Synopsys: From Logic Synthesis to Silicon-to-Systems Dominance

I. Introduction & Episode Roadmap

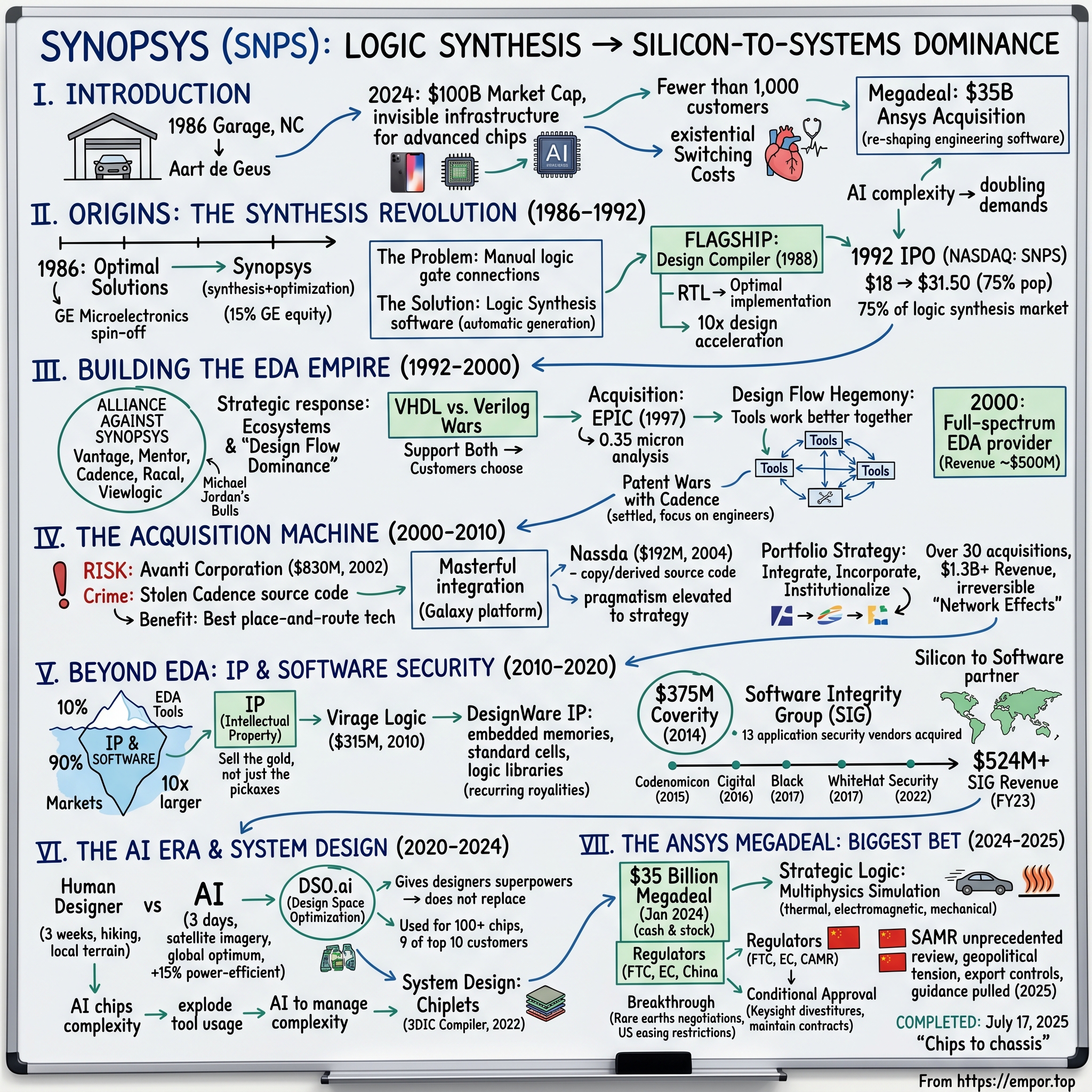

Picture this: It's 1986, and in a modest garage in Research Triangle Park, North Carolina, four engineers are hunched over workstations, wrestling with a problem that's plaguing the entire semiconductor industry. Every chip designer in the world is drowning in complexity—manually connecting thousands of logic gates, one painstaking connection at a time. The process takes months, errors are inevitable, and the industry is hitting a wall.

These four engineers—led by a young Dutch immigrant named Aart de Geus—believe they have the answer: software that can automatically synthesize chip designs from high-level descriptions. The venture capitalists they pitch to are skeptical. "You're telling us you can replace months of manual work with a computer program?" one asks. De Geus, with characteristic confidence, replies: "Not replace. Transform."

Fast forward to 2024: That garage startup is now Synopsys, the 12th largest software company in the world, with a market capitalization approaching $100 billion. The company that started by automating logic gate connections now powers virtually every advanced chip design on the planet—from the processors in your iPhone to the AI accelerators training ChatGPT. In an era where a single cutting-edge chip can cost $500 million to develop and contain over 100 billion transistors, Synopsys has become the invisible infrastructure that makes modern electronics possible.

But here's what's remarkable: While most software companies achieve scale through consumer adoption or enterprise seats, Synopsys has built one of the world's most valuable software businesses by serving fewer than 1,000 customers. Their secret? Those customers include every major semiconductor company on Earth, and once they're in, they almost never leave. The switching costs aren't just high—they're existential. Ripping out Synopsys tools from a chip design flow would be like performing heart surgery on yourself while running a marathon.

Today, Synopsys stands at an inflection point. The company just completed the largest acquisition in electronic design automation history—a $35 billion megadeal for simulation giant Ansys that reshapes the entire landscape of engineering software. Meanwhile, artificial intelligence is driving unprecedented complexity in chip design, with some AI accelerators now consuming more electricity than small cities and requiring cooling systems that rival data centers. The question isn't whether the world needs more sophisticated design tools—it's whether Synopsys can evolve fast enough to meet demands that double every few years.

This is the story of how a company selling tools that 99.9% of people have never heard of became indispensable to the $600 billion semiconductor industry. It's a tale of technical revolution, strategic acquisition mastery, and the relentless pursuit of abstraction—because in the world of chip design, every new level of abstraction unlocks exponential value. As we'll see, Synopsys didn't just ride the waves of semiconductor evolution; it created many of them.

II. Origins: The Synthesis Revolution (1986–1992)

The conference room at General Electric's Microelectronics Center in Research Triangle Park had that peculiar tension of a team on the verge of mutiny. It was early 1986, and Aart de Geus, a 31-year-old engineering manager who'd arrived from the Netherlands just seven years earlier, was facing down his superiors with an ultimatum that would reshape an entire industry.

"We've built something revolutionary here," de Geus told the GE executives. "But you're treating it like a cost center for internal use. This synthesis technology could transform how every chip in the world gets designed. If GE won't commercialize it, we will."

The backstory reads like a classic immigrant success tale with a silicon twist. De Geus had landed in Dallas in 1979, barely speaking English, to pursue graduate studies at Southern Methodist University. Within months, he'd gone from writing basic electrical engineering teaching programs to hiring fellow students to code for him—displaying the entrepreneurial instincts that would later build an empire. At GE, he'd assembled a dream team: David Gregory, a methodical engineer who understood the nitty-gritty of chip architecture; Bill Krieger, who could translate complex algorithms into working code; and they'd soon be joined by Alberto Sangiovanni-Vincentelli from Berkeley, an academic heavyweight who literally wrote the book on circuit simulation.

What they'd developed at GE was genuinely paradigm-shifting. Imagine if architects had to specify the position of every single brick in a skyscraper, calculating load-bearing requirements by hand for each one. That's essentially what chip designers were doing in 1986—manually connecting individual logic gates, a process that could take months for even moderately complex designs. De Geus's team had created software that could take a high-level description of what a chip should do—written in a language similar to software code—and automatically generate the optimal gate-level implementation. They called it "synthesis," and it compressed months of work into hours.

GE's response was corporate myopia at its finest: "Interesting tool. We'll use it internally to design our own chips. No need to sell it outside." For a company that made everything from light bulbs to jet engines, software tools for chip design barely registered as a business opportunity. The synthesis technology that could revolutionize a global industry was destined to remain locked inside GE's labs.

De Geus knew better. He'd witnessed firsthand the explosion in chip complexity—designs were doubling in transistor count every two years, but human productivity wasn't keeping pace. Every semiconductor company was hitting the same wall: designs too complex for humans to optimize manually, release cycles stretching longer, and error rates climbing. The industry needed automation, and synthesis was the answer.

The negotiations with GE were surprisingly swift. The conglomerate, focused on its core businesses and perhaps relieved to avoid a brain drain, agreed to let the team leave with the technology in exchange for a 15% equity stake in the new company. In 1986, Optimal Solutions was born in a Research Triangle Park garage, though the name wouldn't last long—it turned out another company already had dibs on it. Within months, they'd rebrand as Synopsys, a portmanteau of "synthesis" and "optimization."

The early days were classic startup chaos. De Geus coded through the night while Gregory cold-called potential customers during the day. They had a technology nobody understood marketing for a problem many companies didn't yet realize they had. Their first demo at LSI Logic—then a major player in custom chips—was almost comical in its ambition. "We can reduce your design time by 10x," de Geus promised. The LSI engineers laughed. Then they saw it work.

The Design Compiler, Synopsys' flagship product launched in 1988, wasn't just an incremental improvement—it was a fundamental reimagining of how chips got designed. Instead of specifying how a chip should be built (the gate-level netlist), designers could specify what it should do (the RTL or Register Transfer Level description). The software would figure out the optimal implementation, considering timing, power, and area constraints simultaneously. For chip designers, it was like going from assembly language to Python overnight.

Customer adoption followed a pattern that would become Synopsys' signature: start with the innovators desperate for any edge, prove massive productivity gains, then watch as their competitors scrambled to catch up. Sun Microsystems used Design Compiler to accelerate their SPARC processor development. MIPS Technologies credited it with enabling their RISC architecture to compete with Intel. By 1990, nine of the top ten computer makers were customers.

But de Geus understood something crucial: in the EDA business, being first isn't enough—you have to become the standard. Synopsys didn't just sell tools; they evangelized a methodology. They published papers, sponsored university research, and most cleverly, made their tools the easiest to teach in engineering schools. A generation of chip designers would learn synthesis on Synopsys tools, creating a moat measured not in features but in muscle memory. The IPO story itself was quintessentially '90s Silicon Valley. On February 26, 1992, Synopsys went public on NASDAQ at $18 a share, closing its first trading day at $31.50—a 75% pop that would make modern IPOs blush. The company offered 1.55 million shares while existing stockholders offered 450,000 shares, raising capital that would fuel the next phase of growth.

What's remarkable in hindsight is the speed of Synopsys' ascent. In fewer than 10 years after its founding, Synopsys had achieved a run rate of $250 million—transforming from garage startup to the dominant force in logic synthesis. By the time of the IPO, they owned more than 75% of the logic synthesis tools market, which had become EDA's hottest growth area.

The synthesis revolution wasn't just about automating manual work—it fundamentally changed who could design chips and how fast innovation could happen. Suddenly, a small team could design a complex ASIC in months rather than years. Startups could compete with established giants. The entire semiconductor industry accelerated, and at the center of it all was a Dutch immigrant who'd seen the future in a GE conference room and refused to let it remain locked away.

III. Building the EDA Empire (1992–2000)

The year 1992 should have been Synopsys' victory lap. Fresh off their blockbuster IPO, with nine of the top ten computer makers as customers and ownership of 75% of the logic synthesis market, de Geus and his team had every reason to celebrate. Instead, they found themselves in the crosshairs of an industry-wide conspiracy to dethrone them.

The alliance that formed against Synopsys read like a who's who of EDA royalty. Vantage Analysis Systems, the leading VHDL simulator vendor, orchestrated a coalition of eight synthesis vendors, joining forces with broad-based suppliers including Mentor Graphics, Cadence Design Systems, Racal-Redac, and Viewlogic. Their mission: pool resources, share technology, and collectively unseat Synopsys from its synthesis throne. It was the EDA equivalent of the entire industry ganging up on Michael Jordan's Bulls.

De Geus' response revealed the strategic thinking that would define Synopsys for decades: "They think this is about competing products. It's about ecosystems." While competitors focused on matching Synopsys' features, de Geus was already three moves ahead, building what he called "design flow dominance"—ensuring that Synopsys tools weren't just best-in-class individually, but indispensable when used together.

The strategy manifested in what became known as the "VHDL vs. Verilog wars"—a standards battle that would determine how engineers described their designs for the next generation. While competitors bet heavily on VHDL (backed by the U.S. Department of Defense), Synopsys made a crucial decision: support both languages equally well. "Let the customers choose," de Geus told his team. "We'll be there regardless." It was expensive, requiring duplicate development efforts, but it meant Synopsys could sell to everyone while competitors fought religious wars over standards. The acquisition strategy crystallized in 1997 with the EPIC Design Technology purchase, strengthening Synopsys' position in place-and-route technology. The deal revealed de Geus' philosophy: don't just acquire products, acquire the future. EPIC's specialty was deep submicron analysis, verification and reliability tools, with no overlap with Synopsys' toolset—exactly the kind of complementary technology that would become essential as chips shrank below 0.35 microns.

But the real genius wasn't in individual acquisitions—it was in creating what de Geus called "design flow hegemony." Every tool Synopsys acquired or built was engineered to work better with other Synopsys tools than with competitors' products. Not through deliberate incompatibility—that would anger customers—but through subtle optimizations, shared data formats, and integrated debugging that made the all-Synopsys flow just... smoother. A designer might start with a competitor's tool for one step, but the friction of integration would gradually push them toward the Synopsys alternative.

The late '90s also saw Synopsys navigate one of the industry's most vicious patent wars. Cadence and Synopsys traded lawsuits like boxers trading punches, each claiming the other had stolen critical intellectual property. The legal bills mounted into tens of millions, and the uncertainty spooked customers who feared their chosen vendor might be forced to pull products from the market. De Geus' solution was characteristically pragmatic: settle everything, cross-license liberally, and focus on competing in the market rather than the courtroom. "Lawyers don't design chips," he'd tell his board. "Engineers do."

By 2000, Synopsys had transformed from synthesis specialist to full-spectrum EDA provider. They offered tools for every step of chip design: synthesis, simulation, timing analysis, physical design, and verification. The company that started with one breakthrough product now had dozens, each reinforcing the others in an intricate web of dependencies that made switching costs astronomical.

The numbers told the story: from $50 million in revenue at IPO to approaching $500 million by decade's end. But more importantly, Synopsys had become something more than a tools vendor—they'd become the de facto standard for how chips got designed. Engineering schools taught on Synopsys tools. Industry conferences featured Synopsys methodologies. Even competitors had to ensure compatibility with Synopsys formats.

The empire was built. Now came the hard part: defending it while continuing to grow.

IV. The Acquisition Machine: Consolidation & Expansion (2000–2010)

The board meeting in early 2002 had the atmosphere of a war cabinet. Synopsys executives sat around the conference table, reviewing a proposal that would either cement their market dominance or destroy the company's reputation forever. The target: Avanti Corporation, their bitter rival, currently under criminal investigation for stealing Cadence's source code. The price: $830 million. The risk: astronomical.

"You want us to buy a company whose executives might go to jail?" one board member asked incredulously.

De Geus leaned forward, his Dutch accent lending gravity to his words: "I want us to buy the best place-and-route technology in the industry. The executives aren't the technology. And everyone deserves redemption."

The Avanti acquisition would become Synopsys' most significant and controversial acquisition. The backstory read like a Silicon Valley noir thriller. Avanti had been founded by former Cadence employees who'd allegedly taken more than farewell drinks when they left—prosecutors claimed they'd taken millions of lines of source code. The resulting legal battle had consumed the EDA industry for years, with Avanti paying Cadence hundreds of millions in settlements while maintaining their innocence.

But beneath the scandal lay remarkable technology. Avanti's place-and-route tools—the software that determined exactly where transistors and wires went on a chip—were genuinely superior to anything else on the market. Their customers, including many of Synopsys' own users, swore by Avanti's tools for the most challenging designs. The criminal investigation had depressed Avanti's stock price to a fraction of its technical value.

De Geus saw opportunity where others saw toxicity. The acquisition wasn't just about technology—it was about healing an industry torn apart by litigation. By bringing Avanti into the Synopsys fold, de Geus could end the patent wars, integrate best-in-class physical design tools, and send a message that Synopsys was more interested in building the future than litigating the past.

The integration was masterful in its delicacy. Rather than dismantling Avanti or conducting purges, Synopsys kept the engineering teams intact, treating them as conquering heroes rather than conquered foes. The Avanti tools were carefully woven into the Synopsys flow, creating what became known as "Galaxy"—the industry's first truly integrated design platform from RTL to silicon. Just two years later, in 2004, Synopsys pulled off another redemption acquisition—Nassda Corporation for $192 million. Like Avanti, Nassda was embroiled in litigation with Synopsys itself. Former Synopsys employees had founded Nassda, allegedly taking trade secrets to create their flagship HSIM simulator. A 2004 court ruling found that the first 60,000 lines of HSIM's source code were "copied or derived" from Synopsys materials.

But rather than pursue damages through the courts, de Geus saw a bigger picture. Nassda's circuit simulation tools, despite their questionable origins, had evolved into genuinely superior technology that Synopsys customers needed. The acquisition deal was structured brilliantly: Synopsys paid $192 million for the company, while the Nassda executives accused of theft agreed to pay Synopsys $61.6 million in settlement—essentially reducing the net cost to around $130 million for technology worth far more.

"By acquiring Nassda rather than continuing through the courts, Synopsys can preserve Nassda's products and continue long-term support of Nassda's customers," Rex Jackson, Synopsys' general counsel, explained. It was pragmatism elevated to strategy—why destroy value in litigation when you could capture it through acquisition?

The acquisition machine wasn't just about buying competitors. Throughout the 2000s, Synopsys executed a portfolio strategy that would make a venture capitalist jealous. They acquired point tools that filled gaps (InnoLogic Systems for equivalence checking), emerging technologies that represented the future (iRoC for radiation-effects modeling), and service companies that brought customer relationships (The Silicon Group for design services).

Each acquisition followed what became known internally as the "three-I framework": Integrate the technology, Incorporate the talent, Institutionalize the knowledge. Unlike many serial acquirers who gutted their purchases for IP, Synopsys treated acquisitions as organ transplants—carefully preserving what made them valuable while connecting them to the larger organism.

The numbers told the story of transformation. By 2010, Synopsys had completed over 30 acquisitions, spending billions to assemble the industry's most comprehensive toolset. Revenue had grown from around $500 million in 2000 to over $1.3 billion by decade's end. But more importantly, the company had evolved from a tools vendor to something more profound: the platform on which the entire semiconductor industry operated.

The integrated design platform Synopsys built through acquisitions created what economists call "network effects on steroids." Each new tool made existing tools more valuable. Each new customer made the platform more attractive to other customers. Each new design success became a reference that sold the next deal. The acquisition machine hadn't just grown Synopsys—it had fundamentally changed the competitive dynamics of the EDA industry, creating barriers to entry measured not in millions but in billions of dollars.

V. Beyond EDA: The IP & Software Security Pivot (2010–2020)

The PowerPoint slide that Aart de Geus presented to his board in early 2010 contained a single, stark image: an iceberg. Above the waterline sat "EDA Tools"—Synopsys' traditional business. Below, taking up 90% of the image, loomed "IP & Software"—markets ten times larger than EDA but completely untapped by Synopsys.

"We're selling pickaxes in a gold rush," de Geus told the board, his Dutch accent lending gravity to the metaphor. "But what if we could sell the gold itself?"

The opportunity was massive but required a fundamental rethinking of Synopsys' business model. In EDA, you sold tools that customers used to create their own designs. In IP (Intellectual Property), you sold pre-designed, pre-verified blocks that customers could drop into their chips like Lego pieces. Instead of selling the CAD software architects use, you'd be selling blueprints for entire floors of the building. The Virage Logic acquisition in 2010 for $315 million was de Geus' masterstroke in IP strategy. Virage brought embedded memories with test and repair, non-volatile memories (NVMs), standard cell libraries, and programmable cores for control and multimedia sub-systems. But more importantly, it brought credibility. Virage was the #3 semiconductor IP provider with the #1 embedded SRAM, #1 BIST, #1 Logic Libraries, #1 DDR, #1 NVM, the ARC CPU cores and audio/video interface technology.

The economics of IP were fundamentally different from EDA tools. With EDA, you sold licenses measured in hundreds of thousands of dollars to hundreds of customers. With IP, you could charge millions for a single block of verified design—and then collect royalties on every chip manufactured using that IP. It was the difference between selling fishing rods and taking a percentage of every fish caught.

"IP is the ultimate sticky business," de Geus explained to investors. "Once our IP is designed into a customer's chip, it's there for the life of that product line. Switching costs aren't just high—they're prohibitive. You'd have to redesign the entire chip. "But the real surprise came in 2014 with the $375 million acquisition of Coverity, marking Synopsys' entry into software security—a market that had nothing to do with chips. Or so it seemed. De Geus saw what others missed: as chips became more complex and software-defined, the line between hardware and software security was blurring. A vulnerability in chip design could be exploited through software; a software bug could compromise hardware security features.

Since spinning out of a Stanford research project 10 years ago, Coverity had been developing revolutionary technology to find and fix defects in software code before it is released, improving software security. The technology was genuinely impressive—static analysis that could find bugs that human code reviewers would miss. But more importantly, it gave Synopsys entry into a completely new customer base: enterprise software developers who'd never heard of EDA.

The Software Integrity Group (SIG) that Synopsys built around Coverity would eventually include 13 acquired companies, creating a $500+ million business. In total, the company acquired 13 application security vendors between 2014 and 2023, including Codenomicon in 2015, Cigital in 2016, Black Duck Software in 2017 and WhiteHat Security in 2022. Through these acquisitions, Synopsys amassed a broad application security testing product portfolio and became the largest application security testing vendor by revenue, earning over $524 million in fiscal year 2023.

The strategy wasn't just about diversification—it was about following the value chain. As de Geus explained to investors: "Software is eating the world, but chips are the teeth." Every piece of software ultimately ran on silicon, and Synopsys wanted to be there at every step, from chip design to software security.

By 2020, Synopsys had transformed from an EDA company to what de Geus called a "Silicon to Software" partner. The DesignWare IP portfolio had grown to become the industry's second-largest after ARM, generating recurring revenue streams from royalties. The Software Integrity business, while smaller than EDA, was growing faster and commanding higher multiples.

The numbers told the transformation story: revenue had grown from $1.3 billion in 2010 to over $3.6 billion by 2020. But more importantly, the business model had evolved. No longer just selling tools, Synopsys was selling outcomes—verified IP blocks that worked the first time, security assessments that prevented breaches, design flows that compressed time-to-market.

The pivot beyond EDA wasn't an abandonment of the core business—it was an amplification of it. Every IP sale made EDA tools more valuable (you needed Synopsys tools to integrate Synopsys IP efficiently). Every security assessment created relationships that could lead to chip design wins. The company had built what venture capitalists dream of but rarely achieve: a true platform business with multiple reinforcing revenue streams.

VI. The AI Era & System Design Evolution (2020–2024)

The demo at Synopsys headquarters in early 2020 felt like watching a chess grandmaster get demolished by a computer for the first time. On one screen, a senior chip architect with 30 years of experience was optimizing a complex processor design—tweaking parameters, running simulations, adjusting constraints. On the other screen, Synopsys' new AI system, DSO.ai (Design Space Optimization), was attacking the same problem. The human took three weeks. The AI took three days. And the AI's design was 15% more power-efficient.

"This isn't about replacing designers," Sassine Ghazi, who would become CEO in 2024, carefully explained to the stunned audience. "It's about giving them superpowers."

The development of Synopsys.ai, the company's AI-driven EDA initiative, represented the most fundamental shift in chip design methodology since the invention of synthesis itself. The challenge wasn't just technical—it was existential. If AI could design chips better than humans, what was the role of human designers? And more pressingly for Synopsys, if AI could automate design, would customers need fewer tool licenses?

De Geus and his team bet on a different future: AI wouldn't reduce the need for EDA tools; it would explode it. The reasoning was counterintuitive but compelling. As AI made it easier to explore design alternatives, engineers would explore more of them. As designs became more complex—driven by AI chips that needed unprecedented computing power—the design space would expand exponentially. You'd need AI just to handle the complexity that AI was creating. The results spoke for themselves. Samsung Foundry reported that DSO.ai systematically found optimal solutions that exceeded their previously achieved power-performance-area results in as few as 3 days; a process that typically takes multiple experts over a month of experimentation. SK Hynix used DSO.ai to reduce the footprint of a flash memory chip based on its most advanced process technology by 5%, while reducing the area of the logic cells by about 15%. Initial customer use cases showed productivity boosts of more than 3x, power reductions of up to 15%, substantial die size reductions, and less use of overall resources.

But the real breakthrough wasn't in individual optimizations—it was in changing the entire design paradigm. Traditional chip design was sequential: architect, implement, verify, manufacture. Each step informed the next, but rarely did information flow backward. DSO.ai could explore the entire design space simultaneously, considering millions of potential configurations and learning which combinations worked best together.

"Think of it like this," Ghazi explained to customers. "A human designer is like a hiker trying to find the highest peak in a mountain range. They can only see the local terrain and might settle for a nearby summit. DSO.ai is like having satellite imagery of the entire range—it can identify the true global optimum."

The shift from chip design to system design was equally profound. As chips became too complex for any single company to design entirely from scratch, the industry moved toward chiplets—smaller, specialized chips that could be combined like Lego blocks into larger systems. This wasn't just a technical shift; it was a business model revolution. Instead of one company designing a monolithic chip, you could have specialists: one company making the CPU chiplet, another the GPU, another the memory interface, all connected through standardized interconnects.

Synopsys positioned itself perfectly for this transition. Their 3DIC Compiler, launched in 2022, wasn't just a tool for designing multi-die systems—it was a platform for orchestrating the collaboration between different companies' designs. The software could optimize not just individual chiplets but the interactions between them, managing thermal issues, signal integrity, and power delivery across the entire system.

The numbers by 2024 were staggering. DSO.ai had been used to help tape out 100 different chips, with 9 of Synopsys' top 10 digital implementation customers embracing the technology. Revenue had grown to over $6 billion, with AI-enhanced tools commanding premium prices and driving faster design cycles that paradoxically increased tool usage rather than reducing it.

But perhaps the most profound change was philosophical. For decades, EDA had been about automating what humans did manually. The AI era was about augmenting what humans couldn't do at all. No human could explore trillions of design configurations. No human could simultaneously optimize across dozens of competing constraints. No human could learn from every design ever created and apply those lessons instantly.

As de Geus reflected on the transformation: "AI-designed chips are producing great results that could lead to 1,000 times better performance for chips in the next decade". The technology that had started as a tool to help designers had evolved into a partner that could see possibilities humans never imagined.

VII. The Ansys Megadeal: Biggest Bet Yet (2024–2025)

The boardroom at Synopsys headquarters on January 15, 2024, had the electric tension of a high-stakes poker game reaching its climax. Sassine Ghazi, about to become CEO in just two weeks, stood before the board with a proposal that would either cement Synopsys' dominance for the next decade or potentially destroy shareholder value on an unprecedented scale.

"Thirty-five billion dollars," Ghazi said, letting the number hang in the air. "That's what it will take to acquire Ansys. It's more than our entire market cap was just three years ago. It's the largest acquisition in software history outside of Microsoft's deals. And I believe it's the bargain of the century."

The board members exchanged glances. One finally spoke: "Sassine, Ansys does simulation software for planes, cars, and buildings. We design chips. Where's the synergy?"

Ghazi's response would reshape the entire industry's understanding of what EDA meant in the modern era: "Gentlemen, ladies—chips don't exist in isolation anymore. A modern AI accelerator dissipates 400 watts of power. That heat has to go somewhere. The electromagnetic interference from high-speed signals affects everything around it. The mechanical stress from thermal cycling can crack solder joints. We're not designing chips anymore—we're designing systems. And systems don't respect the boundaries between electronic and mechanical, between thermal and electromagnetic, between silicon and software. "The announcement of the deal in January 2024 sent shockwaves through the industry. Under the terms, Ansys stockholders would receive $197.00 in cash and 0.3450 shares of Synopsys common stock for each Ansys share they owned, valuing the deal at approximately $35 billion based on December 2023 prices. Synopsys intends to fund the $19 billion of cash consideration through a combination of its cash on hand and $16 billion of fully committed debt financing.

The strategic logic was compelling once you understood Ghazi's vision. Modern chip design had become inseparable from system design. A data center AI accelerator wasn't just a chip—it was part of a complex thermal management system, electromagnetic interference environment, and mechanical assembly. The heat generated by one chip affected the performance of neighboring chips. The high-speed signals created electromagnetic fields that could disrupt nearby circuits. The mechanical stresses from thermal cycling could cause failures.

Ansys brought world-class multiphysics simulation—the ability to model heat transfer, fluid dynamics, electromagnetic fields, and mechanical stress simultaneously. Combined with Synopsys' chip design tools, customers could co-optimize the chip and the system it operated in. As Ghazi explained: "Products are increasingly evolving into intelligent systems, capable of reasoning, learning, collaborating, adapting and acting. The industry must re-engineer how products are engineered."

The regulatory gauntlet proved more challenging than anyone anticipated. While the boards approved the deal quickly, government regulators moved at geological pace. The Federal Trade Commission demanded extensive documentation. The European Commission launched a deep investigation. But the real drama came from China.

In May 2024, China's State Administration for Market Regulation (SAMR) took the unprecedented step of calling in the merger for review even though it fell below normal notification thresholds—the first time it had exercised this power for a foreign-to-foreign merger. Chinese customers had complained to regulators about potential bundling issues and concerns that U.S. export controls might affect their access to critical design tools.

The geopolitical tensions reached a boiling point in June 2025. New U.S. export regulations on electronic design technology forced Synopsys and other EDA companies to temporarily suspend sales to China. The timing couldn't have been worse—right in the middle of merger negotiations with Chinese regulators. Synopsys had to pull its financial guidance, sending the stock into a tailspin.

"We're caught between two superpowers using technology as a weapon," one Synopsys executive privately lamented. "We just want to sell software, but we're being treated like arms dealers."

The breakthrough came in July 2025. After the U.S. eased some export restrictions following negotiations over rare earth materials, China's SAMR gave conditional approval. The conditions were stringent: Synopsys had to maintain existing contracts with Chinese clients, continue supplying EDA products on fair and non-discriminatory terms, and ensure interoperability with competing solutions. Additionally, Synopsys agreed to divest its Optical Solutions Group and Ansys's PowerArtist tool to Keysight Technologies to address competitive concerns.

On July 17, 2025, Synopsys completed its acquisition of Ansys. The final price tag had ballooned with market movements, but the strategic value remained clear. As Ghazi offered additional perspective on the implications: the combined Synopsys/Ansys would be able to support virtual design and optimization of automotive systems "from chips to chassis" before production even begins.

The integration challenges ahead were massive. Two different corporate cultures, overlapping products in some areas, and the need to maintain innovation while merging operations. But the potential was even greater: a company that could design and simulate everything from the quantum effects in a 3-nanometer transistor to the aerodynamics of the drone that transistor would power.

VIII. Current Position & Market Dynamics

Standing in August 2025, Synopsys commands a market capitalization hovering around $97 billion, making it the world's 166th most valuable company. The numbers alone tell a story of dominance: full-year 2024 revenue of $6.127 billion, up approximately 15% year-over-year, with gross margins that typically exceed 70%—the hallmark of a software business with minimal marginal costs and maximal pricing power.

But numbers only capture part of the story. Today's Synopsys operates as three interlocking empires, each reinforcing the others in ways competitors struggle to replicate.

The first empire, EDA, remains the crown jewel. Here, Synopsys doesn't just lead—it defines the industry. Their tools are so deeply embedded in customer workflows that switching would be like performing brain surgery on yourself. The business model is elegantly brutal: time-based licenses that create predictable, recurring revenue streams. Customers pay whether they use the tools or not, because the alternative—not having access when needed—is unthinkable. The stickiness is legendary; customer retention rates approach 95%, and many relationships span decades.

The second empire, IP, has evolved into what investment analysts call "the ultimate annuity business." Once Synopsys IP gets designed into a customer's chip, it generates revenue for years—license fees upfront, royalties on every chip manufactured. With the industry's second-largest IP portfolio after ARM, Synopsys provides the building blocks for everything from USB interfaces to AI accelerators. The beauty is the network effect: the more customers use Synopsys IP, the more it gets validated and improved, making it more attractive to future customers.

The third empire, Software Integrity (though being divested), represented the company's boldest bet: that the convergence of hardware and software security would create entirely new markets. While ultimately deemed non-core, the journey into software security proved the company's ability to expand beyond traditional boundaries.

Geographically, Synopsys' footprint reads like a map of global technology power. The United States remains the largest market, contributing 44.71% of total revenue (approximately $2.74 billion). But the real story is in the diversification: China at 16.15% ($989.52 million) despite increasing restrictions, Korea at 12.62% ($773.02 million) driven by Samsung and SK Hynix, Europe at 10.03% ($614.58 million), and another 16.49% spread across emerging markets.

The Armenia operation deserves special mention—more than 1,000 employees across offices in Yerevan and Gyumri, making Synopsys one of the largest IT employers in the country. It's a masterclass in global talent arbitrage: world-class engineers at a fraction of Silicon Valley costs, working on core R&D that drives the entire company's innovation.

Customer concentration tells the real story of market dynamics. Synopsys serves fewer than 1,000 customers globally, but those customers include every major semiconductor company, every significant systems company, and increasingly, the hyperscalers designing their own chips. The top 10 customers likely account for over 30% of revenue—concentration that would terrify most companies but reflects Synopsys' irreplaceable position in the technology stack.

The competitive landscape has crystallized into what industry insiders call "the eternal triangle": Synopsys, Cadence, and Siemens EDA (formerly Mentor Graphics) controlling approximately 75% of the global EDA market. But each has carved out strongholds. Synopsys dominates synthesis and digital implementation. Cadence leads in custom IC design and PCB tools. Siemens brings strength in automotive and systems design. The competition is fierce but rational—everyone knows that mutually assured destruction helps no one.

The three-segment strategy creates what de Geus calls "multiple ways to win." EDA grows with chip complexity—every new process node, every increase in transistor count, every new design challenge drives tool usage. IP grows with chip volume—more chips mean more royalties. Software Integrity (before divestment) grew with security concerns—every breach, every vulnerability, every regulation drove demand.

The moats are not just wide; they're multidimensional. Technical moat: decades of R&D crystallized in algorithms that would take competitors years to replicate. Ecosystem moat: integration with foundry processes, IP libraries, and customer workflows that create switching costs measured in years and millions of dollars. Talent moat: many of the world's best chip design experts work at Synopsys, creating tools for their peers. Customer relationship moat: multi-decade partnerships where Synopsys engineers know customer designs better than the customers themselves.

As Sassine Ghazi surveys the empire in 2025, the position is enviable but not unassailable. Open-source EDA tools are emerging from universities and tech giants' internal teams. China is pouring billions into developing domestic alternatives. Cloud-native startups are targeting specific niches with AI-first approaches. The game board is more complex than ever, but Synopsys holds most of the critical pieces.

IX. Playbook: Business & Strategic Lessons

The Synopsys playbook reads like a masterclass in building an indispensable technology platform, but the lessons go far deeper than typical business strategy. After nearly four decades, patterns emerge that reveal not just how to build a dominant company, but how to architect inevitability itself.

The Platform Consolidation Strategy: Engineering Lock-In Through Integration

Synopsys didn't just build better tools—they built better handcuffs, and convinced customers to put them on willingly. The genius wasn't in any individual product but in how products worked together. Each tool was designed to work 20% better with other Synopsys tools than with competitors' offerings. Not through deliberate incompatibility—that would anger customers—but through thousands of micro-optimizations that collectively created massive efficiency gains.

Consider the Design Compiler to IC Compiler flow. Individually, each tool faces competition. Together, they share data structures, constraint formats, and optimization algorithms in ways that shave weeks off design cycles. A customer might consider switching one tool, but switching both means retraining engineers, rewriting scripts, and accepting months of lower productivity. The technical debt compounds with each additional Synopsys tool adopted, until switching becomes economically irrational.

Riding Technology Waves: The Art of Perpetual Reinvention

Every major technology shift could have obsoleted Synopsys. The move from bipolar to CMOS, from micron to nanometer geometries, from single-core to multi-core, from digital to mixed-signal, from chips to chiplets—each transition threatened existing tools and created openings for new competitors. Synopsys not only survived these transitions but used them to strengthen their position.

The key insight: treat disruption as a revenue opportunity, not a threat. When designs moved below 90 nanometers and new physical effects emerged, Synopsys didn't just patch existing tools—they acquired companies like Avant! and Nassda that had built new solutions from scratch. When AI emerged as a design paradigm, they didn't bolt on machine learning features—they rebuilt entire tool flows around AI-native architectures.

M&A as Core Competency: The Science of Strategic Acquisition

Over 100 acquisitions without a major failure is statistically improbable unless you've turned M&A into a science. Synopsys developed a framework that venture capitalists now study:

First, acquire problems, not just products. Every acquisition targeted a specific customer pain point that Synopsys couldn't address organically fast enough. Avant! brought physical design when customers were struggling with deep submicron effects. Virage brought IP when customers wanted pre-validated blocks. Coverity brought security when software vulnerabilities became board-level concerns.

Second, preserve the magic. Unlike traditional acquirers who gut purchases for IP and lay off teams, Synopsys treated acquisitions like organ transplants. Key teams stayed intact, often in their original locations. The Nassda team that allegedly stole Synopsys code? They were welcomed as heroes and given resources to enhance their tools. This approach turned potential competitors into innovation engines.

Third, integrate gradually. Rather than forcing immediate integration, Synopsys followed an "embrace, extend, integrate" strategy. New tools first worked alongside existing ones, then gradually shared more infrastructure, finally becoming indistinguishable parts of the platform. Customers barely noticed the transitions, but suddenly found their workflows more efficient.

Customer Lock-In Through Workflow Integration

The most powerful lock-in isn't technical—it's procedural. Synopsys tools didn't just process designs; they shaped how engineers thought about design itself. The concepts embedded in Design Compiler—synthesis, constraints, optimization—became the mental models for an entire generation of chip designers.

Universities taught using Synopsys tools, creating graduates who thought in Synopsys paradigms. Design methodologies published by Synopsys became industry standards. Even competitors had to ensure their tools could read Synopsys formats and follow Synopsys flows. The company had achieved the ultimate platform effect: they didn't just win in the market; they defined what the market was.

Balancing Innovation vs. Acquisition

The perpetual challenge for any acquisitive company: how do you maintain internal innovation when employees know you can just buy whatever you need? Synopsys solved this through careful portfolio management.

Core technologies—synthesis, place-and-route, timing analysis—remained primarily internal development, with acquisitions adding complementary capabilities. Emerging areas—AI, cloud, security—were jump-started through acquisition then enhanced internally. The message to employees was clear: acquisitions accelerate but don't replace innovation.

The company also mastered the art of "acqui-hiring"—buying small companies primarily for their talent. These weren't traditional acquisitions but rather elaborate recruiting operations, bringing in entire teams with proven chemistry and domain expertise.

The Continuous Leadership Paradox

Under the continuous leadership of co-founder and CEO Aart de Geus for nearly four decades, Synopsys navigated multiple semiconductor industry cycles while maintaining technological leadership. This presents a paradox: how does a company stay innovative under such stable leadership?

The answer lies in de Geus' unusual combination of technical depth and strategic flexibility. Unlike many founder-CEOs who become trapped by their original vision, de Geus continuously reimagined what Synopsys could be. From synthesis to EDA platform to IP powerhouse to AI-driven design—each transformation was radical yet felt natural because the leadership provided continuity of purpose amid discontinuity of strategy.

The succession to Sassine Ghazi in 2024 was masterfully orchestrated—a decades-long apprenticeship that ensured continuity while bringing fresh perspective. Ghazi had been with Synopsys long enough to understand its DNA but brought the outsider's eye needed for the next transformation.

The Invisible Infrastructure Advantage

Perhaps the most underappreciated aspect of Synopsys' strategy: they became invisible infrastructure that customers couldn't live without. Unlike consumer-facing companies that must constantly fight for attention, Synopsys embedded itself so deeply in customer workflows that its presence was assumed, like electricity or running water.

This invisibility is a superpower. Customers don't question essential infrastructure; they build around it. Every year, switching costs increase not through deliberate lock-in but through accumulated dependencies. Scripts reference Synopsys tools. Methodologies assume Synopsys flows. Engineer muscle memory is trained on Synopsys interfaces.

The playbook's ultimate lesson: in technology markets, the most powerful position isn't being the best—it's being inevitable.

X. Bear vs. Bull Case Analysis

Bull Case: The Compound Acceleration Thesis

The optimistic case for Synopsys rests on a fundamental observation: chip complexity isn't just growing; it's growing at an accelerating rate. And Synopsys has positioned itself as the toll-booth operator on the only road to managing this complexity.

Start with the inexorable march of AI. Every major technology company is now designing custom AI chips—Google's TPUs, Amazon's Trainium, Tesla's Dojo, Apple's Neural Engine. These aren't incremental improvements but radical reimaginings of compute architecture, each requiring billions in design investment and the most sophisticated tools available. The TAM expansion is staggering: from serving 20-30 major chip companies to potentially hundreds of AI-ambitious enterprises.

The Ansys integration unlocks value that neither company could achieve alone. Consider thermal management in modern data centers: an AI chip running at 400 watts affects the performance of every component around it. The ability to co-simulate chip behavior and cooling systems in real-time transforms design from sequential to parallel, compressing development cycles by potentially 50%. Customers will pay premium prices for this capability because time-to-market in AI is measured in competitive advantage worth billions.

The business model dynamics are approaching perfection. Recurring revenue now exceeds 90% of total revenue, providing visibility that most software companies dream of. The shift to time-based licenses means Synopsys gets paid whether customers use tools intensively or occasionally—they're paying for insurance, not usage. As designs get more complex, customers need more tool capacity, driving organic seat expansion without additional sales effort.

The AI-powered tools create a virtuous cycle that competitors can't easily replicate. DSO.ai learns from every design it optimizes, getting smarter with each customer deployment. This creates compound advantages: early adopters get good results, their success attracts more customers, more customers generate more learning data, which improves results further. It's the same playbook that made Google's search unassailable, applied to chip design.

Geographic diversification provides multiple growth vectors. Despite tensions, China's semiconductor ambitions require Western tools for at least another decade—they're 5-7 years behind in EDA capabilities. India's semiconductor initiatives are just beginning, with the government committing $15 billion to build domestic capacity. The reshoring of semiconductor manufacturing to the US and Europe creates entirely new customer bases that need full tool suites from day one.

The margins tell the story of a business approaching optimal economics. Gross margins typically exceed 70%, reflecting minimal marginal costs for software delivery. R&D spending, while high in absolute terms, generates returns that compound over decades. Customer acquisition costs are negligible for a company where relationships span decades and expand naturally.

Bear Case: The Icarus Risk Scenario

The pessimistic case starts with a sobering reality: Synopsys has never been more powerful, or more vulnerable. The same factors driving current success create unprecedented risks.

The Ansys integration could become a $35 billion disaster. Merging two companies with different cultures, overlapping products, and complex customer relationships is treacherous at any scale. At $35 billion, failure isn't just expensive—it's existential. Cultural clashes between Synopsys' Silicon Valley ethos and Ansys' industrial simulation heritage could paralyze innovation. Customer confusion over product roadmaps could create openings for competitors. The debt burden limits financial flexibility just as the company needs to invest heavily in integration.

China exposure is a ticking time bomb. With roughly 16% of revenue from China, any escalation in technology restrictions could vaporize $1 billion in annual revenue overnight. The temporary suspension of sales in June 2025 was a warning shot—the next restriction might be permanent. Chinese customers are actively developing domestic alternatives with unlimited government funding. Every year, the quality gap narrows. By 2030, Chinese EDA tools might be good enough for many applications, eroding not just China revenue but creating low-cost competition globally.

Open-source EDA is gaining momentum in ways that mirror Linux's disruption of proprietary operating systems. Google, desperate to reduce EDA costs for its massive chip design efforts, is funding open-source tool development. Universities are contributing algorithms that match commercial capabilities in specific areas. While open-source tools aren't yet comprehensive enough to replace Synopsys, they're good enough to handle 20-30% of design tasks—exactly the low-complexity, high-volume work that provides Synopsys' profit cushion.

Customer concentration creates cascading risk. If Samsung decided to develop internal tools—as Apple did with many software categories—it could crater 5-10% of revenue. The hyperscalers designing their own chips have both the resources and motivation to build proprietary tools. Amazon has already built internal tools for specific design tasks. If this trend accelerates, Synopsys could face the innovator's dilemma: their best customers becoming their biggest competitors.

The debt burden from the Ansys acquisition fundamentally changes the company's risk profile. With $16 billion in new debt, Synopsys must generate consistent cash flows to service obligations. Any revenue disruption—from China restrictions, customer losses, or competitive pressure—could trigger a downward spiral. The company that survived every semiconductor downturn with minimal leverage now faces the next one highly leveraged.

Technical disruption looms from unexpected directions. Quantum computing might obsolete traditional chip design paradigms. Neuromorphic computing could require entirely different design tools. Optical computing is moving from research to reality. Synopsys must invest in all these potential futures while maintaining current tools—a resource allocation challenge that even excellent companies often fumble.

The generational leadership transition adds uncertainty. While Ghazi is highly capable, he lacks de Geus' founder authority and four-decade relationship network. In a relationship business where CEO connections can make or break major deals, this transition occurs just as the company faces its most complex integration challenge ever.

Valuation multiples have expanded to levels that assume perfect execution. Any stumble—an integration delay, a customer loss, a competitive surprise—could trigger multiple compression that erases tens of billions in market value. The stock price embeds expectations that may be mathematically impossible to achieve.

The Verdict: Asymmetric Uncertainty

The bull and bear cases aren't equally weighted—they exist in different timeframes. The bull case is playing out now: AI driving complexity, customers locked in, margins expanding. The bear case represents future risks that could materialize suddenly. This asymmetry makes Synopsys simultaneously a safe haven and a potential value trap.

For investors, the key question isn't whether Synopsys will remain dominant—inertia alone guarantees years of strong performance. The question is whether the company can navigate the Ansys integration while managing geopolitical risks and technical disruption. Success would create one of the most valuable technology companies in history. Failure would be proportionally spectacular. In the end, Synopsys embodies the fundamental tension of platform businesses: the same network effects that create dominance also create fragility.

XI. Epilogue & Future Outlook

As the sun sets over Synopsys' Sunnyvale headquarters in late 2025, Sassine Ghazi stands where Aart de Geus once stood, contemplating a transformation as profound as any in the company's four-decade history. The acquisition of Ansys isn't just closed—it's the opening move in a game whose rules are still being written.

The silicon-to-systems vision that drove the Ansys acquisition represents more than product integration—it's a fundamental reimagining of what design means in an era where the boundaries between hardware, software, and systems have dissolved. A modern AI accelerator isn't just silicon; it's silicon plus cooling plus power delivery plus electromagnetic shielding plus software orchestration. The company that can optimize across all these dimensions doesn't just win design sockets—it shapes what's possible to build.

The numbers suggest a trajectory toward rarified air. With the Ansys integration, combined revenue approaching $10 billion annually, and margins that could expand as AI-driven automation reduces manual design effort, Synopsys could reach a $200 billion market capitalization within five years. That would place it among the 50 most valuable companies globally—extraordinary for a business most people have never heard of.

But the real future isn't in the numbers—it's in the implications of ubiquitous intelligence. As AI moves from data centers to edges, from smartphones to smart dust, the number of custom chips needed explodes exponentially. Every autonomous vehicle needs dozens of custom processors. Every smart city sensor needs optimized silicon. Every augmented reality device needs purpose-built accelerators. The market for chip design tools could expand 10x in a decade.

AI's impact on chip design complexity follows a reflexive loop that benefits Synopsys at every turn. AI applications need specialized chips, which are too complex for human designers, requiring AI-powered tools to design them, which Synopsys provides. The more successful AI becomes, the more it drives demand for the tools needed to create it. It's a perpetual motion machine of complexity and capability.

The emerging competitors aren't traditional EDA companies but the hyperscalers themselves. Google's internal chip design tools, Amazon's custom silicon initiatives, and Microsoft's infrastructure investments suggest a future where the biggest customers might become competitors. But history suggests a different outcome: just as cloud providers still use enterprise software despite building their own versions, chip designers will likely use commercial tools for most tasks while building specialized capabilities for specific needs.

The geopolitical landscape remains the wildcard. The semiconductor industry has become the frontline of great power competition, with chip design tools as critical as the chips themselves. Synopsys must navigate being simultaneously essential to US technological superiority and accessible to global customers. It's a balance that will require diplomatic finesse equal to technical excellence.

What would happen if Synopsys didn't exist? The thought experiment reveals the company's true importance. Chip design would slow to a crawl. Many advanced designs would become economically unfeasible. The pace of innovation in everything from smartphones to supercomputers would decelerate dramatically. In a very real sense, Synopsys is a load-bearing wall in the edifice of modern technology—invisible but essential, unglamorous but irreplaceable.

Looking ahead, three scenarios seem possible:

The Acceleration Scenario: AI drives exponential growth in chip complexity, the Ansys integration succeeds spectacularly, and Synopsys becomes the orchestration layer for all hardware/software/systems co-design. Market cap reaches $300 billion by 2030.

The Steady State Scenario: Growth continues but moderates, competitors nibble at edges without threatening the core, and Synopsys remains dominant but not dramatically more valuable. Market cap reaches $150 billion by 2030.

The Disruption Scenario: Open-source tools gain critical mass, China develops viable alternatives, and hyperscalers build internal capabilities. Synopsys remains profitable but growth stalls. Market cap stagnates around $100 billion.

The probability distribution across these scenarios isn't uniform. The massive switching costs, accumulated technical advantages, and accelerating complexity of chip design make the acceleration scenario more likely than linear extrapolation suggests. But the disruption scenario, while less probable, would be far more consequential—a reminder that in technology, dominance is always temporary, even when it seems permanent.

As we close this analysis, it's worth returning to that Research Triangle Park garage in 1986. Four engineers with an idea about automating chip design have built something that transcends its origins. Synopsys isn't just a tools company—it's the nervous system of the semiconductor industry, the infrastructure that makes all other infrastructure possible.

The story of Synopsys is ultimately a story about abstraction—the most powerful force in technology. Each level of abstraction enables exponentially more complexity while hiding that complexity from users. From transistors to gates, gates to RTL, RTL to systems—each abstraction layer that Synopsys conquered multiplied the value they could create and capture.

The next abstraction layer might be the most profound yet: from designing chips to designing intelligence itself. As AI systems become capable of designing better AI systems, the tools that orchestrate this recursive improvement become infinitely valuable. Synopsys, after four decades of enabling Moore's Law, might be about to enable something even more transformative: the automation of innovation itself.

The future isn't just about silicon or software or systems. It's about the convergence of all three into something we don't yet have words for. Whatever emerges, it will be designed with Synopsys tools, optimized with Synopsys AI, and verified with Synopsys IP. In the grand casino of technology investing, that's as close to a sure bet as exists.

Yet certainty in technology is always an illusion. The only certainty is that the future will surprise us, disrupt our assumptions, and create opportunities we can't currently imagine. For Synopsys, the challenge isn't just to persist but to continue transforming—to be the disruption rather than the disrupted, to obsolete themselves before someone else does.

The company that began by automating logic synthesis might end by synthesizing the future itself. Not a bad outcome for a garage startup. Not a bad bet for investors willing to think in decades rather than quarters. And certainly not a bad business to be in as humanity attempts to build intelligence that surpasses our own.

The story continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube