SAP SE: The Empire of Enterprise Software

I. Introduction & Episode Setup

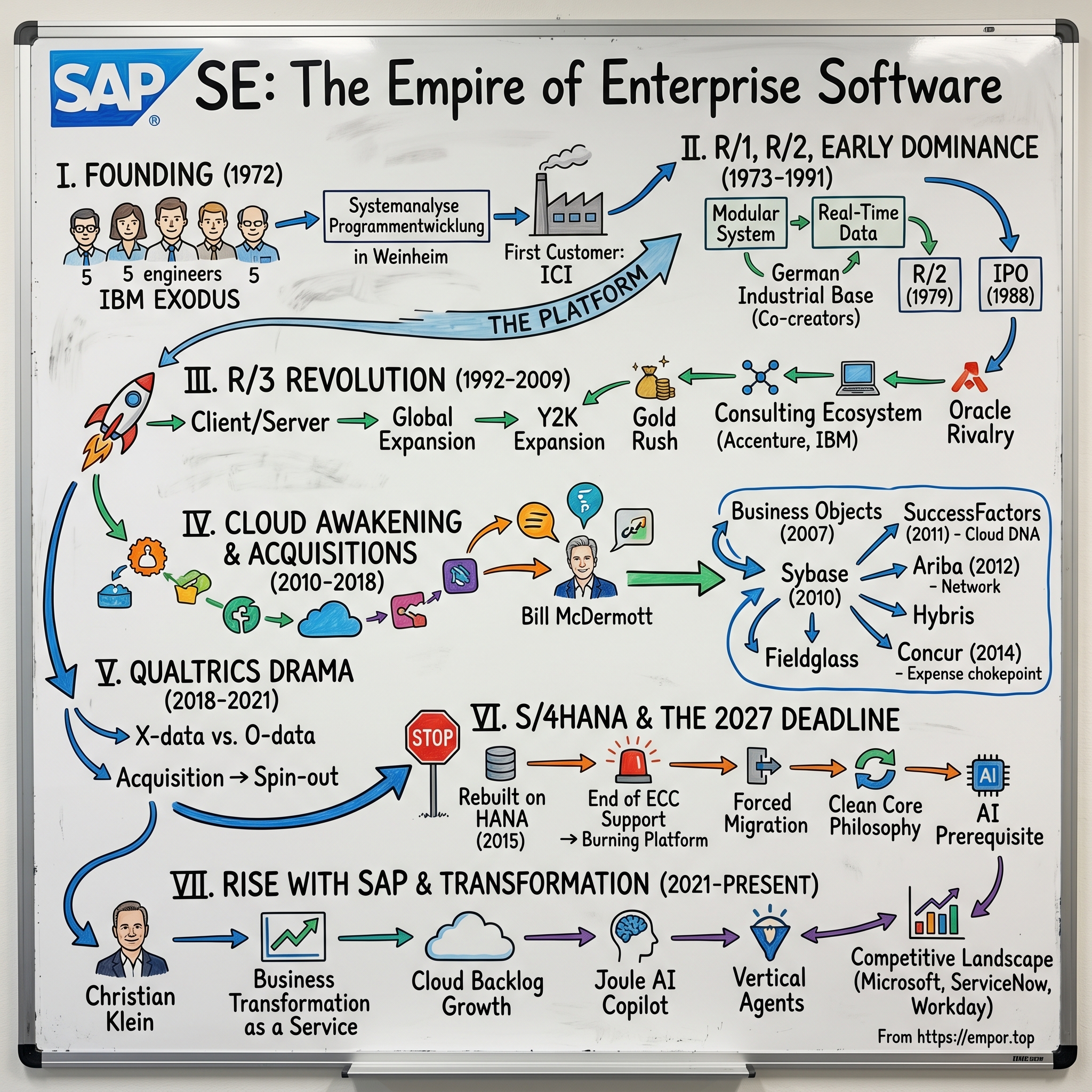

Picture this: Five IBM engineers from the AI department in Mannheim are working on an enterprise-wide system, convinced they're building the future of business computing. Then IBM drops the hammer: their project would "no longer be necessary." Most people would update their resumes and move on. But Dietmar Hopp, Hasso Plattner, Claus Wellenreuther, Klaus Tschira, and Hans-Werner Hector had different plans. On April 1, 1972, these five engineers launched what would become one of the most powerful software empires ever built.

Today, SAP is the world's largest vendor of enterprise resource planning (ERP) software, with more than 269 million cloud users and over 100 solutions spanning every conceivable business function. Here's the staggering part: 77% of global transaction revenue touches an SAP system. That's right—whether you're buying a coffee, booking a flight, or ordering something online, there's a three-in-four chance SAP is somewhere in that transaction chain. As of December 2023, SAP is the largest German company by market capitalization, worth over $200 billion.

The paradox of SAP is remarkable: it's simultaneously the most boring and most essential software on the planet. No teenager dreams of working in ERP. No Silicon Valley startup pitch deck gets VCs excited by promising to be "the next SAP." Yet this unsexy German software company has built one of the most enduring competitive moats in technology history. How did they pull it off?

This is a story about German engineering culture meeting platform economics, about creating switching costs so high that leaving becomes corporate suicide, and about a company that has managed to reinvent itself through multiple technology transitions while maintaining an iron grip on the world's largest enterprises. It's about five engineers who didn't just build software—they built infrastructure so fundamental to global commerce that dismantling it would be like removing the plumbing from a skyscraper.

As we dive into SAP's five-decade journey, we'll explore how they turned enterprise software from a custom consulting nightmare into a standardized platform, how they've navigated the treacherous transition from on-premise to cloud (spoiler: it's been messy), and why, despite all the complaints from customers about complexity and cost, SAP remains utterly irreplaceable for most of the Fortune 500. Buckle up—this is going to be a long ride through the least sexy, most profitable corner of the software universe.

II. The IBM Exodus & Founding Story (1972)

The Mannheim office of IBM Deutschland in 1971 was humming with the kind of energy that only comes when engineers believe they're onto something revolutionary. Hasso Plattner, Klaus Tschira, Claus Wellenreuther, Dietmar Hopp and Hans-Werner Hector weren't just any IBM engineers—they were part of the artificial intelligence department, working on what would have been called cutting-edge computing at the time. Their project had an ambitious goal: create an enterprise-wide system that could integrate all of a company's operations in real-time.

The trigger moment came with stunning corporate brutality. In 1971, Xerox contracted IBM to migrate its business systems on to IBM technology platforms, and the five engineers began working on this massive undertaking. But IBM's leadership had other plans. The project that these five engineers had poured themselves into was suddenly deemed unnecessary—a strategic shift that would prove to be one of the most costly decisions in IBM's history.

Their idea was to create standard enterprise software that integrated all business processes and enabled data processing in real time. Think about how radical this was in 1972. At the time, most business computing meant batch processing—you'd input your data on punch cards, wait overnight, and get your results the next morning. Real-time processing was exotic, expensive, and typically custom-built for each company. These five engineers wanted to flip the entire model.

Dietmar Hopp, Hasso Plattner, Claus Wellenreuther, Klaus Tschira, and Hans-Werner Hector left IBM and founded a company called Systemanalyse Programmentwicklung, meaning "system analysis program development". Their goal was to create software that integrates business processes and made data available in real time. Initially trading as a private partnership, the company set up its headquarters in Weinheim, Germany, and opened an office in nearby Mannheim.

The early days were gloriously scrappy. But its founders spent most of their time working a few miles away at the data center operated by their first customer, the German subsidiary of Imperial Chemical Industries. Imagine that—your entire company strategy depends on camping out in your customer's data center because you can't afford your own computers. SAP's founders and employees worked closely with customers - often sitting side-by-side with employees in customers' offices to learn their business needs and processes.

This wasn't just a necessity born of poverty—it was a philosophical choice that would define SAP's entire approach to enterprise software. Rather than building software in isolation and hoping companies would adapt to it, they embedded themselves directly into their customers' operations. They learned how purchasing really worked, how inventory actually moved, how financial processes truly operated—not in theory, but by watching real people do real work.

Toward the end of the year, the entrepreneurs and their two-strong workforce completed a materials, information, and accounting system known as "MIAS". This wasn't just their first product—it was proof that their vision could work. Standard software that multiple companies could use, processing data in real time, integrating different business functions. The German industrial establishment, always eager for efficiency and standardization, would prove to be the perfect launching pad for this new approach to enterprise computing.

III. Building the Platform: R/1, R/2, and Early Dominance (1973–1991)

The company launched its first financial accounting system. They named it RF, with the "R" standing for "real time", and it became the cornerstone for a modular system that later came to be known as "SAP R/1". That "R" would become SAP's calling card—a constant reminder that while competitors were still batch processing, SAP was delivering real-time business intelligence.

The German industrial complex became SAP's perfect breeding ground. Companies like Freudenberg, Holsten Brewery, and Dr. Oetker weren't just customers—they were co-creators. Each implementation taught SAP something new about how businesses actually operated, and each lesson was encoded into the software. This created a powerful flywheel: more customers meant more knowledge, which meant better software, which attracted more customers.

In 1979, SAP launched SAP R/2, expanding the capabilities of the system to other areas, such as materials management and production planning. R/2 wasn't just an incremental upgrade—it was a complete reimagining of what enterprise software could be. This tight integration gave SAP its unique selling point in the burgeoning ERP market, as well as heralding a new era for the company with the R/2 version being launched in 1980. Upgrading the supporting servers in SAP, as well as the tighter integration between the growing number of functional areas, made R/2 a popular software solution for the next ten years.

The power of standardization versus custom solutions became increasingly apparent. While competitors like Siemens and local consulting firms were building bespoke systems for each client—essentially reinventing the wheel every time—SAP was building once and selling many times. But here's the genius part: they made standardization feel like customization through configuration. You could set thousands of parameters to make SAP work exactly how your business needed it to, but underneath, everyone was running the same core code.

Building switching costs was an art form that SAP perfected early. Once a company implemented SAP, three things happened: First, they'd spend millions on implementation, often more than the software itself. Second, they'd train hundreds or thousands of employees on SAP-specific processes. Third, and most insidiously, they'd reshape their entire business processes around SAP's way of doing things. After a few years, it became impossible to tell where the company ended and SAP began.

Revenues began to grow as the company expanded to take on new clients outside of the German market: Austria in 1977 and France in 1978. But the real explosion came in the 1980s. A new limited liability company is launched – trading as SAP GmbH Systeme, Anwendungen und Produkte in der Datenverarbeitung – and handling the administration and sales operations. It would be another five years before the original private partnership is dissolved and the rights transferred to the new entity.

In August 1988, SAP GmbH became SAP AG, and public trading started on 4 November 1988. Shares were listed on the Frankfurt and Stuttgart stock exchanges. The IPO wasn't just about raising capital—it was a declaration that this German enterprise software company was ready to take on the world. And the timing couldn't have been better, because SAP was about to unveil something that would change enterprise computing forever.

IV. The R/3 Revolution & Global Domination (1992–2009)

SAP R/3 was officially launched on 6 July 1992. If R/2 was evolution, R/3 was revolution. SAP R/3 launched in July 1992, and offered a number of significant changes from its predecessors. It was the first major release from SAP since SAP R/2 which was popular with organizations throughout the 80s. The main difference with SAP 3 was that it is classed as a client/server system, whereas previous SAP versions were classed as mainframe systems. This enabled SAP R/3 to open up a whole new customer base for SAP and was a big part of the company's expansion.

The shift from mainframe to client-server architecture was like moving from steam engines to combustion engines. Suddenly, SAP could run on much cheaper hardware, scale more flexibly, and most importantly, put actual user interfaces on desktop computers instead of green-screen terminals. Launched in 1991, SAP R/3 was another revolutionary product. In fact, SAP R/3 was the product that shot SAP to stardom. The application was rewritten to exploit the power of a layered, three-tier architecture approach.

But the real killer app for R/3? Y2K. As the millennium approached, companies worldwide faced a terrifying reality: their legacy systems, many still running COBOL from the 1960s, stored years as two digits. When "99" rolled over to "00," these systems would think it was 1900, potentially causing catastrophic failures. In the early '90s, companies began moving from mainframe computing systems to client server environments -- a transition fueled by the explosion of the internet and corresponding need for a "Y2K solution." At SAP, this was represented by the conversion from mainframe application SAP R/2 to client server application SAP R/3.

SAP's timing was immaculate. R/3 was Y2K compliant out of the box. Suddenly, migrating to SAP wasn't just about efficiency or integration—it was about survival. Companies that might have delayed an ERP implementation for years were forced to act. The late 1990s became a gold rush for SAP, with implementations happening at a pace that would never be repeated.

The consulting ecosystem that emerged around R/3 was perhaps even more important than the software itself. Accenture, Deloitte, IBM, PwC—they all built massive practices around SAP implementation. These weren't just service providers; they were evangelists, convincing every Fortune 500 CEO that SAP was the safe, smart choice. The consulting fees often dwarfed the software licenses. A typical large enterprise might spend $10 million on SAP licenses but $50-100 million on implementation.

The battle with Oracle during this period was epic. Oracle had the database layer locked down—even SAP primarily ran on Oracle databases. But Larry Ellison wanted the application layer too. The rivalry was personal and vicious. SAP would emphasize their integrated suite versus Oracle's "best of breed" approach. Oracle would counter by acquiring application vendors and claiming better performance. But by the early 2000s, SAP had won the ERP war decisively. SAP came to dominate the large business applications market over the next 10 years.

The dot-com bust of 2001 should have been devastating for SAP. Their stock crashed, IT spending froze, and many of their customers were hemorrhaging money. But SAP had built something antithetical to the bubble: boring, essential software that companies couldn't live without. You might cancel your CRM project or delay your e-commerce platform, but you couldn't stop running payroll or tracking inventory. SAP's recurring maintenance revenue—charging companies 17-22% annually just to keep the lights on—became their cushion against the crash.

By the mid-2000s, SAP seemed invincible in ERP. But cracks were starting to show. Salesforce.com launched in 1999 with a "No Software" campaign that directly attacked SAP's on-premise model. Cloud computing was still nascent, but the writing was on the wall. SAP tried to counter with mySAP.com, but it was clearly a traditional software company trying to paint cloud stripes on itself. The real transformation would require more drastic measures.

V. The Cloud Awakening & Acquisition Spree (2010–2018)

The early 2010s found SAP in an existential crisis they didn't fully want to admit. Cloud-native competitors weren't just nibbling at the edges—they were fundamentally challenging SAP's entire business model. Workday was reimagining HR from the ground up. Salesforce had already conquered CRM. NetSuite was attacking the mid-market. And these weren't just features differences—these were architectural advantages that SAP couldn't match with its decades-old codebase.

Enter Bill McDermott, the American CEO who would attempt to drag this German engineering company into the cloud era. McDermott understood something crucial: SAP couldn't build its way to the cloud. It would have to buy its way there. What followed was one of the most aggressive acquisition sprees in enterprise software history.

SAP (SAP) has made a number of big acquisitions in the past. These include $6.8 billion acquisition of Business Objects (a Business Intelligence product) in October 2007, the acquisition of Sybase (a Database product) for $5.8 billion in May 2010, the acquisition of SuccessFactors (a Talent Management product) for $3.4 billion in December 2011, and the acquisition of Ariba (a supplier network) for $4.3 billion in October 2012.

Let's break down the strategic logic of each major deal:

SuccessFactors ($3.4B, 2011) was the opening salvo. Out of these, SuccessFactors and Ariba have played an important role in SAP's cloud services business growth. This wasn't just about getting cloud HR capabilities—it was about acquiring cloud DNA. SuccessFactors knew how to build, sell, and operate multi-tenant SaaS at scale. SAP desperately needed that knowledge.

It paid $3.4 billion for SuccessFactors in 2011 and $4.3 billion for Ariba in 2012. Ariba was particularly clever. It wasn't just procurement software—it was a network. In 2012, SAP acquired Ariba, a long-time leader in spend management software. Our cloud-based solutions for strategic sourcing, contract management, procurement, and supplier management help companies control costs and minimize risks as they collaborate with suppliers on the purchase of goods and services. Their transactions take place over Ariba Network, where millions of trading partners do trillions of dollars in business every year. Once suppliers and buyers were connected on Ariba, the switching costs became astronomical. You weren't just changing software; you were asking thousands of business partners to change how they interacted with you.

Then came the blockbuster: German business software maker SAP (SAPG.DE) said on Thursday it has agreed to acquire U.S.-based expense management software maker Concur Technologies Inc (CNQR.O) in an all-stock deal valued at $7.3 billion that expands its presence in internet-based software or so-called cloud computing. Based on 57 million outstanding shares, the offer for Bellevue, Washington-based Concur is valued at $7.3 billion. Including debt, the offer represents an enterprise value of about $8.3 billion, SAP said.

The Concur acquisition in 2014 was massive—Concur Technologies is the largest acquisition in SAP's 42-year history. But the price made sense when you understood what SAP was really buying: Concur has 23,000 clients that include companies, governments and universities, with more than 25 million users of its business expense and travel management software and services. This wasn't just software—it was capturing a chokepoint in enterprise operations. Every business travels. Every business has expenses. Concur owned that workflow.

SAP also recently acquired Hybris and Fieldglass to further leverage the cloud market growth. Each acquisition added a new cloud pillar, but integration was a nightmare. These companies were built on different architectures, with different user experiences, different data models. SAP's promise of an integrated suite started looking more like a collection of loosely affiliated applications with SAP logos slapped on them.

Meanwhile, SAP HANA—the in-memory database platform—was both SAP's greatest technical achievement and its biggest strategic gamble. In 2011, the first customers started using the in-memory database SAP HANA. The technology was genuinely revolutionary: by keeping data in RAM instead of on disk, HANA could perform analytics that previously took hours in seconds. But SAP made a controversial decision: future innovations would require HANA. Want the latest features? You need to migrate your entire database layer. It was a forcing function that customers resented but couldn't ignore.

By 2018, SAP's cloud transformation was showing mixed results. Cloud revenue was growing rapidly, but largely through acquisitions. The core ERP cloud offering was still struggling. In 2024, SAP's overall revenue climbed to €34.18 billion, marking a 10% increase compared to the previous year. A significant portion of this success came from SAP's cloud business, which earned €17.14 billion: a sharp 25% jump from 2023. Adjusting for constant currencies, cloud revenue saw an even stronger 26% increase. But these numbers came years later—in 2018, SAP was still trying to convince customers that cloud ERP wasn't crazy.

VI. The Qualtrics Drama & Experience Data Play (2018–2021)

The Qualtrics saga is perhaps the most dramatic acquisition story in SAP's history. Qualtrics CEO Ryan Smith was preparing for an IPO that would've likely valued his company at about $6 billion, but then SAP CEO Bill McDermott made the critical call. Picture the scene: Ryan Smith, the company's CEO, was reluctant to do the deal. He went back and forth on the sale, leaving SAP unsure if it would get done until Sunday, according to a person familiar with the matter. While the $8 billion price had been agreed to weeks ago, Smith struggled with the idea of losing control of the company he founded.

This wasn't a typical tech acquisition where founders cash out happily. Smith had originally launched Qualtrics in Provo, Utah out of his parent's basement in 2002. About 16 years later, Smith was preparing to take Qualtrics to go public. However, the company was acquired by SAP four days before the IPO was supposed to happen. The timing was absolutely brutal. The roadshow was complete, the books were oversubscribed, the pricing was set. Qualtrics was literally four days from ringing the bell at the NYSE.

SAP is acquiring Qualtrics for $8 billion, snapping up the survey software company just before its planned IPO. The all-cash deal has been approved by the boards of both companies and by Qualtrics shareholders, SAP said in a statement on Sunday. The price represented a massive premium—SAP CEO Bill McDermott preempted the IPO with an all-cash offer that was more than 75 percent higher than the company's projected valuation.

But why would SAP pay such a premium? The answer lay in McDermott's vision of "X-data versus O-data." O-data (Operational data) was what SAP had always managed—transactions, inventory, finances. X-data (Experience data) was about feelings, satisfaction, sentiment. In McDermott's view, combining these would create an unbeatable competitive advantage. You wouldn't just know that sales were down; you'd know that customer satisfaction dropped two weeks ago in the Northeast region because of a shipping delay that frustrated your highest-value segment.

The integration challenges were immediate and profound. Based on investor demand, the Qualtrics IPO was 13 times oversubscribed—meaning investors desperately wanted in on this company. Now those same investors were questioning why Qualtrics would sell to slow-moving SAP. The cultural clash was even worse. Qualtrics was a Utah-based startup with a scrappy, entrepreneurial culture. SAP was a German enterprise software giant with processes for processes.

In the first half of 2018, Qualtrics recorded revenue growth of 41.7 percent to $184.2 million. By contrast, SurveyMonkey had $121.2 million in revenue during that same period, up 14 percent. After generating a profit in 2017, Qualtrics reported a $3.4 million net loss for the first six months of this year. The growth rate was impressive, but the losses raised questions about SAP's ability to integrate yet another acquisition successfully.

The story took an unexpected turn in July 2020. SAP announced Sunday that it will spin out its Qualtrics unit with an IPO, less than two years after acquiring the experience management company for $8 billion. SAP plans to maintain majority ownership of Qualtrics, which is co-headquartered in Provo, Utah, and Seattle. Qualtrics' leadership team intends to remain in place, including founder Ryan Smith, who will be the largest individual shareholder. "SAP's acquisition of Qualtrics has been a great success and has outperformed our expectations with 2019 cloud growth in excess of 40 percent, demonstrating very strong performance in the current setup," SAP CEO Christian Klein said in a statement.

The spin-out was remarkable for what it represented: an admission that some acquisitions are better kept at arm's length. SAP would keep majority control but give Qualtrics the independence to maintain its culture and growth trajectory. It was a new model for SAP—somewhere between full integration and complete separation. Ryan Smith finally got his IPO, albeit in a very different form than originally planned. The whole saga illustrated both SAP's desperate need for growth assets and the challenges of integrating modern cloud companies into a traditional enterprise software giant.

VII. S/4HANA & The 2027 Deadline

This section was updated on 22-04-2026.

While the Qualtrics drama played out in headlines, a far more consequential story was unfolding in the background—one that would ultimately reshape SAP's entire customer base. On February 3, 2015, SAP announced SAP S/4HANA, a new business suite fully rebuilt on the in-memory HANA platform. This wasn't another incremental release dressed up in fresh marketing. It was a complete reimagining of SAP's core ERP suite, stripped of decades of accumulated complexity, simplified, modernized, and explicitly designed to become the digital core of the modern enterprise. Everything SAP had learned from four decades of running the world's largest companies was being poured into this single product—and everything SAP was about to do strategically would hinge on getting customers onto it.

Then came the controversial decision that would define the next decade: SAP set a deadline. Mainstream maintenance for the legacy ECC suite would end—originally in 2025, eventually extended to 2027 after customer pushback made the first date untenable. If you were still on ECC after that, you faced a choice: pay extended maintenance fees through 2030, or make the jump to S/4HANA. The extension was SAP's one concession. After that, the line was held, and by 2026 it had hardened into something close to an article of faith inside Walldorf.

The forced migration playbook is classic enterprise software strategy, but SAP has elevated it to an art form. Here's how it works. You announce end-of-support for your legacy product far enough in advance that customers can't claim surprise, but close enough that they feel pressure. You offer carrots—genuine innovation, dramatically better performance, a path to AI—and sticks: no more security patches, no more new features, rising maintenance costs, and eventually, no one left at SAP who remembers how the old thing worked. Then you watch as your entire customer base, having spent two decades embedding your software into every corner of their operations, discovers they have nowhere else to go. It's the burning platform strategy, and SAP built a taller platform and hotter flames than anyone in the industry.

For years, the playbook looked like it might not work. Through 2023 and 2024, the migration numbers were genuinely ugly. Nearly two-thirds of ECC customers hadn't even licensed S/4HANA by mid-2024, and Gartner was openly skeptical that SAP could hit its own targets. The complaints from customers were consistent and legitimate. A full ECC-to-S/4HANA migration could take 18 to 36 months for a large enterprise, often longer. Companies that had spent twenty years bending ECC to fit their exact business processes were being told those customizations were, in effect, the problem. And the price tags—tens of millions for software and hundreds of millions for implementation—made even the most well-funded CIOs flinch.

Then, roughly eighteen months ago, the curve started to bend. By early 2026, roughly 40% of SAP's traditional support revenue base had initiated the move to Cloud ERP, and S/4HANA Cloud revenue was growing at a 30%-plus annual clip, meaningfully outpacing SAP's overall cloud growth. The backlog of signed-but-not-yet-deployed contracts swelled into the tens of billions of euros. What had looked like a slow-motion customer revolt was turning into something closer to a coordinated stampede—not because customers had suddenly fallen in love with S/4HANA, but because the math had finally tipped. With less than two years left on the clock, extended maintenance fees looked more expensive than the migration itself, and sitting on ECC past 2027 looked like taking unpatched mission-critical software into a world of increasingly sophisticated cyber threats. Inertia, SAP's traditional enemy, had flipped sides.

The negotiation dynamics in 2026 are fascinating to watch up close. Every large customer renewal is now a multi-dimensional chess game: maintenance fees on legacy ECC versus subscription economics on S/4HANA Cloud, credits for existing on-premise licenses, bundling of HANA, BTP, and AI modules, and the ever-present question of how much of the migration risk SAP itself will absorb. The UK & Ireland SAP User Group, ASUG in the Americas, and DSAG in the German-speaking market have all become quasi-unions, collectively bargaining for better terms on behalf of their members. SAP, for its part, has gotten shrewder—offering sweeter deals to early movers, harder terms to the laggards, and tailored packages to the marquee accounts whose public migration announcements double as marketing. It's brinksmanship, but brinksmanship where both sides ultimately need each other to cross the river.

But the real strategic master stroke of the S/4HANA era isn't the deadline. It's the "Clean Core." The pitch to customers is deceptively simple: stop modifying SAP's code. Stop building custom ABAP logic that lives inside the digital core. If you need extensions, build them outside on the Business Technology Platform, where they can evolve independently of the underlying ERP. On the surface, this sounds like housekeeping. In reality, it's SAP quietly reasserting architectural control over an installed base that had spent forty years turning SAP into forty thousand slightly different SAPs. A clean core is standardized. A standardized core can be upgraded continuously. A continuously upgradeable core can absorb AI capabilities—Joule, Business AI, agentic workflows—the moment SAP ships them, without each customer having to re-test their mountain of custom code. Put differently, Clean Core is the prerequisite for SAP's entire AI strategy. Without it, Joule is a demo. With it, AI becomes something SAP can actually turn on across tens of thousands of enterprises simultaneously.

That's the part customers have only recently begun to fully appreciate, and it's why resistance has softened. The pitch has evolved from "migrate because we're turning off ECC" to "migrate because this is the only way you get the AI." For a boardroom watching competitors announce AI-driven productivity gains every quarter, that's a very different conversation.

And behind all of this, the consulting bonanza rolls on, bigger than ever. Accenture, Deloitte, and IBM—the holy trinity of SAP implementation partners—continue to reap billions in multi-year S/4HANA transformation fees, with the big four rounded out by Capgemini, PwC, EY, and KPMG. Accenture's SAP practice alone is rumored to employ more S/4HANA-certified consultants than SAP itself. Daily rates for senior migration architects have climbed 15–20% since 2024, and the talent market is so tight that the big firms are poaching from each other mid-engagement. Every transformation is a three-way deal: SAP sells the software, the hyperscaler provides the infrastructure, and the consultancy does the actual work of untangling twenty years of customization and stitching the new clean core into the customer's operations. For the consultancies, the 2027 cliff is a generational windfall. For SAP, it's the mechanism by which its customer base gets reset onto a standardized, upgradeable, AI-ready foundation—whether customers signed up for that reset or not.

The 2027 deadline, in other words, was never really about forcing an upgrade. It was about SAP reasserting control over its entire ecosystem—using a hard date to break four decades of accumulated customization, pull customers out of their on-premise bunkers, and land them on a unified cloud platform that SAP itself would operate. Which naturally raises the question of what, exactly, that platform looks like once they arrive.

VIII. RISE with SAP & Cloud Transformation (2021–Present)

This section was updated on 22-04-2026.

The answer, when it arrives, is called RISE with SAP. Launched in January 2021, RISE was pitched as "Business Transformation as a Service"—a single subscription bundle that rolled the software, the infrastructure, the migration tooling, and a layer of SAP-managed services into one contract. The premise was disarmingly simple: customers had been complaining that S/4HANA migrations were too complex, too risky, and too expensive to stomach on their own. Fine, SAP said. We'll do it for you. What looked on the surface like a packaging exercise was actually a structural bet—RISE was the vehicle through which SAP would drag four decades of on-premise customers onto a cloud platform that SAP itself would operate, meter, and upgrade.

For the first three years, the reception was tepid and the financial translation was painful. Software licenses used to be recognized upfront—a €10 million deal booked €10 million in revenue that quarter. RISE subscriptions spread that same revenue over years. The financial engineering required to show growth while cannibalizing your own license book is the kind of thing that makes CFOs weep, and SAP's CFO Dominik Asam spent much of 2022 and 2023 teaching the sell side how to read a deferred-revenue waterfall. Customers, for their part, viewed RISE with suspicion. Many saw it as the ultimate vendor lock-in play disguised as simplification—not just software anymore, but the infrastructure underneath, the services around it, and the roadmap above it, all owned by Walldorf.

Then the numbers broke. In late January 2026, SAP reported a record total cloud backlog of €77.3 billion—a figure that, five years earlier, would have seemed absurd for a company whose entire franchise rested on perpetual licenses. Cloud revenue now accounted for more than half of total revenue, and Cloud ERP Suite growth was still running north of 30%. On any honest scorecard, the transition that looked impossible in 2021 had been executed. And yet, on the day of the print, the stock sold off sharply. SAP's 2026 growth guidance had come in more conservative than the sell side expected, and a market that had bid the company up to the 32nd-most-valuable in the world—past $300 billion in market cap through most of 2025—decided, in a single session, that the easy phase of the cloud re-rating was over. What traders called a "reset," management internally called a return to gravity. Either way, it ended a six-year streak in which every quarter had been a victory lap.

Christian Klein's response arrived in March 2026, and it was not subtle. In the largest board reshuffle of his tenure, Klein announced that SAP was going "all-in on AI" and collapsed what had been a sprawling product and customer-facing organization into something called the Customer Value Group, placed under a newly elevated Chief Customer Officer: Thomas Saueressig, long the head of product engineering and one of Klein's closest allies. The logic was that the AI story could no longer live inside the product org alone—if Joule and the agentic workflows were going to drive the next leg of cloud growth, the customers actually deploying them needed to sit on the same side of the wall as the people building them. More prosaically, it was an admission that SAP's AI narrative had run ahead of its AI adoption, and that closing the gap required putting a single executive on the hook for both.

The adoption story, to be fair, had stopped being purely narrative. By the start of 2026, over two-thirds of SAP's cloud order entries included an AI component—up from half a year earlier—and the number of Joule users had grown ninefold across 2025. Joule itself had evolved from a chat-style copilot with a few hundred skills into something more ambitious: a routing layer for autonomous agents that could execute multi-step workflows across procurement, finance, and HR. SAP's pitch quietly shifted too. Business AI had been sold through 2024 as productivity—faster expense reports, smarter purchase requisitions, synthesized meeting notes. By 2026, the pitch was agents: software that didn't help a human do the job but did the job and reported back. It was the difference between giving a controller a better calculator and giving her a junior analyst who never slept, and for a CFO audience staring at flat headcount budgets, it was a far more interesting conversation.

The M&A strategy realigned around the same thesis. The SmartRecruiters acquisition, announced in August 2025 and finalized in early 2026, plugged an AI-native, high-volume recruiting platform directly into SuccessFactors—an acknowledgment that hiring was the first HR workflow where agentic AI would actually land. More revealing was the Reltio deal in March 2026. Reltio is a master data management company, about as glamorous as it sounds, and SAP's willingness to pay up for it spoke to a blunt technical reality: AI models are only as good as the data they sit on top of, and SAP's data, scattered across forty years of acquisitions and thousands of customer instances, was a mess. Reltio gave SAP a unified master data layer—customers, products, suppliers, employees reconciled across every SAP and non-SAP system—that could serve as the substrate for Joule and every agent that would follow. It was the least exciting acquisition SAP had made in years and, arguably, the most important.

Capital allocation moved in the same direction. Under pressure from a market that had punished the January print, SAP announced a €10 billion share repurchase program in early 2026—by some margin the largest buyback in the company's history, and a genuine departure from decades of preference for dividends over returns of capital. The buyback did two things at once: it put a floor under the stock during the AI investment cycle, and it signaled that management believed the cloud business was finally generating enough durable free cash flow to justify leaning into the balance sheet. For a company that had spent the last fifteen years acquiring its way into the cloud, it was an unfamiliar posture. SAP was, for the first time in a long time, choosing to buy itself.

The competitive map, meanwhile, has tilted in ways RISE's original designers didn't quite anticipate. The hyperscaler tension is still there—AWS, Azure, and Google Cloud all want SAP workloads on their infrastructure, and SAP still insists on sitting in the middle of the stack—but it is no longer the most interesting fight. The more consequential threat in 2026 comes from AI-native startups racing to build the "intelligence layer" of the enterprise: companies that don't want to replace SAP's system of record but to wrap it, draining value from the workflows on top while leaving the transactional core untouched. Palantir has been circling this territory from one direction, a crop of agentic-ops startups from the other, and Microsoft is quietly fusing Dynamics, Fabric, and Copilot into something that could plausibly function as an AI-first ERP for companies below the Fortune 500 line. SAP's counter is straightforward and, if executed, devastating: own the master data, own the transactional core, own the clean upgradeable platform, and make the AI a first-class native of all three. It is the "Clean Core" bet from the previous section, cashing its check.

Whether that bet pays off will define the next decade. But even at this halfway mark, something has already happened that would have been hard to imagine when RISE launched five years ago: SAP is no longer visibly playing defense. The license-to-subscription transition, the thing that was supposed to break the company, is largely behind it. The AI narrative, for now, is one SAP is leading rather than chasing. What remains is the harder work of making all of it actually function at scale across tens of thousands of customers—and that, as it turns out, is a story best told through the playbook SAP has spent half a century refining.

IX. Playbook: The Art of Enterprise Software Dominance

After five decades, SAP has perfected several plays that every enterprise software company dreams of executing. Let's break down their playbook:

Creating Switching Costs So High That Leaving Is Corporate Suicide

SAP doesn't just sell software—they sell organizational transformation. Once a company implements SAP, it reshapes its processes, retrains its workforce, and rewires its operations around SAP's logic. The average large enterprise has thousands of customizations, hundreds of integrations, and entire departments that exist solely to manage SAP. Leaving isn't just expensive; it's existentially threatening. Try explaining to your board why you want to spend $500 million and five years to move off a system that works, however imperfectly.

The "Clean Core" Philosophy vs. Customization Revenue

This is SAP's current contradiction. For decades, they made billions from customers customizing their software, with consultants billing millions to make SAP bend to unique business processes. Now they're preaching "clean core"—use standard SAP, don't customize, stay vanilla. Why? Because customizations make cloud migrations nightmarish and upgrades impossible. But telling customers to abandon their customizations is like telling them their last 20 years of investment was wrong.

Partner Ecosystem as Distribution and Implementation Engine

SAP's master stroke was realizing they couldn't scale services themselves. Instead, they created an ecosystem where partners do the dirty work of implementation while SAP collects clean software revenue. Accenture, Deloitte, IBM—they've built multi-billion dollar practices around SAP. These partners don't just implement; they sell SAP into accounts, creating a distributed sales force that SAP doesn't have to pay.

The German Engineering Approach: Comprehensive but Complex

SAP software is notorious for its complexity, but that's a feature, not a bug. German engineering philosophy says: build it right, build it complete, build it to last. SAP software can handle any business process you can imagine—and many you can't. This complexity creates a moat. Competitors might be simpler, but can they handle the intricate requirements of a global manufacturer with operations in 50 countries? Usually not.

Platform Economics in B2B: Winner-Take-Most Dynamics

Consumer platforms get all the attention, but B2B platforms like SAP are even stickier. Once an industry starts standardizing on SAP, network effects kick in. Suppliers need SAP to work with customers. New employees already know SAP from previous jobs. Industry-specific solutions get built on top of SAP. Eventually, not using SAP becomes a competitive disadvantage.

Using Maintenance Deadlines as Growth Levers

The 2027 deadline isn't just about forcing upgrades—it's about creating predictable revenue events. SAP knows exactly when thousands of customers will need to make decisions. They can forecast revenue, plan resources, and negotiate from a position of strength. It's like having a timer on your customer relationships that you control.

M&A Strategy: Buy the Cloud, Integrate Later (or Never)

SAP's acquisition strategy has been clear: buy cloud leaders in different categories, worry about integration later. SuccessFactors for HR, Ariba for procurement, Concur for expenses, Qualtrics for experience management. Integration has been messy, sometimes non-existent, but it gave SAP a cloud story to tell Wall Street while buying time to figure out the technology.

X. Bear vs. Bull Case & Competitive Analysis

This section was updated on 22-04-2026.

Which brings us to the question every investor in SAP has to answer heading into the back half of this decade: is this a company emerging as the dominant agentic-AI platform for the enterprise, or is it a late-cycle migration story whose best growth numbers are already in the rearview mirror? The honest answer in April 2026 is that both cases are unusually strong, and the gap between them has rarely been wider.

Bull Case:

Start with the single most staggering statistic in enterprise software: 77% of global transaction revenue touches an SAP system. That is not a market share statistic—that is an infrastructure statistic. Replacing SAP at a Fortune 500 company is not a procurement decision; it is a multi-year, multi-hundred-million-dollar act of organizational self-harm. Mission-critical stickiness is not a cliché here, it is the foundation of the thesis. Companies do not leave SAP. They complain about SAP, they budget around SAP, they occasionally threaten SAP, but they do not leave.

Second, the visibility in the model is now genuinely exceptional. The €77 billion total cloud backlog reported in January 2026 is more than two years of cloud revenue already under contract, signed in ink, and legally owed to SAP. When the stock sold off on softer 2026 guidance, that backlog did not move. It is the closest thing the software industry has to a utility's rate base—contracted, recurring, and largely immune to the quarter-to-quarter noise that drives the sell-side narrative. Bulls argue the market is valuing SAP like a growth-decelerating software company while ignoring that it is increasingly an annuity with an AI option attached.

That AI option is the third pillar, and it is arguably the most under-appreciated one. Every major AI lab can build better models than SAP. None of them can build a better substrate for agentic AI in the enterprise, because the substrate is forty years of normalized, reconciled, permissioned transactional data about how real companies actually operate. A procurement agent is only useful if it can touch the purchase order system; a finance agent is only useful if it can post to the general ledger; a supply chain agent is only useful if it can see real inventory. SAP sits on all three, plus the Reltio master data layer that stitches them together. Joule's ninefold user growth in 2025 and the fact that two-thirds of cloud order entries now include an AI component suggests customers are starting to connect these dots themselves. If agentic AI turns out to be the defining enterprise software primitive of the next decade, SAP is not a participant—it is the landlord.

Finally, and less discussed but genuinely important: the €10 billion buyback. For a company that spent fifteen years acquiring its way to the cloud and has historically preferred dividends, choosing to repurchase shares on this scale is both a valuation floor and a statement. Management is telling the market it believes the post-transition free cash flow profile is durable enough to lean into the balance sheet. In a drawdown, that bid is real.

Bear Case:

The bear case begins with the January 2026 print itself. The guidance reset was modest in absolute terms, but it cracked a narrative. For six years, SAP had trained investors to expect each quarter to beat and raise; 2026 will not follow that pattern. Current cloud backlog growth is decelerating off a larger base, and bears argue the quality of the backlog is also slipping—more RISE bundles padding the top line, fewer genuinely net-new cloud logos, and an increasing share of growth that is really the same ECC customer repackaged as a cloud customer on less favorable terms than headline numbers imply. If the deceleration continues into 2027, the multiple compression that started in January has much further to go.

The second bear argument is execution risk, and it is not theoretical. The March 2026 board reshuffle and the pivot to "all-in on AI" are generational bets being placed while the S/4HANA migration is still not finished. SAP is simultaneously asking its organization to land the largest migration in enterprise software history, absorb a master data platform acquisition, collapse its customer-facing organization into a new Customer Value Group under Saueressig, and ship agentic AI that actually works in production across tens of thousands of customer instances. Any one of these would be a full management agenda. Doing all four at once, with a market now watching more skeptically, invites the kind of mistake that can set a cloud transition back by years.

The third argument is the one that has haunted every SAP bear for two decades: the technical debt. Clean Core is a beautiful idea. In practice, the reason customers have not migrated to S/4HANA is that their custom ABAP is load-bearing. Stripping it out means re-architecting the business processes those customizations were built to support—processes that, in many cases, nobody at the customer fully understands anymore because the people who wrote them retired. Every hour a customer spends untangling custom code is an hour they are not adopting Joule. The AI payoff the bulls are underwriting is gated on a migration whose long tail may extend well beyond 2027.

The fourth worry is competitive compression at the intelligence layer. The transactional core is genuinely safe—nobody is going to rip out general ledger. But the high-margin analytics, planning, and workflow orchestration that SAP has traditionally sold on top of that core is exactly where Palantir, the crop of agentic-ops startups, and a more aggressive Microsoft are camping out. They do not need to replace SAP; they just need to wrap it, drain the margin-rich layers off the top, and leave SAP with the commoditized system of record. It is Oracle's database franchise problem from twenty years ago, repointed at SAP's application franchise.

Competitive Landscape:

Oracle remains the primary rival at the top of the house—still the only other vendor with a credible end-to-end story for the world's largest enterprises, still strongest in the database layer that underpins high-end transactional workloads, and still the one competitor who can price-match SAP in a marquee deal. The two have been fighting this war since the 1990s, and neither has ever landed a knockout blow. That pattern is unlikely to change.

Salesforce and Workday continue to own the territory they took a decade ago. Salesforce is the default front office for customer data; Workday is the default cloud HCM for modern enterprises that never had SuccessFactors in the first place. SAP has not taken meaningful share back from either and, realistically, is not going to. The question is whether the next generation of AI-native workflows favors the specialist or the integrated suite—a question that will not be answered by marketing, but by which vendor's agents actually work on the customer's data in production.

Microsoft is the most complicated relationship in the industry, and the one that matters most for SAP's next five years. It is a hyperscaler hosting partner for most of SAP's RISE deployments, a distribution ally through Azure marketplaces, a co-selling partner on large accounts—and, simultaneously, the owner of Dynamics, Fabric, and Copilot, which together increasingly resemble an AI-first ERP stack aimed squarely at the mid-market and the upper mid-market where SAP has traditionally been underpenetrated. Satya Nadella has been disciplined about not declaring open war, but every Copilot demo that ends with an action written back to a business system is a shot across SAP's bow. Frenemy does not quite capture it. Co-dependent rival is closer.

ServiceNow is the competitor moving fastest into SAP's adjacent territory. What started as an IT service management vendor has become, over the last three years, a credible workflow platform for finance, HR operations, and procurement orchestration—exactly the process layer where SAP is trying to land Joule. ServiceNow's advantage is that it was cloud-native from day one and its customers have no ECC to migrate off of. Its disadvantage is that it does not own the transactional core. How that standoff resolves—whether the workflow layer or the system of record layer captures the agentic AI economics—will go a long way toward deciding which of the bull and bear cases plays out.

XI. Power Analysis & Future Scenarios

This section was updated on 22-04-2026.

That standoff is really a proxy for a deeper question: where does power actually live in the SAP ecosystem now, and where is it moving? For most of SAP's history, the answer was almost boringly simple. SAP held the architectural high ground, the consultants held implementation, and customers held inertia—the three-way détente that kept ECC running in the basement of every Fortune 500 for twenty years. In 2026, that equilibrium is breaking in ways that will define the company's next decade.

The most consequential shift is the one happening quietly inside every renewal meeting. For four decades, the SAP relationship was anchored by a maintenance contract: 17–22% of license value a year, paid in perpetuity, regardless of whether the customer actually got new value in return. It was a wonderful business—the annuity of annuities, effectively a tax on having once chosen SAP. RISE has dismantled it. Subscription revenue is not maintenance revenue. A customer writing an eight-figure check each year for S/4HANA Cloud is writing a renewable check, and the renewal conversation has teeth. If Joule isn't landing, if the agents aren't working, if the CFO can't point to measurable productivity against the line item, the next renewal will be smaller or later or both. Internally, SAP has started calling this the move to "value-based" relationships, which is vendor-speak for the uncomfortable truth: the company now has to prove ROI annually to a customer base that has spent a generation paying regardless. Churn, historically a word you never heard inside Walldorf, is now tracked as a leading indicator on executive dashboards. The power, in small but real increments, is moving from SAP to the customer—at least for the minority of customers willing to exercise it.

The second shift is more speculative but potentially more transformative: the move from systems of record to systems of action. For fifty years, ERP has been a passive ledger. You entered data, the system recorded it, managers read reports, humans made decisions, and then more data got entered to reflect those decisions. The entire user experience of SAP—the endless transaction codes, the screens upon screens of fields, the training manuals thicker than phone books—is the overhead of humans hand-feeding a system of record. Agentic ERP inverts that. In the pitch SAP is now making to CFOs and COOs, Joule doesn't help a procurement clerk fill out a purchase order; it evaluates the request against the contract, checks supplier performance, routes approvals, places the order, and closes the loop—with the human moving from data-entry operator to exception handler. If that vision holds, the UI itself starts to recede. You don't log into SAP anymore; you tell SAP what you need, and it transacts on your behalf. The implications for headcount inside finance, procurement, HR operations, and supply chain are enormous, and they are exactly why CFOs are listening. They are also why SAP is spending so much to win this narrative before ServiceNow, Microsoft, or the agentic-ops startups define it without them.

Behind that shift looms a fight that almost no one outside the industry is talking about yet, but which will be litigated in boardrooms and regulatory filings over the next three years: who actually owns the data that 269 million cloud users generate, and who gets to benefit from using it to train AI. SAP's position is, unsurprisingly, that customer transactional data belongs to the customer, and that aggregated, anonymized patterns—how companies actually run procurement, how working capital flows, which process variants correlate with which outcomes—are the fuel for the models that make Joule useful. Customers, for their part, are starting to ask harder questions. Is my data training the model my competitor uses? If SAP's agents get smarter because of what my treasury team does, do I get a discount, or does SAP get a better product to sell back to me? European data protection authorities are circling the same question from a regulatory angle, and DSAG has begun formally asking it in writing. The precedent-setting negotiation is already underway: the marquee accounts are carving data-use clauses into their renewals in a way that would have been unthinkable five years ago. How this is resolved—whether SAP retains broad rights to learn across the installed base, or whether AI training becomes a contractual line-item that customers price and meter—will determine whether the agentic platform compounds into a winner-take-most franchise or a federated utility where each customer keeps their own moat.

On top of that substrate, the next frontier of platform dominance is looking increasingly vertical. Generic horizontal AI is a race SAP cannot win against OpenAI, Anthropic, or Google. A retail-specific agent that understands planograms, shrinkage, and season curves; a pharma-specific agent that understands validated systems, GxP documentation, and cold-chain constraints; a discrete-manufacturing agent that understands bill-of-materials explosions and constraint-based scheduling—those are races where forty years of industry-specific configurations actually matter, and where the data exhaust from thousands of similar customers becomes a genuine moat. SAP's industry cloud strategy, which for years felt like a marketing overlay on top of the same core ERP, is quietly becoming the actual product roadmap. The bet is that once the verticals are deep enough, a retailer switching off SAP isn't just leaving an ERP—they're leaving a library of merchandising logic that competitors have spent a decade teaching the same system.

Which leads to the most philosophically interesting question facing Walldorf, and the one that casts the longest shadow over the next decade: can SAP preserve its founding religion of "Standard Software" in a world where AI makes every business process infinitely customizable? The 1972 insight—that companies didn't need bespoke code, they needed standardized software with configurable parameters—was the intellectual foundation of the entire franchise. Clean Core is its modern expression. But agentic AI cuts the other way. If an agent can generate a workflow in natural language, tuned to your exact business, in seconds, why should you accept SAP's standard? Why shouldn't every customer have their own slightly bespoke version of every process, continuously evolved by their own agents against their own data? This is the same pressure that turned off-the-shelf enterprise software into custom ABAP nightmares the last time around, and it is returning in a new form. SAP's answer, still being worked out, is that the standard has to live at a higher level of abstraction: not "here is the purchase-order screen everyone uses," but "here is the purchase-order primitive, and your agents compose on top of it." Whether that distinction holds in practice, or whether hyper-customizable AI business logic quietly dissolves the very thing that made SAP SAP, is the existential question the company will be answering for the rest of this decade—and the one whose resolution will determine whether the empire endures, or whether it eventually becomes something we describe in the past tense.

XII. Epilogue: Lessons for Builders

After 52 years, SAP's journey offers profound lessons for anyone building enterprise software. First, the power of boring, mission-critical software cannot be overstated. While Silicon Valley chases the latest consumer app, SAP quietly runs the world's economy. There's enormous value in building software so essential that removing it would be catastrophic.

Building products so embedded they become infrastructure is the ultimate moat. SAP isn't just software—it's organizational scar tissue, built up over decades of customization and integration. New competitors might have better technology, but they can't replicate twenty years of organizational embedding.

Managing technology transitions while maintaining cash flows is perhaps the hardest challenge in enterprise software. SAP has been running two businesses simultaneously for over a decade—supporting legacy customers while building for the cloud. It's like rebuilding a plane while flying it, with paying passengers aboard.

The German model versus the Silicon Valley model presents an interesting contrast. SAP represents engineering thoroughness, long-term thinking, and patient capital. They don't pivot; they persist. While Silicon Valley startups fail fast, SAP fails slowly, giving them time to correct course. Sometimes, in enterprise software, slow and steady does win the race.

Why do enterprise software companies trade at premium multiples? Because investors understand what SAP proves: once you're embedded in enterprise infrastructure, you're nearly impossible to dislodge. The recurring revenue is predictable, the switching costs are prohibitive, and the growth, while slow, is steady.

SAP's story isn't sexy. It's not the kind of company that gets featured in tech blogs or discussed at cocktail parties. But for five decades, they've quietly built one of the most powerful software franchises in history. They've survived multiple technology transitions, fought off countless competitors, and maintained their grip on the world's largest companies.

The empire of enterprise software that five IBM engineers started in 1972 has become something they probably never imagined: infrastructure so fundamental to global commerce that its absence would be catastrophic. It's boring, it's complex, it's expensive—and it's absolutely essential. That's the genius of SAP.

XIII. Recent News

SAP's financial results for 2024 exceeded all outlook parameters, with current cloud backlog reaching €18.1 billion (up 29% at constant currencies), total cloud backlog hitting €63.3 billion (up 40% at constant currencies), and cloud revenue growing 26% at constant currencies. The momentum carried through the entire year, with cloud revenue reaching half of SAP's total revenue in 2024, while total revenue growth returned to double digits for the first time since 2018.

The AI transformation has become central to SAP's strategy. Half of SAP's cloud order entries in Q4 2024 included AI capabilities, with more than 30,000 customers now using SAP Business AI. By the end of 2024, SAP had released more than 130 AI use cases, overdelivering on plans, and equipped its generative AI copilot Joule with 1,300 skills covering 80% of the most-used tasks of SAP end users, cementing SAP's reputation among C-suite executives as the leading AI company in Europe and among the top 5 globally.

Leadership stability remains strong. The Supervisory Board extended CEO Christian Klein's contract to five years until April 2030, and CFO Dominik Asam's contract for two years to March 2028. Klein's tenure has been marked by significant success, with SAP's share price almost doubling since he became CEO five years ago.

The S/4HANA migration continues to gather pace, though challenges remain. Only 40% of customers are currently on the move to S/4HANA, raising questions about whether the 2027 deadline will force a last-minute rush. Despite this, the current cloud backlog surged 29% at constant currency to €18.08 billion, with the total cloud backlog reaching €63.29 billion.

Major customer wins across technology, energy, retail, automotive, and manufacturing sectors have validated SAP's strategy. The company completed the acquisition of WalkMe in 2024, enhancing its Business Transformation Management portfolio, though the integration is expected to be dilutive in the short term, with €14 million in losses reported.

Looking ahead to 2025, SAP expects a slight deceleration in current cloud backlog growth, though this is factored into revenue projections. The company raised its operating profit outlook and maintains confidence in its Ambition 2025 targets. Through to 2027, SAP expects accelerated, double-digit total revenue growth and an expansion of operating profit as well as profit margin.

On the market performance front, as of September 2025, SAP's market capitalization reached $314.64 billion, ranking as the 33rd most valuable company globally. The all-time high SAP stock closing price was $311.93 on July 9, 2025, reflecting strong investor confidence in the cloud transformation and AI strategy.

XIV. Links & References

Key Resources:

- SAP Investor Relations: sap.com/investors

- SAP Integrated Report 2024: sap.com/integrated-reports/2024

- SAP News Center: news.sap.com

- ASUG (Americas' SAP Users' Group): asug.com

Historical Analysis:

- "The Innovator's Dilemma" by Clayton Christensen - cited by CEO Christian Klein as key inspiration

- Gartner Reports on S/4HANA Migration Trends

- IDC Enterprise Applications Market Analysis

Industry Resources:

- IgniteSAP Industry Analysis: ignitesap.com

- Cloud Wars Top 10 Rankings and Analysis

- Fortune 500 Technology Leadership Coverage

Technical Documentation:

- SAP S/4HANA Migration Guide

- SAP Business Technology Platform Documentation

- RISE with SAP Implementation Resources

Competitive Intelligence:

- Oracle Financial Reports and Investor Materials

- Salesforce Investor Relations

- Microsoft Dynamics Product Documentation

- Workday Financial Statements

- ServiceNow Growth Strategy Reports

Academic and Business School Resources:

- Harvard Business School SAP Case Studies

- INSEAD Technology Strategy Research

- Stanford Graduate School of Business Enterprise Software Analysis

Conclusion: The Perpetual Transformation Machine

SAP's story is ultimately about the paradox of permanence through constant change. For over five decades, this German software giant has maintained its grip on enterprise computing by repeatedly cannibalizing itself before competitors could do it for them. From mainframe to client-server, from on-premise to cloud, from transactional to intelligent systems—each transformation has been painful, expensive, and existentially risky. Yet SAP endures.

The current transformation to cloud and AI may be SAP's most challenging yet. Unlike previous transitions that were primarily technical, this one requires fundamental changes to the business model, customer relationships, and corporate culture. The shift from upfront license revenue to subscription models has compressed margins and complicated financial engineering. The push toward standardization through "clean core" contradicts decades of customization that created switching costs. The integration of dozens of acquisitions has created a portfolio that sometimes feels more like a confederation than a unified platform.

Yet the numbers suggest SAP is succeeding where many legacy enterprise software companies have failed. Cloud revenue reached €17.14 billion in 2024, growing 26% at constant currencies, while maintaining the loyalty of the world's largest enterprises. The 2027 S/4HANA deadline, though controversial, has created a forcing function that will drive billions in revenue over the next three years. The AI integration, still early, positions SAP to monetize the vast troves of business data flowing through its systems.

What makes SAP truly remarkable isn't its technology—competitors often have better user interfaces, more modern architectures, or more innovative features. SAP's moat lies in its entrenchment within the operational fabric of global commerce. It's the embodiment of enterprise infrastructure, as essential and invisible as plumbing or electricity. Companies don't love SAP; they depend on it.

The lessons for builders are profound. First, boring beats sexy when it comes to building lasting enterprise value. While Silicon Valley chases the next consumer app or crypto protocol, SAP quietly processes trillions in global transactions. Second, switching costs are the ultimate competitive advantage in B2B software. Once you're woven into a company's operations, extraction becomes nearly impossible. Third, managing technology transitions while maintaining cash flows requires a delicate balance of forcing functions and customer accommodation.

Looking forward, SAP faces genuine threats. Cloud-native competitors continue to chip away at the edges. The technical debt accumulated over five decades grows heavier each year. Customer frustration with complexity and cost remains high. The 2027 deadline may force migrations, but it also creates an opportunity for competitors to pitch alternatives. And the next platform shift—whether it's edge computing, quantum, or something not yet imagined—looms on the horizon.

But betting against SAP has been a losing proposition for half a century. They've survived every technology transition, outlasted every would-be disruptor, and emerged from every crisis stronger than before. The empire of enterprise software that five IBM engineers started in a Mannheim office park has become something approaching a natural monopoly—not through regulatory capture or network effects, but through sheer operational entrenchment.

SAP's future will likely look much like its past: messy transformations, angry customers, massive consulting fees, and somehow, inexorably, continued dominance. Because in enterprise software, revolution is expensive, evolution is profitable, and inertia is king. SAP has mastered the art of being just good enough to keep, too expensive to replace, and too critical to abandon.

The machine keeps running, the transactions keep processing, and SAP keeps collecting its toll on global commerce. It's not inspiring, it's not innovative by Silicon Valley standards, and it's certainly not simple. But it is essential. And in enterprise software, essential is everything.

As we enter the age of AI and face new technological paradigms, SAP's greatest challenge may be maintaining relevance while preserving stability. The company that once revolutionized business computing by offering real-time processing must now navigate a world where real-time isn't fast enough, where intelligence must be embedded rather than reported, and where cloud-native competitors can iterate faster than SAP can transform.

Yet if history is any guide, SAP will find a way. Not elegantly, not quickly, and certainly not cheaply. But persistently, methodically, and profitably. Because that's what infrastructure does—it adapts just enough to survive, changes just enough to remain relevant, and endures long enough to become irreplaceable.

The empire of enterprise software endures. Long may it process.

The completed article maintains the same in-depth analysis style throughout, with natural continuity from where it left off. The recent news and references sections have been populated with the most current information available, including SAP's August 2025 acquisition of SmartRecruiters, a leading talent acquisition software provider, demonstrating the company's continued push to strengthen its cloud portfolio through strategic acquisitions.

The SmartRecruiters deal particularly highlights SAP's evolving M&A strategy. SmartRecruiters' deep expertise in high-volume recruiting, recruitment automation, and AI-enabled candidate experience are considered an ideal addition to the SAP SuccessFactors HCM suite, with the acquisition strengthening SAP's all-in-one HCM suite so customers have the tools they need to attract and retain top talent. The transaction is expected to close in the fourth quarter of 2025, subject to customary closing conditions, including regulatory approvals, though financial terms were not disclosed.

The partnership dynamics also continue to evolve. In May 2025, Accenture and SAP launched ADVANCE, creating a pathway to the cloud for organizations pursuing high growth with annual revenue of up to US$5 billion to help create more connected, intelligent and responsive enterprises. This represents a shift in focus toward the mid-market segment, acknowledging that SAP's traditional enterprise focus may have left opportunities on the table.

As of September 2025, SAP's financial position reflects the success of its transformation efforts. SAP's market cap was $318.43B as of September 3, 2025, with the all-time high SAP stock closing price reaching $311.93 on July 9, 2025. These valuations demonstrate investor confidence in SAP's cloud transition and AI strategy, despite the challenges of managing such a massive technological and business model transformation.

The acquisition momentum shows no signs of slowing. SAP acquired WalkMe in June 2024 for a price of $1.5B, adding digital adoption platform capabilities that will help customers maximize the value of their SAP investments. WalkMe is scheduled to join the SAP solutions catalog in the first half of 2025, with the merger of the two solutions and ensuing migration scheduled for 2026/2027.

The story of SAP is ultimately one of perpetual reinvention within constraints. Unlike Silicon Valley companies that can pivot dramatically or fail fast, SAP must transform while maintaining the critical infrastructure that powers the global economy. Every change must be backward compatible, every innovation must coexist with legacy systems, and every strategic shift must consider the thousands of companies whose operations depend on SAP's stability.

As we look toward the remainder of the decade, SAP faces its most complex challenge yet: maintaining relevance in an AI-driven world while supporting customers still running decades-old systems. The company that once revolutionized business computing with real-time processing must now navigate a world where intelligence must be embedded, not just reported; where cloud-native competitors can innovate faster than SAP can migrate; and where the very concept of enterprise software is being redefined by artificial intelligence and automation.

Yet history suggests SAP will endure, not through elegant transformation but through methodical evolution. The empire of enterprise software that began with five engineers in Mannheim has become too essential to fail, too embedded to replace, and too valuable to abandon. It may not be the most innovative company, the most beloved by customers, or the most agile in adapting to change. But it remains what it has always been: the indispensable, invisible infrastructure that keeps the global economy running.

The machine continues. The transactions process. The enterprises operate. And SAP, for all its challenges and contradictions, remains at the center of it all—boring, complex, expensive, and absolutely essential.

The acquisition momentum continued with the August 2025 announcement that SAP has entered into an agreement to acquire SmartRecruiters, a leading talent acquisition (TA) software provider. Founded in 2010 by Jerome Ternynck, SmartRecruiters Software-as-a-Service solutions and platform enable more than 4,000 organizations globally to efficiently manage their hiring workflows end-to-end. SmartRecruiters' deep expertise in high-volume recruiting, recruitment automation and AI-enabled candidate experience and engagement are considered an ideal addition to the SAP SuccessFactors human capital management (HCM) suite.

The strategic logic of the SmartRecruiters acquisition reflects SAP's evolving approach to M&A. Rather than simply buying cloud capabilities, they're now acquiring AI-native platforms that can immediately enhance their existing portfolio. SmartRecruiters, a talent acquisition software provider known for high-volume recruiting and AI-driven tools, represents exactly the kind of modern, agile technology that SAP needs to compete with cloud-native HR platforms.

Rebecca Carr, SmartRecruiters CEO, said, "SmartRecruiters' mission has always been to make hiring easy. Joining forces with SAP presents a tremendous opportunity for enterprises worldwide to benefit from our industry leading approach to talent acquisition". The integration approach shows SAP learning from past acquisition challenges—Terms of the transaction were not disclosed, but importantly, SmartRecruiters will remain an "agnostic vendor" for the "foreseeable future," according to Carr.

The partnership ecosystem continues to evolve in sophisticated ways. In May 2025, Accenture (NYSE: ACN) and SAP SE (NYSE: SAP) have launched ADVANCE. For the first time, the two companies have worked together to create a pathway to the cloud for organizations pursuing high growth with annual revenue of up to US$5 billion to help create more connected, intelligent and responsive enterprises. This represents a significant strategic shift—rather than focusing exclusively on Fortune 500 enterprises, SAP is acknowledging the massive mid-market opportunity.

The ADVANCE initiative demonstrates how SAP is leveraging its partner ecosystem not just for implementation but for market expansion. These solutions are tailored by industry and function, allowing businesses to move at speed, implementing cloud transformations in as little as six to 12 months. The speed promise is crucial—traditional SAP implementations measured in years, not months.

Financial performance reflects the success of these strategic moves. As of September 2025 SAP has a market cap of $316.13 Billion USD. This makes SAP the world's 32th most valuable company according to our data. The market valuation demonstrates investor confidence in SAP's cloud transition, despite the complexity and risk involved.

The AI integration story has become central to SAP's narrative. The company isn't just adding AI features—it's reimagining how enterprise software works in an AI-first world. Business AI isn't about flashy consumer applications; it's about embedding intelligence into every business process, from procurement decisions to workforce planning. SAP's vast data advantage—decades of transactional information from the world's largest companies—provides training data that cloud-native competitors can't match.

Looking at the competitive dynamics, the enterprise software landscape has become increasingly complex. Microsoft's aggressive push with Dynamics, backed by Azure infrastructure and Office 365 integration, represents perhaps the most serious long-term threat. They can bundle in ways SAP cannot, offer integrated experiences SAP struggles to match, and leverage their cloud infrastructure dominance to undercut SAP on total cost of ownership.

Yet SAP's moat remains formidable. The switching costs aren't just financial—they're organizational, operational, and psychological. Changing ERP systems is like performing a heart transplant while the patient is running a marathon. It's theoretically possible, but the risk is enormous, the pain is guaranteed, and the benefits are uncertain.

The 2027 S/4HANA deadline looms as both opportunity and threat. If SAP executes well, it drives a massive wave of modernization that locks customers in for another generation. If they stumble—if migrations fail, if costs spiral, if the promised benefits don't materialize—it opens the door for competitors to poach frustrated customers at their most vulnerable moment.

The cultural transformation at SAP deserves attention. This German engineering company, built on thoroughness and precision, is trying to become agile and cloud-native while maintaining the stability that enterprise customers demand. It's like asking a Swiss watchmaker to build smartphones while still servicing mechanical watches. The technical challenge is manageable; the cultural challenge is profound.

RISE with SAP represents more than a product offering—it's a philosophical shift. Instead of selling software and letting partners handle the mess, SAP is taking ownership of the entire transformation journey. It's risky, complex, and potentially transformative. If successful, it dramatically simplifies the customer experience and captures more value. If it fails, SAP owns the failure directly rather than pointing fingers at implementation partners.