SharkNinja: From Infomercial Pioneer to NYSE Powerhouse

I. Introduction & Episode Roadmap

Picture this: It's 2:00 AM, and you're channel surfing through late-night television. Suddenly, an energetic host appears on screen, demonstrating a vacuum cleaner that promises to revolutionize your cleaning routine. This wasn't just another infomercial—it was the beginning of a business empire that would grow from less than $250 million in net sales to over $4.3 billion in just 15 years.

The company behind that vacuum? SharkNinja, now trading on the NYSE under the ticker SN, a household name that has fundamentally disrupted not one, but two major appliance categories. How did a century-old sewing machine company transform into a household appliance giant that dethroned Dyson in the U.S. vacuum market and created a billion-dollar blender empire seemingly out of nowhere? On Monday, July 31, 2023, SharkNinja executives rang the opening bell at the New York Stock Exchange to mark the milestone of becoming an independent public company. The stock, trading under ticker symbol SN, rocketed 40% in its first day, closing at $42.31—a triumphant debut that seemed to validate years of careful planning for this moment.

But here's what makes SharkNinja's story truly remarkable: This wasn't your typical Silicon Valley unicorn or a venture-backed startup going public. This was a century-old family business that had quietly built two billion-dollar brands while most investors weren't even paying attention. The company that started selling sewing machines door-to-door had somehow become the number one vacuum brand in America, dethroning the mighty Dyson, and simultaneously created the top-selling blender brand in the United States.

The numbers tell a story of extraordinary growth that few consumer companies have matched. From generating less than $250 million in net sales in 2008, SharkNinja exploded to $3.7 billion in net sales with a CAGR of 20% between 2008 and 2022. By fiscal year 2023, that figure had grown to over $4.3 billion. This wasn't just growth—it was a complete transformation of multiple industries.

What we're about to explore is how a family-run business mastered the art of direct-response television marketing, identified pricing "wastelands" that established players ignored, and built a product development engine that could consistently deliver five-star rated products across 35 different household categories. It's a playbook that combines old-school selling techniques with cutting-edge consumer insights, family business values with private equity sophistication, and American marketing genius with global supply chain expertise.

The journey takes us from Montreal to Boston, from late-night infomercials to the New York Stock Exchange, from CDH Private Equity's boardrooms in Hong Kong to the shelves of every major retailer in America. Along the way, we'll discover how SharkNinja didn't just compete with industry giants—they fundamentally changed the rules of the game.

II. Founding Story & Early Years (1994-2007)

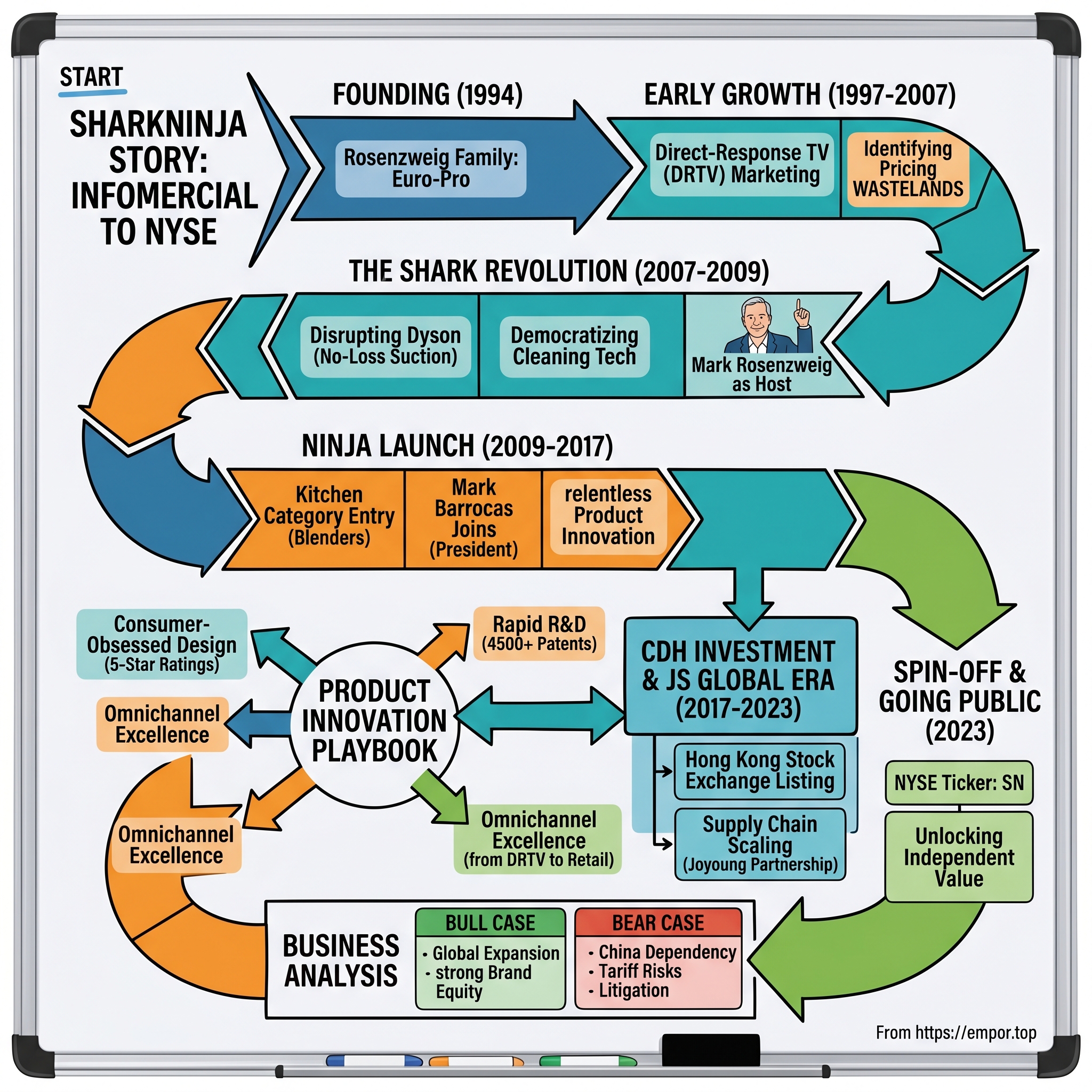

The SharkNinja origin story begins not in Silicon Valley or Wall Street, but in the living rooms and kitchens of North American households where door-to-door salesmen once demonstrated the latest home innovations. The company's DNA traces back to Euro-Pro Operating LLC, a prestigious centennial family enterprise that had been selling household products for generations.

In 1994, Mark Rosenzweig took the reins of what was then primarily a sewing machine company operating out of Montreal, Canada. The Rosenzweig family had built their business the old-fashioned way—through direct sales, personal demonstrations, and an intimate understanding of what homemakers actually needed. This wasn't glamorous work, but it taught them something invaluable: how to read consumer frustration and translate it into product opportunities.

By 1997, Rosenzweig formally founded what would become SharkNinja, still operating from Montreal but with ambitions that stretched far beyond Canada's borders. The following year, 1998, marked a pivotal moment as the company entered the United States market—a move that would ultimately define its destiny.

The late 1990s vacuum cleaner market was a study in contrasts. At the high end, established brands like Hoover and Eureka dominated department stores with $300-500 machines. At the low end, discount retailers sold basic models for under $100 that barely lasted a year. And then there was Dyson, the British newcomer that had begun its American invasion with $500+ vacuums that promised revolutionary "cyclonic" technology.

But Rosenzweig saw something others missed: a massive pricing gap between $150 and $250 where virtually no quality products existed. Industry veterans called this range a "wasteland"—too expensive for bargain hunters, too cheap for premium buyers. It was precisely the kind of market inefficiency that a nimble, family-run business could exploit. In 2003, a critical shift occurred that would define the company's future trajectory. Mark innovated a powerful media and infomercial strategy. High-quality products were sold to retail partners at the same time they appeared on national television infomercials and shopping networks. Mark was the host telling the brand and product stories. This direct-response television (DRTV) approach wasn't just about selling products—it was about building a direct relationship with consumers, understanding their pain points, and iterating rapidly based on feedback.

The numbers validated the strategy: By fiscal 2000, sales reached $100 million dollars and then $250 million by fiscal 2003. But what made this growth remarkable wasn't just the velocity—it was the foundation being laid. With help from his parents, Max and Aviva, he founded Euro-Pro, a company whose goal was to create innovative and exciting products consumers would love and talk about. The first products sold were under the Euro-Pro brand and included domestic ironing systems made in Italy and then quickly followed by steam presses, domestic sewing machines, and food processors.

Between 2003 and 2006, Mark's brother, Stanley Rosenzweig, Harvard MBA, 1991, who had significant experience with larger multinational companies that marketed and manufactured small appliances under proprietary brand names, joined him at Euro-Pro with the goal of helping Mark move the business from Montreal to Boston and to assist restructuring and bringing it to the next level of success. The move to Boston wasn't just geographic—it represented a shift from family business to professional enterprise, from Canadian roots to American ambitions.

By 2007, the stage was set for disruption. The vacuum cleaner market had grown complacent, with established players content to defend their territory rather than innovate. Dyson had proven that consumers would pay premium prices for better technology, but no one had asked whether those same consumers might prefer great technology at half the price. Mark Rosenzweig was about to provide the answer.

III. The Shark Revolution: Disrupting Dyson (2007-2009)

Rosenzweig founded the Shark brand in 2007 with the launch of the No-Loss-of-Suction vacuum technology. The timing couldn't have been more perfect—or more audacious. Dyson had spent years educating American consumers about cyclonic technology and the importance of maintaining suction power. James Dyson's British accent and engineering credentials had become synonymous with vacuum innovation. But there was a problem: Dyson vacuums cost $400-$600, putting them out of reach for most American households. SharkNinja CEO Mark Rosenzweig and President Mark Barrocas awoke to this opportunity and made up their minds to launch vacuums priced at USD 150 or so, a price range then termed as "wasteland." But this wasn't just about undercutting on price—it was about delivering comparable or better performance at a fraction of the cost.

Shark took the United States market by storm in 2007 with its No-Loss-of-Suction vacuum technology. Over the course of the last 17 years, Shark vacuums have become a household staple for good reason. The genius was in the execution: Instead of trying to out-engineer Dyson with new technology, Shark focused on solving the actual problems consumers faced—vacuums that were too heavy, too expensive, and too complicated.

The direct-response television strategy that Mark had pioneered since 2003 became the perfect vehicle for this disruption. While Dyson relied on premium retail placement and word-of-mouth among affluent consumers, Shark went directly to Middle America through infomercials. Mark Rosenzweig himself became the face of the brand, demonstrating products with an enthusiasm that was part QVC, part Steve Jobs keynote.

The contrast was striking: Dyson's James Dyson presented himself as the British inventor-engineer, discussing cyclonic technology and engineering principles. Mark Rosenzweig, on the other hand, was the relatable American entrepreneur showing housewives how the Shark could pick up a bowling ball (demonstrating suction power) or how it could swivel into tight spaces (demonstrating maneuverability). One approach sold engineering; the other sold solutions.

By 2009, the results were undeniable. In 2007, with his father Max's help, the very successful line of Shark steam mops was developed as well as a "no loss of suction" vacuum technology, propelling Euro-Pro gross sales to reach over $400 million US dollars by the end of fiscal 2009. In just two years, Shark had gone from zero to nearly half a billion dollars in sales, capturing significant market share from established players.

But the real disruption wasn't just in market share—it was in consumer perception. Shark had proven that you didn't need to spend $500 for a great vacuum. They had democratized quality cleaning technology, making it accessible to the average American household. This wasn't just a business victory; it was a fundamental shift in how Americans thought about home appliances.

The success caught the attention of another key player who would help take the company to the next level. Mark's good friend, and new partner, Mark Barrocas, a very successful veteran executive at private equity-backed companies, joined Euro-Pro in fiscal 2009 as President. Together, "Mark and Mark" successfully focused on innovative product development and high-quality manufacturing, adding Ninja kitchen appliances and a full line of vacuum cleaners, eventually reaching gross sales of over half a billion US dollars in the fiscal year 2010 and $1 billion in the fiscal year 2013.

IV. The Ninja Launch & Kitchen Domination (2009-2017)

If the Shark revolution was about disrupting an established category, the Ninja launch was about creating an entirely new one. Shortly thereafter, the executive bench was expanded to include Mark Barrocas as SharkNinja's president, driving the launch of the Ninja brand in 2009. This wasn't just adding another product line—it was a calculated bet that the same playbook that worked in vacuums could work in kitchen appliances.

The kitchen appliance market in 2009 was dominated by legacy brands with decades of heritage. KitchenAid stood for professional-grade mixers, Vitamix owned the high-performance blender category at $400+, and Cuisinart controlled the food processor market. Meanwhile, a new entrant called NutriBullet was creating buzz with personal-sized blenders marketed through infomercials. The market was ripe for disruption.

Mark Barrocas brought a different energy to the company. Where Rosenzweig was the inventor-demonstrator, Barrocas was the operator-strategist. His background at private equity-backed companies meant he understood how to scale operations, optimize supply chains, and build organizational capabilities. The two Marks formed a powerful partnership: one focused on product and marketing, the other on operations and growth.

The first Ninja products weren't trying to compete directly with Vitamix's $500 blenders. Instead, they identified another "price wasteland"—the $100-200 range where consumers wanted more than a basic blender but couldn't afford professional-grade equipment. The Ninja Master Prep, launched in 2009, was a revelation: it could chop, blend, and puree with a unique blade design that moved up and down the pitcher rather than just spinning at the bottom.

By 2013, SharkNinja had expanded into the kitchen appliance market with the Ninja Blender, which was pivotal in solidifying its presence in consumers' kitchens. But what made this expansion remarkable wasn't just the products—it was the speed of innovation. While established brands might release one new model every few years, SharkNinja was launching multiple products annually, each addressing specific consumer pain points identified through their direct-response feedback loops.

The multi-category expansion strategy was audacious in its scope. SharkNinja's product portfolio spans 35 household sub-categories, across cleaning, cooking, food preparation, home environment and beauty. This wasn't diversification for its own sake—it was a systematic approach to owning the modern household.

Consider the competitive dynamics: In blenders, they weren't just competing with one player. They were simultaneously taking share from Vitamix at the high end (with products at half the price), NutriBullet in the personal blender space, and traditional players like Oster and Hamilton Beach at the low end. The Ninja brand became synonymous with versatility—one base that could blend, food process, and make dough.

The innovation cycle was relentless. The Ninja Foodi, launched later in this period, combined pressure cooking with air frying—two of the hottest kitchen trends—in one device. This wasn't just product development; it was trend arbitrage. SharkNinja had built an engine that could identify emerging consumer behaviors, rapidly develop products to address them, and get to market faster than anyone else. The company's growth metrics during this period were staggering. Together, "Mark and Mark" successfully focused on innovative product development and high-quality manufacturing, adding Ninja kitchen appliances and a full line of vacuum cleaners, eventually reaching gross sales of over half a billion US dollars in the fiscal year 2010 and $1 billion in the fiscal year 2013. By the end of 2017, SharkNinja employed over 1,000 associates, added robotic vacuums and heated ninja appliances, and reached sales of almost $2 billion.

The financial performance wasn't just about top-line growth—it was about market dominance. Shark became the leading brand in the vacuum market, holding a significant market share of 25%, while Ninja established a strong presence in the blender market with an estimated market share of 18%. These weren't niche products for enthusiasts; they had become mainstream consumer choices.

What made this dual-brand strategy so effective was the synergy between them. Both brands shared SharkNinja's core competencies: rapid product development, direct-to-consumer marketing, and value engineering. But they attacked different parts of the household, allowing the company to cross-sell and build deeper relationships with consumers. A satisfied Shark vacuum customer was more likely to try a Ninja blender, and vice versa.

The company also changed its name in 2015 to capitalize on the prominence and popularity of the brand names. This wasn't just a rebrand—it was a declaration that the company had transcended its Euro-Pro origins to become something entirely new.

By 2017, SharkNinja had built two billion-dollar brands from scratch in less than a decade. They had disrupted multiple categories, taken share from established players, and created a product development engine that could enter new categories at will. But they had also reached a crossroads. To continue growing at this pace, they would need capital, expertise, and global reach that a family-owned business might struggle to provide alone.

V. The CDH Investment & JS Global Era (2017-2023)

In 2017, CDH Private Equity acquired a stake in the company. This wasn't a distress sale or a founder cashing out—it was a strategic decision to find the right partner for the next phase of growth. Rosenzweig explained, "Our collaboration with CDH was the result of a thorough and thoughtful search for the right partner to meet our business objectives."

CDH Investments wasn't your typical Western private equity firm. Based in Beijing with offices across Asia, CDH had a unique proposition: they could provide SharkNinja with access to Asian markets, manufacturing expertise, and crucially, a pathway to scale that preserved the company's entrepreneurial culture. A previous Reuters report indicated a possible sale of the company could value SharkNinja at more than $1.5 billion, including debt—a valuation that reflected the extraordinary value creation over the previous decade.

It was then structured as a subsidiary of JS Global, an investment holding company. JS Global wasn't just a holding company—it was a strategic platform that combined SharkNinja with Joyoung, a leading Chinese kitchen appliance company. The logic was compelling: Joyoung dominated the Chinese market with products tailored to Asian cooking styles, while SharkNinja ruled in North America. Together, they could create a global appliance powerhouse.

In early 2019, the two parties built an offshore platform, JS Global Lifestyle, which controls SharkNinja and Joyoung, and was subsequently listed on the main board of the Hong Kong Stock Exchange in the same year. The IPO raised significant capital and provided liquidity for early investors, but more importantly, it created a currency for acquisitions and a platform for expansion.

The JS Global era accelerated SharkNinja's global expansion in ways that would have been difficult as an independent company. Throughout his 17-year tenure, Mark has orchestrated a series of moves to expand and accelerate the business, including taking the company's former parent public on the Hong Kong Stock Exchange in 2017 and listing SharkNinja on the New York Stock Exchange in 2023.

But the marriage between SharkNinja and JS Global revealed fundamental tensions. The move by JS Global, which is listed in Hong Kong, to separate SharkNinja was because the unit's products were unknown in the Chinese market, even though those products made up a majority of the parent company's sales. SharkNinja accounted for almost half of JS Global's revenue in 2018.

This created a paradox: JS Global's most valuable asset was a business that Asian investors didn't understand. Meanwhile, SharkNinja's management was frustrated that their story wasn't being properly valued in Hong Kong markets. American institutional investors who understood the consumer products space couldn't easily invest in a Hong Kong-listed company, while Asian investors were more interested in Joyoung's China story.

The supply chain relationships during this period were complex but crucial. Since 2020, the company has paid out over $3.3 billion to JS Global subsidiaries to obtain the merchandise and goods, mostly made in China, that it sells to American consumers, and to provide "certain procurement and quality control services." This arrangement gave SharkNinja access to world-class manufacturing at scale, but it also created dependencies that would need to be carefully managed.

Manufacturing and supply chain evolution during this period was remarkable. The company developed a dual-sourcing strategy to reduce risk: "There are no existing long-term manufacturing contracts on which we are substantially dependent and most of our products are dual-sourced." This approach provided flexibility and negotiating leverage while ensuring supply chain resilience.

The financial performance during the JS Global era validated the strategy. For the period ended December 31, 2022, SharkNinja reported net sales of $3.7 billion, total assets of $3.3 billion and net profit of $232 million. But as impressive as these numbers were, both SharkNinja management and JS Global's board recognized that the current structure wasn't optimizing value for either party.

VI. Product Innovation Playbook

The SharkNinja product innovation playbook reads like a masterclass in consumer-obsessed design. At its core is what insiders call the "5-star rating" obsession—a relentless focus on creating products that consumers don't just like, but love enough to evangelize.

The consumer feedback loop system they built was unprecedented in the appliance industry. Euro Pro seeks to solicit consumers' feedbacks and ideas through various approaches and sustain improvement. I've been told by some friend that before Shark vacuums officially hit the market, consumers will be offered hundreds of samples, to facilitate feedback gathering and succeeding product modification. This wasn't focus groups or surveys—this was putting products in real homes and iterating based on actual usage.

The company possesses a portfolio of over 4,500 patents in force in various jurisdictions. But these patents weren't just defensive positions—they represented genuine innovations in everything from cyclonic suction to blade design to heating elements. Each patent was a solution to a specific consumer problem identified through their feedback loops.

The category disruption methodology followed a consistent pattern: 1. Identify a category dominated by either expensive premium products or cheap low-quality ones 2. Find the specific pain points that existing products don't address 3. Engineer a solution that delivers 80% of premium performance at 50% of the price 4. Use direct-response marketing to educate consumers and build the brand 5. Expand into retail once demand is proven

The price-to-value equation mastery was perhaps their greatest innovation. We achieved a gross margin of over 45% for the year ended December 31, 2020 and we are highly focused on returning to approximately that margin level over the longer term. These weren't the razor-thin margins of commodity appliances—these were software-like margins achieved through smart engineering and efficient marketing. The speed of innovation was unmatched in the industry. Our team of over 800+ cross-functional engineers and designers solve consumer problems that others either do not see or are unable to solve. The breadth of our engineering team's competencies allows us to develop innovative products, while our continuous global collaboration produces a rapid and iterative development cycle. Launching approximately 25 new products annually, the company leverages rigorous consumer research, hands-on testing, social media engagement, and a global network of industry experts to deliver five-star-rated products from the start.

But perhaps the most impressive aspect of their innovation engine was how they scaled it globally. Although an American company, their global presence is marked by three R&D hubs that ensure 24-hour innovation across Boston, China and London. This wasn't just about having offices in different time zones—it was about creating a continuous innovation cycle where work never stopped.

The testing process was extraordinary in its rigor. Before launch, every product goes through an extensive real-world testing process in over 750 consumer homes. These tests generate valuable feedback that leads to up to 200 changes being made to each product before it hits the market. This level of pre-launch refinement was unheard of in the industry, where most companies relied on focus groups and limited beta testing.

The investment in R&D was substantial and strategic. Barrocas said that the company is currently investing about 6.5% of sales into research and development. A report from the National Center for Science and Engineering Statistics found that in 2020 the "electrical equipment, appliance, and components" industry spent on average 3.3% of net sales on R&D. A closer analog is the Whirlpool Corporation, owner of Maytag and KitchenAid, which spent ~3% of net sales.

The transition from direct-response DNA to omnichannel excellence was masterful. While the company maintained its direct-to-consumer roots, they had successfully expanded into every major retail channel. The key was that they never abandoned what made them successful—they just added new capabilities on top of their core strengths.

VII. The Spin-off & Going Public (2023)

The Board of JS Global Lifestyle Company Limited announced the spin off of SharkNinja on February 23, 2023. This wasn't a rushed decision—it was the culmination of years of strategic thinking about how to maximize value for all stakeholders.

The strategic rationale for independence was compelling on multiple fronts. Following JS Global's assessment of the overall market positions of product offerings under the Shark, Ninja and Joyoung brands, JS Global recognized that continued success in each market requires geographic-specific considerations, including consumer habits, localized lifestyle differences, cultural differences and consumer and market preferences. As a result, the JS Global board of directors (the "JS Global Board") believes that the best strategy to drive global business growth and expand its presence in localized markets at this time is to separate into its two primary delineated markets: (i) the APAC region and (ii) North America, Europe and other select international markets. JS Global intends to remain listed on the Stock Exchange of Hong Kong (with Joyoung remaining listed on the Shenzhen Stock Exchange) and focus on the APAC region, while SharkNinja, as a separate entity, intends to list on NYSE and focus on North America, Europe and other select international markets.

The spin-off mechanics were elegant in their simplicity. Under the terms of the separation, shareholders who held JS Global ordinary shares on July 4, 2023 (the "Record Date") received a distribution of one SharkNinja ordinary share for every 25 ordinary shares of JS Global held by such shareholder as of the Record Date. This ratio reflected the relative valuations of the two businesses while ensuring broad distribution of SharkNinja shares.

On its first day of trading, shares of SharkNinja jumped 40% to close at $42.31 per share. The market's enthusiastic reception validated years of value creation that had been hidden within the JS Global structure. The company opened for trading at $30.05, implying an initial market cap of $4.2 billion. SharkNinja has the #1-selling vacuum and #1 selling blender brands in the US, with $3.8 billion in annual revenue. It jumped more than 40% on the first day, but finished the week down 11%.

The IPO window dynamics were challenging but ultimately favorable. Zoom in: SharkNinja made the decision to list in the U.S. months ago, but the IPO market was frozen at that time, CEO Mark Barrocas tells Axios. The company had to navigate carefully between market conditions and their strategic objectives.

Financial engineering behind the scenes was complex. SharkNinja said it paid out a $375 million "special cash dividend" to JS Global for the repayment of debt. Two more dividends, in February 2023, paid out an additional $115.4 million to the firm. These payments cleaned up the capital structure and ensured SharkNinja started its independent life with a strong balance sheet.

The geographic focus post-spin was clear: US and Europe versus Asia-Pacific split. The move by JS Global, which is listed in Hong Kong, to separate SharkNinja was because the unit's products were unknown in the Chinese market, even though those products made up a majority of the parent company's sales, Barrocas explains. SharkNinja has had an easier time explaining its business to investors in a market where its products are widely sold, he adds.

VIII. Business Model & Financial Architecture

The financial architecture of SharkNinja reveals a business model that's both elegantly simple and remarkably sophisticated. At its core, the company has built a machine that transforms consumer insights into high-margin products at unprecedented speed and scale.

Revenue breakdown tells the story of balanced diversification. The increase in net sales and Adjusted Net Sales resulted from growth in each of our four major product categories of Food Preparation Appliances, Cooking and Beverage Appliances, Cleaning Appliances and Other, which includes beauty and h[ome environment]. Cooking and Beverage Appliances net sales increased by $36.2 million, or 10.6%, to $379.3 million, compared to $343.1 million in the prior year quarter. Adjusted Net Sales of Cooking and Beverage Appliances increased by $39.7 million, or 11.7%, from $339.6 million to $379.3 million, driven by growth in Europe. Global growth was supported by the success of the outdoor grill and outdoor oven across both the US and European markets. Food Preparation Appliances net sales increased by $121.5 million, or 84.8%, to $264.9 million, compared to $143.4 million in the prior year quarter. Adjusted Net Sales of Food Preparation Appliances increased by $125.9 million, or 90.6%, from $139.0 million to $264.9 million, driven by strong sales of our ice cream makers and portable blenders. Net sales in the Other category increased by $88.3 million, or 176.2%, to $138.4 million, compared to $50.1 million in the prior year quarter.

The gross margin dynamics reveal the power of the model. We believe SharkNinja products allow consumers to navigate daily tasks more efficiently without compromising on quality. This value proposition allows them to command premium pricing while still being perceived as value products—a rare feat in consumer goods.

Marketing spend efficiency is where SharkNinja truly differentiates itself. SharkNinja, the company behind the Shark and Ninja household products brands, has opened the curtain on how it spends its $700 million advertising budget. The company, which sells 36 different types of products—everything from air fryers to vacuums to outdoor grills—is developing 60 products at any given time and typically launches 25 new products per year, according to SharkNinja CEO Mark Barrocas. SharkNinja sells these products through its own website and retailers like Walmart, Sephora, and Bass Pro Shop. To get shoppers interested, the company spends more than $700 million on advertising—roughly 11% of its annual sales—to push its brands through social media influencers, TV infomercials, product integrations, and more.

The supply chain strategy represents a delicate balance between efficiency and resilience. The dual-sourcing approach mentioned earlier provides flexibility, while the relationship with JS Global subsidiaries ensures access to competitive manufacturing costs. "We intend to continue to rely on JS Global for certain supply chain services," the filing said.

The China dependency challenge is real but manageable. While critics point to the risks of tariffs and geopolitical tensions, SharkNinja has built enough flexibility into its supply chain to navigate these challenges. The company's ability to pass through some cost increases to consumers, combined with its operational efficiency, provides buffers against supply chain disruptions.

The financial results speak for themselves. In recent quarters, the company has demonstrated remarkable growth: Net sales increased 31.4% to $1,248.7 million, compared to $950.3 million during the same period last year. Adjusted Net Sales increased 37.9% to $1,248.7 million, compared to $905.6 million during the same period last year, or 37.6% on a constant currency basis.

IX. Competitive Dynamics & Market Position

The competitive landscape in household appliances is a battlefield where SharkNinja has emerged as the disruptor-turned-incumbent. The market share battles tell a story of relentless execution and strategic positioning.

In the vacuum category, the David versus Goliath narrative has flipped. Shark's upright vacuums and Ninja's electric grills each account for 43% of their respective markets in the U.S., the filing showed. From 2019 to 2022, Shark's robot vacuum market share grew from 15% to 25%. Meanwhile, traditional players struggle to maintain relevance. Meanwhile, vacuum rival iRobot, which Amazon has agreed to acquire, is giving up business. The company said in the risk factors section of its most recent annual filing that "increased competitive pressure has resulted and will continue to result in a loss of sales or market share."

Dyson remains the premium competitor, but SharkNinja has effectively boxed them into the ultra-premium segment. Impressively, Shark has become the top-selling vacuum cleaner brand in the US, Canada and the UK, challenging the dominance of brands like Dyson and Hoover. The strategy isn't to beat Dyson at their own game—it's to change the game entirely.

In kitchen appliances, the competition is more fragmented but no less intense. Breville dominates the premium segment with $300+ products, Cuisinart holds the middle market, and KitchenAid leverages its brand heritage. SharkNinja's response? Attack all segments simultaneously with different products at different price points, all under the Ninja brand.

The IP battlefield reveals another dimension of competition. In 2014, Dyson sued SharkNinja for infringement of three vacuum technology patents. After a four-year court case, the court ruled that the patents had not been infringed. These legal victories aren't just about avoiding damages—they validate SharkNinja's innovation credentials and clear the path for continued product development.

Retail relationships have evolved from weakness to strength. Initially dependent on direct-response channels, SharkNinja now commands premium shelf space at every major retailer. The company's ability to drive traffic and sales gives it leverage in negotiations that smaller brands can only dream of.

The e-commerce transformation has been particularly favorable for SharkNinja. Their direct-to-consumer DNA gives them advantages in digital marketing, conversion optimization, and customer data that traditional brands struggle to match. They understand performance marketing in ways that legacy brands are still trying to learn.

X. Playbook: Business & Investing Lessons

The SharkNinja playbook offers lessons that extend far beyond household appliances. These are principles for building dominant consumer businesses in any category.

Finding and exploiting the "price wasteland" is perhaps the most replicable strategy. In every market, there's a gap between cheap/low-quality and expensive/high-quality. Most companies are afraid to attack this middle ground because it requires exceptional execution—you need to deliver quality at scale with attractive margins. SharkNinja proved it's possible.

Building brands through direct response and performance marketing seems antiquated in the age of social media, but SharkNinja shows its enduring power. Direct response forces immediate accountability—either the product sells or it doesn't. This discipline creates a feedback loop that makes every marketing dollar work harder.

The power of dual-brand strategy allowed SharkNinja to attack multiple categories without diluting brand equity. Shark means cleaning, Ninja means kitchen. Simple, clear, powerful. This clarity enables them to compete across dozens of subcategories while maintaining brand coherence.

Speed as competitive advantage isn't just about being first to market—it's about iterating faster than competitors can respond. SharkNinja's ability to innovate and pivot faster than its competitors is rooted in a unique combination of company culture, consumer-centric strategies, and structural advantages that allow them to respond to market demands with lightning speed. Under the leadership of Mark Barrocas, the company has built a framework for rapid product development and market adaptation, which sets it apart in an industry where competitors often move at a slower pace.

Consumer obsession and feedback loops create a moat that's hard to replicate. It's not just about listening to consumers—it's about building systems that turn consumer insights into products faster than anyone else. Consumer First Innovation Wins — Every SharkNinja product must be faster, better, and higher quality than competitors. Five-Star Ratings Drive Demand — Product excellence fuels organic reviews, search rankings, and omnichannel success.

Managing complexity across 35+ categories requires operational excellence that few companies achieve. The key is standardizing the innovation process while allowing for category-specific customization. SharkNinja has built a platform that can enter any household category with a reasonable chance of success.

Cross-border M&A execution taught valuable lessons about aligning interests across cultures and markets. The JS Global partnership worked because both parties understood their strengths and stayed in their lanes.

Public market spin-off dynamics showed how to unlock value trapped in complex corporate structures. The key was patience—waiting for the right market conditions and ensuring both entities would thrive independently.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The bull case for SharkNinja rests on proven execution and massive runway. The innovation engine continues to hum, with a portfolio of more than 5,200 patents worldwide, SharkNinja brings breakthrough ideas to life at a robust speed and scale. In 2024 alone, SharkNinja expanded into four new sub-categories and three additional countries, further strengthening its global reach.

Strong brand equity provides pricing power and customer loyalty. The company has successfully built two billion-dollar brands that resonate with consumers across demographics. This isn't easily replicable—it takes years of consistent execution to build this level of trust.

Geographic expansion opportunities remain substantial. While SharkNinja dominates in North America and is growing in Europe, there are entire continents where the brands have minimal presence. Each new market represents billions in potential revenue.

Category expansion runway seems almost limitless. From the 35 subcategories they're in today, they could easily double that number. Beauty, outdoor, and smart home categories are just beginning.

Gross margin expansion potential exists as the company scales and optimizes its supply chain. The target of returning to 45%+ gross margins would drop significant profit to the bottom line.

Bear Case:

The bear case centers on structural challenges and competitive threats. China supply chain dependencies create vulnerability to tariffs, geopolitical tensions, and supply disruptions. While the company has dual-sourcing for many products, complete independence from Chinese manufacturing would be costly and time-consuming.

Tariff and geopolitical risks could materially impact margins. A significant escalation in US-China trade tensions could force SharkNinja to absorb costs or raise prices, potentially losing market share to competitors with more diversified supply chains.

IP litigation exposure remains a constant threat. As SharkNinja enters new categories and pushes innovation boundaries, they inevitably bump up against existing patents. While they've won important cases, litigation is expensive and distracting.

Intense competition from established players won't abate. Dyson, Bissell, and others aren't standing still. As SharkNinja grows larger, it becomes a bigger target for competitive response.

Consumer discretionary spending sensitivity could impact growth. In a recession, consumers might delay appliance purchases or trade down to cheaper alternatives. SharkNinja's positioning in the middle market could be squeezed from both ends.

XII. Epilogue & Looking Forward

Standing at $5.5 billion in revenue in 2024, SharkNinja has come an extraordinary distance from its door-to-door sewing machine roots. Yet in many ways, the company is just getting started.

The post-spin performance has validated the independence thesis. Free from the complexity of the JS Global structure, SharkNinja can tell its story directly to investors who understand the North American consumer market. The stock market has responded accordingly, though volatility remains as investors digest the company's aggressive growth plans.

Future growth vectors read like a map of modern consumer trends. The beauty category, anchored by the Shark haircare line, is just beginning. Outdoor products capitalize on the pandemic-driven outdoor living boom. Smart home integration could transform every SharkNinja product into a connected device.

AI and IoT integration opportunities are particularly intriguing. Imagine a Shark vacuum that learns your cleaning patterns and schedules itself, or a Ninja blender that suggests recipes based on what's in your fridge. The company's consumer data advantage positions them well for this connected future.

Sustainability initiatives, while not core to the story today, will become increasingly important. In SharkNinja's first ESG Report, Mark unveiled the company's Positive Impact Plan, which sets ambitious commitments on circular economy and repairability requirements, 100% renewable electricity (Scope 2) usage in 2025 and pay equity and opportunities for all associates regardless of race, gender, ethnicity, or other characteristics.

What would success look like in 5 years? A $10 billion revenue run rate seems achievable given current growth rates. Expansion into 50+ subcategories would establish SharkNinja as a true household conglomerate. Geographic diversification reducing North American revenue concentration below 50% would de-risk the business model.

But perhaps the biggest question is whether SharkNinja can maintain its insurgent mentality as it becomes the incumbent. Can a company this large still move like a startup? Can it continue to disrupt categories when it's the market leader?

The answer may lie in the company's cultural DNA. This is still, at heart, the same business that sold sewing machines door-to-door. The direct connection to consumers, the obsession with solving real problems, the willingness to challenge convention—these aren't just strategies, they're embedded values.

As Mark Barrocas puts it, the goal is "positively impacting people's lives every day in every home around the world." It's an ambitious mission, but given SharkNinja's track record of turning ambitious goals into reality, it would be foolish to bet against them.

The SharkNinja story is ultimately about democratization—making quality accessible, making innovation affordable, making the exceptional everyday. In an era of increasing inequality and premium-ization of everything, there's something deeply American about a company that insists great products shouldn't be luxury goods.

From infomercial pioneer to NYSE powerhouse, from family business to global corporation, from challenger to champion—SharkNinja has defied conventional wisdom at every turn. The next chapter promises to be just as unconventional, just as ambitious, and just as focused on that core mission: solving problems that others can't or won't solve.

The vacuum that can pick up a bowling ball. The blender that makes perfect smoothies. The air fryer that changed how America cooks. These aren't just products—they're proof points that innovation doesn't have to be expensive, that disruption can come from anywhere, and that sometimes the best business strategy is simply to obsess over making customers' lives better.

That's the SharkNinja way. And it's just getting started.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube