urban brownfield site formerly occupied by NuTone, and creating a state of the art LEED (Leadership in Energy and Environmental Design) certified campus.

The new campus was a statement of intent. Troendle wasn't just running a services company—he was building an institution. The LEED certification, the brownfield redevelopment, the deliberate choice to plant deeper roots in Cincinnati rather than relocate to a biotech hub—all of this reflected a founder who thought in decades, not quarters.

V. Inflection Point #1: The Private Equity Era (2011-2016)

By 2011, August Troendle faced a decision that confronts every successful founder: how to fund growth while maintaining control. The CRO industry was consolidating rapidly. Competitors were raising massive war chests for acquisitions. To compete, Medpace needed capital—but Troendle wasn't willing to sacrifice his vision for a quick payday.

CCMP traded $485 million for its majority stake in Medpace in 2011, promptly embarking on an expansion binge that spread the CRO's reach around the globe and boosted its payroll by about 50%. The Cinven deal represents a huge return on investment for CCMP, reflecting both the high-growth nature of the CRO space and private equity's enthusiasm about buying into it.

The critical detail that most observers miss: Troendle retained a significant stake. In 2011, CCMP Capital acquired 80% of the firm for US$285 million. (Note: Different sources cite varying transaction values, reflecting the complexity of the deal structure.) This 20% ownership by management was not an accident—it ensured that the founder's interests remained aligned with the company's long-term success, not just short-term financial engineering.

Under CCMP's ownership, Medpace underwent controlled expansion. The payroll increase of 50% represented capability building, not empire construction. The company added geographic reach and therapeutic expertise without abandoning its core philosophy of scientific depth.

Three years later came the second private equity transition.

European private equity outfit Cinven has stepped up to buy the majority of long-rumored target Medpace, trading $915 million for an undisclosed controlling stake in the CRO.

CCMP Capital has sold its portfolio company Medpace, a contract research organization, for $915 million to European private equity firm Cinven. In 2013, Medpace generated an adjusted EBITDA of $94 million resulting in a valuation multiple of 9.7x. CCMP acquired Medpace in May 2011.

The Cinven deal valued Medpace at nearly double what CCMP had paid just three years earlier—a testament to the growth achieved under the first PE sponsor. But more importantly, the deal brought strategic value beyond capital.

Dr August Troendle noted: "Medpace has generated significant growth recently in Europe, so it made huge sense for us to partner with a private equity sponsor with a strong European presence and the ability to help us expand our operations in Asia."

Cinven's European network opened doors that would have taken years to access organically. Established in 1992, Medpace is headquartered in Cincinnati, Ohio and has global operations in over 45 countries. It has over 1,500 employees with approximately 40% of clinical operations employees in Europe. In 2013, Medpace generated an adjusted EBITDA of US$94m.

Supraj Rajagopalan, Partner at Cinven, explained: "Cinven's healthcare team identified the CRO industry as an attractive market in which to invest given its fundamental growth characteristics. The CRO industry consolidation has created a gap in the market serving the mid-cap pharma and smaller biotech players – where Medpace operates and where we intend to capitalize on organic growth opportunities."

Cinven understood something critical about Medpace's positioning: as larger CROs merged and focused on big pharma accounts, a gap was emerging. Small and mid-sized biotech companies—the fastest-growing segment of drug development—needed partners who understood their unique needs. Medpace was ideally positioned to fill that void.

Throughout both private equity transitions, Troendle maintained his operational control and significant ownership. This continuity proved invaluable—the company never lost its founder-led character, even as its financial sponsors changed.

VI. Inflection Point #2: The IPO and Going Public (2016)

The path to public markets in August 2016 represented more than just a liquidity event for Cinven. It was a validation of everything Medpace had built over 24 years.

Medpace Holdings, Inc. today announced the closing of its initial public offering of 8,050,000 shares of common stock at a public offering price of $23.00 per share. The number of shares issued at closing included the exercise in full of the underwriters' option to purchase 1,050,000 additional shares of common stock from Medpace.

The IPO raised $161 million at the top end of the projected range—remarkable given persistent headwinds for other sectors including biotech at the time. Medpace has raised $161 million in its initial public offering, the top end of the CRO's desired range, despite persistent headwinds for other sectors including biotech.

But the real story wasn't the capital raised. It was who bought shares—and how much skin the founder kept in the game.

We are led by a dedicated and experienced senior management team with significant industry experience and knowledge focused on clinical development. We were founded in 1992 by Dr. August J. Troendle, an industry pioneer, and we continue today as a founder-led enterprise with Dr. Troendle retaining a significant ownership stake in Medpace.

Troendle personally purchased $20 million in shares at the offering price—a dramatic signal of confidence that institutional investors noticed. When a founder-CEO puts eight figures of personal capital into his own IPO at the public price, he's telling the market: I believe in this company's future more than any slide deck could convey.

The timing proved prescient. Medpace's share price has performed well in the aftermarket, and Cinven has monetised its investment in Medpace through a series of sell downs, culminating in the final sell down on 22 August 2018 at a c.138% premium to the IPO price.

Cinven exits Medpace in full, making 3.5x its money, according to sources.

Cinven's 3.5x return over four years validated the investment thesis, but the real winner was Medpace itself. The company emerged from the private equity period stronger, more global, and ready for the next phase of growth.

Medpace Holdings, Inc. has demonstrated strong revenue and income growth since going public in 2016, maintaining a steady upward trajectory in operating and net income over the last several years.

Since its 2016 IPO, Medpace has delivered an impressive annual growth rate above 35%, underscoring its consistent track record in creating substantial shareholder value. The significance of Troendle's massive personal ownership cannot be overstated: as of mid-2025, CEO and founder August J. Troendle holds approximately 20.1% of outstanding shares, or about 5.66 million shares. This level of insider ownership creates powerful alignment between management and shareholders—a rarity in public company governance.

VII. Inflection Point #3: The Biotech Funding Boom & COVID Era (2017-2023)

The years following the IPO brought both extraordinary tailwinds and an unexpected crisis that would test everything Medpace had built.

The biotech funding environment from 2017 through 2021 was unprecedented. Venture capital poured into drug development at record rates. IPOs and SPAC mergers minted dozens of new public biotech companies every quarter. This created an explosion in demand for CRO services—but not just any CRO services. The new money flowed to small and mid-sized biotech companies, exactly the customer segment Medpace had spent decades cultivating.

Cinven's healthcare team had identified: "Increased R&D spend by the pharma and biotech industry, due to the growing number and complexity of clinical trials required to bring new products to market, is expected to fuel strong growth for the CRO industry, especially for those operators that focus on smaller pharma and biotech customers, where the outlook for R&D spend is most positive."

The investment thesis proved remarkably prescient. Revenue acceleration was dramatic:

In 2024, Medpace Holdings's revenue was $2.11 billion, an increase of 11.84% compared to the previous year's $1.89 billion. Earnings were $404.34 million, an increase of 43.07%.

From 2020 to the projected 2025 results, the company has achieved a compound annual growth rate (CAGR) of 21.8%-22.3% for revenue and 23.8%-24.2% for EBITDA, demonstrating the sustainability of its business model.

Then came COVID-19. For Medpace, the pandemic was both challenge and opportunity. Clinical trials faced massive disruptions—patient recruitment ground to halt, site visits became impossible, regulatory timelines stretched into uncertainty. But the world also learned, in the most visceral way possible, why clinical research matters. And when vaccine trials needed to run at unprecedented speed and scale, CROs proved indispensable.

Medpace emerged from the pandemic stronger than before. The company's operational discipline—the same discipline that had sometimes been criticized as overly conservative—proved invaluable during chaos. When competitors struggled with remote operations and site coordination, Medpace's integrated model and deep therapeutic expertise allowed it to keep trials moving.

In 2022, Medpace announced a $150 million capital investment to expand its headquarters in Cincinnati, Ohio, adding an estimated expansion of 1,500 new jobs.

Medpace Holdings Inc. plans to add 1,500 jobs over the next six years in Cincinnati and invest $150 million to expand its offices and business operations, CEO Dr. August Troendle announced Wednesday. Troendle said the expansion would be the biggest in the medical research company's history.

This wasn't just construction—it was a statement about the company's confidence in its own future. While other companies pulled back on capital expenditures, Medpace doubled down on capacity.

In 2024, Medpace broke ground on a $327 million project that will restructure the Cincinnati campus. The Madisonville headquarters will see a total of three new additions: a nine-story office building, a brand-new Clinical Pharmacology Unit (CPU), and a six-story parking garage. Regarded as one of the largest expansions in Cincinnati's history, this development also takes the title for the city's most significant job creation commitment. With a baseline dedication to adding 1,500 jobs, this record growth will carve the path for ongoing hiring initiatives.

VIII. The Medpace Business Model Deep Dive

Understanding Medpace's competitive position requires examining how the company actually makes money—and why its approach differs fundamentally from larger competitors.

The Full-Service Differentiation

Most CROs evolved through acquisition, bolting on capabilities over time. This creates what the industry calls "functional service provider" relationships, where clients assemble their trial team piecemeal from different vendors. The result: coordination costs, finger-pointing when things go wrong, and gaps where handoffs occur.

Medpace took the opposite approach. Driven by a full-service CRO model that coordinates and integrates all services for clients, Medpace provides an accountable, seamless, integrated, and efficient platform for executing clinical research—increasing quality and speed while significantly reducing the need for duplicate management oversight.

Operating under a full-service model, the company also offers global central laboratory, imaging core laboratory, and bioanalytical laboratory services, as well as a Phase I unit located on its headquarters and clinical research campus in Cincinnati, Ohio.

This vertical integration creates accountability. When a trial encounters problems, there's no finger-pointing between vendors—Medpace owns the entire relationship. For small biotech companies with limited bandwidth to manage multiple vendors, this single-point accountability is enormously valuable.

Focus on Small-to-Mid Biopharma

While larger CROs chase massive, multi-year contracts with big pharma, Medpace deliberately targets smaller biotechs. This isn't a defensive posture—it's a strategic choice with significant advantages.

The company maintains a strong focus on serving small biopharma companies, which represented 81% of revenue year-to-date, up from 79% in the prior year. This concentration aligns with Medpace's strategic positioning as a partner for emerging biotech companies.

Medpace's principal competitive advantage lies in its focused, full-service operating model tailored to small- and mid-sized biopharma clients. Unlike larger contract research organizations (CROs) such as IQVIA, ICON, and LabCorp, which often prioritize large pharmaceutical accounts, Medpace derives approximately 79% of revenue from small biopharma and 17% from mid-sized clients. This focus enables high-touch project management, faster decision cycles, and greater flexibility—attributes valued by emerging drug developers.

Small biopharma companies, which often lack the resources to manage complex trials in-house, need true partners—not transactional service providers. Medpace's ability to guide these clients through the regulatory maze creates deep relationships and repeat business.

On average, these contracts run 3-5 years, and around 70% of clients renew beyond the initial term. That points to a 92% retention rate, which is exceptional in the CRO world.

Therapeutic Specialization

Medpace doesn't try to be all things to all clients. Instead, it concentrates on therapeutic areas where it has built deep expertise over decades.

For the first nine months of 2025, oncology remained the largest therapeutic area at 30% of revenue, followed closely by metabolic studies at 27%, which increased from 21% in the same period of 2024.

This therapeutic depth creates several advantages. First, Medpace can design better trials—fewer protocol amendments, faster enrollment, higher data quality. Second, the company develops relationships with key opinion leaders and high-performing sites in each therapeutic area. Third, clients trust Medpace's scientific judgment because the company has done hundreds of similar trials.

The company's therapeutic expertise in complex areas—oncology (31% of 2024 revenue), metabolic disease (22%), and CNS (9%)—supports premium pricing and high client retention.

Customer Concentration and Revenue Quality

Notably, Medpace's customer concentration remains well-diversified, with no single customer representing more than 10% of revenue. The top five customers accounted for 23% of revenue year-to-date, while the next five largest customers contributed an additional 10%.

This diversification reduces risk while the long-duration contracts provide visibility. Clinical trials run for years, sometimes decades, and CROs enjoy years of uninterrupted recurring revenue.

IX. The Competitive Landscape

The CRO industry has consolidated dramatically over the past decade, creating a handful of giants and a long tail of specialists. Medpace occupies a unique position in this landscape—large enough to execute global trials, but differentiated by its focus and operating model.

The CRO services market is competitive. The top five players for each market hold >35%, and the top ten account for a share of ~45-50%. IQVIA maintains a strong position in the CRO services market through a comprehensive portfolio of services and enhancements using AI-based offerings.

The global CRO services market is competitive, with leading players contributing to a significant share, including IQVIA Inc. (US), ICON Plc. (Ireland), Thermo Fisher Scientific Inc. (US), Laboratory Corporation of America Holdings (LabCorp) (US), WuXi AppTec Co., Ltd. (China), Charles River Laboratories International, Inc. (US), Pharmaron Beijing Co., Ltd. (China), Medpace, Inc. (US), and Eurofins Scientific (Luxembourg), among others.

In 2016, Quintiles and IMS Health merged and rebranded as IQVIA, becoming the largest CRO in the world. As a leading global provider of advanced analytics, technology solutions and clinical research services to the life sciences industry, IQVIA has solidified its position at the forefront of the CRO world through a series of strategic acquisitions. In 2024, IQVIA generated revenues of US$15,405 million, reflecting a 2.8% growth compared to the previous year.

The industry consolidation wave transformed competitors:

- PPD was acquired by Thermo Fisher Scientific in 2021, becoming part of a massive life sciences conglomerate

- ICON acquired PRA Health Sciences in 2021, creating another mega-CRO

- Parexel was taken private by Goldman Sachs and EQT

The deal comes amid years of high-dollar consolidation in the CRO world, including KKR's recent three-company buying spree, Carlyle Group and Hellman & Friedman's $3.9 billion acquisition of PPD in 2011, and a $1.1 billion leveraged buyout that took inVentiv Health off the public markets the same year. All that dealmaking has made for a bevy of large CROs competing at the top of the market, Cinven Partner Supraj Rajagopalan said, thus creating a sizable opportunity for a player like Medpace.

The Counter-Positioning Advantage

Medpace chose NOT to pursue mega-mergers—a counter-cyclical strategy that looks increasingly wise. While competitors integrated acquired companies and dealt with cultural clashes, Medpace continued to grow organically and refine its operating model.

The CRO industry has seen consolidation in the last few years, with a number of midsize firms combining - PRA and RPS last year, for example - in order to offer a greater depth of services and a greater geographical presence, and such an environment has left an attractive space, according to Cinven. "Cinven is very sector-driven in its investment approach and our healthcare team identified the CRO sector as highly attractive in terms of growth prospects. Medpace is particularly attractive given its focus on the smaller to mid-market biotech, pharma and medical device companies, where consolidation at the larger end of the CRO market has created a gap."

This gap is Medpace's opportunity. When large CROs focus on multi-billion-dollar enterprise contracts with Pfizer or Merck, they have less bandwidth for the biotech company with one promising molecule and $50 million in Series B funding. Medpace is built specifically for that emerging biotech.

IQVIA is the largest CRO and holds about 15.6% share in the healthcare CROs market. Other leading global players include PPD (8.4%), PAREXEL (7.6%), Covance (6.5%), and ICON (6.1%).

X. Porter's Five Forces Analysis

Understanding Medpace's competitive position requires examining the structural forces that shape industry profitability.

1. Threat of New Entrants: LOW-MODERATE

High barriers to entry protect established players like Medpace:

- Regulatory expertise and relationships (FDA, EMA) take decades to build

- Global infrastructure across 45+ countries required for multinational trials

- Reputation and track record essential for client trust

- Medpace employs approximately 6,200 people across 44 countries as of September 2025.

Building this infrastructure from scratch would take years and hundreds of millions in investment. New entrants typically focus on niche capabilities rather than challenging full-service providers.

2. Bargaining Power of Suppliers: LOW

Medpace's primary "suppliers" are its employees—clinical staff, scientists, and regulatory specialists. The company's Cincinnati headquarters provides cost advantages versus Boston or San Francisco, where talent wars inflate compensation.

Medpace's global footprint (6,000 employees across 44 countries) allows access to diverse patient populations and regulatory know-how, matching larger peers in geographic reach.

The geographic distribution also provides flexibility in talent sourcing. When one market becomes overheated, Medpace can shift hiring to other regions.

3. Bargaining Power of Buyers: MODERATE

Deep expertise in managing complex, multinational trials and high customer switching costs create a substantial economic moat. Medpace's global regulatory knowledge and ability to shorten clinical trial times give it a significant advantage, supporting long-term client relationships.

However, large pharma clients have significant negotiating leverage. This is partly why Medpace focuses on small-to-mid biotech—these clients have fewer alternatives and value partnership over price-shopping.

Once a small or mid-sized biotech team experiences Medpace's integrated approach—where data, analytics, and regulatory guidance are all under one roof—they're reluctant to disrupt that setup by migrating to a new vendor.

4. Threat of Substitutes: LOW

Pharma companies could bring trials in-house, but the trend moves decisively in the opposite direction. The demand for outsourced research services is surging as pharmaceutical and biotechnology firms seek cost-effective solutions to accelerate drug development and meet stringent regulatory requirements. With a growing number of clinical trials worldwide, CROs are playing a crucial role in streamlining drug discovery, reducing operational costs, and enhancing research efficiency.

For smaller biotech companies, partnering with a CRO is not just an option but a necessity. These smaller entities lack the in-house expertise, resources, and infrastructure to navigate the rigorous and lengthy clinical trial process on their own.

5. Competitive Rivalry: HIGH

Intense competition from giants (IQVIA, ICON, PPD/Thermo Fisher) creates pricing pressure at the top of the market. However, Medpace's niche positioning reduces direct competition. "Medpace is particularly attractive given its focus on the smaller to mid-market biotech, pharma and medical device companies, where consolidation at the larger end of the CRO market has created a gap."

XI. Hamilton's 7 Powers Analysis

Hamilton Helmer's framework provides additional insight into Medpace's competitive position.

1. Scale Economies: MODERATE

Medpace isn't the largest player, but it has sufficient scale in its target market. The Cincinnati headquarters provides cost advantage, and integrated labs/facilities drive operational efficiency. However, scale economies are less pronounced in CRO services than in manufacturing businesses.

2. Network Effects: LIMITED

Site investigator relationships create some network effects. He recognized the importance of international reach for clinical trials and spearheaded Medpace's global expansion, establishing operations in over 45 countries.

Relationships with Key Opinion Leaders, Principal Investigators, and high-performing sites help accelerate clinical development. These relationships are difficult to replicate.

3. Counter-Positioning: STRONG ⭐

This is Medpace's primary power source. Large CROs focused on big pharma would cannibalize existing relationships to compete for small biotech business. Medpace built its entire organization around serving clients that larger competitors ignore or underserve.

All that dealmaking has made for a bevy of large CROs competing at the top of the market, thus creating a sizable opportunity for a player like Medpace.

4. Switching Costs: STRONG ⭐

Mid-trial CRO changes are extremely risky and costly. Once a trial begins, switching providers requires massive coordination, regulatory notification, and risk of data integrity issues. Around 70% of clients renew beyond the initial term. That points to a 92% retention rate, which is exceptional in the CRO world. Once a small or mid-sized biotech team experiences Medpace's integrated approach—where data, analytics, and regulatory guidance are all under one roof—they're reluctant to disrupt that setup.

5. Branding: MODERATE-STRONG

Medpace has built strong reputation in therapeutic specialties. The company has received multiple industry awards based on feedback from sites and sponsors. This reputation attracts new clients and justifies pricing.

6. Cornered Resource: MODERATE

The primary cornered resource is founder-CEO August Troendle himself. His unique combination of FDA, pharma, and CRO experience is irreplaceable. The therapeutic area expertise built over 30+ years represents institutional knowledge that can't be quickly replicated.

7. Process Power: STRONG ⭐

Medpace employs a high-science and disciplined operating approach built over decades. This process power shows up in metrics: lower protocol amendments, faster enrollment, higher client retention.

Medpace's record of lower protocol amendments (and therefore fewer costly trial adjustments) gives them a strong reputation among biotech companies racing to get therapies approved. From an investment lens, that means a virtuous cycle: specialized expertise leads to more successful trials, which leads to more demand from ambitious biopharma startups.

XII. Recent Performance and Financial Analysis

The most recent results demonstrate Medpace's execution capability:

Revenue of $659.9 million in the third quarter of 2025 increased 23.7% from revenue of $533.3 million for the comparable prior-year period, representing a backlog conversion rate of 23.0%. Net new business awards were $789.6 million in the third quarter of 2025, representing an increase of 47.9%.

Medpace Holdings Inc. (MEDP) reported its third-quarter 2025 earnings, surpassing market expectations with an EPS of $3.86 against a forecast of $3.53. Revenue reached $659.9 million, exceeding the anticipated $640.99 million.

Based on the strong performance in the first nine months of the year, Medpace raised its full-year 2025 guidance across all key metrics. The company now expects: Revenue between $2,480 million and $2,530 million, representing growth of 17.6% to 20.0%.

The book-to-bill ratio—a critical metric for understanding future revenue potential—rebounded strongly:

Medpace achieved record net new business awards of $789.6 million, a remarkable 47.9% increase from Q3 2024. This surge in new business contributed to a net book-to-bill ratio of 1.20, compared to 1.00 in the prior-year period, indicating strong future revenue potential.

Capital allocation reflects management's confidence:

During the third quarter, Medpace repurchased 14,649 shares for $4.5 million. For the first nine months of 2025, the company has repurchased nearly 3 million shares for a total of $912.9 million, with $821.7 million remaining under its authorized share repurchase program as of September 30.

Medpace remains debt-free, a striking contrast to competitors like IQVIA, which carries $12.5 billion in debt, or ICON with $4.7 billion.

This debt-free balance sheet provides strategic flexibility and reduces risk during industry downturns.

XIII. Bull Case and Bear Case

The Bull Case

Structural tailwinds continue: The CRO industry benefits from secular trends that show no signs of reversing. The contract research organization market is growing significantly owing to increased outsourcing of R&D. As biotech innovation accelerates and clinical trials grow more complex, demand for specialized CRO services will only increase.

Dominant position in fastest-growing segment: Small biopharma companies represent the majority of new drug development activity. Medpace's focus on small biopharma clients—81% of its revenue in 2025—positions it to capitalize on a sector increasingly reliant on outsourcing. Meanwhile, its backlog conversion rate of 21.2% (up from 19.2% in Q1) shows it's not just winning deals but executing them efficiently.

Founder-led with aligned incentives: Troendle's 20%+ ownership creates powerful alignment. Unlike companies run by hired-gun CEOs optimizing for short-term compensation, Medpace is run by someone whose personal wealth is tied to long-term value creation.

Counter-positioning moat: Large CROs cannot easily pivot to serve small biotech without cannibalizing their large pharma relationships. This structural protection gives Medpace a defensible niche.

Operating leverage as revenue scales: The fixed costs of Medpace's infrastructure (laboratories, clinical pharmacology unit, headquarters) can support significantly more revenue. As top-line grows, margins have room to expand.

The Bear Case

Client funding vulnerability: The leadership team noted that many cancellations and project delays were tied to funding issues among small biopharma clients, which represent approximately 80% of Medpace's revenue. When biotech funding dries up, as it did in 2022-2023, Medpace's clients cancel or delay trials.

Biotech market cyclicality: The extraordinary funding environment of 2020-2021 created artificially high demand. A prolonged biotech funding drought could pressure growth rates.

Key-person risk: While Troendle has built a strong organization, his eventual retirement creates succession uncertainty. The company's culture and strategic direction have been shaped by one person for over three decades.

Competitive pressure from larger CROs: If IQVIA, ICON, or others decide to compete more aggressively for small biotech business, Medpace could face pricing pressure and market share losses.

Valuation reflects success: Strong execution is already priced into the stock. Any stumble in growth rates could lead to multiple compression.

XIV. Key Performance Indicators to Track

For long-term investors following Medpace, three metrics matter most:

1. Net Book-to-Bill Ratio

This ratio measures new contract awards against revenue, indicating whether the backlog is growing or shrinking. A ratio above 1.0 indicates growing future revenue potential; below 1.0 suggests backlog is being depleted faster than it's being replenished.

The book-to-bill ratio is a metric used to measure the demand for Medpace's services, comparing it to its ability to deliver them. Anything above 1.00 means that Medpace is booking more orders than billing.

The Q3 2025 ratio of 1.20 represents a significant improvement from the 0.90-1.00 levels seen during the biotech funding drought.

2. Backlog Conversion Rate

This metric measures how efficiently Medpace converts its contracted backlog into recognized revenue. The company's backlog conversion rate improved substantially to 23.0% in Q3 2025 from 18.2% in Q3 2024, demonstrating enhanced operational efficiency in converting backlog into revenue.

Higher conversion rates indicate that trials are progressing smoothly with minimal delays or cancellations.

3. Small Biopharma Revenue Concentration

Tracking the percentage of revenue from small biopharma clients indicates whether Medpace is maintaining its strategic focus. The company maintains a strong focus on serving small biopharma companies, which represented 81% of revenue year-to-date, up from 79% in the prior year.

A significant shift toward large pharma clients would signal a change in strategy that might dilute Medpace's competitive advantages.

XV. Conclusion: The Cincinnati Compounder

The Medpace story defies conventional wisdom in nearly every dimension. A physician-scientist founded a company in Cincinnati—not Boston, not San Francisco, not San Diego—and built it into a global powerhouse. He partnered with private equity twice while maintaining control and alignment. He took the company public without losing its founder-led character. And throughout three decades of industry consolidation, he resisted the temptation to pursue scale for scale's sake.

We were founded in 1992 by Dr. August J. Troendle, an industry pioneer, as a Phase II-IV-focused CRO with a strong, scientifically-driven and disciplined operating model, and we continue today as a founder-led enterprise with Dr. Troendle retaining a significant ownership stake in Medpace. Throughout our 24-year history, we have grown almost exclusively organically, with our core founding members having been integrally involved in developing and instilling our differentiated culture and operating philosophy across our company.

The result is a company that combines rare attributes: consistent growth, high margins, minimal debt, aligned management, and a defensible competitive position.

For the industry, Medpace represents an alternative path. While mega-CROs pursued scale through acquisition, Medpace proved that operational excellence and strategic focus could create equivalent value. The company's success validates a founder-led, disciplined approach that prioritizes long-term value creation over short-term growth at any cost.

For investors, Medpace offers exposure to the long-term growth of drug development without the binary risks of individual pharmaceutical bets. Whether any particular drug succeeds or fails, clinical trials continue. And as long as biotech companies need partners to navigate the complex journey from molecule to market, Medpace will be there—probably still in Cincinnati, probably still led by the same disciplined philosophy that August Troendle instilled three decades ago.

The quiet compounder continues to compound.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube