Stifel Financial: The Quiet Empire Builder of Wall Street

Introduction: From Midwest Brokerage to $12 Billion Powerhouse

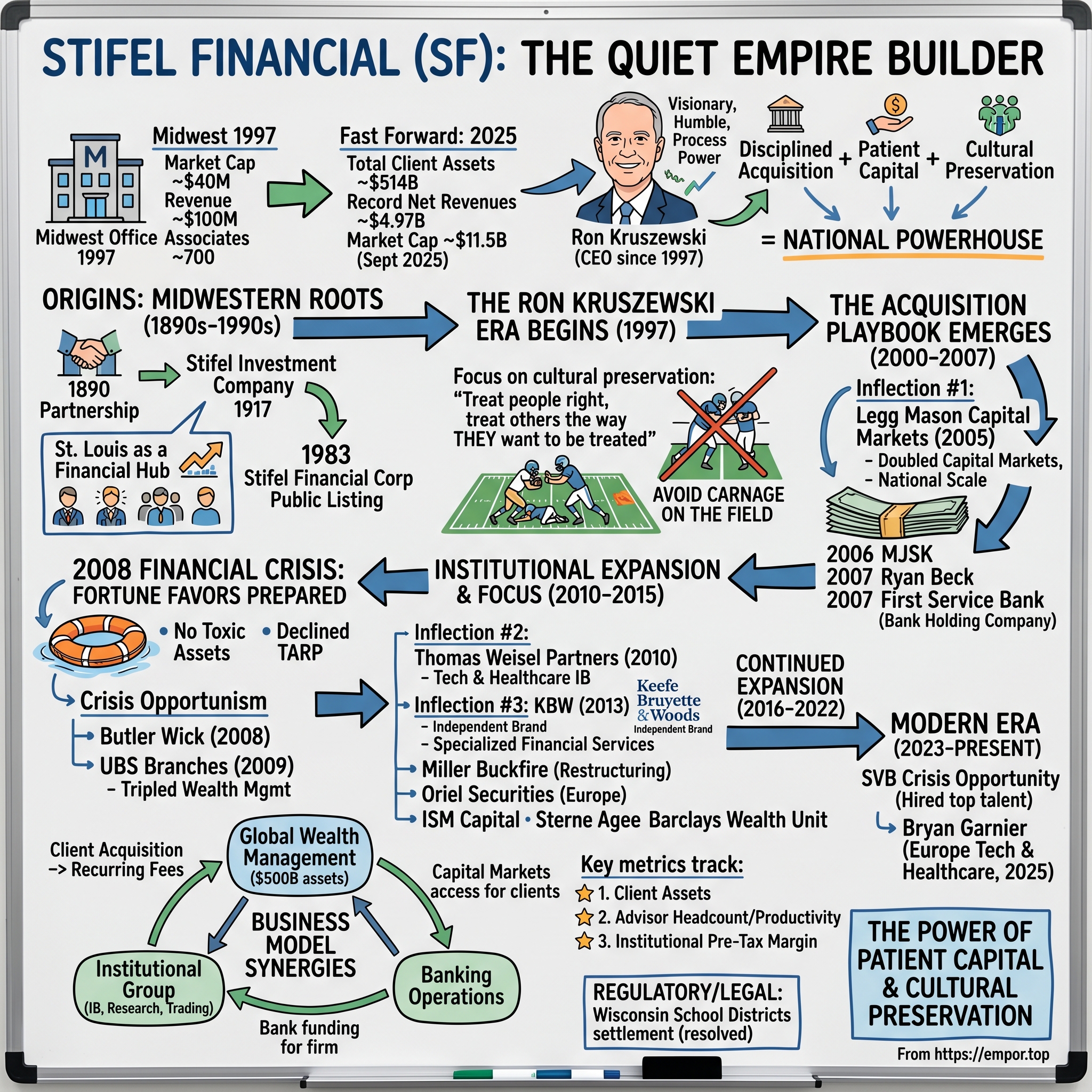

Picture St. Louis in 1997. Downtown, a modest financial services firm occupies a building on Broadway and Washington. Its market capitalization hovers around $40 million. Its annual revenue barely reaches $100 million. Approximately 700 associates staff its regional offices, serving Midwestern families with traditional investment advice.

Fast forward to November 2025. Total client assets under management have climbed to a record $514 billion, including a record $197 billion in fee-based assets. The company reported record net revenues of $4.97 billion for 2024. Since Ron Kruszewski took the helm in 1997, Stifel has boosted revenue from $100 million to $5 billion, while increasing its market cap from $40 million to $8 billion. As of September 2025 Stifel has a market cap of $11.50 Billion USD.

This is the Stifel story—how a regional brokerage from the heartland quietly assembled one of America's most formidable middle-market investment banking and wealth management empires. It's a textbook case in serial acquisition strategy, crisis-era opportunism, and cultural preservation. And it all traces back to one man's nearly 28-year vision for what a financial services firm could become.

In nearly 27 years at the helm, Kruszewski—he's believed to be the longest-tenured current CEO in the wealth management industry—has turned a company of approximately 700 associates generating $100 million in revenue into a massive firm of roughly 10,000 associates producing nearly $5 billion in revenue.

The central thesis of this story is deceptively simple: Stifel proves that disciplined acquisition, patient capital allocation, and cultural preservation can transform a regional player into a national powerhouse—even in an industry dominated by Wall Street giants. But execution of that thesis required navigating multiple market crises, regulatory challenges, and the delicate art of integrating dozens of disparate businesses while maintaining their entrepreneurial DNA.

What follows is an examination of Stifel's journey across three distinct eras: its 135-year history as a Midwestern institution, its transformation under Kruszewski beginning in 1997, and its emergence as a diversified global financial services firm. The patterns embedded in this story offer lessons about patience, opportunism, and the power of compounding both capital and capability over decades.

Origins: The 135-Year History of a Midwestern Institution

The roots of modern Stifel stretch back to the Gilded Age, when St. Louis served as America's gateway to the West and one of the nation's premier financial centers.

Stifel traces its origins to 1890, when Benjamin Altheimer and Edward Rawlings established a partnership in St. Louis, Missouri, to conduct a general securities business. This venture, initially known as Altheimer and Rawlings Investment Company, laid the groundwork for the firm's future operations in investment services.

What gave this small partnership staying power was the arrival of a young man with a conservative disposition. Herman C. Stifel joined the company in 1897 as treasurer, bringing a conservative approach that emphasized the protection of clients' funds during the firm's early decades. Under his influence, the business navigated the economic challenges of the late 19th and early 20th centuries, focusing on building trust through prudent financial practices.

By 1917, the firm had evolved sufficiently to reflect Stifel's prominent role, renaming itself Stifel Investment Company. This change marked a period of steady regional growth in the Midwest, where the company concentrated on brokerage services and municipal bond underwriting.

St. Louis: America's Forgotten Financial Hub

To understand Stifel's DNA, one must understand St. Louis's surprising place in American financial history. Today, when people think of financial services, they picture Manhattan's towers or perhaps Chicago's trading floors. But St. Louis once rivaled both.

Many people don't know this, but back around the 1960s, the No. 2 city to New York, in terms of financial services, investment banking, and brokerage, was St. Louis. Today, you have some great companies: Edward Jones, Wells Fargo Advisors, Stifel, and Benjamin F. Edwards. That's created a very experienced workforce of people who understand our business. So there's a huge advantage in running a financial services firm like Stifel in St. Louis.

This concentration of financial talent wasn't accidental. St. Louis's position as a transportation hub, combined with its role financing westward expansion, created deep capital markets expertise. The city's distance from New York fostered a different culture—one that emphasized relationships over transactions, long-term thinking over quarterly results, and conservatism over speculation.

These values, embedded in the firm's culture over generations, would prove crucial when a new CEO arrived in 1997 with transformative ambitions.

The Modern Corporate Structure Emerges

Stifel Financial Corp. is an American multinational independent investment bank and financial services company created under the Stifel name in July 1983 and listed on the New York Stock Exchange on November 24, 1986. Its predecessor company was founded in 1890 as the Altheimer and Rawlings Investment Company and is headquartered in downtown St. Louis, Missouri.

In July, Stifel becomes a publicly owned corporation as a result of a $1,442,870 share offering. The public listing was modest—the company raised less than $1.5 million—but it established the corporate structure that would eventually enable aggressive growth through stock-based acquisitions.

Throughout the 1980s and early 1990s, Stifel remained primarily a Midwestern brokerage firm providing investment advice to individuals. The firm's leadership, including George Herbert Walker III (yes, related to the Bush family), maintained its conservative regional focus. But as the financial services industry consolidated through the 1990s, Stifel faced a stark choice: grow or get acquired.

The Ron Kruszewski Era Begins: 1997

The transformation of Stifel from regional brokerage to national powerhouse begins with a single hiring decision in 1997. It's a story that starts, improbably, in Crumbstown, Indiana.

Ronald "Ron" Kruszewski was born in 1958 in an unincorporated part of South Bend, Indiana, called Crumbstown. He is the second of four children, all born in succeeding years. "My dad was a barber when I was little," says Ron. "We used to play a game at school where you would put the chalkboard eraser on top of your head and see who could run around the longest before it fell off. I always won because I had the best flattop in town, compliments of my father." As Ron grew up, his father took on other jobs. He became a fireman, and then had a lawn-mowing service. In wintertime, he plowed snow. "I remember getting up before sunrise so that I could ride in the truck with him as he plowed," says Ron. "It seems to me my dad worked all the time. I guess I got my strong work ethic from him. I have always appreciated how hard he worked to take care of our family."

The son of a barber-turned-fireman, Kruszewski didn't have connections to Wall Street or the Ivy League. What he did have was a relentless work ethic and ambition that would take him from small-town Indiana to running one of America's largest independent investment banks.

Building the Foundation: From Accountant to CEO

After graduating from university, Kruszewski became a Certified Public Accountant and joined KPMG as an audit supervisor. Wanting to enter the investment banking industry, he relocated to Chicago and started working for Illinois Company Investment as a senior vice president and chief financial officer. He then became chief financial officer of strategic planning for Robert W. Baird & Co. He was mentored by the firm's CEO, Fred Kasten, who later helped him earn the CEO position at Stifel Financial Corporation.

The mentorship with Fred Kasten proved transformational—not just for Kruszewski's career, but for his leadership philosophy. A gentleman by the name of Fred Kasten taught me to treat people right. After you've been at Stifel for a year, I won't know what school you went to or your grade point average. I won't even know what your IQ is. What I will know is whether you're a good team player and whether you get along and treat people right. That's what Fred taught me and what I try to teach people today.

A Painful Self-Discovery

Before becoming an effective leader, Kruszewski had to confront something uncomfortable about himself. I was the kind of young man who could get most things done. Unfortunately, it'd be like playing football, but I would tackle my own teammates. I'd get things done, but I'd look back, and the carnage on the field would be extensive. In one particular case, back in the 1990s, we were doing a big conversion, and we got it done, but I really trampled over a lot of people.

This self-awareness would become central to Stifel's acquisition strategy. Rather than the typical Wall Street approach of acquiring firms and immediately imposing new cultures and processes, Kruszewski developed a philosophy of cultural preservation that would enable Stifel to integrate dozens of acquisitions while retaining their entrepreneurial character.

"I'm the CEO, so I get a lot of credit for our amazing growth," says Ron, "but it would have been impossible if not for a collective effort. In the end, it comes down to a way of looking at the Golden Rule, which says to treat others the way YOU want to be treated. I turn it around a bit and say we should treat others the way THEY want to be treated. It's never too late to learn this lesson."

Taking the Helm

Ronald J. Kruszewski is Chairman of the Board and Chief Executive Officer of Stifel Financial Corp. and its principal subsidiary, Stifel, Nicolaus & Company, Incorporated. He joined the firm as Chief Executive Officer in 1997 and was named Chairman in 2001.

His tenure began in 1997 when he succeeded George Herbert Walker III; among his first actions was implementing the company's wealth accumulation plan as an employee benefit. Since then, the company has grown significantly by completing a series of acquisitions during the 2000s and 2010s.

In 1997, Ron Kruszewski arrived in St. Louis to start a new job. Stifel was still a small firm at the time, but as the organization's new CEO, Kruszewski was determined to pilot the company into the new millennium and help it reach its full potential in a rapidly changing world. More than two decades later, Kruszewski's tenure has proven to be a success story.

"My success will have very little to do with me and a lot to do with how many people I can get to believe in what we are doing." That note, written by Kruszewski when he walked into the Stifel building for the first time, captures the philosophy that would guide nearly three decades of growth.

The Acquisition Playbook Emerges: 2000-2007

For the first several years of Kruszewski's tenure, Stifel focused on organic growth and small regional acquisitions. But the CEO was studying the industry, watching as consolidation reshaped financial services, and developing the playbook that would eventually transform Stifel.

The strategic vision crystallized into a consistent framework that Kruszewski has articulated repeatedly over the years: build a premier wealth management and institutional services firm through balanced growth—organic expansion supplemented by strategic acquisitions that add capabilities, geography, or specialized expertise.

What made Stifel's approach distinctive was its philosophy toward acquired firms. Rather than the typical private equity approach of extracting synergies through aggressive cost-cutting, Stifel sought to preserve what made acquired businesses successful in the first place.

Inflection Point #1: The Legg Mason Capital Markets Acquisition (2005)

The deal that changed everything came in December 2005, when an unusual opportunity emerged from a complex corporate reshuffling.

Citigroup had acquired Legg Mason's brokerage business, but the capital markets division didn't fit its strategic plans. Stifel saw an opportunity.

On December 1, 2005, Stifel Financial closed on the acquisition of the Legg Mason Capital Markets business (LM Capital Markets) from Citigroup Inc. The LM Capital Markets business acquired included investment banking, equity and fixed income research, equity sales and trading, and taxable fixed income sales and trading (22 offices in the US and Europe and 500 associates). These assets gave the company substantial research and capital market capabilities and transformed the company from a regional firm to a national one.

Stifel, a brokerage and investment banking firm founded in 1890, agreed to pay Citigroup as much as $95 million for the Legg Mason operations, including a premium based on how well it performs over the next three years.

The strategic logic was compelling. Stifel gained instant scale in research, trading, and investment banking. A pivotal deal came in December 2005 with the acquisition of Legg Mason Capital Markets from Citigroup, which more than doubled Stifel's capital markets operations, added institutional sales and trading expertise, and established East Coast offices to transition the firm into a national full-service investment bank.

The integration went smoothly—a pattern that would repeat across future acquisitions. Chairman and Chief Executive Officer, Ronald J. Kruszewski, commented, "Our record first quarter revenues and Core Earnings underscore our excitement about our merger with LM Capital Markets. The integration of people and technology has been seamless and we are well positioned to continue our historical growth, albeit from a higher plateau."

Kruszewski emphasized that turnover was minimal. He said more than 90 percent of the Legg Mason employees are on board to stay with Stifel and that many senior managers have signed employment contracts.

Rapid Expansion Continues: 2006-2007

With the Legg Mason deal proving the acquisition model, Stifel accelerated its pace.

In 2006, the company acquired the Private Client Group of Minneapolis-based Miller Johnson Steichen Kinnard, Inc. (MJSK) (7 offices and 50 financial advisors). In 2007, the company completed the acquisition of Ryan Beck & Co. from BankAtlantic Bancorp (43 offices in 14 states and 1,100 associates). The acquisition significantly increased the company's presence in the East coast.

The firm also opened several Private Client Group offices in the state of California and branched out across the entire West Coast. During the same year, the company completed the acquisition of First Service Financial Company, and its wholly owned subsidiary, FirstService Bank, a St. Louis-headquartered, Missouri chartered bank. As a result of the transaction, the company became a bank holding company and a financial holding company.

The First Service Bank acquisition deserves special attention. By becoming a bank holding company, Stifel gained access to a stable funding source and could offer banking services to wealth management clients—a competitive advantage that would prove crucial during future market disruptions.

By the end of 2007, Stifel had transformed from a regional brokerage into a national full-service firm with presence across the United States. The company had proven it could identify targets, integrate operations, and retain talent. But the real test was coming—a crisis that would separate the well-capitalized opportunists from the over-leveraged casualties.

The 2008 Financial Crisis: Fortune Favors the Prepared

When Lehman Brothers collapsed in September 2008, it triggered the worst financial crisis since the Great Depression. Banks that had appeared invincible disappeared overnight. Bear Stearns was sold for $10 per share. Merrill Lynch was absorbed by Bank of America. The government created TARP—the Troubled Asset Relief Program—injecting $700 billion to prevent complete systemic collapse.

In this environment, most financial services firms fought for survival. Stifel went shopping.

The Contrarian Move

Stifel "has proven to be among the most resilient broker/dealers through the recent financial crisis, has a lack of toxic and credit exposure, and less volatile business mix, has allowed it to be proactive in building out its institutional businesses."

Stifel's conservative approach—the DNA inherited from Herman Stifel's emphasis on protecting client funds—meant the firm entered the crisis without the toxic mortgage-related assets that destroyed competitors. The company had liquidity when others were desperate. And it had a CEO with the vision to see opportunity in chaos.

The firm was one of only a handful of financial services companies that declined federal TARP money—a decision that preserved flexibility and avoided the stigma and restrictions that came with government assistance.

Opportunistic Expansion Through the Crisis

In 2008, the company completed its $12 million acquisition of Butler Wick & Company, Inc. from United Community Financial Corp. Butler Wick, a Youngstown, Ohio-based provider of financial advisory services, had offices in Ohio, Pennsylvania and New York (23 offices in three states and 175 associates).

Youngstown investment advisory firm Butler Wick & Co. will be acquired under a definitive agreement with Stifel Financial Corp., a St. Louis brokerage and investment banking firm with offices in 13 Ohio cities. Under the agreement, Stifel will buy Butler Wick for $12 million in cash. That price is a modest premium to book value of the assets acquired. The deal is expected to close by the end of the year. Butler Wick has 175 employees in 23 offices in Ohio, Pennsylvania and New York.

The Butler Wick acquisition exemplified Stifel's crisis playbook. A financially stressed parent company needed to sell assets; Stifel had liquidity and could move quickly; the price was attractive; and the acquisition expanded Stifel's geographic footprint in the Ohio Valley region.

Then came an even bigger opportunity in 2009.

In 2009, the company acquired 56 branches from the UBS Wealth Management Americas (UBS) branch network (56 offices in 24 states and 500 associates).

The UBS deal was transformative. UBS, the Swiss banking giant, was restructuring its U.S. operations amid massive crisis-related losses. Stifel acquired 56 branches across 24 states and 500 financial advisors—roughly tripling its wealth management footprint in a single transaction.

This pattern—crisis creates distressed sellers, Stifel provides liquidity in exchange for valuable assets at attractive prices—would repeat throughout the firm's history. The lesson for investors: in a cyclical industry, the companies that maintain conservative balance sheets during booms often emerge as the biggest winners from inevitable busts.

Inflection Point #2: The Thomas Weisel Partners Merger (2010)

With the crisis-era deals integrated, Stifel turned its attention to building institutional capabilities. The target was a prestigious San Francisco-based investment bank that had fallen on hard times.

Thomas Weisel Partners Group, Inc., also known as TWP or Weisel, is a U.S. growth focused investment banking firm headquartered in San Francisco, California. The firm was launched in January 1999 by Thom Weisel and other personnel from the former Montgomery Securities. In 1997, Thom Weisel helped to orchestrate a $1.3 billion acquisition of Montgomery Securities by NationsBank. The following year, however, NationsBank acquired BankAmerica Corp, which itself had acquired Technology-based rival Robertson Stephens. A culture clash and fight for control ensued at the newly combined investment banking units of what is now known as Banc of America Securities. In the process, senior bankers from Montgomery Securities secured backing from the Silicon Valley Venture Capital community and left to form their own venture: Thomas Weisel Partners.

Thomas Weisel Partners had built a premier franchise in technology and healthcare investment banking, with deep relationships in Silicon Valley's venture capital community. But the firm had struggled to achieve profitability as an independent public company, particularly after the tech bubble burst in 2000 and during the 2008 crisis.

Stifel Financial Corp., a full-service brokerage and investment banking firm, is pleased to announce the completion of the merger with Thomas Weisel Partners Group, Inc. The merger furthers Stifel's mission of building the premier middle-market investment bank with significantly enhanced investment banking, research, and wealth management capabilities. "This transaction continues our commitment to balanced growth by expanding our investment banking platform in key sectors of the global economy. The integration planning process has gone extremely well, and we now look forward to executing our plan with an enhanced platform that is well-positioned to compete in our core competencies and expand into others."

In 2010, Stifel acquired Thomas Weisel Partners Group, Inc. in a transaction valued at approximately $300 million, bringing on board a prominent middle-market investment bank with strong focus on technology and healthcare sectors, and appointing Thomas W. Weisel as co-chairman to advance Stifel's institutional ambitions.

Strategic Rationale

The strategic logic was compelling on multiple dimensions.

With very little overlap in investment banking and research, the combination is additive to the existing platform in a number of ways. The investment banking team consists of more than 250 talented associates providing debt, equity and equity-linked offerings, private placements, and strategic advisory services. In research, the combination creates one of the largest U.S. equity research platforms, with more than 1,000 companies under coverage. The combination also expands Stifel's institutional equity business both domestically and internationally.

Thomas W. Weisel, chairman and chief executive of Thomas Weisel Partners, adds: "There is virtually no overlap in investment banking and less than a ten per cent overlap in research coverage. Our platform adds key growth sectors to Stifel's investment banking business, particularly in technology, healthcare and energy."

According to Stifel's presentation to investors today, the merger fast tracks Stifel's technology and health care investment banking growth and footprint, which would otherwise take years to build.

The Thomas Weisel merger established a pattern that would define Stifel's acquisition strategy: acquire specialized expertise in specific industry verticals rather than trying to build it organically. Technology and healthcare investment banking required deep relationships with venture capitalists, entrepreneurs, and industry executives—relationships that take years to develop. Stifel acquired decades of relationship capital in a single transaction.

Inflection Point #3: The KBW Merger & Institutional Expansion (2011-2015)

The Thomas Weisel deal gave Stifel credibility in technology and healthcare. The next major acquisition would establish the firm as a dominant player in financial services investment banking.

The KBW Acquisition

On 5 November 2012, Stifel Financial announced they would be acquiring KBW in its entirety for $575 million. KBW was the third bank to merge with Stifel since 2010 as part of Stifel's efforts to become the pre-eminent middle-market investment bank. The merger was completed on 15 February 2013.

Keefe, Bruyette & Woods, Inc., a Stifel Company, is an investment banking firm headquartered in New York City, specializing exclusively in the financial services sector. KBW's primary business lines include research, corporate finance, equity sales and trading, equity capital markets, debt capital markets, and asset management. The firm provides a broad range of services to corporate clients such as banking companies, insurance companies, real estate and REITs, broker-dealers, mortgage banks, asset management companies, and specialty finance firms as well as to the institutional investor community. KBW's research analysts cover more than 600 companies in the financial services industry globally. The company, which was founded in 1962, currently has nine offices in the United States as well as an office in London.

The firm was founded in 1962 by Harry Keefe Jr., Gene Bruyette and Norbert Woods. The three founders previously had worked together at Tucker, Anthony & R. L. Day. Beginning in the 1950s, Keefe had been one of the first Wall Street research analysts to focus on bank stocks, which later became the specialty of the firm he co-founded.

The KBW acquisition carried both strategic and emotional significance. The company's prior New York headquarters was located on the 88th and 89th floors of the World Trade Center's South tower at the time of the terrorist attacks of September 11, 2001.

The $575 million acquisition is the largest in Stifel's history.

The combined company will provide investment banking, sales and trading, and research in the financial services vertical through KBW's Keefe, Bruyette & Woods broker-dealer subsidiary, which will continue to operate as an independent subsidiary of Stifel following completion of the transaction. Stifel will utilize KBW's preeminent market brand as a highly focused, specialized financial services platform of choice. Stifel has identified significant synergies that will leverage the integrated platforms and take advantage of Stifel's robust global wealth management capabilities. Annualized net revenues for the two companies are approximately $1.8 billion, based upon 2012 results through September 30, 2012.

The decision to maintain KBW as an independent subsidiary, preserving its brand and specialized culture, exemplified Stifel's acquisition philosophy. Rather than forcing integration, Stifel allowed KBW to continue operating with significant autonomy while benefiting from Stifel's broader platform and resources.

Restructuring Capability: Miller Buckfire

In 2012, Stifel also acquired Miller Buckfire, a restructuring advisory boutique. This gave Stifel countercyclical capability—when the economy struggles and companies face distress, restructuring advisory generates fees. Combined with the firm's conservative balance sheet approach, this positioning meant Stifel could profit from both economic expansion and contraction.

European Expansion

In May 2015, the company acquired the debt capital markets and convertibles specialist ISM Capital LLP.

In 2014, Stifel acquired the London stockbroker Oriel Securities, establishing a meaningful European presence. This gave U.S. middle-market clients access to European capital markets and enabled Stifel to serve cross-border M&A transactions.

Wealth Management Consolidation

In 2015, the company acquired the Birmingham, Alabama based investment bank, brokerage and wealth management firm Sterne Agee Group for $150 million.

In June 2015, the company announced it would acquire Barclays' U.S. wealth and investment management unit, adding substantial assets under management and expanding Stifel's wealth management footprint.

The sheer volume of acquisitions during this period—Stone & Youngberg (municipal finance), Miller Buckfire (restructuring), KBW (financial services), Oriel Securities (European brokerage), ISM Capital (convertibles), Sterne Agee (wealth management), Barclays' wealth unit—demonstrated both Stifel's integration capabilities and its strategic clarity about building a comprehensive middle-market financial services platform.

Continued Expansion: 2016-2022

The pace of acquisitions continued through the late 2010s and early 2020s, with Stifel filling gaps in its platform and expanding internationally.

In January 2016, the company acquired the placement agent Eaton Partners LLC. In March 2018, the company acquired Ziegler Wealth Management. In November 2018, the group acquired German bank MainFirst Bank AG. In 2019, the company acquired First Empire Holding Corp. and its subsidiaries, including First Empire Securities Inc. In November 2021, the company acquired the Memphis, Tennessee based fixed income brokerage Vining Sparks.

Each acquisition served a specific purpose: - Eaton Partners strengthened placement agent capabilities for private equity and hedge fund clients - Ziegler Wealth Management added a respected regional wealth management franchise - MainFirst Bank expanded European presence in key continental markets - First Empire enhanced institutional equity capabilities - Vining Sparks deepened fixed income expertise and community bank relationships

The Vining Sparks acquisition in particular demonstrated Stifel's understanding of relationship banking. Vining Sparks had built a 90-year franchise serving community banks—the exact client base that Stifel's KBW subsidiary advised on M&A transactions and that Stifel Bank could serve with deposit and lending products. The acquisition created cross-selling opportunities across the entire platform.

Modern Era: 2023-Present

SVB Crisis Opportunity

In March 2023, Silicon Valley Bank collapsed in the second-largest bank failure in U.S. history. For most financial firms, the regional banking crisis was a source of anxiety. For Stifel, it was an opportunity.

Stifel Financial Corp. today announced a significant expansion of its business serving growth companies in the venture community through the addition of three key partners formerly with Silicon Valley Bank, ("SVB"). Jake Moseley, Matt Trotter, and Ted Wilson all join Stifel as Managing Directors and will immediately assume leadership roles in Stifel's Venture Banking Group. They are based in the San Francisco Bay area. "Adding these talented new partners is yet another example of our commitment to growth companies, venture capital, and the entire innovation ecosystem," said Stifel Chairman and CEO Ron Kruszewski.

Some of SVB's top bankers are already gone. Driving the news: Stifel this morning announced that it's hired Jake Moseley, Matt Trotter and Ted Wilson as managing directors in its venture lending business. Why it matters: While everyone's been focusing on the assets, some of SVB's rivals have been focusing on the people. And the people could be of greater long-term value. What they're saying: Stifel CEO Ron Kruszewski tells Axios that venture lending, like wealth management, is heavily reliant on relationships.

The larger goal is to become more ingrained in the entrepreneurial community and serve as a hub that connects founders, CFOs and investors through the cultivation of new relationships—something that SVB had excelled at. "We are going to be a very significant player in venture banking and in the venture ecosystem," said Chris Reichert, chief executive at Stifel's commercial banking business.

Then in September 2024, Stifel expanded further. Stifel launched a new life science and healthcare venture banking practice entirely made up of ex-Silicon Valley Bank employees, including three vice presidents and six senior bankers, the bank said Tuesday. Senior bankers Jackie Spencer, Anthony Flores, Milo Bissin, Julie Ebert, Timothy Lew and Sam Subilia have all been named managing directors at Stifel. Also joining Stifel are Vice Presidents Tessa Dibble and Lindsey Seidner, Senior Vice President Ariana DaCruz and four junior bankers. The expansion adds to Stifel's venture and fund banking arm, which launched in 2019. Stifel's venture banking business was previously expanded by a group of SVB bankers who jumped ship to Stifel weeks after the regional banking crisis took down SVB in March 2023.

Stifel has more than doubled venture client deposits in the past year, the bank said, and has more than $10 billion in loan commitments.

This pattern—capitalizing on competitors' distress to acquire talent and relationships—exemplifies the Kruszewski playbook that has driven Stifel's growth for nearly three decades.

Bryan Garnier Acquisition: European Healthcare and Technology

In January 2025, Stifel announced its latest major acquisition.

Stifel Financial Corp. today announced it has signed a definitive agreement to acquire Bryan, Garnier & Co. ("Bryan Garnier"), a leading independent full-service investment bank focused on European technology and healthcare companies. Bryan Garnier represents an ideal partner," said Ronald J. Kruszewski, Stifel Chairman and CEO. "Its culture and long-term history of providing clients with high quality advice in two of our largest investment banking growth verticals is highly complementary with Stifel's business. This combination is a logical next step in the evolution of Stifel's global advisory business."

Founded in 1996, Bryan Garnier & Co is an independent partnership with around 200 employees located in major financial centers in Europe and the US.

ST. LOUIS, June 2, 2025 – Stifel Financial Corp. (NYSE: SF) today announced the completion of its acquisition of Bryan, Garnier & Co. ("Bryan Garnier"), a leading independent full-service investment bank specializing in the European technology and healthcare sectors.

"This partnership enhances our European capabilities and moves us closer to our goal of being the premier global investment bank for the middle market. Together, we're creating a transatlantic advisory platform built for long-term growth."

Since 2020, Stifel and Bryan Garnier have collectively led over 500 European technology and healthcare transactions, encompassing advisory services, sponsor-led mergers & acquisitions, equity, and debt deals. This combined experience positions the firm as a formidable player in the European investment banking landscape.

Recent Financial Performance

Ronald J. Kruszewski, Chairman and Chief Executive Officer, said "Stifel generated record net revenue and the second highest earnings per share in our history in 2024. The fact that we accomplished this level of performance in a year when our Institutional segment was rebounding from a very difficult operating environment in 2023 is a testament to the strength and diversity of our business model. Given our long history of profitable growth, Stifel is well positioned to capitalize on improving market conditions in 2025 and to achieve our short and long term targets."

Stifel Financial Corp. today reported net revenues of $1.4 billion for the three months ended September 30, 2025, compared with $1.2 billion a year ago. Net income available to common shareholders was $202.1 million, or $1.84 per diluted common share.

Ronald J. Kruszewski, Chairman and Chief Executive Officer, said "Our third-quarter results once again highlight the strength of Stifel's balanced business model and disciplined execution. We delivered record net revenue of more than $1.4 billion and $1.95 in earnings per share, the third highest in our history, driven by record results in Global Wealth Management and a 34% increase in Institutional revenue."

Business Model Deep Dive

Understanding Stifel requires understanding its three operating segments and how they interact to create competitive advantages.

Segment 1: Global Wealth Management

Financial Advisors in nearly 400 Private Client Group offices across the U.S., responsible for $500 billion in client assets.

Global Wealth Management reported record net revenues of $907.4 million for the three months ended September 30, 2025 compared with $827.1 million during the third quarter of 2024. Pre-tax net income was $342.7 million compared with $301.7 million in the third quarter of 2024.

Record client assets of $544.0 billion, up 10% over the year-ago quarter.

The wealth management segment provides the foundation for Stifel's business model. It generates recurring fee-based revenue from assets under management, produces stable cash flows that fund acquisitions, and creates cross-selling opportunities for investment banking and banking products.

Importantly, Stifel has invested heavily in technology to support its financial advisors. The intersection of advice and technology remains a primary strategic focus, with clients able to aggregate portfolios, monitor balance sheets, access research, and interact with advisors through digital platforms.

Segment 2: Institutional Group

Stifel provides both equity and fixed income research. It is the largest provider of US equity research.

Institutional Group reported net revenues of $500.4 million for the three months ended September 30, 2025 compared with $372.4 million during the third quarter of 2024. Pre-tax net income was $89.3 million compared with $41.8 million in the third quarter of 2024.

Advisory revenues increased 31% from the year-ago quarter driven by higher levels of completed advisory transactions. Equity capital raising revenues increased 55% from the year-ago quarter driven by higher volumes as clients actively engaged in capital raising opportunities in a more constructive market environment. Fixed income capital raising revenues increased 19% over the year-ago quarter primarily driven by higher bond issuances reflecting a more favorable financing environment.

The institutional segment houses investment banking (M&A advisory, equity and debt capital markets), equity and fixed income research, and institutional sales and trading. It's organized around specialized industry verticals including technology, healthcare, financial services (via KBW), consumer/retail, industrials, and others.

This segment is inherently more volatile than wealth management, as investment banking revenues depend on M&A activity and capital markets conditions. However, it provides growth optionality and strategic value—companies that use Stifel's investment banking services often become wealth management clients for executives and key employees.

Segment 3: Banking Operations

Stifel Bank & Trust provides both retail and commercial banking services. The bank offers consumer and commercial lending solutions and deposit accounts, serving as a funding source for the broader firm while generating net interest income.

The banking segment creates competitive advantages for both other segments. Wealth management clients can access securities-based lending, mortgages, and banking services through their financial advisor relationship. Institutional clients benefit from Stifel's ability to provide financing alongside advisory services.

Business Model Synergies

The three segments interact in ways that create competitive advantages difficult for competitors to replicate:

- Client Acquisition: Investment banking mandates create relationships with corporate executives who become wealth management clients

- Cross-Selling: Wealth management clients need banking services; banking clients need investment advice; companies advised on M&A need capital markets services

- Information Advantages: Deep research coverage informs investment banking advice; investment banking relationships inform research; both inform wealth management recommendations

- Funding Efficiency: The bank provides low-cost deposit funding; wealth management provides stable fee income; investment banking provides growth

Playbook: Business & Leadership Lessons

The Kruszewski Leadership Philosophy

"To grow a company," Kruszewski says, "you need to lead by letting people be the best they can be. I get a lot of credit for being CEO, but I stand on the shoulders of 10,000 people who are very good at what they do."

This humility isn't performative—it's embedded in how Stifel operates. The firm's acquisition strategy specifically aims to preserve entrepreneurial cultures rather than impose centralized control.

Acquisition Integration Philosophy

Stifel's approach to M&A integration differs markedly from typical Wall Street practice. The firm aims to preserve and enhance the independent excellence of acquired firms, letting brands uphold the reputations they've dedicated themselves to cultivating. While maximizing operational efficiency through integration, the primary goal is always to better serve clients.

This philosophy explains why KBW maintains its distinct brand, why Thomas Weisel Partners' venture relationships remain intact, and why acquired teams often stay rather than depart post-acquisition.

Seven Key Business Lessons from the Stifel Story

-

Conservative Balance Sheets Enable Opportunistic Growth: By avoiding excessive leverage and toxic assets, Stifel maintains the capacity to acquire during crises when competitors are distressed sellers.

-

Cultural Preservation Creates Acquisition Currency: Stifel's reputation for respecting acquired firm cultures makes it an attractive acquirer, improving deal flow and reducing integration friction.

-

Specialization Through Acquisition: Rather than trying to build expertise organically in every industry vertical, Stifel acquires established franchises with existing relationships and track records.

-

Diversification Reduces Volatility: The combination of fee-based wealth management, transaction-based investment banking, and spread-based banking smooths earnings across economic cycles.

-

Geographic Concentration as Competitive Advantage: St. Louis's deep financial services talent pool provides recruiting advantages and lower costs compared to New York.

-

Patient Capital Compounding: Nearly 28 years of consistent strategy execution has compounded both financial results and organizational capabilities.

-

Relationships Over Transactions: In an industry often characterized by short-term thinking, Stifel's emphasis on long-term relationships creates sustainable competitive advantages.

Competitive Positioning & Investment Framework

Competitive Landscape

Stifel Financial Corp's key competitors and market peers include Raymond James Financial Inc with 19,000 employees and $14.9B revenue, Jefferies Financial Group Inc with 7,671 employees and $10.5B revenue, T. Rowe Price Group Inc with 8,158 employees and $7.1B revenue, and Piper Sandler Companies with 1,805 employees and $1.5B revenue.

Stifel - Absolute inorganic growth machine. If there is anything they don't do phenomenally right now, they'll acquire a business to fit that piece of the puzzle within a few years. Again, see massive upside ahead for these guys. Will grow well beyond the Baird's & Blair's of the world.

Stifel Financial is a diversified financial-services provider that generates revenue from wealth management, investment banking, and lending. The firm was founded in 1890 as a St. Louis-based full-service brokerage but has been transformed under CEO Ronald Kruszewski through a slew of acquisitions into a globally competitive wealth manager, investment bank, and retail and institutional brokerage. The firm generated $5.0 billion in revenue in 2024, with roughly two-thirds derived from wealth management and one-third derived from investment banking and trading.

Porter's Five Forces Analysis

Threat of New Entrants: LOW - High regulatory barriers (broker-dealer, bank holding company, investment banking licenses) - Significant capital requirements - Established relationships take years to develop - Research platform requires substantial ongoing investment

Bargaining Power of Suppliers: MODERATE - Key "suppliers" are talented employees (bankers, advisors, analysts) - Competition for top talent is intense - Stifel mitigates through ownership culture and competitive compensation

Bargaining Power of Buyers: MODERATE - Institutional clients can negotiate fees on large transactions - Wealth management clients are more fragmented with less negotiating power - Switching costs exist (advisor relationships, account complexity)

Threat of Substitutes: MODERATE - Passive investing threatens traditional wealth management - Technology platforms (Robinhood, etc.) serve different market segments - AI could potentially disrupt research value proposition - Middle-market focus provides protection (smaller transactions require advisory expertise)

Competitive Rivalry: HIGH - Numerous well-capitalized competitors - Industry consolidation ongoing - Fee pressure in wealth management - Transaction fees under pressure from electronification

Hamilton Helmer's 7 Powers Framework

Scale Economies: PRESENT - Research platform costs spread across larger revenue base - Technology investments leveraged across more advisors - Compliance infrastructure serves entire organization

Network Effects: LIMITED - Not a primary driver of competitive advantage - Some network effects in venture banking (connecting founders with VCs)

Counter-Positioning: PRESENT - Cultural preservation approach differs from private equity-style acquirers - Middle-market focus avoids direct competition with bulge bracket firms

Switching Costs: MODERATE - Advisor-client relationships create stickiness - Complexity of transferring accounts creates friction - Institutional clients have lower switching costs

Cornered Resource: PRESENT - KBW's financial services expertise - Long-tenured advisor force with deep client relationships - Specialized industry knowledge across verticals

Process Power: PRESENT - Acquisition integration capabilities refined over 30+ deals - Cultural assessment and preservation methodology - Demonstrated ability to retain talent post-acquisition

Branding: MODERATE - Strong brand in specific verticals (KBW in financials) - Reputation for relationship-focused service - Less brand recognition than larger competitors

Bull Case

The bull case for Stifel centers on several interconnected themes:

Continued Acquisition Execution: Stifel's proven M&A playbook should enable continued roll-up of smaller competitors and expansion into new verticals. Clients look at us differently. We have become so much more relevant given all the capabilities that we can provide, whether it's wealth management, a bank, institutional advice, capital raising, M&A. With this positive momentum, we are setting our sights on a transformative era for the firm, to double our size by attaining $10 billion in annual revenue and managing $1 trillion in client assets.

Investment Banking Recovery: The M&A and capital markets recovery should benefit Stifel's institutional segment, which has significant operating leverage.

Wealth Management Growth: Continued recruiting of financial advisors, combined with market appreciation, should drive wealth management revenue growth.

Interest Rate Environment: The banking segment benefits from higher interest rates through expanded net interest margins.

Market Share Gains: Ongoing industry consolidation provides opportunities to acquire talent and assets from distressed competitors.

Bear Case

The bear case requires considering several risk factors:

CEO Succession: Kruszewski has led Stifel for nearly 28 years. He's believed to be the longest-tenured current CEO in the wealth management industry. Succession planning and execution represent a key risk.

Cyclical Exposure: Despite diversification, Stifel remains sensitive to equity market performance, M&A activity levels, and interest rates.

Integration Risk: While Stifel's track record is strong, acquisition integration always carries execution risk, particularly as deals increase in complexity.

Technology Disruption: Passive investing, robo-advisors, and AI could pressure traditional business models.

Regulatory Environment: Financial services regulation continues to evolve, potentially impacting business practices and compliance costs.

Competition for Talent: The industry's competitive dynamics around advisor and banker compensation could pressure margins.

Stifel's diversified investment banking model and middle-market exposure could position the company to outperform during a surge in financial sponsor activity. Simultaneous declines in risk appetite, asset prices, and short-term interest rates could significantly diminish Stifel's earnings power.

Key Metrics to Track

For investors following Stifel's performance, three KPIs deserve primary focus:

-

Client Assets Under Administration — This represents the aggregate value of client assets across wealth management accounts. Growth in client assets drives fee-based revenue (wealth management fees are typically charged as a percentage of AUM) and indicates success in advisor recruiting and client retention. The record $544 billion in client assets reported in Q3 2025 represents the cumulative result of decades of organic growth and acquisitions.

-

Financial Advisor Headcount & Productivity — The number of financial advisors and their production (revenue per advisor) indicate organic growth momentum. Stifel's recruiting success—recruited 33 financial advisors during the quarter, including 16 experienced employee advisors, and 1 experienced independent advisor, with total trailing 12 month production of $18.9 million—reflects the firm's competitive positioning in attracting talent.

-

Institutional Segment Pre-Tax Margin — The institutional segment (investment banking, research, trading) has significant operating leverage. In strong markets, margins expand rapidly; in weak markets, they compress. Institutional Group reported net revenues of $1.6 billion for the year ended December 31, 2024 compared with $1.2 billion in 2023. Pre-tax net income was $223.4 million compared with $2.1 million in 2023. This dramatic margin recovery demonstrates the operating leverage inherent in the business.

Regulatory and Legal Considerations

Investors should note historical regulatory matters, though Stifel has generally navigated these successfully:

The Securities and Exchange Commission sued Stifel Nicolaus on August 10, 2011, claiming the firm duped five Wisconsin school districts into buying $200 million in "unsuitable" securities tied to collateralized debt obligations. The investments, which the school districts had purchased in 2006 with $163 million in borrowed funds and $37 million of their own money, were "far more risky" than Stifel Nicolaus advertised.

On March 19, 2012, it was announced that a settlement had been reached with the school districts to jointly pursue a $200 million lawsuit against Royal Bank of Canada, alleging that they are liable for the original misrepresentation. Royal Bank of Canada had already settled with the Securities and Exchange Commission in September 2011 for $30.4 million. In March 2012, Stifel settled with the school districts for $13 million. In 2016, the Wisconsin school districts secured a settlement with Stifel and RBC for $217.9 million, $63.9 million in cash and $154 million in debt forgiveness.

This matter, while significant, has been resolved and reflects pre-crisis practices that the industry has broadly moved away from.

Conclusion: The Power of Patient Capital and Cultural Preservation

The Stifel story offers a compelling case study in how patient, disciplined execution of a consistent strategy can transform a regional player into a national powerhouse. From its origins in 1890 St. Louis through its transformation under Ron Kruszewski beginning in 1997, the firm has demonstrated that success in financial services doesn't require the biggest balance sheet or the most aggressive tactics.

Stifel has gone from $100 million in revenue to nearly $5 billion in revenue, from a $40 million market cap to an $8 billion market cap. Yet I feel we're just beginning. People will say, "Well, that growth has been phenomenal. What's next?" My answer: the same amount of growth going forward because we are so well positioned in this marketplace.

What makes Stifel's approach distinctive is its integration philosophy—the commitment to preserving entrepreneurial cultures rather than imposing centralized control. In an industry often characterized by cutthroat competition and short-term thinking, Stifel has built durable competitive advantages through relationship-focused, long-term oriented management.

The firm's conservative approach to balance sheet management—evidenced by its decision to decline TARP funds during the 2008 crisis—has repeatedly enabled opportunistic acquisitions during periods of industry distress. From Butler Wick and UBS branches during the financial crisis to SVB talent during the 2023 regional banking crisis, Stifel has consistently transformed others' adversity into its own advantage.

Looking forward, the key questions for investors center on execution: Can Stifel continue to identify and integrate acquisitions successfully? Can the firm navigate an eventual CEO succession? Can its middle-market focus and relationship-oriented approach remain competitive as technology reshapes financial services?

Nearly 135 years since its founding and approaching three decades under Kruszewski's leadership, Stifel has built something rare in financial services: a firm that has grown dramatically while maintaining the cultural characteristics that enabled that growth in the first place. Whether that balance can be sustained through the next phases of evolution will determine whether Stifel's quiet empire-building continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube