HONASA Consumer: The Digital-First Beauty Revolution

I. Cold Open & Hook

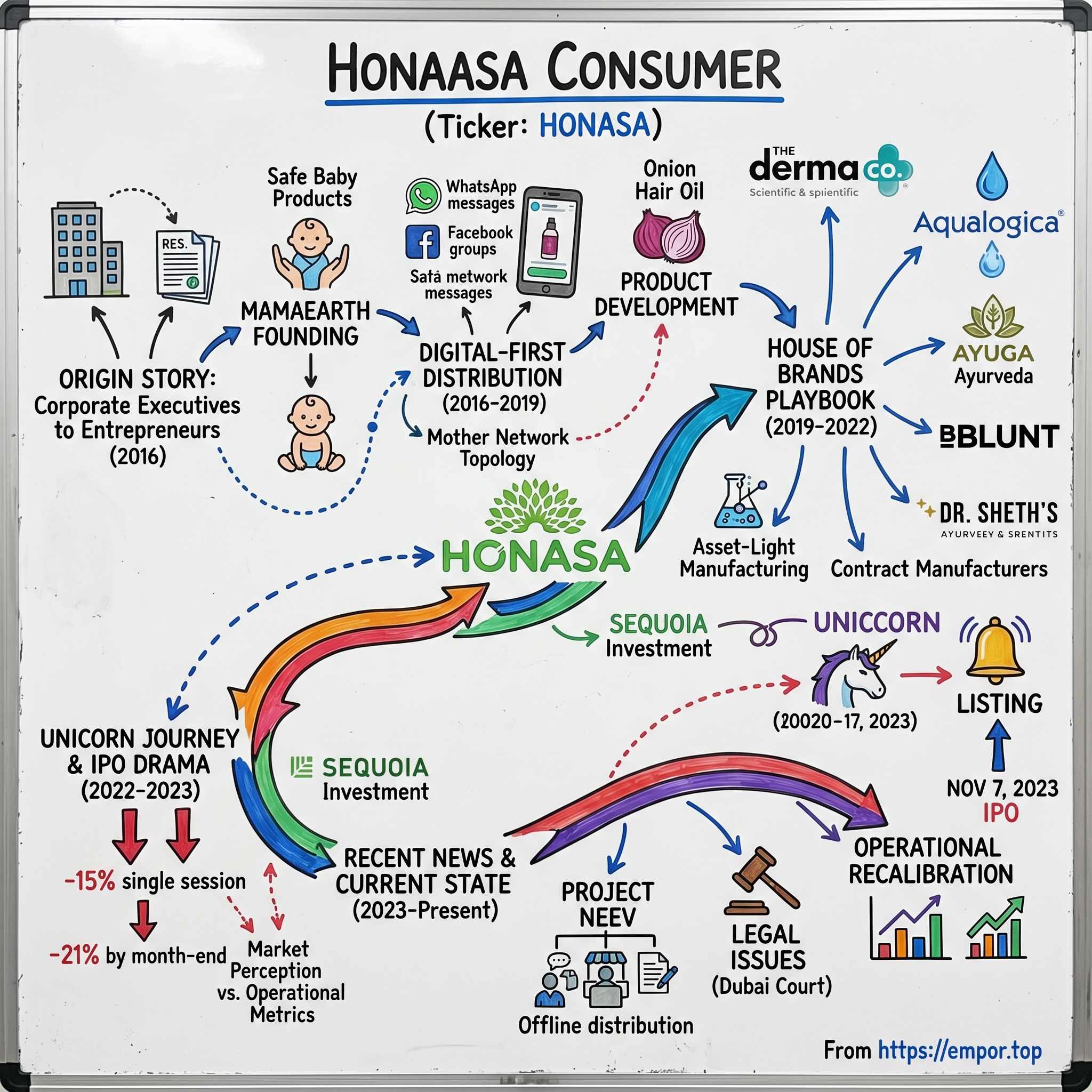

The Mumbai stock exchange floor buzzed with unusual energy on November 7, 2023. Honasa Consumer Limited, the parent company of Mamaearth, was about to list after raising ₹1,700 crores in one of the year's most anticipated IPOs. Founders Varun and Ghazal Alagh rang the ceremonial bell, their faces beaming as confetti rained down. The stock opened at ₹330, above its issue price of ₹324. Victory, it seemed, was theirs.

Three days later, the celebration turned sour. The stock crashed 15% in a single session. By month's end, it had fallen 21% below the IPO price, wiping out ₹2,500 crores in market value. Retail investors who had bet their savings on India's "fastest-growing D2C beauty brand" watched their investments evaporate. The financial press, which had celebrated the company's unicorn status just months earlier, now questioned whether this was another overhyped startup story.

Yet beneath the market drama lies a more complex narrative. In just seven years, two corporate executives with no background in beauty or retail built a ₹1,900 crore revenue business from their Gurgaon apartment. They convinced millions of Indian mothers to switch from century-old brands to products from a company that didn't exist before 2016. They created not one but six beauty brands, each targeting different consumer segments with surgical precision. The story they wanted investors to believe was compelling: India's beauty market was ripe for disruption. Traditional FMCG giants moved slowly, millennials craved authenticity, and digital channels could bypass decades of distribution monopolies. Honasa positioned itself as India's largest digital-first beauty and personal care company by revenue in FY24, with Mamaearth ranking as the third-largest skincare brand in India according to Euromonitor.

But here's what makes this story worth dissecting: This isn't just about whether Honasa can survive the post-IPO bloodbath. It's about whether digital-first consumer brands in emerging markets can build lasting moats, or if they're simply arbitraging temporary inefficiencies that incumbents will eventually close. It's about whether purpose-driven branding translates to pricing power, or if it's just expensive marketing speak. And ultimately, it's about whether two outsiders cracked a code that Hindustan Unilever and P&G missed, or if they're burning cash on a mirage.

The company reported its highest-ever Q1 revenue of ₹595 crores and profit of ₹41 crores with a 7.7% EBITDA margin, yet the stock has crashed 40.5% in one year with a market cap of ₹9,089 crores. The disconnect between operational metrics and market perception tells us something profound about how investors evaluate new-age consumer businesses.

As we unpack this seven-year journey from a Gurgaon apartment to the NSE trading floor, we'll explore not just what happened, but why it matters for the future of consumer entrepreneurship in India and beyond. Because Honasa's story—whether it ends in triumph or tears—is writing the playbook that hundreds of founders will follow or avoid.

II. The Origin Story: Corporate Executives to Entrepreneurs (2016)

The conference room at Hindustan Unilever's Gurgaon office hummed with the usual Monday morning energy in early 2016. Varun Alagh, then in his early thirties, sat through another brand strategy meeting, his mind elsewhere. After years climbing the corporate ladder—from his engineering degree at Delhi University to an MBA from XLRI, through stints at HUL, Diageo, and Coca-Cola—he had mastered the art of building brands for others. But something was shifting.

That evening, Varun came home to find his wife Ghazal hunched over her laptop, surrounded by research papers and product labels. A computer applications graduate from Panjab University with software engineering certification from NIIT, Ghazal had always approached problems with an engineer's precision. But this wasn't about code—it was about chemistry. Specifically, the chemistry in their newborn's skincare products.

"Look at this," she said, pointing to an ingredient list that read like a chemical weapons manifest: sulfates, parabens, mineral oils, synthetic fragrances. The couple had been searching for safe baby products after Ghazal developed concerns about toxins during her pregnancy. What they discovered horrified them. Products marketed to parents with images of pure, happy babies contained ingredients banned in several European countries.

The moment of crystallization came during a late-night conversation in their Gurgaon apartment. "We're not activists," Varun would later recall in interviews. "We're parents who couldn't find what we needed." But they were also strategists who recognized a massive market failure. India's baby care market was dominated by international giants selling formulations designed for Western markets, and local players competing purely on price with questionable quality.

Ghazal's approach was methodical. She spent months researching international safety standards, discovering something called Made Safe certification—a US-based standard that verified products were made without thousands of banned substances. No Indian brand had ever pursued it. "If we're going to do this," she told Varun, "we're going to be Asia's first."

The decision to leave corporate life wasn't taken lightly. Varun was on the fast track at his company, with stock options and a trajectory toward senior leadership. Ghazal had opportunities in tech. Their families thought they were insane. "You want to leave Hindustan Unilever to sell baby shampoo?" Varun's father asked incredulously.

But Varun had observed something profound during his years in FMCG. The playbook hadn't changed in decades: develop products in R&D labs, test with focus groups, launch with massive TV campaigns, fight for shelf space, repeat. Digital was treated as an afterthought, a 5% budget allocation for "experimental" marketing. Young parents, meanwhile, were making purchase decisions in WhatsApp groups and Facebook communities, seeking peer validation rather than celebrity endorsements.

On September 16, 2016, they incorporated Honasa Consumer Private Limited. The name itself was revealing—not "Mamaearth Private Limited" but "Honasa," a made-up word that could house multiple brands. From day one, they weren't thinking about building a product; they were architecting a platform.

The fundamental insight that would drive everything came from a simple observation: Millennials didn't just buy products; they bought into purposes. They wanted to know the founder's story, the ingredient sources, the manufacturing process. They valued transparency over tradition, certification over celebrity. This wasn't just a demographic shift—it was a complete rewiring of how trust was built in consumer markets.

The early days were unglamorous. Varun and Ghazal operated from their apartment, using their savings to fund initial product development. They found a small manufacturer in Baddi, Himachal Pradesh, willing to work with their stringent requirements. The first product wasn't fancy—a basic baby shampoo that took six months to formulate because they refused to use sulfates, which meant reimagining the entire chemistry of how cleaning agents worked.

They faced rejection after rejection. Retailers wouldn't stock an unknown brand. Distributors demanded margins that would make the products unprofitable. Online marketplaces had thousands of baby products; visibility required advertising budgets they didn't have. One major retailer's buyer told them bluntly: "Come back when you have hundred crores in revenue."

But Ghazal had discovered something powerful: mother's groups on Facebook with hundreds of thousands of members, all sharing product recommendations, horror stories about allergic reactions, and desperate searches for safe alternatives. These weren't customers; they were co-conspirators in a mission to protect their children from harmful chemicals.

The couple made a contrarian bet. Instead of hiring a traditional sales team, they hired community managers. Instead of paying for billboards, they sent free products to micro-influencers—mothers with 5,000 followers who commanded more trust than Bollywood celebrities. Instead of promising overnight transformation, they promised gradual, safe improvement.

By December 2016, three months after incorporation, they had their first hundred orders. Not through Amazon or Flipkart, but through WhatsApp messages from mothers who had heard about them in Facebook groups. The orders came with notes: "Finally, someone who understands," "Thank you for caring about ingredients," "My baby's rash cleared up in three days."

Varun understood something from his FMCG days that would become central to their strategy: In consumer goods, distribution is destiny. But he also understood that digital platforms had fundamentally changed what distribution meant. You didn't need to be in 100,000 stores if you could be on 100,000 phone screens.

The Alaghs were building more than a business; they were architecting a new playbook for consumer brands in the digital age. Every decision—from incorporating as a house of brands to focusing on certification over celebrity—was designed for a world where trust traveled through networks, not newspapers.

As 2016 ended, Honasa had sold products worth ₹50 lakhs, tiny by FMCG standards but significant for a bootstrap startup. More importantly, they had proven their hypothesis: Modern parents would pay a premium for products that aligned with their values, and they would find those products through digital communities rather than traditional advertising.

The foundation was set. What came next would either validate their contrarian approach or prove that the FMCG giants had been right all along.

III. Cracking the Code: Digital-First Distribution (2016-2019)

The Mamaearth war room in early 2017 looked nothing like a traditional FMCG headquarters. No sales maps with pins marking distributor territories, no shelf-space planograms, no field force deployment charts. Instead, the walls were covered with printouts from WhatsApp conversations, Facebook group analytics, and customer journey maps that looked more like spider webs than funnels.

Ghazal stood before a whiteboard, mapping what she called the "mother network topology." She had identified 847 active parenting groups across Facebook, WhatsApp, and Telegram, with a combined membership of 3.2 million Indian mothers. Each group had its own culture, its own influencers, its own pet concerns. The Bangalore Moms Connect obsessed over organic certification. The Delhi NCR Mothers Group debated pollution's effect on baby skin. The Mumbai Mommies Network shared horror stories about humidity-induced rashes.

"We're not selling to customers," Ghazal explained to their small team. "We're joining conversations."

The traditional FMCG playbook would have demanded ₹50 crores just to launch: celebrity endorsements, TV campaigns, trade margins, shelf-space fees. Honasa had ₹50 lakhs. This constraint forced innovation that would define their entire trajectory.

Their first breakthrough came through what Varun called "the confession strategy." Instead of creating polished marketing content, they published raw, unfiltered posts about their own parenting struggles. Ghazal wrote about crying in a pharmacy, overwhelmed by ingredient lists. Varun shared his guilt about missing pediatrician appointments due to work. These weren't ads; they were diary entries that happened to mention their products.

The response was explosive. Mothers began sharing these posts with comments like "Finally, founders who get it." But more importantly, they started sharing their own stories. Within months, Mamaearth's Facebook page became a support group where product promotion was almost incidental to community building.

The numbers told a story that would have seemed impossible to FMCG veterans. By mid-2017, Mamaearth was acquiring customers at ₹250 each—one-tenth the cost of traditional brands. Their repeat purchase rate hit 38% within three months, unheard of for a new beauty brand. But these metrics came with a catch: they were spending 35-40% of revenue on digital marketing, a ratio that would make traditional companies gasp.

The advertising paradox became clear early. Digital marketing was both cheaper and more expensive than traditional advertising. Cheaper per customer acquired, but expensive as a percentage of revenue because the revenue base was small and the market was nascent. Every month, Varun faced the same decision: reduce marketing spend to show profitability, or maintain spending to drive growth. He chose growth, every time.

But the real innovation wasn't in spending; it was in listening. Every customer service complaint became a product development input. When mothers complained about pump bottles being hard to use with one hand while holding a baby, Mamaearth redesigned all packaging. When customers said they wanted to understand ingredients, the company created India's first ingredient transparency app that explained what each component did in simple language.

The community-driven product development created a virtuous cycle. In 2017, Mamaearth launched seven products. By 2018, they had twenty-three. By 2019, forty-one. Each launch wasn't a guess; it was a response to thousands of conversations. The onion hair oil that became their bestseller? Suggested by a mother from Pune who shared her grandmother's recipe in a Facebook comment.

The digital-first approach revealed unexpected insights about Indian consumer behavior. Urban mothers didn't shop for baby products; they researched them. The average customer visited the Mamaearth website 7.3 times before making a first purchase. They read reviews, compared ingredients, watched unboxing videos, and sought opinions in their WhatsApp groups. The purchase was just the culmination of a trust-building journey that took weeks.

This understanding led to another contrarian decision: radical transparency. While competitors hid behind proprietary formulations, Mamaearth published everything. Source of ingredients, manufacturing process, safety testing results, even failed experiments. They created a "Why This Ingredient?" section for every product that explained the scientific reasoning in layman's terms.

The transparency strategy had an unexpected benefit: it turned customers into evangelists. Mothers became ingredient experts, debating the merits of coconut-derived sulfates versus synthetic alternatives in their groups. They weren't just buying Mamaearth; they were defending it with scientific arguments provided by the company itself.

By late 2018, a pattern emerged that would define their growth strategy. A product would launch digitally, gain traction in specific communities, hit a revenue threshold, then expand to marketplaces, and finally to offline retail. This reversed the traditional FMCG sequence and dramatically reduced the risk of inventory buildup.

The platform economics were compelling. Customer acquisition through Facebook and Google cost ₹250-300. The average first order was ₹648. By the third purchase, lifetime value exceeded ₹2,400. The math worked, but only if you could stomach the upfront investment and wait for the payback period.

But digital-first had limitations. Seventy percent of customers still wanted to touch and feel products before buying. Rural markets remained unreachable. Premium positioning meant excluding price-sensitive segments. The question wasn't whether to go offline, but when and how.

The answer came through an unlikely source: pharmacies. Unlike general trade stores that demanded 40% margins, pharmacies operated on 20-25% margins and attracted trust-seeking customers. Mamaearth began selective offline expansion in 2019, but with a twist—they only entered stores where they already had strong digital presence. If a zip code showed high online order density, they would approach nearby pharmacies. The digital heatmap became the offline expansion blueprint.

The masterstroke came in 2019 with the launch of their Direct-to-Consumer (D2C) website. While Amazon and Flipkart drove volume, the D2C platform provided something invaluable: first-party data. Every click, scroll, and cart abandonment taught them about customer behavior. They could test price points, run exclusive launches, and build direct relationships without marketplace intermediaries taking 15-20% commissions.

The technology stack they built would have impressed Silicon Valley: predictive analytics for inventory management, automated customer segmentation for personalized marketing, real-time sentiment analysis of social media conversations, and dynamic pricing algorithms that adjusted based on demand patterns. This wasn't a beauty company with a website; it was a tech company that happened to sell beauty products.

The results by end-2019 validated the model: ₹110 crore revenue, 20x growth in three years, 2 million customers acquired primarily through digital channels, and presence in 500 offline stores selected through digital data. More importantly, they had built a repeatable playbook that could work for any product category targeting digitally-savvy consumers.

But success brought scrutiny. Competitors began copying their transparency marketing. Digital advertising costs started rising as more brands competed for the same keywords. The question loomed: Was this sustainable, or were they simply the first to exploit a temporary arbitrage opportunity?

The answer would come through diversification—not just of products, but of entire brands. The house of brands strategy that seemed ambitious in 2016 would become essential for survival.

IV. The House of Brands Playbook (2019-2022)

The conference room in Honasa's new Gurgaon office bristled with tension in October 2019. Varun faced his leadership team with a proposal that sounded like heresy: launch a completely new brand, The Derma Co., targeting a different audience with different messaging, while Mamaearth was still finding its feet.

"We're barely profitable with one brand, and you want to launch another?" his CFO challenged.

Varun pulled up a slide showing search trends. "Dermatologist recommended" searches had grown 400% in two years. "Retinol India," "salicylic acid benefits," "niacinamide serum"—technical ingredients were entering mainstream vocabulary. Young Indians weren't just buying products; they were becoming amateur dermatologists, influenced by Korean beauty trends and YouTube skincare educators.

But Mamaearth couldn't credibly pivot to science-forward messaging. Its entire identity was built on natural, toxin-free positioning. Trying to sell peptides and acids under the Mamaearth brand would confuse the carefully cultivated mother community. The solution: create an entirely different brand with its own identity, team, and positioning.

The Derma Co. launched in December 2019 with a radically different approach. Where Mamaearth emphasized natural and safe, The Derma Co. promised "active ingredients at active concentrations." Where Mamaearth's packaging featured soft pastels and baby imagery, The Derma Co. opted for clinical blacks and whites with percentage callouts—"10% Niacinamide," "2% Salicylic Acid."

The masterstroke was the acquisition strategy. Instead of competing with Mamaearth for the same Facebook audiences, The Derma Co. targeted Reddit skincare communities, Instagram's #SkincareAddicts, and YouTube comment sections under dermatologist videos. The customer acquisition cost was 40% higher—₹420 versus ₹300—but the average order value was double: ₹1,300 versus ₹650.

Within six months, The Derma Co. hit ₹25 crore in revenue. The velocity shocked even Varun. But more importantly, it proved the playbook could be replicated. Each brand became a laboratory for testing different aspects of the digital-first model.

The expansion accelerated. Aqualogica launched in 2021, targeting the overlooked sunscreen market with hydration-focused messaging. Where established brands treated sunscreen as a necessary evil, Aqualogica positioned it as a skincare essential, creating India's first "sunscreen wardrobe"—different formulations for different occasions.

Ayuga entered the Ayurvedic space, but with a twist. Instead of competing with Patanjali on price or Forest Essentials on luxury, it targeted the "modern traditionalist"—young professionals who wanted Ayurvedic benefits without the Sanskrit terminology and elaborate rituals. Products were named simply: "The Night Cream," "The Face Wash," with Ayurvedic ingredients mentioned secondarily.

The acquisition spree added established brands to the portfolio. BBlunt, purchased in 2021, brought salon-grade hair styling to the portfolio. Dr. Sheth's, acquired in 2022, provided instant credibility in the dermatologist-recommended segment. Each acquisition wasn't just about adding revenue; it was about acquiring capabilities, customer bases, and market knowledge that would take years to build organically.

The product development velocity reached staggering proportions. While Mamaearth remained the flagship brand, Honasa operated The Derma Co, BBlunt, Dr Sheth's, Aqualogica, and Staze 9to9. The company launched 91 products in FY21, 122 in FY22, and 252 in FY23. By Q1 FY24 alone, they added another 89 products. This wasn't product development; it was product manufacturing at software deployment speed.

The secret lay in the asset-light manufacturing model. Honasa partnered with 37 contract manufacturers, each specializing in different formulations. A sunscreen manufacturer in Baddi, a serum specialist in Gurgaon, a hair care expert in Chennai. This network allowed them to launch products in 45 days from concept to shelf, versus the industry standard of 12-18 months.

But the real innovation was in how these brands cross-pollinated. Customer data from Mamaearth informed product development for The Derma Co. Supply chain efficiencies gained from one brand reduced costs for all. Marketing insights from failed campaigns became learning inputs for future launches. Each brand wasn't just a revenue stream; it was a data generator for the entire portfolio.

The portfolio strategy created unexpected synergies. A Mamaearth customer who aged out of baby products could graduate to The Derma Co. for skincare. A Derma Co. customer looking for natural alternatives could discover Ayuga. The customer lifetime value extended from single-brand loyalty to ecosystem engagement.

The financial engineering was equally sophisticated. Each brand operated as an independent unit with its own P&L, but shared common infrastructure: technology platforms, warehousing, customer service, and data analytics. This reduced operational costs by 30% compared to running independent companies while maintaining brand autonomy.

The challenges were substantial. Managing multiple brand identities required different creative agencies, influencer networks, and communication strategies. Inventory complexity multiplied—instead of managing 50 SKUs, they were juggling 500. Channel conflicts emerged when retailers questioned why they should stock multiple brands from the same company competing in the same category.

The biggest risk was dilution. Would consumers trust a company that launched a new brand every few months? Could quality be maintained at such velocity? Were they building brands or just launching products with different labels?

The market's response was mixed but generally positive. Dr Sheth's became the fourth brand from Honasa's portfolio to enter the ₹150 crore club in terms of annual recurring revenue after Aqualogica and The Derma Co. The Derma Co achieved an annual recurring revenue of ₹380 crore, while Aqualogica became the fastest to achieve an ARR of ₹180 crore.

But the strategy also revealed a fundamental truth about digital-first brands: customer acquisition costs were rising across the board. Facebook's algorithm changes, iOS privacy updates, and increased competition meant that the cost to acquire a customer through digital channels had doubled from 2019 to 2022. The only way to maintain economics was to extract more value from each customer—hence the push toward multiple brands and higher-priced products.

The house of brands strategy was both a growth accelerator and a hedge against platform dependency. If one brand faced backlash or one channel became uneconomical, the portfolio provided resilience. But it also raised questions about focus, quality, and long-term sustainability.

By late 2022, Honasa operated six brands, 500+ products, across online and offline channels, with presence in international markets. The complexity was staggering, but so was the opportunity. The playbook was proven: identify a consumer segment through digital listening, launch a targeted brand with precise positioning, scale through digital channels, then expand offline.

The question was no longer whether the model worked, but whether it could work at public market scale. The answer would come through an IPO that would test every assumption about digital-first consumer brands.

V. The Unicorn Journey & Pre-IPO Drama (2022-2023)

The Sequoia Capital India (now Peak XV Partners) office in Bangalore hummed with nervous energy on a humid January morning in 2022. Varun and Ghazal sat across from Mohit Bhatnagar, managing director, making their final pitch for what would become a watershed moment—not just for Honasa, but for India's entire D2C ecosystem.

"Your marketing spend is 38% of revenue," Bhatnagar pointed out, his tone neutral but probing. "HUL spends 13%. How do you justify that to public market investors who will compare you to traditional FMCG?"

Varun had rehearsed this answer a hundred times, but his response still carried conviction: "HUL built their brands over decades when TV reach was cheap and retail was concentrated. We're building in months in a fragmented digital ecosystem. The question isn't the absolute spend—it's the return on that spend."

The data was compelling. Customer payback period: 11 months. Contribution margin after marketing: 12%. Year-three customer retention: 34%. These weren't FMCG metrics; they were SaaS metrics applied to consumer goods. Sequoia understood this language.

Three weeks later, the term sheet arrived: $52 million for a $1.2 billion valuation. Honasa had become a unicorn.

The announcement triggered a media frenzy. "Mamaearth Parent Joins Unicorn Club," screamed headlines. But inside Honasa, the celebration was muted. Everyone understood what this meant: the IPO clock had started ticking. Sequoia didn't invest at billion-dollar valuations for modest exits. The public markets beckoned, ready or not.

The transformation began immediately. Honasa hired investment bankers from Kotak and JM Financial. PWC came in to audit three years of financials. Legal teams from Cyril Amarchand Mangaldas began drafting the Draft Red Herring Prospectus (DRHP). The startup was becoming a corporation, with all the attendant complexity and compliance requirements.

But the biggest change was operational. Public markets wouldn't tolerate 38% marketing spend. The mandate came down: improve margins without sacrificing growth. It seemed impossible, but Ghazal had an idea.

"We've been paying for customers," she told the leadership team. "What if we made customers pay for access?"

Thus was born the Mamaearth subscription program—₹299 for annual membership that provided 20% discounts, early access to launches, and exclusive products. Within six months, 200,000 customers had subscribed, generating ₹6 crores in high-margin revenue while reducing the effective customer acquisition cost by 30%.

The margin improvement tactics multiplied. Private label manufacturing for international brands generated 40% gross margins. Exclusive SKUs for modern trade prevented price comparison. Dynamic pricing algorithms adjusted rates based on inventory levels and demand patterns. Every basis point mattered now.

December 2022 marked a crucial milestone: Honasa filed its DRHP with SEBI. The 500-page document revealed everything—the good, bad, and ugly of building a digital-first consumer brand. Revenue had grown to ₹1,282 crores in FY22. But losses persisted: ₹150 crores in FY20, ₹36 crores in FY21, though narrowing to ₹18 crores in FY22.

The public response was polarized. Supporters saw India's answer to The Honest Company or Glossier—digital-native brands that had disrupted established categories. Critics saw another loss-making startup trying to cash out at public expense.

The pre-IPO period became a masterclass in narrative management. Ghazal appeared as a judge on Shark Tank India, building personal brand equity while subtly promoting Honasa's entrepreneurial credentials. Varun's LinkedIn posts, mixing business insights with poetry, went viral. They weren't just selling shares; they were selling a story.

The celebrity endorsement strategy shifted into overdrive. Shilpa Shetty became brand ambassador for Mamaearth. Samantha Ruth Prabhu endorsed The Derma Co. These weren't cheap—industry sources suggested multi-crore deals—but they provided the mainstream validation that digital-first brands often lacked.

Behind the scenes, the financial engineering intensified. In the first half of fiscal 2024, Honasa Consumer delivered revenue of ₹961 crore, up 33% over the previous year. The company achieved something remarkable: negative working capital of minus five days, meaning they collected money from customers before paying suppliers—a cash flow dream.

The distribution expansion accelerated dramatically. The company increased its offline distribution to 165,937 outlets as of September 2023, a growth of 47% over the previous year. This wasn't just about revenue; it was about proving to public investors that the company wasn't dependent solely on digital channels.

But challenges mounted. Distributor complaints surfaced about inventory dumping—Honasa allegedly forcing excess stock onto partners to inflate revenue numbers. Former employees leaked stories about toxic work culture and unrealistic targets. Competitors launched copycat products with similar "toxin-free" messaging, eroding Mamaearth's differentiation.

The most serious challenge came from an unexpected source: influencer backlash. Several prominent skincare influencers began questioning Mamaearth's "natural" claims, pointing out that many ingredients were synthetic derivatives. The hashtag #MamaEarthExposed trended for three days, forcing Ghazal to personally respond with ingredient explanations.

The SEBI approval process dragged on. Questions about related party transactions, sustainability of marketing spend, and competitive moats required detailed responses. The market window was closing—tech stocks globally were correcting, and IPO appetite was waning.

Finally, in October 2023, SEBI approval came through. The IPO would raise ₹400 crores in fresh capital, with existing investors selling ₹1,300 crores worth of shares. The price band was set at ₹308-324 per share, valuing the company at approximately ₹10,500 crores at the upper end.

The roadshow began—Mumbai, Singapore, London, New York. Varun and Ghazal pitched to institutional investors who grilled them on everything from customer retention rates to regulatory risks. The feedback was mixed. Growth investors loved the story but worried about valuations. Value investors appreciated the improving margins but questioned the sustainability of digital-first models.

The retail portion of the IPO opened on October 31, 2023. The minimum investment of ₹14,168 meant small investors could participate. The marketing campaign went into overdrive—front-page newspaper ads, YouTube testimonials, influencer endorsements. This wasn't just an IPO; it was positioned as a movement—"Be Part of India's Beauty Revolution."

But the subscription numbers told a different story. The retail portion was subscribed only 1.35 times, significantly below the 5-10x oversubscription seen in hot IPOs. Institutional investors showed more interest, subscribing 3.2 times, but the lukewarm retail response was a warning sign ignored in the euphoria.

The stage was set for November 7, 2023—listing day. Years of building, months of preparation, weeks of roadshows had led to this moment. The Alaghs stood at the NSE, ready to ring the bell that would transform their startup into a public company.

What happened next would challenge everything they believed about building consumer brands in the digital age.

VI. The IPO Saga: Triumph or Cautionary Tale? (October-November 2023)

The NSE trading floor at 9:00 AM on November 7, 2023, crackled with anticipation. Ghazal Alagh, dressed in a pink saree that matched Mamaearth's signature color, stood next to Varun at the ceremonial bell. Their children, whose safety concerns had sparked this entire journey, watched from the gallery. The bell rang. Confetti fell. Honasa Consumer Limited was now a public company.

The stock opened at ₹330, a modest 1.9% premium to the issue price of ₹324. Relief washed over the leadership team. They had avoided the embarrassment of a listing-day decline. By noon, the stock touched ₹344, and financial news channels declared the IPO a success. "Digital-First Beauty Brand Makes Successful Debut," scrolled across business news tickers.

Varun's LinkedIn post that evening was characteristically poetic: "From a mother's concern to a million mothers' trust, from a Gurgaon apartment to Dalal Street, today isn't an end but a beautiful beginning." It garnered 50,000 likes within hours. The narrative seemed secure—David had not just faced Goliath but had joined Goliath's club.

But markets have a way of humbling narratives.

November 8 brought the first wobble. The stock declined 3.2% as profit-booking began. "Normal post-listing correction," analysts assured. November 9 saw another 4% drop. Still within acceptable ranges, market experts claimed.

November 10 shattered all pretense of normalcy.

The stock crashed 15% in a single session, triggering lower circuit limits. Volume spiked to 10 times the average as institutional investors dumped shares. By day's end, Honasa traded at ₹276, 15% below its IPO price. ₹2,500 crores in market value had evaporated in three days. Retail investors who had invested their savings watched in horror as their investment turned red.

The post-mortem revealed multiple triggers. A prominent proxy advisory firm had issued a report questioning the sustainability of Honasa's business model, specifically highlighting that marketing expenses were being capitalized rather than expensed in some instances. Foreign institutional investors, who had subscribed hoping for a quick flip, were rushing for exits. But the deeper issue was valuation—at ₹10,500 crores, Honasa was valued at 8x revenue, while established FMCG companies like Dabur traded at 5x.

The founder's response made things worse. Varun posted another LinkedIn update, this time defensive: "Short-term market movements don't define long-term value creation." While factually correct, it came across as tone-deaf to retail investors nursing losses. The comments section turned hostile: "Easy to be philosophical with our money," read one viral response.

The media, which had celebrated the unicorn story, now sharpened their knives. "Honasa Horror: How India's Hottest D2C Brand Became Its Coldest IPO," read one particularly brutal headline. Financial influencers who had recommended the IPO went silent or posted disclaimers about "market risks."

Behind closed doors at Honasa headquarters, crisis meetings ran late into the night. The IPO proceeds—₹400 crores in fresh capital and ₹1,300 crores to selling shareholders—had been collected. Sequoia and other early investors had partially exited at IPO price, booking substantial returns. But the public market judgment was clear: the story wasn't worth the price.

The statutory quiet period prevented management from making public statements or providing guidance. They could only watch as analysts downgraded ratings and target prices. Morgan Stanley set a target of ₹250, implying another 10% downside. Jefferies was more optimistic at ₹300, but still below IPO price.

The distributor crisis chose this moment to explode. The All India Consumer Products Distributors Federation (AICPDF) held a press conference alleging that Honasa had dumped ₹50-100 crores worth of inventory onto distributors before the IPO to inflate revenue numbers. They claimed expired products weren't being replaced and payment terms had been unilaterally changed. While Honasa denied the allegations, the timing couldn't have been worse.

Social media turned vicious. The same communities that had built Mamaearth now questioned everything. "Were we just marketing experiments?" asked one viral post in a mothers' group. Influencers who had promoted the brand faced backlash for "selling out to corporate interests." The carefully cultivated community trust was fracturing.

By month-end, the stock had stabilized around ₹255, 21% below IPO price. The company was still worth ₹8,300 crores—massive by any standard—but the narrative had shifted from growth story to cautionary tale. The question everyone asked: Was this a temporary correction or the beginning of a longer decline?

The answer lay in the quarterly results that would follow. In Q2FY24, Honasa reported a 93% year-on-year increase in net profit to ₹29.4 crore, with consolidated revenue growing 21% to ₹496.1 crore. The numbers were solid, but the market remained skeptical.

The IPO aftermath revealed fundamental tensions in how digital-first consumer brands were valued. Public markets wanted the growth of tech companies with the margins of FMCG companies—an impossible combination. They wanted digital efficiency without digital marketing costs. They wanted disruption without risk.

The Alaghs learned a painful lesson: Building a business and building market confidence were different games with different rules. The former rewarded innovation and risk-taking; the latter punished anything that deviated from established patterns.

Looking back, the IPO was both triumph and cautionary tale. Triumph because a seven-year-old startup had achieved what most entrepreneurs only dream of—taking their company public, creating wealth for employees and investors, and establishing a permanent capital base. Cautionary because it showed the limits of narrative in the face of hard numbers.

The ₹10,500 crore valuation question would define everything that followed. Was it justified by the fundamentals—growing revenue, expanding margins, strong brand portfolio? Or was it bubble valuation, inflated by unicorn hype and FOMO? The market had rendered its initial verdict, but the story was far from over.

VII. Post-IPO Reality & Competitive Dynamics (2023-Present)

The Honasa war room in March 2024 looked different from its IPO celebration venue just four months earlier. The stock price ticker on the wall showed ₹287, still 11% below IPO price. But inside, a transformation was underway—less visible than stock movements but more fundamental to the company's future.

"We need to stop thinking like a startup and start executing like a corporation," Varun told his leadership team. The mandate was clear: deliver consistent quarterly results, expand distribution without destroying margins, and somehow maintain the innovation velocity that had built the company.

The first major decision post-IPO was surprising: pulling back from international expansion. Honasa had been selling in the Middle East and Southeast Asia, markets that seemed natural for Indian beauty brands. But the unit economics didn't work. Customer acquisition costs in Dubai were 3x higher than India, while average order values were only 1.5x higher. The expansion was quietly shuttered, though never officially announced.

The domestic focus intensified with Project Neev, a complete overhaul of offline distribution. Under Project Neev, Mamaearth completed the appointment of Tier I distributors across the top 50 cities, expanding its distribution network by 22% year-on-year to reach over 216,000 FMCG retail outlets as of December 2024, according to NielsenIQ data.

But this expansion came with unexpected pain. The company took a ₹70 crore hit as it revamped its offline business model, shifting from supplying to super stockists to dealing directly with distributors. The traditional trade, which Honasa had initially bypassed through digital channels, extracted its pound of flesh for late entry.

The competitive landscape shifted dramatically. Hindustan Unilever, which had dismissed D2C brands as "niche players" in 2019, launched Wellbeing Nutrition and acquired Oziva. Procter & Gamble India created a "Future Brands" division specifically to compete with digital-first players. Nykaa, once a partner, launched its own private labels directly competing with Honasa's portfolio.

The most interesting competitor emerged from an unexpected source: Emami acquired Dermicool and repositioned it with digital-first marketing, essentially copying Honasa's playbook but with decades of distribution muscle. Within six months, Dermicool's online sales grew 400%, proving that traditional players could adapt faster than expected.

The margin pressure intensified. Digital advertising costs continued rising—customer acquisition through Facebook had reached ₹500 by mid-2024, double the 2019 levels. Meanwhile, offline distribution demanded higher margins than D2C channels. The company was caught between two worlds, paying the costs of both without fully capturing the benefits of either.

In Q2 FY25, Honasa reported its first quarterly loss in five quarters, posting a net loss of ₹19 crore compared to a profit of ₹29 crore in the same period last year, with revenue declining 7% year-on-year to ₹462 crore. The market reaction was swift and brutal—the stock fell another 8% on results day.

The inventory crisis with distributors reached a crescendo. Distributors under the All India Consumer Products Distributors Federation accused the company of pushing excess inventory and delaying replacement of damaged goods, resulting in losses estimated between ₹50-100 crore for distributors. While Honasa maintained these were "isolated incidents," the reputational damage was real.

But amidst the challenges, green shoots emerged. In Q3 FY25, Honasa posted a net profit of ₹26 crore, unchanged from the same period last year but a sharp recovery from the Q2 loss of ₹24.3 crore. Revenue jumped 7.52% year-on-year to ₹536.73 crore, with quarterly growth of 11.39%.

The product portfolio rationalization showed results. Instead of launching 89 products per quarter, Honasa reduced new launches to 20-25, focusing on hero SKUs that drove 70% of revenue. The "long tail" of slow-moving products was eliminated, improving inventory turns from 4x to 6x annually.

Gross margins improved by 200 basis points to 72%, primarily due to better sourcing and optimized ad spends. The company reduced digital ad dependency by 15%, shifting toward influencer marketing and traditional media for more sustainable brand recall.

The organizational culture underwent a subtle but significant shift. The "move fast and break things" startup mentality gave way to "move deliberately and build things to last." Quality control, previously outsourced to manufacturers, was brought in-house with a 50-person team. Customer complaints, once handled by chatbots, were now personally reviewed by senior management.

The brand portfolio strategy evolved from expansion to consolidation. Ayuga, which had never gained traction, was quietly discontinued. Resources were concentrated on four core brands: Mamaearth, The Derma Co., Aqualogica, and Dr. Sheth's. Each brand was given specific growth and margin targets, with leadership compensation tied to both metrics.

The public market discipline, painful as it was, forced operational improvements that had been postponed during the growth-at-all-costs phase. Systems were implemented for demand forecasting, inventory management, and trade partner management. The company hired senior executives from HUL and P&G, bringing traditional FMCG expertise to complement digital-native DNA.

By late 2024, a new equilibrium emerged. The market cap had stabilized around ₹9,089 crores, down 40.5% from its peak but still representing a successful outcome for early investors. Revenue reached ₹1,994 crores with profit of ₹71.2 crores, proving that profitability was possible even with high marketing costs.

The transformation from startup to corporation was incomplete but progressing. The company that had disrupted traditional beauty was itself being disrupted by traditional players adopting digital strategies. The moat that seemed impregnable—direct customer relationships and community trust—proved more fragile than expected when subjected to public market scrutiny.

Yet Honasa's position remained formidable. As India's largest digital-first BPC company by revenue, with Mamaearth ranking as the third-largest skincare brand in India, the company had achieved what most startups only dream of. The question was whether it could maintain this position while satisfying the conflicting demands of growth and profitability.

The post-IPO reality was neither the disaster critics predicted nor the triumph supporters expected. It was something more mundane but perhaps more valuable: a lesson in building sustainable businesses in the harsh light of public market scrutiny. The story was still being written, one quarter at a time.

VIII. The Business Model Deep Dive

The spreadsheet on CFO Ankur Agarwal's screen told a story that would make traditional FMCG executives dizzy. Customer acquisition cost: ₹487. First order value: ₹680. Gross margin: 72%. Marketing expense: 35% of revenue. Contribution margin after all variable costs: 8%. These weren't the comfortable economics of Colgate or Dove—they were the knife-edge margins of a digital-first disruptor.

"Every percentage point matters," Ankur explained to a room of analysts during an investor call. "The difference between 8% and 10% contribution margin is the difference between sustainable growth and cash burn."

The unit economics revealed the fundamental challenge of D2C beauty in India. Unlike the US where average order values exceeded $50, Indian consumers spent cautiously. The typical Mamaearth customer ordered 2.3 products worth ₹680 on their first purchase. Only 34% returned for a second purchase within 90 days. By month 12, just 18% remained active. The entire business model depended on that 18%—the loyalists who ordered monthly and spent ₹1,200 per transaction.

The manufacturing strategy was both brilliant and constraining. The company operated almost debt-free, partnering with 37 contract manufacturers instead of building factories. This asset-light model meant Honasa could launch products in 45 days and scale production instantly. But it also meant gross margins were 10-15 percentage points lower than companies with captive manufacturing.

The working capital dynamics defied FMCG convention. Traditional beauty companies operated on 60-90 day payment cycles. Honasa had engineered negative working capital—collecting from customers in 3 days through digital payments while paying suppliers in 45 days. This 42-day float generated ₹150 crores in free cash at any given time, effectively funding operations without external capital.

But the model had hidden vulnerabilities. Digital marketing costs weren't just expenses—they were investments with uncertain returns. A Facebook campaign costing ₹10 lakhs might generate ₹30 lakhs in immediate sales but ₹100 lakhs in lifetime value—or it might not. The attribution models were sophisticated but ultimately probabilistic. When iOS 14.5 killed tracking, customer acquisition costs spiked 40% overnight as targeting precision collapsed.

The portfolio economics added another layer of complexity. Mamaearth operated at 12% EBITDA margins but required minimal marketing investment given brand maturity. The Derma Co. burned cash with 40% marketing spend but grew at 100% annually. Aqualogica sat in between—profitable but requiring investment to scale. The portfolio math worked only if mature brands funded emerging ones, a delicate balance easily disrupted.

The channel economics varied dramatically:

- D2C website: 45% gross margin, ₹487 CAC, 2.8x LTV/CAC

- Amazon/Flipkart: 30% gross margin (after fees), ₹210 CAC, 1.9x LTV/CAC

- Modern retail: 25% gross margin, zero CAC, but high fixed costs

- General trade: 20% gross margin, zero CAC, but working capital intensive

The optimal mix remained elusive. Too much D2C meant unsustainable marketing costs. Too much offline meant margin compression. Too much marketplace meant platform dependency. Honasa tried to maintain 40% D2C, 35% marketplace, 25% offline, but market forces constantly pushed against this equilibrium.

The subscription experiment revealed both opportunity and limitation. The Mamaearth Plus program had 200,000 members paying ₹299 annually for 20% discounts. The math was attractive—₹6 crores in upfront cash, 25% higher lifetime values, 50% better retention. But scaling beyond early adopters proved difficult. Indian consumers remained transactional, unwilling to commit to beauty subscriptions the way they did for streaming services.

Inventory management was where the model nearly broke. The combination of 500+ SKUs, multiple channels, and seasonal demand created complexity that algorithms couldn't fully solve. The company maintained 45 days of inventory, but mismatches were common. Sunscreen sold out in summer while face wash accumulated. The write-offs—₹25 crores in FY23—were painful reminders that bytes and atoms operated by different rules.

The technology infrastructure, built for digital-first operations, struggled with offline requirements. The ERP system designed for D2C couldn't handle distributor hierarchies. The demand forecasting models trained on online data failed to predict offline patterns. The company spent ₹50 crores in FY24 just integrating systems—a hidden tax on omnichannel ambitions.

Competition revealed the model's ultimate test. When Himalaya launched a digital-first sub-brand with 20% lower prices, Honasa faced an impossible choice: match prices and destroy margins, or maintain prices and lose share. They chose a third path—loyalty programs and bundling—but it only delayed the reckoning. Price competition in beauty was inevitable; the only question was when margins would compress to FMCG norms.

The international expansion failure provided sobering lessons. The unit economics that worked in India—where digital advertising was cheap and labor costs low—collapsed in developed markets. Customer acquisition in Singapore cost ₹2,000. Fulfillment in Dubai cost 5x India rates. The model wasn't portable; it was specifically adapted to India's unique combination of digital penetration, price sensitivity, and demographic dividend.

For the nine-month period ending December 2024, revenue reached ₹1,533.3 crore, reflecting 5.8% year-on-year increase, though adjusting for inventory correction, revenue stood at ₹1,596 crore, marking 10.2% growth. The numbers suggested stability but not the explosive growth that justified premium valuations.

The debt-free status, initially a badge of honor, became a strategic question. With interest rates at historic lows, leverage could have accelerated growth or funded manufacturing facilities. But the founders' conservatism—rooted in middle-class values—prevented what might have been value-accretive financial engineering.

The ultimate question remained unanswered: Was this a transitional business model, bridging analog and digital eras, or a sustainable new paradigm? The margins suggested the former—too thin for traditional retail, too volatile for predictable growth. But the customer relationships suggested the latter—direct, data-rich, and defensible.

The spreadsheet on Ankur's screen updated with Q3 results. CAC down to ₹425. Contribution margin up to 9.5%. Small improvements, but in a business of thin margins, small improvements were the difference between success and failure. The model wasn't broken, but neither was it proven. It existed in that uncomfortable space between innovation and sustainability, where most disruption ultimately lives or dies.

IX. Power & Competitive Moats

The question hung in the Bangalore conference room like incense smoke: "What exactly is Honasa's moat?" The venture capitalist asking it managed a ₹5,000 crore fund and had seen hundreds of D2C brands claim disruption only to be crushed by incumbents. Varun's answer would determine whether they participated in the next funding round.

"Our moat isn't one thing," Varun began, pulling up a slide titled 'The Honasa Flywheel.' "It's the compounding effect of multiple small advantages that become insurmountable when combined."

The first claimed advantage was data, but the reality was nuanced. Honasa knew the purchase history of 2 million customers, their browsing patterns, cart abandonments, and review sentiments. They could predict with 73% accuracy which customer would churn and 67% accuracy what product they'd buy next. But HUL had data on 100 million customers through retail partnerships. The question wasn't who had more data but who could act on it faster.

The community moat seemed stronger. The 50,000-member Mamaearth Moms Facebook group, the 200,000 Instagram followers, the WhatsApp broadcast lists reaching 500,000 parents—these weren't just marketing channels but trust networks. When a mother posted about her baby's rash clearing after using Mamaearth, it carried more weight than any advertisement. But communities were fickle. The same network that built the brand could destroy it with one viral complaint.

Speed-to-market was tangible. Honasa could identify a trend on social media, develop a product, and launch within 45 days. When "glass skin" became a Korean beauty trend, Honasa had a serum in market before L'Oreal had finished consumer research. But this advantage was eroding. HUL had created "speed teams" that operated outside normal bureaucracy. P&G partnered with contract manufacturers to match Honasa's agility. The window was closing.

The portfolio effect created defensive depth. A customer acquired for Mamaearth baby products could be retained through The Derma Co. for teenage acne, Aqualogica for sun protection, and Dr. Sheth's for anti-aging. The lifetime value extended across decades, not years. But managing multiple brands diluted focus and increased complexity. Each brand needed its own positioning, inventory, and marketing—coordination costs that scaled faster than synergies.

Digital-native DNA was both power and prison. Every Honasa employee understood attribution models, conversion funnels, and cohort analysis. Traditional companies hired digital talent but struggled with cultural integration. A HUL marketer thought in television rating points; a Honasa marketer thought in cost-per-click. But being digital-native also meant weakness in traditional retail—the relationships, intuitions, and unwritten rules that governed 75% of beauty sales.

The founder brand provided differentiation but also dependency. Ghazal's story—mother turned entrepreneur—resonated with target customers who saw themselves in her journey. Her Instagram posts about balancing business and family generated engagement that money couldn't buy. But founder dependency was dangerous. What happened when Ghazal stepped back? Could the brand survive without its origin story?

Price positioning occupied an interesting space. Honasa products were 20-30% premium to mass market but 40-50% discount to premium brands. This "masstige" positioning captured aspiring middle-class consumers who wanted better than Dabur but couldn't afford Forest Essentials. But this segment was exactly where every brand wanted to be, making it the most competitive price point in Indian beauty.

The balance sheet provided unexpected power. Being debt-free meant Honasa could weather downturns without covenant pressures. They could invest counter-cyclically, buying distressed brands or hiring talent when competitors retrenched. But it also meant missing opportunities that leverage could have enabled. The conservative capital structure was both shield and shackle.

Network effects, the holy grail of digital businesses, remained elusive. Unlike platforms where each user made the product better for others, Honasa customers didn't directly benefit from network growth. The communities created weak network effects—more members meant more reviews and recommendations—but nothing like the exponential value creation of true platforms.

Regulatory advantages emerged unexpectedly. Honasa's early investment in certifications—Made Safe, Ecocert, dermatologically tested—created barriers competitors struggled to match. Getting Made Safe certification took 18 months and ₹50 lakhs per product. For a company with 500 SKUs, this meant ₹25 crores and years of lead time—a moat built from bureaucracy.

But the ultimate test of power was pricing ability, and here the evidence was mixed. Honasa had raised prices 8-12% annually, above inflation but below premium brands' 15-20% increases. Volume declined 5% with each 10% price increase, suggesting moderate but not strong pricing power. Customers valued the brand but not unconditionally.

The venture capitalist interrupted: "So you're saying you have lots of small moats but no castle wall?"

Varun smiled. "We're saying the age of castle walls is over. Modern competition is about adaptability, not fortification. Our moat is our ability to build new moats faster than competitors can cross old ones."

It was a clever answer but also an admission. Honasa didn't have the distribution dominance of HUL, the innovation engine of L'Oreal, or the heritage of Forest Essentials. What it had was agility, data, and deep understanding of digital-native consumers. Whether these advantages would compound into lasting power or erode under competitive pressure remained the billion-dollar question.

The meeting ended without commitment. The venture capitalist needed to "discuss with partners," corporate speak for uncertainty. As they left, one associate whispered to another: "Great execution, unclear defensibility."

That assessment—great execution, unclear defensibility—captured Honasa's strategic position perfectly. They had built something impressive through superior tactics and timing. Whether tactical advantage could transform into strategic power would determine if Honasa became India's Estée Lauder or another footnote in D2C history.

X. Bear & Bull Cases

The Goldman Sachs equity research floor in Mumbai buzzed with debate in February 2025. Two analysts, Priya (the bear) and Arjun (the bull), were preparing opposing recommendations on Honasa Consumer. Their debate would influence institutional investors controlling ₹50,000 crores in assets.

The Bear Case: A House of Cards

Priya pulled up her first slide: Customer Acquisition Economics. "The math doesn't work long-term," she began. "CAC has risen from ₹250 in 2019 to ₹487 today. It's approaching first order value of ₹680. When CAC equals AOV, the model breaks."

Her analysis was thorough. Digital advertising costs were inflating 20-25% annually as more brands competed for the same eyeballs. Meanwhile, iOS privacy changes and cookie deprecation would make targeting less effective, pushing CAC higher. She projected CAC would hit ₹750 by 2027, making customer acquisition unprofitable even considering lifetime value.

"Look at the cohort data," Priya continued. "Month-12 retention is 18%. That means 82% of customers never become profitable. The entire business depends on finding that 18%, but as the market saturates, that percentage will shrink, not grow."

The competitive dynamics were equally concerning. With promoter holding at just 35%, founders lacked the control to make long-term decisions that might hurt short-term results. Every quarter would be scrutinized, forcing management to optimize for immediate metrics rather than sustainable growth.

"HUL has launched fifteen digital-first brands in the last two years," Priya noted. "They're copying Honasa's playbook but with 100x the resources. P&G India increased digital spending by 200%. The arbitrage opportunity that Honasa exploited—traditional players ignoring digital—no longer exists."

The brand portfolio strategy looked increasingly fragile. Managing six brands meant six times the complexity but not six times the value. Each brand cannibalized others—a Derma Co. customer was a lost Mamaearth customer. The overhead costs of maintaining multiple brands would eventually force consolidation, destroying the portfolio value thesis.

The offline expansion was destroying margins without delivering proportional growth. General trade demanded 40-45% margins versus 25% for D2C. Inventory requirements for 200,000 stores meant working capital would turn positive, eliminating the cash flow advantage. The company was essentially becoming the traditional retailer it had disrupted.

"The IPO valuation was based on 30% growth and expanding margins," Priya concluded. But actual growth is now 5.8% year-on-year, and margins are compressing. The market has already corrected 40%, but there's another 30% downside to reach fair value of ₹200 per share."

The Bull Case: The Digital Transformation Play

Arjun's counter-argument started with market structure. "India's beauty market is ₹80,000 crores and growing 15% annually. Honasa has less than 3% share. Even maintaining share in a growing market means doubling revenue by 2028."

The demographic tailwind was undeniable. 65% of India's population was under 35, digitally native, and entering prime consumption years. Beauty spend per capita was $8 in India versus $80 in China and $300 in the US. As incomes rose, beauty consumption would explode, and digital-first brands were best positioned to capture this growth.

"The bear case assumes CAC keeps rising linearly," Arjun argued. "But Honasa is already adapting." The company had reduced digital ad dependency by 15%, shifting to influencer marketing and traditional media. The subscription program, loyalty initiatives, and referral incentives were reducing effective CAC. He projected CAC would stabilize at ₹500-550, maintaining unit economics.

Mamaearth's position as the third-largest skincare brand in India proved execution capability. In a market with 5,000 beauty brands, achieving top-three status in seven years demonstrated something special—whether product quality, marketing effectiveness, or brand resonance.

The offline expansion, while margin-dilutive short-term, was strategically essential. 70% of beauty purchases still happened offline. The 22% year-on-year expansion to 216,000 outlets created a physical moat that pure-digital players couldn't match. Once established in retail, displacement was difficult—shelf space was finite and switching costs high.

"The portfolio strategy is misunderstood," Arjun continued. "It's not about managing six brands but about owning customer segments." Mamaearth owned mothers, Derma Co. owned millennials, Aqualogica owned sun protection. Each brand was a call option on its segment's growth. Even if half failed, the winners would compensate.

The technology infrastructure was years ahead of traditional competitors. Honasa's data models, attribution systems, and automated marketing platforms couldn't be replicated by simply hiring digital talent. This was organizational capability built over years, not quarters.

Recent results showed resilience: EBITDA margins of 5% and gross margins improving to 72%. Management had proven they could optimize when necessary. The loss in Q2 was due to one-time distribution transition costs, not structural issues.

"At current valuations, the market is pricing in failure," Arjun concluded. "₹280 per share implies zero growth and margin compression. Any positive surprise—a successful new brand, international breakthrough, or acquisition—could drive 50% upside. The risk-reward is asymmetric."

The Verdict

The debate crystallized the fundamental question: Was Honasa a temporary arbitrage play or a permanent disruptor? Bears saw unsustainable economics propped up by venture capital. Bulls saw early innings of a massive transformation.

Both cases had merit. The bear case rightly identified the fragility of high-CAC models and competitive threats. The bull case correctly highlighted demographic tailwinds and execution track record. The truth, as often, lay somewhere between.

Honasa wasn't going to zero—the brand equity, distribution network, and customer base had real value. But neither was it returning to IPO valuations without fundamental improvement in unit economics or dramatic market share gains. It would likely muddle through, generating modest returns for patient investors but disappointing those expecting venture-scale outcomes.

The real lesson was about market evolution. Honasa had brilliantly exploited a moment when digital disruption was possible but traditional players hadn't responded. That moment was ending. The future belonged not to pure-digital or pure-traditional players but to hybrids that combined both capabilities. Whether Honasa could evolve from disruptor to incumbent would determine its ultimate fate.

XI. Lessons & Takeaways

The Harvard Business School case study on Honasa Consumer, published in early 2025, became required reading for entrepreneurship courses worldwide. Not because Honasa was an unqualified success, but because it crystallized the challenges of building consumer brands in the digital age. The lessons extracted from their journey would influence a generation of founders.

Founder-Market Fit Trumps Everything

The Alaghs succeeded where others failed not because they were better operators but because they were authentic representatives of their target market. Ghazal wasn't playing a mother concerned about baby products; she was one. This authenticity resonated in every customer interaction, from product development to marketing messages.

But founder-market fit had a dark side. As the company scaled beyond baby products into skincare and cosmetics, the authenticity diluted. Ghazal couldn't credibly represent every customer segment. The attempt to be everything to everyone weakened the core narrative that had built the brand.

The lesson: Founder authenticity is powerful but doesn't scale infinitely. Companies must decide whether to remain niche and authentic or grow and gradually transfer trust from founders to institution.

Community Building vs. Customer Acquisition

Honasa's early success came from building communities, not acquiring customers. The distinction mattered. Communities were self-reinforcing—members recruited other members, created content, and provided support. Customers were transactional—they bought and left.

But communities couldn't be manufactured. Honasa's attempt to replicate the Mamaearth mother's community for other brands failed. The Derma Co. Facebook group had 50,000 members but minimal engagement. Aqualogica's Instagram generated likes but not loyalty. Communities formed around shared identity and values, not products.

The lesson: Build communities before products. Once you have customers trying to convert them to community members rarely works. But communities that organically adopt products become powerful distribution engines.

The Capital Efficiency Paradox

Honasa raised relatively little capital—₹500 crores pre-IPO versus billions for comparable US brands. This capital efficiency forced creativity, leading to innovations like negative working capital and asset-light manufacturing. Constraints bred innovation.

But capital efficiency also meant under-investment in crucial areas. Brand building required sustained spending over years. Technology infrastructure needed upfront investment. International expansion demanded patient capital. By optimizing for efficiency, Honasa may have sacrificed scale.

The lesson: Capital efficiency is valuable but not virtuous in itself. Some opportunities require aggressive investment. The key is knowing when to be efficient and when to be aggressive—a judgment call that determines startup fate.

Digital-First Doesn't Mean Digital-Only

Honasa's journey proved that starting digital was smart but staying digital was limiting. The expansion to 216,000 retail outlets was necessary for scale but diluted the digital-first advantage. The company became what it had disrupted—a traditional retailer with digital capabilities.

The integration was harder than expected. Digital and offline required different skills, systems, and strategies. Inventory that turned in days online sat for weeks offline. Pricing that worked on the website failed in stores where competitors sat adjacent. The omnichannel promise proved easier to articulate than execute.

The lesson: Digital-first is a go-to-market strategy, not a permanent business model. Eventually, companies must serve customers wherever they shop. The challenge is maintaining differentiation while adopting traditional channels.

The Purpose-Profit Tension

Honasa built its brand on purpose—safe products for babies, clean beauty for conscious consumers. This purpose attracted customers willing to pay premiums for aligned values. But purpose and profit increasingly conflicted.

Manufacturing truly natural products cost more than synthetic alternatives. Sustainable packaging reduced margins. Ethical sourcing limited supplier options. Every purpose-driven decision had profit implications. As public company pressure intensified, purpose gradually gave way to pragmatism.

The lesson: Purpose drives differentiation but costs money. Companies must decide whether purpose is core to strategy or marketing decoration. Consumers can sense the difference, and authenticity has value—but that value has limits.

Building in Public: Asset or Liability?

The Alaghs built Honasa transparently—sharing struggles, celebrating wins, admitting mistakes. This transparency built trust and community. Customers felt like participants, not purchasers. The founder's accessibility humanized the brand.

But transparency became a burden post-IPO. Every decision was scrutinized. LinkedIn posts were parsed for hidden meanings. The quarterly earnings cycle forced short-term thinking. The same transparency that built the brand now constrained strategic flexibility.

The lesson: Transparency is powerful for building but problematic for optimizing. Startups benefit from radical openness; public companies require strategic opacity. Managing this transition determines whether founder-led companies survive public markets.

The Platform Paradox

Honasa conceived itself as a platform for launching brands, not a single brand company. This platform thinking enabled rapid expansion but also created complexity. Each brand needed unique positioning but shared infrastructure. The economics worked in spreadsheets but struggled in reality.

The platform approach assumed capabilities were transferable—that knowing how to build one digital brand meant you could build any digital brand. But beauty consumers weren't monolithic. What worked for mothers didn't work for teenagers. Each segment required deep understanding, not surface pattern matching.

The lesson: Platforms require standardization; brands require differentiation. The tension between efficiency and uniqueness is irreconcilable. Companies must choose: be a platform that enables others or a brand that stands for something specific.

Speed vs. Sustainability

Honasa's ability to launch products in 45 days was remarkable. But speed came at a cost. Quality issues emerged. Inventory piled up. SKU proliferation confused customers. The very agility that enabled disruption became a liability at scale.

Slowing down felt like death in startup culture, but sustainable growth required patience. Building brand equity took years, not quarters. Customer loyalty developed through consistency, not novelty. The market rewarded growth until it didn't, then punished its absence.

The lesson: Speed is a tactic, not a strategy. Knowing when to accelerate and when to consolidate separates successful companies from failed experiments. The transition from sprinting to marathoning determines long-term survival.

The Ultimate Question

As the case study concluded, it posed a question that resonated beyond Honasa: In an age where distribution barriers have fallen and capital is abundant, what creates lasting value in consumer businesses?

Honasa's journey suggested the answer wasn't technology, capital, or even brand. It was the ability to continuously earn customer trust in an environment where trust was increasingly scarce. Whether through product quality, founder authenticity, or community connection, trust was the ultimate moat.

But trust was also fragile. One bad product, one tone-deaf communication, one quarter of missed expectations could destroy years of relationship building. The digital age had democratized company building but also amplified the consequences of mistakes.

The Honasa story wasn't finished. Whether it became India's first global beauty brand or another cautionary tale about D2C excess remained to be written. But the lessons from its journey—about authenticity, community, purpose, and trust—would influence entrepreneurs long after the stock price was forgotten.

XII. Recent News & Current State

The boardroom at Honasa's Gurgaon headquarters in August 2025 reflects a company in transition. The stock ticker on the wall shows ₹284.60, still 12% below IPO price nearly two years after listing. But the atmosphere isn't one of crisis—it's of methodical recalibration.

The Legal Overhang

The Dubai court saga with former distributor RSM General Trading continues to cast a shadow. RSM secured a ruling for AED 25.07 million (around INR 57 crores) in damages for alleged unlawful termination of their distributorship agreement. While the Delhi High Court granted an anti-enforcement injunction against the execution proceedings in Dubai, the dispute highlights the complexities of international expansion that Honasa underestimated.

The company maintains that it does not own any assets in the UAE, limiting enforcement options. But the reputational damage lingers. Every quarterly call includes questions about legal provisions, and the uncertainty weighs on institutional investor sentiment.

Operational Transformation

The numbers tell a story of stabilization rather than stellar growth. Honasa reported its highest-ever Q1 revenue of ₹595 crores and profit of ₹41 crores with a 7.7% EBITDA margin in FY26. But the journey has been volatile—the company posted a net profit of Rs 26 crore in Q3 FY25, unchanged from the same period last year, but a sharp recovery from a loss of Rs 24.3 crore in Q2 FY25.

The distribution overhaul under Project Neev has been both necessary and painful. The company took a Rs 70 crore hit in the quarter as it revamped its offline business model, shifting from supplying to super stockists to dealing directly with distributors. But the long-term benefits are emerging: The company expanded its distribution network by 22% year-on-year, reaching over 2.16 lakh FMCG retail outlets as of December 2024.

Strategic Refinements

The scattershot approach of launching hundreds of products has given way to focused execution. "Our gross margin improved by 200 basis points this quarter, reaching 72%, primarily due to better sourcing and optimized ad spends," Alagh explained. The company reduced its digital ad dependency by 15%, shifting towards influencer marketing and traditional media for more sustainable brand recall.

Market Perception

The stock market remains skeptical. With a market cap of ₹9,089 crores, down 40.5% in one year, investors are pricing in continued challenges. The stock has experienced varied returns, with a notable year-to-date return of 12.53%, contrasting with a one-year decline of 38.71%.

Brokerage opinions reflect this uncertainty. Emkay Global reduced the target price by 50% to INR 300 from INR 600, citing weak Q2 FY25 results and challenges in revenue growth and margins. The consensus seems to be that while the business isn't broken, the premium valuation is no longer justified.

Leadership Changes

The organizational churn continues with key departures and appointments. Honasa Consumer appointed Yatish Bhargava as Chief Business Officer to enhance its omnichannel strategy. These changes signal a shift from founder-driven to professional management, necessary for scale but potentially diluting the authentic voice that built the brand.

The Sustainability Question

Beyond financial metrics, Honasa is attempting to build credibility through impact initiatives. The "Plant Goodness Initiative" promotes afforestation, "Young Scientists" instills climate change understanding among school children, "Fresh Water for All" provides clean water access to rural areas, and "BBlunt Shine Academy" empowers women through vocational training. Whether these initiatives translate to brand loyalty remains uncertain.

The Path Forward

The recent performance suggests Honasa is finding its footing as a public company. For the nine-month period ending December 2024, revenue reached Rs 1,533.3 crore, reflecting a 5.8% year-on-year increase, or Rs 1,596 crore marking 10.2% growth when adjusted for inventory correction.

But the fundamental questions remain unanswered. Can a digital-first brand maintain its differentiation as it scales through traditional channels? Will the multi-brand strategy create lasting value or dilute focus? Can the company reduce marketing dependence without sacrificing growth?

The market has rendered its verdict through the stock price—Honasa is a decent business trading at a fair valuation, not the revolutionary disruptor worth premium multiples. The company that promised to reinvent beauty retail has become what it disrupted: a traditional FMCG company with better digital capabilities.