Mr. Cooper Group: From Ashes to America's Largest Mortgage Servicer

I. Introduction & Episode Roadmap

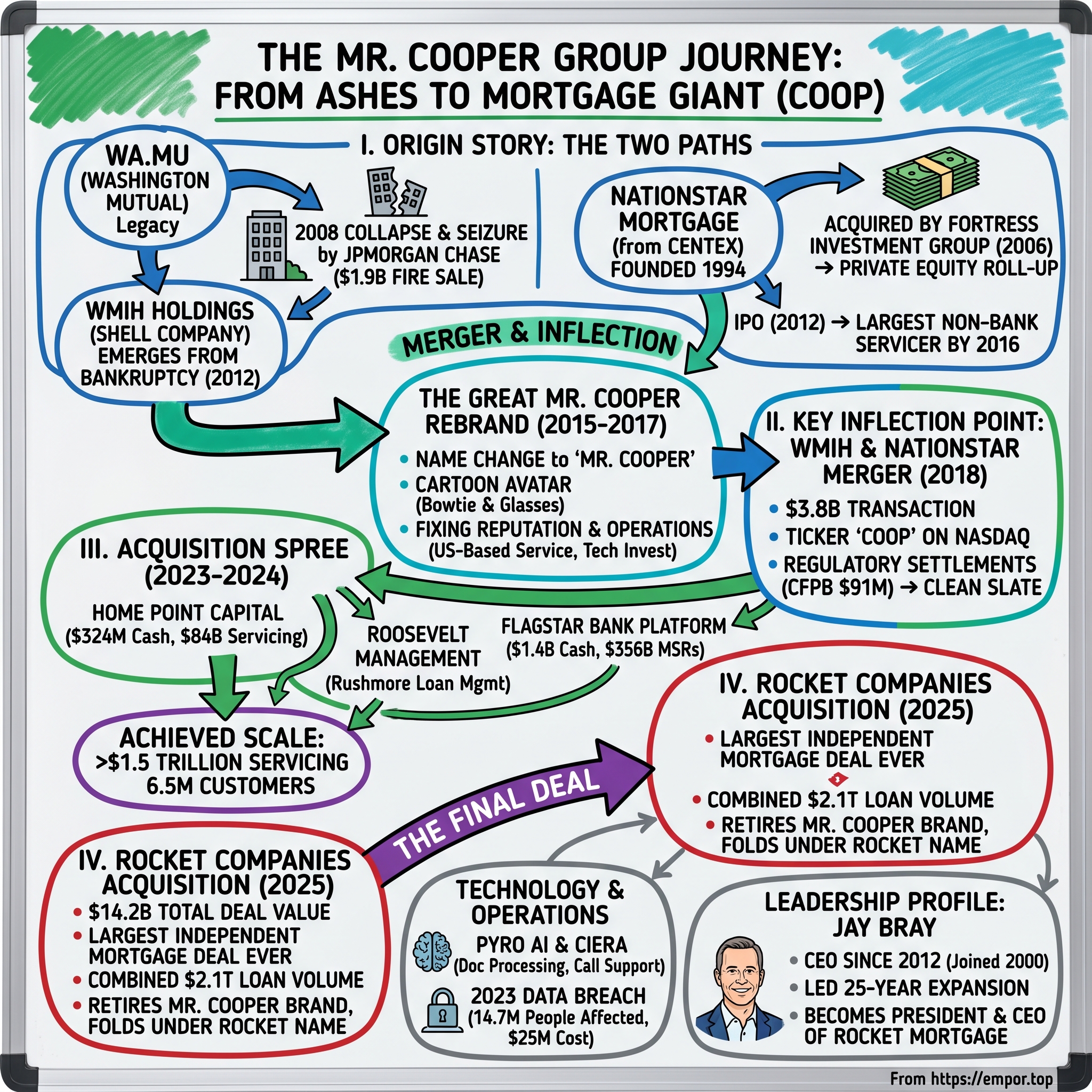

Picture the unlikely journey: a company born from the ashes of the largest bank failure in American history merges with a scrappy subprime mortgage servicer founded in a Denver garage, rebrands around a fictional cartoon avatar wearing a turquoise bowtie, and ultimately gets acquired in the largest independent mortgage deal ever. This is the story of Mr. Cooper Group—and it reads like a fever dream of American capitalism.

As of the first quarter of 2025, Mr. Cooper Group's servicing portfolio had grown by 33% year-over-year, reaching $1.514 trillion. The company served over 6.5 million customers. That staggering scale represents one of the most remarkable corporate transformations in modern financial services history.

The question that animates this story: How did a subprime mortgage originator become the nation's largest independent mortgage servicer, and how does the wreckage of the largest bank failure in U.S. history tie into this narrative?

The answer involves understanding the peculiar corporate lineage of Mr. Cooper Group. WMI Holdings Corporation was incorporated as the Washington National Building Loan and Investment Association on September 25, 1889, after the Great Seattle Fire destroyed 120 acres of the central business district of Seattle. The newly formed company made its first home mortgage loan on the West Coast on February 10, 1890. That company would eventually become Washington Mutual—the poster child for subprime lending excess—before its catastrophic collapse in 2008.

Meanwhile, the initial establishment of what would become Mr. Cooper Group occurred in Denver, Colorado, in 1994, under the name Nova Credit Corporation. This modest company would be transformed by private equity, taken public, and ultimately merged with the zombie shell of Washington Mutual to create something entirely new.

Rocket Companies has officially completed its $14.2 billion acquisition of Mr. Cooper Group, marking the largest independent mortgage deal in U.S. history and creating a new dominant player that combines origination, servicing, and real estate search under one brand.

The themes woven through this story illuminate broader truths about modern American finance: the opportunity that flows from crisis, the private equity playbook for roll-ups and consolidation, the power of rebranding to reshape perception, and the relentless logic of scale in industries defined by razor-thin margins and regulatory complexity.

II. Origin Story Part 1: Washington Mutual & The 2008 Financial Apocalypse

The WaMu Legacy

To understand Mr. Cooper Group, you must first understand the institution whose corporate shell gave it life. Washington Mutual didn't start as a reckless subprime lender. During most of the 119 years after its founding, the bank had a reputation as a prudently run institution that stashed away money in good times in order to weather bad ones. It began a student saving program in the 1920s, bailed out the Continental Mutual Savings Bank during the Depression (its first acquisition of another bank), and pioneered The Exchange, the nation's first shared cash-machine network, in the 1970s.

The transformation began in the 1980s. Washington Mutual began to show larger ambitions, acquiring the Spokane-based brokerage firm Murphey Favre and converting from mutual ownership to a publicly traded company on March 11, 1983. A Murphey Favre executive, Kerry Killinger, quickly climbed the Washington Mutual corporate ladder and was CEO by 1990. He put the bank on a path of rapid expansion, as it acquired more than two-dozen other financial firms in the Northwest and as far afield as New York and Phoenix.

By 2001, WaMu, as it was by then universally known, was the largest mortgage originator in the country.

Killinger articulated a vision that would prove fatally ambitious. He said "We hope to do to this industry what Walmart did to theirs, Starbucks did to theirs, Costco did to theirs and Lowe's-Home Depot did to their industries." The idea was to democratize banking—to serve customers other banks ignored. The execution proved disastrous.

Under Kerry Killinger's leadership as CEO, Washington Mutual shifted toward high-growth lending in the early 2000s, emphasizing volume over traditional underwriting rigor to expand market share amid rising housing demand. This transition accelerated after the 1999 acquisition of subprime lender Long Beach Mortgage, which marked WaMu's entry into riskier loan segments, followed by increased subprime production starting in 2003 with $4.5 billion securitized that year, rising to $29 billion by 2006.

On June 30, 2008, WaMu had total assets of $307 billion, with 2,239 retail branch offices operating in 15 states, with 4,932 ATMs, and 43,198 employees. It held liabilities in the form of deposits of $188.3 billion, and owed $82.9 billion to the Federal Home Loan Bank, and had subordinated debt of $7.8 billion.

The Subprime Crisis & Bank Run

The institution Killinger built was a house of cards, and the housing collapse that began in 2006 set those cards tumbling. As the biggest bank in United States history to fail, WaMu became the poster child for subprime lending, originating and securitizing hundreds of billions of dollars in high-risk, low-quality mortgages. In fact, its CEO, Kerry Killinger, proudly described his company as the "Walmart of Banking" because it focused on the lower- and middle-class customers.

The internal culture at WaMu rewarded volume over prudence. Washington Mutual was rewarding its loan officers for the volume of loans they approved as well as how quickly they approved them. They often overcharged customers—no one seemed to care. The most productive loan officers gained entrance into the "President's Club," where they received perks and bonuses, such as all-expense paid trips to Hawaii. CEO Killinger himself made $25 million in 2008, the year his company failed.

Senator Carl Levin, chairman of the Senate Subcommittee investigating the crisis, captured the essence of WaMu's business model with damning precision: the bank had built "a conveyor belt of toxic mortgages to feed Wall Street's appetite for mortgage-backed securities."

By mid-2008, confidence in WaMu was collapsing. From that date through September 24, 2008, WaMu experienced a bank run whereby customers withdrew $16.7 billion in deposits over those nine days, and in excess of $22 billion in cash outflow since July 2008, both conditions which ultimately led the Office of Thrift Supervision to close the bank.

The Seizure & JPMorgan Chase Fire Sale

On the afternoon of September 25, 2008, Washington Mutual, the nation's largest savings and loan bank, was seized by the federal Office of Thrift Management. It is the largest bank failure in United States history.

The speed of the collapse was breathtaking. Normally, bank seizures take place after the close of business on Fridays. However, due to the bank's deteriorating condition and leaks that a seizure was imminent, regulators felt compelled to act a day early.

Under the deal, JPMorgan Chase acquired all the banking operations of WaMu, including $307 billion in assets and $188 billion in deposits, for a price of $1.9 billion plus debt assumptions. That price—roughly 62 cents per $100 of assets—reflected the toxic nature of WaMu's loan portfolio. Jamie Dimon, JPMorgan's CEO, had been circling WaMu for months. In March 2008, on the same weekend that JPMorgan Chase Chairman and CEO Jamie Dimon negotiated the takeover of Bear Stearns, he secretly dispatched members of his team to Seattle to meet with WaMu executives, urging them to consider a quick deal. However, WaMu Chairman and CEO Kerry Killinger rejected JPMorgan Chase's offer that valued WaMu at $8 a share.

Six months later, Dimon got his prize at a fraction of the price.

The WaMu collapse was devastating for equity investors who had held on to the end and for bondholders. Both were wiped out. WaMu stock, which had traded as high as $45.91 a share in 2006, stood at 16 cents when the New York Stock Exchange halted trading in the shares.

But the story doesn't end with the seizure. On September 26, 2008, Washington Mutual, Inc. and its remaining subsidiary, WMI Investment Corp., filed for Chapter 11 bankruptcy. The company was promptly delisted from trading on the New York Stock Exchange, and commenced trading via Pink Sheets.

The holding company was left with assets, tax attributes, and ongoing litigation claims—a zombie entity searching for resurrection.

The Shell Company Waiting Game

A seventh plan of reorganization was announced in February 2012 and the company finally emerged from Chapter 11 bankruptcy the following month as WMI Holdings Corporation. By 2015, WMI Holdings was able to raise $598 million and was looking for new acquisitions.

On March 19, 2012, WMIH emerged from bankruptcy proceedings as the successor to Washington Mutual, Inc. Upon emergence from bankruptcy, WMIH had limited operations other than WMMRC's legacy reinsurance business, which is being operated in runoff mode and has not written any new business since September 26, 2008.

This shell company—with its valuable tax assets and cash—was an acquisition vehicle waiting for a target. The story of how it found that target requires us to turn to an entirely different narrative thread: the rise of Nationstar Mortgage.

III. Origin Story Part 2: Nationstar's Rise from Centex

The Centex Years (1994-2006)

While Washington Mutual was building its subprime empire in Seattle, a much smaller company was taking shape in the Mountain West. Nationstar was founded as Nova Credit Corporation in Denver, Colorado in 1994.

In 1997, the company relocated to Dallas, Texas, following its acquisition by Centex Homes, and was subsequently renamed Centex Credit Corporation. Centex Homes was one of the nation's largest homebuilders, and Nova Credit Corporation became their in-house financing arm—the captive lender that helped Centex customers close on their newly built homes.

In 2001, Centex Credit Corporation was merged into Centex Home Equity Company, LLC, a Delaware limited liability company (CHEC). In 2006, our Initial Stockholder acquired all of its outstanding membership interests (the Acquisition), and CHEC changed its name to Nationstar Mortgage LLC.

The company operated as Centex's subprime mortgage originator and servicer until 2005, when Centex made a strategic decision to refocus on its core homebuilding business. In 2005, the decision was made to withdraw Centex Homes from non-home-building businesses, including the mortgage business.

The Fortress Acquisition & Private Equity Transformation

Enter Fortress Investment Group—the private equity firm that would transform a captive homebuilder lender into a national mortgage servicing powerhouse.

Fortress Investment Group acquired Centex Home Equity and renamed it Nationstar Mortgage in 2006. Per Fortress' website, its initial outlay for Nationstar was $450 million.

The timing was critical. Fortress saw something others missed: while mortgage origination was about to collapse as the housing bubble burst, mortgage servicing—the mundane business of collecting payments, managing escrow accounts, and working out delinquent loans—was poised to explode. The coming wave of distressed mortgages would need servicers with the infrastructure and expertise to handle modifications, forbearance agreements, and foreclosures.

Mortgage servicing possesses characteristics that appeal to sophisticated investors: counter-cyclical cash flows (when rates rise and originations collapse, existing servicing portfolios become more valuable), regulatory complexity that creates barriers to entry, and massive scale economics (the cost to service one additional loan is minimal once the infrastructure exists).

The 2008 crisis became Nationstar's tailwind. As banks retreated from mortgage servicing, regulatory pressure intensified, and massive portfolios of distressed mortgages needed management, Nationstar was positioned to absorb the excess.

Going Public & Scaling Up

In March 2012, Nationstar Mortgage Holdings, Inc. went public with an initial public offering on the New York Stock Exchange.

The IPO prospectus revealed a company laser-focused on growth. We believe the greatest opportunities will be available to servicers with the proven track record, scalable infrastructure and range of services that can be applied flexibly to address different organizations' needs. To position ourselves for these opportunities, since 2010 we have expanded our business development team and hired a dedicated senior executive whose primary role is to identify, evaluate, and enhance acquisition and partnership opportunities across the mortgage industry. We have also expanded and enhanced our loan transfer, collections and loss mitigation infrastructure in order to be able to accommodate substantial additional growth. We expect these efforts to position us to be a key participant in the long term restructuring and recovery of the mortgage sector.

That positioning paid off. After its IPO in March 2012, Nationstar Mortgage introduced Xome, an online real estate marketplace. By 2016, Nationstar had become the largest non-bank mortgage servicer in the United States.

Fortress is also the majority shareholder in Nationstar Mortgage, soon to be known as Mr. Cooper. Per the latest data from Nasdaq, Fortress owns nearly 70% of Nationstar.

Fortress's playbook worked brilliantly: buy a distressed asset cheaply, invest in operational infrastructure, roll up competitors, grow to scale, and then monetize the investment through a public offering or sale. But Nationstar had a problem—its reputation.

IV. Key Inflection Point #1: The Mr. Cooper Rebrand (2015-2017)

Why Rebrand? The Reputation Problem

This tale begins with a company called Nationstar Mortgage. Based in Coppell, Nationstar had a reputation — not a good one. The company was slapped with more than a thousand lawsuits, many from furious customers who claimed their homes were wrongly foreclosed.

The former Nationstar was among the most complained-about companies, according to the Consumer Financial Protection Bureau's reports on consumer complaints. Nationstar was also previously hit by the Bureau with the largest civil penalty ever imposed, in the amount of $1.75 million, for Home Mortgage Disclosure Act violations.

The timing of the rebranding announcement was telling. In August 2017, Nationstar Mortgages, LLC, announced it was changing its name to Mr. Cooper after releasing its worst financial report to date. In 2017, after the company released its worst financial report ever, it announced that it would go by the name of Mr. Cooper.

The question every business school case study would ask: when a company has both operational problems and a damaged reputation, do you fix operations first, or do you rebrand to buy yourself time? Nationstar chose to do both simultaneously—an ambitious gamble.

The Transformation Journey

The rebrand wasn't a quick coat of paint. The newly combined company will also lean hard into the Mr. Cooper brand, which Nationstar officially adopted last year and began moving toward way back in 2015. The process took nearly two years because, according to company communications, they weren't just rebranding—they were reinventing everything.

The company made substantive changes: moving customer service operations back to the United States, eliminating fees for on-time online payments, investing over $90 million in technology and infrastructure, and completing more than 50,000 hours in customer service training. Mr. Cooper's spokeswoman told me in her emailed answers that your new company rebranding and staff retraining has "led to a 70 percent reduction in customer complaints since 2016."

The Mr. Cooper Identity

The name itself was radical—and intentionally so. CEO Jay Bray said at the 2017 introduction that the avatar was "a bit radical." "We want to make an emotional connection," he said.

The visual identity featured a cartoonish avatar—a hipster-looking character with wide-rimmed glasses and a turquoise bowtie. He's an avatar. The cartoonish Mr. Cooper cuts a quirky figure with his headphones, wide-rimmed glasses and turquoise-colored bowtie.

The company stated that the name change was meant to "personalize the mortgage experience". The idea was to evoke the friendly neighborhood milkman or mailman—a trusted figure who shows up reliably. Think of it as the mortgage industry's version of "Flo from Progressive" or the Geico Gecko—an attempt to humanize an industry that customers often experience as faceless and frustrating.

Marketing professors were intrigued. SMU marketing adjunct professor Brenda Demith told me, "What they wanted was that cache of making it seem like he was a real person instead of a conglomerate, a big company that thinks of you as a number."

The rebranding was a calculated bet that perception could be reshaped, that operational improvements combined with a fresh identity could give the company a second chance. The jury remains out on whether a leopard can change its spots, but the rebrand bought Nationstar the time and space to pursue the next phase of its transformation.

V. Key Inflection Point #2: The WMIH Merger (2018)

The Deal Structure

In 2018 Nationstar and WMI Holdings Corporation (WMIH), the corporate successor to the defunct Washington Mutual, merged. As a result Nationstar was delisted from the New York Stock Exchange and WMIH changed its name to Mr. Cooper Group.

The companies did not provide specific financial details, but the deal's original announcement pegged the merger as a $3.8 billion transaction.

Under the terms of the agreement, Nationstar shareholders may choose to receive $18 in cash or 12.7793 shares of WMIH common stock for each share of Nationstar common stock they currently own. Nationstar stock closed Monday's trading at $17.10, while WMIH closed Monday's trading at $0.80.

Upon completion of the deal, Nationstar shareholders will own approximately 36% of the combined company and WMIH shareholders will own approximately 64%.

The structure was ingenious. WMIH was a shell company with valuable tax attributes and cash, but no operating business. Nationstar was an operating company with a damaged reputation. By merging Nationstar into WMIH and adopting the Mr. Cooper brand, the combined entity could claim a fresh start—both psychologically and (to some degree) legally.

Why This Deal Made Sense

For Fortress, the deal represented a partial exit. Fortress, which was acquired late last year by SoftBank Group in a $3.3 billion deal, is cashing out roughly half of its Nationstar shares. Fortress currently owns approximately 68.1 million shares of Nationstar's stock, or 71.06% of the company. Fortress has agreed to the deal and is taking cash for approximately 34 million of its shares. At $18 per share, Fortress will take away roughly $612 million in the deal and will maintain ownership of roughly half of its shares.

Compare that $612 million payout to Fortress's initial $450 million investment. Even after cashing out half, Fortress retained substantial equity in a company positioned to continue consolidating the mortgage servicing industry.

The combined company will have more than 3 million customers and is one of the nation's largest mortgage servicers, combining its own portfolio with subservicing contracts from several large operators.

WMIH changed its name to Mr. Cooper Group Inc., and began trading on NASDAQ under the ticker symbol 'COOP' on October 11, 2018.

Regulatory Settlements & Clean Slate

The rebranding didn't make the regulatory challenges disappear—they had to be addressed. Cooper paid out millions of dollars in settlements in New York and California due to various violations of state banking laws. In 2020, Mr. Cooper agreed to a $91 million settlement with the CFPB.

In 2020, Mr. Cooper agreed to pay $91 million to settle a case brought by the U.S. Consumer Protection Bureau over improper foreclosures. Most of the money was returned to victims. The company paid states $110 million to settle more claims and another $5.8 million to settle a class action lawsuit.

The CFPB settlement was significant not just for its size, but for its scope. In 2014, the Iowa state Attorney General formed a multistate coalition to investigate the company over a series of complaints regarding mortgage servicing issues. According to the lawsuit, in 2012, the company—then operating as Nationstar—began purchasing mortgage servicing portfolios from competitors, which allowed it to quickly grow into the nation's largest non-bank servicer.

The settlements cleared the legal overhang and allowed management to focus on growth. In 2020, Mr. Cooper originated over 146,000 mortgages with a total value of over $36 billion.

VI. Key Inflection Point #3: The Acquisition Spree (2023-2024)

Home Point Capital Acquisition

With its regulatory house in order and its operations humming, Mr. Cooper went on an acquisition tear. Mr. Cooper Group Inc. and Home Point Capital Inc. announced the signing of a definitive agreement for Mr. Cooper to acquire all outstanding shares of Home Point for approximately $324 million in cash.

Homepoint was the third largest wholesale lender in the country, following behind United Wholesale Mortgage (UWM) and Rocket Mortgage. Amid high mortgage rates, low inventory and fierce competition, Homepoint's overall origination came in at $27.7 billion in 2022, a 71.6% decline compared to 2021.

In total, Mr. Cooper is acquiring Home Point's $84 billion servicing portfolio, which will contribute to Mr. Cooper's return on equity with an estimated 10% increase to operating earnings in the first year.

Approximately 98.5% of the shares outstanding were tendered. All of the conditions of the offer have been satisfied, and Mr. Cooper has accepted for payment for $2.33 per share.

The Home Point deal exemplified Mr. Cooper's opportunistic strategy: acquiring distressed competitors whose high fixed costs made them vulnerable in a difficult rate environment. Mr. Cooper's scale made integration economics work that wouldn't pencil for smaller acquirers.

Roosevelt Management Company Acquisition

In July 2023, the Company also acquired all the equity interests of Roosevelt Management Company, including Rushmore Loan Management Services.

The Roosevelt acquisition added a different capability: third-party capital management. The private New York-based company, founded in 2008, manages capital on behalf of insurance companies, pension funds, hedge funds and other investors—providing Mr. Cooper with diversified revenue streams beyond traditional servicing.

Flagstar Acquisition

The biggest deal of the 2023-2024 cycle came in late 2024. Mr. Cooper Group has struck a deal to acquire a third-party origination (TPO) platform and $356 billion in mortgage servicing rights (MSRs), advances and subservicing contracts from Flagstar Bank, owned by New York Community Bancorp (NYCB). As part of the deal, the Dallas-based servicer and lender will pay $1.4 billion in cash. The transaction, which will add 1.3 million customers to Mr. Cooper, is expected to close in the fourth quarter of 2024.

The pending transaction appears to be the largest mortgage M&A deal of the 2022-2024 cycle, and represents a TPO exit for NYCB/Flagstar, which has been a player in the space since 1987.

The deal illustrated a broader industry dynamic: regulated banks increasingly prefer to exit mortgage servicing, which carries regulatory complexity and interest rate risk. NYCB recognized "the inherent financial and operational risk in a volatile interest rate environment, along with increased regulatory oversight for such businesses."

The transaction included acquisition of MSRs, advances, subservicing contracts, and Flagstar's third-party origination platform for approximately $1.3 billion in cash. Mr. Cooper's Chairman and CEO Jay Bray commented, "This acquisition demonstrates our ability to deliver full-service solutions to financial institutions and other clients, helping them manage their balance sheet and legacy and ongoing operations to achieve their strategic goals. We welcome Flagstar's customers, clients, and team members to Mr. Cooper and expect to fully integrate operations onto our platform during early 2025."

Scale Achievement

Mike Weinbach, Mr. Cooper Group President, added, "We now serve more than 6 million customers, and for every single customer we are dedicated to keeping the dream of homeownership alive."

The acquisition spree accomplished what Jay Bray had long targeted: "This acquisition adds scale to our platform, bringing us closer to our $1 trillion strategic target, while enhancing returns due to attractive yields and positive operating leverage," Jay Bray said in a news release announcing the deal.

By early 2025, Mr. Cooper had exceeded that $1 trillion target and established itself as the undisputed largest non-bank mortgage servicer in America. The stage was set for the final act.

VII. Key Inflection Point #4: The Rocket Companies Acquisition (2025)

The Deal Announcement

On March 31, 2025, the mortgage industry received seismic news. Rocket Companies (NYSE: RKT), the Detroit-based fintech platform including mortgage, real estate, title and personal finance businesses, announced a definitive agreement to acquire Mr. Cooper.

The acquisition was an all-stock transaction for $9.4 billion in equity value, based on an 11.0x exchange ratio. Under the terms of the agreement, Mr. Cooper shareholders will receive a fixed exchange ratio of 11.0 Rocket shares for each share of Mr. Cooper common stock. This represents a $143.33 per share value based on the closing price as of March 28, 2025, and a premium of 35% over the volume weighted average price (VWAP) of Mr. Cooper's common stock for the 30 days ending March 28, 2025.

Rocket Companies has closed its acquisition of Mr. Cooper for $14.2 billion. The final acquisition price is 51 percent higher than the $9.4 billion price tag announced in March, due to Rocket's recent stock rally.

The largest independent mortgage deal in history unites America's leading originator with the nation's top servicer to transform homeownership for America.

Strategic Rationale

The industrial logic was compelling. Combined company to service more than $2.1 trillion in loan volume. Integrating Rocket's originations-servicing recapture flywheel with Mr. Cooper's servicing platform will drive down costs and improve the experience for the companies' nearly 10 million combined clients, representing one in every six mortgages.

The mortgage business has long struggled with a fundamental problem: originators acquire customers at great expense, then lose them when they refinance with a competitor. Servicers have the customer relationship but often lack the origination capability to capture refinancing business. Rocket Mortgage has ranked #1 in J.D. Power's mortgage servicer study for 10 years and #1 in mortgage origination 12 times, driving the company's 83% recapture rate – triple the industry average. With a significantly larger servicing portfolio, Rocket is poised to sustain its industry-leading retention and recapture rates.

By combining Rocket's origination dominance with Mr. Cooper's servicing scale, the merged entity can capture customers throughout their entire homeownership lifecycle.

Leadership Transition

By integrating Mr. Cooper's servicing strength with Rocket's origination capabilities and AI technology and established strong national brand, our goal is to lower costs and make the process easier. After 25 years driving the expansion and culture of Mr. Cooper, Jay Bray will join Rocket as the new President and CEO of Rocket Mortgage.

"This transaction brings to a close a multi-year journey during which Mr. Cooper grew to become the nation's largest servicer and produced enormous value for our clients, partners, stakeholders and investors," Bray said. "Now, by joining forces with Rocket, we start a new journey, which I believe offers an even bigger opportunity. Through the power of our platform and our people, we will create a more personalized experience that makes owning a home more attainable and easier to navigate. Together, we will deliver the change the housing industry needs."

Going forward, the company is retiring the Mr. Cooper branding and folding all operations and services under the Rocket name.

The fictional Mr. Cooper avatar—born to help Nationstar escape its troubled past—will not survive the merger. The brand served its purpose: transforming perception, enabling consolidation, and ultimately creating something valuable enough to attract a $14.2 billion bid.

VIII. Technology & Operations Deep Dive

The Servicing Platform

What made Mr. Cooper valuable enough to command the largest independent mortgage deal in history? Beyond scale, the answer lies in the operational infrastructure and technology platform the company built.

Key offerings include: mortgage servicing (comprehensive servicing solutions enhancing customer experience through innovative tools and personalized service), subservicing (managing mortgage loans on behalf of other financial institutions), private label subservicing, special servicing (targeted assistance for homeowners facing financial difficulties), master servicing, and direct-to-consumer originations.

Mr. Cooper's technology investments centered on Pyro AI, the company's patented artificial intelligence and machine learning platform. Under his leadership, Mr. Cooper developed Pyro AI, its patented artificial intelligence and advanced machine learning platform, and built an industry-leading digital platform, among other award-winning innovations that have driven the company's ability to grow and achieve best-in-class customer service and recapture rates.

So if you look at just 2023, we processed about 70 million documents and we have a 25 member team that does exception handling and retraining of documents. The broader point is, we have been building up a maturity within the space of ML and AI in areas where we felt we could make the biggest dent with the biggest productivity.

Our vision was to create an agentic framework that supports our call center agents by leveraging Google Cloud's Vertex AI platform. CIERA's AI agents handle repetitive and complex tasks, allowing our team to focus on what technology can't. Guided by the principle that AI enhances human performance, these digital collaborators are designed to deliver accurate, comprehensive, and human-centered solutions.

The CIERA (Coaching Intelligent Education & Resource Agent) framework represents Mr. Cooper's approach to AI: augmenting human agents rather than replacing them. But even if I save one minute per phone call, times 4 or 5 million, that's huge. And Pyro is helping our agents prepare for what the customer is going to ask next based on the 100 other similar calls we've already seen in a similar context. Another way we are deploying AI is by pre-fetching information that we know the agent has to go look for. That way they are focused on the customer and their experience. A lot of our deployments with AI are designed to take the edge off of that particular conversation so the focus can be on the empathy and the emotional side of the customer interaction.

Data Breach & Crisis Management

No technology story is complete without addressing security, and Mr. Cooper faced a significant challenge in late 2023. Through our investigation, we determined that there was unauthorized access to certain of our systems between October 30, 2023 and November 1, 2023. Mortgage lender Mr Cooper has now admitted almost 14.7 million people's private information, including addresses and bank account numbers, were stolen in an earlier IT security breach, which is expected to cost the business at least $25 million to clean up.

The personal information in the impacted files included your name, address, phone number, Social Security number, date of birth, bank account number.

The breach affected both current and former customers—including some who hadn't been customers for nearly two decades. The Mr. Cooper mortgage cyber attack affected a total of 14.7 million people. Roughly 4 million of them were current customers of the company, the rest 10.7 million were past customers and loan applicants.

To help support our customers, we are offering two years of free credit monitoring and identity protection services through TransUnion to any former or current Mr. Cooper customer. Mr. Cooper says it is actively monitoring the dark web without any evidence that the data related to this incident has been further shared, published, or otherwise misused.

The breach triggered class action lawsuits and underscored the regulatory and operational risks inherent in managing sensitive financial data at scale. It also highlighted why the regulatory burden in mortgage servicing creates barriers to entry—and why scale matters for absorbing compliance costs.

IX. Leadership Profile: Jay Bray

Jay Bray has served as Mr. Cooper Group's CEO since 2012. Bray's track record includes working with Arthur Andersen as an audit manager and holding various leadership roles at Bank of America. He holds a BAA in Accounting from Auburn University and is a Certified Public Accountant in Georgia.

Jay has also served in various leadership roles at Nationstar since joining the company in 2000. Jay has more than 30 years of experience in the mortgage servicing and originations industry. From 1988 to 1994, he worked with Arthur Andersen in Atlanta, Georgia, where he served as an audit manager from 1992 to 1994. From 1994 to 2000, Jay held a variety of leadership roles at Bank of America and predecessor entities, where he managed the asset backed securitization process for mortgage-related products, developed and implemented a secondary execution strategy and profitability plan and managed investment banking relationships, secondary marketing operations and investor relations.

The 25-year journey from Nationstar to national champion reflects Bray's leadership philosophy: customer-centricity as competitive advantage, technology investment as operational leverage, and aggressive M&A as the path to scale economics.

Bray joined Nationstar in 2000, two years after arriving from Bank of America. He was present through the Fortress acquisition, the 2008 crisis, the IPO, the rebranding, and every major acquisition. That continuity provided institutional knowledge and strategic consistency rare in an industry marked by revolving-door leadership.

Currently, Jay Bray, our President & Chief Executive Officer, serves as Chairman of the Board. Our Board has determined that, at this time, this current structure, with a combined Chairman and Chief Executive Officer role and an independent lead director, is in the best interests of the Company and its stockholders. The Board believes the combined role of Chairman of the Board and Chief Executive Officer promotes unified leadership and execution of our strategic plan.

Bray's compensation structure aligned him with shareholders—over 85% of his target total compensation was "at risk" and subject to meeting financial or performance targets. That alignment helped drive the aggressive growth strategy that made Mr. Cooper attractive to Rocket.

Now at Rocket as President and CEO of Rocket Mortgage, Bray led Mr. Cooper for 25 years, "during which Mr. Cooper grew to become the nation's largest servicer and produced enormous value for our clients, partners, stakeholders and investors."

X. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

The barriers to entering mortgage servicing at scale are formidable. Regulatory complexity creates a compliance moat—servicers face oversight from the CFPB, state attorneys general, and state banking regulators, each with different requirements. The compliance infrastructure required to service loans in all 50 states represents a substantial fixed cost.

Scale economics create natural moats. Servicing over $1 trillion in loans requires massive operational infrastructure—call centers, document management systems, escrow administration capabilities, and loss mitigation expertise. The incremental cost to service one additional loan is minimal once that infrastructure exists, but building it from scratch requires years of investment.

However, fintech disruptors with deep pockets and technology-first approaches can enter. Banks with existing infrastructure can expand servicing operations relatively easily. The barrier is high but not impenetrable.

2. Bargaining Power of Suppliers: LOW

The primary "suppliers" in mortgage servicing are loan originators selling mortgage servicing rights (MSRs). This market is highly fragmented, with thousands of originators producing loans that require servicing.

Counter-cyclical dynamics favor MSR acquirers: when interest rates rise, origination volumes collapse, forcing originators to sell MSR portfolios to raise capital. This dynamic creates regular buying opportunities for scaled servicers like Mr. Cooper (now Rocket).

The company's ability to close acquisitions quickly and absorb large portfolios made it a preferred buyer, giving it negotiating leverage over smaller sellers.

3. Bargaining Power of Buyers: MEDIUM

The buyer landscape in mortgage servicing is bifurcated. Individual homeowners have essentially no choice in who services their loan—servicers are assigned by loan owners, and homeowners cannot switch. This captive customer base provides stable revenue.

However, institutional clients—banks, GSEs, and other financial institutions choosing subservicers—have significant leverage. These sophisticated buyers can evaluate servicer performance, compare pricing, and switch subservicers. The competitive pressure from this segment disciplines pricing and service quality.

Rocket Mortgage has ranked #1 in J.D. Power's mortgage servicer study for 10 years and #1 in mortgage origination 12 times, driving the company's 83% recapture rate – triple the industry average. Recapture rates—the ability to retain customers when they refinance—represent a critical competitive dimension where technology and service quality determine outcomes.

4. Threat of Substitutes: LOW

Mortgage servicing is essential infrastructure. Someone must collect payments, manage escrow accounts, report to credit bureaus, and work with delinquent borrowers. There is no substitute for these functions.

Potential disruption from blockchain-based smart contracts or decentralized finance remains distant. The regulatory complexity and consumer protection requirements embedded in mortgage servicing make it resistant to technological disintermediation.

The trend among banks has actually been to outsource servicing rather than bring it in-house, suggesting the specialized capabilities required favor dedicated servicers.

5. Industry Rivalry: HIGH

Despite consolidation, significant competitors remain. In the non-bank servicer category, Pennymac, Freedom Mortgage, and loanDepot maintain substantial market positions. PFSI's primary competitors include Profolio Home Mortgage, Freedom Mortgage, Mr. Cooper.

Bank servicers—Wells Fargo, JPMorgan Chase, Bank of America—retain large portfolios, though the trend has been toward outsourcing.

Competition occurs on multiple dimensions: pricing (basis points charged per loan), service quality (complaint rates, customer satisfaction), technology capabilities, and geographic coverage. The combination of high fixed costs and commoditized service creates persistent margin pressure.

The Rocket-Mr. Cooper combination represents a structural shift in this competitive landscape. A week later, Rocket Companies and Mr. Cooper's shareholders approved the merger — opening the door for Rocket to reclaim its spot as the nation's leading mortgage lender, a title that was snatched away by rival United Wholesale Mortgage in 2022.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Mr. Cooper's primary competitive advantage. The cost to service one additional loan approaches zero once infrastructure exists. The $1.5+ trillion portfolio spreads fixed costs across millions of accounts.

Network Effects: Limited direct network effects, but the data accumulated from servicing millions of loans creates valuable insights for risk management, pricing, and customer retention.

Counter-Positioning: The rebrand from Nationstar to Mr. Cooper represented a form of counter-positioning—attempting to compete on customer experience in an industry known for poor service. However, this remains a work in progress.

Switching Costs: Moderate for institutional subservicing clients (who can evaluate alternatives) but high for individual homeowners (who cannot choose their servicer).

Cornered Resource: The combined Rocket-Mr. Cooper entity possesses unique assets: Rocket's origination technology and brand, Mr. Cooper's servicing infrastructure and portfolio scale.

Process Power: Mr. Cooper's Pyro AI platform and operational efficiency represent proprietary processes developed over years that would be difficult for competitors to replicate quickly.

Key Performance Indicators to Monitor

For investors tracking mortgage servicers, three metrics merit close attention:

1. Recapture Rate: The percentage of refinancing customers who stay with their current servicer rather than switching to a competitor. This metric directly measures a servicer's ability to monetize its customer relationships and represents the strategic logic behind the Rocket-Mr. Cooper combination. Industry average hovers around 25-30%; Rocket claims 83%.

2. Cost to Service (per loan): Operating expenses divided by loans serviced. This metric reveals operational efficiency and the benefits of scale. Mr. Cooper's technology investments in Pyro AI and CIERA aimed specifically at reducing this metric.

3. Unpaid Principal Balance (UPB) Growth: The total value of loans serviced. Growth can come from organic originations, MSR acquisitions, or subservicing contracts. This metric indicates market share trajectory and scale leverage. Mr. Cooper's 33% year-over-year growth to $1.514 trillion demonstrated aggressive consolidation.

Myth vs. Reality

Myth: Mr. Cooper was always a troubled company with a bad reputation.

Reality: The company's reputation problems stemmed from a specific period of rapid growth through distressed MSR acquisitions (2012-2016), during which operational capacity lagged portfolio expansion. Substantive operational improvements—including $90+ million in technology investment, elimination of payment fees, and U.S.-based customer service—produced measurable results (70% reduction in complaints). The regulatory settlements cleared legal overhangs. However, customer experience remains a work in progress, and the cybersecurity breach in 2023 created new reputational challenges.

Myth: The Rocket acquisition was opportunistic—Mr. Cooper was struggling.

Reality: Mr. Cooper was performing well when acquired. The company had grown servicing to $1.5+ trillion, completed successful integrations of multiple acquisitions, and was generating consistent profitability. Rocket paid a 35% premium over the 30-day average trading price because Mr. Cooper possessed strategic value—the largest servicing portfolio in the industry—not because it was distressed.

Myth: Mortgage servicing is a dying business.

Reality: Banks are exiting mortgage servicing, but the loans still need to be serviced. This creates opportunity for scaled non-bank servicers who can absorb portfolios banks no longer wish to hold. The Flagstar acquisition exemplified this dynamic—NYCB recognized the regulatory and interest rate risks of mortgage servicing and chose to exit. Mr. Cooper was positioned to absorb those portfolios efficiently.

Material Risks & Overhangs

Regulatory Risk: Mortgage servicing faces intensive regulatory oversight from the CFPB, state attorneys general, and state banking regulators. Political shifts can dramatically change enforcement priorities. The pending CFPB directorship and potential regulatory changes create uncertainty around compliance requirements.

Interest Rate Sensitivity: While servicing is often described as counter-cyclical to origination, MSR valuations are sensitive to interest rate movements and prepayment expectations. Rapid rate declines can compress MSR values and accelerate prepayments, reducing servicing fee income.

Cybersecurity: The 2023 data breach affecting 14.7 million customers exposed material cybersecurity vulnerabilities. Ongoing litigation and remediation costs, plus potential future incidents, represent operational and financial risk.

Integration Risk: The Rocket-Mr. Cooper combination requires integrating two large organizations with different cultures, technology platforms, and operational processes. Integration failures could impair projected synergies and disrupt customer experience.

Concentration Risk: The combined Rocket-Mr. Cooper entity will service one in every six mortgages in America. This scale attracts regulatory scrutiny and creates systemic importance that may invite additional oversight.

Conclusion: The Arc of Financial History

The Mr. Cooper story encapsulates three decades of transformation in American mortgage finance. It begins with Washington Mutual's 119-year journey from prudent Seattle savings and loan to subprime poster child, through the largest bank failure in American history. A corporate shell emerges from bankruptcy, carrying tax assets and a search for purpose.

Simultaneously, a Denver garage startup becomes a Dallas mortgage servicer, gets acquired by private equity, survives the 2008 crisis by servicing the distressed loans others created, goes public, accumulates regulatory baggage, rebrands around a cartoon avatar, and consolidates its way to industry leadership.

These two threads merge in 2018, creating Mr. Cooper Group. The combined entity executes an aggressive roll-up strategy, acquiring Home Point, Roosevelt, and Flagstar's mortgage operations in rapid succession. The company reaches $1.5 trillion in servicing, becoming America's largest non-bank mortgage servicer.

Then Rocket Companies writes the final chapter—acquiring Mr. Cooper for $14.2 billion, the largest independent mortgage deal in history. The fictional Mr. Cooper avatar is retired. Jay Bray, who spent 25 years building the company, becomes President and CEO of Rocket Mortgage. The servicing powerhouse built from Washington Mutual's ashes joins the origination leader to create an integrated mortgage platform serving nearly 10 million homeowners.

The strategic question now shifts to execution: Can Rocket realize the synergies that justified a $14.2 billion price tag? Can the combined entity maintain service quality while integrating complex operations? Will the 83% recapture rate that defined Rocket's model translate to Mr. Cooper's customer base?

For investors, the Mr. Cooper story offers enduring lessons: that crisis creates opportunity for the prepared, that scale economics matter tremendously in operationally intensive businesses, that reputation can be reshaped (though not easily or quickly), and that consolidation in fragmented industries tends toward logical endpoints where the largest players acquire their rivals.

The dream of homeownership—which Mr. Cooper pledged to keep alive—continues. The fictional avatar who represented that dream is gone. But the infrastructure serving those dreams has never been larger, and the next chapter is being written under the Rocket brand.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube