Zscaler: The Zero Trust Revolution

I. Introduction & Episode Roadmap

Picture this: every second, half a trillion pieces of data flow through invisible checkpoints in the cloud—emails, files, login attempts, API calls—all scrutinized by algorithms that trust nothing and verify everything. This is the world Zscaler built, processing 500 billion transactions daily through what they call the Zero Trust Exchange. From a standing start in 2007, this San Jose-based company has fundamentally rewired how enterprises think about security, reaching $2.2 billion in annual revenue and serving over 40% of the Fortune 500.

The story of Zscaler (NASDAQ: ZS) isn't just about cloud security or sophisticated proxy architectures. It's about a serial entrepreneur from a village without electricity who saw the internet becoming the corporate network a full decade before COVID made it obvious. It's about betting $50 million of personal wealth when venture capitalists thought the idea was premature. And it's about building a company that makes money by assuming everyone—including your own employees—could be a threat.

Today we're diving deep into how Jay Chaudhry built his fifth successful company, why Zscaler's timing was both too early and exactly right, and whether this $30 billion market cap company can maintain its lead as Microsoft, Google, and Palo Alto Networks circle like sharks. We'll explore the technical moat that makes Zscaler's architecture nearly impossible to replicate, the M&A strategy that's assembled a comprehensive platform piece by piece, and the financial engine that's generating nearly $600 million in free cash flow.

The fundamental question we're wrestling with: Has Zscaler permanently disrupted the $50 billion security market, or are we witnessing the peak of a first-mover advantage that's about to erode? The answer lies in understanding not just what Zscaler built, but why they built it the way they did—starting in a village called Panoh.

II. Jay Chaudhry: The Serial Entrepreneur's Origin Story

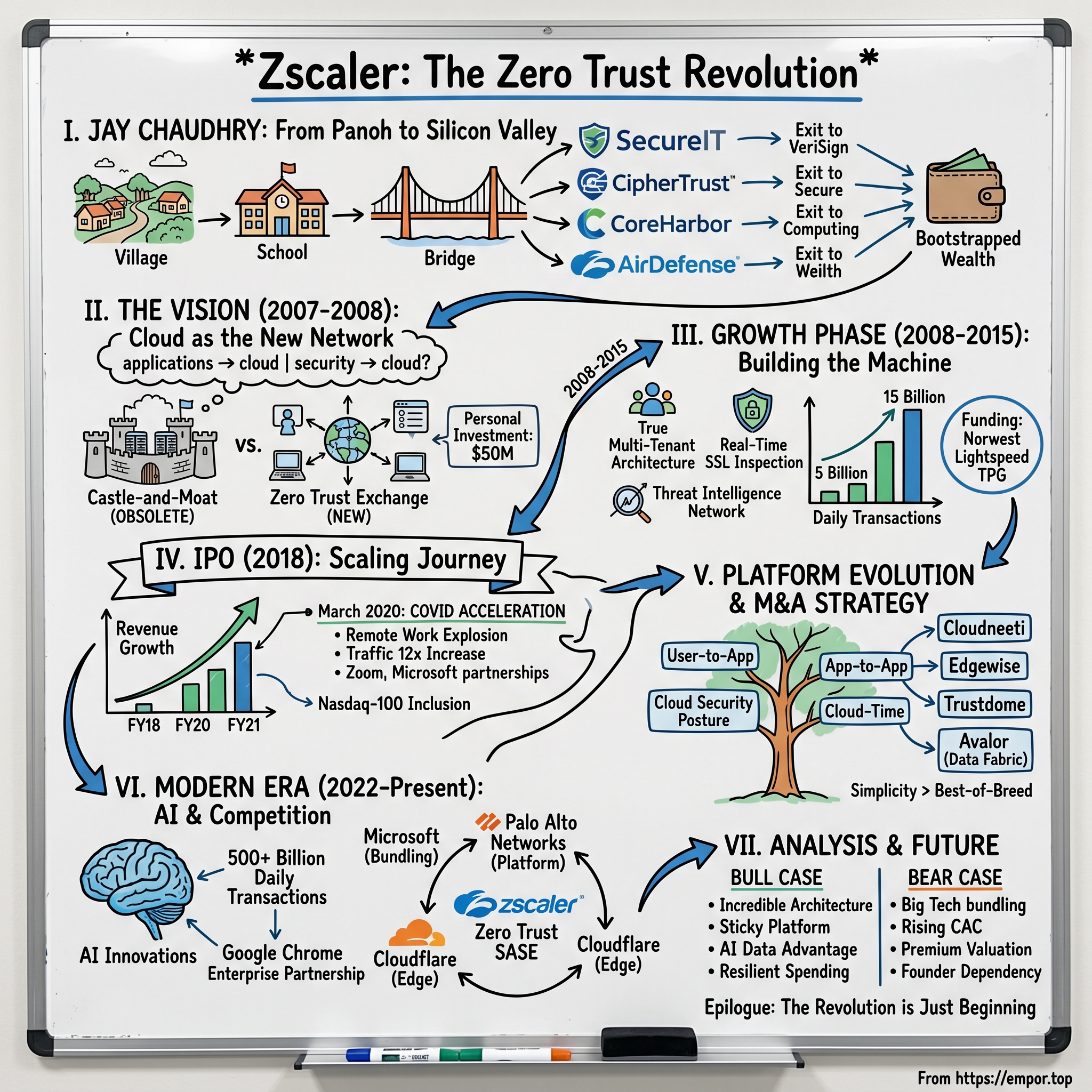

The village of Panoh sits in the foothills of the Himalayas, population 800, where young Jagtar Singh Chaudhry—later Jay—grew up without electricity or running water. His parents were small-scale farmers who couldn't read or write. The nearest high school was a four-mile walk each way. This isn't the typical Silicon Valley founder mythology of garage startups and Stanford dorms—this is about as far from Palo Alto as you can get, both geographically and economically.

Jay's break came through India's famously meritocratic engineering entrance exams. He earned admission to IIT BHU (Banaras Hindu University), one of India's most prestigious technical institutes. But even at IIT, the idea of entrepreneurship was foreign. "In India at that time, you either became an engineer or a doctor" Jay would later recall. "Starting a company wasn't even in the vocabulary."

After graduating in 1980, Jay did what ambitious Indian engineers did: he came to America for graduate school. The University of Cincinnati wasn't MIT, but for someone from Panoh, it was a gateway to possibilities unimaginable back home. He earned master's degrees in industrial engineering and computer engineering, then began a 25-year apprenticeship in corporate America—IBM, NCR, Unisys—learning the enterprise technology playbook from the inside. The entrepreneurial switch flipped in 1996. Jay and Jyoti had been watching the internet explosion—Netscape's IPO, the browser wars, the promise of universal connectivity. Netscape had just launched and gone public, and Jay was fascinated by it. He said, "If Marc Andreessen could start a company—he was a young guy right out of college—why shouldn't I start a company?" The couple saw a simple truth: if every business connected to the internet, they'd need security. No Gartner reports, no market studies—just gut instinct that this was the moment.

They emptied their life savings—roughly $500,000—to launch SecureIT, the first pure-play internet security service. This wasn't venture-backed Silicon Valley glamour; this was betting everything on an idea. In 1998, Jay was a first-time entrepreneur selling the startup he launched with his wife Jyoti, SecureIT, to VeriSign in an all-stock deal worth $70 million.

But here's where Jay's story diverges from typical founder narratives. More than 70 of SecureIT's 80 employees "on paper, were millionaires" with stock options after VeriSign's stock soared post-acquisition. "People were going crazy in the company, because they had never thought of so much money. A lot of them were buying new houses. They were buying new cars. I know one guy, he took six months off, rented a mobile home and went around the country."

This wasn't luck—it was architecture. Because Jay and Jyoti had bootstrapped SecureIT without venture capital, they could afford to be generous with equity. The night of his farewell party at VeriSign, Jay went home and did the math: "I looked at the spreadsheet of all the stock options they had, and I multiplied by the stock price of VeriSign. That's when I realized that the math was about 70 or 80 millionaires." But Jay wasn't done building. Between 2000 and 2006, he founded and led CipherTrust, the industry's first email security gateway, before its merger with Secure Computing. The idea came directly from his SecureIT experience, where he'd become familiar with emerging attack vectors. The technology was built from scratch and was later acquired by Secure Computing Corporation in 2006 for $274 million.

In parallel, Jay was building a portfolio of security companies like a venture capitalist investing in himself. CoreHarbor, a managed e-commerce platform, sold to USi/AT&T. AirDefense, a wireless security pioneer he founded in 2002, went to Motorola. Each exit added to his war chest and his understanding of enterprise security gaps. By 2007, he'd built and sold four companies, never taking venture capital after SecureIT, funding everything from his own proceeds.

The pattern was clear: Jay wasn't just a serial entrepreneur; he was systematically mapping the security landscape, identifying gaps, building solutions, and moving to the next frontier. Each company taught him something critical—SecureIT showed him the power of being first, CipherTrust proved the value of platform thinking, AirDefense demonstrated the importance of emerging threat vectors. These weren't random bets; they were reconnaissance missions for what would become his magnum opus.

III. The Founding Vision: Cloud as the New Network (2007-2008)

In 2007, while the world was debating whether businesses would ever trust the cloud with critical data, Jay Chaudhry saw something different. He'd been watching Marc Benioff build Salesforce into a multibillion-dollar company by moving CRM to the cloud. But if applications were moving to the cloud, Jay reasoned, why were companies still backhauling internet traffic through corporate data centers just to inspect it? The entire castle-and-moat security architecture was about to become obsolete.

"I wanted to build the Salesforce of security," Jay would later say. The idea was audacious: create a global cloud platform that would sit between users and the internet, inspecting every packet, blocking threats, and enforcing policies without any hardware, without any backhauling, without the latency and complexity of traditional approaches. Users could be anywhere, applications could be anywhere, and Zscaler would be the secure gateway between them.

Jay and his co-founder K. Kailash began building in stealth mode. This wasn't a pivot from on-premise to cloud; this was architecting for a world that didn't exist yet—where the corporate network would effectively disappear, where employees would work from coffee shops and airports as easily as from offices, where applications would live in multiple public clouds rather than corporate data centers. The technical challenges were immense. Building a globally distributed proxy architecture that could inspect SSL traffic at scale, maintain state across multiple data centers, and deliver sub-second latency—all while competing against established vendors with billions in revenue—seemed impossible. But Jay had a secret weapon: he was betting the company with his own money. The company launched its cybersecurity platform in 2008.

The first funding came not from Sand Hill Road but from Jay and Jyoti's bank account—$50 million of their personal wealth went into building Zscaler. This wasn't hubris; it was conviction. As Jay would later explain, "The financial risk of SecureIT was, like, 1,000 times more than the risk of Zscaler. The amount I invested in Zscaler was a small fraction of my net worth. But Zscaler was much harder."

In 2008, Norwest Venture Partners finally saw what Jay saw, leading a $12 million Series A round. But venture capital was secondary to finding the right early customer—someone willing to bet their organization's security on an unproven cloud platform from a company with no revenue, no reference customers, and a vision that most CISOs thought was insane.

That customer turned out to be Arc Mid-Hudson, a not-for-profit in New York State supporting individuals with intellectual and developmental disabilities. A Zscaler customer since 2007, The Arc Mid-Hudson is a not-for-profit human services organization in New York State dedicated to supporting more than 1,300 individuals with intellectual and developmental disabilities. They didn't choose Zscaler because it was safe—they chose it because their distributed workforce across 50 sites needed something traditional security couldn't provide.

Kenneth Dales, CIO at The Arc Mid-Hudson, would later reflect: "The Zscaler Zero Trust platform helps ensure that the systems used by our employees work as smoothly, efficiently, and securely as possible without getting in the way of providing the highest level of care for our clientele." Fifteen years later, Arc Mid-Hudson is still a Zscaler customer—a testament to getting the technology right from day one.

The platform launch in 2008 marked a philosophical break from decades of security thinking. Instead of trusting the internal network and distrusting the internet, Zscaler trusted nothing. Every user, every device, every application had to prove its identity and authorization for every transaction. This wasn't just moving security to the cloud; it was inverting the entire trust model of enterprise IT.

IV. Building the Machine: Growth Phase (2008-2015)

The years between 2008 and 2012 were Zscaler's wilderness period. While Salesforce was proving the cloud model for applications and AWS was winning infrastructure, security remained stubbornly on-premise. CISOs would listen to Jay's pitch, nod politely, then ask about the appliance version. There wasn't one. There would never be one. This was cloud-native or nothing. The validation came in August 2012 when Zscaler secured $38 million in funding from strategic investors, including Lightspeed Ventures. This wasn't desperation capital—the company was already cash-flow positive. The company's singular focus on securely enabling businesses for the accelerating challenges of mobility, cloud applications and social media had yielded solid gross margins and high sales growth, turning the company cash flow positive. As Jay explained: To date, we have resisted outside investment despite numerous inquiries from top-tier investors

The timing of this round was crucial. By 2012, Zscaler was processing over 5 billion transactions daily for 8 million users across 160 countries. The platform wasn't theoretical anymore—companies like La-Z-Boy and Telefónica were running production traffic through it. Ravi Mhatre from Lightspeed saw what others missed: "Many web security vendors are putting appliances in the cloud and calling it cloud security. Zscaler is the only company that has the right architecture to securely enable the mobile, cloud and social media applications that often bypass traditional security altogether."

The technical moat was deepening. While competitors were virtualizing appliances and calling it cloud, Zscaler had built a true multi-tenant architecture from scratch. Every packet flowing through the system made the threat detection smarter. Every new customer added to the network effect. This wasn't just software; it was a living, learning organism that got better with scale. By 2015, the cloud security market was reaching an inflection point. Microsoft's Office 365 was gaining traction, AWS was becoming mission-critical infrastructure, and CISOs were finally accepting that the perimeter was dissolving. TPG Capital saw the moment and led a $100 million round in August 2015, valuing Zscaler at over $1 billion—officially minting it as a unicorn. TPG invested in Zscaler, alongside existing investors EMC and Lightspeed Ventures, who also contributed to the round.

The numbers told the story: thousands of enterprises and government organizations, including United Airlines, Humana, NBC and National Health Services of the UK, were protecting more than 13 million employees with Zscaler, securing more than 15 billion Internet requests and stopping more than 100 million cyber-threats per day. The platform had scaled from processing millions of transactions to billions, from hundreds of users to millions.

But perhaps more importantly, Zscaler had achieved something rare in enterprise software: negative churn. Customers weren't just staying; they were expanding. As companies moved more applications to the cloud, as remote work became more common, as BYOD policies proliferated, Zscaler's value proposition only grew stronger. The Zero Trust Exchange wasn't just a product; it was becoming essential infrastructure for the cloud era.

The architecture Jay and team had built was proving its worth. While competitors were still shipping appliances or hastily moving their software to AWS, Zscaler had purpose-built a global proxy network that could inspect SSL traffic at scale, apply machine learning to threat detection, and deliver sub-100 millisecond latency from anywhere to anywhere. This wasn't software running in the cloud; this was software built for the cloud, from the ground up.

V. The IPO and Scale Journey (2018-2021)

March 16, 2018 marked Zscaler's coming-out party. The company raised $192 million in its IPO, becoming the first tech unicorn to go public that year. The stock opened at $27.50, a 60% premium to its $16 offering price, giving the company a market cap of over $3 billion. For Jay, who still owned 23% of the company (worth about $700 million at IPO), this wasn't an exit—it was a beginning.

The public markets initially struggled to understand Zscaler. Was it a firewall company? A VPN replacement? A cloud security play? The answer was yes to all, and more—Zscaler was proposing a fundamental rearchitecture of enterprise security. Instead of securing the perimeter, you secure the transaction. Instead of trusting the network, you trust nothing. Instead of backhauling traffic, you inspect it wherever it originates.

Wall Street education would take time, but the business kept executing. Revenue grew from $190 million in fiscal 2018 to $431 million in fiscal 2020—a 127% increase in two years. The company was adding marquee logos: 195 of the Global 2000 were now customers. Billings growth consistently exceeded 40%. The rule of 40 (growth rate plus profit margin) was consistently above 50.

Then came March 2020, and everything changed overnight.

COVID-19 didn't create the remote work trend—it accelerated it by a decade in three months. Suddenly, every company's network perimeter didn't just have holes; it ceased to exist entirely. VPNs that were designed for a few hundred remote users were being asked to handle tens of thousands. Legacy firewalls sitting in empty office buildings were useless. The castle had no walls, and the moat had evaporated.

Zscaler's traffic exploded. In April 2020 alone, the platform saw a 12-fold increase in remote user traffic. Companies that had been piloting Zscaler for small groups rushed to deploy it enterprise-wide. Zoom (yes, that Zoom) became a customer, needing to secure its suddenly remote workforce. The sales cycle compressed from months to weeks, sometimes days. This wasn't digital transformation anymore; it was digital triage. The stock price reflected this new reality. From a March 2020 low of around $50, Zscaler shares rocketed to over $300 by February 2021—a 500% gain in less than a year. Announced by Nasdaq on Friday, December 10, 2021, shares of Zscaler will be included in the Nasdaq-100 Index effective prior to market open on Monday, December 20, 2021. The addition to this prestigious index—alongside companies like Apple, Microsoft, and Google—validated Zscaler's transformation from upstart to essential infrastructure.

Jay's reflection on this milestone captured the moment perfectly: "Our growth has been fueled by enterprises that are phasing out the legacy networking and security architecture built around firewalls and VPNs, and are embracing the Zscaler Zero Trust Exchange." What had seemed futuristic in 2007 was now inevitable. The internet had become the corporate network, just as Jay had predicted.

The competitive landscape was also shifting. Palo Alto Networks, Fortinet, and Zscaler were all added to the NASDAQ-100 simultaneously—a recognition that cybersecurity had become as fundamental to the digital economy as semiconductors or software. But while competitors were acquiring their way into cloud security, Zscaler had been purpose-built for it. This architectural advantage was about to fuel an aggressive M&A strategy of its own.

VI. Platform Evolution & M&A Strategy

Jay Chaudhry's approach to M&A reflects a fundamental truth about platform businesses: you can either be comprehensive or best-of-breed, but rarely both. Zscaler chose comprehensive, systematically acquiring technologies that filled gaps in the Zero Trust Exchange. Each acquisition wasn't just about adding features; it was about deepening the moat.

The strategy began modestly. Zscaler acquired the AI and machine-learning technology of TrustPath in August 2018; the browser security company Appsulate for $13 million in May 2019; cloud security posture management startup Cloudneeti in April 2020; and microsegmentation firm Edgewise Networks in May 2020. These weren't blockbuster deals—they were surgical strikes, adding specific capabilities that would take years to build internally.

The TrustPath acquisition brought advanced AI for threat detection, critical as attack patterns became more sophisticated. Appsulate added browser isolation technology, protecting users from web-based threats without impacting performance. Cloudneeti provided visibility into cloud misconfigurations—the source of most breaches. Edgewise brought zero trust networking between applications, extending Zscaler's reach from user-to-app to app-to-app security.

The company purchased cybersecurity startup Trustdome in April 2021; Indian cybersecurity startup Smokescreen Technologies in May 2021; and cloud security firm ShiftRight for $25.6 million in September 2022. Smokescreen's deception technology added another layer—creating fake assets that lure attackers and provide early warning. ShiftRight brought application security testing capabilities, helping developers find vulnerabilities before deployment. The most significant acquisition came in March 2024: Avalor, reportedly for $310 million in cash and equity. This wasn't just another tuck-in—"AI is only as good as the underlying data, and many solutions lack the additional context and knowledge from data sources across the enterprise to truly leverage security specific AI models," said Jay Chaudhry. "Zscaler operates the world's largest security cloud with the most relevant data to train security specific large language models (LLMs) and with the Avalor acquisition, we can more effectively identify vulnerabilities, while predicting and preventing breaches".

Avalor's Data Fabric for Security with over 150 pre-built integrations, combined with Zscaler's 400 billion daily transactions, created a data advantage that would be nearly impossible for competitors to replicate. Avalor's Data Fabric for Security ingests, normalises, and unifies data across enterprise security and business systems to deliver actionable insights, analytics, and operational efficiencies.

The M&A strategy reveals a deeper truth about security platforms: comprehensiveness beats best-of-breed when the threat landscape is this complex. A CISO managing 50 different security tools can't respond fast enough when attacks happen in milliseconds. By assembling a complete platform through targeted acquisitions, Zscaler could offer something powerful: simplicity. One vendor, one platform, one throat to choke when something goes wrong.

But the real genius was in the integration strategy. Unlike many acquirers who leave purchases as standalone products, Zscaler absorbed each technology into the Zero Trust Exchange. Every acquisition made every other component stronger. Threat intelligence from one product improved detection across all products. This wasn't empire building; it was ecosystem engineering.

VII. Financial Performance & Business Model

The numbers tell a story of relentless execution. Revenue grew from $1.091 billion in fiscal 2022 (62% growth) to $1.617 billion in 2023 (48% growth) to $2.168 billion in 2024 (34% growth). While growth rates declined, this is the law of large numbers at work—maintaining 30%+ growth at $2 billion scale is exceptional in enterprise software.

More impressive is the free cash flow story. Fiscal 2024 generated $585 million in free cash flow, a 27% margin—remarkable for a company still growing at this pace. This isn't the typical SaaS playbook of growth at any cost; Zscaler has proven it can grow and generate cash simultaneously. The unit economics work because the platform architecture works: high gross margins (around 80%), efficient customer acquisition, and expanding revenue per customer.

The customer metrics reveal the platform's stickiness. Over 8,650 customers including 30% of the Forbes Global 2000 trust Zscaler with their security. Net retention consistently exceeds 120%, meaning existing customers increase spending by 20%+ annually. This expansion happens naturally—as companies adopt more cloud services, enable more remote workers, or face new compliance requirements, they need more Zscaler.

Processing 500+ billion daily transactions creates a powerful flywheel. More data improves threat detection. Better threat detection attracts more customers. More customers generate more data. This network effect, combined with switching costs (who wants to rearchitect security mid-flight?), creates a moat that deepens with scale.

The SaaS metrics that matter all point in the right direction. Customer acquisition cost payback is under 18 months. Gross retention exceeds 95%. The magic number (net new ARR divided by sales and marketing spend) consistently exceeds 1.0. These aren't just good numbers; they're best-in-class for enterprise software.

But perhaps the most telling metric is one that doesn't appear in financial statements: architectural advantage. Every competitor trying to move from appliances to cloud faces a multi-year rebuilding process. Meanwhile, Zscaler adds capabilities, expands geographically, and deepens relationships with existing customers. Time is the scarcest resource in technology transitions, and Zscaler bought itself a decade head start by betting on the cloud in 2007.

VIII. Modern Era: AI, Competition & Future Bets (2022-Present)

The modern Zscaler operates at massive scale. Zscaler had 7,348 employees as of July 31, 2024, processing those 500 billion daily transactions across 150+ data centers globally. This isn't just growth; it's the emergence of a new kind of security infrastructure—one that learns from every threat, adapts to every attack, and gets stronger with every customer.

AI has become the new battleground, and Zscaler's approach reflects Jay's architectural thinking. Rather than bolt on AI features, they're building AI into the platform's DNA. The appointment of Phil Tee as EVP of AI Innovations signals serious investment here. But the real advantage isn't the algorithms—it's the data. With visibility into more traffic than almost anyone except the hyperscalers, Zscaler can train models on real-world attack patterns at unprecedented scale.

The competitive dynamics have intensified dramatically. Microsoft's push into security (now a $20 billion business) poses an existential question: can independent security vendors survive when the platform providers offer "good enough" security bundled for free? Palo Alto Networks, under Nikesh Arora's leadership, has been acquiring aggressively to build a platform to rival Zscaler's. Cloudflare approaches from below, leveraging its edge network to add security capabilities.

Yet Zscaler keeps winning marquee customers. The Nokia migration from traditional firewalls represents the kind of transformation that defines eras—a massive, global enterprise ripping out decades of network security infrastructure to go all-in on Zero Trust. The Google Chrome Enterprise partnership validates the browser-as-a-security-perimeter thesis. These aren't just sales wins; they're votes of confidence in Zscaler's architectural vision. The January 2024 launch of Zscaler Zero Trust SASE represents the culmination of the platform strategy. Zscaler, Inc. (NASDAQ: ZS), the leader in cloud security, announced Zscaler Zero Trust SASE, an industry first, single-vendor SASE solution built utilizing Zscaler Zero Trust AI to help organizations reduce cost and complexity while implementing Zero Trust security across users, devices, and workloads. This isn't just adding SD-WAN capabilities; it's reimagining how networks and security converge in a zero trust world.

The international expansion story remains compelling but complex. Different regions have different regulatory requirements, data residency needs, and security priorities. Europe's GDPR, China's data localization laws, India's emerging privacy regulations—each requires not just compliance but architectural adaptation. Zscaler's 150+ data centers globally provide the infrastructure, but success requires more than presence; it requires local expertise and trust-building that takes years to develop.

IX. Playbook: Business & Investing Lessons

The Zscaler story offers a masterclass in founder-driven platform building, but the lessons extend far beyond Jay Chaudhry's personal journey. This is fundamentally about the difference between missionaries and mercenaries in technology markets. Jay wasn't chasing a trend or flipping a company—he was solving a problem he'd seen evolve across two decades in enterprise IT. The $50 million personal investment wasn't bravado; it was conviction that the future would unfold largely as he envisioned.

Platform thinking versus feature thinking separates the winners from the also-rans in enterprise software. Palo Alto Networks started with next-generation firewalls—a feature. Zscaler started with a vision of the internet as the corporate network—a platform. This distinction matters because platforms create ecosystems, features create products. Platforms get stronger with scale, features get commoditized. Platforms define categories, features compete within them.

The capital efficiency question challenges Silicon Valley orthodoxy. Zscaler took external capital not because it needed it, but because going public without any would seem odd. This self-funding approach preserved ownership (Jay still owns approximately 38% with his family) but more importantly, it enforced discipline. When you're spending your own money, every hire matters, every feature ships, every customer counts. Venture capital can accelerate growth, but it can also accelerate waste.

The enterprise sales motion in cybersecurity requires a unique balance. You're selling to paranoid people (CISOs) about invisible threats using intangible products that prevent events that haven't happened yet. Trust becomes the product. This is why Zscaler's "customer zero" approach—keeping Arc Mid-Hudson happy for 15+ years—matters more than any marketing campaign. In security, references aren't just helpful; they're existential.

Network effects in security operate differently than in consumer platforms. It's not about more users making the product more valuable to other users—it's about more data making threat detection more accurate for everyone. Every packet inspected, every threat blocked, every anomaly detected makes the next detection slightly better. Scale becomes intelligence, intelligence becomes value, value attracts more scale.

Timing markets requires patience that most founders lack. In 2007, Zscaler was arguably five years too early. Cloud adoption was nascent, remote work was rare, and most CISOs still believed in perimeters. But being early allowed Zscaler to build without competition, to learn from early adopters, to refine the architecture before the market exploded. By 2018, when competitors finally understood the opportunity, Zscaler had a decade head start.

Jay's ownership philosophy deserves special attention. Maintaining 38% ownership through multiple funding rounds and an IPO requires saying no repeatedly—no to dilutive rounds, no to aggressive VCs, no to quick exits. This isn't about greed; it's about control. When you own 38%, you can think in decades, not quarters. You can make bold bets that might take years to pay off. You can weather downturns without panic. Ownership equals optionality.

X. Analysis & Bear vs. Bull Case

Bull Case: The Inevitable Architecture

Zero Trust isn't a feature or a product category—it's an architectural shift as fundamental as the move from mainframes to client-server or from on-premise to cloud. Every major technology transition creates dominant platforms that define the new paradigm. Zscaler has positioned itself as the Zero Trust platform, processing 500 billion transactions daily and protecting 40% of the Fortune 500.

The FY2025 guidance of $2.60-2.62 billion in revenue represents 30%+ growth at massive scale. More importantly, the company generates real cash—nearly $600 million in free cash flow—while still investing aggressively in R&D and sales. This isn't the typical SaaS story of buying growth with losses; Zscaler has achieved the rare combination of growth and profitability.

Platform stickiness in security exceeds almost any other software category. Once Zscaler becomes the security layer for an enterprise, ripping it out means re-architecting security from scratch—a multi-year project no CISO wants to undertake. Net retention above 120% proves customers don't just stay; they expand. As companies add users, adopt more cloud services, or face new compliance requirements, Zscaler revenue grows naturally.

Security spending has proven remarkably resilient through economic cycles. Even in downturns, companies don't cut security—breaches are too costly, regulations too stringent, risks too high. If anything, economic uncertainty increases security concerns as companies worry about insider threats from laid-off employees and increased cybercrime during recessions.

AI creates new attack vectors that traditional security can't address. Deepfakes, AI-generated phishing, automated vulnerability discovery—the threat landscape is evolving faster than human security teams can adapt. Zscaler's data advantage (those 500 billion daily transactions) provides the training set for AI models that can detect AI-generated threats. This creates a virtuous cycle: more sophisticated threats require more sophisticated defense, which requires more data, which Zscaler has more of than almost anyone.

Bear Case: The Perils of Premium Valuation

Valuation concerns are legitimate at current multiples. Trading at 15-20x forward revenue (depending on the day), Zscaler is priced for perfection. Any growth deceleration, margin compression, or execution stumble could trigger a violent re-rating. The stock's volatility—capable of 20% moves on earnings—reflects this precarious balance between growth expectations and fundamental reality.

Big Tech's entry into security changes the competitive dynamics fundamentally. Microsoft's security business now exceeds $20 billion annually—larger than Zscaler's entire market cap. When Microsoft bundles security with Office 365 or Azure, when Google packages it with Workspace, when Amazon includes it with AWS, the "good enough" problem becomes existential. Why pay for best-of-breed when good enough is free?

Legacy vendors aren't standing still. Palo Alto Networks, with its aggressive M&A strategy, is assembling a platform to rival Zscaler's. Fortinet brings decades of enterprise relationships. Cisco has distribution power. These aren't startups that will run out of money—they're multi-billion dollar companies with resources to compete indefinitely. The question isn't whether Zscaler's architecture is superior (it probably is), but whether superior is enough when competitors are good enough and cheaper.

Sales efficiency metrics show concerning trends. Customer acquisition costs are rising, sales cycles are lengthening, and growth rates are decelerating. This is natural as companies scale, but it raises questions about the next leg of growth. The easy wins—cloud-forward companies desperate for modern security—have been captured. The next wave requires convincing laggards with legacy infrastructure, a much harder and more expensive sale.

Concentration risk with a founder-CEO who owns 38% creates unique governance challenges. Jay Chaudhry has built an exceptional company, but he's also irreplaceable in a way that should concern investors. At 66, succession planning becomes critical. The history of founder-dependent companies post-founder is mixed at best. When vision, strategy, and execution all flow from one person, what happens when that person steps aside?

XI. Epilogue & Looking Forward

Jay Chaudhry's journey from a village without electricity to an $11.5 billion net worth reads like fiction, but the real story isn't about wealth—it's about timing a fundamental shift in how the world works. The boy who walked four miles to school saw that the internet would become the network before almost anyone else. The entrepreneur who'd already built four successful companies bet everything on a fifth because he understood that security without trust is an oxymoron.

What would success look like in five years? Zscaler at $10 billion in revenue, processing trillions of transactions daily, securing not just users and applications but entire supply chains, IoT networks, and critical infrastructure. The Zero Trust Exchange becomes as fundamental to the internet as DNS or BGP—invisible but essential plumbing that makes digital commerce possible.

But success might also look different—Zscaler as the security layer of a larger platform, acquired by Microsoft or Google or Amazon for $100+ billion, Jay's architecture finally achieving the ubiquity it deserves. Or perhaps Zscaler becomes the acquirer, rolling up the security industry the way Oracle consolidated databases or Salesforce absorbed CRM.

The broader implications extend beyond corporate IT. As governments grapple with cyber warfare, as critical infrastructure faces nation-state attacks, as privacy becomes a human right rather than a feature, the principles Zscaler pioneered—trust nothing, verify everything, inspect always—become societal imperatives. The company selling enterprise security might be building the foundation for digital civilization.

For founders, the lessons are clear but challenging. Building in regulated markets like security requires patience measured in decades, not years. It requires capital efficiency that comes from spending your own money first. It requires the courage to be early and the persistence to be right. Most importantly, it requires solving real problems rather than chasing trends—being a missionary in a world of mercenaries.

The Zero Trust revolution isn't complete—it's barely begun. As computing moves to the edge, as AI creates new attack surfaces, as quantum computing threatens current encryption, the need for adaptive, intelligent, distributed security only grows. Zscaler has positioned itself at the center of this transformation, but maintaining that position requires continuous innovation, flawless execution, and a bit of luck.

Jay Chaudhry often returns to Panoh, the village where his story began. He's brought medical services, funded education, and invested in infrastructure. But perhaps his greatest contribution isn't what he's built for Panoh, but what Panoh built in him—the understanding that transformation isn't just possible; it's inevitable for those willing to see the future and build toward it. The boy walking to school in the dark became the man illuminating the path to Zero Trust. The journey from Panoh to NASDAQ wasn't just about distance traveled—it was about futures imagined and architectures realized.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube