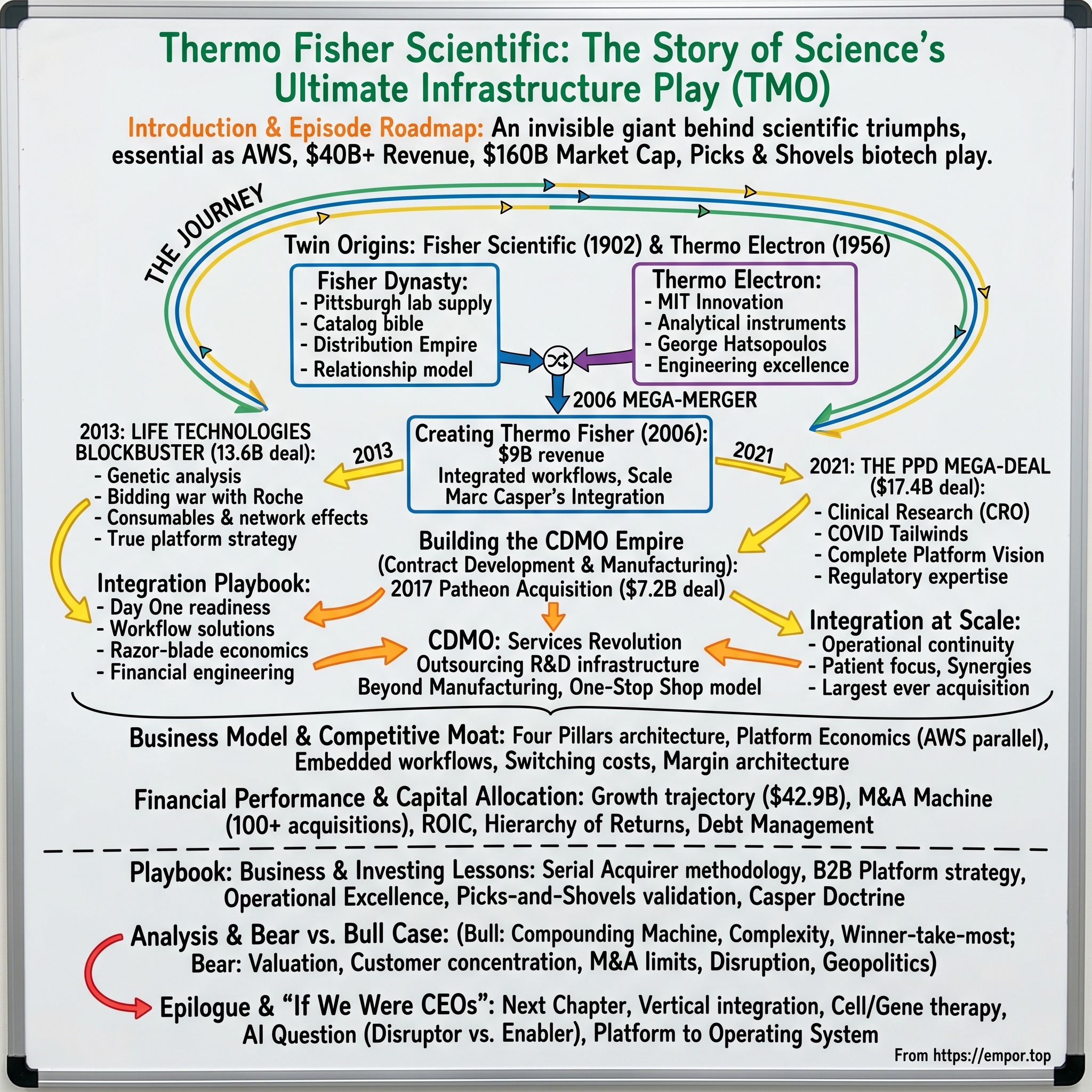

Thermo Fisher Scientific: The Story of Science's Ultimate Infrastructure Play

I. Introduction & Episode Roadmap

Picture this: Every COVID-19 vaccine dose administered globally, every cancer drug approved by the FDA, every genetic breakthrough making headlines—behind each of these scientific triumphs stands an invisible giant. A company so embedded in the fabric of modern science that removing it would be like trying to extract AWS from the internet. That company is Thermo Fisher Scientific, and its story is one of the most remarkable platform plays in business history.

With over $40 billion in annual revenue and a market capitalization hovering around $160 billion on the NYSE under ticker TMO, Thermo Fisher has quietly become what venture capitalists would call the ultimate "picks and shovels" play in biotechnology. But calling it just a lab equipment company would be like calling Amazon merely an online bookstore. This is the story of how two century-old scientific supply companies merged, then systematically acquired their way to becoming the indispensable infrastructure layer for global scientific research and drug development.

The narrative arc we're about to explore isn't just about M&A prowess—though with over 100 acquisitions integrated successfully, that's certainly part of it. It's about recognizing a fundamental shift in how science gets done: from individual labs buying equipment to entire pharmaceutical companies outsourcing their R&D infrastructure. It's about building switching costs so high that customers would rather renegotiate contracts than contemplate alternatives. And it's about timing—being perfectly positioned when a global pandemic suddenly made vaccine development the world's top priority.

What makes Thermo Fisher particularly fascinating for students of business strategy is its deliberate transformation from product company to platform. While tech companies get attention for platform economics, Thermo Fisher has quietly built one of the most powerful B2B platforms in existence—one where customers don't just buy products but embed their entire drug development pipelines into Thermo Fisher's ecosystem. The company doesn't just sell you a mass spectrometer; it runs your clinical trials, manufactures your drugs, and manages your laboratory operations.

This episode will trace the parallel histories of two scientific dynasties—Fisher Scientific and Thermo Electron—through their 2006 merger that created a $9 billion entity, then follow the aggressive acquisition strategy that built today's $40 billion colossus. We'll examine the operational playbook that allows them to consistently extract value from acquisitions, the platform economics that create virtually impenetrable competitive moats, and the strategic vision that positioned them as the AWS of biotechnology before anyone knew that's what the industry needed.

For investors, this is a masterclass in compound value creation through disciplined capital allocation. For operators, it's a blueprint for building mission-critical B2B platforms. And for anyone interested in how modern science actually gets done, it's an essential piece of infrastructure hiding in plain sight. Let's dive into how a merger of two equipment suppliers became the backbone of global scientific innovation.

II. The Twin Origins: Thermo Electron & Fisher Scientific

The Fisher Dynasty: From Pittsburgh Laboratory to Distribution Empire

In 1902, Chester G. Fisher wasn't thinking about building a scientific empire. The 23-year-old engineer from Pittsburgh simply noticed that researchers at local steel companies and universities were frustrated by the difficulty of obtaining laboratory supplies. Equipment was scattered across dozens of specialized vendors, delivery was unreliable, and quality was inconsistent. Fisher saw an opportunity that would define the next century of scientific commerce: centralized distribution with guaranteed quality.

Fisher Scientific International started in a small Pittsburgh storefront, but Chester Fisher's innovation wasn't the products he sold—it was the catalog he created. The Fisher Scientific Catalog became the bible of laboratory procurement, a comprehensive tome that eventually grew to over 2,000 pages, listing everything from beakers to bunsen burners, chemicals to chromatography columns. By standardizing product specifications and guaranteeing next-day delivery to major research centers, Fisher transformed laboratory procurement from an arcane art to a predictable business process.

The company's growth tracked perfectly with America's scientific ascent. During World War II, Fisher Scientific equipped the Manhattan Project laboratories. In the 1950s, as the NIH budget exploded and pharmaceutical companies proliferated, Fisher was there with distribution centers strategically located near every major research hub. By the 1960s, the Fisher catalog wasn't just a purchasing tool—it was how scientists discovered what equipment existed. If Fisher didn't carry it, researchers often didn't know it was available.

What made Fisher particularly powerful was its relationship model. While competitors focused on transactional sales, Fisher embedded account managers directly within major research institutions. These weren't just salespeople; they were consultants who understood research workflows, anticipated equipment needs, and often knew about new projects before they were formally funded. This customer intimacy at scale became a cornerstone of what would later make Thermo Fisher so formidable.

Thermo Electron: The MIT Innovation Machine

Meanwhile, in Cambridge, Massachusetts, a very different scientific story was unfolding. In 1956, George N. Hatsopoulos, fresh from his MIT mechanical engineering PhD, partnered with Harvard Business School graduate Peter M. Nomikos to found Thermo Electron Corporation. Where Fisher was about distribution and relationships, Thermo Electron was about innovation and engineering excellence.

Hatsopoulos was a serial inventor with a particular genius for analytical instruments—the sophisticated machines that could detect trace amounts of pollutants, analyze molecular structures, or measure isotope ratios with extraordinary precision. The company's early breakthrough came from environmental monitoring equipment, perfectly timed for the environmental movement of the 1960s and the creation of the EPA in 1970. Suddenly, every factory needed continuous emissions monitoring, and Thermo Electron's instruments became the gold standard.

But what truly set Thermo Electron apart was its unusual corporate structure—what Hatsopoulos called the "spinout strategy." Rather than keeping all innovations under one roof, Thermo Electron would spin out promising technologies as separate public companies while maintaining majority control. This created incredible incentives for innovation: scientists could become entrepreneurs while still having access to Thermo Electron's resources. By 2000, Thermo Electron had spawned 23 public companies, creating a constellation of specialized technology leaders all orbiting the parent company.

This strategy had profound implications for Thermo Electron's culture and capabilities. While Fisher Scientific excelled at understanding what customers needed, Thermo Electron excelled at inventing what customers didn't yet know they needed. The company pioneered mass spectrometry techniques that would later become essential for drug discovery. They developed thermal analysis instruments that enabled the semiconductor revolution. They created analytical tools that made modern environmental regulation possible.

By 2004, Thermo Electron had grown to over $2 billion in revenue, but the spinout strategy was becoming unwieldy. Investors complained about the complexity, and Hatsopoulos's successor, Marijn Dekkers, began consolidating the empire. Between 2001 and 2006, Thermo Electron bought back most of its spinouts, simplifying the structure and preparing for what would become the deal of the century.

Parallel Paths Converging

Throughout the late 20th century, Fisher Scientific and Thermo Electron were often competitors, sometimes partners, but always aware of each other. Fisher would distribute Thermo's instruments. Thermo would sometimes acquire the same innovative companies Fisher was eyeing. They served the same customers but from different angles—Fisher as the trusted supplier, Thermo as the technology innovator.

The competitive landscape they operated in was fragmenting and consolidating simultaneously. On one hand, scientific research was becoming increasingly specialized, spawning thousands of niche equipment manufacturers. On the other hand, customers—particularly big pharma companies—were demanding integrated solutions. They didn't want to manage relationships with hundreds of vendors; they wanted one throat to choke.

By 2005, both companies recognized that the future belonged to scale. Fisher Scientific, under CEO Paul Montrone, had already embarked on an acquisition spree, buying Apogent Technologies for $3.5 billion in 2003. Thermo Electron, under Marijn Dekkers, was rapidly consolidating its structure and acquiring complementary businesses. The logic of combination was becoming irresistible: Fisher's distribution married to Thermo's technology, Fisher's customer relationships combined with Thermo's innovation engine.

The stage was set for a merger that would reshape the scientific equipment industry and create a platform for unprecedented growth. Neither company fully grasped what they were about to build—a scientific infrastructure giant that would eventually touch every major drug development program on Earth.

III. The Mega-Merger: Creating Thermo Fisher (2006)

The Announcement That Shook the Industry

On May 8, 2006, the scientific community woke up to news that would fundamentally reshape their industry. Thermo Electron and Fisher Scientific, two titans that had defined different aspects of laboratory science for generations, announced they would merge in a tax-free, stock-for-stock exchange. The combined entity would employ 30,000 people and generate approximately $9 billion in annual revenue—instantly creating the world's largest scientific equipment company.

The announcement came after months of secret negotiations, code-named "Project Titan," conducted in hotel suites and lawyers' offices across Boston and New York. Paul Montrone, Fisher's CEO, had initiated the discussions, recognizing that the industry was at an inflection point. "We could either eat or be eaten," he would later tell investors. "We chose to feast together."

The strategic rationale was compelling on paper. Fisher brought unmatched distribution capabilities—relationships with over 350,000 customers, warehouses strategically positioned globally, and a logistics network that could deliver products to any major laboratory within 24 hours. Thermo brought technological leadership—breakthrough analytical instruments, proprietary technologies in mass spectrometry and chromatography, and an innovation pipeline that consistently produced industry-firsts.

But beyond the operational synergies, both leadership teams saw something larger: the opportunity to fundamentally change how scientific research was conducted. Instead of researchers cobbling together equipment from dozens of vendors, they could offer integrated workflows. Instead of selling products, they could sell outcomes. The vision was nothing less than becoming the operating system for global scientific research.

Regulatory Hurdles and the Art of the Deal

Not everyone was convinced this combination should proceed. The Federal Trade Commission launched an extensive review, concerned about the merged entity's dominance in several key markets. The investigation focused particularly on centrifugal evaporators—specialized equipment used in drug discovery where the combined company would control over 90% of the market.

The FTC's scrutiny revealed just how entrenched both companies had become in critical scientific workflows. Testimony from pharmaceutical companies described switching costs that weren't just financial but operational—changing equipment vendors could delay drug development programs by months, potentially costing billions in lost revenue. Academic researchers testified that certain Thermo instruments were so standard in their fields that papers using alternative equipment faced additional scrutiny from peer reviewers.

After months of negotiations, a compromise emerged. Fisher would divest Genevac, its centrifugal evaporator business, to a competitor. It was a small price to pay—Genevac represented less than 1% of combined revenues—but the process provided valuable lessons about antitrust navigation that would prove crucial in future acquisitions.

On November 9, 2006, the merger officially closed. The integration began immediately, and it was here that Marc Casper, then president of Fisher's laboratory products and services division, began to distinguish himself. While Montrone and Dekkers focused on Wall Street and strategic vision, Casper dove into the operational details that would determine whether this merger would create value or destroy it.

Marc Casper's Integration Masterclass

Marc Casper had been with the combined company since 2001, originally joining Thermo Electron as Vice President of the Life Sciences sector. His background combined strategy consulting at Bain & Company with operational experience running laboratory businesses. His early career at both Bain & Company and Bain Capital gave him a rare combination of strategic thinking and financial acumen that would prove invaluable in the integration ahead.

Casper's approach to integration was methodical yet aggressive. Rather than the typical playbook of cutting costs and eliminating redundancies, he focused on revenue synergies—getting Fisher's sales force to sell Thermo's instruments, using Thermo's technology to enhance Fisher's service offerings. He established "integration labs" where teams from both companies worked side by side to redesign workflows, combining the best practices from each organization.

One early win came from bundling. Casper's team discovered that while pharmaceutical companies might spend months evaluating a $500,000 mass spectrometer purchase, they rarely scrutinized the thousands of smaller purchases for consumables and basic equipment. By bundling high-margin consumables with instrument sales, offering volume discounts for enterprise-wide agreements, and guaranteeing service levels across the entire product portfolio, they could increase share of wallet while actually reducing customers' total cost of ownership.

The cultural integration proved more challenging. Fisher's culture was sales-driven and customer-focused, with a "whatever it takes" mentality. Thermo's culture was engineering-driven and innovation-focused, with a "build the best product" ethos. Rather than choosing one over the other, Casper instituted what he called "dual citizenship"—employees would maintain their functional excellence while adopting enterprise-wide values around customer success and operational efficiency.

Setting the Foundation for Future Growth

By the end of 2007, the integration was ahead of schedule. The company had achieved $150 million in cost synergies—50% above initial targets—while maintaining customer retention rates above 95%. More importantly, they had validated the platform thesis: customers were indeed willing to consolidate vendors in exchange for integrated solutions and superior service.

The merged entity's first major strategic move came in 2007 with the acquisition of Biolab, a European distributor that strengthened their presence in emerging markets. This wasn't just about geographic expansion; it was about testing the acquisition playbook that would define the next decade. Could they integrate companies quickly? Could they maintain innovation while achieving scale? Could they preserve entrepreneurial culture within a large corporation?

The answers were increasingly yes. Casper, who would become CEO in October 2009, was developing what would become known internally as the "Thermo Fisher Way"—a systematic approach to acquisition, integration, and value creation that would enable them to successfully absorb over 100 companies over the next 15 years.

The 2008 financial crisis actually accelerated their strategy. While competitors retrenched, Thermo Fisher used its strong balance sheet to acquire distressed assets at attractive valuations. They picked up specialized technology companies whose venture funding had dried up. They consolidated with regional distributors struggling with working capital. Each acquisition added capabilities, customer relationships, or geographic presence that would have taken years to build organically.

By 2009, when Casper officially took the CEO role, Thermo Fisher Scientific was no longer just a combination of two legacy companies. It had become something new: a platform for consolidating the fragmented life sciences industry, a machine for turning scientific innovation into shareholder value, and increasingly, the indispensable partner for global pharmaceutical development. The foundation was set for what would become one of the most successful serial acquisition strategies in corporate history.

IV. The Life Technologies Blockbuster (2013)

The Prize Everyone Wanted

In late 2012, whispers began circulating through the biotech industry about a potential mega-deal that would reshape the landscape. Life Technologies Corporation—itself a 2008 merger between Invitrogen and Applied Biosystems—was in play. With roughly $3.8 billion in annual revenue and leadership positions in genetic analysis, the company represented the crown jewel of life sciences tools. For Marc Casper and Thermo Fisher, it was the opportunity to transform from a large equipment company into the definitive platform for biotechnology.

Life Technologies wasn't just another acquisition target; it was a collection of assets that had defined modern molecular biology. Applied Biosystems had invented the automated DNA sequencer that made the Human Genome Project possible. Invitrogen had built the gold standard in cell culture media and molecular biology reagents—the basic building blocks that every laboratory needed daily. Together, they controlled technologies that were becoming fundamental to the future of medicine: next-generation sequencing, synthetic biology, and cell therapy.

The strategic importance went beyond individual products. Life Technologies had something Thermo Fisher desperately wanted: consumables with razor-blade economics. While Thermo Fisher sold expensive instruments that customers bought once every five to ten years, Life Technologies sold reagents and materials that laboratories consumed daily. These recurring revenues were not only more predictable but came with switching costs that bordered on prohibitive—changing your cell culture media supplier meant potentially invalidating years of experimental data.

The Bidding War with Roche

The bidding process that began in January 2013 quickly turned into one of the most intense acquisition battles in biotech history. Life Technologies' board met on Saturday to review three takeover offers from Thermo Fisher, Sigma-Aldrich, and a private equity consortium consisting of Blackstone Group, Carlyle Group, KKR, and Temasek Holdings. But the real drama came from an unexpected player: Hoffmann-La Roche, the Swiss pharmaceutical giant that had unsuccessfully pursued Illumina the previous year for $6.8 billion.

Roche's interest made strategic sense but also raised alarm bells. Unlike the other bidders who would operate Life Technologies as an independent supplier to the industry, Roche might integrate it into their pharmaceutical operations, potentially limiting access for competitors. This fear drove up the bidding as other pharma companies urged financial buyers to prevent Roche from controlling such critical infrastructure.

The private equity consortium, initially confident with their $65 per share offer backed by enormous financial firepower, found themselves outmaneuvered. They raised their offer on Friday to about $67 per share, but it was still short of Thermo Fisher's bid. Marc Casper had played the game perfectly, understanding that this wasn't just about price but about strategic fit and execution certainty.

Thermo Fisher ultimately won with an offer of $76.00 in cash per fully diluted common share, or approximately $13.6 billion, plus the assumption of net debt at close ($2.2 billion as of year end 2012). The premium—nearly 40% above Life Technologies' price before the sale process began—reflected not just the competitive dynamics but Casper's conviction that this was a transformative opportunity.

The Integration Playbook Perfected

The Life Technologies integration became the template for every major Thermo Fisher acquisition that followed. Casper deployed what he called "Day One readiness"—having integration teams embedded at Life Technologies locations the moment the deal closed on February 3, 2014. These weren't corporate raiders looking to slash costs; they were operators focused on preserving what made Life Technologies valuable while eliminating redundancies.

The first priority was protecting the crown jewels. Ion Torrent, Life Technologies' next-generation sequencing platform, was growing rapidly and competing effectively against market leader Illumina. Rather than forcing Ion Torrent into Thermo Fisher's existing structure, Casper gave it protected status—maintaining its separate R&D budget, preserving its entrepreneurial culture, and even keeping its distinct branding. Casper noted that while Thermo Fisher was modeling overall organic growth of 3 percent for Life Tech, Life Tech's Ion Torrent business was anticipated to grow at a "much faster rate."

The second priority was managing regulatory complexity. As part of obtaining antitrust approval, Thermo Fisher had agreed to sell its cell culture (sera and media), gene modulation and magnetic beads businesses to GE Healthcare for $1.06 billion. This divestiture, while painful, actually helped focus the combined entity on higher-margin, more differentiated technologies.

Customer retention became an obsession. Thermo Fisher created "customer success teams" that included representatives from both legacy organizations, ensuring no relationship fell through the cracks during integration. They offered multi-year contracts with price protection to nervous customers, trading short-term margin for long-term stability. The strategy worked: customer retention exceeded 97% in the first year post-merger.

Financial Engineering and Value Creation

The financial architecture of the Life Technologies deal showcased Thermo Fisher's sophisticated approach to capital allocation. Thermo Fisher obtained committed bridge financing from JP Morgan and Barclays, expecting to pay for the deal through a combination of $9.5 billion to $10 billion in cash and debt and up to $4 billion in equity. This structure minimized dilution while maintaining financial flexibility for future acquisitions.

The synergy targets seemed aggressive at announcement—$275 million in annual cost synergies and $60-80 million in revenue synergies within three years. But Casper's team systematically exceeded every target. They consolidated 130 facilities down to 80. They leveraged Thermo Fisher's global scale to renegotiate supplier contracts. They cross-sold Life Technologies' consumables through Fisher's distribution network and Fisher's services through Life Technologies' installed base.

The real genius was in the revenue synergies. Thermo Fisher discovered that Life Technologies customers typically also bought from multiple other vendors. By bundling Life Technologies' products with Thermo Fisher's broader portfolio, they could offer "workflow solutions" that increased average deal sizes by 40%. A customer buying an Ion Torrent sequencer would also get sample preparation reagents, data analysis software, and service contracts—all from one vendor with one invoice.

Building the Platform Strategy

The Life Technologies acquisition marked Thermo Fisher's transformation from a holding company of scientific businesses to a true platform company. The difference was integration depth. Rather than operating acquired companies as independent divisions, Thermo Fisher began weaving them into an interconnected ecosystem where each acquisition made the others more valuable.

Consider the network effects: Life Technologies' sequencing instruments generated data that required Thermo Fisher's analytical software. The analytical results suggested follow-up experiments using Thermo Fisher's mass spectrometers. The mass spec data needed validation using Life Technologies' PCR instruments. Each product created demand for others, locking customers into an expanding web of interdependencies.

This platform approach also changed how Thermo Fisher thought about acquisitions. They weren't just buying revenues or technologies; they were buying nodes in a network. The value of each node increased with the size of the network, creating a compounding effect that justified premium valuations. When competitors complained about Thermo Fisher "overpaying" for assets, they were missing the network value that only Thermo Fisher could unlock.

By 2015, the Life Technologies integration was complete and exceeding all targets. The deal was expected to add $.90 to $1.00 to adjusted EPS in the first full year after the close of the acquisition. But more importantly, it had transformed Thermo Fisher from a large equipment company into the essential platform for life sciences research. The stage was set for even bolder moves into contract research and manufacturing that would define the company's next chapter.

V. Building the CDMO Empire: Patheon Acquisition (2017)

The Services Revolution

By 2016, Marc Casper could see a fundamental shift occurring in the pharmaceutical industry. Big pharma companies, facing patent cliffs and pipeline pressures, were increasingly outsourcing everything from drug development to manufacturing. Small biotech companies, flush with venture capital but lacking infrastructure, needed partners who could take them from concept to commercialization. The Contract Development and Manufacturing Organization (CDMO) market—essentially the outsourced infrastructure for drug development—was exploding, projected to reach $40 billion by 2020.

Thermo Fisher had already dipped its toes into services through organic growth and small acquisitions, but Casper wanted to dive into the deep end. The target he identified was Patheon N.V., a global CDMO with a fascinating history of its own. Originally spun out of Toronto-based Cangene Corporation in 1999, Patheon had grown through aggressive acquisition to become one of the world's largest CDMOs, with particular strength in complex drug formulation and commercial-scale manufacturing. What made Patheon particularly attractive was its transformation story under CEO James Mullen, the former CEO of Biogen. Starting in 2012, Mullen had orchestrated a string of acquisitions including Banner Pharmacaps for $255 million, Gallus BioPharmaceuticals, and the 2014 merger with DSM's pharmaceutical business that created DPx Holdings in a $2.6 billion deal. Patheon had become a consolidation platform in its own right, rolling up the fragmented CDMO industry just as Thermo Fisher was doing in laboratory equipment.

The Strategic Rationale: Beyond Manufacturing

On May 15, 2017, Thermo Fisher announced it would acquire Patheon for $35.00 per share in cash, valuing the company at approximately $7.2 billion including $2 billion in net debt. The premium was substantial—about 35% above Patheon's trading price—but Casper saw value that went beyond the numbers. Thermo Fisher completed its acquisition of Patheon N.V., a leading contract development and manufacturing organization (CDMO) serving the pharmaceutical and biotechnology sectors, for approximately $7.2 billion.

"This isn't just about adding manufacturing capacity," Casper explained to investors. "It's about becoming our customers' partner from discovery through commercialization." The vision was breathtaking in scope: a pharmaceutical company could use Thermo Fisher's instruments for drug discovery, its clinical trial services for development, and now Patheon's facilities for manufacturing. No other company could offer this end-to-end capability.

Patheon generated fiscal 2016 revenue of approximately $1.9 billion and brought with it 9,000 employees and manufacturing sites across Canada, the continental US, Puerto Rico, France, the United Kingdom, Italy, Austria, Germany, the Netherlands, Japan, and Australia. But more importantly, it brought deep relationships with every major pharmaceutical company. Clients included Merck, Novartis, Takeda, Sanofi Aventis, Amgen, and Avanir Pharmaceuticals. As of 2016, Patheon had manufactured or developed more than 800 products.

The CDMO market itself was undergoing rapid transformation. Pharmaceutical companies were increasingly adopting an "asset-light" model, preferring to outsource manufacturing rather than build their own facilities. This was especially true for biologics—complex protein-based drugs that required specialized manufacturing expertise. Small biotech companies, which increasingly dominated drug discovery, had neither the capital nor the expertise to build manufacturing facilities. They needed partners who could take them from lab bench to pharmacy shelf.

Integration as Transformation

The Patheon integration became a masterclass in preserving entrepreneurial culture within a large corporation. Rather than immediately rebranding Patheon facilities as Thermo Fisher sites, Casper maintained the Patheon brand as a service offering within Thermo Fisher's portfolio. This wasn't just about marketing; it was about maintaining the trust and relationships that Patheon had built over decades.

The integration team, led by executives from both companies, focused on three priorities. First, maintaining operational continuity—not a single customer shipment could be delayed during integration. Second, cross-selling opportunities—introducing Patheon's manufacturing customers to Thermo Fisher's analytical services and vice versa. Third, capability expansion—using Thermo Fisher's balance sheet to fund expansion of Patheon's most constrained facilities.

Thermo Fisher continues to expect to realize total synergies of approximately $120 million by year three following the close, consisting of approximately $90 million of cost synergies and approximately $30 million of adjusted operating income benefit from revenue-related synergies. But the real value came from revenue synergies that weren't fully captured in these projections.

Consider a typical scenario: A biotech company developing a new cancer drug would start by using Thermo Fisher's research tools for discovery. As the drug moved into development, they would engage Thermo Fisher's clinical trial services. When it came time for manufacturing, instead of finding a new partner, they could seamlessly transition to Patheon's facilities. This continuity reduced risk, accelerated timelines, and created switching costs that bordered on prohibitive.

The One-Stop Shop Reality

The Patheon acquisition fundamentally changed how pharmaceutical companies thought about Thermo Fisher. Previously, they were a vendor—important but replaceable. Now, they were a strategic partner embedded throughout the drug development process. The conversation shifted from "What equipment do you need?" to "How can we help you get your drug to market faster?"

This transformation was particularly powerful in biologics, where manufacturing complexity created enormous barriers to entry. Biologics aren't synthesized chemically like traditional drugs; they're produced by living cells, making manufacturing as much an art as a science. A small change in temperature, pH, or nutrient concentration could render an entire batch worthless. Patheon's expertise in biologics manufacturing, combined with Thermo Fisher's analytical capabilities, created an unmatched platform for biological drug development.

The financial impact was immediate and substantial. For the remainder of 2017, the transaction is expected to be approximately $0.09 accretive to adjusted earnings per share, with expectations of about $0.30 per share in the first full year. But these numbers understated the strategic value. Thermo Fisher had entered a $40 billion market growing at double-digit rates, with competitive advantages that would be nearly impossible for others to replicate.

Building the CDMO Platform

Post-acquisition, Thermo Fisher didn't rest on its laurels. They immediately began investing in expanding Patheon's capabilities, particularly in high-growth areas like cell and gene therapy manufacturing. These next-generation therapies required entirely new manufacturing processes—instead of making pills or proteins, manufacturers were modifying patients' own cells or creating viral vectors to deliver genetic therapies.

The company also leveraged Thermo Fisher's global reach to expand Patheon's geographic footprint. New facilities were opened in high-growth markets, particularly in Asia where pharmaceutical manufacturing was growing rapidly. Existing facilities were upgraded with Thermo Fisher's latest analytical equipment, allowing for better quality control and faster batch release.

The integration with Thermo Fisher's other services created powerful network effects. Data from manufacturing could inform clinical trial design. Insights from clinical trials could optimize manufacturing processes. The entire system became a learning platform, continuously improving and creating value that no standalone CDMO could match.

By 2019, the Patheon integration was complete and exceeding all targets. But more importantly, it had proven the power of Thermo Fisher's platform strategy. The company wasn't just acquiring revenues; it was building an ecosystem where each new capability made every other capability more valuable. The stage was set for the next transformative acquisition that would complete the platform: the purchase of PPD and entry into clinical research services.

VI. The PPD Mega-Deal: Completing the Platform (2021)

Seizing the COVID Moment

The COVID-19 pandemic transformed many industries, but perhaps none more dramatically than clinical research. Suddenly, the world needed vaccines and treatments developed at unprecedented speed. Clinical trials that normally took years needed to be completed in months. The entire pharmaceutical industry was stress-testing its infrastructure, and at the center of this storm stood companies like PPD, running the clinical trials that would determine which treatments worked. Marc Casper had been eyeing the clinical research organization (CRO) space for years, but PPD represented something special. Founded in 1985 by Fred Eshelman as a one-person consulting firm in North Carolina, PPD had grown into a global powerhouse with $4.7 billion in revenue in 2020, 26,000 employees, and operations in 650 facilities around the world. Most notably, they were managing trials for Moderna's COVID-19 vaccine—a credential that carried enormous weight in 2021.

On April 15, 2021, Thermo Fisher announced it would acquire PPD for $47.50 per share for a total cash purchase price of $17.4 billion plus the assumption of approximately $3.5 billion of net debt. The total deal value of nearly $21 billion made it Thermo Fisher's largest acquisition ever, but Casper saw it as the capstone of a decade-long strategy.

"We are very excited to officially welcome our PPD colleagues to Thermo Fisher Scientific," said Marc N. Casper. "Expanding our value proposition for our biotech and pharmaceutical customers with the addition of PPD's leading clinical research services advances our work in bringing life-changing therapies to market, benefitting patients around the world."

The Complete Platform Vision

The strategic logic was compelling on multiple levels. First, PPD filled the last major gap in Thermo Fisher's end-to-end offering. Now, a pharmaceutical company could literally outsource every step of drug development to Thermo Fisher: discovery using their research tools, preclinical testing using their analytical instruments, clinical trials through PPD, and manufacturing through Patheon. As one industry executive put it: "Not only will they make your drug and test your drug, they will do all your clinical trials."

Second, the CRO market itself was experiencing unprecedented growth. The $50 billion clinical research services industry was growing at double-digit rates, driven by the explosion in biotech funding, the complexity of modern clinical trials, and the pressure to accelerate drug development timelines. COVID-19 had only accelerated these trends, with every pharmaceutical company scrambling to expand their clinical trial capacity.

Third, PPD brought capabilities that would enhance Thermo Fisher's existing businesses. PPD's patient recruitment networks could accelerate enrollment for clinical trials using Thermo Fisher's companion diagnostics. PPD's real-world evidence capabilities could inform manufacturing decisions at Patheon facilities. PPD's regulatory expertise could help navigate approval processes for drugs manufactured using Thermo Fisher's technologies.

COVID Tailwinds and Perfect Timing

The timing of the PPD acquisition was particularly astute. COVID-19 had demonstrated the critical importance of clinical research infrastructure. Governments were pouring unprecedented funding into vaccine and therapeutic development. Pharmaceutical companies were racing to build pandemic preparedness capabilities. The entire industry was recognizing that speed to market could mean the difference between success and failure—not just commercially, but in terms of public health impact.

PPD's role in the Moderna vaccine trials had elevated its profile significantly. They had demonstrated the ability to run complex, global clinical trials at unprecedented speed while maintaining rigorous quality standards. This track record made them invaluable to pharmaceutical companies planning their next generation of drug development programs.

The pandemic had also created favorable financing conditions. Interest rates were at historic lows, making the debt component of the acquisition extremely attractive. Thermo Fisher's stock was trading at all-time highs, giving them currency for the equity portion. And the market was rewarding companies with COVID-19 exposure, making the acquisition immediately accretive to valuation multiples.

Integration at Scale

The PPD integration represented Thermo Fisher's most complex challenge yet. With 26,000 employees across 650 facilities, PPD was essentially a company the size of the original Thermo Fisher merger. But Casper's team had now perfected their integration playbook over dozens of acquisitions.

The first priority was maintaining operational continuity. Clinical trials cannot be paused or delayed—patients' lives literally depend on them continuing. Thermo Fisher established a "clinical continuity team" that ensured every ongoing trial continued without interruption. Not a single trial was delayed due to the acquisition, a remarkable achievement given the scale of the integration.

The second priority was preserving PPD's culture of scientific rigor and patient focus. Clinical research requires a different mindset than manufacturing or equipment sales—it's fundamentally about human health and safety. Thermo Fisher maintained PPD's quality systems, standard operating procedures, and regulatory frameworks intact, while gradually introducing Thermo Fisher's operational excellence practices.

The integration also revealed unexpected synergies. PPD's global clinical trial infrastructure could be leveraged to accelerate adoption of Thermo Fisher's diagnostic products in emerging markets. PPD's relationships with hospital networks created new channels for Thermo Fisher's clinical diagnostic products. The combined data from clinical trials, manufacturing, and real-world evidence created insights that neither company could have generated alone.

Financial Impact and Value Creation

The financial impact was immediate and substantial. The transaction is expected to contribute $1.50 to Thermo Fisher's adjusted earnings per share in 2022. Thermo Fisher continues to expect to realize total synergies of approximately $125 million by year three following close, consisting of approximately $75 million of cost synergies and approximately $50 million of adjusted operating income benefit from revenue-related synergies.

But the strategic value went far beyond these numbers. The PPD acquisition completed Thermo Fisher's transformation into a true platform company. They were no longer just a supplier to the pharmaceutical industry; they were an integral part of the drug development ecosystem. The switching costs for customers using multiple Thermo Fisher services had become astronomical—not just financially, but operationally and regulatorily.

The market recognized this transformation. Despite the massive price tag, Thermo Fisher's stock rose on the announcement and continued climbing as integration proceeded ahead of schedule. Analysts began comparing Thermo Fisher not to other scientific equipment companies but to platform giants like Microsoft or Amazon Web Services. The comparison was apt: just as AWS had become the indispensable infrastructure for internet companies, Thermo Fisher had become the indispensable infrastructure for pharmaceutical development.

By the completion of the acquisition on December 8, 2021, Thermo Fisher had assembled all the pieces of its platform strategy. From research tools to clinical trials to manufacturing, they could support every step of the drug development process. The company that began as two equipment suppliers had transformed into something unprecedented: a fully integrated pharmaceutical development platform that touched virtually every drug in development globally. The stage was set for leveraging this platform to drive the next phase of growth in an industry being transformed by precision medicine, cell and gene therapy, and artificial intelligence.

VII. The Business Model & Competitive Moat

The Four Pillars of Thermo Fisher's Architecture

Thermo Fisher's organizational structure reflects its evolution from equipment supplier to integrated platform. The company operates through four main segments, each representing a different layer of the scientific value chain. The Laboratory Products and Biopharma Services segment contributing a total revenue of US$23.2b (54% of total revenue) has become the dominant force, encompassing everything from basic lab supplies to complex clinical trials and drug manufacturing services through PPD and Patheon.

The beauty of this structure lies not in the individual segments but in how they reinforce each other. Analytical technologies (17% of sales) creates the sophisticated instruments that generate data. Life science solutions (23%) provides the reagents and consumables these instruments need to function. Specialty diagnostics (11%) translates research discoveries into clinical applications. And the massive lab products and services segment ties it all together, providing both the distribution infrastructure and the high-touch services that make customers dependent on Thermo Fisher for their entire workflow.

This isn't just diversification for its own sake. Each segment creates demand for the others in a virtuous cycle. A customer buying a mass spectrometer needs consumables, service contracts, and often clinical trial services to validate their discoveries. A pharmaceutical company using Patheon for manufacturing needs analytical instruments for quality control and PPD for clinical trials. The more deeply embedded a customer becomes in one part of the ecosystem, the more likely they are to use other parts.

Platform Economics: The AWS Parallel

The comparison to Amazon Web Services isn't just marketing rhetoric—it's a surprisingly accurate analogy for understanding Thermo Fisher's competitive position. Like AWS, Thermo Fisher provides the infrastructure layer that entire industries are built upon. Just as startups don't build their own data centers, biotech companies increasingly don't build their own laboratories or manufacturing facilities. They rent capacity from Thermo Fisher.

The economics are strikingly similar. Both businesses have massive upfront capital requirements that create barriers to entry. Both benefit from incredible economies of scale—the cost per unit of service decreases as volume increases. Both create switching costs that border on prohibitive—migrating from AWS can cripple a tech company, and changing CROs mid-clinical trial can doom a drug development program.

But Thermo Fisher's switching costs might actually be higher than AWS's. When a pharmaceutical company embeds Thermo Fisher products into their standard operating procedures, those procedures become part of regulatory filings. Changing vendors doesn't just require retraining staff and replacing equipment; it requires regulatory reapproval, revalidation of processes, and potential delays in drug development programs worth billions of dollars.

Consider the depth of integration: A typical large pharmaceutical company might have thousands of Thermo Fisher products in their catalog, hundreds of service contracts, dozens of ongoing projects with Patheon, and multiple clinical trials running through PPD. The idea of replacing all of this isn't just expensive—it's operationally impossible. No other company has the breadth to offer a credible alternative across all these touchpoints.

The Competitive Moat Deconstructed

Thermo Fisher's competitive advantages compound on each other in ways that make the business nearly impossible to disrupt. Start with scale: with $42.88 billion in revenue, they're larger than their next three competitors combined. This scale allows them to outspend everyone on R&D, offer better pricing through purchasing power, and maintain a global presence that smaller competitors can't match.

But scale alone doesn't explain the moat. The real power comes from what economists call "network effects" and "economies of scope." Every new product Thermo Fisher launches makes their platform more valuable to existing customers. Every new customer makes the platform more attractive to suppliers and partners. Every acquisition adds capabilities that enhance other parts of the business.

The company's global reach amplifies these advantages. UNITED STATES generated $22.50 B in revenue, representing 52.48% of its total revenue. The biggest region for Thermo Fisher Scientific is the UNITED STATES, which represents 52.48% of its total revenue. But their presence in Europe (25.32% of revenue) and Asia Pacific (18.55%) isn't just about market access—it's about being embedded in every major pharmaceutical and research cluster globally. When a drug is developed in Cambridge, manufactured in Singapore, and tested in North Carolina, Thermo Fisher is involved at every step.

Customer Relationships as Strategic Assets

With 125,000 employees globally, Thermo Fisher has built something unique in B2B: customer intimacy at scale. This isn't the typical vendor-customer relationship where interactions are limited to purchase orders and service calls. Thermo Fisher employees are embedded within customer organizations, often with permanent desks at major pharmaceutical companies. They attend planning meetings, contribute to research discussions, and become part of the customer's extended team.

This deep integration creates information advantages that are hard to replicate. Thermo Fisher knows what drugs are in development years before they're public. They understand customer needs before customers fully articulate them. They can anticipate demand shifts and adjust capacity accordingly. This information flows both ways—customers rely on Thermo Fisher's market intelligence to inform their own strategies.

The relationship model varies by customer type but is always sticky. For big pharma, Thermo Fisher provides enterprise-wide agreements that cover everything from basic supplies to complex services, with dedicated account teams that function almost as outsourced procurement departments. For academic institutions, they provide grant-writing support, educational programs, and flexible payment terms that align with funding cycles. For small biotechs, they offer turnkey solutions that allow virtual companies to operate without any internal infrastructure.

Pricing Power and Margin Architecture

Despite operating in what should be competitive markets, Thermo Fisher maintains remarkable pricing power. Consumables generated $17.59 B in revenue, representing 41.02% of its total revenue. Instruments generated $7.45 B in revenue, representing 17.37% of its total revenue. Service generated $17.85 B in revenue, representing 41.62% of its total revenue. This mix is carefully orchestrated to maximize margin capture across the customer lifecycle.

The instrument business often operates at lower margins, sometimes even at a loss for strategic accounts. But once an instrument is installed, it creates an annuity stream of consumables and service revenues that can last decades. A mass spectrometer might generate $2 million in consumables revenue over its lifetime versus a $500,000 initial purchase price. Service contracts add another layer, typically priced at 10-15% of equipment value annually with 60%+ gross margins.

The services businesses—clinical trials and manufacturing—operate on a different model but with similar economics. These are typically multi-year contracts with built-in price escalators and minimum volume commitments. The capital intensity creates barriers to entry, while the regulatory requirements create switching costs. Once a drug is approved using Thermo Fisher's manufacturing process, changing vendors requires extensive regulatory work that customers desperately want to avoid.

What's remarkable is how Thermo Fisher has maintained or expanded margins despite massive acquisitions. This isn't financial engineering—it's operational excellence. They consistently find ways to extract more value from acquired assets through cross-selling, operational improvements, and scale economies. The margin structure becomes self-reinforcing: higher margins fund more R&D and acquisitions, which strengthen the platform, which supports higher margins.

VIII. Financial Performance & Capital Allocation

The Growth Trajectory Decoded: From $9B Merger to $42.9B Revenue Giant

The transformation represents one of the most successful value creation stories in corporate history. Full year 2024 revenue was $42.88 billion, flat versus prior year, but this headline number masks the underlying strength of the business model. The company has maintained an EBITDA of $10.84 billion with a current EBITDA margin of 25.12%—remarkable for a company of this scale operating in theoretically competitive markets.

What's most impressive isn't the absolute growth but the consistency of execution through multiple economic cycles. The company navigated the 2008 financial crisis by acquiring distressed assets. It capitalized on the biotech boom of the 2010s through strategic acquisitions. It turned the COVID-19 pandemic into an opportunity to accelerate its platform strategy. Each crisis became a catalyst for strengthening competitive position.

The financial architecture supporting this growth is sophisticated yet disciplined. Fourth quarter 2024 GAAP diluted EPS grew 14% to $4.78, while adjusted EPS grew 8% to $6.10. This divergence between GAAP and adjusted earnings reflects the ongoing integration costs from acquisitions, but also demonstrates the company's ability to consistently extract value from deals over time.

The M&A Machine: 100+ Acquisitions and Counting

Thermo Fisher's acquisition track record defies conventional wisdom about serial acquirers. Over 100 acquisitions since the 2006 merger should have resulted in integration fatigue, cultural dilution, or at minimum, declining returns on invested capital. Instead, the company has maintained or improved returns with each major deal, suggesting a repeatable, scalable acquisition model that actually improves with practice.

The discipline starts with target selection. Thermo Fisher doesn't chase hot technologies or engage in bidding wars for trophy assets (with rare strategic exceptions like Life Technologies). They look for companies with strong market positions, sticky customer relationships, and clear synergy potential. Critically, they walk away from deals that don't meet their return thresholds—for every acquisition completed, dozens are evaluated and rejected.

The integration playbook has been refined to an art form. Day one readiness means integration teams are embedded before deals close. The first 100 days focus on maintaining business continuity while identifying quick wins. Years one and two emphasize cross-selling and operational improvements. By year three, the acquisition should be fully integrated and exceeding synergy targets. This isn't theoretical—it's been validated across dozens of deals.

Financial engineering enhances returns but doesn't drive them. The company uses a mix of cash, debt, and occasionally equity to optimize cost of capital. They're aggressive about refinancing acquired debt at lower rates. They extract working capital improvements through scale purchasing power. But the real value creation comes from revenue synergies—getting acquired products into Thermo Fisher's distribution channels and Thermo Fisher products into acquired customer bases.

Return on Invested Capital: The Ultimate Scorecard

While revenue growth and margin expansion get attention, return on invested capital (ROIC) tells the real story of value creation. Despite deploying over $50 billion in acquisitions since 2006, Thermo Fisher has maintained ROIC consistently above their cost of capital, often in the mid-teens—exceptional for a capital-intensive business.

This isn't financial engineering—it's operational excellence. Each acquisition adds assets that generate returns above the cost of acquiring them. The network effects mean that each new node in the platform makes existing nodes more valuable. A customer using both Patheon and PPD services is more profitable than two separate customers using one service each.

The company's capital efficiency has actually improved over time, contrary to what you'd expect from a mature business. This comes from several sources: shifting mix toward higher-margin services, increasing utilization of manufacturing assets, and leveraging fixed costs across a larger revenue base. The PPD acquisition, for instance, added a capital-light clinical research business that enhanced overall returns despite its massive price tag.

Capital Deployment Priorities: The Hierarchy of Returns

Thermo Fisher's capital allocation follows a clear hierarchy designed to maximize long-term value creation. During 2024, the company returned $4.6 billion of capital to shareholders through stock buybacks and dividends, but this comes only after funding higher-return opportunities.

The first priority is always organic investment in R&D and capacity expansion. Despite the focus on acquisitions, the company spends over $1 billion annually on R&D, consistently launching products that maintain technology leadership. Recent innovations like the Thermo Scientific™ Iliad™ demonstrate that innovation hasn't been sacrificed for financial engineering.

The second priority is strategic M&A, but only when returns exceed organic opportunities. The discipline here is remarkable—the company has walked away from numerous high-profile auctions when prices exceeded their return thresholds. They're willing to be patient, sometimes tracking companies for years before conditions align for an acquisition.

The third priority is returning capital to shareholders, but even here there's sophistication. Share buybacks are accelerated when the stock is undervalued and slowed when it's expensive. The dividend, while modest, has grown consistently, signaling confidence in long-term cash generation. The balance between buybacks and dividends optimizes for different shareholder preferences while maintaining financial flexibility.

Debt Management and Financial Flexibility

Despite aggressive acquisitions, Thermo Fisher has maintained investment-grade credit ratings and substantial financial flexibility. The debt strategy is sophisticated: using different instruments (term loans, bonds, commercial paper) to optimize cost and duration, maintaining multiple undrawn credit facilities for opportunistic moves, and aggressively refinancing when rates are favorable.

The company's ability to access capital markets on favorable terms is itself a competitive advantage. When the PPD opportunity arose in 2021, Thermo Fisher could commit $17.4 billion knowing they could finance it attractively. Smaller competitors simply can't match this financial firepower, creating a self-reinforcing cycle where scale begets scale.

What's remarkable is how debt has been deployed to enhance rather than endanger the business. Each major debt-funded acquisition has been followed by rapid deleveraging through cash generation and synergy realization. The company typically returns to target leverage ratios within 18-24 months of major deals, maintaining dry powder for the next opportunity.

The financial model has proven remarkably resilient through cycles. During COVID-19, when many companies were drawing credit lines defensively, Thermo Fisher was deploying capital offensively, acquiring PPD at an attractive valuation while competitors were retrenching. This countercyclical capability—having financial strength when others are weak—has been a consistent source of value creation over the past two decades.

IX. Playbook: Business & Investing Lessons

The Serial Acquirer Playbook: When Lightning Strikes Repeatedly

The conventional wisdom about serial acquirers is that they eventually stumble—integration complexity compounds, cultures clash, returns diminish. Thermo Fisher has defied this pattern for nearly two decades, executing over 100 acquisitions while maintaining or improving operational metrics. The secret isn't just disciplined execution; it's building an organization designed for perpetual integration.

Most companies treat acquisitions as discrete events requiring extraordinary effort. Thermo Fisher treats them as business as usual. They maintain permanent integration teams who move from deal to deal, accumulating expertise. They've codified integration into repeatable processes—playbooks for IT system migration, customer communication templates, day-one readiness checklists. What would paralyze other organizations has become routine.

The cultural element is critical but counterintuitive. Rather than imposing a monolithic culture, Thermo Fisher preserves what makes acquired companies valuable while instilling common operational standards. The Patheon brand was maintained because customers valued it. PPD's clinical trial methodology was preserved because it was industry-leading. But all acquired companies adopt Thermo Fisher's customer service standards, quality systems, and financial controls.

The timing of integration matters as much as the method. Thermo Fisher uses what they call "earned autonomy"—newly acquired companies initially operate with significant independence, earning greater integration as they demonstrate capability. This prevents the organizational rejection that often dooms acquisitions while ensuring eventual standardization. It's a biological model rather than a mechanical one—grafting rather than bolting on.

Platform Strategy in B2B: The Untold Story

While platform strategies get attention in consumer technology, Thermo Fisher has quietly built one of the most powerful B2B platforms in existence. The principles are similar—network effects, switching costs, ecosystem lock-in—but the execution is fundamentally different in B2B contexts where relationships, trust, and regulatory compliance matter more than user experience.

The key insight was recognizing that customers don't want products; they want outcomes. A pharmaceutical company doesn't want a mass spectrometer; they want to know their drug is pure. They don't want clinical trial services; they want FDA approval. By organizing around customer outcomes rather than products, Thermo Fisher created a platform that becomes more valuable as customers use more of it.

The platform economics are compelling. Customer acquisition costs are amortized across multiple products and services. Cross-selling is natural rather than forced—a customer using Thermo Fisher for manufacturing naturally needs their analytical services for quality control. Pricing power increases with wallet share—enterprise agreements provide discounts but increase total spending. The lifetime value of platform customers dwarfs that of product customers.

But building a B2B platform requires patience that most companies lack. It took years for customers to trust Thermo Fisher with mission-critical services like clinical trials. It required massive upfront investments in capabilities that wouldn't pay off immediately. It meant accepting lower margins initially to build scale. Most importantly, it required resisting the temptation to exploit lock-in too aggressively, which would destroy trust.

Operational Excellence as Core Competency

In an era obsessed with disruption and innovation, Thermo Fisher has built enormous value through operational excellence—doing ordinary things extraordinarily well. Their competitive advantage isn't breakthrough technology or proprietary algorithms; it's the ability to deliver products on time, answer service calls quickly, and integrate acquisitions smoothly.

This operational focus permeates the organization. The company's PPI Business System (Practical Process Improvement) isn't just corporate jargon—it's a comprehensive approach to continuous improvement that touches every employee. Warehouse workers track picking accuracy. Service technicians measure first-call resolution rates. Integration teams monitor synergy realization. What gets measured gets managed, and what gets managed gets better.

The compound effect of operational excellence is profound. A 1% improvement in inventory turns across a $40 billion company releases hundreds of millions in working capital. A 2% improvement in service efficiency allows technicians to handle more calls without hiring. These aren't transformational changes—they're incremental improvements that compound over decades into insurmountable advantages.

Critically, operational excellence becomes self-reinforcing. Customers choose Thermo Fisher not because they're cheapest or most innovative, but because they're reliable. This reliability premium allows higher margins, which fund further operational improvements, which enhance reliability further. It's a virtuous cycle that's nearly impossible for competitors to break.

Customer Intimacy at Scale: The Ultimate Paradox

Conventional strategy suggests companies must choose between customer intimacy and operational scale. Thermo Fisher has achieved both through a carefully orchestrated model that combines high-touch relationships with standardized operations. It's mass customization applied to B2B services.

The model starts with segmentation—not by industry or size, but by customer need complexity. A small biotech with a novel drug needs extensive hand-holding; a large pharma buying routine supplies needs efficient transactions. Resources are allocated accordingly, with dedicated teams for strategic accounts and self-service options for transactional purchases.

Technology enables intimacy without sacrificing efficiency. Customer portals remember purchase history and suggest reorders. Account managers have visibility into all customer touchpoints across the enterprise. Predictive analytics identify when customers might need support before they ask for it. It's algorithmic intimacy—using data to appear more personal while actually being more systematic.

The real innovation is making customers feel like partners rather than purchasers. Thermo Fisher employees work on-site at major accounts. They attend customer planning meetings. They understand not just what customers buy but why they buy it. This deep integration creates switching costs that go beyond the financial—replacing Thermo Fisher would mean replacing trusted advisors who understand the business.

The Picks-and-Shovels Thesis Validated

The California Gold Rush maxim—sell picks and shovels to miners rather than mining yourself—has become a Silicon Valley cliche. But Thermo Fisher represents perhaps the purest expression of this strategy in modern business. They don't develop drugs; they enable drug development. They don't treat patients; they enable treatment. They capture value from innovation without bearing innovation risk.

This positioning provides remarkable resilience. When drug development fails—and it usually does—Thermo Fisher has already been paid for their services. When it succeeds, they participate through volume growth without bearing regulatory risk. They benefit from pharmaceutical innovation regardless of which companies or technologies win.

The strategy extends beyond risk mitigation to value capture. Pharmaceutical companies spend roughly 20% of revenue on R&D, and a significant portion flows to companies like Thermo Fisher. As drug development becomes more complex and expensive, more of that spending goes to specialized service providers rather than internal capabilities. Thermo Fisher is perfectly positioned to capture an increasing share of an expanding pie.

Management Quality: The Casper Doctrine

Marc Casper's leadership represents a masterclass in long-term value creation. Since becoming CEO in 2009, he's overseen a five-fold increase in revenue and an eight-fold increase in market capitalization. But more impressive than the results is the consistency of approach—no pivots, no transformations, just relentless execution of a clear strategy.

Casper's background—Bain consultant turned operator—shows in his analytical approach to strategy and disciplined approach to execution. Every major decision can be traced back to core principles: strengthen the platform, serve customers better, create shareholder value. This consistency allows the organization to move fast because everyone understands the decision framework.

The cultural elements Casper emphasizes seem mundane but prove powerful. Customer focus isn't just rhetoric—executive compensation is tied to customer satisfaction scores. Operational excellence isn't just aspiration—every employee has metrics tied to process improvement. Innovation isn't just R&D spending—it's embedded in how every function operates.

Perhaps most importantly, Casper has built a deep bench of leadership talent. The executives running major divisions could be CEOs elsewhere. The integration teams include future general managers. This talent depth enables simultaneous execution of multiple complex initiatives—integrating PPD while acquiring Olink while expanding in China. It's organizational capacity that compounds like financial capital.

Timing Markets: Playing the Long Game

While Thermo Fisher doesn't explicitly time markets, their major moves have demonstrated remarkable timing. The 2006 merger came just before the biotech boom. The Life Technologies acquisition captured the genomics revolution. Patheon positioned them for the outsourcing wave. PPD capitalized on COVID-driven clinical trial demand.

This isn't luck—it's patient opportunism. Thermo Fisher tracks markets and companies for years before acting. They build relationships with targets long before making offers. They maintain financial flexibility to move when opportunities arise. When markets dislocate—2008, 2020—they're buyers, not sellers.

The key insight is that in B2B markets, timing isn't about predicting inflection points but about positioning for inevitable trends. Pharmaceutical outsourcing wasn't a sudden shift but a gradual evolution over decades. Precision medicine wasn't a breakthrough but a convergence of multiple technologies. By positioning early for obvious long-term trends, Thermo Fisher appears prescient when they're really just patient.

The platform strategy provides another timing advantage: optionality. Because Thermo Fisher serves every part of the pharmaceutical value chain, they benefit regardless of which trends accelerate. If small molecule drugs resurge, they have the capabilities. If cell therapy dominates, they're ready. If AI transforms drug discovery, they'll provide the instruments and services to enable it. It's strategic positioning that doesn't require precise timing—just conviction that science will advance and complexity will increase.

X. Analysis & Bear vs. Bull Case

Bull Case: The Compounding Machine

The bull case for Thermo Fisher starts with a simple observation: they've become systemically important to global pharmaceutical development. Like Microsoft in enterprise software or TSMC in semiconductors, their embedded position creates competitive advantages that compound over time. The more critical they become, the harder they are to displace, which allows them to capture more value, which funds further entrenchment.

The secular tailwinds are undeniable and accelerating. Global healthcare spending will reach $18 trillion by 2030, driven by aging populations, rising wealth in emerging markets, and continuous scientific advancement. More importantly, the complexity of drug development is increasing exponentially. Cell and gene therapies require entirely new development and manufacturing paradigms. Precision medicine demands sophisticated diagnostics and companion tests. AI-driven drug discovery will generate thousands of candidates requiring validation. Each increase in complexity strengthens Thermo Fisher's position as the essential infrastructure provider.

The platform dynamics create winner-take-most economics. The primary driver behind last 12 months revenue was the Laboratory Products and Biopharma Services segment contributing a total revenue of US$23.2b (54% of total revenue). As this segment grows, it pulls through demand for analytical instruments, diagnostics, and consumables. Every customer added to one service becomes a cross-selling opportunity for others. Every acquisition strengthens the platform's gravitational pull. Competitors can match individual products but can't replicate the ecosystem.

The financial model has proven remarkably resilient through cycles. Full year revenue was $42.88 billion, flat versus prior year, but this masks underlying strength as the company cycled through COVID comps. The ability to maintain margins while integrating massive acquisitions demonstrates operational excellence that's difficult to replicate. With annual revenue over $40 billion and a proven ability to deploy capital at attractive returns, the company has multiple levers for value creation.

The mission alignment with global health trends provides both purpose and profit. Our Mission is to enable our customers to make the world healthier, cleaner and safer. This isn't corporate platitude—it's strategic positioning. As governments and societies prioritize health infrastructure, pandemic preparedness, and environmental monitoring, Thermo Fisher benefits from policy support and public investment. They're selling what the world needs more of.

Management quality and execution consistency provide confidence in long-term value creation. Under Marc Casper's leadership since 2009, the company has navigated multiple cycles, integrated transformative acquisitions, and consistently exceeded targets. The deep bench of talent and proven playbooks suggest this execution can continue even through leadership transitions.

Bear Case: The Risks Hiding in Plain Sight

The bear case begins with valuation. After years of multiple expansion, Thermo Fisher trades at premium multiples that embed high expectations for growth and margin expansion. Any disappointment—a failed acquisition, integration hiccup, or market slowdown—could trigger significant multiple compression. The stock has become a "crowded long" among institutional investors, amplifying downside risk if sentiment shifts.

Customer concentration presents underappreciated risk. While Thermo Fisher serves hundreds of thousands of customers, the top 20 pharmaceutical companies drive an outsized portion of revenue and profits. These sophisticated buyers have recognized their dependence on Thermo Fisher and are actively working to maintain competitive alternatives. Some are insourcing previously outsourced activities. Others are funding competitors to ensure supply diversity. The customer base that created Thermo Fisher's moat could also breach it.

The acquisition strategy, while successful historically, faces mathematical limits. As Thermo Fisher grows larger, finding acquisitions that move the needle becomes harder. The PPD deal at $17.4 billion may have exhausted large-scale opportunities in core markets. Future growth will increasingly depend on organic expansion, where Thermo Fisher's track record is less exceptional. The company must also integrate these massive acquisitions while maintaining operational excellence—a challenge that grows with each deal.

Technological disruption, while often overstated, presents real risks. AI and automation could commoditize some analytical services. Distributed manufacturing technologies could reduce reliance on centralized CDMOs. Synthetic biology could simplify drug production. While Thermo Fisher would likely adapt to these changes, the transition could pressure margins and require massive reinvestment.

Geopolitical risks are rising and particularly acute for Thermo Fisher. Asia Pacific generated $7.96 B in revenue, representing 18.55% of its total revenue. China represents both a growth opportunity and a vulnerability. Rising tensions could force customers to diversify supply chains away from any single provider. National security concerns about biotechnology could restrict Thermo Fisher's ability to serve certain markets or acquire certain technologies.

Regulatory changes could fundamentally alter the business model. Drug pricing reform could pressure pharmaceutical R&D budgets, flowing through to reduced demand for Thermo Fisher's services. Changes to FDA approval processes could alter clinical trial requirements. Environmental regulations could increase costs for chemical and biological manufacturing. While Thermo Fisher has navigated regulatory changes before, the political focus on healthcare costs creates unprecedented uncertainty.

The hidden risk might be success itself. Thermo Fisher has become so essential to pharmaceutical development that they're attracting scrutiny. Customers worry about dependency. Regulators question market concentration. Competitors collaborate to provide alternatives. The moat that protects the business also makes it a target.

The Balanced View: Exceptional Business, Full Valuation

The reality is that both cases have merit. Thermo Fisher has built one of the great B2B platforms of our time, with competitive advantages that would take decades and tens of billions of dollars to replicate. The secular growth drivers are real and accelerating. Management has proven exceptional at capital allocation and operational execution.

But excellence is increasingly priced in. The stock market has recognized what Thermo Fisher has built, and multiples reflect expectations for continued exceptional execution. The margin of safety that existed when the company was seen as just an equipment supplier has evaporated. Today's investors are betting on flawless execution of an increasingly complex strategy.

The key question isn't whether Thermo Fisher is a good business—it's exceptional. The question is whether it's a good investment at current valuations. For long-term investors who believe in the secular trends and management's ability to execute, the premium might be justified. For value investors seeking asymmetric risk-reward, the opportunity may have passed.

What's certain is that Thermo Fisher will remain central to how science gets done for decades to come. Whether that centrality translates to superior investment returns depends on execution, valuation, and the unpredictable evolution of technology and regulation. The company has earned the benefit of the doubt through consistent execution, but in investing, past performance really doesn't guarantee future results.

XI. Epilogue & "If We Were CEOs"

The Next Chapter: Where Does Thermo Fisher Go From Here?

Standing at the helm of a $40 billion revenue colossus with dominant positions across the life sciences value chain, the strategic options for Thermo Fisher's next decade are both expansive and constrained. The company has essentially won the horizontal integration game in traditional life sciences tools and services. The question now is whether to go deeper, go broader, or go somewhere entirely new.

The obvious path is deeper vertical integration into areas adjacent to current capabilities. Artificial intelligence and machine learning for drug discovery represents a $50 billion market by 2030 where Thermo Fisher could leverage its data advantage. Every instrument they've sold, every clinical trial they've run, every drug they've manufactured generates data. Properly integrated and analyzed, this could become the foundation for AI-driven services that don't just support drug development but actively direct it.

Cell and gene therapy manufacturing remains subscale and artisanal, exactly the kind of fragmented market Thermo Fisher has successfully consolidated before. These therapies require entirely new manufacturing paradigms—living cells as factories, viruses as delivery vehicles, patient-specific production runs. The company's recent investments suggest they see this opportunity, but the full strategic commitment would require acquisitions and investments in the tens of billions.