TD SYNNEX: The Invisible Giant of the IT Supply Chain

I. Introduction: The $60 Billion Company You've Never Heard Of

Picture this: Every time a small business in Des Moines buys a new server, every time a hospital in Munich upgrades its cybersecurity infrastructure, every time a school district in São Paulo refreshes its laptop fleet—there's a company quietly orchestrating the transaction. It's not the manufacturer whose logo adorns the box. It's not the local reseller who shook hands with the IT director. It's the invisible layer in between, a company most consumers have never heard of, yet one that touches virtually every technology purchase on the planet.

TD Synnex Corporation is an American IT distribution company with a workforce of 22,000 in over 100 countries. It was formed in 2021 by the merger of Synnex and Tech Data. With trailing twelve-month revenue approaching $61 billion, TD Synnex's TTM revenue is $60.97 Billion USD as of November 2025—more than Nike, more than Starbucks, more than Lockheed Martin—yet the average person on the street couldn't tell you what the company does.

The answer, at its simplest, is: TD SYNNEX moves boxes. It buys technology products from manufacturers like Microsoft, Cisco, Dell, and HP, warehouses them across a global logistics network, and sells them to the resellers, system integrators, and managed service providers who ultimately serve end customers. But that description undersells the complexity and strategic importance of what the company actually does.

TD SYNNEX's competitive advantages include its extensive vendor relationships with over 1,500 technology suppliers, broad geographic reach across more than 100 countries, and comprehensive service capabilities spanning from basic distribution to complex systems integration. The company provides the financing, technical validation, sales enablement, and integration support that makes the technology supply chain function. Without companies like TD SYNNEX, every manufacturer would need its own sales force reaching hundreds of thousands of smaller customers. Without distributors, every reseller would need separate credit lines and relationships with thousands of vendors.

With the merger of Tech Data and Synnex, TD Synnex becomes the largest IT distributor having a combined revenue of $59.8 billion, which surpasses Ingram Micro, whose 2020 revenue was $49.1 billion. The company now stands as the undisputed global leader in its space, a position earned through decades of strategic maneuvering, disciplined execution, and a willingness to make bold bets at inflection points.

Canalys (part of Omdia) estimates that the global IT distribution market stood at US$463 billion in 2024. The sector is increasingly concentrated, with the top 15 distributors generating sales of US$287 billion, commanding over 61% of the total. TD SYNNEX, as the largest player, sits at the apex of this consolidation.

How did we get here? How did a Taiwanese immigrant's computer parts export business and a Florida entrepreneur's printer ribbon company—started six years apart, on opposite coasts—eventually converge into the world's largest IT distributor? And more importantly for investors: What does this invisible infrastructure company's future look like in an age of cloud computing, AI infrastructure buildouts, and direct-to-customer sales models?

The story of TD SYNNEX is, in many ways, the story of the technology industry itself—from mainframes to PCs, from on-premise servers to cloud subscriptions, from selling boxes to orchestrating solutions. It's a story worth understanding.

II. Origins: Two Immigrant Stories (1974-1990)

The Tech Data Story: Printer Ribbons in the Sunshine State

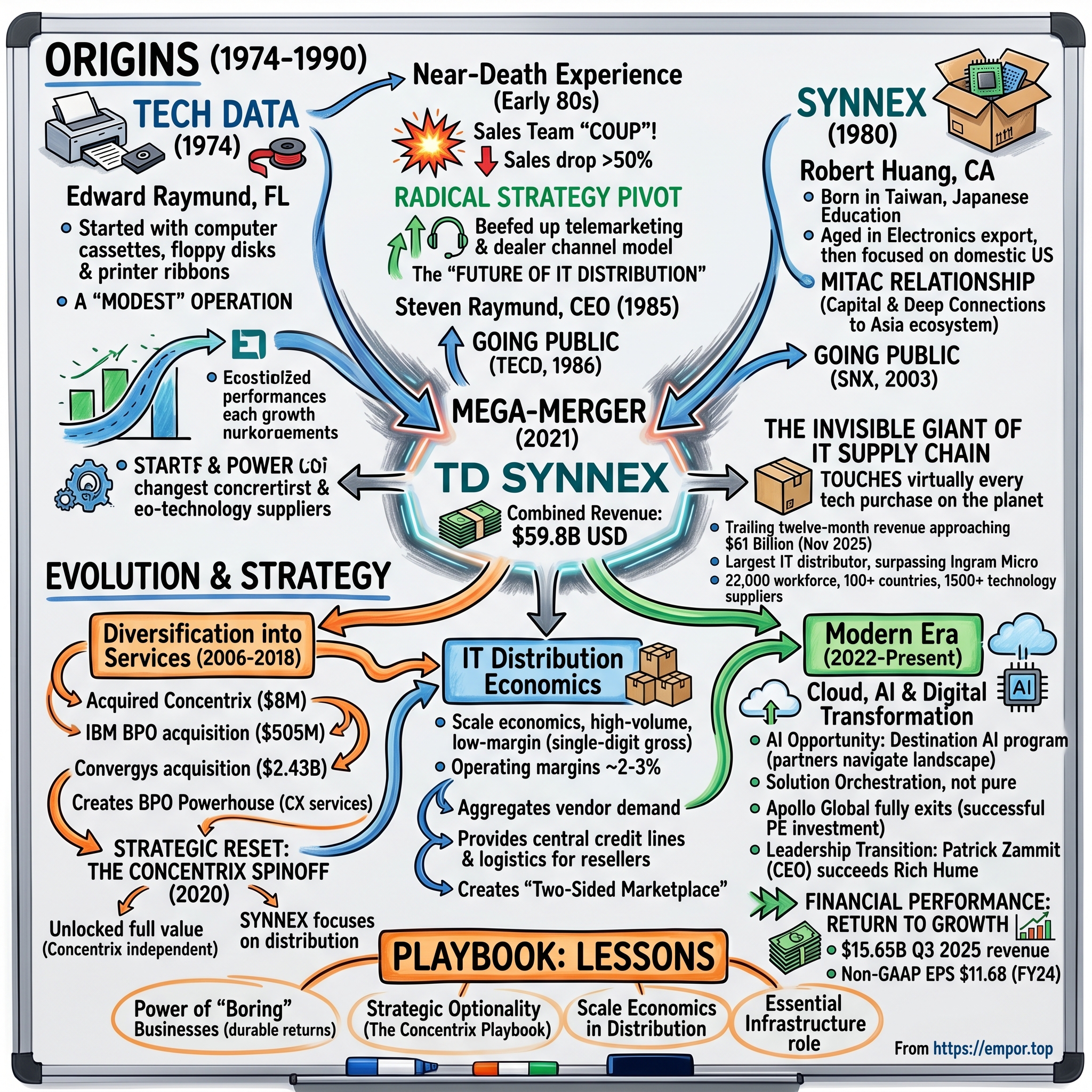

Edward Charles Raymund (August 26, 1928 – December 9, 2008) was an American businessman and the founder of Tech Data Corp. Raymund was born to a poor family on August 26, 1928 in Hollywood, California, and raised in Los Angeles. He served in the Army Air Corps and attended the University of Southern California on the G.I. Bill. After school, he worked as an electronics manufacturer's representative in Southern California. He moved to Florida eight years later where he saw an opportunity due to the state's rapid growth.

In the 1960s, Raymund was distributing high-volume sockets and capacitors in central Florida. In 1974, he founded Tech Data which initially sold computer memory cassettes, floppy disks, and printer ribbons; and added monitors, printers, add-on cards, and eventually IBM PCs in the 1980s.

The company was started by Edward Raymund to market computer supplies to large institutions in central Florida. Its customers at that time were end-users rather than resellers, primarily hospitals and government agencies. These institutional customers purchased disk packs, tape, and other data-processing paraphernalia for use with their mainframe and mini computers.

By the early 1980s, the company had annual sales of about $2 million. It was a modest operation—about a dozen employees handling customer orders from a small office and warehouse near Clearwater, Florida. But two developments—one inside the company, one in the broader industry—would transform Tech Data's trajectory.

Around that time, several developments both inside the company and in the computer industry as a whole led to profound changes in the way Tech Data was to do business. The emergence of personal computers (pcs) in 1980 created an exciting new market niche that was wide open for exploitation.

The other development was more dramatic—and nearly destroyed the company. Steven Raymund, Edward's 25-year-old son, came to work for the company. Put to work on the upcoming Tech Data catalog, Steve initially had no intention of making the situation permanent. Gradually, however, his interest in the company's operations increased. As the elder Raymund began spending less time at Tech Data to concentrate on his other company, Tech Rep Associates, Steven Raymund took on more responsibilities, eventually becoming operations manager at Tech Data.

What happened next reads like a corporate thriller. This development did not sit at all well with the sales force, which had hoped to buy the company out from Raymund in the near future; Steven Raymund's sudden rise to prominence meant that a buyout was unlikely. About a month after Steven Raymund received his new title, a group consisting of Tech Data's key salespeople staged a coup of sorts. The group of five gathered at the office on a Saturday and proceeded to photocopy all of the company's customer records and vendor information.

The following Monday, Raymund found letters of resignation on his desk from the five, who then went to work for a nearby competitor. The impact of this mass desertion at Tech Data was immediate and brutal. It quickly became apparent that the salespeople had taken many of the company's best customers with them. Monthly sales figures dropped by more than 50 percent, and the company began losing money. In fact, the situation became so bad that the elder Raymund considered shuttering Tech Data so that he could devote more resources to his other company, which was thriving.

The near-death experience forced a radical strategic pivot. Instead, the Raymunds undertook a radical shift in strategy. Rather than replace the departed field sales force, they beefed up their telemarketing staff, which was much less expensive to support. They then began to aggressively court computer dealers in addition to end-users. The company also began to pay more attention to direct mail, purchasing mailing lists and sending out catalogs in greater numbers.

This pivot—from field sales to telemarketing, from end-users to dealer channel—would prove prescient. The Raymunds had inadvertently stumbled onto the future of IT distribution: a high-volume, low-touch model serving a fragmented base of resellers.

In 1985, his son, Steven Raymund, became CEO. Under Steve's leadership, the company went public on NASDAQ in 1986 under the ticker symbol TECD and began its international expansion, acquiring ParityPlus in Canada in 1989 and eventually entering Europe through France in 1994.

The SYNNEX Story: From Osaka Paper Boxes to Silicon Valley

Half a world away, a different origin story was unfolding. Synnex was founded by its longtime chief executive officer, Robert Huang. He was born in Taiwan in 1945, the son of a Japanese-educated father who launched a paper trading company, Nichidai Trading, which he relocated to Osaka, Japan, in 1955 to be closer to Western markets, which at the time were beginning to import a great deal of Chinese noodles and relied on the paper boxes Nichidai Trading manufactured.

Huang attended high school in Japan and stayed in the country to earn an Electrical Engineering degree from Kyushyu University. Then in 1968 he moved to the United States for his postgraduate studies, earning a master's degree in electrical engineering from the University of Rochester, followed by a master's in management science from the Massachusetts Institute of Technology's Sloan School of Management. Huang returned to Japan to take a job with chipmaker Advanced Micro Devices, eventually becoming an international sales manager.

There he learned a great deal about Japanese management styles, attention to detail, and frugality. He applied these lessons when he returned to California and struck out on his own in 1980 to launch Compac Microelectronics, Inc., later to take the Synnex name. Compac started out exporting computer parts into Asian markets, but soon Huang became fearful of instability in the region and around 1983 focused the company on domestic markets, particularly the West Coast.

Huang's Japanese management training would become central to SYNNEX's DNA—a relentless attention to detail, operational frugality, and long-term thinking that would set the company apart from its more aggressive American competitors.

Overall, the company fared well but after several years, when annual sales reached around $40 million, it hit a ceiling. Huang told Silicon Valley/San Jose Business Journal in a 2004 profile, "I felt we were stretching cash." As a result he sold control of the company and stayed on to run it.

This decision connected SYNNEX to a critical partner: MiTAC Holdings, a Taiwanese conglomerate. The MiTAC relationship would provide both capital and deep connections to Asia's burgeoning technology manufacturing ecosystem. MiTAC Holdings Corp. and its affiliates, which collectively owns about 17% of Synnex shares as of 22 January 2021, voted their shares in favor of the transaction that would eventually create TD SYNNEX.

The Business Model Innovation: Understanding Distribution

To understand what Tech Data and SYNNEX were building, one must first understand the peculiar economics of IT distribution. At its core, distribution is a "boxes moving" business—buying products from manufacturers, warehousing them, and selling them to resellers. The gross margins are tissue-thin, typically in the single digits. Operating margins hover around 2-3%.

Why would anyone want to be in such a low-margin business? The answer lies in scale economics, working capital management, and the value of being the "connective tissue" between fragmented supply and fragmented demand.

Consider the alternative: Microsoft, with its thousands of products, would need relationships with hundreds of thousands of small resellers across 100+ countries. Each reseller would need credit facilities, technical training, and logistics support. The transaction costs would be prohibitive. Distributors solve this by aggregating demand and providing a single point of contact for vendors while simultaneously aggregating supply and providing a single source for resellers.

The business model creates what industry observers call a "two-sided marketplace": More vendors attract more resellers (who want one-stop shopping), and more resellers attract more vendors (who want reach into fragmented markets). Once a distributor achieves scale, the flywheel becomes self-reinforcing.

Both Tech Data and SYNNEX understood these dynamics and spent the next three decades executing against them—building logistics networks, establishing vendor relationships, developing credit underwriting capabilities, and acquiring smaller distributors to achieve the scale necessary to survive in a consolidating industry.

III. The Evolution of IT Distribution (1990-2005)

Tech Data's Aggressive Expansion

Under Steven Raymund's leadership, Tech Data pursued an aggressive acquisition-led growth strategy. The company understood that scale was destiny in distribution—only the largest players would have the purchasing leverage, logistics efficiency, and capital base to survive.

AG $395 million in stock for its 80 percent holding in Munich-based distributor Computer 2000 AG (the remaining shares were picked up in 2000). This purchase lifted Tech Data's total revenues to nearly $12 billion, noted Computer Reseller News. Computer 2000 had operations in more than 30 countries, some (in the Middle East and South America) new to Tech Data.

The Computer 2000 acquisition was transformative, giving Tech Data a European footprint that would prove strategically valuable for decades. After putting the company's U.S. operations in the hands of company president Tony Ibarguen, CEO Steve Raymund temporarily moved to Paris to be closer to the expanding business in Europe. In the western hemisphere, Tech Data set up distribution centers in Sao Paulo, Brazil and Miami. Globelle Corporation was added in 1999, doubling the size of Tech Data's Canadian business north of the border.

Tech Data is now one of the world's largest distributors of IT products and services, generating $37.7 billion in net sales for the fiscal year ended January 31, 2017. The company ranked No. 83 on the 2018 Fortune 500 and one of Fortune's "World's Most Admired Companies."

SYNNEX's Organic Growth Philosophy

While Tech Data grew through acquisitions, SYNNEX under Robert Huang pursued a more measured approach emphasizing organic growth, operational excellence, and careful capital allocation. The company went public in 2003 on the New York Stock Exchange under the ticker symbol SNX.

Speaking on behalf of SYNNEX Board of Directors, Mr. Steffensen said, "We are forever indebted to the contributions of Bob Huang. Bob founded SYNNEX in 1980 and over the past 30 years, nurtured SYNNEX to a $7+ billion Fortune 500 company."

Huang's attention to detail and frugality became legendary within the company. Unlike the more glamorous tech companies of Silicon Valley, SYNNEX operated with the discipline of a Japanese manufacturing firm—every cost scrutinized, every process optimized, every dollar of working capital carefully managed.

The Competitive Landscape: A Three-Horse Race

By the early 2000s, IT distribution had consolidated into a three-horse race globally: Ingram Micro (the long-time leader), Tech Data (the aggressive challenger), and SYNNEX (the disciplined operator). Each had distinct strengths: Ingram Micro had the broadest global reach; Tech Data had the strongest European presence; SYNNEX had the tightest operations and the deepest connections to Asian manufacturing.

TD SYNNEX operates in the highly competitive global technology distribution market, competing with several major players across different geographic regions and product categories. The company's primary competitors include Ingram Micro, which is owned by HNA Group and serves as another global technology distributor with strong presence in cloud services and mobility solutions.

The competitive dynamics were intense but stable. With operating margins of 2-3%, there was little room for error—or for aggressive price wars. The three leaders tacitly understood that destroying profitability would benefit no one.

IV. Key Inflection Point #1: The Concentrix Diversification (2006-2018)

The Bold Bet on Services

Robert Huang's SYNNEX was about to make a move that would puzzle industry observers: diversifying from distribution into business process outsourcing (BPO). In hindsight, the logic was clear—distribution margins were compressing, and the company needed higher-margin revenue streams. But at the time, the acquisition of Concentrix seemed like an odd fit.

Synnex, a Fortune 200 company, founded in 1980, acquired Concentrix in 2006 for about $8 million. In 2013, Synnex acquired IBM's worldwide customer care business process outsourcing (BPO) services business for $505 million.

Concentrix traces its origins to an independent customer engagement services provider based in New York, which SYNNEX Corporation acquired in September 2006 for approximately $8 million. The acquired entity had generated about $15 million in revenue in the 12 months ending December 31, 2005, primarily through integrated marketing solutions.

What began as a tiny $8 million acquisition would, over the next 14 years, be built into a global BPO powerhouse. In September 2013, SYNNEX Corporation announced its acquisition of IBM's worldwide customer care business process outsourcing operations for $505 million, consisting of $430 million in cash and $75 million in SYNNEX stock. The deal, which added over $1.2 billion in annual revenue and positioned the combined entity as a top global player in customer relationship management services, was integrated into SYNNEX's Concentrix subsidiary, significantly expanding its scale in customer engagement outsourcing. Initial closing occurred in February 2014, with full integration enhancing Concentrix's capabilities in sectors such as technology and telecommunications.

The Convergys Acquisition: Creating a BPO Powerhouse

On 28 June 2018, Convergys and Synnex announced they have reached a definitive agreement in which Synnex would acquire Convergys for $2.43 billion in combined stock and cash, and integrate it with Concentrix. On 5 October 2018, the merger was completed.

This was a massive bet. Convergys was a Cincinnati-based customer management company with its own long history. The acquisition more than doubled Concentrix's scale and created one of the world's largest customer experience outsourcing providers.

Concentrix, a global business services company, reports approximately $4.7 billion in annual revenue. By 2020, the services business had grown from that initial $8 million acquisition to nearly $5 billion in annual revenue—a remarkable value creation story within a distribution company.

The Dual-Engine Business Model

For much of the 2010s, SYNNEX operated an unusual dual-engine business model: low-margin, high-volume distribution on one side; higher-margin, labor-intensive BPO services on the other. The businesses had little operational synergy—distribution is about moving products; BPO is about managing people. But financially, the combination worked: Concentrix's higher margins and more stable cash flows offset distribution's cyclicality and thin margins.

The strategic question was whether this conglomerate structure was serving shareholders optimally or whether the market was applying a "conglomerate discount" to the combined entity.

V. Key Inflection Point #2: The Concentrix Spinoff (2020)

The Strategic Reset

On 9 January 2020, Dennis Polk, President and Chief Executive Officer of Synnex, announced plans to separate SYNNEX and Concentrix into two publicly traded companies. The spinoff was completed on 1 December 2020, with Synnex shareholders getting one share of Concentrix for each share of Synnex they held.

The announcement came with a clear strategic rationale: each business deserved its own focus, its own capital allocation strategy, and its own investor base. Distribution investors wanted low leverage and working capital efficiency; BPO investors wanted growth investments and margin expansion.

"We are pleased to announce the completion of the separation transaction and wish the Concentrix team well as an independent publicly traded company," said Dennis Polk, President and CEO of SYNNEX. "I am excited for the future of SYNNEX and the ongoing value we expect to deliver to our vendors, customers, associates and shareholders."

The Strategic Logic

"As a leading global provider of CX solutions and technology, we are truly excited to celebrate our listing day and start this next exciting chapter," said Chris Caldwell, President and CEO of Concentrix. "Operating as an independent company will allow us to accelerate innovations and make additional investments that drive higher value for our clients, their customers, and our shareholders."

The spinoff thesis proved prescient. On March 29, 2023, Concentrix announced the acquisition and merger of Concentrix and Webhelp in a transaction worth $4.8 billion. The overall combined company value was estimated to total around $9.8 billion. In September 2023, the European Commission had approved the acquisition, under EU Merger Regulations.

Concentrix, now free from its parent's capital constraints, could pursue large-scale M&A that would have been impossible within SYNNEX's conglomerate structure. Meanwhile, SYNNEX could focus entirely on its distribution business—and prepare for what would become the most transformative deal in its history.

Unlocking Value Through Focus

The Concentrix build-then-spinoff playbook represents a masterclass in corporate strategy and value creation. SYNNEX acquired a tiny marketing services company for $8 million, invested in organic and inorganic growth over 14 years, built it into a $5 billion business, and then spun it off to unlock its full value.

For investors, this demonstrated management's capital allocation skills and willingness to prioritize shareholder value over empire building. The spinoff set the stage for SYNNEX's next chapter.

VI. Key Inflection Point #3: The Mega-Merger with Tech Data (2021)

Apollo's Tech Data Play

The 2021 merger that created TD SYNNEX has roots in an earlier transaction: private equity firm Apollo Global Management's acquisition of Tech Data.

NEW YORK, June 30, 2020 (GLOBE NEWSWIRE) -- An affiliate of certain funds managed by affiliates of Apollo Global Management, Inc. today announced completion of its acquisition of Tech Data Corporation, one of the world's largest technology distributors. Chief Executive Officer Rich Hume will continue to lead Tech Data from its headquarters in Clearwater, Florida.

The transaction gives Tech Data an enterprise value of approximately $6 billion and included a $3.75 billion equity.

The Apollo acquisition had a fascinating backstory. Apollo, a $325 billion private equity firm based in New York, originally offered $130 a share last November, for a total purchase price of $5.4 billion. During a "go-shop" period, Tech Data, a global technology distributor for companies like Apple and Cisco, reached out to 60 companies in search of a better deal. The best competing offer, $140 a share, came from Berkshire Hathaway, the giant investment and holding company run by Omaha billionaire Warren Buffett. But Buffett dropped out of the bidding after Apollo raised its offer to $145 a share.

That Warren Buffett was interested in Tech Data speaks volumes about the quality of the business. The Oracle of Omaha famously looks for businesses with durable competitive advantages, strong cash generation, and capable management—exactly the profile of a leading IT distributor.

The Transformative Merger

On 22 March 2021 it was announced that Synnex will merge with Tech Data for a sum of 7.2 billion USD, including debt. Synnex shareholders received 55% of the merged company. On September 1, 2021, Synnex completed a merger with Tech Data. This merger created a new company with $59.8 billion in revenue, TD Synnex. Through the combination of both companies, TD Synnex becomes the largest IT distributor, surpassing Ingram Micro.

At closing former Synnex shareholders owned 55% of TD Synnex while Apollo Global Management, the previous owner of Tech Data, owned 45%.

The merger combined complementary strengths: SYNNEX's dominant position in the Americas and Asia-Pacific with Tech Data's established European operations. Together, they created a global powerhouse with unmatched scale.

Like others in distribution, Ingram Micro's Kirk Robinson has a "healthy respect" for what will be a "formidable foe" when the pending merger between SYNNEX and Tech Data closes later this year. But the essence of Robinson's take on the epic deal boils down to two words: game on. "You couldn't ask for anything better," says Robinson, who is Ingram's senior vice president and chief country executive for the U.S. "Any company needs good, strong competition to raise their own bar, so we're looking forward to it."

Leadership and Integration

TD Synnex is led by former Tech Data CEO, Rich Hume. The leadership structure reflected the merger's dynamics: Tech Data's CEO would run the combined company, but SYNNEX's shareholders owned the majority.

TD Synnex overtook Ingram to become the world's largest IT distributor by sales when it formed via the merger of Tech Data and Synnex in 2021.

The competitive implications were significant. For decades, Ingram Micro had been the industry leader. Now it faced a competitor with comparable scale and resources—a true duopoly at the top of global IT distribution.

VII. The Modern Era: AI, Cloud, and Digital Transformation (2022-Present)

Financial Performance: Return to Growth

After the inevitable post-pandemic normalization that affected all tech distributors, TD SYNNEX returned to growth in fiscal 2024. The company's revenue reached $15.84bn during the fiscal fourth quarter, a ten per cent increase compared to the same period last year ($14.4bn in Q4 FY23). These results surpass the company's $14.9bn to $15.7bn expectations. This series of strong quarters ensured an overall good fiscal year for the company, which reported a 1.6 per cent growth revenue in FY24, rising to $58.45bn, compared to $57.55bn the year prior.

Non-GAAP gross billings were $80.1 billion in fiscal 2024 compared with $77.2 billion in the prior year. The non-GAAP operating income for fiscal 2024 was down 0.9% to $1.627 billion. The non-GAAP operating margin was 2.78% for fiscal 2024, down 7 bps compared with the previous year's reported figure. Non-GAAP EPS for fiscal 2024 increased 3.7% year over year to $11.68.

TD SYNNEX had revenue of $15.65B in the quarter ending August 31, 2025, with 6.58% growth. This brings the company's revenue in the last twelve months to $60.97B, up 6.94% year-over-year.

As of October 2025 TD Synnex has a market cap of $12.34 Billion USD. This makes TD Synnex the world's 1620th most valuable company according to our data.

Apollo's Exit and Ownership Transition

Throughout 2024, Apollo Global Management systematically reduced its position in TD SYNNEX through multiple secondary offerings.

Paul, Weiss advised certain entities managed by affiliates of Apollo Global Management, Inc. as the selling shareholders in an $881 million secondary public offering of 8,768,750 shares of TD SYNNEX Corporation common stock.

Paul, Weiss represented certain entities managed by affiliates of Apollo Global Management, Inc., as the selling shareholders, in a $1.3 billion secondary public offering of 12,075,000 shares of TD SYNNEX Corporation common stock.

TD SYNNEX Corporation today announced the pricing of the previously announced secondary public offering of 5,309,299 shares of its common stock. All of the shares in the offering are being sold by certain entities managed by affiliates of Apollo Global Management, Inc. (the "Selling Stockholders") and represent all the remaining shares owned by the Selling Stockholders.

By April 2024, Apollo had fully exited its position—a successful private equity investment that saw the firm buy Tech Data for $6 billion, merge it with SYNNEX, and exit through public market sales.

Leadership Transition

TD SYNNEX today announced that Patrick Zammit will become Chief Executive Officer, succeeding Rich Hume, who will retire after a transformative tenure as CEO. Zammit, who has served as the company's chief operating officer since January 2024, brings a wealth of experience and a proven track record of driving growth and operational excellence.

Hume joined what was then Tech Data in 2016 as COO, taking over as CEO in 2018. During his tenure, he has helped lead the company through a period of significant growth and transformation, including the acquisition of Avnet TS, taking the company private in partnership with Apollo Asset Management and the successful merger of Tech Data and SYNNEX.

Zammit led the European region beginning in 2017, following Tech Data's acquisition of Avnet Technology Solutions. His role expanded in 2021 to include responsibilities for the APJ region. His tenure at Avnet, which began in 1993, saw him in various management roles, culminating as Global President of the Technology Solutions division.

Patrick Zammit has served as CEO of TD SYNNEX since September 2024, leading the company's strategic direction and overseeing global operations. Previously, he was Chief Operating Officer (COO), coordinating strategies to drive profitable growth and accelerate the adoption of high-growth technologies.

Strategic Priorities: AI and Cloud

TD SYNNEX has positioned itself aggressively around the AI opportunity, launching its Destination AI program to help partners navigate the emerging technology landscape.

TD SYNNEX (NYSE:SNX), a leading global distributor and solutions aggregator, today announced the next evolution of its global, industry-leading Destination AI™ program designed to modernize partners' go-to-market strategies and capitalize on the growing demand for AI-enabled solutions. "The global AI landscape has changed dramatically since the launch of Destination AI™, unlocking new opportunities for growth and business transformation," said Mark Martin, TD SYNNEX. As AI matures, the market is increasingly focusing on integrated, AI-enabled technologies across security, networking, storage, cloud and more.

The latest evolution of TD SYNNEX's AI program marks a clear shift in strategy—from enabling general awareness of AI technologies to facilitating structured, scalable implementation. According to the company, the original version of Destination AI focused on introducing AI concepts and building a foundational understanding of the market.

TD SYNNEX (NYSE:SNX), a leading global distributor and solutions aggregator for the IT ecosystem, today announced the launch of its Destination AI™ Practice Accelerator in North America to fast-track AI go-to-market efforts and monetization for partners. The program provides personalized support to partners looking to deliver specialized AI solutions to their customers. According to TD SYNNEX's recently released Direction of Technology report, partners are rapidly increasing investments in AI, with nearly half of all channel partners planning to offer AI-driven solutions in the next two years.

By embedding AI as a standard consideration within the broader IT portfolio—rather than treating it as a niche solution—TD SYNNEX aims to normalize adoption and reduce risk for buyers. Unlike hyperscale cloud providers or niche AI vendors, TD SYNNEX operates as a connective layer in the technology stack. It does not build proprietary software but instead provides distribution, technical validation, sales enablement, and integration support across a wide ecosystem of products.

VIII. Playbook: Business and Investing Lessons

The Power of "Boring" Businesses

TD SYNNEX represents a classic "boring" business that generates durable returns despite—or perhaps because of—its lack of glamour. Distribution is not sexy. Operating margins of 2-3% don't make headlines. But the business has critical characteristics that create value over time:

-

Essential infrastructure: Technology vendors need distributors; resellers need distributors. The intermediary role is difficult to disintermediate entirely.

-

Working capital advantages: The largest distributors can negotiate better terms from vendors and offer better financing to resellers, creating a self-reinforcing advantage.

-

Scale economics: Every additional vendor and reseller on the platform makes the platform more valuable, driving consolidation toward the largest players.

FPA Queens Road Small Cap Value Fund stated the following regarding TD SYNNEX Corporation (NYSE:SNX) in its third quarter 2025 investor letter: "TD SYNNEX Corporation (NYSE:SNX) is the largest information technology (IT) distributor globally. 20 years ago, IT distribution involved getting personal computers (PCs), servers, and routers from the manufacturer to the customer. But TD Synnex adds value by acting as an outsourced sales force for its suppliers and providing IT consulting to its customers. The business has evolved, and the company sells increasing amounts of software, security solutions, cloud licenses, and other growth-y IT at attractive margins. Shares have performed well this year as billings growth has rebounded to a double digit rate, led by TD Synnex's more complex and higher margin Advanced Solutions portfolio. We believe that SNX shares are still attractive at the current valuation of roughly 12x this year's earnings."

Scale Economics in Distribution

The top three – TD Synnex, Ingram Micro and Arrow (ECS and electrical components) – generated gross sales of nearly US$170 billion, more than a third of the total. Market leader TD Synnex's scale is tremendous, with 2024 gross billings of US$80.1 billion making it larger than the vast majority of the vendors it distributes. It spans almost every technology segment, and with an advanced solutions arm generating US$47 billion gross sales, it is by far the world's largest specialist distributor.

TD SYNNEX's competitive advantages include its extensive vendor relationships with over 1,500 technology suppliers, broad geographic reach across more than 100 countries, and comprehensive service capabilities spanning from basic distribution to complex systems integration. The company's scale, resulting from the SYNNEX-Tech Data merger, positions it as one of the top two global technology distributors alongside Ingram Micro, enabling it to negotiate favorable terms with vendors and provide competitive pricing to reseller partners.

Strategic Optionality: The Concentrix Playbook

The Concentrix build-then-spinoff strategy represents a masterclass in corporate finance:

- Acquire a small platform business (2006: Concentrix for $8 million)

- Invest in growth, both organic and inorganic (2013: IBM BPO; 2018: Convergys)

- Build into a meaningful business unit (by 2020: ~$5 billion revenue)

- Spin off to unlock full value (2020: Concentrix goes public)

The approach demonstrates management's willingness to take long-term bets, execute disciplined M&A, and ultimately prioritize shareholder value over corporate empire-building.

Capital Allocation Philosophy

TD SYNNEX returns substantial capital to shareholders while maintaining the working capital necessary to operate the distribution business. The company returned 72% of its free cash flow to shareholders through buybacks and dividends during fiscal year 2024. The company generated $513 million in free cash flow in Q4, meeting its target of $1 billion for the full fiscal year 2024.

IX. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The IT distribution business has massive barriers to entry: - Capital requirements for inventory, warehousing, and logistics are substantial - Vendor relationships take decades to build - TD SYNNEX's approximately 23,000 co-workers are dedicated to uniting compelling IT products, services and solutions from 2,500+ best-in-class technology vendors. Their edge-to-cloud portfolio is anchored in some of the highest-growth technology segments including cloud, cybersecurity, big data/analytics, AI, IoT, mobility and everything as a service. - Credit facilities and ERP integration create significant switching costs

No meaningful new entrant has emerged in broadline distribution in decades. The last "new" entrants were regional players that were subsequently acquired by the majors.

2. Bargaining Power of Suppliers (Vendors): MODERATE-HIGH

Large vendors like Microsoft, HP, Dell, and Cisco hold significant pricing power. However, distributors provide essential reach to SMB customers that vendors cannot economically serve directly. The relationship is symbiotic: vendors need TD SYNNEX's logistics and market access; TD SYNNEX needs vendor products and programs.

3. Bargaining Power of Buyers (Resellers/Customers): MODERATE

Large VARs and MSPs have negotiating leverage, but switching costs exist—credit lines, systems integration, relationship histories, training certifications. TD SYNNEX's scale allows it to offer competitive pricing and financing that smaller distributors cannot match.

4. Threat of Substitutes: MODERATE (and rising)

The rise of hyperscaler marketplaces is dramatically reshaping the dynamics for distribution. AWS, Google Cloud and Microsoft are seeing tremendous growth in channel partner private offers for third-party vendors selling through their marketplaces, themselves becoming de facto distributors. AWS Marketplace is now, by this definition, a top 10 global IT distributor.

Direct-to-customer cloud models represent the most significant substitution threat. However, the complexity of multi-vendor solutions creates continued need for aggregation and integration services. TD SYNNEX is adapting by investing in its StreamOne cloud marketplace and positioning as a "solutions orchestrator" rather than a pure product distributor.

5. Competitive Rivalry: HIGH

TD Synnex overtook Ingram to become the world's largest IT distributor by sales when it formed via the merger of Tech Data and Synnex in 2021. The industry has consolidated into a duopoly at the top, with TD SYNNEX and Ingram Micro commanding the lion's share of global distribution. Thin margins intensify competitive pressure, but rational competitors generally avoid destructive price wars.

Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG ✅

As the largest IT distributor globally, TD SYNNEX benefits from: - Procurement leverage with vendors - Logistics and warehousing efficiencies that improve with volume - IT systems amortized across a massive transaction base - Credit underwriting capabilities that scale

2. Network Effects: MODERATE ✅

TD SYNNEX operates a two-sided marketplace: more vendors attract more resellers (who want one-stop shopping), and more resellers attract more vendors (who want maximum reach). The StreamOne cloud platform enhances ecosystem stickiness as partners integrate more deeply with TD SYNNEX's digital tools.

3. Counter-Positioning: LIMITED ❌

The distribution business model is well-understood. Competitors can (and do) replicate TD SYNNEX's strategies. There's no fundamental structural advantage that incumbents cannot copy.

4. Switching Costs: MODERATE ✅

Credit facilities and payment terms create lock-in. Systems integration with reseller ERP systems raises switching costs. Training and certification programs for partners build relationship stickiness. However, resellers often work with multiple distributors simultaneously, limiting the impact.

5. Branding: LIMITED ❌

This is a B2B business with limited brand power to end consumers. Relationships, pricing, and execution drive business—not brand equity.

6. Cornered Resource: LIMITED ❌

No exclusive vendor relationships exist. Human capital, while valuable, is portable.

7. Process Power: MODERATE ✅

Distributors are evolving into data-led organizations, with platforms powered by AI and analytics to support e-commerce, subscription and cloud models, integrated with vendors, partners and hyperscaler marketplaces to deliver automation at scale.

Decades of logistics optimization, sophisticated demand forecasting, and credit underwriting capabilities create process advantages that are difficult—but not impossible—to replicate.

Summary: Scale Economies and Network Effects are TD SYNNEX's primary "powers," with meaningful but secondary contributions from Switching Costs and Process Power. The business is defensible but not impregnable.

X. Bull vs. Bear Case

Bull Case

AI Infrastructure Catalyst: The accelerating buildout of AI infrastructure creates significant demand for the hardware, networking, and integration services that TD SYNNEX distributes and supports. The company's Destination AI program positions it to capture this opportunity.

Cloud Marketplace Growth: Worldwide end-user spending on public cloud services is forecast to total $723.4 billion in 2025, up from $595.7 billion in 2024, according to the latest forecast from Gartner, Inc. TD SYNNEX's cloud marketplace and "as-a-service" capabilities allow it to participate in this growth, not just be disrupted by it.

Duopoly Dynamics: Only two global-scale IT distributors remain. This oligopolistic structure generally supports rational competitive behavior and stable margins. But as the IT industry rapidly evolves, the competitive battleground is fast moving toward digital platforms, next-generation technologies, new business models and services.

Margin Expansion Potential: Post-merger synergies continue to be realized. The shift toward higher-margin Advanced Solutions and services creates operating leverage.

Essential Infrastructure: Technology spending continues to grow faster than GDP globally. Gartner experts forecast IT spending will reach $5.74 trillion globally. That's an impressive 9.3% increase over 2024. As a toll-booth on much of this spending, TD SYNNEX benefits from secular tailwinds.

Bear Case

Disintermediation Risk: Direct vendor-to-customer sales, especially through cloud marketplaces, threaten the traditional distribution model. If vendors decide they can reach customers more efficiently directly—or through hyperscaler marketplaces—distributors become less essential.

Thin Margins: The non-GAAP operating margin was 2.78% for fiscal 2024, down 7 bps compared with the previous year's reported figure. Operating margins of ~3% leave little room for error. Any significant cost increases or pricing pressure could dramatically impact profitability.

Cyclicality: Enterprise IT spending is sensitive to economic conditions. Recessions typically hit technology budgets, and distributors—with their thin margins and high inventory levels—feel the pain acutely.

Working Capital Intensity: The business requires substantial inventory and receivables financing. Rising interest rates increase the cost of this working capital.

Commodity Business: Beyond scale, there's limited differentiation in the core distribution business. Resellers often work with multiple distributors and chase the best price.

Key KPIs to Monitor

For investors tracking TD SYNNEX, three metrics matter most:

-

Gross Billings Growth: Because cloud services are often recognized net (revenue only reflects TD SYNNEX's margin, not the full transaction value), gross billings provide a better picture of business volume than reported revenue. Watch for gross billings growth relative to the overall IT market.

-

Non-GAAP Operating Margin: In a thin-margin business, small improvements in operating margin have outsized impacts on earnings. Track whether the company is maintaining discipline and achieving post-merger synergies.

-

Advanced Solutions Mix: The percentage of revenue and billings from higher-margin Advanced Solutions (cloud, cybersecurity, data/AI) versus lower-margin endpoint products indicates whether TD SYNNEX is successfully evolving from "box mover" to "solutions orchestrator."

XI. Epilogue: The Road Ahead

TD SYNNEX stands at an interesting inflection point. The company has successfully consolidated with its largest competitor, achieved unmatched scale, returned capital to shareholders, and positioned for the AI and cloud transition. But significant questions remain.

Can a distribution company transform into a "solutions orchestrator" that captures value in the AI era? Or will hyperscaler marketplaces and direct vendor sales gradually disintermediate traditional distribution? Can TD SYNNEX's thin-margin model generate adequate returns in a higher-interest-rate environment with elevated working capital costs?

The latest evolution of TD SYNNEX's AI program marks a clear shift in strategy—from enabling general awareness of AI technologies to facilitating structured, scalable implementation.

The company is betting that its unique position—connected to 2,500 vendors and 150,000 customers across 100+ countries—creates value that cannot be easily replicated. As AI makes technology more complex, not simpler, the argument goes, the need for aggregation, integration, and support actually increases.

That's precisely the opposite of what many industry observers predicted last decade as the rise of cloud computing and everything as a service rendered the warehousing and finance services that distributors were best known for less and less relevant. "I wouldn't want to be anybody who wrote an article on the death of distribution, because at this point they might look a little bit foolish," Robinson says.

Robert Huang started exporting computer parts from California in 1980. Edward Raymund was selling printer ribbons in Florida in 1974. Neither could have imagined that their businesses would eventually merge into a $60 billion global technology infrastructure company. But that's exactly what happened—through disciplined execution, strategic M&A, and the relentless pursuit of scale in a business where scale is everything.

The story of TD SYNNEX is a reminder that unsexy businesses can generate tremendous value over time. Not every great investment is a high-growth technology disruptor. Sometimes, the best opportunities are found in the infrastructure layers that make everything else possible—the distributors, the logistics providers, the behind-the-scenes operators that keep the technology industry running.

TD SYNNEX may be invisible to most consumers. But for investors willing to look beyond the glamour of the technology sector's marquee names, this invisible giant offers a fascinating case study in building durable competitive advantage through operational excellence, strategic M&A, and the patient accumulation of scale.

XII. Key Dates & Milestones

| Year | Event |

|---|---|

| 1974 | Edward Raymund founds Tech Data in Clearwater, Florida |

| 1980 | Robert Huang founds Compac Microelectronics (later SYNNEX) in California |

| 1986 | Tech Data goes public on NASDAQ |

| 1998 | Tech Data acquires Computer 2000 AG, expanding European presence |

| 2003 | SYNNEX goes public on NYSE |

| 2006 | SYNNEX acquires Concentrix for ~$8 million |

| 2013 | SYNNEX acquires IBM's worldwide BPO services business for $505 million |

| 2017 | Tech Data acquires Avnet Technology Solutions |

| 2018 | SYNNEX acquires Convergys for $2.43 billion, integrates with Concentrix |

| 2020 | Apollo acquires Tech Data for ~$6 billion |

| 2020 | SYNNEX spins off Concentrix |

| 2021 | SYNNEX and Tech Data merge, creating TD SYNNEX ($7.2 billion deal) |

| 2024 | Apollo fully exits TD SYNNEX through secondary offerings |

| 2024 | Patrick Zammit becomes CEO, succeeding Rich Hume |

Disclosure: This article is for informational purposes only and does not constitute investment advice. The author does not own shares in TD SYNNEX or any companies mentioned.

XIII. Further Reading & Resources

For investors and industry observers seeking deeper understanding of TD SYNNEX and the IT distribution landscape, several resources merit attention.

Primary Sources

TD SYNNEX Investor Relations provides comprehensive access to annual reports, SEC filings, earnings call transcripts, and investor presentations. The company's 10-K filings offer detailed breakdowns of segment performance, risk factors, and management's discussion of strategic priorities.

Direction of Technology Report: TD SYNNEX publishes this annual survey examining trends across the channel ecosystem. The report provides valuable insights into partner sentiment, technology adoption patterns, and emerging opportunities in areas like AI, cloud, and cybersecurity.

Industry AnalysisCanalys/Omdia (now combined as one entity) provides the industry's most comprehensive analysis of the distribution landscape. Their regular reports track distributor performance, market share dynamics, and evolving channel models. The global IT distribution market stood at US$463 billion in 2024, with the top 15 distributors generating sales of US$287 billion and commanding over 61% of the total.

Despite continued macroeconomic uncertainty and geopolitical turbulence, distribution is set for a stronger 2025, as the recovery in PCs and infrastructure gathers pace, while high-growth segments such as cybersecurity, cloud and software see increased momentum through the two-tier channel.

Analyst Coverage

TD SYNNEX receives coverage from multiple Wall Street analysts. The company has a consensus price target of $133 based on the ratings of 15 analysts, with the high at $165 issued by RBC Capital in February 2025 and the low at $90 issued by Credit Suisse in June 2023.

Analyst consensus remains cautiously bullish, with 80% of analysts retaining "buy" ratings, citing the company's 193% five-year total shareholder return (including dividends) as proof of its durable business model.

Industry Publications

CRN (Computer Reseller News) and Channel Futures provide ongoing coverage of the IT channel ecosystem, including distributor strategies, vendor programs, and partner sentiment. These publications offer ground-level perspectives on how distributors like TD SYNNEX serve their reseller communities.

Academic and Strategic Frameworks

For readers interested in the theoretical underpinnings of TD SYNNEX's competitive position, Michael Porter's "Competitive Strategy" and Hamilton Helmer's "7 Powers: The Foundations of Business Strategy" provide useful analytical frameworks. This article has applied both to TD SYNNEX's business model; readers may find value in exploring these frameworks in greater depth.

XIV. Conclusion: The Invisible Infrastructure That Makes Technology Possible

TD SYNNEX represents a peculiar kind of business success story—one built not on breakthrough innovation or charismatic founders, but on operational excellence, disciplined capital allocation, and the patient accumulation of scale in an unglamorous industry.

From Robert Huang's computer parts export business in California to Edward Raymund's printer ribbon company in Florida, the journeys that converged to create TD SYNNEX span five decades of technology industry evolution. Along the way, both companies survived near-death experiences, made bold strategic bets, and ultimately recognized that in distribution, scale is destiny.

The company's recent financial performance validates this thesis. In Q3 2025, non-GAAP diluted earnings per share soared 25% year-over-year to $3.58, supported by a 26.7% year-over-year increase in operating income to $383.7 million and gross margin expansion to 7.22%—a 68-basis-point improvement. Advanced Solutions non-GAAP gross billings grew by 12% year-over-year to $12.8 billion, while Endpoint Solutions increased by 13% to $8.8 billion.

The company has made significant progress in growing strategic technologies from 17% of non-GAAP gross billings in FY 2021 to 28% in Q2 FY25. This shift toward higher-value segments—cloud, security, data, AI, and hyperscale infrastructure—reflects management's understanding that the company must evolve beyond traditional "box moving" to remain relevant.

In 2025, industry observers expect TD SYNNEX and Arrow to gain market share in federal distribution, as the sector diversifies amid increased competition. The federal channel represents a significant growth opportunity, particularly as government agencies invest in AI and cybersecurity infrastructure.

The competitive landscape remains dynamic. Global spending on cloud infrastructure services reached US$95.3 billion in Q2 2025, up 22% year-on-year, with market momentum remaining stable and year-on-year growth exceeding 20% for the fourth consecutive quarter. This cloud spending surge presents both opportunity and threat for TD SYNNEX—opportunity to the extent the company captures cloud-related distribution; threat to the extent hyperscaler marketplaces disintermediate traditional distribution.

The question that will define TD SYNNEX's next chapter is whether the company can complete its transformation from product distributor to solutions orchestrator. The Destination AI program, the StreamOne cloud marketplace, and investments in technical services all point in this direction. But execution remains the challenge.

For investors, TD SYNNEX offers exposure to the essential infrastructure of the technology industry at a valuation that reflects its "boring" business model rather than its strategic importance. The company's scale advantages, disciplined capital allocation, and positioning in high-growth technology segments create a defensible business that generates consistent cash flows and returns capital to shareholders.

Robert Huang once described his Japanese management training as emphasizing "attention to detail and frugality." Those values—decidedly unsexy in an industry obsessed with disruption and moonshots—built a company that now touches virtually every technology purchase on the planet. In an age of hype and hyperbole, TD SYNNEX offers a reminder that durable value creation often comes not from the brilliant flash of innovation, but from the steady accumulation of small advantages over decades.

The invisible giant of the IT supply chain remains, as it has been for 45 years, quietly indispensable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube