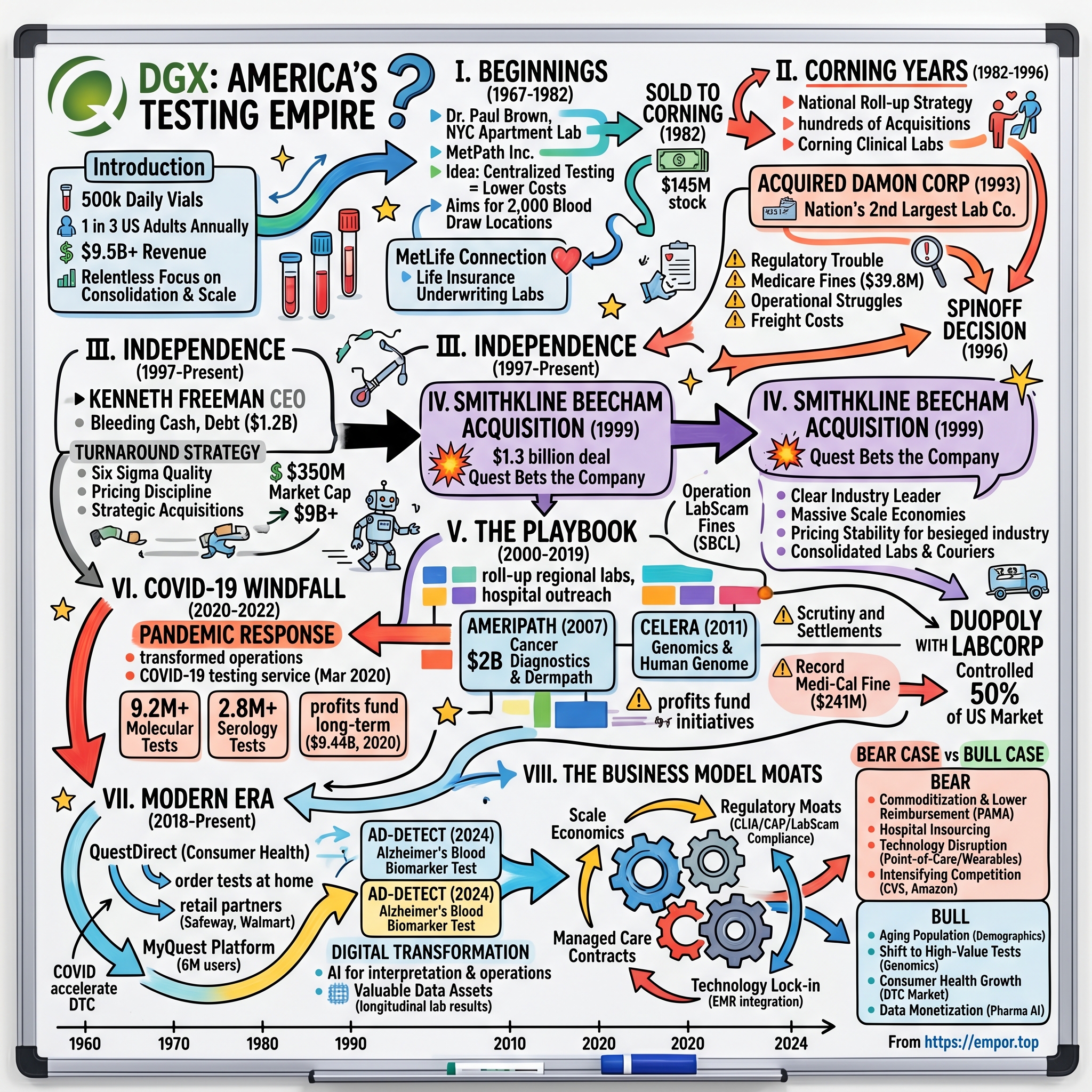

Quest Diagnostics: From Insurance Lab to America's Testing Empire

I. Introduction & Episode Setup

Picture this: A nurse in suburban Kansas draws blood from a patient at 7 AM. By noon, that vial has traveled through a logistics network more sophisticated than FedEx, been processed by robots that would make Tesla jealous, and generated results accessible to doctors across three different hospital systems. This happens 500,000 times every single day at Quest Diagnostics facilities across America.

The company touches one in three American adults annually—a staggering 26% market share that makes it the undisputed king of clinical diagnostics. With over $9.5 billion in annual revenue and a market cap north of $20 billion, Quest has built one of healthcare's most durable monopolies. Yet most investors can't explain how a two-bedroom Manhattan apartment laboratory became the testing empire that processes everything from routine cholesterol panels to cutting-edge Alzheimer's biomarkers.

Here's what makes this story fascinating: Quest didn't invent any breakthrough technology. They didn't have a charismatic founder with a reality distortion field. What they had was something far more powerful—a relentless focus on consolidation, scale economics, and operational excellence in an industry everyone else ignored. While Silicon Valley chased the next Theranos-style disruption, Quest quietly built an unassailable moat through 400+ acquisitions, turning the messy, fragmented world of medical testing into a streamlined duopoly.

The timing couldn't be more relevant. As healthcare shifts toward prevention, personalized medicine explodes, and AI transforms diagnostics, Quest sits at the intersection of every major trend. They're not just running blood tests—they're sitting on one of healthcare's most valuable data assets, with longitudinal lab results for tens of millions of Americans.

This is the story of how insurance company bureaucrats built a healthcare colossus, why the boring business of blood testing generates software-like margins, and what happens when an industry consolidates from 20,000 players to essentially two. It's about network effects in test tubes, regulatory moats measured in decades, and why your doctor probably doesn't have a choice about where to send your lab work.

II. Origins: The MetPath Beginning (1967-1982)

The year was 1967, and Dr. Paul Brown had a problem. As a pathologist working with New York hospitals, he watched as lab results took days or even weeks to process. Errors were common, costs were astronomical, and hospitals were drowning in inefficiency. Brown's solution seemed almost quaint by today's standards: he rented a two-bedroom apartment on Manhattan's Upper East Side, installed some basic lab equipment, and incorporated Metropolitan Pathology Laboratory, Inc.—MetPath for short.

What Brown understood, and what would become Quest's founding insight, was that laboratory testing was fundamentally a scale business masquerading as a medical service. Every hospital running its own lab was like every household generating its own electricity—theoretically possible, but economically insane. By centralizing testing, Brown could spread fixed costs across more samples, invest in better equipment, and deliver faster, more accurate results at lower prices.

The connection to Metropolitan Life Insurance Company wasn't accidental. Met Life had been running clinical labs since the 1890s as part of their life insurance underwriting process—they needed to know if applicants were healthy before writing policies. By the 1960s, they had one of the most sophisticated lab operations in the country, processing hundreds of thousands of tests annually. When regulatory changes made it harder for insurance companies to own clinical labs directly, Met Life's lab business needed a new home. Enter Dr. Brown and his apartment laboratory. Brown started with just $500 and was "amazed at the sky-high test prices charged by hospitals and clinics." In those early days, pap slides were stained on top of a bathtub—a far cry from today's automated systems that can process millions of samples. But Brown had a grander vision. Despite these humble beginnings, his early vision was to have labs in major cities and 2,000 blood draw locations—remarkably prescient given Quest operates roughly 2,200 patient service centers today.

The genius of Brown's approach was recognizing that diagnostic testing wasn't really a medical business—it was a logistics and scale business wrapped in a lab coat. While hospitals saw testing as a necessary evil, Brown saw it as an opportunity to apply industrial efficiency to healthcare. By 1969, he'd renamed the company MetPath and moved operations to Teaneck, New Jersey, where he could build out proper laboratory infrastructure.

By 1975, MetPath had one of the best equipped and largest medical laboratories in the world, offering more than 600 laboratory tests in 11 cities and performing more than two million lab tests a month. The tests were processed at a highly automated central laboratory in Hackensack, New Jersey, with 80% of results delivered within 24 hours after collection. The economics were revolutionary: MetPath's average billing per patient transaction was only $9, while hospitals routinely charged three to five times that amount.

The growth trajectory was staggering. By 1979, MetPath was challenging Damon Corp. for first place in the clinical laboratory testing field. The company had net income of $3.8 million in fiscal 1978 on revenues of $53.4 million. Brown had built something unprecedented: A new $25 million laboratory in Teterboro, New Jersey, completed in 1978, was easily the industry's largest and capable of analyzing up to 30,000 samples a day. Fifty local offices made daily collections, shipping them via same-day air freight to the laboratory, with results transmitted to telecommunications terminals.

But success brought its own challenges. MetPath had acquired small testing laboratories throughout the country and built a second clinical laboratory near Chicago's O'Hare Airport. The expansion raised the company's debt so precipitously that in 1982 it was sold to Corning Glass Works for stock worth about $145 million. Brown had built the foundation of what would become Quest, but he'd also discovered a fundamental truth about the diagnostics business: scale requires capital, and capital requires partners with deep pockets.

III. The Corning Years: Building a National Network (1982-1996)

When Corning Glass Works acquired MetPath in 1982, they weren't just buying a laboratory—they were buying a vision of what healthcare could become. Corning saw in MetPath what others missed: a platform for rolling up a fragmented industry that was ripe for consolidation. The timing was perfect. Medicare funding was exploding, malpractice suits were driving defensive medicine, and managed care was just beginning to demand cost control. Corning had the capital, the management expertise, and most importantly, the patience to build something massive.

The acquisition strategy was breathtaking in its ambition. By 1994, Corning Clinical Laboratories accounted for $1.7 billion of the parent company's $4.8 billion in sales and was the nation's largest clinical laboratory company. This wasn't organic growth—this was empire building through hundreds of acquisitions, methodically buying up regional labs, specialty testing companies, and hospital outreach programs across the country.

The crown jewel of this acquisition spree came in 1993 when Corning acquired Damon Corp., the nation's fifth largest owner of clinical testing laboratories, with 14 in the United States and one in Mexico and about 220 satellite labs in remote U.S. locations. This made Corning Lab Services the nation's second largest laboratory testing company. The Damon acquisition was particularly strategic—it gave Corning instant scale in markets where they had been weak, and more importantly, it eliminated a major competitor who had been struggling financially after a leveraged buyout.

But growth came with growing pains. The regulatory environment was becoming increasingly hostile to aggressive billing practices that had been industry standard for decades. MetPath and Metwest—a California-based spinoff from MetPath—agreed in 1993 to pay the federal government $39.8 million to settle charges that they had submitted Medicare claims for unnecessary blood tests. In 1995 Corning Clinical Laboratories agreed to pay the federal government $8.6 million for tests that doctors never ordered.

These weren't just fines—they were warning shots. The government was signaling that the Wild West days of laboratory billing were over. The industry's dirty secret was that many labs had been running panels of tests when doctors ordered just one or two, then billing Medicare for everything. It was technically efficient from a laboratory perspective—if you're already analyzing a blood sample, why not run every test possible? But it was also fraudulent from a billing perspective.

The operational challenges were equally daunting. Although MetPath remained autonomous and its revenue kept growing, the company found itself overwhelmed by freight costs. It also had lost business to smaller labs as testing equipment became smaller and more affordable. The very centralization that had been MetPath's strength was becoming a weakness as technology democratized testing capabilities.

Corning's response was to transform the entire operating model. Instead of one or two mega-labs, they built a network of regional laboratories that could serve local markets more efficiently. This reduced freight costs, improved turnaround times, and made the company more responsive to local physician needs. It was a massive undertaking—essentially rebuilding the entire infrastructure while maintaining operations.

Despite net revenues of $1.63 billion in 1995, Corning Clinical Laboratories lost $52.1 million, after the parent company took a charge of $62 million to increase accounts receivable because of the billings problems. Moreover, Corning Clinical Laboratories' long-term debt reached almost $1.2 billion. The integration of hundreds of acquisitions had created a billing nightmare. Each acquired lab had its own systems, processes, and relationships with insurers. Consolidating all of this into a single, compliant billing operation was like performing surgery on a patient while they're running a marathon.

By 1996, Corning had had enough. In 1996 Corning decided to spin off its laboratory testing and pharmaceutical services businesses to shareholders, creating two independent public companies. The laboratory testing business became Quest Diagnostics Inc. Corning, on the last day of 1996, distributed all outstanding shares of common stock of the new company to Corning stockholders, with one share distributed for each eight shares of Corning.

The spinoff wasn't an admission of failure—it was a recognition that the laboratory business needed focused leadership and a dedicated capital structure. Corning had built something remarkable: a national laboratory network with unmatched scale and capabilities. But they'd also created a complex beast that needed its own identity and strategy to thrive in an increasingly challenging healthcare environment. The stage was set for Quest Diagnostics to emerge as an independent powerhouse.

IV. Independence & The Freeman Era (1997-1999)

January 1, 1997. Quest Diagnostics was born—not with fanfare, but with crisis. On December 31, 1996, Quest Diagnostics became an independent company as a spin-off from Corning. Kenneth W. Freeman was appointed as CEO during this transition. The company Freeman inherited was bleeding cash, burdened with nearly $1.2 billion in debt, and had just posted a $626 million loss. Wall Street valued the entire enterprise at just $350 million—less than the cost of a single modern laboratory facility.

Freeman wasn't the obvious choice. A career Corning executive who'd spent most of his time in financial and operational roles, he'd only joined Corning Clinical Laboratories in May 1995. But Freeman had something more valuable than industry experience: he understood turnarounds. And he understood that Quest's problems weren't technical—they were cultural and strategic.

"I wanted to take a company that was hostile and hierarchical, and not particularly disciplined, and create a values-oriented, honest, disciplined company where the people respected each other," Freeman would later reflect. The company he inherited was a Frankenstein's monster of hundreds of acquisitions, each with its own systems, cultures, and ways of doing business. Physician complaints were rampant. Billing was a disaster. Employee morale was in the basement.

Freeman's first move was counterintuitive: instead of cutting costs, he invested in quality. He implemented Six Sigma throughout the organization—not as a cost-cutting exercise, but as a way to rebuild trust with physicians. Every error, every delayed result, every billing mistake was tracked, analyzed, and systematically eliminated. It was expensive, time-consuming, and initially made financial results worse. But Freeman understood that without operational excellence, nothing else mattered.

The second pillar of Freeman's strategy was pricing discipline. The industry had been in a race to the bottom, with labs undercutting each other to win managed care contracts. Freeman took a different approach: Quest would compete on quality and service, not price. "Over the past five years, Surya Mohapatra has been my closest partner in developing and executing our business strategy, from driving Six Sigma quality to raising our commitment to pricing discipline and introducing new tests and technologies," Freeman would later say about his partnership with his eventual successor.

But Freeman's boldest move was his acquisition strategy. While the company was still struggling to integrate Corning's hodgepodge of acquisitions, Freeman was already planning the deal that would transform the industry. Quest acquired a clinical laboratory division of Branford, Connecticut–based Diagnostic Medical Laboratory, Inc. (DML) in 1997, demonstrating that even in turnaround mode, the company could execute strategic acquisitions.

The real prize, however, was SmithKline Beecham Clinical Laboratories (SBCL). As one of the "Big Three" national labs alongside Quest and LabCorp, SBCL controlled roughly 20% of the U.S. clinical laboratory market. The company had been built through aggressive acquisition but was struggling with integration and facing its own operational challenges. SmithKline Beecham, the pharmaceutical parent, wanted out of the diagnostics business to focus on drug development.

Freeman saw opportunity where others saw risk. Acquiring SBCL would instantly make Quest the undisputed industry leader, create massive economies of scale, and most importantly, give Quest the leverage to rationalize pricing in the industry. But pulling off such a deal while Quest was still in turnaround mode would require financial engineering, operational excellence, and perfect execution.

He led the dramatic turnaround of Quest Diagnostics as chairman and chief executive officer through 2004. Exceptional value was created for shareholders by executing a dramatic financial turnaround, establishing industry leadership, demonstrating effective growth through acquisition, and driving organic growth. Quest Diagnostics provided the third highest five-year shareholder returns among the Fortune 500 (1999-2003). Market capitalization increased from approximately $350 million at the time of the spin-off to more than $9 billion.

The transformation was already showing results. By 1998, just two years after independence, Quest had stabilized operations, improved service levels, and begun generating positive cash flow. Wall Street was taking notice—the stock had more than doubled from its spin-off lows. But Freeman knew this was just the beginning. The real test would come with the SmithKline Beecham acquisition, a deal that would either establish Quest as the industry's dominant force or destroy the fragile turnaround Freeman had engineered.

V. The SmithKline Beecham Acquisition: Industry Transformation (1999)

The phone call came on a Friday afternoon in February 1999. Jan Leschly, CEO of SmithKline Beecham, wanted to talk. The pharmaceutical giant was ready to divest its clinical laboratory business, and they wanted to move fast. For Freeman and Quest, this was the opportunity of a lifetime—and potentially a company-ending disaster if executed poorly.

Quest Diagnostics Incorporated announced that it had completed the acquisition of the clinical laboratory operations of SmithKline Beecham plc for approximately $1.3 billion in cash and stock—a staggering sum for a company that had been valued at just $350 million three years earlier. The deal structure was audacious: $1 billion in cash plus stock, at a time when Quest's entire market cap was barely $2 billion. Freeman was essentially betting the company.

The strategic logic was compelling. SmithKline Beecham Clinical Laboratories (SBCL) was an American-based medical laboratory company that was acquired by Quest Diagnostics in 1999 for $1.3 billion. SBCL brought 28 major laboratories, 900 patient service centers, and most importantly, relationships with thousands of physicians and managed care organizations that Quest couldn't reach. The combined entity would have revenues exceeding $3 billion, making it far larger than any competitor.

But SBCL came with baggage. In 1989, SBCL had to pay a $1.5 million fine for illegal laboratory referral kickbacks. In 1997, Operation LabScam forced SBCL to agree to pay a $325 million settlement for billing Medicare and Medicaid for tests that physicians were misled into believing were free. The regulatory scrutiny was intense, and Quest would inherit all of SBCL's compliance challenges.

The negotiation drama was worthy of a thriller. Freeman had to convince Quest's board to approve the largest acquisition in laboratory history while the company was still recovering from its spin-off. He needed to secure $1 billion in financing at favorable terms. And he had to do it all while maintaining operational performance and keeping the deal secret from competitors, particularly LabCorp, who would surely try to disrupt the transaction if they knew.

The financing was particularly creative. Quest issued convertible preferred stock to SmithKline Beecham, giving the pharmaceutical company a significant stake in the combined entity. This aligned interests—SmithKline wanted Quest to succeed—while preserving cash for integration costs. The deal also included complex earn-outs and performance metrics that would determine the final purchase price.

"Starting today, the new Quest Diagnostics is the clear industry leader in diagnostic testing, information and services, well positioned for profitable growth," said Kenneth W. Freeman. But Freeman knew the real work was just beginning. Integration would make or break the combined company.

The integration challenge was unprecedented. Quest was essentially doubling in size overnight, combining two companies with different systems, cultures, and operational approaches. Freeman's approach was ruthlessly systematic. He ran a selection process where all 200 senior leaders had to undergo an independent assessment to determine who would get the top jobs. There would be no "winners" and "losers" based on prior affiliation—only the best would survive.

Quest Diagnostics' agreement to buy SmithKline Beecham Clinical Labs brings together two of the three largest clinical labs in the country and makes Quest the largest reference laboratory in the country. Quest hopes to expand its national presence, better manage costs, capitalize on both companies' information expertise and bring a measure of pricing stability to a besieged industry.

The market implications were profound. Before the acquisition, the laboratory industry was locked in a destructive price war. Three roughly equal competitors—Quest, SBCL, and LabCorp—were undercutting each other to win managed care contracts. With Quest now controlling nearly 30% of the market, the dynamics changed completely. Quest could enforce pricing discipline, refuse unprofitable contracts, and force the entire industry toward more rational economics.

The operational synergies were even more impressive than the strategic benefits. By consolidating overlapping laboratories, Quest could eliminate billions in redundant costs. Route density improved dramatically—instead of three different companies sending couriers to the same medical office building, Quest could serve all clients with a single pickup. Laboratory utilization increased, spreading fixed costs over more tests and improving margins.

On February 9, 1999, Quest Diagnostics Incorporated signed an agreement to purchase SmithKline Beecham Clinical Laboratories (SBCL). It was the largest laboratory acquisition up to that point. The acquisition transformed not just Quest, but the entire diagnostics industry. It proved that scale mattered, that consolidation could create value, and that the fragmented laboratory market was ripe for further rollup. For Freeman and Quest, it was vindication of their strategy. For competitors, it was a wake-up call that the industry would never be the same.

VI. The Consolidation Playbook (2000-2019)

The boardroom at Quest's Lyndhurst headquarters was buzzing with nervous energy on April 16, 2007. Surya Mohapatra, who had succeeded Freeman as CEO in 2004, was about to announce the company's boldest acquisition since SmithKline Beecham: Quest Diagnostics has signed a definitive agreement to acquire AmeriPath in an all cash transaction valued at approximately $2 billion, including approximately $770 million in debt at closing.

AmeriPath represented something different for Quest—a move beyond traditional clinical testing into the high-margin, high-growth world of anatomic pathology and cancer diagnostics. AmeriPath, a company controlled by Welsh, Carson, Anderson and Stowe IX, L.P., is a leading provider of dermatopathology, anatomic pathology and esoteric testing with annualized revenues in excess of $800 million.

"This acquisition will establish our leading position in cancer diagnostics with a focus on dermatopathology, anatomic pathology and molecular diagnostics," said Surya N. Mohapatra. The strategic logic was compelling: cancer diagnostics was growing at double-digit rates, driven by an aging population and advances in personalized medicine. Dermpath Diagnostics has an industry-leading team of over 80 board-certified dermatopathologists who interpret 2.4 million biopsies annually.

But the AmeriPath deal was just the beginning of Quest's consolidation playbook. Over the next decade, the company would execute dozens of acquisitions, each carefully chosen to either expand geographic reach, add new testing capabilities, or strengthen relationships with key customer segments. The Celera acquisition in 2011 marked Quest's bold entry into genomics. Quest Diagnostics announced today the successful completion of its acquisition of Celera Corporation for $8 per share, representing a transaction value of approximately $344 million, net of $327 million in acquired cash and short-term investments. Celera sequenced the human genome at a fraction of the cost of the publicly funded Human Genome Project, using about $300 million of private funding versus approximately $3 billion of taxpayer dollars.

The playbook Quest developed during this period was remarkably consistent: identify fragmented segments of the diagnostics market, acquire the leading players, consolidate operations, and leverage scale to improve margins. Hospital outreach became a particular focus. Rather than competing with hospitals, Quest partnered with them, taking over their money-losing lab operations and converting them into profit centers.

The strategy wasn't without risks. Quest Diagnostics set a record in April 2009 when it paid $302 million to the government to settle a Medicare fraud case alleging the company sold faulty medical testing kits. In May 2011, Quest paid $241 million to the state of California to settle a False Claims Act case that alleged the company had overcharged Medi-Cal and provided illegal kickbacks.

These settlements were painful but instructive. Quest learned that scale brought scrutiny, and that compliance had to be built into every acquisition from day one. The company developed sophisticated compliance systems, invested heavily in billing accuracy, and made regulatory expertise a core competency.

Meanwhile, the duopoly with LabCorp was becoming increasingly entrenched. Quest accounted for the largest share of the esoteric testing market in 2023, with the two companies controlling roughly 50% of the U.S. clinical laboratory market between them. This concentration created enormous barriers to entry—new competitors couldn't match the route density, couldn't negotiate comparable reimbursement rates, and couldn't afford the regulatory infrastructure required to operate at scale.

The technology investments during this period were equally strategic. Quest built one of healthcare's most sophisticated IT infrastructures, connecting thousands of physician offices, hospitals, and health systems. This wasn't just about efficiency—it was about creating switching costs. Once a physician's office was integrated with Quest's systems, changing labs became a major operational headache.

By 2019, Quest had executed over 400 acquisitions since its founding, transforming from a single lab in Manhattan to a national network processing over 150 million requisitions annually. The consolidation playbook had worked brilliantly, creating a business with software-like margins in what was ostensibly a commodity service. But the world was about to change dramatically, and Quest would face its biggest test—and opportunity—yet.

VII. The COVID-19 Windfall & Transformation (2020-2022)

March 2020. The world stopped, but Quest's laboratories couldn't. Within days of the WHO declaring a pandemic, Quest's phone lines were overwhelmed with desperate calls from hospitals, governments, and physicians. The company that had spent decades building infrastructure for routine testing was suddenly America's frontline defense against an invisible enemy.

Steve Rusckowski, Quest's CEO since 2012, faced an unprecedented challenge. In March 2020, the company launched a COVID-19 testing service. But launching was one thing—scaling was another. Quest needed to transform its entire operation overnight, converting routine testing capacity to COVID diagnostics while maintaining essential services for cancer patients, transplant recipients, and other critical cases.

The numbers tell a story of explosive growth: As of July 2020, Quest had performed more than 9.2 million COVID-19 molecular tests and 2.8 million serology tests. By the fourth quarter of 2020, the transformation was complete. The company reported net revenues of more than $3 billion for the quarter ended Dec. 31, up almost 56% from $1.93 billion during the same period in 2019.

"In a year dominated by the pandemic, Quest brought critical COVID-19 testing to our country, and delivered record revenues, earnings and cash from operations for the fourth quarter and full year 2020," Rusckowski said. The full year revenues of $9.44 billion, up 22.1% from 2019, represented the largest single-year growth in Quest's history.

But this wasn't just about running more tests. Quest had to completely reimagine its logistics network. The company's fleet of couriers, which normally collected routine samples, became a critical piece of pandemic infrastructure. New biosafety protocols had to be implemented across thousands of patient service centers. Laboratory workers became essential heroes, working double shifts to process the tsunami of samples.

The operational challenges were staggering. Quest and other major diagnostic labs were at the center of scrutiny over the summer, when demand for COVID-19 testing services rose dramatically amid a resurgence of infections across parts of the country, particularly the Sun Belt. Turnaround times stretched to 7-10 days during peak periods, rendering tests nearly useless for contact tracing. Political pressure mounted as the Trump administration blamed labs for testing delays.

Quest's response was to throw money at the problem—and it worked. The company invested hundreds of millions in new equipment, hired thousands of workers, and opened dedicated COVID testing facilities. By Q4 2020, Quest's CFO Mark Guinan said the company conducted 12.5 million COVID-19 molecular tests in the fourth quarter and about 1 million serology tests.

The financial windfall was extraordinary. Operating margins expanded dramatically as Quest leveraged its fixed infrastructure across massive testing volumes. The company's stock price surged, and Rusckowski announced the company would increase its dividend by 10.7% to 62 cents per quarter and authorize a $1 billion increase in its share repurchase plan.

But Quest's leadership knew this was temporary. "We did see that in Q1 and we see it happening in the country," Rusckowski said about declining PCR test demand as vaccines rolled out. The company's strategic response was brilliant: use COVID profits to accelerate long-term initiatives that had been on the drawing board for years.

Quest invested heavily in advanced diagnostics, genetic testing, and most importantly, direct-to-consumer capabilities. With the pandemic accelerating interest in consumer-initiated testing, Quest expanded its existing direct-to-consumer operations in an effort to capture $250 million of the emerging DTC market, which it estimates will be worth $2 billion by 2025.

The decline came faster than expected. By Q3 2022, Quest reported Covid-19 testing revenue decline about 55% to $316 million. Revenue from Quest's base business, however, grew by about 5% to $2.17 billion from $2.06 billion, driven by high volumes of non-Covid testing. The company had successfully managed the transition from COVID windfall back to normal operations—but "normal" was now different.

CEO-elect Jim Davis said during a Thursday earnings call that the company had seen some of the highest base testing volumes in its history for non-Covid-related tests. The pandemic had fundamentally changed consumer behavior. People were more health-conscious, more willing to get tested, and more comfortable with at-home collection. Quest had used the COVID crisis not just to generate profits, but to accelerate a transformation that might have taken a decade otherwise.

VIII. Modern Era: Consumer Health & Digital Transformation (2018-Present)

In November 2018, Quest launched QuestDirect, a consumer-initiated testing service that allows patients to order health and wellness lab testing from home. The timing seemed odd—why would a B2B laboratory company suddenly pivot to consumers? But Steve Rusckowski and his team saw something others missed: the healthcare system was about to be disrupted, and Quest could either be the disruptor or the disrupted.

"Quest has long been a pioneer in consumer health and an advocate of empowering consumers with diagnostic insights," said Steve Rusckowski. The launch represented a fundamental shift in Quest's business model. For fifty years, the company had sold exclusively through physicians. Now, it was going directly to consumers with 35 test packages including general health, men's and women's health, digestive health, heart health, infectious disease and sexually transmitted disease testing.

The strategy was controversial internally. Sales teams worried about alienating physician customers. Legal worried about liability. Operations worried about complexity. But Rusckowski pushed forward, understanding that consumer behavior was changing faster than the healthcare system could adapt.

Quest's approach was deliberately different from Silicon Valley disruptors like Theranos (which had spectacularly imploded) or newer entrants like Everlywell. Quest wasn't trying to bypass the healthcare system—it was trying to supplement it. Every QuestDirect test included physician oversight and the option for telehealth consultation. Results were delivered through MyQuest, the company's patient platform used by six million people, and could be easily shared with the patient's regular physician.

The retail partnerships were equally strategic. The company further expanded convenient access to testing services through its recent collaborations with Safeway and Walmart, and expects to have well over 200 patient service centers in retail store locations by the end of 2018. This wasn't just about convenience—it was about normalizing laboratory testing as a routine part of health maintenance, like picking up vitamins at the pharmacy.

Then COVID hit, and everything accelerated. Quest set up QuestDirect in 2018 but the service came of age last year as non-coronavirus revenue doubled. Factoring in COVID-19 tests, sales increased by eight times. Quest has sold more than 30,000 tests for active COVID-19 infections and 280,000 antibody kits. Suddenly, consumers who had never heard of direct-to-consumer testing were ordering COVID tests online and collecting samples at home.

The pandemic didn't just drive volume—it changed consumer expectations permanently. People expected to order tests online, get results on their phones, and consult with physicians via video. Quest was perfectly positioned to capitalize on this shift. With COVID-19 pandemic accelerating interest in telehealth and consumer-initiated testing, Quest is expanding its existing DTC operation to try to capture $250 million of the emerging market, which Quest estimates will be worth $2 billion by 2025.The future arrived in April 2024 when Quest has added a new blood screening to their AD-Detect product line. This test will analyze the blood for a specific Alzheimer's protein, pTau-217. Quest Diagnostics announced the launch of a new blood biomarker test for phosphorylated tau 217, a biomarker associated with Alzheimer's Disease, supported by research as useful for an early diagnosis of AD.

This wasn't just another test—it was Quest positioning itself at the forefront of one of healthcare's most pressing challenges. With 6 million Americans suffering from Alzheimer's and no cure in sight, early detection through blood testing could revolutionize treatment. The test is the latest addition to the AD-Detect™ portfolio of blood tests for assessing the risk of Alzheimer's Disease, which also includes testing for an array of AD biomarkers.

The strategic brilliance was in the execution. Rather than developing tests in isolation, Quest built an entire ecosystem. Patients could order tests through QuestDirect, get blood drawn at any of Quest's 2,000 patient service centers, receive results through MyQuest, and consult with physicians via telehealth. The AD-Detect test lists for $399—expensive for consumers but a fraction of the cost of PET scans or spinal fluid analysis.

The competition from Silicon Valley was intensifying. Companies like Color, Everlywell, and dozens of venture-backed startups were trying to disrupt the diagnostics industry. But Quest had advantages they couldn't match: regulatory expertise built over decades, a physical infrastructure spanning the country, and most importantly, trust. The survey data show 26% of people name Quest when asked to list places they can go to receive lab tests—far ahead of any competitor.

The digital transformation extended beyond consumer testing. Quest was building sophisticated AI and machine learning capabilities to improve test interpretation, predict disease patterns, and optimize operations. The company's database—containing decades of test results for hundreds of millions of Americans—was becoming one of healthcare's most valuable assets. Pharmaceutical companies paid millions to access anonymized data for drug development. Health systems used Quest's analytics to identify at-risk populations.

But perhaps the most radical transformation was in Quest's business model itself. The company was evolving from a fee-for-service laboratory to a data and insights company that happened to run labs. Direct-to-consumer revenue was growing at double-digit rates. Subscription services for chronic disease monitoring were being piloted. Partnerships with tech companies were bringing laboratory testing to smartphones and wearables.

By 2024, Quest had successfully navigated the post-COVID transition while positioning itself for the future of healthcare. The company that started in a Manhattan apartment processing basic blood tests was now at the forefront of precision medicine, offering everything from whole genome sequencing to AI-powered disease prediction. The transformation was complete, but the journey was far from over.

IX. Playbook: The Quest Business Model

The Quest business model is deceptively simple: collect samples, run tests, deliver results. But beneath this simplicity lies one of healthcare's most sophisticated operational machines, generating software-like margins from what appears to be a commodity service. Understanding how Quest makes money—and more importantly, how it defends those profits—reveals why the company has dominated American diagnostics for decades.

Start with the economics of a single test. When a doctor orders a basic metabolic panel, the actual cost of reagents and supplies might be $2-3. The labor to process it, another $2-3. Overhead allocation, maybe $5. So Quest's all-in cost might be $10 for a test that bills to insurance at $50-100. These aren't exact numbers—Quest guards its cost structure carefully—but the margins are undeniable. The company consistently generates EBITDA margins north of 20%, remarkable for what's ostensibly a service business.

Scale is the first moat. Quest processes over 150 million requisitions annually across its network of laboratories. This volume allows the company to negotiate reagent prices that smaller labs can't touch. A regional laboratory buying 10,000 test kits pays multiples of what Quest pays for millions. The company's purchasing power extends to everything from needles to IT systems, creating a cost advantage that compounds with every acquisition.

Route density is the second moat, and perhaps the most underappreciated. Quest operates roughly 2,200 patient service centers and employs thousands of phlebotomists and couriers. The economics here are fascinating: the first stop on a courier route might lose money, the second breaks even, but by the tenth stop, the marginal cost approaches zero. A Quest courier picking up samples from a medical building with twenty physician offices has radically different economics than a competitor serving just two or three. This density creates a virtuous cycle—more stops mean lower costs, which enables competitive pricing, which attracts more customers, which increases density.

The third moat is regulatory. Quest maintains certifications from the Clinical Laboratory Improvement Amendments (CLIA), College of American Pathologists (CAP), and dozens of state agencies. Each certification requires extensive documentation, regular inspections, and sophisticated quality systems. But more importantly, Quest's history of regulatory settlements—painful as they were—has forced the company to build compliance infrastructure that new entrants can't replicate. The company employs hundreds of regulatory specialists, maintains detailed audit trails for billions of tests, and has developed proprietary systems for billing compliance that took decades to perfect.

Managed care contracting represents the fourth moat. Quest has contracts with essentially every major insurance company in America. These aren't simple fee schedules—they're complex agreements covering thousands of tests, with different rates for different markets, elaborate performance metrics, and multi-year terms. The negotiation leverage here is extraordinary. Insurance companies need a national laboratory network to serve their members. Only Quest and LabCorp can provide that. This creates a bilateral monopoly where both sides need each other, resulting in stable, predictable pricing that's largely insulated from competitive pressure.

The technology moat is evolving but increasingly important. Quest's laboratory information systems connect to thousands of electronic health records, practice management systems, and hospital networks. Once a physician's office is integrated with Quest's ordering system, switching becomes a massive operational headache. The company processes millions of electronic orders daily, each one creating switching costs and customer lock-in.

Capital allocation at Quest follows a predictable pattern. The company generates roughly $1.5 billion in free cash flow annually. About a third goes to dividends, another third to share buybacks, and the final third to acquisitions. This balanced approach has created tremendous shareholder value while maintaining flexibility for strategic moves. The acquisition strategy is particularly disciplined—Quest typically pays 8-12x EBITDA for targets, integrates them within 18-24 months, and achieves cost synergies of 20-30% through elimination of redundant infrastructure.

The competitive dynamics with LabCorp deserve special attention. The two companies have achieved a stable duopoly that would make any economist suspicious. They rarely compete aggressively on price, seldom poach each other's major contracts, and have carved up certain geographic markets with surgical precision. This isn't explicit collusion—that would be illegal—but rather a tacit understanding that mutually assured destruction benefits nobody. When regional laboratories try to undercut on price, Quest and LabCorp can selectively match pricing in that specific market while maintaining margins elsewhere.

The hospital relationship strategy is particularly clever. Rather than competing with hospitals, Quest partners with them. The company manages hospital outreach programs, providing the infrastructure for hospitals to offer laboratory services to external physicians. Hospitals get to keep their brand and patient relationships while Quest handles the operational complexity. It's a win-win that further entrenches Quest's position while avoiding channel conflict.

Risk management at Quest is sophisticated and multi-layered. The company maintains massive insurance policies for errors and omissions, regulatory violations, and cyber incidents. But more importantly, Quest has diversified its risk across thousands of tests, millions of patients, and hundreds of facilities. No single test, customer, or facility represents more than a tiny fraction of revenue. This diversification, combined with the essential nature of diagnostic testing, makes Quest remarkably resilient to economic cycles.

The data strategy is still emerging but potentially transformative. Quest sits on one of the world's largest databases of clinical laboratory results—decades of longitudinal data for hundreds of millions of patients. This data, properly anonymized and analyzed, is invaluable for pharmaceutical companies developing new drugs, insurance companies assessing risk, and health systems managing populations. Quest is just beginning to monetize this asset, but the potential is enormous.

The lesson for investors is clear: Quest has built a business with multiple reinforcing moats that become stronger over time. Scale leads to cost advantages which enable competitive pricing which attracts volume which increases scale. It's a flywheel that's been spinning for fifty years and shows no signs of slowing down. For competitors, the lesson is equally clear: competing with Quest head-on is nearly impossible. The only viable strategies involve finding niches Quest doesn't serve, developing new testing technologies Quest doesn't offer, or fundamentally reimagining the laboratory business model itself.

X. Bear vs. Bull Case & Competitive Analysis

The Bull Case: An Essential Service in an Aging Society

The bull case for Quest starts with demographics, and demographics are destiny. By 2030, every Baby Boomer will be over 65, creating an unprecedented wave of healthcare utilization. Older adults require 3-5 times more laboratory testing than younger populations—monitoring chronic conditions, screening for cancer, managing medications. Quest processes tests for one in three American adults today; that penetration will only increase as the population ages.

The economics of diagnostic testing are improving, not deteriorating. While headlines focus on reimbursement pressure, the reality is more nuanced. Yes, Medicare rates for routine tests have declined, but test mix is shifting toward higher-value, higher-margin procedures. Genetic testing, molecular diagnostics, and specialty assays command prices 10-100x higher than basic blood work. Quest's acquisition strategy has positioned it perfectly for this shift—AmeriPath brought cancer diagnostics, Celera brought genomics, and the AD-Detect portfolio targets the enormous Alzheimer's market.

The consumer health transformation is just beginning. Quest's direct-to-consumer revenue is growing at 20%+ annually from a small base. With healthcare deductibles rising and consumers taking control of their health, the addressable market for consumer-initiated testing could reach $10 billion by 2030. Quest's brand recognition, physical infrastructure, and regulatory compliance give it massive advantages over venture-backed startups trying to disrupt from the outside.

Technology is a tailwind, not a threat. Every advance in testing technology—next-generation sequencing, liquid biopsies, AI-powered interpretation—requires massive capital investment, regulatory expertise, and distribution infrastructure. Quest has all three. The company can adopt new technologies faster than startups can scale, and with better economics. The company's venture investments and partnerships ensure it won't be blindsided by disruption.

The data moat is becoming unassailable. Every test Quest processes adds to a database that becomes more valuable over time. This isn't just about selling anonymized data—it's about developing proprietary algorithms, identifying disease patterns, and creating predictive models that no competitor can replicate. In an AI-driven future, data is the ultimate competitive advantage, and Quest has more clinical laboratory data than anyone.

The Bear Case: Commoditization and Disruption

The bear case starts with a simple observation: laboratory testing is becoming a commodity. The tests Quest runs today are largely the same as twenty years ago. Yes, there are new markers and methodologies, but a CBC is still a CBC, a lipid panel is still a lipid panel. As testing becomes standardized and automated, margins should compress to commodity levels. Quest's 20%+ EBITDA margins look unsustainable in this light.

Reimbursement pressure is relentless and accelerating. The Protecting Access to Medicare Act (PAMA) mandated significant cuts to laboratory reimbursement, and while implementation has been delayed, the direction is clear: the government wants to pay less for testing. Commercial payers follow Medicare's lead. As value-based care models proliferate, laboratories become cost centers to be minimized, not revenue generators to be optimized.

Hospital insourcing is a real threat. Large health systems are increasingly bringing laboratory services in-house, viewing testing as a core competency that shouldn't be outsourced. Every hospital that insources is lost revenue for Quest, and hospitals represent the highest-volume, most profitable customers. The partnership model Quest has developed may slow this trend but won't stop it.

Technology disruption is coming from unexpected angles. Point-of-care testing is improving rapidly—why send blood to Quest when a device in the physician's office can deliver results in minutes? At-home testing is proliferating—continuous glucose monitors, wearable biosensors, and smartphone-based diagnostics bypass traditional laboratories entirely. The iPhone disrupted cameras, music players, and GPS devices; could it disrupt laboratory testing too?

Competition is intensifying from all directions. Laboratory Corporation of America Holdings (LabCorp) remains a formidable competitor with similar scale and capabilities. Regional laboratories are consolidating and becoming more sophisticated. Hospital networks are creating their own laboratory consortiums. Even non-traditional players like Amazon, CVS Health, and Walmart are entering healthcare services. The cozy duopoly with LabCorp may not last.

The labor challenge is acute and worsening. Quest employs thousands of medical technologists, phlebotomists, and couriers. These jobs require specialized skills but offer modest pay. Labor shortages are driving wage inflation, while automation threatens to eliminate jobs and create social backlash. The company's dependence on human labor in an increasingly automated world is a vulnerability.

Regulatory risk never goes away. Quest has paid billions in settlements over the years, and the government's focus on healthcare fraud shows no signs of abating. One major compliance failure—contaminated tests, systematic billing errors, a data breach exposing patient information—could trigger massive fines, operational restrictions, and reputational damage that takes years to recover from.

Competitive Landscape: The Duopoly Under Pressure

Laboratory Corporation of America Holdings (LabCorp) remains Quest's primary competitor and mirror image. With roughly $12 billion in revenue and 20% market share, LabCorp has similar scale, margins, and strategic positioning. The two companies have achieved a stable equilibrium—competing enough to avoid antitrust scrutiny but not so aggressively as to destroy profitability. This détente has served shareholders well but may be unsustainable as new entrants attack from the edges.

Regional laboratories are consolidating and professionalizing. Companies like Sonic Healthcare, BioReference Laboratories, and regional health system labs are forming alliances, sharing best practices, and achieving scale that begins to rival the nationals. These players often have deeper local relationships, faster turnaround times, and more flexibility than Quest or LabCorp.

The hospital laboratory market is evolving rapidly. Large systems like Mayo Clinic, Cleveland Clinic, and Kaiser Permanente operate sophisticated laboratories that compete with Quest for outreach business. These hospital labs have advantages—brand recognition, integrated medical records, physician loyalty—that Quest can't match. The trend toward health system consolidation strengthens these competitors.

Technology companies are nibbling at the edges. Amazon's acquisition of One Medical, CVS's expansion into primary care, and Walmart's health clinic initiative all include laboratory services. These players won't compete with Quest directly but will cherry-pick profitable testing segments. More concerning are companies like Everlywell, LetsGetChecked, and other direct-to-consumer testing companies that bypass traditional channels entirely.

The Theranos shadow still looms. While the company was a fraud, the vision—distributed, miniaturized testing—remains compelling. Legitimate companies are working on microfluidics, lab-on-a-chip technologies, and point-of-care diagnostics that could eventually obsolete centralized laboratories. Quest must balance skepticism of unproven technologies with vigilance against genuine disruption.

International expansion remains limited. Unlike pharmaceuticals or medical devices, laboratory testing is inherently local. Samples need to be processed quickly, regulations vary by country, and reimbursement systems are incompatible. Quest has minimal international presence, leaving it dependent on the U.S. market while missing growth opportunities in emerging markets.

The Verdict: A Resilient Incumbent with Hidden Vulnerabilities

The weight of evidence favors the bulls, but not overwhelmingly. Quest's moats are real and durable—scale economies, network effects, regulatory barriers, switching costs. The company generates prodigious cash flow, has proven resilient through multiple cycles, and serves an essential function that isn't going away. Demographics provide a multi-decade tailwind, and Quest's strategic positioning in advanced diagnostics and consumer health creates optionality for various future scenarios.

But the bears have valid concerns. Margins feel unsustainably high for what's increasingly a commodity service. Reimbursement pressure is structural, not cyclical. Technology disruption may come slowly, but it will come. And Quest's dependence on the U.S. healthcare system—with all its inefficiencies and distortions—makes it vulnerable to policy changes that could reshape the industry overnight.

For investors, Quest represents a classic "quality at a reasonable price" opportunity. The company won't grow at venture capital rates, but it doesn't need to. Steady mid-single-digit revenue growth, margin maintenance through operational efficiency, and aggressive capital return can generate attractive returns with limited downside. The key risks to monitor are reimbursement changes, hospital insourcing trends, and emerging competition from technology companies.

The most likely scenario is continued slow consolidation of the laboratory industry, with Quest and LabCorp maintaining dominant positions while adapting to new technologies and business models. The companies that threaten Quest won't attack head-on but will slowly erode the edges of its business—consumer testing here, point-of-care there, AI interpretation somewhere else. Quest's challenge is to cannibalize itself before others do, embracing disruption while leveraging its incumbent advantages. The company that started in a Manhattan apartment has proven remarkably adaptable over five decades. The next decade will test that adaptability like never before.

XI. Epilogue: The Future of Diagnostics

Standing in Quest's newest facility in Clifton, New Jersey, you glimpse the future of medical diagnostics. Robots glide silently along tracks in the ceiling, delivering samples to automated analyzers that process thousands of tests per hour. AI algorithms flag abnormal results for human review. Data streams to physicians' smartphones in real-time. It's a far cry from Dr. Brown's apartment laboratory, yet the mission remains unchanged: deliver accurate results that improve health outcomes.

The next decade will bring transformative changes to diagnostic testing. Liquid biopsies will detect cancer years before symptoms appear. Pharmacogenomic testing will personalize medication selection, eliminating trial-and-error prescribing. Continuous monitoring through wearables will replace episodic testing, generating streams of data that AI systems analyze for patterns humans would miss. The question isn't whether these changes will occur, but who will capture the value they create.

Quest's position in this future is strong but not guaranteed. The company's advantages—scale, infrastructure, regulatory expertise—remain valuable in a world of precision medicine. Processing a liquid biopsy requires the same logistics network as processing a blood count. Interpreting genomic data requires the same quality systems as interpreting cholesterol levels. The core competencies Quest has built over fifty years translate remarkably well to emerging technologies.

But success will require continued evolution. Quest must become a technology company that happens to run laboratories, not a laboratory company that uses technology. This means investing aggressively in AI and machine learning, partnering with or acquiring digital health startups, and reimagining the entire testing experience from ordering to interpretation. The company's recent moves—QuestDirect, AD-Detect, consumer partnerships—suggest management understands this imperative.

Value-based care presents both opportunity and threat. As healthcare shifts from fee-for-service to value-based models, diagnostic testing becomes an investment in prevention rather than a billable service. This could compress margins as health systems demand lower prices. But it could also expand volumes dramatically as early detection and continuous monitoring become standard. Quest's vast database positions it uniquely to demonstrate the value of testing in improving outcomes and reducing total costs.

The personalized medicine revolution is Quest's to lose. The company already processes genetic tests through its partnership with Ancestry and its ownership of Celera's assets. As costs plummet and applications multiply, genetic testing will become as routine as cholesterol screening. Quest's challenge is to move beyond processing tests to interpreting results, providing actionable insights that justify premium pricing. This requires not just technology but also genetic counselors, clinical decision support, and physician education—services that leverage Quest's medical expertise.

International expansion remains the great untapped opportunity. While Quest focuses on the U.S. market, diagnostic testing is exploding globally. China's diagnostic market is growing at 15% annually. India's middle class demands world-class healthcare. Africa leapfrogs traditional infrastructure with mobile-enabled testing. Quest could export its expertise, technology, and operational excellence to these markets through joint ventures, licensing deals, or acquisitions. The company that conquered America could conquer the world.

The social impact of Quest's work deserves recognition. Every day, the company's tests detect diseases early, monitor treatment effectiveness, and provide peace of mind to worried patients. During COVID-19, Quest's testing capacity literally saved lives. As genetic testing advances, Quest will help identify predispositions to disease, enabling preventive interventions that spare suffering and reduce costs. This isn't just a business—it's a public health infrastructure that benefits society enormously.

Environmental and social governance (ESG) considerations are becoming central to Quest's strategy. The company processes millions of samples daily, generating significant waste. Transportation networks burn fossil fuels. Data centers consume massive amounts of electricity. Quest is investing in sustainable practices—electric vehicles, renewable energy, waste reduction—that reduce environmental impact while potentially lowering costs. The company's commitment to accessible testing, regardless of patient ability to pay, demonstrates social responsibility that resonates with stakeholders.

What would success look like in ten years? Quest in 2035 might be unrecognizable from today. The company could be the Amazon Web Services of healthcare data, providing analytical infrastructure that powers thousands of digital health applications. It could be the trusted intermediary between consumers and their health data, helping people understand and act on genetic, proteomic, and metabolomic information. It could be the platform that enables truly personalized medicine, with every treatment tailored to individual biology.

Or Quest could be disrupted, its centralized laboratory model obsoleted by distributed testing, its margins compressed by commoditization, its relevance diminished by new entrants who better understand the digital-first, consumer-centric future of healthcare. The company's history suggests it will adapt and thrive, but past performance doesn't guarantee future results.

For investors, Quest represents a fascinating study in competitive advantage, industry structure, and strategic adaptation. The company has built formidable moats that generate substantial economic value. But moats can become prisons if they prevent companies from embracing necessary change. Quest's challenge is to leverage its strengths while remaining flexible enough to evolve with—or ahead of—the market.

For entrepreneurs, Quest offers lessons in the power of consolidation, the importance of operational excellence, and the value of patient capital. Dr. Brown didn't set out to build a $20 billion company; he wanted to make testing more efficient and affordable. By focusing relentlessly on that mission while opportunistically acquiring and integrating competitors, Quest created enormous value for all stakeholders.

For society, Quest poses important questions about healthcare infrastructure, market concentration, and the balance between efficiency and competition. Is a diagnostic duopoly optimal, or does it stifle innovation? Should testing be a competitive market or a regulated utility? How do we ensure that advances in diagnostics benefit all patients, not just those who can afford them? These questions lack easy answers but deserve serious consideration.

The story of Quest Diagnostics is far from over. The company that began in a Manhattan apartment, survived the Corning years, engineered the SmithKline Beecham acquisition, consolidated an industry, and thrived through COVID stands at another inflection point. The choices made in the next few years will determine whether Quest leads the transformation of diagnostics or becomes a casualty of it. Based on history, betting against Quest seems unwise. But in technology-driven disruption, history is an imperfect guide.

What's certain is that diagnostic testing will become more important, not less. As medicine becomes increasingly precise, data-driven, and preventive, the need for accurate, accessible, affordable testing will only grow. Whether Quest Diagnostics continues to meet that need, and capture the value it creates, remains to be seen. The next chapter of this remarkable American business story is still being written, and it promises to be as dramatic as everything that came before.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube