AutoZone: From Auto Shack to America's Parts Powerhouse

I. Introduction & Episode Roadmap

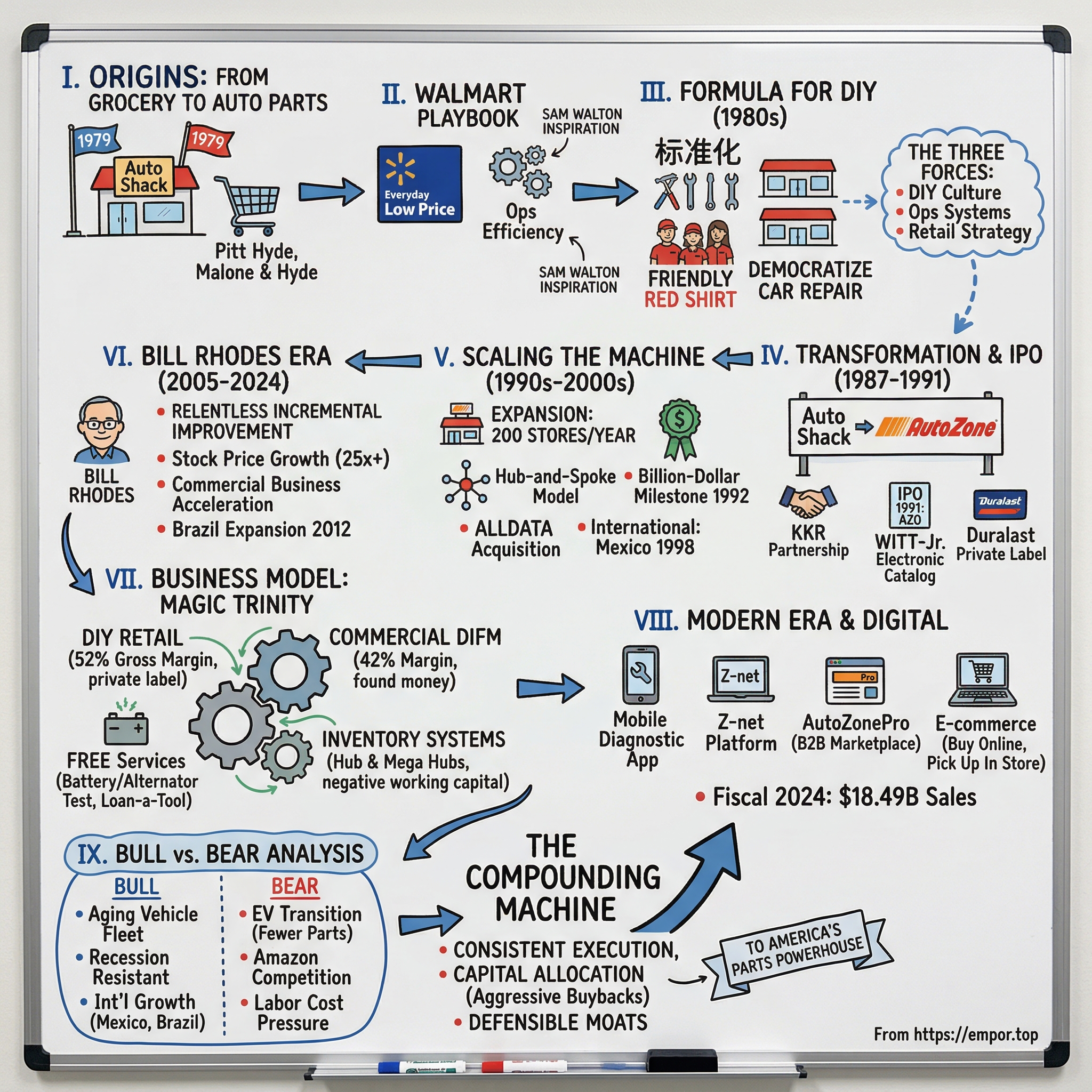

Picture this: It's a sweltering July 4th, 1979, in Forrest City, Arkansas. While most Americans are lighting fireworks and grilling burgers, Doc Crain is unlocking the doors to a 6,000-square-foot store called Auto Shack. The shelves are stocked with alternators, brake pads, and motor oil. By day's end, he'll ring up exactly $300 in sales—hardly the stuff of retail legend. Yet this modest opening would mark the birth of what would become AutoZone, today's $60 billion automotive parts empire with over 7,140 stores spanning from Alaska to Brazil.

The central question isn't just how a grocery wholesaler's experimental side project transformed into America's largest aftermarket automotive parts retailer. It's how AutoZone cracked the code on something deceptively complex: turning the mundane necessity of car maintenance into a repeatable, scalable, wildly profitable retail formula. While competitors focused on professional mechanics or tried to be everything to everyone, AutoZone bet on a different thesis—that millions of Americans would fix their own cars if given the right tools, parts, and crucially, the confidence to do it.

This is a story about more than retail execution. It's about understanding cultural shifts before they happen—recognizing that the DIY movement wasn't just about saving money but about American self-reliance. It's about operational excellence that would make even Toyota engineers jealous. And it's about the paradox of building a tech-forward business that still wins because a human in a red shirt can tell you exactly which alternator fits your 2003 Honda Civic.

What unfolds is a masterclass in category creation and dominance. You'll discover how a Memphis grocery dynasty applied Walmart's playbook to auto parts, why giving away services for free became a profit center, and how aggressive financial engineering turned a commodity retailer into one of the stock market's greatest compounders. Along the way, we'll explore the three forces that shaped AutoZone's ascent: the DIY culture boom of the 1980s, the operational systems that created competitive moats, and the focused retail strategy that resisted every temptation to diversify.

For investors and operators alike, AutoZone offers profound lessons about building defensible positions in unglamorous markets, the compounding power of consistent execution, and why sometimes the best business model is the one that looks boring from the outside. Because while Silicon Valley was chasing the next big disruption, AutoZone was quietly printing money by helping Americans keep their aging cars running—one brake pad at a time.

II. The Malone & Hyde Origins: A Grocery Empire's Auto Dreams

The AutoZone story doesn't begin in an auto shop or a Detroit boardroom. It starts in the wood-paneled offices of Malone & Hyde, a Memphis wholesale grocery empire that by the late 1970s was supplying over 2,000 supermarkets across the South. The company's chairman, J.R. "Pitt" Hyde III, was a third-generation grocery man who'd grown up stocking shelves and understood retail in his bones. But in 1978, something shifted his perspective entirely.

That year, Hyde joined the board of a small Arkansas retailer called Walmart. Sam Walton was revolutionizing retail with everyday low prices, sophisticated logistics, and a fanatical focus on operational efficiency. Hyde watched Walton turn discount retail from a race-to-the-bottom commodity business into a precision machine. The lessons were intoxicating: control your supply chain, systematize everything, and treat store operations like a science experiment where you're constantly testing and refining.

Back in Memphis, Hyde couldn't shake a nagging thought. Malone & Hyde was successful but vulnerable—grocery wholesaling was consolidating, margins were shrinking, and the company needed diversification. Hyde began studying different retail sectors with the analytical rigor of a McKinsey consultant. Electronics? Too volatile. Clothing? Too fashion-dependent. Then he noticed something interesting about automotive aftermarket parts: steady demand, minimal fashion risk, and fragmentation so extreme that no single player controlled even 2% of the market.

The auto parts industry in 1978 was a sleepy backwater dominated by mom-and-pop stores and wholesale jobbers who'd operated the same way since the 1950s. Store owners kept catalogs the size of phone books, inventory management meant walking the aisles with a clipboard, and customer service often amounted to gruff mechanics telling weekend warriors they were in over their heads. Hyde saw opportunity in this dysfunction—what if someone applied modern retail principles to this antiquated industry?

Hyde assembled a small team and gave them a mission: create an auto parts concept that would do for car maintenance what McDonald's did for hamburgers—standardize it, systematize it, and scale it. They spent months visiting auto parts stores across the country, taking notes on everything from store layouts to customer interactions. What they found confirmed Hyde's thesis: the industry was ripe for disruption. Stores were dark, cluttered, and intimidating. Inventory was haphazard. Pricing was opaque. Most importantly, nobody was really serving the emerging DIY customer who wanted to fix their own car but needed help figuring out how.

The first Auto Shack store represented Hyde's attempt to reimagine the auto parts store from first principles. Instead of dingy warehouses, the stores would be bright and welcoming. Instead of surly mechanics, friendly staff would offer free advice. Instead of hunting through catalogs, customers could quickly find what they needed. And borrowing directly from Walmart's playbook, prices would be consistently low rather than relying on weekly specials and promotions.

When Doc Crain opened that first store on July 4, 1979, he was implementing a radical experiment. The store carried 3,000 SKUs—a fraction of what traditional parts stores stocked—but they were the parts that moved fastest. The layout was logical: batteries up front where customers expected them, fluids and filters in the middle, hard parts in the back. Most revolutionary of all, prices were clearly marked and non-negotiable. In an industry where haggling was standard, this was heresy.

That first day's $300 in sales wouldn't impress anyone, but Hyde saw something others missed. Customers weren't just buying parts; they were asking questions, seeking advice, treating the store as a resource rather than just a transaction point. One customer bought brake pads and spent 20 minutes getting instructions on how to install them. Another came in for oil but left with a complete tune-up kit after talking to Crain about his car's symptoms. This wasn't just retail—it was retail plus education, and that combination would prove magical.

Within months, the Forrest City store was exceeding projections. More importantly, it was attracting a different customer than traditional parts stores—younger, less experienced, but eager to learn. These weren't professional mechanics or car enthusiasts; they were regular people trying to save money by doing their own maintenance. Hyde had found his market, and it was bigger than anyone imagined. The grocery king had discovered his next empire, and it would be built not on food, but on America's other essential need: keeping their cars running.

III. The Auto Shack Years: Finding the Formula (1979–1987)

By 1981, Auto Shack had grown to 31 stores across Arkansas, Tennessee, and Mississippi, but the real action was happening inside each location. Store managers were conducting thousands of tiny experiments—which products to stock, how to train employees, what services to offer for free. The company was less a traditional retailer and more a learning laboratory, with each store feeding insights back to Memphis headquarters.

The early 1980s provided the perfect tailwind. The oil crisis had made fuel-efficient cars popular, but it also meant Americans were keeping their existing vehicles longer. The average car age increased from 5.7 years in 1970 to 7.6 years by 1985. Simultaneously, a DIY movement was sweeping America—This Old House premiered on PBS, Home Depot was expanding rapidly, and fixing things yourself became not just economical but culturally cool. Auto Shack was perfectly positioned to ride both waves.

The company's real innovation wasn't products but process. While competitors operated each store like an independent kingdom, Auto Shack standardized everything. Store layouts were identical—a customer could walk into any location and find oil filters in the exact same spot. Employee training followed a strict curriculum that emphasized customer service over technical knowledge. The philosophy was simple: hire friendly people and teach them about cars, rather than hire car experts and hope they're friendly.

This approach created some memorable moments. In 1983, a store manager in Jackson, Mississippi, noticed customers struggling with battery installation. Without asking permission, he started installing batteries for free in the parking lot. Word spread to Memphis, and within six months, free battery installation was standard at every Auto Shack. The service cost virtually nothing—it took five minutes and required just a wrench—but it transformed customer relationships. Suddenly, Auto Shack wasn't just selling batteries; it was solving problems.

The competition initially dismissed Auto Shack as amateur hour. Traditional parts stores served professional mechanics who knew exactly what they needed and valued depth of inventory over customer service. NAPA, Genuine Parts, and Carquest had sewn up the professional market with credit accounts, daily delivery, and vast catalogs. But Hyde wasn't trying to compete for professional mechanics—he was creating an entirely new market segment.

By 1985, the formula was crystallizing. Stores averaged 6,500 square feet, carried 12,000 SKUs, and generated roughly $1.2 million in annual sales. The economics were compelling: 38% gross margins, 8% operating margins, and inventory turns of 3.2x annually—significantly better than traditional parts stores. More importantly, same-store sales were growing 8-10% annually as customers discovered they could actually maintain their own vehicles.

The cultural element proved as important as the financial metrics. Auto Shack developed an almost missionary zeal about democratizing car repair. Employee training manuals from this era read less like retail operations guides and more like manifestos about empowering everyday Americans. Store managers were encouraged to host Saturday morning clinics on basic maintenance. Some locations partnered with high schools to teach students about cars. This wasn't corporate PR—it was building a customer base from scratch.

Competition began taking notice by 1986 when Auto Shack crossed 100 stores and approached $150 million in revenue. Sears launched a standalone auto parts concept. Western Auto tried modernizing stores. Regional chains began copying the bright, clean store format. But they missed the secret sauce—Auto Shack wasn't just selling parts; it was selling confidence. Every free service, every patient explanation, every successful DIY repair created a customer for life.

The limitations of the "Auto Shack" name became apparent as expansion accelerated. The name suggested discount, even shabby—fine for rural Arkansas, problematic for suburban expansion. Plus, Radio Shack's lawyers were making uncomfortable noises about trademark infringement. Hyde knew the company needed a rebrand that reflected its evolution from scrappy startup to serious retail player. The stage was set for transformation, both in name and ambition.

IV. The AutoZone Transformation & IPO (1987–1991)

The year 1987 marked a pivot so dramatic that employees later referred to it as "the revolution." Hyde made two bold moves simultaneously: he divested every division of Malone & Hyde except Auto Shack—selling off the grocery business his family had built over generations—and rebranded the entire chain as AutoZone. The new name suggested authority, completeness, a destination rather than just a store. The logo—a bold red and yellow sunrise—promised a new day in auto parts retail. The transformation wasn't just cosmetic. Hyde brought in Kohlberg Kravis Roberts (KKR), the legendary leveraged buyout firm, as majority partner in 1985. KKR's involvement brought Wall Street discipline to what had been a family business. They instituted rigorous financial controls, demanding 20% annual returns and pushing for rapid expansion. But more importantly, KKR brought credibility—suddenly AutoZone wasn't just a regional parts chain but a serious player backed by the firm that would later engineer the RJR Nabisco takeover.

The real breakthrough came with technology. In 1987, AutoZone introduced WITT-Jr. (What It Takes To Do The Job Right Jr.), the industry's first electronic catalog system. While competitors still flipped through paper catalogs the size of phone books, AutoZone employees could instantly look up any part, check inventory across the network, and access warranty information. Customers were amazed—what used to take 20 minutes now took 20 seconds. The company introduced an electronic catalog used to look up parts, check warranties, and view inventory.

June 1988 marked another defining moment with the launch of Duralast, AutoZone's private label brand. The timing was perfect—consumer trust in store brands was rising, and AutoZone needed better margins to fund expansion. Duralast batteries promised three-year free replacement warranties when competitors offered one year. The brand would eventually expand to brake pads, alternators, and dozens of other categories, becoming synonymous with quality and value in the DIY market.

The symbolic importance of July 4, 1989, can't be overstated. Exactly ten years after opening that first store in Forrest City, AutoZone celebrated its 500th location. Hyde threw a company-wide party, flying in store managers from across the country. The message was clear: this wasn't just about hitting a number but proving that a focused, systematic approach to retail could create exponential growth. In a decade, they'd gone from one store to 500, from $300 in daily sales to over $500 million annually.

In 1991, Hyde and KKR took the company public. Its stock began trading on the New York Stock Exchange using the ticker symbol "AZO." The IPO priced at $27.50 per share on April 1, 1991, with KKR held on to 68% of shares, AutoZone managers received 16%, former managers received 6%, and the final 10% was left for other investors. The offering raised capital for expansion but more importantly validated the model—Wall Street was betting that America's DIY auto repair culture would continue growing.

Behind the financial engineering was operational innovation that competitors couldn't match. The Electronic Store Management System, rolled out in 1991, brought bar-coding and scanning to every location. This wasn't just about faster checkout—it created a real-time data stream showing exactly what was selling, where, and when. Store managers could see their performance metrics updated hourly. Memphis headquarters could spot trends across regions instantly. The company that started with handwritten receipts was now running one of retail's most sophisticated information systems.

By 1991's end, AutoZone operated 596 stores across 16 states with revenues approaching $820 million. In December 1991, AutoZone held its first shareholders' meeting and announced a revenue increase of over 20% to $818 million. Same-store sales grew 12% annually. The company employed 7,500 "AutoZoners"—Hyde insisted on this term rather than employees, building an identity around belonging to something bigger. The transformation from Auto Shack to AutoZone was complete, setting the stage for national dominance.

V. Scaling the Machine: Growth & Systems (1990s–2000s)

The early 1990s at AutoZone resembled a military campaign more than traditional retail expansion. Every Monday morning, the war room at Memphis headquarters buzzed with activity as executives pored over heat maps showing competitor locations, demographic data, and expansion opportunities. The goal was audacious: add 200 stores annually while maintaining operational excellence. This wasn't growth for growth's sake—it was systematic market domination.

The company introduced an electronic Store Management System, allowing for bar-coded prices and faster customer transactions. But the real magic happened when AutoZone connected these systems across stores in 1994, creating one of retail's first real-time inventory networks. A customer in Dallas looking for a specific alternator could know instantly if it was available in Fort Worth. Store managers could transfer inventory between locations with a few keystrokes. What seemed routine by today's standards was revolutionary for auto parts retail.

The billion-dollar milestone came in 1992—not just a round number but a psychological barrier that separated serious retailers from regional players. Sales exceeded $1 billion for the first time in the same year, with the store count reaching 678 and expansion into Wisconsin. AutoZone celebrated by doing something characteristic: they invested the profits right back into technology, launching satellite communications that connected every store to Memphis headquarters. Weather delay in Tennessee? Inventory spike in Texas? Management knew instantly.

The commercial program launch in 1996 represented AutoZone's biggest strategic gamble yet. For years, the company had deliberately ignored professional mechanics, focusing entirely on DIY customers. But data showed a massive untapped market—independent repair shops that needed parts quickly but didn't want to maintain huge inventories. AutoZone's solution was elegant: treat commercial customers like super-DIYers, offering the same prices but adding delivery and credit terms. The 1996 acquisition of ALLDATA for $56.75 million in stock proved transformational beyond its modest price tag. ALLDATA was purchased by AutoZone with the vision of providing the best combination of service, repair information, and parts. ALLDATA gave AutoZone something no competitor possessed: comprehensive OEM repair information that professional mechanics relied on. Now AutoZone could serve both DIY customers in stores and commercial accounts needing technical data. The synergies were immediate—AutoZone's commercial customers got world-class repair information while ALLDATA gained distribution through thousands of stores.

International expansion began modestly but strategically. AutoZone opened its first international store in Nuevo Laredo, Mexico in December 1998, choosing a border town where they could test cross-cultural retail while maintaining supply chain proximity. The Mexico strategy differed from U.S. expansion—stores were smaller, labor was cheaper, and DIY culture was less developed. But AutoZone adapted, emphasizing commercial sales and building relationships with local mechanics who influenced consumer purchases.

The hub-and-spoke model introduced in 2002 revolutionized inventory management. Traditional stores carried 12,000-15,000 SKUs, enough for common repairs but lacking depth for complex jobs. Hub stores, strategically placed in metro areas, carried 40,000+ SKUs and could deliver to satellite stores multiple times daily. This meant a customer in a suburban store could access hub inventory within hours, not days. The model squared the circle—maintaining lean store inventory while offering vast selection.

AutoZone debuted on the Fortune 500 list in 1999, a symbolic moment that validated two decades of growth. But the real achievement was operational: same-day parts availability in most markets, 15-minute average transaction times, and inventory turns approaching 4x annually. Competitors scrambled to copy the hub model, but AutoZone had a five-year head start in site selection, systems integration, and logistics optimization.

By 2004, AutoZone operated 3,219 stores across 48 states with revenues exceeding $5.3 billion. The company had become a machine—opening a new store every 40 hours, generating $1.6 million in average store sales, and maintaining EBITDA margins above 20%. International operations expanded to 49 stores in Mexico, proving the model could travel. Yet the biggest transformation was still ahead, as a new CEO would take AutoZone from successful retailer to one of the stock market's greatest compounding stories.

VI. The Bill Rhodes Era: Operational Excellence (2005–2024)

In 2005, William C. Rhodes III was named president and CEO, marking the beginning of what would become one of the most successful CEO tenures in retail history. Rhodes wasn't an outsider with a turnaround mandate—he'd been with AutoZone since 1994, running stores, managing regions, understanding the business from the ground up. His appointment signaled continuity, but Rhodes had bigger ambitions than just maintaining the status quo.

Rhodes introduced a deceptively simple strategy he called "1TEAM Going the Extra Mile." Behind the corporate speak was a radical idea: what if AutoZone optimized every single aspect of the business by just 1-2% annually? Not revolutionary changes, just relentless incremental improvement. Better inventory placement might save 30 seconds per transaction. Improved delivery routing could cut commercial delivery times by five minutes. Tiny gains that compounded into extraordinary results.

The numbers tell the story: under Rhodes' leadership from 2005 to 2024, AutoZone's stock price increased more than 25 times, from roughly $80 to over $2,000 per share (adjusting for splits). Even more remarkably, AutoZone became one of only a handful of companies to grow both revenue and earnings per share every single year for two decades—through the financial crisis, COVID-19, and multiple recessions. This wasn't luck; it was operational excellence elevated to an art form.

The commercial business acceleration under Rhodes transformed AutoZone from primarily a retail operation to a hybrid retail-wholesale powerhouse. Commercial sales, which were barely 10% of revenue in 2005, grew to over 25% by 2020. Rhodes understood that professional mechanics were influencers—when they recommended AutoZone parts, retail customers followed. The company invested heavily in commercial infrastructure: delivery vehicles, credit systems, dedicated sales teams, and relationship management tools that rivaled any B2B software company.

Technology investments during the Rhodes era weren't flashy but foundational. The Z-net system evolved into a comprehensive platform managing everything from inventory to customer relationships. Mobile apps launched in 2010 weren't just shopping tools but diagnostic assistants—scan a check engine code, and the app would explain the problem and recommend parts. The company spent hundreds of millions on technology, but always with a clear ROI thesis tied to operational efficiency or customer experience.

The mega hub strategy, refined under Rhodes, became AutoZone's secret weapon. By 2019, the company operated 58 mega hubs carrying over 100,000 SKUs each. These weren't just warehouses but precision distribution centers using algorithms to predict part demand down to the store level. A mega hub could serve 150+ stores within a 200-mile radius, with multiple daily deliveries. Competitors tried copying the model but lacked the density to make the economics work.

In June 2007, Bill Rhodes was also made chairman, consolidating leadership as AutoZone navigated the financial crisis. While competitors retrenched, Rhodes accelerated expansion, opening stores in abandoned Circuit City and Borders locations at fire-sale prices. The crisis validated AutoZone's thesis—when times get tough, people fix cars rather than buy new ones. Revenue grew every quarter through the recession, a testament to the business model's resilience.

Brazil expansion in 2012 represented Rhodes' boldest international move. Unlike Mexico, Brazil had no geographic proximity and a completely different automotive market. But Rhodes saw opportunity in Brazil's massive vehicle fleet and underdeveloped parts infrastructure. The expansion was methodical—starting with São Paulo, learning the market, adapting the model. By 2020, Brazil operations were profitable and growing rapidly, proving AutoZone could succeed globally.

The digital transformation under Rhodes was evolutionary, not revolutionary. While pure-play e-commerce companies burned cash chasing growth, AutoZone built digital capabilities that enhanced stores rather than replaced them. Buy online, pick up in store became seamless. Commercial customers could order through apps with delivery tracking. The website became a diagnostic tool, not just a catalog. By 2020, digital influenced over 60% of transactions, even if the final purchase happened in stores.

Capital allocation during the Rhodes era deserves its own business school case study. Between 2005 and 2024, AutoZone repurchased over $25 billion in stock, reducing share count by 75%. Rhodes understood that in a mature industry with consistent cash flow, returning capital to shareholders often beat empire building. The buyback program, combined with operational improvements, created a virtuous cycle—fewer shares meant higher EPS, which supported higher stock prices, which made buybacks more accretive.

Rhodes' final years as CEO focused on succession planning and sustainable growth. Commercial sales accelerated, reaching 30% of revenue. International operations expanded to over 700 stores. The domestic store count surpassed 6,000 locations. Most importantly, the culture of continuous improvement was deeply embedded. When Rhodes transitioned to Executive Chairman in January 2024, with Phil Daniele becoming CEO, he left behind not just a successful company but a self-improving machine built to compound value for decades.

VII. The Business Model: DIY, DIFM, and Inventory Magic

AutoZone's business model appears simple on the surface—buy parts wholesale, sell them retail, repeat. But beneath this simplicity lies one of retail's most sophisticated operating systems, fine-tuned over four decades to extract maximum value from every transaction, every square foot, and every inventory dollar. Understanding how AutoZone makes money requires understanding three interconnected engines: the DIY retail business, the commercial DIFM (Do-It-For-Me) segment, and the inventory management system that powers both.

The DIY business remains AutoZone's foundation, generating roughly 70% of revenue from customers who walk into stores seeking parts for their own repairs. These transactions average $30-40 but carry gross margins approaching 52%—extraordinary for retail. The secret lies in private label penetration. Duralast, AutoZone's flagship brand, commands premium prices despite being a store brand because customers trust its quality and lifetime warranties. When a customer buys a Duralast alternator, AutoZone captures the entire value chain from manufacturing to retail.

The commercial business serves professional mechanics and repair shops, operating on a completely different model. Average tickets run $75-100, but margins are lower—around 42%—because commercial customers demand credit terms and delivery. Yet the economics are compelling: commercial sales require minimal additional store investment beyond delivery vehicles and drivers. A store doing $2 million in retail sales can add $800,000 in commercial revenue using the same inventory, same staff during slow periods, same real estate. It's essentially found money.

The hub and mega hub network represents operational leverage at its finest. A typical store might turn inventory 3.5 times annually. Hub stores, because they're constantly fulfilling transfers to satellite stores, turn inventory 5-6 times. Mega hubs, serving hundreds of stores, can turn inventory 8-10 times. This velocity means AutoZone can carry vast selection—over 110,000 unique SKUs across the network—while maintaining industry-leading return on invested capital.

Free services represent AutoZone's most counterintuitive profit driver. Battery testing, alternator testing, code reading, and the famous Loan-a-Tool program all cost money to provide but generate zero direct revenue. Yet these services are the cornerstone of customer acquisition and retention. A customer who gets a free battery test is 70% likely to buy a battery if it fails. Someone who borrows a tool successfully completes their repair and returns for oil, filters, and other maintenance items. The lifetime value of these customers dwarfs the service costs.

The Loan-a-Tool program deserves special attention as a masterpiece of customer psychology. Customers deposit the full tool purchase price, which is refunded upon return. Most customers return tools, but AutoZone wins either way. If tools aren't returned, AutoZone sells a tool at full margin. If they are returned, AutoZone has created a loyal customer who successfully completed a repair and will return for future parts. The program essentially offers free tool rental funded by customer float—brilliant financial engineering disguised as customer service.

Private label economics transformed AutoZone from retailer to quasi-manufacturer. Duralast products, sourced primarily from Asian manufacturers to AutoZone specifications, generate margins 10-15 percentage points higher than national brands. Customers pay premium prices because Duralast offers lifetime warranties that national brands don't match. When a Duralast part fails under warranty, AutoZone's cost is just the wholesale price, but the customer becomes even more loyal because the warranty was honored without question.

Supply chain relationships, built over decades, create a hidden moat. AutoZone's scale allows it to bypass distributors and buy directly from manufacturers, capturing additional margin. Payment terms negotiated during flush times—often 60-90 days—mean AutoZone sells inventory before paying for it, generating negative working capital. Vendors accept these terms because AutoZone represents 10-20% of their business and pays reliably. New entrants can't replicate these relationships or terms without similar scale.

The partnership with St. Jude Children's Research Hospital, running since 1998, exemplifies how community involvement drives business results. AutoZone has raised over $30 million for St. Jude, but the real value is employee engagement and customer perception. AutoZoners feel proud working for a company that supports children's health. Customers choose AutoZone over competitors partially because of this association. It's corporate social responsibility that directly impacts same-store sales.

Data and analytics capabilities, built quietly over decades, rival any tech company. AutoZone knows which parts fail when, in which zip codes, on which vehicles. This allows precision inventory management—stores in snow country stock different parts than stores in Phoenix. The system automatically adjusts for local demographics, weather patterns, even regulatory changes. When California mandates new emissions standards, affected stores automatically receive compliant parts before customers ask for them.

The commercial credit program showcases sophisticated financial services within retail operations. AutoZone extends credit to thousands of repair shops, essentially becoming their banker. Terms are typically net-30, but AutoZone's cost of capital is far lower than what shops would pay for traditional financing. This credit becomes switching cost—shops won't change suppliers and lose established credit lines. Bad debt runs less than 1% because AutoZone knows exactly how much each shop sells and can adjust credit limits in real-time.

The economics compound powerfully: 52% gross margins on DIY, 42% on commercial, 3.5x inventory turns, negative working capital, 20%+ ROIC. Add aggressive share buybacks, and you get a financial model that turns steady 4-5% revenue growth into double-digit earnings per share growth. It's not revolutionary—it's the methodical optimization of every aspect of selling auto parts, refined over 45 years into a nearly perfect retail machine.

VIII. Modern Era: Digital, Data, and Dominance (2010s–Today)

The 2010s began with AutoZone facing an existential question: could a traditional retailer survive the digital disruption that had already claimed Borders, Circuit City, and countless others? Amazon was expanding into auto parts. Pure-play digital competitors like RockAuto were growing rapidly. Venture-backed startups promised to revolutionize parts distribution. Yet by 2024, AutoZone had not just survived but thrived, growing revenue to $18.49 billion while maintaining industry-leading margins. The secret wasn't fighting digital but embracing it in distinctly AutoZone fashion. The mobile app, launched in 2010, wasn't trying to replicate Amazon's one-click purchasing. Instead, it became a diagnostic companion. Scan a VIN barcode, get exact part numbers. Input symptoms, receive likely causes. The app drove foot traffic to stores rather than replacing visits. By 2015, over 40% of DIY customers used the app during their repair journey, but 85% still completed purchases in-store where they could ask questions and get free testing.

Fiscal 2024 demonstrated AutoZone's continued momentum with total sales growth of 5.9% while earnings per share increased 13.0%. Revenue reached $18.49 billion, a 5.92% increase from 2023, marking another year of consistent growth. But the real story was margin expansion and operational leverage—growing EPS at twice the rate of sales through disciplined cost management and aggressive buybacks.

The commercial business digital transformation proved even more impactful. AutoZonePro, the B2B platform, gave repair shops Amazon-like convenience with AutoZone's reliability. Shop owners could see real-time inventory across nearby stores, place orders for multiple locations, access repair data through ALLDATA integration, and track delivery vehicles in real-time. By 2020, over 70% of commercial orders originated digitally, though relationships and delivery speed remained the competitive differentiators.

E-commerce evolution at AutoZone defied Silicon Valley orthodoxy. While competitors built massive distribution centers for direct-to-consumer fulfillment, AutoZone turned every store into a mini-fulfillment center. Buy online, pick up in store became the dominant digital transaction method, accounting for over 60% of online orders. This hub-and-spoke approach meant no additional infrastructure investment while maintaining the human interaction DIY customers valued.

The AutoZone Media Network, launched quietly in 2022, represented a new frontier in monetization. With millions of loyalty members and detailed purchase histories, AutoZone knew exactly which customers needed brake pads, when they'd need them, and which brands they preferred. Suppliers paid premium rates to reach these high-intent customers through targeted emails, app notifications, and in-store displays. The network generated over $100 million in high-margin revenue by 2024, essentially pure profit dropping to the bottom line.

Data capabilities evolved from operational tool to competitive weapon. AutoZone's systems tracked over 280 million VINs, knowing the maintenance history and likely future needs of nearly every vehicle in America. This allowed predictive inventory management—stocking parts before customers knew they needed them. When a 2015 Honda Civic hit 60,000 miles, AutoZone stores in that zip code automatically received the spark plugs, filters, and fluids that vehicle would likely need.

Competition with Amazon proved less existential than expected. Amazon struggled with automotive parts' complexity—millions of SKUs, fitment challenges, and customers' need for advice. AutoZone's response was strategic jujitsu: partner where it made sense, compete where they had advantage. AutoZone products appeared on Amazon, but complex repairs requiring diagnosis and installation advice remained AutoZone's domain. The companies weren't really competing for the same transactions.

Domestically, the business faced challenges from deferrals across discretionary merchandise categories, but saw accelerating Commercial sales performance, with international businesses performing well, up roughly 10% on a constant currency basis. This dichotomy—weakness in DIY discretionary spending but strength in commercial and international—showcased the portfolio's resilience.

The competitive landscape shifted dramatically as Advance Auto Parts struggled and consolidated. O'Reilly remained AutoZone's primary rival, but the market was increasingly bifurcating: AutoZone and O'Reilly capturing share at the top, Amazon dominating simple commodity purchases, and everyone else fighting for survival. AutoZone's scale advantages—buying power, distribution efficiency, technology investments—became increasingly insurmountable for smaller players.

Store expansion continued at a measured pace, with 6,364 stores in the U.S., 763 in Mexico and 109 in Brazil for a total store count of 7,236 as of May 4, 2024. The company added 213 net new stores in fiscal 2024, maintaining disciplined growth while focusing on same-store sales and margin expansion. Each new store was profitable within 12 months, generating 20%+ returns on invested capital—remarkable in retail's current environment.

Modern AutoZone represents a paradox: a traditional retailer thriving in the digital age by being selectively digital. The company embraced technology where it enhanced the core value proposition—diagnosis, inventory management, commercial efficiency—while maintaining the human elements that differentiated it. In an era of retail apocalypse, AutoZone proved that execution, consistency, and deep customer understanding could still triumph over disruption.

IX. Playbook: Business & Investing Lessons

AutoZone's four-decade journey from a single Arkansas store to a $60 billion market cap offers a masterclass in building and sustaining competitive advantage in retail. The lessons extend far beyond auto parts, providing a template for category dominance, operational excellence, and long-term value creation that any business can study and adapt.

Category Killer Dynamics: Depth Over Breadth

AutoZone's fundamental insight was that specialization beats diversification in retail. While competitors like Sears and Walmart treated auto parts as one category among many, AutoZone made it their entire world. This focus enabled expertise accumulation—AutoZoners became trusted advisors, not just clerks. The lesson: owning a niche completely beats competing partially in multiple categories. Depth of knowledge, inventory, and service creates moats that breadth can never match.

The Power of Consistent Execution and Compound Growth

AutoZone's financial performance seems almost boring in its consistency—20+ years of consecutive comparable store sales growth, EPS growth every year regardless of economic conditions. But this consistency is the point. Small improvements—1% better inventory turns, 0.5% higher margins, 2% productivity gains—compound into extraordinary results over decades. The company's mantra of "1TEAM Going the Extra Mile" embedded continuous improvement into corporate DNA. For investors, this predictability reduces risk and enables higher valuations.Strong Financial Performance: The Numbers Behind the Magic

For the twelve week periods ended November 23, 2024, and November 18, 2023, net cash flows from operating activities provided $811.8 million and $830.3 million, respectively, demonstrating remarkable cash generation consistency. Annual cash flow from operating activities for 2024 was $3.004 billion, a 2.15% increase from 2023. These aren't just numbers—they represent a business model that converts sales into cash with minimal friction, enabling aggressive capital returns and self-funded growth.

Capital Allocation: Aggressive Share Buybacks and Returns

AutoZone's share repurchase program represents one of the most successful capital allocation strategies in retail history. Since 1998, the company has reduced share count by approximately 89%, turning modest revenue growth into explosive EPS expansion. The math is compelling: 5% revenue growth plus 5% share count reduction equals 10% EPS growth before any operational improvements. This isn't financial engineering masking operational weakness—it's amplifying operational strength.

Building Defensible Moats in Commodity Retail

AutoZone proves that moats exist even in commodity businesses. Their advantages compound: scale enables better purchasing terms, which improves margins, which funds technology investments, which enhances customer experience, which drives volume, which increases scale. Breaking into this virtuous cycle requires massive capital, operational excellence, and decades of relationship building—barriers that pure financial capital can't overcome.

Culture as Competitive Advantage: "AutoZoners" and Customer Service

The "AutoZoner" identity isn't corporate propaganda but genuine cultural differentiation. Employees take pride in helping customers solve problems, not just processing transactions. This manifests in measurable ways: lower turnover (industry-leading retention rates), higher customer satisfaction scores, and employees who become product experts rather than temporary retail workers. Culture can't be copied through consultant reports or management reshuffles—it must be built over decades.

Technology as Enabler, Not Disruptor

AutoZone's technology strategy offers a contrarian lesson: sometimes the best digital strategy is selective digitization. Rather than trying to out-Amazon Amazon, AutoZone digitized what enhanced their core value proposition—inventory management, diagnostic tools, B2B ordering—while maintaining human touchpoints where they mattered. Technology amplified existing advantages rather than replacing the business model.

The Power of Private Label in Building Margins

Duralast demonstrates how private label can transcend cost savings to become a competitive advantage. By offering superior warranties, consistent quality, and ubiquitous availability, Duralast commands premium prices despite being a store brand. The lesson: private label succeeds when it offers genuine value beyond price, creating customer preference rather than grudging acceptance.

Network Effects in Physical Retail

AutoZone's hub-and-spoke model creates network effects typically associated with digital platforms. Each new store makes the network more valuable by justifying broader hub inventory. Each hub enables better store service. More stores mean more commercial density, making delivery economics work. This physical network effect is harder to build but more durable than digital equivalents.

The Resilience of Need-Based Retail

AutoZone's performance through multiple recessions proves that need-based retail—products customers must buy rather than want to buy—offers remarkable stability. When the economy weakens, people defer new car purchases and fix existing vehicles. When the economy strengthens, more miles driven means more maintenance. This counter-cyclical dynamic smooths revenue across economic cycles.

Operational Leverage Through Incremental Improvement

The "1TEAM Going the Extra Mile" philosophy embedded continuous improvement into daily operations. A 1% improvement in inventory turns, a 0.5% reduction in shrink, a 2% increase in commercial delivery efficiency—individually meaningless, collectively transformational. This Japanese-style kaizen approach to retail operations created competitive advantages that revolutionary strategies rarely achieve.

The Value of Patient Capital and Long-Term Thinking

AutoZone's success required patient capital and long-term thinking increasingly rare in public markets. Investments in hub stores, technology systems, and commercial capabilities took years to pay off. Share buybacks required conviction that the business would compound value over decades. This long-term orientation, enabled by consistent execution that earned investor trust, created space for strategies that quarterly-focused competitors couldn't pursue.

The AutoZone playbook isn't about finding the next big thing—it's about executing the current thing better than anyone else, every day, for decades. It's proof that in business, as in investing, compound interest remains the most powerful force, whether applied to capital, operations, or competitive advantages.

X. Analysis & Bear vs. Bull Case

Bull Case: The Resilient Compounder

The bull thesis for AutoZone rests on multiple reinforcing pillars that suggest continued outperformance regardless of broader economic conditions. Start with the fundamental driver: America's aging vehicle fleet. The average vehicle age has climbed from 9.6 years in 2002 to over 12.5 years today, a trend accelerated by COVID-era supply chain disruptions that pushed new car prices to record highs. Every additional year of vehicle age dramatically increases maintenance needs—a 12-year-old car requires 50% more annual maintenance spending than an 8-year-old car. With new vehicle prices remaining elevated and interest rates constraining affordability, this aging trend shows no signs of reversing.

The recession-resistant nature of AutoZone's business model provides another compelling argument. Historical data proves that AutoZone thrives during downturns—comparable store sales grew throughout the 2008-2009 financial crisis and accelerated during the 2020 pandemic. The logic is intuitive: when budgets tighten, people fix rather than replace vehicles. This counter-cyclical dynamic means AutoZone wins regardless of economic conditions—prosperity increases miles driven and maintenance needs, while recessions drive repair over replacement.

International expansion represents a massive, underleveraged growth opportunity. With only 763 stores in Mexico and 109 in Brazil, AutoZone has barely scratched the surface of markets with combined populations exceeding 350 million and rapidly growing vehicle ownership. Mexico operations already generate 20%+ returns on invested capital, proving the model translates. Management targets 200 international store openings annually by 2028, which could add 2-3% to total company growth while requiring minimal corporate infrastructure investment.

The commercial business acceleration story remains in early innings. At roughly 30% of sales, AutoZone's commercial penetration significantly lags O'Reilly's 40%+, suggesting substantial room for growth. Every commercial customer added creates recurring revenue streams, as repair shops develop dependencies on AutoZone's delivery speed, credit terms, and ALLDATA integration. Commercial sales grew 4.5% in Q4 2024 despite broader DIY weakness, demonstrating the segment's momentum.

Capital allocation optionality provides multiple paths to value creation. With $3+ billion in annual operating cash flow and minimal capital requirements—new stores require just $1.5 million investment—AutoZone can simultaneously fund growth, reduce share count, and maintain investment-grade credit ratings. The company's proven ability to deploy capital at 20%+ returns, whether through new stores or buybacks, creates a powerful compounding machine.

Bear Case: Structural Headwinds and Disruption Risks

The bear thesis begins with the electric vehicle transition, which represents an existential threat hiding in plain sight. EVs require 70% fewer parts than internal combustion engines—no oil changes, no transmission fluid, no spark plugs, minimal brake wear due to regenerative braking. While EV adoption has been slower than predicted, the direction is unmistakable. Major automakers have committed to predominantly electric lineups by 2035. When the fleet tips electric—even if that's 15 years away—AutoZone's addressable market could shrink by 30-40%.

Amazon and digital competition pose an accelerating threat that AutoZone may be underestimating. While AutoZone dismisses Amazon as serving different use cases, Amazon's automotive sales are growing 20%+ annually and approaching $20 billion. Younger consumers comfortable with YouTube repair videos and next-day delivery may never develop the store-visiting habits AutoZone depends on. The company's digital investments, while competent, lag pure-play competitors in user experience and convenience.

Geographic concentration creates vulnerability to regional disruptions. With 87% of stores in the United States, AutoZone lacks the geographic diversification of truly global retailers. This concentration exposes the company to U.S.-specific risks: regulatory changes, minimum wage increases, domestic recession, or shifts in American driving patterns. The slow pace of international expansion—adding just 50-70 stores annually—means this concentration risk will persist for decades.

Labor cost pressures threaten the operating model in ways management may be underappreciating. AutoZone's value proposition depends on knowledgeable employees providing free diagnostic services and installation assistance. But with unemployment at historic lows and wage pressure intense, maintaining service quality while controlling costs becomes increasingly difficult. Store payroll already deleveraged in recent quarters, and this pressure will likely intensify.

Valuation concerns suggest limited upside even if execution remains flawless. At 20x forward earnings and 7x EV/EBITDA, AutoZone trades at premium multiples that assume continued perfection. Any stumble—a quarterly earnings miss, same-store sales deceleration, or margin compression—could trigger multiple compression that overwhelms operational progress. The stock's 150% five-year outperformance has pulled forward years of returns.

The Balanced View: Navigating Contradictions

The reality likely lies between these extremes. AutoZone faces genuine structural challenges—EV transition, digital competition, labor pressures—but possesses equally genuine competitive advantages that provide time and resources to adapt. The company's track record of navigating industry transitions suggests capability to evolve.

Consider how AutoZone could pivot for an electric future: EVs still require tires, brakes, cabin filters, windshield wipers, and collision parts. The company could expand into EV-specific categories like charging equipment, battery thermal management products, or sophisticated diagnostic tools for EVs' complex electronics. The ALLDATA acquisition positions AutoZone to become the information provider for EV repair, a potentially lucrative niche.

The Amazon threat might be overstated given the complexity of automotive parts. Unlike books or electronics, auto parts require precise fitment information, often need immediate availability, and benefit from expert guidance. AutoZone's omnichannel model—buy online, pick up in store—leverages physical presence as an advantage rather than liability. The company could further differentiate through services Amazon can't match: free testing, installation assistance, tool lending.

International expansion, while slow, is deliberate and derisked. AutoZone isn't making expensive acquisitions or massive infrastructure bets. Each new market is tested carefully, systems are refined, and profitability is proven before acceleration. This measured approach might frustrate growth investors but reduces the risk of value-destroying international adventures that plagued other retailers.

The valuation premium might be justified by quality and consistency. In a world of retail disruption, AutoZone's predictability has scarcity value. The company has grown EPS for 20+ consecutive years, maintained investment-grade credit through multiple cycles, and returned over $25 billion to shareholders. This isn't a speculative growth story but a proven compounding machine that arguably deserves a quality premium.

For investors, AutoZone represents a fascinating study in contradictions: a traditional retailer thriving in the digital age, a simple business model with complex competitive advantages, a mature company still finding growth, and a premium valuation that might be justified. The investment decision ultimately depends on time horizon and risk tolerance—those seeking explosive growth will be disappointed, but investors valuing consistent compounding and defensive characteristics might find AutoZone's risk-reward compelling even at current valuations.

XI. Epilogue & "If We Were CEOs"

Phil Daniele inherited the CEO role in January 2024 not with a crisis to solve but with a machine to keep humming. After spending over a decade in AutoZone's executive ranks, including leading the commercial business transformation, Daniele represents continuity rather than change. Yet continuity in retail is increasingly difficult when the ground beneath keeps shifting—electric vehicles gaining share, Amazon expanding aggressively, and a new generation of consumers who might never have changed their own oil.

If we were running AutoZone, the strategic priorities would balance defending the castle while building new fortifications for tomorrow's battles.

Priority One: Accelerate the Electric Vehicle Parts Opportunity

The EV transition isn't AutoZone's death sentence—it's a massive product cycle opportunity hiding in plain sight. EVs are computers on wheels, requiring specialized diagnostic equipment, unique fluids, complex cooling systems, and high-voltage safety equipment. We'd create "EV Zones" within stores, staffed by certified high-voltage technicians, stocked with EV-specific products, and equipped with Level 2 chargers in parking lots. Partner with EV manufacturers to become the authorized parts supplier for out-of-warranty vehicles. Acquire or develop EV diagnostic capabilities that independent repair shops desperately need. The goal: own the EV aftermarket before it fully emerges.

Priority Two: Transform International from Growth Option to Growth Engine

AutoZone's international operations are underexploited assets. We'd dramatically accelerate expansion, targeting 200+ new international stores annually by 2026, not 2028. Brazil offers massive potential—240 million people, 50 million vehicles, and fragmented competition. Mexico's proximity enables supply chain leverage and cross-border synergies. But think bigger: India's vehicle parc is exploding, Southeast Asia lacks organized auto parts retail, and even Europe's independent aftermarket remains fragmented. Each market would require localization—different product mix, service levels, and operating models—but the core competencies of inventory management, private label, and customer service translate globally.

Priority Three: Monetize Data and Information Assets

AutoZone sits on one of the most valuable datasets in automotive—280 million VINs, billions of transaction records, detailed repair histories. This data has untapped monetization potential. Launch AutoZone Intelligence, a B2B data service selling insights to manufacturers, insurers, and fleet operators. Predictive maintenance alerts for commercial customers. Dynamic pricing based on local demand patterns and competitive intelligence. Partner with connected car platforms to predict part failures before they happen. The data strategy isn't about competing with tech companies but leveraging unique automotive insights they can't access.

Priority Four: Reimagine the Store Experience for Next-Generation DIY

Young consumers might not change oil, but they modify cars, add accessories, and personalize vehicles. Transform select stores into "AutoZone Experience Centers"—part retail, part education, part community hub. Host Saturday morning clinics teaching basic maintenance. Create Instagram-worthy installation bays where customers can work on their cars with expert guidance. Launch AutoZone University online, with certification programs that create customer lock-in. Partner with high schools and community colleges to build the next generation of DIYers. The goal isn't just selling parts but creating car enthusiasts.

Priority Five: Build a Commercial Marketplace Platform

AutoZone's commercial business could be dramatically expanded through technology. Create AutoZone Pro Marketplace, connecting independent repair shops with parts suppliers, tools, equipment, and services. Shops could order from multiple suppliers through one platform, access financing, find temporary technicians, and manage their entire operations. AutoZone would take transaction fees while becoming indispensable to shops' daily operations. Think of it as the Shopify for auto repair shops—enabling their success while capturing value from the entire ecosystem.

Priority Six: Aggressive Domestic Consolidation

With Advance Auto Parts struggling and regional chains under pressure, a consolidation opportunity is emerging. We'd selectively acquire distressed competitors' best locations, converting them to AutoZone stores at fraction of greenfield cost. But more interestingly, acquire specialized chains that expand capabilities—a performance parts chain for enthusiasts, a collision parts specialist, a commercial-focused wholesaler. Each acquisition would bring new customers, capabilities, and defensive positioning.

Priority Seven: Financial Engineering 2.0

While maintaining the successful buyback program, we'd explore innovative capital strategies. Issue 100-year bonds at historically low rates to lock in cheap capital. Create a REIT structure for owned real estate, unlocking billions in value. Launch AutoZone Ventures, investing in automotive startups that could disrupt or complement the business. Implement a dividend to attract income investors while maintaining buyback flexibility. The balance sheet strength AutoZone has built enables creative capital allocation that competitors can't match.

The Cultural Imperative

Beyond strategic initiatives, preserving and evolving AutoZone's culture remains paramount. The "AutoZoner" identity—helpful, knowledgeable, customer-focused—created the company's success. But culture isn't static. We'd evolve it for new realities: embrace technology fluency alongside mechanical knowledge, reward innovation alongside execution, celebrate international diversity alongside American roots. Create AutoZoner equity programs that make every employee an owner. Establish AutoZone Labs where employees can experiment with new concepts. The goal: maintain the cultural core while adapting to new realities.

Final Reflections on Building Enduring Retail Franchises

AutoZone's journey from a single Arkansas store to a $60 billion enterprise offers timeless lessons about building enduring businesses. Success came not from revolutionary innovation but from evolutionary improvement—doing thousands of small things slightly better than competitors, every day, for decades. The company proved that even in commodity retail, competitive advantages can be built through operational excellence, cultural consistency, and patient capital allocation.

The challenges ahead are real—technological disruption, changing consumer preferences, new competitive threats. But AutoZone's history suggests an organization capable of adaptation without losing its core identity. The company that started selling carburetors now sells sophisticated electronics. The retailer that began with paper catalogs now runs one of retail's most sophisticated digital platforms. The regional chain that served rural Arkansas now operates across three countries.

For the next CEO, the mandate is clear: honor the past while building the future. Preserve what makes AutoZone special—the culture, the customer focus, the operational discipline—while boldly pursuing new opportunities. The automotive aftermarket will look radically different in 2040 than today, but cars (in whatever form) will still need maintenance, consumers will still need help, and operational excellence will still create value.

AutoZone's story isn't finished. The most interesting chapters—navigating the EV transition, expanding globally, digitalizing the commercial business—are just being written. The company that Pitt Hyde founded to democratize auto repair faces its biggest transformation yet. But if history is any guide, AutoZone will emerge stronger, more valuable, and still helping Americans keep their vehicles running—one part at a time, one customer at a time, one store at a time.

The lesson for builders and investors alike: in a world obsessed with disruption, there's immense value in consistency. In a market that rewards growth, there's power in compound returns. In an economy that celebrates innovation, there's profit in perfecting execution. AutoZone didn't just build a parts retailer—it built a compounding machine that turns the mundane necessity of vehicle maintenance into extraordinary shareholder returns.

That machine keeps humming today, ready for whatever roads lie ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube